?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study examines the effect of ownership structure on the risk-taking behavior of banks in ASEAN countries. Using a sample of 96 commercial banks in ASEAN countries from 2002 to 2018, the study demonstrates that the relationship between ownership structure and bank risk-taking behavior is correlated with the characteristics of individual banks in terms of quantile regression. First, state ownership and foreign ownership affect bank risk-taking positively in high-risk banks while negatively in low-risk banks. Second, the relationship between ownership concentration and risk-taking is negative in all distributions of bank risk. These findings suggest that appropriate ownership structure can constrain bank risk-taking activities in accordance with the level of risk of each bank.

PUBLIC INTEREST STATEMENT

Bank risk is a major concern of bank regulators, bank shareholders, and the public at large because of the potential contagion across the financial sector and the possible consequent meltdown of the financial system. One of the mechanisms to control bank risk-taking is finding an appropriate ownership structure. Literature about the effect of ownership structure on bank risk is the assumption that there is an optimal ownership structure that is common to all banks. This study investigates the hypothesis that there is no optimal ownership structure for all banks. By using the quantile regression technique, this study finds that the relationship between ownership structure and bank risk-taking behavior is correlated with the characteristics of individual banks in terms of quantile regression. Our study is of interest to policymakers and bank shareholders since it provides an understanding of the relationship between ownership structure and bank risk-taking.

1. Introduction

The financial crisis of 2007–2008 highlighted once again the far-reaching impact of the risk-taking behavior of banks on global economic stability and welfare (Bernanke, Citation1983; Calomiris & Mason, Citation2003a, Citation2003b). Regulators responded by putting stricter and more effective capital adequacy standards in place to control the risk-taking behavior of banks. This restrictive regulatory response has galvanized a great deal of debate among regulators, policymakers, and financial economists. The opponents of restrictive regulation advance the argument that self-regulation through effective corporate governance and market discipline will better ensure optimal risk-taking by financial institutions.

As a key component of internal bank governance (see Macey & O’hara, Citation2003) the role of ownership structure in monitoring management and its relationship to risk-taking has been largely investigated in empirical literature regarding corporate governance. In terms of state ownership, political interference usually comes at the expense of corporate profitability due to the deliberate policies of politicians seeking to transfer resources to their supporters (Shleifer, Citation1998; Shleifer & Vishny, Citation1986). This suggests that state-owned banks might be seen as vehicles for raising capital to finance projects with high social returns but possibly engendering high-risk. There does also exist, however, some contradictory data. Bank controlled by government has also been found to be associated with lower risk in Russia (Fungáčová & Solanko, Citation2009). Boubakri et al. (Citation2013) find evidence that state ownership is negatively related to corporate risk-taking. In terms of foreign ownership, Demirgüç-Kunt et al. (Citation1998) find that foreign ownership reduces financial fragility and makes banks less prone to harm caused by financial crises. Supporting this view, Barth et al. (Citation2004) find that barriers to foreign bank entry are positively associated with bank fragility. Choi and Hasan (Citation2005) show that the extent of foreign ownership has a significantly negative effect on bank risk in South Korea. In a sampling of Taiwanese banks, Chou and Lin (Citation2011) support the notion that foreign banks are less risky and provide evidence that foreign ownership of an institution is associated with a lower number of overdue loans and higher levels of regulatory capital. Mixed empirical evidence regarding ownership concentration and bank risk-taking is also documented in some literature. Ownership concentration has been found to be associated with higher risk (Laeven & Levine, Citation2009) as well as higher insolvency risk, and greater return volatility (Haw et al., Citation2010). Liu and Yeh (Citation2018) find banks with a concentration of shares owned by financial intermediaries and non-financial firms experience greater risk fluctuation during acquisition years. In contrast, ownership concentration has been found to be associated with a lower level of risk-taking (García-Marco & Robles-Fernández, Citation2008), better loan quality, lower asset risk and lower insolvency risk (Iannotta et al., Citation2007), and a lower non-performing loan ratio and better capital adequacy ratio (Shehzad et al., Citation2010) in Spanish commercial banks. Overall, the findings in literature of correlation between ownership structure (i.e., state ownership, foreign ownership, and ownership concentration) and bank risk-taking are mixed.

While the findings are mixed, the approach used in studying the relationship between ownership structure and bank risk is, for the most part, identical. Underlying these studies on the effect of ownership structure on bank risk is the assumption that there is an optimal ownership structure which is common to all banks, and that banks which diverge from the optimal level of these characteristics will experience higher risk. In this paper, by focusing on the three abovementioned aspects of ownership structure, we investigate the hypothesis that there is no optimal ownership structure for all banks. In this study, we use a novel statistical technique called the quantile regression approach as introduced by Koenker and Bassett (Citation1978). The quantile regression approach allows parameters defining the effect of exogenous variables to vary across different quantiles of bank-risk distribution. This will give a complete picture of the relationship between ownership structure and bank risk-taking. From this framework, our study makes a major methodological contribution by providing evidence that the relationship between ownership structure and bank risk-taking behavior depends on the level of risk of each individual bank. This gap is also potentially serious from a policy perspective. Any contemplated change of ownership structure should take into consideration the level of risk that will result in order to formulate an appropriate risk management strategy.

The rest of the paper is structured as follows: Section 2 outlines the review of literature and the development of hypotheses. Section 3 lays out the description of the data, measure of variables and the model applied in the paper. The empirical results are reported in Section 4 and concluding remarks are contained in Section 5.

