?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

In a developing country like Ghana, Micro, Small, and Medium Scale Enterprises (MSMEs) play an important role in the socio-economic development of the economy. Payment of income tax by MSMEs remains one of the key sources of government revenue for development activities in Ghana. However, not much is known regarding the compliance of MSMEs with income tax administration in Ghana. Understanding income tax administration compliance and associated challenges among MSMEs could assist relevant policy actors in designing strategies to improve income tax administration in Ghana. Against this background, a mixed-method study involving 210 (200 MSMEs and 10 key informants) sample was conducted to examine the compliance of MSMEs with income tax administration in the Nkwanta South District of Ghana. The study revealed a lack of tax education, high tax rate, low level of income, and high household consumption levels as the dominant and influential factors to tax compliance among the MSMEs. The study further showed that challenges associated with tax administration include low institutional capacity, inadequate resources, negative public attitude towards tax payment, lack of collaboration between the tax agencies, and political interference. Based on these findings, it is important for policymakers and tax collection institutions to strengthen and streamline existing measures to ensure effective income tax administration in Ghana.

PUBLIC INTEREST STATEMENT

Like other developing countries, the Ghanaian government relies heavily on income tax to implement most developmental projects. Given this background, we sought to examine the compliance of MSMEs with income tax administration in the Nkwanta South District of Ghana. We identified several factors influencing compliance with income tax administration among MSMEs in the study district. We further found a number of challenges hindering effective income tax administration in the study area. Policy recommendations aimed at lessening the challenges of income tax administration compliance have been offered for implementation by policy actors.

1. Introduction

The motivation to improve internal revenue has made tax administration and policy formulation a priority for governments in developing countries (Ayee, Citation2010; Brautigam & Knack, Citation2004; Conteh & Ohemeng, Citation2009; Ohemeng & Owusu, Citation2015; Paepe & Dickinson, Citation2014). It has been established that taxes represent one of the major sources of government revenue for developmental activities in both developed and developing countries (Ayee, Citation2010; Owusu and Ohemeng, 2013). Therefore, to strengthen revenue mobilization in Ghana at the local level, Metropolitan, Municipal and District Assemblies (MMDAs) have been given the mandate to collect taxes and levies to support internal development (Armah et al., Citation2014). The composition of these taxes by MMDAs at the local level includes investment income, specialized funds- stool lands and royalties, fines, property rates, licenses, trading services among others (Ankamah, Citation2012; Kessey, Citation1995).

At the local level, Micro, Small, and Medium Enterprises (MSMEs) constitute one of the key corporate organizations in Ghana. Whereas enterprises with 10 or more workers are classified as medium and large scale, those with workers below 10 are termed as micro and small scale (Kayanula and Quartey, Citation2000). The MSMEs are perceived to be the engine of growth in every developing country (Rochaa, Citation2014) because of their specific attributes including employment capacity, ability to discover new opportunities, dynamism, and commercialization of economic activities (Spence, Citation2007). Of particular concern is that the MSMEs sector remains the major employment opportunity (Sydney, Citation2012) because it offers employment to about 85% of the labor and contributes 70% to Ghana’s Gross Domestic Product (Abor & Quartey, Citation2010).

Aside from these contributions to the economy of Ghana, MSMEs are supposed to pay tax to facilitate development activities. Yet, studies suggest that MSMEs have the tendency of evading tax as compared to the larger firms (Kirchler et al., Citation2006; Schuetze, Citation2002). The reason could be that individual MSME pays a little amount of tax as compared to the amount paid by larger establishments. In view of this, tax agencies and authorities tend to concentrate more on the larger businesses and neglect the smaller firms (Bird & Zolt, Citation2013; Atawodi & Ojeka, Citation2012). This explains the need to determine the compliance of MSMEs with income tax administration in Ghana.

Evidence suggests that studies on tax compliance among MSMEs have been focused on countries such as Indonesia (Hanum & Hasibuan, Citation2019; Inasius, Citation2019; Mukhlis & Simanjuntak, Citation2016) and South Africa (Wadesango et al., Citation2018). Few Ghanaian studies have given little attention to challenges facing tax administration (Abdul–Razak & Adafula, Citation2013; Agbadi, Citation2011; Okpeyo et al., Citation2019; Kuug, Citation2016). Understanding the compliance with income tax administration and associated challenges among MSMEs is critical to informing policymakers in the design of strategies to improve revenue mobilization for development in Ghana. The purpose of this study is to examine the compliance of MSMEs with income tax administration in the Nkwanta South District of Ghana.

2. Theoretical framework underpinning taxation and rate of compliance

Theories are propounded on the basis to explain, predict and help understand occurrences and facts, and to some degree challenge and broaden existing knowledge within the limits of some bounding assumptions (Bartole, Citation2012; Swann, Citation2003). Every research is rooted in a theory that informed the problem, questions, and possibly the objectives of the study (Van der Vorm et al., Citation2009). This study was based mainly on the Allingham and Sandmo theory of taxation with some supporting theories such as the Economic Based and the Social Psychological theories.

2.1. The A–S model of taxation

The Allingham and Sandmo theory explains the decision of the taxpayer based on the assumption that, the taxpayer’s real decision cannot be determined and accounted for concerning their inputs supply (labor and capital) and gross earnings as individuals and business entities. Ultimately, the theory focused on the taxpayers in the economy by observing the taxpayer at the time of filing his/her tax returns. The theory tries to predict the taxpayer in terms of the amount of his/her income to report and how much to evade. According to the theory, if the taxpayer decides to evade tax and it is not detected by the tax authority, his decision is represented by the equation as shown below:

Where; Y = taxpayer’s income

t = tax rate

E = the amount evaded (income underreported)

G—E = the reported income

The tax payer’s gross income is denoted by “G”. If a tax payer reports income fully, the equation would have been “tG” (where “t” is the tax rate multiplied by the gross income “G”). Meaning a tax payer has paid tax fully. However, because a tax payer has underreported his/her income which is denoted by “E”, the income equation would be Y = G—t(G—E). This means the underreported income has been deducted before taxation has now taken place.

However, according to the theory, if it is detected the taxpayer has underreported, he/she pays a penalty rate of tax (θ) on the amount of income evaded and the taxpayer’s equation of income is stated as:

Where;

The theory assumes that the taxpayer’s probability of detection is denoted by “p”. If She/he then decides the amount to evade to increase his/her expected utility, the equation will be represented as shown below:

It can be deduced from the theory that taxpayers are considered to be risk-averse in their decision regarding tax payment. However, a larger gross income earner would evade more if it is deemed that, individuals become highly enthusiastic and involve themselves more in perilous activities as they become better-off. According to the A-S model, the additional tax rate is having an economic consequence on the state. Meaning that a higher tax rate comes with two effects—income and substitution effects. The income effect is negative: a high rate of tax makes the taxpayer poorer and for that matter less willing to pay their taxes. However, the substitution effect is applied in the direction of increased evasion: meaning, a high tax rate makes the taxpayer evade more. The study employed the Allingham and Sandmo model of taxation to analyze the technicalities and difficulties involved in administering income tax on companies, firms, and other smaller enterprises. The theory applies to this study because all the theoretical concepts and variables in the model explain exactly the behavior and perception of the taxpayer concerning income tax administration among all businesses of different scales. It is very true that adherence to tax compliance is possible among the larger and medium scale enterprises but not among the smaller businesses.

2.2. Economic based theory

This theory classifies taxpayers into two categories. That is, the habitual compliers—taxpayers who report their incomes truthfully regardless of their pecuniary interest (Feld & Frey, Citation2007) and secondly, taxpayers who act strategically, that is, they examine their incentive carefully and act accordingly to maximize their expected utility, given the probability of audit associated with the income they choose to report (Atawodi & Ojeka, Citation2012). The economic-based theory explains that taxpayers are unethical and would always want to maximize their expected utility by “playing the audit lottery”. They are manipulated by monetary benefits such as enhancing their profit and explore the likelihood of detection. As such they analyze alternative compliance paths (whether or not to evade tax), the possibility of being detected, and the resulting consequences. They then select the alternative path that maximizes their expected after-tax returns after adjusting for risk (Trivedi et al., Citation2005).

