?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The primary aim of the present research was to fill the significant gap in the accounting literature, which is widely acknowledged, regarding the association between conservative accounting and the value of cash, particularly in emerging Islamic stock markets. By using a sample including all the firms listed on the Tehran Stock Exchange from 2008 to 2017, we regress the value of cash on accounting conservatism with regard to the moderator role of audit quality (audit tenure, audit opinion, audit size, and earnings management as proxies for audit quality). Generally, the findings not only confirm a positive relationship between accounting conservatism and cash value in the absence of audit quality but also suggest that ignoring the important role of audit quality mechanism can result in wrong conclusions concerning the effect of accounting conservatism on cash value, especially in developing countries such as Iran, due to concentrated government and institutional ownership structures. This cross-sectional analysis based on firm growth leads to the conclusion that analysis regarding the relationship between accounting conservatism and cash value must be taken into account by highlighting the impact of macroeconomic variables and political economy. Furthermore, the findings of the current study suggest that the application of monitoring and controlling theories calls for more inquiry.

PUBLIC INTEREST STATEMENT

Accounting conservatism in the form of asymmetrically timely gain and loss recognition, increase the value of a firm’s cash holdings. For reasons related to either higher levels of cash flow sensitivity or high financing costs, many firms accept a conservative approach to cash holdings policies. The findings not only confirm a positive relationship between accounting conservatism and cash value in the absence of audit quality but also suggest that ignoring the important role of audit quality mechanism can result in wrong conclusions concerning the effect of accounting conservatism on cash value, especially in developing countries such as Iran, due to concentrated government and institutional ownership structures.

1. Introduction

The current research attempts to clarify the role of audit quality and firm growth either as corporate governance mechanisms or firm value factors affecting the relationship between accounting conservatism and the cash value. For reasons related to either higher levels of cash-flow sensitivity or high financing costs, many firms accept a conservative approach to cashholding policies (Bernstein, Citation1994). Based on Aghaei et al.’s study (Aghaei et al., Citation2010) Iranian firms that hold large amounts of cash are increasingly unlikely to invest in projects or distribute them to shareholders, but the greater potential for incorrect use of CEOs raises questions about the practice of increasing cash value by holding large amounts of cash.

The conservatism principle recognizes expenses and liabilities as soon as possible when there is uncertainty about the outcome, but only recognizes revenues and assets when they are assured of being received. Thus, the accounting conservatism principle leads to enhanced value of firm cash flow (Louis et al., Citation2012). This practice, which is known as asymmetric timing, has a conservative impact on earnings. Conservative accounting system can mitigate the agency problem between the manager and shareholders of a firm, which arises from information asymmetry (Lee, Citation2014). Consequently, the conservative accounting structure is considered as both helpful in decreasing agency problems and increasing company performance by reducing the possibility for lower value of cash in firms linked to decisions made causing problems of overinvestment (Louis et al., Citation2012). In this study, we will study the issue that companies that accept conservatism are less likely to be involved in overinvestment activity owing to the timely recognition of losses restricting the amount of discretionary cash flow by managers. Also, when conservative accounting structures are utilized, stockholders and the board are more likely to both detect unsuitable investment plans and to lobby for more appropriate management decisions (Louis et al., Citation2012; Watts, Citation2003).

The value of an additional dollar in cash holdings increases in accounting conservatism, suggesting that accounting conservatism is associated with a more efficient use of cash holdings (Louis et al., Citation2012). The origin of many topics on cash value is asymmetric information. The value of firm cash holdings is lower in states with a higher degree of asymmetric information (Drobetz et al., Citation2010). Corporate cash value and asymmetric information are strongly interrelated. The information asymmetry aspect of agency theory constitutes a relevant risk and hinders principal-agent relationships. Cash can be a curse and a blessing; cash is more valuable for financially constrained firms than for unconstrained firms and less valuable for poorly governed firms than for well-governed firms (Dogru & Bulut, Citation2018). According to agency theory, prior research shows that, the abuse of cash by managers can, in turn, make investors consider cash as being of lower value. For example, Dittmar and Mahrt-Smith (Citation2007) state that the value of cash holdings will be decreased by weak corporate governance. In other words, a higher level of audit quality would encourage managers to present high-quality financial reporting. Consequently, it will encourage owners to monitor and control.

Non-quality profits lead to an abnormal allocation of resources from the perspective of investors. Financial statement quality will be improved by auditing, standards development, and some other instruments (Healy & Palepu, Citation2001). And this leads to a reduction in information asymmetries among stakeholders. The mentioned relationship can be explained from different viewpoints. First, high-quality disclosure leads to a reduction in information asymmetries among decision makers. Secondly, the disclosure of information publicly can prevent the distribution of inappropriate information (Shehata, Citation2014). In addition, improving information quality reduces the expected abnormal return. Information asymmetry between the board and investors is one of the reasons for earnings management. Reducing information asymmetry leads to information gap fulfillment process between managers and others. Also, this decreases managers’ ability with respect to earnings management. On the other hand, there is a negative and significant relationship between earnings management and accounting conservatism (Etemadi et al., Citation2012).

