Abstract

In recent years, financial institutions especially universal/commercial banks across Africa have been faced with forceful mergers and acquisitions. These occurrences impede the level of financial inclusion and reduces public confidence in the financial system as a whole. This study assessed the effect of credit and operational risk on the financial performance of universal banks in the context of the structural equation model (SEM). Data were collected from all the 24 universal banks in Ghana without missing variables and using the PLS-SEM, the results showed that credit risk influences financial performance negatively contrary to the empirical study but in line with the information asymmetry tenant of the lemon theory. It was also found that operational risk influences the financial performance of the universal banks in Ghana negatively. Furthermore, the study indicated that bank specific variables measured by (asset quality, bank leverage, cost to income ratio and liquidity) significantly influence credit risk, operational risk as well as the financial performance of the universal banks positively. We recommend that banks be encouraged to cut-down their lending rates in other to decrease credit risk and subsequently boost profitability. Regarding operational risk, banks should reduce leverage and have their portfolio more concentrated on liquid investment income so as to boost profitability.

PUBLIC INTEREST STATEMENT

The banking sector of every country plays a significant role as intermediary in its economic development by channelling funds to the needed sectors of the economy. In administering this significant role, banks are exposed to risk resulting from inadequate internal processes, systems and external events (operational risk). Also, the risk that borrowers will default in repayment of interest and the principal loans on time (credit risk) is of concern. These risks have a high tendency of adversely affecting the financial performance of these institutions. Using the partial-least-squares structural equation module (PLS-SEM), which involves robust path analysis, it was revealed that credit and operational risk adversely influence the financial performance of banks but in line with the lemon theory, information asymmetry leads to more credit risk which could negatively influence the profitability of the universal banks. To ensure the survival and avoid the forceful mergers and acquisitions which has engulfed the industry in recent years, this study provides useful recommendations.

1. Introduction

The focus of most universal banks across the globe has been on risk management (Saunders & Cornett, Citation2006). Issues related to the risk management of universal banks are credit risk, liquidity risk, off-balance sheet risk, foreign exchange risk, operational risk and interest rate risk. Enhancing the argument on how risk affects financial performance may cutback the probability of insolvency and provide greater stability of the universal banks. It must be noted that the operational undertakings of every institution is utmost to the success and survival of that entity. From this backdrop, operational risk is explained as the loss resulting from inadequate or failed internal processes, people and systems or from external events (Basel Committee on Bank Supervision, Citation2006). This includes legal risk arising from events such as internal and external fraud, employment practices and workplace safety, products and business practices, damage to physical assets, business disruptions, system failures and process management. The Basel Committee on Bank Supervision (Citation2006) posit that operational risk makes the financial stability and performance of the financial sector more volatile. This assertion implies that if operational risk is not addressed systematically, it can result in non-consistent performance which may adversely affect the banks’ net worth with disastrous systemic consequences (Hess, Citation2011; Andersen, Hager, Maberg, Naess, & Tungland, Citation2012; Cagan, Citation2009; Kirkpatrick, 2009; Rose, Citation2009).

In addition to operational risk management, the fundamental role of banks in any economy is credit creation. According to Kargi (2011), the credit function of banks augments the ability of investors to take advantage of profitable projects they desire. However, this role makes banks vulnerable to credit risk. Credit risk has been the reason behind the rising interest in risk management. The Basel Committee on Banking Supervision (Citation2016) explained pertinent issues in credit risk as the possibility of losing an outstanding loan partly or totally, as a result of default. A vivacious credit risk framework is thus, critical for banks to boost their profitability and avoid forceful mergers and acquisition. The higher the acquaintance of a bank to credit risk, the higher the propensity of the bank to experience financial crisis and vice-versa. Among other risks faced by banks, credit risk play an important role on banks’ financial performance since a large chunk of banks’ revenue accrues from loans from which interest is derived. However, interest rate risk is directly linked to credit risk inferring that increment in interest rate increases the chances of loan default. Credit risk and interest rate risk are intrinsically related to each other and not separable as Drehman, Sorense and Stringa (2008) stipulated. Increasing amount of non-performing loans (NPLs) in the credit portfolio is inimical to achieving bank objectives.

Kargi (Citation2014) indicated that the increasing inclination for greater risk has resulted in insolvency and failure of a large number of the banks. The major cause of serious banking problems continues to be directly linked to low credit standards for borrowers, counterparties, insufficient attention to changes in economic and other circumstances can lead to deterioration in the credit standing of banks’ counter parties and poor portfolio management. The mounting wave of NPLs of banks made the Basel II Accord place much emphasis on credit risk management practices. Adherence to the Basel Accord indicates that a sound approach to dealing with credit risk management has been taken and may eventually enhance a bank’s financial performance. Effective credit risk management, support the viability and profitability of the banks and contribute to systemic stability and growth of the economy (Psillaki,Tsolas & Margaritis, 2010; Anaman, Gadzo, Gatsi, & Pobbi, Citation2017).

Being aware of the effect of credit and operation risk management in providing an extensive approach for managing these risks, the Basel Committee on Banking Supervision implemented the Basel I Accord in 1988, followed by the Basel II Accord in 2004 and the Basel III accord having identified the loopholes of previous accords to deal with credit risk management during financial crisis (Jayadev, 2013; Ouamar, 2013). However, the full benefits of implementing the Basel I and II Accords has not yet been realised in Ghana as expected. The total credit in the banking sector of Ghana stood at GH¢29.1 billion in August 2015, GH¢28.7 billion by the close of September 2016 and as at December 2017 the Gross Credit Advances stood at GH¢37.66 billion representing 1.3 percent contraction in real growth, compared with the 1.9 percent growth in the same period last year (Bank of Ghana Annual Report, Citation2017).

