?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The need for the Ghanaian government to generate enough revenue for development is becoming increasingly crucial in this era of slow growth, growing unemployment and high debt. However, tax revenue performance over the years reveals an unstable pattern. One key factor that has been overlooked in the literature in terms of the determinants of tax revenue is exchange rate volatility. Coming from the background of volatility in Ghana’s exchange rate, could it be the reason for the instability in the trend of tax revenue? This question is the subject matter of this study. To estimate the effect of exchange rate volatility on tax revenue, the study employed the Auto Regressive Distributed Lag (ARDL) technique after the yearly exchange rate volatilities had been generated using the GARCH(1,1) method. The results of the study suggest that exchange rate volatility has a deleterious effect on tax revenue both in the short-run and long-run but the effect is more pronounced in the long-run than the short-run. The study recommends that the Bank of Ghana step-up its exchange rate stabilization efforts to reduce exchange rate risk imposed on international trade players.

PUBLIC INTEREST STATEMENT

The need for developing countries to mobilize adequate revenues is becoming increasingly crucial amid systemic and macroeconomic constraints. For Ghana, one of such pressing challenges is the frequent volatility in its real exchange rate. This study therefore explored the effect of real exchange rate volatility on tax revenue generation. The results of the study suggest that real exchange rate volatility has a deleterious effect on tax revenue both in the short-run and long-run but the effect is more pronounced in the long-run than the short-run. The study recommends that the Bank of Ghana steps-up its exchange rate stabilization efforts to reduce the exchange rate risk imposed on international trade players.

1. Introduction

To a large extent, the growth and development of every nation depends on tax revenue mobilisation. The World Bank (Citation1988) defines tax as a compulsory, unrequited payments made to the central government by individuals, businesses or institutions. Globally, taxes play a significant role in the economy at both micro and macro levels. Firstly, tax is the main source of central government revenue, since its collection is mandatory and regular. Secondly, taxes help governments to provide the social and public needs by providing public goods and services. Thirdly, governments need tax revenue to establish armed forces and judicial systems to ensure security and justice for the society (Aizenman, Jinjarak, Kim, & Park, Citation2015).

Lee and Gordon (Citation2005) reckon that taxes can also be a powerful means to achieving the goals of social progress and economic development. Taxes also serve as a tool for encouraging the growth of certain activities by way of giving exemptions; discourage use of certain products by way of imposing heavier charges like those taxes imposed on tobacco products; or strengthen anaemic enterprises through exemptions (Arnold, Citation2008). Moreover, local industries may be protected through taxation by imposing high custom duties on foreign goods. Taxes can also be used to reduce inequities or inequalities in wealth and income as in the case of estate and income tax.

Several studies have contributed to the debate on the main determinants of tax revenue efforts around the world. Studies including but not limited to Gaalya (Citation2015), Gupta (Citation2007), Brafu-Insaidoo and Obeng (Citation2008), Teera and Hudson (Citation2004), Gupta, Clements, Bhattacharya, and Chakravarti (Citation2004), Cummings, Martinez-Vazquez, McKee, and Torgler (Citation2006), Tanzi (Citation1989), and Chelliah (Citation1992) have enumerated structural and institutional factors influencing tax revenue generation. Variables including GDP per capita, foreign aid, foreign direct investment, inflation, real exchange rate, trade openness, sectoral contribution to GDP, debt to GDP, corruption, rule of law among others have been widely explored as the main determinants of tax performance. For instance, Gaalya (Citation2015) has shown that foreign aid impacts tax revenue negatively while Gupta (Citation2007) and Brafu-Insaidoo and Obeng (Citation2008) provided evidence to show that per capita income induces revenue mobilisation efforts in Sub-Sahara Africa.

One key factor that is yet to be explored in terms of the determinants of tax revenue is exchange rate volatility. So far, the empirical discourse generally focuses on the association between real exchange rate and tax revenue. For instance, Adam, Bevan, and Chambas (Citation2001) argued that a real depreciation of the real exchange rate is revenue inducing in Sub-Sahara Africa. Fierro and Reisen (Citation1990) also provided evidence to show that a devaluation of the exchange rate has an overall positive effect on revenue generation in Korea and Mexico. Notwithstanding this, the literature is not exhaustive at least as these studies failed to explore the impact of the risk characterising the real exchange rate on tax revenue generation. A review of the literature shows that theoretical and empirical works are silent on the subject matter. This is basically the void this study seeks to fill. According to Ozturk (Citation2006), exchange rate volatility refers to the persistent up and down movements in the barter price of a country’s currency. In recent times, exchange rate volatility has dominated the literature in international trade and finance particularly due to its effects on developing economies. Since exchange rate volatility is not observed overtime, several methods, for instance, the moving average, the standard deviation method, as well as the Generalised Autoregressive Conditional Heteroscedascity (GARCH) have been used to capture periodic volatilities in a country’s exchange rate.

