Abstract

This study examines the link between bank restructuring and bank efficiency in Vietnamese banks employing the Data Envelopment Analysis (DEA) and Stochastic Frontier Analysis (SFA) approach. The data sample includes 26 commercial banks over the period 1999–2015. Our finding indicates that Vietnamese government’s restructuring policies in the first stage have not been beneficial for banks implementing restructuring. Regarding the effect of different restructuring methods, we show that the privatization of state-owned commercial banks, state intervention and mergers and acquisitions (M&As) do not substantially improve efficiency. Besides, we find that bank efficiency declines during bank restructuring period because of not only transition cost but also the change of other environment variables, such as financial crisis or domestic economy slowdown.

PUBLIC INTEREST STATEMENT

This article examines the link between bank restructuring and bank efficiency in Vietnamese banks employing the DEA/SFA approach. The data sample includes 26 commercial banks over the period 1999–2015. Our finding indicates that Vietnamese government’s restructuring policies in the first stage have not been beneficial for banks implementing restructuring. Regarding the effect of different restructuring methods, we show that the privatization of state-owned commercial banks, state intervention and mergers and acquisitions (M&A) do not substantially improve efficiency. Besides, we find that bank efficiency declines during bank restructuring period because of not only transition cost but also the impact of other environment variables, such as financial crisis or domestic economy slowdown.

1. Introduction

The link between bank restructuring and bank efficiency is an appealing area that draws strong attention from both academic and industry practitioners. Vietnam offers an interesting case to analyze this link however this issue remains unexplored. This paper investigates the association between bank restructuring and bank efficiency in Vietnamese banking system. We employ the Data Envelopment Analysis (DEA) and Stochastic Frontier Analysis (SFA). Our data sample includes 26 commercial banks covering the period 1999–2015.

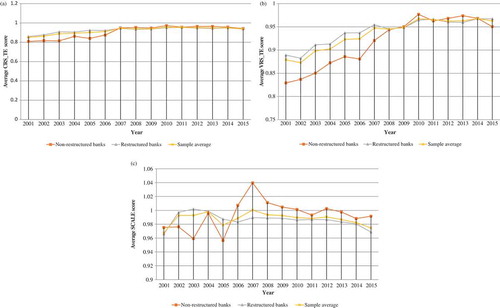

Figure 2. Comparison of performances between non-restructured banks and restructured banks (Step 1 and Step 3 DEA).

Note: CRS_TE: constant variable to scale of technical efficiency; VRS_TE: variable return to scale technical efficiency; SCALE: Scale efficiency.

A huge volume of previous studies suggest that financial reform improves efficiency. For example, Berg and Jansen (Citation1992) and Zaim (Citation1995) claim that bank efficiency is improved after deregulation. Similarly, Kumbhakar and Sarkar (2003) assert that the performance of private banks is improved as a result of financial deregulation. Brissimis, Delis, and Papanikolaou (Citation2008) find a positive impact of banking sector reform on banking efficiency. Koutsomanoli-Filippaki, Margaritis, and Staikouras (Citation2009) conclude that the productivity of Central and Eastern Europe improves because of the implementation of institutional and structural reforms during the time 1998–2003.

In contrast, many other studies find that financial reform has no impact on efficiency. For example, banking efficiency of large banks in the United States is relatively unchanged by deregulation (Elyasiani & Mehdian, Citation1995). Park and Weber (Citation2006) provide empirical evidence to assert that bank efficiency declines in Korea over the period 1992–2002. In addition, Fu and Heffernan (Citation2009) state that X-efficiency drops substantially and banks’ operation are below efficiency scale in Chinese banking system.

In another study, Banker, Chang, and Lee (Citation2010) investigate the impact of banking system reforms on bank productivity. Their empirical results indicate that the average technical efficiency of Korean commercial banks decreases during the financial crisis of 1997–1998, improves within three years later as bank restructuring occurs, and continues to improve through 2005. Besides, Banker et al. (Citation2010) finds that regulatory changes aiming at strengthening bank’s capital structure and improving risk management do not have any impact on bank productivity.

Previous studies on the link between bank restructuring and efficiency focus on changing bank efficiency score pre, during and post restructuring period. However, not many studies separate the impact of environment variables from the effect of the bank restructuring approach. To address this issue, we use the three stage DEA/SFA method to investigate the impact of bank restructuring on efficiency. This approach allows us to separate the environment impact from the restructuring impact.

Vietnamese government has started the privatization of state commercial banks to push these banks reaching the regional and international prudential standards since 2000. However, restructuring activities are not strongly and intensively conducted until 2005. During period from 2007 to 2008, two largest state commercial banks including Vietcombank and Vietinbank go through privatization. After the privatization process, their financial strength indicators increase significantly and their nonperforming loan ratios are among the lowest level. Moreover, these banks play an important role in the financial market after the privatization. Currently, Vietcombank and Vietinbank are two commercial banks having the largest charter capital in Vietnam. Their total assets have risen significantly.

In addition, some other banks enter the financial system from the transformation of rural commercial banks into urban ones during the period 2005–2007. The “upgrade” of these banks in the banking system is an extremely important step. It not only raises charter capital of commercial banks, but also changes the management mechanism in accordance with the international trend.

