?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study aims at finding out the determinants of Indian commercial banks profitability. Profitability of Indian banks is measured by three important variables namely, Return on Assets (ROA), Return on Equity (ROE) and Net Interest Margin (NIM). The study also uses a set of independent variables such as bank-specific factors which include bank size, assets quality, capital adequacy, liquidity, operating efficiency, deposits, leverage, assets management and the number of branches. Pooled, fixed and random effects models and Generalized Method of Moments (GMM) are built on panel data of 10 years for more than 60 commercial banks of India.

The study also takes into account Gross Domestic Product (GDP), inflation rate, interest rate and exchange rate as macroeconomic determinants. The results of the study show that all bank-specific factors, except the number of branches, exhibited significant impacts on profitability as measured by NIM. The findings also show that all macroeconomic determinants used in the study are found to be significant with negative impacts on Indian commercial banks profitability. Furthermore, the results show that bank size, number of branches, assets management ratio and leverage ratio are highly significant variables of profitability in the context of Indian commercial banks as measured by ROA. The results give a better insight into the Indian banking sector and the determinants of its profitability

PUBLIC INTEREST STATEMENT

This paper examines the factors that affect the profitability of Indian commercial banks. India is the largest country in South Asia with a considerable financial system characterized by diversified financial institutions. So, knowing the factors that affect the profitability of its banking sector is very important to everybody in the country. The study uses secondary data that were collected from the Reserve Bank of India (RBI) database. Different analytical models are used to test the impact of the micro and macro factors on the Indian banking profitability. The results revealed that bank size, number of branches, assets management ratio and leverage ratio are the most important bank-specific determinants of profitability of Indian commercial banks as measured by ROA. The study recommended that regulators and policymakers should consider the macroeconomic factors in such a way that improve the profitability of the Indian banks.

1. Introduction

India is one of the largest countries in South Asia region with a sound financial system characterized by a diversified portfolio of financial institutions (Ghosh, Citation2016). Currently, India is one of the fastest-growing economies in the world. There are many banks and financial institutions in India, and they perform different tasks in economic activities. Indian banking is receiving more attention recently because of a higher Gross Domestic Product (GDP) growth rates.

There is no doubt that banks convert deposits into productive investments as a method to facilitate economic growth in any country (Levine et al., Citation2000; Tabash & Dhankar, Citation2014; Tabash, Citation2018). A reliable and efficient banking system has to achieve three goals: to give a considerable profit, to offer a high-quality service to customers, and to have sufficient funds to lend to borrowers. The growth of any economy largely depends on its banking sector. Hence, the importance of bank profitability in the economy can be determined at the micro and macro levels. At the micro level, profit is a determinant and required for any competitive banking institution. Every bank tries to earn and achieve good profits in order to be in the business especially at the time of growing competition in the financial markets. At the macro level, a profitable banking sector should be able to absorb external negative shocks and to achieve the stability of the financial system.

The study of profitability of the banking sector is of a great interest in the developed economies. However, in emerging economies like India, the number of studies that focus on profitability of commercial banks is not too many. In this context, the study of the profitability of commercial banks in India will be of greater interest for policymakers and finance scholars. This means the understanding of the determinants of bank profitability is essential and pivotal to the stability of the economy because the well-being of the banking sector is very critical to the welfare of the economy at large.

In the early of the 1990s, India has achieved a significant progress in the performance and efficiency of its banking sector o (Ghosh, 2016). After 1991, the Indian banking sector has contributed and supported other major industries (Singh, Sidhu, Joshi, and Kansal, Citation2016). The banking system in India is a mixture of public, private, foreign, regional rural, urban cooperative and rural cooperative banks (Shrivastava, Sahu, and Siddiqui, Citation2018). Commercial banks in India dominate the financial system and play a major role in economic development. Taking into account the vibrant, competitive Indian environment, commercial banks should manage optimally their asset allocation to enhance its profitability (Viswanathan, Ranganatham, and Balasubramanian, Citation2014).

1.1. Study objectives, problem statement and importance

The purpose of the current study is to examine the effect of internal and external determinants on Indian commercial banks profitability. The existing study concentrates on a very important sector, banking sector, in an emerging economy like India. Taking into account some new governmental policies such as the demonetization process that could influence the profitability of Indian banks. Furthermore, fraud cases that came to the surface recently in February 2018 when tax department of India discovered that Indian banks could take a hit of more than U.S. $ 3.0 billion as a result of Punjab National Bank scam which is the second-biggest governmental bank in the country. Moreover, the Reserve Bank of India (RBI) showed in the bi-annual financial stability report on (30 June 2017) some big issues regarding the sustainability of the Indian banking system.

Reserve Bank of India (RBI) warned that the banking sector is under severe pressure, due to increased bad loans and an increase in bank fraud. Based on the above concerns, the current study brings the attention of policymakers and researchers to work and study the bank-specific factors that could affect the profitability of Indian commercial banks. The paper is structured as follows: Section 2 presents the related literature review of banking profitability. Section 3 gives a description of the determinants of profitability of Indian commercial banks. Section 4 provides descriptions of the data and research methodology Section 5 shows the econometric results and discussions. Section 6 concludes this paper with recommendations.

2. Literature review

Extensive research in many countries and regions around the globe has been conducted for examining the factors that influence a bank’s profitability. Prior studies of a bank’s profitability can be classified into three categories. First, studies related to a bank’s profitability determinants that are empirically examined in different countries around the world (e.g. Perera and Wickramanayake (Citation2016) who studied 122 countries, Dietrich and Wanzenried (Citation2014) who studied 118 countries and Masood and Ashraf (Citation2012) who studied 14 countries). Second, studies that compare a bank’s profitability determinants among different banks in the same region (e.g. Chowdhury and Rasid (Citation2017) who studied GCC countries, Petria, Capraru, and Ihnatov (Citation2015) who studied EU 27 countries, Roman and Camelia (Citation2015) and Dietrich and Wanzenried (Citation2011) who studied CEE countries, Menicucci and Paolucci (Citation2016) who studied Europe, Jara-Bertin, Moya, and Perales (Citation2014) who studied, Lemma and Negash (Citation2013) who studied Nine African countries). Finally, studies that have investigated a bank’s profitability determinants and focused only on a single country. For example, Zouari-Ghorbel (Citation2014) and Bougatef (Citation2017) who studied Tunisia, Marijana, Poposki, and Pepur (Citation2012) who studied Macedonia, Tan and Floros (Citation2015) and Tan (Citation2016) who studied China, Bouzgarrou, Jouida, and Louhichi (Citation2017) who studied France, Bose, Saha, Zaman, and Islam (Citation2017) and Robin, Salim, and Bloch (Citation2018) who studied Bangladesh, Athanasoglou, Brissimis, and Delis (Citation2008) who studied Greece, Ramlan and Adnan (Citation2016) Malaysia, de Mendonça and da Silva (Citation2018) Brazil, Kapaya and Raphael (Citation2016) who studied Tanzania, Growe, DeBruine, Lee, and Maldonad (Citation2014) who studied the United States, AL-Omar and AL-Mutairi (Citation2008) who studied Kuwait and Almaqtari, Al‐Homaidi, Tabash, and Farhan (Citation2018) and Singh and Sharma (Citation2016) who studied India (see Table below).

