?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Study examines the role of financial literacy and financial self-efficacy of individuals in explaining their behavior to have financial accounts. Study has used the questionnaire based survey and collected the data responses from 564 adults belonging to Sahiwal division. The binary logistic regression model is utilized to estimate the probability of having financial accounts in relation to individual’s financial literacy and financial self-efficacy level. Estimated results show that individual’s financially literacy level is positively related with individual’s account ownership model among the selected group. While individual’s financial self-efficacy level does not explain any positive significant impact on individual’s account ownership model. Other socio-demographic variables like gender, marital status, education, occupation, and income level are also found to have influential impact on the individuals’ account ownership behavior in Pakistan. Study recommends that financial literacy is pertinent to have equitable financial inclusion in the economy.

PUBLIC INTEREST STATEMENT

Financial inclusion became the most important determinant for inclusive economic growth world widely and got the attention of policy makers in economies especially in developing economies like Pakistan. We investigate the impact of financial literacy and financial self-efficacy on financial account ownership behavior in Pakistan. Financial literacy in individuals stimulates better emotional state of authorization and informed judgment regarding finance choices. Estimated results show that financial literacy leads to increase the financial inclusion across all segments of society irrespective of age, sex, marital status, occupation, income, and geographical location. The present study is an attempt at academia level, to understand, support, and contribute toward “The National Financial Inclusion Strategy (NFIS),” implemented by State Bank of Pakistan (SBP) in collaboration to Government of Pakistan.

1. Introduction

Financial inclusion refers to have an account in recognized financial organization which enables people to formally save, borrow cash, to have insurance and to use payment services (Allen et al., Citation2016). Financial inclusion mobilizes a large chunk of savings and encourages the investors to take risk and invest more and thus contribute to economic growth. It helps in making more accurate and more faster transactions in bulk, that increases the economic growth (Sapovadia, Citation2017). It helps to access to bank deposits enabling the individuals to save and invest in a safer environment. It reduces the poor household’s vulnerability to adverse income shocks. Wider access to finance enables both producers and consumers to make timely transactions and raise their welfare status (Naveen K Shetty & Veerashekharappa, Citation2009). Financial inclusion further facilitates the all types of foreign inflows either remittances or bonds or portfolio or direct investment. (Alfaro et al., Citation2004; Jayaraman et al., Citation2018; Toxopeus & Lensink, Citation2008). While lack of financial inclusion may lead to continuous income inequality, enhance poverty level, and lower economy growth (Demirgüç-Kunt & Klapper, Citation2013).

A well-developed, sound financial system of an economy ensures access and use of hurdle-free financial services such as account ownership, savings, borrowings, money transfers, and payments to people who are not involved in formal financial system (Cámara & David, Citation2015). Financial inclusion also promotes financial stability by strengthening the financial institutions (Cull et al., Citation2012). Financial inclusion helps in broadening the markets for financial service providers. It helps to allocate the funds efficiently among the competing users. It reduces the risk via providing a good portfolio diversification of services including insurance (Din et al., Citation2020; Mohy Ul Din et al., Citation2017). It is revealed that broadening the financial credit to large chunk of enterprises reduces the probability to have the nonperforming loans and being defaults among the financial institutions, thus promotes financial stability (Morgan & Pontines, Citation2014).

Literature revealed that about 50% of total adult population (i.e. 2.2 billion) is banked while rest 50% of them are unbanked (Cull et al., Citation2013; Demirgüç-Kunt & Klapper, Citation2013). Almost 62% of worldwide unbanked adults (nearly 2.2 billion) belong to Africa, Asia, Latin America, and Middle East, of which 1.5 billion belong to East and South Asia (Cull et al., Citation2013). According to World Bank report 2015, South Asia has very low level of financial inclusion (46%) as compared to East Asia and Pacific (69%) (World Bank, Citation2015). Among South Asian countries, Pakistan has low level of financial inclusion, i.e. 11–13% as compared to Sri Lanka (82%), India (53%), and Bangladesh (31%) (Mani, Citation2016) (Table ).

Literature evidenced that there is a strong relationship exists among financial development, financial inclusion and inclusive economic growth of developing countries (Thorsten Thorsten Beck et al., Citation2009; Kefela, Citation2010; L. F. Klapper & Panos, Citation2012; L. Klapper & PANOS, Citation2011). Therefore, a large number of developing economies are continuously making efforts in order to increase the financial access of people to financial services but somehow these efforts remain unsuccessful in terms of reach towards the potential level (Demirguc-Kunt et al., Citation2015). The obstacles on this way are both supply side and demand side in nature as suggested by (Beck & De La Torre, Citation2007).

The supply side barriers include weak financial infrastructure, legal and regulatory barriers, lack of competition, gender biases in financial institution practices, and inadequate provision of financial products according to customers’ needs (T Beck et al., Citation2009; Cámara et al., Citation2017; CCmara & Tuesta, Citation2015; Kumar et al., Citation2019; Nandru et al., Citation2016; Sarma, Citation2012). While on a demand side, economic reasons such as lack of money and personal factors such as individual’s lack of financial knowledge, lack of self-confidence, cultural, and gender norms restrict the individual for demanding financial products or services (Beck & De La Torre, Citation2007; Demirguc-kunt & Klapper, Citation2012; Ghosh & Vinod, Citation2017). The personal reasons include individual’s lack of financial knowledge, lack of self-efficacy or confidence, and individuals own feeling that they do not require financial services. Likewise in Pakistan, it is observed that around 53.8% of the individuals consider income and heavy documentation is the main hurdle of unbanked, while half of the population, i.e. around 50.7 percent of people are unbanked due to their personal reasons (Nenova & Niang, Citation2009; Nenova et al., Citation2009).

