?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

We investigate how funding liquidity affects the bank lending using a large sample of US bank holding companies. We document a consistent evidence of a lower loan growth for banks that rely more on deposits. The quantile regressions which dissect the lending behavior of banks at the right tail of loan growth distribution point out the leveraged effect of funding liquidity is larger in high-loan-growth banks. The negative effects of funding liquidity on lending seem to be clearer before the crisis and especially for large banks. Interestingly, we do not find any evidence of the relation between lending and funding liquidity after the crisis period. We believe our study is of interest to regulators and policymakers.

PUBLIC INTEREST STATEMENT

Banks play an important role in our economies, assuming the role of providing the necessary liquidity to informationally opaque borrowers without capital market opportunities, supplying liquid funds and payment services to households, which is the main driver for the economy functioning. We examine the impacts of funding liquidity on one of the main functions of banks—lending, and document that banks with a higher proportion of deposits will decrease their lending. The study shows this negative impact varies across business cycles and bank size. Our study is of interest of policymakers since it provides an understanding of how bank intermediation roles may respond to an introduction of the liquidity regulations.

1. Introduction

In the aftermath of the financial crisis of 2007 with the collapse of a number of banks and the ensuing economic recessions, many critics are advanced, but one of the most cited reasons is related to inefficient regulatory, high debt levels and insufficient liquidity buffers (Hugonnier and Morellec (Citation2017)). Banks experience funding liquidity problems when facing the dry-up of capital markets. This relates to the liquidity channel of financial transmission through which market funding liquidity shocks are propagated to bank lending and the real economy (de Haan and van den End (Citation2013)).

In this paper, we focus on the financial market-related funding sources. More specifically, we investigate the effects of funding liquidity on bank lending. This question is of great interest of regulators and policymakers since prior the crisis of 2007–2009 credit and the prices of assets growth up tremendously, house prices growth up of more than 10% from 2002–2007 without any evidence of the improvement of borrower quality (Acharya and Richardson (Citation2009)). And this precipitous increase in asset volume and prices met with a descent fall, which consequently affects negatively the real sector.

There is a growing literature related to the bank liquidity risk management (e.g. Khan, Scheule, & Eliza (Citation2017)). Funding liquidity risk, which plays a key role in all historical banking crises, is defined as the possibility that over a specific horizon the bank will become unable to settle obligations with immediacy (Drehmann and Nikolaou (Citation2013)). Recently, some document that liquidity risk has a negative effect on the bank risk-taking, i.e. a decrease in liquidity risk contributes to higher bank risk-taking (Dahir, Fauziah, and Noor Azman (Citation2018); Khan et al. (Citation2017)). Vazquez and Federico (Citation2015) document that banks with weaker structural liquidity and higher leverage in the pre-crisis period were more likely to fail afterward. The likelihood of bank failure also increases with pre-crisis bank risk-taking. Acharya and Naqvi (Citation2012) develop a theoretical model explaining how abundant liquidity exacerbates the risk-taking moral hazard at the bank, rising to excessive lending and then asset price bubbles. Based on these evidences, some may argue a positive relation between bank lending and funding liquidity.

However, in the aftermath of the financial crisis, regulators recognize the need to strengthen the liquidity management and financial stability of banks, then develop frameworks for assessing liquidity in banking in addition to more stringent capital adequacy rules. To comply with these new standards, banks have to improve their capital buffer, change the structure of their balance sheet improving the liquidity of their assets and the stability of their funding (Roulet (Citation2018)). Banks with adequate funding liquidity are less likely to experience liquidity crunches. By consequent, banks may restraint to originate credits to satisfy with the liquidity requirements to maintain greater liquidity. Literature on bank liquidity risk also documents the precautionary motivation for banks to ration credits (Allen and Gale (Citation2004)). Banks respond to the fear of a potential future liquidity shock—that may lead to a mandatary to liquidate illiquid asset—by holding more liquid assets (self-insurance) (Diamond and Rajan (Citation2011)). Gale and Yorulmazer (Citation2013) suggest that banks may be wary about lending, then respond by hoarding liquidity for precautionary reasons (i.e. against potential shocks of liquidity in the future) or for strategic reasons (i.e. to exploit of potential asset liquidation). Furthermore, a more reliance to deposit may induce banks to be firmly monitored by depositors, since depositors could punish banks by ex-post withdraw their funds (in extreme case, depositor runs), and by ex-ante adjust the funding costs (Tran and Nguyen (Citation2018)). Then, we suggest banks that rely more on deposits may be more cautious to lend comparing to other banks. Taken together, we suggest that there may be a negative relation between bank lending and funding liquidity.

