?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Terrorism plays a pivotal role in influencing the stock indexes of many countries. This research article claims to be first in accessing the asymmetrical effect of multiple categories of terroristic activities on stock indexes in the presence of macroeconomic volatility. This research utilized a Non-linear autoregressive distributive lag model (NARDL) to find out the asymmetrical relationship between terroristic disruptions and stock indexes. Data on terroristic attacks have been incorporated from 2002 to 2015, and more than 4600 observations taken into account. Positive shocks to attacks on mosques, killed in mosque attacks, killed in drone attacks, and army personal fatalities are negatively affecting the stock prices in the short run. Results indicated that such disruption causes a temporary negative effect on stock indexes only in the short run but in the long-run stock exchange remains resilient against such disruptions.

PUBLIC INTEREST STATEMENT

Do you think that terrorism has a negative impact on stock indexes?

This is the first research article that has found the non-linear effect of multiple attacks on stock indexes in the short run and long run. Interestingly, research findings indicate that positive shocks to attacks on mosques, killed in mosque attack, army personal fatalities, and killed in drone attacks are negatively associated with stock indexes only in the short run. However, the long-run effect of positive shocks to killings in drone and killed in mosque attacks on stock indexes are insignificant and positive shocks to army personal killed and attacks on mosque are having a positive effect on stock indexes. This shows that the KSE remains resilient against the number of terrorist attacks in the long run.

1. Introduction

In a particular contrast with bigger economies, smaller economies are extremely susceptible to huge losses caused by multiple terrorist attacks due to limited resources, knowledge repositories and limited preparedness levels (Anh Phuong, Citation2009; Kaveh Shahraki, Citation2011). The IMF report indicates that greater and more effective financial organizations can survive the aftershocks triggered by domestic and global terroristic disruptions (Nedelescu, Citation2005). Diversifiable organizations are more resilient to such disruption and negative environmental turbulences. After the 9/11 attacks, terroristic disturbances were created in Pakistan and Iran, disrupting the financial markets of the leading stock exchanges in both nations: Tehran and Karachi stock exchange (Kumar, Citation2013). This study intends to investigate whether or not Pakistan stock exchange is resistant to various environmental upheavals, such as domestic terrorism and macroeconomic instability? The economic situation of Pakistan has started to change after the terrorist attacks of 9/11. Ohio State University has demonstrated that business success rates remain at risk of terrorism in the US; Dow Jones industrial averages were dropped one day before 9/11 to 9600 points, but after the assault, the stock market collapsed because of the chaotic, volatile circumstance and plummeted to 7600 points (Essaddam & Karagianis, Citation2014; Melnick & Eldor, Citation2010).

Drone attacks in Pakistan have also been increased from 1 in 2004 to more than 118 in 2010. In 2003, 140 civilians were killed, but numbers were still small, in contrast to 2738 civilians in 2011 (BBC news headline, Citation2005; Bennett-Jones, Citation2011; Malik, Citation2011; Robert, Citation2012). Our study desires to contribute an effort towards finding the resilience capability of the Pakistani stock exchange. Resilience in the community can also be known as social vulnerability. We all have seen a momentum boom in the annual death rate due to terrorism from 168 in 2001 to more than 35000 deaths approximately in 2011 (Malik, Citation2011) In Oct 2004, 30 innocent Shias have been killed in ‘Sialkot Shia mosque’ and 45 Shias (Shi’a) have been martyred in a bomb attack in Baluchistan during 2005 in Pakistan (BBC news headline, Citation2005). These events have not only damaged Pakistan’s international image for internal stability but have also played a significant role in restricting foreign direct investment. More than 3400 bomb blasts within-country along with 283 suicidal attacks from 2001 to 2011 have resulted in multibillion dollar loss to Pakistan’s economy (Malik, Citation2011; Nisar, Citation2015). Political instability, high crime rate, civil dishonesty like corruption and ethnic clashes aggravated the situation to most (Bennett-Jones, Citation2011; Nisar, Citation2015; Malik, Citation2011; Bennett-Jones, Citation2011; BBC news headline, Citation2005; Kaveh Shahraki, Citation2011; Mengyun et al., Citation2018).

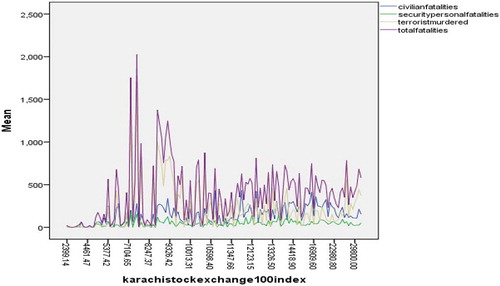

Figure 1. Civilian fatalities, security personal fatalities, terrorist murdered, total fatalities and KSE 100 index.

Figures and explain that in the presence of multiple terroristic disruptions, the KSE-100 index is continuously increasing. According to Figure , when the KSE-100 index has exceeded 7104.65 points, there were also significant amounts of civilian casualties owing to terrorist activities, but the Karachi stock exchange performed exceptionally well and achieved around 29000 index points in the presence of economic upheaval and terroristic disturbances. In Figures and , however, the KSE-100 index still reflected certain volatility movements during these terroristic assaults, which also inspire researchers to find out the short- and long-term asymmetrical impact of these multiple categories of terroristic attacks on stock prices in presence of macroeconomic volatility.

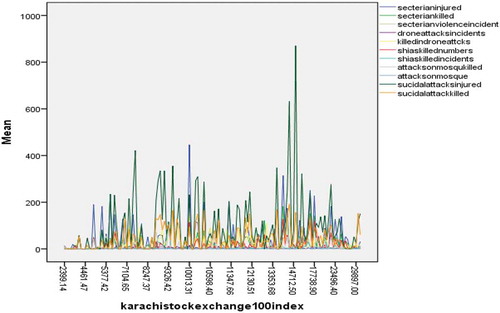

Figure 2. Response of KSE-100 index against multiple disruptions such sectarian injured, sectarian killed, sectarian violence incidents, drone attacks, killed in drone attacks, Shia killed, Shia killed incidents, attacks on mosques, attacks on mosques killed, suicidal attacks, suicidal attacks injured.

In the existing literature, the only symmetrical effect of terroristic attacks have been examined on stock exchanges (Corbet et al., Citation2018; Gok et al., Citation2020; Laila & Guruprasad, Citation2019; Liu & Pratt, Citation2017; Narayan et al., Citation2018; Orbaneja et al., Citation2018; El Ouadghiri & Peillex, Citation2018; Papakyriakou et al., Citation2019; Tingbani et al., Citation2019), this is first research which accounts for short-term and long-term asymmetrical co-integration between terroristic attacks and stock indexes in order to find out short-term and long-run stock exchange resilience in Pakistan. We have also included macroeconomic volatility as control measure for more robust estimates.

