?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper examines the effect of financial system development on oil-dominant economy of Nigeria using Zivot-Andrews unit root test and Autoregressive Distributed Lag (ARDL) model over the period 1981 to 2015. The motivation of this paper is that the study distinguished the impact of financial system development on the non-oil sector from the oil sector. The study also differs from the usual yet unsatisfactory approach of measuring financial system development in Nigeria to build an index as a measure that characterizes the whole development in the financial sector using Principal Components Analysis (PCA). The result reveals that there exist mediating factors that alter the impact of finance on growth. Specifically, the findings indicate that financial system development has a negative and insignificant impact on the growth of oil sector while the influence of financial system development on the growth of non-oil sector is positive and significant. The study therefore recommend that policymakers should channel the high receipts from the export of crude to productive investments through financial institutions that will allocate the resources more efficiently to improve the quality of investment capable of driving growth.

PUBLIC INTEREST STATEMENT

Theoretical and empirical evidence have shown that financial system development stimulates economic growth. However, there are potential heterogenous impact of finance on growth in an oil-dominant economy that is yet to be rigorously investigated in existing studies. This paper examines whether oil and non-oil sectors benefits equally from the financial development impact. The estimation results show evidence of heterogeneity on the influence of finance on growth in oil-dependent economy of Nigeria. Whereas financial development is insensitive to the growth of the oil sector, non-oil sector growth is substantially driven by financial development. The weakness of financial development in resource mobilization and efficient allocation in the oil sector could be attributed to resource course syndrome and thus explain reasons why the natural resources in Nigeria do not trickle down to address her economic growth sustainability needs. We conclude that policymakers should reform the activities of financial institution across all sectors.

1. Introduction

Nigeria has for over the last four decades depended precariously on oil revenue. However, the recent fall in oil price has led to recourse to economic diversification as the engine of growth and development. As a result, the interest in transforming the oil-dependent economy of Nigeria into a vibrant and technologically driven economy has however led to several economic reforms starting from Structural Adjustment Programme (SAP) in 1986. The preponderance of all the policy reforms anchored on the financial sector. This is so as economists and policymakers have shown both theoretically and empirically that sound and functioning financial system is capable of driving sustainable economic growth. For instance, the new endogenous growth theory identified technological innovation as a major source of change in production process that is capable of maintaining long-term growth without exogenous technological change. The earlier study of Schumpeter (Citation1911) provided a detailed explanation on how technological innovation via financial services penetration raises the ratios of private domestic savings, capital accumulation and efficient allocation of resources that culminates into sustainable economic growth. The empirical inquiry of McKinnon (1973) and Shaw (1973) reinforced Schumpeter’s assertion on the crucial role of financial system development in ensuring economic growth. Further empirical investigations show that a well and functioning financial system does not only encourage technological innovation but also augment natural endowment for the growth process (Greenwood & Jovanovic, Citation1990; King & Levine, Citation1993). Therefore, the role financial system development perform in a natural resource-dominant economy is also fundamental (Badeeb et al., Citation2016; Samargandi et al., Citation2014).

However, the extant empirical studies on financial system development and economic growth in abundant-oil economy appeared not only mixed but also varied. For instance, some existing studies argue that oil revenue provides an extra resource to the financial institutions for economic activities (i.e. natural resource blessing) while others have that, high oil dependence in an economy could inhibit the institutional capacity of financial system to efficiently accumulate and allocate capital to the most productive uses suggesting natural resource curse (Badeeb et al., Citation2016). This is because to them, liberal trade policies that enhance agricultural, manufacturing and other non-oil sector will receive less support when the economy starts witnessing oil windfall. Consequently, the non-oil sector will be weakened, less competitive and unattractive during oil windfall suggesting a weak or no linkage with financial system development (Kurronen, Citation2015; Nili & Rastad, Citation2007; Yuxiang & Chen, Citation2011). Empirical evidence also shows that nations that have large proportion of its national wealth stored in a natural resource tend to have weak financial institution as there will be low demand for financial services in the conduct of economic activities (Badeeb et al., Citation2016). This evidence suggests that oil-dominant economy could indirectly impede saving and investment if the need for financial intermediation is insignificant in the stream of oil rent. For instance, in Nigeria currently, the economic investment actors are overwhelmingly dominated by Multinational Corporation in the oil sector with little or no demand for financial services in the conduct of their businesses. But in 1960s, there was a wide range of economic investment actors across all sectors of the economy. Then, economic investment actors were prominent in cocoa, groundnut, and oil palm production with less foreign presence who depended hugely on financial services for their economic activities. However, the unprecedented rise in crude oil earnings in 1970s shifted the activities of economic investment actors in manufacturing, agriculture, and services sectors to oil sector with greater participant of foreign actors (Ohiorhenuan, Citation1990). The dominance of foreign investment actors especially in oil sector in 1970s and 1980s led to policy shift towards state-led growth or economic nationalism. For instance, the Nigerian Enterprises Promotion Decree that restricted foreign actors in economic participation forced foreign actors to form joint venture with state actors mainly in oil industry and consequently the contribution of private investment to GDP declined from 14.6% in 1973 to 6% in 1981 and to 1.5% in 1985. The restriction of foreign actors was lifted except in oil industry in 1995 by Nigerian Investment Promotion Commission Act. Prompted by dwindling government revenue triggered by international crude oil price fall, economic reform towards private sector-led growth through National Economic Empowerment and Development Strategy (NEEDS) was formulated. This approach relinquished most of the state enterprise to private investment actors and accordingly the contribution of private investment to growth improved. In 1999, the contribution of private investment stood at 13% and rose to 16.2% in 2002 but declined once again to 12% in 2005 (Ekpo, Citation2016).