The report further posited that the current stock of NPLs translated into an NPL ratio of 22.7 percent in December 2017 from 17.3 percent in December 2016. In addition to the marginal pickup in the year-on-year growth in the stock of NPLs, the increased NPL ratio was attributable to a slowdown in industry loans (from 17.6% in December 2016 to 6.4% in December 2017) but the reason given by the regulatory body may not clutch based on the information asymmetry tenant of the lemon theory hence the need for an empirical study to assess the situation (Akerlof, Citation1970). In addition, adjusting the universal banking sector’s NPLs for the fully provisioned loan loss category, the ratio stood at 10.8 percent in December 2017 compared with 8.4 percent in December 2016. From the operational perspective, the biggest universal bank in Ghana in terms of asset size, GCB bank through the intervention of the Central Bank,(Bank of Ghana) took over two universal banks in 2017 in a move to reduce the hash effect of the collapses on customers of those banks (Ghana Banking Survey, Citation2017). To protect customers and restore confidence in the banking sector, the Bank of Ghana increased the minimum capital requirement from GH¢120 million to GH¢400 million representing over 233 percent increase which is expected to be fully complied with by December 2018.

There is no doubt that the retrenchment of credit and increases in bad loans hamper the financial performance of banks as depicted in literature (Noman, Pervin, Chowdhury, & Banna, Citation2015; Ruziqa, Citation2013; Salah & Fedhila, Citation2012; Corcoran, Citation2010; Hsieh & Lee, Citation2010; Hosna, Bakaeva & Juanjuan, 2009; Li & Zou, Citation2014; Apanga, Appiah, & Arthur, Citation2016). The study conducted by Muriithi (2017) also indicated that operational risk affect performance but neither of these studies used latent variables to represent credit and operational risk in a structural equation model (SEM) nor combined both credit and operational risk to access the magnitude of their effect on the financial performance of financial institutions. This study therefore seeks to ascertain the effect of both operational risk and credit risk on banks performance using the Partial Least Squared Structural Equation Module (PLS-SEM) that involves path analysis statistical techniques. This model includes the bank specific variables as control variable and then justifies the relationship among credit risk, operational risk and financial performance. Nitzl (Citation2016) opined that SEMs offer flexibility for testing such models, allowing one to use multiple predictors and criterion variables, construct latent (unobservable) variables, model errors in measurement for observed variables, and test mediation and moderation relationships in a single model. Based on the empirical results, this study provides some suggestions for the regulation of banking sector particularly the universal banks in Ghana.

The remainder of this paper is organized as follows. Section 2 develops a framework for testing and verifying the relationship among credit risk, operational risk and profitability for Universal Banks in Ghana. Section 3 then describes the data and empirical methodology. Next, Section 4 presents the empirical results. Finally, Section 5 details the conclusions.

2. Literature review

Operational and credit risk defines the survival and the competitive nature of the activities in the financial sector most importantly their profitability. This study examines the influence of credit and operational risk on the profitability of universal banks in Ghana. This study attempts to build a research model by examining the problems arising from previous studies.

2.1. Theoretical postulates

This study is discussed on the premises of Information asymmetry, which is one of the tenants of the lemon theory propounded by Akerlof in 1970. According to Tupangiu (Citation2017), information asymmetry depicts relationships where an agent holds information while another does not hold it. Thus, to the extent that one of the parties to the financing agreement has information more or less accurate than another, the asymmetry of information appears to be a major constraint in the financing of a project. Universal Banks, in their capacity as financial intermediary responsible for asset transformation need more information to assess the borrower before funds are channelled to them. From this backdrop, according to Akerlof (Citation1970) the lemon theory postulates that given an inefficient Credit reference bureau system, it will culminate into the existence of information asymmetry between regulatory body and the universal banks as well as the customers of the banks and the management of the universal banks. Banks may find it difficult to distinguish credit worth borrowers from bad borrowers, which may result in adverse selection and moral hazards problems. Bofondi and Gobbi (Citation2003) posit that adverse selection and moral hazard have led to substantial build-up of NPLs of banks, which has eventually exposed them to high credit risk as well as operational risk. Derban, Binner, and Mullineux (Citation2005) and Ahmed, Rahman and Ahmed (Citation2006) suggested that borrowers be screened particularly by banking institutions in the form of credit assessment. From the perspective of operations of the banks, the lemon theory postulates that it might result in adverse selection on the part of the customers as well as the directors of the bank. The adverse selection from the perspective of managers will lead to operational problems and eventually affect the performance of the banks.

2.2. Framework and hypothesis development

Ruziqa (Citation2013) examined the impact of credit and liquidity risk on financial performance of Indonesian Conventional Bank with total asset above 10 trillion Rupiah from 2007 to 2011. Performance measures employed in this study were return on asset (ROA), return on equity (ROE) and net interest margin (NIM). Credit risk management was measured by non-performing loan ratio (NPLR). The findings indicated that credit risk management has negative significant effect on ROA and ROE. Both credit risk management and liquidity ratio (LR) were found to have insignificant impact on NIM. Ruziqa (Citation2013) did not use the SEM which uses path analysis; hence, the author was not able to test credit risk against the latent profitability variables. In addition, Li and Zou (Citation2014) two proxies for credit risk and one proxy for credit risk management, that is the NPLR had a significant effect on both ROE and ROA while capital adequacy ratio (CAR) was insignificant in explaining both ROE and ROA.

To address the issue of not using more bank specific variables, the findings of Noman et al. (Citation2015) indicated a robust statistically significant negative effect of non-performing loans to gross loans (NPLGL) ratio and loan loss reserve to gross loans (LLRGL) ratio on all profitability indicators. Their result analysis also found a statistically significant negative effect of CAR on ROA. Additional analysis also proved that the effect of the implementation of Basel II is significantly positive on NIM but significantly negative on ROA. Kolapo, Ayeni, and Oke (Citation2012) also found a positive relationship between credit risk management and the profitability (ROA) of five Nigerian commercial banks from 2000 to 2010. The results showed that the effect of credit risk management on bank performance measured by the ROA of banks is cross-sectionally invariant.

