?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The study analysed the factors that affect the internal governance quality of corporations in Ethiopia. It performed an ordered logistic regression analysis on a randomly selected sample of 76 corporations to analyse the effect of the ownership structure, form of ownership (private or government), leverage, corporate size, and sales growth on the internal governance quality score (IGQS). The governance quality score was measured using 20 indices categorized into four perspectives: disclosure, board characteristics, ethics, and shareholder rights. In this study, a significant positive effect of the corporate size and sales growth on the IGQS was found. In addition, government-owned corporations were found to perform better than privately owned corporations. It is recommended that appropriate authorities and officials should encourage the use of the corporate governance system in privately owned corporations and the convergence of internal governance quality of the two groups of corporations to the highest level.

PUBLIC INTEREST STATEMENT

Due to various phenomena, such as the business scandals and financial crises that have occurred in several parts of the business world, corporate governance is attracting the attention of researchers, policy makers, and even politicians. The study analysed the factors that affect the internal governance quality of corporations in Ethiopia. The governance quality score was measured using 20 indices categorized into four perspectives: disclosure, board characteristics, ethics, and shareholders’ rights. In this study, a significant positive effect of the corporate size and sales growth on the IGQS was found. In addition, government-owned corporations were found to perform better than privately owned corporations. It is recommended that appropriate authorities and officials should encourage the use of a corporate governance system among privately owned corporations and the convergence of the internal governance quality of the two groups of corporations to its highest possible level.

1. Introduction

The corporate business form has no long history and tradition in Ethiopian business. However, over the past two decades, this business form has been emerging in the nation’s business environment. The presence of an ambitious growth and transformation plan (GTP), the development of diversified sources of energy projects, cheap labour, and land, and the potential market have all created fertile ground for corporations to flourish in the country (Figure ).

Figure 1. Government and privately owned corporations (Source: The study findings).

Corporations, one of the three business forms, are characterized as legal entities that result in the separation of the capital provider (shareholders) and the management (agent). In publicly held companies, stockholders are separated from the control of the corporation and the control is transferred to the hands of managers. The separation of ownership and control creates a kind of principal–agent relationship between shareholders and managers (Reeve et al., Citation1999; Frank & Sergeja, Citation2007). The modern organization of industrial companies was an automatic response to technological, and its first step was the enlargement of firms which was suggested by Chandler (Citation1997). According to him, large companies required vertical integration to minimize costs and dependence on other companies. Chandler believes that traditionally joint stock corporations are seen as indispensable to rapid economic progress because they foster capital pooling, risk sharing and governance, but recent research has shown that when alternative forms were available in history, specifically the private limited liability company, the joint-stock form was adopted much less frequently.

In a situation in which capital is invested by one party and managed by another, the manager cannot be expected to watch over the investment with the same anxious vigilance as investors do. This may result in the agency problem, which is the risk of the managers working for their own interest at the expense of the shareholders’ interest. Therefore, to avoid undesirable risk concerning managers, there should be an internal and external legal framework through which the operations of a corporation and its decision patterns can be governed. A well-governed corporation needs to balance the roles of shareholders, managers, and the board of directors (BOD) at the same time as meeting all its obligations to a broad array of stakeholders. The potential problems linked with the separation of ownership and control paved the way for the field of corporate governance to emerge (Denis, Citation2001).

Corporate governance has an effect on corporations’ financing and investment pattern, and this in turn influences their pace and direction of prosperity. Effective corporate governance promotes the efficient use of resources within both the firm and the wider economy (Klapper, Citation2004; Stijn & Burcin, Citation2012). On the other hand, poor corporate governance facilitates the collapse of a corporation. Though there is no evidence to show that weak corporate governance can cause a financial crisis, studies in East Asia have proved that weak corporate governance can aggravate an already-occurring crisis, such as the East Asian financial crisis of 1997 to 1998, to its worst level (Cliffe, Citation2002; Driscoll & Evans, Citation2005; Weiss, Citation2008).

To ensure good corporate governance, it is necessary to establish well-defined rules and regulations, and these call for appropriate government officials and policy makers. In addition to the legal framework, there are some factors, in fact with legal ground, within a corporation that can exert an impact on corporate governance. Such factors include the ownership structure, leverage, firm size, firm age, proportion of independent non-executive directors on the board, audit committee (AC), family members on the board, assets-in-place, compensation contracts, profitability, and industry type (Haniffa & Cooke, Citation2002).

Various authors and researchers have dealt with the quality of corporate governance from different perspectives. Ho and Wong (2001) examined the composition of the BOD, the existence of an AC, the existence of dominant personalities, and the proportion of family members on the board in Hong Kong–listed companies to deal with this issue. Brown and Caylor (Citation2006) identified seven internal and external governance measures as drivers of corporate governance: board members are elected annually; the company either has no poison pill or has one approved by shareholders; option repricing has not occurred within the last 3 years; the average options granted in the past 3 years as a percentage of the basic shares outstanding have not exceeded 3 per cent; all the directors have attended at least 75 per cent of the board meetings or had a valid excuse for non-attendance; the board guidelines are in each proxy statement; and the directors are subject to stock ownership guidelines.

The main objective of this study is to analyse the factors that determine the internal governance quality of corporations in Ethiopia. More specifically, this paper aims:

To examine whether the ownership structure is a determinant factor of the internal governance quality.

To find out whether and to what extent the dimensions of the internal governance quality differ in private and government ownership.

To analyse the effect of the corporation size on internal governance.

To investigate the impact of capital structure corporations on the internal governance quality.