2. Review of literature and development of hypotheses

2.1. State ownership and bank risk-taking

The economic theory of privatization concerning the inefficiency of state-owned enterprises provides us with the theoretical background to develop our hypotheses on bank risk-taking by a government. Clarke et al. (Citation2005) find that state-owned banks might become tools for raising capital to finance projects with high social returns but possibly engendering high risk or to provide financing to favored entities such as state-owned enterprises. Moreover, state-owned banks find it difficult to resist harmful government interference, whereas private banks are more able to oppose it (Shirley & Nellis, Citation1991; Shleifer & Vishny, Citation1997). Kick and Von Westernhagen (Citation2009) find that state ownership may increase bank fragility given weaker banking skills, weak governance structures, unstable business models, and overall misaligned incentives in government-owned banks resulting in lower efficiency and lower profitability thus leading to said fragility. Moreover, lower performance incentives (Shleifer & Vishny, Citation1997) and “soft” budget constraints (Sheshinski & López-Calva, Citation2003) in state-owned banks can also result in excessive risk-taking. Consequently, an increase in the level of state control may further increase risk-taking. We propose the following hypothesis:

H1a: Government ownership of banks is positively related to bank risk-taking.

Based on agency theory, the banking sector is also affected by the well-known owner–manager agency conflict (Fama & Jensen, Citation1983). Many studies agree that agency conflicts may counteract the increase in risk-taking arising from the moral hazard problem. Shareholders might encourage bank management to invest in high-risk projects but managers may be reluctant to risk their wealth, their specific human capital, or the advantages associated with controlling the firm. This risk aversion may lead them to choose safer investment projects or to operate with larger amounts of capital than owners would consider optimal. These managers will avoid very risky strategies to protect their jobs, since they are not going to receive any extra compensation for trying to obtain higher profits by taking a greater risk. Some theoretical and empirical studies in the literature state that the risk-taking behavior of organizations depends on the identity of the controlling shareholders (Barry et al., Citation2011; John et al., Citation2008). State ownership is considered a source of inefficiency due to government bureaucracy and lack of capital market monitoring. Indeed, within state-owned entities managers are not sufficiently controlled compared to their counterparts in private banks. Thus, they deploy less effort than their private counterparts or divert resources for personal benefit (Lang & So, Citation2002). As a result, managers of state banks tend to accept less risky projects. This leads us to propose the following hypothesis:

H1b: Government ownership of banks is negatively related to bank risk-taking.

2.2. Foreign ownership and bank risk-taking

Most studies find that the entry of foreign banks into developing countries improves human capital and skills and may lead to more diverse products, to better use of up-to-date technologies, and to knowledge transfer. Regarding its impact on risk-taking, foreign ownership is one of the factors for risk-taking for several reasons: First, foreign owners may exhibit a higher preference for risk because they can better diversify risk. Second, foreign banks are more efficient and take more risk compared to their domestic counterparts (Lassoued et al., Citation2016). Indeed, they have better access to capital markets and are better able to serve an international clientele that is not easily served by domestic banks (Berger et al., Citation2005). Foreign ownership increases the supply of credit and improves the allocation of said credit to domestic firms which strengthens the local financial system (Giannetti & Ongena, Citation2009). Moreover, Levine (Citation1996) suggests that foreign banks not only improve the quality and availability of financial services due to high competition, but that they also introduce better skills and technology, enhance the supervisory and legal framework of banks, and enhance access to international capital markets. The findings of certain empirical studies on the effect of foreign ownership on bank risk also support to this view. Laeven (Citation1999) finds that foreign-owned banks take more risk than state-owned, company-owned, and family-owned banks in Asian markets. Yeyati and Micco (Citation2007) state that foreign banks are associated with a higher risk than domestic banks in a sample of Latin American banks. Rokhim and Susanto (Citation2011) find that increasing foreign ownership reduces profitability and increases competition and risk. Levine and Barth (Citation2001) find that barriers to foreign bank entry are positively associated with bank fragility. Chen et al. (Citation2017) use panel data of more than 1300 commercial banks in 32 emerging economies during 2000–2013 and find that foreign-owned banks take on more risk than their domestic counterparts. Accordingly, we proffer this hypothesis:

H2a: Foreign ownership of banks is positively related to bank risk-taking.

As a counter-argument one might cite that foreign banks can have difficulty managing from a distance and coping with different economic and regulatory environments (Berger et al., Citation2005). Although foreign shareholders have advantages that allow them to take more risk, they may have difficulty getting managers to agree to take the risk they require. Due to problems inherent in agency, a manager in a bank with high foreign ownership may take less risk than another in order to protect their job. There exist empirical studies that lend support to this view. Demirgüç-Kunt et al. (Citation1998) find that foreign ownership reduces financial fragility and makes banks less prone to financial crisis. Supporting this view, Barth et al. (Citation2004) find that barriers to foreign bank entry are positively associated with bank fragility. Chou and Lin (Citation2011), in a sample of Taiwanese banks, support the notion that foreign banks are less risky and provide evidence that foreign ownership of institutions is associated with a lower number of overdue loans and a higher level of regulatory capital. ElBannan (Citation2015) also finds a negative relationship between foreign ownership and bank risk-taking in Egypt. Thus, we propose the following hypothesis:

H2b: Foreign ownership of banks is negatively related to bank risk-taking.

