?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The study is intended to investigate the symmetrical relationship between macroeconomic variability and KSE-100 indexes by employing the ARDL model with bound testing procedure and error correction model. Authors have also examined whether the linkages between macroeconomic variability and KSE-100 indexes change in the wake of the 2008 Global economic recession. Macroeconomic variability is represented by fluctuations in interest rates, consumer price index, and Money supply (M2). Monthly level data representing macroeconomic volatility has been incorporated from the trading economics website and validated from the Pakistan bureau of statistics. Four different types of unit root tests like augmented dickey fuller test, KPSS, and Philips Peron unit root are also employed for the identification of seasonality effects in data. To identify structural breaks and linearity in data, the Zivot Andrew unit root test and BDS test for nonlinearity have also been employed respectively. This study adds to the existing literature by classifying investor’s different reactions to fluctuation in macroeconomic variability before and after the international economic recession. Our study results proposed that in the long run and before the international economic crunch, the money supply and interest rates have an inverse relationship with stock indexes but CPI has a direct and significant relationship. However, after the 2008 economic crisis and for a longer horizon, stock indexes have been impacted positively by money supply, and IR has formulated an inverse relationship with KSE-100 indexes. This indicated that the association between macroeconomic variations and KSE-100 indexes changes following the 2008 international economic crisis.

PUBLIC INTREST STATEMENT

Results proposed that in the longer term and before the 2008 international economic recession, the MS and IR have an inverse relationship with stock indexes but CPI have a direct and significant relationship. However, after the international financial crunch and in the long run, stock indexes are impacted positively by money supply, but IR has formulated an inverse relationship with KSE-100 indexes. However, CPI remains statistically insignificant. This illustrates that the symmetrical association between macroeconomic fundamentals and KSE-100 indexes is impacted after the occurrence of a global financial crisis. We have also utilized control measures like terroristic disruptions which may represent the country risk factors. This research article also poses important practical relevance for the Central Bank of Pakistan to consider the regime before making adjustments towards increasing or decreasing the flow of capital and policy rates within the economy. An increase in money supply is more favorable after the crisis rather than before the crisis regime for short-term and long-term investors of KSE-100 indexes.

1. Introduction

Pakistan’s economic growth in the fiscal year 2008–09 is significantly impacted by macroeconomic variations such as appreciating inflationary pressures, unemployment, high cost of borrowing and appreciated dollar prices against Pakistani rupee (Asad & Farooq, Citation2009; MengYun et al., Citation2018; Shaker et al., Citation2018; Sheikh, Asad, Ahmed et al., Citation2020). It had been a year owing to rising inflationary pressures and the emaciated output of industries. Moreover, increased global oil prices (Asad & Qadeer, Citation2014), unemployment and decreased money supply has stunned the economy with intensified trade gaps, high inflation, and the exchange rate fluctuation. Country’s economic circumstances during economic crisis 2008 have remained adverse because of persistent militant activities, volatility in macroeconomic determinants, electricity shortages and shocks to money supply of the country. As a consequence of these pressures, the economy has experienced a medium-term shift in policy. Global economic crisis-affected country ability to pay back foreign debt, because of the same reason a responsive debt strategy for the monitoring, evaluating and managing the currency risks has been established. However, political actions were aimed toward economic stability with a targeted process of recovery that started in the financial year 2009–10. This research article poses an interesting research question regarding the contribution of 2008 global economic depression in changing symmetrical relationship between macroeconomic variability and stock indexes. The economic period of Pakistan from 2002 to 2015 had suffered from intensified terroristic disruptions (Almansour et al., Citation2016; Hussain et al., Citation2017; MengYun et al., Citation2018), therefore we have also incorporated selected terroristic disruptions representing monthly time series data during the period from 2002 to 2015. Moreover, Economic period in Pakistan from 2002 to 2015 had also suffered from intensified macroeconomic fluctuations (Hussain et al., Citation2017; MengYun et al., Citation2018), therefore we have also incorporated selected macroeconomic fundamentals representing monthly time series data during the period from 2002 to 2015.