Table results evidenced that main reason of unbanked in Pakistan is either individuals have not enough financial capabilities or they are not fully aware of the potential benefits of being financially included in the system, i.e. demand side factors (Ghaffar & Sharif, Citation2016; Mindra & Moya, Citation2017; Mindra et al., Citation2017), or financial system is unable to understand the needs of the individuals and unable to respond it accordingly, i.e. supply side factors (Miller et al., Citation2009). Thus it is pertinent to investigate the underlying causes in bringing up the vulnerable group of individuals into inclusive financial market.

Table 1. Financial inclusion across South Asian countries (Percentage of adults)

Table 2. Barriers to financial inclusion in Pakistan

Although a number of studies have studied the financial inclusion in context of Pakistan (Kemal, Citation2019; Kumail Abbas Rizvi et al., Citation2017; Shaikh et al., Citation2017; Zulfiqar et al., Citation2016). Almost all of them remain focused on the supply side factors, and hardly none of the one has examined the role of demand side factors such as financial capabilities including financial literacy and financial self-efficacy. Building on this research gap, the present study is intends to study the individuals’ financial literacy, and financial self-efficacy in explaining the their behavior to have the financial accounts in Pakistan.

So the underlying objectives are as follows:

✓ To study the relationship between individual’s financial literacy level and financial account ownership behavior in Pakistan.

✓ To study the relationship between individual’s financial self-efficacy level and financial account ownership behavior in Pakistan.

✓ To study the mediation impact of individual’s financial self-efficacy level on the relationship between financial literacy and financial account ownership behavior in Pakistan.

There are two main contributions: first, study has examined the role of financial literacy and financial self efficacy in explaining the individual’s behavior to have formal financial accounts. Second, study contributes in terms of study area selection. The earlier conducted surveys such as SBP Access to Finance (A2F) Survey conducted in year 2008 and in year 2015, both were undertaken in large cities such as Islamabad, Lahore, Karachi, and Faisalabad while small cities were ignored. However studying small divisions are also important to bring forth the equitable financial inclusion in limited areas as well. The present study had been undertaken in Sahiwal division that includes three relatively small districts named Sahiwal, Okara, and Pakpattan. The study will help to identify the problems of financial account ownership in these areas and thus will contribute in policy formulation at national level. The paper is organized into five sections. Section 2 provides a brief literature review; Section 3 elaborates on the data, model and method used; Section 4 discusses the empirical results and findings; and Section 5 concludes the discussion and provides policy implications stemmed from this analysis.

2. Literature review

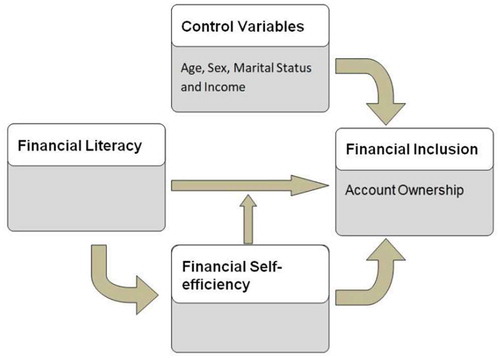

According to Sen’s Capability approach, all forms of capabilities are important for individual’s functioning achievement that in turn enhances their well-being (Robeyns, Citation2003, Citation2006; Sen, Citation2007). Evans (Citation2002) states that individuals have many resources whose values are only recognized when they have the capabilities to transform them into valuable products. He found that the interrelated capabilities within individuals affect their well-being outcomes (Evans, Citation2002). The underlying study derived the theoretical framework based on Sen’s capability approach (Sen, Citation2007) and examined the relationship between financial capabilities including financial literacy and financial self-efficacy on individual’s account ownership behavior (Figure ).

Financial inclusion is defined as inclusion of people into the formal financial system. It enables the people to have an account in banks which further encourage them to save, borrow, and transfer money officially (Serrao et al., Citation2012; Zins & Weill, Citation2016). However, the actual realization of benefits being formally financially included depends upon individuals financial capabilities. Financial capabilities such as financial literacy and financial self-efficacy enables individuals to make better economic decisions, raise their rights and responsibilities by using the financial services, and to know and manage risk and return efficiently (Maslow, Citation1943). For example, capabilities regarding financial management skills such as financial literacy and financial self-efficacy are the abilities that motivate the individuals for well managing of their lifetime events such as housing, education, illness, marriage, or retirement planning through financial inclusion (Ghaffar & Sharif, Citation2016; Mindra et al., Citation2017).

Financial literacy refers to as information, awareness, and knowledge of the people about financial products, institutions, and terms related to everyday decision making like interest rate, inflation, savings, borrowings, risk, return, etc.; and practical know how about financial products and terms (Lusardi & Mitchell, Citation2011; World Bank, Citation2013). World is facing recession, high food and fuel costs, bankruptcy, credit contraction, and harsh drop in savings. These stressors affect the people, families, and societies. So, sound financial decisions and safety in a frighteningly difficult world requires the individuals to must have knowledge about their personal finance and develop their money management skills (Mccormick, Citation2009). Because individual’s informed financial decision can increase risk sharing, decrease economic instability, improve intermediation, and enhance inclusive financial system (Cole et al., Citation2011). In low-income economies, formal financial access is limited and only a few percentages of people have access to sophisticated financial products, e.g. bank account, savings, and borrowings due to limited financial knowledge even among the entrepreneurs (Akudugu, Citation2013; Xu & Zia, Citation2012). Barbić et al. (Citation2016) also confirmed that individuals do not use the financial products because of less financial knowledge and skills (Barbić et al., Citation2016). Kostov et al. (Citation2015) found that the individuals need basic knowledge even to open and own an exclusive financial account, that is rare in most cases (Kostov et al., Citation2015). Similarly, Bongomin et al. (Citation2016) concluded financial literacy is important because it can empower the poor to evaluate, compare financial products, and make informed financial choices and decisions (Bongomin et al., Citation2016). Financial literacy may help in decision making process, and may improve the saving rates and credit worth of debtors and consequently results into more financial access and utilization of financial products (Bongomin et al., Citation2016). Thus, financial literacy is assumed to be here a great predictor of behavior toward having a formal financial accounts and also help to alleviate the undesirable factors of financial inclusion like lack of trust, documents, and money as discussed by (Akudugu, Citation2013; Lotto, Citation2020).