In the existing literature, some of the research articles have reported the negative/adverse influence of terroristic attacks on stock market indexes (Corbet et al., Citation2018; El Ouadghiri & Peillex, Citation2018; Gok et al., Citation2020; Jakob & Christoffer, Citation2017; Laborda & Olmo, Citation2019; Laila & Guruprasad, Citation2019; Papakyriakou et al., Citation2019; Shaikh, Citation2019). However, some of the research articles report that terrorism strengthens stock market integration between domestic and international stock markets (Narayan et al., Citation2018), this type of integration is results of short-term contagion effect. There is no consensus in the literature that whether Pakistan’s stock exchange is resilient to different categories of terroristic attacks based on real-world daily time series data. Moreover, in existing literature, some authors have utilized proxies and dummy variables regarding terroristic attacks in Pakistan (Shahbaz, Citation2013) and OECD member countries (Narayan et al., Citation2018), whereas other considered few specific events of terroristic attacks while investigating the terroristic impact on the stock exchange (Chesney et al., Citation2011; Essaddam & Karagianis, Citation2014; Jakob & Christoffer, Citation2017; Liu & Pratt, Citation2017; Melnick & Eldor, Citation2010; El Ouadghiri & Peillex, Citation2018; Papakyriakou et al., Citation2019) and didn’t consider the real time-series data of multiple categories of terroristic attacks in Pakistan as is undertaken by our research. However, some of the research articles incorporate time-series data and utilize EGARCH models to investigate the impact of terrorism on the Turkish stock exchange (Gok et al., Citation2020). This research article contributes to the existing literature by finding out the asymmetric effect of different types of terroristic attacks on stock market indexes in the presence of exchange rate volatility. Different categories of terroristic attacks such as attacks on a mosque, sectarian killed, army personal killed, the total number of fatalities, civilian fatalities, terrorists murdered, killed in drone attacks and killed in mosque attacks are taken into consideration after close observation of multiple daily timelines representing terroristic attacks in Pakistan.

2. Literature review

Based on the findings of existing research on psychological endurance, individuals are having the capacity to cope with stress. Organizational resilience is also linked to the capability to resist, absorb and withstand shocks while producing a capacity to bounce back from these shocks and regained original position (Baltaci, Citation2014; Hatler, Citation2013; Kärrholm, Citation2014; Rapp, Citation2014). In certain situations, through resilience, the company has not only learnt to survive shocks, to endure distress but also has managed to preserve or sustain its initial or more superior role (Lucini, Citation2013). The main origin of the word resilience is traced from the disaster management studies where authors have emphasized on the importance of communities for coping against the disasters or shocks rather than the system (becker, Citation2014; Bell, Citation2002). In organizational resilience, the system plays an important role to absorb shocks and then produce dynamic capabilities to regain the original position or somewhat better than the earlier (Proag, Citation2014).

A study on more than 300 students during the devastating earthquake in Japan showed that psychological resilience plays a significant role in the coping against post-traumatic stress disorder (Kusumastuti et al., Citation2014). Strattaa (Citation2015) stated that psychological resilience is simply the capacity of an individual to overcome stress or disruptions. The stock market’s resilience is the ability to thrive, endure, and rebound from economic fluctuation. Preparation often forms an essential part of the stock market resilience for risk management. The degree of preparedness also depends on a country’s macroeconomic stability and economic condition (Valérie Angeona, Citation2015). The resilient index also plays an important role in fostering the speed of recovery. The resilience index is not only the capability of any organization to tolerate the disastrous event but is also a dynamic capability that will make an organization more capable to bring change for continual progression (Adam Rosea, Citation2013). Resilience management is the foundation for strong, legitimate, and rigor structure; whose boundaries are protected from the forecasted disrupted event and whose walls are constituted to bear environmental turbulences (Trærup, Citation2012).

Melnick and Eldor (Citation2010) conducted an economic study to understand that how media scrutinizes and report a terrorist incident, such as the number of published articles, the spacing of stories, the use of images, and the scale of the headlines affects stockholder’s discernment. The media reporting is an actual outlet for economic loss by extremism. The results also revealed that the economic harm incurred by terroristic acts rises monotonously as media attention grows. Papakyriakou et al. (Citation2019) have found that stock indexes dramatically decrease on the particular event day and the next trading day. Authors furthermore analysed the investor’s attitude after the attacks and these attitudes are depending upon the contents of the country’s news and social networking outlets. Kollias et al., (Citation2013) found that terroristic insurgencies influence the covariance between stock market returns of the US, stock market returns of Europe (such as CAC40, DAX, FTSE100), and oil prices by utilizing Non-linear BEKK-GARCH modelling. Terrorism attacks unforeseeably impacted the correlation between CAC40, DAX, and oil returns, and have no major influence on the S&P500, FTSE100, and oil indexes relationships.

The impact of terroristic events on indices was analysed from the usage of both event study analyses and daily time series data by employing exponential generalized autoregressive conditional heteroscedasticity (E-GARCH) modelling (Gok et al., Citation2020). El Ouadghiri and Peillex (Citation2018) suggested that US media exposure to Islamic extremism has a significant effect on American Islamic stock prices. Another research reported that foreign terrorist attacks inside Europe do not pose a substantial risk of stock market instability for Ireland and Spain, however, the instability of the domestic stock market is substantially enhanced due to domestic terrorism (Corbet et al., Citation2018). The rise of ISIS motivated fear in France, Germany, Greece, Italy, and the UK has been strongly affecting market fluctuations since 2011. Terrorism attacks are also having an indirect effect on the stock market of respective domestic countries through effecting tourism and other economic sectors. Liu and Pratt (Citation2017) utilized foreign tourism demand models to measure the connection between terrorism and tourism in 95 distinct countries and territories. After income regulation, the authors found that terrorism didn’t contribute to long-term and short-term impact on international tourism demand with the aid of panel data models. However, time-series modelling found a limited effect of terrorism on tourism in the short run and longer term in only 9 countries out of 95.

Chesney et al. (Citation2011) illustrated the consequences of terroristic attacks on financial markets, as well as the impacts of assaults on commodities and bonds, and analysed the impact of terrorist activities at regionally, industrial, international and domestic levels. They further contrast the effect of terrorism on capital markets with the impacts of natural catastrophic hazards and industrial cataclysmic incidents based on three methods: case analyses, non-parametric, and GARCH—EVT techniques. The findings of the study advocated that the best suitable way of measuring the effect of terrorism on the financial market is a non-parametric strategy. The Swiss stock market and American stock market are both affected by the largest amount of terroristic attacks; however, the intensity of the negative impact of terroristic attacks is greater in the Swiss stock market. Shahbaz (Citation2013) explored the co-integrating association between inflation, economic development, and terroristic attacks in Pakistan by employing time series data for the duration between 1971 and 2010. In the ARDL with the bound testing approach, the reliability of the long-term interaction is furthermore calculated by utilizing rolling window methodology. Empirical results supported the long-term association between terroristic attacks in Pakistan, inflation, and economic development. Moreover, the bidirectional causality between recession and terroristic activities is also estimated by using the VECM Granger-causality framework, and the results are furthermore confirmed by the variance decomposition approach. Therefore, findings suggested that the persistence of low inflation is effective in minimizing terrorism. Apart from causing significant collateral destruction and injury, terroristic attacks may have a negative effect on the national and global economies and on the trust of shareholders. The crippling consequences of terrorism discourage global investments in terror affected countries and/or impair the willingness of local citizens to participate in the overseas-affected economies, which isolates economies and thus precludes a detrimental association between terrorism and the integration of financial markets. This is generally called the flight-to-security (Narayan et al., Citation2018).

In the context of eight-member countries of intergovernmental organizations for economic cooperation and development, Narayan et al. (Citation2018) have utilized pooled ordinary least square regression with cross-sectional dependence to investigate the correlation between terrorism and multinational investment in portfolio by covering the period from 2001 to 2014. Findings showed that portfolio choices are vulnerable to domestic terrorism in eight OECD nations, excluding France and Italy. In the deflationary and inflationary phases of home and host countries, portfolio decisions have often been discerned to react differently to domestic terrorism. Authors have found that domestic terrorism is having a positive and significant effect on stock market integration for Australia, Germany, England, and Turkey. However, most of US and Canadian investors drawn their investment out from terroristic susceptible countries and moved towards safer horizons. The flight to safety hypothesis is established for the US and Canada. The goal of Jakob and Christoffer (Citation2017) study is the systemic, structured, and comprehensive strategy to complement existing literature on the relationship between stock indexes and terrorism. Their research supported the idea of utilizing a multi-dimensional framework to view violent incidents as a diverse collection of cases. The methods utilized in the event analysis investigated the impact of 46 terroristic incidents in OECD countries covering the period from 1990 to 2016 on financial markets in the United States, the United Kingdom, Spain, and Denmark.