2.3. The social psychological theory

The social psychology theory which is in contrast with the first two theories holds the view that, in evaluating the citizen’s tax compliance behavior, one must start answering the question: how is the taxpayer viewing or considering the state in mind? (Noguera et al., Citation2014). According to this theory, the way people think concerning the occurrences in society influences their way of values, reaction, interaction, behavior, and attitude rather than the truth and realism towards tax compliance (Lewis, Citation1978). Meaning that the impression people get in mind when issues concerning tax policies and regulations are mentioned is made up of the social-psychological determinant of tax compliance behavior (Lewis, 1978; Noguera et al., Citation2014). The theory also posits that the taxpayer’s propensity to react favorably or otherwise to a tax situation depends largely on his attitude, moral and ethical values as influential factors (Ajzen & Fishbein, Citation1977; Eagly and Chaiken, Citation1993). Also, it clear that there are various ways an individual’s attitude can be measured concerning taxation. That is, the individual’s way of judging the state and the government policies (Schmolders, 1970), his prejudiced appraisal of the tax evasion (Porcano, Citation1988), and then conclude with a moral and ethical attitude towards tax evasion (Orviska and Hudson, Citation2003). Kirchler et al. (Citation2007) observed that personal norms are seen as the interior and typical way of behavior such as unselfishness, norm-dependency, or religious beliefs which is generally associated with high tax ethics and readiness to obey or conform. Generally, this theory believes that noncompliance will be high if individuals get the information or clue that, justices are tempered with mercy when people evade tax (Orviska and Hudson, 2002).

3. Setting and methods

3.1. Study area

The study was conducted in the Nkwanta South District in Volta Region, Ghana. This is because the district has a large number of MSMEs. Despite the prevalence of MMSEs in the district, the Assembly struggles to mobilize enough Internally Generated Fund (IGF) to undertake development activities (Nkwanta South District Assembly, Citation2016). The location of the district explains the role it plays in trade with Togo as a country. The location of the district allows the people of Volta, in general, to trade directly with the people of Togo in all kinds of goods and services (Ghana Statistical Service, Citation2014). Hence the majority of the people are engaged in MSMEs and for that matter are supposed to perform their national duties of paying tax for national development. Besides, the study area allows for businesses with other surrounding districts such as Kadjebi, Nkwanta North, and Krachi East. This has contributed to enhancing business activities in the study area. That is, there is always a ready market for both agriculture and manufactured products. Due to the position, there are seven markets in the area drawing people from other areas to the district for business activities (Ghana Statistical Service, Citation2014). However, the position of the district, has an adverse effect on the administration of income tax. This is because many of the businessmen move to Togo by dodging their tax responsibilities thereby leading to tax evasion. Figures and are maps showing the location and position of the region in the national context as well as the location of the district in the regional context.

Figure 1. Map of Volta region in National Context.

The region is bounded by Eastern region to the west, the Northern region to the North, Greater Accra region to the South and the Republic of Togo to the Eastern part. This is clearly in fig. 3.1.

Figure 2. Map of Nkwanta South District in a Regional Context.

Exchange of goods and services is carried out between the district and Togo and this enhances or boosts the economic activities of the businessmen (MSMEs) by improving their wellbeing. Its interaction with the surrounding districts serves as an avenue through which many enterprises are created in the district. This can be taken as an advantage by the tax institutions in the area to mobilize revenues to support development.

3.1.1. Sampling process

Sampling process is important in every research because it helps to determine the representiveness and generalization of the study findings (Bruijnzeels et al., Citation1998). The study made use of an integration of sampling techniques involving both probability and non-probability approaches. Under the non-probability sampling, a purposive sampling technique was used to choose the institutions (GRA and NSDA). The use of a purposive sampling technique to select ten (10) officers from the various tax collection institutions was due to their knowledge of income tax administration in the study area. Studies have indicated that the purposive sampling technique is used to select participants who have knowledge about the issue under investigation (Denscombe, Citation2014, Citation2010; Kyale Citation1996).

Probability sampling procedures such as stratified and simple random sampling were used to ensure that every MSMEs has an equal chance of taking part in the study (Babbie and Mouton, Citation2004). These types of probability techniques were chosen based on the uniqueness of the targeted MSMEs, source of data, available resources, and its ability to yield required data towards meeting the study objectives (Antony et al., Citation2008). Given the above discussion, a sample size of 200 respondents was chosen for the quantitative aspect of the study (see Table ) . Based on the population of the MSMEs in each selected community, Slovin’s formula for calculating the sample size was used to estimate the sample size as;

Table 1. Selected communities with market centers and MSMEs in the district

Sample size (n) = N

Where; N = total population of MSMEs, e = margin of error

With a total population of stratified MSMEs of 398,

N = 396, Confidence level = 95%, Margin of error (e) = 0.05

n = 398 398(0.05)2

n = 398

1.995

n = 200

Also, Table shows how the Slovin’s formula was used to sample the MSMEs based on their scale of operation in the study area.

Table 2. Selection of MSMEs based on scale of operation in the study district

Therefore, a total number of 200 MSMEs made up of dressmakers, hairdressers, storekeepers, food vendors, and local industries were sampled with the micro-enterprises dominated with a total number of 120, followed by small enterprises with 60 sample size and medium enterprises came last with 20 sample size. In all, the sample size was 210 (200 MSMEs and 10 officers from the various tax collection institutions).

4. Data collection instrument and procedure

The complex nature of the study necessitated the adoption of a mixed-method approach, thus the use of both quantitative and qualitative (Hurmerinta-Peltomäki and Nummela, Citation2006). Because of this, both qualitative and quantitative methods of data collection were used in collecting data on compliance with income tax. The use of these varied tools and techniques such as interview guides, observation guides, and structured questionnaires were informed by the wide range of data sources and information needed to address the study objective. In the first place, the questionnaires were made up of close-ended in nature (Ozuru et al., Citation2007). It was administered to the selected MSMEs in the district. The questionnaire was made up of specific questions on issues such as factors affecting income tax compliance among MSMEs, the behaviour of tax officials on the field, tax laws and policies, annual incomes, income statements and deductions, tax registration and filing procedures, method of tax collection, measures and strategies to improve compliance rate among others. The administration of each questionnaire lasted 20 minutes on the average.

The interview guides, on the other hand, were used to collect information from the GRA officers and the officials from the Nkwanta South District Assembly (Budget Officer, District Planner, and the Rural Enterprise Project Officer) as well as executives of business associations. The interview guides captured questions on factors influencing tax administration, the effectiveness of tax administration as well as challenges associated with tax administration. All interviews took place at convenient place with the aim of minimizing distraction and ensuringthat the participants feel free to talk. The interview was conducted in English because they were able to speak and understand English. Interview lasted approximately 25 minutes on the average. Aside from the interview and questionnaire administration, direct observation was used as a method of data collection. This was based on the principles of the social psychology theory that emphasized values, attributes, and the general behavior of the taxpayer regarding tax compliance. Observation, as adopted, was used to get a better understanding of the behavior and the attitude of both the taxpayer and the tax officials during tax collection within the District. The observation technique was also focused on tax payment by MSMEs, time of tax collection as well as facial and body expressions and behaviors of both tax collectors and taxpayers. In taking into consideration ethical compliance, we sought both verbal and informed consent from the respondents after explaining the purpose of the study to them. They were further assured of strict confidentiality of the information they provided.