These two strands of literature are not mutually exclusive. We examine in this study the association of bank lending and bank funding liquidity using a large sample of US bank holding companies (BHC) from 2000:Q1 to 2017:Q4. Relying on the richest and the most complete database related to banking institutions that provides the detail of banks operating in hundreds of local markets allows us to analyze the data at the highest frequency possible Tran, Hassan, and Houston (Citation2019a).

Controlling for the effects of different bank characteristics and time fixed effects, we document consistent evidence on a lower loan growth for banks that are more likely to rely on deposits. The evidence suggests that banks with a high proportion of stable funding such as deposits are less likely to lend. When performing investigation across the distribution of lending with the quantile regressions, we document that the relationship between bank lending and funding liquidity is actually not uniform in sign, but decreases significantly in magnitude with the increase of quantiles of lending. For banks with low loan growth, the coefficients on funding liquidity are positive. It becomes negative with the increase of quantile, suggesting that a more rely on deposits as funding decreases bank lending. This also suggests that high-loan-growth banks, leveraged by higher reliance on deposits, are more likely to decrease lending. Our study also provides evidence of how this negative relationship between lending and funding liquidity varies across bank size and time periods.

Our study contributes to the literature in several ways. First, our study contributes to the bank funding liquidity literature by providing one of the first investigation of the effects of funding structure on bank lending decisions. Our main results suggest that higher reliance on deposits would lower the loan growth of banks, and this effect is more emphasized for large banks. Second, we provide the evidence of the effects of funding liquidity over the entire range of the lending distribution. The traditional inference technique reflects specifications reflect the conditional average association between bank lending and bank funding liquidity with the assumption of the homogeneity of the effects of funding liquidity to bank lending Tran et al. (Citation2019a). Our quantile regressions document that funding liquidity not only affects the conditional average of lending but also influences the dispersion of lending. Third, our study documents one of the first evidence of the impacts of funding liquidity on bank lending after the crisis, where we do not find any relation between lending and funding liquidity for all size range of banks.

The next section describes the data. Section 3 reports the main results. We provide additional tests in Section 4. Section 5 concludes the study.

2. Data

We extract our sample from the quarterly Y-9 C regulatory reports which are filled by bank holding companies (BHC) with assets of 150 USD million and over. Our data cover the period 2000:Q1 to 2017:Q4. All bank-quarter observations with missing or incomplete financial data on accounting variables are removed. Following Berger & Christa (Citation2013); Tran & Ashraf (Citation2018); Tran, Hassan, & Houston (Citation2019b); Tran et al. (Citation2019a), all observations with the capital ratio less than 1% are replaced by 1% to avoid distortion in ratios that contain equity. We also exclude observations with negative or nonexistent outstanding loans or deposits. All financial ratios are winsorized at 1% level on the top and bottom of their distribution to dampen the effects of outliers.

3. Does funding liquidity affect bank lending?

3.1. Main findings

We conduct multivariate analysis to formally investigate the magnitude of banks’ funding liquidity on bank lending after controlling other control variables. Specifically, our empirical specification is as follows:

where is the measure of lending growth (LENDING) of bank i at time t. We use the growth rate of loans following prior literature such as Cornett, Jamie John McNutt, and Tehranian (Citation2011), Ibrahim and Syed Aun (Citation2018), Kim and Sohn (Citation2017) as the main proxy in our investigation. Our variable of interest is the funding liquidity (FUL), which is defined as the ratio of deposits over total assets.

is the vector of control variables. In assessing the impact of funding liquidity on bank lending, we control for several time-varying bank characteristics. The bank lending may differ according to bank size, or between banks with different leverage, we include banks' size (SIZE), capital ratio (CAPITAL). We also control for differences in profitability by including banks' performance (EARNINGS) and loss indicator (DUM_LOSS). We include the bank business model (DIVERSIFICATION). See Table for definitions, and Table for summary descriptive.