Essaddam and Karagianis (Citation2014) explored the interrelationship between terroristic attacks and the economy, with an emphasis on US stock market volatility affected by terrorist attacks. Menace arises due to terroristic attacks should be considered as a significant element to estimate market return variability and should be included in the forecasting of variance in market returns. With an approach to volatile event case analysis and a modern methodology of bootstrapping, on the day of the assault, stock market variability rises and remains impactful for at least 15 days after the day of the assault. The authors have furthermore observed the increasing variability of market returns of firms operating in industrialized nations. The vulnerability of the institution to terroristic attacks incidents differs due to the complexity of the geographical location of the country in which the institution is currently operating (Essaddam & Karagianis, Citation2014). Arin et al. (Citation2008) investigated the impact on capital markets of violence and terroristic attacks by utilizing data from six separate capital markets and suggested that violence is having a major influence on equity and bond prices, and in developing markets the size of these impacts is even higher.

2.1. Do estimation of NARDL model for asymmetric impact of terroristic disruption on KSE-100 indexes is an appropriate choice?

Laila and Guruprasad (Citation2019) utilised ARDL modelling approach in order to investigate the symmetrical association between terroristic attacks and stock indexes. Feridun and Shahbaz (Citation2010) examined the causality between defence expenditure and terroristic incidents in Turkey by employing the ARDL model and Granger-causality approach. Findings indicated that higher terroristic incidents are granger causing higher defence expenditure. Despite this, it can be argued that military counter-terrorism initiatives alone are not enough to deter extremism. Karamelikli et al. (Citation2019) have estimated the long-term and short-term influence of terrorist attacks on Turkish domestic tourism by using an asymmetrical ARDL model covering the period from 2007 to 2016. Results have suggested an asymmetrical association between terroristic disruptions, inbound and domestic tourism. International and domestic tourists have behaved differently to the rise or decline in terroristic disruptions.

The escalated terror attacks in Africa have systemic consequences for a region that relies extensively on international direct investment for an improvement in its growth cycle. By analysing cross-sectional time-series data on terroristic incidents and international financial flows, Onanuga et al. (Citation2020) have contributed empirically to the terroristic disruptions and capital flow literature. Authors have employed an asymmetrical panel-based ARDL modelling approach and found that terroristic activities negatively impact international foreign direct investment for longer horizons, however, military expenditure is directly associated with an increased inflow of capital within the region. Meierrieks and Schneider (Citation2016) utilized a panel-based ARDL modelling approach and analysed the impact of illegal drug prices on terrorism by covering the period from 1984 to 2007 for 58 countries. Authors have concluded that the prices of addiction- driven illegal substances are co-integrated with more terroristic violence for longer horizons through utilising the conception of a crime-terrorism connection. Nevertheless, for the shorter horizon, drug price inflation has a depreciative impact on terroristic incidents, likely because terrorist organizations react to enhanced drug industry appeal by granting criminal preference over terrorist operations. Fareed et al. (Citation2018) utilised non-linear ARDL model in order to explore asymmetrical nexus between economic development, tourism and the terroristic disruptions within Thailand by employing time series yearly data from 1990 to 2017. Authors have suggested the presence of asymmetrical connotation between underlying variables and furthermore purposed that symmetrical considerations while exploring the nexus between economic development and terrorism may lead towards spurious results.

3. Data

Daily data on multiple terroristic attacks are collected from south Asian terrorism portal administrated by institute of conflict management. South Asian terrorism portal is having multiple timelines representing various terroristic attacks from January 2002 to December 2015. Each timeline containing descriptive and comprehensive details about specific types of terrorist attacks is scanned and compiled into a unique dataset consisting of eight categories such as total army personal killed, terrorist killed, civilian killed, sectarian killed, killed in response to attacks on mosques, total number of fatalities, attacks on mosques and drone attacks.Footnote1 This is the first research article utilizing different categories of terroristic attacks on daily basis in Pakistan in order to find out short-run and long-run resilience of KSE-100 index. KSE-100 index consists of 100 chosen firms focused on the maximum degree of Free-Float Capitalization, and accounts for around 80 percent of the total Free-Float Capitalization of exchange-listed organizations. In existing literature, some research articles have utilized Engle–Granger method after applying stationary test on time series data and investigate the effect of terrorism on stock prices in Pakistan (Abdullah, Citation2013; Shahbaz, Citation2013). However, they have only utilized certain dummy variables as the representation of terroristic attacks and no effort has been made in order to observe daily timelines of terrorist attacks or to collect data representing multiple categories of attacks such as drone attacks, attacks on mosque, attacks on sectarian groups etc. Some researchers have also utilized autoregressive distributive lag model in order to find out Short- and long-term co-integrating association between the terrorism and other global equity indices including FTSE, DJI, NIKKEI, SSEC and DAX (Laila & Guruprasad, Citation2019). Few researchers such as Sheikh, Asad, Ahmed et al. (Citation2020) and Sheikh, Asad, Mukhtar et al. (Citation2020) have estimated that non-linear models have better predictability to capture asymmetries between variables.

4. Methodology

This research article has embraced the importance of both ARDL and NARDL model in order to find out symmetrical and asymmetrical effect of multiple terroristic attacks on KSE-100 index. Positive influence of terroristic attacks on KSE-100 index will provide significant proof that Pakistan stock exchange is resilient against these attacks.

4.1. Unit root testing for stationary

Non-linear ARDL and Linear ARDL models are estimated if variables are integrated at same order or some variables are stationary at the level and some of them became stationary after first differencing or none of the variables is I (2) (Awodumi & Adewuyi, Citation2020; Baz et al., Citation2019; Charfeddine & Barkat, Citation2020; Salvatore, Citation2019). Appropriate integration of variables is estimated by utilizing three different unit root tests such as Philips person (PP), augmented dickey fuller test (ADF) and KPSS unit root test. These three different unit root tests are widely used together in multiple research articles (Muhammad, Citation2017a; Rajesh, Citation2019). The appropriateness of utilizing these unit root tests together is to confirm that neither of variables is becoming stationary at second differing. Results for unit root tests are presented in Tables –.

Table 1. Descriptive statistics

Table 2. ADF unit root test

Table 3. PP unit root test

Table 4. KPSS unit root test

4.2. BDS test for checking the appropriateness of NARDL estimation

Applicability of linear or nonlinear ARDL model is furthermore confirmed by BDS testing approach (Brooks, Citation1996; Kim et al., Citation2003). BDS test is used by a variety of research articles in order to confirm that whether the time series data are identically distributed and independent (Brooks, Citation1996; Galadima & Aminu, Citation2020; Kim et al., Citation2003). In case of BDS test, if null hypothesis is rejected, this will confirm the utilization of NARDL model instead of ARDL model as an appropriate choice and valid decision. However, for further robustness, coherent estimation and in order to bring rigor, we have applied Both ARDL by (Pesaran et al, Citation2001) and NARDL model by (Shin et al, Citation2014) in order to compare the results from both models. BDS equation can be written as,

BDS test can be written in following manner and results are reported in Table ,

Table 5. BDS test for independence and identical distribution of time series

is defined as standard deviation of

.

