?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

We investigate the governance sensitivity of foreign institutional investors’ (FII) ownership in a large emerging market setting of India, characterized by highly concentrated insider ownership. More specifically, we focus on the moderating role of firm size and price to book value (PB) in determining the relationship between FII ownership and board characteristics, such as board size, outside director ratio, CEO duality, and board meeting attendance. Our methodology emphasizes the importance of contextual analysis in studies relating to institutional investors’ preferences. We find that FIIs prefer bigger boards and greater board independence in larger and growth firms (higher PB). Further, FIIs prefer firms that have separate CEO and Chairman of the board positions in growth firms.

PUBLIC INTEREST STATEMENT

We investigate the governance sensitivity of foreign institutional investors (FII) in a large emerging market setting of India, characterized by highly concentrated insider ownership. More specifically, we focus on the moderating role of firm size and market to book value (PB) in determining the relationship between FII ownership and board characteristics, such as board size, outside director ratio, CEO duality, and board meeting attendance. We find that FIIs prefer bigger boards and greater board independence in larger and higher PB firms (growth firms). Further, FIIs prefer firms that have separate CEO and Chairman of the board positions in growth firms.

1. Introduction

Foreign capital is an important source of finance for emerging market firms due to the limited availability of domestic sources. However, access to foreign capital is uneven across firms. Firm-level corporate governance is one factor that explains differential access to foreign capital (Leuz et al., Citation2010). Foreign investors tend to avoid firms with weak corporate governance mechanisms due to a lack of trust. The lack of trust among foreign investors induced by poor firm information environments is particularly relevant in markets with high levels of insider ownership concentration that can potentially exacerbate the risk of expropriation by the controlling shareholders.

Our focus in this paper is to examine the role of corporate governance mechanisms of firms in determining foreign institutional investor (FII) preferences in an emerging market setting, characterized by highly concentrated insider ownership. More specifically, we investigate the incremental effect of board characteristics as a determinant of foreign institutional ownership and their interactions with firm characteristics, such as market capitalization and market-to-book value ratio.

To establish the empirical relationship between FII ownership and board characteristics, we explore the data on Indian listed firms for the period from April 2004 to March 2019. The period of study includes an evolving regulatory framework on corporate governance (Dixit, Citation2015). In the year 1999, India adopted a major governance reform, Clause 49 that requires public companies to have, among other things, several internal control systems, including a minimum number of independent directors. Black and Khanna (Citation2007) note that the Indian stock markets reacted positively to the introduction of Clause 49, in contrast to the negative reaction of the US markets to the adoption of the Sarbanes-Oxley Act in 2002. They argue that similar reforms can have different effects in countries with different institutional environments.

The Indian market, characterized by highly concentrated ownership, provides the controlling shareholders a disproportionate control over the firms’ cash flows that have the potential to create agency issues when inside—owners act opportunistically and accrue private benefits at the expense of other shareholders. The inside—owners (also known as promoters), on average, own close to 50% of the shares of Indian listed companies. In contrast, ownership in developed economies is quite diffuse. In firms with diffuse ownership, the agency problem is primarily between the owners and the managers (Jensen & Meckling, Citation1976). Whereas, in firms with concentrated ownership, particularly those in which the controlling shareholders participate in the management of the firm, the nature of the agency problem shifts to one between minority and controlling shareholders (also known as secondary agency issues). The social connections between the influential inside owners and directors further complicate the problem.

A sizable literature investigates the determinants of institutional investor ownership. They focus on examining institutional demand for stock characteristics, momentum investing or past returns, and corporate governance mechanisms of firms (Bennett et al., Citation2003; Bushee et al., Citation2013; Gompers & Metrick, Citation2001; Sias, Citation2007). The studies that focus on stock characteristics show that firm size, market liquidity, and share price positively affects institutional ownership. Prior literature on momentum investing behavior of institutional investors is largely inconclusive (Sias, Citation2007). However, little is known about the corporate governance preferences of institutional investors, particularly foreign institutions investing in firms operating in relatively weak information environments such as emerging markets. Bushee et al. (Citation2013) investigate the association between total institutional ownership and firms’ corporate governance mechanisms and documents weak evidence on the same.

Due to the large portfolios often held by institutional investors, and the associated high monitoring costs, institutional investors have strong incentives to discipline and monitor the managers. One approach to influence the governance mechanisms is by taking an active role in the governance of their portfolio firms by waging public or private campaigns (Bushee et al., Citation2013). Gillan and Starks (Citation2000) note that this kind of activism has evolved to be an important part of financial markets. However, the implications of such activism by investors is often uncertain and costly. An alternate approach employed by institutional investors is to invest in firms that acquire preferred governance characteristics and disclosures practices and avoid the rest.

To examine the consequences of board characteristics on the investment preferences of foreign investors, we employ a contingency approach as advocated by Ferreira et al. (Citation2017) and Zona et al. (Citation2013). Contingency theory emphasizes the importance of contextual factors in determining the effectiveness of a given structure (Birkinshaw et al., Citation2002). We hypothesize that the effect of board characteristics on FII ownership can vary depending on the firm size and book value multiple (market-to-book ratio).

