Abstract

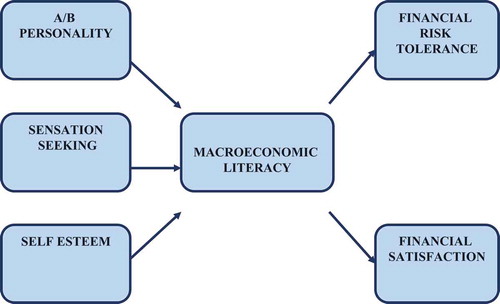

The purpose of the current research was to analyze the impact of biopsychosocial indicators on the financial risk tolerance (FRT) and financial satisfaction along with the mediating role of macroeconomic literacy in these associations. For this purpose, three indicators names as “personality type, self-esteem, and sensation seeking” were used to check the impact of biopsychosocial indicators on FRT and financial satisfaction. The current study was conducted in China where the data was collected from retail investors through structured questionnaire. The purposive sampling technique was used to decide the sample from the population. The data were collected from 1134 retail investors and SPSS and AMOS were used to analyze the data by applying SEM. Findings of the current study revealed that the personality, self-esteem and sensation seeking have significant influences on FRT. It has been further found that the personality type and self-esteem have significant influences on the financial satisfaction. Results further confirmed the mediating role of macroeconomic literacy between self-esteem and FRT, personality type and FRT, self-esteem and financial satisfaction, and personality type and financial satisfaction. However, no significant mediating role of macroeconomic literacy was found between sensation seeking and FRT, and sensation seeking and financial satisfaction. The current study and findings will be of great importance for theory and practice regarding financial/investment decision making and FRT.

PUBLIC INTEREST STATEMENT

This study focuses on the biopsychosocial factors of the financial risk tolerance (FRT) and satisfaction. Furthermore, it aims that how the indicators used in his study have affected the retail investors. . The practical contribution of the current study will be realized among retail investors because they will get assistance through the current study and its findings that how their personality, self-esteem, and sensation seeking can determine their FRT and financial satisfaction. The policy makers of China and other countries can also get considerable assistance through the suggestions of the current study while making macroeconomic and investment policies.

1. Introduction

In modern era with a lot of continuous financial as well as non-financial fluctuations, the factors of FRT and financial satisfaction entail a large importance that are derived by a number of factors. FRT and financial satisfaction entail a great importance in the decision making process regarding any investment or financial activity. There are four elements that tend to determine the financial or investment decision that are “goals, financial stability, time horizon, and financial risk tolerance.” Among these determining elements of investment or financial decisions, the FRT is of key concern in the current research because the risk tolerance is very necessary in modern world for investors. The risk tolerance pays off to the investor in form of various positive outcomes including higher returns, higher satisfaction, and wealth accumulation etc. (Larkin, Lucey, & Mulholland, Citation2013). Due to the great importance of the FRT in the financial decision making process, modern researcher have been extensively attracted to this domain and therefore, different studies are found in existing literature in which different antecedents and consequences of FRT have been examined (Awais, Laber, Rasheed, & Khursheed, Citation2016; Finke & Huston, Citation2003; Hvide & Panos, Citation2014; Kannadhasan, Aramvalarthan, Mitra, & Goyal, Citation2016; Kuzniak, Citation2016). However, there is scarcity of specific literature about the role of different biopsychosocial factors in determining the FRT and financial satisfaction of investors. The FRT mainly refers to the willingness of investors to embrace the negative fluctuations in the value of his/her investment and to accept the adverse outcomes that might be different from the expected outcomes. The FRT can facilitate the achievement of financial goals, wealth accumulation, and proper portfolio allocation (Bossone, Citation2019; Hoque, Wong, & Carducci, Citation2015). The association of assessment of FRT of investors is essentially needed to align the investment decision with the goals and preferences of investors because the factor of FRT varies from investor to investor. Some investors have high level of FRT so, they are always willing to make an investment decisions in which uncertainties are high while some other investors have lower level of FRT as they are always unwilling to make an investment or financial decision, which involves uncertainties (Larkin et al., Citation2013).

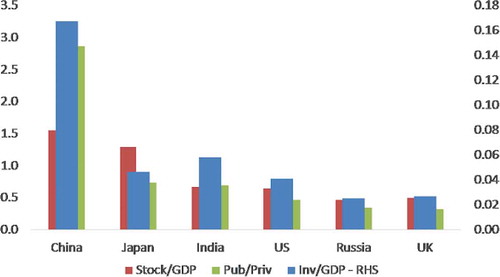

Above-mentioned figure presenting the china ratio of microeconomic literacy among six countries, and this was more than 3.0.There are different factors that play a great role in determining the FRT of an investor including social, environmental, psychological, and other individual factors. Past studies have attempted to investigate different factors and traits that are associated with FRT e.g., (Grable & Joo, Citation2004; Hoque et al., Citation2015). However, the current literature seems to be limited about the empirical evidences of the linkage between biopsychosocial indicators and FRT because there is very limited literature about the assessment of FRT through biopsychosocial indicators. Biopsychosocial indicators refer to the demographic, social, and cultural factors because they involve personality traits, birth order, age, gender, and ethnicity. This classification of factors involved in assessment of FRT was performed by Irwin (Citation1993) who classified these indicators in two main categories named as “environmental factors” and “biopsychosocial factors.” The phenomenon through which the biopsychosocial factors influence the FRT of an individual investor is relatively unexplained as compared to other factors (Kannadhasan et al., Citation2016). Therefore, the first objective of the current research is to analyze the impact of biopsychosocial factors on the FRT of investor. To meet this objective, the A/B personality, sensation seeking, and self-esteem are analyzed in terms of their impact on FRT.

