?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Like most of International Institutions, the Central Bank of West African States (BCEAO) considers universal access to finance as key to empowering disadvantaged people. Fitting into that context, this study aims to assess the accelerating role of digital technologies using mobile phone penetration and internet usage as broad indicators, on the dynamics of financial inclusion in WAEMU. Using data from the Central Bank of West African States (BCEAO) and the International Telecommunication Union (ITU) over the periods 2006–2017, we estimated first a random effect model and thereafter a system GMM devised by Arrelano-Bover/Bundell-Bond, to correct the endogeneity issue raised from the static model. Findings show that beyond the specific effects of mobile phone penetration and Internet usage, the joint use of these two technologies is very key to financial inclusion in the WAEMU countries. It urges then for policy makers to take steps toward the availability, accessibility, affordability and to design flexible legislation pertaining to mobile financial services providers in order to accelerate financial inclusion in that region.

PUBLIC INTEREST STATEMENT

This article investigates the dynamics of financial inclusion in the West African Economic and Monetary Union (WAEMU) countries. Data from 08 countries over the periods 2006–2017 were collected and analysed using the Generalized Method of Moments (GMM). There was evidence to show that financial inclusion proxied by the Global Rate of Financial Services Utilization (GRFSU) responds positively and significantly to the joint utilization of mobile phones and internet. It urges then for policy makers to take steps toward the availability, accessibility, affordability and to design flexible legislation pertaining to mobile financial services providers in order to accelerate financial inclusion and alleviate poverty in that region.

1. Introduction

Financial development including financial inclusion is becoming increasingly part of the top priority agenda of most international organizations. In fact, the United Nations (UN) has made financial inclusion a priority issue for economic development by 2020. In the same vein, the World Bank has made universal access to finance a central pillar of the global fight against poverty (World Bank, Citation2015). For the G20, policies that promote the expansion of banking services can be a major tool for financial inclusion by facilitating access to deposit, credit and payment services (Busch, Koetter, Krause, & Tonzer, Citation2017). Similarly, the 2017’s Financial Inclusion Action Plan (FIAP) reaffirmed the G20’s commitment to advancing financial inclusion for the benefit of all disadvantaged people (GPFI, Citation2017). According to the Financial Inclusion Alliance (FIA), access to financial services is a basic principle for financial inclusion (Financial Inclusion Alliance [FIA], Citation2018). In the same vein, the Central Bank of West African States has set a target of 75% of adults to be financially included by 2020 (BCEAO, Citation2017). Consequently, it has been implemented several reforms to boost financial inclusion in that region. These reforms consisted of providing infrastructure conducive to banking activity, supporting the activities of microfinance institutions and developing electronic money (BCEAO, Citation2017). However, while about two billion people worldwide still lack access to formal financial services (Demirgüç-Kunt, Klapper, Singer, & Hess, Citation2017), most of the financially excluded people hold a mobile phone as an asset (GSMA, Citation2017). Information and Communication Technologies (ICT) including smartphones and broadband internet are therefore very important for developing access to secure and affordable financial services such as payments, domestic and international transfers, insurance, credit and savings (Alliance for Financial Inclusion [AFI], Citation2018; Patwardhan, Singleton, & Schmitz, Citation2018). To this end, JIM KIM, the president of the World Bank had issued a call for action toward universal financial inclusion by 2020 (UFA2020) especially through the issuance of bank cards and mobile money. This must involve public and private stakeholder to provide technologies to last miles at an affordable price. Similarly, Bill & Melinda Gates Foundation (Citation2015), stated that two billion of financially excluded people will access financial services and make payments via mobile phone. In addition, several empirical studies have highlighted the accelerating role of digital technologies in financial inclusion. In fact, according to Morawczynski (Citation2009), the mobile finance increases savings and especially the financial empowerment of women. Similarly, Klein and Mayer (Citation2011) argue that mobile banking services provide an electronic payment register to the financially excluded people who otherwise preferred cash transactions. Digital financial inclusion can make a difference for underserved low-income households, as well as for small and medium enterprises (SMEs). Digital financial services can make life easier for clients by allowing them to make small transactions and better manage their expenditures and incomes. Financial services including payment, transfer, savings, and credit provided by the digital transaction platform as well as data collected on the users of those services can enable providers to offer additional financial services tailored to the needs of their customers. Moreover, digital financial inclusion can also reduce the risk of loss, costs, theft or other financial crimes pertaining to cash transactions (GSMA, Citation2017).

However, considering the WAEMU countries, characterized by low financial inclusion and high mobile telephony penetration through the extension of mobile phone network over rural areas (GSMA, Citation2018; Senou, Ouattara, & Acclassato Houensou, Citation2019), digital finance appears to be the ultimate solution to financial and social exclusion. Specifically, mobile money is a powerful tool for integrating disadvantaged into the formal financial sector (GSMA, Citation2015). Yet, according to BCEAO (Citation2018), 21.9 million WAEMU individuals have an electronic financial account compared to 11 million in 2013. In addition, from 2.6 million bank accounts in 2006, there were about 7.8 million in 2014, while e-money rose dramatically from 366,000 in 2010 to 16 million in 2014. The number of electronic money service points improved from zero points of service in 2009 to 24,300 points of service in 2014 (BCEAO, Citation2016). However, despite this positive trend in digital finance, financial inclusion in WAEMU compared to other regions remains very low to achieve the Sustainable Development Goals. This study aims then to assess the impact of financial services enabled by digital technologies on financial inclusion in WAEMU.

Findings of this study show that the advent of digital technology has contributed significantly to financial inclusion in WAEMU. In addition, the dynamics of financial inclusion differ across countries and the effect of mobile phones and Internet users on financial inclusion is perceived differently from one country to another. It stands out that the availability of the Internet on mobile phones promotes greater financial inclusion than the mobile phone per se. Therefore, beyond the traditional financial services provided by digital technologies including payment, savings, credit, mobile technologies are well designed to offer last generations’ financial services.