2.3. Ownership concentration and bank risk-taking

There are two opposing hypotheses regarding the impact of ownership concentration on risk-taking. The first states that diversified owners have incentives to increase bank risk after collecting funds from debt holders and depositors (Esty, Citation1998; Galai & Masulis, Citation1976). To the extent that debt holders (depositors) can only ex-post and inadequately monitor and control the actions of shareholders, shareholders can increase the value of their equity call options by increasing the risk of the underlying assets of a bank (Saunders et al., Citation1990). Moreover, shareholders with diversified portfolios do not have their capital locked into a particular firm and hence may push managers to pursue greater risk. From this perspective, the resulting prediction is that banks with less- concentrated ownership structure tend to take more risk. Therefore, we propose the following hypothesis:

H3a: Ownership concentration of banks is negatively related to bank risk-taking.

In another view based on agency theory, the ability of a bank’s stockholders to maximize the value of their equity call options by increasing risk depends in part on the preferences of the bank’s managers. Pathan (Citation2009) analyzes moral hazard and argues that major shareholders in banks have incentives to increase risk-taking and to transfer wealth away from the deposit insurers by pursuing riskier investments. This will be particularly the case when stockholders have significant power. When bank ownership concentration is high, bank shareholders may have the power to make managers take more risk. In support of this view we propose the following hypothesis:

H3b: Ownership concentration of banks is positively related to bank risk-taking.

3. Data description and methodology

3.1. Data description

This paper uses data from Bankscope (Orbis Bank Focus) for the period 2002–2018. The sample covers Vietnam, Laos, Cambodia, Myanmar, Thailand, Brunei, Indonesia, the Philippines, Singapore, and Malaysia. We select banks that have sufficient information about ownership structure published in annual reports as well as on bank and national stock exchange websites. Most variables are collected from the Bankscope database while detailed information on bank ownership structures was hand-collected. After exclusion of observations with missing data, our data set consists of 1,067 bank-year observations for 96 banks.

3.2. Research methodology

3.2.1. Measures of bank risk-taking

We primarily measure bank risk-taking using the Z-score of each bank. This captures the probability of default of a country’s banking system. The Z-score is a widely used measure of bank risk-taking (Angkinand and Wihlborg, Citation2010; Barry et al., Citation2011; Demirgüç-Kunt & Huizinga, Citation2013; Laeven & Levine, Citation2009). It combines banks’ buffers (capital and profits) with the risks they face (measured by the standard deviation of returns). The Z-score measures the number of standard deviations to which a return realization has to fall in order to deplete equity.

It is estimated as:

where ROA is the return on assets and Sd (ROA) is the standard deviation of ROA. E/A is the equity on assets ratio. Thus, the Z-score is the number of standard deviations by which a bank’s return on assets has to fall in order for the bank to become insolvent. A higher Z-score implies a lower probability of insolvency and higher stability; therefore, it indicates that a bank is more stable and less risky.

3.2.2. Measures of ownership structure

As mentioned above, we create three ownership variables which may have an effect on bank risk-taking:

State ownership: proportion of equity held by the government

Foreign ownership: proportion of equity held by foreigners

Ownership concentration is a dummy variable which receives 1 if a bank has at least one shareholder which holds 10% or more of voting rights and otherwise receives 0. If no one shareholder holds 10% or more of the voting rights, the bank is classified as widely held (Caprio et al., Citation2007)

3.2.3. Measures of control variables

At the bank level, we use a natural logarithm of total assets to control for size as larger banks are frequently the beneficiaries of “too big to fail” policies. To consider the fact that better-diversified banks are assumed to be less risky, we control for diversification measured by a diversification index (Demirgüç-Kunt & Huizinga, Citation2010; Laeven & Levine, Citation2009). We use the ratio of loan loss provisions to total assets as a measure of asset quality. Zhang et al. (Citation2014) find that banks which have been selected for IPOs and foreign investment are significantly more efficient than others and that listed banks may be controlled better than unlisted banks. We expect that a publicly listed bank will have a lower risk than one that is not listed. The IPO is a dummy variable that receives a value of 1 if a bank is listed in any 1 year of observation and 0 if otherwise. A banking crisis is also an important factor that may affect bank risk-taking. This study controls banking crises by creating a dummy variable that takes on the value of 1 if the country is going through a systemic crisis in that year and 0 if it is not. We expect that a banking crisis will increase bank risk. In addition, we use net interest margin (NIM) to understand the impact of banking spreads with regards to their “traditional activities” on bank risk-taking. Higher values are expected to indicate reduced risk.

This study also includes several state-level variables to control for differences in economic development across countries. First, we include a logarithm of GDP per capita to capture the economic development of the country. Second, we control the level of bank competition by using a concentration (CR3) ratio (Chong et al., Citation2013). Competition increases bank-risk as espoused by Keeley (Citation1990) in the franchise value paradigm. The argument is that higher competition reduces banks’ market power and profit margins. Some studies (Beck et al., Citation2013; De Nicoló et al., Citation2006) have provided evidence to support this view. They find a significant and negative relationship between risk and competition. Based on previous studies, we expect that there will be a positive relationship between competition and bank risk. All variables are summarized and explained in Table .

Table 1. Definitions of variables

3.2.4. Empirical models

We examine the effect of ownership structure on risk-taking based on the following model:

where: is the θth quantile regression function, BRT is bank risk measured by Z-score. OWS is a matrix of ownership structure variables. CONT is a matrix of control variables,

and

are the parameters to be estimated,

is the idiosyncratic error term. The definition of all variables in the regression EquationEquation (2)

(2)

(2) is summarized in Table .