Obstfeld and Rogoff (Citation1998), Calderón (Citation2004), and Hau (Citation2002) have shown that exchange rate volatility is more pronounced in more open economies by asserting that the more volatile the exchange rate becomes, the riskier trade becomes impacting tax revenue adversely. According to Côté (Citation1994), exchange rate volatility can affect trade players directly, through uncertainty and adjustment costs, and indirectly, through its effect on the structure of output, investment and government policy. This suggests that in economies where exchange rate volatility persists, the degree of openness to trade or trade liberalisation policies could have a greater impact on revenue generation. As De Grauwe (Citation1988) noted, exchange rate volatility can have a detrimental impact on trade and by extension, trade tax revenue depending on the degree of risk aversion of trade players. In small open economies like Ghana, where forward contracts are less utilised by trade players, the overall implication of this is that exchange rate volatility can have a short-term and long-term impacts on trade taxes. Even though flexible exchange rate is supposed to be self-correcting following persistent instability, at least theoretically, the long and slow adjustment period, in reality, could generate higher risk with deleterious effects on exports volumes and by extension trade tax revenue (De Vita & Abbott, Citation2004).

As Ghana continues to open up to trade, trade taxes could be mostly affected if volatility in the real exchange rate persists. Ghana’s heavy reliance on imports poses various challenges to the economy including exchange rate volatility. But is there evidence of exchange rate volatility in Ghana? Recent studies by Alagidede and Ibrahim (Citation2017), Tarawalie, Sissoho, Conte, and Ahortor (Citation2013), and Obeng (Citation2018) provide evidence of high exchange rate volatility in Ghana and the West Africa Monetary Zone (WAMZ). Particularly, Alagidede and Ibrahim (Citation2017) further provide evidence to support the claim that deviations resulting from shocks to Ghana’s exchange rate market take about 15 years to be corrected.

The Ghana cedi has depreciated against its major trading currencies especially the US Dollar, although, not monotonously, as the Ghana cedi recorded some stability between 2002 and 2007 (Alagidede & Ibrahim, Citation2017). Ghana redenominated her currency on 1 July 2007, where US$1 was exchanged for 93 pesewas. Following this move is a persistent depreciation of the cedi. For instance, the end of July 2009, US$ 1 was exchanged for GH¢1.49. However, between August 2009 and March 2010, the Cedi marginally appreciated by 3 percent. Most recently, the cedi has been very volatile. For instance, at the beginning of January 2014, a dollar was exchanged for GH¢2.21 and by the end of September 2014, the Cedi–Dollar exchange rate stood at GH¢3.20—denoting about 44.65 percent depreciation (Alagidede & Ibrahim, Citation2017).

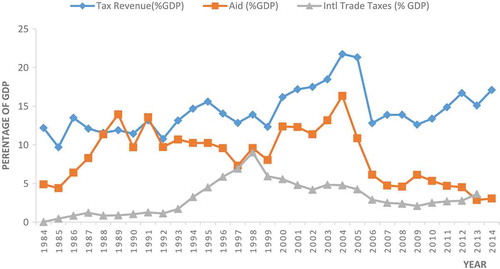

Ghana’s tax revenue to GDP remains low at an average of 14 percent compared to Sub-Saharan African average of 18 percent. Generally, tax revenue performance in the past decade has not been so encouraging as the country has barely improved on its total tax revenue to GDP of 17.5 percent realised in 2011. Below is a comparative analytical trend of overall tax revenue to the government from both domestic and international sources.

A careful look at Figure reveals that the trends of overall tax-to-GDP, trade taxes, and aid performance have been largely unstable. For instance, trade taxes rose steadily from a little over 0.1 to 9 percent from 1984 to 1998. On Aid, receipt was also encouraging as it increased from 5 percent in 1984 to 16 percent in 2004 though there were significant fluctuations 1990, 1992, and 1997. Lastly, on tax to GDP, the trend was also encouraging as the trend basically increased from 9.7 percent in 1997 to 21.8 percent in 2004. Could this unstable trend in tax revenue be due to the risk associated with the real exchange rate?

Figure 1. Plot of Major Components of Tax Revenue (1984–2014).

1.1. Motivation and significance of the study

The motivation for the study lies in estimating the effect of exchange rate volatility on tax revenue in Ghana in a bid to informing policymakers on the impact of exchange rate volatility on revenue generation efforts. While anecdotally, volatility in the Ghana cedi has been attributed to macroeconomic instability, very little attempt has been made to explore its impact on revenue generation efforts. Generally, discussions surrounding the fluctuations in Ghana’s exchange rate are only gleaned from public discourses on the economy with very little empirical and theoretical content. Understanding the impact of exchange rate volatility on tax revenue is essentially an empirical question. First, the study contributes to the literature by informing policymakers on the responsiveness of tax revenue to a given degree of exchange rate volatility; second, the implication of trade liberalisation policies on tax revenue given exchange rate volatility.

The rest of the article is presented as follows: Section 2 focuses on the literature review while the model is discussed in Section 3. The results and discussion are presented in Section 4. In Section 5, the conclusions and policy recommendations are presented.