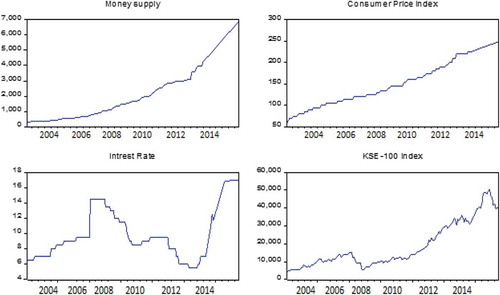

Figure 1. Macroeconomic variability and KSE-100 indexes

Figure shows that international economic depression of 2008 has adversely impacted KSE-100 indexes. Stock indexes of Karachi stock exchange depreciated from 15500 points to only 5000 points approximately. According to Figure , comparison of KSE-100 indexes with IR, CPI and MS also explains that stock indexes and macroeconomic factors exhibited impulsive characteristics during the worldwide economic recession of 2008. This furthermore motivates the researchers to explore the symmetrical associationship between macroeconomic volatility and Karachi stock exchange indexes in three different regimes, e.g., pre-economic crunch period, postinternational economic recession period, and when a whole period is taken into account. Tabash et al. (Citation2020) also investigated that non-linear estimations for exploring exchange rate and stock index nexus is more robust and effective as comared to the linear modelling techniques

The foremost aim of our study is to investigate the short run and long run symmetrical effect of macroeconomic variability on Karachi stock exchange before the global economic recessionary period, after the recessionary regime, and when the whole sample duration is taken into contemplation. In this research article, we have utilized the ARDL model to investigate the symmetrical association between macroeconomic variability in presence of terroristic disruptions. This research adds to the prevailing literature in following several ways. Firstly, in existing literature, some of the research articles have found a direct and positive influence of interest rates (Adjasi, Citation2009; Ali, Citation2019; Alkhuzaie & Asad, Citation2018; Ghulam, Citation2018; Kocaarslan & Soytas, Citation2019; Shrestha & Liu, Citation2008), money supply (Chiang Leong & Hui, Citation2014; Shrestha & Liu, Citation2008) and inflation (Adjasi, Citation2009; Shrestha & Liu, Citation2008) on stock indexes, whereas other have reported a negative influence of selected macroeconomic variations such as interest rates (Ho, Citation2018), inflation (Camilleri et al., Citation2019; Chiang Leong & Hui, Citation2014; Ho, Citation2018) and money supply (Adjasi, Citation2009; Adjasi et al., Citation2011) on stock indexes. There is no consistency in results reported by existing literature. Moreover, limited effort has been made to study the influence of international economic crunch in changing the symmetrical cointegrating association between macroeconomic fluctuation and Karachi stock exchange indexes. However, some of the research articles have studied the symmetrical relationship (Ajaz et al., Citation2017; Ho, Citation2018; Shakil et al., Citation2018) and other have considered asymmetries within time series for purpose of investigating the nonlinear linkages between macroeconomic fluctuations and stock indexes of developed countries (Charfeddine & Barkat, Citation2020; Kocaarslan & Soytas, Citation2019; Rajesh, Citation2019; Salvatore, Citation2019) rather than developing context such as Pakistan. We have considered the Pakistan stock exchange because of its exceedingly unpredictable characteristics (Sheikh et al., Citation2020).

Secondly, most of the research articles are based upon multivariate panel data analysis while considering the effect of macroeconomic changeability on stock indexes (Al‐Najjar & Taylor, Citation2008; Andriansyah & Messinis, Citation2019; Gregoriou et al., Citation2015; Sheikh et al. (Citation2018); Spilioti, Citation2016; Tuna, Citation2018; Ulusoy & Demiralay, Citation2017; Yan et al., Citation2016; Zafar et al., Citation2019) and haven’t examined the tendency of the international economic crisis in changing symmetrical linkages between macroeconomic variations and developing country’s stock indexes in presence of terroristic disruptions as a control measure. Furthermore, some of the research articles utilized time-series data but have employed asymmetrical models like NARDL (Jung et al., Citation2020; S. Kumar, Citation2019; Liang et al., Citation2020; Salvatore, Citation2019) and the EGARCH model (Pandey & Vipul, Citation2018; Sikhosana & Aye, Citation2018) for the nonlinear impact of macroeconomic capriciousness on stock indexes without considering regime, i.e. economic crisis and adoption of proper control measures and risk factors (terroristic disruptions). According to our best knowledge, this is the first research article that considers the tendency of the 2008 international economic recession in changing the symmetrical association between macroeconomic variability and Karachi stock exchange indexes before the international recessionary period, after the recession, and over the whole sample duration.