The rest of the article is organized as follows: Section 2 presents the state of financial inclusion in the WAEMU countries. Section 3 summarizes the related literature, while the methodology and data are presented in Section 4. We conclude this study with a concluding remark and some policy recommendation in Section 5.

2. State of financial inclusion in WAEMU

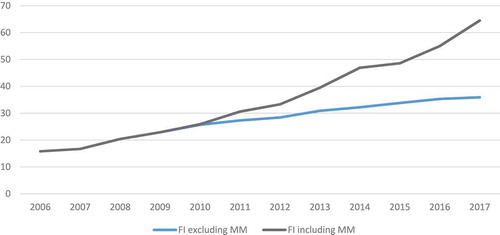

The financial ecosystem of WAEMU is characterized by a diversity of stakeholder including among other banks, microfinance institutions (MFIs) and Mobile Network Operators (MNOs). Indeed, like bank and microfinance institutions, mobile network operators are increasingly entering the financial market by reaping the benefit of their infrastructure potential to offer financial services. This helps fill the financial services gaps left by financial institutions. In fact, the banking sector has been developing these last decades with about 144 financial institutions including 126 banks and 18 credit institutions in WAEMU. In addition, nearly 600 microfinance institutions and 38 mobile phone-enabled financial services have been numbered (BCEAO, 2018). Yet, postal financial services, as well as rapid transfers’ institutions, are enriching the financial landscape of WAEMU. Figure displays the dynamics of financial inclusion in terms of Broad Banking Penetration Rate (BBPR) and Global Rate of Financial Services Utilization (GRFSU) in WAEMU.

Figure 1. Financial inclusion dynamics in WAEMU.

In fact, the Broad Banking Penetration Rate measures the percentage of adult people holding an account at bank, postal services, National Savings Fund, national treasure as well as at microfinance Institutions. However, the advent of mobile money in 2008 in most of the WEAMU countries has changed the magnitude of the financial inclusion. The Financial Inclusion appears then as an extension of the Broad Banking Penetration Rate to the percentage of the adult population holding an electronic account especially mobile banking and mobile money account. From 15.8% in 2006, the broad Banking Penetration Rate increased to 35.9% in 2017 whilst the Global Rate of Financial Services Utilization increased to 64.5% over the same period. It results then a gap of 28.6% filled by mobile financial services. It is obvious that the advent of electronic money and especially mobile banking and mobile money in WAEMU has contributed significantly to the expansion of financial services to last miles. According to the 2018’s report by the Central Bank of the WAEMU’s States, in 2017, the most performed country in WAEMU as far as Broad banking penetration (BBPR) and the Global Rate of Financial Services Utilization (GRFSU) are concerned was Benin. With 27.2% for BBPR and 82,1% for GRFSU rate in 2017, Benin is followed by Togo with 24.3% and 79.6%, Burkina Faso with 22.2% and 68.8%, Senegal with 19.6% and 64.1%, Ivory Cost with 16.6% and 60.7%. These statistics are very striking because of the reverse trend witnessed by the usual leading countries such as Ivory Coast and Senegal. However, experts argued that there is a number of strategies designed and implemented by the government of Benin in terms of expanding financial access to the disadvantaged people (BCEAO, Citation2017). They also argued that Benin has a higher ratio of point of services (POS) in WAEMU. With 371 POS for 1000 Km squares, it is followed by Togo and Senegal with, respectively, 265 and 206 POS for 1000 Km squares. Niger is lagged behind with nearly 17 POS for 1000 Km squares (BCEAO, Citation2017).

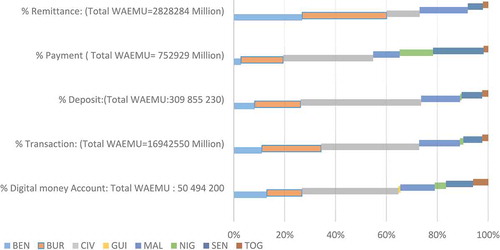

However, taking into account the socioeconomics characteristics, the above trend changes consistently. The disparity between countries may reveal the specificities of legal, sociological, cultural or religious norms or may even result from income or education gap between these countries. Indeed, out of 50,494,200 electronic money accounts, Côte d’Ivoire alone accounts for 37.92%, followed by Burkina Faso, Mali, Benin and Senegal, which each detains more than 13% of electronic money subscribers in WAEMU. However, Bissau Guinea has the lowest rate in WAEMU with less than 0.74% of electronic money account holders (Figure ).

Figure 2. Mobile financial services in WAEMU.

In addition, beyond the adoption of banking and electronic financial services, the financial inclusion can also be measured through the utilization of financial services (Figure ). Thus, the simple increase in the banking penetration of adults’ populations leads to an effective inclusion if and only if the financial account holders use them for savings, payment, and transfer as well as for credit purposes. From Figure , it appears that the total amount of mobile financial transaction operated in WAEMU in 2017 is about 16,942,550 million FCFA in value. Nearly 38.56% of that transaction is operated in Côte d’Ivoire followed by Burkina Faso with more than 23.21% and then Mali, Benin, Senegal with 16.01%, 11.09%, and 7.44%, respectively. However, Bissau Guinea and Togo have poorly performed with less than 3% of the total mobile financial transactions. This disparity has changed slightly in terms of payment where Côte d’Ivoire is still the leading country in that region with more than 35.35% of digital payments, followed by Senegal with nearly 19.87%. On the contrary, Côte d’Ivoire is relegated to the fourth place behind Burkina Faso with 33.14%, Benin with 26.93%, and Mali with 18.87% as far as domestic transfers are concerned. It stood out a positive correlation between transfer and the rate of poverty which indicates the issue of social security network enabled by domestic transfers in those countries.