Over the period from 2011 to 2013, weak banks are urged to perform restructuring. This program is supported and monitored by the government and the State Bank of Vietnam. During this phase, different forms of restructuring include recapitalization,Footnote1 M&As, privatization, assistance from the State Bank of Vietnam, and the establishment of Vietnam Asset Management Company (VAMC) to solve the non-performing loans problem. In recent years, M&As is an important method to restructure banks in Vietnam (Vo, Citation2018, forthcoming).

The paper has relevant policy implications. Bank restructuring is an important program for emerging countries to build a prudential financial system. Evaluating the association between restructuring program and bank efficiency is important to achieve a successful implementation of government policy.

The remainder of this paper is structured as follows. The global evidence of bank restructuring and bank efficiency is introduced in Section 2. The sample data and methodology used to test the hypothesis related to the research questions are presented in Section 3. The empirical results for the hypothesis testing of the research questions are reported in Section 4. Finally, Section 5 concludes the paper.

2. Restructuring and bank efficiency

2.1. Mergers among domestic banks

During the Asian banking crisis, mergers are an effective approach employed by Asian countries to contain severe banking problems. Mergers are considered the least costly way to restructure banking system (Hawkins & Turner, Citation1999). At the same time, Berger, Demsetz, and Strahan (Citation1999) indicate that mergers may improve efficiency if greater diversification improves the risk—return trade-offs. They suggest that regulators may act to encourage consolidation in periods of financial crisis. Athanasoglou and Brissimis (Citation2004) argue that mergers and acquisitions (M&As), in particular those involving small banks, have a positive effect on cost and profit efficiency and that scope exists for further improvement in efficiency. Similarly, Staub, E Souza, and Tabak (Citation2010) suggest that state-owned banks are significantly more cost efficient than foreign, private domestic and private with foreign participation.

However, there is insufficient evidence to support the notion that banks in industrialized countries gains from mergers in developing countries. For example, Krishnasamy, Hanuum Ridzwa, and Perumal (Citation2004) document improvement in production efficiency of Malaysian post-merger banks in 2000–2001. The authors note that the overall rise in total factor productivity is driven more by technological progress of the banking system than individual bank technical efficiency. Moreover, Peng and Wang (Citation2004) suggest that bank mergers could enhance cost efficiency of Taiwanese banks.

Even though there has been many studies showing that M&As have positive effects on banking system efficiency, some authors argue that regulatory reform, large-scale consolidation, and competitive pressure from other European countries have changed substantially the banking environment, with potentially offsetting effects on the overall degree of competitiveness (Angelini & Cetorelli, Citation2003; Berger, Young, & Udell, Citation2001). Additionally, Yudistira (Citation2004) suggests in his research that Islamic banks suffer slight inefficiencies during the global crisis 1998–1999. Efficiency differences across the sample data appear to be mainly determined by country-specific factors.

2.2. Allowing for foreign bank entries

The Vietnamese law on foreign investment is amended in 1995 which comes into effect from 1997. This regulation allows foreign investors the ability to acquire sanitized and recapitalized banks which in some cases had been consolidated with the branch networks and assets of other troubled banks. Between 1997 and 2004, foreign bank penetration recapitalized Mexico’s banking sector by over US$8.8 billion, equivalent to 42% of banking sector capital in 2004 (Schulz, Citation2006). In most Asian countries, barriers to entry have been relaxed and foreign banks have been allowed to increase their presence. A 30% ceiling on foreign ownership of banks is retained in Malaysia, whereas a 60% interest in an existing domestic bank is allowed in Philippines (Unite & Sullivan, Citation2003).

2.3. State intervention or receiving state assistance

The government may directly improve bank capital by purchasing new shares or rolling over long-term debts of the troubled banks (Daniel, Citation1997). Thoraneenitiyan and Avkiran (Citation2009) suggest that the larger concentration of state bank ownership have more unfavourable influence on bank efficiency. Borish, Long, and Noel (Citation1995) indicate that bank recapitalization which is accompanied by changes in bank incentive structures develops better. Fane and McLeod (Citation2002) show that owners provide 20% of the capital shortfall and the remaining 80% is provided by the government under Indonesia’s joint recapitalization program. In particular, Basel III requirements for better-quality capital and liquidity buffers enable institutions to better withstand distress (Lee & Hsieh, Citation2013). Although financial reforms (such as liberalizing direct credit or interest rate control) refer to more liberalization and competition, they may overall bring synergy to diversified banks. Hasan and Marton (Citation2003) analyse the experience and developments of Hungarian banking sector during the transitional process from a centralized economy to a market-oriented system; their paper shows that early reorganization initiatives, flexible approaches to privatization and liberal policies towards foreign banks’ involvement with the domestic institutions helped to build a relatively stable and increasingly efficient banking system. Ariff and Can (Citation2009) report new findings on bank efficiency in East Asian countries for the pre- and post-IMF restructuring periods; they find that bank efficiency has improved, but only to the pre-IMF intervention level, and that restructured banks are not more efficient than their un-restructured counterparts. In addition, some studies investigate that foreign-owned banks are more efficient than domestic-owned banks (Philippon & Schnabl, Citation2013; Walker, Citation1998; Weill, Citation2003).