Prior literature documents that the prevailing information environment and legal frameworks guide the investment allocation of foreign investors across firms in emerging markets. Aggarwal et al. (Citation2005) examine the influence of country and firm-level governance policies on the investment allocation decisions of US mutual funds. After controlling for the country characteristics, they document the positive influence of transparency on the investment decisions of US mutual funds in emerging markets. In the same vein, Chan et al. (Citation2005) show that, foreign investment inversely relates to expropriation risk. Ferreira et al. (Citation2017) documents that domestic institutions have an information advantage relative to foreign institutions, particularly in less efficient stock markets characterized by more significant information asymmetry problems. Further, Leuz et al. (Citation2010) argue that information asymmetry problems magnify the challenges encountered by foreign investors while evaluating the governance structure of firms.

Our empirical analysis reveals that board size and FII ownership have a negative association, suggesting that FIIs prefer firms that have smaller boards. However, firm size positively moderates the relationship between board size and FII ownership, indicating that FIIs prefer bigger boards in larger firms. Similarly, FIIs prefer larger boards in growth firms (firms with higher PB ratios) that are more likely to have higher non-financial disclosures and unclear growth fundamentals. We also find that foreign investors prefer higher outside director ratios in larger firms and growth firms, as indicated by the significant positive interaction between firm size and PB ratio with outsider ratio. Finally, we show that FIIs prefer CEO non-duality in firms with higher PB ratios, as shown by the significant negative interaction of PB ratio and the indicator variable for CEO duality.

Our study makes two important contributions. First, it shows how the relationship between board characteristics and foreign institutional ownership changes according to firm characteristics (firm size) and market-based signals (market-to-book value). Our approach helps in understanding the role of contingencies in the relationship between FII ownership and board characteristics. Second, by studying a unique emerging market (India) setting, characterized by secondary agency problems between controlling and minority shareholders in a relatively weak information environment, we expect to extend prior research to a hitherto unexplored setting. To the best of our knowledge, the data we use is thus far unexplored in the context of FII ownership sensitivity to corporate governance mechanisms.

2. Related literature

According to Shleifer and Vishny (Citation1997), corporate governance is a straightforward agency problem and refers to the various constraints that either manager put on himself or investors put on managers to reduce agency problems. They note that the study of corporate governance is practically important due to a great deal of disagreement on the appropriateness of the existing mechanisms, even in the advanced economies.

Several studies have documented the role of institutional investors in monitoring and disciplining management. Bushee et al. (Citation2013) investigates the relationship between institutional investors’ ownership preferences and corporate governance mechanisms of firms and show that large investors with a preference for growth firms are more likely to be sensitive to firm-level governance mechanisms. They note that good governance mechanisms help in decreasing the monitoring costs of investors. Leuz et al. (Citation2010) investigate whether governance concerns would result in fewer foreign holdings and documents that foreign investors hold fewer shares in firms that have ownership structures that are more conducive to expropriation risk by insiders. Additionally, they show that the effect of firm-level governance on foreign investment even more pronounced in countries with weak disclosure regulation and investor protection laws.

Previous studies such as Bushee et al. (Citation2013) have used board characteristics such as board size, outsider ratio, CEO-duality as proxies for measuring corporate governance. Yermack (Citation1996) examines the relationship between board size and market valuation and documents an inverse association for a sample of 452 large US industrial corporations. He shows that the greatest loss in firm value occurs when boards grow from small to medium size. Additionally, he argues that companies with small boards have better operating and profitability ratios. Jensen (Citation1993) notes that small boards help in improving firm performance and suggests that boards with more than eight members are less likely to be effective. Eisenberg et al. (Citation1998) examine the relationship between board size and profitability for a sample of small Finnish firms and document a negative correlation. Their result corroborates the findings of Yermack (Citation1996) for a sample of firms substantially smaller. Mak and Kusnadi (Citation2005) examine the impact of corporate governance mechanisms on firm value using a sample of 460 firms listed on the Singapore Stock Exchange and Kuala Lumpur Stock Exchange and shows that there exists a negative relationship between board size and firm value.

Board of directors have the responsibility of monitoring and disciplining the management. Further, investors expect board members, particularly outside directors, to provide timely and value relevant information that would help in mitigating the information asymmetry problems. However, some previous studies have expressed their skepticism about the effectiveness of outside directors. In one of the early studies, Jensen (Citation1993) alludes to the issue of information problems in large corporations hindering the ability of highly talented board members in contributing to mitigate the agency problems. Duchin et al. (Citation2010) investigate the effectiveness of outside directors by empirically estimating the relationship between firm performance and the change in the percentage of independent directors for a sample of US firms over the period 2000–2005. They find that, on average, outside directors’ do not help or hurt performance. However, the effectiveness of outside directors is conditional on the cost of information acquisition. The effectiveness significantly improves when the information cost is low and decreases when the cost is high.

In contrast, Bowman and Min (Citation2012) investigate the impact of a regulatory change that requires Korean firms to increase the outside director ratio and finds that increased board independence helps to attract more foreign investment. However, they find that the effectiveness of outside director system on foreign ownership is less effective for chaebols (family-controlled Korean conglomerates). Overall, some of the recent studies suggest that one cannot expect a uniform performance effect of board independence across all firms.