Table 1. Variables definitions

Table 2. Summary statistics

We use the lag of one period of FUL and all control variables to take into account that the information from the balance sheet is available to the public with a certain delay. We include time-fixed effects to control for the macroeconomic conditions, common across banks.

is the error term. Since LENDING is likely to be correlated within a bank over time, standard errors used to assess significance are corrected for heteroscedasticity and bank-level clustering.

Table shows our main results. Our baseline model (Model (1)) shows that the coefficient on FUL is negative and highly significant at the 1% level. One standard deviation increase of FUL, holding all other equal, results in a decrease of the bank lending of 2.1 bps (i.e. the coefficient of FUL, −0.019, times the standard deviation of FUL, 0.111). The finding suggests an economically large, negative relation between the bank lending and the funding liquidity. This result indicates that banks would decrease their lending in case of having a large portion of their funding from depositors.

Table 3. Baseline multivariate analysis

In Model (2), we rank FUL variable into quartiles and create a variable called FUL_DQRT, which takes a value ranging from 1 (lowest) to 4 (highest). This approach allows us to generate greater variation in the distribution of the bank’s funding liquidity. We obtain a negative and significant coefficient on FUL_DQRT.

Our baseline model already includes control variables documented in prior literature, but there may exist some omitted and correlated variables. In Models (3), we extend our baseline model by controlling for the effect of the quality of bank’ loan portfolio as measured by the ratio of non-performing loans over the total loans (NPL), dividend policy (DIVIDEND), macroeconomic indicators (UNEMPLOYMENT). Again, we observe that higher FUL banks decrease their lending.

In Model (4), we exclude banks that engage M&A (proxies as the growth rate of assets over quarter higher than 20%) from our baseline model since banks may decide to acquire target banks that focus more on lending activities. Our results remain unchanged with the negative coefficient between FUL and LENDING.

One may have concerns that our sample includes the financial crisis of 2007–2009 which may critically bring about a large change in the environment where banks function, resulting a large structural break in bank’s lending decisions and their funding liquidity. In Model (4), we perform our main specification by excluding the crisis period and still obtain qualitative results.

In Model (5), instead of lagging all explanatory variables of one period, we lag them two periods. In unreported tests, we also lag three and four periods. In all specifications, we still receive similar results. In Model (6) and (7), we use alternative measures of LENDING and FULL, respectively, and still obtain similar results.

In summary, we obtain a consistent evidence on the effect of funding liquidity to bank lending decisions. We find that banks that rely more on deposits are more likely to reduce their loan growth.

3.2. Quantile regressions

Our main purpose in this research is to examine the association between bank lending decisions and their funding liquidity. Bank’s stakeholders such as investors, regulators, and policymakers seem to be more interested in lending behaviors of banks at the tails of the distribution of loan growth, since extremely low (high) loan growth may in the same extent negatively affect the economy due to the problem of credit allocation to the real sector.

The above specifications reflect the conditional average association between bank lending and bank funding liquidity with the assumption of the homogeneity of the effects of funding liquidity to bank lending (Tran, Hassan, and Houston (2019)). We now perform the quantile regression—a generalization of median regression analysis to other quantiles—to investigate whether the relation between FUL and LENDING differs across the distribution of LENDING. Rather than relying on a single description of the central behavior of the sample, the quantile approach explores a range of conditional quantile functions—models in which quantiles of the conditional distribution of the deposit rates are expressed as functions of observed covariates, which in turn allows us to explore potential forms of conditional heterogeneity (Tran et al. (Citation2019a)). Furthermore, the quantile regression approach avoids the restrictive assumption that the error terms are identically distributed at different distributions of the bank’s lending decisions (Klomp and de Haan (Citation2012)).