To analyse the effect of sales growth on the internal corporate governance quality.

The paper is divided into five sections. Section 2 introduces literature works of different scholars and authors on the determining factors that affect the quality of internal governance. Section 3 discusses the research methodology and the data that were employed in this study. Section 4 contains the results and a discussion. The final section summarizes the main findings of the paper and states their implications for policy.

2. Literature review

This section reviews the literature works of different scholars and authors on the determining factors that affect the quality of internal governance in the corporate form of business.

2.1. Definitions of corporate governance

Owing to their contribution to economic development, corporations are the most crucial form of business organization. They can pool financial and non-financial resources from various investors; they can, due to economies of scale, operate effectively and efficiently; and they can serve the market better by increasing the supply or decreasing the price. Hence, corporations are owned by a very great number of investors, called shareholders. According to Article 307 (1) of the Ethiopian commercial code (CCE), a corporation is established by not fewer than five members (Asnakech, Citation2012; Gebeyaw, Citation2012).

Widely spread ownership, especially in large corporations, entails the separation of ownership and control (Ros & Terry, Citation2000). As cited by Denis (Citation2001), Adam Smith, in his Wealth of Nations, stated that because a corporation’s resources are provided by stockholders and controlled by managers, managers cannot be expected to watch over the corporation with the same anxious vigilance.

Corporate governance entails the development of monitoring and evaluation systems to shape the management’s finance and investment decision behaviour and ensure that the management behaves in the best interests of the shareholders (Lawrence & Marcus, Citation2006). Corporate governance has been defined differently by different scholars. Rezaee (Citation2009, pp. 306–307) defined it as “an ongoing process of managing, controlling, and assessing business affairs to create shareholder value and protect the interests of other stakeholders.” Moreover, the author pinpointed seven essential functions of corporate governance: oversight, managerial, compliance, internal audit, advisory, external audit, and monitoring. It is a means to delineate effectively the rights and responsibilities of each group of stakeholders in the company (Denis, Citation2001; Ho and Wong, 2001). On the other hand, corporate governance refers to the set of mechanisms that influence the decisions made by managers when ownership and control are separated (Larcker, Richardson, & Tuna, Citation2007; Eloisa, Citation2016). Corporate governance is a broad concept, and it encompasses internal factors (internal corporate governance mechanisms) and external factors (such as the legal framework and legal institutions).

2.1.1. Function and determinants of corporate governance

Many papers have dealt with the function and the determinants of corporate governance. This section reviews the main determining factors affecting the internal governance quality of corporations.

Controlling shareholders have a negative effect on the corporate governance of their firms. The empirical results show that the internal corporate governance mechanism as a monitoring tool may not work due to resisting controlling shareholders. In this sense, the controlling shareholders of a firm with a concentrated ownership structure are harder to monitor or check for misbehaviour than professional managers. Shivdasani and Yermack (Citation1999) claimed that the involvement of the Chief Executive Officer (CEO) influences the selection of new directors when the ownership distribution of the firm is dispersed and when he or she is the controlling shareholder in concentrated ownership structures (Sang-Woo & Chong, Citation2004; Coram et al., Citation2008; Rainsbury et al., Citation2008).

2.1.2. Normative categorizations

Since the last decade, the number of corporate business organizations has been increasing at a remarkable rate in Ethiopia. Thus, the concept of corporate governance has just recently emerged following the introduction of corporations. All the large-scale business organizations in Ethiopia can be classified into three types: those established by issuing stock to the public, private limited companies, and endowments. In the Commercial Code of Ethiopia (CCE) Art. 304:1, a corporation, also referred to as a share company, is defined as a company of which the capital is fixed in advance and divided into shares and of which the liabilities are met only by the assets of the company.

Any Ethiopian corporation is required by law to appoint one or more auditors and one or more assistant auditors elected at a general meeting. They are responsible for auditing records and securities; verifying the validity and reliability of records and financial reports; certifying that the reports of the BOD reflect the correct state of the company’s affairs; and carrying out special audits given by the management (CCE Art 368:1 and 374). Hence, the appointment of auditors is a legal mechanism to strengthen the internal corporate governance in Ethiopia (Hussein, Citation2012). The CCE contains some restrictions on the appointment of auditors to avoid possible conflicts of interest; however, it says nothing about their composition and the frequency of their meetings.

Since corporations are a recent phenomenon in Ethiopia, the literature related to the subject is limited. However, the Ethiopian Institute of Corporate Governance, which was established on 26 October 2013, is responsible for controlling the ethics and conduct of companies in the country.

2.2. Justifications for the approach in this study

In this study, we considered and adopted the corporate governance quality indicators used by Silveira et al. (Citation2004) and Frank and Sundgren (Citation2012). Frank and Sundgren examined the existence of an AC, the financial expertise within the AC, the frequency of AC meetings per year, internal audit functions, risk management functions, the code of conduct, and whistle-blower provisions to analyse the corporate governance quality in Sweden. The existence of an AC is the first indicator considered. The AC plays an important role in enhancing good internal corporate governance by influencing the top management’s thoughts regarding internal control and other core activities.

In addition, we referred to Toledo’s governance index (GOV-I) to assess good governance practices in Spain. The GOV-I is composed of four dimensions (and 25 sub-indices) created as a proxy for the quality of governance in the sample companies. The four dimensions are (1) access to and content of the information; (2) the structure of the board; (3) the ownership structure and control; and (4) progressive practices. We examined those dimensions and the questions compounding the index. We observed that those two main references (Silveira et al., 2007; Frank & Sundgren, Citation2012) share empirically supported internal governance indicators, which helped us to measure the governance scores of our sample corporations.