3. Literature review

Financial market imperfections impede poor people who lack collateral and credit history to access financial services (Aghion & Bolton, Citation1997; Banerjee & Newman, Citation1993). Indeed, theoretical literature has fundamentally emphasized on the importance of financial development for an economy (Levine, Citation2005; Schumpeter, Citation1934). These precursors argue that a developed financial system enables access to broad finance through efficient capital allocation and proposes an efficient investment choice. Indeed, Schumpeter (Citation1934) in his theory of economic development showed the importance of innovation and credit for economic agents. For Levine (Citation2005) a broad financial development induces economic growth. Thus, financial intermediation provides information on investment opportunities, directs savings towards investments and manages the risk associated with those investments.

3.1. Financial inclusion: concept and challenges

Financial inclusion can be defined as an access to and use of appropriate, accessible and affordable financial services (Klapper & Singer, Citation2014). According to Dube, Chtakunye, and Chummun (Citation2014), financial inclusion ensured not only access to financial services but also promotes economic growth and the culture of savings in rural areas. Indeed, a large body of research has evidenced the positive impact of financial inclusion on development through the accessibility, security, and affordability of financial services.

For Park and Mercado (Citation2015), financial inclusion appears as a critical element that induces inclusive growth since access to finance allows the economic agent to make long-term consumption and investment decisions, participate in productive activities and deal with shocks. Similarly, Patwardhan et al. (Citation2018) show that financial inclusion is not an end per se but rather a means to an end. However, the conventional financing system that is expected to play this role has a number of limitations that lead to an inadequate delivering of financial services to the disadvantaged populations (Sapovadia, Citation2018).

One of these limitations is the lack of infrastructure to provide banking services (Gas, Citation2017). Indeed, following the initiatives of Muhammad Yunus’ Grameen Bank in the 1970s, a range of solutions was found to advance financial inclusion in the 1980s (Nhavira, Citation2015). They consisted in multiplying the installations of Automatic Tellers Machines (ATM) in rural areas. Similarly, Brown, Benjamin, and Karolin (Citation2016) argued that the proximity of bank branches to populations is very critical for financial inclusion. However, the implementation of this banking infrastructure had proved to be very costly for Banks, given the small size of their clientele and the large costs of investing in banking infrastructure (David-West, Citation2016). For illustrative purposes, the Reserve Bank of India considered that it is impossible to have Automatic Tellers Machines (ATM) in all villages because of the high cost pertaining to these infrastructures. Moreover, physical transactions with financial institutions are often subject to manipulation, error and omission (Sapovadia, Citation2018). However, Dupas, Karlan, Robinson, and Ubfal (Citation2016) empirically tested the effect of expanding access to the basic bank account in Uganda, Malawi and Chile. They show that as the number of deposits increased, there was no clear effect on the increase or the decrease in savings and income. Even better, Karlan et al. (Citation2014) emphasized the challenges of financial market imperfections and deviations for a broad access to finance. All these authors are unanimous on the importance of digital technology for an effective financial inclusion.

3.2. Digital technology and financial inclusion

The theory relating digital technology and financial inclusion begins with the fact that most financially excluded people hold at least one mobile phone as an asset and that the provision of financial services through this technology could accelerate the financial inclusion of the poor (World Bank, Citation2014b). Indeed, Ozili (Citation2018) shows that digital finance impacts financial inclusion through the access of vulnerable communities to financial services as well as through the profitability of banks due to the benefit reaping from the non-installation of new branches. Similarly, Chu (Citation2018) finds mobile technology to be a springboard for digital financial inclusion. Indeed, he shows that key-driven factors of the proliferation of mobile technology such as the accessibility, availability and affordability of an open financial ecosystem are also the driven factors of a strong and sustainable digital financial inclusion (Chu, Citation2018). Mobile technology, therefore, came as a better alternative to correct the imperfections of the formal finance (Alexandre & Eisenhart, Citation2013). For example, the Global Partnership for Financial Inclusion emphasized on the development and the rapid penetration of digital innovations in finance to accelerate the delivering of financial services. Similarly, by investigating the impact of remittances on financial inclusion in El Salvador on 937 households using instrumental variable technology, Anzoategui, Demirguc-kunt, and Periåla (Citation2014) find a positive impact of remittances on financial inclusion in terms of increased household deposits, but unfortunately non-significant and robust effect on credits. For these authors, strong financial inclusion through digital technology can reduce the costs of sending and receiving transfers, which could further motivate migrants to send and households to receive remittances. Ravi and Gakhar (Citation2015) in the same vein show that the comparative advantage in terms of infrastructure and customers’ network allows digital technologies to accelerate access to financial services. Moreover, Björkegren and Grissen (Citation2015) find that access to credit via digital technologies is a promise for financial inclusion. Thus, using the mobile phone to make credit can help predict credit payments by households and avoid defaults. Sinha and Highet (Citation2017) similarly argue that mobile technology in developing countries is conducive to an effective penetration of the financing system to underserved populations. For example, prior to the introduction of MPESA in Kenya, only 26.4% of adults had access to formal financial services in 2006. This rate increased to 66.7% in 2013 (Muthiora, Citation2015).

However, beyond the adoption of a digital technology, a complete digital inclusion of an economy requires the extension of telecommunications services to the poor in rural areas, which is very important to provide a platform of digital communication between clients and mobile money agents in rural areas. This digital inclusion urges then the provision of a system of payment on the basis of these established telecommunication services controlled by regulation to clarify the requirements regarding the “know your client” and the legal status of mobile money agents (AFI, Citation2018). And finally, access for the poor to all their financial and non-financial needs online (Koh, Phoon, & Ha, Citation2018). The authors also argue that the positive effects of digital finance on well-being are perceived through access to, savings accounts, social and institutional inclusion, and access to a diverse and improved range of financial services such as payments, savings and microcredits.