We document interesting results. The coefficients on FUL in Models (1)–(9) show the impact of FUL on LENDING decreases significantly in magnitude with the increase of quantiles. For banks with low loan growth (i.e. 10th and 20th), the coefficients on FUL are positive. It becomes not statistically different from 0 at 30th of LENDING before becoming statistically negative with the increase of quantile, suggesting that a more rely on deposits as funding decreases bank lending. This evidence is interesting, showing us the relationship between FUL and LENDING is not uniform in sign.

To provide a potential explanation for this evidence, we tabulate LENDING and NPL by each decile of LENDING in Panel B, Table . For banks with low loan growth (i.e. 10th and 20th, with an average LENDING of 0.003 and 0.009, respectively), we observe that these banks experience a higher rate of non-performing loans than other banks, suggesting that banks with low loan growth may have higher risk-taking behaviors than other banks. Following the theory of Acharya and Naqvi (Citation2012), an increase of funding liquidity may consequently exacerbate the risk-taking moral hazard at banks, rising then to an increase of lending. This positive relationship is quickly offset with an increase of quantile. For banks with higher loan growth (i.e. from 40th), we observe that their NPLs are lower, suggesting a lower risk-taking behavior at those banks. This suggests that those banks may tend to restrain the lending to respond to the fear of a potential future liquidity shock.

Table 4. Quantile regression

Table 4. (Continued)

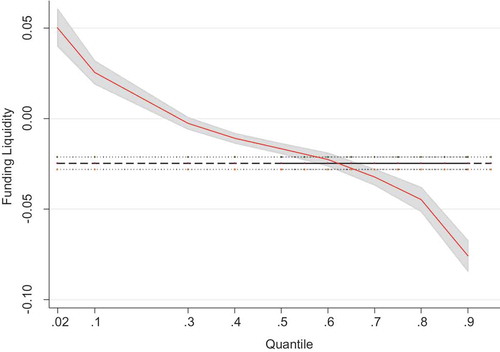

In an unreported test, we perform inter-quantile regressions (i.e. regressions of difference-in-quantiles) to assess whether these differences of coefficients on FUL across LENDING’s quantiles are significant. We observe the interquartile differences are significantly different from zero. We plot the estimated effect of FUL from night separate quantile regressions for the quantiles ranging from 0.10 to 0.90 in Figure .

Figure 1. Funding liquidity and bank lending—Quantile Analysis Estimates

Overall, these results document that funding liquidity not only affects the conditional average of lending but also influences the dispersion of lending.

4. Further investigations

4.1. How does the crisis affect the relation between bank lending and funding liquidity?

The banking crisis would be a unique occasion to analyze how banks effectively manage their funding liquidity and how banks adjust their lending decisions. Banks may experience further difficulties and higher probabilities of failure during the crisis time. Depositors consequently become more aware of the risk of losing their deposits, and then they increase market discipline during the crisis (Tran and Nguyen (Citation2018)). By prudent, banks may hold more cash and more liquid assets, in detriment of their capability to make new loans. However, during turmoil times, government is more likely to intervene to reinforce the safety nets of banks, due to the potential detrimental effects of bank failures. Gatev and Strahan (Citation2006) document inflows of deposits during the periods of low market liquidity, whereas Cornett et al. (Citation2011) observe an increase of retail deposits inflow during the last crisis. With flush liquidity, it may lower the sensitivity of bankers’ payoffs to downside risks and inducing excessive credit volume and asset price bubbles (Acharya and Naqvi (Citation2012)).

In this section, we investigate whether the association between bank lending and funding liquidity changes during crisis periods. Our study starts from 2000:Q1 then covers the crisis period from 2007:Q3-2009:Q2 following Acharya and Mora (Citation2015).