3. Materials and methods

This study was designed to investigate the factors affecting the internal governance quality of corporations in Ethiopia. This section discusses the research methodology of the study in more detail. The formal hypotheses addressed in this study are the following:

H1: There is a direct association between diffused ownership and internal governance quality.

H2: There is no difference between private or governmental ownership in internal governance quality.

H3: There is a positive association between firm size and internal governance quality.

H4: There is a positive association between leverage and internal governance quality.

H5: There is a positive association between a firm’s sales growth and its internal governance quality.

3.1. Description of the study area and sample

The target population for this study was the different corporations in Ethiopia. Hence, our research utilized data that were collected from the head offices of the corporations, mainly located in Addis Ababa.

3.2. Sample and data type

A sample of 76 companies was chosen randomly, comprising sectors including manufacturing, services (excepting banks), and trade. Our study used both archival data and survey data. To test the proposed research hypotheses, we conducted a survey among the corporations in Ethiopia in 2014. The survey method is appropriate for studies, such as the present one, that seek cross-sectional variation and association. Secondary information was gathered from publicly available annual accounts of the corporations, and variables such as total assets, total debts, and total revenues were found in the profit and loss statements and the balance sheets of the same.

To select the survey respondents, we approached the corporations at the board level. Besides, with the help of the human resource managers, respondents in each company were selected based on their familiarity with the theme of our study (functional areas where they work).

3.3. Data and methodology

The collected data were analysed using (1) descriptive statistical tools such as a measure of central tendency and a measure of dispersion and (2) ordered logistic regression. The ordered logistic regression model is used to identify the factors that affect internal corporate governance and to determine the direction of their effect (Murad, Fleischman, Sadetzki, Geyer, & Freedman, Citation2003).

3.4. Operationalization of internal governance quality score (IGQS)

In this study we used an ordinal scale, the IGQS, which takes higher values if a company has taken certain actions that might improve the internal governance quality. The measure is based on the Ethiopian corporate governance framework and the Committee of Sponsoring Organizations of the Treadway Commission (COSO) guidelines for IC, as well as prior studies.

Gauging the quality of corporate governance is subjective and can be controversial. Analysts are unlikely to agree on whether or not a certain aspect of corporate governance should be included, how much weight should be given to each aspect, and what scores should be given to responses to individual questions (Nam & Nam, Citation2004). However, we tried to address the problem of subjectivity in this study by incorporating many questions on various elements of corporate governance characteristics and aggregating the scores based on those numerous questions.

This paper assessed the internal governance quality of selected Ethiopian corporations, which were chosen randomly, based on indicators with a relevant relationship to internal governance as used by Frank and Sundgren (Citation2012). These authors identified an indicator variable that could measure the internal governance quality of Swedish corporations, including whether a company has an AC, a sufficient number of AC meetings during the year, financial expertise on the AC, an internal auditing function, a risk management function, a provision for whistle-blowing, and a code of conduct. Our methodology is in line with the study by Frank and Sundgren (Citation2012), although we did not consider the whistle-blowing provision variable in our case, as there is little empirical evidence of the implementation of the protection in Ethiopia. In addition, we referred to Silveira et al. (2007), who used corporate GOV-Is to measure firm-level governance quality in Brazil. We also adopted Toledo’s (n.d.) GOV-I, used to assess good governance practices in Spain. The GOV-I is composed of four dimensions (25 sub-indices) created as a proxy for the quality of governance in the sample companies. The four dimensions are (1) access to and content of the information; (2) the structure of the board; (3) the ownership structure and control; and (4) progressive practices. We examined those dimensions and the questions compounding the index and selected many of the questions included in the first three dimensions.

Generally, although the use of the corporate governance code in Ethiopia is quite new in comparison with developed nations, where the use of a nation-wide code of corporate governance has a long tradition, we believe that our variables revealed the local context well and measured the governance quality of the Ethiopian corporations considered in the study.

Based on the above discussion, we now specify the IGQS for this study. We use the IGQS as an indicator variable taking values between 0 and 20 depending on how many of the following criteria are met in the sample firms.

IGQS = DISCLOSURE + BOARD + ETHICS + RIGHTS

DISCLOSURE ‒ This dimension includes four corporate GOV-Is related to access to information in the firm: (1) whether the company produces its legally required financial reports by the required date; (2) whether the company discloses enough information or analysts’ presentations with which any investor can make projections for the company; (3) whether the company discloses on its website or in its annual report compensation information for the CEO and board members; and (4) whether the company specifies in its charter, annual reports, or other means sanctions against the management in the case of violations of its desired corporate governance practices.

BOARD ‒ This dimension includes seven board composition and functioning indexes in the firm: (1) whether the Chairman of the Board and the CEO are different persons (no CEO duality); (2) whether the company has monitoring committees, such as a compensation and/or nomination and/or AC; (3) whether the board is clearly made up of outside and possibly independent directors; (4) whether there are frequent AC meetings during the fiscal year (the AC meets at least twice a year); (5) whether there is financial expertise within the AC (accountant, auditor, financial officer); (6) whether internal audit functions (in-house or external) are present in the company; and (7) whether there are risk management functions in the company.

ETHICS ‒ This dimension includes three indexes with respect to ethics and conflicts of interest in the firm: (1) whether the company submits to arbitration in place of regular legal procedures in the case of corporate governance malpractices; (2) whether executive and non-executive directors’ percentage of beneficial shares exceeds 5 per cent; and (3) whether there are ethical guidelines or a code of conduct in the company.

