?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study investigates the impact of trade openness along with bank size, bank growth, liquidity, deposit insurance, industry centralization, and capital stringency on risk-taking behavior of commercial banks of Bangladesh. To examine the relationships, it considers 32 commercial banks over a period of 2000 to 2017. The main result of this study reveals that trade openness provides ample opportunities in lending activities of commercial banks and aids decreasing credit risk as well as overall bank risk. Hence, it has great implications for the policymakers to promote trade openness and make banks more competitive.

PUBLIC INTEREST STATEMENT

This paper investigates the relationship between trade openness and bank credit risk-taking behavior in the context of a developing economy like Bangladesh. The main result shows a negative and significant effect of trade openness on bank risk-taking. It means trade openness provides ample spaces for banks doing their operations through lending activities and fostering banks reducing credit and overall risk sharply. The result supports the openness theory of financial development. Hence, it has great implications for the policymakers to promote trade openness in a large scale for making banks more competitive in developing economic countries.

1. Introduction

In the modern era, banks are the most powerful financial organizations in Bangladesh as well as all over the world. Banks provide essential funds that contribute to economic development. Banks are related to some risk, among which credit risk is one of them. Credit risk is the risk of default on a debt that may arise from a borrower failing to make required payments. On the other hand, trade openness refers to the inward or outward orientation of a given country’s economy. As Bangladesh is a developing country, more trade is gradually opening. Recently, 61 banks are operating in Bangladesh. The commercial Banks in Bangladesh play a vital in trade openness. All commercial banks in Bangladesh provide loan as a major amount of their capital to the traders. That is why commercial banks and the trading systems are directly related to Bangladesh. As Banks provide a loan as capital to the trade organizations, there avails the question of loan default or credit risk.

During the global financial crisis during 2007–2008, the concentration may provide to the real result that the banking system has on economy Agnello and Sousa (Citation2011). This crisis indicates the emergency of bank regulation to decrease the risk taken by the banks. The unsteady nature of banks and the propensity of taking more risk are reflected by the recent banking crisis. Lots of proposals that are formulated to provide strength to the liquidity and capital regulation for enhancing higher flexible banking industry approved by G-20.

In this paper, we investigate the relationship between trade openness and bank credit risk-taking behavior. The openness theory of financial development argues that the integration of a country in global goods and the capital market can promote its development (Rajan & Zingales, Citation2003).

Though a banking system plays a very significant role in the development of the economy, there is very few research on this topic. The valuation of a bank’s credit risk, as well as overall risk, is very necessary for the stakeholders who use their information such as government, borrower, shareholders, and various regulatory authorities. Shareholders are concerned about the systematic risk and overall risk. Borrowers are concerned about the financial condition of a bank and for this reason, they are interested in credit risk . In accordance with this theory in developing and underdeveloped countries, the established attribute industrial interest groups do not support financial development for the reason of its increasing competition by making it easy to enter the market. Trade openness limits the power capability of incumbents to oppose financial development. It also creates a stimulus for them to support and increase financial viability.

It is found that higher trade openness decreases bank credit risk-taking. Over the period of 1998 to 2012 in Bangladesh, trade openness provides diversification opportunities to banks in performing lending activities, which decreases the overall risk of banks. B. N. Ashraf et al. (Citation2016), Yanikkaya (Citation2003) have examined the arguments of openness theory empirically and largely support the higher trade and financial openness in developing countries is positively correlated with financial development. This is a macro-level analysis and shows how openness affects the bank’s risk-taking behavior. Excessive bank credit to the business sector beyond the optimal level increases the risk. Besides, Credit risk is also related to the GDP of a country. For example, Zheng et al. (Citation2017b), Zheng and Moudud-Ul-Huq (Citation2017) who have explained that the likelihood is that a financial crisis would occur in a country is higher where the private credit to GDP ratio is higher.

The higher trade openness provides diversification opportunities, lowers the price for consumers and leads to more efficient economic growth. This study is examined whether or not trade openness provides opportunities to the banks in the loan market. Openness theory of financial development argues that opening up a country to both international trade and financial flows can promote financial development. However, the major objective of the study is to examine whether trade openness decreases risk-taking behavior or not. Therefore, this study shades lights to the existing study by showing the relationship of bank size, bank growth, and credit risk; examining the liquidity impact on credit risk; and revisiting the impacts of industry-level facts (such as capital stringency, industry concentration, and deposit insurance) on risk-taking behavior of banks in Bangladesh.

The rest of the study proceeds as follows: section two presents the literature review and hypothesis, section three represents data and variables, four presents empirical results, and five represents conclusions and recommendations.