In another study, Salah and Fedhila (Citation2012) established a negative association between credit risk and performance. Conversely, other researchers like Boahene, Dasah, and Agyei (Citation2012) established a positive relationship between credit risk management and profitability, measured by ROE of banks in Ghana between 2005 and 2009. This sample period even though improves on Amidu and Hinson (Citation2006), is related to the situation before the credit crunch in 2008 and the euro-zone crisis which subsequently had it’s real effect on the Ghanaian economy from 2012 to date. The study by Apanga et al. (Citation2016) was done post the global financial crises but the thrust of the study was the identification of the credit risk management practices and juxtaposing them with the recommendations in the Basel II accord. Nevertheless, these findings were not analysed in the context of the lemon theory through the SEM. From this backdrop, the first hypothesis is developed to guide the study.

Hypothesis 1: Credit risk positively influences the profitability of the universal banks in Ghana.

In discussing the effect of operational risk on profitability, Liu (Citation2003) used the SEM to test and verify the relationships among industry structure, business strategy and profitability. The evidence suggests that larger life insurance companies may adopt a conservative strategy of pursuing gradual growth in Taiwan. However, the conservative strategy generally has problems dealing with dynamic markets. Consequently, if a major change occurs in the investment environment, the larger scale insurers will suffer major losses. Chen, Chen, Chen, and Liao (Citation2009) having used the SEM approach in examining the effect of operational risk on profitability and choosing institution leverage and portfolio concentration as proxies for operational risk, found that operational risk exerts a negative and significant effect on profitability of the life insurance industry. Nair and Fissha (Citation2010), indicated the degree of loan delinquencies or impaired loans in a rural bank’s loan portfolio is often considered the best leading indicator for the operational efficiency and found an adverse relationship with performance. Therefore, this study develops the second hypothesis.

Hypothesis 2: Operational risk negatively influences the profitability of the Universal Banks in Ghana.

2.3. Indicators of variables used for the study

According to Ara, Bakaeva, and Sun (Citation2009), as cited in Li and Zou (Citation2014), the Basel Accord links the minimum regulatory capital requirement with the underlying risk exposure of banks, which implies that there is a correlation between the risk exposure of the banks and the amount of minimum capital requirement. This implies that the relevance of capital management in risk management and the compliance with the regulatory requirement cannot be overemphasized when discussing risk management indicators. From this backdrop, Brewer and Jackson (Citation2006), regards NPLR as a significant economic indicator of credit risk. The research of Boudriga, Taktak, and Jellouli (Citation2009), posit that CAR seems to reduce the level of problem loans which means higher CAR leads to less credit exposures.

However, the study by Goddard, Molyneux, and Wilson (Citation2004) on factors of profitability of banks in Europe, found a direct association between the CAR which was measured as bank capital and reserves to total assets (The World Bank, Citation2017) and profitability. Conclusively, the choice of CAR and NPLR as proxies for credit is based on their properties and frequency of occurrences in previous studies. CAR measures the amount of bank’s capital which is related to the amount of risk weighted credit exposure and also legalized in Basel regulation and must be an imperative factor in credit risk management. As for NPLR, it is relevant with bank loans. Bad loans have close relationship with banks credit risk and sway the efficiency of credit risk management. Thus, we consider it would be even-handed to use CAR and NPLR as indicators for credit risk.

Operational Risk (OR) is the risk of direct and indirect loss resulting from inadequate internal processes, people and systems or from external events. According to the Basel II accord, based on the level of sophistication of the activities of financial institution, their operational risk management systems and practices has the option of using the basic indicator approach; standardized approach and alternative standardized approach that is available to entities that demonstrate that the use of this measure produces a better and improved operational risk charge. Base on this premises, Jou (Citation1999); Liu (Citation2003); Chen et al. (Citation2009); Tafri, Hamid, Meera, and Omar (Citation2009); Gatsi, Gadzo, and Oduro (Citation2016); Gadzo and Asiamah (Citation2018); used bank leverage (BL) which was measured as the reserves divided by shareholders equity as an indicator of efficient management of operations and portfolio concentration as measures of operational risk. The justification is that a well-drawn operations of an entity necessitates an increase in the reserves which will eventually be on a higher side when expressed by the shareholders equity. According to Chen et al. (Citation2009), portfolio concentration is also involved to assess the role of regulatory supervision on operational risk and they found a positive relationship between them. Salas and Saurina (Citation2002) indicates the tendency of state-owned banks to take risker projects than to provide more favourable credits for small and medium firms, so that it will encourage the development of the economy. But such risk taking behaviour will lead to higher level of bank leverage.

The profitability variables adopted for the study were NIM and ROE. NIM measures the gap between what the bank pays savers and what the bank receives from borrowers. Thus, NIM focuses on the traditional borrowing and lending operations of the bank (Shen, Chen, Kao, & Yeh, Citation2009;Gatsi, Gadzo and Akoto Citation2014). NIM is also the difference between interest income generated (by banks) from loans and interest expense paid out to depositors, relative to average earning assets. It shows the profit a bank is making from its basic function, out of its average earning assets. Higher NIM convinces banks to give out more loans and hence, increase its credit and operational risk management levels. Studies that have employed NIM as a profitability measure include Heffernan and Fu (Citation2008), Nguyen (Citation2012), Lee, Hsieh, and Yang (Citation2014) and Noman et al. (Citation2015).The next profitability measure employed in this study is return on average equity (ROAE). Net Income refers to the net income after tax whiles average total equity is the capital contributed by the bank’s shareholders.

This measure is good at indicating efficiency of management and banks’ financial performance. It shows how competent management is using shareholders’ equity to generate net profit. According to Masood and Ashraf (Citation2012), this is measured as net profit/total equity. Gatsi et al. (Citation2016), further argued that ROE is the most important indicator of a firm’s financial performance and growth potential. It is the rate of return to shareholders or the percentage return on each cedi of equity invested in the bank. Banks specific variables such as asset quality (AQ), equity ratio (ER), cost to income ratio (CIR) and LR have been proven by literature to be effective as controlling variables when conducting a research on both credit risk and operational risk. The test of AQ on the financial performance of firms has been an area of constant research to establish if there exists any relationship between them. Gatsi, Anipa, Gadzo and Ameyibor (Citation2016) concluded that a firm that retains large investments in tangible assets will have smaller costs of financial distress than a firm that relies on intangible assets. Also Osuji and Odita (2012) found that AQ is a major determinant of firm’s performance. From the Ghanaian perspective, Gadzo and Asiamah (Citation2018) found a positive relationship between the financial performance of financial institutions and AQ.

