Abstract

The mediating mechanism of dividend policy remained untapped between financial performance, uncertainty, corporate social responsibility (CSR) and stakeholders’ interest. However, this study contributes to the body of knowledge and discovers the mediating role of dividend policy between financial performance, uncertainty, CSR and stakeholders’ interest. Data is collected through a questionnaire from CFO’s/financial managers of Pakistani corporate sector. Structural Equation Modeling (SEM) is used to analyze the results through AMOS. Uncertainty, CSR, and stakeholders’ interests have a significant impact on financial performance. It is found partial mediation between uncertainty and financial performance whereas dividend policy fully mediates the CSR, stakeholders’ interest and financial performance.

Public Interest Statement

Dividend policy is one of the most important areas in corporate finance research. Dividend policy determines the payout ratio from profits to the shareholders. A smooth dividend policy enhances firms’ performance. Dividend policy needs a careful selection of its determinants. Major theoretical advances in dividend policy decision-making have been made over the last few decades. However, different researchers assume that uncertainty, corporate social responsibility (CSR) and stakeholders’ interest are the important determinants of dividend policy. These determinants might help in boosting up the sales revenue which may lead to an increase in financial performance. In fact, increase in profits would give the high chance of paying out the dividend to shareholders.

1. Introduction

Financial performance of the firm is among the key areas of interest for managers, practitioners, and academics. Researchers have examined determinants of a firm’s financial performance and identified several of them, depending on the level of firm, industry, and country (Capon, Farley and Hoenig, Citation1990). However, the literature has paid little attention to the mediating mechanisms of dividend policy, CSR, stakeholders’ interest, and uncertainty in the financial performance. This neglect is more pronounced, especially, in the context of emerging markets, which have in recent times become an important center of corporate activity in the global economy. Pakistan, as a dynamic emerging economy, is going through phases of uncertainty, which is taking its toll due to lack of any serious academic research involving the corporate sector, including CSR, the absence of mediating mechanism. Considering the interrelationship of dividend policy and financial performance (Kajola, Adewumi, & Oworu, Citation2015), in this study dividend policy is used as a mediator between uncertainty, CSR, stakeholders’ interest and financial performance.

As previously noted, the nexus of uncertainty, CSR and stakeholders’ interest, dividend policy and financial performance has been well documented in the literature. It thus becomes prudent to look that whether dividend policy provides a link/bridge between these variables or not. Excellent management, technical and fundamental analysis, better forecasting may nullify the impact of uncertainty on financial performance. Similarly, as mentioned before CSR might be irrelevant towards financial performance so is the case of stakeholders’ interest. In that case, it is dividend policy which provides the way via which these variables affect the financial performance of a firm. Obviously, it can be argued that firm performance is more dependent on technical aspects like sales revenue. Uncertainty, CSR, and stakeholders’ interest might help in boosting up the sales revenue but even that would not guarantee an increase in financial performance. In fact, increase in profits would lead to a high chance of paying out the dividend to shareholders which will then determine the performance of the firm. It means that CSR, uncertainty and stakeholders’ interest would not cause only direct impact on financial performance rather the relationship between them is through 0;the dividend policy of a firm. The objective of this study is to check the mediating role of dividend policy among its determinants and financial performance.

The rest of the paper is structured in the following sections. Section 2 explains the underpinnings and hypotheses development while section 3 deals with the identification of method, data, and variables used in the empirical analysis. Section 4 discusses the empirical results followed by a conclusion in section 5.