4.3. NARDL model and asymmetrical error correction term

Non-linear autoregressive distributive lag model is an advance form of linear ARDL model and is also having capacity to convert all independent variables into positive and negative shocks. NARDL model can estimate long run co-integration between positive and negative shocks of terroristic attacks and stock market index in order to investigate investor’s symmetrical and asymmetrical response to multiple terroristic attacks. Estimation of NARDL model is also having other benefits relation to its capacity to provide vigorous results irrespective of variables are becoming stationary at level or first differencing(Awodumi & Adewuyi, Citation2020; Charfeddine & Barkat, Citation2020). Mathematical form of ARDL model is given below in EquationEquations (1)–(Equation2

) represents general form of error correction term for symmetrical ARDL model

In EquationEquation (2), dependent variable is KSE-100 stock indexes, and

sign associated with dependent variable indicates that dependent variable KSE100INDEX is in differences,

and

are appropriate lag orders of stock indexes as a dependent variable and multiple terroristic attacks as independent variables, respectively. b and c denote short-run coefficients of dependent variable (KSE100index) and independent variable i.e. multiple terroristic attacks respectively.

,

represents short-run and long-run effect of macroeconomic volatility in form of exchange rate fluctuation on stock indexes. Exchange rate (USD/PKR) is used as proxy for macroeconomic volatility and incorporated in model for control measures. Therefore,

and

represented short-run and long-run effect of terroristic attacks on stock indexes, respectively. Error term in EquationEquations (1

) and (Equation2

) is represented by

. The objective of linear ARDL model is to formulate long-run and short-run co-integration between the number of multiple terroristic attacks and stock indexes, long-run co-integration is determined on the basis of value of F statistics.

If value of F statistics is greater than upper and lower-bound critical value, then null hypothesis of no co-integration(=

is rejected (

≠

. There are two critical values such as upper bound and lower bound. Upper-bound critical values should be used to compare with F statistics in the case when all incorporated variables are integrated at first differencing, I (1). However, if all variables are stationary at level, then F statistics should be greater than lower-bound critical values in order to establish long-run co-integration between dependent and independent variables. In case of mixed variables i.e. some of them are I (0) and some are I (1), then, F statistics value should be greater than both upper and lower limits for long-run co-integrating symmetrical relationship. Asymmetric long-run equilibrium relation is established by (shin et al, 2014) in the following manner,

In above EquationEquation (3), long-run asymmetric coefficients are represented by

, and deviation from long-run equilibrium is denoted by

as error term. Positive and negative term of vector of regressors

is represented as

Partial sums of positive and negative shocks of can be explained as,

Asymmetrical error correction can be able to establish long run asymmetrical co-integration between stock indexes and multiple terroristic attacks provided its value should be in (–) and significant. Asymmetrical error correction model can written as follow by conjoining EquationEquation (3) with EquationEquation (2)

of symmetrical error correction term,

Asymmetrical ARDL model can be written as

In NARDL model, short-run and long-run symmetrical or asymmetrical co-integrating relationship between KSE-100 indexes and multiple terroristic attacks can be established if value of F statistics is greater than upper bound and lower-bound critical value, therefore, its implementation is similar to ARDL model. However, NARDL is having capability to breakdown every independent variable into its partial sums of positive and negative shocks. Short-run and long-run asymmetrical relationship between dependent and independent variables can be established if wald test statistics reject null hypothesis of short-run symmetry ( and long-run symmetry(

=

). Therefore, presence of long run (

≠

) and short run asymmetrical relation (

is estimated on basis of Wald test statistics, once co-integration is established (Awodumi & Adewuyi, Citation2020; Baz et al., Citation2019; Charfeddine & Barkat, Citation2020; Muhammad, Citation2017b; Rajesh, Citation2019; Salvatore, Citation2019).

5. Results

Table displays the results of descriptive statistics regarding the number of terroristic attacks in Pakistan during 2002–2015. Data is initially collected from the South-Asian terrorism portal by manually scanning daily descriptive timelines listed in chronological order on the institute of conflict management website. More than 4600 observations regarding multiple categories of terroristic attacks have been taken into account and these daily level observations have been transformed into monthly level data.Footnote2 The main purpose of this transformation is to find out the short run and long run asymmetrical effect of multiple categories of terroristic attacks on Pakistan’s stock exchange in the presence of macroeconomic volatility as a control measure.

In the existing literature on the relationship between terrorism and economic growth, researchers have utilized monthly time series data to investigate the real determinants of terroristic attacks in Pakistan. Ismail and Amjad (Citation2014) investigated that in addition to some other reasons, the motivation behind terrorist attacks is essentially deprivation, low economic development, and inflation by using monthly time series data and with aid of advanced econometric techniques such as Johnsen Julius co-integration and Error correction model. Findings suggested that Inflation as a significant cause of macroeconomic uncertainty in Pakistan which needs to be reduced if economic development is to be followed by the government.

Descriptive figures indicate the tremendous casualties in the war against terrorism in Pakistan. Mean values of total military personal deaths and civilian casualties were 41 and 138 in any month respectively, however, in a particular single month, Pakistan also experienced the highest loss of human capital due to 432 civilian deaths and 157 military staff casualties. On average, 24 individuals from sectarian groups, 20 from drone attacks, and 8 people in attacks on mosques have been killed each month during the war on terror from 2002 to 2015. The highest value of casualties due to attacks on sectarian groups, drone attacks, and attacks on a mosque has been reached at 181, 146, and 103, respectively, in a specific single month. Interestingly, descriptive statistics also explain that KSE-100 indexes are having a minimum value of 2399.14 and a maximum value of 29984 in presence of terroristic disruptions. This furthermore motivates the researcher to investigate the short-run and long-run asymmetrical effect of these attacks on the KSE-100 index. Our study also investigates that either KSE-100 index is resilient to these multiple terroristic attacks or not? Tables – explain the result of unit root analysis to find out that either variable is having any seasonality effect or not.

Tables – explain the results of different types of unit root test to confirm that variables are not suffering from the seasonality effect. Furthermore, these tests also help to determine that none of the variables turns out to be stationary at 2nd differencing. The null hypothesis in the case of ADF and PP test is that data is having a seasonality effect or non-stationary in nature. The null hypothesis of PP and ADF cannot be rejected for all independent variables except the exchange rate and dependent variable (stock indexes). Similar to ADF, the PP test shows that all variables are becoming stationary at level except stock indexes as dependent and exchange rate as an independent variable, which means that stock indexes and exchange rates are having a seasonality effect at the level and first differencing make them free from seasonality effect or non-stationarity. KPSS results show that the null hypothesis of stationarity is not rejected for all independent variables except exchange rates, stock index, and attacks on mosque. According to ADF, PP, and KPSS, some of the variables are becoming stationary at the level and some are after first differencing. These results confirm that the utilization of LARDL and NARDL for analysis is apposite and accurate. The BDS test of nonlinearity confirms that the NARDL model is more appropriate to find out the asymmetrical effect of terroristic attacks on stock prices.

Table reports that an asymmetrical co-integrating relationship cannot be established between stock indexes and multiple categories of terroristic attacks. This is furthermore confirmed by the BDS test of non-linearity that NARDL estimation is a more appropriate model for study. Table reports that there exists an asymmetrical relationship between multiple terroristic attacks and stock indexes, as the value of F statistics is greater than upper bound and lower-bound critical values which means that the null hypothesis of no co-integration can be rejected. Table reports the asymmetrical results of multiple categories of terroristic attacks and stock indexes. Each variable is decomposed into positive and negative shock to find out the asymmetrical relationship between stock indexes and terroristic attacks. Table is divided into two portions such as short-run effect and long-run effect. The first portion deals with the short-run effect of multiple terroristic attacks on stock indexes, and the second portion explains that either relationship between terrorist attacks and stock indexes is symmetrical or asymmetrical in the long run. The symmetrical and asymmetrical effect of terroristic attacks on stock indexes in the short and long run is confirmed while utilizing Wald test statistics, and Wald test results are given in Table .

