?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

South Africa is a developing country faced with diverse challenges like high unemployment, poverty, inequality and low economic growth. In an attempt to address these issues, government can embark on borrowing and incur public debt. Countries that run large persistent public debt signal negative perceptions to investors as the debt might lead to credit risk posed by currency weakness and credit downgrades. The study investigated if public debt can influence public investment and ultimately economic growth. The autoregressive distributive lag, Granger causality, impulse response function and variance decomposition were applied to achieve the objectives. The cointegration test has found the existence of long-run relationship among the investigated variables. It turns out that in the long run there is a negative relationship between public debt and investment. Since there is direct link between investment and economic growth, there is an inverse relationship in the public debt economic growth nexus. The error correction mechanism confirmed that the system can adjust to equilibrium at a speed of 17%. There is bi-directional Granger causality relationship between public debt and economic growth. The impulse response function has found that, one standard deviation shock in public debt inversely affect economic growth. Variance decomposition results indicate that a shock to public debt account for 16.39% fluctuations in economic growth. It is recommended that a capital scarce country be encouraged to borrow so that more capital can be accumulated. However, the later stage of borrowing marked with high level of debt will lead to subdued growth.

PUBLIC INTEREST STATEMENT

This research paper analyzed how the level of public debt can affect public investment and economic growth. The South African economy has been growing after the transition of the country into democracy. However, as time goes on, the global economy was hit by economic and financial crisis in 2007 until 2009. Because of that economic and financial crisis, many countries experienced technical recessions including South Africa.

Despite weak levels of economic growth and discouraged investment activities, South Africa had to borrow money to keep the economy functioning. Therefore, it became a concern for this study to revisit the period starting after apartheid regime, to investigate how the growing level of public debt triggered low levels of investment and economic growth. The study, therefore, used the data after apartheid and applied several econometrics techniques to analyze data and come up with certain conclusions and policy recommendations, in the interest of improving policy certainty for better economic performance in future.

1. Introduction

South Africa is a developing country faced with diverse challenges of high unemployment, poverty, inequality and low economic growth. Its economic growth slowed from an average of 4.3% between 2000 and 2007 to 1.9% between 2008 and 2015 (Chirwa & Odhiambo, Citation2015; Marek, Shakill, Yashvir, & Luchelle, Citation2016). In 2015/2016 fiscal year the trend was shocking as public debt doubled and reached 44.3% of gross domestic product (GDP). In an attempt to address these issues, government committed to stabilize public debt in the 2014 medium term budget policy statement (Marek et al., Citation2016) and the country also adopted a National Development Plan policy to commit to have inclusive and dynamic growth by 2030 (National Development Plan, Citation2011). The economy should be close to full employment, have skillful citizens, ensure more diverse ownership of production and provide resources to pay for investment. Countries need policies to ensure a growing economy so as to minimize government intervention in the economy and reduce budget deficit (Jacobs, Schoeman, & Van Heerden, Citation2002). One of the strategies that can be used to boost the economy is to borrow in order to uplift the investment activities of a country. Investments have been identified as major channel through which the government development goals can be met and grow the economy (Hoag & Hoag, Citation2006).

Public debt is the money owned by the government from either foreign lenders or from citizens within the country which increases as the government engage more on deficit spending (Bonga, Chirowa, & Nyamapfeni, Citation2015; Jaejoon & Manmohan, Citation2014). Public debt makes it possible for government to invest in those areas that are critical for the economy whereby tax revenue is not enough to finance such projects. It should be noted that financing government expenditure through public debt can be detrimental to the economy (Ramos, Veronique, Helene, & Margaret, Citation2013; Tsoulfidis, Citation2007). In the instances where government expenditure is unproductive, that is expenditure to pay for government employees and expenditure on army maintenance, it follows that public debt undermines the capacity of the economy to gain momentum. However, if such expenditures are compulsory, their source of financing should be through taxation, instead of borrowing (Tsoulfidis, Citation2007).

The government can embark on three financing activities to boost the economy, namely printing money, collecting taxes or borrowing. The government borrows and incurs public debt as it needs to fill the gap between tax revenues and expenditure so as to carry its developmental functions smoothly, especially investment activities. The level of economic growth can significantly lose momentum when the country reaches debt threshold or public debt overhang. That might be through higher interest rates, higher inflation and crowding out private investment (Boccia, Citation2013). Taking higher interest rate for instance, creditors may set higher interest rates due to low confidence in the ability of the country to settle its debt. As a result, higher interest rates induce high debt cost, forcing government to impose more tax on the citizens (Hoag & Hoag, Citation2006), inducing the likelihood of economic doldrums and depress government expenditure in other areas. Most importantly, higher interest rates may result in low investment, leading to sluggish economic growth in the rest of the economy. This can simultaneously induce current account deficit and decline in economic growth forcing the country to borrow more thus increase its debt service (Iyoha, Citation1999). Furthermore, when the debt is accumulated, the cost of servicing this debt would come from taxes on future production. As a result, investment would be discouraged, hence crowding out of investment (Tabengwa, Citation2014).