2. Theoretical framework and hypotheses development

Uncertainty means ambiguous, unclear situation. It also means discrepancy in information. High level of uncertainty would cause management of firms to be defensive and take precautionary measures which may cause management to save money for future and may decrease the chances to payout dividend. Management can convince shareholders in this situation too by arguing about complexity in the environment and changing situations. Management of a firm, as supposed in agency theory (Jensen & Meckling, Citation1976) is selfish and watch its self-interest which is their job, salary, and benefits. Management thus would avoid any uncertainty that might lead to future business failure which will affect their lives. Management would thus be keen to save money or invest it somewhere to get a return in the future to avoid uncertainty. This may lead them to not pay any due dividend. Previous research on the related topic has shown that cash flow uncertainty is an influencing factor toward dividend policy. Cash flow uncertainty affects dividend payout policy among agency conflict, investment opportunities, and capital mix (Chay & Suh, Citation2009). Walkup (Citation2016) find that uncertainty significantly affects the firms’ dividend payout policy. As market uncertainty increases, firms with low cash flow levels tighten dividend policy to conserve cash while firms with high cash flow levels become opportunistic through the use of share repurchases. The literature points out that uncertainty can be specific that affect the adoption of financial decisions, rather than something categorized as general (Dixit, Dixit, Pindyck, & Pindyck, Citation1994). Therefore, uncertainty needs to be analyzed properly before making the dividend payout decision. Dealing with uncertainty can be a determinant of dividend policy adopted by the financial executives. Theoretically, uncertainty causes a slowdown in business operations, lead to confusion in the minds of workers, which can result in lower productivity, profitability and thus poor financial performance. Harash, Alsaadi, and Al-Timimi (Citation2014) argue that challenges towards financial performance evolve with changing uncertainties.

The debate on the relationship between CSR and financial performance is started six decades before. The literature provides the mix results on the direction of causality between CSR and financial performance. Cochran and Wood (Citation1984) find the association between CSR and financial performance. Torugsa, O’Donohue, and Hecker (Citation2012) stat that proactive CSR positively influences the financial performance. Van Beurden and Gössling (Citation2008) explore the literature review on the relationship between CSR and financial performance and they claim that literature provides clear evidence of a positive association between CSR and financial performance. CSR activities of a firm generate interest of the public in the firm. Positive social activities undertaken by the firm results to gain a name among people and they will remember the name of the firm/brand. At the time of purchase of any product or service because of recognizing the brand, unconsciously or consciously people would purchase that brand. This means that CSR activities would boost up the revenues of a company. When a company gets more, it pays more to shareholders to give a positive signal about the financial health of the company. As the signaling theory (Ross, Citation1977) predicts, dividend payment by firms is perceived by the investors/market as a sign of good health, implying that firms are earning more, which increase the chance to payout the dividend to the shareholders, a positive effect of CSR activities. Put differently; the result enjoys broad empirical support. Positive financial performance means high returns, and those returns may be compensated to investors by giving a dividend. CSR affects firm performance since its inception, which is intended to increase competitive advantages. So, a positive association between CSR and firms’ performance can be expected. Firms that consider CSR activities are engaged in less risky investment in the future as compared to firms that are not involved in CSR activities at all. CSR activities are considered as similar to risk management at long-term basis (Brine, Brown, & Hackett, Citation2007). Chih, Miao, and Chuang (Citation2014) argue that firms could improve performance by increasing CSR activities because such activities do not erode firm profitability. Furthermore, CSR can also increase firm value and performance (Harjoto & Jo, Citation2015). However, some notable features of the findings are that the positive relationship appears to dominate the recent literature. Hirigoyen and Poulain-Rehim (Citation2015) find that CSR significantly and positively affects the financial performance of the firm.

A firm’s management should consider itself as stakeholders, and all the operations of the firms should reflect their interests, needs, and viewpoints (Friedman & Miles, Citation2006). Identifying stakeholders’ interest is also one of the key objectives, which needs to comply with the normal or routine operations of the business and helps to gain success (Mitchell, Agle, & Wood, Citation1997). Social impact hypothesis shows a positive association of meeting the interests of all stakeholders’ and the firm’s output in financial terms (Freeman, Citation1984). As a part of the policy, when all views of stakeholders are considered favorably it is expected that they would increase the firm’s output in financial terms. Freeman (Citation1984) notes that a top long-term objective of any firm is to create value at the stakeholder’s end. The association of management and stakeholder has an important effect on the firm’s output in financial terms. Managers’ job is to create and maintain the favorable environment so that all stakeholders can contribute their skills and knowledge for the betterment of the firm (Freeman, Wicks, & Parmar, Citation2004). From the firms’ perspective, those who take opinions of stakeholders’ into consideration tend to do good in financial terms in the future. When a firm fulfills the needs of its all stakeholders, it would expect favorable firm’s output in financial terms in the coming future (Freeman, Citation1984). Prior studies report a significant positive relationship between stakeholder interest and financial performance (Ayuso, Rodríguez, García-Castro, & Ariño, Citation2014; Freeman et al., Citation2004). Shareholders are the biggest stakeholders in any firm. Shareholders have their money at stake in the organization. The firm, by its definition, exists to provide/increase the wealth of its owners, i.e., shareholders. The two possible channels by which shareholders get that income is dividend and capital gain. If the organization watches for the interest of its biggest stakeholder then it may favor higher dividend payments to its shareholders. This means that stakeholder’s protecting interest of stakeholder may have a significant impact on the dividend policy of a firm. Even minority stakeholders would also want shareholders to be happy by getting money to avoid any conflict with them as shareholders are the actual owners of the firm.