Financial Self-Efficacy is the level of confidence an individual has on his ability to access, use financial products or services, undertake a financial decision, and deal with the complex financial situation (Amatucci & Crawley, Citation2011; Ghosh & Vinod, Citation2017). Financial self-efficacy is related to social cognitive theory, which states that perceptions of self-efficacy influences every facet of individual’s lives containing their objectives, their choices and their determination in achieving tasks, positive or negative patterns of thought and the measure of their persistence in facing problems. Also, individual’s recognition of self-efficacy influences how to perform, think, feel, and self-motivate themselves (A. Bandura, Citation1991, Citation2005). It is observed that over the years the self-efficacy variable truly mediates the relationship between several variables and desired action executions in particular domains. As self-efficacy due to its greater predictive power influences individual tasks or choices directly when it is domain-specific and to perceive positive outcomes indirectly that individuals frequently expect. And individual desired behavior can be acquired and regulated based on their self-efficacy in order to obtain a certain outcome (A. Bandura, Citation1977, Citation2005). Families and school provide formal as well as informal environment whereas parents and teachers teach them skills, develop confidence, and understandings of what is acceptable behavior. Thus, it is essential to build knowledge and confidence to make decisions (Danes & Haberman, Citation2007). Further, individuals with sufficient financial knowledge and information are self confident of on their capabilities in making successful transactions. Besides, self-efficacy also indirectly played a helpful role in the procedure of cognitive thinking to achieve desired action driven by the willpower apart from the skills individuals endowed (Hejazi et al., Citation2008).

Figure 1. Research framework.

2.1. Research hypotheses

Based on literature, this study develops hypotheses as follows:

H1: There is a significant positive relationship between financial literacy and financial account ownership behavior.

H2: There is a significant positive relationship between financial self-efficacy and financial account ownership behavior.

H3: There is a significant positive relationship between financial literacy and financial self-efficacy level.

H4: Individual’s financial self-efficacy level mediates the relationship between individual’s financial literacy level and financial account ownership behavior.

Individual socio-demographic characteristics such as gender, marital status, education, income, andlocation are also expected to influence the financial inclusion; therefore included in the analysis (Atinc et al., Citation2011; Park & Mercado, Citation2015; Zins & Weill, Citation2016). Besides, occupation needs also encourage the individuals to be involved in formal financial system, therefore also included in the analysis (Nandru et al., Citation2016).

3. Study settings and design

The study used the cross sectional research design to examine the relationship among the underlying variables at a specific point in time (Sedgwick, Citation2014). The target population for the study consists of all adult individuals both having and non-having financial accounts belonging to 20+ year’s age group, in Sahiwal, Okara, and Pakpattan. Study surveyed the respondents through a self-administered questionnaire and collected the required data information from the respondents. The questionnaire instrument is built keeping in review all ethical standards and finally approved by the Research ethics committee at COMSATS University Islamabad, Sahiwal Campus.

The developed questionnaire consists of questions related to the socio-demographic characteristics of the individual, financial inclusion, financial literacy and financial self-efficacy. Furthermore, study used the purposive sampling technique to select the sample units, i.e. individuals (Palys, Citation2008). A sample of 564 respondents was considered, that is enough to represent the target population of Sahiwal Division, Pakistan (Pallant, Citation2011). A brief introduction related to the main purpose of this survey and its information utilization is provided to the surveyed respondents. Besides, respondents have given the free choice either to participate or not participate in the survey. Respondents are assured and clarified that the collected information will be utilized only for the academic purposes and will not be shared with anyone for some other purposes. Thus study followed the all ethical standards set by the Ethics Review Committee at COMSATS University Islamabad, Sahiwal Campus.

3.1. Measurement

3.1.1. Financial inclusion

Financial inclusion variable is defined as a dichotomous binary variable (i.e. if having an account Y = 1 and Not having an account Y = 0). While socio-demographics variables are defined on categorical and nominal scale (Pakistan Economic Survey, Citation2015) (Table ).

3.1.2. Financial literacy

Financial literacy’s scale was adopted (Mindra & Moya, Citation2017; World Bank, Citation2015). It consists of 8 items and responses are collected on five point likert scale from “strongly disagree” to “strongly agree.” The construct is reliable as its computed Cronbach’s alpha score and composite reliability score are 0.907 and 0.902 respectively i.e. greater than of 0.7 value (see Table ).

Table 3. Measurements of variables

Table 4. Reliability analysis

3.1.3. Financial self-efficacy

Financial self-efficacy’s scale items are also adopted from (Ghosh & Vinod, Citation2017; Mindra & Moya, Citation2017). It consists of eight items and measured on 5- point likert scale ranged between “Not at all true” to “Exactly true.” The computed Cronbach’s alpha score and composite reliability score are 0.904 and 0.908 respectively. Both scores are found to be greater than 0.7, thus showing and validating the reliability of the construct.

Study defined the financial inclusion in terms of individual’s financial account ownership. It is a dichotomous variable, having two discrete outcomes: (1) Individual has a formal financial account ownership and (2) individual does not have a formal financial account ownership. Study used the binary logistic regression as the most suitable technique in case of binary nature dichotomous dependant variable (Baron & Kenny, Citation1986).