Table 6. ARDL co-integration results

Table 7. NARDL estimation

Table 8. Asymmetrical co-integration test with bound testing approach

Table 9. Wald test for short-run and long-run asymmetries

Table explains that positive shock to mosque attacks killings, attacks on the mosque, army personal killed, and killed in drone attacks is having an inverse impact on stock indexes in the short run. This means that investors are reacting negatively to news of multiple terroristic attacks and this reaction is reflected in the form of depreciation in stock indexes. However, only positive shocks to killed in mosque attacks, army personal killed, and sectarian killed are having a negative impact on stock indexes and negative shocks to these variables remain statistically insignificant. This means that only positive shocks associated with these specific categories of terroristic attacks are creating abundant aggression in investors and they are reacting adversely and negatively to these shocks. The negative impact of positive shocks to attacks on a mosque and killed in mosque attack is greater as compared to positive shocks of army personal killed and killed in drone attacks, for example, with 1% increase in attacks on mosques and killed in mosque attacks depreciates the stock indexes by 0.29% and 0.37%, respectively. However, 1% increase in positive shocks to security personal killed and killed in drone attacks is causing a 0.124% and 0.069% decrease in stock indexes in the short run. Interestingly, investors react positively to these specific categories of terroristic attacks in the long run. In the long run, positive shocks to army person fatalities and mosque attacks are having a positive effect on stock indexes and investors didn’t react to positive and negative shocks to killings in drone attacks and mosques. This means that the Karachi stock exchange of Pakistan has become resilient against these terroristic attacks in the long run. Discussion sections explain reasons that why investors reacted negatively to these categories of terroristic attacks in the short run and why reacted positively in the long run.

6. Discussion

Firstly, resilience in a community can also be recognized as social susceptibility. Resilience in the community depends upon the absorbing capacity and dynamic capabilities of communities to resist disruption within the environment (Wisner, Citation2015). The baseline resilience indicator for different communities has been estimated through the utilization of certain economic indicators like infrastructure and institution development status (Cutter et al., Citation2015). In the case of an organization, there are firm-level variables that play an important role in managing the resilience within the firm like profitability, total assets, paid-up capital, cash, and stock dividends.

Resources that are available for community play a moderating role for building resilience within the framework (Arrivillagaa, Citation2015; Joerina, Citation2012; Kofi Akamania, Citation2014; Ranjan, Citation2014). Resources within an organization like profitability, assets and total sales play moderating variables to cope against any disruption within the framework. Profitability, total assets and increase in the number of sales are main sources for building absorbing capacity, dynamic capability and capacity to resist disruptions. There is possibility that in the short term, investors may be concerned about environmental problems such as terroristic disruptions, but they did not put much focus on the disruption in the long term because these terroristic events are not affecting the productivity and profitability of the firms.

Profitability is a firm-level variable within a financial statement providing support for resilience against future disastrous situation. Profitability also plays an important role for strategic planning and policies implementation when a company decides to compete in a market (Stierwald, Citation2009). Companies with larger profits are having greater chances to compete in environment against disruptions than lower profitable firms. Profitability is firm-level variable exhibiting inherited properties of providing resilience against frontal attacks whether these attacks are in shape of competing company’s product or its policies (Olhager, Citation2002).

Secondly, according to the prospect theory of Daniel Kahneman; every investor has their different preferences to buy the stock. Some investors buy attention-grabbing stock (Barber, Citation2007). They have spent a huge time to realize the return of those stocks and then invest in these stocks. The firm with greater profitability, extraordinary asset accumulation, and lower financial charges also enable an investor to grab stocks of these firms. Data from 1996 to 1997 have been observed in Korea and disclosed that international investors are less willing to invest at times of crisis (Hyuk Choea, Citation1999). Thus, at the time of crisis profitability of the firm decreases and has been providing a negative force of attraction for all these international and local investors in the short run. Individuals also tendon news regarding their purchase activity of different stocks (Melnick & Eldor, Citation2010; El Ouadghiri & Peillex, Citation2018; Papakyriakou et al., Citation2019). There is a possibility that only in the short run, the different type of terroristic activities as like security personal killed and killed in mosque attacks may provide distortion in between the buying and selling pattern of stocks. Chesney et al. (Citation2011) stated that certain terroristic events have a temporary effect on stock indexes only on day of happenings. Therefore, negative news like security personals killed, attacks on mosques, killed in attacks on mosques, and killed in drone attacks also having a negative effect on stock prices in the short run only. However, civilians killed, a terrorist killed and the total number of fatalities is having a positive influence on stock indexes in the short run and long run. This means that investors only reacted negatively to positive shocks of killing in mosque attacks, mosque attacks, security personal killings, and killed in drone attacks in the short run. One of the primary reasons for the negative reaction of investors to positive shocks of these terrorist attacks in the short run only is due to the psychological affiliation of Pakistan’s stock exchange investors with religious monuments like mosques and patriotic love with security individuals fighting against terrorism in Pakistan. Terroristic events damaging the religious houses of worship and killings of security forces generate aggression in investors which may lead towards the negative fluctuation in stock indexes.

Another reason that why positive shocks to certain independent variables like killed in mosque attacks, mosque attacks, security personal fatalities, and killed in drone attacks are harming stock indexes in the short run only is due to the factor that investors consider only these attacks as a benchmark of intensive environmental turbulence. Because of these specific environmental turbulences, investors begin to sell their shares at low prices which have affected the stock prices in a negative way (Corbet et al., Citation2018; Melnick & Eldor, Citation2010). However, these environmental turbulences may not affect micro firm-level variables like profitability, which may be a reason that investors respond positively to positive shocks of these terroristic attacks.

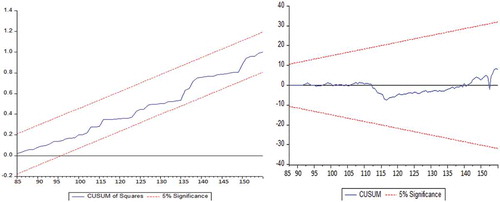

Table and Figure report the asymmetrical effect of multiple categories of terroristic attacks on stock indexes in presence of macroeconomic volatility and stability of model, respectively. Table reports that there exist asymmetrical relationship between stockindexes, army personal killed, terrorist killed and exchange rate both in short run and long run. However, in short run there exists asymmetrical relationship between all categories of terroristic attacks and stock indexes except total number of fatalities.

Figure 3. CUSUM of square and CUSUM stability test for NARDL model.

7. Conclusion and future research directions

This research article contributes to the existing literature in the following ways. Firstly, daily activities of multiple terroristic attacks from 2002 to 2015 have been taken into account to find out the asymmetrical effect of terroristic attacks on stock indexes in the presence of macroeconomic volatility. The Institute of conflict management has descriptive timelines representing the daily terroristic activities of the South Asian region. Each daily timeline is scanned and more than 4600 observations have been taken into account. Later on, terroristic attacks are divided into different categories such as attacks on the mosque, killed in mosque attacks, army personal killed, sectarian killed, killed in drone attacks, civilians killed, the total number of fatalities, and terrorist killed. Daily time-series data of multiple categories of terroristic attacks are further transformed into monthly data because our research objective is to find out the asymmetrical effect of these terroristic attacks on stock indexes in the presence of macroeconomic volatility. Secondly, this research article contributes to the existing literature by finding out the positive and negative effects of different terroristic activities on stock indexes by utilizing the Non-linear autoregressive distributive lag model. However, in the existing literature, most of the research articles only acknowledged specific terroristic attacks like the 9/11 incident in the US or bomb blasts in Bombay, India while finding the symmetrical effect of these terroristic attacks on stock indexes using event study methodology. This is the first research article that has found the effect of multiple attacks on stock indexes in the short run and long run. Interestingly, research findings indicate that positive shocks to attacks on mosques, killed in mosque attack, army personal fatalities, and killed in drone attacks are negatively associated with stock indexes only in the short run. However, the long-run effect of positive shocks to killings in drone and killed in mosque attacks on stock indexes are insignificant and positive shocks to army personal killed and attacks on mosque are having a positive effect on stock indexes. This shows that the Karachi stock exchange remains resilient against the number of terrorist attacks in the long run. The results section explains in great detail that why positive shocks of these terroristic attacks are affecting negatively in the short run, and why they are affecting stockindexes in a positive manner for the longer run. Findings also show that only total fatalities and civilian fatalities are having a positive effect on KSE-100 indexes in the shorter run and longer run.