2. Literature review and hypothesis

This study examines how trade openness and other factors such as bank size, bank growth, liquidity, capital stringency, deposit insurance, and industry concentration affect bank risk-taking behavior of banks with trade openness. Bangladesh is not a fully developed country, it is a developing country, and the pattern of risk-taking behavior of this country may be different in many ways. Despite the above international studies, the bank risk-taking behavior, particularly on the basis of current trade openness situation particularly in Bangladesh, has not been studied and tested. This study is an endeavor to fill this significant gap by examining the trends of trade openness and banks' risk-taking behavior. In the context of Bangladesh, higher trade openness may increase the loan diversification opportunities between internationally trading firms and domestic firms.

2.1. (a) Trade openness and credit risk

According to Pigka-Balanika (Citation2013), trade openness is an engine for economic growth and it has a positive and statistically significant relationship between them. Openness and economic growth are not necessarily always positive. It brings a lot of benefits to many developing countries. The following studies, e.g., (B. Ashraf et al., Citation2017; Pigka-Balanika, Citation2013) examined that trade openness on bank risk-taking behavior has a strong negative impact. The higher trade openness provides international diversification opportunities to banks and decreases the impact of the domestic financial crisis on bank risk (B. Ashraf et al., Citation2017). Trade openness is a statistically important determinant of the variation in financial development across countries as well as economic institutions (Baltagi et al., Citation2009; Lalon, Citation2015). The objective of credit management is to maximize the outcomes of performing asset and minimize the performance of the nonperforming asset as well as ensure the optimal point of loan and advances along with their efficient management. A number of studies examined the arguments of openness theory (Baltagi et al., Citation2009, Citation2013) and largely supported this theory from the context of developing countries. The excessive bank risks to the private sectors beyond the optimal level accompanied by lower credit standards accumulate and higher the risk of financial sectors. Similarly, a large number of studies found that the likelihood of a financial crisis occurred in a country is higher when the private credit to GDP ratio is larger (Borio & Drehmann, Citation2009). As a result, the lending guidelines should include industry and business segment focus, types of loan facilities, single borrower and group limit, lending caps. It should adopt a credit grading system. All facilities should be assigned a risk grade. Trade openness, which may have either a positive or negative impact on bank risk-taking behavior. Firstly, we can assume that trade oneness may have a negative impact on risk-taking because it provides loan diversification opportunities. This study builds on the stand of literature examining bank risk-taking based on the trade openness perspective of commercial banks of Bangladesh. In addition, the extant literature has focused on the structure of the banking industry (Boyd & De Nicolo, Citation2005; Goetz, Citation2010). Banking regulation (B. N. Ashraf et al., Citation2016). A number of recent macro-level studies found that internationally integrated industries lead to international diversification which is less exposed to domestic economic condition. As a result, trading borrowers become fewer defaulters of bank loan which help to decrease credit risk. We will examine other elements and their impact on credit risk from the context of commercial banks in Bangladesh.

2.2. (b) Bank size and credit risk

Bank size is considered as one of the most significant elements in the risk-taking behavior of banks. Large size banks can generate different activities. As a consequence, they can diversify their portfolio which led to a decrease in their risk (Roy, Citation2008). A significant positive relationship found about this phenomenon by Jacques and Nigro (Citation1997), Zheng et al. (Citation2017b), Zheng and Moudud-Ul-Huq (Citation2017), S. Moudud-Ul-Huq (Citation2018), and S. Moudud-Ul-Huq (Citation2019b), among others. On the other hand, a negative relationship with bank size and the risk was found by Aggarwal and Jacques (Citation1998). That means banks with large size take fewer risks than bank with small size. Many studies found that banks of large size are better in evaluating hard information loan applicants and small banks are good at evaluating soft information loan applicants. Petersen and Rajan (Citation2002) found that a large number of studies proved that bank with smaller size lends more loans to local firms than that of larger banks. Rahman et al. (Citation2015), S. Moudud-Ul-Huq et al. (Citation2018c), and S. Moudud-Ul-Huq et al. (Citation2018a) have been significantly assumed that bank equity varies to size and considered them as a measure of banks overall risk. According to Stever (Citation2007), the resources and assets held by small banks individually have less credit risk than large banks. The rates of loan charge of and default are higher in large banks. Banks which have small size prefer to make safe loans than large banks. (Berk, Citation1995) concludes that indicators impose a discount on firms with high systematic risk. This study will determine the impact of bank size on credit risk positively or negatively.

2.3. (C) Bank growth and credit risk

Bank growth is a bank-level variable which is an important determinant of bank risk. Zheng and Moudud-Ul-Huq (Citation2017), Zheng et al. (Citation2017b) suggest that banks with higher growth rate are riskier. Banks that have a higher growth rate than competitors attract more bank customers by providing low loan rates. In contrast, Köhler (Citation2015) shows that banks with a larger fraction of income from not interest activities become more stable and steadier. This effect depends upon the size of a bank. Banks with larger growth are more likely to engage in more likely balance sheet activities and they are more likely in violating trading activities. This study examines the impact of bank growth on the credit risk of the bank.