Table 1. Review of related literature

Majority of the prior studies have measured profitability by ROA and ROE. For example, Chowdhury and Rasid (Citation2017); Naeem, Baloch, and Khan (Citation2017); Zampara, Giannopoulos, and Koufopoulos (Citation2017); Tiberiu (Citation2015); Singh and Sharma (Citation2016). However, bank’s profitability was investigated by prior research as a function of both bank-specific (internal) and macroeconomic (external) determinants. Bank specific determinants are related to the direct result of managerial decisions of a bank (Louzis, Vouldis, & Metaxas, Citation2012; Rjoub, Civcir, & Resatoglu, Citation2017; Saona, Citation2016; Singh & Sharma, Citation2016). Several studies such as Petria et al. (Citation2015); Salike and Ao (Citation2017); Tiberiu (Citation2015); Pathneja (2016); Rashid and Jabeen (Citation2016); Garcia and Guerreiro (Citation2016); Singh and Sharma (Citation2016); Rani and Zergaw (Citation2017); Rjoub et al. (Citation2017); Zampara et al. (Citation2017); Bougatef (Citation2017) assessed bank-specific determinants including variables such as capital adequacy ratio, asset quality ratio, liquidity ratio, operating efficiency ratio, deposits ratio and bank size.

On the other hand, macroeconomic factors are determinants that are related to economic, industrial and legal environments that are out of a bank’s control (Ongore & Kusa, Citation2013). Macroeconomic determinants comprise variables such as GDP, inflation rate, interest rate and exchange rate (Acaravci & Çalim, Citation2013; Chowdhury & Rasid, Citation2017; Jara-Bertin et al., Citation2014; Marijana et al., Citation2012; Masood & Ashraf, Citation2012; Menicucci & Paolucci, Citation2016; Saona, Citation2016; Pasiouras & Kosmidou, Citation2007).

Although extensive research has been conducted on banks’ profitability determinants in different countries, a comprehensive empirical evidence from emerging and developing countries have either yielded ambiguous evidence or mixed results (Almaqtari et al., Citation2018). With regard to banks’ profitability determinants studies in the Indian context, there are not too many studies that investigate this issue. Singh and Sharma (Citation2016) have examined bank-specific and macroeconomic factors that determined the liquidity of Indian banks. Further, Almaqtari et al. (Citation2018) have examined “bank-specific and macroeconomic factors that determined the profitability of Indian commercial banks. They found that bank size, assets management ratio has a significant impact on banks’ profitability as measured by both ROE and ROA. In addition, while operational efficiency, the number of branches and leverage ratio were found to have an impact on ROA, both assets quality and liquidity ratios had a positive and significant effect on ROE. Furthermore, the results revealed that macroeconomic factors such as GDP, inflation rate, exchange rate, interest rate, financial crisis have a significant effect on the ROE. However, inflation rate, exchange rate, the interest rate, and demonization are only found to have a significant effect on ROA.

Accordingly, the current research aims to investigate Indian commercial banks’ profitability determinants. More specifically, it empirically evaluates bank-specific and macroeconomic determinants that may have an impact on Indian commercial banks’ profitability as measured by ROA, ROE and NIM. The present study bridges a serious gap in Indian banks’ profitability literature. Furthermore, the current study extends, contributes and builds on the work of Almaqtari et al. (Citation2018) who ignored a major proxy of banks’ profitability namely; Net Interest Margin NIM and comprehensively investigated bank-specific and macroeconomic determinants of Indian commercial banks. The current study also uses different econometric techniques for analysis of data, which give more sound results.

3. Profitability determinants of Indian commercial banks

3.1. Dependent variables

Majority of prior profitability studies commonly used two main proxies to measure profitability which are ROA and ROE (e.g. Athanasoglou et al., Citation2008; Garcia & Guerreiro, Citation2016; Naeem et al., Citation2017; Pathneja, 2016; Singh & Sharma, Citation2016; Tabash, Citation2018; Tiberiu, Citation2015; Zampara et al., Citation2017). However, this study uses ROA, ROE, and NIM as proxies for banks’ profitability. ROA is measured as the percentage of a year’s net profit to the total assets of the same year (see Table ). Similarly, ROE is calculated as the percentage of a year’s net profit to the total equity of the same year. Further, NIM is measured by net interest income divided by total assets (Rani & Zergaw, Citation2017; Saif, Citation2014; Sarkar, Sarkar, & Bhaumik, Citation1998 and Yeon & Kim, Citation2013).

Table 2. Definitions and measurements of variables

3.2. Explanatory variables

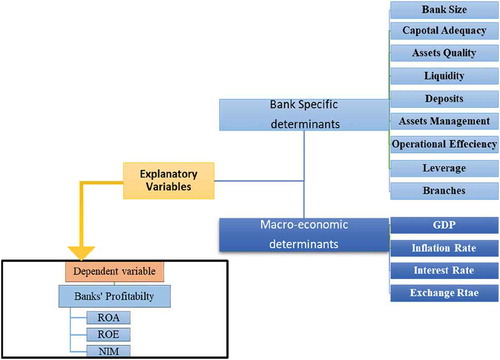

Figure provides two categories of explanatory variables namely; bank-specific and macroeconomic determinants. Bank-specific determinants comprise bank size, assets quality, capital adequacy, liquidity, operating efficiency, deposits, leverage, assets management and the number of branches. Macroeconomic determinants of banks’ profitability include GDP, inflation rate, interest rate, and exchange rate. Following is an explanation of both the categories of explanatory variables.

Figure 1. Framework of the study.

3.2.1. Bank specific determinants

3.2.1.1. Assets size (LNAS)

Prior studies used total assets as a proxy for measuring bank size. More specifically, they are used the natural logarithm of total assets as a measure for bank size (Acaravci & Çalim, Citation2013; AL‐Omar and AL‐Mutairi, Citation2008; Anbar & Alper, Citation2011; Bougatef, Citation2017; Chowdhury & Rasid, Citation2017; Masood et al., 2012; Petria et al., Citation2015; Singh & Sharma, Citation2016). Anbar and Alper (Citation2011) and Masood and Ashraf (Citation2012) reported a positive effect of banks size on banks’ profitability. Whereas, Gul, Irshad, and Zaman (Citation2011) and Singh and Sharma (Citation2016) found a negative effect on banks’ profitability.

3.2.1.2. Capital adequacy (CAD)

Capital adequacy is measured by the percentage of equity to total assets. It is an essential ratio that determines capital strength (Abel & Roux, Citation2016; Anbar & Alper, Citation2011; Masood & Ashraf, Citation2012). Ebenezer, Omar, and Kamil (Citation2017) revealed that there is a positive association between both the banks’ profitability and capital adequacy ratio.

3.2.1.3. Assets quality (AQ)

The percentage of loan to total assets is widely used by prior studies as a measure for assets quality. It is expected to have a negative impact on a bank’s profitability except when the bank is at unbearable risk levels (Rani & Zergaw, Citation2017).

