?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The main purpose of this study is to establish the mediating role of financial intermediaries in the relationship between financial literacy and financial inclusion of the poor in developing countries with data from rural Uganda. The data for this study were analyzed using Partial Least Square (PLS). The results revealed that financial intermediaries significantly mediates the relationship between financial literacy and financial inclusion. The presence of financial intermediaries such as microfinance banks enhance financial literacy to increase the scope of financial inclusion of the poor in rural Uganda. Thus, policy makers and advocates of financial literacy, especially in developing countries should use financial intermediaries such as microfinance banks to roll out financial literacy programs. This can be achieved through provision of financial literacy clinics, workshops and seminars where the poor can learn about personal finance using hands-on approach. This will help them to make wise financial decisions and choices towards consumption of complex financial products offered by the rural-based financial institutions.

PUBLIC INTEREST STATEMENT

The Organization for Economic Cooperation and Development (OECD) observes that the level of financial literacy still remains low globally with majority of the population, especially in developing countries unable to compute interest rates. Similarly, the provision of more complex financial products by financial institutions to the poor who are financially illiterate has made them more vulnerable to unscrupulous providers of financial services. Thus, there is dire need for financial literacy to help the poor to make wise financial decisions. Consequently, financial intermediaries such as microfinance banks that link the surplus and deficit units, especially in the rural areas can act as channels for delivering financial literacy. Indeed, financial literacy clinics, workshops, and seminars can be conducted by financial intermediaries to equip the poor with knowledge and skills to make wise financial decisions and choices.

1. Background

Currently, financial inclusion has become a buzz-word and a mainstay of banking the unbanked population globally. The World Bank, the United Nations, the G20, Financial Inclusion Experts Group, and the networks of Central Banks argue that access to basic financial services (financial inclusion) like credit, savings, payments, insurance, and remittances by all individuals remain a universal fundamental human rights, especially in the twenty-first century. This is because it economically and socially empowers them to achieve improved welfare (World Bank, Citation2018).

Financial inclusion scholars like Okello et al. (Citation2017); Demirgüç-Kunt, Klapper, Singer, Ansar, and Hess (Citation2018); Karlan et al., (Citation2016); Demirgüç-Kunt, Klapper, and Singer (Citation2017); Chandan and Mishra (Citation2010) suggest that the presence of financial institutions’ structures such as offices, branches, and personnel can promote increased access to financial services, especially in rural areas. Besides, the advocates of micro-financing (United Nation Development Programme, Citation2006; Armendariz de Aghion and Morduch, Citation2005; Yunus, Citation2005) argue that provision of financial services through setting-up of microfinance structures in the rural areas can lead to increased financial inclusion, especially among the poor. Contextually, financial inclusion among the rural poor in Uganda has been promoted by the presence of microfinance banks such as FINCA, PRIDE, UWONET, and BRAC in the rural areas (Bank of Uganda, Citation2017).

Nevertheless, while several strategies have been adopted from both the supply and demand sides to increase the level of financial inclusion, the current GLOBAL FINDEX Survey Data indicates that about 1.7 Billion adults globally remain unbanked with majority living in developing countries (Demirgüç-Kunt, Klapper, Singer, Ansar, and Hess, 2018). The data further shows that the level of financial illiteracy among the adult population stands at 62 percent. In Uganda, the FinScope Survey data (2018) reveals that only 5 percent of the rural adult population use both formal and informal saving mechanisms with only 2 percent borrowing from the formal sources. The discrepancies in the level of access and usage strands are partly due to the complex nature of financial products and services offered by the financial institutions.

Consequently, the Organization for Economic Cooperation and Development – OECD (Citation2009) suggests that financial literacy is relevant for individuals who are presented with complex financial products and services. Indeed, financial literacy help individuals, especially the poor to make wise financial decisions and choices before consuming complex financial products. Scholars like Lusardi et al. (Citation2017), Lusardi and Tufano (Citation2008), Lusardi and Mitchell (Citation2014), and Atkinson and Messy (Citation2013) contend that financial literacy equips rural-based poor individuals with knowledge and skills so that they are capable of evaluating sophisticated financial products offered by financial institutions.

However, the OECD (Citation2017) observes that while financial literacy programs have been conducted globally, the level of financial literacy still remains unacceptably low, especially among the poor who live in developing countries because of the limited strategies in delivering it.

Accordingly, Cohen (Citation2010) argues that in an effort towards promoting financial literacy, a multi-stakeholder framework involving financial intermediaries as a channel through which financial literacy programs can be delivered should be adopted. Indeed, financial intermediaries like microfinance banks can help in conducting financial literacy programs since they play a role in safekeeping deposits, providing credit to households, and building wealth (Dugyala, Citation2018). Recent research shows that financial education programs offered by American Bankers Association resulted in improved savings among community members in Alabama and Wisconsin in the United States of America (American Bankers Association website, Citation2018).

While, nascent studies like Okello et al. (Citation2017); Lusardi, Michaud, and Mitchell (Citation2017); Grohmann et al. (Citation2017); Skimmyhorn (Citation2016); Klapper et al., (Citation2015); Lusardi and Tufano (Citation2008), Prina (Citation2015), and Jamison et al. (Citation2014) reveal that financial literacy is important in increasing the scope of financial inclusion, there is limited or no evidence on the mediating role of financial intermediaries in the relationship between financial literacy and financial inclusion of the poor in developing countries. The above financial inclusion studies make no reference to the role of financial intermediaries such as microfinance banks as a channel through which financial literacy programs can be delivered, especially among the poor in rural communities. More so, a previous study by Cole et al. (Citation2010) also showed that there was no effect of financial literacy delivered by non-bank financial institutions on financial inclusion in Indonesia.

Thus, the main purpose of this study is to establish the mediating role of financial intermediaries in the relationship between financial literacy and financial inclusion of the poor in developing countries with data from rural Uganda. This current study provides evidence on the significant role of microfinance banks in delivering financial literacy to the poor in order to increase the scope of financial inclusion. It adds to the existing literature and theory by identifying microfinance banks as a channel through which financial literacy can be delivered, especially in rural areas where there are limited structures for conducting financial literacy programs.

2. Literature review

2.1. Theory of financial intermediation

The financial intermediation theory is based on the premise of minimizing transaction costs that arise from lack of information in a direct trade. Gurley and Shaw (Citation1960) argue that intermediaries such as banks acquire information that is not readily available in the market from surplus and deficit units and use it to enable savings and borrowing (Mathew and Thompson, Citation2008). Therefore, banks rely on the acquired information for screening and defining its new clients to whom it extends financial services such as loans (Rau, Citation2004; Nissanke and Stein, Citation2003). The costs incurred by banks in the intermediation process in the market determine the penetration level and provision of financial services. Thus, banks safely manage cash and help intermediate between the net savers and borrowers.

Consequently, since banks link the surplus and deficit units within the financial market, they become useful in analyzing and designing the national financial literacy curriculum and guide. This is because they are more informed about the existing financial literacy gaps and deficiency among both the surplus and deficit units. The banks can develop money management modules that directly fit within the existing financial literacy gaps among the savers and borrowers, especially in developing countries. Indeed, some banks have adopted financial literacy as a functional unit in their retail banking services (American Bankers Association website, Citation2018).

