?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper investigates the impact of financial development on economic growth in Pakistan using the Markov Switching Model over the period 1980–2017. The results based on two-state Markov switching model confirm the Schumpeter’s view that finance spurs growth. The result reveals that financial development augments economic growth in both high and low economic growth regimes in Pakistan. However, the impact of financial development on economic growth is found to be relatively higher in the high-growth regime. This implies that economic growth responds differently to financial development in low-growth and high-growth regimes. Among the control variables, trade openness and government expenditures impact economic growth positively, while labour force exerts a negative impact on economic growth.

Public Interest Statement

The financial sector is an indispensable sector that contributes to augmenting economic growth. Its importance for developing countries like Pakistan is imperative. Pakistan liberalized her financial sector in the early 1990s with the objective that the financial sector will play a better role in economic growth. Unfortunately, Pakistan has observed spurts and reversals in economic growth. This study aims to investigate the regime impacts of financial development on economic growth. The results suggest that policymakers may formulate the regime-specific policies for spurring economic growth. The study found that financial sector alone cannot spur economic growth. Therefore, the policies to enrich the role of other macroeconomic variables be reinforced so that capital, labour, government expenditures and trade openness can become stimulant for economic growth. Further, central bank may formulate regime-specific policies, specifically policies to enhance financial development role in low economic growth regime. The outreach of insurance, pension and bond markets be strengthened.

1. Introduction

The relationship between financial development and economic growth is a much-debated issue in the empirical literature. A large volume of empirical literature concluded that financial development spurs economic growth (Beck & Levine, Citation2004; Jalil & Ma, Citation2008; Khan, Qayyum, & Sheikh, Citation2005; Khan & Senhadji, Citation2000; King & Levine, Citation1993; Levine, Citation1997, Citation2005; Rajan & Zingales, Citation1998). They considered that a well-structured financial system as a pre-requisite for economic growth. The theoretical link between financial development and economic growth can be traced back to the seminal work by Schumpeter (Citation1912). Schumpeter (Citation1912) argued that a well-functioning financial system is pivotal for economic growth. The advocates of financial development asserted that a well-developed financial system is a key condition for industrialization (Gerschenkron, Citation1962), which was endorsed by McKinnon (Citation1973) and Shaw (Citation1973). They argued that liberal financial markets promote economic growth, while repressive financial markets retard it. Thus, McKinnon (Citation1973) and Shaw (Citation1973) supported the adoption of liberal policies, which are essential for sustainable economic growth. In the late 1980s and early 1990s, endogenous growth theories have also evolved the role of financial development as a key determinant of economic growth (Berthelemy & Varoudakis, Citation1996).Footnote1 The endogenous growth theorists argued that financial development helps to improve the efficiency of capital allocation, improve management of liquidity risks, efficiently diversify investor’s portfolios and enhance the efficacy of investment projects. These factors can increase capital productivity, which exerting a positive impact on economic growth (Bencivenga & Smith, Citation1991; Greenwood & Jovanovic, Citation1990; King & Levine, Citation1993; Levine, Citation1991; Saint-Paul, Citation1992). On the other hand, Lucas (Citation1988) claimed that the importance of financial markets in economic development is overstressed in academic discussions. Schularick and Taylor (Citation2012) and Mian and Sufi (Citation2014) maintained that, without proper rules and regulations, finance can become a powerful force for planting the seeds of future crises with adverse implications for economic growth and social welfare.

However, empirical findings are mixed with respect to the overall conclusions regarding the finance–growth nexus. For example, one strand of literature such as Greenwood and Jovanovic (Citation1990), King and Levine (Citation1993), Demetriades and Hussein (Citation1996), Berthelemy and Varoudakis (Citation1996), Christopoulos and Tsionas (Citation2004), Abu-Bader and Abu-Qarn (Citation2008) and Rousseau and Wachtel (Citation2011) concluded positive association between financial development and economic growth. The other strand of literature (for instance, Demetriades & Rousseau, Citation2016; Luintel & Khan, Citation1999; Naceur & Ghazouani, Citation2007; Narayan & Narayan, Citation2013; Singh, Citation1997) concluded that financial markets exert a negative or no impact of financial development on economic growth.

Another strand of literature (for example, Deidda & Fattouh, Citation2002) showed that a positive association between financial development and economic growth disappeared beyond a threshold of around $852 of initial income level. Beck, Degryse, and Kneer (Citation2014) and Arcand, Berkes, and Panizza (Citation2015) identified the threshold beyond which financial depth no longer has a positive impact on economic growth. Rioja and Valev (Citation2004) concluded that the relationship between financial development and economic growth varies according to the level of financial development. Shen and Lee (Citation2006) revealed a weak and inverse U-shaped relationship between economic growth and banking sector development. However, the relationship becomes stronger when the square of stock market variables are included.