Another factor, which entails a great role in financial or investment decision making is the financial satisfaction, which refers to the perceived fulfillment of financial objectives. The financial satisfaction is of great concern in modern era where it is very difficult to cope with financial uncertainties therefore, there is need to investigate the factors that can contribute to the financial satisfaction of investors (Archuleta, Dale, & Spann, Citation2013). To respond to this need, the second objective of the current study is to assess the influence of biopsychosocial factors (A/B personality, sensation seeking, and self-esteem) on the financial satisfaction of investor. The macroeconomic literacy has the potential to link these factors with FRT and financial satisfaction because the macroeconomic literacy refers to the knowledge and awareness of the macroeconomic concepts. When an investor is better able to understand and evaluate the macroeconomic trends then he/she is in better position to enhance his/her FRT and financial satisfaction. The macroeconomic literacy enables the investor to predict and accept the negative fluctuations, which means that the macroeconomic literacy has the potential to enhance the FRT. Furthermore, having awareness about the macroeconomic trends and concepts, an investor becomes better able to link his/her negative or positive financial outcomes with macroeconomic trends so, the level of financial satisfaction of investor increases. It means that the macroeconomic literacy entails a great importance in determining the FRT and financial satisfaction of investors (Baker & Ricciardi, Citation2014; Lipshits, Barel-Shaked, & Ben-Zion, Citation2019). However, the macroeconomic literacy also depends on different individuals and social factors. The biopsychosocial factors under current examination including the A/B personality, sensation seeking, and self-esteem tend to influence the macroeconomic literacy of individuals. However, this mediation of macroeconomic literacy has not been efficiently explained in past literature. Therefore, another objective of the present research is to analyze the mediating role of macroeconomic literacy in the relationship between biopsychosocial factors and FRT and between biopsychosocial factors and financial satisfaction. Although, a very few past studies have examined the role of biopsychosocial factors in the FRT however, the impacts of these factors on FRT and financial satisfaction have not been examined in a combined research ever before. Therefore, the current study will offer a unique contribution to the existing literature regarding FRT, financial satisfaction, and financial/investment decision making.

The remaining part of this paper consists of four sections including literature review, research methods, analysis &findings, discussion of findings, and conclusion of this study.

2. Literature review

2.1. Prospect theory

Prospect theory also called as risk aversion theory is a psychological theory that involves the process of decision making in the conditions of risk. This theory was established by Daniel and Amos and was first published in 1979 in Econometrica (Abdellaoui, Bleichrodt, l’Haridon, & Van Dolder, Citation2016). This theory is based on human psychological behaviors in decision-making process. This theory was originally based on a series of financial bets and gambling instead of economic decision making. But over the time it undergone certain changes and now it is used to study human behavior while making decisions. Prospect theory has two phases, which include an editing phase and an evaluation phase. We are familiar with the decision making process in which we encounter a certain problem, identify some relative criteria, give weight age to that criteria, develop different alternatives, evaluate them and then select the best alternatives (Barberis, Citation2013). As this theory is based on decision making so its first phase i.e., editing phase means that a person having some problem has different options for its solution and one of the best options can be chosen. The second phase involves the complete screening of those options available for solution. This screening or evaluation is done on the basis of some already decided criteria. By giving weight ages to the options available and scoring them, the option with the highest score is selected and used to solve the problem. This decision making depends upon a number of factors, one of which is bio psychosocial indicators. Bio psychosocial indicators include type A/B personality, sensation seeking, and self-efficacy (Kai-Ineman & Tversky, Citation1979). These different indicators lead to different behaviors of people in response to certain problems because people make expectations and evaluate alternatives available on the basis on these indicators. Knowledge of macroeconomics which include different monetary policies, different economic aspects such as interest rate, unemployment etc. and their ultimate effects on a country’s economy is also involved in the decision making process of people. Having better macroeconomic literacy leads to more rational decisions (Muth, Citation1961). Risks are an important factor in this regard where people have to deal with risks by using their personality type and literacy of macroeconomic policies. So, all the above-mentioned aspects are based on the prospect theory. This theory can also be used to study different relationships between the above-mentioned variables i.e., bio psychological indicators, macroeconomic literacy, FRT and satisfaction (Rieger, Wang, & Hens, Citation2014).

2.2. Impact of bio psychosocial indicators on FRT

Researches have shown that personality traits are an important factor to consider while studying the human behavior of decision making. According to MBTI model of personality traits, each person has specific features which indicate that how that person will react under specific circumstances. For example, there two types of investors i.e., active and passive (Grable & Lytton, Citation1999). Passive investors earn money with little effort and by investing others money while active investors work hard for earning money and invest their own capital we can say that although the risk is same for both active and passive investors, but as active investors have invested in their own capital they have more tolerance of risk as compared to passive investors. In the current study, we will be discussing type A/B personality traits in decision-making process (Grable, Citation2000). First, we will discuss the difference between type A and type B people. Type A people are consistent, competitive, hardworking, aggressive, and time constrained. On the other hand, type B people are much relaxed, calm, and easy going. From these properties it is quite clear that type A people are having more tolerance to risks as compared to type B. similarly, type A people are more attracted towards success as it is very valuable for them while type B people are contented with being average. A few studies have been conducted to show the relationship between A/B personality traits and FRT (Hallahan, Faff, & McKenzie, Citation2004). These studies have shown that type A investors are more risk tolerant than type B ones because they have better knowledge, experience and they possess more capital. The other BPS indicator which is sensation seeking refers to the seeking of new and unique experiences and tolerating risks for them. We can say that this trait occurs as a result of some chemical reaction in brain, which stimulates excitement in that person’s mind. This excitement compels him to take new risks, which make him satisfied. This trait can be experienced while travelling to some adventurous spot or in some gambling activity (Jacobs-Lawson & Hershey, Citation2005). Financial investment is another important aspect of this personality trait. Studies have revealed that the people with sensation seeking traits are more tolerant to risks as compared to the people with no sensation seeking. Financial risk behavior can easily be studied under this trait. We have another BPS indicator, self-esteem. It refers to confidence in oneself to have the required capabilities to achieve some goals. It is not necessary that self-esteem is only positive, it may be negative too (Yao, Gutter, & Hanna, Citation2005). People with positive self-esteem have confidence in themselves on the other hand people with negative self-esteem are always confused and scared of consequences. Researches have shown that the people with positive self-esteem are more tolerant to risks as compared to people with negative self-esteem. As we know that any investment has its results in the future, so investors have to deal with the risks associated with investments (Yao, Hanna, & Lindamood, Citation1983). If, for example, the investors face loss in their investment, the people having high self-esteem take it positively well as compared to the people with negative self-esteem. Also, high self-esteem people don’t regret that they get into loss because it will ultimately lower they self-esteem, which is a valuable asset for them. Prospect theory is also based on the effects of these indicators on FRT (Smith & Stewart, Citation1963). Researches have shown that self-esteem affects the level of risk tolerance in one way or the other. We can generate the following hypothesis:

H1: Bio psychosocial indicators have significant impact on financial risk tolerance

H1 (a): A/B personality has significant impact on financial risk tolerance

H1 (b): Sensation seeking has significant impact on financial risk tolerance

H1 (c): Self-esteem has significant impact on financial risk tolerance

2.3. Impact of bio psychosocial indicators on financial satisfaction

Financial satisfaction refers to the contentedness of a person’s financial situation. In this era with a large number of financial risks, it has become very difficult to cope with them and be satisfied with financial condition. So it is very important to study the aspects which contribute to the financial satisfaction (Archuleta et al., Citation2013). In the current study, we will be focusing on some of the BPS indicators which include A/B personality, self-esteem and sensation seeking. As we know that type A and B personalities have different qualities which ultimately affect financial satisfaction. Type A people are more competitive, hardworking and aggressive toward their work while type B people are relaxed, easy going and work under minimum pressure. Studies have shown that type A people are more satisfied financially because they have confidence in their hard work which eventually pays off. Even if they face some loss, they keep their spirits high and work even harder in future to get desired results (Joo & Grable, Citation2004). They are time constrained, i.e. they tend to complete their work within time, which ultimately benefits them in the form of financial satisfaction, because when they complete their tasks they get paid for it and may also get bonuses for showing better performances. They are risk tolerant so they can be satisfied even if they experience some loss in an investment, they can handle it very well (Xiao, Tang, & Shim, Citation2009). Sensation seeking people are always discovering new ways to experience some adventure and in financial context, they take risks to invest money somewhere even if they are not certain about the consequences. But usually these consequences result into something positive and cause financial satisfaction. Self-esteem in another indicator of BPS, which has impact on financial satisfaction (Zeger & Liang, Citation1986). People having positive self-esteem are much confident for their hard work and thus receive fruitful results. Even if they experience something negative, they tend to channelize into something positive to keep their spirit high. Otherwise their self-esteem will be lowered. This positive attitude towards self-esteem results into financial satisfaction of the person. Prospect theory also has some implications towards the relationship between BPS indicators and self-satisfaction in context of the people’s expectations towards future events (Von Neumann & Morgenstern, Citation1953). All the above discussion indicates that there is impact of BPS indicators on financial satisfaction. We can develop following hypothesis:

H2: Bio psychosocial indicators have significant impact on financial satisfaction

H2 (a): A/B personality has significant impact on financial satisfaction

H2 (b): Sensation seeking has significant impact on financial satisfaction

H2 (c): Self-esteem has significant impact on financial satisfaction

2.4. Mediating role of macroeconomic literacy between bio psychosocial indicators and FRT

Macroeconomics literacy refers to the appropriate knowledge about certain macroeconomic concepts such as fiscal and monetary policy, interest rates, unemployment etc. for better formation of expectations towards the future events and the effect of these expectations on the economy of the country (Hanley, Negassa, Edwardes, & Forrester, Citation2003). Poor literacy of macroeconomics leads to the ineffective monetary policies introduced by govt. as people are not aware of their consequences. Basically, the microeconomics literacy is based on the formation of expectations about certain things such as investment, saving, unemployment etc. these expectations are aided by different BPS indicators. We will be studying the mediating role of macroeconomic literacy between BPS indicators and FRT under the light of prospect theory (Wang & Fischbeck, Citation2004). Type A/B personality people have different attitudes toward the macroeconomic literacy ML. Type A people are competitive, hardworking, and confident so they tend to keep themselves aware of different aspects related to economics. As all the investors have to deal with those economic aspects such as investment, saving, interest rates etc., so having knowledge about them is necessary to perform better. This leads to higher ML rate in type A people (Kahneman & Tversky, Citation2013). On the other hand, type B people are relatively relaxed and calm and they do not bother much about having knowledge about economic concepts so they show less literacy of economic concept. We can conclude that higher ML leads to more risk tolerance. Sensation seeking people are always looking for new and unique ways to utilize their skills so they ultimately tend to have more knowledge about the latest concepts about economics leading to higher ML rate. As they are aware of these concepts, so they make their expectations accordingly and thus high ML rate results in high FRT (Stanovich, Citation2016). Self-esteemed people have confidence in their abilities so with minimum efforts they acquire most of the aspects of macro economy and work according to them. Due to their confidence and high ML, they become tolerant to financial risks. So, we can conclude that ML has important mediating role between BPS indicators and FRT (Thaler, Citation1999). We can conclude the following hypothesis:

H3: Macroeconomic literacy has significant mediating role between Bio psychosocial indicators and financial risk tolerance

H3 (a): Macroeconomic literacy has significant mediating role between A/B personality and financial risk tolerance

H3 (b): Macroeconomic literacy has significant mediating role between Sensation seeking and financial risk tolerance

H3 (c): Macroeconomic literacy has significant mediating role between Self-esteem and financial risk tolerance