By contrast, another scientists use panel data econometrics for efficiency measurement and productivity decomposition in the banking system of an emerging economy. Fethi, Shaban, and Weyman-Jones (Citation2012) suggest that in the financial crisis, the attempt to recapitalize banking system has potential to impose significant costs. Similarly, Wruck (Citation1990) find evidence on financial restructuring and distress costs which demonstrates that financial distress has benefits as well as costs, and that financial and ownership structure affect the net costs. Furthermore, Hasan and Marton (Citation2003) examine the impact of bank privatization in transition countries and show that both the method and the timing of privatization matter to performance; specifically, voucher privatization does not lead to increased efficiency and early-privatized banks are more efficient than later-privatized banks, even though we find no evidence of a selection effect.

2.4. The privatization of state-owned commercial banks

Privatization of state commercial banks is an important restructuring approach and several papers show that privatization is a good way to improve banking efficiency. For instance, Eckel, Eckel, and Singal (Citation1997) suggest that a change from government to private ownership improves economic efficiency. Patti and Hardy (Citation2005) state that the privatized banks improve their profit efficiency in the period immediately follow their privatization. Similarly, Berger, Hasan, and Zhou (Citation2009) analyze the efficiency of Chinese banks over 1994–2003. Their results conclude that Big Four banks are by far the least efficient; foreign banks are most efficient; and minority foreign ownership is associated with significantly improved efficiency. Nakane and Weintraub (Citation2005) indicate that state-owned banks are less productive than their private peers, and that privatization increases productivity. Williams and Nguyen (Citation2005) find that state banks are less efficient than private banks and privatization can increase revenue and total assets of each bank in the short to medium term.

On the other hands, some papers argue that privatization does not seem to have an immediate effect on improved efficiency (Clarke, Cull, & Shirley, Citation2005; Kraft, Hofler, & Payne, Citation2006; Williams & Nguyen, Citation2005). In addition, Boubakri, Cosset, Fischer, and Guedhami (Citation2005) suggest that banks selected for privatization have a lower economic efficiency, and a lower solvency than banks with government ownership. Kraft and Tırtıroğlu (Citation1998) find that new banks are shown to be more X-inefficient and more scale-inefficient than either old privatized or old state banks.

3. Data and methodology

3.1. Data

We have the data for 26 banks’ financial statements from Bankscope covering the period from 1999 to 2015 due to the limited availability (The list of banks which perform restructuring is in Appendix). We divide the sample period into two stages, first period from 1999 to 2006 and second period from 2007 to 2015 to investigate the difference of bank efficiency between pre and during restructuring period. Firstly, we choose the pre-restructuring period from 1999 to 2006 since 2006 was the year that State bank of Vietnam began to prepare for banking restructuring plan and also in that time, Vietnam participated in WTO—open to a general opportunity for the commodity and service of Vietnam to a larger market. Secondly, because Government’s banking restructuring proposal according to decision No. 254/QĐ-TTg lasted until 2015, we finish our research period at 2015. Therefore, all banks are obtained to get original inputs and outputs the research period, from 1999 to 2015. The sample includes banks which are influenced by the banking crisis in 2008 then implement restructure. Annual data are used to measure technical efficiencies. Unconsolidated financial data obtained from the Bankscope database are used to analyse the changes in bank performance during the implementation period of pre, during restructuring.

Besides, we categorize the sample into two main groups: (1) a group of banks without restructuring, and (2) a group of banks implementing restructuring measures. We further divide the second group into three sub-groups of banks to examine the impact of different restructuring measures. These groups include (i) banks subjected to merger and acquisition; (ii) banks with State Bank of Vietnam or government intervention; and (iii) banks which are result of privatization of state-owned commercial banks.

3.2. Methodology

The Data Envelopment Analysis (DEA) approach identifies the best-practice decision making units (DMU) on the efficient frontier and determines the inefficiencies for the others in the sample accordingly. The DEA frontier is formed as the piecewise linear combinations that connect the set of these best-practice observations, yielding a convex production possibilities set.

Stochastic frontier analysis (SFA) is a method of economic models. It has its starting point in the production model at random frontier is introduced by Meeusen and Van Denk Broeck (Citation1977). SFA has reviewed efficient “cost” and “profit” Approach “Marginal Costs” to measure the degree to minimize overall costs (i.e. cost-effectively) company. Pattern-wise, not negative component cost inefficiencies are added rather than in random specification. ”Analysis of margins” will consider the case of the manufacturer is considered to be the manufacturer of profit maximization (both output and input to the company’s decision) and not cost reduction (in which the output level is considered to be exogenous). The specification here is similar to the “production frontier” one.

Avkiran and Rowlands (Citation2008) introduce a three-stage DEA/SFA analysis. In this method, total input and output slacks are estimated at the same time against the same reference set. The three-step DEA/SFA technique could separate the effect of restructuring methods and environment variables on bank efficiency. This allows for the analysis of factors affecting bank efficiency during bank restructuring period. In this paper, we adopt this method to consider the environmental effects in our analysis.