2.4. (d) Liquidity and credit risk

A large level of liquidity ratio implies that there is a risk for not having enough cash held by the banks to face the demand of the deposit withdrawals. Liquidity refers to how easily a bank’s assets can be converted into cash at a lower cost. Banks with higher liquidity ratio are less likely to face risk arises in operations. Cai and Thakor (Citation2008) examined the interact competition on liquidity risk and on the interaction between liquidity and credit risk and found out the condition under which large interbank competition increase loan liquidity and decrease a bank’s overall risk which includes both liquidity and credit risk. Zheng et al. (Citation2017a), Gupta and Moudud-Ul-Huq (Citation2020) suggest that the relationship which is determined between competition and bank risk-taking is not strong enough to variations in assumption and may not even true (Cai & Thakor, Citation2008). Boyd and De Nicolo (Citation2005) found that risk-taking refers to discover the credit or default risk. It is clearly important to understand how liquidity affects credit risk. Many interesting questions arise from this study: (1) how liquidity and credit risk of a bank interrelated? (2) what kind of relationships exists between liquidity and credit risk?

2.5. (f) Capital Stringency and credit risk

Agoraki et al. (Citation2011) suggested that banks that have market power tend to take lower credit risk and have the lower possibility of default loans. Components of capital stringency are BASEL risk-weight, credit risk-weight, market risk-weight, etc. According to Agoraki et al. (Citation2011), restriction on activities, capital requirement, and supervisory power have significant influence as shaping risk behavior of individual bank. But banks behave differently under various institutional settings. The regulatory effects which are adopted by transition banking systems are different from developing banking systems. Capital Stringency may affect competition and risk-taking in various ways (Berger & Udell, Citation2002; Haselmann & Wachtel, Citation2007). The entry of newcomers can be restricted by capital stringency. Few banks will be able to meet the costs that are fixed by regulation. According to Bolt and Tieman (Citation2004), more stringent capital recruitment compels and a bank to set more strict acceptance procedure to grant new loans. Whether few researchers suggested that capital or asset restriction could be useful in decreasing risk within a competitive environment (Matutes & Vives, Citation2000; Repullo, Citation2004).

2.6. (g) Industry concentration and credit risk

Industry concentration is a structural characteristic of the business sector which is considered as a degree of production in an industry is dominated by a few large firms. Cornelli et al. (Citation2006) suggested that industry expertise is significant for banks and analyze banks' stimulus to achieve expertise in evaluating the creditworthiness of borrowers in the industry. He also indicated that the models of credit risk should consider banks' industry expertise as an indicator of the relation between credit risk and factory. From a recent survey of banks' internal credit rating assignment process, the Basel committee found that formal industry analysis plays an important role in evaluating ratings to banks’ borrowers, such analysis is given by internal economic analysis units with the aim of providing a general view of an industrial outlook of the relevant borrowers.

2.7. (h) Deposit Insurance and credit risk

Deposit insurance is a measure which is implemented in many countries to protect the bank deposit arising from losses caused by the failure of a bank to pay its debt when due. The consequence of deposit insurance decreases the incentive of bank customers which lead to a larger amount of risk (Anginer et al., Citation2013). It was concluded that during the period of bank financial crisis, bank risk is lower and systemic stability is higher in countries which implemented deposit insurance. Merton (Citation1977) found the relationship between deposit insurance and banking stability. Deposit insurance is the interest of sincere depositors to save them from the financial crisis of banks that can also enhance social development. Similar to this view, Gropp and Vesala (Citation2004) indicated that the adoption of deposit insurance is related to fewer bank risks in the European Countries. Chernykh and Cole (Citation2011) also found that the implementation of deposit insurance in Russia and results in better financial intermediation. Deposit insurance promotes moral hazard problems in banking sectors by providing incentives to banks to take the exclusive risk (Anginer et al., Citation2013). Insufficient market discipline leads to exclusive risk-taking and results in banking crisis (Barth et al., Citation2004; Demirgüç-Kunt & Kane, Citation2002).

However, the relationship between deposit insurance, bank risk-taking, and systemic stability is opposite in the crisis period of 2007–2009. There is a widespread agreement that deposit insurance affects bank risk in stabilization and moral hazard ways. This study tests the relationship between deposit insurance and bank credit risk.

This study also examines other elements and their impact on credit risk from the context of developing countries like Bangladesh.