RIGHTS ‒ This dimension includes six indexes related to shareholders’ rights in the firm: (1) whether the company pays (interim and final/annual) dividends in an equitable and timely manner; that is, all shareholders are treated equally and paid within 30 days after being (i) declared for interim dividends and (ii) approved by the annual general meeting (AGM) for final dividends; (2) whether shareholders have the right to participate in amendments to the company’s constitution and the authorization of additional shares; (3) whether the company provides non-controlling shareholders with the right to nominate candidates for the BOD/commissioners; (4) whether shareholders have the opportunity, evidenced by an agenda item, to approve remuneration (fees, allowances, benefits-in-kind, and other emoluments) or any increases in remuneration for the non-executive directors/commissioners; (5) whether the company disclosed the voting results, including approving, dissenting, and abstaining votes for each agenda item, for the most recent AGM; and (6) whether the company’s ordinary or common shares have one vote for one share.

3.5. Model specification and variable definitions

We tested the study’s five hypotheses (refer to Section 2.2) using ordered logistic regressions, and the measurement of the dependent and experimental variables was based mainly on the model developed by Silveira et al. (Citation2004) and Frank and Sundgren (Citation2012).

where: IGQS = DISCLOSURE + BOARD + ETHICS + RIGHTS (refer to Section 3.4 for a detailed discussion).

Notice: 1) the dependent variable IGQS was measured using 20 indicators of equal weight, which were categorized into four perspectives: disclosure, board characteristics, shareholders’ rights, and code of ethics; 2) the independent variables include new variables PRIVOWN and SGROWTH in the model, which were not previously considered in the study conducted in Sweden by Frank and Sundgren (Citation2012), because we supposed that the ownership type and sales growth of a firm significantly affect its internal governance quality in Ethiopia. However, our study dropped the variables related to additional issuance of shares, whether the company business is performed abroad, and whether the company was obliged to follow the code at the time of the survey submission to enable us to consider the local corporate governance practices.

We present below the operational definitions of the variables included in the regression model.

3.6. Perspectives of the dependent variable

DISCLOSURE ‒ The “disclosure” dimension was measured based on the four indices indicating access to information, which take one for presence and zero for absence of the indices. The value of this dimension ranges from zero to four.

BOARD ‒ The “board” dimension was measured based on the seven indices related to board characteristics, which take one for presence and zero for absence of the indices. The value of this dimension ranges from zero to seven.

ETHICS ‒ The “ethics” dimension was measured based on the three indices related to ethics and conflict of interest, which take one for presence and zero for absence of the indices. The value of this dimension ranges from zero to three.

RIGHTS ‒ The “rights” dimension was measured based on the six indices related to shareholders’ rights, which take one for presence and zero for absence of the indices. The value of this dimension ranges from zero to six.

3.7. Independent variables

DIFFUSED ‒ This is a dummy variable taking the value one if no individual shareholder controls more than 20 per cent of the shares of the company and zero otherwise.

PRIVOWN ‒ This is a dummy variable that takes the value one if the firm is privately owned and zero otherwise.

LnASSETS ‒ This is the natural logarithm of the total assets (in 2012).

TD/TA—This represents total debt/total assets (in 2012).

SGROWTH ‒ This is the sales growth over the 2008‒2012 period (2012 sales/2008 sales).

Perceived RISK ‒ On a 5-degree Likert-type scale, the respondent was asked to indicate whether the company’s risk is higher than that of the average company. One stands for totally disagree and five stands for totally agree.

Attitude RISK ‒ On a 5-degree Likert-type scale, the respondent was asked whether the company deliberately invests more in competence and external consultancy to secure its financial reporting. One stands for totally disagree and five for totally agree.

INDUST ‒ This is a dummy taking the value one for manufacturing companies and zero otherwise.

FINSERV ‒ This is a dummy taking the value one for companies in the financial sector (excluding banks) and zero otherwise.

TRADE ‒ This is a dummy taking the value one if the firm is in the trading/services sector and zero otherwise.

= the error term.

4. Results

This study focused on analysing the critical factors that affect the internal governance quality of corporations in Ethiopia. In this chapter, we present and discuss the results of the study. The findings of the study generated enough facts to enable the researchers to achieve the objectives effectively.

4.1. Descriptive statistics

4.1.1. Number of participants by line of business

The number of companies included in the study was 76, as shown below along with the various types of business (Table ). Referring to Table , 22 industries, 17 financial services, and 37 trading companies were surveyed in this study.

Table 1. Description of surveyed corporations

4.1.2. The dimension of the dependent variable IGQS

The dependent variable in the study was the internal corporate governance quality score (IGQS) of the sample firms. Table below shows the descriptive statistics of the elements making up the IGQS.

Table 2. Description of the dependent variable and its dimensions

As shown in the table, the mean value of the dependent variable IGQS is 14.39. Its minimum and maximum values, out of 20, are 4 and 19, respectively. This implies that, though the mean value is above average, the level of the IGQS of the surveyed corporations is highly divergent, with a range of 15. The mean value of the IGQS perspectives is as follows: disclosure 3.11, board 5.19, ethics 1.69, and stakeholders’ rights 5. As can be seen from the table, the board characteristics of the surveyed corporations are highly fragmented, as the range of the board perspective is large.