The logistic regression model was estimated as follow:

Where i = 1,2,3 … n

is the log of the odds ratio in favor of individuals having a formal financial account in a financial institution, i.e. the ratio of the probability that an individual will have a formal financial account (pi) to the probability that it will not have a formal financial account in a financial institution

. In this way, the dependent variable Yi represents the “financial inclusion” that assumes two values: (1) Y assumes value ”1,” if the person has a formal financial account in a l financial institution; and (2) Y assumes value “0” if the person do not has a formal financial account in a financial institution. The logistic regression estimation also provides the odd ratios. For example, if the estimated odd ratio pi = 0.8, it means that odds are “4” to “1” in favor of having an account to not having a account. While βo is the intercept; βi is the coefficient of the independent variable Xi (Brooks, Citation2008; Greene, Citation2012). Study examined the financial literacy and financial self-efficacy impacts on the dependent variable along with related socio-demographic factors such as gender, marital status, education, and income (see Table ). The collected data set was analyzed by using SPSS descriptive analysis, correlation analysis and logistic regression model.

Table 5. Variables specification and measurement

4. Results and discussion

4.1. Socio-demographics characteristics and financial inclusion (account ownership)

Table gives a summary of the socio-demographic details of the 564 respondents selected in this study. Respondents were categorized on marital status, gender, residence, age, education, occupation, and income basis. There were 322 males and 242 females in the selected sample. Among males 64% of respondents were found to have financial account and among females only 42% of respondents were found to have the financial accounts. About 55% of married respondents and 53% of unmarried were found to have the formal financial accounts. The respondents were selected from both urban and rural area of Sahiwal division. 301 respondents are belonged to urban area, while 263 respondents are belonged to rural areas. About 58% of the respondents belonging to the urban area were found to be financially included, while relatively less, i.e. 50% of the respondents belonging to rural area were found to have the formal financial accounts (see Table ). Respondents were also categorized on the basis of age as well. There were 303 respondents who aged between 20 and 30 years and 50% of them were financially included. While 204 respondents who aged between 31 and 40 years, about 57% of them were financially included; 46% of respondents who aged between 41 and 50 years, about 63% of them were found to be financially included; while only 11 respondents who were aged above 51 years were found to be financially included. It implied that the respondents who were belonged to higher age group were more financially included as compared to the respondents who were belonged to lower age group (see Table ). It may be because that people belonging to higher age groups were well settled, have permanent source of income and financially sound profession, and thus majority of them had the formal financial accounts.

Table 6. Financial inclusion and exclusion across socio-demographic group

Study also classified respondents on the basis of education i.e. less educated, educated and highly educated class. Data results show that majority (83%) of the respondents who belonged to uneducated class do not have financial accounts. While among educated class about 48.9% of respondents and among highly educated classes about 73.6% of respondents were found to have formal financial accounts. It means education level exerts positive impact on financial account ownership behavior. Respondents were also categorized on the basis of their occupation. There were about 233 respondents who were formally employed, 142 respondents were informally employed, 120 respondents were unemployed, and 69 respondents were students. Among 233 formal employed respondents, about 78% of respondents are financially included, on the contrary, among 142 informal employed respondents, 45 % of them are financially included. Similarly, among 120 unemployed respondents, only 23 % respondents are financially included and among 69 students only 46 % of them were financially included. It implies that people who are formally employed, i.e. salaried class maintain the financial accounts.

Income levels also explain the extent of financial account ownership behavior among the respondents. It is revealed that respondents who belonged to lower income groups (Rs. 0–30,000) were relatively less financially included (about 40.3% of them) as compared to those who belonged to the higher income group categories (see results in Table ) On average, the financial inclusion is turned out to be 54.4% in Sahiwal division, which is relatively higher than other areas in Punjab Pakistan.

Descriptive statistics of variables are shown in Table . The computed average financial literacy score is about 3.96 for selected sample, it implies that on average all respondents are financially literate. The means score of financial self efficacy is turned out to be 4.04, it implies that all respondents have good financial confidence as well. Data normality is tested by skewness and kurtosis. The skewness values of all variables lie between +1 and −1 and kurtosis values lie between +2 and −2. Results show that underlying data collected on financial inclusion (account ownership), financial literacy and financial self-efficacy belongs to normal distribution.

Table 7. Descriptive statistics and data normality results

The Pearson correlation coefficients results revealed the significant positive linear association between financial literacy and financial account ownership behavior. Similarly, estimated results revealed significant positive linear association between financial self-efficacy level and financial account ownership (see Table ).

Table 8. Correlation analysis

4.2. Estimated logistic regression results

Estimated results report significant positive (b = 1.499, SE = .19, OR = 4.48) impact of financial literacy level on financial account ownership behavior. The estimated odd ratio of financial literacy variable is 4.48, which indicate that the more financially literate a person, the more possibility he/she is to have a bank account ownership by a factor of 4.48, all other factors being equal (see Table ).

Table 9. Dependent variable (financial inclusion in terms of account ownership)

Similarly, gender (if a person is male), marital status (if a person is married), education (if a person is highly educated), Occupation (if the person is formally employed) and income (if a person earns higher than 30,000 rupees) are significant predictors of explaining the financial account ownership behavior at 5% level of significance. Also, the estimated odds of a person who is a male are more (about 2.28 times more) than a female person. This is a clear cut gender gap problem. Country’s female labor force participation is very low i.e. only about 25% even among the educated women. They prefer to remain in their houses, and do not want to work. Since they are not employed in formal sector, they do not earn regular income and so not having the financial accounts. In short, females in Pakistan are less financially included mainly because of the male dominant system of the society (SBP Financial Access Survey Citation2015). They have been kept behind men in each and every sphere of life; therefore have less education, less formal employment, less income, less knowledge of financial products and less financial self-efficacy levels. World Fact Book (Citation2017), also confirmed that females are financially excluded mainly because of two reasons: First, cultural and religious norms they keep around them. Second are the institutional factors. Study results coincide to the earlier studies results, that recognized the gender gap is a worldwide phenomenon (Almenberg & Dreber, Citation2015; Demirguc-Kunt et al., Citation2015; Ghosh & Vinod, Citation2017; Kairiza et al., Citation2017; Nanziri, Citation2016).

