?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Entrepreneurial firms in their early stages cannot finance their own capital sufficiently; hence, external investment is crucial for their survival. Angels, venture capital, and governmental support have played key roles in entrepreneurial financing. Accelerators, a new type of early-stage investor, have been rapidly growing in recent years, and have attracted strong attention. They provide financial support to entrepreneurial firms in their early stages along with mentorship, education, and networking services. However, the advantages of accelerators over existing funding avenues have yet to be proven. Therefore, this study analyzes the behavior and performance of accelerators, angels, and venture capital. We used 30,523 investment data regarding accelerators, angels, and venture capital from the CrunchBase database. By conducting multiple regression and survival analyses, we found that the performance of accelerators differs from that of venture capital, but is similar to that of angels. While accelerators’ investees perform well post funding, venture capitals’ investees perform well in terms of survivability. This study empirically verifies accelerator-related qualitative research. Additionally, we believe our results will contribute to future accelerator-related research and policy.

PUBLIC INTEREST STATEMENT

Nascent entrepreneurial firms often face difficulties with funding due to high level of uncertainties and information asymmetries. Angels and early stage venture capitals are traditional investors for those firms, while public grant or guarantee also play important parts in financing entrepreneurial firms.

The accelerator, a relative new type of investors, are thought to be different from angel investor or early stage venture capital because it emphasizes non-financial support such as mentorship, education, and networking, enabling companies to grow faster. The study tries to empirically test whether it is different from other type of investors. The results of this study illustrates that the accelerator is different from the venture capital but not very different from the angel investor. The study implies that the activities of accelerators may be in the process of development and may find raison d’etre in the near future.

1. Introduction

Entrepreneurial firms, which can commercialize new ideas, perform a major role in enhancing national competitiveness (Bygrave & Zacharakis, Citation2014). However, most entrepreneurial firms are faced with a shortage of internal funds and external financing, which significantly affects their survivability (Shrader & Simon, Citation1997). Since entrepreneurial firms are typically high-risk and high-return investments, investors tend to be prudent when selecting a target firm (Drover et al., Citation2017; Fried & Hisrich, Citation1994; Tyebjee & Bruno, Citation1984). This suggests that entrepreneurial firms may face many difficulties in securing external financing when they do not have enough working capital.

For this reason, although investments (angels and venture capitals (VCs)) and various governmental supports are available, the investment and support available to these firms in their early stages are still insufficient. Due to this shortage, accelerators are gaining more attention as a brand-new funding type for entrepreneurial firms.

Unlike previous investor types, accelerators provide not only financial support but mentorship, education, and networking services also to support firms’ growth. However, the performance of the accelerator program compared with that of previous investor types is still debatable. With the emergence of business angels, angel co-funding, and micro-VC, the role of traditional investors has broadened (Geibel & Yang, Citation2018; Mayer, Schoors, & Yafeh, Citation2005; Samir, Citation2014). It is now common for other types of investors to provide non-financial support for their investees Thus, researchers raise the question of whether accelerators are really a new investor type or not.

The main reason for this argument is the lack of empirical studies regarding accelerators, as not enough data is available. Few empirical studies have been conducted (Hallen, Bingham, & Cohen, Citation2014); however, these only consider star accelerators like “Y-Combinator,” “Techstars,” and “500 startups.” Therefore, with insufficient information, it is difficult to understand what accelerators really are.

Many countries think that there are weaknesses in their entrepreneurial ecosystems, although the substance of the accelerator is not clearly verified. Many of these countries have interest in the new type of accelerator. They have supported in several ways in order to benchmark the success story of star accelerators. These efforts, however, are likely to be inefficient without a proof that the accelerator is not an effective type of investment, and consequently concomitant measures are unnecessary. On the other hand, even in the opposite case, if we can clearly define the type of accelerator, then we will be able to use them more efficiently in the entrepreneurial ecosystem.

In this study, using the Crunchbase DB data, the behaviors and performances of accelerators, angels, and VCs are analyzed. It is an extensive empirical study including all existing investment deals trackable, especially focusing on the behaviors and performances of accelerators The result illustrate interesting features of accelerators. They seem different, but not different enough from angel investors in terms of performances of investees. These results will help researchers gain more interest in the differentiation of the accelerator and angel. It also makes us wonder if we should differentiate between the accelerator and angel in policy. It calls for further research for the accelerators “phenomena” spreads globally with the high level of expectation by both governments and academia. Because it is an initial empirical study of the accelerator, which means that all roles of accelerator was not included. The use of CrunchBase DB is another very important contribution of the study, which opens ample venue for empirical research in entrepreneurial finance.

2. Literature review

2.1. Accelerator-related extant studies

Systems that provide mentorship, education, and networking services to entrepreneurial firms in their early stages emerged in the mid-2000s, starting in Silicon Valley, USA; accelerators came into focus when Y-Combinator was established in 2005. An accelerator is a unique investor type, different from existing investments such as VCs, angels, and incubators, and they provide both financial and non-financial support (Cohen & Hochberg, Citation2014).

Accelerators provide contextual support, such as mentorship, education, consulting, and human network services, for entrepreneurial firms in their beginning stages to allow them to achieve rapid growth within a short period (Bliemel et al., Citation2016; Levinsohn, Citation2014; Miller & Bound, Citation2011).

Recently, accelerator programs have been rapidly growing the United States and Europe (Kim & Yum, Citation2014; Miller & Bound, Citation2011). However, whether accelerators are a new investor type or not is still controversial among researchers and in the market.

Cohen (Citation2013) stated that an accelerator is a different type of investment institution, which provides more contextual support rather than financial investment, compared to angels and incubators. Moreover, its target firms are mostly entrepreneurial firms in their early development stages, which are risky firms, and are not of particular interest to existing investors (Hallen et al., Citation2014). Additionally, accelerators prefer to invest when VCs believe that profitability is low (Miller & Bound, Citation2011). Choi and Kim (Citation2016) stated that accelerators increase the survival probability of entrepreneurial firms and provide higher and faster returns on investment compared to VCs. Other studies state that due to the differing perspectives in the market regarding accelerators and other investors, accelerators play an important role in constructing effective venture ecosystems. However, some studies state that additional verification is necessary regarding accelerators. It is difficult to test the effectiveness of accelerators empirically, since the measurement of their performance is limited due to their short history (Kang, Citation2014).