3.2.1.4. Liquidity (LIQ)

The ratio of liquid assets to total assets is used as a measurement for liquidity (Bougatef, Citation2017; Chowdhury & Rasid, Citation2017; Jara-Bertin, Moya, and Perales, Citation2014; Menicucci & Paolucci, Citation2016). Greater the ratio of liquidity, more is the cost of higher return. Further, inadequate liquidity levels may lead to a bank’s failure. Prior studies have reported mixed evidence regarding the effect of liquidity on banks’ profitability (Issn, Ebenezer, Ahmad, & Bin, Citation2017; Loh, Citation2017).

3.2.1.5. Deposits (DEP)

The ratio of total deposits to total assets is commonly used by previous studies as a measure for deposits ratio (Acaravci & Çalim, Citation2013; Menicucci & Paolucci, Citation2016; Zampara et al., Citation2017). Gul et al. (Citation2011) concluded a negative link between banks’ profitability and deposits ratio.

3.2.1.6. Asset management (AM)

Assets management ratio is measured by ratio of operating income to total assets. Masood, Ashraf and Ashraf (2012) reported that there is a positive relationship between banks’ profitability and higher assets management ratio.

3.2.1.7. Operating efficiency (OPEF)

Rashid and Jabeen (Citation2016) defined operating efficiency as the percentage of operating expenses divided by interest income. The lower operating efficiency ratio, the greater management efficiency is.

3.2.1.8. Leverage (LEV)

Bose et al. (Citation2017) defined leverage ratio as the percentage of total debt divided by total assets. Athanasoglou et al. (Citation2008) argue that lower leverage (higher equity) leads to greater ROA but lower ROE.

3.2.1.9. Branches (BRNCH)

The absolute number of branches that a bank has is used to denote branches. It expresses the market share and the geographical distribution of the bank.

3.2.2. Macroeconomic determinants

3.2.2.1. Annual real GDP

Numerous studies have used GDP as a macroeconomic factor and a common measure that is used to measure the aggregate economic activity within an economy (Francis, Citation2013; Marijana et al., Citation2012; Masood, Ashraf, and Ashraf, 2012; Ongore & Kusa, Citation2013; Pasiouras & Kosmidou, Citation2007; Petria et al., Citation2015; Rani & Zergaw, Citation2017; Saona, Citation2016; Singh & Sharma, Citation2016).

3.2.2.2. Annual inflation rate (INF)

It reflects the increasing trend in the general level of levels of goods and services prices. Further, it reflects the purchasing power of a currency (Singh & Sharma, Citation2016). Inflation rate has been widely used by prior studies of banks’ profitability (Anbar & Alper, Citation2011; Chowdhury & Rasid, Citation2017; Jara-Bertin et al., Citation2014; Masood, Ashraf, and Ashraf, 2012).

3.2.2.3. Interest rate (INTR)

The interest rate reflects the lending interest rate that a bank gains. Mixed evidence was reported by prior studies of the effect of interest rate on banks’ profitability. While Rashid and Jabeen (Citation2016) reported a negative effect of interest rate on banks’ performance, Yahya, Akhtar, and Tabash (Citation2017) found a positive effect.

3.2.2.4. Exchange rate (EXCH)

The average of the exchange rate during a fiscal year is used as a measurement for exchange rate. Chowdhury and Rasid (Citation2017) and Menicucci and Paolucci (Citation2016) suggested that foreign exchange rate should be used as an important factor for banks’ profitability.

4. Data and methodology

This section provides a discussion of data collection, sampling procedure, models and econometric tools used by this study.

4.1. Data collection and sampling

The database of the Reserve Bank of India (RBI) provides all the information related to the banking system in India. It has been considered as the most authenticate database for banking information in India. It provides information for 93,913 rural cooperative banks, 1,574 urban cooperative banks, 56 regional rural banks, and 101 commercial banks (see Table ). These commercial banks comprise 46 foreign banks, 21 national banks, 6 State Bank of India (SBI) and its associates, 26 private banks and 2 other banks. As the present study considers only commercial banks, a sample of 69 banks based on the availability of the data for the time period of this study is selected. This forms a panel of balanced data set of 690 bank year observation. A panel of 69 commercial banks over a period of 10 years from 2008 to 2017 is employed.

Table 3. Sample selection

Due to the unavailability of data and the approach used by the present study to empirically examine the profitability determinants of the Indian banks, the sample of this study considered only the Indian commercial banks. Further, as the public banks (national banks and SBI and its associates) contribute about 70% of the total assets of the banks in India, this study is limited to the commercial banks and excluded the rural cooperative banks, the urban cooperative banks, and the regional rural banks. Accordingly, 68% of the total number of commercial banks working in India including the public banks (national banks and SBI and its associates) is selected as a sample for this study.

This could provide an evidence of the factors that may affect Indian banks’ profitability during the period from 2008 to 2017. This period has witnessed different challenges for the Indian banking system. One of the critical challenges that was encountered by the Indian commercial banks during this period is the declining of the financial performance. Apart from this, the demonetization process started in November 2016, fraud cases which hit some commercial banks and some other financial challenges in this period made the investigation of this topic very important and interesting which may provide an evidence for bankers and policymakers.

To compare the sample of the present study with the sample used by some other studies, most of the prior studies that have investigated banks’ profitability have been used in the panel data. For example, Zouari-Ghorbel (Citation2014) used 16 Tunisian banks over a period from 2003 to 2012, Chowdhury and Rasid (Citation2017) employed a sample from 29 banks from GCC countries during 2005–2013, Marijana et al. (Citation2012) analysed 16 Macedonian banks over a period between 2005 and 2010, Tan and Floros (Citation2015) sampled 101 banks from China during 2003–2009, Bose et al. (Citation2017) used a sample of 30 Bangladeshi banks over a period from 2009 to 2014, Tan (Citation2016) fetched data of 41 Chinese banks for a period from 2003 to 2011, Ramlan and Adnan (Citation2016) studied 5 Malaysian banks from 2006 to 2011, de Mendonça and da Silva (Citation2018) used 18 Brazilian banks from 2001 to 2015 and Growe et al. (Citation2014) employed data of 105 banks in the United States from 1994 to 2011.

However, in the Indian context, there are not many studies that investigate commercial banks’ profitability. In this regard, only a few studies were found. Rao, Rezvanian, and Nyadroh (Citation2009) investigated 55 banks from 1998 to 2003, Bapat (Citation2017) used 42 banks during 2007–2013, Ahamed (Citation2017) analysed 107 banks from 1998 to 2014, Reddy (Citation2011) examined 87 banks during 1992–2006, and Singh and Sharma (Citation2016) drew a sample of 59 banks from 2000 to 2013. It was observed that the year 2014 is the most recent year included by prior studies conducted in India. However, the study of Almaqtari et al. (Citation2018) has the same sample of banks and years of the current study with a different scope which makes the current study is an extension of it and debates the issue of banks’ profitability from a different scope, perspective, and methods of analysis.