According to Li and Zou (Citation2014), CIR also known as operating cost ratio may have a mixed effect on the financial performance. Li and Zou (Citation2014) posit that firms with higher operating cost ratio might use relatively higher revenue. This suggests a positive relationship between firm cost to income and financial performance. On the other hand, firms with more operating cost ratio may not be aligned to high retained earnings which imply a negative impact on its financial performance. Masood and Ashraf (Citation2012) argued that liquidity, equity to asset ratio, loan loss ratio, cost of income ratio, deposits structure, assets structure and expenditure item are statistically relevant variables to be used as controlling variables in studies with banks. In order to assess the relationship between performance and internal bank characteristics, Chen et al. (Citation2009), utilized several bank ratios namely fund source management, equity to asset ratio, loan loss ratio, cost of income ratio and found a positive impact on financial performance. This study chooses the observed variables for each latent variable based on the studies mentioned above. However, due to the dynamic nature of the banking sector, market conditions clearly are continually changing. To avoid obtaining incorrect results in this research model, this study adds the bank specific variables as latent variable into the model as a control variable.

3. Theoretical model

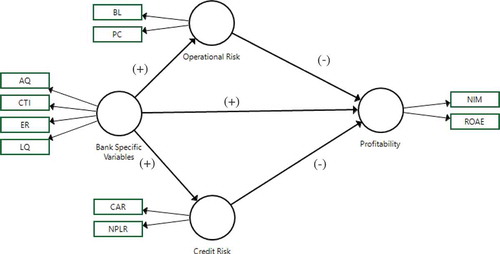

The theoretical model (original model) includes an exogenous latent variable and three endogenous latent variables. From Table , the exogenous latent variable is a bank specific variables reflected by three observed variables. The bank specific latent variable includes AQ, CIR, ER and liquidity (LQ). The model employs three endogenous latent variables, including operational risk, credit risk (n2) and profitability (n3) as demostrated in Table . Operational risk is reflected by bank leverage (y1), portfolio concentration (y2); meanwhile, credit risk is reflected by NPL rate (y3) and CAR (y4); finally profitability is reflected by NIM (y5) and ROAE (y6). Therefore the theoretical model is shown in Figure .

Figure 1. Theoretical model.

Source: Authors construct (2018).

Following the literature reviewed, it is expected that credit risk which is measured by CAR and NPLR is to be influenced positively by the bank specific variables while credit risk in turn affects profitability negatively. Operational risk which is measured by bank leverage and portfolio concentration is influenced by the bank specific variables positively and in turn has an adverse relation with profitability.

4. Empirical methodology

4.1. Research approach and design

The research design employed in this study was an explanatory study also called a “causal research design”. In such studies, the researcher is faced with “cause-and-effect” problems with the major task for the researcher being the separation of such causes. The explanatory study was deemed most suitable for our topic because the ultimate aim of the study is to test how credit risk and operational risk could influence profitability of universal banks

4.2. Data

Data for the empirical analysis were obtained from the annual report of the universal banks in Ghana and the Pwc Banking annual banking survey for universal banks in Ghana. The study observed the universal banks in Ghana from 2007 to 2016. To minimise the possibility of biased results, only firms for which data are available throughout the sample period are included. After deleting missing values and incomplete data, the sample includes a total of 24 banks out of the possible 29 banks. 3 of the banks out of the 29 had issues with the regulatory body so they were not included in the analysis. Furthermore, 2 were not having complete data for the study period.

4.3. Structural equation modelling

SEMs offer litheness for testing such models, allowing one to use multiple predictors and criterion variables, construct latent (unobservable) variables, model errors in measurement for observed variables, and test mediation and moderation relationships in a single model (Bentler & Huang, Citation2014; Bisbe & Malagueño, Citation2015; Hair, Sarstedt, Pieper, Ringle, & Mena, Citation2012; Nitzl, Citation2016). SEM covers all the reflective indicators in one construct. The two types of SEM are the Covariance-based structural equation modelling (CB-SEM) and partial least squares structural equations modelling (PLS-SEM) used in research. On account of theoretical and methodological issues, there had been an increase in use of PLS-SEM compared to that of CB-SEM (Hair, Sarstedt, Ringle, & Mena, Citation2012; Ringle, Wende & Becker, Citation2015). According to Kumar and Sujit (Citation2018), variance which predicts construct relationship is explained effectively by PLS-SEM and this method emphasizes on maximizing the explained variance of the endogenous latent variables instead of replicating the theoretical covariance matrix. PLS-SEM methodology becomes very useful to conduct predictive analysis with highly complex data. This methodology estimates latent variables through composites, which are exact linear combinations of the indicators assigned to the latent variables (Nitzl, Citation2016).

From this backdrop, the partial least-squares structural equation modelling methodology (PLS-SEM) was employed to examine the effect of operational risk and credit risk on the profitability of universal banks in Ghana. The PLS-SEM methodology was adopted based on the assumption that the profitability, operational and credit risk are often latent which cannot be observed directly because using ratios, profitability cannot be measured directly unless more than one profitability ratio is used. Credit risk and operational risk on the other hand are measured using more than one variable. Based on this premises, profitability, credit risk and operational risk are all latent variables. We use the Smart-PLS software to apply PLS-SEM as this technique effectively handles nonlinear relationships.

5. PLS- SEM results

As a first step in PLS-SEM, missing data imputation is carried out by Stochastic Multiple Regression Imputation algorithm. The latent constructs consist of reflective measurement scale which are interchangeable and must be highly correlated. In the initial assessment of the model, the loadings of all the variable indicators in the constructs is used for scale purification. Any indicator which has less than 0.5 loading is dropped from the model. This means that the indicator is different from the rest and must be dropped.