4.1.3. IGQS dimensions by form of ownership

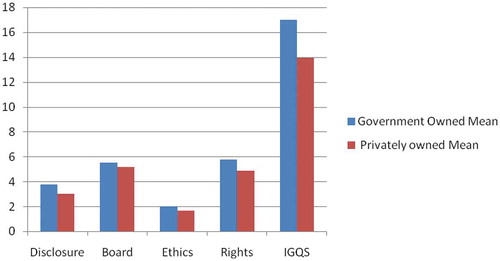

The next table and graph show whether the IGQS dimensions differ for private and government ownership of the sampled companies. Accordingly, we observed that the mean IGQS value for public ownership and private ownership is 17 and 13.96, respectively. Even the individual corporate governance dimensions show a higher value for public firms than private firms. The results indicate that the internal corporate governance is better in government-owned companies than in private ones. This finding is consistent with the empirical result of Anthony and Vining (Citation1989), who reported weak support for the property rights theory of the firm, which proposes that privately owned companies outperform state-owned ones.

Table compares the mean values of the four perspectives of the IGQS for privately owned and government-owned corporations. Government-owned corporations scored higher than privately owned corporations, and the mean difference is statistically significant at the 1 per cent level of significance. Government-owned corporations performed relatively better on disclosure, code of ethics, and shareholders’ rights; however, there is no statistically significant mean difference in the board characteristics of both privately owned and government-owned corporations. Since the concerns of privately owned and government-owned corporations may not be the same, the difference in the mean value may be attributed to the existence of free riding in the privately owned corporations.

Table 3. Spearman correlation between the IGQS components

Table 4. Mean difference of IGQS dimensions by form of ownership

4.1.4. Descriptive statistics of the independent variables

Table shows the mean, minimum, and maximum values of the independent variables (test and control variables) considered in the model. We can see that the average company in the study has leverage of about 37 per cent; perceives its business as moderately risky (2.3 out of 5); has an above-average attitude towards risk (3.3 out of 5); and grows annually at about 9.6 per cent. Furthermore, it can be seen from the table that 58 per cent of the companies have no individual owner who owns more than 20 per cent of the outstanding shares and 21.4 per cent of the companies are engaged in financial service provision, mainly insurance services. Besides, around 86 per cent of the surveyed firms are privately owned corporations; the total assets of the companies extend from 0.87 million birr to 4,070 million birr; the average age of the firms is 21.6 years; and the average board size is 6.

Table 5. Descriptive statistics of independent variables

On the other hand, Table shows the Pearson correlation between the independent variables. Most variables show low to moderate correlation with one exception. The gearing level of the company, measured by the ratio of total debt to total assets employed, shows quite a high correlation of 0.75 with the sales growth variable.

Table 6. Pearson Correlations of the independent variables

4.2. Inferential statistics

In this study we tried to identify the determinants of the internal corporate governance quality of share companies in Ethiopia. We used an ordinal logistic regression to test the association between our measure of internal governance quality and the explanatory variables. The results are discussed below.

4.2.1. Spearman correlations of the components of the dependent variable IGQS

Table shows the Spearman rank correlations of the components included in the aggregated dependent variable IGQS. The correlations between DISCLOSURE and the remaining variables is positive and moderate, indicating that the companies’ behaviour in providing access to firm information shows their overall merit when internal governance is concerned. Among the components of the dependent variable, the highest correlation (54.43 per cent) occurs between the variables representing board composition and functioning and shareholder rights in the firms. The table also reports the correlation between the aggregated IGQS variable and each of the components included in the score. As expected, all four indicator variables are relatively highly correlated with the dependent variable.

4.2.2. Overall test of the relationship

The presence of a relationship between the dependent variable and a combination of independent variables is based on the statistical significance of the chi-square after the independent variables have been added to the analysis. In this analysis, the model chi-square value is 79.44 with 10 d.f. and a pseudo-R2 of 52 per cent, which indicate that the model provides a reasonably good description of the data. Hence, the existence of a relationship between the independent variables and the dependent variable is supported.

4.2.3. Control variables

The following observations can be made related to the control variables in our regressions. The Perceived RISK and Attitude RISK variables have positive statistically significant coefficients at the 5 per cent and the 1 per cent significance level, respectively. This shows that a higher level of risks related to the operation of the company is likely to be associated with higher internal governance quality. The other control variables are generally insignificant.

We asked the respondents whether they agreed with the statement that “the risks associated with the operations of their corporation were higher than other similar corporations within the same industry.” The perceived risk (Perceived RISK) was measured on a Likert scale ranging from one to five. The variable has a positive and statistically significant coefficient. This indicates that companies with high perceived risk have higher values of the IGQS.

Companies that have a risk-taking culture might also take greater risks with respect to internal governance quality. In our study we assumed that the presence of a risk management function helps to improve the internal governance quality of corporations. Attitudes towards risks were measured on a 5-grade Likert scale, and the respondents were asked whether they agreed with the statement that “the culture in their company was to accept relatively high risks” (Attitude RISK). This variable has a positive and statistically significant coefficient, indicating that the attitude towards risks in a company is also likely to affect the incentives to invest to improve the IGQS.

These results are consistent with those of Frank and Sundgren (Citation2012), who reported that larger companies are more likely to have risk management functions and achieve better corporate governance. This is because the higher the level of risk management attitudes in a firm’s BOD, the greater the demand for good corporate governance in general. Thinking about risk helps to manage the risks that face the internal governance of a corporation. Corporations normally realize that commitment to strengthening risk management functions helps them to develop appropriate controls and prevent questionable and fraudulent practices (COSO, Citation1992; Desender & Lafuente, Citation2007). Although the empirical support is generally insignificant, the age of the firm and the number of people on the board of a corporation are negatively associated with the dependent variable, the IGQS.