Following Tran, Hassan, and Houston (2019), Tran, Hassan, and Houston (2019), we first use the variation in bank lending and bank characteristics in a panel setting to examine whether the bank lending during the crisis differs from the pre-crisis period, taking into account the changes of bank characteristics. To do so, we regress Equation (1) for the pre-crisis period. Next, we use the estimated coefficients to predict LENDING during the crisis. By comparing these predicted LENDING with actual LENDING during the crisis, we document how LENDING during the crisis should be if they were in pre-crisis time. The results are shown in Table , Panel A. We observe LENDING would decrease during the crisis, since the difference is negative and statistically significant at the 1% level.

Table 5. The effects of the crisis

Following Peria, Soledad, and Schmukler (Citation2001), Tran and Nguyen (Citation2018), we go further by evaluating separately the response of bank lending on bank funding liquidity before, during and after the crisis, i.e. 2000:Q1-2007:Q2, 2007:Q3-2009:Q2, and 2009:Q3-2017:Q4, respectively. The results are shown in Table , Panel B.

We find that the coefficient on FUL is negative and statistically significant before the crisis (Model (1)), suggesting that the more banks rely on deposits, the more they decrease the loan growth during normal times. During the crisis time, the coefficient on FUL is still negative and marginally statistical significant (at 10%) but is greater (i.e. less negative) than the coefficient on FUL before the crisis (i.e. −0.012* vs −0.025***). This evidence is consistent with the theory of Acharya and Naqvi (Citation2012), as well as the empirical findings of Cornett et al. (Citation2011), which suggest that banks that rely more on stable funding (i.e. deposits) may increase their loan growth during the crisis time. This evidence is also consistent with Tran and Nguyen (Citation2018) where they document depositors still monitor banks during this crisis time, but to a lesser extent than during normal times due to the moral hazard induced by the government intervention. For the period after the crisis, we do not find any evidence of the association between LENDING and FUL. A speculative explanation of the relationship between LENDING and FUL after the crisis is the offsetting effect of the precautionary behavior documented before the crisis and the increased moral hazard induced by the government intervention starting from the crisis.

Summarizing, the evidence in this section suggests that banks that rely more on stable financing such as deposits are more likely to lend more during the crisis time.

4.2. The size effects

In this section, we investigate the size effects of banks, which is documented in previous studies that bank size may affect the market perception of the bank risk. Small banks focus more on entrepreneurial-type small businesses, which emphasizes the close monitoring as documented in Diamond and Rajan (Citation2001). Those type of banks are more likely to rely on local funds, which are mostly deposits. On the other hand, large banks may be subject to greater scrutiny from regulators and market discipline and have easy access to funding from national and international capital markets (Berger and Bouwman (Citation2009), Tran et al. (Citation2019b)).

Following Berger, Ghoul, Guedhami, and Roman (Citation2016), Tran et al. (Citation2019a), we re-perform our main investigation by bank size ranges (Small banks with assets under 1 USDB, Medium banks with assets between 1 USDB and 5 USDB, and Large banks with assets over 5 USDB) over full period (i.e. 2000:Q1-2017:Q4) to examine whether our main finding is concentrated on a particular bank size range. Table shows the results.

Table 6. The effects of bank size

In Models (1)–(3), we find that higher reliance on deposits is associated with lower loan growth across all size classes; however, the effects have the U-inverted shape. The negative effect on loan growth is lowest for medium banks whereas highest for large banks.

However, the loan decisions may change over the period as explained in the above section. We then re-perform our analyses during different periods: before the crisis (Models (4)–(6)), during the crisis (Models (7)–(9)), and after crisis (Models (10)–(12)).

For the periods before the crisis, we still obtain the negative effects on loan growth across bank size range; however, the effects seem to be amplified, especially with large banks. Indeed, before the crisis, large banks that rely more on deposits are more likely to decrease their loan growth. The potential explanation is as follows. Large banks may focus on other high-yield and highly complex activities than traditional banking activities (i.e. distributing loans). Also, those banks are more likely to involve in market-based activities, to “originate-and-distribute” rather than “originate-and-hold” loans as in other banks.