One reason for variation in empirical results could be the heterogeneity in the level of financial development and income across countries (Odedokun, Citation1996; Rioja & Valev, Citation2014). The other reason for variation in results could be the non-linear relationship between financial development and economic growth. Demirguc-Kunt, Feyen, and Levine (Citation2013) show that as countries develop economically, the association between an increase in economic output and an increase in bank development becomes smaller, whereas the association between an increase in economic output and an increase in stock market development becomes larger. Like-wise, Ibrahim (Citation2015) argued that a linear relationship is restrictive in the wave of policy shifts. Hence, findings based on the linear relationship may be considered as biased. Many researchers (Abdmoulah & Jelili, Citation2013; Cecchetti, Kharroubi Citation2012; Deidda & Fattouh, Citation2002; Doumbia, Citation2016; Jude, Citation2010) concluded non-linear and non-monotonic relationship between financial development and economic growth.

Since the late 1980s, the majority of developing countries, including Pakistan, initiated a series of reforms for liberalization of their financial system. These policy shifts lead to a non-linear relationship between finance and growth. The non-linear relationship implies that financial development and economic growth behave differently in different regimes (Demetriades & Hook Law, Citation2006).

With regard to Pakistan, a considerable amount of studies have used a linear approach and concluded a positive relationship between financial development and economic growth.Footnote2 It is observed that financial sector reforms have changed the finance–growth nexus from linear to non-linear. Despite the vital role of finance in socio-economic development in Pakistan, very little research work has been done on this issue. Hence, it is pertinent to investigate the non-linear aspect of finance–growth nexus as the analysis may provide deeper insights for policymakers to derive sound policy recommendations.

This study contributes to the existing literature by investigating the impact of financial development on economic growth using the Markov switching approach. This approach is superior to examine the dynamic behavior of the finance–growth relationship in different policy regimes. Secondly, Hsu, Tian, and Xu (Citation2014) explored that the capital market induces greater productivity gain and faster technology innovation than banking sector development. Additionally, as the economy develops, the marginal contribution of banks to economic growth declines, while that of capital markets increases. Hence, market-based finance has a comparative advantage in promoting technological innovation and productivity enhancement, and in financing possibly new sources of long-term economic growth. Therefore, this study uses a comprehensive financial development index (FDI) constructed by the International Monetary Fund (IMF) that covers stock markets, insurance sector, mutual funds and financial institutions to capture the impact of financial sector on economic growth.

The rest of the paper is organized as follows: Section 2 deals with model specification, empirical methodology, variable description and financial development index. Section 3 discusses empirical findings, while Section 4 delineates conclusion and policy recommendations.

2. Empirical methodology

2.1. Model specification

To examine the impact of financial development on economic growth in Pakistan, we followed the growth model of Odedokun (Citation1996). It is based on the one-sector standard neo-classical aggregate production function in which financial development constitutes an input. The specification of aggregate production function is of the following form:

where is a real gross domestic product at time t,

is labour force,

is physical capital,

measures the level of financial development and other factors such as trade openness (

), inflation (

) and government expenditures (

) are associated with economic growth. Besides labour force, physical capital and level of financial development, we included trade openness (

) to capture the importance of international factors in influencing economic activity (Charfeddine & Mrabet, Citation2015). Higher level of exports relative to imports causes real

to increase but its effect on real GDP in developing countries can also be negative. Inflation (

) is included to capture the macroeconomic stability and business environment following Beck, Levine, and Loayza (Citation2000). An increase in inflation increases macroeconomic uncertainty, which is likely to have a negative impact on economic growth as well as hurt financial activities. Rising inflation causes the interest rate to increase, which adversely affects private investment and hence economic growth. The ratio of government consumption relative to GDP is incorporated to measure government efficiency. The impact of government consumption relative to GDP on real GDP in developing countries is generally negative due to the relative inefficiency of the public sector. By taking logarithms of EquationEquation (1)

(1)

(1) and after appropriate manipulation, EquationEquation (1)

(1)

(1) can be rewritten as:

where and

are, respectively, parameters and the error term. The main objective of this study is to explore the non-linear relationship between finance and growth. Therefore, we employ the Markov switching modelling approach to investigate the non-linear behavior of financial development and economic growth in Pakistan.

2.2. Data and methodology

This study utilized annual data over the period 1980–2017. The variables used in this study include economic growth proxied by real GDP following Samargandi, Fidrmuc, and Ghosh (Citation2015). The control variables are employed labour force

, physical capital

proxied by gross fixed capital formation relative to GDP, trade openness

is the sum of exports plus imports relative to GDP, inflation

is the average annual growth of the consumer price index with 2010 as the base year and government consumption expenditure relative to GDP

. Data on these variables are collected from World Development Indications

, Pakistan Economic Survey (various issues) and Annual Reports of the State Bank of Pakistan.