Dividend policy refers to the payout of dividend to shareholders, which include regulations and guidelines used by a company about making payments (Nissim & Ziv, Citation2001). Theoretical inquiry into the relationship between dividend and financial performance dates back to 1961 when Miller and Modigliani (Citation1961) argue that dividend is irrelevant to the financial performance of firm showing that the firm’s value is independent of the fact that whether it pays dividend or not rather; instead, it is dependent on the fundamentals of the firm. Subsequent research has shown mixed results on the relationship between the firm’s financial performance and dividend policy, some showing a positive relationship (Amidu, Citation2007), few report negative relationship (Fukuda, Citation2000) while some found none between them (DeAngelo, DeAngelo, & Skinner, Citation1996; Grullon, Michaely, Benartzi, & Thaler, Citation2005). Recent research, however, points to a positive relationship between dividend payout and financial performance (Kajola et al., Citation2015). Hoang and Hoxha (Citation2016) argue that dividend smoothing is sensitive to financing and investing decisions of the firm. Apparently, the stream of researchers reporting positive relationship seems dominant. However, the importance of mediating mechanism in assessing the nexus of financial performance and its determinants has not garnered much academic curiosity and has thus remained untapped, something this present study aims to address. With that objective in mind, several hypotheses are developed and test them using relevant data within the specified theoretical framework of this study which is shown in Figure .

Figure 1. Theoretical framework.

H1: Uncertainty negatively affects the firm’s financial performance.

H2: CSR positively effects the firm’s financial performance.

H3: Stakeholder interest positively affects the firm’s financial performance.

H4: Dividend policy positively affects the firm’s financial performance.

H5: Uncertainty negatively affects the firm’s dividend policy.

H6: CSR positively affects the firm’s dividend policy.

H7: Stakeholder interest positively affects the firm’s dividend policy.

H8: Dividend policy mediates uncertainty and the firm’s financial performance.

H9: Dividend policy mediates CSR and the firm’s financial performance.

H10: Dividend policy mediates stakeholder interest and the firm’s financial performance.

3. Data and methodology

For the purpose of this study, 11 leading industries (Banking, Insurance, Telecommunication, Automobile, Cement, Fertilizer, Oil and Gas, Sugar, Textile, Tobacco, and Pharmaceutical) of the corporate sector of Pakistan are selected. I received 209 responses to the questionnaireFootnote1 from 321 CFOs/Finance Managers of selected industries of the corporate sector. Table describes the information of total companies of the corporate sector listed at Pakistani Stock Exchange (PSX) in 2012–2013 and response from each industry are given as well. Data is collected through a survey at the end of 2013.

Table 1. Industry-wise listed companies and response (2012–2013)

Survey method is used for data collection. Survey method is better to collect data directly to elicit information on the respondents’ behavior and their interrelationship (Bloch, Ridgway, & Dawson, Citation1994). The Structural Equation Modeling (SEM) is applied to analyze the results, interpretation and visual presentation (Nachtigall, Kroehne, Funke, & Steyer, Citation2003). A two-step procedure is used as outlined by Prabhu (Citation2007) and Hoyle and Smith (Citation1994) to assess the mediating role of dividend policy.