For the period during the crisis, we do not obtain any relation between FUL and LENDING for small and medium banks whereas we still observe the negative effect on FUL in large banks. For the period after the crisis, we do not obtain any association between FUL and LENDING across all size classes.

5. Conclusions

In this study, we provide one of the first large-sample examination of the effects of funding liquidity on the loan growth of banks. Our finding shows evidence of lower loan growth for banks that rely more on stable funding sources such as deposits. However, this relationship is not uniform in sign when we investigate across the distribution of LENDING. We document that banks with lower loan growth tend to increase LENDING with an increased FUL, whereas banks with higher loan growth are more likely to decrease LENDING with an increased FUL. We also examine whether the relationship between FUL and LENDING varies across circumstances. This negative effect on loan growth is observed clearly before the crisis, especially for large banks, and to a lesser extent during the crisis, and disappear after the crisis. Our results are of interest to regulators and policymakers seeking regulatory policies on liquidity such as those of Basel III. Our main evidence suggests that an increase in stable funding may lead to a decrease in lending. This effect may be mitigated with the intervention of the government during the turmoil times. We believe that our study provides an understanding of how bank intermediation role may respond to an introduction of the liquidity regulations.

Additional information

Funding

Notes on contributors

Dung Viet Tran

Dung Viet Tran is a lecturer of Finance at the faculty of Banking of Banking University Ho Chi Minh city (BUH), and a non-resident Fellow of IPAG Business School in Paris, France. He obtained his PhD from University Grenoble Alpes (France), and has been a visiting scholar at the University of Alberta, University Laval (Canada), University of New Orleans (US), University of Kent (UK) among others. He has taught derivatives, risk management, and quantitative methods classes at both MSc and undergraduate levels. His research covers a variety of topics related to financial institutions and empirical corporate finance, including capital structure, dividend policy, bank risk taking behaviors, earnings management, systemic risk among others.

References

- Acharya, V., & Naqvi, H. (2012). The seeds of a crisis: A theory of bank liquidity and risk taking over the business cycle. Journal of Financial Economics, 106, 349–16. doi:10.1016/j.jfineco.2012.05.014

- Acharya, V. V., & Mora, N. (2015). A crisis of banks as liquidity providers. The Journal of Finance, 70, 1–43. doi:10.1111/jofi.12182

- Acharya, V. V., & Richardson, M. (2009). Causes of the financial crisis. Critical Review, 21, 195–210. doi:10.1080/08913810902952903

- Allen, F., & Gale, D. (2004). Financial fragility, liquidity, and asset prices. Journal of the European Economic Association, 2, 1015–1048. doi:10.1162/JEEA.2004.2.6.1015

- Berger, A. N., & Bouwman, C. H. S. (2009). Bank liquidity creation. Review of Financial Studies, 22, 3779–3837. doi:10.1093/rfs/hhn104

- Berger, A. N., & Christa, H. S. B. (2013). How does capital affect bank performance during financial crises? Journal of Financial Economics, 109, 146–176. doi:10.1016/j.jfineco.2013.02.008

- Berger, A. N., Ghoul, S. E., Guedhami, O., & Roman, R. A. (2016). Internationalization and bank risk. Management Science, 63, 2283–2301. doi:10.1287/mnsc.2016.2422

- Cornett, M. M., Jamie John McNutt, P. E. S., & Tehranian, H. (2011). Liquidity risk management and credit supply in the financial crisis. Journal of Financial Economics, 101, 297–312. doi:10.1016/j.jfineco.2011.03.001

- Dahir, A. M., Fauziah, B. M., & Noor Azman, B. A. (2018). Funding liquidity risk and bank risk-taking in BRICS countries. International Journal of Emerging Markets. doi:10.1108/IJoEM-03-2017-0086

- de Haan, L., & van den End, J. W. (2013). Banks’ responses to funding liquidity shocks: Lending adjustment, liquidity hoarding and fire sales. Journal of International Financial Markets, Institutions and Money, 26, 152–174. doi:10.1016/j.intfin.2013.05.004