4.2. Model specification and econometric tools

Menicucci and Paolucci (Citation2016) stated that prior studies employed a functional linear model to investigate the issues of bank profitability. They argue that it is the proper form of analysis to examine banks’ profitability. In the same context, different studies used different models to assess the determinants of banks’ profitability. While, Rjoub et al. (Citation2017), Pathneja (2016), and AL‐Omar and AL‐Mutairi (Citation2008) used linear regression models with pooled, fixed or/and random effect models, Bougatef (Citation2017), Chowdhury and Rasid (Citation2017), Rashid and Jabeen (Citation2016), Saona (Citation2016), Louzis et al. (Citation2012), Masood and Ashraf (Citation2012) and Dietrich and Wanzenried (Citation2014) employed both linear regression model and GMM. Accordingly, following those studies that conducted both linear regression model and GMM, this study uses the same tools for analysing the determinants of Indian banks’ profitability. Using the panel approach in the present study is justified by two main merits that have been advocated by Hsiao (Citation2003); Baltagi (Citation2005). They revealed that panel analysis provides an efficient econometric estimate as compared to cross-sectional or time-series data sets and Kyereboah-Coleman (Citation2007) advocated that panel analysis has the power to control for individual heterogeneity and multicollinearity.

Thus, this study has employed a balanced panel data of 69 Indian commercial banks over a period from 2008 to 2017. At the initial stage of the data analysis, an examination of all assumptions required for the linear regression used was met. Then, the study conducted a linear regression of pooled, fixed and random effect models to increase and make the estimates more consistent and comparable.

Different studies have constructed a structure of panel analysis (Chowdhury & Rasid, Citation2017; Brooks, Citation2014; Masood, Ashraf, and Ashraf, 2012). The present study follows the same structure and context of these studies using the following panel data equation:

Where refers to the profitability(dependent variable),

is the intercept term on the explanatory variables,

is a k × 1 vector of parameter to be estimated, and vector of observations is

which is 1 × k, t = 1…, T; n = 1,…, N. the practical and operational form. Equation (1) can be defined as follows:

Profitability is measured by ROA, ROE and NIM. Bank-specific variables comprise of capital adequacy, assets quality, liquidity, deposits, assets management, operational efficiency, asset size, leverage and branches. However, macroeconomic variables are “GDP, inflation rate, interest rate and exchange rate”. Thus, Equation (2) could be restructured and expanded using the three proxies of profitability as follows:

Where i indicates an individual bank; t refers to year; β1: β13 are the coefficients of determinant variables and ε is the error term; and all other variables are as defined in Table . These three models have been constructed to examine the factors that may determine banks’ profitability in India. The models were framed based on that banks’ profitability in India as a function and is dependent on both bank specifics and macroeconomics. Each regression model was estimated using pooled, fixed and random effect model. Further, the Hausman test is conducted to decide the appropriate model between both fixed and random effect estimates. If the value of Hausman test is greater than the critical chi-square χ2 0.5,10 = 9.341 or χ2 0.005,10 = 25.182, then the fixed effects model is the proper estimate (Pasiouras & Kosmidou, Citation2007). Accordingly, Hausman test was used by this study to compare between fixed effect and random effect model.

In addition to the linear regression models used by this study, a GMM estimator was used. Athanasoglou et al. (Citation2008) reported that GMM account for possible correlations between the independent variables. Similarly, problems related to individual heterogeneity are some justifications for using GMM (Saona, Citation2016). Both difference and system GMM estimators are appropriate for samples with small T, large N panels; independent variables that are not strictly exogenous; fixed individual effects; heteroscedasticity and autocorrelation (Roodman, Citation2006). The difference of GMM estimators can be subjected to serious finite sample biases if the instruments used have near unit root properties (Chowdhury & Rasid, Citation2017). Then, following Saona (Citation2016) the application of a dynamic model of banking profitability takes the following form:

Where represents the vector of the intra-bank determinants of profitability,

is the vector of the extra-bank determinants and

,

and εit measure the individual effect, the temporal effect, and the stochastic error, respectively. Specifically

And

5. Data analysis and results

5.1. Descriptive statistics

Table illustrates descriptive statistics for the variables used in this study. It provides details in the form of maximum, minimum, mean, median and the standard deviation for the dependent variable and its explanatory variables. The results demonstrate the trend of profitability measurements; ROA, ROE and NIM over the period 2008–2017. Similarly, the results show the descriptive statistics for bank-specific and macroeconomic variables for the same period. The results reveal that ROA, ROE and NIM each range between minimum values of −4.2, −44. 37 and 0.22 and maximum values of 10.23, 31.37 and 7.34 with a mean of 1.17, 10.16 and 3.02 respectively. This signifies negative skew distribution during 2008–2017. The results in Table also indicate that there is a variation between the mean values and standard deviation of both bank-specific and macroeconomic variables for the same period. Bank specific determinants have an average value of 12.65 for LNAS, the ratio of CAD, AM, DEP, and OPEF are 19.30%, 2.59%, 71.55% and 2.0 3% with standard deviation of 2.24%, 16.85%, 1.69%, 18.52% and 1.27% respectively.

Table 4. Descriptive statistics

On an average, AQ, LIQ and LEV have values of 3.92%, 3.65% and 4.34% with standard deviation of 0.47 %, 0.28% and 0.34% respectively. The variation between the mean values and the median values of all variables signifies that there is a considerable heterogeneity among the selected banks. From macroeconomic context, GDP ranges between a minimum value of 3.89 and a maximum value of 10.26 with a mean value of 7.33. Similarly, inflation fluctuates between a minimum value of 4.91 and a maximum value of 11. 99 with a mean value of 8.32. More specifically and with regard to industry-specific variables, interest rate has a mean value of 7.10 with a standard deviation of 1.06 and (Min. = 4.75, Max. = 8.00). The exchange rate also has an average value of 52.94 (Min. = 41.49, Max. = 67.18).

5.2. Correlation and multicollinearity diagnostics

Table demonstrates Pearson correlation matrix and multicollinearity diagnostics for profitability measurements, bank-specific and macroeconomic variables. Concerning bank-specific variables, the results indicate that AQ, BRNCH, LEV and LNAs have a negative association with ROA and NIM but a positive correlation with NIM. In the same vein, DEP and LIQ show a negative link with all profitability measures; ROA, ROE, and NIM. This may indicate that DEP and LIQ contribute negatively to the profitability of the Indian banks.

Table 5. Correlation matrix and multicollinearity diagnostics

Further, the results illustrate that CAD and OPEF have a positive correlation with both ROA and NIM but a negative relationship with ROE. With regard to macroeconomic variables, the results indicate that all macroeconomic determinants except for INTR have a negative correlation with all profitability measures; ROA, ROE, and NIM. EXCH, GDP and INF show a negative association with ROA, ROE, and NIM. However, INTR has a positive association with the three measures of profitability; ROA, ROE, and NIM. The results also show that the highest value of correlation exhibited between two variables is 0.67 which was found in case of LEV and LNAS which indicates the absence of multicollinearity issues among variables. For more reliable analysis, multicollinearity diagnostics was conducted using both VIF and Tolerance tests. The results in Table , Panel B reports VIF and Tolerance values for all independent variables. VIF has a maximum value of 3.75 and the lowest value of tolerance is 0.27 which indicate that there are no multicollinearity problems among independent variables.