2.5. Mediating role of macroeconomic literacy between bio psychosocial indicators and financial satisfaction

Macroeconomic literacy can be related to different BPS indicators. Type A/B personality has different impacts on ML rate because type A people have higher tendency to acquire ML owing to their competitiveness and strong will power. On the other hand, B type people are not that much into learning about economic factors (Bar-Hillel & Procaccia, Citation2011). They just remain contented with what they currently have unlike type A people. As a result, type A people work according to economic factors which ultimately give financial benefits and they have high financial satisfaction owing to their high ML rate. Researches have shown that sensation-seeking people have high ML rate because they are always trying to do something innovative and learn new things (Burke & Manz, Citation2014). This high ML rate results in financial satisfaction because they are contented with their sensation seeking abilities. Studies have shown the significant impact of self-esteem on financial satisfaction. Mediating role of ML is also very important in this regard (Frederick, Citation2005). People with positive self-esteem have enough confidence in their abilities, still they learn more and more about economic conditions so that they can make decisions according to them. This increases ML rate in them and as their decisions give financial benefits, they feel financially satisfied. Prospect theory has major role in decision making of people which can be evaluated on the basis of BPS indicators (Yaari, Citation1987).The theory has explained that ML significantly participates in increasing the level of financial satisfaction. The theory has taken this concept as a base that having the prospect knowledge and the literacy regarding macroeconomic factors, one can gain higher level of satisfaction financially moreover, the theory not only discussed how ML can enhance the financial satisfaction but also explained that how biopsychosocial indicators work to enhance the ML in the first place, so in this theory, the impact of ML is discussed as a mediator between biopsychosocial indicators and financial satisfaction. This discussion shows important mediating role of ML between BPS indicators and financial satisfaction. We can develop the following hypothesis:

H4: Macroeconomic literacy has significant mediating role between Bio psychosocial indicators and financial satisfaction

H4 (a): Macroeconomic literacy has significant mediating role between A/B personality and financial satisfaction

H4 (b): Macroeconomic literacy has significant mediating role between Sensation seeking and financial satisfaction

H4 (c): Macroeconomic literacy has significant mediating role between Self-esteem and financial satisfaction

2.6. Framework of study

2.6.1. Prior Published Papers

Following table has a look on prior published papers related to this study topic and discussed results and methods of already published papers.

3. Methodology

3.1. Population and sampling

The current study has been conducted to assess the impact of biopsychosocial indicators on the FRT and financial satisfaction along with the mediating role of macroeconomic literacy in these relationships. To complete this study, the study was conducted in China so, the population of the current study consists of retail investors of China. The sample was selected through purposive sampling because:

The purpose of the current study was to assess the individual factors of investors that determine their FRT and financial satisfaction. The key reason for selecting the retail investors of China for this study was the consistently growing number of retail investors in China. Therefore, there was need to study the factors that enhance the FRT and financial satisfaction of Chinese investors. The sample size was 1470 because the data were collected from 1470 retail investors of China. Out of 1470 questionnaires, 336 questionnaires were returned and after screening, 1134 responses were used for analysis.

3.2. Data collection and procedures

The data collection tool used for the current study was “structured questionnaire” because it was the most suitable tool to collect data about FRT, financial satisfaction, macroeconomic literacy, self-esteem, sensation seeking, and personality type. The questionnaire was developed by using Chinese language so that the Chinese investors could understand it. When, questionnaire was finalized it sent to retailer through emails, LinkedIn accounts and Facebook accounts to collect more data in efficient way. Furthermore, the content validity of the scale was properly checked. The researcher collected data through self-administered questionnaire. The specific data collection method was used so that the questions will already be defined about the different variables and respondents will be open for their opinion to reply to the questions. The questionnaires were sent to the respondents by a virtual way like the researcher sent the questionnaires to the Chinese respondents by emailing them, and the emails were extracted from the databases of the Chinese investors, moreover, the researcher also followed the LinkedIn accounts of those Chinese investors with the help of the emails that were extracted lastly, the researcher also followed the Facebook accounts of those Chinese investors with the help of the emails extracted. After all of these extractions, the researcher sent the questionnaires to all of the Chinese investors selected as a sample on Facebook and LinkedIn accounts as well.

3.3. Validity, reliability and common bias method

The validity and reliability of the data and scales were checked in the current study through AMOS and SPSS. The indicators of Cronbach alpha and CR have been used to assess the reliability of data while the convergent validity was checked through three key criteria i.e. items loading which must be greater than 0.70, composite construct reliability which should be greater than 0.80 and average variance extracted which should be greater than 0.50. The discriminant validity was assessed by ensuring that the square root of AVE should be greater when correlated with other constructs. The method of Donaldson and Grant-Vallone (Citation2002) and Donaldson and Grant-Vallone (Citation2002) was used to eliminate the issue of common method bias. The “Harman’s single factor test” was applied to ensure the inexistence of this issue so, the risk of common method bias has been eliminated.

3.4. Measurement of variables

There are six variables in the current study i.e. A/B personality type, self-esteem, and sensation seeking as independent variables, financial satisfaction and FRT as dependent variables and macroeconomic literacy as a mediator. All three independent variables (i.e. A/B personality type, self-esteem, and sensation seeking) and the FRT were measured by using the measurement scales adopted by Kannadhasan et al. (Citation2016). The financial satisfaction was measured by using the scale adopted by Kirbiš, Vehovec, and Galić (Citation2017). The macroeconomic literacy was measured by using the measurement method adopted by Lipshits et al. (Citation2019).

3.5. Hypothesis testing

The analysis was completed through SPSS and AMOS. To check the hypotheses of the current study, the structural equation modeling was used through which the indirect, direct, and total effects of self-esteem, sensation seeking, and personality on financial satisfaction and FRT were found. Based on the significance of results, the decision about the acceptance or rejection of hypotheses was made. Before applying SEM, the model fitness was checked though AMOS.