On CEO- duality, Jensen (Citation1993) advocates that firms should separate the positions of CEO and Chairman of the board for the board to perform its critical functions. Finkelstein and D’aveni (Citation1994) employ a contingency-based approach to investigate a firms’ likelihood of using a dual CEO structure. They argue that CEO duality is not always dysfunctional as proposed by agency theory, and non-duality is not always dysfunctional, as suggested by organizational theory. Instead, the effectiveness of CEO duality is contingent upon the informal CEO power and firm performance. When either CEO power or firm performance is high, CEO duality is more likely to be dysfunctional as predicted by agency theory. On the contrary, low CEO power and poor firm performance, necessitates the presence of strong leadership, thereby making non-duality more dysfunctional.

Board meeting attendance is a direct proxy to measure director effort and commitment towards the shareholders. Chou et al. (Citation2013) investigates the relationship between firm profitability and meeting attendance of directors for a sample of approximately 650 non-financial Taiwanese firms and finds that high meeting attendance by directors’ themselves can enhance firm performance. However, attendance by their representatives has an adverse effect.

2.1. Data and variables

2.1.1. Data

To explore the objectives stated above, we employ the PROWESS database, provided by the Centre for Monitoring Indian Economy (CMIE).Footnote1 The sample period begins from the financial year 2005 and ends in the financial year 2019 (April 2004—March 2019). The total sample consists of 34,428 firm–year observations after removing missing values for all variables employed in the study. For our sample firms, the financial year starts in April and ends in March.

Table presents the summary statistics of percentage ownership by different investor categories such as FII, mutual funds, Indian and foreign promoters, and overall institutions. FII ownership as the proportion of shares held by FIIs in aggregate at the end of a financial year. Panel A shows that mean ownership by FIIs is 2.1% higher than that of domestic mutual funds. Further, the mean promoter ownership is close to 50%, indicating the level of ownership concentration. Panel B presents summary statistics for firms that have positive FII ownership. More than 50% of firm-year observations in our sample have positive FII ownership.

Table presents the summary statistics for the explanatory variables used in the regression analysis. The mean BM ratio for our sample is 1.03, and a typical firm has a market capitalization of INR 2175.43 Million. The average board size for our sample is 9.02 numbers, and the percentage of outside directors is 43%. In unreported analysis, we find that the mean BM ratio for firm-years with positive FII ownership is 0.84, and the mean board size is 10.57 numbers.

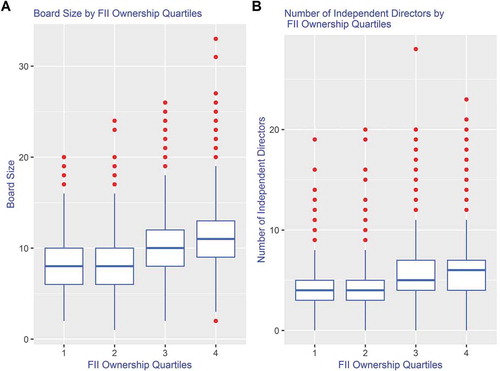

Table presents the fraction of firms with positive FII ownership by year. The data suggests that the number of firms with FII ownership is showing a consistent increase from the financial year 2005 to 2019. Moreover, the number of firms with FII ownership increased from 1179 in the financial year 2008 to 1198 in the year 2009, suggesting that the recent financial crisis did not have a visible negative effect on foreign demand for Indian equity ownership. Figure plots the relationship between FII ownership quartiles and two important board characteristic variables, the board size, and the number of independent directors. For this purpose, each year, we sort firms into quartiles based on FII ownership. The plots show that as FII ownership increases, median board size and number of independent directors’ increases, suggesting that FIIs have a higher preference for bigger boards and a higher number of outside directors. Further, our unreported analysis reveals that out of the total 17,262 firm—years that have positive FII ownership, CEO—duality is absent in 96% of the firm-years.

Figure 1. Panel A shows the relationship between board size and FII ownership quartiles

3. Variables

3.1. Measuring corporate governance

Following Bushee et al. (Citation2013), we use board characteristics that include board size, fraction of independent directors, CEO duality, and board meeting attendance as corporate governance proxies.

3.1.1. Board size (n_dir)

Prior studies show that board size affects the efficiency of board decision making. Lipton and Lorsch (Citation1992) argue that larger boards are effective monitors, but are slower in making decisions. They attribute the relative lack of effectiveness to factors, such as lack of cohesiveness among the board members, and lack of time. The complexity of the matters, coupled with the power of the top management, exacerbates the board effectiveness problem. Hence, they suggest that the costs of larger boards outweigh the benefits of more efficient monitoring. Jensen (Citation1993) argues that CEOs have greater control over boards that have more than eight members. Consistent with Lipton and Lorsch (Citation1992), Yermack (Citation1996) argues that larger boards have greater coordination problems relative to smaller ones, and evidences an inverse relationship between board size and firm value. Our proxy for the board size is the yearly sum of the number of directors.