5.3. Results of model estimation

Table shows the empirical results of the estimates for the models framed in Equations (1–5). The results report three estimates for each model. The three estimates are pooled OLS, fixed and random effect models. The results provide an estimation for each model and are presented into two categories; Bank specific and macroeconomic determinants of profitability. Overall, the results reveal that the adjusted R square for ROA is 0.53 for both pooled and random effect models but it is 0.66 in case of fixed effect model. This indicates that both bank-specific and macroeconomic determinants contribute about 53% and 66% respectively to the profitability as measured by ROA. Further, the adjusted R square of ROE is 0.45 for pooled model, 0.46 for fixed effect model and 0.22 for random effect model. This signifies that both bank-specific and macroeconomic determinants explain about 45%, 46%, and 22% respectively of the variation of banks’ profitability. Furthermore, regarding NIM, the results show that the values of adjusted R squared are 0.40, 0.49 and 0.40 for pooled, fixed and random effect models respectively. This signifies that both bank-specific and macroeconomic determinants explain about % 40, %49 and %40 of bank’s profitability. All the three models applied with its sub-models (pooled, fixed and random) are found to have a p value of less than 1% which indicate that these models are fit and significant.

Table 6. Model estimation results summery

To compare and evaluate between fixed and random effect models, the Hausman test is conducted. The results show that the p value of Hausman test is more than 5% (p value>0.05) suggesting that random effect model is accepted and statistically preferred over fixed effect model.

5.3.1. Bank specific determinants

As illustrated in the random effect model in Table for ROA, among bank-specific factors, only AM ratio, LEV ratio, and LNAS are found to have statistically significant impact on ROA. AM ratio and LEV ratio both have significant impact at the level of 1% (p value = 0.00 < 0.01) while LNAS is significantly high at the level of 5% (p value = 0.02 < 0.05). They are all found significant at the level of 1% significance level. The coefficient of AM ratio and LNAS are found to be positive revealing that they have a statistically significant positive impact on ROA. This is consistent with (Chowdhury & Rasid, Citation2017; Jara-Bertin et al., Citation2014; Masood et al., 2012; Menicucci & Paolucci, Citation2016) who reported that banks with greater assets size lead to higher profitability, but is inconsistent with Athanasoglou et al. (Citation2008) who revealed that bank size does not significantly influence a bank’s profitability. However, LEV ratio has a negative coefficient suggesting that ROA is negatively affected by the ratio of total liabilities to total assets.

Concerning the impact of bank-specific determinants on ROE, the results reveal that AM ratio, AQ ratio, and LNAS have statistically significant positive impact on ROE while LEV ratio and OPEF have a negative impact. This suggests that both total operating expenses and total liabilities scaled by total assets are high as compared to total assets, which affect negatively the profitability of Indian banks. This is in accordance with Marijana et al. (Citation2012), AL-Omar and AL-Mutairi (Citation2008) and Petria et al. (Citation2015). They argue that operating expenses contribute importantly and it is a significant determinant of a bank’s profitability. This argument is also supported by Salike and Ao (Citation2017) and Mauricio Jara-Bertin et al., (Citation2014). They have provided an evidence that operational efficiency is an important determinant that explains significantly a bank’s profitability. Contradictory, Francis (Citation2013), Yahya et al. (Citation2017) Chowdhury and Rasid (Citation2017) revealed that operational efficiency ratio has statistically significant negative effect on ROA. However, Naeem et al. (Citation2017) found an insignificant association and a negative impact of operational efficiency ratio on ROA.

Concerning NIM, the results reveal that all bank-specific factors except BRNCH have statistically significant impact on NIM. They all have a positive coefficient sign except LEV ratio which has a negative coefficient revealing that they have statistically significant positive impact on NIM. The negative coefficient of LEV ratio indicates a negative impact and decrease in the profitability of Indian banks as measured by NIM.

Overall, it is notably depicted from the results that LEV ratio has statistically significant negative impact on all measurements of profitability; ROA, ROE, and NIM. This impact is consistent in all the three models applied; pooled, fixed and random across the profitability measurements. Further, it is observed that liquidity has no statistically significant impact on both ROA and ROE. This contradicts (Bougatef, Citation2017; Jara-Bertin et al., Citation2014; Petria et al., Citation2015) who found that a bank’s profitability is positively related to liquidity. In contrast, Menicucci and Paolucci (Citation2016) reported that higher the deposits and loans ratio of a bank, the more profitable the bank become.

5.3.2. Macroeconomic determinants

Regarding the effect of macroeconomic determinants on the profitability of Indian banks, the results in Table show that all macroeconomic determinates except GDP have statistically significant effect on ROA. Both EXCH rate and INTR rate exhibited a significant and negative effect on ROA revealing an inverse contribution to the profitability of Indian banks as measured by ROA. This outcome is consistent with Rashid and Jabeen (Citation2016) who have reported that lending interest rate affects negatively the performance of banks. However, this finding contradicts Tiberiu (Citation2015) who reported that the interest rate margins positively affect the banks’ profitability. Further, a contradictory result was found by Saona (Citation2016) who concluded a positive relationship between a bank’s profitability and foreign exchange.

With respect to ROE, only EXCH rate and GDP show statistically significant effect on ROE. EXCH rate exhibits a negative effect while GDP shows a positive impact on ROE. This result is supported by Louzis et al. (Citation2012), Marijana et al. (Citation2012) and Petria et al. (Citation2015) who supported that the economic growth has an influence on bank profitability but contradicts Rashid and Jabeen (Citation2016) who found that GDP has a negative influence on the performance of banks.

However, among macroeconomic factors, only EXCH rate has a statistically significant impact on NIM. It has a negative coefficient revealing a negative influence on NIM. Overall, EXCH rate shows statistically significant negative impact on the three profitability measures; ROA, ROE and NIM across the three models conducted. This could be attributed to the declining exchange rate represented by the exchange rate of the Indian rupee to the U.S. $ (41.49 in 2008 and 67.18 in 2017).

ROA is the ratio of bank net profit to total assets, ROE is the ratio of net profit to shareholders’ equity, NIM is the ratio of interest-bearing assets LNA is the natural logarithm of total assets, CAD is the capital adequacy ratio (%), AQ is the assets quality (%), LIQ is the liquidity ratio (%), DEP is the deposits of the total assets (%), AM is the assets management (%), OPEF is the ratio of operating efficiency (%), LEV is the financial risk (%), BRNCH is the No. of branches, GDP is the real gross domestic product (%), INF is the annual inflation rate(%), INTR is the lending Interest rate (%), EXCH is the exchange rate

5.4. GMM estimation

Table reports the results of GMM estimation. With respect to ROA, the results show that among the internal bank-specific factors; AM ratio, LNAS, LEV ratio and BRNCH are significantly related to ROA. These variables except LEV ratio have positive coefficient which signifies that AM ratio, LNAS and BRNCH are positively and significantly related to ROA. However, among macroeconomic factors, only GDP and INTR rate show significant evidence at the level of 1% (p value < 0.01). They are both associated negatively with ROA.