5. Reliability and validity of the study

The exact representation of the elements or inhabitants under study is known as reliability (Joppe, Citation2000). Similarly, if the outcome of the research can be reproduced using the same or similar methodology, then the instruments and the techniques employed in the study are said to be reliable. Validity determines whether the research accurately determines or measures what it was meant to measure and how precise the research outcomes are (Wainer and Braun, Citation1988). The doctrine of validity is critical about the measuring tools and methods adopted in the study. Validity and reliability are the guiding principles and objectives of all scientific inquiries (Denscombe, Citation2010). Hence, it is necessary to put in place mechanisms that will lead to the reliability of the study findings to ensure its broader validity. This was important to ensure the study measures what it aimed at measuring for generalization (Spriggs and Hansford, Citation2000). To ensure that data gathered was relevant and that error margin minimized, the following steps were taken to ensure reliability and validity. In the first place, a pre-test was carried out in Nkwanta town (one of the communities) in the study district and 10 questionnaires were administered to a few selected MSMEs to get a clear understanding of how respondents understood the questions. This was important to know the adequacy, clarity, relevance, suitability, and feasibility of the questionnaire as an instrument that was to be used in the study. Furthermore, purposive sampling was employed to choose communities based on the zonal classification and areas of dominant marketing activities to ensure that, respondents are selected from at least each zone in the study district (Martsolf et al., Citation2006). This was to ensure the possibility of getting views that represent the entire area. Concerning the MSMEs, the use of a stratified and simple random sampling technique helped to ensure that respondents were spread across all parts of the study area. This helped to provide a good representation of all aspects of MSMEs in the study area. Also, the triangulation of data was carried out to ensure validity (Rhineberger et al., Citation2005). Initially, data from MSMEs was triangulated with institutional data to understand the true nature of tax compliance. All the above measures were adopted to enhance the reliability and validity of data collected.

6. Data analysis

Data were processed through a series of procedures involving daily editing of data at the time of collection and final editing after the entire fieldwork was completed. This was important as it helped quicker detection of mistakes which in some cases led to returning to respondents for clarification (Yukselturk & Bulet, Citation2007). Instruments were then coded into the SPSS (SPSS version 18) to facilitate analysis. Both descriptive statistics (percentages and frequencies) and inferential statistics (ordinal logistic regression) were used to analyze quantitative data. Results were presented in the form of tables and figures. On the other hand, the analysis of qualitative data was done using thematic analysis. In this case, we developed themes from the interviews we conducted with the institutions such as the Nkwanta South District Assembly and GRA about challenges facing tax administration in the study area.

7. Analysis and discussion

7.1. Socio-demographic characteristics of the respondents

To understand the context of the study and also highlight the validity of the statistics gathered, it is very imperative to discuss the demographic characteristics of the respondents from whom information was sourced. This section of the study focuses on the characteristics of respondents that are considered prudent to the study. Concerning the study topic, age, sex distribution, educational level, marital status, type of business, working status, and many others were considered.

7.1.1. Age distribution of respondents

Age is an important determinant of one’s ability to participate in tax payment in the development of the economy as a whole. About 51% of the respondents were aged between 31 and 45 years of age (see Table ).

Table 3. Age distribution of respondents

Economically, this high proportion of the working force in the district can serve as an engine for rapid growth and development. Concerning the high percentage of the labor force, MSMEs in the study district should be contributing enormously through tax to ensure growth and development.

7.1.2. Sex distribution of respondents

About the sex distribution, the respondents were 83 (41.5%) males as against 117 (58.5%) females as shown in Table . This implies that the females are self-reliant and are competing on equal grounds with the males based on business in the district.

Table 4. Sex distribution of respondents

Women’s dominance in micro, small and medium scale enterprises in the study district imply that the majority of them are solely responsible for the general out-keep of their household in terms of food, education, health, and shelter. It also, implies that they can equally contribute their share of development through taxation on equal grounds with the men.

7.1.3. Level of education of respondents

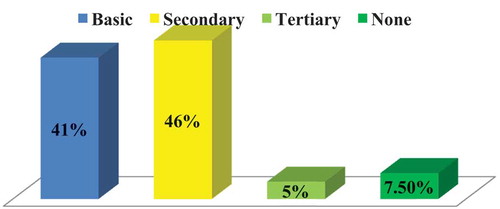

An individual’s ability to read and write explains to some degree his/her literacy rate in society. Also, people’s mental and psychological abilities to understand and connect fiscal policies and decisions taken by the government concerning creating a favorable environment to enhance economic activities in the economy are crucial in determining the tax compliance rate among the MSMEs. Besides, proper record keeping requires fluency in reading and writing. The educational status of the respondents is a potential advantage for assessment and collection of income tax as they can easily understand assessment procedures and also be prepared to pay their taxes when it is explained to them. The educational level of the respondents is shown in Figure .

Figure 3. Level of education of respondent.

Most of the MSMEs have got some level of academic qualification: a total of 82 respondents representing 41% had completed basic school, 93 respondents representing 46% responded that they had completed senior high school, 10 respondents representing 5% indicated they had completed tertiary level of education and 15 respondents representing (7.5%) indicated they had no form of education in their life. Therefore, the majority of the respondents have some form of education to improve their business activities.

7.1.4. Marital status of respondents

Marital status can have an important effect on optimal household decisions and thereby affect the compliance rate of business owners. About 84% were married (see Table ).

Table 5. Marital status of respondents

Possibly, this can increase the rate of consumption because married couples with children in the family would have their marginal propensity to consume higher thereby reducing the level of income in the business. As a result of a reduction in income, business owners can be influenced in their decisions for income tax compliance. Economically, an individual who is single and determines can manage his/her resources to an appreciable level than married couples with children regarding incomes that go into consumption and savings. This explains why the majority of the MSMEs responded to low business incomes and high consumption as factors influencing their income tax compliance. These factors (low incomes and high consumption) were also mentioned by Atawodi and Ojeka (Citation2012) in their studies on factors influencing tax compliance in Nigeria.

7.2. Business information of respondents

This section of the analysis reflects on the business details of respondents that were very crucial to taxation policies vis-à-vis respondents’ compliance in the study district. The key component of fiscal policy looks at taxes the government chooses to levy, in what amount, and on whom. This can best be tackled when the business information of MSMEs are known to the tax authorities. Efficiency, fairness, equity, and the economic principle of taxation can be ensured and enhanced the business environment when such information as to working status, location of the business, number of employees, annual income, and financial record-keeping among others are known to the government and its tax agencies. Findings on this information from the study district are discussed below.

7.2.1. Working status of respondents

The working status of the respondents was investigated to ascertain whether they owned the business or are managers of the businesses. The rationale is to determine whether respondents file for tax and/or allow for tax assessment in the business ventures. The survey result pointed out that, 141 (70.5%) respondents admitted they are the real owners of the business while 59 (29.5%) respondents said they are managers of the business as shown in Table .

Table 6. Working status of respondents

The statistics of the working status of the MSMEs presented a nice opportunity for tax agencies to interact well with the business owners for adequate information on their businesses that will improve income tax administration.

7.2.2. Location of business of MSMEs

The location of the various MSMEs in the district is very crucial to both GRA officials and the District Assembly. This helps the institutions to find the business owners, assess, and collect taxes from them. From the field survey as many as 170 (85%), business owners indicted that, their business has a permanent location. Further, 23 (11.5%) responded that they roam from places to places to transact their business while 7(3.5%) respondents said they have a permanent location and still roam sometimes as shown in Table .

Table 7. Location of respondents’ business site

This suggests that the idea of MSMEs not being located due to their mobility is posing a slight problem in the study district. This is because it will be difficult to find and assess them for tax.