3.3. Environmental variables

To investigate the impact of environmental factors (zj) that may distort the validity of the initial efficiency analysis, three bank restructuring measures and six country-specific factors are included in the second-stage analysis. The first group of independent variables was used to test the association between restructuring measures and bank efficiency. These include dummy variables for domestic banks in different subgroups: mergers and acquisitions (M&As), privatization (COP) and state intervention (SI).

3.3.1. Data envelopment analysis

As mentioned previously, Data Envelopment Analysis (DEA) approach is a linear programming technique that identifies the best-practice decision making units (DMU) on the efficient frontier and determines the inefficiencies for the others in the sample accordingly. The DEA frontier is formed as the piecewise linear combinations that connect the set of these best-practice observations, yielding a convex production possibilities set. Therefore, DEA does not require the explicit specification of the underlying production relationship. However, DEA assumes there is no noise in constructing the frontier and no luck that temporarily gives a DMU a better measured performance over other units. Thus, any error in a unit’s data may be reflected as a change in its measured efficiency.

Furthermore, the inconclusive conclusion in the current literature on which factors (external or environmental factors) influence the sample homogeneity assumption leads to the bias in relative efficiency scores. For example, Berger and Humphrey (Citation1992) suggest that banking industry is extremely sensitive to macro-economic conditions and banking crises are more likely to affect bank efficiency.

3.3.2. Data envelopment analysis with the consideration of environmental effects

We use three-step DEA which allows us consider and assess the association of external or environmental factors besides the influence of three restructuring methods (M&As, government intervention, and privatizing state-owned commercial banks) for bank efficiency. This method is carried out as follows:

Step 1: Since our data range from 1999 to 2015 and the Vietnamese bank restructuring starts from 2007 to 2015, we divide our sample period into two stages. The first period is from 1999 to 2006 (pre-restructuring) and second is from 2007 to 2015 (during restructuring).

Step 2: Input and output variables from banks obtained from stage 1 are used for decomposing. The SFA regressions are then used to obtain inputs and outputs adjusted for the effect of restructuring methods and environment factors.

Step 3: Combining the non-oriented analysis in step 1 with adjusted input and output data obtained from step 2 and then comparing two results.

In our paper, three inputs and three outputs are used in step 1. We include deposits (TD), interest expense (IE) and non-interest expense (NE) as the input variables. Three bank outputs are used to capture both traditional and non-traditional activities of banks including total loans (TL), interest revenue (IR) and non-interest revenue (NR).

In DEA, three inputs and three outputs under the intermediation approach are specified productivity model. Assuming that a bank plays a crucial role as an intermediary in the financial system to mobilize funds between depositors and borrowers at the lowest cost, the total deposits, interest expense and non-interest expense are chosen as the input variables. These variables have been widely used in the bank efficiency literature. The amount of total deposits is proposed as the first input in the analysis. Although purchased funds might be of interest, its use is hampered by lack of availability of such data in many banks, particularly small banks. The second input, interest expenses, represent interest payable on any type of borrowings—bonds, loans, convertible debt or lines of credit. It is basically calculated by the proxy measure of personnel expenses. Finally, non-interest expenses, including employee salaries and benefits, equipment and property leases, taxes, loan loss provisions and professional service fees, measure the operating costs. Three bank outputs capture both traditional bank lending activities and non-traditional activities: total amount of loans, interest revenue and non-interest revenue. Total amount of loans is adjusted for nonperforming loans in order to compare banks on the same level playing field in terms of loan quality. Interest revenue account reports the interest earned by a bank during the time period indicated in the heading of the income statement in opposition to non-interest revenue. As suggested by Isik and Hassan (Citation2002), non-traditional bank functions such as off-balance sheet activities are becoming more important and exclusion of these items may bias bank performance measurement.

3.3.3. Environmental variables in step 2

To discover the impact of environmental factors on the validity of the initial efficiency analysis, three bank restructuring measures, six country-specific factors are included in step 2.

The first group of independent variables was used to test the association between restructuring measures and bank efficiency including dummy variables for domestic bank mergers and acquisition (M&As), privatization (COP) and state intervention (SI). These variables are defined as follows.

M&As: the mergers and acquisitions of two or more domestic banks, while maintaining the majority of domestic ownership in the period from 2011 to 2015, both voluntary and mandatory. Banks which have merger take value of 1 and 0 otherwise.

Privatization: the state or government agency decision in implementing a privatization of state-owned commercial banks between 2007 and 2015. Bank which has privatization take the value of 1 and 0 otherwise.

State intervention: Bank takes the value of 1 if it has the state intervention and 0 otherwise.

Table summarizes the variables employed in the analysis.

Table 1. The environment variables include six variables representing country-specific factors

In this SFA model, three inputs and three outputs are independent variables, and three restructuring variables and environment variables are dependent variables. If independent variables have a positive effect on dependent variables suggesting that independent variables have positive effect on inefficiency (Avkiran & Rowlands, Citation2008). Step 3 is similar to the step 1 of the DEA approach; however, the inputs and outputs are replaced with the adjusted inputs and outputs obtained in step 2.

To analyses the efficiency of banking system, we use three efficiency indicators including constant variable to scale of technical efficiency, variable return to scale technical efficiency and scale efficiency. These three indicators are calculated using Stata package.