However, given the rapid development of mobile technology in developing countries, many studies have highlighted the accelerating role of mobile technology in financial inclusion and inclusive development in Africa (Adrianaivo & Kpodar, Citation2012; Beck, Senbet, & Simbanegavi, Citation2014; Cull, Gine, Harten, Heitmann, & Rusu, Citation2018). Indeed, Adrianaivo and Kpodar (Citation2012) investigated the impact of mobile phone on economics growth on 44 African countries from 1988 to 2007. They found, using a GMM system that the rapid expansion of mobile phones positively and significantly impacts economic growth through financial inclusion. Similarly, Beck et al. (Citation2014) in a study on the financial behavior of Kenyan households found that holding a mobile phone improves the likelihood of accessing financial services in Kenya. Moreover, the Mobile Money Global Event (Citation2017) organized by the GSMA in Tanzania confirms these results and shows that the progress of the adoption and effective use of mobile money in recent decades is a promise for the decades ahead (GSMA, Citation2017).

Digital technology is all the more important as it accelerates international transfer operations as far as cost and delivering time are concerned. To this end, a study by the World Bank in Citation2016 showed that the traditional transfer system charges nearly 10% as transfer fees for a minimum delivering time of 1 day, while the Bit Pesa in East Africa and the Rebit in the Philippine charge less than 3% as transfer fee for an immediate delivering (World Bank, Citation2016). For example, the sender in the UK buys and sends some bitcoins which are immediately transformed in Kenyan Shilling at a reception in Kenya by the recipient (Sapovadia, Citation2018). Similarly, Alampay, Moshi, Ghosh, Peralta, and Harshanti (Citation2017) in a systematic review of 2,758 empirical studies on the impact of mobile financial services in middle and low-income countries find that mobile financial services users receive a higher amount of transfer than non-users. Moreover, they find that mobile money induces an increase in savings. In the same vein, Jack and Suri (Citation2014) show that people are increasingly using MPESA to save. They also note that transfers via MPESA are fast, instantaneous and cheaper. Thus, during an idiosyncratic shock or an unfortunate event, individuals benefit some transfers from their relatives through mobile money (Jack & Suri, Citation2014). Mobile money has also reduced informal savings practices which consisted of save monies under mattresses or participate to tontine systems, resulting in an increased demand for banking services (Jack & Suri, Citation2014; Osafo-Kwaako, Singer, White, & Zouaoui, Citation2018). By investigating the impact of mobile money on household transfer in Uganda, Munyegera and Matsumoto (Citation2014) find that MPESA users and in particular individuals working in cities and having relatives in villages make more transfers than non-users of MPESA. Similarly, Ghosh (Citation2012) shows that people in Uganda use their electronic wallet to save money. In Bangladesh, a guide prepared by Sinha and Highet (Citation2017) on the financial inclusion of women through digital technologies shows that the use of these technologies has increased transfer amounts, women’s savings and even access to credit; which creates many opportunities for the empowerment of these women. In addition, online payments are becoming increasingly important. This is in line with the 2015’s World Bank report entitled “Innovative Digital Payment Mechanisms Supporting Financial Inclusion”, which shows that mobile money is not only a transfer tool but also induces saving, access to microcredit and increased international transfers (Gas, Citation2017).

4. Methodology and data

This study aims at assessing the impact of digital technologies on the dynamics of financial inclusion in WAEMU. The study follows the theoretical approach devised by Adrianaivo and Kpodar (Citation2012) who investigated the relationship between financial inclusion and mobile phone using an econometric model presented as follows:

Where denotes the log of financial inclusion,

denotes the log of ICT indicators including mobile phone and internet subscribers,

is a matrix of other control variables such as broad money M2, GDP per capita, population, inflation rate and

denotes the random error term.

The estimation strategy used in this study passes through two main steps. We first estimate a fixed or random effect model following the Hausmann test (Hausmann, Citation1978). However, the very short time dimension of our study already suggests the relevance of the random effect model. In addition, the random effect model imposes the strict exogeneity of independent variables meaning that they must be uncorrelated with both country and time-specific effects. Otherwise, the random effect model becomes biased and inconsistent (Baltagi, Citation2008). We estimate this static model just to assess the effect of the implementation of digital finance on financial inclusion in WAEMU.

The second steps of the estimations strategy are to check the robustness of the estimates in considering a dynamics in the analysis of the relationship between financial inclusion and digital technologies in WAEMU. To this end, a dynamic panel model will be estimated. According to Baltagi (Citation2008), most macroeconomic relationships are dynamic in nature and one of the advantages of panel data modeling is to allow the researcher to fully understand the dynamics of adjustments. The interest of introducing dynamics in this analysis is to, capture the dynamic effects of current and previous shocks in the model (Hsiao, Citation1986), control the unobserved and missing variables as well as allow the identification of country-specific effects (Arellano & Bond, Citation1991). As a matter of fact, the GMM system will be estimated because the financial inclusion may depend on its previous values which absent in the model may create the problem of endogeneity.