2.3. Financial development index

Adu et al. (Citation2013) argued that a single proxy of financial development cannot adequately capture the impact of financial development. Thus, this study uses a broader FDI constructed by Svirydzenka (Citation2016)Footnote3 and was updated by the IMF till 2017.Footnote4 While capturing financial institutions, this index detentions the banking and insurance sectors besides taking into account the mutual and pension funds. For financial markets, it accounts for non-banking financial institutions, equity and bond markets. Thus, FDI is broader in the sense that it captures the depth, access and efficiency of both the financial institutions and financial markets.Footnote5 The IMF’s FDI also overcomes the limitation of single or few variables' considerations in the construction of index, and hence it provides a better snapshot of the financial development of a country.

2.4. Regime switching model

The present study uses a Markov regime-switching methodology to investigate the impact of financial development on economic growth along with other control variables, such as labour force, physical capital, government spending relative to GDP, trade openness relative to GDP and inflation, associated to economic growth. The motivation for using the

method was the shifts in financial policy in the late 1980s in Pakistan. In examining the finance–growth relationship, we assume the two-state

model (MS(2)) following Fallahi (Citation2011).Footnote6 We consider mean (

), variance (

) and financial development (

) as regime-switching variables, while labour force (

), physical capital (

), trade openness (

), government consumption expenditures (

) and inflation (

) as non-switching variables.

2.5. Markov regime-switching approach

The time series being used in the model is assumed to be stationary and depends on the latent process. Hence, the states (

, where t = 0, 1) are unobservable around which time series evolves. We assume that the mean (

where t = 0, 1), variance (

, where t = 0, 1) and coefficients of financial development (

where t = 0, 1) are regime-dependent. It means that these parameters evolve around the regimes. We suppose two regimes; regime 0 is associated with high average economic growth, whereas regime 1 is linked with low average economic growth. It is assumed that when the economy is expanding because of financial development, the average growth in the economy is expected to be higher, while volatility is assumed to be lower. Thus,

and

, indicating high growth–low volatility regime and vice versa. The specific form of MS(2) can be written as

In EquationEquation (3)(3)

(3)

is change in real GDP,

is state-dependent intercept,

denotes state- dependent switching variable, that is,

FD and

are state-invariant variables such as

and

, while

). The probabilities will be

and

where and

are the probabilities remaining in regime 0 and regime 1, respectively, while

and

indicating the movement of probability from one regime to another. Thus,

In MS (2) model, the mean and variance are expected to behave as

where = 0 refers to high average growth regime and

= 1 refers to low average growth regime.

EquationEquations (6)(6)

(6) and (Equation7

(7)

(7) ) are generated by ergodic probabilities which are given in EquationEquations (8)

(8)

(8) –(Equation11

(11)

(11) ).

We have used more than 1000 starting values for estimated specification to optimize parameters globally.Footnote7 Besides, we also considered the maximum log-likelihood ratio () test, residual analysis and Regime Classification Measure (

) to select the best model (Charfeddine & Goaied, Citation2019; Charfeddine & Guegan, Citation2011).Footnote8

3. Empirical results and discussion

3.1. Preliminary investigation

Descriptive statistics are reported in Table (panel A), whereas correlation analysis is given in panel B of Table . The descriptive statistics reveal that the average change in all variables is positive except trade openness. The maximum level of economic growth was 0.086 which corresponds to the year 2005, while the minimum level of economic growth was 0.004 which coincides with 2009 when the economy was in a slump. The mean value of financial development changes was 0.0029 with the maximum level observed to be 0.074, while the minimum level was −0.075. The government expenditures, trade openness and physical capital were relatively more volatile than other variables. The standard deviation shows that changes in real GDP, labour force and financial development have almost similar variability. All the variables are positively skewed. The data have a heavier tail than normal distribution in financial development, physical capital, labour force, inflation and government expenditures. The kurtosis is greater than 3 except for real GDP changes and changes in trade openness. The normality is not achieved in labour force and government expenditures since the Jarque–Bera statistics are significant at 1% and 5% level of significance, respectively.

Table 1. Descriptive statistics and correlation analysis

In panel B of Table , the correlation analysis is reported. The real GDP has a negative correlation with labour force and inflation, whereas rest variables have a positive correlation with real GDP. More importantly, real GDP has a positive correlation with financial development. The physical capital and trade openness have a high correlation with real GDP. However, financial development has a negative correlation with the labour force, trade openness, government expenditures and inflation.

To test the presence of non-linearity in a finance–growth relationship, we employ the Brock, Dechert, and Scheinkman (Citation1987) (BDS) test. The BDS test reveals that an increment to a data series is independent and identically distributed (). This test is based on the correlation that measures the frequency with which temporal patterns are repeated in the data. The rejection of the null hypothesis implies that the data are

, and the relationship is non-linear. Table reports the result of the BDS test.