3.1. Pilot testing

In this study, the 5-point Likert scale is used in the questionnaire. The validity of the instrument is checked through confirmatory factor analysis (CFA) to check the measurement problems of the instrument. Scale validity is important to provide enough support to the instrument in different cultures (Nunnally & Bernstein, Citation1978). CFA is the best approach to determine the strength (strong or weak) of the latent variable (Steenkamp and Baumgartner, Citation2000). Pilot testing is done on 153 responses and the values of model fit indexes are 0.948, 0.861, 0.915, 0.903 and 0.057 for goodness of fit index (GFI), adjusted goodness of fit index (AGFI), comparative fit index (CFI), Tucker-Lewis coefficient (TLI), Root mean square error of approximation (RMSEA) respectively, which show a good fit model.

Convergent validity is explained in Table , standardized estimates are used to make the decision of valid or invalid items from each variable. The item is considered valid if the factor loading is above or equal to 0.50 (Cua, McKone, & Schroeder, Citation2001). It is observed that maximum questions of the instrument are valid to measure the theoretical framework in Pakistani corporate sector. Fornell and Larcker (Citation1981) suggest that Average Variance Extracted (AVE) of the construct should be greater than or equal to 0.50, which indicates convergent validity. Therefore, the AVE value of all variables is greater than the role of thumb; it means that there is less variance explained by an error in the items than the variance of the latent variable. The criteria given by Netemeyer, Bearden, and Sharma (Citation2003) for Construct Reliability (CR) is greater than 0.70. Here, the CR value of uncertainty, CSR, stakeholders’ interest, financial performance, and the dividend is greater than 0.70 that means construct reliability for internal consistency is there.

Table 2. Convergent validity

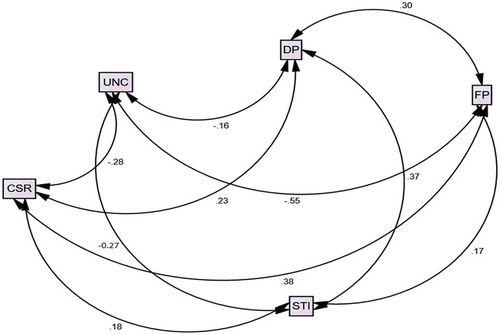

Figure describes the covariance diagram is used to check the discriminant validity. The sign of covariance confirms the direction of the relationship between two variables and covariance values are further used to calculate the inter-construct correlation (IC). Square of inter-construct correlation (SIC) value is used to make a decision of discriminant validity. On the bases of IC weights decision of discriminant and nomological validity are made and explained in below tables.

Figure 2. Covariance diagram.

Table explains that the entire constructs are discriminately valid. Fornell and Larcker (Citation1981) describe that the value of AVE should be greater than SIC for both constructs, and it is proved there is discriminant validity. Nomological validity is tested by examining whether the inter-construct correlations between the constructs in the measurement model make sense. For this purpose, the correlation coefficient should be in line (±) and significant with the direction of baseline theory/concept (Fornell & Larcker, Citation1981). Therefore, it is accessed that all the constructs/variables are logically & significantly interlinked to each other and make sense. The IC value suggests there is a significant association among constructs.

Table 3. Discriminant and nomological validity of the construct

Table presents the variables, their source, number of items, number of valid items and their reliability. Internal consistency each variable is measured by Cronbach’s Alpha (Hair, Anderson, Tatham, & Black, Citation1998). All values for Alpha are higher than 0.70 suggesting that the instrument is reliable.

Table 4. Variables, their source, number of items, number of valid items and their reliability

4. Empirical analysis

I used different tests to analyze the collected data. Table presents the results of the adaptability test of the model, i.e. GFI, AGFI and chi-square are parsimonious fit measures, and CFI is a measure of incremental fitness (Keramati, Mehrabi, & Mojir, Citation2010). The fitness indexes of the direct model (without a mediator) and indirect model (with a mediator), as suggested by McAulay, Zeitz, and Blau (Citation2006), Roh, Ahn, and Han (Citation2005), Hair et al. (Citation1998), clearly demonstrate the desired model fitness. All mentioned criteria indicate the best choice for this study model at suggested levels.