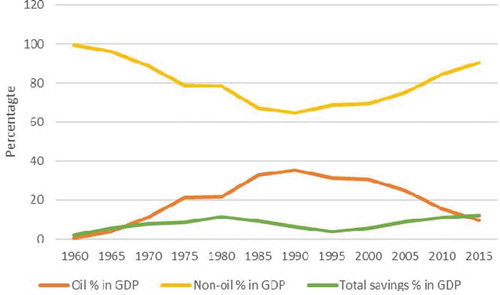

Based on this backdrop, the contributions of oil and non-oil to GDP in Nigeria have varied overtime. As shown in Figure , the contribution of non-oil sector in GDP contracted sharply during the oil boom in 1770s and 1980s, and savings generally slowed more gradually during this period and this low national savings will undesirably affect mobilization of financial resources by the financial institution which will in turn reduce the available fund for investment and thereby inhibiting growth (Obamuyi & Olorunfemi, Citation2011). A fall in international crude oil price mirrored a decrease in oil sector contribution to GDP while non-oil sector has shown a trend of recovery since then.

Figure 1. Share of the oil, non-oil sector and national savings (% of GDP).

Hence, oil-dominant economy may not only hinder financial system development but could also lead to low growth due to weak financial system development that serve as an engine for economic growth (Kurronen, Citation2015). Furthermore, Beck (Citation2011) argued that the dichotomy in the finance-growth nexus in the oil-dependent economy is due to structural differences and the role financial institutions play in different countries. His empirical result submits that the finance-growth nexus has no significant difference in both oil-rich and non-oil rich economies. However, by considering the degree of oil dependence, Beck found that nations that rely heavily on oil-export tend to have lesser financial system development and as such allocate little credit to the private sector, notwithstanding the huge amount of oil rent.

Following the conflicting views, it is very crucial to examine the effect of financial system development on oil-rich economy of Nigeria as few empirical studies that tried to validate the association between financial system development and economic growth in oil-dominant economy, ended with divergent views. To this end, existing studies have left some voids especially in oil-dominant economy like Nigeria where this perspective investigation is lacking. Thus, this investigation is important as there is a potential in structurally moderating the finance-growth relationship that previous studies have not rigorously investigated. To fill this void, this paper innovatively unravels the impact of finance on the oil-rich economy of Nigeria in two-folds. First, this paper examines the relationships in two distinct models via oil and non-oil sector growth using Nigerian data. The motive for the departure from the previous studies stems from the fact that lumping oil and non-oil sector growth in the same analysis in an oil-dominant economy could lead to a biased result because of the crowding effect of the oil sector on non-oil sector. Therefore, to generalize the impact of financial system development on economic growth in an oil-dominant economy without identifying the direction of the impact for policy action can be misleading because the impact may be conditioned by sectors. This outcome is fundamental for policy formulation and implementation.

Second, there is no recognized consensus as to which variable is best suited to measure financial system development in Nigeria. Studies that investigated the finance-growth nexus with different measures subsequently come up with deferent results like in the case of King and Levine (Citation1993), Agu and Chukwu (Citation2008), Ibrahim and Shuaibu (Citation2013), and Oriavwote and Eshenake (Citation2014). In-depth review of existing literature indicates that the differences in empirical result are because of differences in the variables used to measure financial system development. This is in line with Agu and Chukwu (Citation2008) who empirically argued that the choice of proxy for financial system development influences the association of financial system development and economic growth. This study, therefore, departs from the usual yet questionable approach of measuring financial system development to build an index that captured overall characteristics of development in the financial sector using Principal Components Analysis (PCA) (Çoban & Topcu, Citation2013; Samargandi, Fidrmuc and Ghosh, Citation2014). Also, the use of PCA overcomes the problem of multicollinearity usually observed when using a closely related variable. This paper, therefore, tends to bridge these gaps in the literature.

The pertinent question to address in this study is “does financial system development effect differs from oil and non-oil sector growth in Nigeria?” The findings of this paper could be substantial to policy-makers in Nigeria and other oil-dominant nations may wish to know the independent impacts of financial system development on the growth of oil and non-oil sector.