3.1.2. Outsider ratio (n_ind)

Independent directors are considered more effective monitors of the firm. Rosenstein and Wyatt (Citation1990) show that share prices react positively after outside director appointments. Helland and Sykuta (Citation2005) document that firms that are targets of shareholder litigation have a lower percentage of outside directors, and smaller boards, suggesting that outside directors and bigger boards do a better job of monitoring the monitor. Bhagat and Black (Citation2002) examine the relationship between board independence and firm performance for a sample of large US firms and finds that firms with more independent firms do not perform better than others do. However, several recent studies argue that independent directors are less effective when the firms’ information environment is opaque, plausibly due to the relatively higher cost of acquiring and processing information.

3.1.3. CEO duality (dual)

Being equipped with the most relevant private information about the firms’ prospects, CEO-Chairman is the most influential person on the board. He controls the flow of information to the board and board meetings. The dependence of the board on the CEO-Chairman dilutes the role as an effective monitor of the management. We code the variable “dual” as 1 when the role is combined and 0, otherwise.

3.1.4. Board meeting attendance (attd)

Attendance at the board meetings is an indicator of the director’s effort in monitoring the management and indirectly measures his/her effectiveness. Following Bushee et al. (Citation2013), we use an indicator variable coded as “1” if any director misses 75 percent or more of board meetings and 0 otherwise.

3.2. Moderators

3.2.1. Firm Size (SIZE)

Kang (Citation1997) show that foreigners have a higher preference for large firms, as they are better informed about. The preference for large firms could be due to the higher market liquidity and greater investor attention, potentially mitigating the problems due to information asymmetries. We measure firm size as the logarithm of market capitalization, measured on the first trading day of January. Measuring market capitalization on the first trading day of January enables us to establish better the cause-effect relationship between firm size and FII ownership, measured at the end of the fiscal year (31st, March).

3.2.2. Book-to-Market Value (BM)

Lakonishok et al. (Citation1992) show that stock markets are overly optimistic about low BM firms as they naively over-extrapolate the earnings growth of such firms. Further, the rapid growth of low BM firms makes their current tangible fundamentals less important than their hidden fundamentals or growth fundamentals. Hence, it is highly likely that stock markets overvalue such firms, thereby increasing the risk of negative earnings surprises. We measure BM the log of book-to-market value, measured on the first trading day of January, consistent with our approach of measuring the higher frequency explanatory variables with lags.

3.3. Control variables

We employ a set of control variables, previously documented as determinants of institutional ownership (Gompers & Metrick, Citation2001). We control for liquidity (TURN) by taking the logarithm of average yearly turnover for the stock scaled by the yearly shares outstanding. Average yearly turnover is equal to the sum of the average yearly stock turnover of the two prominent exchanges in India, the Bombay Stock Exchange (BSE) and National Stock Exchange (NSE). Prior research employs stock return volatility as a proxy for risk. We compute volatility (VOL) as the standard deviation of the past twelve months returns, before the fiscal year-end. Further, to capture the momentum (RET-1) effect, we employ the twelve-month lagged return. Lastly, share price (PRICE) is the log of the share price on the first trading day of January.

4. Hypothesis Development

4.1. Board size, FII ownership and the moderating effects of firm size and PB ratio

Prior literature broadly divides the functions of boards into three: resource mobilization, governance, and strategic. In its resource mobilization function, boards link firms to the external world and help in securing critical resources. The resource dependency theory argues that large and diverse boards are more effective in getting timely access to critical resources (Goodstein et al., Citation1994). In its governance function, boards have the role of controlling managerial opportunism and ensuring that organizational decision making is consistent with stakeholder interests. Finally, in its strategic role, boards involve in taking important decisions, particularly during periods of internal and external turbulence.

While large and diverse boards would be useful in fulfilling the resource mobilization and governance functions, they may not be suited in quickly responding to changes in both internal and external business environments. Lipton and Lorsch (Citation1992) state that as the board size increases beyond ten members, they become dysfunctional. Further, they argue that smaller boards allow directors to have productive discussions, and to reach a consensus from their deliberations. Additionally, slower decision-making plagues bigger boards.

Large firms attract more investor attention and analysts’ following. Prior research recognizes that analysts’ following can potentially improve firms’ information environment. Hence, large investors would be less concerned about the governance of large firms relative to smaller ones. Further, large firms would have better access to relevant resources due to a bigger scale of operations. These arguments suggest that investors in large firms would give a higher weight to the strategic role of boards relative to the monitoring and resource mobilization functions.

Agile strategic decision making by boards is essential for firms operating in turbulent business environments such as emerging markets. Uncertain environments magnify the challenges for decision-makers, particularly in smaller firms. Hence, investors would have a higher preference for smaller boards in smaller firms. However, as firm size increases, investors would outweigh the benefits of comprehensive decision making over the costs associated with slower decision making by larger boards. Based on these arguments, we conjecture that as firm size increases, FIIs would prefer larger boards, suggesting a positive moderating effect of size on the relationship between board size and FII ownership.

Higher PB firms or “growth” firms have unclear growth fundamentals with a significant value attached to non-financial disclosures. Prior research documents that good governance practices positively influences investments by institutions. Unclear growth fundamentals, coupled with the need for risk capital, increases the criticality of the role played by boards in growth firms. Additionally, high PB firms require the quick mobilization of state-of-the-art resources for fueling their growth. Bigger boards that have better access to resources have the potential to contribute partly surmounting the challenge of mobilizing value-enhancing resources. Hence, based on the previously mentioned arguments, we conjecture that PB ratios would have a positive moderating effect on the relationship between board size and FII ownership.