This research article has found the resilience of the Karachi stock exchange in the long run. Future research should be conducted on the asymmetrical effect of multiple terroristic attacks on stock indexes of other south Asian economies. Moreover, it is also important to find out the role of firm-level variables in managing the resilience of the Karachi stock exchange in the long run. ARDL and NARDL models can be utilized to find out the effect of terroristic attacks on firm-level variables like profitability, assets, sales, revenues, etc. Pakistan and the whole world is affected due to coronavirus cases, another important research idea is to find out the symmetrical and asymmetrical effect of coronavirus cases and death on stock indexes by using certain control measures like GDP, energy utilization, Money supply, etc (see Sheikh et al., Citation2018).

Policy recommendations

This research article contributed empirically by finding out the asymmetrical effect of multiple terroristic attacks on stock indexes. This is an important practical implication for academicians to study the short-run and long-run asymmetrical effect of multiple categories of terroristic attacks on the stock index of IRAN, INDIA, and IRAQ. There exists an asymmetrical relationship between stock indexes and terrorism rather than linear. This research also poses important policy guidelines for security agencies of Pakistan to deal with attacks on mosques, killing in mosque attacks, security personal fatalities and killed in drone attacks during the war on terrorism to make the stock exchange resilient in the short run. Short-term investors should also consider that certain terroristic attacks are having a negative effect on stock indexes in the short run so they should take into account the importance of terroristic attacks while investing in the stock exchange. However in long run, the KSE-100 indexes remained resilient.

correction

This article has been republished with minor changes. These changes do not impact the academic content of the article.

Additional information

Funding

Notes on contributors

Mosab I. Tabash

Dr Mosab I. Tabash is program director for Master of Business Administration at college of business, Al Ain University, UAE. He has also published numerous works in high impact factor Scopus and web of science journals.

Umaid A. Sheikh

Umaid A. Sheikh is expert in econometrics and is having interest for exploring symmetrical and asymmetrical linkages between macroeconomic and stock indexes. Previously he has also published numerous research articles in Web of Science Core Collection, Scopus indexed and Australian Business Dean Council. He is interested in applying Linear and Non-linear econometric approach for finding innovative interesting and “never explored before” linkages between variables of interest.

Muzaffar Asad

Dr Muzaffar Asad has completed his PhD from Malaysia and now associated with University of Bahrain as Assistant Professor. Previously, he has served Foundation University Islamabad as Associate Professor and University of Central Punjab, Lahore as Assistant Professor.

Notes

1. Drone attacks means total number of attacks made by US security agencies within Pakistan’s territories in order to destroy terroristic camps and militant strongholds (Warrior, Citation2015). Although it also questions Pakistan’s supremacy and sovereignty but Government of Pakistan regularly issue multiple stances that US security agencies are doing these attacks in collaboration with Pak Armed forces.

2. Observation on daily basis have been transformed into monthly basis by counting daily number of terroristic attacks of different categories for every month from 2001–2015. Major purpose of doing this is because of our research objective; to find out the effect of terroristic attacks on stock market in presence of macroeconomic volatility (Exchange rate). In existing literature many researchers have utilized monthly values of exchange rate in order to find out their effect on stock prices(Adjasi et al., Citation2011; Ajaz et al., Citation2017; Andriansyah & Messinis, Citation2019; Hyde, Citation2007; Kisswani & Elian, Citation2017; Mathur & Shekhawat, Citation2018; Salvatore, Citation2019; Umar & Sun, Citation2015). Daily exchange rate fluctuation for 14 years is very hard to get, equally non-existent and empirically undetermined.Kashif (Citation2019) found the determinants of terrorism by using monthly time series data of inflation, GDP and poverty.

References

- Abdullah, A. (2013). Terrorism and stock market development: Causality evidence from Pakistan. Journal of Financial Crime, 20(1), 116–23. https://doi.org/10.1108/13590791311287364

- Adam Rosea, E. K. (2013). An economic framework for the development of a resilience index for business recovery. International Journal of Disaster Risk Reduction, 72–83.

- Adjasi, C. K. D., Biekpe, N. B., & Osei, K. A. (2011). Stock prices and exchange rate dynamics in selected African countries: A bivariate analysis. African Journal of Economic and Management Studies, 2(2), 143–164. https://doi.org/10.1108/20400701111165623

- Ainuddina, S. (2012). Community resilience framework for an earthquake prone area in Baluchistan. International Journal of Disaster Risk Reduction, 2(1), 25–36. https://doi.org/10.1016/j.ijdrr.2012.07.003

- Ajaz, T., Nain, M. Z., Kamaiah, B., & Sharma, N. K. (2017). Stock prices, exchange rate and interest rate: Evidence beyond symmetry. Journal of Financial Economic Policy, 9(1), 2–19. https://doi.org/10.1108/JFEP-01-2016-0007

- Andriansyah, A., & Messinis, G. (2019). Stock prices, exchange rates and portfolio equity flows: A toda-yamamoto panel causality test. Journal of Economic Studies, 46(2), 399–421. https://doi.org/10.1108/JES-12-2017-0361

- Anh Phuong, C. E. (2009). Acts Of Terrorism And Their Impacts on stock index returns and Volatility: The case of karachi and Tehran stock exchanges. International Journal of Economics Research, 12–24.

- Arin, K. P., Ciferri, D., & Spagnolo, N. (2008). The price of terror: The effects of terrorism on stock market returns and volatility. Economics Letters, 101(3), 164–167. https://doi.org/10.1016/j.econlet.2008.07.007

- Arrivillagaa, M. (2015). Resilience processes in women leading community based organizations providing HIV prevention services. HIV & AIDS Review, 85–89.

- Awodumi, O. B., & Adewuyi, A. O. (2020). The role of non-renewable energy consumption in economic growth and carbon emission: Evidence from oil producing economies in Africa. Energy Strategy Reviews, 27, 100434. https://doi.org/10.1016/j.esr.2019.100434

- Baltaci, H. Ş. (2014). Validity and reliability of the resilience scale for early adopscents. Procedia - Social and Behavioral Sciences, 454–468.

- Barber, B. M. (2007). All that glitters: The effect of attention and news on the buying behavior of individual and institutional investors. The Review of Financial Studies, 785–818.

- Baz, K., Xu, D., Ampofo, G. M. K., Ali, I., Khan, I., Cheng, J., & Ali, H. (2019). Energy consumption and economic growth nexus: New evidence from Pakistan using asymmetric analysis. Energy, 189, 116254. https://doi.org/10.1016/j.energy.2019.116254

- BBC news headline, N. (2005, 9). Pakistan ‘extremist leader’ held. Retrieved September, 2005, from BBC news http://news.bbc.co.uk/2/hi/south_asia/4289740.stm

- becker, P. (2014). Sustainability science; Managing risk and resilience for sustainable dovelopment. Elsevier.

- Bell, M. A. (2002). The Five Principles of Organizational Resilience. The gartner(A Research Review), 1–7.