2.2. Angel-related extant studies

An angel is a representative investor type during the early stages of an entrepreneurial firm. In the 1920s, investors who anonymously invested in Broadway operas were called angels. They invested in operas that were of good quality but lacked funding.

Rosenbusch, Brinckmann, and Müller (Citation2013) state that most angels are former entrepreneurs or managers, who are investing their acquired wealth back into society. Therefore, angels are primarily concerned with the growth of the funded firms, unlike other investors that expect high returns.

Angel investments are mainly focused on early-stage firms and prefer to participate directly in their management after providing financial support. They use their knowledge, skills, and experience to help the funded firms survive and grow (Mason & Harrison, Citation2008).

Although investments and management environments vary widely from country to country, typical angel investors are similar. According to Ramadani (Citation2009), angels in each country have similar characteristics. Most angels are men with managerial experience and knowledge, aged between 40 and 65 years old (Hill & Power, Citation2002). Additionally, angels prefer investing in areas near (typically 50–100 miles) their location (Reitan & Sorheim, Citation2000).

Apart from their financial role, angels often participate in management in various ways, and this support helps funded firms to develop further (Ardichvili, Cardozo, Tune, & Reinach, Citation2002; Politis, Citation2008; Sørheim, Citation2005).

Angels frequently pursue non-financial goals rather than financial returns. Data gathering and analysis regarding angels were difficult because many of their private investments were included as well. Therefore, despite the many perspectives regarding angels, there is no doubt that they are interested in the early-stage entrepreneurial firms.

2.3. Venture capital-related extant studies

According to Kenney (Citation2000), VCs invest mostly in entrepreneurial firms that have high potential and technology, but suffer from a lack of financing in the early stages, and generate profit by selling shares or initial public offerings.

Investing in private companies, supporting entrepreneurial firms with knowledge accumulated from various investment experiences, and attracting external financing were the typical types of VCs in the US in the mid-1980s. However, newer types of VCs have been introduced to reflect changes in markets and the characteristics of international markets. Moreover, the role of VCs has been expanded since then. Reflecting these trends, several studies have been conducted regarding the investment behaviors of VCs.

According to Gupta and Sapienza (Citation1992), VCs that are highly experienced in a specific industry tend to invest in entrepreneurial firms in their early stages. Ko and Lee (Citation2016), Lim and Kim (Citation2015), and Mayer et al. (Citation2005) also state that investment timing and strategies differ depending on the source of VC. Moreover, Norton and Tenenbaum (Citation1993) asserted that VCs tend to concentrate their investment in firms during their early stages in a specific industry, instead of investing in a variety of firms in different developmental stages or different industries to diversify their high investment risk.

However, young VCs prefer to invest in relatively mature firms (Gompers, Citation1996). This is because young VCs want to go public, or be listed as soon as possible by gaining a market reputation for investing in such firms. Thus, young VCs might prefer to invest in relatively mature firms, which have already met the requirements to go public and whose implicit risk is lesser than younger firms that do not have adequate knowledge and business experience.

Thus, many studies provide different views toward the preferred timing of VC investment. From a traditional perspective, however, VCs mostly invest later than the other investors.

Recently, a new type of VC has emerged called “Micro-VC”. According to Samir (Citation2014), micro-VC bridges the gap between existing angels and VCs. Unlike VC, micro-VC makes investments on a small scale and increases its contextual support for targeted firms, similar to accelerators, to avoid high investment risk. The emergence of micro-VC makes the definition of VC ambiguous.

3. Research model and hypotheses

Based on the previous studies mentioned above, this study examines whether accelerators, angels, and VCs differ from each other in reality.

Studies regarding investment by angels place importance on entrepreneurial factors. Haar, Starr, and MacMillan (Citation1989) studied American angels and considered honesty, credibility, and passion of the entrepreneur and their start-up team as the most important decision-making factors.

Angels normally conduct less due diligence before investing than VCs, and tend to rely on their instincts or intuition (Mason & Harrison, Citation1996). Further, angels usually consider a company’s location, their reputation, and whether there are any joint investors, before investing (Haines, Madill, & Riding, Citation2003; Sudek, Citation2006).

Angels are difficult to analyze and define as objects of study, since they prefer to invest in related companies like those belonging to their relatives (Mason & Harrison, Citation2008). Thus, most studies regarding investor type were conducted considering VCs rather than angels (Elitzur & Gavious, Citation2003).

Gupta and Sapienza (Citation1992) claimed that the size of the investment institution affects investment behavior. Moreover, large VC firms easily select their target companies and tend to invest in different types of entrepreneurial firms in diverse industries and locations, since they can support the firm to ensure they make profits after investment.

In contrast, Sorenson and Stuart (Citation2001) found that VCs were reluctant to invest in other countries or distant firms and considered the investor and funded firm’s geographical position, industrial differences, post-investment care, differences in policies and laws before investing. However, Cuervo-Cazurra and Dau (Citation2009) and Khoury, Junkunc, and Mingo (Citation2015) state that market policy is more important than geographical position, which does not have a major influence on investment behavior since geographical risk can be measured.

Moreover, according to Norton and Tenenbaum (Citation1993), if a VC has sufficient experience in a specific sector and is able to absorb the risk, or even reduce the risk of entrepreneurial firms in the early development stages, then it prefers to invest in high gain investments and makes repetitive investments during its investment period.

Although there have been much research on behaviors of each type of investors—angels and VCs, (Nelson & Sidney, Citation2005; Shin, Mendoza, Hawkins, & Choi, Citation2017; Stinchcombe, Citation2000), comparative studies on the investment behaviors due to investor types have not much been performed. It becomes more interesting and complex question recently, for many new types of entrepreneurial investors emerge—angel syndicate, micro-VCs, and accelerators. (Cohen, Citation2014; Cohen & Hochberg, Citation2014; Samir, Citation2014). We therefore try to test whether the conventional categorization of investors accord with the behavioral differences.

H1: Investment behaviors differ depending on investor type.

H1-1: Funded firm’s age differs depending on investor type.