H1a: Firm size positively moderates the effect of board size on FII ownership

H1b: PB positively moderates the effect of board size on FII ownership

4.2. Outsider ratio, FII ownership and the moderating effects of firm size and PB ratio

Corporate governance literature argues that boards of directors monitor the actions of the management and helps in ameliorating the potential agency conflicts with the shareholders. Typically, boards have a mixture of insiders and outsiders, with significant cross-sectional variation across firms. Typically, the management that includes the CEO of the firm controls the process of selecting the board members and its composition. The process of endogenously selecting the board members weakens the incentives for them to monitor the management and the CEO. In particular, directors of a firm wanting to build a reputation as expert monitors face the difficult challenge of choosing between being a strict monitor or a person who does not want to make a problem for the CEO. Moreover, a highly influential and performing CEO exacerbates the problem for the directors, thereby weakening the independence of the board.

In such instances, investors depend on outside directors to provide value-relevant information monitoring. Outside directors in their role as monitors and advisors of firms, must acquire and process substantial firm-specific information. They face significant challenges in acquiring and processing information, especially when the information environment is opaque.

Further, considering that the growth fundamentals of high PB stocks are unclear, the process of procuring and processing high-quality information requires significant director skill and effort. Investors, particularly international investors, rely on outside directors providing value-relevant information and expertise. Based on these arguments, we hypothesize that both firm size and PB ratios would positively moderate the relationship between outsider ratio and FII ownership.

H2a: Firm size positively moderates the effect of outsider ratio on FII ownership

H2b: PB positively moderates the effect of outsider ratio on FII ownership

4.3. CEO-Duality, FII ownership and the moderating effects of firm size and PB ratio

CEO duality refers to a board structure in which the Chief Executive Officer is the Chairman of the Board (Yang & Zhao, Citation2014). Prior literature examining the efficacy of CEO duality has produced mixed evidence. Studies favoring CEO duality argues that CEOs are privy to high-quality firm-specific information acquired through running the daily operations. The main argument against dual leadership is that CEOs, as agents of the shareholders, will choose a set of activities that are sub-optimal to maximizing firm value (Jensen & Meckling, Citation1995). Nevertheless, our objective is not to resolve the conflict on CEO duality. Instead, our focus is to examine the role of firm size and PB in determining the relationship between FII ownership and CEO duality.

Considering that high PB firms encounter frequent exogenous shocks from the market participants, the information benefits of dual CEOs can potentially enhance the market power of firms. Additionally, the external environment of high PB or growth firms demands fast and frequent decision-making. Dual leadership allows firms to respond quickly to new information generated both within and outside the firms. However, from the perspective of investors, assessing the fundamental value of growth stocks only based on financial disclosures is likely to be less accurate relative to value stocks. For high PB firms, the current disclosed fundamentals would be less relevant than other non-financial measures. The need to assess the value of growth firms using qualitative non-financial disclosures necessitates the presence of an extra chain of command that separates the leadership. Hence, based on this argument, we hypothesize that, as PB increases, FIIs would prefer the CEO and Chairman to be two different individuals in their investee firms.

Consistent with the argument that FIIs would outweigh the benefits of comprehensive decision making over fast and frequent decision making in large firms, we hypothesize that firm size would negative moderate the relationship between CEO-duality and FII ownership.

H3a: Firm size negatively moderates the effect of CEO—Duality on FII ownership

H3b: PB negatively moderates the effect of CEO—Duality on FII ownership

4.4. Board meeting attendance, FII ownership and the moderating effects of firm size and PB ratio

The directors provide valuable information and strategic inputs to both the management and the investors. Hence, understanding the working behavior of directors is an important input to the investment decision process. The directors mainly collect information on the firm’s activities by attending the board meetings. Since high PB firms are more sensitive to exogenous shocks, we conjecture that FIIs would expect the directors of such firms to put in more effort relative to the low PB firms. Hence, we hypothesize that PB negatively moderates the relationship between FII ownership and poor attendance. Similarly, we expect a negative moderating effect of firm size on the relationship between FII ownership and poor attendance.

H4a: Firm size negatively moderates the effect of poor attendance on FII ownership

H4b: PB negatively moderates the effect of poor attendance on FII ownership

5. Empirical results

The following generic quarterly regression equation represents the overall framework that we estimate on twelve models for the period April 2004 to March 2018:

In Model 1 we examine the relation between FII ownership (and a set of control variables similar to Gompers and Metrick (Citation2001) that are known to affect institutional ownership such as stock turnover, volatility, past returns (12 months), share price, price to book value, and size. In Model 2, in addition to the control variables, we include the four board characteristics (board size, outside director ratio, and indicator variables for CEO duality and greater than 75% absence for board meeting). Model 2 is the base model for all subsequent estimations.

Further, using Models 3 to 6, we separately estimate the moderating effect of firm size with each of the board characteristics. For this, we append the base model with the respective interaction terms. In Model 7, we append the base model with the full set of interactions of firm size with the four board characteristics. Like Models 3 to 7, we estimate the moderating effect of BM in Models 8 to 12. In all the panel regressions, we employ the fixed effects estimation methodology with time effects.