4.3. Results of the hypothesis tests

Five test variables and five control variables were considered in the model. Of these, four test variables and two control variables were found to be significant at least at the 10 per cent significance level. The significant test variables include PRIVOWN (the form of ownership: private or government), corporate size (expressed in terms of Lnasset), leverage (the ratio of total debt to total asset), and sales growth; the significant control variables are perceived risk and attitude towards risk. On the contrary, DIFFUSED is statistically insignificant. Apart from corporate size and sales growth, the directions or signs of the test variables do not agree with the hypothesis. The most significant IGQS determinants are sales growth and attitude towards risk, with a p-value of at most 0.01.

DIFFUSED was used to test our H1. It can be seen from Table that the measure has a negative sign, although a positive sign was expected. The coefficient, however, is not significant at the 0.10 level (two-tailed tests) when the model is estimated. The finding shows that, among the sample companies in Ethiopia, those with more dispersed ownership have undertaken more actions that arguably improve the internal governance quality. Thus, the empirical result rejects the hypothesis that there is a direct association between diffused ownership and internal governance quality.

Table 7. Ordinal logistic regressions of internal corporate governance quality on test and control variables

H2 was developed to determine whether there is difference in the internal governance quality of privately owned and governmental corporations. PRIVOWN is the empirical measure and the coefficient has a negative and statistically significant value, whereas government-owned companies are likely to have a better internal governance quality than privately owned companies. Thus, the result does not provide empirical support for H2, which stated that there is no difference between governmental and private ownership in internal governance quality. This could be due to several reasons: for instance, the government is not the ultimate owner but an agent of the ultimate owners, so the incentives of the government may deviate from those of the owner, and the government as the owner faces many conflicts of interest and is concerned about other factors, such as employment (Claessens et al., Citation2000). Thus, considering the deficiency of clearly defined rules and regulations and regulatory institutions to govern the acts of corporations, privately owned corporations may try to free ride without fair investment in internal governance quality.

H3 proposed a positive association between corporate size and internal governance quality. The empirical result, as shown in Table , shows that the coefficient of LnASSETS is positive and significant at the 0.05 level. These results show that larger companies have higher IGQS values.

H4 focused on the association between leverage and internal governance quality. It can be seen from Table that the coefficient of TD/TA is negative and significant at the 0.01 level in the two-tailed tests in the regression. The sign of the coefficient, however, does not agree with the hypothesis. However, an alternative explanation that we cannot rule out is that lenders have a substitution role with respect to governance characteristics.

H5 referred to the relationship between the sales growth of a firm and its internal governance quality. Specifically, it proposed that there is a positive association between a firm’s sales growth and its internal governance quality. According to Table above, the coefficient of the sales growth variable, SGROWTH, is positive and significant at the 0.01 level in the two-tailed tests in the regression model. This result implies that firms need to secure a high degree of internal controls and consequently achieve a high IGQS to remain in business and grow their sales volume and dollars over the years.

5. Discussion and conclusions

Due to various phenomena, such as the business scandals and financial crises that have occurred in several parts of the business world, corporate governance is attracting the attention of researchers, policy makers, and even politicians. This section deals with the key findings regarding the factors that determine the internal corporate governance quality of Ethiopian corporations and their implication. A combination of 20 indicators was identified as a measure of the outcome variable (internal corporate governance quality), as used by Silveira et al. (Citation2004) and Frank and Sundgren (Citation2012). These indicators were categorized into 4 perspectives: disclosure, board, shareholders’ right, and code of ethics (Carol, Citation2002). The outcome variable was then regressed using ordered logistics against explanatory variables: ownership concentration, type of ownership (government or privately owned), corporate size, leverage, sales growth, perceived risk, attitude towards risk, type of business, board size, and age. To test the hypotheses, 76 companies were surveyed. Of the 10 explanatory variables included in the model, the type of ownership (government or privately owned), firm size, leverage, sales growth, perceived risk, and attitude towards risk were found to be statistically significant at the 5 per cent level.

According to the result, the trend of the AC for publicly traded companies, in many developed and emerging countries is from non-existence to voluntarily and now is being mandatory (Bhasin, Citation2012). Similarly, previous study by Forker (Citation1992), Ho and Wong (2001) in Hong Kong evidenced that companies with AC are more likely to enhance good corporate governance than those with no AC. The ownership structure affects other elements of corporate governance. According to the result, controlling shareholders have a strong incentive to monitor the management of firms and can be the most important part of corporate governance. Similarly, existing theories and empirical studies that analyse ownership structure in Sweden generally identify that block shareholders spend more time, effort and expense to monitor the firm closely due to their large stakes (Frank & Sundgren, Citation2012).

The essential implications of this study are described in the following. The quality of internal governance of government-owned companies is likely to be relatively better than that of privately held companies. This result contradicts the hypothesis that there is no difference between governmental and privately owned corporations regarding internal governance quality. It implies that the internal governance quality of privately held companies falls below that of government-owned corporations. The result is inconsistent with previous studies such as Lemmon and Lins (Citation2003) who argued that the ownership structure (diffused) in eight East Asian countries is a determinant factor for corporate governance. This suggests a need for intervention by appropriate authorities and officials to strengthen the corporate governance system of privately owned corporations, to enable the internal governance quality of the two groups of corporations to converge, and to increase the quality to the highest level possible. Thus, due to the lack of clearly defined rules and regulations and regulatory institutions to govern corporations’ actions, privately owned corporations may try to free ride without fair investment in internal governance quality.