2.2. Financial literacy and financial inclusion: the role of financial intermediaries

Financial markets around the world have become increasingly accessible to individuals, including the poor who demand for financial products from diverse financial intermediaries. Specifically, the World Bank (Citation2014) data on “access to finance for all” reveals that while there is increased credit accessibility with high opportunities to borrow, banks have provided sophisticated financial products and services that are difficult to understand, especially by the poor who are illiterate.

Accordingly, financial literacy becomes important to enable consumers, particularly the poor who use these financial products and services to make wise financial decisions and choices (Lusardi, Citation2015). Financial literacy help consumers by offering them the knowledge they need to make sound financial decisions and secure their economic futures. While program design and financial product integration are key factors for a successful financial literacy program, effective delivery channels for reaching target populations are equally important.

Therefore, since financial intermediaries link both the surplus and deficit units who may be financially illiterate in the financial market (see for e.g. Allen et al., Citation2016; Beck & De La Torre, Citation2006), promoting financial literacy requires a multi stakeholder framework built around consumers, the financial services industry and the government as a regulator. The banks can provide financial literacy that improves financial knowledge with improved financial behavior through “teachable moments”, which can result in the availability of financial tools or direct and easy access to financial products. Askari Bank (Citation2018) observes that financial institutions like banks are uniquely positioned to provide financial literacy as they can bridge theoretical economic concepts such as scarcity and opportunity cost, with practical “money-in-the pocket” services. Thus, connecting financial education with financial products allow all individuals to become fully integrated in the traditional financial system, setting them on the path to wealth accumulation. The financial literacy programs provided by banks with specialized products design helps those outside the mainstream financial channels like the poor to transition into the traditional banking system with ease, clarity, and little cost.

Scholars like Mejia (2018) and Joshi (Citation2014) contend that microfinance banks can play a great role in promoting financial literacy through an integrated approach based on the supply side initiatives on financial inclusion. Additionally, since banks have continuously developed new financial products and services for the different consumers, they are in better position to train the consumers as they consistently provide the financial services. More specifically, advice offered by the Reserve Bank of India (RBI) to banks to set up Financial Literacy Centres (FLC) to conduct outdoor financial literacy in all the districts, resulted in increased financial literacy in India. Correspondingly, Grohmann et al. (Citation2017) revealed that bank branch penetration significantly promoted financial literacy and ultimately financial inclusion across 143 countries globally. Therefore, we hypothesize that:

H1:Financial intermediaries significantly and positively mediate the relationship between financial literacy and financial inclusion of the poor in developing countries.

2.3. Financial intermediaries and financial inclusion

Levine, Loayza, and Beck (Citation2000) observe that financial institutions such as banks play a vital role in the society because they create efficiencies geared towards economic growth. By engaging in maturity intermediation, financial institutions offer liquidity to savers and, at the same time, longer-term funds to investors (see also King and Levine, Citation1993).

Contrary to Akerlof’s (Citation1970) asymmetric information notion, Allen and Santomero (Citation1996) state that in the traditional Arrow–Debreu model of resource allocation, firms and households interact through markets and financial intermediaries play no role. When markets are perfect and complete, the allocation of resources is Pareto efficient and there is no scope for intermediaries to improve welfare. However, since markets have imperfections and information asymmetry exist in real economic world of Adam Smith, financial intermediaries have emerged to eliminate, at least partially, the costs associated with information asymmetry in financial markets (Gurley & Shaw, Citation1960).

Consequently, in the absence of perfect market under the “Arrow—Debreu sense”, financial intermediaries such as banks use the information obtained from the lenders and borrowers ex-ante and ex-post to solve the problem of adverse selection and moral hazard in the process of lending. Therefore, financial intermediaries apply costly verification/monitoring and auditing procedures, and forced execution of the debtor due to existence of informational asymmetry (Leland & Pyle, Citation1977).

Financial intermediaries create avenues, which ensure that the individuals and entities which have excess funds are able to invest and earn a return. Besides, those with deficit and require financing for their viable investments are able to borrow sufficient funds at a cost. Indeed, financial intermediaries provide the necessary link between the lenders and borrowers in the financial market. This is consistent with Chandan and Mishra (Citation2010); Ergungor (Citation2010); and Kempson et al. (Citation2004) who argue that financial intermediaries such as banks carry out financial intermediation services by allocating surplus resources from savers or depositors to borrowers. The effectiveness of the microfinance banks in carrying out financial intermediation depends on their ability to assess the benefits and costs of developing suitable financial products that meet customers’ requirements. Cull et al., (Citation2016) revealed that microfinance providers improved profitability among rural-based women entrepreneurs due to increase in their lending. In addition, Johnson and Nino-Zarazua (Citation2009) also found that the presence of MFIs and trust led to more lending in Kenya. Hence, we hypothesize that:

H2:Financial intermediaries significantly and positively affect financial inclusion of the poor in developing countries.

2.4. Financial literacy and financial inclusion

The Organization for Economic Corporation and Development (2009) argues that since financial literacy is linked to borrowing, saving, and spending patterns among diverse sections of consumers of financial products, it is important for economic growth and financial stability, especially among individuals who lack financial knowledge and skills.

Financial literacy help individuals such as the poor to acquire knowledge, understanding of financial concepts and risks, skills, motivation, and confidence to apply such knowledge and understanding in order to make effective decisions across a range of financial contexts, thus, resulting in improved financial wellbeing. Lusardi et al. (Citation2017) argue that more financially literate employees are better investors. Moreover, the higher returns earned by the more financially savvy are an important contributor to household wealth inequality.

Thus, financial literacy is important for the poor who face difficulty in making financial decisions that can have important consequences in their life. Lusardi and Mitchell (Citation2014) observe that more financially savvy people are more likely to plan, save, invest in stocks, and accumulate more wealth. Additionally, Lusardi and Tufano (Citation2008) also suggest that financially literate individuals are less likely to have credit card debt, and when they do borrow, they manage loans better, paying off the full amount each month rather than just the minimum due. Furthermore, Clark, Lusardi, and Mitchell (Citation2016) also state that being more financially literate is associated with higher contribution rates in retirement savings plan. Previous study by Van Rooij et al. (Citation2011) using data from the advanced financial literacy questions that were added to the Dutch DNB Household Survey found that financially sophisticated households were more likely to participate in the stock market. Similarly, Carpena, Cole, Shapiro & Zia (Citation2011) found that financial literacy program led to large and statistically significant improvements in individuals’ awareness of financial products and services available to them, as well as their familiarity about the details of such products and services in Asia. Indeed, financial literacy help individuals, especially the poor to make wise financial decisions and choices before consuming financial services offered by financial intermediaries. Therefore, we hypothesize that:

H3:Financial literacy significantly and positively affect financial inclusion of the poor in developing countries.