- Bennett-Jones, O. (2011). Pakistan a failed state or a clever gambler. Retrieved, 2015, from BBC news South asia http://www.bbc.co.uk/news/world-south-asia-13318673

- Brooks, C. (1996). Testing for non-linearity in daily sterling exchange rates. Applied Financial Economics, 6(4), 307–317. https://doi.org/10.1080/096031096334105

- Charfeddine, L., & Barkat, K. (2020). Short- and long-run asymmetric effect of oil prices and oil and gas revenues on the real GDP and economic diversification in oil-dependent economy. Energy Economics, 86, 104680. https://doi.org/10.1016/j.eneco.2020.104680

- Chesney, M., Reshetar, G., & Karaman, M. (2011). The impact of terrorism on financial markets: An empirical study. Journal of Banking & Finance, 35(2), 253–267. https://doi.org/10.1016/j.jbankfin.2010.07.026

- Corbet, S., Gurdgiev, C., & Meegan, A. (2018). Long-term stock market volatility and the influence of terrorist attacks in Europe. The Quarterly Review of Economics and Finance, 68(1), 118–131. https://doi.org/10.1016/j.qref.2017.11.012

- Cutter, S. L., Ash, K. D., & Emrich, C. T. (2015). The geographies of community disaster resilience. Global Environmental Change, 65–77.

- El Ouadghiri, I., & Peillex, J. (2018). Public attention to “Islamic terrorism” and stock market returns. Journal of Comparative Economics, 46(4), 936–946. https://doi.org/10.1016/j.jce.2018.07.014

- Essaddam, N., & Karagianis, J. M. (2014). Terrorism, country attributes, and the volatility of stock returns. Research in International Business and Finance, 31, 87–100. https://doi.org/10.1016/j.ribaf.2013.11.001

- Fareed, Z., Meo, M. S., Zulfiqar, B., Shahzad, F., & Wang, N. (2018). Nexus of tourism, terrorism, and economic growth in Thailand: new evidence from asymmetric ARDL cointegration approach. Asia Pacific Journal of Tourism Research, 23(12), 1129–1141. doi:10.1080/10941665.2018.1528289

- Feridun, M., & Shahbaz, M. (2010). FIGHTING TERRORISM: ARE MILITARY MEASURES EFFECTIVE? EMPIRICAL EVIDENCE FROM TURKEY. Defence and Peace Economics, 21(2), 193–205. https://doi.org/10.1080/10242690903568884

- Galadima, M. D., & Aminu, A. W. (2020). Nonlinear unit root and nonlinear causality in natural gas - economic growth nexus: Evidence from Nigeria. Energy, 190(1), 116415. https://doi.org/10.1016/j.energy.2019.116415

- Gok, I. Y., Demirdogen, Y., & Topuz, S. (2020). The impacts of terrorism on Turkish equity market: An investigation using intraday data. Physica A: Statistical Mechanics and Its Applications, 540, 123484. https://doi.org/10.1016/j.physa.2019.123484

- Hatler, C. (2013). Resilience building: A necessary leadership competence. Nurse Leader, 32–34, 39.

- Hussain, S. S. J., Josef, S. P., Ravinesh, K. R., & Tanveer, A. (2017). The impact of terrorism on industry returns and systematic risk in Pakistan: A wavelet approach. Accounting Research Journal, 30(4), 413–429. https://doi.org/10.1108/ARJ-09-2015-0114

- Hyde, S. (2007). The response of industry stock returns to market, exchange rate and interest rate risks. Managerial Finance, 33(9), 693–709. https://doi.org/10.1108/03074350710776244

- Hyuk Choea, B.-C. K. (1999). Do foreign investors destabilize stock markets? The Korean experience in 1997. Journal of Financial Economics, 54(2), 227–264. https://doi.org/10.1016/S0304-405X(99)00037-9

- Ismail, A., & Amjad, S. (2014). Determinants of terrorism in Pakistan: An empirical investigation. Economic Modelling, 37, 320–331. https://doi.org/10.1016/j.econmod.2013.11.012

- Jakob, L. J., & Christoffer, B. N. (2017). Global catastrophe effects – The impact of terrorism ☆. In T. J. Andersen (Ed.), The responsive global organization (pp. 205–238). Emerald Publishing Limited. https://doi.org/10.1108/978-1-78714-831-420171008

- Joerina, J. (2012). Assessing community resilience to climate-related disasters in Chennai, India. International Journal of Disaster Risk Reduction, 1(1), 44–54. https://doi.org/10.1016/j.ijdrr.2012.05.006

- Karamelikli, H., Khan, A. A., & Karimi, M. S. (2019). Is terrorism a real threat to tourism development? Analysis of inbound and domestic tourist arrivals in Turkey. Current Issues in Tourism, 1–17. doi:10.1080/13683500.2019.1681945

- Kärrholm, M. (2014). Spatial resilience and urban planning: Addressing the interdependence of urban retail ares. Cities, 36(1), 121–130. https://doi.org/10.1016/j.cities.2012.10.012

- Kashif, M. (2019, January 1). Nonlinear effect of FDI, economic growth, and industrialization on environmental quality. (A. Ayesha, Ed.). Management of Environmental Quality: An International Journal. https://doi.org/10.1108/MEQ-10-2018-0186

- Kaveh Shahraki, S. F. (2011). The effect of terrorism on financial markets; Tehran & karachi stock exchange price index. Interdeciplinary Journal Fo Contemporary Research in Business, 47–58.

- Kim, H. S., Kang, D. S., & Kim, J. H. (2003). The BDS statistic and residual test. Stochastic Environmental Research and Risk Assessment, 17(1), 104–115. https://doi.org/10.1007/s00477-002-0118-0

- Kisswani, K. M., & Elian, M. I. (2017). Exploring the nexus between oil prices and sectoral stock prices: Nonlinear evidence from Kuwait stock exchange. Cogent Economics & Finance, 5(1), 1286061. https://doi.org/10.1080/23322039.2017.1286061

- Kofi Akamania, P. I. (2014). Barriers to collaborative forest management and implications for building the resilience of forest-dependent communities in the Ashanti region of Ghana. Journal of Environmental Management, 11–21.

- Kollias, C., Kyrtsou, C., & Papadamou, S. (2013). The effects of terrorism and war on the oil price–stock index relationship. Energy Economics, 40, 743–752. https://doi.org/10.1016/j.eneco.2013.09.006

- Kumar, S. (2013). Impact of terrorism on international stock markets. Journal of Applied Business and Economics, 8(2), 43–60. https://doi.org/10.1108/17468801311306984

- Kusumastuti, R. D., Husodo, Z. A., Suardi, L., & Danarsari, D. N. (2014). Developing a resilience index towards natural disasters in Indonesia. International Journal of Disaster Risk Reduction, 1, 327–340. https://doi.org/10.1016/j.ijdrr.2014.10.007

- Laborda, R., & Olmo, J. (2019). An Empirical Analysis of Terrorism and Stock Market Spillovers: The Case of Spain. Defence and Peace Economics, 1–19. doi:10.1080/10242694.2019.1617601

- Laila, M., & Guruprasad, S. (2019). Impact of terrorism on stock markets across the world and stock returns: An event study of Taj attack in India. Journal of Financial Crime, 26(3), 793–807. https://doi.org/10.1108/JFC-09-2018-0093

- Liu, A., & Pratt, S. (2017). Tourism’s vulnerability and resilience to terrorism. Tourism Management, 60, 404–417. https://doi.org/10.1016/j.tourman.2017.01.001

- Lucini, B. (2013). Social capital and sociological resilience in Megacities context. International Journal of Disaster Resilience in Built Environment, 4(1), 58–71. https://doi.org/10.1108/17595901311299008

- Malik, E. (2011). War on terror: Pakistan reminds Americans of its sacrifices, with an ad. Retrieved, 2015, from The express tribune with the international new york times http://tribune.com.pk/story/250532/war-on-terror-pakistan-reminds-americans-of-its-sacrifices-with-an-ad/