2. Brief literature review

Plethora of empirical literature exists on the finance-growth nexus. However, this study recognizes but eschews other literature and focuses only on recent studies based on oil-rich economies. Nili and Rastad (Citation2007) conducted a comparative study on the impact of financial system development on economic growth for 12 oil-rich countries and 132 non-oil rich countries for the period 1992–2001. The result indicates that the dominant role of the public sector in resource allocation resulting from oil wealth leads to weaker investment quality in oil economies with an underdeveloped financial system leading to insignificant growth. Similarly, Beck (Citation2011) examined whether finance-growth nexus for 153 countries portend a similar effect in both oil-dominant countries and non-oil-dominant countries for the period 1980–2007. Their findings showed that economies that rely heavily on natural endowment tend to have weak financial system development with little or no credit to the private sector and low stock market capitalization. Samargandi et al. (Citation2014) examined the influence financial system development has on oil and non-oil sector of Saudi Arabia over the period 1968 to 2010. The paper shows that in oil-rich economy, financial system development has a negative effect on oil sector growth whereas the non-oil sector has a positive effect on non-oil sector growth. A similar result was also found in the banking sector impact on growth. For example, Barajas et al. (Citation2016) discovered a weaker impact of the banking sector in the growth process of 146 oil-exporting nations over the period 1975–2005. Badeeb et al. (Citation2016) also investigated the presence of oil curse in the finance and economic growth relationship in Malaysia. The authors revealed via investment quality and quantitative channel that oil resources have insignificant and/or indirect effect on finance and economic growth relationship. Nwani and Orie (Citation2016) studied finance-growth nexus by distinguishing financial system development into a bank base and market base financial institution for the period 1981 to 2014 using ARDL model. The findings indicate that both bank base and market base financial system development has an insignificant contribution to economic growth in Nigeria. The authors attributed their findings to the dominant role of the oil sector in Nigeria’s economy. However, Badeeb and Lean (Citation2017) reveal that even though natural wealth impedes growth, an in-depth financial sector is capable of nullifying the resource cause into blessing.

The framework of this study is anchored on supply leading hypothesis. The hypothesis states that supply creates its own demand. This means that supply of credit by financial system will create firms’ demand for that credit to finance economic investment. The proponent of this hypothesis is Schumpeter (Citation1911) and supported by Gurley and Shaw (Citation1967), King and Levine (Citation1993), and McKinnon (Citation2010) among other. The empirical evidence supports that financial dept spurs growth in an economy by revealing that supply of financial services create its demand and thus afford market for individual, firms and government in the modern-growth sectors. This in turn fosters economic growth. A study across 80 economies by King and Levine (Citation1993) using ordinary least square shows that financial system development is a substantial element of the growth process in an economy. The study also identified a causal effect suggesting that repressed financial system development could inhibit growth. A similar study by Ibrahim and Shuaibu (Citation2013) found using the autoregressive distributed lag model and Toda and Yamamoto (1995) augmented Granger causality framework that financial system development promotes growth for the period of the study 1970 to 2010. Karimo and Ogbonna (Citation2017) also used the Toda-Yamamoto augmented Granger causality approach to show the direction of causality between financial development and economic growth in Nigeria. The findings lend support to the supply-leading hypothesis for the period 1970 to 2013. Ogwumike and Salisu (Citation2012) employed a vector autoregressive Granger causality approach to investigate finance-growth nexus. The empirical evidence also supports the supply-leading hypothesis.

3. Empirical model and data

The paper adopted the econometric model approach where economic growth is described as a function of financial system development and other factors associated with finance and growth (Levine, Citation1997). However, following Samargandi et al. (Citation2014), economic growth in this study is decomposed into non-oil and oil sector proxied by real gross domestic product of non-oil sector (RGDPN) and real gross domestic product of oil sector (RGDPO). We specified two models with the dependent variable RGDPN for model one and RGDPO for model two. These models are express thus:

where FD denotes the index of financial system development, OILP stands for oil price of the international crude, TO is the trade openness, INV stands for investment and is the error term. The variables in the models are in logarithmic form. However, financial system development variables were converted to logarithmic form after computing the index values.

The study employed annual time-series data that spans through the period 1981–2015. The real GDP data for the non-oil sector and real GDP data for the oil sector are measured as constant 2010 basic price generated from Statistical Bulletin 2018 of the Central Bank of Nigeria. The oil price is measured by international crude Brent spot price (in US dollars per barrel) sourced from world energy BP statistical review in June 2018. The degree of openness to trade is proxied by share of total trade (exports plus imports) to GDP, and the investment variable is proxied by real gross fixed capital formation and both are generated from World Development Indicators (WDI) of the World Bank.

The measurement of financial system development is challenging because there is no uniform agreement as to which measure is most appropriate owing to the wide range of financial services available in the financial sector. Divers financial institutions provide different services to the system. However, bank-based and stock market-based play the most significant role in the developed economy (Kar & Mandal, Citation2014; Rioja & Valev, Citation2014). However, this paper focused mainly on bank-based financial sector for two main reasons. First, empirical evidence has shown that in a developing economy such as Nigeria, the stock market is relatively weak, under-developed and systematically insignificant to stimulate economic growth. Second, time-series data for the stock market within the period of our study for Nigeria is not readily available (see World Bank Financial Structure Database, Citation2012).

Considering Beck et al. (Citation2010) and Cihak et al. (Citation2012), four financial system development variables were chosen. The variables employed are deposit money bank assets to GDP (dbagdp), liquid liabilities as a proportion to GDP (llgdp), private credit as a share to GDP (pcrdbgdp), and ratio financial system deposits to GDP (fdgdp). The four financial system development data were generated from the Financial Structure Database of World Bank 2018. The ratio of money supply (M2) to nominal GDP as a proxy for financial system development was not considered in this study for a reason. King and Levine (Citation1993), and Khan and Senhadji (Citation2003) among other researchers argue that M2/GDP indicator does not capture the ability of financial intermediaries in mobilizing savings and efficient allocation of resources instead it measures the ability of financial intermediaries in providing transaction services and thus, concentrates mainly on the level of monetization. However, in developing countries, monetization can be increased without financial system development occurring (Demetriades & Luintel, Citation1996; Luintel & Khan, Citation1999; Ogwumike & Salisu, Citation2012).