3. Methodology and data approach

3.1. Research design, population and sample

The data for this study were collected from poor households located in the northern, eastern, central and western regions in rural Uganda through a cross-sectional research design. This study focused on rural Uganda because 75 percent of the population is rural-based with limited access to financial services (FinScope, Citation2018). Therefore, a total population of 1.2 million poor households residing in rural areas in Uganda was considered for this study according to Uganda Bureau of Statistics—UBOS (Citation2012). The data were collected from a total sample of 400 poor households located in the northern, eastern, central and western regions in rural Uganda. The sample for this study was arrived at using the formulae for sample size determination adopted from Yamane (Citation1973).

Where; n = sample size; N = total population; e = tolerable error (0.05% or 95%).

Therefore, sample size for the households was derived from:

Simple random sampling method was used to select the samples for this study. This was done in order to give all the poor households equal chances of being included in the study. Accordingly, the data for this study were collected from a total sample of 400 poor households located in the northern, eastern, central and western regions in rural Uganda who were randomly selected.

3.2. Sampling method and procedure

Multi-stage sampling technique using regions, districts, and villages was used to identify poor households to be sampled. The four regions included northern, eastern, central, and western regions in rural Uganda. Further, after identifying the regions, simple random sampling technique was then applied to select two districts located in the four regions. The districts created after 2002 were not reflected independently but captured from their original districts. Therefore, in order to identify the samples for this study, simple random sampling was used to select poor households who responded in this study.

In addition, three poverty indicators of households’ utilities, housing conditions, and households’ welfare recommended by the Uganda Bureau of Statistics—UBOS (Citation2012) were also used in identifying poor households for this study. The selected poor households were assigned unique numbers to avoid double inclusion in this study. This selection criteria were applied until a total sample of 400 poor households was arrived at to participate in this study. The units of analyses for this study were the poor households and the units of inquiry were the poor households’ heads. The poor households’ heads were preferred because most studies involving households, especially in Uganda makes reference to households’ heads. This is because they are in better position to provide more information about their particular households. The results from this study revealed that 100 percent response rate was achieved in this study.

3.3. Measurement of study variables

The main purpose of this study is to establish the mediating role of financial intermediaries in the relationship between financial literacy and financial inclusion of the poor in developing countries with data from rural Uganda. The variables for this study included financial literacy, financial intermediation, and financial inclusion.

Financial literacy was the independent variable, while financial intermediation was the mediator variable and financial inclusion was the dependent variable. The items used for measuring the variables were adopted from previous studies published in internationally referenced Journals. Prior to developing the final items to measure the constructs, different views were sought from professionals, academics, and practitioners to improve on the content validity of the instrument.

The concept of financial literacy was measured using 10 questions developed and modified from Atkinson and Messy (Citation2012); Lusardi and Mitchell (Citation2009), Cole et al. (Citation2011), Lusardi and Mitchell (Citation2006), Lusardi (Citation2003), and Holzmann (Citation2010); Kempson (Citation2008) that were adopted and used to measure financial literacy. Financial intermediation by microfinance banks was measured using 14 questions developed and modified from Dutta and Dutta (Citation2011); Allen et al., (Citation2011); Yaron et al. (Citation1997). Finally, the variable of financial inclusion was measured using 10 questions adopted and modified from previous studies like ACCION (Citation2011); AFI, Citation2010; Čihák et al. (Citation2012); Claessens (Citation2006); Kempson (Citation2006); Ardic et al. (Citation2011); Kendall et al., (Citation2010); Beck and De La Torre (Citation2006).

The questions used to measure the variables under this study were put on a 5-point likert scale to obtain responses from the selected poor households. The likert scale ranged between 1 and 5 with (1) strongly disagree; (2) disagree; (3) not sure; (4) agree; and (5) strongly agree. The 5-point likert scale was used because of its versatility, clarity, simplicity and wide application in social science research as recommended De Vellis (Citation2003), Likert (Citation1932), and Johns (Citation2010).

3.4. Data collection and instruments

The data for this study were collected from a randomly selected sample of 400 poor households located in the northern, eastern, central and western regions in rural Uganda using a semi-structured questionnaire. The questionnaires were administered to poor households’ heads who were clients of PRIDE Microfinance bank. The respondents who responded in this study were randomly selected from poor households located in the northern, eastern, central and western regions in rural Uganda. This is because the rural areas in Uganda have the largest number of poor households who have limited access to financial services as compared to the urban and semi-urban areas in Uganda (FinScope, 2018).

3.5. Test for common method bias

The test for common method bias was performed to ensure that the results were not bias. Initially, all the questions used to measure the variables under this study were adopted and modified from previous studies. Besides, all the questions were made simple and concise to ensure that the respondents understood them clearly. Furthermore, the data were also collected at the same time using the same instrument developed for all the variables under this study. Thus, two approaches were used:

Firstly, we examined the exploratory unrotated factor analysis to generate the results of Harman’s single-factor test using statistical packages for social sciences (Podsakoff et al., Citation2003). This was done to determine whether a single factor emerged that explained the majority of the variances within the variable of financial inclusion. The results from the factor analysis indicated that the first factor accounted for 19.7 percent variation in financial inclusion with Eigen value of 12.411, and together with the other factors, they explained 79 percent of financial inclusion. This confirmed that multiple factors emerged from the variable of financial inclusion to explain its variation. Therefore, this result suggested that the data did not suffer from common method bias.

Secondly, because of the growing dispute about the merits of Harman’s single factor test, the results from Harman’s single-factor test were compared by examining a correlation matrix of the constructs using Pearson’s correlations to determine if any of the correlations were above 0.90 among the formative indicators. The results indicated that the correlations were below the suggested upper limit. This showed evidence of non-existence of common method bias in the data for this study.

3.6. Data management and analysis

Data management involves data capturing, checking and finding errors in the data file, and correcting the existing errors in the data file (Field, Citation2005; Pallant, Citation2005; Hair et al., Citation2010). The errors may arise during data collection due to incorrect responses, careless scoring, and missing instruments. Therefore, the data collected from the field were captured into the statistical package for social sciences (SPSS) and checks for anomalies were performed on the data. The checks for data entry errors, missing values, outliers, and normality were performed. The missing values analysis was tested by running frequencies for all the items in the questionnaire. The results showed that missing values existed in the data, which were missing at completely random (MCAR) and at less than 5 percent that was recommended for replacement as stipulated by Field (Citation2005). Therefore, the missing values in the data were replaced by linear interpolation as recommended by Field (Citation2005). Besides, the test for existence of outliers in the data was carried out through the use of box plots. The results indicated that outliers were not a problem in the data. In addition, the histogram and the normal pp plots were also used to check whether the data were normally distributed. The results showed that the histogram was bell-shaped and the normal pp plots had values that were falling along the straight line meaning that the data were normally distributed.

3.7. Testing for mediation effect in Partial Least Square (PLS)

Prior to testing for the mediation effect, SPSS was adopted to establish whether the data were good for further statistical tests. Thereafter, PLS was used to establish the mediating role of financial intermediaries in the relationship between financial literacy and financial inclusion of the poor in developing countries with data from rural Uganda.

3.7.1. Measurement models

According to Hair et al. (Citation2016), measurement models are constructed to establish the relationships between the observed measures and underlying factors of a variable grounded on the existing theoretical underpinnings in the study. Thus, the measurement models are constructed in PLS to determine the construct, content, convergent and discriminant validities to assess the relationships between the observed measures and the underlying factors for all the variables under study.