Results proposed that in the longer term and before the 2008 international economic recession, the MS and IR have an inverse relationship with stock indexes but CPI have a direct and significant relationship. However, after the international financial crunch and in the long run, stock indexes are impacted positively by money supply, and IR has formulated an inverse relationship with KSE-100 indexes. However, CPI remains statistically insignificant. This illustrates that the symmetrical association between macroeconomic fundamentals and KSE-100 indexes is changed after the occurrence of a global financial crisis. We have also utilized control measures like terroristic disruptions which may represent the country risk factors. This research article also poses important practical relevance for the Central Bank of Pakistan to consider the regime before making adjustments towards increasing or decreasing the flow of capital and policy rates within the economy. An increase in money supply is more favorable after the crisis rather than before the crisis regime for short-term and long-term investors of KSE-100 indexes.

2. Literature review

The literature review is segregated into three sections. The theoretic foundations behind the role of macroeconomic fluctuations in effecting stock indexes of developed and developing economies are explained in the first section. In the second section, the authors have enlightened the specific role of the CPI, MS, and IR in affecting stock price volatility. Third section deals with rationalization behind the inclusion of certain control variables like terroristic attacks in effecting the stock prices.

2.1. Efficient market hypothesis (EMH) and arbitrage pricing theory (APT) in explaining the macroeconomic-stock price nexus

In the existing literature, several researchers have investigated associations between macroeconomic variations and stock prices by utilizing advanced econometric techniques and validated the arbitrage pricing theory in explaining macroeconomic-stock price nexus (Christofi, Citation1993; Günsel et al., Citation2009). Andreas (1993) segregated their analysis on basis of influential capacity of the composite leading and lagging macroeconomic variables in influencing industrial stock returns and found that composite lagging economic factors have been more effectually impacting and framing investor’s psychological intentions towards stock returns than composite leading economic factors. Günsel et al. (Citation2009) have utilized the ordinary least square regression by incorporating monthly data from 2001 to 2005 and found cointegrating linkages between a series of macroeconomic variability and the Istanbul stock exchange.

Variations in macro-economy and stockholder’s sentiments originated the stock price volatility in the London stock exchange. Spilioti (Citation2016) have utilized time series and panel data models to investigate the differences between forecasted returns and realized stock returns. Authors have estimated fundamental values of stock return by employing Barberies et al. (Citation1998) valuation model and found that deviations of realized stock prices from forecasted stock prices are generally due to variations in investors’ sentiments and the number of macroeconomic fluctuations. In existing published research articles, the Arbitrage pricing theory (APT) and efficient market hypothesis (EMH) have been utilized as the theoretical underpinning in explaining the possible association between macroeconomic changeability and stock prices. APT purposed a symmetrical association between fluctuation in macroeconomic factors and stock prices (Andreas., 1993; Günsel et al., Citation2009; Mollick & Nguyen, Citation2015) and EMH stated that internal firm level and external news is previously incorporated in stock prices (Andriansyah & Messinis, Citation2019; Floros & Vougas, Citation2008; Othman et al., Citation2019; Wickremasinghe, Citation2011). Therefore, on basis of public information, investors can’t earn higher than the market average. Wickremasinghe (Citation2011) refuted the semistrong version of the EMH by establishing a shorter and longer-term association between macroeconomic fluctuations and stock indexes. Singhania and Prakash (Citation2014) indicated that South Asian stock prices can be predicted on basis of previous stock price movements and therefore efficient market hypothesis has been rejected for India, Pakistan, Sri-Lankan, and Bangladesh stock exchange.

Floros and Vougas (Citation2008) utilized EMH to explain the short-run and long-run association between Greek stock index futures contracts traded at Athens stock exchange and spot prices by utilizing daily observations from 1999 to 2001. Authors have found that Greek future prices can predict spot prices traded at Athens derivate exchange during the 1999–2000 financial crisis. Reid and Gupta (Citation2013) have utilized event study methodology in parallel with the Bayesian vector auto regression model for estimating the immediate effect of macroeconomic news on stock exchange and the dynamic linkages between macroeconomic variations and stock indexes, respectively. Findings based on the event study methodology suggested that monetary policy shocks negatively influence the South African stock market. Moreover, authors have also utilized the Bayesian VAR model and found that inflationary pressure impacts the stock market of the whole South African region. Building upon arbitrage pricing theory, Saumya (Citation2012) recommended investing in those shares that are affected by sentiment risks of investors especially when the market is following depreciating trends because such stocks are hard to value and difficult to arbitrage. Mollick and Nguyen (Citation2015) utilized the APT to explain the asymmetric association between fluctuations in currency values, oil prices, and yield return on major stock prices of the US oil and gas sector during the global financial crisis.