2. Literature review

The empirical link between exchange rate volatility and tax revenue generation is largely non-existent in the literature. The best the empirical literature offers is the effect of exchange rate on tax revenue generation. For instance, Adam et al. (Citation2001) provide evidence to show that a real depreciation of the real exchange rate is revenue inducing in Sub-Sahara Africa. In most cases, the empirical relationship has been between exchange rate volatility and Trade (see Tatliyer & Yigit, Citation2016; in the case of United States; De Vita & Abbott, Citation2004; for Turkey; Tchokote, Uche and Agboola, Citation2015; and Tarawalie, Sissoho, Conte, and Ahortor, Citation2013, for WAMZ).

3. Data description and sources

The study used annual time series data spanning 1984 to 2014 to test the hypothesis that exchange rate volatility affects tax revenue generation. Following the empirical literature, the study explored the effect of exchange rate volatility together with per capita income, Inflation, Trade openness, share of industry in GDP, and foreign aid on tax revenue mobilisation in Ghana.

The dependent variable, tax revenue, was captured as a ratio of total tax revenue to GDP (Gaalya, Citation2015 and Gupta, Citation2007). Per capita income was measured by GDP per the total population. With theoretical foundation from the ability to pay theory, Per capita income signifies a higher capacity of the populace to pay taxes as well as a greater capacity of policymakers to levy and collect them (Chelliah, Citation1971). This is buoyed by increased demand for public expenditure and urbanization (Tanzi, Citation1992). Inflation was measured by the end of period average. Tax revenue from inflation could rise mostly due to seigniorage, excessive borrowing and high unproductive expenditures as the populace in the formal sector are pushed into a high income bracket (Rad, Citation2003; Gupta, Citation2007). Trade openness proxied by sum of total export and import to GDP matters for tax revenue performance as they take placed at specified places Gupta (Citation2007); the choice of industrial contribution to GDP follows logic and empirical evidence as the industrial sector is less difficult to tax in developing countries (Gupta, Citation2007; Baunsgaard & Keen, Citation2009; Teera & Hudson, Citation2004) while foreign aid captured as net official development assistance matters as tax performance may decline in the recipient country following aid (Pivovarsky et al., Citation2003; Franco-Rodriguez, Morrissey & McGillivray, Citation1998; and Mahdavi, Citation2008). The data for all the variables were sourced from the World Development Indicators.

3.1. Modeling exchange rate volatility

Since exchange rate volatility is not observable, it had to be generated. Following the literature, the GARCH (1,1) by Bollerslev (Citation1990) was used as it allows variances of errors in the exchange rate to be time dependent.

The GARCH (1,1) modeling process commences with mean equation (1) which expresses changes in the real effective exchange rate, , as a function of its lagged value. The error term,

is normally distributed with zero mean and a variance,

. The variance,

is then used to specify the GARCH (1,1) model of interest as in equation (1).

≈ N(0,

)

where: ∆= difference log of the real effective exchange rate from period

to

= variance of the error term et

= the ARCH term

= the GARCH term

From equation 2, the variance equation has one ARCH term (i.e. ) and one GARCH term (

). The dependent variable (

) represents the conditional variance, α and β represent the lagged squared error term (ARCH effect) and conditional volatility (GARCH effect) respectively.

3.2. The model

3.2.1. Theoretical foundation

Theoretically, the link between exchange rate volatility and tax revenue is not clear. The study is in line with the buoyancy theory of tax systems. The approach measures growth in duty revenue as a result of growth in income, reflecting the combined effects of tax base expansion and discretionary changes in tax rates, base definition, and changes in collection and enforcement of law. Discretionary changes in the tax rate is often resorted to following loss of international competitiveness and persistent volatility of the exchange rate (Brafu-Insaidoo & Obeng, Citation2008).

3.2.2. Empirical foundation

Analysis of the existing literature by Bahl (Citation1972), Lotz and Morss (Citation1970), Gupta (Citation2007), Stotsky and WoldeMariam (Citation1997), Khattry and Rao (Citation2002), and Tanzi and Blejer (Citation1988) reveal that studies exploring tax revenue generation mostly used the behavioural approach. The approach regresses tax revenue on factors that serve as proxies for a country’s tax performance. We express the approach as follows:

Where TR is tax revenue, Y is GDP, and K is a vector of tax handles.

By adapting the functional models put forward by Gaalya (Citation2015) and Le, Moreno-Dodson, and Rojchaichaninthorn (Citation2008), the study specifies a model which expresses tax to GDP as functionally related to the level of economic development and sophistication, and the degree of trade openness and exchange rate volatility (see equation 4).

where; is the natural log, TR is Tax to GDP ratio,

is tax intercept, GPC is Gross Domestic Product per capita, OPN is Trade Openness, IND is Industry output to GDP ratio, INF is Inflation rate, EXV is Exchange Rate Volatility,

is Exchange Rate Volatility and Trade openness interaction, while

is the error term.

3.2.3. Estimation strategy

To be able to capture the long-run and contemporaneous effects of exchange rate volatility on tax revenue, the Autoregressive Distributed Lag (ARDL) to cointegration technique put forward by Pesaran, Shin, and Smith (Citation2001) was applied. We thus transform equation (4) into the ARDL form (see equation 5)

Where, represent the long-run elasticities while

are the short-run elasticities. We then proceeded to estimate the results after establishing cointegration among the variables using the bounds testing approach. Lastly, the Granger causality test was performed to determine the predictive effects among exchange rate volatility, tax revenue and the control variables.