In a simple way, a dynamic panel model can be presented as follows:

where and

are scalars and

is the individual effect. The empirical specification of the dynamic panel model can be written as follows:

where denotes the financial inclusion and is measured by the Global Financial Services Utilization Rate (GFSU).

denotes the first period lagged value of the financial inclusion.

is a Dummy variable that takes 1 from the year when the Money mobile for unbanked is implemented. ICT refers to the number of mobile phone holders and Internet users.

denotes other control variables including Broad money (M2), Inflation rate, population, GDP per capita, Net interest rate and Bank Branch. However, in including the lagged of the dependent variable in the model, the dynamic panel regression is characterized by two sources of temporal persistence: self-correlation due to the presence of the lagged dependent variable among regressors and individual effects characterizing heterogeneity among individuals (Baltagi, Citation2008). The literature has identified a number of issues that could impede the robustness of the model. Several estimation techniques such as the Arellano and Bond (Citation1991) GMM system, Arellano and Bover (Citation1995), and Blundell and Bond (Citation1998) are proposed to solve these problems.

This study uses the Blundell & Bond (Citation1998) approach rather than the Arellano and Bond (Citation1991) one because the first approach is more appropriate when the number of panel periods is very short. In addition, the validity of the used instruments must be verified to ensure that the results are valid. According to Roodman (2009), the GMM system must be used with great care and several tests must be done to ensure the consistency of the results especially when the number of periods is small and the number of instruments is high. This is because many instruments would result in biased results. We thus adopt the two stages GMM system of Windmeijer (Citation2005) with a robust option pertaining to small sample sizes.

The data used in this study are mainly drawn from the Central Bank of West African States (BCEAO) database and the World Development Indicators database (2017). This study includes the eight (08) WAEMU’s countries from 2006 to 2017. The choice of these countries is based on the sharing of the same currency that is the CFA franc. This then concedes a very crucial homogeneity in the analysis of the effect that monetary and financial innovations can have on financial inclusion. Although very short, the time period of the study is justified by the availability of data over this period. We could have used the monthly or quarterly data to get a larger sample, but the unavailability of those data has bounded the sample to 12 years and 8 countries either 96 observations.

5. Results and discussion

Table displays the descriptive statistics. From that table, it stands out that on average the financial inclusion measured by the Global Rate of Financial Services Utilization (GUFS), is 29.67% with a standard deviation of 20.06% showing the high variability of the financial inclusion rate across the WAEMU countries and over the period of the study. In addition, this variability is confirmed by the banking infrastructure potential which has an average of about 109 points of banking services across these countries. Indeed, access to banking financial services in WAEMU is still very low because of the demographic structure of the population as well as the issue of financial education. It can also be supported by the large gap between the deposit and credit rate at plays in that region. Thus, the net interest gap deviation from than average (4.11%) is critical to discourage access to banking financial services. For example, the share of credit allocated to the private sector by banks is on average 18.66% of GDP, with a maximum share of 37.86% for the most banked economies like Côte d’Ivoire and Senegal. Access to credit in WAEMU is highly constrained because of the requirement of collateral to ensure repayment, albeit credits are key to allowing the development of microenterprises and the creation of sustainable jobs. This low access to credit services supports the low financial inclusion rate of African countries in general and WAEMU countries in particular. Besides, the GDP per capita is also patchy across the WAEMU countries. Assessing, on average, at 276,061 FCFA, this level of per capita income peaks in some countries at 703,175 FCFA. The WAEMU’s economies also have a major advantage in terms of broad money and inflation. In fact, the broad money, that is to say, the entire fiduciary currency plus the quasi-currency is on average 1762.696 billion FCFA per country, for a maximum amount of 8574.9 billion FCFA. This confirms the adequacy of the total amount of money needed in accordance with the dynamics of these economies.

Table 1. Descriptive statistics

This favors, through monetary policies, the stability of the currency and, in turn, the low inflation rate in WAEMU (2.20% on average). On the other hand, the WAEMU countries have a diverse demographic structure with an average population of around 12 million while the employed labor force is nearly 4,876,951. However, some studies have shown that one of the areas where Africa has been successful is in mobile technology and in particular mobile phone access. In fact, the number of mobile phone users is nearly 58.27 while those who use the internet are about 5.25 users per 100 inhabitants. This confirms the major role of information and communication technologies in the development of developing countries in general and in WAEMU countries in particular.

Table presents the estimation results of the Random effect Model (Column 1) and the Arrelano–Bover/Bundell–Bond Dynamic Model (Column 2). We use the Global Rate of Financial Services Utilization (GRFSU) as a proxy for financial inclusion. However, the random effect model estimates show at first glance that the advent of digital technologies is non-essential for financial inclusion. On the contrary, it came out from the results of the random effect model that the introduction of mobile money services in WAEMU countries is very critical for financial inclusion albeit the confused effect of digital technologies in that area. Indeed, this effect is about 5.99% with a degree of significance of 10%. Besides, the share of credit in GDP granted to the private sector affects positively at 5% level the financial inclusion in WAEMU. This show the importance of credit for small businesses to grow and its effect on the savings behavior of those people. However, although the specific effect of mobile phone and internet on financial inclusion is negative in the static model, the interaction variable of mobile phone and Internet is very conducive to financial inclusion. It positively impacts at 10% level the dynamics of the financial Inclusion in WAEMU. In addition, some variables including the Broad money, population, labor, Bank branch were expected to positively impact the dynamics of financial inclusion. Unfortunately, those variables are either negatives or non-significantly positive in the random effect model. Although paradoxical, these results justify the possible endogeneity problem often raised in static models. Therefore, considered as more robust than the Arellano and Bond method, the Arellano-Bover/Bundell-Bond system will help correct this endogeneity by regressing in the model the endogenous variable on its first period lagged value and on the first period lagged values of some predetermined variables as well as on other exogenous regressors (Maddala, Citation1983). Moreover, considered as very crucial in dynamic models, the coefficient of the lagged endogenous variable is significant at 1% level and lies between 0 and 1.

Table 2. Estimation results

They, therefore, indicate that the financial inclusion rate of the previous periods significantly determines the current financial inclusion rate and suggests a catch-up effect. A null coefficient would indicate a complete catch-up, while a coefficient between 0 and 1 indicates a partial catch-up. Economically, these coefficients indicate that countries with strong financial inclusion tend to cover most of their past financial inclusion gap.