Table 5. Model fit index

After determining the model fit, the regression coefficients are estimated. Prabhu (Citation2007) approach is followed to check the mediation between dependent and independent variables and to observe the existence of full or partial mediation in the model. As a first step, the direct effect of the independent variables on the dependent is checked. In the second step, the indirect effect of independent variables on the dependent variable through the mediating variable is checked.

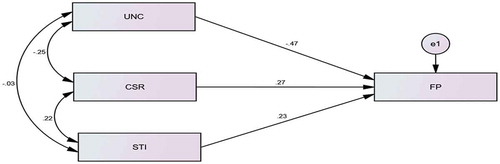

Figure reveals the direct effect of uncertainty, CSR, and stakeholders’ interest on financial performance.

Figure 3. Direct effects without mediation.

The results in Table suggest that financial performance has a significant negative relationship with uncertainty whereas a significant positive relationship with CSR and stakeholders’ interest which proves H1, H2, and H3. The results indicate that uncertainty has a negative effect on the financial performance of the corporate sector in Pakistan. This result has serious policy implications for economic experts of Pakistan. For the development of the corporate sector, they need to reduce uncertainties in socio-economic governance of Pakistan. Further, significant positive relationship of CSR and stakeholder interest with financial performance suggests that managers of the corporate sector in Pakistan need to improve their corporate governance to safeguard interests of their stakeholders and consider CSR as an investment (not an expense) that helps to improve the financial performance of their organization. After analyzing the direct relationships, a two steps procedure is used to check the mediating effect of dividend policy which is shown in Figure .

Table 6. Regression weights: (direct effects)

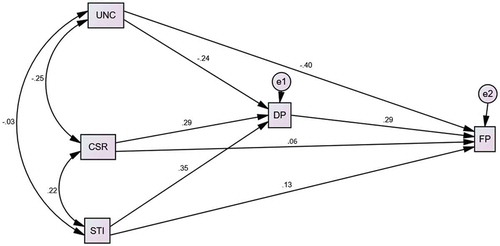

Figure 4. Indirect effects with the mediator (dividend policy).

The relationships between uncertainty, CSR and stakeholders’ interest and dividend policy show statistically significant in Table , which are supporting hypotheses H4, H5 and H6. It further reveals that the relationship between dividend policy and financial performance is statistically significant; thus it enables to confirm hypothesis H7.

Table 7. Regression weights: indirect effects

In Table , the relationships between uncertainty, CSR and stakeholders’ interest and financial performance with the inclusion of dividend policy as a mediating variable shows that value of uncertainty is significantly reduced; thus confirming partial mediation and proves H8. Whereas, the insignificant relationship between CSR and stakeholders’ interest and financial performance shows complete mediation of dividend policy; thus supporting hypotheses H9 and H10. The purpose of the present study is to investigate the mediating role of dividend policy among uncertainty, CSR, stakeholders’ interest and financial performance. The companies which are relatively more profitable, less risky, mature and stable then there are more chances to pay a dividend in comparison to companies that do not pay any dividend. Historically, a number of studies have examined the dividend policy that directly affects the organization’s financial performance. The direct and indirect impact of dividend policy are identified in this study and are supported by Bae, Kang, and Wang (Citation2011). The present study finds that uncertainty has a direct impact on the financial performance as well as the mediation role of dividend policy with financial performance. These findings are in line with the findings of Ittner and Larcker (Citation2001). The current findings suggest that the relationship between financial performance and CSR is significant and supported by the study of Chih et al. (Citation2014). The investigation reveals that the relationship between CSR and dividend policy is statistically significant which is aligned by the works of the Niazi, Hunjra, Rashid, Akbar, and Akhtar (Citation2011). The relationship between stakeholders’ interest and financial performance is also significant; therefore, it is concluded that the interest of stakeholders’ significantly impacts the financial performance of an organization. This finding is supported by the results of Freeman et al. (Citation2004).