In the current research, the impact of audit quality specific-indicators (as proxies: audit tenure, audit opinion, audit size, and earnings management) on cash value has been considered. Audit quality was recognized as the degree to which an audit report is free from deficiencies and distortions which can show themselves later on. The quality of an audit was measured in terms of an auditor’s ability to report financial distortions willingly and without bias. Recent research has shown that the audit quality in Iran is at a low level (Mahdavi & Namazi, Citation2017; Etemadi & Abdoli, Citation2018). Alavi-Tabari and Haji-Moradkhani (Citation2015) state that for increasing audit quality, we must do the following things; determine audit fees, revise the auditing instructions, develop ongoing professional education, publish and interpret challenging accounting standards, develop continuous auditing. Audit quality and firm growth play key roles in agency relationship and cash-holding policies that further affect the value of cash.

According to Louis et al. (Citation2012) and Lin et al. (Citation2018) accounting conservatism in the form of asymmetrically timely gain and loss recognition, increase the value of a firm’s cash holdings. We will use Louis et al.’s work as a starting point to examine links among audit quality, firm growth, accounting conservatism, and cash value. The current research aimed to determine whether there is a positive relationship between accounting conservatism and cash value depending on the higher level of audit quality or lower level of audit quality and firm growth. Our results are useful for informing policymakers. Therefore, the present study sought to fill the investigational gap in examining the relationship between cash value and accounting conservatism as well as determining the effect of different auditing quality indexes on such relationships in the companies listed on TSE.

Section 2 introduces the theoretical background, presents our hypotheses, and reviews the related literature. Section 3 describes the data and explains our empirical methodology. Section 4 reports our main empirical results. Finally, Sections 5 and 6 provide discussion and conclusion and limitation and future research respectively.

2. Background and hypotheses development

2.1. Accounting conservatism and cash value

Accountants traditionally expressed conservatism in this way, “anticipate no profits but anticipate all losses” (e.g., Bliss, Citation1924; Basu, Citation1997). Prior research suggests two alternative perspectives on the relationship between accounting conservatism and corporate governance. First, the contractual role of accounting leads to accounting conservatism (Watts & Zimmerman, Citation1986). Also, Ahmed and Duellman (Citation2007) showed that accounting conservatism helps the board in resolving agency problems. Hence, bad corporate governance mechanism will require higher levels of conservative accounting. Second, the alternative perspective is that the relationship is positive in that good corporate governance mechanisms bring about better control in top levels of management and thus will favor the utilizing of accounting conservatism (Buallay, Citation2019). Various corporate governance practices may imply different information environments. If conservative accounting is an instrument able to reduce agency problems, it is expected that a weak corporate governance structure will lead to a more important conservative accounting from the stakeholder’s perspective.

It will be argued that firms accepting accounting conservatism practices are less likely to be involved in overinvestment of free cash flow. The managers utilize free cash flow for self-interest and for expanding management tenure (Muller-Kahle et al., Citation2014). This, more likely leads to investing in low-value projects. Consistent with our expectations, significant increase was found in compensation. This is also true with respect to increasing compensation by higher-level firm growth. Therefore, in this situation, we should look for a mechanism to mitigate agency problems between the managers and shareholders. One of the mechanisms is conservative accounting.

The consensus among researchers is that accounting conservatism practices decrease the conflict of interest associated with the conflicting interests between the managers and other stakeholders. In other words, increasing cash value in the future. Therefore, this assertion will be examined through the following established hypothesis:

H1. There is a positive and significant relationship between accounting conservatism and cash value.

2.2. The effect of auditor tenure and audit size on the relationship between conservative accounting and cash value

Recent research asserts that auditor tenure has been a hot topic in auditing literature, particularly since the accounting scandals early in the 21st century. There are two viewpoints concerning the impact of audit tenure on accounting conservatism. First, the competence view: this refers to the prolongation of audit tenure which should allow the auditor to obtain more knowledge about the client’s activities. This brings about better service and audit quality (Azevedo & Costa, Citation2012). Increasing the audit quality as one of the proxies of the quality of accounting information leads to less information asymmetry (Brown et al., Citation2004; Clinch et al., Citation2011). Greater asymmetric information between insiders and other stakeholders results in lower gains and greater losses and larger asymmetric recognition of gains and losses as reflected in present financial statements (Chi et al., Citation2009). In addition, asymmetric information leads to conservative accounting. Thus, we expect a positive influence of audit tenure on conservative accounting.

Second, the independence view: this refers to a longer relationship which leads to the auditor having greater proximity to clients, which negatively affects the quality of services provided. Regulators and the public have expressed concerns that prolongation of audit tenure may diminish auditor independence, objectivity, and thus audit quality. With regard to the first viewpoint, we predict a negative relationship between audit tenure and conservative accounting. Thus, modified impact of audit tenure on the relationship between accounting conservatism and cash value is predictable.