H1-2: Funded firm’s previous funding amount differs depending on investor type.

H1-3: Present funding amount toward the funded firm differs depending on investor type.

For hypothesis 1, the objective is to examine if the accelerator is a new type of investor with a unique investment behavior. The next objective is to test whether the different investment behaviors (if exist) lead to different investment performances. Investment performance can be analyzed from the perspective of the funded firm, i.e., the investee.

There are ongoing arguments about how an entrepreneurial firm’s performance should be measured, and changes in financial statements is not an inadequate measure since funded firms take time in all stages to realize their ideas and to complete development. Accelerators, especially, have to substitute established performance indicators since they have different investment behaviors and provide additional support to funded firms.

Additionally, previous studies measure the performance of accelerators based on scale of investment, employment creation, current operating status, and return on investment of funded firms (Mejia & Gopal, Citation2015). However, performance measurements used in the previous studies do not consider the effect of an industry on a firm’s performance (Tyebjee & Bruno, Citation1984).

Shane (Citation2009) found that there were no big differences in funded firms’ survivability between an economic boom and depression by comparing seven American companies’ survival rates in the 1980s and 1990s. This shows that an entrepreneurial firm’s survivability is steady regardless of time or economic trends.

Survival is a sufficient goal for entrepreneurial firms to be competitive and grow dramatically due to uncertainty (Lim et al., Citation2008). From the perspective of firm dynamics, a firm’s survivability is the result of the composite activity performed in the firm (Lee, Citation1998). Therefore, this study does not consider general investment performance, but rather, post-investment performance, which is the result of external investment and value addition activities, and survivability.

So we set the followed hypothesis to test the performance of funded firms.

H2: Funded firms’ performances differ depending on investment behaviors.

H2-1: Post funding timing differs due to the funded firm’s age.

H2-2: Post funding timing differs due to the previous funding amount of the funded firm.

H2-3: Post funding timing differs due to the present funding amount of the funded firm.

In general, external investment in a firm can be expected to be profitable the higher the risk it takes. However, according to Shane and Venkataraman (Citation2000), uncertainties due to the information asymmetry or market imbalances may vary depending on the level of investor’s capacity. The early investors have the experience or knowledge to determine a firm’s success in advance or have capabilities to increase the company’s chances of success (Choi & Kim, Citation2016; Chun & Ha, Citation2016; Gompers, Citation1996; Gupta & Sapienza, Citation1992, Hur, Yoon, & Lee, Citation2002). Therefore, even if the same investment is made, different outcomes may be achieved depending on the capabilities of the investor.

In particular, the accelerator says that the contextual support capability is excellent and that it can reduce the risk of firms (Birdsall, Jones, Lee, Somerset, & Takaki, Citation2013; Cohen, Citation2013; Cohen & Hochberg, Citation2014; Kim & Yum, Citation2014). Therefore, it is expected to show high performance regardless of differences in investment behaviors if the accelerator’s contextual support is excellent as they say.

In this study, the following assumptions were based on the prior study that there would be differences in the performance of firms depending on the capabilities of the investor type.

H3: Funded firms’ performances differ based on investor type.

H3-1: Post funding timing differs based on investor type.

H3-2: Funded firm’s survivability differs based on investor type.

The overall research model is shown in Figure .

Figure 1. Research model.

4. Methodology

4.1. Empirical model

In this study, multiple regression and survival analyses are used for hypothesis verification.

For the analysis of hypothesis 1, dummy variables with the accelerator as 0 were used for the multiple regression analysis, with the model as follows:

where: IB is the investment behavior, ac for the accelerator. Investment behavior was measured by hypothesis as funded firm’s age, previous funding amount, and present funding amount. IT is a dummy variable that represents the type of investor, an for the angel, and vc for the VC. This model refers to the investment behavior of the accelerator when the two independent variables are not affected. Through this model, we can check when the accelerator will be investing. It is also possible to compare investment behavior among investor types according to the value of each variable.

The model for hypothesis 2 as follows:

where: PT is the post funding timing, FA for funded firm’s age, PVA for previous funding amount, PSA for present funding amount. This model helps to review how differences in investment behavior identified in hypothesis 1 affect the performance of post funding timing by the funded firms. It is possible to verify how the current status of funded firms that the age, previous funding amount, and present funding amount affect the post funding timing.

In hypothesis 3, as in hypothesis 1, multiple regression analyses using dummy variables were used, and further survival analysis was used.

The model for hypothesis 3–1 as follows:

where: Variables used in this model were previously described. What we see in this model is whether there is a difference in the post funding timing, one of the performances of the funded firm’s, depending on the type of investor. It is also possible to review whether the performance of the angel and VC are high or low compared to the accelerator.

The cox regression models for hypothesis 3–2 used in survival analysis are as follows:

where: Hi(t) means the probability of a hazard at observation time t for a case with an independent variable, and H0(t) is the baseline hazard rate at observation time t if it has not independent variable. Meanwhile, exp refers to the hazard ratio of independent variables, AC for the accelerator and VC for the VC. This independent variable represents the relative hazard rate to the closing of the funded firms when investing in each type of investor and the baseline hazard rate is based on the hazard rate of the angel. Hazard rates allow us to determine how each type of investor affects the survivability.

4.2. Measurement

This study analyzes the types of accelerators, angels, and VCs based on the Crunchbase DB,Footnote1 which provides a profile of investment firms, funded firms, and investment-related information. The database may not be credible since it updates firms’ information in a way similar to Wikipedia. However, this database has already been used in various related studies (Arora & Nandkumar, Citation2012), and has been verified frequently in the past (Alexy, Block, Sandner, & Ter Wal, Citation2012; Block & Sandner, Citation2009).

CrunchBase provides researchers with investment-related data free of charge. This study obtained accelerator, angel, and VC investment information by Crunchbase DB.

This study adopts CrunchBaseDB’s definition of investor’s type.

The variables that make up investment behavior were measured in the following way. The funded firm’s age is the date between the establishment and the investment. The previous funding amount means any type of fund that the funded firm previously invested in. The present funding amount is an investment to be observed in this study. All amounts are in US dollars.