Table presents the results of the panel regressions. Model 1 reports a statistically significant relationship between level FII ownership and our control variables. Consistent with previous literature, firm size, share price, and share turnover are positively associated with FII level ownership. The results indicate that an increase in volatility has a significant negative effect on FII ownership. Model 2 includes firm and board characteristics. The coefficient of board size and outsider ratio is positive and significant. The positive association between FII ownership and board size suggests that FIIs prefer larger boards, plausibly due to their monitoring effectiveness. Similarly, foreign institutions show a significant preference for a higher fraction of independent directors. This result contradicts several recent studies that argue that busy independent directors and independent directors who are more socially connected to the CEO, and sympathetic to the management tend to be less effective in their role (Chidambaran et al., Citation2012; Cohen et al., Citation2012; Liu et al., Citation2017).

Models 3–6 reports the moderating role of firm size on the relationship between FII ownership and each of the board characteristics. In particular, model 3 shows that firm size positively moderates the impact of board size on FII ownership, suggesting that for bigger firms, as board size increases, FII ownership increases. Model 4 shows that firm size positively moderates the relationship between foreign ownership and the fraction of independent directors, suggesting that in bigger firms, FIIs would give a higher value for board independence. The results of Model 5 indicates that firm size positively moderates the relationship between CEO-duality and FII ownership. More specifically, the finding suggests that foreign investors prefer to have the same person as CEO and Chairman of the board for bigger firms. The result of model 5 contradicts our hypothesis that as firm size increases, FIIs would prefer leadership separation to duality.

In model 7, we run panel regressions by including the main effects of all four variables representing board characteristics, interactions between firm size and board characteristic variables, and control variables. We find that the coefficient signs of the interactions of board size and board independence with the firm size are positively significant, suggesting that as firm size increases, FIIs prefer bigger boards. This result is inconsistent with the finding of Yermack (Citation1996) that there is a significant negative relation between board size and firm performance. The interactions of CEO-duality and poor attendance with firm size are not significant in Model 7.

Models 8–12 run panel regressions in the same vein as models 2–7, using price-to-book value (PB) as the moderating variable. Similar to the interaction of board size and firm size (model 2), model 8 shows that PB positively moderates the relationship between FII ownership and board size. The positive moderating effect of PB on the ownership—board size association, suggests that as the PB ratio increases, FIIs have a higher preference for firms with relatively larger boards. High PB firms, often referred to as ‘growth firms” in literature, have many value relevant non-financial sources of disclosure other than financial statements. The potential information asymmetries caused by non-financial disclosures of high PB firms magnifies the investment challenges faced by foreign investors. Hence, the preference by FIIs for larger boards could plausibly be due to its better monitoring roles and better quality information diffusion.

In model 8, we update model 2 with the interaction of PB with board size. The coefficient of the interaction term suggests that PB positively moderates the relationship between board size and FII ownership. The result is significant at the 1% level. Model 9 is an update of model 2 with the interaction of PB and outside director ratio. The significant negative coefficient suggests that as PB increases, FIIs prefer lesser board independence. In model 12, we include all the interactions between PB and board characteristics. In this model, the interactions of board size, outsider ratio, and CEO—duality with PB are significant at the 5% level.

The positive coefficient of the interaction of PB and outsider ratio supports our argument that FIIs put a higher value on the advisory role played by outside directors in growth firms. This could be due to the high and difficult to assess market valuations of growth firms. Consistent with our finding, Fich (Citation2005) documents that those firms desiring to exploit their growth fundamentals seek the expert advice of well performing outside directors. Alternatively, acceptance of outside directorships signals the markets that growth fundamentals and the prospects of the appointing firms’ are positive. Moreover, unaffiliated monitoring by outside directors could potentially mitigate the expropriation risk feared by outside owners, particularly foreign investors.

The Hausman test for choosing between fixed effects and random effects model suggests using the later. Hence, in all our models, we estimate the fixed effects model by controlling for time effects.

6. Conclusion

Our study examines the ownership preferences of foreign investors in an emerging market setting, characterized by weak information environments, and high insider ownership concentration. Following the argument of Forbes and Milliken (Citation1999) that board effectiveness depends on the context, we employ a contingency-based approach in this study. More specifically, we investigate the contextual relationship between FII ownership and board characteristics by separately using firm size and price to book value as the context defining variables. Our study provides evidence on the role of corporate governance mechanisms in an emerging market where investor protection is relatively weak and where foreign investment is particularly important.

Consistent with Yermack (Citation1998) that firms with smaller boards create more value relative to bigger boards, we find that there is a negative association between FII ownership and board size. However, our results also indicate that firm size positively moderates the relationship between board size and FII ownership, suggesting that FIIs prefer bigger boards in larger firms. One plausible explanation for this preference could be that bigger boards with divergent views would improve board vigilance and would limit the chances of expropriation by managers and controlling shareholders, suggesting that FIIs outweigh the benefits of monitoring over the associated coordination problems.