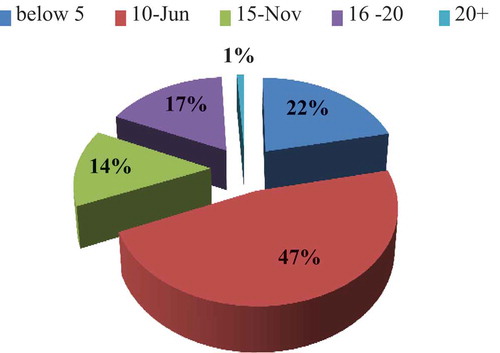

7.2.3. Duration of operation of MSMEs

Findings indicate that the startup businesses and those in their short term periods (from 1–5 years) are 43 representing 21.5%, and respondents who indicated they are in operation for 10–20 years are 155 representing 77.5%. Only 2 (1%) respondents indicated they are operating in their businesses for more than 20 years now as illustrated in Figure .

Figure 4. Duration of Operation of Respondents.

This implies that most MSMEs are well established and have gained ground in their businesses hence might have been assessed and paying their taxes as required. But this is not the case in the study district because a high proportion of MSMEs have been operating for several years without registering with the tax agencies and thereby not contributing to national development through the payment of tax.

7.2.4. Number of employees of MSMEs

About 122 (61%) business owners indicated they have employees ranging from 1–5 in their businesses while 39 (19.5%) respondents pointed out that they have 6–10 employees. Also, 31 (15.5%) responded they have 11–20 employees in their businesses. However, 8 (4%) respondents indicated they have no employees in their businesses (see Table ).

Table 8. Number of employees of respondents

The implication from the foregoing discussion is that MSMEs in the district are dominated by micro-businesses. Such businesses are small in terms of business capital, asset base, and annual returns. Hence they find it difficult to voluntarily comply with income tax administration and policies.

7.2.5. Respondent annual income

In every effective tax administration, taxes are computed based on the individual’s income received hence, it is imperative and crucial for business owners to report their annual incomes accurately. This is because over-assessment will affect the MSMEs income levels and under assessment will reduce government tax revenue.

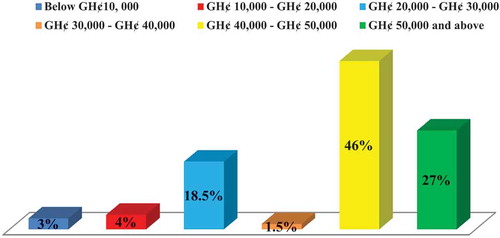

Figure 5. Respondents annual income

From Figure , respondents out of 200 representing 3% received below GH¢ 10,000 as their income annually, 8 (4%) indicated they received between GH¢ 10,000 and GH¢ 20,000 annually while 37(18.5) said their annual income ranges between GH¢ 20,000 and GH¢ 30,000. The smallest percentage of respondents (1.5%) said they received GH¢ 30,000 and GH¢ 40,000 annually whilst the highest percentage of respondents (46%) responded they received between GH¢ 40,000 and GH¢ 50,000 annually and 27% indicated their annual income lies above GH¢ 50,000. Studying the trend of responses, it is obvious that the majority of the MSMEs earn above GH¢ 20,000 annually. It means their financial position is strong and can be assessed for tax.

7.2.6. Records keeping of respondents

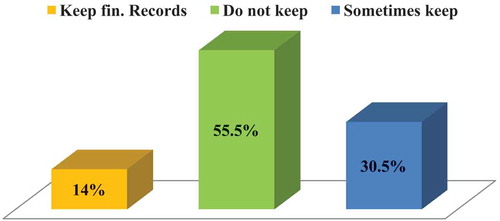

The field survey revealed that, out of the 200 MSMEs, only 28 (14%) responded they keep a financial record in their business operations while 111 respondents representing 55.5% responded they do not keep any business financial records. Further, 61 (30%) respondents did indicate they sometimes keep a business record but not always as shown in Figure .

Figure 6. Business record keeping of respondents.

Concerning the business record keeping of the respondents, the number of people who keep records are few and cannot tell if the records kept are accurate and authentic for tax assessment for filing. However, 86% of the respondents cannot present any record and this affects the tax administration in terms of registration, tax filing, and assessment because valuable information to carry out taxation cannot be provided by such businessmen. This affects revenue mobilization through tax and creates difficult conditions for the tax officials in their assessment procedures.

7.3. Factors influencing MSMEs income tax compliance

The study revealed that high tax rate, level of income, tax education, level of consumption, and behavior of tax officials are the main factors influencing MSMEs’ income tax compliance in the Nkwanta South district. Ordinal regression was computed to determine how the independent variables (registration of the business, tax rate, level of incomes, tax education, level of consumption, and behavior of tax officials) contributed to the dependent variable (tax compliance) among MSMEs.

7.3.1. Statistical findings—Ordinal regression

From the data collected through the questionnaire, results indicated that more than 70% of the MSMEs admitted practicing tax evasion and avoidance. That is, they sometimes underreport their gross incomes (G) to maximize their utility for money. This is in line with the Allingham and Sandmo taxation model (Y = G—t(G—E)). The study, therefore, investigated the factors that led to the underreporting of incomes by the taxpayers.

A five-point Likert-scale was employed in the administration of questionnaires with scales ranging from ―Strongly Agree‖ denoted by 1 to ―Strongly Disagree represented by 5 with neutral scores amid the two extremes. The result of the factors influencing MSME income tax compliance is presented in Tables –1. Further interpretations and discussions relied solely on the findings from the field survey.

Table 10. Model fitting information of ordinal regression

Table 11. Goodness-of-fit of ordinal regression

Table 12. Pseudo R-square of ordinal regression

Table 13. Factors affecting MSME income tax compliance

Table shows the model fitting table which depicts the −2 Log Likelihood for the intercept and the final models. It determines whether the model proves the ability to predict the outcome variable. Hence, it compares the model with intercept only (baseline) against the model with all the explanatory variables (the final model) to see if the final model significantly improves the fit to the data.

From the model fitting as indicated in Table , a Chi-Square value of 151.052 with a degree of freedom of 23 and a significant level of.000 (p < 0.05) implies that the final model gives a significant improvement over the baseline model. This means that tax education, tax rate, level of income, consumption levels, the behavior of tax officials, and registration of businesses determine the tax compliance of MSMEs. That is, a unit change in the independent variables (registration of the business, tax rate, level of incomes, tax education, level of consumption, and behavior of tax officials) will cause a proportional change in the dependent variable (tax compliance).

Table depicts the Pearson’s chi-square statistics as well as chi-square statistics based on deviance. It tests whether the observed data are consistent with the fitted model. The result indicates that the model is significant but does not predict as good as the observed data because p < 0.05. Table shows the goodness-of-fit model of Pearson and Deviance with the degrees of freedom 297 and p-values of 0.000

Table shows the Pseudo R-square of three different levels: Cox and Snell, Nagelkerke, and MacFadden values. It tells the proportion of variations in the outcome variable that can be clarified or explained by the predictors as mentioned above. A Pseudo-R-square value (Cox and Snell) of 0.53 means that 53% of the variations in tax compliance as a dependent variable can be elucidated by the predictors (registration of the business, tax rate, level of incomes, tax education, level of consumption and behavior of tax officials). Also, Nagelkerke and McFadden Pseudo R-square values of 0.550 and 0.227 imply that 50% and 22.7% of the variations in the dependent variable can be predicted by the independent variables respectively. The remaining percentages of variations are contributed by some extraneous variables lying beyond the model. This means that lack of tax education, high tax rate, low level of income, high consumption, non-registration, and the behavior of tax officials are not the only factors influencing compliance to tax administration in the district. Some other factors are not captured in the study model which contribute significantly to influence tax compliance among the MSMEs.

Table depicts a case processing summary model of the MSMEs’ response to the questionnaires administered. From Table , the question of lack of tax education being a factor affecting tax compliance was asked. Findings from the field survey indicate that a total of 145 respondents representing (72.5%) agreed to the fact that tax education is very crucial to tax compliance while 37 (18.5%) respondents disagreed with the question with 18 (9%) respondents remaining neutral.