Performance was measured by post funding timing and survivability after investment, the post funding timing is the date between the present funding and the subsequent investment, and the survivability is the date between the present investment and the business closure date.

4.3. Data and sample characteristics

Based on previous studies that investigated the differences between the investment strategies and behaviors of entrepreneurial firms after the 2008 financial crisis and their performance (Choi & Kim, Citation2016), we collected data from January 2009 to December 2015 from Crunchbase DB.

The total investment data collected was 30,523 items, including 6,831 accelerator investments, 5,412 angel investments, and 18,280 VC investments.

Pearce (Citation2014) provides 17 industry sectors that VCs favor; this study follows Pearce’s (Citation2014) industry classification rule to classify industries in the Crunchbase DB. The countries were reclassified and divided into the following 7 groups based on the frequency of investment: United States of America, Canada, Germany, the United Kingdom, Israel, China, and the low-frequency countries group.

According to previous studies, the characteristics of the industry or the level of competition may affect the performance of firms (Barron, West, & Hannan, Citation1994; Short, Ketchen, Palmer, & Hult, Citation2007). In addition to differences in the country’s policies and laws affect investment-related activities (Sorenson & Stuart, Citation2001).

Therefore, in this study, we controlled industry sector, country, and additional information that are funded firm’s endowed resource (total number of investors in the past) and investor’s experience(total number of investment in the past). In addition, we controlled the average amount invested to control the size of funded firms and investors.

5. Results

Accelerators, angels, and VCs showed different behaviors when selecting the funded firm. Descriptive statistics are illustrated as follows.

The sample includes 30,523 total investment records. Funded firms got financed by investors, average 1,097.26 days after its foundation. In addition, average duration from firm foundation to first investment deal is 679.95 days. Meanwhile, the present investment took 469.87 days on average after the most recent investment, and the post investment was confirmed after 403.06 days. The funded firms received an average of 2,844,644 dollars. Investors had an average fund of 7,995,400 dollars. On average, funded firms that invested from the angel were found that they had attracted investment of 7,461,467 dollars from 5.73 investors (Table ).

Table 1. Descriptive statistics: total

Total 6,831 investment records of the accelerator show that funded firms got financed by accelerators, average 535.74 days after foundation, and the first investment was made after 403.73 days from its establishment. In addition, the present investment was made after 301.92 days on average since its last investment, and the post investment was confirmed after 306.00 days. The funded firms received an average of 375,993 dollars. Accelerators had an average fund of 579,577 dollars. On average, funded firms that invested from the accelerator were found that they already received investments of 243,612 dollars from 3.27 investors. Funded firms that received the investment of the accelerator through descriptive statistics were found to be relatively nascent firms compared to the overall average, and smaller funding amounts were frequently made. The accelerators are also likely to push ahead with relatively small size funds for nascent entrepreneurial firms (Table ).

Table 2. Descriptive statistics: investment of accelerators

Total 5,412 investment records of the angel show that funded firms got financed by angels, average 596.89 days after its foundation, and average duration from firm foundation to first investment deal is 467.56 days. In addition, the present investment took 335.47 days on average after the most recent investment, and the post investment was confirmed after 387.40 days. The funded firms received an average of 1,529,508 dollars. Angels had an average fund of 3,015,850 dollars. On average, funded firms that invested from the angel were found that they had attracted investment of 287,724 dollars from 3.15 investors. Angel’s investment is likely to be made at a larger amount and later timing than those of the accelerator. However, although the amount of previous funding by entrepreneurial firms was more likely to be invested by the angel, the average number of investors was less (Table ).

Table 3. Descriptive statistics: investment of angels

Total 18,280 investment records of the VC show that funded firms got financed by VCs, average 1,433.39 days after its foundation, and the first investment was made after 835.56 days from its establishment. In addition, the present investment was made after 522.55 days on average since its last investment, and the post investment was confirmed after 439.17 days. It was longer than that of accelerator or angel. The funded firms received an average of 4,053,297 dollars. VCs had an average fund of 12,154,932 dollars. On average, funded firms that invested from the VC were found that they already received investments of 12,301,174 dollars from 6.60 investors. A review of the average value of descriptive statistics confirms that VC invests in the entrepreneurial firms with relatively proven histories, compared to the other two types of investors (Table ).

Table 4. Descriptive statistics: venture capital investments

5.1. Investment behavior regarding investor type

We conducted multiple regression analysis to test whether investment behaviors depend on investor type.

The regression equation is significant (F = 175.932, p = 0.000) and the explanation is 12.9%. No meaningful difference was found between accelerators and angels when their different behaviors were compared to the funded firms’ age (p = 0.633), however, it was found that VCs usually invested in firms 777.58 days (p = 0.000) after their establishment (Table ).

Table 5. Results of multiple regression analysis of firms’ age (days) depending on investor type

The estimated model based on the analysis results as follows:

There is no statistically significant difference in funded firm’s age invested by the accelerator and angel through the model. VC is found to be investing more than 778 days later.

Likewise, previous funding amount (F = 10.115, p = 0.000) and present funding amount (F = 43.135, p = 0.000) is significant, although the explanation is slightly lower at 1.8% and 4.1%, respectively. At the time of investment, no differences were found in previous funding amount (p = 0.432) or present funding amount (p = 0.346) between accelerators and angels. However, like the case of the funded firms’ age, there was a clear difference for VCs, a difference of 14,887,343.03 dollars in previous funding amount (p = 0.000), and 14,887,343.03 dollars in present funding amount (p = 0.000) were found (Tables and ).

Table 6. Results of multiple regression analysis of previous funding amount depending on investor type

Table 7. Results of multiple regression analysis of present funding amount depending on investor type

The estimated models based on the analysis results as follows:

From the analysis, we could not find any differences between accelerators and angels, but accelerators invest lower amounts in young firms than VCs.

Therefore, these results partially support Hypothesis 1.

5.2. Funded firms’ performances depending on investment behaviors

Multiple regression analysis of investment behavior and post funding timing showed that post funding timing increased proportionately with the funded firms’ age (p = 0.000). Moreover, as the previous funding amount increases, the post funding timing becomes shorter (p = 0.008), and this could be because the previous funding amount might have created a halo effect for post funding. However, the present funding amount did not show any meaningful relationship with post funding (p = 0.401). The regression equation is significant (F = 10.985, p = 0.000) and the explanation is 4.6% (Table ).