Table 2. Results of BDS test

The results of the BDS test (Table ) suggest that the relationship between finance and growth is non-linear because all the reported dimensions are significant at 1% level of significance. Therefore, we can infer that approach is appropriate to investigate the finance–growth relationship. Since

approach requires that all the variables included in the model must be stationary, we, therefore, applied Augmented Dickey–Fuller (ADF) and Phillips–Perron (PP) tests to determine the non-stationarity of the variables. The results are reported in Table .

Table 3. Results of unit root tests

The results of ADF and PP tests show that all the differenced variables are stationary at the 1%, 5% and 10% level of significance, respectively.

3.2. Regime switching model

The impact of financial development on economic growth was examined using the Markov switching framework. We limit our analysis to two regimes because of the small sample and better interpretation of the relationship between financial development and economic growth. Fallahi (Citation2011) found that (2) specification better fits the macroeconomic relationships. For comparison purposes, we also estimate a linear finance–growth model. The descriptive statistics and diagnostic tests based on the residuals obtained from the estimation of linear and

(2) models are reported in Table . The statistics show that both models have good residual properties. The residuals have normal distribution as indicated by the insignificance of the Jarque–Bera test. The

, Ljung-Box

and

statistics confirm the absence of heteroscedasticity and autocorrelation in the estimated residuals. Furthermore, the value of

was 1.7887, which is closer to 0, confirming that

(2) model is a true data-generating process (

). The information criterion reveals that

,

and

have smaller values in

than a linear model. On the basis of information criterion, diagnostic tests and

, we can infer that

better fits the data with regard to the relationship between financial development and economic growth in Pakistan for the period 1980–2017.

Table 4. Residual analysis of linear and models

Now, we proceed with the results of linear and (2) model which are reported in Table .

Table 5. Estimates of linear and model (1980–2017)

The results show that the estimated coefficients ( and

are significant at the 1% level of significance. Regime 0 is characterized as a high-growth regime where economic activities expand significantly. For instance, regime 0 has the highest value of the intercept coefficient,

, with the lowest value of volatility,

. High mean value with low volatility suggests that this regime coincides with a period of economic expansion. Regime 1 corresponds to a period of lowgrowth where the estimated value of the intercept coefficient is

, and relatively high value of variance is

. The result indicates that

with

. The analysis based on the values of means and variances confirms that regime 0 corresponds to high growth with low volatility and regime 1 coincides to low growth with high volatility. Thus, it can be deduced that the low-growth regime is more volatile than a high-growth regime.

In terms of regression parameters, it is found that financial development exerts a positive and significant impact on economic growth in both regimes. However, the impact of financial development in a high-growth regime is relatively higher than low-growth regime. In a high-growth regime, the results reveal that with 1% increase in financial development, economic growth increases by 0.6489%. However, in low-growth regime, a 1% increase in financial development would increase economic growth by 0.1727%. In high-growth regime, financial development stimulates economic growth by 3.76 times higher than low-growth regime. Although these results confirm that the financial sector is pivotal to promote economic growth in Pakistan, however, the response of economic growth to financial development is different in both regimes. This outcome endorses the view that the relationship between financial development and economic growth is non-monotonic and regime-dependent in developing countries like Pakistan.Footnote9 This finding is inconsistent with Jalil and Ma (Citation2008), Lal, Muhammad, Hussain, and Jalil (Citation2009), Jalil and Feridun (Citation2011), Farooq, Shahbaz, Arouri, and Teulon (Citation2013) and Naveed and Mahmood (Citation2019).

Among the non-switching variables, the results reveal that the labour force exerts a significant negative impact on economic growth. The result discloses that with a 1% increase in the labour force, economic growth falls by 0.456%. The negative impact of the labour force on economic growth is not surprising because Pakistan is a labour-intensive country and a major proportion of labour is unskilled. Our results are consistent with Ali and Mustafa (Citation2012) and Bist (Citation2018). However, the larger negative magnitude of the labour force is a puzzle for developing country like Pakistan since it drags economic growth considerably. Trade openness has a significant positive association with economic growth, confirming the validity of trade-led growth hypothesis. The result indicates that the role of trade openness is pivotal for Pakistan because trade allows attracting technological knowledge. The larger magnitude indicates that trade openness contribute better with economic growth in Pakistan. This finding is consistent with Jalil and Feridun (Citation2011) and Farooq et al. (Citation2013). To further improve the role of trade openness, Pakistan may further liberalize its trade regime to gain benefits of an open economy. Government expenditures relative to GDP are positively related to economic growth. A 1% increase in the growth of government expenditures () contributes 0.0410% to economic growth in Pakistan. This finding suggests that government consumption is conducive to economic growth in Pakistan. Adu et al. (Citation2013) also found a positive effect of government expenditures on economic growth.