4. Empirical results

4.1. Step 1: Initial results

Table presents the Summary statistic of dummy variables and six variables representing country-specific factors. According to data collected, Vietnam’s GDP growth rate in 1999 was 4.8% and to 6.7% in 2015 (IMF). GDP growth accelerated from 6.8% in 2000 to 8.5% in 2017. The highest GDP growth rate over the 16 years in the study period was 8.5% in 2007, before the global financial crisis in 2008. Then the GDP growth rate decreased from 6.3% in 2012 due to the consequences of the economic crisis. By 2013, Vietnam’s economy gradually regains its stability and growth. GDP growth started to rise slightly from 5.4% to 6.7% in 2015. The lowest real interest rate was −5.2% in 2007 and the highest was 7.3% in 2015. Change in terms of trade fluctuations unstable over the years. Inflation in 1999 was 4.1%, and then fluctuated between −1.7% and 6.5% from 2000 to 2015. However, the Inflation index in 2008 and 2011 was unusually high due to the global financial crisis, they are 23.1% and 18.7% respectively. Real domestic credit growth was the lowest at 8.9% in 2012 and the highest at 51.4% in 2007. The figures show that Vietnam has achieved remarkable growth in the transition period. However Vietnam also faces up with the high volatility in the economy, such as the impact of the global economic crisis, high volatility of inflation, fiscal deficits, exchange rate fluctuations, etc. In general, Vietnam Economics gradually gained stability from 2013 to 2015.

Table 2. Summary statistic of dummy variables and environment variables

Table presents descriptive statistics on efficiency variables from DEA model and explanation variables. The lower and upper quartiles of the efficiency scores in DEA step 1 are 0.7570 and 1.1193, respectively. The mean of technical efficiency scores is 0.9292 and the standard deviation is 0.03. In DEA step 3, under affection of many factors as 3 restructuring methods and 6 environmental variables as well as the combination of these two group of former factor, the minimize of technical efficiency is 0.9778, scale technical efficiency is 0.9809 and scale efficiency is 0.9872, the minimize happens when the efficiency was affected by all nine variables, the different among these efficiency score are not large and they are relative to the maximize of them. The gap of operating efficiency among commercial banks over this period is relatively small as the banks are closely supervised and comply with common policies imposed by the State Bank of Vietnam.

Table 3. Descriptive statistics of step 1 and step 3 DEA’s variables

Table 4. SFA regression step 2

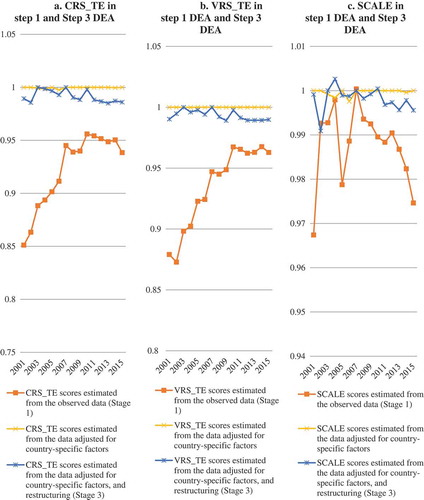

In analysing the results of DEA step 1 (Figure ), the average operating efficiency increases from 85% to more than 95% between 1999 and 2011, then decrease in the period 2011–2015 (a decrease from a peak of more than 95% to less than 93% in 2015). This might be because of the banking crisis and restructuring policies of government. This is commonly viewed as the transition costs during restructuring (Hsiao, Chang, Cianci, & Huang, Citation2010). We also find that the efficiency declines during the early stage of restructuring period as a transition cost to transfer from the old model to the new one. This finding is consistent with the results of Taiwan banking system (Hsiao et al., Citation2010). To analyse the connection among the restructuring, environment variables and performance of commercial banks in Vietnam during the sample period, we carried out step 2.

Figure 1. Bank efficiency in DEA step 1 and step 3.

Note: CRS_TE: constant variable to scale of technical efficiency; VRS_TE: variable return to scale technical efficiency; SCALE: Scale efficiency.

By comparing performance of banks implemented restructuring and those do not implement restructuring, the results show the effectiveness of the restructuring where efficiency of restructuring bank during the period 1999–2008 is higher than that of banks which do not implement restructuring. This is the period of high economic growth and central bank conducts monetary policy extensions. However, before 2009, the efficiency of banks implementing restructuring is sharply lower than that of banks which do not implement restructuring. This is explained by the fact that during the period 1999 and 2008, these banks aggressively pursue profits and conduct extensive lending expansion to boost profit.

However, after 2009, due to the influence by the global economic crisis and other domestic factors, these banks severely suffer from huge bad debts. Moreover, liquidity risk increases resulting in a reduction of operational efficiency. These banks are required to implement restructuring measures by the government.

Besides, the results also show that in the first phase of the restructuring program from 2011 to 2015, performance of banks which implementing restructuring continues to decline. This is partly because of the restructuring measures are not effective, as described in step 2 and partly because of the transition cost in the early stages make the banks incur greater costs to generate output factors. This is consistent with prior studies, for example, Hsiao et al. (Citation2010) and Thoraneenitiyan and Avkiran (Citation2009), which show that bank efficiency drops during restructuring period and this is considered as transition cost. However, a main difference in our result is that bank efficiency drops during restructuring not only transition cost but also the impact of environment variables, such as financial crisis or the weakness of domestic economy.