Firm size and sales growth have a positive impact on the quality of internal governance. This result is consistent with the hypothesis stating that the internal governance quality directly correlates with the firm size and sales growth. The relatively complicated structure of larger corporations and corporations with high sales growth requires well-defined and functional corporate governance. This result is consistent with Frank and Sundgren (Citation2012) who found a significant positive relationship between corporate size and IGQS. Although direction of the relationship is not clear, Adams (Citation2002) also reported that corporate size is an important variable to determine the level of disclosure which is one the perspective of IGQS in this study. This relationship could be because governance mechanisms consume corporate resources and larger firms would have better capacity to invest and ensure good corporate governance quality.

However, in the case of leverage, the study result shows a negative correlation between leverage and internal governance quality. This result contradicts the hypothesis that proposes a positive association between leverage and internal governance quality. In general, a higher debt ratio indicates a larger amount of interests and principals to be paid periodically, and the management would be under pressure to ensure sufficient cash to cover the periodic payments; this in turn can be ensured through efficient internal governance. Moreover, regarding the ownership structure, the direction of the relationship between the IGQS and the variable DIFFUSED is not as predicted, and the association is not statistically significant.

This research adds to the existing body of literature by investigating and analysing the determining factors of internal corporate governance quality. Moreover, it can improve stakeholders’ understanding on the determinants of internal corporate governance quality in private and publicly held corporations in Ethiopia.

Additional information

Funding

Notes on contributors

Yrgalem Gebreslassie Adane

Yrgalem Gebreslassie Adane is a lecturer and certified IFRS trainer at the Department of Accounting and Finance, College of Business and Economics, Mekelle University (MU). She has over 10 years of experience in teaching, research, and community service.

Tadesse Getacher Engida

Tadesse Getacher Engida is a Ph.D. candidate at the Business Economics Group, Department of Social Sciences, Wageningen University & Research. He has wide research interests in production economics, accounting, and financial economics.

Yitbarek Abrha Asfaw

Yitbarek Abrha Asfaw is an assistant professor and certified IFRS trainer at the Department of Accounting and Finance, College of Business and Economics, Mekelle University (MU). He has over 11 years of experience in teaching, research, and community service.

Hossein Azadi

Hossein Azadi is a senior researcher at the Department of Geography, UGent, Belgium. He is also a scientific staff at Department of Engineering Management, UAntwerp, Belgium. As a senior researcher, he has focused on applying mixed-method approach on socio-economic impact assessments of agri-rural development projects.

Steven Van Passel

Steven van Passel is currently full professor of Environmental Economics at the University of Antwerp and Hasselt University. As an ecological and environmental economist, he is interested in conceptual and methodological aspects of assessing sustainability and in clean technologies. Within this context, he has different peer reviewed journal publications and he is responsible for several research projects.

References

- Adams, C. A. (2002). Internal organisational factors influencing corporate social and ethical reporting: Beyond current theorising. Accounting, Auditing & Accountability Journal, 15(2), 223–250. doi:10.1108/09513570210418905

- Anthony, E. B., & Vining, A. (1989). Ownership performance in competitive environments: A comparison of the performance of private, mixed and state-owned enterprises. Journal of Law and Economics, 1, 1–33.

- Asnakech, G. A. (2012). Revisiting the Ethiopian bank corporate governance system: A glimpse of the operation of private banks. Law, Social Justice & Global Development Journal (LGD), 1, 1–37.

- Bhasin, M. L. (2012). Corporate governance through an audit committee: An empirical study international. Journal of Managerial & Financial Accounting, 4(4), 339-365.

- Brown, L. D., & Caylor, M. L. (2006). Corporate governance and firm valuation. SSRN Electronic Journal, 25(4), 409-434.

- Carol, A. (2002). Internal organisational factors influencing corporate social and ethical reporting beyond current theorising. Accounting. Auditing & Accountability Journal, 15(2), 223–250. doi:10.1108/09513570210418905

- Chandler, A. D., Jr. (1997). The visible hand: The managerial revolution in American Business. USA: Harvard University Press.

- Cliffe, D. A. (2002). King report on corporate governance for South Africa: What it means to you. Retrieved from www.cliffedekker.com. doi:10.1044/1059-0889(2002/er01)

- Coram, P., Ferguson, C., & Moroney, R. (2008). Internal audit, alternative internal audit structures and the level of misappropriation of assets fraud. Accounting and Finance, 48, 543–559.

- COSO. (1992). Internal control-integrated framework, committee of sponsoring organizations of the Treadway commission. USA.

- Claessens, S., Djankov, S., Lang, L. 2000. ‘The separation of ownership and control in East Asian corporations’. Journal of Financial Economics, 58, 81–112 (PDF) Principal-principal agency. Available from: https://www.researchgate.net/publication/274546006_Principal-principal_agency [accessed Oct 21 2018].

- Davies, S. (1992). Green conditionality and food security: Winners and losers from the greening of aid. Journal of International Development, 4(2), 151–165. doi:10.1002/(ISSN)1099-1328

- Denis, D. (2001). Twenty-five years of corporate governance research and counting. Review of Financial Economics, 10, 191–212. doi:10.1016/S1058-3300(01)00037-4

- Desender, K., & Lafuente, E. (2007). The influence of board composition, audit fees and ownership concentration on enterprise risk management. Working Paper, Universitat Autonoma de Barcelona, 1–40.

- Dey, A. (2008). Corporate GOVERNANCE AND AGENCY CONflICts. Journal of Accounting Research, 46(5), 1143–1181.