3. Econometric model

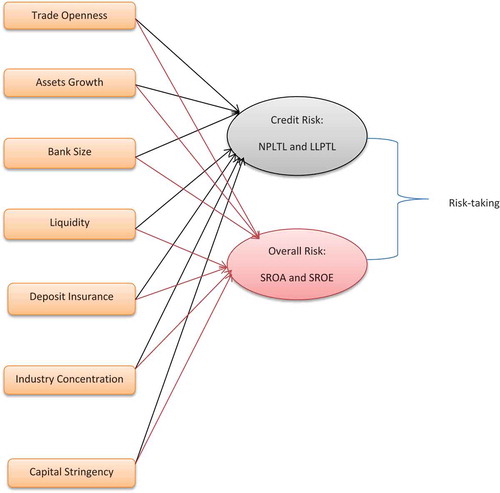

To examine the impact of trade openness on bank risk, we develop the following model (also see Figure ):

where, in separate regressions, the dependent variable Yi,t represents: the ratio of nonperforming loan to total loan (NPLTL) is the main measure of performance, and additionally, we use three alternative measures for risk of which the ratio of loan loss provision to total loan (LLPTL) is the alternative proxy for NPLTL. Another two measures for overall risk have been used such as the standard deviation of return on assets (SROA), and the standard deviation of return on equity (SROE) for bank in year

, where, in equation, subscripts i refers the number of banks (i.e., i = 1,2,3, … 32 banks of Bangladesh); j and k cover the number of bank-level and industry-level control variables, respectively, and t indicates period (i.e., t = 2000, 2001, 2002, … 2017), β is the series of parameters to be estimated and

is the error term.

The variable denotes the bank-specific control variables such as assets growth (AG), bank size (SIZE), and liquidity (LIQUIDITY). On the one hand, the

represents the industry-level variables, i.e., deposit insurance (DI), industry concentration (IC), and capital stringency (CS).

3.1. (a). Conceptual Framework

Figure 1. The impacts of trade openness and other control variables on bank risk-taking.

4. Data and variables

4.1. Data

This study uses bank-level, macroeconomic, and industry-level control variables. As a source of bank-level data, bank-focus database and financial database of annual reports are chosen. The monetary units are in US dollar and in constant prices where appropriate. After excluding missing and inconsistent data, finally, we have 32 commercial banks including government banks, private banks, Islamic and conventional banks of Bangladesh over the period of 2000 to 2017 and allowed 530 bank-year observations. For macroeconomic data, we relied on the World Development Indicator database and we gathered industry-level data from Bangladesh bank and Dhaka Stock Exchange (DSE).

4.2. Variables

4.2.1. Dependent variables

Our main risk variable is NPLTL. We also use three alternative measures for risk (please see section 3 and Table ), they are LLPTL, SROA, SROE. NPLTL is the credit risk indicator which represents the ratio of non-performing loans to total loans. Another credit risk indicator is LLPTL which is the ratio of loan loss provisions to the total loss.

SROA is the standard deviation of the annual values of return on an asset before loan loss provision and taxes, and measure the volatility of the bank’s total operating income (σ(ROA = Net Income After Tax/Total Assets). SROA also represents the overall operating risk of a bank. SROE is the standard deviation of return on equity (σ(ROE = Net Income After Tax/Total Shareholders’ Equities). Above all, alternative measures of risk have been used to check and validate the main result.

4.2.2. Main variable

Trade openness is the main independent variable. Trade openness is equal to (Export + Import)/GDP. Here, Exports Imports and GDP are measured in US dollar.

4.2.3. Bank control variables

In this study, three bank-level control variables were used: 1. Bank Size. 2. Bank Growth 3. Liquidity. Bank size is the logarithm of bank annual total assets (S. Moudud-Ul-Huq, Citation2019a) (S. Moudud-Ul-Huq et al., Citation2018a) (S. Moudud-Ul-Huq, Citation2020) (S. Moudud-Ul-Huq et al., Citation2020) (S. Moudud-Ul-Huq et al., Citation2020). Bank growth is the year to year asset growth of a bank. The banks which have high growth can have different risk-taking incentive than small or low growth bank (B. Ashraf et al., Citation2017). Liquidity is the ratio of total loans to the total deposit. In respect of credit risk, it is considered an important one. High level of liquidity is represented as a high level of loans and advances which means there is a high level of investment in risk-weighted assets. Therefore, it will lead the bank to a high level of risk (Berger & Udell, Citation1995).