Also, 150 (75%) respondents indicated that tax rates are too high and it affects the rate of tax compliance with 33 (16.5%) respondents disagreeing with the question. 17 (8.5%) respondents remained neutral to the question concerning the tax rate. Moreover, 81(40.5%) respondents responded to the question that high consumption affects tax compliance in the district as against 44 (22%) respondents who disagreed with the question. Whilst 75 (37.5%) respondents cannot tell whether high consumption affects tax compliance or not hence remains neutral to the question.

About the low level of income affecting tax compliance, 127 (63.5%) respondents agreed and 47 (23.5%) respondents disagreed with 26 (13%) remaining neutral. Also, the behavior of tax officials was recognized as a factor influencing tax compliance and when asked, 172 (86%) respondents agreed and 15 (7.5%) respondents disagreed with 13 (6.5%) respondents remaining neutral to the question. Finally, 160 (80%) respondents indicated they agree to the fact that the non-registration of businesses by business owners contributes to noncompliance. 22 (11%) respondents disagreed with this fact with 18 (9%) remaining neutral to the question.

A high percentage (72%) of respondents indicated that tax education is crucial. This implies that the majority of the MSMEs are not aware of their tax obligation in the study district. Besides, as high as 75% of respondents did indicate that the tax rate is too high and will have to be reviewed. Furthermore, 40% of the respondents admitted that, due to some factors such as large household size and extended family systems, a large amount of income goes into consumption. Moreover, the government does not support their (MSMEs) businesses financially, hence the level of income is always low.

Also, 88% of the respondents agreed (agreed and strongly agreed) that the non-registration of business affects tax compliance in the study area. This issue was attributed to the negative attitude towards tax payment and partly due to the behavior of the tax officials. This has contributed to the lack of business information about MSMEs at the institutional level. The few business owners who did register did not provide accurate information. With the issue of tax official poor behavior, respondents admitted that it can be minimized. The social psychology theory posits that, with regular interaction and visits, tax officials and taxpayers will eventually develop mutual trust that will improve compliance. Inasmuch as some of the economic factors reflect on the assumptions outlined by Trivedi and Shehata (Citation2005) in the economic deterrence theory, others such as non-registration and tax education are different in context. However, the points of intersection concerning influential factors are tax rates, level of incomes, and the willingness to maximize expected utilities. Considering the social factors, the social psychology theory by Noguera et al. (Citation2014), outlined perception, attitude, business morals, and ethical values as influential factors to tax compliance. The field observation also revealed attitude, perception, and moral values as mentioned in the social psychology theory.

7.4. Effectiveness of the tax administration

To ascertain how effective the tax administration in the district is, an interview was conducted with the district manager of Ghana Revenue Authority as well as the budget officer at the district assembly. Measurement of effectiveness with regard to this study: MSME income tax compliance included frequent monitoring and assessment, regular visits or meetings, frequent dissemination of tax information (tax laws, new rates, tax incentives, etc), staff strength and punctuality in office and number of cases recorded as non-compliance as well as the ability to implement the non-compliance law of offenses and their corresponding penalties. The interview conducted revealed that to some extent the tax administration in the district is not effective.

7.4.1. Mode and criteria of tax collection

Findings from the interview revealed that there was no criterion used to classify businesses or enterprises into micro, small and medium scales in the district especially those without files with GRA and the district assembly. Instead, with the GRA, they use the tax stump designed by the national tax authority for retailers and these were in categories of GH¢10.00, GH¢30.00, and GH¢ 45.00 for micro (petty traders), small and medium retailers respectively.

However, the tax stumps are not fixed; rather they keep changing from time to time. It was also realized that there was no threshold concerning income levels especially the micro-enterprises and the GRA mainly relies on their judgment to assess the micro-businesses for tax. Also, the tax stump is fading out of the system hence the GRA no longer uses it. But currently, the tax procedure or process in place is the ―temporal jacket”. The temporal jacket is done by assessing the businesses with some fixed amount to be paid as tax, monitoring them to ensure if there is sustenance without complaint, and then, compile their information to the national level for input processing after which taxation continuous. However, the businesses with files undergo the normal procedures of tax filings, assessment, and tax collection using the rates. The District Assembly uses a fixed-rate designed by the Ministry of Local Government and Rural Development in partnership with the Auditor Generals’ Department. The Assembly also collects taxes in the form of market tolls using fixed rates for all the scales of enterprises in the district.

This is however different compared to what has been found in the literature. The NBSSI classified all businesses into micro, small, and medium scale enterprises. These criteria of NBSSI included the size of the employees, ownership type, total capital base/assets, annual turnover, and market share of businesses with their thresholds. This has become the standardized criteria of classifying MSMEs. Unfortunately, the tax authorities in the study district do not utilize these standardized criteria for tax assessment and collection.

7.4.2. Frequent visit, monitoring and assessment

From the interview, it was revealed that the tax agencies do not carry out a frequent visit, monitoring, and assessment to all the MSMEs. This is because it was found that 42 (21%) respondents indicated they undertake their businesses by roaming and have never been taxed and also others (25) indicated they were not regular at their workshops. They carry out their business transaction by roaming. Also, findings from the field interview revealed that administering tax on the vocational and technical self-employed businesses such as the hairdressers, dressmakers, and local manufacturing firms is tedious due to their inconsistency at their workplaces. Hence they usually rely on their associations formed, to collect some set amount of money (subject to negotiation) from them through the executives of the associations as tax for the year. This is because they are not able to reach all the MSMEs since some operate in areas (houses) of which they do not have information about them. This hinders the tax administration and reduces expected revenue thereby restricting the government in providing the necessary facilities to enhance business activities and the general welfare of the citizens. Abdallah (Citation2008) noted that, concerning the course of the government and the determination of the parliament, the rationale in administering tax is to develop taxes in agreement with the standards and principles that will raise adequate revenues to meet the requirements of the state. He further explained that by so doing the administrators must embark on frequent visits, monitoring, and assessment to determine the foundation evaluation and procedure for the collection that is as easy, efficient, and reasonable as possible, and to build up auditing and other mechanisms.

7.4.3. Frequent dissemination of tax information (awareness creation)

Findings from the interview revealed that generally, the GRA does not carry out tax educational campaign at the district level because it is beyond their operational functions. Instructions or orders must come from the national headquarters or the regional office to permit the exercise of an educational campaign. This is posing a serious problem to the tax collection process because the majority of the MSMEs need awareness creation, explanation, persuasion, and examples to be convinced to pay their taxes. However, at the District Assembly level, the situation was a bit different. That is, the Assembly is a semi-autonomous body that has the right to carry out any form of an educational campaign to create awareness. But the Assembly was not able to do so due to inadequate finance. The study revealed that the cost of tax administration is always higher than the tax revenue when the Assembly embarks on tax educational campaign. However, the local media (FM station) is sometimes utilized but not very frequent usually once every year.

7.4.4. Staff strength and work schedules

Findings from the interview revealed that the staff strength at both the District GRA branch and the District Assembly was less, making the tax administration process ineffective in their operations. The administrative structure of the Ghana Revenue Authority at the district level is headed by the Sub-Manager followed by the cashier and finally the C.E.D.M Head as shown in Figure .

Figure 7. Structure of the tax administration authority in the district.

The required number of staff adequate to run the tax administration at the district level successfully is five and above because the district is large and it will ensure wide coverage in their operations. However, at the District Assembly level, the budget officer did indicate that they do employ about ten (10) temporal field officers to undertake the tax collection process on their behalf. But tax revenue does not improve because the field officers sometimes exchange the tax revenue for food items and other goods to themselves. Even though literature is silent on the required number of personnel at each branch office of the GRA at the district level, the size of the district and type of business undertaking in the district needs to be considered highly when recruiting and posting officials to the various district branch offices.