3.2.5. Estimation method

The study correlates effective ownership structure to risk-taking in banks with different levels of risk. General regression methods, such as Pool OLS, random-effect, and fixed-effect estimator focus only on the central tendency of the distribution which does not allow for the possibility that the impact of explanatory variables can be different for different levels of bank risk. Quantile regression, as introduced by Koenker and Bassett (Citation1978), is an extension of classical least-squares estimation of conditional mean models. Indeed, it enables us to estimate not one-point estimation, but a set of models for conditional quantile functions. Quantiles describe a fragmentation of a frequency distribution into equal intervals based on the value of the dependent variable. Quantile regression is stated to be more robust to non-normal errors and outliers. It also gives a larger characterization of the data, allowing us to consider the effect of the independent variables on the entire distribution of the response variable, not merely its conditional mean. Furthermore, quantile regression does not require strict assumptions as with classical linear regression such as normality, homoscedasticity, or absence of outliers (Johnston & DiNardo, Citation1963).

Formally, following Koenker and Bassett (Citation1978) and assuming that the θth quantile of the conditional distribution of the dependent variable, yit, is linear in xit, the conditional quantile regression model can be expressed as follows:

where represents the θth conditional quantile of yit on the (K × 1) vector of independent variables xit. βθ is the unknown vector of parameters to be estimated for different values of θ in [0, 1]; and εθit is the error term. The value Fit(.|xit) denotes the conditional distribution of the target variable conditional on it. For different values of θ in [0, 1], the quantile regression method permits us to visit the entire distribution of y conditional on x. The estimator for βθ is obtained through the following minimization problem:

The optimization problem in EquationEquation (4)(4)

(4) allows us to obtain the θth quantile regression estimator

minimizing the absolute value of a weighted sum of the residuals between observed values yit and fitted values

. A weight of θ is attributed to observations with negative residuals (the first term in EquationEquation (4)

(4)

(4) ) and a weight of (1 − θ) to observations with positive residuals (the second term in EquationEquation (4)

(4)

(4) ).

The innovation of this study is that it investigates the impact of ownership structure variables on various distributions of bank risk through quantile regression. An additional advantage of using quantile regression is that it can mitigate certain statistical problems such as sensitivity to outliers and non-Gaussian error distribution (Barnes & Hughes, Citation2002). We estimate the coefficients at nine quantiles, namely the 10th, 20th, 30th, 40th, 50th, 60th, 70th, 80th, and 90th, using the same list of ownership structure and control variables. It is expected that different effects of the explanatory variables at each quantile will be reflected in the size, sign, and significance of estimated coefficients of the different variables.

Additionally, this study employs ordinary least squares (OLS) and the two-stage system-GMM (S-GMM) regression method to compare the results of quantile regressions. Since bank risk-taking and ownership structure determinations are simultaneous, modeling the relationship between the two can be problematic if there is no proper treatment for the endogeneity which occurs. We test the instrument validity by using Hansen’s J statistic of overidentifying restrictions. The Hansen J statistic is used in place of the Sargan test of over-identifying restrictions because of its consistency in the presence of autocorrelation and heteroscedasticity (Neanidis & Varvarigos, Citation2009; Roodman, Citation2007). Then, we use the Arellano and Bond (Citation1991) tests for order serial autocorrelation. For system-GMM, we only check for the absence of second-order serial autocorrelation.

4. Empirical analysis

4.1. Descriptive statistics

The overall descriptive statistics of the major variables are described in Table . The mean of the Z-score is 27.172, the minimum value is −2.619, and the maximum value is 95.516 demonstrating that bank risk differs greatly from bank to bank in ASEAN countries. Furthermore, Z-scores are significantly skewed to the right meaning that they have long right tails. The skewed distribution of Z-scores raises the efficiency of quantile regression. The average state ownership is 20.7% and the average foreign ownership is 16.1%. This means that bank control by government and/or foreigners in ASEAN region is not really high. However, average ownership concentration is 0.848 which is quite high in this region.

Table 2. Descriptive statistics

Table presents the Pearson’s pairwise correlation coefficients for independent variables used in the regression models to examine whether highly correlated variables exist. The Z-score is positively correlated with foreign ownership and ownership concentration but negatively with state ownership. This indicates that foreign ownership and ownership concentration negatively affect bank risk and state ownership may positively affect bank risk. We find that the largest absolute value of correlation coefficients is 0.620 for a positive correlation between bank size (Size) and GDP per capita (GDP). This indicates that their inclusion will not present any problem of multi-collinearity since they are less than 0.70 (Kennedy, Citation2008). The pairwise correlation measures may be highly unreliable indicators of the relationships among the variables because other variables are likely to affect bank risk. Hence, we carry out tests of our main hypotheses using a multiple regression framework.

Table 3. Correlation matrix of main regression variables

Table presents univariate comparisons of independent variables by risk-taking quartile. This study addresses whether the characteristics of banks which have high risk-taking, such as those banks in the fourth quartile, differ from those with low risk-taking, such as those in the first quartile. We also test the hypothesis that the fourth-quartile banks differ significantly from the first-quartile banks using a T-test.

Table 4. Independent variables by bank risk-taking quartiles

The univariate relation between risk-taking and state ownership and foreign ownership is not monotonic. The state ownership and foreign ownership are about 20% and 16%, respectively, in each quartile. Ownership concentration increases monotonically with bank risk-taking. The average level of ownership concentration increases over the first three quartiles and reaches its highest level in the high-risk banks. Moreover, the average ownership concentration in low-risk banks is significantly lower than that in high-risk banks.