Table 8. Results of multiple regression analysis of funded firms’ performances depending on investment behavior

The estimated model based on the analysis results as follows:

Therefore, hypotheses 2–1 and 2–2 were supported, but Hypothesis 2–3 was rejected.

5.3. Funded firms’ performances depending on investor type

The results of the multiple regression analysis that is in the middle of investor type and post funding timing, The regression equation is significant (F = 10.985, p = 0.000) and the explanation is 4.6%. It is shown that angels (p = 0.000) and VCs (p = 0.000) had longer post funding timings than accelerators (Table ).

Table 9. Results of multiple regression analysis in post funding timing (days) depending on investor type

The estimated model based on the analysis results as follows:

Therefore, Hypothesis 3–1 is strongly supported.

To analyze survivability as a performance measure, this study conducted a survival analysis that utilized the Cox proportional hazards model.

Survival analysis is mainly used in medical statistics, but is useful in the study of early-stage firms whose investment performance cannot be determined by estimating financial performance. Additionally, survival analysis considers the effects of censored data (like mergers and acquisitions (M&A) or neglected observations). Moreover, unlike the analysis of financial performance, which can be affected by external factors such as industry or policy, survival analysis is appropriate for entrepreneurial firm performance research as the continuous effect can be analyzed.

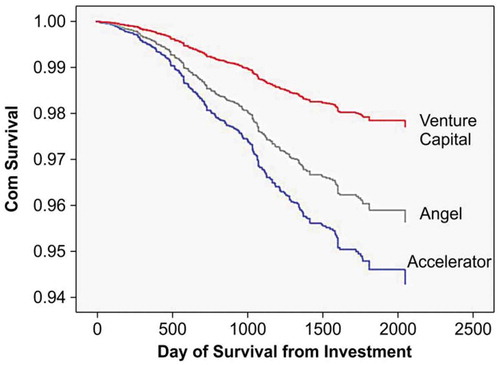

We calculated the survival and hazard functions at the mean of covariates to determine whether there is difference in funded firms’ survivability based on investor type. The results differ from that of the multiple regression analysis, where we analyzed survivability as a performance variable. In multiple regression analysis, accelerators indicated the fastest post funding, followed by angels and VCs, in that order; however, in survival analysis, accelerators showed the lowest survivability, while VC showed the highest.

Chi-square is 158.643, the significance level is .000, and the analytical model is deemed suitable. B is the regression coefficient for each independent variable, Ward is the square of the regression coefficient divided by the standard error, and the larger the value of Ward, the smaller the significance probability. Compared to the investment by the angel, the hazard rate increased by 0.32h0(t) when it comes to the accelerator and decreased by 0.48h0(t) with VC. This relationship can also be verified by having a hazard ratio greater or less than 1 (Table ).

Table 10. Results of survival analysis

The estimated model based on the analysis results as follows:

Based on the results, it can be stated that faster post funding does not guarantee a funded firm’s long-term survivability. This is contrary to Hypothesis 3–1; meanwhile, Hypothesis 3–2 was supported by the survival analysis.

Each investor type showed different survivability in the following order: VCs, angels, and accelerators were recorded at 99.5%, 98.5%, and 98.0% respectively, after three years, and 98.0%, 96.0%, and 94.5% after seven years of investment (Figure ).

Figure 2. Survivability.

Thus, the behavior of accelerators is different from that of VCs but is similar to that of angels. Moreover, post funding timing was shorter when the funded firm’s age was short and previous funding amount was bigger. However, additional research is required regarding funded firm’s performance, due to the opposing results of post funding timing and survivability (Table ).

Table 11. Hypothesis test results

6. Conclusion

6.1. Summary of research results

With a rapid change of a market, the entrepreneurial firms have been in the middle of great attention because they can commercialize various ideas and create added value.

Since most of the firms in the early stage generally cannot finance their capital sufficiently all by themselves, investments from external investors are the key factor for their survival and growth. Owing to the high level of uncertainty, however, it is difficult to attract the external investors. (Gregory, Rutherford, Oswald, & Gardiner, Citation2005).

There are various kinds of systems for entrepreneurial firms like angels, VCs, and governmental supports. Nevertheless, Entrepreneurial firms are still facing the financial problem. Due to this shortage, accelerators are getting more attention as a brand-new investor type for entrepreneurial firms (Cohen & Hochberg, Citation2014). Unlikely to prior investors, accelerators not only support financially but also provide mentorship, education, and networking services in order to support firm’s growth (Cohen, Citation2013; Kim & Yum, Citation2014).

It is, however, still controversial among researchers. The main reason for this argument is the lack of empirical studies regarding accelerators, as not enough data is available (Mayer et al., Citation2005; Samir, Citation2014). Accelerator’s existing investment characteristic and performance are based on their own opinion or some limited investigation of well-known accelerators.

This study analyzes empirically based on CrunchBase DB, which collects and provides investment information related to entrepreneurial firms. We have verified that the characteristics and performance of the accelerator are distinct from the prior investors. The results obtained from the empirical study are as follows.

The accelerator invests when the entrepreneurial firm is young than the VC invest. In general, the accelerator will invest in entrepreneurial firms with smaller accumulated investments compared to VC. We were able to see that the current amount of investment by the accelerator was also less than that of VC. However, there was no such difference with Angel. Therefore, we have found that the accelerator has a different investment behavior than VC. On the other hand, we have concluded that it is similar to Angel.

This investment behavior has been shown to affect post funding timing. Post funds have been delayed as the age of entrepreneurial firms increases, and the more previous fund amount, the faster they can attract. This means that as the age of firm grows, the interval increases between invests. It, meanwhile, can be interpreted that previous investment history sends a signal that it is a good business entrepreneurial firm.

The accelerator attracted fast post investments compared to other types of investors and VC was found to be the slowest. While the accelerator selects entrepreneurial firms with less investment history in the past than VC, post investment has attracted more quickly. This is a possible outcome, considering that the last stage of their program is demo day.

However, another performance variable, the survival rate, showed the worst result of the accelerator’s investment, in contrast to the results in the post funding timing.