Some scholars have found a link that reduction of public debt, especially foreign debt, can stimulate growth in the economy (Bonga et al., Citation2015; Jaejoon & Manmohan, Citation2014; Qudah, Citation2016). Public debt should to be used for projects of investment that should translate into economic growth and jobs, which ultimately improve well-being for citizens. This paper attempts to find out if there is a link between public debt and investments, and furthermore, if the investment channel can be stimulated by public debt so as grow the economy. The study needs to answer the research question that can increase public debt influence investments and ultimately promote economic growth in a developing country context.

2. Literature review

2.1. Theoretical literature

The theoretical arguments on public debt were discussed with respect to the Classical, Ricardian’s, Keynesian views and endogenous growth model. The Classicals viewed public debt as a capital injection to be used for production investment rather than consumption by individuals (Say, Citation1880). This implied that government expenditure should not be financed by means of borrowing regardless of the circumstances. Furthermore, the existing public debt should effectively be dealt with immediately (Churchman, Citation2001; Medeiros, Cabral, Baghdassarian, & Almeida, Citation2005; Mohanty & Mishra, Citation2016). The concern was the possibility of constraints that monetary policy might experience as a result of the structure and the size of the public debt. Governments consider borrowing as an alternative for taxes, thus allowing expenditure to increase without immediate changes in tax rates (Pascal, Citation2012).

The Keynesian model stipulates that high debt levels increase taxes which negates positive effects of public spending by decreasing investment, lowering consumption, reducing employment and reducing the growth rate of the economy. However, at moderate levels, public debt may increase the economic growth rate (Kamudia, Citation2015). Government can use the creation of debt for productive investment that could increase national income and stimulate economic growth. If public debt is directed otherwise, it might result into some challenges. For instance, a rise in government expenditure fuels the domestic economic activity and crowds in private investment (Biza, Kapingura, & Tsegaye, Citation2013). As claimed by crude closed economy theory of Keynesian, the increasing government expenditure is linked to higher national output, which leads to employment (Makin, Citation2015). However, the funds available for investment may be crowded out by increased government expenditure. The requirement to fill the saving–investment gap as provided by the Keynesian framework is foreign investment or foreign aid (Mongale, Petersen, Meniago, & Petersen, Citation2013).

The preference of Ricardo for tax-financed government spending other than public borrowing has been legitimized by the social benefits of capital growth. According to Churchman (Citation2001), Ricardo argues that if public debt were to be used for financing spending by government during war for instance, there would be serious repercussions within the economy after the war time. This is simply because in order to service the accumulated debt, taxation would have to be imposed. The consequence of today’s government borrowing as stated by Ricardian’s Equivalence is the future increase in taxation above normal level (Modgliani, Citation1961). As a result, this would neutralize the impact of public debt on economic growth.

The following channels amongst others initiate the influence that public debt have on economic growth: private saving, investing in public projects, the aggregate of factor productivity and real interest rates. As highlighted by Baaziz (Citation2015), public debt determines economic growth via domestic savings and investment. Furthermore, huge amounts of public debt impose danger on domestic saving and investment via the crowding out effect, and as a result cause economic growth to shrink. The controversies on these theoretical views emerged from Ricardian equivalence theory to argue that public debt does not influence economic growth. The argument is based on the view that increasing private saving resulting from more tax cut financed through large amount borrowed will offset the public saving drop (Kibet, Citation2013; Kourtellos, Stengos, & Tan, Citation2013). Therefore, according to Baaziz (Citation2015), minor public debt affects economic growth positively; however, when public debt goes beyond certain limit, it will inversely affect economic growth.

The endogenous growth model in the assumption of constant tax rate and interest rate adheres that increasing public debt reduces the growth rate of an economy and as such future generations would be disadvantaged as a result (Saint-Paul, Citation1992). For the reduction in debt to have a positive effect, there should be an investment subsidy such that the government pays a portion of interest cost of capital. Since the private return of capital will now be higher, people save, consume less and increase economic growth.

2.2. Empirical literature

The impact of public debt on economic growth in advanced and less advanced countries is marked by wide body of literature (Eberhardt & Presbitero, Citation2015; Lopes, Ferreira-Lopes, & Sequeira, Citation2015; Nantwi & Erickson, Citation2016; Stylianou, Citation2014). There is a complex and different relationship between public debt and economic growth across countries. The debt–growth nexus should take into account debt composition, variety of country characteristics which could constrain government choices and affect the economy’s vulnerability to crises. There are several studies conducted using different econometric approaches to investigate public debt and economic growth. For instance, some scholars found that public debt inversely affect economic growth, meaning that reduction of public debt would stimulate economic growth (Baaziz, Citation2015; Bonga et al., Citation2015; Checherita & Rother, Citation2010, Citation2010; Qudah, Citation2016; Tabengwa, Citation2014). Generally, such a relationship would depress private investment. Countries with higher average debt to GDP ratio are more likely to see negative effects on their long run growth performance (Reinhart & Rogoff, Citation2010).