- Diamond, D. W., & Rajan, R. G. (2001). Liquidity risk, liquidity creation, and financial fragility: A theory of banking. Journal of Political Economy, 109, 287–327. doi:10.1086/319552

- Diamond, D. W., & Rajan, R. G. (2011). Fear of Fire Sales, Illiquidity Seeking, and Credit Freezes. The Quarterly Journal of Economics, 126, 557–591. doi:10.1093/qje/qjr012

- Drehmann, M., & Nikolaou, K. (2013). Funding liquidity risk: Definition and measurement. Journal of Banking & Finance, 37, 2173–2182. doi:10.1016/j.jbankfin.2012.01.002

- Gale, D., & Yorulmazer, T. (2013). Liquidity hoarding. Theoretical Economics, 8, 291–324. doi:10.3982/TE1064

- Gatev, E., & Strahan, P. E. (2006). Banks’ advantage in hedging liquidity risk: Theory and evidence from the commercial paper market. The Journal of Finance, 61, 867–892. doi:10.1111/j.1540-6261.2006.00857.x

- Hugonnier, J., & Morellec, E. (2017). Bank capital, liquid reserves, and insolvency risk. Journal of Financial Economics, 125, 266–285. doi:10.1016/j.jfineco.2017.05.006

- Ibrahim, M. H., & Syed Aun, R. R. (2018). Bank lending, deposits and risk-taking in times of crisis: A panel analysis of Islamic and conventional banks. Emerging Markets Review.35, P. 31–47. https://www.sciencedirect.com/science/article/abs/pii/S1566014117302418

- Khan, M. S., Scheule, H., & Eliza, W. (2017). Funding liquidity and bank risk taking. Journal of Banking & Finance, 82, 203–216. doi:10.1016/j.jbankfin.2016.09.005

- Kim, D., & Sohn, W. (2017). The effect of bank capital on lending: Does liquidity matter? Journal of Banking & Finance, 77, 95–107. doi:10.1016/j.jbankfin.2017.01.011

- Klomp, J., & de Haan, J. (2012). Banking risk and regulation: Does one size fit all? Journal of Banking & Finance, 36, 3197–3212. Systemic risk, Basel III, global financial stability and regulation. doi:10.1016/j.jbankfin.2011.10.006

- Peria, M., Soledad, M., & Schmukler, S. L. (2001). Do depositors punish banks for bad behavior? Market discipline, deposit insurance, and banking crises. The Journal of Finance, 56, 1029–1051. doi:10.1111/0022-1082.00354

- Roulet, C. (2018). Basel III: Effects of capital and liquidity regulations on European bank lending. Journal of Economics and Business, 95, 26–46. Research in European Banking and Finance. doi:10.1016/j.jeconbus.2017.10.001

- Tran, D. V., & Ashraf, B. N. (2018). Dividend policy and bank opacity. International Journal of Finance & Economics, 23, 186–204. doi:10.1002/ijfe.1611

- Tran, D. V., Kabir, M. H., & Houston, R. (2019a). Activity strategies, information asymmetry, and bank opacity. Economic Modelling, 83, 160–172. doi:10.1016/j.econmod.2019.02.008

- Tran, D. V., Kabir, M. H., & Houston, R. (2019b). How does listing status affect bank risk? The effects of crisis, market discipline and regulatory pressure on listed and unlisted BHCs. The North American Journal of Economics and Finance, 49, 85–103. doi:10.1016/j.najef.2019.03.007

- Tran, D. V., & Nguyen, D. K., 2018, (How) Do depositors respond to bank’s discretionary behaviors? Market discipline, deposit insurance and crisis (SSRN Scholarly PaperSSRN Scholarly Paper).

- Vazquez, F., & Federico, P. (2015). Bank funding structures and risk: Evidence from the global financial crisis. Journal of Banking & Finance, 61, 1–14. doi:10.1016/j.jbankfin.2015.08.023