Physical capital and inflation exert an insignificant impact on economic growth. The insignificant finding of physical capital for a low-income country like Pakistan is consistent with Bist (Citation2018). However, physical capital is the main ingredient of aggregate production function and its insignificant role is quite astonishing. Pakistan has to take corrective measures so that the physical capital stock may positively contribute to economic growth.

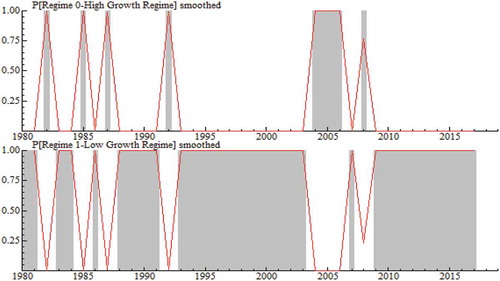

The duration of regime classification with respect to is reported in Table . The results show that both regimes are persistent because the estimated transition probabilities are greater than 0.5. Furthermore, low-growth regime was more persuasive than that of high-growth regime. For example, there is a 78.38% probability of staying in low-growth regime, which is higher than the probability of staying in high-growth regime (21.62%). Similarly, the steady-state probabilities also confirm that the economy remains more in low-growth regime (79.10%) than in high-growth regime (20.90%).

Table 6. Duration of regime classification of MS(2)

The behaviour of smoothed probabilities is depicted in Figure , which also confirms that smoothed probabilities are persistent in both regimes.

Figure 1. Smoothed probabilities of

4. Conclusion and policy implications

This study investigates the regime-specific relationship between financial development and economic growth for the period 1980–2017. The analysis is based on a two-state Markov switching approach. The results support the presence of a non-linear relationship between financial development and economic growth in Pakistan. The result reveals that financial development exerts a significant positive impact on economic growth in high- and low-growth regimes. However, the impact of financial development on economic growth was relatively strong in the high-growth regime. This implies that economic growth responds differently to financial development in high- and low-growth regimes in Pakistan. This further implies that the relationship between financial development and economic growth is non-linear.

Among the non-switching variables, labour force contributes negatively to economic growth, while physical capital and inflation exert an insignificant effect on economic growth. The impact of trade openness and government expenditures on economic growth is positive and significant. The results based on regime smoothed probabilities and regime classification reveal that a high-growth regime is relatively unsustainable in Pakistan during the period 1980–2017.

Important policy implications from the above analysis are: the impact of financial development on economic growth seems to be stronger in high-growth than in low-growth regime. This reveals that the impact of financial development on economic growth is non-linear and regime-dependent. Therefore, the policymakers may consider non-linear aspects while formulating financial development policy. Besides the role of financial development, macroeconomic variables also play an important role to enhance economic growth. Therefore, policymakers may consider trade openness and government expenditures to achieve sustainable economic growth.

The present study extends the understandings of finance–growth nexus in Pakistan in the regime-switching framework. However, the findings are subject to some limitations. The present study focuses only on two regimes. However, it would be more insightful to exploit the possibility of multiple regimes. The effect of financial development, following sudden changes in the political regime, would be interesting to study. It would also fruitful to test the finance–growth nexus using the cross-country panel data. We leave this for future research.

Correction

This article has been republished with minor changes. These changes do not impact the academic content of the article.

Additional information

Funding

Notes on contributors

Abdul Rahman

Abdul Rahman holds MS degree in Banking and Financial Economics. He also holds M.A.Economics and MBA Finance besides professional banking diplomas and certificates. His area of interest relates to financial economics, international trade, risk management and monetary economics.

Muhammad Arshad Khan

Muhammad Arshad Khan holds PhD inEconomics from the Pakistan Institute of Development Economics, Islamabad. He has more than 25 years of teaching/research experience in reputed research institutes and Universities. His teaching and research interests includes advanced micro and macroeconomics, macro econometric modeling, and international trade and finance. He has more than 50 research publications in the journals of international repute

Lanouar Charfeddine

Lanouar Charfeddine holds PhD in Economics from the University Paris II – Pantheon – Assas, France. His research areas include nonlinear models, energy economics, and fiscal and monetary policies. He has published several articles in internationally respected peer-reviewed journals.

Notes

1. A comprehensive survey of the literature is available in the works by Levine (Citation1997), Ang (Citation2008) and Stolbov (Citation2013).

2. For instance, Khan et al. (Citation2005), Tahir (Citation2008), Khan (Citation2008), Naveed and Mahmood (Citation2019), among others. A brief review of studies is given in Table A (Appendix).

3. We are thankful to the anonymous reviewer who motivated to use a broader financial development index constructed by the International Monetary Fund.