Some scholars found a positive relationship between public debt and economic growth (Mohanty & Mishra, Citation2016; Reinhart and Rogoff (Citation2010). Sanchez-Juarez and Garcia-Almada (Citation2016) found that countries that show a positive relationship are those diverting debt usage from production to other functions which could lead to unsustainable public finance in the medium term. The evolution of market economies is expected to be affected by fiscal policy and particularly government’s debt policy (Greiner, Citation2013). Other scholars found no causality on the debt–growth nexus because the level of debt in developing countries cannot explain the slowdown of investment (Cohen, Citation1993; Panizza and Presbitero, Citation2014).

Moss and Chiang (Citation2003) indicated the important channels underpinning the link between public debt and economic growth. The first channel they have shown is debt overhang, which is thought to exist when the burden of country’s high debt dampens the incentive for investment because investors expect the future taxes of returns to capital to be imposed for the purpose if servicing debt (Moss & Chiang, Citation2003). The new investments in heavily indebted countries may be delayed because of unpredictable outcomes of debt rescheduling negotiations. The second channel is liquidity constraint, which is imposed by debt service. The large payments of debt service may induce lower growth through deprivation of the country’s foreign exchange needed for the imported capital goods.

Baseerit (Citation2005) also posited that the earlier stage of borrowing is normally marked with enhanced growth resulting from modest debt level. This view is supported theoretically by neoclassical growth models, in the sense that, capital scarce countries are encouraged to borrow so that they increase their accumulation of capital. The later stage of borrowing marked with high debt as pointed out by Baseerit (Citation2005) leads to subdued growth. Medeiros et al. (Citation2005) in their study of public debt strategic planning and benchmark in Brazil stated that if the public debt is managed, the burden of tax could be reduced through the changing return on debt. The strategy is that optimally the structure of the debt would depend on how inflation, changes in government expenditure and revenue interact. The interaction between those three will vary from country to country depending how the tax system is structured, and also depending on how government is committed to its expenditure and the different types of shocks that may be experienced in the economy.

In a study by Agim (Citation2014), it is posited that, surging levels of public debt is a result of fiscal policies that are not sound. The weakening of economic institutions induces the probability of debt distress in the form of persistent weak economic policies and high vulnerability to external shocks (Acemoglu & Robinson, Citation2008; Makin, Citation2015; Yasemin, Citation2017). The probability of debt crisis as emphasized within empirical literature is positively associated with higher levels of total debt and higher shares of short-term debt, and inversely associated with economic growth (Kraay & Vikram, Citation2006). It is challenging to reform economic institutions since economic institutions depend on the nature of political institutions and how political power is distributed among society (Acemoglu & Robinson, Citation2008; Ferraz & Duarte, Citation2015; Megersa & Cassimon, Citation2015).

3. Research methodology

To achieve the aim of whether there is an impact of public debt on public investments and economic growth, the autoregressive distribution lag (ARDL) and Granger causality have been employed.

3.1. Model specification

In order to respond to the question of whether public debt can influence investment and ultimately affect economic growth, the model from the works of Sanchez-Juarez and Garcia-Almada (Citation2016), Ramirez and Erquizio (Citation2012) and Diaz (Citation2010) among others were adopted. To capture specific characteristics of the South African economy, budget deficit and trade openness were used as control variables in the post-apartheid era, post 1994 (Diaz, Citation2010). Trade openness is represented by the ratio of exports and imports to GDP as adopted from Yanikkaya (Citation2003). The estimated linear model is as follows:

where INV represents fixed investment measured by total assets of public investment corporation, PD public debt, BD budget deficit, RE ratio of exports to GDP and RI ratio of imports to GDP.

3.2. Data

The study utilized South African quarterly time series data in the period from 1995 to 2016. Data used in the study is obtained from the South African Reserve Bank.

3.3. Estimation techniques

Most time series data are non-stationary, therefore the first step when dealing with time series is to test for unit roots. The study adopts the Augmented Dickey Fuller (ADF) test and Phillips Perron (PP) test. According to Cheng and Annuar (Citation2012), unit root tests (also known as test of stationarity) are performed to determine order of integration of variables since this can influence its behavior and therefore the methodology to analyze data (Fadli et al., Citation2011). The statisticians advocated that transformation of integrated into stationary time series requires that series be differenced successively prior to using models in order to avoid spurious regressions (Dolado, Gonzalo, and Marmol, Citation1999; Bum, Citation2009).

The autoregressive distributive lag (ARDL) model was employed to investigate the public debt–investment nexus. The ARDL bounds test endorsed by Pesaran, Shin, and Smith (Citation2001) was used to test if cointegration exists in the series. The presence of cointegration implies the existence of long-run equilibrium relationship among variables under investigation. The bounds test is advantageous where unit root test indicate different orders of integration and faced with small sample size (Pesaran & Shin, Citation1997). The bounds test give two critical values, the lower and upper bound critical values. The computed F-statistic should lie above the upper bound test to indicate that cointegration exists. The ARDL approach captures the short- and long-run relationship simultaneously, and also provides the error correction mechanism (ECM). The ECM indicates the speed of adjustment and the negative significant coefficient implies that any short-run variations will give rise to stable long-run relationship between variables, and the model will converge to equilibrium. The error correction coefficient is important in the error correction estimation since the greater coefficient indicates higher speed of adjustment of the model from the short run to the long run. The value added by ARDL approach is that it assumes variables are endogenous and can accommodate structural breaks in the time series (Pesaran & Shin, Citation1997).