- Mathur, S. K., & Shekhawat, A. (2018, January 1). Exchange rate nonlinearities in India’s exports to the USA. (S. Abhishek, Ed.). Studies in Economics and Finance. https://doi.org/10.1108/SEF-07-2015-0179

- Meierrieks, D., & Schneider, F. (2016). The short- and long-run relationship between the illicit drug business and terrorism. Applied Economics Letters, 23(18), 1274–1277. Retrieved from https://doi.org/10.1080/13504851.2016.1150942

- Melnick, R., & Eldor, R. (2010). Small investment and large returns: Terrorism, media and the economy. European Economic Review, 54(8), 963–973. https://doi.org/10.1016/j.euroecorev.2010.03.004

- MengYun, W., Imran, M., Zakaria, M., Linrong, Z., Farooq, M. U., & Muhammad, S. K. (2018). Impact of terrorism and political instability on equity premium: Evidence from Pakistan. Physica A: Statistical Mechanics and Its Applications, 492, 1753–1762. https://doi.org/10.1016/j.physa.2017.11.095

- Muhammad, A. (2017a). Modelling the asymmetric impact of defence spending on economic growth: An evidence from non-linear ARDL and multipliers. Journal of Economic and Administrative Sciences, 33(2), 131–149. https://doi.org/10.1108/JEAS-03-2017-0010

- Muhammad, A. (2017b). Modelling the asymmetric impact of defence spending on economic growth. Journal of Economic and Administrative Sciences, 33(2), 131–149. https://doi.org/10.1108/JEAS-03-2017-0010

- Narayan, S., Le, T.-H., & Sriananthakumar, S. (2018). The influence of terrorism risk on stock market integration: Evidence from eight OECD countries. International Review of Financial Analysis, 58, 247–259. https://doi.org/10.1016/j.irfa.2018.03.011

- Nedelescu, R. B. (2005, March). Impact of terrorism on financial Market. International Monetary fund(IMF) WORKING PAPER, 1–25.

- Nisar. (2015). Neighbouring country fuelled terror fire in Pakistan; Nisar (Defense Minister). Retrieved, 2015, from International the news By Mir khalil ur rehman http://www.thenews.com.pk/Todays-News-13-36014-Neighbouring-country-fuelled-terror-fire-in-Pakistan-Nisar

- Olhager, J. (2002). Manufacturing flexibility and profitability. International Journal of Production Economics, 67–78.

- Onanuga, A. T., Odusanya, I. A., & Adekunle, I. A. (2020). Terrorism and financial flows in Africa. Behavioral Sciences of Terrorism and Political Aggression, 1–18. doi:10.1080/19434472.2020.1736128

- Orbaneja, J. R. V., Iyer, S. R., & Simkins, B. J. (2018). Terrorism and oil markets: A cross-sectional evaluation. Finance Research Letters, 24(1), 42–48. https://doi.org/10.1016/j.frl.2017.06.016

- Papakyriakou, P., Sakkas, A., & Taoushianis, Z. (2019). The impact of terrorist attacks in G7 countries on international stock markets and the role of investor sentiment. Journal of International Financial Markets, Institutions and Money, 61(3), 143–160. https://doi.org/10.1016/j.intfin.2019.03.001

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289–326. doi:10.1002/(ISSN)1099-1255

- Proag, V. (2014). Acessing and measuring resilience. Procedia Economics and Finance, 18(2), 222–229. https://doi.org/10.1016/S2212-5671(14)00934-4

- Rajesh, S. (2019). Dynamism between selected macroeconomic determinants and electricity consumption in India. International Journal of Social Economics, 46(6), 805–821. https://doi.org/10.1108/IJSE-11-2018-0586

- Ranjan, E. S. (2014). A study on community’s perception on disaster resilience concept. Procedia Economics and Finance, 18(3), 88–94. https://doi.org/10.1016/S2212-5671(14)00917-4

- Rapp, B. B. (2014). Stakeholder management in disaster restoration projects. International Jounral of Desaster Resilience in Built Environment, 182–193.

- Robert, Y. H. (2012). Preparedness: The state of the art and future prospects. Disaster Prevention and Management: An International Journal, 404–417.

- Salvatore, C. (2019). The long-run interrelationship between exchange rate and interest rate: The case of Mexico. Journal of Economic Studies, 46(7), 1380–1397. https://doi.org/10.1108/JES-04-2019-0176

- Shahbaz, M. (2013). Linkages between inflation, economic growth and terrorism in Pakistan. Economic Modelling, 32, 496–506. https://doi.org/10.1016/j.econmod.2013.02.014

- Shaikh, I. (2019). The impact of terrorism on Indian securities market. Economic Research-Ekonomska Istraživanja, 32(1), 1744–1764. https://doi.org/10.1080/1331677X.2019.1638284

- Sheikh, U. A., Asad, M., Ahmed, Z., & Mukhtar, U. (2020). Cogent Economics & Finance Asymmetrical relationship between oil prices, gold prices, exchange rate, and stock prices during global financial crisis 2008: Evidence from Pakistan Asymmetrical relationship between oil prices, gold prices, exchange rate, and stock prices during global financial crisis 2008 : Evidence from. Cogent Economics & Finance, 8(1), 1-36. https://doi.org/10.1080/23322039.2020.1757802

- Sheikh, U. A., Asad, M., & Mukhtar, U. (2020). Modelling asymmetric effect of foreign direct investment inflows (FDI), carbon emission (☐☐☐) and economic growth(EG) on energy consumption(CE) of South Asian region: A symmetrical and asymmetrical panel autoregressive distributive lag model approach. Accountancy Business and the Public Interest, 193–221.

- Sheikh, U. A., Chaudhry, H., & Mukhtar, U. (2018). Financial and non-financial determinants of Asian automobile stock prices. Accountancy Business and the Public Interest, 142–162.

- Shin, Y., Yu, B., & Greenwood-Nimmo, M. (2014). Modelling Asymmetric Cointegration and Dynamic Multipliers in a Nonlinear ARDL Framework. In R. C. Sickles & W. C. Horrace (eds.), BT - Festschrift in Honor of Peter Schmidt: Econometric Methods and Applications (pp. 281–314). Springer New York. https://doi.org/10.1007/978-1-4899-8008-3_9

- Stierwald, A. (2009). Determinants of firm profitability - The effect of productivity and its persistence. Melbourne Institute of Applied Economic and Social Research;The University of Melbourne, 41–71.

- Strattaa, P. (2015). Resilience and coping in trauma spectrum symptoms prediction: A structural equation modeling approach. Personality and Individual Differences, 55–61. https://doi.org/10.1016/j.paid.2014.12.035

- Tingbani, I., Okafor, G., Tauringana, V., & Zalata, A. M. (2019). Terrorism and country-level global business failure. Journal of Business Research, 98, 430–440. https://doi.org/10.1016/j.jbusres.2018.08.037

- Trærup, S. L. (2012). Informal networks and resilience to climate change impacts: A collective approach to index insurance. A Global Enviornemnt Change, 22(1), 255–267. https://doi.org/10.1016/j.gloenvcha.2011.09.017

- Umar, M., & Sun, G. (2015). Country risk, stock prices, and the exchange rate of the renminbi. Journal of Financial Economic Policy, 7(4), 366–376. https://doi.org/10.1108/JFEP-11-2014-0073

- Valérie Angeona, S. B. (2015). Reviewing composite vulnerability and resilience indexes: A sustainable approach and application. World Development, 24(March), 2015.

- Warrior, L. C. (2015). Drones and Targeted Killing: Costs, Accountability, and U.S. Civil-Military Relations. Orbis, 59(1), 95–110. https://doi.org/10.1016/j.orbis.2014.11.008

- Wisner, B. (2015). Community resilience to disasters (2nd ed.). International Encyclopedia of the Social & Behavioral Sciences.