Table 8. Comparison of direct and indirect effects (dividend policy)

5. Conclusion

The overall results clearly show that uncertainty, CSR, and the stakeholders’ interest have a significant impact on firms’ financial performance. This study discovers the mediating role of dividend policy among its determinants and the financial performance. It finds that uncertainty has a negative impact on dividend policy and financial performance hence, it is investigated that uncertainty has a significant impact on financial performance partially mediated by dividend policy. It has been found that dividend policy completely mediates between CSR, stakeholders’ interest and financial performance. The point to ponder is, how appropriate the concerning authorities make dividend policy and how this decision can be helpful in enhancing the financial performance of the firms? The result sheds considerable light on the issue; it seems that the financial managers should be trained enough to make decisions of effective dividend policy for achieving the ultimate goal of organizational success and value creation. The progressive financial performance of the firms attracts more capital to the market by building up investors’ and stakeholders’ confidence. Thus, the better dividend policy decision makes the stakeholders’ skeptical about the validity of their actions.

The findings of this study are useful for funds providers, such as creditors and shareholders/investors, with the view of external financing requirements of firms. It follows that capital providers should seek to invest in firms which care for society and stakeholders as such firms are more willing to give a dividend. Based on the findings of this study, it is suggested to the CFO/Finance managers of Pakistani corporate sector should incorporate the uncertainty, CSR and stakeholders’ interest while making dividend policy decisions. Furthermore, it is recommended that companies shall take initiative in CSR activities and emphasize the uncertain situation in financial decision-making. The present research can be extended by comparing high performing and low performing firms. Industry-wise analysis of this issue can be a good future study. The working capital, implications of financial ratios and treasury operations management can be incorporated in this conceptual framework for the future study.

Additional information

Funding

Notes on contributors

Ahmed Imran Hunjra

Dr. Ahmed Imran Hunjra is Post-Doctoral Fellow at School of Accounting, Finance and Economics, The University of Waikato, New Zealand & Assistant Professor at University Institute of Management Sciences-PMAS- Arid Agriculture University Rawalpindi, Pakistan. Ahmed has more than ten years teaching and research experience in total. Ahmed areas of research interest are Corporate Finance, Corporate Governance, Financial Risk Management, and Portfolio Management. Ahmed has supervised 39 MS/MPhil and 02 PhDs scholars of different universities to the successful culmination of their degrees. Furthermore, one of his PhD scholars has submitted his thesis for final defense, 04 doctorate & 06 MS candidates have successfully defended their proposal. Ahmed has published 30 plus research papers in national and international journals; his seven research papers are under review and five are in their final phases.

Notes

1. met CFOs/Finance Managers in person.

References

- Amidu, M. (2007). How does dividend policy affect performance of the firm on Ghana Stock Exchange? Investment Management and Financial Innovations, 4(2), 103–112.

- Ayuso, S., Rodríguez, M. A., García-Castro, R., & Ariño, M. A. (2014). Maximizing stakeholders’ interests: An empirical analysis of the stakeholder approach to corporate governance. Business & Society, 53(3), 414–439. doi:10.1177/0007650311433122

- Bae, K. H., Kang, J. K., & Wang, J. (2011). Employee treatment and firm leverage: A test of the stakeholder theory of capital structure. Journal of Financial Economics, 100(1), 130–153. doi:10.1016/j.jfineco.2010.10.019

- Bloch, P. H., Ridgway, N. M., & Dawson, S. A. (1994). The shopping mall as consumer habitat. Journal of Retailing, 70(1), 23–42. doi:10.1016/0022-4359(94)90026-4

- Brine, M., Brown, R., & Hackett, G. (2007). Corporate social responsibility and financial performance in the Australian context. Economic Round-Up, 2, 47–58.

- Capon, N., Farley, J. U., & Hoenig, S. (1990). Determinants of financial performance: A meta-analysis. Management Science, 36(10), 1143–1159. doi:10.1287/mnsc.36.10.1143

- Chay, J. B., & Suh, J. (2009). Payout policy and cash-flow uncertainty. Journal of Financial Economics, 93(1), 88–107. doi:10.1016/j.jfineco.2008.12.001

- Chih, H. H., Miao, W. C., & Chuang, Y. C. (2014). Is corporate social responsibility a double-edged sword? Evidence from fortune global 500 companies. Journal of Management, 31(1), 1–19.