One of the main objectives of empirical econometrics is to study the causal relationships among economic variables. As mentioned by Jung (Citation1986), Granger causality’s predictability and exogeneity are quite useful in empirical work. The Granger causality measures if a certain event happens before another, and helps to predict that event (Sorenson, Citation2005; Stern, Citation2011). Variables are said to Granger-cause one another if the past values of a certain variable assist in prediction of current level of another variable given the applicable information. The purpose of causality test is to check how the variables react to each other, and it determines whether the paired time series data has a correlation or not.

The dynamic specification of the econometric model is examined by several test statistics, which becomes invalid when the model is estimated in the presence of contemporaneous correlation between errors and regressors (Ekaterini, Citation1998). It is therefore important for diagnostic check of normality, serial correlation and heteroskedasticity (Griliches, Citation1961; Kleiber & Zeileis, Citation2008; Zeilies & Hothorn, Citation2002). There is a possibility that the model may be unstable, and for that reason, the Cumulative Sum (CUSUM) and Cumulative Sum of Squares (CUSUM of Squares) will be conducted to test for stability of the model. CUSUM of squares is used as a recursive structural stability test, which is usually applied to observations that run forward from start to finish of a given time interval (Pesaran, Citation2002).

The analysis of Vector Auto regression often centers on the calculation of impulse response function and forecast error variance decomposition, which tracks the evolution of economic shock through the system (Swanson & Granger, Citation1997). Therefore, dynamic interaction among the variables is investigated by generating variance decompositions (VDCs) and impulse response functions (IRFs). Since the validity of causality tests as postulated by Soytas and Sari (Citation2003) is applicable within the sample period, the variance decomposition is utilized to assess the validity of causality beyond the sample period. The variance decomposition allows for examination of the out-of-sample causality among the variables within VAR system.

4. Empirical results and discussion

In compliance with the methodology discussed in the previous section, this section presents the empirical analysis and interpretation of the findings.

4.1. Unit root test and ARDL results

Variables in the model exhibited different orders of integration when the ADF test and PP test were used. For instance, the PP results indicated that public debt and ratio of exports to GDP were stationary at level I(0). All other variables became stationary at first differencing, indicating that the variables are integrated of order one (1). Then, we proceed with the bounds test as it can estimate variables both at level and of first order of integration (Pesaran et al., Citation2001).

Table presents cointegration results of the bounds testing. The public debt–investment model has five variables. Therefore, there are four independent variables in the model, hence k = 4. The calculated F-statistics is 12.16, which is greater than the lower bounds critical value of 3.29 and the upper critical value of 4.37 at 1% level of significant. Therefore, there is cointegration amongst the variables, meaning in the long run the variables are co-moved (Pesaran et al., Citation2001).

Table 1. ARDL bounds test results, 1995–2016

Having found the evidence of the long-run relationship through the bounds testing, the coefficients of long run are projected. Table shows short- and long-run coefficients of the public debt–investment model. The results display a significant negative long-run relationship between the investment and public debt when trade openness and budget deficit were used as controlled variables. However, the relationship is insignificant in the short run. This negative long-run relationship is in line with the findings of Ramirez and Erquizio (Citation2012); Fincke and Duarte (Citation2015) and Kamudia (Citation2015). The argument to the negative relationship is that government borrowing uses up private savings that would have been used by private sector for investment. Increasing public debt results into fewer funds for private investment (Kamudia, Citation2015). High debt ratio and high percentage of tax revenue collected from citizens will be used to pay interest accruing from public debt (Marek, Citation2014). This reduces funds left for investment purposes. Furthermore, high costs of servicing the debt could have unfavorable consequences like import strangulation that can impede export growth. The error correction term denoted by EC has a negative sign, indicating that the system will eventually revert to equilibrium (Table ). Thus, long-run disequilibrium will be corrected through short-run adjustments, and lead the system to equilibrium in the short run at a speed of 17%.

Table 2. ARDL short- and long-run results, 1995–2016

It has been discussed in literature that reduction in public debt can stimulate growth in the economy (Bonga et al., Citation2015; Eberhardt & Presbitero, Citation2015; Jaejoon & Manmohan, Citation2014; Qudah, Citation2016). So, the channel via an increase in public debt would increase interest rates and therefore cost of private credits. Investors would be discouraged by high interest rates and accumulate less capital which would upshot into low economic growth. Some authors have found a direct link between investment and economic growth (Romp & De Haan, Citation2005; Shrithongrung & Kriz, Citation2014). Baseerit (Citation2005) posited that the earlier stage of borrowing is normally marked with enhanced growth resulting from modest debt level. This view is supported theoretically by neoclassical growth models, in the sense that, capital scarce countries are encouraged to borrow so that they increase their accumulation of capital (Mohanty & Mishra, Citation2016; Reinhart & Rogoff, Citation2010). However, the later stage of borrowing marked with high debt as pointed out by Baseerit (Citation2005) leads to subdued growth. This is backed by Bonga et al. (Citation2015) who posited that policymakers commonly understand public debt as the cause of subdued economic growth.