4. Results and discussion

Descriptive statistics was presented to show the location, variability and the distribution of the data. The descriptive statistics showed that all the variables have positive average values but for exchange rate volatility and the interaction term for trade openness and exchange rate volatility (see Appendix A). For instance, the mean tax to GDP is approximately 14 percent while the average inflation rate is also 22 percent. The average per capita income of Ghanaians over the study period is also GHȻ 777. Also, the minimal deviation of the variables from their means as shown by the standard deviation gives indication of minimal variability of the data over the period under consideration.

4.1. Evidence of real exchange rate volatility in Ghana

Appendices B and C show the result providing evidence of high and persistent volatility in Ghana’s real exchange rate. The coefficient of the squared residuals for the series is significant at 1 percent. The sum of α and β is approximately equal to 1 indicating that the volatility is highly persistent suggesting the presence of volatility clustering. This implies that the real exchange rate contains time varying effect, hence linear models cannot realistically explain its behavioural pattern. There is therefore a justification for adopting the GARCH (1,1) models for estimating the volatility in Ghana’s real exchange rate. Moreover, the ARCH [1] which is the serial LM test shows the absence of serial correlation in the residuals (see Appendix C).

4.2. Analysis on Tax to GDP and exchange rate volatility

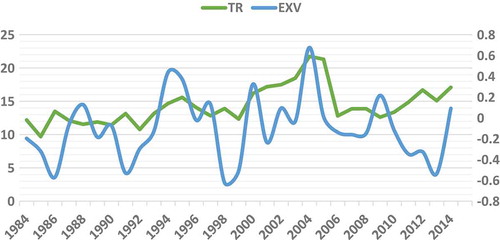

A trend analysis of tax to GDP and exchange rate volatility over the study period is shown in Figure .

Figure 2. Trend of Tax to GDP and Exchange Rate Volatility (1984–2014).

Figure shows that from 2004, where the exchange rate was volatile upward, Ghana’s tax to GDP was as high as 21.8 percent. This was very encouraging but the figure reduced sharply to 12.8 percent in 2006 before rising to 13.8 percent in 2008. In the period 2008 to 2014, where the volatility of the exchange rate seems prevalent, tax to GDP fell from 13.8 percent in 2008 to 12.6 percent in 2009 and increased thereof to 16.7 percent in 2012 before declining to 15.1 percent in 2013. This clearly shows that there is some form of dependency of Ghana’s tax performance on exchange rate volatility.

4.3. Unit root tests

As advised by Dickey and Fuller (Citation1979), and Phillips and Perron (Citation1988), the statistical properties of the variables were determined. The results of the ADF and PP tests for unit root with intercept and trend are provided in Appendices D and E, respectively. The null hypothesis is that the series is non-stationary, or contains a unit root. The rejection of the null hypothesis is based on the MacKinnon (Citation1996) critical values. The results revealed that all the variables were either integrated of order zero, I(0), or order one, I(1). Since the test results confirmed the absence of I(2) variables, the ARDL technique was thus appropriate for the estimation.

4.4. Bounds test for cointegration

From Table , the F-statistics that the joint null hypothesis of lagged level variables is zero was rejected at 5 percent level of significance. Since the calculated F-statistics of approximately 5.4 exceeded the upper bound’s critical value of (3.2), there is an evidence of cointegration among the variables.

Table 1. Bounds test results for cointegration

4.5. Long-run and short-run results

4.5.1. Long-run results

From the standard regression statistics in Table , approximately 86 percent of the variations in tax revenue is explained by the independent variables. Also, a DW-statistics of approximately 1.96 shows that there is no autocorrelation in the residuals. The coefficient of the lagged error correction term exhibits the expected negative sign and is statistically significant at 1 percent. It is evident that approximately 94 percent of the disequilibrium caused by previous year’s shocks converges back to the long-run equilibrium in the current year.

Table 2. Long-Run and Short-Run Estimates

The long-run results reveal that exchange rate volatility is detrimental to tax revenue generation in Ghana. The coefficient of exchange rate volatility is negative and statistically significant at 1 percent suggesting that a 1 percent increase in exchange rate volatility leads to approximately 0.85 percent shortfall in tax revenue. As argued by Obeng (Citation2018) and De Grauwe (1988), the result has theoretical underpinning in that the more volatile the exchange rate, the riskier trade becomes and for small open economy like Ghana, its consequence is felt on tax revenue. The implication of this is that it behoves the monetary authorities to stabilise the barter price of the cedi as the country risks losing tax revenue.

We provide evidence to show that in the presence of exchange rate volatility, the more the Ghana liberalises trade, the more the country loses tax revenue.