7.4.5. Penalty of fines and awareness of tax law by respondents

Triangulation was used as an approach or strategy to evaluate the intensity of responses and findings from the field survey. To establish how effective the tax administration is, respondents were interviewed using questionnaires on their awareness of the tax laws of the country and also determine whether they were fine whenever they show noncompliance. Findings from the field survey indicate that 199 respondents representing (99.5%) said they have any knowledge of the tax laws of the state while one respondent responded that he/she is aware of at least one tax law. On the other hand, 197 (98.5%) respondents indicated they were never fined as penalty even though they do not regularly pay tax or do not pay at all. While 3 respondents said they were fined for not paying their tax through the locking of their shops. This implies that the tax administration needs to be empowered and some policies reformed to ensure effectiveness and efficiency in their operations. From the foregoing discussion, it is obvious that considering the effectiveness of the tax administration, the study revealed that, the taxpayers lack the basic tax information that may motivate them to adhere to tax laws.

Also, frequent visits, monitoring, and assessment are a matter of concern. Besides, the institutions are experiencing low staff strength as well as not embarking the standardized criteria of classifying MSMEs and thereby carry out assessments accordingly. It was evident that, 99.5% of the respondent interviewed said they do not have any knowledge about the tax laws of the country. Meanwhile, Bird and Zolt (Citation2008) stated that a good and effective tax administration must have its tax laws to be simple, clear, known, and understandable to the taxpayer. This is not the practical case revealed through the interview in the study district. Respondents also indicated that they never experienced fine as a penalty even though do not submit their tax returns or pay any form of tax. Hence, it is obvious that the offenses and their penalties in tax administration as revealed in literature do not apply to them. Furthermore, as Udechukwu (Citation2003) indicated , the amount of tax to be paid ought to be certain, and based on a particular criterion and not arbitrary; however, this is not the case in the study district as revealed in this study. The tax authorities usually tax arbitrarily based on their discretion and judgment especially the micro and small scale traders or retailers in the district.

7.5. Challenges facing the tax administration

Several challenges were identified during the interview with the tax officials and the association executives of the MSMEs in the district which explains the difficulty involved in tax collection at the local level. These challenges identified impede the assessment and collection of MSME income tax.

7.5.1. Low institutional capacity and inadequate resources

Finding from the interview conducted shows that, both institutions in the district: the GRA and the NSDA are short of requisite resources in terms of qualified personnel and logistics for the effective operation of their duties. About the personnel, the GRA indicated they need an additional five field officers with a minimum qualification of Higher National Diploma (HND) in Accounting or Economics. The District Assembly indicated they need at least ten personnel with a minimum qualification of a secondary education as field officers. All the tax collection institutions do not have vehicles, engine motors, information and telecommunication gadgets, field attire for identification among others to carry out their duties effectively across the entire district. This has, therefore, adversely affected their assessment and collection of tax, frequent tax educational campaigns, and virtually rendered them ineffective and inefficient in their delivery.

7.5.2. Inadequate information on chargeable income

The relevant information or data needed for levying income tax were mostly non-existing because the field survey revealed that 124 (62%) MSMEs indicated they did not register their businesses and file for tax. Even instances where the well-established medium enterprises register and file for tax, whether data provided on their income statement is accurate and authentic remains another dicey issue. Besides, findings from the interview of the two institutions indicate that the MSMEs usually provide unreliable information on their businesses to the tax officials creating many inaccuracies to slow down their duties. According to the officials, this has manifested itself in various ways such as under valuation and under assessment of income tax leading to evasion. That is, tax officials are forced to assess the MSMEs for tax based on the inaccurate business information provided. This contributes to the low revenue mobilization and constraint socio-economic development of the nation.

7.5.3. Negative public attitude towards tax payment

During the interview, tax officials in both institutions lamented on the poor and negative attitude exhibited by individuals in the district towards tax payment. They indicated that, unless individuals require a tax clearance certificate which will compel such persons to voluntarily comply with tax payment, they do not see the need to do so. This negative attitude affects the operations of tax collection. The district budget officer explains that this negative attitude is more severe anytime the District Assembly prints stickers that would be sold to the people to raise funds for internal development.

Inference from the field survey on MSME response indicated a few reasons for such a negative attitude. Their concerns were that they do not see or feel the impact of the taxes paid to the government or the district assembly. Others expressed their concern by saying the government does not support their businesses hence do not see any reason for paying tax. Some said paying tax will reduce the business capital and also affect their income for consumption. It can be deduced from these two statements that, the MSMEs lack some vital tax information that needs to explain to them to enhance the rate of compliance and payment.

7.5.4. Lack of collaboration and co-operation between agencies

Another serious challenge identified which is contributing to low tax collection was the absence of joint operation by the tax institutions (GRA and the NSDA). In their operation, they lack co-operation and co-ordination as to how to form a linkage in their operation of tax collection and the ability to involve other departments such as the information service and the law enforcement agencies to assist in enhancing compliance. Both agencies were seen to be using different methods of assessing income tax thereby creating inconsistencies concerning taxes raised for stump duties. The District Assemblies’ rates of tax for the MSMEs differ from the tax rate used by the GRA on the same MSMEs in the district.

7.5.5. Political interference

Findings from the interview also revealed political interference as another challenging factor in the tax administration process in the district. Politics has more often intervened in the tax administration to grant favors to individual business owners believed to be party affiliate anytime a legal action is to be taken on them for noncompliance or any form of evasion. In the Nkwanta South district, the semi-autonomous revenue authority struggles to keep its operational autonomy because of political influence. There are instances where the sitting Member of Parliament or the District Chief Executive or even Party Chairperson intervene by granting bails, opened up locked shops for MSMEs, and also used their authorities and offices to exempt people believed to be party financiers in the district from paying tax. Clear evidence of this interference occurred when a party chairman intervened for 12 different MSMEs for failing to submit their tax returns and had their shops locked up.

8. Conclusion and policy recommendations

The objective of the study was to examine the compliance of MSMEs with income tax administration in the Nkwanta South District of Ghana. The study revealed that lack of tax education, non-registration, low incomes, high tax rates, and high consumption are the primary factors affecting compliance with income tax administration among MSMEs in the Nkwanta South District. The study found that there are no effective criteria for assessment and collection of tax revenue especially from the micro and small retailers in the district. Some challenges the tax administration is facing in the district included low institutional capacity and inadequate resources, inadequate tax information on chargeable incomes, negative attitude towards tax payment, and political interference. Hence, the Nkwanta South district’s inability to effectively mobilize internally generated funds (IGFs) can be partly attributed to noncompliance with tax administration by MSMEs in the district. This is because income tax is one of the components of the IGF in every MMDA. Based on this, policymakers and tax collection institutions in the district and Ghana as a whole need to bring to light urgent and realistic procedures to design tax policies and collection mechanisms to improve income tax adminstration. Therefore, we provide the following specific recommendations to enhance income tax compliance in the Nkwanta South District of Ghana.

8.1. There should be tax education and awareness campaign

The Ghana Revenue Authority and the Metropolitan, Municipal and District Assemblies (MMDAs) should design a tax education and awareness program that will run regularly to educate and sensitize taxpayers on issues such as tax incentive, tax exemptions, the general importance of paying tax and utilization of tax revenue among others. Such programs can be a quarterly forum for discussion on taxation, monthly dissemination of tax information regarding revenue collected and expenditures made on visible projects and undertaking tax programs on the local media station (FM station) by hosting the MSME executives and relevant stakeholders in the district to define clearly the usage of the tax revenue to quash the unappealing perception and negative attitude of people towards tax payment.