6. Internal consistency reliability assessment

Traditionally, the “Cronbach’s alpha” is used to measure internal consistency reliability but it tends to provide a conservative measurement in PLS-SEM. According to Hair et al. (Citation2012), prior literature has suggested the use of composite reliability as a replacement.

From this backdrop, the study reported the composite reliability in Table . The satisfactory range for composite reliability values are 0.60 to 0.70 in exploratory research and 0.70 to 0.90 in more advanced stages of research. As shown in Table , the composite reliability score of all the latent construct are in the range 0.797 to 0.947 indicating that the latent variables are reliable. since the construct qualify composite reliability test along with the criteria of average variance extracted (AVE) value is greater than 0.5, the latent variables are retained in the model. Again, Table shows the indicator reliability which is basically the squares of the loading. It can be seen that all the indicators reliability values are much larger than the minimum acceptable level of 0.4 and close to the preferred level of 0.7.

Table 1. Measurement of variables

Table 2. Reliability and validity of latent construct

7. Convergent validity

According to Wong (2013), it is relevant to check the construct validity of each variable AVE. If all the AVEs are greater than the threshold of 0.5 the convergent validity is confirmed. From Table , all the AVEs are more than 0.5 so the convergent validity is confirmed.

8. Discriminant validity

Hair et al. (Citation2012) as sited in Kumar and Sujit (Citation2018) argued that discriminant validity certifies that a construct measure is empirically distinctive and represents facts of interest that other measures in an SEM do not capture.

Table shows the Fornell–Larcker criterion which suggests that the square root of AVE must be greater than the correlation of the construct with all other constructs in the structural model. Table shows the correlations among latent variables with square root of AVE by each latent variable. It can be seen that each latent variable AVEs is higher than the correlation of the latent variables indicating discriminant validity of the latent variables.

Table 3. Correlation among latent variables with square roots of AVEs

9. Correlation matrix

The correlation matrix is presented to assess the extent of correlation among the variables and examine the likelihood of multi-collinearity among the regressors. It also establishes whether there is a positive or negative relationship between dependent variables and the independent variables. This is vital as it shows whether there is any relationship between the indicators of credit risk, operational risk and profitability.

The result in Table indicates that the extents of correlation among the regressors were minimal and there is no presence of multicollinearity. The results also shows that there is a significantly negative association between all the credit risk variables as well as operational risk variables and ROAE which is one of the profitability indicators. The association between the NIM and operational risk variables also indicated a negative relationship.

Table 4. Correlation matrix

10. Results of the measurement model of PLS-SEM

To ensure the robustness of the relationship between the latent variables, many schemes are used to estimate the Path coefficient of the measurement model. According to Kock (2014) as cited in Kumar and Sujit (Citation2018), this stable method relies directly on the application of exponential smoothing formulas and yield estimates of the actual standard errors that are consistent with those obtained through bootstrapping.

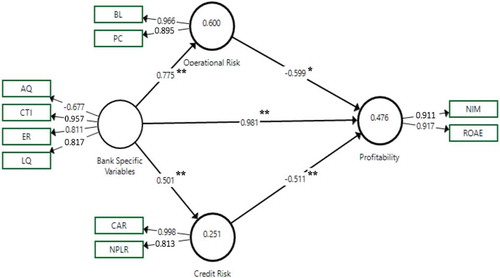

This method has proven to yield more precise estimates of the actual standard errors when the linear models are tested using PLS regression and robust path analysis. In Figure however, the significance and the R2 are presented. The model wise dependent latent variable R2 showed that both credit risk and operational risk explains 47.6 percent of the profitability of the universal banks in Ghana. On the other hand, the bank specific variables explains 60 percent of operational risk and 25.1 percent of credit risk. This means that the chosen bank specific variables explains operational risk much better than credit risk.

Figure 2. Result of linear bootstrapping path coefficient.

**Indicates significant at 5% level of significance, i.e. p = <0.05.*Indicates significant at 10% level of significance, i.e. p = <0.10

11. Discussion of results

This section presents the discussion and analysis of the findings in Figure and Table . From the structural path significance in bootstrapping in Table , credit risk had a statistically significant negative relationship with the profitability of the universal banks. The coefficient of −0.511 and p-value of 0.026 (p < 0.05) show that the negative relationship is statistically significant. This implies that universal banks that are exposed to high credit risk experiences lower financial performance. Using the proxies for credit risk (CAR and NPLR) to explain this outcome, it can be seen that based on the measurement of CAR, when CAR is high, it means that the banks’ total capital and reserves are bigger than their total asset.

Table 5. Structural path significance in bootstrapping

From this backdrop, a higher capital and reserves as against total asset means the banks have less assets which can be transformed in to products for the customers of the banks. In the long run, universal banks will possess less assets to be used to create interest income and will lead to their inability to boost financial performance. With respect to the NPL rate, a higher NPLR implies that less is recouped for any credit extended to customers, the culminating effects is the erosion of the assets of the banks. The results also posit that anytime both NPLR and CAR are high, the credit risk exposure of the universal banks increase and eventually leads to low levels of profit. Analysing this from the information asymmetry tenants of the lemon theory, it presupposes that anytime there is information asymmetry between the loan provider (the universal banks) and the customers seeking the loan, it is likely to result into a high NPL rate. Furthermore, it can be deduced that with a low-quality collateral to redeem the debts, the long run effect is the banks losing assets and interest incomes.