, from the descriptive statistics,

= −0.0993

The result suggests that given exchange rate volatility, policies that aim at liberalising Ghana’s trade is harmful to tax revenue generation. We show that in the presence of exchange rate volatility, a 1 percent increase in trade openness leads to approximately 0.31 percent decline in tax revenue. The test for the joint significance is statistically significant at 5 percent (see Appendix F). Plausibly, for developing countries like Ghana whose trade receipts are mainly from primary products, frequent misalignment of the exchange given the fairly elastic nature of its products leads to some marginal shortfall in tax revenue.

On the contrary, it is evident that a 1 percent increase in exchange rate volatility given trade openness affects Ghana’s tax revenue generation.

, from the descriptive statistics,

= 2.2729

We provide statistical evidence to shows that a 1 percent increase in exchange rate volatility in the presence of trade openness results in approximately 0.8 percent decline in tax revenue. The result brings to the fore the effect of exchange rate volatility on tax revenue due to the risk it imposes on trade players as argued by Obeng (Citation2018).

We found an unconventional result for trade openness. We found that trade openness has a suppressing effect on tax revenue generation in Ghana. The result is statistically significant at 5 percent corroborating that of Gupta (Citation2007) who found that a reduction in tariff rates are associated with reduction in tax revenue. In addition, Keen and Simone (Citation2004) argued that other than reduction in tariff rates, revenue may increase provided trade liberalisation occurs through tariffication of quotas, eliminations of exemptions, reduction in tariff peaks and improvement in customs procedure. The import of this is that policies aimed at further liberalising Ghana’s trade can be harmful to revenue generation. This could be curtailed by scrutinising trade agreements, discouraging corruption at the custom divisions through better conditions of service and prosecution.

We found foreign aid to have a positive effect on tax revenue mobilisation. There is a statistical evidence that an increase in foreign aid by 1 percent improves tax revenue by 0.23 percent. Gupta et al. (Citation2004) pointed out that advanced countries can help improve resource mobilisation efforts of developing countries by ensuring that aid flows are channelled into poverty reduction and infrastructural development due to its potency of generating higher future incomes. The result is in line with that of Benedek, Crivelli, Gupta, and Muthoora (Citation2014) and Clist (Citation2010) who found that concessional loans are associated with higher domestic revenue mobilization.

As expected, per capita income proved revenue inducing. We find that a 1 percent increase in per capita income improves revenue generation by approximately 0.62 percent, ceteris paribus. The finding concurs that of Chelliah (Citation1971), Teera and Hudson (Citation2004), Gupta (Citation2007), and Brafu-Insaidoo and Obeng (Citation2008). Gupta (Citation2007) particularly argues that rising levels of per capita income is associated with higher levels of tax revenue generation due to improved capacity of the state to levy and collect them arising from improved economic status of the populace, high demand for public services, and urbanization.

Finally, the contribution of the industrial sector to GDP has a significant favourable effect on tax revenue mobilisation. The result illustrates an increase in tax revenue of approximately 0.85 percent if there is a 1 percent increase in the share of industrial contribution to GDP. In developing countries like Ghana, manufacturing enterprises are easier to tax since business owners typically keep better books of accounts and records. The result supports that of Agbeyegbe, Stotsky, and WoldeMariam (Citation2006), and Ahmed and Muhammad (Citation2010) in which the latter concludes that the manufacturing sector of developing countries has positive impact on tax collection. Companies are required by law to provide records of accounts and pay all taxes of time. The implication of this is that the establishment of new enterprises, sustainability of existing firms, and support for manufacturing industries has the potency of improving tax revenue performance.

4.5.2. Short-run results

The coefficient of exchange rate volatility is negative and statistically significant at 1 percent. Relatively, the result is less pronounced in the short-run. Plausibly, in the short-run, since transactions have already been agreed on, even in the presence of exchange rate volatility, substantial amount of flow of goods and services across borders still take place. However, as the volatility persists for a long time, high adjustment cost induce trade players focus on domestic consumers or reduce the amount of goods exported or imported or both.

In conformity to the long-run results, we provide evidence to show that the more the country liberalises its trade with the rest of the world, the more the country loses tax revenue.

, from the descriptive statistics,

= −0.0993

The test for the joint significance (see Appendix G) means that the net effect is statistically significant at 1 percent. This means that in a presence of exchange rate volatility, a 1 percent increase in trade openness leads to approximately 0.37 percent loss in tax revenue.

In the same way, we show from the net-effect that given the level of trade openness, an increase in exchange rate volatility affects tax revenue generation adversely.

, but from the descriptive statistics,

The result is statistically significant at 5 percent (see Appendix G). The finding concurs that of Obeng (Citation2018) who showed that exchange rate volatility is a risk factor to trade. This in effect, has a deleterious impact on tax revenue.

Consistent with long-run results, the contribution of the industrial sector to GDP, foreign aid and inflation proved tax revenue inducing at various levels of significance while trade has a statistically suppressing effect on tax revenue at 5 percent level of significance.