Another important socio-demographic variable is the individual’s marital status that has significant impact on financial inclusion. The odd ratio associated with marital status indicates that person who is married having account 1.82 times more than the unmarried person. It is true because after a certain age, when person have stable income flow then intend to save for her family, children, education, other needs, etc. empirical findings are consistent to the studies conducted by (Demirgüç-Kunt et al., Citation2013; Hilary et al., Citation2017; Kumar, Citation2013; Lotto, Citation2018; Love, Citation2010).

Education has also significant impact on financial account ownership behavior at 5% level of significance. Odd ratios comparison of highly educated (2.58), educated (1.24) in comparison to less educated (i.e. primary educated) respondents indicate that educated and highly educated people are more like to have financial accounts in comparison to the less-educated respondents. It suggests that when person become highly educated, his probability to be included in the proper financial system increases.

Estimated results show that the occupation also has a significant determinant for financial account ownership behavior. The odd ratios comparison associated with formal (3.06), informal employed (0.96), and unemployed (1.34) indicates that formally employed people are more (three times more) likely to be involved in financial inclusion than informally employed and unemployed people. It may be because formally employed people have financial accounts to receive their incomes. While the people who are informally employed, they have irregular patterns in their income, so they do not maintain the financial accounts most often. Similarly the unemployed persons, they lack money to have financial accounts.

Income level is also an important determinant to financial account ownership model in an economy. Estimated odd ratio associated with high income class is 5.626, that imply the odd chances of having a financial account is about five times more for high income individual than a person belonging to the low income class. Similarly the average probability to have the financial account is twice for a person who is earning income between 31,000 and 60,000 rupees than a person who is earning below 30,000. So it is revealed that with the rise in income level, the tendency to have the formal financial accounts rises among the selected respondents, or we can say that people who have high earnings are more like to be involved in financial inclusion than low earning people and they all are marginally significant. Study results are in line with the earlier studies (Demirguc-Kunt et al., Citation2015; Zulfiqar et al., Citation2016).

Following the Mindra and Moya (Citation2017) study, we also tested for the indirect mediation impact of financial self efficacy level on the relationship between financial literacy and financial account ownership model (see Table ).

Table 10. Dependent variable (financial self-efficacy)

R2 is 0.225; Model F statistics is also significant at 5% level of significance.

Although study found a strong positive impact of financial literacy on financial self-efficacy (b = .38, t = 12.79, p = 0.00), but we found no mediation impact of financial self-efficacy level on the relationship between financial literacy and financial account ownership model (see Table ). We have also tested the mediation impact significance using the Sobel test (Preacher & Leonardelli, Citation2001). Estimated results indicate that there is no significant mediation impact of financial self-efficacy found on the relationship between the financial literacy and the financial account ownership behavior (see Table ).

Table 11. Mediation impact of financial self- efficacy on financial literacy and financial inclusion relationship

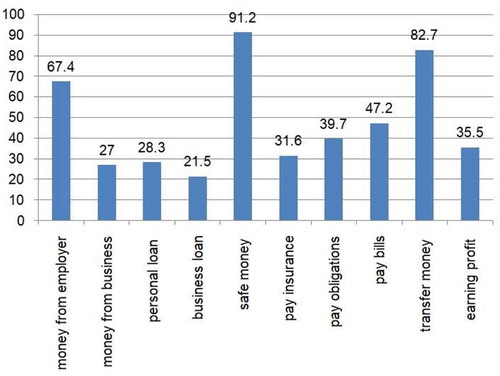

It may be true because we measured the financial inclusion in terms of just having financial accounts. Our survey results show that majority of the respondents have financial accounts just to keep the money safe (about 91%)); to transfer and receive money from the people living abroad (83%); to receive salaries (67%) and to earn profit (36%) from fixed deposits (see Figure ). While financial self efficacy does play a role in financial inclusion in terms of usage and quality of financial accounts as defined by Mindra and Moya (Citation2017). And financial self-efficacy do not have impact on just to have the financial accounts as shown in the estimated results reported in Table , where individual’s financial self-efficacy has shown no significant direct impact (b = .18, SE = .18, OR = 1.199) on financial account ownership model.

Figure 2. Purpose of having financial accounts in Sahiwal division (Source: Author’s survey).

5. Conclusion and policy implications

Financial inclusion has a great importance for the economy’s inclusive growth worldwide and it became a policy part of many economies especially developing economies. For this purpose, many developing economies are trying to increase the financial inclusion focusing on both supply side and demand side determinants. The sole responsibility of supply side factors, i.e. provision of easy and reliable formal financial products and services to a large number of people within an economy remains with the regulatory authority bodies of the financial sector, while demand side factors, e.g. individual’s personal capabilities such as financial knowledge, belief, and financial self efficacy of the individual to acquire and use the financial services. The present study has investigated the impact of financial literacy and financial self-efficacy on financial account ownership behavior in Pakistan. We have measured the individual’s financial inclusion in terms of having a financial account in a financial institution. Estimated results show that the financial literacy has a strong positive impact on financial account ownership behavior. However, financial self efficacy does not play a significant role in financial account ownership model. Actually people in Pakistan own financial accounts normally to receive salaries, to receive loans and to make payments, and financial self-efficacy, i.e. individuals self-confidence related to the usage of financial products does not matter here. All other variables like age, marital status, occupation, income also explain the individual account ownership behavior.

Study recommends that financial literacy leads to increase the financial inclusion across all segments of society in Pakistan irrespective of age, sex, marital status, occupation, and income and geographical location. Financial literacy in individuals stimulates better emotional state of authorization and informed judgment regarding finance choices. The study contributes to the National Financial Inclusion Strategy (NFIS) that was implemented by State Bank of Pakistan (SBP) in collaboration to Government of Pakistan.

Acknowledgments

All views and opinions expressed in this paper solely belong to authors. There is no responsibility lies with the Department and University.