4.2. Granger causality test results

There is bi-directional Granger causality relationship between public debt and economic growth (Table ). However, in the case of investment and economic growth, as well as government deficit and economic growth, there is unidirectional relationship from investment and government deficit to growth.

Table 3. The results of Granger causality test

In line with this outcome, Rajan (Citation2005) argued that countries with weak economic growth are likely to run large government deficit, which leads to more borrowing. Hence, causality runs from low economic growth to high public debt. In such cases, where the causality runs from low growth to high public debt, the debt relief will fail to spur more growth (Yasemin, Citation2017). However, this depends with the way the borrowed funds are utilized. For instance, if the borrowed funds are being spent on productive investments, it is then most likely that economic growth would accelerate, resulting from public debt. Similarly, the Granger causality results indicate that investment can cause economic growth.

4.3. The diagnostic tests and the test of stability results

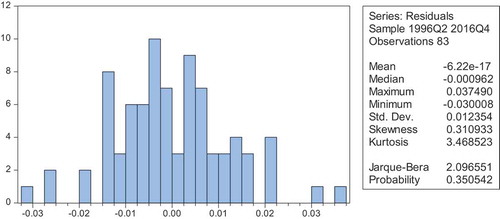

The diagnostic and stability tests include testing for serial correlation, heteroskedasticity, test of normality and CUSUM and CUSUM of squares tests of stability. The VEC Residual Serial Correlation LM Test of serial correlation indicates the probability value of 0.8660, which is more than 5% significance, indicating the acceptance of null hypothesis. This means the model does not have serial correlation. The four tests used to check for heteroskedasticity complemented each other to confirm that the model does not have heteroskedasticity. The p-values for both F-statistic and Observed R2 in Breusch-Pegan-Godfrey test, white test, Harvey test and Glejser test are more than 5%, indicating the absence of heteroskedasticity. The Kurtosis of 3.468 which is above 3 indicates that residuals of the model are normally distributed (Figure ).

Figure 1. Normality test results.

Source: Author compilation.

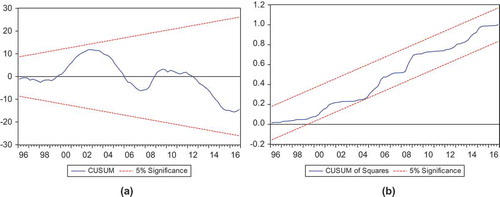

The stability test results are shown in Figure panels (a) and (b). The CUSUM and CUSUM of squares are the tests used to check stability within the model. The results of stability test show evidence that the model is stable. This is indicated by a movement of blue lines located within the critical lines (two-red dotted lines) in the figures. Therefore, at 5% level of significance, the CUSUM and CUSUM of Squares stability tests confirm good performance of the model.

Figure 2. CUSUM test and CUSUM of squares.

Source: Author compilation.

4.4. Variance decomposition results

The variance of the forecast error in economic growth is attributable to innovations to its own innovations, as well as to public debt, investment and government deficit. As shown in Table , four quarters have been chosen to explain variance decomposition. Firstly, when the variance of the forecast error in economic growth is attributable to its own innovations, economic growth accounts for 94.57103% variation of the fluctuation in economic growth (own shock) in the second quarter. In the fourth quarter, shock in the economic growth accounts for 66.55% fluctuations.

Table 4. Variance decomposition results

A shock to public debt causes 1.51% fluctuation in economic growth in the second quarter. In the short term, it appears that a shock to public debt does not cause much fluctuation in economic growth. Hence, the earlier stage of borrowing enhances growth resulting from modest debt (Baseerit, Citation2005). In the fourth quarter, a shock to public debt account for 16.39% fluctuations in economic growth. Thirdly, quarter two shows that a shock to investment account for 3.30 fluctuations in economic growth, while in quarter four, a shock to investment accounts for 12.79% fluctuations in economic growth. Lastly, a shock to government deficit in quarter two accounts for 0.62 fluctuations in economic growth, and in the fourth quarter a shock to government deficit accounts for 4.25% fluctuations in economic growth.

4.5. Impulse Response Function (IRF) results

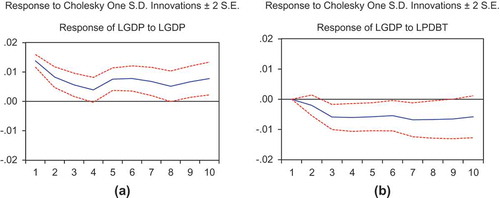

The results of impulse response function as presented in Figure indicate how one standard deviation shock to the residual induces the reaction of variables toward each other (Swanson & Granger, Citation1997).

Figure 3. Impulse response function results.

Source: Author compilation.