4.6. Diagnostic tests

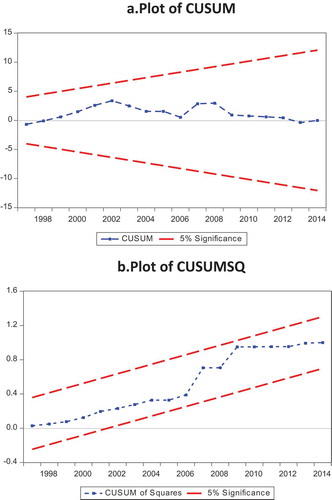

It is evident from Table that the estimated model passes all the diagnostic tests indicating that the model is a fit of the data. It is clear that the model passes the test of misspecification, heteroscedasticity, normality and serial correlation. Moreover, Appendix H depicts the plots of CUSUM and CUSUMSQ for the estimated ARDL model. The plots suggest the stability of the coefficients meaning that the coefficients are not changing systematically or erratically.

Table 3. Diagnostic Tests

To examine the predictability of exchange rate volatility on tax revenue, the Granger (Citation1988) causality test was conducted to determine the linear causation among the variables (see Appendix I). The results suggest a unidirectional causality from exchange rate volatility to tax revenue. Moreover, the results show a unidirectional causality from the share of industry in GDP to tax revenue. Lastly, a unidirectional causality from tax revenue to foreign aid was found.

5. Conclusion and recommendation

The study set out to test the hypotheses that exchange rate volatility has both short-run and long-run impact on tax revenue generation in Ghana using annual data spanning 1984 to 2014. In order to estimate the long-run relationship as well as the contemporaneous effects, the ARDL bounds testing technique to cointegration was employed.

Both the long-run and short-run results found statistically significant positive effects of per capita income, foreign aid and the share of the industrial sector to GDP on tax revenue generation. Inflation was positive and statistically significant only in the short-run. However, exchange rate volatility, and the net effect of exchange rate volatility and trade openness interaction proved tax revenue hindering both in the short-run and long-run.

On macroeconomic stability and particularly on real exchange rate, one policy implication of the finding is that, domestically, the Bank of Ghana should step-up its exchange rate stabilisation efforts to reduce exchange rate risk imposed on trade players. Moreover, the Bank of Ghana should sensitize trade players on the need to patronise hedging or forward contracts. This will go a long way to ensure steady flow of trade and international trade taxes

Coming from the background of the contribution of the industrial sector to tax revenue, it is recommended that, as a way of improving tax revenue, the government should create an enabling environment for the private sector to expand and/or establish new small or medium scale enterprises. The ripple effect of this on the industrial sector and the economy as a whole will further improve tax revenue performance.

The significant negative effect of trade openness on tax revenue suggests that policies aimed at further liberalising trade will be harmful to revenue generation. The study recommends that the Government of Ghana through the Ministries of Trade and Finance should take steps to review trade agreements like the Interim Economic Partnership Agreement (I-EPA) that seeks to open the Ghanaian economy to the rest of the world.

In our future endeavours, we will explore the effect of exchange rate volatility on tax revenue mobilization efforts in the WAMZ

Correction

This article was originally published with errors, which have now been corrected in the online version. Please see Correction (https://doi.org/10.1080/23322039.2018.1552821)

Additional information

Funding

Notes on contributors

Isaac Kwesi Ofori

Isaac Kwesi Ofori holds MPhil. in Economics from UCC, Ghana. Mr. Ofori is a Research Assistant at the Directorate of research, Innovation and Consultancy, UCC. His research interests are public sector economics, international economics, economic growth and development, and monetary economics. He is an active member of the African Economic Research Consortium (AERC), Kenya.

Camara Kwasi Obeng

Camara Kwasi Obeng obtained his PhD in Economics from UCC, Ghana. He is an active member of the AERC, Kenya; the African Econometrics Society, South Africa; the Poverty and Economic Policy (PEP) Network, Canada; the Global Economic Modeling (ECOMOD) Network, USA; and the International Input–Output Association, Austria.

Mark Kojo Armah

Mark Kojo Armah received his PhD at the University of Hull Business School’s Centre of Economic Policy (CEP) in the U.K. He has consulting experiences with the AERC based in Nairobi, Kenya. His research interests include exchange rate economics, applied general equilibrium and poverty analysis in developing countries.

References

- Adam, C. S., Bevan, D. L., & Chambas, G. (2001). Exchange rate regimes and revenue performance in Sub-Saharan Africa. Journal of Development Economics, 64(1), 173–213. doi:10.1016/S0304-3878(00)00129-2

- Agbeyegbe, T. D., Stotsky, J., & WoldeMariam, A. (2006). Trade liberalization, exchange rate changes, and tax revenue in Sub-Saharan Africa. Journal of Asian Economics, 17(2), 261–284. doi:10.1016/j.asieco.2005.09.003

- Aggrey, J. (2011). Determinants of tax revenue: Evidence from Ghana (Doctoral dissertation, thesis submitted to the Department of Economics, University of Cape Coast [Google Scholar]).

- Ahmed, Qazi Masood and Muhammad, Sulaiman D., Determinant of Tax Buoyancy: Empirical Evidence from Developing Countries (April 3, 2010). European Journal of Social Sciences, Vol. 13, No. 3, pp. 408-418, 2010. Available at SSRN: https://ssrn.com/abstract=1583943.