4. Findings

The current study is about the impact of biopsychosocial indicators on the FRT and financial satisfaction with the mediating role of macroeconomic literacy. For this purpose, the data collected from 1134 retail investors was put into analysis to assess the hypotheses of the current study. The demographic analysis revealed that out of 1134 respondents, there were 432 males and 702 females. It means that the proportion of female investors in the current sample was greater than that of male investors. The demographic of education revealed that there were 48.8% investors in the current sample who were post graduated and 40.3% investors who were Master degree holders. The education of 7.6% respondents was graduation while the least number of respondents (3.3%) were having other qualification. It means that most of the respondents of the current study were literate people and were having high qualifications. The age of most of the respondents was between 21 and 30 years (82.5%) while 13.9% investors were of age ranging from 31 to 40 years. There were 3% investors who were of age ranging from 41 to 50 years however, there were the least number of respondents (i.e. 0.7) who were of age more than 50 years.

4.1. Descriptive statistics

The descriptive statistics of the current variables have been presented in Table in which the mean value, skewness, and standard deviation are key indicators considered to make decision about the normality and adequacy of the current data.

Table 1. Descriptive Statistics

The results of descriptive analysis are indicating that mean value of all current variables including A/B personality, sensation seeking, self-esteem, macroeconomic literacy, FRT and financial satisfaction are lying between their respective minimum value and maximum value. It depicts that there is no extreme value in the data of any of these variables so, it is confirmed that there is no outlier in the data. Further adequacy and normality of data is confirmed through the value of skewness, which should be between −1 and +1. The results are confirming that there is normality in the data because statistics of skewness of all variables is ranging from −1 to +1. The standard deviation against all variables is also indicating that there is acceptable variation in the data so, the adequacy, normality, and acceptability of the data is confirmed. Further suitability of data was proved by KMO and Bartlett’s test (see Table ).

Table 2. KMO and Bartlett’s Test

The value of KMO for the current data is 0.947, which is more than 0.6, and the significance value in Bartlett’s test is less than 0.01. It means that the suitability of the current data is confirmed.

4.2. Reliability, convergent validity and discriminant validity

To assess the reliability of the current data, the indicator of composite reliability was checked while the internal consistency and multicollinearity were checked through AVE, MSV, and correlations. The results of convergent and discriminant validity have been presented in Table .

Table 3. Convergent Validity and Discriminant Validity

The value of CR for A/B personality, sensation seeking, self-esteem, macroeconomic literacy, FRT, and financial satisfaction is more than 0.7, which means that all scales are reliable. The AVE of all variables is more than 0.7, which is showing that more than 50% variation has been explained by these variables. The value of MSV for all of them is less than their respective AVEs so, these results are confirming the convergent validity of data. The results of correlation can be seen in Table to confirm that each variable has the highest correlation with itself than its correlation with any other variable. For instance, the correlation of macroeconomic literacy with itself is 0.896 while its correlations with all other variables are less than 0.896. Hence, the discriminant validity of the current data is also confirmed.

4.3. Confirmatory Factor Analysis (CFA)

To check the model fitness of the current model containing A/B personality, sensation seeking, self-esteem, macroeconomic literacy, FRT, and financial satisfaction, the CFA was applied on the current data through which the results given in Table were found.

Table 4. CFA

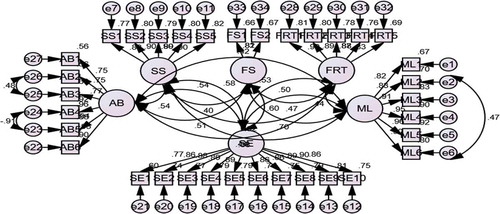

The results of model fitness indicate that value of CMIN/DF is <3, GFI is 0.810 (i.e. >0.80), CFI is 0.941 (i.e. >0.90), IFI is also >0.90, and the RMSEA is less than 0.08. It means that resulting values of all indicators are falling within threshold range so, the current model is goof fit. Figure and Figure represents the CFA of the current study.

Figure 1. Macroeconomic literacy

Figure 2. CFA

4.4. Structural equation modeling

To check the hypotheses of the current study, the SEM was performed through which the direct, indirect and total effects of variables were computed. Table provides the summary of results of SEM.

Table 5. SEM Results

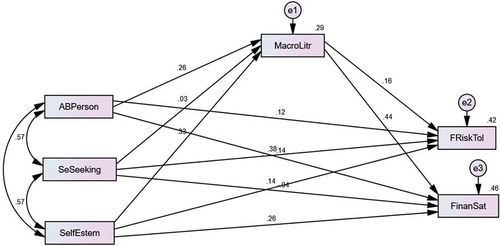

The results of SEM are depicting that A/B personality has a significant positive impact on FRT and a significant positive impact on financial satisfaction. The impacts of self-esteem on FRT and FS are also significant and positive. The sensation seeking has a significant positive impact on FRT and however, it has no significant impact on financial satisfaction. It can be seen that the total effects of self-esteem on FRT and financial satisfaction, and the total impacts of A/B personality on the FRT and financial satisfaction are not equal to their respective direct effects. However, the total impact of sensation speaking on FRT is equal to its direct impact on FRT. The inequality of direct and total effects of self-esteem and A/B personality reveal that there is some sort of mediation between their relationships. The indirect impacts of self-esteem on financial satisfaction and FRT are significant and positive which is due to the macroeconomic literacy. The indirect impact of sensation seeking on FRT and financial satisfaction is insignificant which means that there is no mediation of any variable between these relationships. The indirect impacts of A/B personality on financial satisfaction and FRT are also significant which means that there is some mediating impact. The significant indirect impacts on financials satisfaction and FRS in these relationships are caused by macroeconomic literacy because it has significant positive impacts on financial satisfaction and macroeconomic literacy. Hence, the overall results of SEM reveal that the personality type has significant and positive impacts on FRT and financial satisfaction and significant mediation of macroeconomic literacy between both these relationships. Furthermore, the self-esteem has significant and positive impacts on financial satisfaction and FRT and significant mediation of macroeconomic literacy between both these relationships. Sensation seeking has a significant positive impact on FRT. Sensation seeking has no significant impact on financial satisfaction and there is no significant mediation of macroeconomic literacy in both relationships of sensation seeking. Figure represents the screenshot of SEM taken from AMOS.