Estimations of the dynamics model show that digital finance through mobile money and mobile banking technologies positively and significantly affects the dynamics of financial inclusion in the WAEMU countries at 10% level. This impact is also predetermined by the development of mobile phones penetration coupled with the broadband Internet access across the WAEMU countries. Indeed, phone and internet variables are all considered as potential instruments in the dynamic model. Although results show a negative effect of the internet on financial inclusion, the use of that technology on mobile phones is very important for massive financial inclusion. Moreover, the negative effect of the internet on financial inclusion indicates that this technology is not yet widely adopted in the WAEMU countries due to the constraints of accessibility, availability, and affordability pertaining to it.

In fact, consistent with Evans (Citation2016) that investigated the determinants of financial inclusion in Africa using two dynamic panel approaches, we find that mobile phone access positively but not significantly affects financial inclusion in WAEMU. In addition, our findings are in line with those of Adrianaivo and Kpodar (Citation2012) who indicated that the Information and Communication Technologies are a vehicle for financial inclusion and, in turn, induce inclusive development. Unfortunately, contrary to results of Sarma and Pais (Citation2011) indicating that, access to Internet is a key element in the digital economy and has led to the acceleration of financial inclusion, the coefficients related to the density of Internet users per 100 have overturned this accelerating role of ICT on financial inclusion. Though counterintuitive, this result aligns with the realities of developing countries where access to online banking services other than mobile banking is not yet well established in the banking culture of these populations. In fact, people often prefer mobile money to internet banking services because of its practicability and security. But it still urges to point out that the interaction Mobile phone-internet increases the financial inclusion by 1.01%. This interaction, although its effect is not very significant and robust, indicates that the ease with which people can access their account online in a touch on their smartphone is very critical for the sustainability and efficiency of financial institutions in providing financial services for the disadvantaged people. To this end, it is clear that the availability and accessibility of mobile phones coupled with the use of the Internet is very crucial for financial inclusion in developing countries. This is evidenced in Kenya where the M-PESA that fundamentally relies on mobile phone has changed the financial landscape of Kenya (Jack & Suri, Citation2011; Ndung’u, Citation2018). Yet, these authors indicate that without digital technologies, the financial inclusion in Africa and by the way in WAEMU countries would be a myth. This is because the entry of new players other than banks into the financial services market is made possible by the dynamics of Information and Communication Technologies in Africa (GSMA, Citation2016). In addition, several other variables significantly determine the dynamics of the financial inclusion in WAEMU. We have among other, the population; the broad money (M2), the bank branch, the number of employees and the inflation rate. Indeed, the results of the dynamic panel estimation indicate that population growth is strongly unfavorable to financial inclusion. This result is unfortunately in contrast to those of Chithra and Selvam (Citation2013)who have shown that population growth is one of the key determinants of financial inclusion. These results indicate that in developing countries, like WAEMU, demography generates more poor people who do not necessarily have access to formal financial services. However, with digital technologies such as mobile phone enable financial services, these excluded populations can easily and adequately access financial services. Moreover, like Adrianaivo and Kpodar (Citation2012), the results of the dynamic model show that the broad money is a key determinant of access to financial services. This because with a large amount of money, bank and other financial institutions will be willing to provide loan to people at a low interest rate. However, it is worth noting that the previous financial inclusion rate is very determinant in the current financial inclusion level. This because the coefficient related to the lagged of financial Inclusion is 97.2 and significant at 1% level.

6. Concluding remarks

The objective of this study was to assess the impact of digital technologies on the dynamics of financial inclusion in WAEMU countries. Using data from the BCEAO, the World Bank and the ITU databases, we first estimated a static panel model and then a dynamic panel model to address the endogeneity problems often raised in static models. From the estimate results, it appears that the advent of digital technology has contributed significantly to financial inclusion in WAEMU. In addition, the dynamics of financial inclusion differ from one country to another and the effect of mobile phone and internet on financial inclusion is perceived differently across countries in the WAEMU region. The results show that the simultaneous use of the Internet and mobile phone is more conducive to financial inclusion than the separate use of these technologies. This is because, beyond mobile money, the digital inclusion of an economy through the adoption of second and third generations’ mobile money services is becoming increasingly a major issue in the WAEMU countries. Payments and other online transactions require strong internet connectivity. In addition, online banking services are made possible by the use of the internet on smartphones and take a large part of digital finance in developing countries. Moreover, it can be seen that beyond digital technology, the net interest rates at plays in the banking system, the amount of credit granted to the private sector as well as the amount of money in circulation in an economy are all key-driven factors of financial inclusion in WAEMU. To this end, it urges for policy makers to promote the use of digital technologies by making them affordable, available and accessible even in the remote areas. Furthermore, the extension of communication networks in rural areas is a big issue. This may pass by the development of infrastructure conducive to innovation. Moreover, public awareness of adopting second and third-generation mobile money services is very critical to a digital inclusion of all WAEMU economies. Given the comparative advantage in terms of infrastructures of mobile telephone operators, it would also be advantageous for banks and microfinance institutions to change their business model by collaborating more with Mobile Network Operators. The States as well as the Central Bank, for their part, must make the regulation governing digital financial services flexible in order to encourage new players to enter into the digital finance market. In addition, that regulation may lead to data protection for clients.

Additional information

Funding

Notes on contributors

Melain Modeste Senou

Melain Modeste Senou is a scholar of the African Economic Research Consortium (AERC), Nairobi and affiliated to the Economics Department of Felix Houphouet Boigny University, Abidjan, Ivory Coast. His research interests revolve around inclusive finance and economic development issues.