Also, there are two viewpoints regarding the impact of audit size on audit quality. Recent research has shown that there is a positive relationship between audit quality and audit size (e.g. Deltas & Doogar, Citation2004; Fuerman, Citation2006; Wang et al., Citation2014). On the other hand, many researchers have argued that “big audit firms” might not always provide higher audit quality compared to others (e.g., Salehi et al., Citation2008). Also, Knechel (Citation2009) demonstrated that audit quality depends essentially on clients’ specific characteristics. Based on previous arguments it is clear that we cannot consider negative or positive impacts of audit size on conservative accounting. Thus, ambiguous influence of audit size on the relationship between accounting conservatism and cash value is approved. Therefore, our next hypotheses are established as follows:

H2. The incentive effects of audit tenure increase (decrease) the positive influences of conservative accounting structure on cash value.

H3. The incentive effects of audit size increase (decrease) the positive influences of conservative accounting structure on cash value.

2.3. The effect of audit opinion on the relationship between conservative accounting and cash value

Audit opinion has been seen as an audit quality proxy (Blacconiere & DeFond, Citation1997; M. DeFond & Zhang, Citation2014). Recent research asserts that higher audit quality plays a key role in decreasing earnings management through accrual accounting and it may improve earnings quality (Lin & Hwang, Citation2010; Chen et al., Citation2011). We would most likely justify this negative association by increasing future litigation. Also, companies with a higher level of abnormal accruals experience worse stock return performance in the following period (Alhadab & Clacher, Citation2018). When we compare low and high-quality audit firms, high-quality auditors carry out scrutiny of financial statements to prevent any litigation by other stakeholders (Hogan, Citation1997). Heninger (Citation2001) asserts that the litigation risk is positively related to the increase of income abnormal accrual. Auditors, therefore, face a higher litigation risk if client undertake greater accrual earnings management. In comparison with good news, bad news leads to further fluctuations in earnings and returns. Given this argument, when analyzing earnings conservatism, utilizing a Basu (Citation1997) regression, the differential bad news coefficient with respect to good news is abnormally inflated (Lara et al., Citation2007). Thus, we predict a negative and significant relationship between earnings management and conservative accounting. This means that audit quality increases the positive influences of conservative accounting structure on cash value. Accordingly, the fourth hypothesis is expressed as follows:

H4. The incentive effects of audit opinion increase the positive influences of conservative accounting structure on cash value.

2.4. The effect of earnings management on the relationship between conservative accounting and cash value

Managers can influence accounting conservatism (based on good news-bad news) through accrual and real activities. Lara et al. (Citation2007) show that managers utilized the upward earnings management, pre-bankruptcy. Also, they demonstrated that earnings management in distressed firms leads to a decrease in the accounting conservatism as a proxy of accounting information reliability. In other words, compensation (Meek et al., Citation2007; Almadi & Lazic, Citation2016), earnings smoothing (DeFond & Park, Citation1997; Li & Richie, Citation2016), reputation (Beyer & Dye, Citation2012; Gonzalez & Garcia-Meca, Citation2014), and bankruptcy (Habib et al., Citation2013; Campa & Camacho-Minano, Citation2015) are factors affecting earnings management. Based on the aforementioned incentives, we predict a reduction of accounting information reliability and conservative accounting (e.g., Lara et al., Citation2007; Etemadi et al., Citation2012). Thus, it seems earnings management diminishes conservative accounting and consequently, leads to a reduction of the firms’ cash value. In sum, the above arguments will be tested empirically through the following hypothesis.

H5. The incentive effects of earnings management decrease the positive influences of conservative accounting structure on cash value.

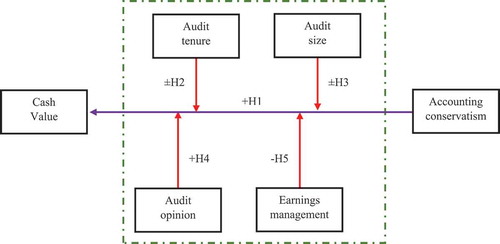

Finally, based on the aforementioned argument, we assert that firms with higher growth could mitigate the positive relationship between accounting conservatism and cash value. Owing to these firms taking on high-risk investment projects they will mitigate the cash value in the future. Conceptual framework of current study is shown in Figure .

Figure 1. Conceptual framework of current research.

Overall, the current study focused on the impact of accounting conservatism on a company’s increased cash value as well as the decisive role of the auditing process in decision-making and cash management. Since the auditing quality is expected to reduce the agency conflict and information asymmetry among the managers and owners and improve the cash efficiency and its effective use through optimal allocation of cash resources and encouraging the companies, hence, the market attaches much more importance to the cash holdings of the companies with high-quality auditing reports. Therefore, directly examining the relationship between the company’s cash value and accounting conservatism, we can also better explain the mentioned relationship, making use of the role of different indexes of auditing quality.