Nonetheless, this paper argues that an index would be more robust to capture various measures of financial system development rather than using either single measure that may not capture the entire aspect of financial system or multiple measures that are usually associated with the problem of multicollinearity. Therefore, in this study, we follow Ang and McKibbin (Citation2007), Çoban and Topcu (Citation2013), and Samargandi et al. (Citation2014), among others, to build an index for financial system development using principal component analysis (PCA) approach that captures several aspects of financial sector at the same time.

4. Methodology: PCA and ARDL model

The main object of PCA is to transform the various indicators into a new index yet maintain all the information and variation available in the dataset within a different set of indicators. PCA is generally utilized as a method of reducing variables or identifying the pattern and nature of association amongst variables included in the model. PCA aggregate the individual variable information in the model into mutually independent principal components. Every principal component is the weighted average of the overall variables and the weights is that form the new index is computed on the inner correlation of all the individual variables. The number of principal components created are generally uncorrelated and while the first principal component typically has the highest variation of the original variables and thus, stands to be the best and selected principal component to represent the aggregate measure of financial system development (see Ang & McKibbin, Citation2007).

By applying the PCA methodology, we build a financial system development index similar to Huang (Citation2011), Saci and Holden (Citation2008), Schwab and Sala-i-Martin (2011), and Çoban and Topcu (Citation2013). Table show the list of variables and their souces, while the result of PCA is shown in Table .

Table 1. List of variables

Table 2. Eigenvalues, proportion and eigenvectors of each first principal component

ARDL model is employed to estimate Equationequation 1(1)

(1) and Equation2

(2)

(2) . Following Pesaran et al. (Citation2001), ARDL is transformed linearly to form unrestricted error correction model (UECM) thereby integrating both short-run information dynamics with that of long-run equilibrium information without loss of information from the long-run equilibrium. Thus, we re-specify Equationequation 1

(1)

(1) and Equation2

(2)

(2) employing the ARDL-UECM framework.

By conducting ARDL bounds testing, two steps are involved. First, we pre-test for long-run relationship by testing for co-integration via OLS regression and Wald Test or F-test. The pre-test for co-integration entails comparing F-statistic computed with that of the generated upper critical bounds (UCB) and lower critical bounds (LCB) developed by Pesaran et al. (Citation2001) to ascertain whether the null hypothesis should be rejected or not. Null hypothesis (H0) state that

H0: for no co-integration against the alternative

H1: for co-integration.

The series are co-integrated if F-statistic computed is greater than the UCB implying that H0 of no co-integration is rejected; and not co-integrated if F-statistic computed is less than LCB implying that H0 cannot be rejected. However, if the F-statistic computed lies between the UCB and LCB, the test is uncertain. Recently Narayan (Citation2005) has argued that the critical bounds developed by Pesaran et al. (Citation2001) is inappropriate for small samples, therefore they generate a new set of critical values for data with small sample size within the range of 30 to 80 observation which is suitable for our study. Therefore, considering the size of our observation, appropriate critical values will be extracted from the Narayan (Citation2005).

Second, we estimate the long-run coefficient and also use error correction model to estimate short-run dynamics if co-integration is confirmed. To estimate ARDL long-run models we specify Equationequation (5)(5)

(5) and (Equation6

(6)

(6) ) thus:

The optimum lag length P for the autoregressive distributed lag model for Equationequation (5)(5)

(5) and (Equation6

(6)

(6) ) is ascertained by Akaike Information Criterion and Schwarz Information Criteria lag selection criteria with lag combination that minimizes these criteria. Whereas the coefficient of the short-run dynamics is estimated thus:

where ECMt -I = the residual or error correction term ensuing from the tested long-run equilibrium relationship, is the coefficient signifying the speed of adjustment back to the level of long-run equilibrium relationship after a short-run shock, and εt is the white noise.

5. Results and discussion

5.1. Multicollinearity test

To avoid the problem associated with multicollinearity among regressor, correlation test was carried out to investigate the degree of association among the independent variables. The results are presented in Table , which shows that the values of the correlation coefficients were less than 0.8 in absolute terms suggesting the absence of a multicollinearity problem.

Table 3. Correlation matrix

5.2. Unit root analysis of the time series

Even though the ARDL approach does not need the stationarity of series, as it could be used regardless of whether series is integrated of I(0), I(1), or mixture of I(0) and I(1). However, it is worthy to note that the order of integration of the series should not be higher than one. Hence, to ascertain the suitability of ARDL, the stationarity test will confirm whether the order of integration is higher than one or not.