8.2. Auctioning the tax collection rights

The study recommends that the government should privatize the tax administration especially at the local level where assessment and collection of the tax dues by the state agencies are cumbersome. That is, the collection right and authority of taxation should be subjected to bidding among individual firms to buy. This, in effect, will encourage and serve as an incentive for higher assessment and increase collection rate. Ones the private firm is in control, it will ensure voluntary compliance with a little negotiation and neglect the conflict of interest that exists when the government is in control of the tax administration due to political considerations. It will also lead to a greater and more predictable revenue collection. The alternative to this view is that the government in collaboration with the Ghana Revenue Authority should intensify the effective implementation of the Tax Identification Number (TIN) in the country to ensure wider coverage of taxpayers. This will help to broaden the tax net to include all the MSMEs in the informal sector of the country. It will also resolve the problem of non-registration and non-filing of tax by micro and small business owners.

8.3. Tax administration by means of “association taxation”

The study also recommends group or association taxation method of tax collection especially in the rural areas of the economy. The strategy of ―identifiable group taxation‖ should be implemented by the government so that the tax authorities can deal with the taxpayers through their associations by dialogue, negotiation, and collection. The MSMEs in the Nkwanta South District have associations that exist in the form of Hairdressers, Dressmakers, Food vendors, Retailers Associations among others. It is therefore left onto the government through its revenue agencies to tax the required amount of revenue from the Association’s Fund so that the executives of the association will then distribute the amount taxed among its members. This will help to reduce the collection cost as well as improve compliance. This is because people at the local level feel comfortable working with the native men than the tax officials who are considered strangers in their area. Using the association for taxation, it will make members feel that becoming tax compliant will grant them some level legitimacy and this will help to avoid more arbitrary harassment by tax officials and other law enforcement agencies.

8.4. Streamlining or reorganizing tax administration into various segments

In order to strengthen monitoring, service, and evaluation for tax administrators, there is the need to recognize the tax administration at the local level to have separate departments in dealing with MSMEs based on their scale type. This stemmed from the fact that MSMEs differ in terms of scale and business type. Hence, the services provided should not be the same for all the firms with varying levels in size and activities.

Segmentation of the tax management will provide adequate or enough motivation for tax administrators to concentrate on each scale of the businesses in both revenue collection and provision of service to foresee their needs. Also, a Block Management System (BMS) should be adopted to promote compliance by registering all legible traders and business enterprises. This can be done by mapping the entire market area and dividing into small manageable blocks for a BMS team to move block by block to identify, register, educate and interact with business owners in the informal sector of the economy. This will help to increase the registration process for formalization and the widening of the tax base in the country.

8.5. The government must emphasize and ensure transparency, service, and engagement

Auditing, accountability, and the extent to which tax officials and agencies will exhibit transparency emphasizes and foresters some amount of voluntary compliance among the taxpayers at the local level of the country. Besides, the act of the government delivering well-defined benefits to taxpayers with the provision of resource support and services in the form of the provision of social amenities that will enhance taxpayers’ overall wellbeing and at the same time improve their business. This is a strategy to ensure tax compliance and it will help build a strong sentiment of patriotism and development of trust in the tax officials among taxpayers. Furthermore, the tax agencies and revenue collectors should communicate information on revenue and expenditure to the public especially the taxpayers from time to time to keep them informed on their contributions. This can be done by relating increases in tax revenue collected to some tangible or visible expenditure and developmental projects that will benefit the tax payers.

Additional information

Funding

Notes on contributors

Charles Peprah

Charles Peprah holds a PhD in International Development. He is a Senior Lecturer at the Department of Planning, KNUST. His research interest covers policy analysis, economic planning, and policy, public health, and health services research. His research mainly focuses on qualitative, quantitative, and mixed methods approach. He is a member of Ghana Institute of Planners and CIHCM. The authors of this research jointly investigate the compliance of MSMEs with income tax administration in the Nkwanta South District of Ghana.

References

- Abdallah, A. N. (2008). Taxation in Ghana, principles, practice and planning (2nd ed.) [ Unpublished]. Black mask publications.

- Abdul–Razak, N., & Adafula, C. J. (2013). Evaluating taxpayers attitude and its influence on tax compliance decisions in Tamale, Ghana. Journal of Accounting and Taxation, 5(3), 48–25 doi:10.5897/JAT

- Abor, J., & Quartey, P. (2010). Issues in SME Development in Ghana and South Africa. International Research Journal of Finance and Economics, 39(6), 215–228

- Agbadi, S. B. (2011). Determinants of tax compliance: A case study of vat flat rate scheme traders in the Accra metropolis (Master’s thesis), Kumasi, Ghana: KNUST.

- Ajzen, I., & Fishbein, M. (1977). Attitude-behavior relations: A theoretical analysis and review of empirical research. Psychological Bulletin, 84(5), 888. https://doi.org/10.1037/0033-2909.84.5.888

- Ankamah, S. S. (2012). The Politics of Fiscal Decentralization in Ghana: An Overview of the Fundamentals. Public Administration Research, 1(1), 172–220 doi:10.5539/par.v1n1p33

- Antony, J., Kumar, M., & Labib, A. (2008). Gearing six sigma into UK manufacturing SMEs: Results from a pilot study. The Journal of the Operational Research Society, 59(4), 482–493. https://doi.org/10.1057/palgrave.jors.2602437

- Armah, M. K., Brafo-Insaidoo, W., & Akapare, I. A. (2014). Trade liberalization and import revenue: Evidence from Ghana. Journal of Economics, Commerce and Management, 2(9),1-18.

- Atawodi, O. W., & Ojeka, S. A. (2012). Factors that affect tax compliance among small and medium enterprises (SMEs) in North Central Nigeria. International Journal of Business and Management, 7(12), 87. https://doi.org/10.5539/ijbm.v7n12p87

- Ayee, J. R. A. (2010). Good tax governance in Africa [Paper presented]. Workshop organized by the Centre for African Budget Initiative (CABRI) and the African Tax Association Forum (ATAF), Pretoria, South Africa.

- Babbie, E., & Mouton, J. (2004). The practice of social research (SA ed.). Cape Town.

- Bartole, T. (2012). The structure of embodiment and the overcoming of dualism: An analysis of Margaret Lock’s paradigm of embodiment. Dialectical Anthropology, 36(1–2), 89–106. https://doi.org/10.1007/s10624-012-9266-x

- Bird, R. M., & Zolt, E. M. (2008). Technology and taxation in developing countries: From hand to mouse. National Tax Journal, 61(4), 791–821. https://doi.org/10.17310/ntj.2008.4S.02

- Bird, R. M., & Zolt, E. M. (2013). Taxation, inequality and fiscal contracting in the Americas UCLA School of Law, Law-Econ Research Paper No. 13-14; Rotman School of Management Working Paper No. 2321868. SSRN. http://ssrn. com/abstract=2321868

- Bräutigam, D. A., & Knack, S. (2004). Foreign Aid, Institutions, and Governance in Sub‐Saharan Africa. Economic development and cultural change, 52(2),255-285. doi:10.1086/380592

- Bruijnzeels, M., Van der Wouden, J., Foets, M., Prins, A., & Van den Heuvel, W. (1998). Validity and accuracy of interview and diary data on children’s medical utilisation in the Netherlands. Journal of Epidemiology and Community Health, 52(1), 65–69. https://doi.org/10.1136/jech.52.1.65

- Conteh, C., & Ohemeng, F. L. K. (2009). The politics of decision-making in developing countries: A comparative analysis of privatization decisions in Botswana and Ghana. Public Management Review, 11(1), 57–77. https://doi.org/10.1080/14719030802493429

- De Paepe, G., & Dickinson, B. (2014). Tax revenues as a motor for sustainable development. Organisation of Economic Co-operation and Development (ed) Development co-operation report, 91-97.

- Denscombe, M. (2010). The good research guide for small-scale social research projects (4th ed.). Open University Press.

- Denscombe, M. (2014). The good research guide: for small-scale social research projects. McGraw-Hill Education (UK)

- Eagly, A. H., & Chaiken, S. (1993). The psychology of attitudes. Harcourt brace Jovanovich college publishers.