As demonstrated in panel (a), one positive standard innovation to economic growth leads to positive reaction to itself in the selected ten quarters. Thus, one standard deviation shock in public debt will inversely affect economic growth (panel (b)). This is in line with what Bonga et al. (Citation2015) have posited to say, commonly, policymakers understand public debt as the cause of subdued economic growth. Furthermore, Moss and Chiang (Citation2003) coined out the liquidity constraint channel imposed by debt service. Hence, large payments of debt service may induce lower growth through deprivation of the country’s foreign exchange needed for the imported capital goods.

5. Conclusion and recommendations

The study aimed to investigate if public debt has an impact on public investment and economic growth in a developing country. The ARDL, Granger causality, variance decomposition and impulse response functions have been employed in the analysis. In order to achieve the stated objectives, the South African quarterly data was obtained from the South African Reserve bank in the period from 1994 to 2016.

The cointegration test has found the existence of long-run relationship among the investigated variables. It turns out that in the long run there is a negative relationship between public debt and investment. Since there is direct link between investment and economic growth, there is an inverse relationship in the public debt economic growth nexus. The ECM confirmed that the system can adjust to equilibrium at a speed of 17%. There is bi-directional Granger causality relationship between public debt and economic growth. The impulse response function has found that one standard deviation shock in public debt inversely affects economic growth. Variance decomposition results indicate that a shock to public debt account for 16.39% fluctuations in economic growth.

Public debt should be used for projects of investment that should translate into economic growth and jobs, which ultimately improve well-being for citizens. Therefore, it is recommended that a capital scarce country like South Africa can be encouraged to borrow so that there is an increase in the accumulation of capital. However, public debt needs to be managed and kept under control as high debt would have negative effects in the long run and the later stage of borrowing marked with high debt will lead to subdued growth. For future areas of research, it can be explored whether the quality of public sector, such as with lower rate of mobilizing revenue, low transparency and poor budget management, can influence economic growth so as to reduce public debt.

Additional information

Funding

Notes on contributors

Thobeka Ncanywa

Thobeka Ncanywa is a Senior Lecturer (PhD) at the University of Limpopo in South Africa. She has expertise in Micro Economics, Education Economics and Macro Economics. She has worked as an educator in the Department of Education (1993–2012) and joined the University ecosystem as a Lecturer from 2012 to date. She has published in international journals and also presented research articles in Conferences.

Marius Mamokgaetji Masoga

Marius Mamokgaetji Masoga is a Masters student at the University of Limpopo. He participated in several activities such as research workshops, research conferences and GTAC and National Treasury Winter School amongst others. In 2017, Marius was selected as semi-finalist (top 20) of Nedbank and Old mutual budget speech competition.

References

- Acemoglu, D., & Robinson, J. (2008). The role of institutions in growth and development. Commission on Growth and Development Working paper, No.10.

- Agim, K. (2014). Revisiting the public debt-growth puzzle: Evidence from Balkan countries. International Journal of Business and Economics Perspective, 9(1), 150–162.

- Baaziz, Y. (2015). Does public debt matter for economic growth? Evidence from South Africa. Journal of Applied Business Research, 31(6), 2187–2196.

- Baseerit, N. (2005). Thresholds in debt-growth relationship. Paper presented at PhD conference at the University of Leicester..

- Biza, R. A., Kapingura, F. M., & Tsegaye, A. (2013). Do budget deficit crowd out private investment? An analysis of the South African economy. Paper presented at the Financial Globalisation and Sustainable Finance: Implications for Policy and Practice, Cape Town.

- Boccia, R. (2013). How the United States’ high debt will weaken the economy and hurt Americans, backgrounder, The Heritage Foundation. Leadership for America, no. 2768.

- Bonga, W. G., Chirowa, F., & Nyamapfeni, N. (2015). Growth–debt nexus: An examination of public debt levels and debt crisis in Zimbabwe. Journal of Economics and Finance, 6(2), 09–14.

- Bum, S. K. (2009). Impact of the global financial crisis on Asia-Pacific real estate markets: Evidence from Korea, Japan, Australia and U.S. REITs. Pacific Rim Property Research Journal, 15, 398–416. doi:10.1080/14445921.2009.11104288

- Checherita, C., & Rother, P. (2010). The impact of high and growing public debt economic growth: An empirical investigation for the Euro Area. Journal of European Economic Review, 56(4), 1392–1405. doi:10.1016/j.euroecorev.2012.06.007

- Cheng, F. F., & Annuar, N. (2012). Dynamic relationship between bonds yields Malaysia, Singapore, Thailand, India and Japan. International Journal of Academic Research in Business and Social Sciences, 2(3), 220–229.

- Chirwa, T. G., & Odhiambo, N. M. (2015). Growth dynamics in South Africa: Key macroeconomic drivers and policy challenges. Journal of Global Analysis, 5(2), 10–31.

- Churchman, N. (2001). David Ricardo on public debt (First ed.). UK: Palgrave Macmillan, Studies in history of Economics.

- Cohen, D. (1993). Low investment and large LDC debt in the 1980s. American Economy Review, 83(2), 437–449.

- Dao, B. T. (2013). The relationship between budget deficit and economic growth in Vietnam. Online article, Retrieved from: https://ssrn.com/abstract=2514134

- Diaz, E. (2010). Internal public debt, interest rate and restriction on productive investment. Comercio exterior, 60(1), 38–56.