Prior to the unit root test, the study carried out Quandt-Andrews unknown breakpoint test to check the presence of structural break. Quandt-Andrews test result confirmed the presence of structural break in the series. The test confirmed the obvious fact since financial variables included in the model have experienced several structural changes ranging from SAP in 1986 to bank consolidation exercise in 2005. Therefore, the Zivot-Andrews test for unit root, which account for structural breaks was performed to check the orders of integration of the variables. Zivot-Andrews developed three models for unit root test base on the forms of structural break: model A which allows one-time change in the variable in the level form; model B which allows one-time change in the slope of the trend variable; model C which allows a one-time change in the variable at both level and the slope of the trend. Zivot-Andrews specified the three regression models as follow:

where is an indicator dummy variable that capture mean shift occurring at time

(that is at each likely break-date), and

denote shift in the trend occurring at time

. The dummy variables

and

are defined thus:

and

Model C was used for RGDPN because the variable contain trend though the graphic approach was not reported to concise space. Whereas other series, we applied model A. The stochastic test results using the Zivot-Andrews test are shown in Table . The empirical results show that only investment is stationary at a 1% level of significance, whereas all other series are stationary at first difference. This order of integration in Table confirmed the appropriateness of the ARDL model for the analysis of the data.

Table 4. Zivot-Andrews unit root test

5.3. Co-integration test

The ARDL bound test results for co-integration are presented in Table . The result shows that co-integration exists in both Model 1 and Model 2 since the computed F-statistic is greater than the UCB value at the 1% level of significance using unrestricted intercept and restricted trend for model 1 and restricted intercept and no trend in model 2.

Table 5. ARDL bounds co-integration test result

5.4. Long-run impact

Table presents the long-run impact result. The result indicates that financial system development has a positive and significant impacted on non-oil sector growth in Nigeria at a 1% level of significance. The result is supported by the recent study of Samargandi et al. (Citation2014), who find a positive impact of financial system development on non-oil sector growth in Saudi Arabia. The magnitude of this impact is an indication that financial system development is a robust determinant of non-oil sector growth. Our result is also in line with Yuxiang and Chen (Citation2011) who assert that the non-oil sector has a positive relationship with financial system development. The result is also in tandem with supply- leading hypothesis that emphasis the key role of financial system in mobilizing financial resources from the surplus economic agents and allocate them to deficit economic agents which helps in promoting growth in different sectors.

Table 6. Estimated long run coefficients using ARDL approach

Contrarily, in model 2, the impact of financial system development is positive but not significant on oil sector growth in Nigeria. This suggests that although finance may be necessary for economic growth, the capacity of the financial institution to mobilize resources from the surplus savings to deficit spending is weak in the oil sector. The finding is consistent with Samargandi et al. (Citation2014) who found in Saudi Arabia that financial system development does not have any effect on oil sector growth. This empirical finding could be a result of exclusive control of the oil sector by the government and the attendant oil rent is large enough to finance not only itself but also the economy as a whole resulting in natural resource curse in financial system development. This entails that financial system development plays an insignificant role in the growth of the oil sector. The implication is that the impact of financial system development on the whole economy may disappear in an oil-dependent economy because financing policies that improve other real sectors of the economy may receive less support in the presence of oil rent (Barajas et al. 2013). Similarly, Kurronen (Citation2015) argued that firms in oil sector depend less on external finance and thus, credit demand in the oil sector could be very little leading to smaller and less sensitive financial system. The coefficient of oil price is positively related to the growth of the non-oil sector. The result is consistent with Nwani and Orie (Citation2016). The result means that one percentage rise in oil price will lead to 0.46% and 0.25% increase in economic growth in non-oil and oil sector respectively. This finding is not surprising in an oil rich economy, suggesting that oil price is substantial in spurring growth in Nigeria.

Exploring the contributions of other control variables on growth, it can be observed from the findings that among the antecedent of growth, trade openness is negatively correlated to growth which contradict the trade-led growth hypothesis that emphasize that trade openness enhances growth via spillover effects. However, the unexpected result is in line with some previous studies that found trade openness to be negatively related to growth (Khobai et al., Citation2018; Nwafor et al., Citation2005). The potential cause of the adverse relation may not be unconnected to the fact that trade openness leads to decline in fiscal revenue of the state which decreases government savings (Urama et al., Citation2012) This is so especially in Nigeria with mono economy structure that depend hugely on import. Therefore, revenue loss due to tariff cut as a result of trade openness (as in case of ECOWAS and other preferential trade arrangement) may have outweigh the gain from higher trade volume due to trade liberalization (African Trade Policy Centre [ATPC], Citation2004). Furthermore, trade openness has resulted to economic distortions that encourage illegal trade (Folami and Naylor (Citation2017) to such an extent that the net effect of trade openness on economic growth is negligible or even negative (Adeola & Evans, Citation2017; Shittu, Citation2012). In contrast, trade openness has a positive and significant impact on the oil sector. The result appears to confirm a well-known fact that oil exports in Nigeria contribute more than 80% of her total export earnings suggesting a high degree of openness in the oil sector. The findings also show that international oil price impact positively and significantly on both oil and non-oil sector in Nigeria.

The result also shows that the impact of investment on both oil and non-oil sector in Nigeria is negative and significant. A study by Nwabu (Citation2005) affirms to this relationship. Even though literature has identified a share of investment as a robust factor for economic growth, empirical evidence has shown that in the oil-dependent economy, investment has a poor quality (Nili & Rastad, Citation2007). The poor quality may be attributed to inefficiency in the use of capital since a state with high volume of unearned income such as oil rent, implicitly have less incentive to optimize the resources (Bräutigam & Knack, Citation2004). For instance, the channel through which financial system development spur growth is by allocation of resources both in quantity and quality to productive investment. In an oil rich economy, most of the investible fund originate from oil revenue, where surprisingly financial system development is weak. Thus, the oil driven investible fund would be inefficiently allocated to the extent that the net effect on growth could be insignificant or even negative. These suggest that while financial system development could be directly weakened in oil-dominant economy, investment is indirectly weakened through inefficient allocation. This argument is supported in the work of Omotor (Citation2007) who found that investment is negatively linked to growth in Nigeria.