- Driscoll, R., & Evans, A. (2005). Second-generation poverty reduction strategies: New opportunities and emerging issues. Development Policy Review, 23(1), 5–25. doi:10.1111/dpr.2005.23.issue-1

- Eloisa, P. T. 2016. Quality of governance and firm performance: Evidence from Spain. Universitat Autònoma de Barcelona – Dept. Economia de l’Empresa. Spain (Unpublished).

- Forker, J. (1992). Corporate governance and disclosure quality, accounting and business. Accounting and Business Research, 22, 111–124. doi:10.1080/00014788.1992.9729426

- Frank, H., & Sergeja, S. (2007). Characteristics of internal management control systems in Slovenian banks. Area of Research, 1, 1–64.

- Frank, P., & Sundgren, S. (2012). Determinants of internal governance quality: Evidence from Sweden. Umea School of Business and Economics, Umea University, Umea, Sweden. Emerald Group Publishing Limited, Managerial Auditing Journal, 27(7), 639–665. Retrieved from http://www.emeraldinsight.com/journals.htm?articleid=17043945

- Gebeyaw, S. B. (2012). A critical analysis of The Ethiopian Commercial Code in Light of OECD principles of corporate governance, dissertation F1002 (pp. 1–45). Institute of Advanced Legal Studies. School of Advanced Study, University of London, UK.

- Haniffa, R., & Cooke, T. (2002). Culture, corporate governance and disclosure in Malaysian corporations. Abacus, 38(3), 317-349.

- Hussein, A. T. (2012). Overview of corporate governance in Ethiopia: The role, composition and remuneration of boards of directors in share companies. Mizan Law Review, 6(1), 45–76.

- Klapper, L. L. I. (2004). Corporate governance, investor protection, and performance in emerging markets. Journal of Corporate Finance, 10, 703–728. doi:10.1016/S0929-1199(03)00046-4

- Larcker, D. F., Richardson, S. A., & Tuna, I. (2007). Corporate governance, accounting outcomes, and organizational performance. The Accounting Review, 82(4), 963–1008. doi:10.2308/accr.2007.82.4.963

- Lawrence, D. B., & Marcus, L. C. (2006). Corporate governance and firm valuation. Journal of Accounting and Public Policy, 25(4), 409–434. doi:10.1016/j.jaccpubpol.2006.05.005

- http://wizard.korea.ac.kr/user/aicg/data/kyungsuh4.pdf

- Lemmon, M. L., & Lins, K. V. (2003). Ownership structure, corporate governance, and firm value: Evidence from the East Asian Financial crisis. The Journal of Finance, 58, 1445–1468. doi:10.1111/1540-6261.00573

- Madan, L. B. (2012). Audit committee mechanism to improve corporate governance: Evidence from a developing country. Scientific Research, Modern Eonomiy, 3, 856–872.

- Minga, N. (2013). Corporate governance and ownership structure: The case of Ethiopia. Ethiopian E-Journal for Research and Innovation Foresight. Special Issue on the Ethiopian Economy, 5(1), 33–50.

- Murad, H., Fleischman, A., Sadetzki, S., Geyer, O., & Freedman, L. S. (2003). Small samples and ordered logistic regression. American Statistical, 57, 155–160. doi:10.1198/0003130031892

- Nam, S.W., Nam, I.C. 2004. Corporate governance in Asia: Recent Evidence from Indonesia,Republic of Korea, Malaysia and Thailand, Asian Development Bank Institute, Tokyo.

- Rainsbury, E., Bradbury, M., & Cahan, S. (2008). Firm characteristics and audit committees complying with ‘Best practice’ membership guidelines. Accounting & Business Research, 38, 393–408. doi:10.1080/00014788.2008.9665773

- Reeve, J., Bolt, E., & Cai, Y. (1999). Autonomy-supportive teachers: How they teach and motivate students. Journal of Educational Psychology, 91, 537–548.

- Rezaee, Z. (2009). Corporate governance and ethics. The International Journal of Accounting, 44, 306–307. doi:10.1016/j.intacc.2009.06.003

- Ros, H., & Terry, C. (2000). Culture, corporate governance and disclosure in Malaysian corporations. Presented at the Asian AAA World Conference in Singapore, Malaysia, pp. 1–28, Retrieved from https://business-school.exeter.ac.uk/documents/papers/accounting/2000/0007.pdf.

- Sang-Woo, N., & Il Chong, N. (2004). Corporate governance in Asia: Recent evidence from Indonesia, Republic of Korea, Malaysia, and Thailand. Asian Development Bank Institute, Japan. Retrieved from http://www.adb.org/sites/default/files/publication/159384/adbi-corp-gov-asia.pdf

- Shivdasani, A., & Yermack, D. (1999). CEO involvement in the selection of new board members: An empirical analysis. Journal of Finance, 54, 1829–1853. doi:10.1111/0022-1082.00168

- Silveira, A. M., Barros, l. A., Fama, R. 2004. Determinants of CorporateGovernance Quality of Brazilian Listed Companies. IV Meeting of the Brazilian FinanceSociety, Rio de Janeiro, July (2004). Available at <http://www.sbfin.org.br/> (only in portuguese).

- Stijn, C., & Burcin, Y. (2012). Corporate governance and development. A Global Corporate Governance Forum Publication. Washington, DC. Retrieved from http://www.ifc.org/wps/wcm/connect/518e9e804a70d9ed942ad6e6e3180238/Focus10_CG%26Development.pdf?MOD=AJPERES

- Weiss, J. (2008). The aid paradigm for poverty reduction: Does it make sense? Development Policy Review, 26(4), 407–426. doi:10.1111/j.1467-7679.2008.00416.x