Step 2: SFA regression results

Table represents the regression estimates by applying SFA step 2. The results indicate a positive relationship between M&As and most of bank input and output slacks. In other words, merged banks manage resources less efficiently during post-restructuring period because takeover banks bear the inefficiency of other banks.

Conversely, the coefficients of COP and SI are both positive and statistically significant. A positive relationship between SI and bank inefficiencies is consistent with the current literature (Hawkins & Turner, Citation1999; Thoraneenitiyan & Avkiran, Citation2009). Detailed results show that the rate has higher effect on SI input variables than the output variables. This reveals the fact that banks which are supported by the government through recapitalization face higher marginal costs to generate revenue or lower efficiency. This is consistent with the practical fact in Vietnam where most banks received government support are state-owned commercial banks. These banks often incur higher expenses to sponsor government and community activities.

The privatization of state-owned commercial banks increases input and output variables which are equivalent to the increase in bank inefficiency. A positive relationship between COP and input, output variables is inconsistent with previous literature on privatization in the context of emerging countries which finds private banks are more efficient than state-owned commercial banks. The results reveal that the privatization is nominal since the government still holds a huge number of shares in state-owned commercial banks after privatization process which does not lead to spontaneous efficiency.

The results show that in addition to the effect of restructuring variables, bank performance is also affected by environmental variables such as growth, interest, trade, credit growth, inflation and fiscal policy. Specially, economic growth has a negative effect on inefficient index. Interest rates have a positive and significant effect on the inefficiency index. Rising interest rates will increase the cost for enterprises. Further, increased inflation also reduces the operational efficiency of commercial banks.

Step 3: DEA results on adjusted data

Figure shows step 3 DEA efficiency scores, adjusted the association between the influence of restructuring variables and the operating environment variables. The results suggest that after adjusting the operating environment, efficiency scores improve substantially and exhibit less dispersion. This supports the proposition that some banks that operated in a low (or high) efficiency, partly because the environment is also affected by restructuring programs and other country-specific factors.

Figure also shows comparisons of efficiency scores between step 1 and step 3 DEA. The step 1 is estimated by using observed data representing bank managerial efficiency only. After that, in step 3, we adjust the country-specific factors and re-calculate efficiency scores. The higher efficiency scores after adjusted for country-specific factors suggest that country-specific factors has a negative effect on bank efficiency estimates because when its effect is adjust the efficiency scores are, on average, pulled up by 6–15%. Then, the efficiency scores after adjusted all effects (step 3) are the highest, confirming that restructuring measures and country-specific factors have negative effects on bank efficiency estimates. The key message here is that the largest effect on bank efficiency is attributed to country-specific factors, whereas the influence of restructuring is relatively low.

Besides, the results in Figure also show that in the first stage of the restructuring from 2011 to 2015 under the restructuring scheme of the government, the performance of banks implementing restructuring continues to decline, partly because of the restructuring measures are not effective, as described in step 2, partly because of transition cost in the early stages make the banks incur greater costs to generate output factors.

5. Conclusion

Our paper describes the overall picture of the restructuring process in Vietnam’s early stages. The study offers an analysis of bank restructuring in a small and transitional economy. We find that the privatization of state-owned commercial banks is not effective in improving efficiency because the government still maintains major holdings. Moreover, as indicated in previous studies, there is a positive relationship between state intervention and bank inefficiency. Most of state-owned banks backed by the government through recapitalization sustain higher marginal costs to generate revenue with higher inefficiency. In addition, the consolidation and merger of banks has some positive effects. The risk of bad debt and liquidity of troubled banks leads to the decrease in effectiveness of bank consolidation. With regard to the effect of restructuring methods, we show that the change of bank ownership of state-owned commercial banks does not change much the operational structure of commercial banks. Therefore we suppose that government should decrease its intervention in market, actively allow privatization the state-owned commercial bank as well as continue to integrative policies to enhance competition and transparency of banking system.

Overall, the finding suggests that the first restructuring phase has not improved the operating efficiency of commercial banks. However, this results in transition cost and dead weight losses that taxpayers must bear. Further, the system of commercial banks faces many other issues such as partial privatization, and the inequality between state-owned commercial banks and private banks in getting government support. In addition, we find that the environmental variables strongly affect bank performance. Particularly, economic growth and operational efficiency are a positive relationship while interest rates and inflation has a negative impact on performance.

The results have implications for government policies, especially in emerging markets. Conducting bank restructure is important to improve the soundness of the banking system. However, it is important to control the associated adverse effects in order to improve the efficiency of the banking system.

Acknowledgements

This paper was presented at the INFINITI Conference, Ireland 2016, and benefited from comments and discussions from conference participants. We acknowledge the constructive comments and helpful suggestions from the two anonymous referees. Financial support from the University of Economics Ho Chi Minh City to conduct this research is acknowledged. Any remaining errors or shortcomings are our own responsibilities.

Additional information

Funding

Notes on contributors

Xuan Vinh Vo

Xuan Vinh Vo is currently working for the University of Economics Ho Chi Minh City and CFVG Ho Chi Minh City. His main research areas are corporate finance, investment management and banking studies.