5.5. Short-run impact and adjustment

Table reports the empirical results of the short-run (error correction model) for the two specifications. From the model results, the parameter of the error-correction term at a 1% level of significance is found to be negative thereby validating the earlier established long-run relationship between dependent and independent variables. The magnitude of this coefficient (−0.38) implies that the speed of adjustment back to the equilibrium state whenever there is a shock in the previous year is 4.56 and 7.20 months in non-oil and oil sector respectively.

Table 7. Short-run error correction estimates

5.6. Results of diagnostic tests

The diagnostic test result is reported in Table to evaluate the model findings. The test includes the serial correlation, heteroscedasticity, and functional form. For serial correlation, the p-value of the Chi-Square distribution is higher than the 5% significance level. Thus, we do not reject the null hypothesis and admit that the error term is not serially correlated in the model and no heteroscedasticity. The Ramsey reset test also shows that the functional form for the models is well specified.

Table 8. ARDL-VECM model diagnostic tests

5.7. Model stability test

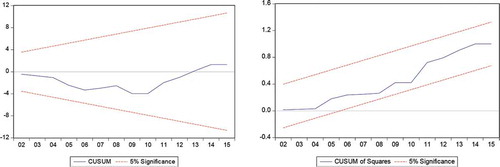

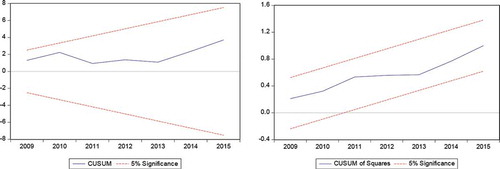

CUSUM and CUMSUMSQ test results are reported in Figures and show the stability of long- and short-run coefficients in the model. The plot in Figures and indicate that CUSUM and CUSUMSQ statistics are within the 5 percent critical bound. This implies that all the coefficients in the models are stable.

Figure 2. Plot of CUSUM and CUSUMSQ for coefficient stability for ECM model (1).

Figure 3. Plot of CUSUM and CUSUMSQ for coefficient stability for ECM model (2).

6. Conclusion, policy implication and recommendation

The paper studied the impact of financial system development and economic growth in an oil-dominant economy of Nigeria from 1981 to 2015. The study distinguished the impact of financial system development on the non-oil sector from the impact of financial system development on the oil sector by disaggregating the real sector growth into the oil sector and non-oil sector growth. Four financial system development variables (deposit money bank assets to GDP (dbagdp), liquid liabilities as a proportion to GDP (llgdp), financial system deposits as percentage of GDP (fdgdp) and ratio of private credit to GDP (pcrdbgdp) were used to construct financial system development index using principal component analysis, in addition to other control variables like oil price, investment and trade openness. The study applied the ARDL test techniques to establish the short-run dynamics and long-run impact in the model. The choice in favour of ARDL became necessary due to the order of integration of the series.

From the analysis, the study discover that financial system development is a significant determinant in the path to achieve non-oil sector growth while financial system development is insignificant in the path to achieving the growth of the oil sector in Nigeria. The implication of this result could imply that the insignificant impact of financial system development on oil sector might outweigh the significant impact of financial system development on non-oil sector. This is possible considering the inherent economic nature of Nigeria, which is predominantly an oil-dominant economy suggesting that the impact of financial system development on the overall economy might be insignificant. For instance, Nwani and Orie (Citation2016) find that financial system development impact is insignificant in the oil-dependent economy of Nigeria. Therefore, the imbalances in the financial system development pattern in the real sectors (oil and non-oil) of the economy in Nigeria undermine the objective of building productive capacity for structural transformation and economic growth. This also has lots of implications on the country’s structural transformation through trade openness. In the presence of natural resource curse, no matter how wide open an economy is, such a country will never attract the necessary growth required to transform the economy. However, Badeeb et al. (Citation2017) found that a well financial sector development is capable of transforming oil resource curse into blessing by appropriate allocation of domestic savings including oil rent to productive investment. Several diagnostic tests were employed to ascertain the reliability of our findings on both short-run and long-run models. The results show that both models pass through all the tests validating the stability of the model. CUSUM and CUSUMSQ also provide evidence in support of the stability of the model.

Based on the aforementioned, there is possibility that public office holder may be exploiting the dominant role of public sector in resource allocation driven by oil revenue to conceal rent-seeking behaviours which ultimately shift financial resources away from the financial sector resulting in weak financial development. Thus, the policy implications of this paper are quite clear. Weak financial system development in general and oil-sector in particular, can be overcome with better and reformed financial institutions. Therefore, the study recommends that financial sector should be more involved in productive investment activities to enhance its role in fostering non-oil growth. To achieve this objective, a well-structured financial reform is needed to lessen the dominance of the oil sector in resource allocation, and strengthen the resource mobilization and allocation efficiency in the financial intermediary sector. In this regard, policymakers should consider channelling the sovereign wealth fund (that is, national savings from oil rent) to non-oil sector through development banks whose responsibility includes empowering productive firms. Additionally, policy makers should channel the high receipts from the export of crude oil through the CBN-Anchor Borrowers’ Programme (ABP). ABP is CBN financial intervention programme established in 2015 to create economic linkage between smallholder farmers and sound large-scale processors with a view to increasing agricultural output. The programme thrust of the ABP is to increase banks’ financing to the agricultural sector to boost production. These policies and programmes of the government will provide financial system development with sufficient credit to private sector vis-à-vis non-oil sector.