4.2.4. Industry-level variable

Bank industry is directly related to credit risk which plays an important role in the risk-taking behavior of banks. The variables are 1. Capital Stringency, 2. Industry Concentration. 3. Explicit Deposit Insurance. Capital stringency represents the state in which the bank has complied with the BASEL requirements. It reflects the type of fund that may be used as capital. Banking industry pattern may influence the risk-taking behavior of a bank significantly. For that reason, we include the banking industry concentration variable. This is defined as the percentage of total asset of all banks in a country. Deposit insurance is a measure to implement for the protection of bank depositors either fully or partly. Deposit insurance is a dummy variable which equals 1 if the bank's explicit deposit insurance otherwise 0.

5. Empirical results

The empirical result consists of three parts, those are: Descriptive Statistics, Correlation Analysis and, Main Results. The results are broadly described below:

5.1. Descriptive statistics

Descriptive statistics of all are presented in the following Table . Our main risk is NPLTL. We also use three alternative measures of risk, they are LLPTL, SROA and SROE.

Table 1. Description of the variable

Table 2. Descriptive statistics

Table displays that the mean value of NPLTL and LLPTL are 0.749 and 0.292, respectively. The NPLTL ranges from a maximum.45 to a minimum .00 with a standard deviation of .0825. On the other hand, LLPTL ranges from a maximum .54 to minimum .00 with a standard deviation of. 0411. It is also observed that the average credit risk that is proxied by SROA and SROE are .817 and 10.770, respectively. SROA takes the maximum and minimum value of 3.73 and .00, respectively. The maximum value of SROE is 51.91 and the minimum value is .84. Average Trade Openness is .3508 and ranges from a maximum and minimum value of .46 and .24 with a standard deviation of .060. The average value, maximum, minimum and standard deviation with a median of Liquidity, Bank Size, Bank Growth, Capital stringency, Industry Concentration, and Deposit Insurance have also been portrayed in Table .

5.2. Correlation analysis

Pearson correlation coefficients between variables are presented in Table . The main objective of our paper is to determine the impact of trade openness on bank risk-taking behaviour. From Table we see that trade openness is negatively and significantly correlated with both credit risk and overall risk which means that with higher trade openness, credit risk and overall risk-taking behaviour of banks decreasing. It is also revealed from the table that bank growth has a negative significant relationship with credit risk. Bank size has a positive significant relationship and it suggests that bank with high growth has high risk. Liquidity has a negative significant relationship with the risk that implies that bank with higher liquidity takes a low level of risk. Deposit insurance is a dummy variable which significantly negative relation with risk. Industry concentration has positive significant and capital stringency has a negative significant impact on risk. Moreover, the highest correlation between independent variables (size and trade openness) is 0.497. As per Kennedy (Citation2008), if the correlation exceeds 0.70, then it shows a multicollinearity problem. Hence, there is no issue of multicollinearity in the model which we have been used in this study.

Table 3. Correlation matrix

5.3. Main results

In this study, the Generalized Method of Moments (GMM) system panel estimator has been used which is developed by Alonso-Borrego and Arellano (Citation1999) and Blundell and Bond (Citation2000) and applied for our dynamic panel data to address the endogeneity and unobserved heteroscedasticity and autocorrelation problems of the model (S. Moudud-Ul-Huq et al., Citation2018a). Table shows the main results from the GMM estimator. In this paper, our prime variable is NPLTL, we also used three alternative risk measures SROA, SROE, and LLPTL. Our main concern is to find out the relationship between trade openness and credit risk. We also used two other independent variables to examine the impact on credit risk. They are the bank-level variables and industry-level variables.

Table 4. The effect of trade openness on risk

From Table , it is observed that trade openness is negatively and significantly related to credit risk proxied by NPLTL and LLPTL and overall risk proxied by SROA and SROE. It implies that the higher the trade openness, the lower the bank overall and credit risk which supports the results of B. Ashraf et al. (Citation2017) and opposite of Luo et al. (Citation2016). Bank growth (AG) is positively related to NPLTL, LLPTL which indicates a higher probability of generating credit risk and overall risk with accelerating banking assets. The result corroborates to Zheng et al. (Citation2017b). And SROA were negatively and significantly related to SROE. Bank size is positively and significantly related to the three risks except for SROA which is complied with the theory of “too-big-to-fail” and the result of Zheng and Moudud-Ul-Huq (Citation2017), indicating that larger the bank size greater the possibility to become failure with a high burden of risk. Liquidity is significantly and negatively related to the two-credit risk and positively related to overall risk. It means that banks with higher liquidity take lower credit risks. Deposit insurance is a dummy variable which is negatively and significantly related to bank risks. Capital stringency is negatively and significantly related to credit risk where insignificantly negatively related to SROA and positively related to SROE. At the end, J-statistic supports the instruments which we have been used here. AR (1) and AR (2) are first and second-order autocorrelation. Ultimately, it validates our main results that also glimpse the test of goodness of fit.