3.7.2. Content validity

The analysis of content validity involves measuring all constructs included and represented in particular theories used in a study (Crocker & Algina, Citation1986; DeVellis, Citation1991; Gregory, Citation1992). Therefore, factor loadings are used to assess content validity through analysis of cross-loadings among the constructs as recommended by Hair et al. (Citation2010). Accordingly, as a rule of thumb, if any item loaded higher on other constructs than their loading, it will be deleted.

3.7.3. Convergent validity

According to Sekaran (Citation2000), convergent validity examines whether the measures of the items correlate highly with each other. Convergent validity ensures that the items effectively reflect their corresponding factor (Zhou, Citation2013). Thus, it indicates the degree to which a factor positively correlates with another factor of the same construct (Hair et al., Citation2014). The rule of thumb is that convergent validity can be examined through loadings, composite reliability, and average variance extracted (AVE) generated by PLS output. The items must be highly loaded and statistically significant in order to measure their respective constructs. The items’ loadings should be at least 0.5 and above, while the Average Variance Extracted (AVE) should not be below 0.5 and the composite reliability (CR) should be above 0.7 (Hair et al., Citation2014). Consequently, any item or indicator that is loaded below 0.5 will be deleted and only fewer items that loads highly are retained in order to achieve the desired AVE and CR as recommended by Hayduk and Littvay (Citation2012). Therefore, retaining fewer best items can help to build sound theoretical model that aid in deriving recommendations for policy.

3.7.4. Discriminant validity

The discriminant validity measures how items correlate or fail to correlate highly with each other under the constructs used to measure the same variable (Sekaran, Citation2000). The discriminant validity shows the degree to which a construct is actually different from another that is assumed to measure the same variable based on sound theoretical and empirical underpinnings (Hair et al., Citation2010). The discriminant validity is achieved only if all the diagonal values (square roots of AVE) are higher than the off diagonal values located in the same rows and columns based on the criterion set by Fornell and Larcker (Citation1981).

3.7.5. Constructing structural equation model

The structural equation model (SEM) shows the interrelationships among the latent constructs and observable variables in a proposed model as a succession of structural equations derived from a sound theoretical foundation (Hair et al., Citation2010). The direct effect indicates the effect of independent variable (exogenous) on a dependent variable (endogenous), whereas an indirect effect represents the effect of the independent (exogenous) variable on dependent (endogenous) variable through a mediating variable (Baron & Kenny, Citation1986), which is termed as the mediating effect. In addition, Hair et al. (Citation2016) also recommend that the key criteria of significance of the path coefficients, the level of R2 values, the f2 effect size, the predictive relevance Q2, and the q2 effect size should be considered in assessing the structural model in PLS-SEM. Overall, the structural equation model can be derived as below:

Where:

fin = financial inclusion (dependent variable)

β1finlit = beta coefficient of financial literacy (independent variable)

β2fintermed = beta coefficient of financial intermediation (mediator variable)

β3med = beta coefficient of mediation effect

c = constant

4. Statistical analysis results

4.1. Sample characteristics

The results from this study revealed that most (64 percent) of the poor households were headed by male while 36 percent by female households’ heads. Besides, the results indicated that most (37 percent) of the respondents were in the 26-33 age bracket and only 5 percent in the 50+ age bracket. Further analysis of the results also indicated that 57 percent of the households had 6-10 members while 14 percent had more than 10 members. Similarly, the results showed that 47 percent of the households used paraffin lantern as source of lighting and 0.8 percent used firewood for lighting. Additionally, the results showed that 60 percent of the households’ heads were able to read and write while 40 percent were not able to read and write. This is indicated in Table .

Table 1. Sample characteristics

4.2. Constructing the measurement models

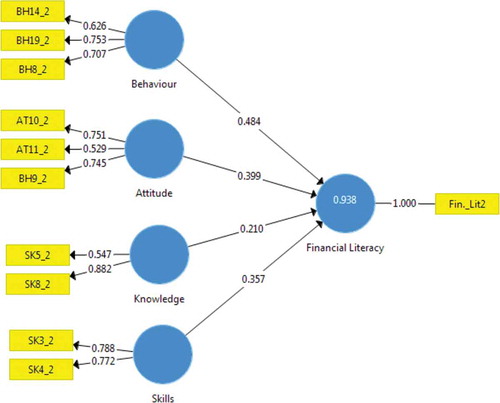

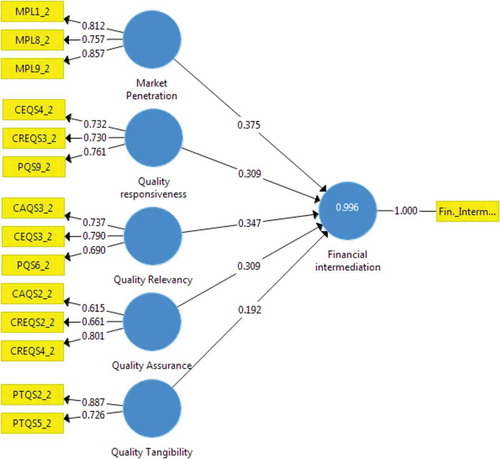

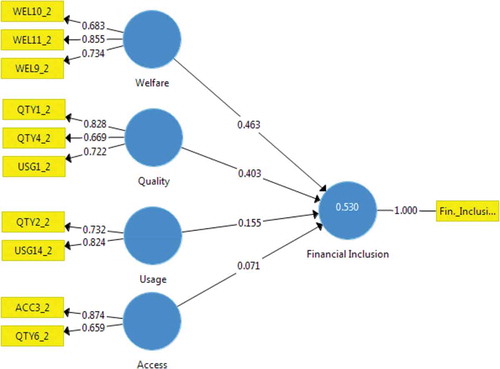

The measurement models for financial literacy, financial intermediation by microfinance banks, and financial inclusion were constructed to test for validity and reliability of the manifest as indicated in Figure , and . The results indicated that the items’ loadings, AVE, and composite reliability were above the recommended cut-off points as stipulated by Bagozzi and Yi (Citation1988). Besides, the Cronbach’s (α) for all the variables were above 0.7 as suggested by Nunnally (Citation1978). In addition, the results from the discriminant validity were also good and tenable. The results for the items’ loadings, AVE, composite reliability, Cronbach’s (α), and discriminant validity are indicated in Tables , , and .

Table 2. Factor loadings and cross loadings for the variables

Table 3. Factor loadings significant for the variables

Table 4. Convergent validity analysis

Table 5. Discriminant validity analysis

Figure 1. Measurement model for financial literacy.

Figure 2. Measurement model for financial intermediation.

Figure 3. Measurement model for financial inclusion.