4.2. Effect of ownership structure on bank risk-taking

We present the results of analysis of the relationship between ownership structure and bank risk-taking in Table . Columns (1) and (2) present the results for the model with the dependent variable Z-score using OLS and System GMM method, respectively. The results show that the coefficient on SO is negative with Z-score in both the OLS and System GMM model and only significant in the System GMM model. The coefficient on FOW is positive (negative) with the Z-score in OLS (System GMM) model but not significant. However, the coefficient on OWN is positive with the Z-score in the OLS model and remains unchanged in the system GMM model. In columns 3–11, we report the results of the quantile regression method for quantiles from 10th to 90th.

Table 5. The effect of ownership structure on bank risk-taking

The first variable of ownership structure, state ownership, is significantly negative in relation to Z-score at lower levels of distribution (10th, 20th, and 30th quantiles). This indicates that state ownership increases risk-taking in banks with high-risk levels (i.e., low Z-score) and lends support to the H1a hypothesis. This result also supports the findings of Kick and Von Westernhagen (Citation2009): In banks with high-risk levels, state ownership may make for weaker banking skills, weak governance structures, and unstable business models which, in turn, increase risk and lead to fragility. However, in Table the coefficient of state ownership with Z-score becomes significantly positive at the higher quantiles (80th and 90th quantiles) of the distribution. This indicates that state ownership reduces risk-taking in banks with low-risk levels (i.e., high Z-score) and supports the H1b hypothesis. A characteristic of low-risk banks is that managers tend to pursue a low-risk strategies and increased state ownership may allow those managers to more easily implement risk-averse policies.

Similarly, FOW is significantly negative in relation to Z-score at lower levels of distribution (10th, 20th and 30th quantiles). The implication here is that foreign ownership can increase risk-taking in banks with high-risk levels. This result supports hypothesis H2a and is consistent with certain past studies (for example, Chen et al., Citation2017; Rokhim & Susanto, Citation2011; Yeyati & Micco, Citation2007). The coefficient of state ownership with Z-score, however, becomes significantly positive at the higher quantiles (60th, 70th, 80th and 90th quantiles) of the distribution. This indicates that foreign ownership reduces risk-taking in banks with low-risk levels and supports hypothesis H2b. It is consistent with agency theory which recognizes the conflict of interest between foreign shareholders and managers the fact that this difficulty in controlling managers of companies with a majority of foreign shareholders might result in bank managers being more risk averse.

In addition, we find the positive coefficient on OWN with Z-score in nearly 10 quantiles (from 30th to 80th quantile) and these coefficients increase throughout the quantiles. This indicates that ownership concentration can reduce bank risk-taking and supports hypothesis H3a. Given their high concentration, powerful shareholders may exert pressure on management to enhance risk-taking and thus reduce the agency problem. This result is consistent with past studies (García-Marco & Robles-Fernández, Citation2008; Iannotta et al., Citation2007).

Overall, our results suggest that the effect of ownership structure is not homogenous across quantiles of bank-risk variables. There is no optimal ownership structure to constrain bank risk because the relationship depends on the level of risk of each individual bank.

4.3. Comparison of banks with various pairs of quantiles

In order to check the significance of the differences with regard to the coefficients of ownership structure variables across different bank-risk quantiles, this study employs a bootstrap procedure which is extended to construct a joint distribution to test various pairs of quantiles (Chuang et al., Citation2009; Kuan et al., Citation2012; Tao et al., Citation2009). Table illustrates the F-tests for the equality of quantile slope coefficients across the various pairs of quantiles with regard to the coefficients of ownership structure variables. Following previous studies, these tests are based on the bootstrap standard errors using 1000 replications. The results of the F-tests almost reject the null hypothesis of the equality coefficients for pairs of quantiles. These results indicate that the impact of ownership structure on bank risk-taking differs between high-risk and low-risk banks.

Table 6. Inter-quantile comparison of the coefficient

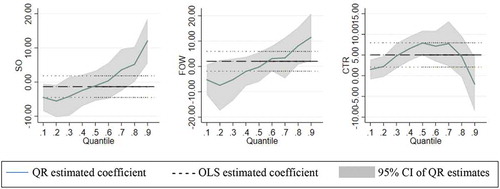

We continue to plot the coefficients of the bank capital variable along the vertical axis and the quantiles along the horizontal axis. The solid line in the middle of the shaded area reflects the estimations of the coefficient with the quantile regression across different quantiles. The horizontal dashed line is the (constant) OLS estimate. The shaded gray area depicts a 95% confidence band for the quantile regression estimates.

As can be seen from Figure , the coefficients of the quantile regression for SO and FOW variables are negative at low quantiles but turn positive at higher quantiles. Most of the coefficients of the quantile regression for OWN variables are positive. Some coefficients are below the OLS estimate for some quantiles and others are above for certain other quantiles. This reveals that the quantile regression produces estimates that are different from the OLS and that, overall, the effect of ownership structure is not homogenous across the distribution bank risk. Therefore, the quantile regression gives a more complete picture of the relationship between ownership structure and bank risk-taking.

Figure 1. Quantile and OLS estimates of SO on Z-score.

4.4. Quantile regression with instrument variables

In this section, we address the potential endogeneity problem in our models and consider the quantile regression estimation of a panel data model with endogenous independent variables, where we allow the endogenous variable to be correlated with unobserved factors affecting the response variable. The model applies the framework analyzed by Chernozhukov and Hansen (Citation2008) on instrumental variables for quantile regression.