In addition, whenever the CAR of the banks falls below the regulatory threshold of 10% as stipulated by the Bank of Ghana, the universal banks are left with less funds to lend to customers to attract the necessary interest income which will boost their financial performance. Comparing the results to empirical literature, this study is not consistent with the findings of Boahene et al. (Citation2012), Kolapo et al. (Citation2012), and Apanga et al. (Citation2016) whose outcome found a positive relationship between financial performance and credit risk. This is because each of these studies used one proxy for credit risk and another proxy for profitability and also did not perform a path analysis with the bank specific variable which were used in the current study. The findings from this study further give credence to the use of SEM in analysis of studies of this nature. From this backdrop, the first hypothesis which stated that “H1 Credit risk positively influences the profitability of the universal Banks in Ghana” is rejected on the grounds that credit risk had a statistically significant negative influence on the universal banks of Ghana. Therefore, the current study does not conform to other empirical works done in the context of Ghana. The possible reason is the structural model methodological approach which used latent variables for the analysis instead of the single measurement variables used by previous studies.

Again, from Table and Figure , operational risk which was measured by bank leverage and portfolio concentration showed a statistically significant negative relationship with financial performance. This denotes that an increase in the operational risk of the universal banks leads to a fall in their financial performance. Analysing this result from the latent variables of operational risk, it can be deduced that a high bank leverage stems from the losses resulting from inadequate systems. This comes with the obligation of paying more in terms of interest payment on the part of the banks. Payment of debt obligations reduces the inflows of the bank which affect the financial performance adversely. From the portfolio concentration perspective, inefficiencies in the processes in addition to information asymmetry results in adverse selection of investment portfolio. Also, when there is a distortion in communication between management and shareholders of the banks, the resultant effect is an adverse selection of leverage policies. A continuous occurrences of this phenomena according to Gadzo and Asiamah (Citation2018), leads to a highly leveraged bank and eventually results in erosion of net interest income of the banks.

This findings is consistent with the studies by Chen et al. (Citation2009) and Nair and Fissha (Citation2010) whose study indicated a negative relationship between operational risk and financial performance. In addressing Hypothesis 2 which stated that “Operational risk negatively influences the profitability of the Universal Banks in Ghana.” The hypothesis is not rejected because the study established a negative (−0.599) influence of operational risk on the profitability with a p-value of 0.083 and since the p < 0.1. Table , also indicated that the bank specific variables which were measured by liquidity, ER, CIR and AQ significantly influence both operational risk and credit risk positively. In that, these variables moderate how both credit and operational risk affect the profitability of the banks.

This infers that a highly liquid bank with large ER; AQ and CIR is likely to increase both operational risk and credit risk of the banks and has a high probability of affecting their profitability adversely. In relation to the direct relationship between the bank specific variables and profitability the study recorded a statistically positive relationship with a p value of 0.053. This finding shows that banks with higher AQ has a higher possibility of experiencing an enhanced profitability and vice versa. This is because, a high AQ means high level of technology to compete with competitors in the industry and this will eventually result to an increase in net interest income if the bank is able to outwit the giants in the industry.

12. Conclusions

The study concludes that credit risk influences profitability negatively contrary to the hypotheses of a positive influence from the reviewed literature. Consequently, its findings are not in consensus with the numerous empirical works which have concluded that bank performance is positively related to credit risk but in line with the lemon theory, information asymmetry leads to more NPLs which negatively influence the profitability of the universal banks. Results from the study also disclosed that operational risk of banks have significant negative effect on the profitability of Universal Banks in Ghana. This suggests that as banks increase their operational risk exposure and the amount of profit levels dwindles. Furthermore, the study results indicated that banks’ specific variables measured by (AQ, bank leverage, CIR and liquidity) significantly positively influence credit risk, operational risk as well as the profitability of the universal banks. In other words, the more efficient and larger a bank is, the more profits it makes.

13. Recommendations

Based on the results of the study, it is crucial that banks implement efficient credit risk and operational risk management measures in place to safeguard the financial performance of the banks. This will not only safeguard the assets of the banks and protect investors’ interests but also inure to the benefit of individuals, business entities and the entire economy at large. Regulators should also set policies that will strengthen the banking industry particularly policies that bothers around risk management in the banking sector. When potential customers have access to a range of portfolio, they are able to compare returns of the various portfolios and assess the security of their investment among the banks and the securities market operators. This tends to have a positive impact on the general development of the banking sector by increasing competitiveness in the financial sector as banks are pressurized to improve their financial soundness. On the negative association between profitability and credit risk management, it is proposed that banks be encouraged to cut down their lending rates cautiously so that more clients can access loans which in turn decrease credit risk and subsequently boost profitability further as the industry is already doing well in terms of profitability. The banks could also divert funds available for fee-generating activities into loan-generating activities. Nonetheless, borrowers should pay the full interest plus principal on time to ensure profitability as anticipated, is attained. Regarding operational risk, where a negative relationship was found between operational risk and profitability, it is recommended that banks reduce leverage and have their portfolio more concentrated on investment income so as to boost profitability. Regarding the positive relationship between efficiency and profitability, banks are urged to reduce their operating cost as compared to their operating income so as to improve profitability.

Additional information

Funding

Notes on contributors

Samuel Gameli Gadzo

Samuel Gameli Gadzo is a Lecturer at the Department of Banking and Finance, University of Education Winneba, Ghana. He is also a member of the Institute of Chartered Accountants (Ghana). His research interest focuses on degree of leverage, corporate banking and finance, taxation and fiscal policy and corporate and financial markets governance.

Holy Kwabla Kportorgbi

Holy Kwabla Kportorgbi is a Chartered Accountant and a lecturer at GIMPA Business School Accra, Ghana. He is a member of the Institute of Chartered Accountants (Ghana). His research interest concentrates taxation and fiscal policy, financial reporting, auditing and assurance, management accounting and corporate governance.

John Gartchie Gatsi

John Gartchie Gatsi (PhD) is a professor of Finance in the department of Finance, University of Cape Coast, Ghana. He is currently, the head of the department of Finance, University of Cape Coast. His research interests include corporate social responsibility, corporate and financial markets governance, capital structure, and oil and gas management.

Related Research Data

References

- Ahmed, E., Rahman, Z., & Ahmed, R. I. (2006). Comparative analysis of loan recovery among nationalized, private and Islamic commercial banks of Bangladesh. BRAC University Journal, 3(1), 35–16.