6.2. Implications

Existing studies regarding accelerators were mostly limited to a few institutions or were only pilot studies; this study, however, examines whether accelerators, angels, and VCs are different investor types, and whether there are differences between them in investment performance by using Crunchbase DB.

The following results were obtained by using both multiple regression analysis and the Cox proportional hazards model:

There are differences between accelerators and VCs’ investment behavior. Accelerators, mainly invest in entrepreneurial firms earlier than VCs do. However, accelerators share similar investment behaviors with angels. This result confirms the assertion made in previous research that accelerators are a new type of investor, and that they invest in relatively early-stage firms. On the other hand, no differences were found between accelerators and angels.

Moreover, we identified that the funded firm’s shorter age and bigger previous funding amount tend to result in shorter post funding timing. This seems to reflect the trend that exceptional young firms obtain small-scale investments more often. This result may be influenced by survival bias. Firms that receive external investment would generally be better and last longer. However, the firms that did not receive external funding closed shortly, having little influence on the total data.

The bigger the previous funding amount, the shorter the post funding timing, which may be attributed to a halo effect; however, we need to confirm that the present funding amount did not affect post funding.

Accelerators, known for their relatively systematic additional support, showed the shortest post funding timing among the investors. Post funding timing was short for angels (pursue funded firm’s growth) and VCs (pursue funded firm’s initial public offering (IPO)). This relationship is opposite in survivability, and is caused by the difference in strategies depending on the investor type. Accelerators focus more on an idea’s commercialization in the early stages and help firms graduate to the post funding stage called “Demo Day”, rather than focus on long survivability. Consequently, accelerators make funded firms reach the post funding stage faster, but do not affect their survival or growth after market entry. In contrast, VCs maintain a relatively long investment period, and prefer exit-methods that might provide high profits like an IPO.

The results suggest a few implications. First, many previous studies have failed to capture the behaviors of accelerators mainly due to the difficulty of data collection (Dempwolf, Auer, & D’Ippolito, Citation2014). However, the study adopts CrunchBase DB and successfully finds the difference of accelerators and other types of investors in terms of investment behaviors.

Second, the results of the study calls of scrutiny to the booming accelerators. Since the accelerators are believed to be most critical in entrepreneurial ecosystem, the number of them has grown rapidly and been supported by many governments around the globe (Cohen & Hochberg, Citation2014; Kim & Yum, Citation2014). However, the result of the study shows the survival rate is the lowest in the case of the firms invested by the accelerator. More fine grain research is a must for justification of public support for accelerators.

Finally, the results of this study will contribute to a better idea about the accelerator. The evidence that the accelerator differs from the Angel will be used as a basis for future research and new policies. However, there may be research that refute these results and discover other meanings of the accelerator. We welcome this as well. Because it is all a way to help the accelerator efficiently, also be a way to improve the entrepreneurial ecosystem.

It does not mean, however, an accelerator is inefficient nor ineffective. Accelerators may be in the early stage of gaining legitimacy from investor network and potential investees. Or, they may invest with non-financial purpose which cannot be easily captured by the analysis adopted by this study. However, it should be emphasized that much more studies are required to cope with the huge growth of accelerators in entrepreneurial ecosystem.

What is important is that this study has led to an empirical study of the accelerator and, as a result, there has been a difference in general perception. There was also clearly an area where the accelerator had an advantage. Therefore, this study is meaningful as a starting point where future research or policies on the accelerator consider ways to reduce weakness and increase strength.

6.3. Limitations and future directions

This study addressed the controversy surrounding accelerators by using limited secondary data. As a result, we found that accelerators, as a new investor type, could solve the issue of external financing. Therefore, with the role of accelerators activated, we hope to improve the entrepreneurial ecosystem.

This study has several limitations. First, there were difficulties in analyzing and understanding the Crunchbase DB, since the database had many missing values. Moreover, as using the database is a “wiki way” of collecting data, transcription errors are inevitable. However, since this database has been utilized in previous research (Alexy et al., Citation2012; Block & Sandner, Citation2009), its reliability, apart from the missing values, has already been clarified. The Crunchbase DB still has a limitation in recognizing environments and their behavior since only a simple hypothesis is available due to its restrictions as a secondary database.

Second, our regression equation shows a low level of explanation. This is because investors consider many factors besides the variables included in our research models when they select the entrepreneurial firm for investing. However, we selected variables that are known to be able to see the differences in investor types among the factors that investors consider in investing. We examined whether the accelerator was of a new type and they achieved a differentiated performance. Nevertheless, as an initial empirical study of the accelerator, there have been many concerns about the choice of variables, and these are needed to be improved with a further study.

Despite the above limitations, this study is significant as an empirical work regarding accelerators, and has implications for future research. In future studies, further analysis of investment behaviors and performances should be conducted, apart from investor type. Moreover, in-depth research regarding accelerators’ value addition activities, such as mentoring, education, consulting, and human networking, which reduce the risks of entrepreneurial firms, should be conducted.

Additional information

Funding

Notes on contributors

Yunsoo Choi

Yunsoo Choi is a senior researcher at the Entrepreneurship Research Team of Korea Entrepreneurship Foundation (KOEF). He holds a PhD in management from Kookmin University. His main research interests are entrepreneurship and entrepreneurial ecosystems.

Dohyeon Kim

Dohyeon Kim is a professor at the College of Business Administration, Kookmin University and Dean of the Graduate School of Global Entrepreneurship in the same university. He holds a PhD in engineering from Seoul National University and another PhD in management from the University of Warwick. He has been interested in corporate entrepreneurship and entrepreneurial finance.

The two authors are members of the Global Entrepreneurship Monitor (GEM) team in Korea

Notes

1. CruchBase DB is a database that provides information related to startups and 100 NASDAQ companies, managed by TechCrunch; it mainly provides information regarding institutional and individual investors, investment news, and other events of the firms (http://data.crunchbase.com).