4. Data are available at https://data.imf.org/?sk=F8032E80-B36C-43B1-AC26-493C5B1CD33B.

5. For detail review, see Svirydzenka (Citation2016).

6. Although we can consider more than two regimes, which is quite possible in the MS framework, we have also tried MS (3) specification but the statistical analysis provided weak convergence, hence we preferred MS(2) model.

7. For detail, see Hamilton (Citation1990).

8. Following Ang and Bekaert (Citation2002), we have calculated for 2-states as:

The RCM value ranges between 0 (perfect regime classification) to 100 (no regime classification).

9. Whenever productivity increasing effect of financial development is larger than the productivity decreasing effect, there may be a non-monotonic relationship between financial development and economic growth.

References

- Abdmoulah, W., & Jelili, R. B. (2013). Access to finance thresholds and the finance‐growth nexus. Economic Papers: A Journal of Applied Economics and Policy, 32(4), 522–15. doi:10.1111/1759-3441.12059

- Abu- Bader, S., & Abu- Qarn, A. S. (2008). Financial development and economic growth: Evidence from six MENA countries. Review of Development Economics, 12(4), 803–817.

- Adu, G., Marbuah, G., & Mensah, J. T. (2013). Financial development and economic growth in Ghana: Does the measure of financial development matter? Review of Development Finance, 3(4), 192–203. doi:10.1016/j.rdf.2013.11.001

- Ali, R., & Mustafa, U. (2012). External debt accumulation and its impact on economic growth in Pakistan. The Pakistan Development Review, 79–95. doi:10.30541/v51i4IIpp.79-96

- Ang, A., & Bekaert, G. (2002). Regime switches in interest rates. Journal of Business & Economic Statistics, 20(2), 163–182. doi:10.1198/073500102317351930

- Ang, J. B. (2008). A survey of recent developments in the literature of finance and growth. Journal of Economic Surveys, 22(3), 536–576. doi:10.1111/j.1467-6419.2007.00542.x

- Arcand, J. L., Berkes, E., & Panizza, U. (2015). Too much finance? Journal of Economic Growth, 20(2), 105–148. doi:10.1007/s10887-015-9115-2

- Beck, T., Degryse, H., & Kneer, C. (2014). Is more finance better? Disentangling intermediation and size effects of financial systems. Journal of Financial Stability, 10, 50–64. doi:10.1016/j.jfs.2013.03.005

- Beck, T., & Levine, R. (2004). Stock markets, banks, and growth: Panel evidence. Journal of Banking and Finance, 28(3), 423–442. doi:10.1016/S0378-4266(02)00408-9

- Beck, T., Levine, R., & Loayza, N. (2000). Finance and the sources of growth. Journal of Financial Economics, 58(1–2), 261–300. doi:10.1016/S0304-405X(00)00072-6

- Bencivenga, V. R., & Smith, B. D. (1991). Financial intermediation and endogenous growth. The Review of Economic Studies, 58(2), 195–209. doi:10.2307/2297964

- Berthelemy, J. C., & Varoudakis, A. (1996). Economic growth, convergence clubs, and the role of financial development. Oxford Economic Papers, 48(2), 300–328. doi:10.1093/oxfordjournals.oep.a028570

- Bist, J. P.(2018). Financial development and economic growth: Evidence from a panel of 16 African and non-African low-income countries. Cogent Economics & Finance, 6(1), 1449780. doi:10.1080/23322039.2018.1449780

- Brock, W. A., Dechert, W. D., & Scheinkman, J. A. (1987). A test for independence based on the correlation dimension. Working Paper No.870, Social Systems Research Institute, University of Wisconsin-Madison.

- Cecchetti, S. G., & Kharroubi, E.. (2012). Reassessing the impact of finance on growth. Bank for International Settlements Working Paper No. 381. Available at https://www.bis.org/publ/work381.pdf

- Charfeddine, L., & Goaied, M. (2019). Tourism, terrorism and political violence in Tunisia: Evidence from Markov-switching models. Tourism Management, 70, 404–418. doi:10.1016/j.tourman.2018.09.002

- Charfeddine, L., & Guegan, D. (2011). Which is the best model for the US inflation rate: A structural change model or a long memory process? The IUP Journal of Applied Economics, 10(1), 5–25.