Additional information

Funding

Notes on contributors

Irem Batool

The present research is the joint collaborative efforts of the authors. Ms. Nimra Noor is a MS scholar at Department of Management Sciences, COMSATS University Islamabad Sahiwal Campus. She has conducted this research for her MS dissertation under the supervision of Dr. Irem Batool. Dr. Irem Batool is working as an assistant professor at Department of Management Sciences, COMSATS University Islamabad, Sahiwal Campus since 2012. She obtained her PhD degree in Economics from Technical University Braunschweig at Germany. Previously she had also worked with Monetary Policy Department and Research Department at State Bank of Pakistan (Pakistan Central Bank), Karachi. She used to work on multidimensional microeconomic and macroeconomic issues specifically relating to Pakistan Economy.

References

- Access to Finance Survey: A2F Survey. (2015). State Bank of Pakistan. Retrived from https://www.cia.gov/library/publications/download/download-2017/index.html

- Akudugu, M. (2013). The determinants of financial inclusion in Western Africa : Insights from Ghana. Research Journal of Finance and Accounting , 4(8), 1-9. https://www.iiste.org/Journals/index.php/RJFA/article/view/6688

- Alfaro, L., Chanda, A., Kalemli-Ozcan, S., & Sayek, S. (2004). FDI and economic growth: The role of local financial markets. Journal of International Economics, 64(1), 89–112. https://doi.org/10.1016/S0022-1996(03)00081-3

- Allen, F., Demirguc-Kunt, A., Klapper, L., & Martinez Peria, M. S. (2016). The foundations of financial inclusion: Understanding ownership and use of formal accounts. Journal of Financial Intermediation, 27(C), 1–30. https://doi.org/10.1016/j.jfi.2015.12.003

- Almenberg, J., & Dreber, A. (2015). Gender, stock market participation and financial literacy. Economics Letters, 137, 140–142. https://doi.org/10.1016/j.econlet.2015.10.009

- Amatucci, F. M., & Crawley, D. C. (2011). Financial self-efficacy among women entrepreneurs. International Journal of Gender and Entrepreneurship, 3(1), 23–17. https://doi.org/10.1108/17566261111114962

- Atinc, G., Simmering, M. J., & Kroll, M. J. (2011). Control variable use and reporting in macro and micro management research. Organizational Research Methods, 15(1), 57–74. https://doi.org/10.1177/1094428110397773

- Bandura, A. (1977). Self-efficacy: Toward a unifying theory of behavioral change. Psychological Review, 84(2), 191–215. https://doi.org/10.1037//0033-295x.84.2.191

- Bandura, A. (1991). Social cognitive theory of self-regulation. Organizational Behavior and Human Decision Processes, 50(2), 248–287. https://doi.org/10.1016/0749-5978(91)90022-l

- Bandura, A. (2005). The evolution of social cognitive theory. In K. G. Smith, & M. A. Hitt (Eds.), Great Minds in Management (pp. 9-35). Oxford: University Press.

- Barbić, D., Palić, I., Bahovec, V., Palić, I., & Bahovec, V. (2016). Logistic regression analysis of financial literacy implications for retirement planning in Croatia. Croatian Operational Research Review, 7(2), 319–331. https://doi.org/10.17535/crorr.2016.0022

- Baron, R. M., & Kenny, D. A. (1986). The moderator-mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6), 1173–1182. https://doi.org/10.1037/0022-3514.51.6.1173

- Beck, T., & De La Torre, A. (2007). The basic analytics of access to financial services. Financial Markets, Institutions and Instruments, 16(2), 79–117. https://doi.org/10.1111/j.1468-0416.2007.00120.x

- Beck, T., Demirguc-Kunt, A., & Honohan, P. (2009). Access to financial services: measurement, impact, and policies. The World Bank Research Observer, 24(1), 119–145. https://doi.org/10.1093/wbro/lkn008

- Beck, T., Demirgüç-Kunt, A., & Honohan, P. (2009). Access to financial services: Measurement, impact, and policies. The World Bank Research Observer, 24(1), 119–145. https://doi.org/10.1093/wbro/lkn008

- Bongomin, G. O. C., Ntayi, J. M., Munene, J. C., & Nabeta, I. N. (2016). Social capital: Mediator of financial literacy and financial inclusion in rural Uganda. Review of International Business and Strategy, 26(2), 291–312. https://doi.org/10.1108/ribs-06-2014-0072

- Brooks, C. (2008). Introductory Econometrics for Finance (2nd ed.). Cambridge University Press. https://doi.org/10.1017/cbo9780511841644

- Cámara, N., & David, T. (2015). Factors that matter for financial inclusion: Evidence from Peru. AESTIMATIO, 9(2015), 8–29. https://doi.org/10.5605/ieb.10.1

- Cámara, N., Research, B., & Tuesta, D. (2017). Bank of Morocco – CEMLA – IFC Satellite Seminar at the ISI World Statistics Congress on “Financial Inclusion” Marrakech, Morocco.

- CCmara, N., & Tuesta, D. (2015). Measuring Financial Inclusion: A Muldimensional Index. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.2634616

- Cole, S., Sampson, T., & Zia, B. (2011). Prices or knowledge? What drives demand for financial services in emerging markets? Journal of Finance, 66(6), 1933–1967. https://doi.org/10.1111/j.1540-6261.2011.01696.x

- Cull, R., Demirguc-kunt, A., & Layman, T. (2012). Financial inclusion and stability: What does research show? CGAP Brief. https://doi.org/10.1002/jid

- Cull, R., Demirguç-Kunt, A., & Morduch, J. (eds). (2013). Banking the world: Empirical foundations of financial inclusion (pp. vi, 511). MIT Press. https://doi.org/10.2307/j.ctt5vjqzp

- Danes, S. M., & Haberman, H. R. (2007). Teen financial knowledge, self-efficacy, and behavior: A gendered view. Journal of Financial Counseling and Planning, 18(2), 48-60.