Additional information

Funding

Notes on contributors

Oliver E. Ogbonna

Ogbonna E. Oliver is currently a PhD student in the Department of Economics, University of Nigeria Nsukka, Enugu State, Nigeria. As a researcher in the fields of development Economics, he specializes on areas related to Macroeconomic Modelling and Forecasting, Monetary and Financial Economics, and International Economics.

Ikechukwu A. Mobosi

Ikechukwu Andrew Mobosi is a PhD candidate at the level of final report in the Department of Economics, University of Nigeria Nsukka, Enugu State, Nigeria. He specializes in quantitative Economics.

Okwudili W. Ugwuoke

Okwudili Walter Ugwuok is postgraduate student in the Department of Economics, Federal University Lafia, Nasarawa State, Nigeria. His research interest is on Development economics.

References

- Adeola, O., & Evans, O. (2017). Financial inclusion, financial development, and economic diversification in Nigeria. The Journal of Developing Areas, 51(3), 1–16. https://doi.org/10.1353/jda.2017.0057

- African Trade Policy Centre (ATPC). (2004). Fiscal implications of trade liberalization on African countries (African Trade Policy Centre (ATPC) work in Progress, No. 5), United Nations. Economic Commission for Africa.

- Agu, C. C., & Chukwu, J. O. (2008). Toda and Yamamoto causality tests between “bank based” financial deepening and economic growth in Nigeria. European Journal of Social Science, 7(2), 189–198.

- Ang, J. B., & McKibbin, W. J. (2007). Financial liberalization, financial sector development and growth: Evidence from Malaysia. Journal of Development Economics, 84(1), 215–233. https://doi.org/10.1016/j.jdeveco.2006.11.006

- Badeeb, R. A., Lean, H. H., & Clark, J. (2017). The evolution of the natural resource curse thesis: A critical literature survey. Resources Policy, 51(1), 123–134. https://doi.org/10.1016/j.resourpol.2016.10.015

- Badeeb, R. A., Lean, H. H., & Smyth, R. (2016). Oil curse and finance–growth nexus in Malaysia: The role of investment. Energy Economics, 57(5), 154–165. https://doi.org/10.1016/j.eneco.2016.04.020

- Barajas, A., Chami, R., & Seyed Reza, Y. (2016). The finance and growth nexus re-examined: Do all countries benefit equally? Journal of Banking and Financial Economics, 1(5), 5–38. https://doi.org/10.7172/2353-6845.jbfe.2016.1.1

- Beck, T. (2011). Finance and oil: Is there a resource curse in financial system development? (European Banking Centre Discussion Paper No. 2011–007). Tilburg University.

- Beck, T., Demirgüç-Kunt, A., & Levine, R. (2010). Financial institutions and markets across countries and over time: The updated financial system development and structure database. The World Bank Economic Review, 24(1), 77–92. https://doi.org/10.1093/wber/lhp016

- Bräutigam, D. A., & Knack, S. (2004). Foreign aid, institutions, and governance in sub-Saharan Africa. Economic Development and Cultural Change, 52(2), 255–285. https://doi.org/10.1086/380592

- Cihak, M., Demirguš-Kunt, A., Feyen, E., & Levine, R. (2012). Benchmarking financial system development Around the World (Policy Research Working Paper, (6175)).

- Çoban, S., & Topcu, M. (2013). The nexus between financial system development and energy consumption in the EU: A dynamic panel data analysis. Energy Economics, 39, 81–88. https://doi.org/10.1016/j.eneco.2013.04.001

- Demetriades, P. O., & Luintel, K. B. (1996). Financial system development, economic growth and banking sector controls: Evidence from India. The Economic Journal, 359–374. https://doi.org/10.2307/2235252

- Ekpo, U. N. (2016). Determinants of private investment in Nigeria: An empirical exploration. Journal of Economics and Sustainable Development, 7(11), 80–92.

- Folami, O. M., & Naylor, R. J. (2017). Police and cross-border crime in an era of globalisation: The case of the Benin–Nigeria border. Security Journal, 30(3), 859–879. https://doi.org/10.1057/sj.2015.17

- Greenwood, J., & Jovanovic, B. (1990). Financial system development, growth, and the distribution of income. Journal of Political Economy, 98(5, Part 1), 1076–1107. https://doi.org/10.1086/261720

- Gurley, J. G., & Shaw, E. S. (1967). Financial structure and economic development. Economic Development and Cultural Change, 15(3), 257–268. https://doi.org/10.1086/450226

- Huang, Y. (2011). Determinants of financial system development. Palgrave Macmillan.

- Ibrahim, T. M., & Shuaibu, M. I. (2013). Financial system development: A Fillip or Impediment to Nigeria’s Economic Growth. International Journal of Economics and Financial Issues, 3(2), 305–318.