References

- Alexy, O. T., Block, J. H., Sandner, P., & Ter Wal, A. L. (2012). Social capital of venture capitalists and start-up funding. Small Business Economics, 39(4), 835–851. doi:10.1007/s11187-011-9337-4

- Ardichvili, A., Cardozo, R. N., Tune, K., & Reinach, J. (2002). The role angel investors in the assembly of non-financial resources of new ventures: Conceptual framework and empirical evidence. Journal of Enterprising Culture, 10(1), 39–65. doi:10.1142/S021849580200013X

- Arora, A., & Nandkumar, A. (2012). Insecure advantage? Markets for technology and the value of resources for entrepreneurial ventures. Strategic Management Journal, 33(3), 231–251. doi:10.1002/smj.v33.3

- Barron, D. N., West, E., & Hannan, M. T. (1994). A time to grow and a time to die: Growth and mortality of credit unions in New York City, 1914-1990. American Journal of Sociology, 100(2), 381–421. doi:10.1086/230541

- Birdsall, M., Jones, C., Lee, C., Somerset, C., & Takaki, S. (2013). Business accelerators: The evolution of a rapidly growing industry. Dostupno na http://startupaccelerator.com/sites/default/files/cambridge_startup_% 20accelerator_res earch. pdf.[pristupljeno: 3.10. 2015].

- Bliemel, M. J., Flores, R. G., de Klerk, S., Miles, M. P., Costa, B., & Monteiro, P. (2016). The role and performance of accelerators in the Australian startup ecosystem. Department of Industry, Innovation & Science (Made public 25 May, 2016); UNSW Business School Research Paper No. 2016MGMT03. Available at SSRN: https://ssrn.com/abstract=2826317 or http://dx.doi.org/10.2139/ssrn.2826317

- Block, J., & Sandner, P. (2009). What is the effect of the financial crisis on venture capital financing? Empirical evidence from US Internet start-ups. Venture Capital, 11(4), 295–309. doi:10.1080/13691060903184803

- Bygrave, W. D., & Zacharakis, A. (2014). Entrepreneurship (3rd ed.). Hoboken, NJ: John Wiley & Sons.

- Choi, Y. S., & Kim, D. H. (2016). A comparative study of the accelerator and venture capital through investment behavior. Asia-Pacific Journal of Business Venturing and Entrepreneurship, 11(4), 27–36. doi:10.16972/apjbve.11.4.201608.27

- Chun, Y. W., & Ha, K. S. (2016). A study on the effect of venture capitals’ investments capabilities on the investment performance of venture company. Journal of the Korea Industrial Information Systems Research, 21(6), 125–135. doi:10.9723/jksiis.2016.21.6.125

- Cohen, S. (2013). What do accelerators do? Insights from incubators and angels. Innovations, 8(3–4), 19–25. doi:10.1162/INOV_a_00184

- Cohen, S., & Hochberg, Y. V. (2014). Accelerating startups: The seed accelerator phenomenon. SSRN Electronic Journal. doi:10.2139/ssrn.2418000

- Cuervo-Cazurra, A., & Dau, L. A. (2009). Promarket reforms and firm profitability in developing countries. Academy of Management Journal, 52(6), 1348–1368. doi:10.5465/amj.2009.47085192

- Dempwolf, C. S., Auer, J., & D’Ippolito, M. (2014). Innovation accelerators: Defining characteristics among startup assistance organizations. www.sba. gov/advocacy: Small Business Administration.

- Drover, W., Busenitz, L., Matusik, S., Townsend, D., Anglin, A., & Dushnitsky, G. (2017). A review and road map of entrepreneurial equity financing research: Venture capital, corporate venture capital, angel investment, crowdfunding, and accelerators. Journal of Management, 43(6), 1820–1853. doi:10.1177/0149206317690584

- Elitzur, R., & Gavious, A. (2003). Contracting, signaling, and moral hazard: A model of entrepreneurs, ‘angels,’ and venture capitalists. Journal of Business Venturing, 18(6), 709–725. doi:10.1016/S0883-9026(03)00027-2

- Fried, V. H., & Hisrich, R. D. (1994). Toward a model of venture capital investment decision making. Financial Management, 23(3), 28–37. doi:10.2307/3665619

- Geibel, R., & Yang, J. (2018). Extended study on characterizing business angels and their impact on start-up success. GSTF Journal on Business Review (GBR), 5(1), ISSN 2251-2888. Available at: http://dl6.globalstf.org/index.php/gbr/article/view/882

- Gompers, P. A. (1996). Grandstanding in the venture capital industry. Journal of Financial Economics, 42(1), 133–156. doi:10.1016/0304-405X(96)00874-4

- Gregory, B. T., Rutherford, M. W., Oswald, S., & Gardiner, L. (2005). An empirical investigation of the growth cycle theory of small firm financing. Journal of Small Business Management, 43(4), 382–392. doi:10.1111/jsbm.2005.43.issue-4

- Gupta, A. K., & Sapienza, H. J. (1992). Determinants of venture capital firms’ preferences regarding the industry diversity and geographic scope of their investments. Journal of Business Venturing, 7(5), 347–362. doi:10.1016/0883-9026(92)90012-G

- Haar, N. E., Starr, J., & MacMillan, I. C. (1989). Informal risk capital investors: Investment patterns on the East Coast of the USA. Journal of Business Venturing, 3(1), 11–29. doi:10.1016/0883-9026(88)90027-4

- Haines, G. H., Jr, Madill, J. J., & Riding, A. L. (2003). Informal investment in Canada: Financing small business growth. Journal of Small Business & Entrepreneurship, 16(3–4), 13–40. doi:10.1080/08276331.2003.10593306

- Hallen, B. L., Bingham, C. B., & Cohen, S. (2014). Do accelerators accelerate? A study of venture accelerators as a path to success? Academy of Management Proceedings, 2014(1), 12955. doi:10.5465/ambpp.2014.185

- Hill, B. E., & Power, D. (2002). Attracting capital from angels: How their money - and their experience - can help you build a successful company. New York, NY: John Wiley & Sons.

- Hur, N. S., Yoon, B. S., & Lee, K. W. (2002). The impact of the certification role of venture capitalists on IPOs in the KOSDAQ. The Korean Journal of Financial Management, 19(1), 153–181.

- Kang, Y. R. (2014). Start-up support system status in Europe’s major economies: About accelerator. Broadcasting and Communications Policy, 26(4), 44–52.