- Akerlof, G. A. (1970). The market of lemons: Quality uncertainty and market mechanism. The Quarterly Journal of Economics, 84(3), 488–500.

- Amidu, M., & Hinson, R. (2006). Credit risk management, capital structure and lending decisions of Banks in Ghana. Banks and Bank Systems, 1(1), 93–101.

- Anaman, E. A., Gadzo, S. G., Gatsi, J. G., & Pobbi, M. (2017). Fiscal aggregates, government borrowing and economic growth in Ghana: An error correction approach. Advances in Management & Applied Economics, 7(2), 83–104.

- Andersen, L. B., Hager, D., Maberg, S., Naess, B., & Tungland, M. (2012). The financial crisis in an operational risk management context: A Review of causes and influencing factors. Reliability Engineering and System Safety, 105, 3–12.

- Apanga, M. A., Appiah, K. O., & Arthur, J. (2016). Credit risk management of Ghanaian listed banks. International Journal of Law and Management, 58(2), 162–178.

- Ara, H., Bakaeva, M., & Sun, J. (2009). Credit risk management and Profitability in Commercial Banks in Sweden (Master thesis). University of Gothenburg. Retrieved from https://gupea.ub.gu.se/bitstream/2077/20857/1/gupea_2077_20857_1.pdf

- Bank of Ghana. (2017). Summary of economic and financial data. Retrieved from https://www.bog.gov.gh/Monetary-policy/press_releases/2851-mpc-press-release-jan-2017

- Basel Committee Banking Supervision. (2016). Consultative document on standardized measurement approach for operational risk. Retrieved from https://www.bis.org/bcbs/publ/d355.pdf.

- Basel Committee on Banking Supervision (BCBS). (2006). Basel II: International convergence of capital measurement and capital standards: A Revised Framework—Comprehensive Version. Retrieved from http://www.bis.org/publ/bcbs128.htm

- Bentler, P. M., & Huang, W. (2014). On components, latent variables, PLS and simple methods: Reactions to ridgon’s rethinking of PLS. Long Range Planning, 47(3), 138–154.

- Bisbe, J., & Malagueño, R. (2015). How control systems influence product innovation process: The role of entrepreneurial orientation. Accounting and Business Research, 45(3), 356–386.

- Boahene, S. H., Dasah, J., & Agyei, S. K. (2012). Credit risk management and profitability of selected banks in Ghana. Research Journal of Finance and Accounting, 3(7), 6–14.

- Bofondi, M., & Gobbi, G. (2003). Bad loans and entry in local credit markets. Rome, Bank of Italy. Research Department.

- Boudriga, A., Taktak, N. B., & Jellouli, S. (2009). Banking supervision and non- performing loans: A cross-country analysis. Journal of Financial Economic Policy, 1(4), 286–318.

- Brewer, E., III, & Jackson, W. E., III. (2006). A note on the “risk-adjusted” price–Concentration relationship in banking. Journal of Banking & Finance, 30(3), 1041–1054.

- Cagan, P. (2009). Managing operational risk through the credit crisis. The Journal of Compliance, Risk & Opportunity, 3(2), 19–26.

- Chen, J., Chen, M., Chen, T., & Liao, W. (2009). Influence of capital structure and operational risk on profitability of life insurance industry in Taiwa. Journal of Modelling in Management, 4(1), 7–18.

- Corcoran, C. (2010). A reassessment of regulated bank capital on profitability and risk. International Business & Economics Research Journal, 9(3), 97–100.

- Derban, Y., Binner, G., & Mullineux, A. (2005). Loan repayment performance in community development finance institutions in the UK. Small Business Economics, 25, 319–332.

- Drehmann, M., Sorensen, S. & Stringa, M. (2008). The integrated impact of credit and interest rate risk on banks: An economic value and capital adequacy perspective. Bank of England working papers 339, Bank of England. Gadzo, S. G., & Asiamah, S. K. (2018). Assessment of the relationship between leverage and performance: An empirical study of unlisted banks in Ghana. Journal of Economics and International Finance, 10(10), 123–133.

- Gatsi, J. G., Anipa, A. A., Gadzo, S. G., & Ameyibor, J. (2016). Corporate social responsibility, risk factor and financial performance of listed firms in Ghana. Journal of Applied Finance & Banking, 6(2), 21–38.

- Gatsi, J. G., Gadzo, G. S., & Akoto, R. (2014). Post-Merger analysis of the financial performance of SG-SSB. International Journal of Financial Economics, 3(2), 80–91.

- Gatsi, J. G., Gadzo, S. G., & Oduro, R. (2016). Degree of leverage and risk adjusted performance of listed financial institutions in Ghana. Journal of Business and Management, 18(1), 44–50.

- Ghana Banking Survey. (2017). Retrieved from http://www.pwc.com/en_GH/gh/pdf/ghana-banking-survey-2017- pwc.pdf.

- Goddard, J., Molyneux, P., & Wilson, J. O. (2004). The profitability of European banks: A cross-sectional and dynamic panel analysis. The Manchester School, 72(3), 363–381.

- Hair, J., Sarstedt, M., Ringle, C., & Mena, J. (2012). An assessment of the use of partial least squares structural equation modelling in marketing research. Journal of the Academy of Marketing, 40, 414–433.

- Hair, J. F., Sarstedt, M., Pieper, T., Ringle, C. M., & Mena, J. A. (2012). The use of partial least squares structural equation modelling in strategic management research: A review of past practices and recommendations for future applications. Long Range Planning, 45(5–6), 320–340.

- Heffernan, S., & Fu, M. (2008). The determinants of bank performance in China. Journal of Banking and Finance, 2(1), 1–30.

- Hess, C. (2011). The impact of the financial crisis on operational risk in the financial services industry: Empirical evidence. The Journal of Operational Risk, 6(1), 23–35.