6. Conclusion

This study develops and tests the model for bank risk-taking behaviour on the basis of trade openness, bank growth, bank size, liquidity, deposit insurance, industry concentration, and capital stringency by using a sample of 32 commercial banks for a period of 2000 to 2017. The prime objective of this study is to identify the impact of trade openness on bank risk-taking behaviour. In this study, we used two types of risks, namely, credit risk (NPTL and LLPTL) and overall risk (SROA and SROE) in our analysis. Finding suggests that trade openness is negatively related to bank credit risk and overall risk. Hence, regulators need to promote bank for open operations and ensure ample spaces for competition. We find that bank growth has a positive relation with risk, and banks with large growth have large risk. So, it will be suggested that banks with higher growth have to maintain a credit limit for getting rid of the risk. Banks with large size take a higher risk than bank with small size. This is an important bank risk determinant. It is concluded that large banks are more likely to take the risk of loan default. Larger banks should be careful in providing loans to the credit sector. Another risk determiner is liquidity. Liquidity is not so much important for overall risk but credit risk. Liquidity has a positive relation with overall risk and negative relationship with credit risk. That indicates that the banks which have higher liquidity are in the risk of credit risk than that of smaller banks. The results also show that industry concentration is positively related to credit risk. Higher industry concentration caused a higher risk. We found capital stringency has a negative relationship with risk. Higher capital stringency lowers the risk. So, banks should hold capital above the minimum requirements to absorb potential future risk. It is also evident from the empirical results that deposit insurance has a negative relation with bank credit risk. Therefore, higher deposit insurance helps to decrease the credit risk of a bank.

This analysis provides beneficial information to the bank regulatory authority, traders, government, creditors, shareholders, bondholders, and other relevant stakeholders to judge the true risks of commercial banks in Bangladesh. Future research would be carried out in considering non-bank financial institutions such as insurance and leasing firms and considering cross-country analysis to get more insightful information regarding this issue.

Cover image

Source:

Additional information

Funding

Notes on contributors

Sk Alamgir Hossain

Sk Alamgir Hossain, a Ph.D. student in Business Administration under the School of Management at Huazhong University of Science and Technology, China, has been teaching as an Assistant professor in the Department of Finance at Jagannath University, Dhaka, Bangladesh. His research interest is in the areas of bank risk management, corporate banking, electronic banking, and new-age technology.

Syed Moudud-Ul-Huq

Dr. Syed Moudud-Ul-Huq is an Associate Professor and the Chair of the Department of Business Administration and Accounting at Mawlana Bhashani Science and Technology University (MBSTU). His primary research interests are Financial Economics, Risk Management, Econometric Modeling etc. He has published in International Journal of Emerging Markets, Research in International Business and Finance, Eurasian Economic Review, Journal of Financial Regulation and Compliance, Global Business Review etc.

Marufa Binta Kader

Marufa Binta Kader is currently doing her master’s in business administration at Mawlana Bhashani Science and Technology University. Her primary interest of research is financial economics.

References

- Aggarwal, R., & Jacques, K. T. (1998). Assessing the impact of prompt corrective action on bank capital and risk. Economic Policy Review, 4.

- Agnello, L., & Sousa, R. M. (2011). Can fiscal policy stimulus boost economic recovery? Revue économique, 62(6), 1045–14. https://doi.org/10.3917/reco.626.1045

- Agoraki, M.-E. K., Delis, M. D., & Pasiouras, F. (2011). Regulations, competition and bank risk-taking in transition countries. Journal of Financial Stability, 7(1), 38–48. https://doi.org/10.1016/j.jfs.2009.08.002

- Alonso-Borrego, C., & Arellano, M. (1999). Symmetrically normalized instrumental-variable estimation using panel data. Journal of Business & Economic Statistics, 17, 36–49.

- Anginer, D., Demirguc-Kunt, A., Huizinga, H., & Ma, K. (2013). How does corporate governance affect bank capitalization strategies? The World Bank.

- Ashraf, B., Arshad, S., & Yan, L. (2017). Trade openness and bank risk-taking behavior: Evidence from emerging economies. Journal of Risk and Financial Management, 10(3), 15. https://doi.org/10.3390/jrfm10030015

- Ashraf, B. N., Zheng, C., & Arshad, S. (2016). Effects of national culture on bank risk-taking behavior. Research in International Business and Finance, 37, 309–326. https://doi.org/10.1016/j.ribaf.2016.01.015

- Baltagi, B. H., Demetriades, P. O., & Law, S. H. (2009). Financial development and openness: Evidence from panel data. Journal of Development Economics, 89(2), 285–296. https://doi.org/10.1016/j.jdeveco.2008.06.006