Figure 3. SEM

5. Discussion of results

The current study was about the impact of biopsychosocial factors on FRT and financial satisfaction along with the mediating role of macroeconomic literacy. In response to the first hypothesis of the current study (i.e. A/B personality has significant impact on FRT), the data collected from retail investors of China revealed that there is significant positive impact of A/B personality on FRT. It has been found that the personality type determines the FRT of investors because the investors with personality type A are more likely to have higher FRT while the investors with personality type B are less likely to have higher FRT. These results are aligned with previous researches and their results e.g., (Grable & Lytton, Citation1999; Grable, Citation2000; Hallahan et al., Citation2004; Jacobs-Lawson & Hershey, Citation2005; Larkin et al., Citation2013). These studies provide theoretical support to the current findings by regarding the personality trait and type as an important aspect in FRT. The second hypothesis of the current study was “Sensation seeking has significant impact on financial risk tolerance.” This hypothesis has also been accepted because the results revealed that the sensation seeking behavior of investors lead them to be involved in risky situations and financial decisions so their, FRT is also higher than other investors without sensation seeking behavior. These results are also aligned with past findings for instance, Jacobs-Lawson and Hershey (Citation2005) also indicated that sensation seeking is an important indicators of high FRT. The third hypothesis of the current research was “Self-esteem has significant impact on financial risk tolerance.” The current findings led the researcher to accept this hypothesis because the results revealed that the self-esteem makes the investors to be involved in high-risk financial situations, which means that their FRT is high. These results regarding impact of self-esteem also find support from past studies and their results e.g., (Larkin et al., Citation2013; Smith & Stewart, Citation1963; Yao et al., Citation1983). Hence, it has been found that biopsychosocial indicators have significant effects on FRT.

The next hypothesis of this study was “A/B personality has significant impact on financial satisfaction,” which has been evidentially accepted through current results. It has been found that personality type significantly influences the FRT satisfaction of investors. These results find theoretical support from the findings of J. E. Grable and Joo (Citation2004) and Xiao et al. (Citation2009). The next hypothesis of the study was “Sensation seeking has significant impact on financial satisfaction.” The current results have revealed that this hypothesis is rejected because there was no significant impact on financial satisfaction reported by sensation seeking behavior of investors. These results are somehow contrary to the previous study of Hoque et al. (Citation2015). The reason behind this insignificant impact of sensation seeking on financial satisfaction may be due to the particular factors of Chinese investors studied in this study, i.e., environmental or demographic factors. The last hypothesis regarding the impact of biopsychosocial indicators on financial satisfaction was “Self-esteem has significant impact on financial satisfaction.” The results of the current study have supported this hypothesis so, this hypothesis is also accepted, and it is suggested that high self-esteem leads the investors to the high financial satisfaction. These findings get theoretical support from past findings e.g., (Kannadhasan et al., Citation2016; Larkin et al., Citation2013; Zeger & Liang, Citation1986). In response to the hypotheses regarding the mediating role of macroeconomic literacy in the relationships between biopsychosocial factors and FRT, the present findings revealed that H3 (a) and H3 (c) are accepted while H3 (b) is rejected. Hypothesis H3 (b), which was about mediating the role of macroeconomic literacy between sensation seeking and FRT. This hypothesis has been rejected because according to the results and analysis of the study, there is a significant relationship between macroeconomic literacy and FRT, because it is proved that the macroeconomic literacy puts a significant impact on FRT but the impact of SS on macroeconomic literacy is not significant so it can be concluded that the impact of macroeconomic literacy on FRT is significant but the impact of macroeconomic literacy as a mediator between SS and FRT was not significant, and there is no significant mediating role of macroeconomic literacy between sensation seeking and FRT while macroeconomic literacy plays the role of significant mediator in the relationship between A/B personality type and FRT and between self-esteem and FRT. Similarly, the current results have revealed that macroeconomic literacy is a significant mediator in the relationship between self-esteem and financial satisfaction and between personality and financial satisfaction however, it is not a significant mediator in the relationship between sensation seeking and financial satisfaction. Therefore, H4 (b) is rejected while H4 (a) and H4 (c) are accepted through the support of current results. The results regarding the mediating role of macroeconomic literacy in these relationships are largely supported by past studies of Lipshits et al. (Citation2019), Xu and Zia (Citation2012) and Awais et al. (Citation2016).

6. Conclusion

The aim of this research was to analyze the impact of biopsychosocial indicators on FRT and financial satisfaction along with the mediating role of macroeconomic literacy. The current study was conducted in China where the data were collected from retail investors through questionnaire. The SEM applied on the data revealed that all hypotheses of this research except three are true. It has been found that sensation seeking, self-esteem, and personality A/B type have significant impacts on FRT. It has been further revealed that self-esteem and personality A/B type have significant impacts on financial satisfaction but sensation seeking does not influence the financial satisfaction significantly. Furthermore, the results suggested that macroeconomic literacy is a significant mediator in the relationships of self-esteem with financial satisfaction, self-esteem with FRT, personality A/B type with financial satisfaction, and personality A/B type with FRT. However, the macroeconomic literacy is not a significant mediator in the relationships of sensation seeking with financial satisfaction and FRT.

6.1. Implications of study

The current study will be a great contribution to the theory and practice because it will open new areas of discussion and analysis for researchers of FRT, financial decision making and financial satisfaction. The theory regarding the financial decision making and FRT will be enhanced. The practical contribution of the current study will be realized among retail investors because they will get assistance through the current study and its findings that how their personality, self-esteem, and sensation seeking can determine their FRT and financial satisfaction. The policy makers of China and other countries can also get considerable assistance through the suggestions of the current study while making macroeconomic and investment policies.