- Charfeddine, L., & Mrabet, Z. (2015). Trade liberalization and relative employment: Further evidence from Tunisia. Eurasian Business Review, 5(1), 173–202. doi:10.1007/s40821-015-0020-6

- Christopoulos, D. K., & Tsionas, E. G. (2004). Financial development and economic growth: Evidence from panel unit root and co-Integration tests. Journal of Development Economics, 73, 55–74. doi:10.1016/j.jdeveco.2003.03.002

- Deidda, L., & Fattouh, B. (2002). Non-linearity between finance and growth. Economics Letters, 74(3), 339–345. doi:10.1016/S0165-1765(01)00571-7

- Demetriades, P., & Hook Law, S. (2006). Finance, institutions and economic development. International Journal of Finance and Economics, 11(3), 245–260. doi:10.1002/(ISSN)1099-1158

- Demetriades, P. O., & Hussein, K. A. (1996). Does financial development cause economic growth? Time series evidences from 16 countries. Journal of Development Economics, 51, 387–411. doi:10.1016/S0304-3878(96)00421-X

- Demetriades, P. O., & Rousseau, P. L. (2016). The changing face of financial development. Economics Letters, 141, 87–90. doi:10.1016/j.econlet.2016.02.009

- Demirgu¨ c¸-Kunt, A., Feyen, E., & Levine, R. (2013). The evolving importance of banks and securities markets. The World Bank Economic Review, 27(3), 2013 476–490. doi:10.1093/wber/lhs022

- Doumbia, D. (2016). Financial development and economic growth in 43 advanced and developing economies over the period 1975–2009: Evidence of non-linearity. Applied Econometrics and International Development, 16, 13–22.

- Fallahi, F. (2011). Causal relationship between energy consumption (EC) and GDP: A Markov-switching (MS) causality. Energy, 36(7), 4165–4170. doi:10.1016/j.energy.2011.04.027

- Farooq, A., Shahbaz, M., Arouri, M., & Teulon, F. (2013). Does corruption impede economic growth in Pakistan? Economic Modelling, 35, 622–633. doi:10.1016/j.econmod.2013.08.019

- Gerschenkron, A. (1962). Economic backwardness in historical perspective: A book of essays (No. 330.947 G381). Cambridge, MA: Belknap Press of Harvard University Press.

- Greenwood, J., & Jovanovic, B. (1990). Financial development, growth, and the distribution of income. Journal of Political Economy, 98(5, Part 1), 1076–1107. doi:10.1086/261720

- Hamilton, J. D. (1990). Analysis of time series subject to changes in regime. Journal of Econometrics, 45(1–2), 39–70. doi:10.1016/0304-4076(90)90093-9

- Hsu, P. H., Tian, X., & Xu, Y. (2014). Financial development and innovation: Cross-country evidence. Journal of Financial Economics, 112(1), 116–135. doi:10.1016/j.jfineco.2013.12.002

- Ibrahim, M. H. (2015). Oil and food prices in Malaysia: A nonlinear ARDL analysis. Agricultural and Food Economics, 3(1), 2. doi:10.1186/s40100-014-0020-3

- Jalil, A., & Feridun, M. (2011). Impact of financial development on economic growth: Empirical evidence from Pakistan. Journal of the Asia Pacific Economy, 16(1), 71–80. doi:10.1080/13547860.2011.539403

- Jalil, A., & Ma, Y. (2008). Financial development and economic growth: Time series evidence from Pakistan and China. Journal of Economic Cooperation, 29(2), 29–68.

- Jude, E. C. (2010). Financial development and growth: A panel smooth regression approach. Journal of Economic Development, 35(1), 15–33. doi:10.35866/caujed

- Khan, M., Qayyum, A., & Sheikh, S. (2005). Financial development and economic growth: The case of Pakistan. The Pakistan Development Review, 44(4), 819–837. doi:10.30541/v44i4IIpp.819-837

- Khan, M. A. (2008). Financial development and economic growth in Pakistan: Evidence based on autoregressive distributed lag (ARDL) approach. South Asia Economic Journal, 9(2), 375–391. doi:10.1177/139156140800900206

- Khan, M. M. S., & Senhadji, M. A. S. (2000). Financial development and economic growth: An overview. IMF Working Paper No. WP/00/29, International Monetary Fund Washington DC. doi:10.5089/9781451874747.001

- King, R. G., & Levine, R. (1993). Finance and growth: Schumpeter might be right. The Quarterly Journal of Economics, 108(3), 717–737. doi:10.2307/2118406

- Lal, I., Muhammad, S. D., Hussain, A., & Jalil, M. A. (2009). Effects of financial structure and financial development on economic growth: A case study of Pakistan. European Journal of Social Sciences, 11(3), 419–427.

- Levine, R. (1991). Stock markets, growth, and tax policy. The Journal of Finance, 46(4), 1445–1465. doi:10.1111/j.1540-6261.1991.tb04625.x

- Levine, R. (1997). Financial development and economic growth: Views and Agenda. Journal of Economic Literature, 35(2), 688–726.

- Levine, R. (2005). Finance and growth: Theory and evidence. Handbook of Economic Growth, 1, 865–934.