- Aizenman, J., Jinjarak, Y., Kim, J., & Park, D. (2015). Tax revenue trends in Asia and Latin America: A comparative analysis (No. w21755). Cambridge, MA: National Bureau of Economic Research.

- Alagidede, P., & Ibrahim, M. (2017). On the causes and effects of exchange rate volatility on economic growth: Evidence from Ghana. Journal of African Business, 18(2), 169–193. doi:10.1080/15228916.2017.1247330

- Arnold, J. (2008). “Do Tax Structures Affect Aggregate Economic Growth?: Empirical Evidence from a Panel of OECD Countries”, OECD Economics Department Working Papers, No. 643, OECD Publishing, Paris, https://doi.org/10.1787/236001777843

- Bahl, R. W. (1972). A representative tax system approach to measuring tax effort in developing countries. Staff Papers, 19(1), 87–124. doi:10.2307/3866441

- Baunsgaard, T., & Keen, M. (2009). Tax Revenue and (or) Trade Liberalization. IMF Working Paper 2005-112. Journal of Public Economics, 94, 563-577.

- Benedek, D., Crivelli, E., Gupta, S., & Muthoora, P. (2014). Foreign aid and revenue: Still a crowding-out effect? FinanzArchiv: Public Finance Analysis, 70(1), 67–96. doi:10.1628/001522114X679156

- Bollerslev, T. (1990). Modelling the coherence in short-run nominal exchange rates: A multivariate generalized ARCH model. The Review of Economics and Statistics, 72, 498–505. doi:10.2307/2109358

- Brafu-Insaidoo, W. G., & Obeng, C. K.(2008). Effect of import liberalization on tariff revenue in Ghana, Vol. 180. Nairobi: African Economic Research Consortium. Retrieved from http://dspace.africaportal.org/jspui/bitstream/123456789/32108/1/RP180.pdf.

- Calderón, C. (2004). Trade openness and real exchange rate volatility: Panel data evidence. Documentos De Trabajo, Banco Central De Chile, 294, 1.

- Chelliah, R. J. (1971). Trends in taxation in developing countries. Staff Papers, 18(2), 254–331. doi:10.2307/3866272

- Chelliah, R. J. (1992). Tax reforms committee. Government of India, Ministry of Finance, Department of Revenue, The University of Michigan.

- Clist, P. (2010). Aid allocation, composition and effects. University of Nottingham. Retrieved from http://eprints.nottingham.ac.uk/11642/

- Côté, A. (1994). Exchange rate volatility and trade. Bank of Canada. Retrieved from http://www.banqueducanada.ca/wp-content/uploads/2010/04/wp94-5.pdf

- Cummings, R. G., Martinez-Vazquez, J., McKee, M., & Torgler, B. (2006). Effects of tax morale on tax compliance: Experimental and survey evidence. Basel: Center for Research in Economics, Management and the Arts.

- De Grauwe, P. (1988). Exchange rate variability and the slowdown in growth of international trade. (IMF Staff Papers35(1)).Washington, DC. USA: IMF Staff Papers.

- De Vita, G., & Abbott, A. (2004). Real exchange rate volatility and US exports: An ARDL bounds testing approach. Economic Issues, 9(1), 69–78.

- Dickey, D. A., & Fuller, W. A. (1979). Distribution of the estimators for autoregressive time series with a unit root. Journal of the American Statistical Association, 74(366a), 427–431.

- Fierro, V., & Reisen, H. (1990), “Tax revenue implications of the real exchange rate: Econometric evidence from Korea and Mexico”, OECD Development Centre Working Papers, No. 12, OECD Publishing, Paris, DOI: 10.1787/171303142365.

- Franco-Rodriguez, S., Morrissey, O., & McGillivray, M. (1998). Aid and the public sector in Pakistan: Evidence with endogenous aid. World Development, 26(7), 1241-1250.

- Gaalya, M. S. (2015). Trade liberalization and tax revenue performance in Uganda. Modern Economy, 6(02), 228. doi:10.4236/me.2015.62021

- Granger, C. W. (1988). Some recent development in a concept of causality. Journal of Econometrics, 39(1–2), 199–211.

- Gupta, A. S. (2007). Determinants of tax revenue efforts in developing countries.IMF Working Papers, pp. 1-39, 2007. Available at SSRN: https://ssrn.com/abstract=1007933

- Gupta, S., Clements, B., Bhattacharya, R., & Chakravarti, S. (2004). Fiscal consequences of armed conflict and terrorism in low-and middle-income countries. European Journal of Political Economy, 20(2), 403–421. doi:10.1016/j.ejpoleco.2003.12.001

- Hau, H. (2002). Real exchange rate volatility and economic openness: Theory and evidence. Journal of Money Credit and Banking, 34(3), 611–630.

- Keen, M., & Simone, A. (2004). Tax policy in developing countries: Some lessons from the 1990s and some challenges ahead. In Sanjeev Gupta, Benedict Clements, & Gabriela Inchauste (Eds.), Helping Countries Develop: The Role of Fiscal Policy. Washington, DC: International Monetary Fund.