- Cochran, P. L., & Wood, R. A. (1984). Corporate social responsibility and financial performance. Academy of Management Journal, 27(1), 42–56.

- Cua, K. O., McKone, K. E., & Schroeder, R. G. (2001). Relationships between implementation of TQM, JIT, and TPM and manufacturing performance. Journal of Operations Management, 19(6), 675–694. doi:10.1016/S0272-6963(01)00066-3

- DeAngelo, H., DeAngelo, L., & Skinner, D. J. (1996). Reversal of fortune dividend signalling and the disappearance of sustained earnings growth. Journal of Financial Economics, 40(3), 341–371. doi:10.1016/0304-405X(95)00850-E

- Dixit, A. K., Dixit, R. K., Pindyck, R. S., & Pindyck, R. (1994). Investment under uncertainty. Princeton, NJ: Princeton University Press.

- Elijido-Ten, E., Kloot, L., & Clarkson, P. (2010). Extending the application of stakeholder influence strategies to environmental disclosures: An exploratory study from a developing country. Accounting, Auditing & Accountability Journal, 23(8), 1032-1059.

- Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50. doi:10.1177/002224378101800104

- Freeman, R. E. (1984). Strategic management: A stakeholder approach. Boston, MA: Pitman.

- Freeman, R. E., Wicks, A. C., & Parmar, B. (2004). Stakeholder theory and “the corporate objective revisited”. Organization Science, 15(3), 364–369. doi:10.1287/orsc.1040.0066

- Friedman, A. L., & Miles, S. (2006). Stakeholders: Theory and practice. Oxford: Oxford University Press.

- Fukuda, A. (2000). Dividend changes and earnings performance in Japan. Pacific-Basin Finance Journal, 8(1), 53–66. doi:10.1016/S0927-538X(99)00024-4

- Grullon, G., Michaely, R., Benartzi, S., & Thaler, R. H. (2005). Dividend changes do not signal changes in future profitability. The Journal of Business, 78(5), 1659–1682. doi:10.1086/jb.2005.78.issue-5

- Hair, J. F., Anderson, R. E., Tatham, R. L., & Black, W. C. (1998). Multivariate data analysis (5th ed.). New Jersey: Prentice-Hall International, Inc.

- Harash, E., Alsaadi, J., & Al-Timimi, S. (2014). Financial performance of SMEs—Evidence on the influence of environmental uncertainty: A conceptual framework. China-USA Business Review, 13(8), 540–545.

- Harjoto, M. A., & Jo, H. (2015). Legal vs. normative CSR: Differential impact on analyst dispersion, stock return volatility, cost of capital, and firm value. Journal of Business Ethics, 128(1), 1–20. doi:10.1007/s10551-014-2082-2

- Hirigoyen, G., & Poulain-Rehim, T. (2015). Relationships between corporate social responsibility and financial performance: What is the causality? Journal of Business and Management, 4(1), 18–43.

- Hoang, E. C., & Hoxha, I. (2016). Corporate payout smoothing: A variance decomposition approach. Journal of Empirical Finance, 35, 1–13. doi:10.1016/j.jempfin.2015.10.011

- Hoyle, R. H., & Smith, G. T. (1994). Formulating clinical research hypotheses as structural equation models: A conceptual overview. Journal of Consulting and Clinical Psychology, 62(3), 429–440.

- Ittner, C. D., & Larcker, D. F. (2001). Assessing empirical research in managerial accounting: A value-based management perspective. Journal of Accounting and Economics, 32(1–3), 349–410. doi:10.1016/S0165-4101(01)00026-X

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360. doi:10.1016/0304-405X(76)90026-X

- Kajola, S. O., Adewumi, A. A., & Oworu, O. O. (2015). Dividend pay-out policy and firm financial performance: Evidence from Nigerian listed non-financial firms. International Journal of Economics, Commerce and Management, 3(4), 1–12.