The interpretation of the coefficients on ownership structure variables (SO, FOW, and OWC) in Table qualitatively remains the same as our first result. For instance, the statistically significant negative coefficients on SO and FOW with Z-score at lower level of quantiles (10th, 20th, 30th quantile) and positive and significant at higher level (90th quantile) suggest that state ownership and foreign ownership are positively or negatively associated with bank risk depending on level of bank risk. Similarly, the positive coefficients on OWC with Z-score at all levels of risk suggest that ownership concentration is negatively related to bank risk. Overall, the quantile regression with instrument variables in Table supports that even after controlling the endogeneity problem ownership structures are found to relate to bank risk in a manner consistent with expectations.

Table 7. The effect of ownership structure on bank risk-taking—Quantile regression with instrument variables

4.5. Alternative measurement of risk-taking

Following Glaser and Müller (Citation2010), we now extend our analysis by employing Altman’s Z-score (see Altman, Citation1968) as an alternative risk measure:

where x1 is the working capital/total assets, x2 the retained earnings/total assets, x3 the earnings before interest and taxes/total assets, x4 the market value of equity/total assets, and x5 is sales/total assets. The higher the Altman Z-score, the lower the odds that a bank is heading for bankruptcy and the higher the stability.

We use Altman’s Z-score as a proxy for bank risk-taking and estimate EquationEquation (4)(4)

(4) by conventional quantile regression of Koenker and Bassett (Citation1978). The effect of ownership structure on the Altman Z-score across quantiles is presented in Table . The SO is significantly negative in relation to Altman’s Z-score at lower levels of distribution (10th, 20th, and 30th quantiles) and turns positive and significant at higher levels (70th and 80th). The coefficient on FOW with Altman’s Z-score is negative at lower levels of distribution and turn positive at higher levels but not significant. We also find that OWC has a significantly positive coefficient for the 20th, 40th, and 80th quantile and insignificant for other quantiles. These results are fairly consistent with our first result.

Table 8. The effect of ownership structure on bank risk-taking as measured by Altman’s Z-score

5. Conclusion

A number of studies have been done to explain the relationship between ownership structure with respect to corporate governance and bank risk-taking and have reached different conclusions. By using the quantile regression approach, we add to this empirical literature by providing some evidence for this difference. Rather than confirming the homogenous relationship between ownership structure and bank risk-taking as found in past studies, we discover that this relationship depends on the level of risk of each individual bank. Specifically, state ownership and foreign ownership affect bank risk-taking positively in high-risk banks but negatively in low-risk banks. Moreover, the relationship between ownership concentration and risk-taking is negative in all distributions of bank risk. Our results are robust to using alternative measure and methodology. The implication of the results is that high-risk banks should adjust their ownership structure by reducing foreign and state ownership and by increasing the ownership concentration to avoid excessive risk and agency problems. Low-risk banks, however, should increase foreign ownership, state ownership, and ownership concentration in order to maintain a low level of risk.

Acknowledgement

The author would like to thank the editor and other anonymous reviewers for constructive comments and suggestions. We also thank Dr Phu Quoc Pham (University of Economics Ho Chi Minh City) and Dr Chau Le Ho An (University of Lincoln) for all support. Special thanks are also due to an anonymous reviewer of the journal for helpful ideas towards improving the quality of the paper.

Additional information

Funding

Notes on contributors

Quang Khai Nguyen

Quang Khai Nguyen is a researcher at School of Banking, University of Economics Ho Chi Minh City (UEH). His research covers a variety of topics related to financial institutions and empirical corporate finance and banking, including capital structure, corporate governance, risk taking behaviors, earnings management, bank stability

References

- Altman, E. I. (1968). Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. The Journal of Finance, 23(4), 589–19. https://doi.org/10.1111/j.1540-6261.1968.tb00843.x

- Angkinand, A., & Wihlborg, C. (2010). Deposit insurance coverage, ownership, and banks’ risk-taking in emerging markets. Journal of International Money and Finance, 29(2), 252–274. https://doi.org/10.1016/j.jimonfin.2009.08.001

- Arellano, M., & Bond, S. (1991). Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. The Review of Economic Studies, 58(2), 277–297. https://doi.org/10.2307/2297968

- Barnes, M. L., & Hughes, A. T. W. (2002). A quantile regression analysis of the cross section of stock market returns.

- Barry, T. A., Lepetit, L., & Tarazi, A. (2011). Ownership structure and risk in publicly held and privately owned banks. Journal of Banking & Finance, 35(5), 1327–1340. https://doi.org/10.1016/j.jbankfin.2010.10.004

- Barth, J. R., Caprio, G., & Levine, R. (2004). Bank supervision and regulation: What works best?

- Beck, T., De Jonghe, O., & Schepens, G. (2013). Bank competition and stability: Cross-country heterogeneity. Journal of Financial Intermediation, 22(2), 218–244. https://doi.org/10.1016/j.jfi.2012.07.001

- Berger, A. N., Clarke, G. R., Cull, R., Klapper, L., & Udell, G. F. (2005). Corporate governance and bank performance: A joint analysis of the static, selection, and dynamic effects of domestic, foreign, and state ownership. The World Bank.

- Bernanke, B. S. (1983). Non-monetary effects of the financial crisis in the propagation of the great depression. National Bureau of Economic Research.