Huu Huan Nguyen

Huu Huan Nguyen is currently working for the University of Economics Ho Chi Minh City. His expertise is in Banking and Finance. His main research areas are corporate finance, investment management and banking studies.

Notes

1. M&As: Mergers and Acquisitions.

References

- Angelini, P., & Cetorelli, N. (2003). The effects of regulatory reform on competition in the banking industry. Journal of Money, Credit, and Banking, 35(5), 663–684. doi:10.1353/mcb.2003.0033

- Ariff, M., & Can, L. (2009). IMF bank-restructuring efficiency outcomes: Evidence from East Asia. Journal of Financial Services Research, 35(2), 167–187. doi:10.1007/s10693-008-0047-2

- Athanasoglou, P., & Brissimis, S. (2004). The effect of M&A on bank efficiency in Greece. Germany: University Library of Munich.

- Avkiran, N. K., & Rowlands, T. (2008). How to better identify the true managerial performance: State of the art using DEA. Omega, 36(2), 317–324. doi:10.1016/j.omega.2006.01.002

- Banker, R. D., Chang, H., & Lee, S.-Y. (2010). Differential impact of Korean banking system reforms on bank productivity. Journal of Banking & Finance, 34(7), 1450–1460. doi:10.1016/j.jbankfin.2010.02.023

- Berg, S., & Jansen, E. S.,, & . (1992). Malmquist indices of productivity growth during the deregulation of Norwegian banking, 1980–89. The Scandinavian Journal of Economics, 94, S211–S28. doi:10.2307/3440261

- Berger, A. N., & Humphrey, D. B. (1992). Measurement and efficiency issues in commercial banking. In Output measurement in the service sectors (pp. 245–300). University of Chicago Press.

- Berger, A. N., Demsetz, R. S., & Strahan, P. E. (1999). The consolidation of the financial services industry: Causes, consequences, and implications for the future. Journal of Banking & Finance, 23(2), 135–194. doi:10.1016/S0378-4266(98)00125-3

- Berger, A. N., Hasan, I., & Zhou, M. (2009). Bank ownership and efficiency in China: What will happen in the world’s largest nation? Journal of Banking & Finance, 33(1), 113–130. doi:10.1016/j.jbankfin.2007.05.016

- Berger, A. N., Young, R. D., & Udell, G. F. (2001). Efficiency barriers to the consolidation of the European financial services industry. European Financial Management, 7(1), 117–130. doi:10.1111/eufm.2001.7.issue-1

- Borish, M. S., Long, M. F., & Noel, M. (1995). Restructuring banks and enterprises: Recent lessons from transition countries. The World Bank.

- Boubakri, N., Cosset, J.-C., Fischer, K., & Guedhami, O. (2005). Privatization and bank performance in developing countries. Journal of Banking & Finance, 29(8), 2015–2041. doi:10.1016/j.jbankfin.2005.03.003

- Brissimis, S. N., Delis, M. D., & Papanikolaou, N. I. (2008). Exploring the nexus between banking sector reform and performance: Evidence from newly acceded EU countries. Journal of Banking & Finance, 32(12), 2674–2683. doi:10.1016/j.jbankfin.2008.07.002

- Clarke, G. R., Cull, R., & Shirley, M. M. (2005). Bank privatization in developing countries: A summary of lessons and findings. Journal of Banking & Finance, 29(8–9), 1905–1930. doi:10.1016/j.jbankfin.2005.03.006

- Daniel, J. A. (1997). Fiscal aspects of bank restructuring. IMF Working Paper, 97, 1. doi:10.5089/9781451847215.001

- Eckel, C., Eckel, D., & Singal, V. (1997). Privatization and efficiency: Industry effects of the sale of British Airways. Journal of Financial Economics, 43(2), 275–298. doi:10.1016/S0304-405X(96)00893-8

- Elyasiani, E., & Mehdian, S. (1995). The comparative efficiency performance of small and large US commercial banks in the pre- and post-deregulation eras. Applied Economics, 27(11), 1069–1079. doi:10.1080/00036849500000090

- Fane, G., & McLeod, R. H. (2002). Banking collapse and restructuring in Indonesia, 1997–2001ʹ. The Cato Journal, 22, 277.

- Fethi, M. D., Shaban, M., & Weyman-Jones, T. (2012). Turkish banking recapitalization and the financial crisis: An efficiency and productivity analysis. Emerging Markets Finance and Trade, 48(sup5), 76–90. doi:10.2753/REE1540-496X4806S506

- Fu, X. M., & Heffernan, S. (2009). The effects of reform on China’s bank structure and performance. Journal of Banking & Finance, 33(1), 39–52. doi:10.1016/j.jbankfin.2006.11.023

- Hasan, I., & Marton, K. (2003). Development and efficiency of the banking sector in a transitional economy: Hungarian experience. Journal of Banking & Finance, 27(12), 2249–2271. doi:10.1016/S0378-4266(02)00328-X

- Hawkins, J., & Turner, P. (1999). Bank restructuring in practice: An overview. BIS Policy Paper, 6.