4.3. Constructing structural equation model

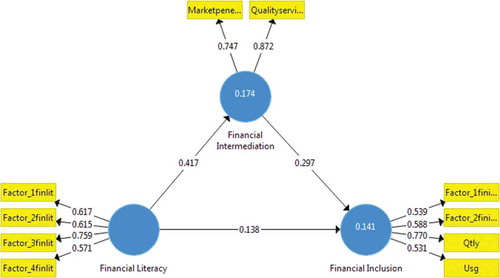

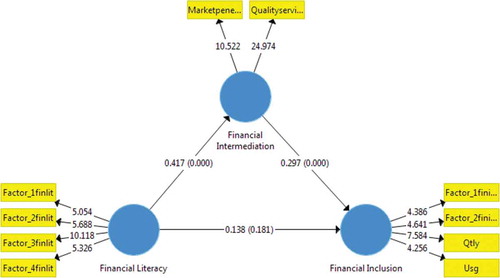

A structural model (SEM) combining all the variables (independent, mediator and dependent) under this study was constructed as indicated in Figures and . The results from the PLS-SEM bootstrap analysis revealed that all the hypotheses derived in this study were achieved and tenable as shown in Table .

Figure 4. PLS SEM algorithms with both direct and indirect effects.

Figure 5. PLS SEM algorithms with t-vales and p-values.

Referring to hypothesis (H1) of this study, a test for mediation effect involving 5000 sub-samples through bootstrap was requested in PLS sub-menu and outputs generated by carrying out the calculation. The results indicated that financial intermediation by microfinance banks plays significant roles in promoting financial literacy and financial inclusion of the poor (β = 0.124; t = 2.863; p > 0.005). This is indicated in the model below.

Similarly, the results from this study showed that financial intermediation by microfinance banks plays significant roles in promoting financial inclusion of the poor (β = 0.297; t = 3.713; p < 0.001) as indicated in Figure . This confirms hypothesis (H2) of this study. This is indicated in the model below.

Furthermore, the results also revealed that financial literacy significantly affects the financial inclusion of the poor (β = 0.138; t = 3.468; p < 0.001) as indicated in Figure . This lends support to hypothesis (H3) of this study. This is indicated in the model below.

4.4. Predictive relevancy (Q2) of the model

While predicting the relevance of the model under this study, the R2 and cross validated redundancy were used to examine the predictive relevance of the model. The coefficient of determination measures the model’s predictive power and is calculated as the squared correlation between a specific endogenous construct’s actual and predicted values. The coefficient represents the exogenous latent variables’ combined effects on the endogenous latent variable (Rigdon, Citation2012; Sarstedt, Ringle, Henseler & Hair, Citation2014).

Hence, it logically follows that if a variable significantly predicts an outcome, then it should have a b-value significantly different from zero. This is tested using a t-test. The t-statistic tests the null hypothesis that the value of b is zero. Therefore, if it is significant, we accept the hypothesis that the b-value is significantly different from zero and the predictor variable contributes significantly to the ability to estimate values of the outcome (Field and Hole, Citation2003; Field, Citation2005). Consequently, R2 was used to explain by how much the predictor variables explained the predicted value of the outcome in this study. The results indicated that 14 percent of the variation in financial inclusion is explained by financial literacy and financial intermediation by microfinance banks. This is in line with Falk and Miller (Citation1992) who argue that R2 of 0.10 and above is acceptable.

Besides, cross-validated redundancy was used to examine the quality of the model in this study. This was done through the blinding folding technique in PLS as recommended by Chin (Citation1998). The rule of thumb is that some data values should be removed, which would be estimated as missing values. The omission distance for the blind folding running is seven and after which certain values would be generated and a comparison made in order to test how close the real result is from the assumed results. The rule for the predictive relevance is that the value must be above zero as it is applicable in this study. Thus, the results from this study revealed cross-validated redundancies of 0.102 and 0.130 for financial inclusion and financial intermediation by microfinance banks, respectively. This confirms the adequacy of the predictive relevance of the model as indicated in Table . This supports the argument that a model with Q-value larger than zero has a predictive relevance as recommended by Hair et al. (Citation2016).

4.5. Effect size (f2) of the model

The effect size (f2) is computed by excluding an exogenous variable from the model and including the exogenous construct in the model to compare the change in R2 to determine the effect size. Accordingly, Cohen (Citation1988) stipulates that f2 values of 0.02, 0.15, and 0.35 indicate small, medium, and large effects of the exogenous latent variable, respectively (see also Hair et al., Citation2014). The results in Table showed that all the variables have small and medium effect sizes indicating the contribution of each to the overall predictive model.

Table 6. Results of hypotheses testing

Table 7. Blind folding and predictive relevance of the model for mediation

Table 8. Effect size of exogenous variables on endogenous variable of financial inclusion

5. Discussion of results

The main purpose of this study is to establish the mediating role of financial intermediaries in the relationship between financial literacy and financial inclusion of the poor in developing countries with data from rural Uganda.

The results from this study indicated that financial intermediation by microfinance banks plays significant roles in promoting financial literacy and financial inclusion of its rural-based clients. This finding is consistent with the argument that banks can provide financial literacy that improves financial knowledge with improved financial behavior through “teachable moments”, which can result into the availability of financial tools or direct and easy access to financial products. Indeed, according to Askari Bank (Citation2018), financial institutions like banks are uniquely positioned to provide financial literacy as they can bridge theoretical economic concepts such as scarcity and opportunity cost, with practical “money-in-the pocket” services. Therefore, connecting financial education with financial products allow all individuals to become fully integrated in the traditional financial system, setting them on the path to wealth accumulation. The financial literacy programs provided by banks with specialized products designed helps those outside the mainstream financial channels like the poor to transition into the traditional banking system with ease, clarity, and little cost. This findings correspond to advice offered by the Reserve Bank of India (RBI) to banks to set up Financial Literacy Centres (FLC) to conduct out-door financial literacy in all the districts, which resulted in increased financial literacy in India. This confirms our hypothesis (H1) of the study.

Besides, the results from this study revealed that financial intermediation by microfinance banks plays significant roles in promoting financial inclusion of its rural-based clients. This confirms hypothesis (H2) of the study. Levine, Loayza and Beck (2000) argue that financial institutions such as banks play a vital role in the society because they create efficiencies geared towards economic growth. Therefore, by engaging in maturity intermediation, financial institutions offer liquidity to savers and at the same time, longer-term funds to investors (King and Levine, 1993). Financial intermediaries create avenues, which ensure that the individuals and entities that have excess funds are able to invest and earn a return. Indeed, financial intermediaries provide the necessary link between the lenders and borrowers in the financial market. Scholars like Chandan and Mishra (Citation2010); Ergungor (Citation2010) contend that financial intermediaries such as banks carry out financial intermediation by allocating surplus resources from savers to borrowers who lack funds for investment.

Furthermore, the results from this study also showed that financial literacy significantly affects the financial inclusion of rural-based clients. This lends support to hypothesis (H3) of the study. Consistent with this result, the OECD (2009) argues that since financial literacy is linked to borrowing, saving, and spending patterns among diverse sections of consumers of financial products, it is important for economic growth and financial stability. Financial literacy is vital for individuals who lack financial knowledge and skills that can facilitate them to make sound and wise financial decisions and choices. Consequently, financial literacy helps individuals such as the poor to acquire knowledge, understanding of financial concepts and risks, skills, motivation and confidence to apply such knowledge and understanding in order to make effective decisions across a range of financial products and services. This finding corresponds to Van Rooij et al. (Citation2011) who found that financially sophisticated households were more likely to participate in the stock market.