- Kar, S., & Mandal, K. (2014). Re-examining the finance-growth relationship for a developing economy: A time series analysis of post-reform India. The Journal of Developing Areas, 48(1), 83–105. https://doi.org/10.1353/jda.2014.0017

- Karimo, T. M., & Ogbonna, O. E. (2017). Financial deepening and economic growth nexus in Nigeria: Supply-leading or demand-following? Economies, 5(1), 4. https://doi.org/10.3390/economies5010004

- Khan, M. S., & Senhadji, A. S. (2003). Financial system development and economic growth: A review and new evidence. Journal of African Economies, 12(2), ii89–ii110. https://doi.org/10.1093/jae/12.suppl_2.ii89

- Khobai, H., Kolisi, N., & Moyo, C. (2018). The relationship between trade openness and economic growth: The case of Ghana and Nigeria. International Journal of Economics and Financial Issues, 8(1), 77.

- King, R. G., & Levine, R. (1993). Finance and growth: Schumpeter might be right. The Quarterly Journal of Economics, 108(3), 717–737. https://doi.org/10.2307/2118406

- Kurronen, S. (2015). Financial sector in resource-dependent economies. Emerging Markets Review, 23, 208–229. https://doi.org/10.1016/j.ememar.2015.04.010

- Levine, R. (1997). Desarrollo financiero y crecimiento económico: Puntos de vista y agenda. The Economic Journal, 35(2), 688–726.

- Luintel, K. B., & Khan, M. (1999). A quantitative reassessment of the finance–growth nexus: Evidence from a multivariate VAR. Journal of Development Economics, 60(2), 381–405. https://doi.org/10.1016/S0304-3878(99)00045-0

- McKinnon, R. I. (2010). Money and capital in economic development. Brookings Institution Press.

- Narayan, P. K. (2005). The saving and investment nexus for China: Evidence from cointegration tests. Applied Economics, 37(17), 1979–1990. https://doi.org/10.1080/00036840500278103

- Nili, M., & Rastad, M. (2007). Addressing the growth failure of the oil economies: The role of financial system development. The Quarterly Review of Economics and Finance, 46(5), 726–740. https://doi.org/10.1016/j.qref.2006.08.007

- Nwabu, G. (2005). Human capital investment, growth and poverty reduction in Sub-Saharan Africa. In AERC Senior Policy Seminar VII, African Economic Research Consortium.

- Nwafor, M., Ogujiuba, K., & Adeola, A. (2005). The impact of trade liberalization on poverty in Nigeria: Micro simulation in A CGE Model (Interim report to the PEP Research Network).

- Nwani, C., & Orie, B. J. (2016). Economic growth in oil-exporting countries: Do stock market and banking sector development matter? Evidence from Nigeria. Cogent Economics and Finance, 4(1), 1153872. https://doi.org/10.1080/23322039.2016.1153872

- Obamuyi, T. M., & Olorunfemi, S. (2011). Financial reforms, interest rate behaviour and economic growth in Nigeria. Journal of Applied Finance & Banking, 1(4), 39–55.

- Ogwumike, F. O., & Salisu, A. A. (2012). Financial system development and economic growth in Nigeria. Journal of Monetary and Economic Integration, 12(2), 91–119.

- Ohiorhenuan, J. F. (1990). The industrialisation of very late starters: Historical experience, prospects, and strategic options for Nigeria (Discussion Paper No. 273). Institute of Development Studies at the University of Sussex.

- Omotor, D. (2007). Financial system development and economic growth: Empirical evidence from Nigeria. The Nigerian Journal of Economic and Social Studies, 49(2), 209–233.

- Oriavwote, V. E., & Eshenake, S. J. (2014). An empirical assessment of financial sector development and economic growth in Nigeria. International Review of Management and Business Research, 3(1), 139.

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289–326. https://doi.org/10.1002/jae.616

- Rioja, F., & Valev, N. (2014). Stock markets, banks and the sources of economic growth in low- and high-income countries. Journal of Economics and Finance, 38(2), 302–320. https://doi.org/10.1007/s12197-011-9218-3

- Saci, K., & Holden, K. (2008). Evidence on growth and financial system development using principal components. Applied Financial Economics, 18(19), 1549–1560. https://doi.org/10.1080/09603100701720286

- Samargandi, N., Fidrmuc, J., & Ghosh, S. (2014). Financial system development and economic growth in an oil-rich economy: The case of Saudi Arabia. Economic Modelling, 43, 267–278. https://doi.org/10.1016/j.econmod.2014.07.042

- Schumpeter, J. A. (1911). The theory of economic development. Harvard University Press.

- Shittu, A. I. (2012). Financial intermediation and economic growth in Nigeria. British Journal of Arts and Social Sciences, 4(2), 164–179.

- Urama, N., Nwosu, E. O., & Aneke, G. (2012). Lost revenue due to trade liberalization: Can Nigeria recover her own? European Journal of Business and Management, 4, 10.

- World Bank Financial Structure Database. (2012) World Bank World Development Indicators (WDI) Database. http://econ.worldbank.org/http://data.worldbank.org/data-catalog/world-development-indicators

- Yuxiang, K., & Chen, Z. (2011). Resource abundance and financial system development: Evidence from China. Resources Policy, 36(1), 72–79. https://doi.org/10.1016/j.resourpol.2010.05.002