- Dolado, J. J., Gonzalo, J., & Marmol, F. (1999). Cointegration: Department of Economics, Department of Statistics and Econometrics. Universidad Carlos III de Madrid.

- Eberhardt, M., & Presbitero, A. F. (2015). Public debt and growth: Heterogeneity and non-linearity. Journal of International Economics, 97, 45–58. doi:10.1016/j.jinteco.2015.04.005

- Ekaterini, K. (1998). Testing for serial correlation in multivariate regression models. Journal of Econometrics, 86(2), 193–220. doi:10.1016/S0304-4076(97)00114-0

- Fadli, F. A., Nurul, S. B., Nurmadihah, J., Zuraida, M., Norazidah, S., & Kamaruman, J. (2011). A vector Error Correction Model (VECM) approach in explaining the relationship between interest rate and inflation towards exchange rate volatility in Malaysia. Journal of World Applied Sciences, 12(3), 49–56.

- Ferraz, R., & Duarte, A. P. (2015). Economic growth and public indebtedness in the last four decades: Is Portugal different from the other PIIGS’ economies? Naše gospodarstvo/Our Economy, 61(2), 3–11. doi:10.1515/ngoe-2015-0021

- Fincke, B., & Duarte, A. P. (2015). On the relation between public debt and economic growth: An empirical investigation.

- Greiner, A. (2013). Sustainable public debt and economic growth under wage rigidity. Metroeconomica, 64(4), 272–292. doi:10.1111/meca.12006

- Griliches, Z. (1961). A note on serial correlation bias in estimates of distributed lag. Journal of Econometrica, 29(3), 65–73. doi:10.2307/1907688

- Hoag, A. J., & Hoag, J. H. (2006). Introductory economics (fourth ed.). Word Scientific publishing Co PTC Ltd.

- Iyoha, M. A. (1999). External debt and economic growth in Sub Saharan African countries: An econometric study. Nairobi: African Economic Research Consortium.

- Jacobs, D., Schoeman, N., & Van Heerden, J. (2002). Alternative definitions of the budget deficit and its impact on the sustainability of fiscal policy in South Africa. Economist, IMF; Professors, Department of Economics, University of Pretoria, Pretoria.

- Jaejoon, W., & Manmohan, S. K. (2014). Public debt and growth: International monetary fund, Washington, DC. Journal of Economica, 82(8), 705–739.

- Jung, W. S. (1986). Financial development and economic growth: International evidence. Economic Development and Cultural Change, 34(12), 333–346. doi:10.1086/451531

- Kamudia, S. (2015). The effects of public debt on private investment and economic growth in Kenya (1980–2013). Thesis

- Kibet, K. S. (2013). Effects of budget deficit and corruption on private investment in developing countries: A panel data analysis. African Journal of Business Management, 7(27), 2720–2732.

- Kleiber, C., & Zeileis, A. (2008). Applied econometrics with diagnostics and alternative methods of regression (First ed.). Econometrics/Statistics. New York.

- Kourtellos, A., Stengos, T., & Tan, C. M. (2013). The effect of public debt on growth in multiple regimes. Journal of Macroeconomics, 38(8), 35–43. doi:10.1016/j.jmacro.2013.08.023

- Kraay, A., & Vikram, N. (2006). When is external debt sustainable? The World Bank Economic Review, 20(3), 341–365. doi:10.1093/wber/lhl006

- Lopes, J. A., Ferreira-Lopes, A., & Sequeira, T. N. (2015). Public debt, economic growth and inflation in African economies. South African Journal of Economics, 84(2), 294–322. doi:10.1111/saje.12104

- Makin, A. J. (2015). Has excessive public debt slowed world growth? Economics, 16(4), 1–17.

- Marek, D. (2014). Factors determining a safe level of public debt. National Research University Higher School of Economics, Moscow Fellow, Centre for Social and Economic Research. email: [email protected]

- Marek, H., Shakill, H., Yashvir, A., & Luchelle, S. (2016). South Africa and the ghost of a rating downgrade to sub-investment grade. Macroeconomics and Fiscal Management-MFM Practice Notes. Washington, D. C.

- Medeiros, O. L., Cabral, R. S. V., Baghdassarian, W., & Almeida, M. A. (2005). Public debt strategic planning and benchmark composition. Brazil: National Treasury Secretariat, Ministry of Finance.

- Megersa, K., & Cassimon, D. (2015). Public debt, economic growth, and public sector management in developing countries: Is there a link? Journal of Public Administration and Development, 35(13), 329–346. doi:10.1002/pad.1733

- Modgliani, F. (1961). Long run implications of alternative fiscal policies and the burden of national debt. Economic Journal, 71, 730–755. doi:10.2307/2228247

- Mohanty, A. R., & Mishra, B. R. (2016). Impact of public debt on economic growth: Evidence from Indian states. Vilakshan, XIMB Journal of Management, 13(6), 1–21.