Wautabouna Ouattara

Wautabouna Ouattara is a Full Professor in the Economics Department at Felix Houphouet Boigny University, Abidjan, Ivory Coast.

Denis Acclassato Houensou

Denis Acclassato Houensou is a Full professor in the Economics Department at the University of Abomey Calavi, Cotonou, Benin.

Related Research Data

References

- Adrianaivo, M., & Kpodar, K. (2012). Mobile phones, financial inclusion, and growth. Review of Economics and Institutions, 3(2), 1–16.

- AFI. (2018). Fintech for financial inclusion: A framework for digital financial transformation. Alliance for Financial Inclusion special Report. https//www.afi-global.org

- Aghion, P., & Bolton, P. (1997). A trickle-down theory of growth and development with debt overhang. Review of Economic Studies, 64(2), 151–172. doi:10.2307/2971707

- Alampay, E. A., Moshi, G. C., Ghosh, I., Peralta, M. L., & Harshanti, J. (2017). The impact of mobile Financial services in low and lower-middle-income countries. (Unpublished)

- Alexandre, C., & Eisenhart, L. C. (2013). Mobile money as an engine of financial inclusion and lynchpin of financial integrity. Washington Journal of Law, Technology and Arts, 8, (3), 285–302.

- Allen, F., Demirgüc-Kunt, A., Klapper, L., & Peria, M. S. M. (2016). The foundations of financial inclusion: Understanding ownership and use of formal accounts. The Journal of Financial Intermediation, 27, 1–30. ( Forthcoming). doi:10.1016/j.jfi.2015.12.003

- Anzoategui, D., Demirguc-kunt, A., & Periåla, M. (2014). Remittances and financial inclusion: Evidence from El Salvador. World Development, 54, 338–349. doi:10.1016/j.worlddev.2013.10.006

- Arellano, M., & Bond, S. (1991). Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. The Review of Economic Studies, 58(2), 277–297. doi:10.2307/2297968

- Arellano, M., & Bover, O. (1995). Another look at the instrumental variable estimation of error components models. Journal of Econometrics, 68(1), 29–51. doi:10.1016/0304-4076(94)01642-D

- Baltagi, B. (2008). Econometric analysis of panel data (Vol. 1). John Wiley & Sons.

- Banerjee, A., & Newman, A. (1993). Occupational choice and the process of development. Journal of Political Economy, 101(2), 274–298. doi:10.1086/261876

- BCEAO. (2016). Conférence régionale de haut niveau sur la finance pour tous: promouvoir l’inclusion financière en Afrique de l’ouest, Session 1: inclusion financière et réduction de la pauvreté: une vue d’ensemble, Sous thème 3: Inclusion financière dans l’UEMOA: état des lieux et stratégie de promotion.

- BCEAO. (2017). Stratégie régional d’inclusion financière dans l’UEMOA (Note d’Information N2/2017).

- BCEAO. (2018). Rapport annuel sur la situation de l’inclusion financière dans l’UEMOA au cours de l’annèe 2017, P. 29.

- Beck, T., Senbet, L., & Simbanegavi, W. (2014). Financial inclusion and innovation in Africa: An overview. Journal of African Economies, 24. doi:10.1093/jae/eju031

- Bill & Melinda Gates Foundation. (2015). 2015 gates annual letter: Our big bets for the future. Seattle: Author.

- Björkegren, D., & Grissen, D. (2015). Behavior revealed in mobile phone usage predicts loan repayment (Working paper). retrieved from SSRN https://ssrn.com/abstract=2611775.

- Blundell, R, & Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87, 115–143.

- Brown, M., Benjamin, G., & Karolin, K. (2016). Microfinance banks and financial inclusion. Review of Finance, 20(pages), 907–946. doi:10.1093/rof/rfv026

- Busch, M. O., Koetter, M., Krause, T., & Tonzer, L. (2017). Broadening the G20 financial inclusion agenda to promote financial stability: The role for regional banking networks. G20 Insights, April, 4.

- Chithra, N, & Selvam, M. (2013). Determinants of financial inclusion: an empirical study on the inter-state variations in india . SSRN-2296096.

- Chu, A. B. (2018). Mobile technology and financial inclusion. In Handbook of Blockchain, Digital Finance, and Inclusion, Volume 1 (pp. 131-144). Academic Press.

- Cull, R., Gine, X., Harten, S., Heitmann, S., & Rusu, A. B. (2018). Agent banking in a highly under-developed financial sector: Evidence from democratic republic of Congo. World Development, 107(2018), 54–74. doi:10.1016/j.worlddev.2018.02.001

- David-West, O. (2016). The path to digital financial inclusion in Nigeria: Experiences of firstmonie. Journal of Payments Strategy and Systems, 9(4), 256–273.

- Demirgüç-Kunt, A., Klapper, L. F., Singer, D., & Hess, J. (2017). The global findex database 2017: Measuring financial inclusion and the fintech revolution (World Bank Policy Research Working Paper).

- Dube, T., Chtakunye, P., & Chummun, B. Z. (2014). Mobile money as a strategy for financial inclusion in rural communities. Mediterranean Journal of Social Sciences, 5(25), 216–224.

- Dupas, P., Karlan, D., Robinson, J., & Ubfal, D. (2016). Banking the unbanked? Evidence from three countries (No. w22463). National Bureau of Economic Research.

- Evans, O. (2016). Determinants of financial inclusion in Africa: A dynamic panel data approach (MPRA Paper No. 81326). Retrieved from https://mpra.ub.uni-muenchen.de/81326/

- Gas, S. A. (2017, July 15). Mobile money, cashless society and financial inclusion: case study on somalia and kenya. Mobile Money, Cashless Society and Financial Inclusion.

- Ghosh, I. (2012, March). The mobile phone as a link to formal financial services: Findings from Uganda. In Proceedings of the Fifth International Conference on Information and Communication Technologies and Development (pp. 140-148). ACM.