3. Empirical models

Our sample consists of all firms listed (165 firms) on the Tehran Stock Exchange (TSE) between 2008 and 2017. The data derives mainly from audited financial statements and annual board reports of the TSE, and Rahavard Novin software, excluding utilities and financial firms. Furthermore, we omitted observations with missing values on variables utilized in the current research. Table presents the summary statistics of the variables. And Figure shows cash value, accounting conservatism, and growth in the period 2008–2017. We utilized the one-way analysis of variance test (ANOVA) and Kruskal–Wallis test because of determining the difference between industrial sectors based on explanatory and control variables (see Table ). Furthermore, correlation analysis has been demonstrated in Table . After data collection, stationarity and non-stationarity must be ensured to avoid false regression. Since the applied regression method is ordinary data, the ADF-Fisher tests were used. Results are shown in Table .

Table 1. Descriptive statistics and non-parametric method for comparing industrial sectors

Table 2. Correlation matri

Table 3. Null: Unit root (assume common Unit root test)

Table 4. Regression result for specified hypotheses

Table 5. Regression result for first and fourth quarter firm growth

Table 6. Variable definition

The model shown as EquationEquation (1)(1)

(1) is based on the prior literature research (Faulkender & Wang, Citation2006; Louis et al., Citation2012; Lin et al., Citation2018). To examine H1, we estimate this equation without the interaction term. A significantly positive

indicates support for H1.

To examine H2, we estimate EquationEquation (2)(2)

(2) with

the interaction term. H2 is considered supported when β3 is significantly negative (positive).

To examine H3, we estimate EquationEquation (3)(3)

(3) with

the interaction term. H3 is considered supported when β3 is significantly negative (positive).

To examine H4, we estimate EquationEquation (4)(4)

(4) with

the interaction term. H4 is considered supported when β3 is significantly positive.

To examine H5, we estimate EquationEquation (5)(5)

(5) with

the interaction term. H5 is considered supported when β3 is significantly negative.

The mentioned variable definitions are listed in Table , panel A.

This study uses the conditional conservative accounting measurement model by Ball and Shivakumar (Citation2005), namely Asymmetric Accrual to Cash-Flow.

The mentioned variable definitions are listed in Table , panel B. EM is accrual-based earnings management. We estimated discretionary accruals using the performance adjusted modified Jones (Citation1991) model as proposed by DeFond and Jiambalvo (Citation1994) and Kothari et al. (Citation2005). In the model, total accruals are regressed on the difference between change in revenue and change in receivables, gross property, plant, and equipment, and return on assets. The model used for the estimation is:

The model (7) residual refers to the earnings management proxy. Also, the components of EM variables definitions are listed in Table , panel C.

4. Findings

Table presents results from a panel data regression analysis comparing conservative accounting practices across firms with and without audit quality proxies. Based on the first model, first hypotheses results indicate that there is a positive and significant relationship between accounting conservatism and cash value (0.004, t-statistic = 2.05). In other words, firms with a high level of conservatism, can improve the firm’s cash value. This is of utmost importance for stockholders and managers. Both managers and shareholders expect that the higher conservative accounting practice, the higher the level of shareholder’s wealth. This can occur through investing in projects with high levels of profitability. Also, earlier research confirms the mentioned results (Louis et al., Citation2012; Lee, Citation2014; Lin et al., Citation2018).

According to second hypothesis which predicted the audit tenure’s positive or negative possible effect on the relationship between accounting conservatism and cash value; the econometrics results show that audit tenure is negatively and significantly related to accounting conservatism; this means the negative and significant effect of AC*AT on cash value (−0.0068, t = −2.95). Thus, due to a poor corporate governance mechanism, increases in the audit tenure will prevent effective monitoring by auditors and it makes less use of accounting conservatism methods by firm managers and they participate in less risky projects for more cash holdings and this can lead to lack of the firm’s cash optimal uses for profitability in the future and in other words mitigation in value of cash and consequently the firms’ value decrease. Therefore, the key factor in decreasing the effect of auditor’s tenure on conservatism is the lack of main observance that was previously posed. In other words, less manager conservatism should be offset by appropriate corporate governance mechanism, and in this case with an increase in audit tenure as a weakness in corporate governance structure this issue is not realized. In other words, poor corporate governance reduces the positive relationship between conservatism and cash value.

Regarding the third hypothesis which predicted the positive or negative possible effect of audit size on the relationship between accounting conservatism and cash value; the results indicated the negative effect of audit size on accounting conservatism, which indicates that the negative and significant effect of AC*AS on cash value (−0.0107, t = −4.45). As mentioned earlier, conservatism can mitigate the agency costs by reducing the conflict of interests between managers and stockholders. In Iran, the Audit Organization is known as big and monopoly audit firms and its negative effect on audit quality has been considered in many of the related studies (Hassas Yeganeh & Azinfar, Citation2010). Mahdavi and Daryaei (Citation2017) discussed the monopoly relations regarding Iran’s audit market, and this monopoly as an audit quality decreasing factor comes to mind. So, due to governmental ownership and unresponsiveness to professional associations, Iranian audit firms considered the level of audit quality that was based on political relations (e.g., Hassas Yeganeh & Azinfar, Citation2010). A decrease in audit quality which means lack of conservatism monitoring mechanisms, indicates that the relationship between conservatism and cash value is mitigated by the moderator role of audit size.