- Boubakri, N., Cosset, J. C., & Saffar, W. (2013). The role of state and foreign owners in corporate risk-taking: Evidence from privatization. Journal of Financial Economics, 108(3), 641–658. https://doi.org/10.1016/j.jfineco.2012.12.007

- Calomiris, C. W., & Mason, J. R. (2003a). Consequences of bank distress during the great depression. American Economic Review, 93(3), 937–947. https://doi.org/10.1257/000282803322157188

- Calomiris, C. W., & Mason, J. R. (2003b). Fundamentals, panics, and bank distress during the depression. American Economic Review, 93(5), 1615–1647. https://doi.org/10.1257/000282803322655473

- Caprio, G., Laeven, L., & Levine, R. (2007). Governance and bank valuation. Journal of Financial Intermediation, 16(4), 584–617. https://doi.org/10.1016/j.jfi.2006.10.003

- Chen, M., Wu, J., Jeon, B. N., & Wang, R. (2017). Do foreign banks take more risk? Evidence from emerging economies. Journal of Banking & Finance, 82, 20–39. https://doi.org/10.1016/j.jbankfin.2017.05.004

- Chernozhukov, V., & Hansen, C. (2008). Instrumental variable quantile regression: A robust inference approach. Journal of Econometrics, 142(1), 379–398. https://doi.org/10.1016/j.jeconom.2007.06.005

- Choi, S., & Hasan, I. (2005). Ownership, governance, and bank performance: Korean experience. Financial Markets, Institutions & Instruments, 14(4), 215–242. https://doi.org/10.1111/j.0963-8008.2005.00104.x

- Chong, T. T.-L., Lu, L., & Ongena, S. (2013). Does banking competition alleviate or worsen credit constraints faced by small-and medium-sized enterprises? Evidence from China. Journal of Banking & Finance, 37(9), 3412–3424. https://doi.org/10.1016/j.jbankfin.2013.05.006

- Chou, S., & Lin, F. (2011). Bank’s risk-taking and ownership structure–Evidence for economics in transition stage. Applied Economics, 43(12), 1551–1564. https://doi.org/10.1080/00036840903018791

- Chuang, -C.-C., Kuan, C.-M., & Lin, H.-Y. (2009). Causality in quantiles and dynamic stock return–volume relations. Journal of Banking & Finance, 33(7), 1351–1360. https://doi.org/10.1016/j.jbankfin.2009.02.013

- Clarke, G. R., Cull, R., & Shirley, M. M. (2005). Bank privatization in developing countries: A summary of lessons and findings. Journal of Banking & Finance, 29(8–9), 1905–1930. https://doi.org/10.1016/j.jbankfin.2005.03.006

- De Nicoló, M. G., Boyd, J. H., & Jalal, A. M. (2006). Bank risk-taking and competition revisited: New theory and new evidence. International Monetary Fund.

- Demirgüç-Kunt, A., Levine, R., & Min, H. G. (1998). Opening to foreign banks: Issues of efficiency, stability and growth. Globalization of World Financial Markets. forthcoming.

- Demirgüç-Kunt, A., & Huizinga, H. (2010). Bank activity and funding strategies: The impact on risk and returns. Journal of Financial Economics, 98(3), 626–650. https://doi.org/10.1016/j.jfineco.2010.06.004

- Demirgüç-Kunt, A., & Huizinga, H. (2013). Are banks too big to fail or too big to save? International evidence from equity prices and CDS spreads. Journal of Banking & Finance, 37(3), 875–894. https://doi.org/10.1016/j.jbankfin.2012.10.010

- ElBannan, M. A. (2015). Do consolidation and foreign ownership affect bank risk taking in an emerging economy? An empirical investigation. Managerial Finance, 41(9), 874–907. https://doi.org/10.1108/MF-12-2013-0342

- Esty, B. C. (1998). The impact of contingent liability on commercial bank risk taking. Journal of Financial Economics, 47(2), 189–218. https://doi.org/10.1016/S0304-405X(97)00043-3

- Fama, E. F., & Jensen, M. C. (1983). Separation of ownership and control. The Journal of Law & Economics, 26(2), 301–325. https://doi.org/10.1086/467037

- Fungáčová, Z., & Solanko, L. (2009). Risk-taking by Russian banks: Do location, ownership and size matter? Экономический журнал Высшей школы экономики, 13(1). http://dx.doi.org/10.2139/ssrn.1313019

- Galai, D., & Masulis, R. W. (1976). The option pricing model and the risk factor of stock. Journal of Financial Economics, 3(1–2), 53–81. https://doi.org/10.1016/0304-405X(76)90020-9

- García-Marco, T., & Robles-Fernández, M. D. (2008). Risk-taking behaviour and ownership in the banking industry: The Spanish evidence. Journal of Economics and Business, 60(4), 332–354. https://doi.org/10.1016/j.jeconbus.2007.04.008

- Giannetti, M., & Ongena, S. (2009). Financial integration and firm performance: Evidence from foreign bank entry in emerging markets. Review of Finance, 13(2), 181–223. https://doi.org/10.1093/rof/rfm019

- Glaser, M., & Müller, S. (2010). Is the diversification discount caused by the book value bias of debt? Journal of Banking & Finance, 34(10), 2307–2317. https://doi.org/10.1016/j.jbankfin.2010.02.017

- Haw, I.-M., Ho, S. S. M., Hu, B., & Wu, D. (2010). Concentrated control, institutions, and banking sector: An international study. Journal of Banking & Finance, 34(3), 485–497. https://doi.org/10.1016/j.jbankfin.2009.08.013

- Iannotta, G., Nocera, G., & Sironi, A. (2007). Ownership structure, risk and performance in the European banking industry. Journal of Banking & Finance, 31(7), 2127–2149. https://doi.org/10.1016/j.jbankfin.2006.07.013

- John, K., Litov, L., & Yeung, B. (2008). Corporate governance and risk‐taking. The Journal of Finance, 63(4), 1679–1728. https://doi.org/10.1111/j.1540-6261.2008.01372.x

- Johnston, J., & DiNardo, J. (1963). Econometric methods. New York.