- Kenney, M. (2000). “Note on “Venture Capital”” (BRIE working paper no. 142). Berkeley: Berkeley Roundtable on the International Economy.

- Khoury, T. A., Junkunc, M., & Mingo, S. (2015). Navigating political hazard risks and legal system quality venture capital investments in Latin America. Journal of Management, 41(3), 808–840. doi:10.1177/0149206312453737

- Kim, Y. J., & Yum, S. H. (2014). Understanding about the venture accelerator and direction of policy (KISDI Premium Report no. 19). Korea: Korea Information Society Development Institute.

- Ko, Y. H., & Lee, H. S. (2016). Interrelation between start-up characteristics and venture capital investment portfolio for strategic decision. Asia-Pacific Journal of Business Venturing and Entrepreneurship, 11(2), 63–73. doi:10.16972/apjbve.11.2.201604.63

- Lee, S. H. (1998). Survival analysis of the small and medium firms in the electronics industry. International Economic Journal, 4(2), 93–112.

- Levinsohn, D. (2014). The role of accelerators in the development of the practising social entrepreneur. Paper presented at Institute for Small Business and Entrepreneurship: The Future of Enterprise: The Innovation Revolution, November 5-6, 2014. Manchester, UK.

- Lim, C. Y., Lee, Y. J., Lee, K. H., Kim, J. S., Bae, Y. I., & Kim, S. J. (2008). An analysis for Korean venture survival. Seoul: Science and Technology Policy Institute.

- Lim, S., & Kim, Y. (2015). How to design public venture capital funds: Empirical evidence from South Korea. Journal of Small Business Management, 53(4), 843–867. doi:10.1111/jsbm.12109

- Mason, C. M., & Harrison, R. T. (1996). Informal venture capital: A study of the investment process, the post-investment experience and investment performance. Entrepreneurship & Regional Development, 8(2), 105–126. doi:10.1080/08985629600000007

- Mason, C. M., & Harrison, R. T. (2008). Measuring business angel investment activity in the United Kingdom: A review of potential data sources. Venture Capital, 10(4), 309–330. doi:10.1080/13691060802380098

- Mayer, C., Schoors, K., & Yafeh, Y. (2005). Sources of funds and investment activities of venture capital funds: Evidence from Germany, Israel, Japan and the United Kingdom. Journal of Corporate Finance, 11(3), 586–608. doi:10.1016/j.jcorpfin.2004.02.003

- Mejia, J., & Gopal, A. (2015). Now and later? Mentorship, investor ties and performance in seed-accelerators. Paper presented at the DRUID15, Rome.

- Miller, P., & Bound, K. (2011). The startup factories. NESTA. Accessed April 14 2015 http://www.nesta.org.uk/library/documents/StartupFactories.pdf

- Nelson, R. R., & Sidney, G.(2005). Winter. 1982. An evolutionary theory of economic change. Cambridge, MA: Belknap Press.

- Norton, E., & Tenenbaum, B. H. (1993). Specialization versus diversification as a venture capital investment strategy. Journal of Business Venturing, 8(5), 431–442. doi:10.1016/0883-9026(93)90023-X

- Pearce, B. (2014). Adapting and evolving: Global venture capital insights and trends 2014. London: Ernst & Young.

- Politis, D. (2008). Business angels and value added: What do we know and where do we go? Venture Capital, 10(2), 127–147. doi:10.1080/13691060801946147

- Ramadani, V. (2009). Business angels: Who they really are. Strategic Change, 18(7‐8), 249–258. doi:10.1002/jsc.852

- Reitan, B., & Sorheim, R. (2000). The informal venture capital market in Norway? Investor characteristics, behaviour and investment preferences. Venture Capital: an International Journal of Entrepreneurial Finance, 2(2), 129–141. doi:10.1080/136910600295747

- Rosenbusch, N., Brinckmann, J., & Müller, V. (2013). Does acquiring venture capital pay off for the funded firms? A meta-analysis on the relationship between venture capital investment and funded firm financial performance. Journal of Business Venturing, 28(3), 335–353. doi:10.1016/j.jbusvent.2012.04.002

- Samir, K. (2014). Revisiting Micro-VC Market. Accessed June 30 2016 http://pevcbanker.com/revisiting-the-micro-vc-market.

- Shane, S., & Venkataraman, S. (2000). The promise of entrepreneurship as a field of research. Academy of Management Review, 25(1), 217–226.

- Shane, S. A. (2009). The illusions of entrepreneurship: The costly myths that entrepreneurs, investors, and policy makers live by. New Haven, CT: Yale University Press.

- Shin, J., Mendoza, X., Hawkins, M. A., & Choi, C. (2017). The relationship between multinationality and performance: Knowledge-intensive vs. capital-intensive service micro-multinational enterprises. International Business Review, 26(5), 867–880. doi:10.1016/j.ibusrev.2017.02.005

- Short, J. C., Ketchen, D. J., Palmer, T. B., & Hult, G. T. M. (2007). Firm, strategic group, and industry influences on performance. Strategic Management Journal, 28(2), 147–167. doi:10.1002/smj.574

- Shrader, R. C., & Simon, M. (1997). Corporate versus independent new ventures: Resource, strategy, and performance differences. Journal of Business Venturing, 12(1), 47–66. doi:10.1016/S0883-9026(96)00053-5

- Sorenson, O., & Stuart, T. E. (2001). Syndication networks and the spatial distribution of venture capital investments. American Journal of Sociology, 106(6), 1546–1588. doi:10.1086/321301

- Sørheim, R. (2005). Business angels as facilitators for further finance: An exploratory study. Journal of Small Business and Enterprise Development, 12(2), 178–191. doi:10.1108/14626000510594593

- Stinchcombe, A. L. (2000). Social structure and organizations. In J. Baum & F. Dobbins (Eds.), Economics meets sociology in strategic management: Advances in strategic management (pp. 229-259). Greenwich, CT: JAI Press.

- Sudek, R. (2006). Angel investment criteria. Journal of Small Business Strategy, 17(2), 89.

- Tyebjee, T. T., & Bruno, A. V. (1984). A model of venture capitalist investment activity. Management Science, 30(9), 1051–1066. doi:10.1287/mnsc.30.9.1051