Based on the fourth hypothesis which predicted the audit tenure’s positive possible effect on the relationship between accounting conservatism and cash value, the econometric results of this hypothesis (model 4) indicated audit opinion as an important factor of corporate governance that actually is a powerful instrument used to control and monitor the behavior of management and enhance the relationship between conservatism and firm value (0.0050, t = 2.77). The findings of this hypothesis are consistent with Etemadi et al. (Citation2012).

Based on the fifth hypothesis in this research, the reducer effect of earning management on the positive relationship between conservatism and firm’s value was not approved (0.0053, t = 0.06). Earning management is an instrument that can lead to a decline in conservatism (upward earning management) and can also increase it (downward earning management). Also, the accrual-based earnings management and real earning management can affect the results. Although many researchers focused on tradeoff between the accrual-based earnings management and real earnings management (Oz & Yelkenci, Citation2018). However, in the current study a rational effect between AC*EM and cash value cannot be found, while earnings management had a downward effect on cash value (−0.0095, t = −2.79).

For a better explanation of the relationship between accounting conservatism and cash value, cross-section data was used during the period 2008–2017 (See Table ). In 2008, higher-growth firms compared with low-growth firms showed that higher-growth is an effective factor for a negative and significant relation between conservatism and cash value. This issue was also repeated in 2010, 2011, 2014, 2015 and 2016. In other years, the positive and significant relation between accounting conservatism and cash value, such as the whole sample, has been confirmed during a period of over 10 years. Based on the current argument, the negative relationship between conservatism and cash value in the aforementioned years refers to the event of a financial crisis, higher—growth firms face less losses when applied less conservatively. Because they have gained the expected growth and investment their surplus financial resources are independent profitable projects with higher risk, which can ultimately lead to an increase in their cash value. In 2008, we faced a global financial crisis and in different periods of time, Iran’s economic situation was under the influence of international sanctions imposed by the United States. Every year, like in 2016, Iran’s economy has been relatively stable. The risk taking of firms with higher growth has led to an increase in their cash value. The cross-sectional analysis leads to the conclusion that analysis relating to the relationship between accounting conservatism and cash value must be carried out by the impact of macroeconomic variables and political economy. The comparison between the adjusted R2 of relationship between independent and control variables with the dependent variable in the analysis of panel and cross-sectional data also shows that in the long run the relationship decreases.

In other words, in the long run, the impact of accounting conservatism on cash value will be influenced by other factors; these factors have not been considered in the present research-specified model.

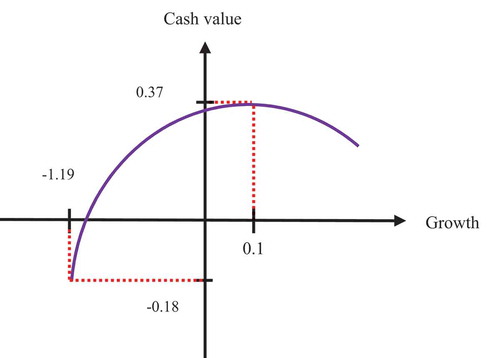

The factors affecting the relationship between accounting conservatism and cash value will be considered, including the macroeconomic factors, as well as the neutralizing effects of corporate governance dimensions on emerging markets such as Iran. Another interesting point in cross-sectional analysis is that higher-growth firms have higher adjusted R2 between independent and dependent variables. This means that the cash value of higher-growth firms can be expected to be more affected than accounting conservatism. Of course, this expectation is consistent with the views of corporate growth as higher-growth firms are more capable of converting financial resources which are more valuable. (For understanding the current argument, see Figures and .)

Figure 2. Cash value tendency and firm growth.

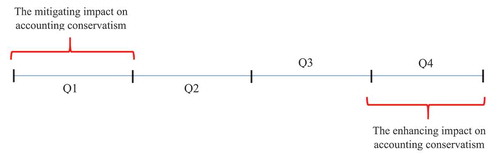

Figure 3. The firm growth and accounting conservatism.

Figure 4. Cash value, accounting conservatism and growth in the period 2008–2017.

5. Discussion and conclusion

The current research employed a sample consisting of all the firms listed on the Tehran Stock Exchange between 2008 and 2017, excluding financial industries, to analyze the roles of audit quality in the relationship between conservative accounting practices and cash holding value. This is a particularly meaningful issue in countries such as Iran. To the best of our knowledge, this is the first attempt to document the relationships among accounting conservatism, cash value, and audit quality. The results show that there is a positive and significant relationship between accounting conservatism and cash value. The most common definition of conservatism is a distinct approach in profits and losses identify. This distinct encounter arises from the different recognition that is considered for profits and losses (Watts, Citation2003). Accounting conservatism with supervision simplification and better managing leads to mitigating the manager’s optimism in financial performance.