- GPFI (2017). 2017 Financial Inclusion Action Plan. https://www.gpfi.org

- GSMA. (2015). State of the industry report: Mobile money. United Kingdom: Author.

- GSMA. (2016). State of mobile money in West Africa. United Kingdom: Author.

- GSMA. (2017). Mobile money global event, Tanzania, 2017. Retrieved from. https://gsma.com/mobilefordevelopment/events/mobile-money-global-event/

- GSMA. (2018). L’économie mobile, l’Afrique de l’Ouest 2018. Retrieved from www.gsma.com

- Hausman, J.A. (1978). Specification tests in econometrics. Econometrica, 46(6), 1251-1271.

- Hsiao, C. (1986). Analysis of panel data. Econometric Society Monograph, 11.

- Jack, W., & Suri, T. (2011). Mobile money: The economics of M-PESA, national bureau of economic research (NBER) (Working Paper, No.16721).

- Jack, W., & Suri, T. (2014). Risk sharing and transaction costs: Evidence from Kenya’s mobile money revolution. American Economic Review, 104(1), 183–223. doi:10.1257/aer.104.1.183

- Karlan, D, Osei, R, Osei-Akoto, I, & Udry, C. (2014). Agricultural decisions after relaxing credit and risk constraints. Quarterly Journal Of Economics, 129(2), 597-652.

- Klapper, L., & Singer, D. (2014). The opportunities of digitizing payments (Working Paper). Washington, DC:the World Bank.

- Klein, M., & Mayer, C. (2011), Mobile banking and financial inclusion. The regulatory lessons (Policy Research Working Paper N° 5664, The World Bank, 32 pages).

- Koh, F., Phoon, F., & Ha, C. D. (2018). Digital financial inclusion in South East Asia. Handbook of Blockchain, Digital Finance, and Inclusion, 2. doi:10.1016/B978-0-12-812282-2.00015-2

- Levine, R. (2005). Finance and growth: theory and evidence. Handbook of economic growth, 1, 865-934.

- Maddala, G. S. (1983). Limited dependent and qualitative variables in econometrics. Cambridge: Cambridge University Press.

- Morawczynski, O. (2009). Examining the usage and impact of transformational M-banking in Kenya. In Internationalization, Design and Global Development, 5623/2009, 495–504.

- Munyegera, G., & Matsumoto, T. (2014). Mobile money, remittances and rural household welfare: Panel evidence from Uganda. Tokyo: GRIPS.

- Muthiora, B. (2015). Enabling mobile money policies in Kenya: Fostering a digital financial revolution. GSMA Mobile Money for the Unbanked.

- Ndung'u, N. (2018). The M-Pesa technological revolution for financial services in Kenya: A platform for financial inclusion. In Handbook of Blockchain, Digital Finance, and Inclusion, Volume 1 (pp. 37-56). Academic Press.

- Nhavira, J. D. G. (2015). Whither financial inclusion? A holistic approach. Journal of Strategic Studies, 5(1), 80–91.

- Osafo-Kwaako, P., Singer, M., White, O., & Zouaoui, Y. (2018). Mobile money in emerging markets: The business case for financial inclusion. McKinsey Global Institute, March. https://www. mckinsey. com/~/media/McKinsey/Industries/Financial% 20Services/Our% 20Insights/Mobile, 20.

- Ozili, K. P. (2018). Impact of digital finance on financial inclusion and stability. Borsa Istanbul Review, 18, 329–340. doi:10.1016/j.bir.2017.12.003

- Park, C., & Mercado, R. (2015). Financial inclusion, poverty, and income inequality in developing Asia (ADB Economics Working Paper Series. No 426).

- Patwardhan, A., Singleton, K., & Schmitz, K. (2018). Financial inclusion in the digital age. International Finance Corporation, World Bank, credit ease and Stanford Business, 66p

- Ravi, S., & Gakhar, S. (2015). Advancing financial inclusion in India beyond the Jan-Dhan Yojana. Brookings India IMPACT Series. Brookings Institution India Center

- Sapovadia, V. (2018). Financial Inclusion, Digital Currency, and Mobile Technology. In Handbook of Blockchain, Digital Finance, and Inclusion, Volume 2 (pp. 361-385). Academic Press.

- Sarma, M., & Pais, J. (2011). Financial inclusion and development: A cross country analysis. Journal of International Development, 23(5), 613–628. doi:10.1002/jid.1698

- Schumpeter, J. A. (1934). The theory of economic development. Leipzig: Dunker and Humbolt. 1912; translated by Redvers Opie, Cambridge, MA, Harvard University Press.

- Senou, M. M., Ouattara, W., & Acclassato Houensou, D. (2019). Is there a bottleneck for mobile money adoption in WAEMU? Transnational Corporations Review, 11(2), 143–156. doi:10.1080/19186444.2019.1641393

- Sinha, T., & Highet, C. (2017). Guide to increasing women’s financial inclusion in Bangladesh through digital financial services. mSTAR, USAID. https://www.findevgateway.org › library › guide-increa.

- Windmeijer, F. (2005). A finite sample correction for the variance of linear efficient two-step gmm estimators. Journal of Econometrics, 126, 25–51.

- World Bank. (2014b, April 10) Digital finance: Empowering the poor via new technologies. Retrieved from http://www.worldbank.org/en/news/feature/2014/04/10/digital-financeempowering-poor-new-technologies.

- World Bank. (2015, April 17). Press release: World bank group and a coalition of partners make commitments to accelerate universal financial access. The World Bank.

- World Bank. (2016). World Development Report 2016: Digital Dividends. Washington, DC: Author. License: Creative Commons Attribution CC BY 3.0 IGO.