Table 7. GMM estimation results summary

Concerning ROE, most bank-specific factors show statistically significant evidence except for LNAS, CAD, and DEP. This indicates that AQ ratio, LIQ ratio, AM ratio, OPEF ratio, LEV ratio and the number of branches is significantly related to ROE. Further, the results also illustrate that all macroeconomics factors are significantly associated with ROE. Notably, all bank-specific factors have a positive coefficient while macroeconomic factors have a negative coefficient. This suggests that bank-specific factors are significantly and positively related to ROE but macroeconomic factors are negatively related to ROE.

However, all bank-specific factors except CAD ratio and BRNCH have statistically significant impacts on NIM. DEP ratio, OPEF ratio, and LEV ratio have statistically significant negative impact on NIM while LNAS, AQ ratio and LIQ ratio are positively related to NIM. Further, all macroeconomic factors except INTR have statistically significant negative impact on NIM.

LAGDV is the lagged of dependent variables, ROA is the ratio of bank net profit to total assets, ROE is the ratio of net profit to shareholders’ equity, NIM is the ratio of interest-bearing assets LNA is the natural logarithm of total assets, CAD is the capital adequacy ratio (%), AQ is the assets quality (%), LIQ is the liquidity ratio (%), DEP is the deposits of the total assets (%), AM is the assets management (%), OPEF is the ratio of operating efficiency (%), LEV is the financial risk (%), BRNCH is the No. of branches, GDP is the real gross domestic product (%), INF is the annual inflation rate(%), INTR is the lending Interest rate (%), EXCH is the exchange rate.

6. Conclusion and recommendations

The present paper investigated the impact of bank-specific and macroeconomic determinants on banks’ profitability. Banks’ profitability as measured by ROA, ROE, and NIM of 69 Indian commercial banks during a period from 2008 to 2017 was a function of both bank-specific and macroeconomic determinants. Bank-specific variables have been considered as independent variables, which comprised of variables namely; assets size, capital adequacy, asset quality, liquidity, deposit, asset management, operating efficiency, financial risk and the number of branches. Similarly, macroeconomic determinants represent the second category of independent variables that included GDP, inflation rate, exchange rate and interest rate.

Regarding bank-specific determinants, the results revealed that Indian commercial banks’ profitability as measured by ROA has a positive relationship with assets, bank size, management ratio and the number of branches but a negative association with leverage ratio. This indicates that bank size, assets management ratio, the number of branches and leverage ratio are the most significant bank-specific determinants that influence Indian commercial banks’ profitability as measured by ROA. From the macroeconomic perspective, the results also found that while inflation rate has a positive association, interest rate, exchange rate and GDP have a negative relationship with Indian commercial banks’ profitability as measured by ROA.

Concerning the effect of bank-specific determinants on Indian commercial banks’ profitability, as measured by ROE, the results found that bank size, assets management ratio, leverage ratio, assets quality ratio, operational efficiency, liquidity ratio, number of branches and all macroeconomic factors have a significant effect on ROE. The results also indicate that there is a negative association between ROE and leverage ratio, operating efficiency, exchange rate, number of branches, inflation rate and interest rate. However, a positive relationship was exhibited between ROE and asset management ratio, bank size, assets quality ratio, liquidity ratio, and GDP.

Regarding profitability of Indian commercial banks’, profitability as measured by NIM, the results revealed all bank-specific factors except a number of branches, which exhibit a significant effect on profitability as measured by NIM. They all have a significant positive impact except for deposits ratio, leverage ratio and operating efficiency which reveals a negative impact on NIM. On the other hand, macroeconomic variables such as exchange rate, interest rate, and GDP show a significant negative effect on profitability as measured by NIM. However, inflation rate exhibited statistically significant negative influence on NIM.

The present study sought to fill a demanding gap in the existing body of literature of banks on specific and macroeconomic determinants of Indian commercial banks’ profitability by providing a new empirical evidence. The outcomes of the present study have significant contributions to the existing stock of literature by comprehensively clarifying and critically analysing the current state of Indian commercial banks’ profitability. More specifically, this study provides an evidence of the factors that may affect Indian banks’ profitability during a period ranging from 2008 to 2017. During this period, Indian commercial banks have witnessed several challenges such as a decline in financial performance, the demonetization process that was started in November 2016 and fraud cases that hit some Indian commercial banks. This made the investigation of this topic very important and interesting and provided empirical evidence for bankers and policymakers.

Regulators and policymakers are recommended to consider the macroeconomic determinants especially industry-specific factors in such a way that can enhance the profitability of the Indian commercial banks. Further, more focus is needed and required by bankers, bank managers, and other professionals on the bank-specific determinants for efficient utilizing of banks’ resources in such a way that they can influence significantly and positively the Indian commercial banks’ financial performance. Future research could examine this topic by including some other bank-specific and macroeconomic determinants. A comparison of banks’ profitability determinants—banks specific and macroeconomic—is also needed between private and public sectors banks.

Additional information

Funding

Notes on contributors

Eissa A. Al-Homaidi

Eissa A. Al-Homaidi is currently a Ph.D. scholar in the Commerce Department, Aligarh Muslim University, India. His research interests include financial reporting, financial performance, disclosure, corporate governance and demonetization.

Mosab I. Tabash

Mosab I. Tabash is currently working as an Assistant Professor of Finance at the College of Business, Al Ain University of Science and Technology, UAE. His research interests include Islamic banking, monetary policies, financial performance, and investments.

Najib H. S. Farhan

Najib H.S. Farhan is currently a Ph.D. scholar at Aligarh Muslim University, India. He professionally uses a number of statistical packages such as SPSS, Eviews, and Stata. He has a series of publications in national and international journals. His research interests include accounting and finance.

Faozi A. Almaqtari

Faozi A. Almaqtari is a Ph.D. scholar at Aligarh Muslim University, India. Mr. Faozi has awarded many prizes for his outstanding academic record during his graduate and postgraduate studies. His research interests include corporate governance and financial performance.

References

- Abel, S., & Roux, P. L. (2016). Determinants of banking sector profitability in Zimbabwe. International Journal of Economics and Financial Issues, 6(3), 845–854.

- Acaravci, S. K., & Çalim, A. E. (2013). Turkish banking sector’ s profitability factors. International Journal of Economics and Financial Issues, 3(1), 27–41.

- Ahamed, M. M. (2017). Asset quality, non-interest income, and bank profitability: Evidence from Indian banks. Economic Modelling, 63, 1–14.

- Almaqtari, F. A., Al‐Homaidi, E. A., Tabash, M. I., & Farhan, N. H. (2018). The determinants of profitability of Indian commercial banks : A panel data approach. International Journal of Finance & Economics, 1–18. doi:10.1002/ijfe.1655

- AL-Omar, H., & AL-Mutairi, A. (2008). Bank-specific determinants of profitability: The case of Kuwait. Journal of Economic and Administrative Sciences, 24(2), 20–34. doi:10.1108/10264116200800006

- Anbar, A., & Alper, D. (2011). Bank specific and macroeconomic determinants of commercial bank profitability: Empirical evidence from Turkey. Business and Economics Research Journal, 2(2), 139.