6. Conclusion of results

The results from this study showed that financial intermediation by microfinance banks plays significant roles in promoting financial literacy and financial inclusion of its rural-based clients. Indeed, existing financial literacy programs and drives can be channelled through existing financial intermediaries’ infrastructures such as bank offices, branches, and points of service to educate the consumers of complex financial products and services, how to make wise financial decisions and choices, and managing their money and finances in the advent of scarce financial resources and shocks.

More so, the results from this study also revealed that financial intermediation by microfinance banks plays significant roles in promoting financial inclusion of its rural-based clients. Financial intermediaries such as microfinance banks, finance house, and other similar licensed financial institutions connect savers and borrowers, and harness fund from savers and give to borrowers who use it for investments. This promotes access to and usage of loans among the unbanked individuals, especially in rural communities.

Finally, the results from this study indicated that financial literacy significantly affects financial inclusion of rural-based clients. Financial literacy is important for the poor who face difficulty in making financial decisions that can have important consequences in their lives. Thus, financial literacy enables individuals, especially the poor to make wise financial decisions and choices before consuming complex and sophisticated financial products offered by financial intermediaries like banks.

7. Practical implications

The policy makers and advocates of financial literacy, especially in developing countries should use financial intermediaries such as microfinance banks to roll out financial literacy programs. This can be achieved through provision of financial literacy clinics, workshops, and seminars where the poor can learn about personal finance using a hands-on approach. This will help them to make wise financial decisions and choices towards consumption of complex financial products offered by the rural-based financial institutions.

Similarly, financial intermediaries in developing countries should be involved in designing the national financial literacy curriculum and guide. This is because they are more informed about the existing financial literacy gaps and deficiency among the poor who resides in rural areas. Indeed, this can be achieved through allowing financial intermediaries to develop modules that directly fit within the existing financial literacy gaps among the poor. Therefore, a consortium should be formed between the financial literacy working groups and microfinance banks to teach their rural-based clients better money management and financial discipline in order to promote financial inclusion.

Besides, microfinance banks should be engaged in disseminating and coordinating financial consumer protection and financial literacy campaigns, they can use their rural-based branches to conduct workshops and trainings on both financial literacy and consumer protection modules. The microfinance banks can act as a distribution point for leaflets, brochures, and handouts containing vital financial literacy information. This will help the rural-based clients such as the poor to gain awareness before consuming existing financial products available on the market.

Finally, the financial literacy working groups should use existing microfinance banks’ structures as Financial Literacy Centres to promote national financial literacy drives. Indeed, microfinance banks’ branches can serve as financial literacy learning centres through which outdoor financial literacy camps can be conducted. This will help in delivering financial literacy to rural-based clients such as the poor.

8. Limitations and areas for future studies

The results for this study were derived from data collected through cross-sectional research design. Thus, future studies may adopt the use of longitudinal data to establish the mediating role of financial intermediaries in the relationship between financial literacy and financial inclusion of the poor. In addition, the samples used in this study were obtained from only the poor living in rural Uganda. Therefore, further studies could collect data from other vulnerable groups such as women, youth and the disabled persons who have been financially excluded.

Additional information

Funding

Notes on contributors

George Okello Candiya Bongomin

George Okello Candiya Bongomin holds a PhD, MSc (Accounting and Finance) and Bachelor’s degree in Commerce from Makerere University Kampala, Uganda. He is a Research Fellow at Faculty of Graduate Studies and Research, Makerere University Business School, Kampala, Uganda and an international financial inclusion scholar. His research interests are in financial inclusion. George Okello Candiya Bongomin is the corresponding author and can be contacted at: [email protected]

John C. Munene

John C. Munene, PhD., is a professor of psychology and Coordinator PhD Programmes, Faculty of Graduate Studies and Research, Makerere University Business School, Kampala, Uganda. His research interests are in industrial and organizational psychology.

Pierre Yourougou

Pierre Yourougou PhD., is a professor of finance and banking. He is Deputy Director General of the National Polytechnic Institute Félix Houphouet-Boigny, Côte d’Ivoire in charge of International Cooperation and Development of the Yamoussoukro Technopole. His research interests are in financial inclusion, development finance, banking and finance, and international cooperation.

References

- ACCION. (2011). Center for Financial Inclusion, Financial Inclusion: What’s the Vision? What would it take for Mexico to achieve full inclusion by the year 2020.

- Akerlof, G. A. (1970). The market for “Lemons”: Quality uncertainty and the market mechanism. The Quarterly Journal of Economics, 84(3), 488–21. https://doi.org/10.2307/1879431

- Allen, F., & Santomero, A. M. (1996). The theory of financial intermediation, 96–132. https://ssrn.com/abstract=7716

- Allen, F., Carletti, E., Cull, R., Qian, Q.J., Senbet, L., & Valenzuela, P. (2011). Improving access to banking: evidence from kenya. World Bank Policy Research Working Paper Series 6593. Washington, DC: The World Bank Publication.

- Allen, F., Demirgüç-Kunt, A., Klapper, L., & Peria, M. S. M. (2016). The foundations of financial inclusion: Understanding ownership and use of formal accounts. Journal of Financial Intermediation, 27(1), 1–30. https://doi.org/10.1016/j.jfi.2015.12.003

- Alliance for Financial Inclusion-AFI. (2010). “The afi survey on financial inclusion policy in developing countries: preliminary findings”. AFI Policy Brief, Bangkok.

- American Bankers Association. (2018). The American Bankers Association (ABA). Washington, D.C. Retrieved from https://www.aba.com/Engagement/Pages/financialed.aspx

- Ardic, O. P., Heimann, M., & Mylenko, N. (2011, January). Access to financial services and the financial inclusion Agenda around the World (A Cross-Country Analysis with a New Data Set), WPS5537. The World Bank Financial and Private Sector Development Consultative Group to Assist the Poor.

- Askari Bank. (2018). Annual Report 2018: The Supervision Department, Askari Bank, Islamabad, Pakistan.

- Atkinson, A., & Messy, F. (2012). Measuring financial literacy: results of the OECD/International Network on Financial Education (INFE) pilot study. Oecd working papers on finance, insurance and private pensions No. 15, OECD. doi:http://dx.doi.org/10.1787/5k9csfs90fr4-en.

- Atkinson, A., & Messy, F. (2013). Promoting financial inclusion through financial education: OECD/INFE evidence, policies and practice (OECD Working Papers on Finance, Insurance and Private Pensions No. 34). OECD Publishing. https://doi.org/10.1787/5k3xz6m88smp-en.

- Bagozzi, R., & Yi, Y. (1988). On the evaluation of structural equation models. Journal of the Academy of Marketing Science, 16(1), 74–94. https://doi.org/10.1007/BF02723327

- Bank of Uganda. (2017). Annual supervision report (2015-2016) (Bank of Uganda).

- Bank, W. (2014). A survey on access to and use of financial services in 152 countries around the world (The 2014 Global Financial (Global Findex) Database). The World Bank.