6.2. Limitations and future research indications

Besides significant contributions of this research, there are a number of limitations of this research that should be considered by future researcher. For instance, the current research only considered three biopsychosocial indicators while demographic and environmental factors were ignored in this study. The future researcher can consider those factors as well to enhance the research. Furthermore, the current study was conducted in particular context of China. Future researchers are directed to conduct cross-national studies to set generalized understanding about the role of biopsychosocial indicators in FRT and financial satisfaction.

Author contributions

Hasnain Naqvi has executed the idea for this research article with the help of Mishal Hasnain and wrote the whole paper. Yushi Jiang helped us in the supervision of the paper and also in reviewing the paper.

Conflicts of Interest

The authors declare no conflict of interest.

Acknowledgements

We gratefully acknowledge the support provided by National Natural Science Foundation of China (No. 71572156), Sichuan Wine Development Research Center (CJZB18-02), Sichuan Circular Economy Research Center (XHJJ-1815), and the Humanity and Social Science Youth foundation of ministry of Education China (19YJC860033) and Southwest Jiao Tong University “One Belt and Road” research task project (268YDYLZ01).

Additional information

Funding

Notes on contributors

Muhammad Hasnain Abbas Naqvi

Muhammad Hasnain Abbas Naqvi is working as Assistant Professor and Head of Department in the National College of Business Administration and Economics, Lahore, Pakistan and is also a PhD Scholar at the School of Economics and Management, Southwest Jiaotong University, Sichuan, Chengdu, PR China. His research interests include social media, online shopping, tourism management, promotion, and user behavior.

Yushi Jiang

Yushi Jiang is a professor at the School of Economics and Management, Southwest Jiaotong University, Sichuan, Chengdu, PR China.

Miao Miao

Miao Miao is an Assistant Professor at the School of Economics and Management, Southwest Jiaotong University, Sichuan, Chengdu, PR China.

Mishal Hasnain Naqvi

Mishal Hasnain Naqvi is Campus Head at the National College of Business Administration and Economics, Lahore, Pakistan. She is also a PhD Scholar at the School of Business and Management, Sichuan University, Sichuan, Chengdu, PR China. Her research interests include advertising, consumer behavior, online shopping and social media.

References

- Abdellaoui, M., Bleichrodt, H., l’Haridon, O., & Van Dolder, D. (2016). Measuring loss aversion under ambiguity: A method to make prospect theory completely observable. Journal of Risk and Uncertainty, 52(1), 1–19. doi:10.1007/s11166-016-9234-y

- Ali, A., Rahman, M. S. A., & Bakar, A. (2015). Financial satisfaction and the influence of financial literacy in Malaysia. Social Indicators Research, 120(1), 137–156. doi:10.1007/s11205-014-0583-0

- Archuleta, K. L., Dale, A., & Spann, S. M. (2013). College students and financial distress: Exploring debt, financial satisfaction, and financial anxiety. Journal of Financial Counseling and Planning, 24(2), 50–62.

- Awais, M., Laber, M. F., Rasheed, N., & Khursheed, A. (2016). Impact of financial literacy and investment experience on risk tolerance and investment decisions: Empirical evidence from Pakistan. International Journal of Economics and Financial Issues, 6(1), 73–79.

- Baker, H. K., & Ricciardi, V. (2014). Investor behavior: The psychology of financial planning and investing. NewYork, NY: John Wiley & Sons.

- Barberis, N. C. (2013). Thirty years of prospect theory in economics: A review and assessment. Journal of Economic Perspectives, 27(1), 173–196. doi:10.1257/jep.27.1.173

- Bar-Hillel, M., & Procaccia, U. (2011). Behavioral economics and the law (in Hebrew). The Federmann Center for the Study of Rationality, the Hebrew University.

- Bossone, B. (2019). The portfolio theory of inflation and policy (in) effectiveness. Economics: The Open-Access, Open-Assessment E-Journal, 13(2019–33), 1–25.

- Burke, M. A., & Manz, M. (2014). Economic literacy and inflation expectations: Evidence from a laboratory experiment. Journal of Money, Credit and Banking, 46(7), 1421–1456. doi:10.1111/jmcb.2014.46.issue-7

- Dinç Aydemir, S., & Aren, S. (2017). Do the effects of individual factors on financial risk-taking behavior diversify with financial literacy? Kybernetes, 46(10), 1706–1734. doi:10.1108/K-10-2016-0281

- Donaldson, S. I., & Grant-Vallone, E. J. (2002). Understanding self-report bias in organizational behavior research. Journal of Business and Psychology, 17(2), 245–260. doi:10.1023/A:1019637632584

- Finke, M. S., & Huston, S. J. (2003). The brighter side of financial risk: Financial risk tolerance and wealth. Journal of Family and Economic Issues, 24(3), 233–256. doi:10.1023/A:1025443204681

- Frederick, S. (2005). Cognitive reflection and decision making. Journal of Economic Perspectives, 19(4), 25–42. doi:10.1257/089533005775196732

- Grable, J., & Lytton, R. H. (1999). Financial risk tolerance revisited: The development of a risk assessment instrument☆. Financial Services Review, 8(3), 163–181. doi:10.1016/S1057-0810(99)00041-4

- Grable, J. E. (2000). Financial risk tolerance and additional factors that affect risk taking in everyday money matters. Journal of Business and Psychology, 14(4), 625–630. doi:10.1023/A:1022994314982

- Grable, J. E., & Joo, S.-H. (2004). Environmental and biophysical factors associated with financial risk tolerance. Journal of Financial Counseling and Planning, 15(1), 73–82.

- Hallahan, T. A., Faff, R. W., & McKenzie, M. D. (2004). An empirical investigation of personal financial risk tolerance. Financial Services Review-greenwich-, 13(1), 57–78.

- Hanley, J. A., Negassa, A., Edwardes, M. D., & Forrester, J. E. (2003). Statistical analysis of correlated data using generalized estimating equations: An orientation. American Journal of Epidemiology, 157(4), 364–375. doi:10.1093/aje/kwf215

- Hoque, M., Wong, A., & Carducci, B. (2015). Do sensation seeking, control orientation, ambiguity, and dishonesty traits affect financial risk tolerance? Managerial Finance.