- Demirguc-kunt, A., & Klapper, L. (2012). “‘Measuring financial inclusion. The Global findex database.’” Policy Research Working Paper. https://doi.org/10.1596/978-0-8213-9509-7

- Demirgüç-Kunt, A., & Klapper, L. (2013). Measuring financial inclusion: explaining variation in use of financial services across and within countries. Brookings Papers on Economic Activity, 2013(1), 279–340. https://doi.org/10.1353/eca.2013.0002

- Demirgüç-Kunt, A., Klapper, L., & Singer, D. (2013). Financial inclusion and legal discrimination against women: Evidence from developing countries. World Bank Policy Research Working Paper. https://doi.org/10.1596/1813-9450-6416

- Demirguc-Kunt, A., Klapper, L., Van Oudheusden, P., & Singer, D. (2015). In The Global Findex Database 2014: measuring financial inclusion around the world, Policy Research Working Paper Series 7255, The World Bank.

- Din, S. M. U., Regupathi, A., Abu-Bakar, A., Lim, C. C., & Ahmed, Z. (2020). Insurance-growth nexus: A comparative analysis with multiple insurance proxies. Economic Research-Ekonomska Istrazivanja, 33(1), 604–622. https://doi.org/10.1080/1331677X.2020.1722954

- Evans, P. (2002). Collective capabilities, culture, and Amartya Sen’s Development as Freedom. Studies in Comparative International Development, 37(2), 54–60. https://doi.org/10.1007/bf02686261

- Ghaffar, S., & Sharif, S. (2016). The level of financial literacy in Pakistan. Journal of Education & Social Sciences, 4(2), 132–143. https://doi.org/10.20547/jess0421604204

- Ghosh, S., & Vinod, D. (2017). What constrains financial inclusion for women? Evidence from Indian micro data. World Development, 92(C), 60–81. https://doi.org/10.1016/j.worlddev.2016.11.011

- Greene, W. W. H. (2012). Econometric analysis (7th ed.). Prentice Hall.

- Hejazi, E., Shahraray, M., Farsinejad, M., & Asgary, A. (2008). Identity styles and academic achievement: Mediating role of academic self-efficacy. Social Psychology of Education, 12(1), 123–135. https://doi.org/10.1007/s11218-008-9067-x

- Hilary, G., Huang, S., & Xu, Y. (2017). Marital status and earnings management. European Accounting Review, 26(1), 153–158. https://doi.org/10.1080/09638180.2016.1266958

- Jayaraman, T. K., Lau, L. S., & Ng, C. F. (2018). Role of financial sector development as a contingent factor in the remittances and growth nexus: A panel study of pacific Island countries. Remittances Review, 3(1), 51–74. https://doi.org/10.33182/rr.v3i1.426

- Kairiza, T., Kiprono, P., & Magadzire, V. (2017). Gender differences in financial inclusion amongst entrepreneurs in Zimbabwe. Small Business Economics, 48(1), 259–272. https://doi.org/10.1007/s11187-016-9773-2

- Kefela, G. T. (2010). Promoting access to finance by empowering consumers -Financial literacy in developing countries. Educational Research and Reviews.

- Kemal, A. A. (2019). Mobile banking in the government-to-person payment sector for financial inclusion in Pakistan*. Information Technology for Development, 25(3), 475–502. https://doi.org/10.1080/02681102.2017.1422105

- Klapper, L., & PANOS, G. A. (2011). Financial literacy and retirement planning: The Russian case. Journal of Pension Economics and Finance, 10(4), 599–618. https://doi.org/10.1017/S1474747211000503

- Klapper, L. F., & Panos, G. A. (2012). Financial literacy and retirement planning in view of a growing youth demographic: The Russian case. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.1809723

- Kostov, P., Arun, T., & Annim, S. (2015). Access to financial services: The case of the `Mzansi’ account in South Africa. Review of Development Finance, 5(1), 34–42. https://doi.org/10.1016/j.rdf.2015.04.001

- Kumail Abbas Rizvi, S., Naqvi, B., & Tanveer, F. (2017). Mobile banking: A potential catalyst for financial inclusion and growth in Pakistan. The Lahore Journal of Economics, 22, 251–281. https://doi.org/10.35536/lje.2017.v22.isp.a11

- Kumar, A., Pal, R., & Pal, R. (2019). Usage of formal financial services in India: Demand barriers or supply constraints? Economic Modelling, 80, 244–259. https://doi.org/10.1016/j.econmod.2018.11.010

- Kumar, N. (2013). Financial inclusion and its determinants: Evidence from India. Journal of Financial Economic Policy, 5(1), 4–19. https://doi.org/10.1108/17576381311317754

- Lotto, J. (2018). Examination of the status of financial inclusion and its determinants in Tanzania. Sustainability (Switzerland), 10(8), 2873. https://doi.org/10.3390/su10082873

- Lotto, J. (2020). Understanding sociodemographic factors influencing households’ financial literacy in Tanzania. Cogent Economics and Finance, 8(1), 1. https://doi.org/10.1080/23322039.2020.1792152

- Love, D. A. (2010). The effects of marital status and children on savings and portfolio choice. Review of Financial Studies, 23(1), 385–432. https://doi.org/10.1093/rfs/hhp020

- Lusardi, A., & Mitchell, O. S. (2011). Financial literacy and retirement planning in the United States. Journal of Pension Economics and Finance. National Bureau of Economic Research. https://doi.org/10.3386/w17108

- Mani, M. (2016). Financial inclusion in South Asia—relative standing, challenges and initiatives. South Asian Survey, 23(2), 158–179. https://doi.org/10.1177/0971523118783353

- Maslow, A. H. A. H. H. (1943). A theory of human motivation a theory of human motivation. Psychological Review, 50(4), 370–396. https://doi.org/10.1037/h0054346

- Mccormick, M. H. (2009). The effectiveness of youth financial education: A review of the literature. Journal of Financial Counseling and Planning. 20(1), 71.