- Baltagi, B. H., Egger, P., & Pfaffermayr, M. (2013). A generalized spatial panel data model with random effects. Econometric Reviews, 32(5–6), 650–685. https://doi.org/10.1080/07474938.2012.742342

- Barth, J. R., Caprio, G., & Levine, R. (2004). Bank supervision and regulation: What works best. Journal of Financial Intermediation, 13(2), 205–248. https://doi.org/10.1016/j.jfi.2003.06.002

- Berger, A. N., & Udell, G. F. (1995). Relationship lending and lines of credit in small firm finance. The Journal of Business, 68(3), 351–381. https://doi.org/10.1086/296668

- Berger, A. N., & Udell, G. F. (2002). Small business credit availability and relationship lending: The importance of bank organisational structure. The Economic Journal, 112(477), F32–F53. https://doi.org/10.1111/1468-0297.00682

- Berk, J. B. (1995). A critique of size-related anomalies. The Review of Financial Studies, 8(2), 275–286. https://doi.org/10.1093/rfs/8.2.275

- Blundell, R., & Bond, S. (2000). GMM estimation with persistent panel data: An application to production functions. Econometric Reviews, 19(3), 321–340. https://doi.org/10.1080/07474930008800475

- Bolt, W., & Tieman, A. F. (2004). Banking competition, risk and regulation. Scandinavian Journal of Economics, 106(4), 783–804. https://doi.org/10.1111/j.0347-0520.2004.00388.x

- Borio, C. E., & Drehmann, M. (2009). Assessing the risk of banking crises–revisited. BIS Quarterly Review, March.

- Boyd, J. H., & De Nicolo, G. (2005). The theory of bank risk taking and competition revisited. The Journal of Finance, 60(3), 1329–1343. https://doi.org/10.1111/j.1540-6261.2005.00763.x

- Cai, J., & Thakor, A. V. (2008, November). Liquidity risk, credit risk and interbank competition. Credit Risk and Interbank Competition, 19, 2008.

- Chernykh, L., & Cole, R. A. (2011). Does deposit insurance improve financial intermediation? Evidence from the Russian experiment. Journal of Banking & Finance, 35(2), 388–402. https://doi.org/10.1016/j.jbankfin.2010.08.014

- Cornelli, F., Goldreich, D., & Ljungqvist, A. (2006). Investor sentiment and pre‐IPO markets. The Journal of Finance, 61(3), 1187–1216. https://doi.org/10.1111/j.1540-6261.2006.00870.x

- Demirgüç-Kunt, A., & Kane, E. J. (2002). Deposit insurance around the globe: Where does it work? Journal of Economic Perspectives, 16(2), 175–195. https://doi.org/10.1257/0895330027319

- Goetz, M. (2010, May). Bank organization, market structure and risk taking: Theory and evidence from US commercial banks. Federal Reserve Bank of Boston Working Paper.

- Gropp, R., & Vesala, J. (2004). Deposit insurance, moral hazard and market monitoring. Review of Finance, 8(4), 571–602. https://doi.org/10.1093/rof/8.4.571

- Gupta, A. D., & Moudud-Ul-Huq, S. (2020). Do competition and revenue diversification have significant effect on risk-taking? Empirical evidence from BRICS banks. International Journal of Financial Engineering, 7.

- Haselmann, R., & Wachtel, P. (2007). Risk taking by banks in the transition countries. Comparative Economic Studies, 49(3), 411–429. https://doi.org/10.1057/palgrave.ces.8100214

- Jacques, K., & Nigro, P. (1997). Risk-based capital, portfolio risk, and bank capital: A simultaneous equations approach. Journal of Economics and Business, 49(6), 533–547. https://doi.org/10.1016/S0148-6195(97)00038-6

- Kennedy, P. (2008). A guide to modern econometrics. Blackwell Publishing.

- Köhler, M. (2015). Which banks are more risky? The impact of business models on bank stability. Journal of Financial Stability, 16, 195–212. https://doi.org/10.1016/j.jfs.2014.02.005

- Lalon, R. M. (2015). credit risk management (CRM) practices in commercial banks of Bangladesh:“A study on basic bank Ltd.”. International Journal of Economics, Finance and Management Sciences, 3(2), 78–90. https://doi.org/10.11648/j.ijefm.20150302.12

- Luo, Y., Tanna, S., & De Vita, G. (2016). Financial openness, risk and bank efficiency: Cross-country evidence. Journal of Financial Stability, 24, 132–148. https://doi.org/10.1016/j.jfs.2016.05.003

- Matutes, C., & Vives, X. (2000). Imperfect competition, risk taking, and regulation in banking. European Economic Review, 44(1), 1–34. https://doi.org/10.1016/S0014-2921(98)00057-9

- Merton, R. C. (1977). An analytic derivation of the cost of deposit insurance and loan guarantees an application of modern option pricing theory. Journal of Banking & Finance, 1(1), 3–11. https://doi.org/10.1016/0378-4266(77)90015-2

- Moudud-Ul-Huq, S. (2018). Banks’ capital buffers, risk, and efficiency in emerging economies: Are they counter-cyclical? Eurasian Economic Review, 1–26.