- Bank, World. (2018). Financial Inclusion: Financial Inclusion is a Key Enabler to Reducing Poverty and Boosting Prosperity. The World Bank Brief. The World Bank, Washington DC.

- Baron, R. M., & Kenny, D. A. (1986). The moderator-mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6), 1173–1182. https://doi.org/10.1037/0022-3514.51.6.1173

- Beck, T., & De La Torre, A. (2006). The basic analytics of access to financial services. Financial Markets, Institutions and Instruments, 16(2), 79–117. https://doi.org/10.1111/j.1468-0416.2007.00120.x

- Carpena, F., Cole, S., Shapiro, J., & Zia, B. (2011). Unpacking the causal chain of financial literacy. Policy Research Working Paper No. 5798/e, World Bank Development Research Group. Washington, DC: The World Bank.

- Chandan, K., & Mishra, S. (2010). Banking outreach and household level access: analyzing financial inclusion in India. [Unpublished M.Phil Thesis]. Mumbai: Indira Gandhi Institute of Development Research (IGIDR).

- Čihák, M., Demirgüç-Kunt, A., Erik, F., & Levine, R. (2012). Benchmarking financial systems around the world (The World Bank Policy Research Working Paper 6175). Washington, DC: The World Bank Publication.

- Chin, W. W. (1998). The partial least squares approach to structural equation modeling. In (Ed.), Modern methods for business research (295–358). Mahwah: Erlbaum.

- Claessens, S. (2006). Access to financial services: A review of the issues and public policy objectives. The World Bank Research Observer, 21(2), 207–240. https://doi.org/10.1093/wbro/lkl004

- Clark, R., Lusardi, A., & Mitchell, O.S. (2016). Employee financial literacy and retirement plan behavior: A case study. Forthcoming Economic Inquiry, 55(1),248-259. doi:10.1111/ecin.12389. Retrieved from https://gflec.org/wp-content/uploads/2016/06/Employee-Financial-Literacy-and-Retirement-Plan-Behavior-EI.pdf?x37611

- Cohen, J. (1988). Statistical power analysis for the behavioral sciences (2nd ed.). Lawrence Erlbaum.

- Cohen, M. (2010). Financial literacy (Innovations in Rural and Agricultural Finance, 2020 Vision for Food, Agriculture and the Environment, Focus Note 18). IFPRI and the World Bank.

- Cole, S., Sampson, T., & Zia, B. (2010). Price or knowledge? What drives demand for financial services in emerging markets? The Journal of Finance, 66(6), 1933–1967.

- Cole, S., Sampson, T., & Zia, B. (2011). Price or knowledge? What drives demand for financial services in emerging markets? Journal of Finance, 66(6), 1933–1967. https://doi.org/10.1111/j.1540-6261.2011.01696.x

- Crocker, L., & Algina, J. (1986). Introduction to classical and modern test theory. Harcourt Brace Jovanovich College Publishers.

- Cull, R., Demirgüç-Kunt, A., & Morduch, J. (2016). The microfinance business model: enduring subsidy and modest profit. Policy Research Working Paper No. 7786. Washington, DC: The World Bank Publishing, World Bank.

- de Aghion, Armendariz., & Morduch, J. (2005). The Economics of Microfinance. Cambridge, MA: The MIT Press.

- De Vellis, R. F. (2003). Scale development: Theory and applications (2nd ed.). Sage.

- Demirguc-Kunt, A., Klapper, L., & Singer, D. (2017). Financial Inclusion and Inclusive Growth – A Review of Recent Empirical Evidence, World Bank Policy Research Paper, No. 8040. Washington, DC: The World Bank Publication.

- Demirgüç-Kunt, A., Klapper, L., Singer, D., Ansar, S. & Hess, J. (2018). The Global Findex Database 2017: Measuring financial inclusion and the fintech revolution. Washington, DC: The World Bank.

- DeVellis, R. F. (1991). Scale development: theory and applications. Applied social research methods series, 26. Newbury Park, CA: Sage Publications.

- Dugyala, R. (2018, August 16). U.S. banks teach financial literacy with hands-on experience. Reuters. https://www.reuters.com/article/usmoney-banking-literacy/u-s-banks-teach-financial-literacy-with-hands-onexperience- idUSKBN1L111J

- Dutta, S., & Dutta, P. (2011). The effect of literacy and bank penetration on financial inclusion in India: A statistical analysis. Napaam: Tezpur University.

- Ergungor, E. O. (2010). Bank branch presence and access to credit in low to moderate income neighborhood. Journal of Money, Credit and Banking, 42 (7), 1321–1349. Blackwell Publishing. https://doi.org/10.1111/j.1538-4616.2010.00343.x.

- Falk, R. F., & Miller, N. B. (1992). A primer for soft modeling. Akron, Ohio: University of Akron Press.

- Field, A. P. (2005). Discovering statistics using SPSS. Sage.

- Field, A. P., & Hole, G. (2003). How to Design and Report Experiment. London: Sage Publishing.

- FinScope. (2018). Topline findings report. Financial Sector Deepening Uganda (FSDU) and UKaid, Uganda Kampala.

- Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50. https://doi.org/10.1177/002224378101800104

- Gregory, R. J. (1992). Psychological testing: History, principles and applications. Boston.

- Grohmann, A., Klühs, T., & Menkhoff, L. (2017). Does financial literacy improve financial inclusion? Cross country evidence. German Research Foundation. http://economics.handels.gu.se/digitalAssets/1643/1643705_71.-kl–hsgrohmannkl–hsmenkhoff_150217—kopia.pdf

- Gurley, J., & Shaw, E. (1960). Money in a theory of finance. Brookings Institution, 1960.

- Hair, J. F., Anderson, R. E., Tatham, R. L., & Black, W. C. (2010). Multivariate data analysis (5th ed.). Prentice Hall.

- Hair, J. F., Jr, Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2014). A primer on partial least squares structural equation modeling (PLS-SEM). Sage.

- Hair, J. F., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2016). A primer on partial. Least squares structural equation modeling (PLS-SEM) (2nd ed.). Sage.

- Hayduk, L. A., & Littvay, L. (2012). Should researchers use single indicators, best indicators, or multiple indicators in structural equation models? BMC Medical Research Methodology, 12(1), 1–17. https://doi.org/10.1186/1471-2288-12-159

- Holzmann, R. (2010). Bringing financial literacy and education to low and middle income countries: The need to review, adjust, and extend current wisdom, World Bank, IZA and CES. Retrieved June, 2012, from. http://erepository.uonbi.ac.ke:8080/xmlui/handle/123456789/9897

- Jamison, J. C., Karlan, D., & Zinman, J. (2014). Financial education and access to savings accounts: Complements or substitutes? Evidence from Ugandan youth clubs (NBER Working Paper No. w20135). Cambridge, MA: National Bureau of Economic Research.

- Johns, R. (2010). Likert items and scales. Survey Question Bank http://www.surveynet.ac.uk/sqb/datacollection/likertfactsheet.pdf

- Johnson, S., & Nino-Zarazua, M. (2009). Financial access and exclusion in Kenya and Uganda. Working Paper No. 1, Bath papers in International Development, Centre for Development Studies, University of Bath, London, February

- Joshi, D. P. (2014). Strategy Adopted for Financial Inclusion. Speech during Workshop of Government of Madhya Pradesh, New Delhi, Government of India, January 2014.