- Miller, M., Godfrey, N., Levesque, B., & Stark, E. (2009). The case for financial literacy in developing countries: Promoting access to finance by empowering consumers. In The international bank for reconstruction and development/The World Bank.

- Mindra, R., & Moya, M. (2017). Financial self-efficacy: A mediator in advancing financial inclusion. Equality, Diversity and Inclusion, 36(2), 128–149. https://doi.org/10.1108/EDI-05-2016-0040

- Mindra, R., Moya, M., Zuze, L. T., & Kodongo, O. (2017). Financial self-efficacy: A determinant of financial inclusion. International Journal of Bank Marketing, 35(3), 338–353. https://doi.org/10.1108/IJBM-05-2016-0065

- Mohy Ul Din, S., Regupathi, A., & Abu-Bakar, A. (2017). Insurance effect on economic growth – Among economies in various phases of development. Review of International Business and Strategy, 27(4), 501–519. https://doi.org/10.1108/RIBS-02-2017-0010

- Morgan, P., & Pontines, V. (2014). Financial Stability and Financial Inclusion. ADBI Working Paper 488. https://doi.org/10.2139/ssrn.2464018

- Nandru, P., Anand, B., Rentala, S., & Byram, A. (2016). Determinants of financial inclusion: Evidence from account ownership and use of banking services. International Journal of Entrepreneurship and Development Studies (IJEDS), 4(2).

- Nanziri, E. L. (2016). Financial inclusion and Welfare in South Africa: Is there a gender gap? Journal of African Development, 18(2), 109-134.

- Nenova, T., & Niang, C. T. (2009). Bringing finance to Pakistan’s Poor. The World Bank. https://doi.org/10.1596/978-0-8213-8030-7.

- Nenova, T., Niang, C. T., & Ahmad, A. (2009). Access to finance: Evidence from the demand side. In Bringing finance to Pakistan’s poor : access to finance for small enterprises and the underserved.

- Pakistan Economic Survey. (2015). Pakistan economic survey. Economic adviser’s wing, finance division, government of Pakistan, Islamabad. https://doi.org/10.1038/479299e

- Pallant, J. (2011). A step by step guide to data analysis using SPSS. Alen & Unwin.

- Palys, T. (2008). Purposive sampling. In L. M. Given (Ed..), The sage encyclopedia of qualitative research methods. https://doi.org/10.1006/cpac.2000.0439.

- Park, C.-Y., & Mercado, R. J. (2015). Financial inclusion, poverty, and income inequality in developing Asia. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.2558936

- Preacher, K. J., & Leonardelli, G. J. (2001, September). Calculation for the Sobel test.

- Robeyns, I. (2003). {SEN}{\textquotesingle}S {CAPABILITY} {APPROACH} {AND} {GENDER} {INEQUALITY}: {SELECTING} {RELEVANT} {CAPABILITIES}. Feminist Economics, 9(2–3), 61–92. https://doi.org/10.1080/1354570022000078024

- Robeyns, I. (2006). The capability approach in practice. Journal of Political Philosophy, 14(3), 351–376. https://doi.org/10.1111/j.1467-9760.2006.00263.x

- Sapovadia, V. (2017). Financial inclusion, digital currency, and mobile technology. Handbook of Blockchain, Digital Finance, and Inclusion. https://doi.org/10.1016/B978-0-12-812282-2.00014-0

- Sarma, M. (2012). Index of financial inclusion – A measure of financial sector inclusiveness. Berlin Working Papers on Money, Finance and Trade Development.

- Sedgwick, P. (2014). Cross sectional studies: Advantages and disadvantages. BMJ, 348(mar262), g2276–g2276. https://doi.org/10.1136/bmj.g2276

- Sen, A. (2007). Capability and Well-Being. In The quality of life (pp. 30–53). Oxford University Press. https://doi.org/10.1017/CBO9780511819025.019.

- Serrao, M. V., Sequeira, A. H., & Hans, B. V. (2012). Designing a methodology to investigate accessibility and impact of financial inclusion. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.2025521

- Shaikh, A. A., Glavee-Geo, R., & Karjaluoto, H. (2017). Exploring the nexus between financial sector reforms and the emergence of digital banking culture – Evidences from a developing country. Research in International Business and Finance, 42, 1030–1039. https://doi.org/10.1016/j.ribaf.2017.07.039

- Shetty, N. K., & Veerashekharappa. (2009). The microfinance promise in financial inclusion: Evidence from India. The IUP Journal of Applied Economics. https://doi.org/10.1016/j.sbspro.2012.03.281

- Toxopeus, H. S., & Lensink, R. (2008). Remittances and financial inclusion in development. Development Finance in the Global Economy. https://doi.org/10.1057/9780230594074_10

- World Bank. (2013). Why financial capability is important and how surveys can help. Financial Capability Survey Around the World.

- World Bank. (2015). The little data book on financial inclusion 2015. The little data book on financial inclusion 2015. The World Bank. https://doi.org/10.1596/978-1-4648-0552-3

- World Bank. (2017). World Bank Fact Book 2017. https://www.cia.gov/library/publications/download/download-2017/index.html

- Xu, L., & Zia, B. (2012). Financial literacy around the world: An overview of the evidence with practical suggestions for the way forward. Policy Research Working Paper. https://doi.org/10.1596/1813-9450-6107

- Zins, A., & Weill, L. (2016). The determinants of financial inclusion in Africa. Review of Development Finance, 6(1), 46–57. https://doi.org/10.1016/j.rdf.2016.05.001

- Zulfiqar, K., Chaudhary, M. A., & Aslam, A. (2016). Financial Inclusion and its implications for inclusive growth in Pakistan. Pakistan Economic and Social Review, 54(2), 297–325.