- Hosna, A., Bakaeya, M., & Juanjuan, S. (2009). Credit risk management and profitability in commercial banks in Sweden. Master Degree Project 2009:36, School of Business, Economics and Law: University of Gothenburg.

- Hsieh, M. F., & Lee, C. (2010). The puzzle between banking competition and profitability can be solved: International Evidence from Bank-level Data. Journal of Financial Services Research, 38, 135–157.

- Jayadey, M. (2013). Basel III implementation: Issues and challanges for Indian banks. IIMB Management Review, 25(2), 115-130.

- Jou, D. G. (1999). Interest rate risk, surplus, leverage and market reward-an empirical study of Taiwan life insurance industry. Journal of Management & Systems, 6(3), 281–300.

- Kargi, S. H. (2011). Credit risk and the performance of Nigerian banks. Published thesis, Department of Accouting, Ahmadu Bello University, Zaira Nigeria.

- Kargi, S. H. (2014). Credit risk management and the performance of Nigerian banks. ACME Journal of Accounting, Economics and Finance, 1(1), 7–14.

- Kirpatrick, G. (2009). The corporate governance lessons from the financial crisis. Financial Market Trends, (1), 61-87.

- Kock, N. (2014). A note on how to conduct a factor- based PLS-SEM analysis. Laredo, TX: ScriptWrap Systems.

- Kolapo, T. F., Ayeni, R. K., & Oke, M. O. (2012). Credit risk management and commercial banks’ performance in Nigeria: A panel model approach. Australian Journal of Business and Management Research, 2(2), 31–38.

- Kumar, B. R., & Sujit, K. S. (2018). Determinants of dividends among Indian firms - An empirical study. Cogent Economics & Finance, 6(1), 1423895.

- Lee, C., Hsieh, M. F., & Yang, S. J. (2014). The relationship between revenue diversification and bank performance: Do financial structures and financial reforms matter? Japan and the World Economy, 29, 18–35.

- Li, F., & Zou, Y.(2014). The impact of credit risk management on Profitability of Commercial Banks: A Study of Europe. Published Thesis by Umeå School of Business and Economics, Sweden.

- Liu, Y. M. (2003). The Effect of Industrial Structure on Business Strategy and Profitability for Life Insurance in Taiwan ( Unpublished Master Thesis). Taichung, Taiwan: Department of Insurance, Chaoyang University of Technology.

- Masood, O., & Ashraf, M. (2012). Bank-specific and macroeconomic profitability determinants of Islamic banks: The case of different countries. Qualitative Research in Financial Markets, 4(2/3), 255–268.

- Muriithi, M. S. (2017). African small and medium enterprises (SMEs) contribution, challanges and solutions. European Journal of Research and Reflection in Management Sciences, 5(1), 36-48.

- Nair, A., & Fissha, A. (2010). Rural Banking: The case of rural and community banks in Ghana, agricultural and rural development. Discussion Paper No. 48, The World Bank, Washington, DC.

- Nguyen, J. (2012). The relationship between net interest margin and non-interest income using a system estimation approach. Journal of Banking and Finance, 36(9), 2429–2437.

- Nitzl, C. (2016). The use of partial least squares structural equation modelling (PLS-SEM) in management accounting research: Directions for future theory development. Journal of Accounting Literature, 37, 19–35.

- Noman, H. M., Pervin, S., Chowdhury, M. M., & Banna, H. (2015). The effect of credit risk management on the banking profitability: A case on Bangladesh. Global Journal of Management and Business Research, 15(3), 41–48.

- Osuji, C. C., & Odita, A. (2012). Impact of capital structure on financial performance of Nigerian firms. Arabian Journal of Business and Management Review, 1(12), 43-61.

- Ouamar, D. (2013). How to implement counterparty credit risk requirements under Basel III: The challenges. Journal of Risk Management in Financial Institutions, 6(3), 327-336.

- Psillaki, M., Tsolas, L. & Margaritis, D. (2010). Evaluation of credit risk based on firm performance. European Journal of Operational Research, Elseviar, 201(3), 873-881.

- Ringle, C. M., Wende, S., & Becker, J.-M. (2015). SmartPLS 3. Boenningstedt: SmartPLS GmbH.

- Rose, C. (2009). New challenges for operational risk after the financial crisis. Journal of Applied IT and Investment Management, 1(1), 27–30.

- Ruziqa, A. (2013). The impact of credit and liquidity risk on bank financial performance: The case of Indonesian Conventional Bank with total asset above 10 trillion Rupiah. International Journal of Economic Policy in Emerging Economies, 6(2), 93–106.

- Salah, N. B., & Fedhila, H. (2012). Effects of securitization on credit risk management and banking stability: Empirical evidence from American Commercial Banks. International Journal of Economics and Finance, 4(5), 194–207.

- Salas, V., & Saurina, J. (2002). Credit risk management in two institutional regimes: Spanish commercial and savings banks. The Journal of Financial Services Research, 22(3), 203–224.

- Saunders, A., & Cornett, M. M. (2006). Financial institutions management a risk management approach. New York, NY: McGraw-Hill.

- Shen, C. H., Chen, Y. K., Kao, L. F., & Yeh, C. Y. (2009, June). Bank liquidity risk and performance. 17th Conference on the Theories and Practices of Securities and Financial Markets, Hsi-Tze Bay. Taiwan: Kaohsiung.

- Tafri, F. H., Hamid, Z., Meera, A., & Omar, M. A. (2009). The impact of financial risks on profitability of Malaysian commercial banks: 1996-2005. International Journal of Social and Human Sciences, 3(3), 807–821.

- The World Bank. (2017). Bank capital to assets ratio (%) | Data | Table. [online]. Retrieved from http://data.worldbank.org/indicator/FB.BNK.CAPA.ZS

- Tupangiu, L. (2017). Information asymmetry and credit risk. Finance: Challenges of the Future, 1(19), 153–157.

- Wong, K. K. (2013). Partial Least Squared Structural Equation Modelling (PLS-SEM) Techniques using SmartPLS. Marketing Bulletin, 24(1), 1-32.