- Khattry, B., & Rao, J. M. (2002). Fiscal faux pas? An analysis of the revenue implications of trade liberalization. World Development, 30(8), 1431–1444. doi:10.1016/S0305-750X(02)00043-8

- Le, T. M., Moreno-Dodson, B., & Rojchaichaninthorn, J. (2008). Expanding taxable capacity and reaching revenue potential: Cross-country analysis. World Bank. Retrieved from https://elibrary.worldbank.org/doi/pdf/10.1596/1813-9450-4559

- Lee, Y., & Gordon, R. H. (2005). Tax structure and economic growth. Journal of Public Economics, 89(5–6), 1027–1043. doi:10.1016/j.jpubeco.2004.07.002

- Lotz, J. R., & Morss, E. R. (1970). A theory of tax level determinants for developing countries. Economic Development and Cultural Change, 18(3), 328–341. doi:10.1086/450436

- MacKinnon, J. G. (1996). Numerical distribution functions for unit root and cointegration tests. Journal of Applied Econometrics, 11(6), 601–618. doi:10.1002/(ISSN)1099-1255

- Mahdavi, S. (2008). The level and composition of tax revenue in developing countries: Evidence from unbalanced panel data. International Review of Economics & Finance, 17(4), 607-617.

- Obeng, C. K. (2018). Is the effect of exchange rate volatility on export diversification symmetric or asymmetric? Evidence from Ghana. Cogent Economics & Finance, 6(1), 1460027.

- Obstfeld, M., & Rogoff, K. (1998). Risk and exchange rates. National bureau of economic research. Retrieved from http://www.nber.org/papers/w6694

- Ozturk, I. (2006). Exchange rate volatility and trade: A literature survey. International Journal of Applied Econometrics and Quantitative Studies, 3(1). Retervied from https://ssrn.com/abstract=1127299

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289–326. doi:10.1002/(ISSN)1099-1255

- Phillips, P. C., & Perron, P. (1988). Testing for a unit root in time series regression. Biometrika, 75(2), 335–346. doi:10.1093/biomet/75.2.335

- Pivovarsky, M. A., Clements, M. B. J., Gupta, M. S., & Tiongson, M. E. (2003). Foreign aid and revenue response: Does the composition of aid matter? International Monetary Fund. Retrieved fromhttps://books.google.com/books?hl=en&id=8kWNUdTCBpYC&oi=fnd&pg=PP2&dq=Gupta,+Clements,+Pivovarsky+and+Tiongson+(2003)+&ots=sIoNBcxN2l&sig=LlnFWnT8WPlTw9d6cQ2XyUa1jY4

- Rad, A. A. (2003). The effect of inflation on government revenue and expenditure: The case of theIslamicRepublicofIran. Retrievedfrom:https://papers.ssrn.com/sol3/papers.cfm?abstract_id=513813

- Stotsky, M. J. G., & WoldeMariam, M. A. (1997). Tax effort in sub-Saharan Africa (No. 97-107). International Monetary Fund.

- Tanzi, V. (1989). The impact of macroeconomic policies on the level of taxation and the fiscal balance in developing countries. Staff Papers, 36(3), 633–656. doi:10.2307/3867050

- Tanzi, V. (1992). 12 structural factors and tax revenue in developing countries: A decade of evidence. Open Economies: Structural Adjustment and Agriculture,68, 267–281.

- Tanzi, V., & Blejer, M. I. (1988). Public debt and fiscal policy in developing countries. In The Economics of Public Debt (pp. 230-263). Palgrave Macmillan, London.

- Tarawalie, A, B., Sissoho, M., Conte, M., & Ahortor, C., R. (2013). Export performance and exchange rate volatility: Evidence from the WAMZ. (Occasional paper series, 1(5). West African Monetary Institute (WAMI).

- Tatliyer, M., & Yigit, F. (2016). Does exchange rate volatility really influence foreign trade? Evidence from Turkey. International Journal of Economics and Finance, 8(2), 33. doi:10.5539/ijef.v8n2p33

- Tchokote, J., Uche, M. E., & Agboola, Y. H. (2015). Impact of exchange rate volatility on net-export in selected West African countries. AshEse Journal of Economics, 1(4), 57–73.

- Teera, J. M., & Hudson, J. (2004). Tax performance: A comparative study. Journal of International Development, 16(6), 785–802. doi:10.1002/(ISSN)1099-1328.

- World Bank. (1988). The theory of taxation for developing countries. New York, NY : Oxford University Press. http://documents.worldbank.org/curated/en/634701468766836980/The-theory-of-taxation-for-developing-countries

Appendices

Appendix B: ARCH Test Result on Real Effective Exchange Rate

Appendix C. GARCH (1, 1) Results for Volatility in the Exchange Rate

Appendix D. Results of Unit Root Test with Trend and constant: ADF Test

APPENDIX E. Results of Unit Root Test with constant and trend: PP Test

Appendix F. Test for Joint Significance on Trade Openness—Exchange Rate Volatility Interaction (Short Run)

Appendix G. Test for Joint Significance on Exchange Rate Volatility—Trade Openness Interaction (Long Run)