- Lucas, R. E., Jr. (1988). On the mechanics of economic development. Journal of Monetary Economics, 22(1), 3–42. doi:10.1016/0304-3932(88)90168-7

- Luintel, K. B., & Khan, M. (1999). A quantitative reassessment of the finance–growth nexus: Evidence from a multivariate VAR. Journal of Development Economics, 60(2), 381–405. doi:10.1016/S0304-3878(99)00045-0

- Mahmood, A. (2013). Impact of financial development on the economic growth of Pakistan. Abasyn Journal of Social Sciences, 6(2), 106–116.

- McKinnon, R. I. (1973). Money and capital in economic development. Washington DC: Brookings Institution.

- Mian, A., & Sufi, A. (2014). House of debt: How they (and you) caused the Great Recession, and how we can prevent it from happening again. London: Publisher location is “The University of Chicago Press, Ltd., London”.

- Naceur, S. B., & Ghazouani, S. (2007). Stock markets, banks, and economic growth: Empirical Evidence from the MENA region. Research in International Business and Finance, 21, 297–315. doi:10.1016/j.ribaf.2006.05.002

- Narayan, P. K., & Narayan, S. (2013). The short-run relationship between the financial system and economic growth: New evidence from regional panels. International Review of Financial Analysis, 29, 70–78. doi:10.1016/j.irfa.2013.03.012

- Naveed, S., & Mahmood, Z. (2019). Impact of domestic financial liberalization on economic growth in Pakistan. Journal of Economic Policy Reform, 22(1) 16-34. doi:10.1080/17487870.2017.1305901.

- Odedokun, M. O. (1996). Alternative econometric approaches for analysing the role of the financial sector in economic growth: Time-series evidence from LDCs. Journal of Development Economics, 50(1), 119–146. doi:10.1016/0304-3878(96)00006-5

- Rajan, R. G., & Zingales, L. (1998). Financial dependence and growth. The American Economic Review, 88(3), 559–586.

- Rehman, W., Fatima, G., & Ahmad, W. (2011). An empirical analysis of financial reforms in Pakistan: Does it affect economic growth?. International Journal of Trade, Economics and Finance, 2(4), 341–345. doi:10.7763/IJTEF.2011.V2.128

- Rioja, F., & Valev, N. (2004). Does one size fit all?: A reexamination of the finance and growth relationship. Journal of Development Economics, 74(2), 429–447. doi:10.1016/j.jdeveco.2003.06.006

- Rioja, F., & Valev, N. (2014). Stock markets, banks and the sources of economic growth in low and high income countries. Journal of Economics and Finance, 38(2), 302–320. doi:10.1007/s12197-011-9218-3

- Rousseau, P. L., & Wachtel, P. (2001). Inflation, financial development and growth. In Economic theory, dynamics and markets (pp. 309–324). Boston, MA: Springer.

- Rousseau, P. L., & Wachtel, P. (2011). What is happening to the impact of financial deepening on economic growth? Economic Inquiry, 49(1), 276–288. doi:10.1111/ecin.2011.49.issue-1

- Saint-Paul, G. (1992). Fiscal policy in an endogenous growth model. The Quarterly Journal of Economics, 107(4), 1243–1259. doi:10.2307/2118387

- Samargandi, N., Fidrmuc, J., & Ghosh, S. (2015). Is the relationship between financial development and economic growth monotonic? Evidence from a sample of middle-income countries. World Development, 68, 66–81. doi:10.1016/j.worlddev.2014.11.010

- Schularick, M., & Taylor, A. M. (2012). Credit booms gone bust: Monetary policy, leverage cycles, and financial crises, 1870–2008. American Economic Review, 102(2), 1029–1061. doi:10.1257/aer.102.2.1029

- Schumpeter, J. (1912). The theory of economic development: An inquiry into profits, capital, credit, interest and business cycle. Cambridge Mass: Harvard University Press.

- Shaw, E. S. (1973). Financial deepening in economic development. New York: Oxford University Press.

- Shen, C. H., & Lee, C. C. (2006). Same financial development yet different economic growth-why? Journal of Money, Credit, and Banking, 38(7), 1907–1944. doi:10.1353/mcb.2006.0095

- Singh, A. (1997). Financial liberalization, stock markets and economic development. The Economic Journal, 107(442), 771–782. doi:10.1111/j.1468-0297.1997.tb00042.x

- Stolbov, M. (2013). The finance-growth nexus revisited: From origins to a modern theoretical landscape. Economics: The Open-Access, Open-Assessment E-Journal, 7(2013–2), 1–22.

- Svirydzenka, K. (2016). Introducing a new broad-based index of financial development. Working Paper No.16/5, International Monetary Fund. doi:10.5089/9781513583709.001

- Tahir, M. (2008). An investigation of the effectiveness of financial development in Pakistan. Lahore Journal of Economics, 13(2), 27–44. doi:10.35536/lje.2008.v13.i2.a2

Appendix A

Table A: A Literature review on finance-growth nexus in Pakistan