Based on the expectation of managers and shareholders, higher accounting conservatism causes an increase in the shareholder’s wealth. This can occur through investing in projects with high level of profitability. When corporate governance mechanism is weak, due to the increase in audit tenure we are faced with ineffective auditor monitoring and managers make less use of accounting conservatism methods and invest in low-level risk projects for more cash holdings which, in turn, can cause a lack of optimal use of cash in the firm cash optimal for future profitability, which means mitigation in the cash value chain ultimately decreases the value of the firm. According to the third hypothesis results, agency costs will be mitigated by conservatism. In Iran, the Audit Organization, as a monopoly audit firm, is an organization in which its negative effect on audit quality has been considered in many researches Figure and .

The result of cross-sectional analysis has shown that in the analysis of the relationship between accounting conservatism and cash value, the effects of macroeconomic variables and political economy analysis should be considered. In comparison with the adjusted R2 of relationship between independent and control variables with the dependent variable in the analysis of panel and cross-sectional data it was found that in the long run, this relationship will decrease. Our econometric results not only confirm a positive relationship between accounting conservatism and cash value in the absence of audit quality but also suggest that ignoring the important role of audit quality mechanism can result in wrong conclusions about the effect of accounting conservatism on cash value, especially in developing countries such as Iran in which a large percentage of firms are characterized by concentrated ownership structures through the government Figure .

6. Limitations and future research

The audit quality framework was used in this investigation, as an important mechanism of corporate governance and a moderator variable for the relationship between cash value and accounting conservatism. Whereas all the mechanisms available in the field of corporate governance (for example, the structures of ownership and board of directors) may play important roles in cash value and the accounting conservatism concept, it is suggested that in future studies the effect of such mechanisms on the relationship between the cash value and accounting conservatism be examined. The lawmakers should create a new and effective law regarding the quality of auditing reports which will reinforce a large part of the corporate governance. The limitations of the present study include the lack of easy access to the information required to process and estimate the hypothesis tests. Additionally, there are unspecified factors in the companies that affect their future events; the lack of sufficient and reliable information in some companies can consecutively lead to their elimination.

Additional information

Funding

Notes on contributors

Abbas Ali Daryaei

Abbas Ali Daryaei received his Ph.D. in accounting from University of Shiraz, Iran in 2015. He is an assistant professor in accounting at Imam Khomeini International University. He has published many books and numerous articles in national and international academic journals. Such as Int. J. Business Forecasting and Marketing Intelligence (Inderscience), Contaduría y Administración (Elsevier), International Journal of Corporate Social Responsibility (Springer), corporate governance (Emerald), The Journal of International Trade & Economic Development (Taylor & Francis Group). Dr Daryaei’s research interests are corporate governance, political economy and auditing.

References

- Aghaei, M., Etemadi, H., Azar, A., & Chalaki, P. (2010). Studding the relationship between corporate governance attributes and the information content of accounting earnings: The role of earnings management. Iranian Journal of Management Sciences, 4 (16), 27–23. (in Persian). https://www.sid.ir/en/journal/ViewPaper.aspx?id=189189

- Ahmed, S., & Duellman, S. (2007). Accounting conservatism and board of director characteristics: An empirical analysis. Journal of Accounting and Economics, 43(2–3), 411–437. https://doi.org/10.1016/j.jacceco.2007.01.005

- Alavi-Tabari, S. H., & Haji-Moradkhani, H. (2015). Relationship between audit quality and stock liquidity. Quarterly Journal of Financial Accounting and Auditing, 9 (19), 503–538. (in Persian). https://www.sid.ir/en/Journal/ViewPaper.aspx?ID=472822

- Alhadab, M., & Clacher, I. (2018). The impact of audit quality on real and accrual earnings management around IPOs. The British Accounting Review, 50(4), 442–461. https://doi.org/10.1016/j.bar.2017.12.003

- Almadi, M., & Lazic, P. (2016). CEO incentive compensation and earnings management: The implications of institutions and governance systems. Management Decision, 54(10), 2447–2461. https://doi.org/10.1108/MD-05-2016-0292

- Azevedo, F. B., & Costa, F. M. (2012). Effete da trocar da firma de auditoria no gerenciamento de resulted das companies aborts brasileiras. RAM Revista De Administração Do Mackenzie, 13(5), 65–100. https://doi.org/10.1590/S1678-69712012000500004

- Ball, R., & Shivakumar, L. (2005). The role of accruals in asymmetrically timely gain and loss recognition. Journal of Accounting Research, 44(2), 207–242. https://doi.org/10.1111/j.1475-679X.2006.00198.x

- Basu, S. (1997). The conservatism principle and the asymmetric timeliness of earnings. Journal of Accounting and Economics, 24(1), 3–37. https://doi.org/10.1016/S0165-4101(97)00014-1

- Bernstein, D. (1994). Imperfect information and agency cost models: Further empirical tests. International Review of Economics and Finance, 3(2), 183–193. https://doi.org/10.1016/1059-0560(94)90032-9

- Beyer, A., & Dye, R. A. (2012). Reputation management and the disclosure of earnings forecasts. Review of Accounting Studies, 17(4), 877–912. https://doi.org/10.1007/s11142-011-9180-5

- Blacconiere, G., & DeFond, M. L. (1997). An investigation of independent audit opinions and subsequent independent auditor litigation of publicly-traded failed savings and loans. Journal of Accounting and Public Policy, 16(4), 415–454. https://doi.org/10.1016/S0278-4254(96)00042-7

- Bliss, J. H. (1924). Management through accounts. The Ronald Press Co.