- Hvide, H. K., & Panos, G. A. (2014). Risk tolerance and entrepreneurship. Journal of Financial Economics, 111(1), 200–223. doi:10.1016/j.jfineco.2013.06.001

- Irwin, C. E., Jr. (1993). Adolescence and risk taking: How are they related.

- Jacobs-Lawson, J. M., & Hershey, D. A. (2005). Influence of future time perspective, financial knowledge, and financial risk tolerance on retirement saving behaviors. Financial Services Review-greenwich-, 14(4), 331.

- Joo, S.-H., & Grable, J. E. (2004). An exploratory framework of the determinants of financial satisfaction. Journal of Family and Economic Issues, 25(1), 25–50. doi:10.1023/B:JEEI.0000016722.37994.9f

- Kahneman, D., & Tversky, A. (2013). Choices, values, and frames. In Handbook of the fundamentals of financial decision making: Part I (pp. 269–278). World Scientific.

- Kai-Ineman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 363–391.

- Kannadhasan, M., Aramvalarthan, S., Mitra, S., & Goyal, V. (2016). Relationship between biopsychosocial factors and financial risk tolerance: An empirical study. Vikalpa, 41(2), 117–131. doi:10.1177/0256090916642685

- Kirbiš, I. Š., Vehovec, M., & Galić, Z. (2017). Relationship between financial satisfaction and financial literacy: Exploring gender differences. Društvena Istraživanja, 26(2), 165–185. doi:10.5559/di.26.2.02

- Kuzniak, S. F. (2016). A test of the effects of biopsychosocial and environmental, social support, and macroeconomic factors on financial risk tolerance. University of Georgia.

- Larkin, C., Lucey, B. M., & Mulholland, M. (2013). Risk tolerance and demographic characteristics: Preliminary Irish evidence. Financial Services Review, 22(1), 77–91.

- Lipshits, R., Barel-Shaked, S., & Ben-Zion, U. (2019). Empirical study relating macroeconomic literacy and rational thinking. Research in Economics, 73, 209–215. doi:10.1016/j.rie.2019.07.001

- Lusardi, A., Mitchell, O. S., & Curto, V. (2010). Financial literacy among the young. Journal of Consumer Affairs, 44(2), 358–380. doi:10.1111/j.1745-6606.2010.01173.x

- Morgeson, F. V., III, Sharma, P. N., & Hult, G. T. M. (2015). Cross-national differences in consumer satisfaction: Mobile services in emerging and developed markets. Journal of International Marketing, 23(2), 1–24. doi:10.1509/jim.14.0127

- Muda, I. (2017). User impact of literacy on treatment outcomes quality regional financial information system. Management Dynamics in the Knowledge Economy, 5(2), 307–326. doi:10.25019/MDKE

- Muth, J. F. (1961). Rational expectations and the theory of price movements. Econometrica: Journal of the Econometric Society, 29, 315–335. doi:10.2307/1909635

- Rai, K., Dua, S., & Yadav, M. (2019). Association of financial attitude, financial behaviour and financial knowledge towards financial literacy: A structural equation modeling approach. FIIB Business Review, 8(1), 51–60. doi:10.1177/2319714519826651

- Rieger, M. O., Wang, M., & Hens, T. (2014). Risk preferences around the world. Management Science, 61(3), 637–648. doi:10.1287/mnsc.2013.1869

- Sivaramakrishnan, S., Srivastava, M., & Rastogi, A. (2017). Attitudinal factors, financial literacy, and stock market participation. International Journal of Bank Marketing, 35(5), 818–841. doi:10.1108/IJBM-01-2016-0012

- Smith, A., & Stewart, D. (1963). An inquiry into the nature and causes of the wealth of nations (Vol. 1). Wiley Online Library.

- Stanovich, K. E. (2016). The comprehensive assessment of rational thinking. Educational Psychologist, 51(1), 23–34. doi:10.1080/00461520.2015.1125787

- Thaler, R. H. (1999). Mental accounting matters. Journal of Behavioral Decision Making, 12(3), 183–206. doi:10.1002/(ISSN)1099-0771

- Topa, G., Moriano, J. A., & Moreno, A. (2012). Psychosocial determinants of financial planning for retirement among immigrants in Europe. Journal Of Economic Psychology, 33(3), 527–537. doi:10.1016/j.joep.2012.01.003

- Von Neumann, J., & Morgenstern, O. (1953). Theory of games and economic behavior (3rd ed.). Princeton university press.

- Wang, M., & Fischbeck, P. S. (2004). Incorporating framing into prospect theory modeling: A mixture-model approach. Journal of Risk and Uncertainty, 29(2), 181–197. doi:10.1023/B:RISK.0000038943.63610.16

- Xiao, J. J., Tang, C., & Shim, S. (2009). Acting for happiness: Financial behavior and life satisfaction of college students. Social Indicators Research, 92(1), 53–68. doi:10.1007/s11205-008-9288-6

- Xu, L., & Zia, B. (2012). Financial literacy around the world: An overview of the evidence with practical suggestions for the way forward. Washington, DC: World Bank Working Paper 6107.

- Yaari, M. E. (1987). The dual theory of choice under risk. Econometrica: Journal of the Econometric Society, 55, 95–115. doi:10.2307/1911158

- Yao, R., Gutter, M. S., & Hanna, S. D. (2005). The financial risk tolerance of blacks, hispanics and whites. Journal of Financial Counseling and Planning, 16(1), 51–62.

- Yao, R., Hanna, S. D., & Lindamood, S. (1983). “Changes in financial risk tolerance, 1983–2001.” Yao, R., Hanna, SD & Lindamood, S.(2004). Changes in financial risk tolerance, 2001, 249–266

- Zeger, S. L., & Liang, K.-Y. (1986). Longitudinal data analysis for discrete and continuous outcomes. Biometrics, 42, 121–130. doi:10.2307/2531248