- Keeley, M. C. (1990). Deposit insurance, risk, and market power in banking. The American Economic Review, 80(5), 1183–1200. https://www.jstor.org/stable/2006769

- Kennedy, P. (2008). A guide to econometrics. Blackwell Publishing.

- Kick, T. B. H. H. T., & Von Westernhagen, N. (2009). Bank ownership and stability: Evidence from Germany. VOX CEPRs Policy Portal.

- Koenker, R., & Bassett, G., Jr. (1978). Regression quantiles. Econometrica: Journal of the Econometric Society, 46(1), 33–50. https://doi.org/10.2307/1913643

- Kuan, T.-H., Li, C.-S., & Liu, -C.-C. (2012). Corporate governance and cash holdings: A quantile regression approach. International Review of Economics & Finance, 24, 303–314. https://doi.org/10.1016/j.iref.2012.04.006

- Laeven, L. (1999). Risk and efficiency in East Asian banks. The World Bank.

- Laeven, L., & Levine, R. (2009). Bank governance, regulation and risk taking. Journal of Financial Economics, 93(2), 259–275. https://doi.org/10.1016/j.jfineco.2008.09.003

- Lang, L. H., & So, R. W. (2002). Bank ownership structure and economic performance. Chinese University of Hong Kong mimeo.

- Lassoued, N., Sassi, H., & Ben Rejeb Attia, M. (2016). The impact of state and foreign ownership on banking risk: Evidence from the MENA countries. Research in International Business and Finance, 36, 167–178. https://doi.org/10.1016/j.ribaf.2015.09.014

- Levine, R. (1996). Foreign banks, financial development, and economic growth. Chapter 6 In C. E. Barfield (Ed.), International financial markets: Harmonization versus competition (pp. 224-254). The AEI Press.

- Levine, R., & Barth, J. (2001). Bank regulation and supervision: What works best? The World Bank.

- Liu, C.-L., & Yeh, Y.-H. (2018). Ownership concentration and bank risk: International study on acquisitions. The European Journal of Finance, 24(9), 761–808. https://doi.org/10.1080/1351847X.2017.1354901

- Macey, J. R., & O’hara, M. (2003). The corporate governance of banks. Economic Policy Review, 9, 1. https://ssrn.com/abstract=795548

- Machado, J. A., & Silva, J. S. (2019). Quantiles via moments. Journal of Econometrics, 213(1), 145–173. https://doi.org/10.1016/j.jeconom.2019.04.009

- Neanidis, K. C., & Varvarigos, D. (2009). The allocation of volatile aid and economic growth: Theory and evidence. European Journal of Political Economy, 25(4), 447–462. https://doi.org/10.1016/j.ejpoleco.2009.05.001

- Pathan, S. (2009). Strong boards, CEO power and bank risk-taking. Journal of Banking & Finance, 33(7), 1340–1350. https://doi.org/10.1016/j.jbankfin.2009.02.001

- Rokhim, R., & Susanto, A. P. (2011, August 23). The increase of foreign ownership and its impact to the performance, competition & risk in Indonesian banking industry. Competition & Risk in Indonesian Banking Industry.

- Roodman, D. (2007). The anarchy of numbers: Aid, development, and cross-country empirics. The World Bank Economic Review, 21(2), 255–277. https://doi.org/10.1093/wber/lhm004

- Saunders, A., Strock, E., & Travlos, N. G. (1990). Ownership structure, deregulation, and bank risk taking. The Journal of Finance, 45(2), 643–654. https://doi.org/10.1111/j.1540-6261.1990.tb03709.x

- Shehzad, C. T., De Haan, J., & Scholtens, B. (2010). The impact of bank ownership concentration on impaired loans and capital adequacy. Journal of Banking & Finance, 34(2), 399–408. https://doi.org/10.1016/j.jbankfin.2009.08.007

- Sheshinski, E., & López-Calva, L. F. (2003). Privatization and its benefits: Theory and evidence. CESifo Economic Studies, 49(3), 429–459. https://doi.org/10.1093/cesifo/49.3.429

- Shirley, M., & Nellis, J. (1991). “Public enterprise reform.” The lessons of experience. World Bank, Economic development Institute.

- Shleifer, A. (1998). State versus private ownership. Journal of Economic Perspectives, 12(4), 133–150. https://doi.org/10.1257/jep.12.4.133

- Shleifer, A., & Vishny, R. W. (1986). Large shareholders and corporate control. Journal of Political Economy, 94(3, Part 1), 461–488. https://doi.org/10.1086/261385

- Shleifer, A., & Vishny, R. W. (1997). A survey of corporate governance. The Journal of Finance, 52(2), 737–783. https://doi.org/10.1111/j.1540-6261.1997.tb04820.x

- Tao, L., Sun, L., & Zou, L. (2009). State ownership and corporate performance: A quantile regression analysis of Chinese listed companies. China Economic Review, 20(4), 703–716. https://doi.org/10.1016/j.chieco.2009.05.006

- Yeyati, E. L., & Micco, A. (2007). Concentration and foreign penetration in Latin American banking sectors: Impact on competition and risk. Journal of Banking & Finance, 31(6), 1633–1647. https://doi.org/10.1016/j.jbankfin.2006.11.003

- Zhang, B., Lin, Y. X., Liu, W., & Sun, J. (2014). Debate on urban development boundary: The perspective of spatial governance in China. Urban Planning Forum.