2.2. Relationship between consumer price index (CPI), interest rates (IR), money supply (MS), and stock indexes (SI)

Laopodis (Citation2008) applied value at risk methodology to evaluate the influence of real investment expenditure on the US stock market covering 40 years period from 1960 to 2005. Results unveiled a substantial association between real investment and stock indexes during the first regime from 1960 to 1990. But this relation has remained insignificant for the second regime covering the period from 1990 to 2015, and real investment expenditure has been adversely impacted because of high stock market growth. Shrestha and Liu (Citation2008) employed linear modelling techniques and established symmetrical cointegration between selected macroeconomic variations and Chinese stock indexes by using monthly data. Results indicated long-term cointegration between MS, IR, exchange rate, inflation, and Chinese stock indexes, and most of the Chinese shareholders are benefited by utilizing diversification strategies and better returns because of the continual growth of the Chinese economy. Agyire‐Tettey and Kyereboah‐Coleman (Citation2008) utilized the error correction method and investigated the influence of macroeconomic variations on Ghana stock indexes by utilizing quarterly data from 1991 to 2005. Authors have found the inverse impact of the high cost of borrowing and inflationary pressure on the Ghana stock exchange. Adjasi (Citation2009) estimated the influence of macroeconomic variation on stock indexes in two stages by utilizing two distinct but advanced econometric techniques such as EGARCH modeling at the first stage and computation of the volatility effect of macroeconomic variables from the square residual of mean at the second stage. EGARCH results reported that higher volatility in interest rates and inflation are having a direct effect on the volatility of stock indexes whereas volatility of oil, gold, and MS depreciates the variability of Ghana stock indexes

Peiró (Citation2016) found that industrial production and interest rate formulate associationship with stock indexes of the three largest European developed economies, e.g., England, Germany, and France, and macroeconomic variations are projected for triggering half of stock prices volatility in the biggest economies of Europe. Nguyen and Ngo (Citation2014) investigated the impact of the seemingly unrelated influence of multiple categories of macroeconomic uncertainty on economically established and emerging Asian economies’ stock indexes by utilizing monthly time series data from 2002 to 2012. Evidence reported that macroeconomic fluctuation in terms of US labor market indicator more strongly influences the Asian stock indexes of emerging as well as developed economies as compared to other categories of US macroeconomic news. Mazuruse (Citation2014) reported a positive influence of inflation, exchange rate, MS, and IR on Zimbabwean Stock indexes. Tiwari et al. (Citation2015) reported a positive influence of inflation on stock indexes by employing continuous wavelet transformation on monthly time series data from 1961 to 2012. Shahbaz (Citation2013) explored the relation between inflationary pressures, economic development, and terroristic disruptive activities using yearly frequency data for the period 1971–2010 as the longest time possible in Pakistan for reliable results. The scientific evidence supported cointegration between the increase in commodity prices, economic development, and extremism by using a symmetrical ARDL modeling approach. Inflation raises terroristic and criminal occurrences, and economic prosperity also contributed greatly toward terrorism.

Mouna (Citation2019) employed a dynamic conditional correlation GARCH model along with a continuous wavelet decomposition technique for purpose of reconnoitering spillover effects between investor attitude, Chinese stock indexes, and oil prices by utilizing monthly and daily time-series data from 2014 to 2016. Findings suggested that there exists a dynamic correlation between Chinese stock price movement and oil price shocks, and the BEKK GARCH model furthermore confirm the association between investor sentiment and oil price volatility. Fatima et al. (Citation2018) found that the impact of negative news on Islamic stock prices is greater as compared to the magnitude of the impact of positive news by utilizing exponential generalized autoregressive conditional heteroskedastic modeling covering the period from 2009 to 2016. Furthermore, authors have also analyzed the spillover impact across various countries and found that appreciation in stock prices in one country also appreciates stock prices in another country. Kumar and Dhankar (Citation2017) utilized the GARCH family of models to examine the influence of international financial variability on stock indexes of the South Asian region for both shorter and longer horizons. The inordinate level of configuration between India, Pakistan, and Sri Lankan stock indexes has been identified by observing considerable similarities in terms of stock yields and stock return variability. South Asian equity markets are profoundly different from one another in terms of competitive market pressures, governmental and economic conditions. Tuna (Citation2018) is aimed at examining the cointegrating association between precious metal stocks, for example, gold, silver, platinum, palladium, and equity markets in 21 developed and 11 developing countries. The research analyzed the long-term relationship between the precious metal stocks and Islamic equity markets in countries clustered according to their growth level by the Morgan Stanley Capital Index (MSCI). Findings suggested that gold, silver, platinum, and palladium are effective diversification tools only in the case of developed countries, and however silver and platinum cannot be included in the list of effective diversification tools for developing countries.