- Mongale, I. P., Petersen, J. M., Meniago, C., & Petersen, M. A. (2013). Household savings in South Africa: An econometric analysis. Mediterranean Journal of Social Sciences, 4(2), 519–530.

- Moss, T. J., & Chiang, H. S. (2003). The other costs of high debt in poor countries: Growth, policy dynamics and institutions. Issue paper on debt sustainability, No. 3, Centre for Global development: Washington D.C.

- Nantwi, V. O., & Erickson, C. (2016). Public debt and economic growth in Ghana. African Development Review, 28(4), 116–126. doi:10.1111/1467-8268.12174

- National Development Plan. (2011). Our future makes it work. Executive summary, 2030, National planning commission.

- Panizza, U., & Presbitero, A. F. (2014). Public debt and economic growth: Is there a causal effect? Journal of Macroeconomics, 41(2), 21–41. doi:10.1016/j.jmacro.2014.03.009

- Pascal, E. C. (2012). Public debt management. UNESCO-EOLSS Encyclopedia, ref. 6. 28.39.EOLSS.

- Pesaran, M. H. (2002). Market timing and return prediction under model instability. Journal of Empirical Finance, 9(2), 495–510. doi:10.1016/S0927-5398(02)00007-5

- Pesaran, M. H., & Shin, Y. (1997). An autoregressive distribution lag modelling approach to cointegration analysis. England: University of Cambridge.

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationship. Journal of Applied Econometrics, 16(3), 289–326. doi:10.1002/jae.616

- Qudah, A. M. (2016). Public debt, external debt and economic growth of Jordan. International Journal of Research in Commerce and Management, 7(4), 11–16.

- Rajan, R. (2005). Debt relief and growth. Finance and Development, 42(2), 1–4.

- Ramirez, R., & Erquizio, A. (2012). Analysis of the electoral political cycle based on public expenditure variables by state in Mexico, 1993–2009. Paradigma Economica, 4, 5–27.

- Ramos, M., Veronique, R., Helene, M., & Margaret, C. (2013). Impact of fiscal policy in an intertemporal CGE model for South Africa. Journal of Economic Modelling, 31(4), 775–782. doi:10.1016/j.econmod.2013.01.019

- Reinhart, C. M., & Rogoff, K. S. (2010). Growth in a time of debt. American Economic Review, 100(2), 573–578. doi:10.1257/aer.100.2.573

- Romp, W., & De Haan, J. (2005). Public capital and economic growth: A critical survey. European Investment Bank Papers, 10(1), 47–70.

- Saint-Paul, G. (1992). Fiscal policy in an endogenous growth model. The Quarterly Journal of Economics, 107(4), 1243–1259. doi:10.2307/2118387

- Sanchez-Juarez, I., & Garcia-Almada, R. (2016). Public debt, public investment and economic growth in Mexico. International Journal of Financial Studies, 4(6), 1–14. doi:10.3390/ijfs4020006

- Say, J. B. (1880). A treatise on political economy on the production, distribution and consumption of wealth. (C. R. Prnsep, Ed). Philadelphia: Claxton, Remsen and Haffelfinger.

- Shrithongrung, A., & Kriz, K. (2014). The impact of subnational fiscal policies on economic growth: A dynamic analysis approach. Journal of Policy Analysis Management, 33, 912–928. doi:10.1002/pam.21784

- Sorenson, E. (2005). Granger causality. Journal of Economics, 1(1), 1–4.

- Soytas, U., & Sari, R. (2003). Energy consumption and GDP: Causality relationship in G-7 countries and emerging markets. Energy Economics, 25(1), 33–37. doi:10.1016/S0140-9883(02)00009-9

- Stern, D. I. (2011). From correlation to Granger causality. Crawford School of Economics and Government, Australian National University: Canberra, ACT 0200, Australia. e-mail: [email protected]

- Stylianou, T. (2014). Debt and economic growth: Is there any causal effect? An empirical analysis with structural breaks and Granger causality for Greece. Theoretical and Applied Economics, XXI, 51–62.

- Swanson, N. R., & Granger, C. W. J. (1997). Impulse response functions based on a causal approach to residual orthogonalization in vector auto regressions. Journal of American Statistical Association, 92(437), 357–367. doi:10.1080/01621459.1997.10473634

- Tabengwa, G. K. (2014). Impact of shocks to public debt and government expenditure on human capital and growth in developing countries. Journal of Economics and Behavioural Studies, 6(1), 44–67.

- Tsoulfidis, L. (2007). Classical economists and public debt. International Review of Economics, 54(1), 1–12. doi:10.1007/s12232-007-0003-8 Retrieved from

- Yanikkaya, H. (2003). Trade openness and economic growth: A cross-country empirical investigation. Journal of Development Economics, 1(72), 57–89. doi:10.1016/S0304-3878(03)00068-3

- Yasemin, B. G. (2017). Debt sustainability in low-income countries: Policies, institutions, or shocks? International Monetary Fund, Working Paper, No. 17(114).

- Zeilies, A., & Hothorn, T. (2002). Diagnostic checking in regression relationships. R News, 2(3), 7–10. Retrieved from http://cran.r-project.org/package=AER