- Karlan, D., McConnell, M., Mullainathan, S., & Zinman, J. (2016). Getting to the top of mind: how reminders increase saving. Management Science, 62(12), 3393–3411.

- Kempson, E. (2006). Policy level response to financial exclusion in developed economies: Lessons for developing countries. Paper presented at the conference for access to finance: Building inclusive financial systems. Washington, DC: The World Bank, The World Bank Conference Paper Series.

- Kempson, E. (2008). Financial education fund: monitoring and evaluation policy and procedures. Financial Education Inception Report, Mimeo, November.

- Kempson, E., Atkinson, A., & Pilley, O. (2004). Policy level response to financial exclusion in developed economies: Lessons for developing economies, the personal finance research centre prepared for the department of international development, University of Bristol. UK: The Department for International Development (DFID).

- Kendall, J., Mylenko, N., Ponce, A., & Bank, World Financial and Private Sector Development Financial Access Team, March 2010. The World Bank Publishing, Washington DC.

- King, R., & Levine, R. (1993). Finance and growth: schumpeter might be right. Quarterly Journal of Economics, 108(3), 717-737.

- Klapper, L., Lusardi, A., & van Oudheusden, P. (2015). Financial literacy around the world: insights from the standards and poor’s ratings service global financial literacy survey. https://www.finlit.mhfi.com

- Leland, H. E., & Pyle, D. H. (1977). Papers and proceedings of the thirty-fifth. Annual meeting of the American finance association, Atlantic City, New Jersey, September. 16-18, 1976. The Journal of Finance, 32(2), 371–387. https://doi.org/10.2307/2326770

- Levine, R., Loayza, N., & Beck, T. (2000). Financial intermediation and growth: causality and causes. Journal Monetary Economics, 46(1), 31-77.

- Likert, R. (1932). A technique for the measurement of attitudes. Archives of Psychology, 140 (1), 44‐53.

- Lusardi, A. (2003). Planning and saving for retirement. Working Paper. DartmouthCollege. http://www.dartmouth.edu/~alusardi/Papers/Lusardi_pdf.pdf

- Lusardi, A. (2015). Financial Literacy: Do People Know The Abcs of Finance? Public Understanding Science. 24(3), 260-71. doi:10.1177/0963662514564516

- Lusardi, A., Michaud, P. C., & Mitchell, O. S. (2017). Optimal financial knowledge and wealth inequality. Journal of Political Economy, 125(2), 431–477. https://doi.org/10.1086/690950

- Lusardi, A., & Mitchell, O. S. (2006). Financial literacy and planning: Implications for retirement wellbeing (Pension Research Council Working Paper 1). The Wharton School.

- Lusardi, A., & Mitchell, O. (2009). How ordinary consumers make complex economic decisions: Financial literacy and retirement readiness. [NBER Working Paper No. 15350]. Cambridge, MA: National Bureau of Economic Research, Inc.

- Lusardi, A., & Mitchell, O. S. (2014). The economic importance of financial literacy: Theory and evidence. Journal of Economic Literature, 52(1), 5–44. https://doi.org/10.1257/jel.52.1.5

- Lusardi, A., & Tufano, P. (2008). [Debt literacy, financial experience and over indebtedness (Working Paper). Brighton, Boston, MA: Harvard Business School.

- Matthews, K., & Thompson, J. (2008). The economics of banking (2nd ed). Chichester: John Wiley & Sons.

- Nissanke, M., & Stein, H. (2003). Financial globalization and economic development: toward an institutional foundation. Eastern Economic Review, 29(2), 287–308.

- Nunnally, J. C. (1978). Psychometric theory. McGraw-Hill.

- Oaks, T., & Devellis, R. F. (1991). Scale development: Theory and applications (Applied Social Research Methods Series 26). Sage.

- OECD. (2009). Financial literacy and consumer protection: overlooked aspects of the crisis. Paris, France: OECD Publishing. www.financial-education.org/dataoecd/32/3/43138294.pdf.

- OECD. (2017). Measuring Financial Literacy. G20/OECD INFE report on adult financial literacy in G20 countries. Paris, France: OECD Publishing

- Okello, G. C. B., Munene, J. C., Ntayi, J. M., & Akol, C. M. (2017). Financial literacy in emerging economies: Do all components matter for financial inclusion of poor households in rural Uganda? Managerial Finance, 43(12), 1310–1331. https://doi.org/10.1108/MF-04-2017-0117

- Pallant, J. (2005). Spss survival manual: a step by step guide to data analysis using spss for windows version 12 (2nd ed.). Crows Nest: NSW: Allen & Unwin.

- Podsakoff, P. M., MacKenzie, S. B., Lee, J. Y., & Podsakoff, N. P. (2003). Common method biases in behavioral research: A critical review of the literature and recommended remedies. Journal of Applied Psychology, 88(5), 879–903. https://doi.org/10.1037/0021-9010.88.5.879

- Prina, S. (2015). Banking the poor via savings accounts: Evidence from a field experiment. Journal of Development Economics, 115(17), 16–31.

- Rau, N. (2004). Financial intermediation and access to finance in African Countries South of the Sahara. Forum Paper, 2004. African development and poverty reduction: the macro-micro linkages, 13–15 october. Paper Presented at Lord Charles Hotel, Somerset West, SA.

- Rigdon, E. E. (2012). Long Range Planning. 45(5–6), 341–358. doi:10.1016/j.lrp.2012.09.010

- Sarstedt, M., Ringle, C. M., Henseler, J., & Hair, J. F. (2014). On the emancipation of pls-sem: A commentary on rigdon (2012). Long Range Planning, 47(3), 154–160.

- Sekaran, U. (2000). Research methods for business: A skill building approach. John Wiley & Sins, Inc.

- Skimmyhorn, W. (2016). Assessing financial education: evidence from boot camp. American Economic Journal: Economic Policy, 8(2), 322–43.

- United Nations Development Program. (2006). Building inclusive financial sectors for development. Department of Economic and Social Affairs. Geneva: The United Nations Publishing.

- Uganda Bureau of Statistics - UBOS. (2012). Poverty Projections Statistical Abstract 2012: Uganda Bureau of Statistics. Government of Uganda.

- Van Rooij, M., Lusardi, A., & Alessie, R. (2011). Financial literacy and stock market participation. Journal of Financial Economics, 101(2), 449–472. https://doi.org/10.1016/j.jfineco.2011.03.006

- Yamane, T. (1973). Statistics: an introductory analysis (3rd ed.). New York, NY: Harper & Row.

- Yaron, J., Benjamin, M. P., & Piprek, G. L. (1997). Rural finance: Issue, design, and best practices (Environmentally and socially sustainable development studies and monograph series 14). The World Bank.

- Yunus, M. (2005). Banker to the Poor: Micro-lending and the Battle against World Poverty, Public Affairs, New York, NY.

- Zhou, T. (2013). Understanding continuance usage of mobile sites. Industrial Management & Data Systems, 113(9), 1286–1299.