Ho (Citation2018) employed linear ARDL model to study the influence of macroeconomic indicators such as interest rate, banking sector development, inflation, interest rate, and trade openness on South African stock market growth by using time series data from 1975 to 2015. Authors have reported that inflation and interest rates impede the South African stock market development, however, banking sector development fosters stock market growth. Abbas et al. (Citation2017) utilized the GARCH model and unrestricted VAR to investigate the impact of macroeconomic volatility on stock indexes of G7 countries in two distinct stages by covering the period from 1985 to 2015. Results reported closer integration of interest rates with stock indexes but the impact of macroeconomic volatility in affecting stock indexes is very lower at the individual level and the impact of macroeconomic volatility transmission on stock indexes becomes stronger at the collective level. In a similar study, Simbolon and Purwanto (Citation2018) investigated whether macroeconomic indicators such as local lending rates, inflationary pressure, currency value fluctuation, and economic growth rates have a direct impact on Indonesian stock prices and found that all variables except GDP growth rate have a significant direct effect on Indonesian real estate stock prices. Authors concentrated mostly on property investment and real estate firms classified in the Indonesian stock exchange, which epitomized the volatile characteristics of most of the real estate firms in those days and their market valuation was highest in 2012.

There’s a debatable question that whether gold can display hedging properties or safer haven for investors at the time of financial mayhem. The aim of Shakil et al. (Citation2018) study, therefore, is to take Saudi Arabia as a case to analyze Saudi Arabia’s gold price connection with main macroeconomic factors such as stock market index, oil prices, exchange rate, IR, and CPI by employing symmetrical ARDL model. Their study findings indicated that gold continues to be a valuable investment in its portfolio and an inflation buffer. Policy measures to restrict imports of gold are practically counterproductive. Camilleri et al. (Citation2019) indicated that the stock indexes of Germany, France, Belgium, and the Netherlands have contributed to inflation over the period from 1999 to 2017 by employing the VAR modeling technique. Furthermore, in almost all selected economies, stock indexes dramatically contribute to an increase in industrial output.

2.3. Relationship between terroristic attacks and stock indexes

Shaikh (Citation2019) investigated impact of multiple terroristic attacks on the Indian stock exchange by using monthly time series data from 1980 to 2014. There were a total number of 9069 terroristic assaults in India, which culminated in 17,953 deaths and 26,732 injured. Many incidents and in particular those around the vicinity of Bombay have more adversely influenced the volatility of Bombay stock indexes as compared to others which have happened in far-flung areas. In the last 15 years, terrorist threats in the Basque Country have declined dramatically and tactics have changed to counter such assaults (Barros et al., Citation2009). While a target style of the assassination was common (killing only leaders, prominent personalities, etc.) and trends that created an urban-insurgency-oriented combat climate, which is referred to as the “kale Borroka” in Basque. Barros et al. (Citation2009) have periodically measured the magnitude of the region’s violence, the effectiveness of mitigating police violence, and stringent protection policies adopted by the authorities were investigated. Results indicated that the stock market index declined as a result of the terroristic incidents in the district.

Aslam and Kang (Citation2015) have found a short-lived effect of terrorism on Pakistan’s stock exchange and the economy rebounds from terrorist impacts within one day. Laborda and Olmo (Citation2019) created an index representing multiple acts of terrorism: domestic terrorism (ETA) and foreign terroristic attacks attributable to Islamic terrorism covering the period from 1973 to 2017 and authors have found that terrorist attacks in Spain have created forecast error variance in stock returns. Terrorism has not affected stock prices directly, but it has inflated investor’s emotions and disillusioned the investors which in return causes stock price fluctuation (Aslam & Kang, Citation2015; Laila & Guruprasad, Citation2019; Narayan et al., Citation2018). The impact of terroristic disruption on stock indexes may vary from one country to another. It may be possible that terroristic disruptions within Pakistan more profoundly and negatively impact stock indexes as compared to terroristic disruptions in India. Corredor et al. (Citation2015) explored the impact of shareholder sentiment on market returns in the Czech Republic, Hungary, and Poland. The findings suggested that the impact of shareholder’s sentiments on values of stock traded in these markets differ greatly in contrast with more mature developed European markets.