Thus far, the evidence on the effectiveness of board independence is mostly inconclusive. Duchin et al. (Citation2010) argue that the effectiveness of outside directors is conditional on the cost of information acquisition. Our results indicate that FII ownership has a negative relationship with board independence, consistent with the argument of Jensen (Citation1993). However, the significant coefficient for the interaction of firm size and outsider ratio suggests that FIIs prefer greater board independence in larger firms. Given that the cost of information gathering would be relatively low in larger firms due to broader analyst following, our result is consistent with the findings of Duchin et al. (Citation2010).

Finkelstein and D’aveni (Citation1994) argue that the effectiveness of the same person holding the position of CEO and Chairman of the board is contingent upon CEO power and firm performance. Our results show that, for firms with higher market-to-book ratios, FII prefers separating the role of CEO and Chairman. The fact that firms with high PB ratios are more likely to be young, growth firms with more non-financial disclosures relative to their matured peers, can potentially lead to opportunistic behavior by CEOs. Fama and Jensen (Citation1983) argues that granting CEOs an influential role on the board increases the likelihood of deviant behaviors. Consistently, our result suggests that as market-to-book ratio increases, FIIs prefer CEO non-duality.

The study suggests that for large and high growth firms operating in emerging markets similar to India, increasing the board size and outsider ratio would help in attracting foreign capital. Future research that focuses on determining the optimal board size and outsider ratio would complement our study. Finally, our results imply that high growth firms, aiming to attract foreign capital, should separate the role of CEO and Chairman.

Additional information

Funding

Notes on contributors

Smitha Nair

Smitha Nair is an Assistant Professor with Department of Management, Amrita Vishwa Vidyapeetham, India. Among research-topics, she explores the specificities of the relationship between corporate governance of firms and the roles and preferences of financial institutions.

Notes

1. PROWESS database is widely used in corporate finance studies involving Indian firms.

References

- Aggarwal, R., Klapper, L., & Wysocki, P. D. (2005). Portfolio preferences of foreign institutional investors. Journal of Banking & Finance, 29(12), 2919–17. https://www.sciencedirect.com/science/article/abs/pii/S0378426604002559

- Bennett, J. A., Sias, R. W., & Starks, L. T. (2003). Greener pastures and the impact of dynamic institutional preferences. The Review of Financial Studies, 16(4), 1203–1238. https://doi.org/10.1093/rfs/hhg040

- Bhagat, S., & Black, B. (2002). The non-correlation between board independence and long-term firm performance. Journal of Corporation Law, 27(2), 231.

- Birkinshaw, J., Nobel, R., & Ridderstråle, J. (2002). Knowledge as a contingency variable: Do the characteristics of knowledge predict organization structure? Organization Science, 13(3), 274–289. https://doi.org/10.1287/orsc.13.3.274.2778

- Black, B. S., & Khanna, V. S. (2007). Can corporate governance reforms increase firm market values? Event study evidence from india. Journal of Empirical Legal Studies, 4(4), 749–796. https://doi.org/10.1111/jels.2007.4.issue-4

- Bowman, R. G., & Min, B. (2012, March). The positive impact of corporate governance on foreign equity ownership: Evidence from Korea. In 2012 financial markets & corporate governance conference. https://doi.org/10.2139/ssrn.2026036

- Bushee, B. J., Carter, M. E., & Gerakos, J. (2013). Institutional investor preferences for corporate governance mechanisms. Journal of Management Accounting Research, 26(2), 123–149. https://doi.org/10.2308/jmar-50550

- Chan, K., Covrig, V., & Ng, L. (2005). What determines the domestic bias and foreign bias? Evidence from mutual fund equity allocations worldwide. The Journal of Finance, 60(3), 1495–1534. https://doi.org/10.1111/j.1540-6261.2005.768_1.x

- Chidambaran, N. K., Kedia, S., & Prabhala, N. R. (2012). CEO-director connections and corporate fraud, fordham University school of business research paper. 96(5). https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1787500, https://doi.org/10.1094/PDIS-11-11-0999-PDN

- Chou, H. I., Chung, H., & Yin, X. (2013). Attendance of board meetings and company performance: Evidence from Taiwan. Journal of Banking & Finance, 37(11), 4157–4171. https://doi.org/10.1016/j.jbankfin.2013.07.028

- Cohen, L., Frazzini, A., & Malloy, C. J. (2012). Hiring cheerleaders: Board appointments of “Independent” directors. Management Science, 58(6), 1039–1058. https://doi.org/10.1287/mnsc.1110.1483

- Dixit, B. K. (2015). Board characteristics, ownership structure and the market for corporate control in India. India finance conference, IIM.

- Duchin, R., Matsusaka, J. G., & Ozbas, O. (2010). When are outside directors effective? Journal of Financial Economics, 96(2), 195–214. https://doi.org/10.1016/j.jfineco.2009.12.004

- Eisenberg, T., Sundgren, S., & Wells, M. T. (1998). Larger board size and decreasing firm value in small firms. Journal of Financial Economics, 48(1), 35–54. https://doi.org/10.1016/S0304-405X(98)00003-8

- Fama, E. F., & Jensen, M. C. (1983). Agency problems and residual claims. The Journal of Law and Economics, 26(2), 327–349. https://doi.org/10.1086/467038

- Ferreira, M. A., Matos, P., Pereira, J. P., & Pires, P. (2017). Do locals know better? A comparison of the performance of local and foreign institutional investors. Journal of Banking & Finance, 82, 151–164. https://doi.org/10.1016/j.jbankfin.2017.06.002

- Fich, E. M. (2005). Are some outside directors better than others? Evidence from director appointments by fortune 1000 firms. The Journal of Business, 78(5). https://doi.org/10.1086/431448

- Finkelstein, S., & D’aveni, R. A. (1994). CEO duality as a double-edged sword: How boards of directors balance entrenchment avoidance and unity of command. Academy of Management Journal, 37(5), 1079–1108.