- Feld, L. P., & Frey, B. S. (2007). Tax compliance as the result of a psychological tax contract: The role of incentives and responsive regulation. Law & Policy, 29(1), 102–120. https://doi.org/10.1111/j.1467-9930.2007.00248.x

- Ghana Statistical Service (2014). 2010 PHC District Analytical Report. Central Gonja District, Government of Ghana.

- Hanlon, M., Mills, L., & Slemrod, J. (2007). An empirical examination of corporate taxnon-compliance. In A. J. Auerbach, J. R. Hines, & J. Slemrod (Eds.), Taxing corporate income in the 21st century. Cambridge University Press.

- Hanum, Z., & Hasibuan, A. A. (2019). Analysis of Factors Affecting Awareness in Reporting Tax Obligations in the Small And Medium Enterprises Sector in Lubuk Pakam District. In International Conference on Global Education (pp. 1793–1801).

- Hurmerinta-Peltomäki, L., & Nummela, N. (2006). Mixed methods in international business research: A value-added perspective. Management International Review, 46(4), 439–459 doi:10.1007/s11575-006-0100-z

- Inasius, F. (2019). Factors Influencing SME Tax Compliance: Evidence from Indonesia. International Journal of Public Administration, 42(5), 367–379 doi:10.1080/01900692.2018.1464578

- Joppe, G. (2000). Testing reliability and validity of research instruments. Journal of American Academy of Business Cambridge, 4(1/2), 49–54

- Kayanula, D. & Quartey, P. (2000). The Policy Environment for Promoting Small and Medium Sized Enterprise in Ghana and Malawi. Finance and Development Research Programme Working Paper. Journal of Economic Policy Analysis in Malawi, 116(8), 911–983

- Kessey, K. D. (1995). Financing Local Government in Ghana; Mobilization and management of Fiscal Resource in Kumasi (4th ed., p. 551). University of Dortmund, Germany: SPRING Centre

- Kirchler, E., Niemirowski, A., & Wearing, A. (2006). Shared subjective views, intent to cooperate and tax compliance: Similarities between Australian taxpayers and tax officers. Journal Of Economic Psychology, 27(4), 502–517. https://doi.org/10.1016/j.joep.2006.01.005

- Kirchler, E., Niemirowski, A. & Wearing, A. (2007). Shared subjective views, intent to cooperate and tax compliance: Similarities between Australian taxpayers and tax officers. Journal of Economic Psychology, 27(4), 502–17 doi:10.1016/j.joep.2006.01.005

- Kuug, S. N. (2016). Factors influencing tax compliance of small and medium enterprises in Ghana. (Master's thesis). University of Ghana, Accra, Ghana

- Kyale, S. (1996). Interviews: An introduction to qualitative research interviewing. Thousand Oaks, CA: Sage Publications

- Lewis, M. (1978). Situational Analysis and the Study of Behavioral Development. In L. Pervin and M. Lewis (Eds.), Perspectives in Interactional Psychology. New York: Plenum

- Martsolf, D., Courey, T., Chapman, T., Draucker, C., & Mims, B. (2006). Adaptive Sampling: Recruiting a Diverse Community Sample of Survivors of Sexual Violence. Journal of Community Health Nursing, 23(3), 169–182 doi:10.1207/s15327655jchn2303_4

- Mukhlis, I., & Simanjuntak, T. H. (2016). Tax compliance for businessmen of micro, small and medium enterprises sector in the regional economy. International Journal of Economics, Commerce and Management, 4(9), 116–126

- Nkwanta South District Assembly. (2016). The Composite Budget of the Nkwanta South District Assembly for the 2016 Fiscal year. Retrieved from https://www.mofep.gov.gh/sites/default/files/composite-budget/2016/VR/Nkwanta-South.pdf

- Noguera, J., Miguel Quesada, F., Tapia, E., & Llàcer, T. (2014). Tax compliance, rational choice, and social influence: an agent-based model. Revue Française De Sociologie (English Edition), 55(4), 765–804. https://doi.org/10.3917/rfs.554.0765

- Ohemeng, Frank L. K.., & Owusu, F. Y. (2015). Implementing a revenue authority model of tax administration in Ghana: An organizational learning perspective. The American Review of Public Administration, 45(3),343-364. doi:10.1177/0275074013487943

- Okpeyo, E. T., Musah, A., & Gakpetor, E. D. (2019). Determinants of Tax Compliance in Ghana. Journal of Applied Accounting and Taxation, 4(1), 1–14

- Orviska, M., & Hudson, J. (2003). Tax evasion, civic duty and the law abiding citizen. European Journal of Political Economy, 19(1), 83–102 doi:10.1016/S0176-2680(02)00131-3

- Ozuru, Y., Best, R., Bell, C., Witherspoon, A., & McNamara, D. (2007). Influence of Question Format and Text Availability on the Assessment of Expository Text Comprehension. Journal of Cognition and Instruction, 25(4), 399–438 doi:10.1080/07370000701632371

- Porcano, T. M. (1988). Correlates of tax evasion. Journal of economic psychology, 9(1), 47–67 doi:10.1016/0167-4870(88)90031-1

- Rhineberger, G., Hartmann, D., & Van Valey, T. (2005). Triangulated Research Designs – A Justification? Journal of Applied Sociology, 22(1), 56–66 doi:10.1177/19367244052200106

- Rochaa, E. A. (2014). The Impact of Business Environment on Small and Medium Enterprise Sector‘s Size and Employment: A Cross Country Comparison. International Journal of Business Management, 62(5), 267–401

- Sandmo, A. (2005). The theory of tax evasion: A retrospective view. National Tax Journal, 58(4), 643–663. https://doi.org/10.17310/ntj.2005.4.02

- Schuetze, H. J. (2002). Profiles of tax non-compliance among the self-employed in Canada: 1969 to1992. Canadian Public Policy, 28(2), 219–238. https://doi.org/10.2307/3552326

- Spence, L. J. (2007). CSR and Small Business in a European Policy Context: The Five “C”s of CSR and Small Business Research Agenda 2007. Business and Society Review, 112(4), 533–552 doi:10.1111/basr.2007.112.issue-4

- Spriggs, J. F., & Hansford, T. G. (2000). Measuring legal change: The reliability and validity of Shepard's citations. Political Research Quarterly, 53(2), 327–341 doi:10.1177/106591290005300206

- Swann, J. (2003). How science can contribute to the improvement of educational practice. Oxford Review of Education, 29(2), 253–268. https://doi.org/10.1080/0305498032000080710

- Sydney, H. (2012). The Development of Small Medium Enterprises and their impact to the Ghanaian Economy. Review of Business Management in Developing Countries, 43(5), 432–551

- Trivedi, V. U., Shehata, M., & dan Mastelman, S. (2005). Attitudes, Incentives, And Tax Compliance. Journal of Economic Psychology, 5, 371–384

- Udechukwu, F. N. (2003). Survey of small and medium scale industries and their potentials in Nigeria. In CBN Seminar on SMIEIS (pp. 2–11)

- Van der Vorm, A., Vernooij-Dassen, M., Kehoe, P., Rikkert, M., Van Leeuwen, E., & Dekkers, W. (2009). Ethical aspects of research into alzheimer disease. A European Delphi study focused on genetic and non-genetic research. Journal of Medical Ethics, 35(2), 140–144. https://doi.org/10.1136/jme.2008.025049

- Wadesango, N., Mutema, A., Mhaka, C., & Wadesango, V. O. (2018). Tax Compliance of Small and Medium Enterprises Through The Self-Assessment System: Issues and Challenges. Academy of Accounting and Financial Studies Journal, 22(3), 1–15

- Wainer, H., & Braun, H. I. (1988). Test validity. Hilldale, NJ: Lawrence Earlbaum Associates

- Yukselturk, E., & Bulut, S. (2007). Predictors for student success in an online course. Journal of Educational Technology & Society, 10(2), 71–83