- Athanasoglou, P. P., Brissimis, S. N., & Delis, M. D. (2008). Bank-specific, industry-specific and macroeconomic determinants of bank profitability. International Financial Markets, Institutions & Money, 18, 121–136. doi:10.1016/j.intfin.2006.07.001

- Baltagi, B. H. (2005). Econometric analysis of panel data. New York, NY: Wiley.

- Bapat, D. (2017). Profitability drivers for Indian banks: A dynamic panel data analysis. Eurasian Business Review, 8(4), 437-451.

- Bose, S., Saha, A., Zaman, H., & Islam, S. (2017). Non-financial disclosure and market-based firm performance: The initiation of financial inclusion Sudipta. Journal of Contemporary Accounting & Economics, 13(3), 263–281. doi:10.1016/j.jcae.2017.09.006

- Bougatef, K. (2017). Determinants of bank profitability in Tunisia : Does corruption matter? Journal of Money Laundering Control, 20(1), 70–78. doi:10.1108/JMLC-10-2015-0044

- Bouzgarrou, H., Jouida, S., & Louhichi, W. (2017). Bank profitability during and before the financial crisis : Domestic vs. foreign banks. Research in International Business and Finance. doi:10.1016/j.ribaf.2017.05.011

- Brooks, C. (2014). Introductory econometrics for finance. Cambridge: Cambridge University Press.

- Chowdhury, M. A. F., & Rasid, M. E. S. M. (2017). Determinants of performance of Islamic banks in GCC countries: Dynamic GMM approach. Advances in Islamic Finance, Marketing, and Management, 49–80. doi:10.1108/978-1-78635-899-820161005

- de Mendonça, H. F., & da Silva, R. B. (2018). Effect of banking and macroeconomic variables on systemic risk: An application of ΔCOVAR for an emerging economy. North American Journal of Economics and Finance, 43, 141–157. doi:10.1016/j.najef.2017.10.011

- Dietrich, A., & Wanzenried, G. (2011). Determinants of bank profitability before and during the crisis: Evidence from Switzerland. Journal of International Financial Markets, Institutions & Money, 21(3), 307–327. doi:10.1016/j.intfin.2010.11.002

- Dietrich, A., & Wanzenried, G. (2014). The determinants of commercial banking profitability in low-, middle-, and high-income countries. In Quarterly review of economics and finance (Vol. 54, pp. 337–354). Board of Trustees of the University of Illinois. doi:10.1016/j.qref.2014.03.001

- Ebenezer, O. O., Omar, W. A. W. B., & Kamil, S. (2017). Bank specific and macroeconomic determinants of commercial bank profitability: Empirical evidence from Nigeria. International Journal of Finance & Banking Studies (2147–4486), 6(1), 25–38.

- Francis, M. E. (2013). Determinants of commercial bank profitability in Sub-Saharan Africa. International Journal of Economics and Finance, 5(9), 134–147. doi:10.5539/ijef.v5n9p134

- Garcia, M. T. M., & Guerreiro, J. P. S. M. (2016). Internal and external determinants of banks ’ profitability the Portuguese case. Journal of Economic Studies, 43(1), 90–107. doi:10.1108/JES-09-2014-0166

- Ghosh, S. (2016). Does productivity and ownership matter for growth? Evidence from Indian banks. International Journal of Emerging Markets, 11(4), 607–631.

- Growe, G., DeBruine, M., Lee, J. Y., & Maldonado, J. F. T. N. (2014). The profitability and performance measurement of U. S. regional banks using “fundamental analysis research.”. Advances in Management Accounting, 189–237. doi:10.1108/S1474-787120140000024006

- Gul, S., Irshad, F., & Zaman, K. (2011). Factors affecting bank profitability in Pakistan. The Romanian Economic Journal, 2(39), 61–87. Retrieved from http://www.rejournal.eu/sites/rejournal.versatech.ro/files/issues/2011-03-01/561/gul20et20al20-20je2039.pdf

- Hsiao, C. (2003). Analysis of panel data. Cambridge: Cambridge University Press.

- Issn, V. O. L. N. O., Ebenezer, O. O., Ahmad, W., & Bin, W. (2017). Finance & banking studies bank specific and macroeconomic determinants of commercial bank profitability: Empirical evidence from Nigeria. Journal of Finance & Banking Studies, 6(1), 25–38.

- Jara-Bertin, M., Moya, J. A., & Perales, A. R. (2014). Determinants of bank performance : Evidence for Latin America. Academia Revista Latinoamericana de Administración, 27(2), 164–182. doi:10.1108/ARLA-04-2013-0030

- Kapaya, S. M., & Raphael, G. (2016). Bank-specific, industry-specific and macroeconomic determinants of banks profitability: Empirical evidence from Tanzania. International Finance and Banking, 3(2), 100–119. doi:10.5296/ifb.v3i2

- Kyereboah‐Coleman, A. (2007). The impact of capital structure on the performance of micro finance institutions. The Journal of Risk Finance, 8(1), 56–71.

- Lemma, T. T., & Negash, M. (2013). Institutional, macroeconomic and firm-specific determinants of capital structure The African evidence. Management Research Review, 36(11), 1081–1122. doi:10.1108/MRR-09-2012-0201

- Levine, R., Loayza, N., & Beck, T. (2000). Financial intermediation and growth: Causality and causes. Journal of Monetary Economics, 46(1), 31-77.

- Loh, C. Z. (2017). Specific risk factors and macroeconomic factor on profitability performance an empirical evidence of Top Glove Corporation Bhd., MPRA Paper 78339, University Library of Munich, Germany.

- Louzis, D. P., Vouldis, A. T., & Metaxas, V. L. (2012). Macroeconomic and bank-specific determinants of non-performing loans in Greece : A comparative study of mortgage, business and consumer loan portfolios. Journal of Banking and Finance, 36(4), 1012–1027. doi:10.1016/j.jbankfin.2011.10.012

- Marijana, Ć., Poposki, K., & Pepur, S. (2012). Profitability determinants of the macedonian banking sector in changing environment. Procedia - Social and Behavioral Sciences, 44, 406–416. doi:10.1016/j.sbspro.2012.05.045

- Masood, O., & Ashraf, M. (2012). Bank‐specific and macroeconomic profitability determinants of Islamic banks. Qualitative Research in Financial Markets, 4(2/3), 255–268. doi:10.1108/17554171211252565

- Menicucci, E., & Paolucci, G. (2016). The determinants of bank profitability : Empirical evidence from European banking sector. Journal of Financial Reporting and Accounting, 14(1), 86–115. doi:10.1108/JFRA-05-2015-0060

- Naeem, M., Baloch, Q. B., & Khan, A. W. (2017). Factors affecting banks’ profitability in Pakistan. International Journal of Business Studies Review, 2(2), 33–49.