- Forbes, D. P., & Milliken, F. J. (1999). Cognition and corporate governance: Understanding boards of directors as strategic decision-making groups. Academy of Management Review, 24(3), 489–505. https://doi.org/10.5465/amr.1999.2202133

- Gillan, S. L., & Starks, L. T. (2000). Corporate governance proposals and shareholder activism: The role of institutional investors. Journal of Financial Economics, 57(2), 275–305. https://doi.org/10.1016/S0304-405X(00)00058-1

- Gompers, P. A., & Metrick, A. (2001). Institutional investors and equity . The Quarterly Journal of Economics, 116(1), 229–259. https://doi.org/10.1162/003355301556392

- Goodstein, J., Gautam, K., & Boeker, W. (1994). The effects of board size and diversity on strategic change. Strategic Management Journal, 15(3), 241–250. https://doi.org/10.1002/()1097-0266

- Helland, E., & Sykuta, M. (2005). Who’s monitoring the monitor? Do outside directors protect shareholders’ interests? Financial Review, 40(2), 155–172. https://doi.org/10.1111/fire.2005.40.issue-2

- Jensen, M. (1993). The modern industrial revolution, exit, and the failure of internal control systems. The Journal of Finance, 48(3), 831–880. https://doi.org/10.1111/j.1540-6261.1993.tb04022.x

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- Jensen, M. C., & Meckling, W. (1995). Specific and general knowledge and organizational structure. Journal of Applied Corporate Finance, 8(2), 4–18. https://doi.org/10.1111/jacf.1995.8.issue-2

- Kang, J. K. (1997). Why is there a home bias? An analysis of foreign portfolio equity ownership in Japan. Journal of Financial Economics, 46(1), 3–28. https://doi.org/10.1016/S0304-405X(97)00023-8

- Lakonishok, J., Shleifer, A., & Vishny, R. W. (1992). The impact of institutional trading on stock prices. Journal of Financial Economics, 32(1), 23–43. https://doi.org/10.1016/0304-405X(92)90023-Q

- Leuz, C., Lins, K. V., & Warnock, F. E. (2010). Do foreigners invest less in poorly governed firms? Review of Financial Studies, 23(3), 3245–3285. https://doi.org/10.1093/rfs/hhn089.ra

- Lipton, M., & Lorsch, J. W. (1992). A modest proposal for improved corporate governance. The Business Lawyer, 59–77. American Bar Association. https://www.jstor.org/stable/40687360?seq=1

- Liu, C., Low, A., Masulis, R. W., & Zhang, L. (2017). Monitoring the monitor: Distracted institutional investors and board governance. European Corporate Governance Institute (ECGI)-Finance Working Paper, (531).

- Mak, Y. T., & Kusnadi, Y. (2005). Size really matters: Further evidence on the negative relationship between board size and firm value. Pacific-Basin Finance Journal, 13(3), 301–318. https://doi.org/10.1016/j.pacfin.2004.09.002

- Rosenstein, S., & Wyatt, J. G. (1990). Outside directors, board independence, and shareholder wealth. Journal of Financial Economics, 26(2), 175–191. https://doi.org/10.1016/0304-405X(90)90002-H

- Shleifer, A., & Vishny, R. W. (1997). A survey of corporate governance. The Journal of Finance, 52(2), 737–783. https://doi.org/10.1111/j.1540-6261.1997.tb04820.x

- Sias, R. W. (2007). Reconcilable differences: momentum trading by institutions. Financial Review, 42(1), 1–22. https://doi.org/10.1111/fire.2007.42.issue-1

- Yang, T., & Zhao, S. (2014). CEO duality and firm performance: Evidence from an exogenous shock to the competitive environment. Journal of Banking & Finance, 49, 534–552. https://www.sciencedirect.com/science/article/abs/pii/S0378426614001344

- Yermack, D. (1996). Higher market valuation of companies with a small board of directors. Journal of Financial Economics, 40(2), 185–211. https://doi.org/10.1016/0304-405X(95)00844-5

- Yermack, D. (1998). Companies’ modest claims about the value of CEO stock option awards. Review of Quantitative Finance and Accounting, 10(2), 207–226. https://doi.org/10.1023/A:1008299824396

- Zona, F., Zattoni, A., & Minichilli, A. (2013). A contingency model of boards of directors and firm innovation: The moderating role of firm size. British Journal of Management, 24(3), 299–315. https://doi.org/10.1111/bjom.2013.24.issue-3

Appendix

Table A1. Descriptive Statistics of Institutional and Promoter Ownerships

Table A2. Summary Statistics the Independent Variables

Table A3. Frequency Distribution of Fii Ownership and Summary Statistics by Year

Table A4. Regression Results for Fii Ownership and Board Characteristics