- Brown, S., Hillegeist, S., & Lo, K. (2004). How disclosure quality affects the level of information asymmetry. Journal of Accounting and Economics, 37(3), 343–366. https://doi.org/10.1016/j.jacceco.2004.02.001

- Buallay, A. (2019). Corporate governance, Sharia’ah governance and performance. International Journal of Islamic and Middle Eastern Finance and Management, 12(2), 216–235. https://doi.org/10.1108/IMEFM-07-2017-0172

- Campa, D., & Camacho-Minano, -M.-M. (2015). Tfhe impact of SME’s pre-bankruptcy financial distress on earnings management tools. International Review of Financial Analysis, 42, 222–234. https://doi.org/10.1016/j.irfa.2015.07.004

- Chen, Y., Fay, S., & Wang, Q. (2011). The role of marketing in social media: How online consumer reviews evolve. SSRN Electronic Journal. DOI: 10.2139/ssrn.1710357

- Chi, W., Liu, C., & Wang, T. (2009). What affects accounting conservatism: A corporate governance perspective? Journal of Contemporary Accounting and Economic, 5(1), 47–59. https://doi.org/10.1016/j.jcae.2009.06.001

- Clinch, G., Stokes, D., & Zhu, T. (2011). Audit quality and information asymmetry between traders. Accounting & Finance, 52(3), 743–765. https://doi.org/10.1111/j.1467-629X.2011.00411.x

- DeFond, M., & Zhang, J. A review of archival auditing research. (2014). Journal of Accounting and Economics, 58(2–3), 275–326. (This issue). https://doi.org/10.1016/j.jacceco.2014.09.002

- DeFond, M. L., & Jiambalvo, J. (1994). Debt covenant violation and manipulation of accruals. Journal of Accounting and Economics, 17(1–2), 145–176. https://doi.org/10.1016/0165-4101(94)90008-6

- DeFond, M. L., & Park, C. W. (1997). Smoothing income in anticipation of future earnings. Journal of Accounting and Economics, 23(2), 115–139. https://doi.org/10.1016/S0165-4101(97)00004-9

- Deltas, G., & Doogar, R. (2004). Product and cost differentiation by large audit firms. University of Illinois, U. C.

- Dittmar, A., & Mahrt-Smith, J. (2007). Corporate governance and the value of cash holdings. Journal of Financial Economics, 83(3), 599–634. https://doi.org/10.1016/j.jfineco.2005.12.006

- Dogru, T., & Bulut, U. (2018). Is tourism an engine for economic recovery? Theory and empirical evidence. Tourism Management, 67, 425–434. https://doi.org/10.1016/j.tourman.2017.06.014

- Drobetz, W., Gruninger, M., & Hirschvogl, S. (2010). Information Asymmetry and the Value of Cash. Journal of Banking and Finance, 34(9), 2168–2184. https://doi.org/10.1016/j.jbankfin.2010.02.002

- Etemadi, H., & Abdoli, L. (2018). Audit quality and financial statement fraud. Journal of Financial Accounting Knowledge, 4 (4), 23–43. (in Persian). http://jfak.journals.ikiu.ac.ir/article_1308_en.html

- Etemadi, H., Momeni, M., & Farajzadeh, H. (2012). Earnings management, how it affects earnings quality firms? Journal of Financial Accounting Research, 2 (12), 101–122. (in Persian). http://far.ui.ac.ir/article_16948_en.html

- Faulkender, M., & Wang, R. (2006). Corporate financial policy and the value of cash. Journal of Finance, 61(4), 1957–1990. https://doi.org/10.1111/j.1540-6261.2006.00894.x

- Fuerman, R. D. (2006). Auditors and the post-2002 litigation environment. Research in Accounting Regulation, 24(1), 40–44. https://doi.org/10.1016/j.racreg.2011.12.005

- Gonzalez, G., & Garcia-Meca, E. (2014). Does corporate governance influence earnings management in Latin American markets? Journal of Business Ethics, 121(3), 419–440. https://doi.org/10.1007/s10551-013-1700-8

- Habib, A., Uddin Bhuiyan, B., & Islam, A. (2013). Financial distress, earnings management and market pricing of accruals during the global financial crisis. Managerial Finance, 39(2), 155–180. https://doi.org/10.1108/03074351311294007