- Moudud-Ul-Huq, S. (2019a). Can BRICS and ASEAN-5 emerging economies benefit from bank diversification? Journal of Financial Regulation and Compliance, 27(1), 43–69. https://doi.org/10.1108/JFRC-02-2018-0026

- Moudud-Ul-Huq, S. (2019b). the impact of business cycle on banks’ capital buffer, risk and efficiency: A dynamic GMM approach from a developing economy. Global Business Review, 0972150918817382.

- Moudud-Ul-Huq, S. (2020). Does bank competition matter for performance and risk-taking? empirical evidence from BRICS countries. International Journal of Emerging Markets, Ahead-of-prin. https://doi.org/10.1108/IJOEM-03-2019-0197

- Moudud-Ul-Huq, S., Ashraf, B. N., Gupta, A. D., & Zheng, C. (2018a). Does bank diversification heterogeneously affect performance and risk-taking in ASEAN emerging economies? Research in International Business and Finance, 46, 342–362. https://doi.org/10.1016/j.ribaf.2018.04.007

- Moudud-Ul-Huq, S, Halim, M. A, & Biswas, T. (2020). Competition and profitability of banks: empirical evidence from the middle east & north african (mena) countries. Journal Of Business Administration Research, 3(), 2. https://doi.org/10.30564/jbar.v3i2.1807

- Moudud-Ul-Huq, S., Zheng, C., & Gupta, A. D. (2018c). Does bank corporate governance matter for bank performance and risk-taking? New insights of an emerging economy. Asian Economic and Financial Review, 8(2), 205–230. https://doi.org/10.18488/journal.aefr.2018.82.205.230

- Moudud-Ul-Huq, S., Zheng, C., Gupta, A. D., & Hossain, S. K. A. (2020). Risk and performance in emerging economies: do bank diversification and financial crisis matter? Global Business Review, 1–27.

- Petersen, M. A., & Rajan, R. G. (2002). Does distance still matter? The information revolution in small business lending. The Journal of Finance, 57(6), 2533–2570. https://doi.org/10.1111/1540-6261.00505

- Pigka-Balanika, V. (2013). The impact of trade openness on economic growth. Evidence in Developing Countries”, Erasmus School of Economics, 1–32.

- Rahman, M. M., Uddin, K. M. K., & Moudud-Ul-Huq, S. (2015). Factors affecting the risk-taking behavior of commercial banks in Bangladesh. Applied Finance and Accounting, 1(2), 96–106. https://doi.org/10.11114/afa.v1i2.850

- Rajan, R. G., & Zingales, L. (2003). The great reversals: The politics of financial development in the twentieth century. Journal of Financial Economics, 69(1), 5–50. https://doi.org/10.1016/S0304-405X(03)00125-9

- Repullo, R. (2004). Capital requirements, market power, and risk-taking in banking. Journal of Financial Intermediation, 13(2), 156–182. https://doi.org/10.1016/j.jfi.2003.08.005

- Roy, A. (2008). Organization structure and risk taking in banking. Risk Management, 10(2), 122–134. https://doi.org/10.1057/palgrave.rm.8250043

- Stever, R. (2007). Bank size, credit and the sources of bank market risk.

- Yanikkaya, H. (2003). Trade openness and economic growth: A cross-country empirical investigation. Journal of Development Economics, 72(1), 57–89. https://doi.org/10.1016/S0304-3878(03)00068-3

- Zheng, C., Das Gupta, A., & Moudud-Ul-Huq, S. (2017a). Do market competition and development indicators matter for banks’ risk, capital, and efficiency relationship? International Journal of Financial Engineering, 4(2n3), 1750027. https://doi.org/10.1142/S242478631750027X

- Zheng, C., & Moudud-Ul-Huq, S. (2017). Banks’ capital regulation and risk: Does bank vary in size? Empirical evidence from Bangladesh. International Journal of Financial Engineering, 4(2n3), 1750025. https://doi.org/10.1142/S2424786317500256

- Zheng, C., Moudud-Ul-Huq, S., Rahman, M. M., & Ashraf, B. N. (2017b). Does the ownership structure matter for banks’ capital regulation and risk-taking behavior? Empirical evidence from a developing country. Research in International Business and Finance, 42, 404–421. https://doi.org/10.1016/j.ribaf.2017.07.035