- Hsiao, H.-C., Chang, H., Cianci, A. M., & Huang, L.-H. (2010). First financial restructuring and operating efficiency: Evidence from Taiwanese commercial banks. Journal of Banking & Finance, 34(7), 1461–1471. doi:10.1016/j.jbankfin.2010.01.013

- Isik, I., & Hassan, M. K. (2002). Technical, scale and allocative efficiencies of Turkish banking industry. Journal of Banking & Finance, 26(4), 719–766.

- Koutsomanoli-Filippaki, A., Margaritis, D., & Staikouras, C. (2009). Efficiency and productivity growth in the banking industry of Central and Eastern Europe. Journal of Banking & Finance, 33(3), 557–567. doi:10.1016/j.jbankfin.2008.09.009

- Kraft, E., Hofler, R., & Payne, J. (2006). Privatization, foreign bank entry and bank efficiency in Croatia: A fourier-flexible function stochastic cost frontier analysis. Applied Economics, 38(17), 2075–2088. doi:10.1080/00036840500427361

- Kraft, E., & Tırtıroğlu, D. (1998). Bank efficiency in Croatia: A stochastic-frontier analysis. Journal of Comparative Economics, 26(2), 282–300. doi:10.1006/jcec.1998.1517

- Krishnasamy, G., Hanuum Ridzwa, A., & Perumal, V. (2004). Malaysian post merger banks’ productivity: Application of Malmquist productivity index. Managerial Finance, 30(4), 63–74. doi:10.1108/03074350410769038

- Lee, -C.-C., & Hsieh, M.-F. (2013). The impact of bank capital on profitability and risk in Asian banking. Journal of International Money and Finance, 32, 251–281. doi:10.1016/j.jimonfin.2012.04.013

- Meeusen, W., & van Den Broeck, J. (1977). Efficiency estimation from Cobb-Douglas production functions with composed error. International economic review, 435–444.

- Nakane, M. I., & Weintraub, D. B. (2005). Bank privatization and productivity: Evidence for Brazil. Journal of Banking & Finance, 29(8–9), 2259–2289. doi:10.1016/j.jbankfin.2005.03.015

- Park, K. H., & Weber, W. L. (2006). A note on efficiency and productivity growth in the Korean banking industry, 1992–2002ʹ. Journal of Banking & Finance, 30(8), 2371–2386. doi:10.1016/j.jbankfin.2005.09.013

- Patti, E. B., & Hardy, D. C. (2005). Financial sector liberalization, bank privatization, and efficiency: Evidence from Pakistan. Journal of Banking & Finance, 29(8–9), 2381–2406. doi:10.1016/j.jbankfin.2005.03.019

- Peng, Y.-H., & Wang, K. (2004). Cost efficiency and the effect of mergers on the Taiwanese banking industry. The Service Industries Journal, 24(4), 21–39. doi:10.1080/0264206042000275172

- Philippon, T., & Schnabl, P. (2013). Efficient recapitalization. The Journal of Finance, 68(1), 1–42. doi:10.1111/j.1540-6261.2012.01793.x

- Schulz, H. (2006). Foreign banks in Mexico: New conquistadors or agents of change? SSRN Electronic Journal. doi:10.2139/ssrn.917149

- Staub, R. B., E Souza, G. D. S., & Tabak, B. M. (2010). Evolution of bank efficiency in Brazil: A DEA approach. European Journal of Operational Research, 202(1), 204–213. doi:10.1016/j.ejor.2009.04.025

- Thoraneenitiyan, N., & Avkiran, N. K. (2009). Measuring the impact of restructuring and country-specific factors on the efficiency of post-crisis East Asian banking systems: Integrating DEA with SFA. Socio-Economic Planning Sciences, 43(4), 240–252. doi:10.1016/j.seps.2008.12.002

- Unite, A. A., & Sullivan, M. J. (2003). The effect of foreign entry and ownership structure on the Philippine domestic banking market. Journal of Banking & Finance, 27(12), 2323–2345. doi:10.1016/S0378-4266(02)00330-8

- Vo, X. V. (2018). M&As in the process of banking consolidation–Preliminary evidence from Vietnam. Asian Journal of Law and Economics. doi:10.1515/ajle-2017-0032

- Walker, G. (1998). Economies of scale in Australian banks 1978–1990*. Australian Economic Paper. doi:10.1111/1467-8454.00007

- Weill, L. (2003). Banking efficiency in transition economies. Economics of Transition, 11(3), 569–592. doi:10.1111/1468-0351.00155

- Williams, J., & Nguyen, N. (2005). Financial liberalisation, crisis, and restructuring: A comparative study of bank performance and bank governance in South East Asia. Journal of Banking & Finance, 29(8–9), 2119–2154. doi:10.1016/j.jbankfin.2005.03.011

- Wruck, K. H. (1990). Financial distress, reorganization, and organizational efficiency. Journal of Financial Economics, 27(2), 419–444. doi:10.1016/0304-405X(90)90063-6

- Yudistira, D. (2004). Efficiency in Islamic banking: An empirical analysis of eighteen banks. Islamic Economic Studies, 12(1), 2–19.

- Zaim, O. (1995). The effect of financial liberalization on the efficiency of Turkish commercial banks. Applied Financial Economics, 5(4), 257–264. doi:10.1080/758536876

Appendix A. Restructuring measures of Vietnamese banks