- Narwal, K. P., & Pathneja, S. (2016). Effect of bank-specific and governance- specific variables on the productivity and profitability of banks. International Journal of Productivity and Performance Management, 65(8), 1057–1074. doi:10.1108/IJPPM-09-2015-0130

- Ongore, V. O., & Kusa, G. B. (2013). Determinants of financial performance of commercial banks in Kenya. International Journal of Economics and Financial Issues, 3(1), 237–252. doi:10.15520/jbme.2015.vol3.iss11.158.pp33-40

- Pasiouras, F., & Kosmidou, K. (2007). Factors influencing the profitability of domestic and foreign commercial banks in the European Union. Research in International Business and Finance, 21, 222–237. doi:10.1016/j.ribaf.2006.03.007

- Perera, A., & Wickramanayake, J. (2016). Determinants of commercial bank retail interest rate adjustments: Evidence from a panel data model. Journal of International Financial Markets, Institutions & Money, 45, 1–20. doi:10.1016/j.intfin.2016.05.006

- Petria, N., Capraru, B., & Ihnatov, I. (2015). Determinants of banks ’ profitability : Evidence from EU 27 banking systems. Procedia Economics and Finance, 20(15), 518–524. doi:10.1016/S2212-5671(15)00104-5

- Ramlan, H., & Adnan, M. S. (2016). The profitability of Islamic and conventional bank: Case study in Malaysia. Procedia Economics and Finance, 35, 359–367. doi:10.1016/S2212-5671(16)00044-7

- Rani, D. M. S., & Zergaw, L. N. (2017). Bank specific, industry specific and macroeconomic determinants of bank profitability in Ethiopia. International Journal of Advanced Research in Management and Social Sciences, 6(3), 74–96.

- Rashid, A., & Jabeen, S. (2016). Analyzing performance determinants: Conventional versus Islamic banks in Pakistan. Borsa Istanbul Review, 16(2), 92–107. doi:10.1016/j.bir.2016.03.002

- Rao, N. V., Rezvanian, R., Nyadroh, E. (2009). Profitability of banks in India: An assessment. Alliance Journal of Business Research, pp. 68–90.

- Reddy, K. S. (2011). Determinants of commercial banks profitability in India: A dynamic panel data model approach. Pakistan Journal of Applied Economics, 21(1&2), 15–36.

- Rjoub, H., Civcir, I., & Resatoglu, N. G. (2017). Micro and macroeconomic determinants of stock prices: The case of Turkish banking sector. Romanian Journal of Economic Forecasting, 20(1), 150–166.

- Robin, I., Salim, R., & Bloch, H. (2018). Financial performance of commercial banks in the post-reform era: Further evidence from Bangladesh. Economic Analysis and Policy, 58, 43–54. doi:10.1016/j.eap.2018.01.001

- Roman, A., & Camelia, A. (2015). The impact of bank-specific factors on the commercial banks liquidity : Empirical evidence from CEE countries. Procedia Economics and Finance, 20(15), 571–579. doi:10.1016/S2212-5671(15)00110-0

- Roodman, D. (2006). How to do xtabond2: An introduction to difference and system GMM in Stata. Center for Global Development Working Paper (103). Available at http://dx.doi.org/10.2139/ssrn.982943

- Saif, A. Y. H. (2014). Financial performance of the commercial banks in the Kingdom of Saudi Arabia: An empirical insight. Masters thesis, Universiti Utara Malaysia. Avaliable at http://etd.uum.edu.my/4587/

- Salike, N., & Ao, B. (2017). Determinants of bank ’ s profitability : Role of poor asset quality in Asia. China Finance Review International. doi:10.1108/CFRI-10-2016-0118

- Saona, P. (2016). Intra- and extra-bank determinants of Latin American Banks ’ profitability. International Review of Economics and Finance, 45, 197–214. doi:10.1016/j.iref.2016.06.004

- Sarkar, J., Sarkar, S., & Bhaumik, S. K. (1998). Does ownership always matter ?— Evidence from the. Journal of Comparative Economics, 281, 262–281. doi:10.1006/jcec.1998.1516

- Singh, A., & Sharma, A. K. (2016). An empirical analysis of macroeconomic and bank-specific factors affecting liquidity of Indian banks. Future Business Journal, 2(1), 40–53. doi:10.1016/j.fbj.2016.01.001

- Shrivastava, R., Sahu, R. K., & Siddiqui, I. N. (2018). Indian rural market: Opportunities and challenges. In proceedings of national conference of innovative solutions for rural developmentof Chhattisgarh, 23-24 Feb, India. Published by International Journal of Advance Research, Ideas and Innovationsin Technology, accessed by. https://www.ijariit.com/conferences/ncisrdc-2018/

- Singh, S., Sidhu, J., Joshi, M., & Kansal, M. (2016). Measuring intellectual capital performance of Indian banks: A public and private sector comparison. Managerial Finance, 42(7), 635-655.

- Tabash M.I.. (2016). An empirical investigation between liquidity and key financial ratios of Islamic banks of United Arab Emirates (UAE) Business and Economic Horizons143 713-724 doi:10.15208/beh

- Tabash, M. I., & Dhankar, R. (2014). The flow of Islamic finance and economic growth: An empirical evidence of Middle East. Journal of Finance and Accounting, 2(1), 11–19. doi:10.11648/j.jfa.20140201.12

- Tan, Y. (2016). The impacts of risk and competition on bank profitability in China. Journal of International Financial Markets, Institutions & Money, 40, 85–110. doi:10.1016/j.intfin.2015.09.003

- Tan, Y., & Floros, C. (2015). Bank profitability and inflation : The case of China. Journal of Economic Studies, 39(6), 675–696. doi:10.1108/01443581211274610

- Tarus, D. K., Chekol, B., & Mutwol, M. (2012). Determinants of net interest margins of commercial banks in Kenya: A panel study. Procedia Economics and Finance, 2, 199–208. doi:10.1016/S2212-5671(12)00080-9

- Tiberiu, C. (2015). Banks ’ profitability and financial soundness indicators : A macro-level investigation in emerging countries. Procedia Economics and Finance, 23, 203–209. doi:10.1016/S2212-5671(15)00551-1

- Viswanathan, P. K., Ranganatham, M., & Balasubramanian, G. (2014). Modeling asset allocation and liability composition for Indian banks. Managerial Finance, 40(7), 700–723.

- Yahya, A. T., Akhtar, A., & Tabash, M. I. (2017). The impact of political instability, macroeconomic and bank-specific factors on the profitability of Islamic banks: An empirical evidence. Investment Management and Financial Innovations, 14(4), 30–39. doi:10.21511/imfi.14(4).2017.04

- Yeon, J., & Kim, D. (2013). Bank performance and its determinants in Korea. Japan & The World Economy, 27, 83–94. doi:10.1016/j.japwor.2013.05.001

- Zampara, K., Giannopoulos, M., & Koufopoulos, D. N. (2017). Macroeconomic and industry-specific determinants of Greek bank profitability. International Journal of Business and Economic Sciences Applied Research, 10(1), 13–22. doi:10.25103/ijbesar

- Zouari-Ghorbel, S. (2014). Macroeconomic and bank-specific determinants of household’ s non-performing loans in Tunisia : A dynamic panel data. Procedia Economics and Finance, 13, 58–68. doi:10.1016/S2212-5671(14)00430-4