- Keramati, A., Mehrabi, H., & Mojir, N. (2010). A process-oriented perspective on customer relationship management and organizational performance: An empirical investigation. Industrial Marketing Management, 39(7), 1170–1185. doi:10.1016/j.indmarman.2010.02.001

- McAulay, B. J., Zeitz, G., & Blau, G. (2006). Testing a “push-pull” theory of work commitment among organizational professionals. The Social Science Journal, 43(4), 571–596. doi:10.1016/j.soscij.2006.08.005

- McCaffery, K., Hutchinson, R., & Jackson, R. (1997). Aspects of the finance function: A review and survey into the UK retailing sector. The International Review of Retail, Distribution and Consumer Research, 7(2), 125–144. doi:10.1080/095939697343076

- Miller, M. H., & Modigliani, F. (1961). Dividend policy, growth, and the valuation of shares. The Journal of Business, 34(4), 411–433. doi:10.1086/jb.1961.34.issue-4

- Mitchell, R. K., Agle, B. R., & Wood, D. J. (1997). Toward a theory of stakeholder identification and salience: Defining the principle of who and what really counts. Academy of Management Review, 22(4), 853–886. doi:10.5465/amr.1997.9711022105

- Nachtigall, C., Kroehne, U., Funke, F., & Steyer, R. (2003). Pros and cons of structural equation modeling. Methods Psychological Research Online, 8(2), 1–22.

- Netemeyer, R. G., Bearden, W. O., & Sharma, S. (2003). Scaling procedures: Issues and applications. Thousand Oaks, CA: Sage Publications.

- Niazi, G. S. K., Hunjra, A. I., Rashid, M., Akbar, S. W., & Akhtar, M. N. (2011). Practices of working capital policy and performance assessment financial ratios and their relationship with organization performance. World Applied Sciences Journal, 12(11), 1967–1973.

- Nissim, D., & Ziv, A. (2001). Dividend changes and future profitability. The Journal of Finance, 56(6), 2111–2133. doi:10.1111/0022-1082.00400

- Nunnally, J., & Bernstein, I. H. (1978). Psychometric theory. New York, NY: McGraw-Hill.

- Prabhu, N. U. (2007). Stochastic processes: Basic theory and its applications. New York, NY: Macmillan Publishers.

- Roh, T. H., Ahn, C. K., & Han, I. (2005). The priority factor model for customer relationship management system success. Expert Systems with Applications, 28(4), 641–654. doi:10.1016/j.eswa.2004.12.021

- Ross, S. A. (1977). The determination of financial structure: The incentive-signalling approach. The Bell Journal of Economics, 8(1), 23–40. doi:10.2307/3003485

- Schulz, A. K., Wu, A., & Chow, C. W. (2010). Environmental uncertainty, comprehensive performance measurement systems, performance-based compensation, and organizational performance. Asia-Pacific Journal of Accounting & Economics, 17(1), 17–39. doi:10.1080/16081625.2010.9720850

- Steenkamp, J. B. E, & Baumgartner, H. (2000). On the use of structural equation models for marketing modeling. International Journal of Research in Marketing, 17(2–3), 195-202. 10.1016/S0167-8116(00)00016-1

- Torugsa, N. A., O’Donohue, W., & Hecker, R. (2012). Capabilities, proactive CSR and financial performance in SMEs: Empirical evidence from an Australian manufacturing industry sector. Journal of Business Ethics, 109(4), 483–500. doi:10.1007/s10551-011-1141-1

- Tyagi, R. (2012). Ph. D Thesis: Impact of corporate social responsibility on financial performance and competitiveness of business: A study of indian firms. Indian Institute of Technology, Roorkee.

- Van Beurden, P., & Gössling, T. (2008). The worth of values–A literature review on the relation between corporate social and financial performance. Journal of Business Ethics, 82(2), 407. doi:10.1007/s10551-008-9894-x

- Verbeeten, F. H. (2006). Do organizations adopt sophisticated capital budgeting practices to deal with uncertainty in the investment decision? A research note. Management Accounting Research, 17(1), 106–120. doi:10.1016/j.mar.2005.07.002

- Walkup, B. (2016). The impact of uncertainty on payout policy. Managerial Finance, 42(11), 1054–1072. doi:10.1108/MF-09-2015-0237