- Hassas Yeganeh, Y., & Azinfar, K. (2010). The relationship between auditing quality and auditing institution’s size. Journal of Accounting and Auditing, 61, 85–97. https://www.sid.ir/en/journal/ViewPaper.aspx?id=202560

- Healy, P. M., & Palepu, K. G. (2001). Information asymmetry, corporate disclosure, and the capital markets: A review of the empirical disclosure literature. Journal of Accounting and Economics, 31(1–3), 405–440. https://doi.org/10.1016/S0165-4101(01)00018-0

- Heninger, G. (2001). The association between auditor litigation and abnormal accruals. The Accounting Review, 76(1), 111–126. https://doi.org/10.2308/accr.2001.76.1.111

- Hogan, W. P. (1997). Corporate governance: Lessons from barings. Abacus, 33(1), 26–48. https://doi.org/10.1111/1467-6281.00002

- Jones, T. (1991). Ethical decision making by individuals in organizations: An issue-contingent model. Academy of Management Review, 16(2), 366–395. https://doi.org/10.5465/amr.1991.4278958

- Knechel, W. R. (2009). Audit lessons from the economic crisis: Rethinking audit quality. Working paper, Maastricht University.

- Kothari, S. P., Leone, A. J., & Wasley, C. E. (2005). Performance matched discretionary accruals measures. Journal of Accounting and Economics, 39(1), 163–197. https://doi.org/10.1016/j.jacceco.2004.11.002

- Lara, J. M., Garcia, B., & Penalva, F. (2007). Accounting conservatism and corporate governance. Review of Accounting Studies, 14(1), 161–201. https://doi.org/10.1007/s11142-007-9060-1

- Lee, T. (2014). Costs of equity and accounting conservatism: A real options approach. University of Auckland Business School.

- Li, S., & Richie, N. (2016). Income smoothing and the cost of debt. China Journal of Accounting Research, 9(3), 175–190. https://doi.org/10.1016/j.cjar.2016.03.001

- Lin, C.-M., Chan, M.-L., Chien, I.-H., & Li, K.-H. (2018). The relationship between cash value and accounting conservatism: The role of controlling shareholders. International Review of Economics & Finance, 55(1), 233–245. https://doi.org/10.1016/j.iref.2017.07.017

- Lin, J. W., & Hwang, M. I. (2010). Audit quality, corporate governance, and earnings management: A meta-analysis. International Journal of Auditing, 14(1), 57–77. https://doi.org/10.1111/j.1099-1123.2009.00403.x

- Louis, H., Sun, A. X., & Urcan, O. (2012). Value of cash holdings and accounting conservatism. Contemporary Accounting Research, 29(4), 1249–1271. https://doi.org/10.1111/j.1911–3846.2011.01149.x

- Mahdavi, G., & Daryaei, A. A. (2017). Attitude toward business environment of auditing, corporate governance and balance between auditing and marketing. Contadina Y Administration, 62(3), 1019–1040. doi: 10.1016/j.cya.2017.04.005

- Mahdavi, G., & Namazi, N. (2017). Ranking the effective measurements on the tasks and position of internal auditing unit in the executive agencies. Journal of Health Accounting, 5 (2), 91–111. (in Persian). doi: 10.30476/JHA.2017.39320

- Meek, G., Rao, R., & Skousen, C. (2007). Evidence of factors affecting the relationship between CEO stock option compensation and earnings management. Review of Accounting and Finance, 6(3), 304–323. https://doi.org/10.1108/14757700710778036

- Muller-Kahle, M. I., Wang, L., & Wu, J. (2014). Board structure: An empirical study of firms in Anglo-American governance environments. Managerial Finance, 40(7), 681–699. https://doi.org/10.1108/MF-04-2013-0102

- Oz, I. O., & Yelkenci, T. (2018). Examination of real and accrual earnings management: A cross-country analysis of legal origin under IFRS. International Review of Financial Analysis, 58, 24–37. https://doi.org/10.1016/j.irfa.2018.04.003

- Salehi, M., Mansoury, A., & Pirayesh, R. (2008). Factors affecting quality of audit: Empirical evidence of Iran. J. Bus. Res., 2(12), 24–32. https://www.ajol.info/index.php/jbr/article/view/43205

- Shehata, N. F. (2014). Theories and determinants of voluntary disclosure. Accounting and Finance Research, 3(1), 18–26. https://doi.org/10.5430/afr.v3n1p18

- Wang, C., Kung, F., & Lin, K. (2014). Does audit firm size contribute to audit quality? Evidence from two emerging markets. Corporate Ownership & Control, 11(2), 108–119. https://doi.org/10.22495/cocv11i2p8

- Watts, R. (2003). Conservatism in accounting part I: Explanations and implications. Accounting Horizons, 17(3), 207–221. https://doi.org/10.2308/acch.2003.17.3.207

- Watts, R. L., & Zimmerman, J. L. (1986). Positive accounting theory. Prentice-Hall.