Across all economies, particularly in developed countries, the investment inflows due to (FDI) are crucial for economic expansion. FDI influxes significantly accelerated over the last few years in several developed nations. However, FDI inflows decreased in Pakistan in the last ten years. Bano et al. (Citation2019) have investigated the factors for decreased FDI inflows into Pakistan, with certain monetary policy measures as control variables and taking into account the major issues such as terrorism, energy deficit, financial insecurity, and political uncertainty. Findings indicated that resource scarcity, financial insecurity, and political uncertainty have negative repercussions and extremism has negligible consequences for Pakistan’s FDI inflows before the economic crisis. Barros and Gil-Alana (Citation2009) examined how severe terrorism in the Basque nation has a detrimental effect on the region’s political and economic growth. Authors have utilized time-series data representing Basque stock market indexes and regression model estimation suggested that terroristic violence lowers financial market performance in the country substantially. Aksoy and Demiralay (Citation2019) examined whether Turkish equity markets and international shareholders responded to Turkey’s terrorist incidents and analyzed the intensity of their response against multiple categories of terroristic attacks. Findings showed that the terrorist attacks have not impacted stock returns, abnormal returns, and the accumulated abnormal returns, but international investors’ sentiments regarding the Turkish stock market have been severely impacted.

3. Data

In this research article, we have incorporated MS,Footnote1 CPIFootnote2, and IRFootnote3 in order to estimate long run association between macroeconomic fluctuations and KSE-100 indexes utilizing time series data from 2002 to 2015. Monthly level data regarding particular macroeconomic factors have been collected from the Pakistan Bureau of statistics and monthly data on stock indexes has been collected from the Pakistan stock exchange web portal. The period is divided into three portions. The first portion is represented as the precrisis period comprising of 84 months from January 2002 to December 2008. The postcrisis period is comprised of 84 months from January 2009 to December 2015 and the third period is represented as a whole sample period in which we have included the whole sample without dividing the time series in pre- and postcrisis. Data on multiple categories of terroristic attacks are collected from daily timelines at the South Asian terrorism portal administered by the institute of conflict management. Each daily timeline representing multiple categories of terroristic attacks such as Bomb blasts, Army person killed, civilians killed, and terrorists killed has been scanned and transformed into monthly data from January 2002 to December 2015. To the best of our knowledge, this is the first research article that has examined the role of the global economic crisis in effecting symmetrical association between macroeconomic volatility and Karachi stock exchange indexes in presence of terroristic disruptions.

3.1. Choice of sample period

Dividing the sample period into different types of regimes (pre-economic recessionary period, post recessionary period and over the whole duration) will enable us to examine whether the investor’s reaction to macroeconomic variations remains the same during three different types of regimes. If investors react differently to macroeconomic variations during the precrisis regime in contrast with the postcrisis regime, this means that consideration of regime is more important while investigating the symmetrical linkages between macroeconomic fundamentals and stock indexes. In the existing literature, researchers have taken into account the whole sample period while exploring symmetrical linkages between variables, this research adds to the literature by finding out that the symmetrical association between macroeconomic fluctuations and stock indexes is actually regime dependent, and investors reacted differently in different regimes. Our choice of sample period is in line with (Anisak & Mohamad, Citation2019; Pandey & Vipul, Citation2018; Sheikh et al., Citation2020; You et al., Citation2017)

4. Research methodology

In the existing literature, some of the research articles examined asymmetrical and symmetrical linkages between macroeconomic variation and stock indexed in a developed country’s context (Charfeddine & Barkat, Citation2020; Kocaarslan & Soytas, Citation2019; Salvatore, Citation2019). One limitation of the NARDL model by (Shin et al., Citation2014) is that it cannot be applied on linear data and can only be implemented on time series data exhibiting non-linear trends by disintegrating regressors into positive and negative signs. We have utilized the BDS test of nonlinearity to determine that either the correct method of estimation is Linear ARDL by (Pesaran et al., Citation2001) or the Non-linear ARDL model by (Shin et al., Citation2013) for estimating cointegration between macroeconomic fluctuation and stock indexes. Furthermore, we have also divided time series into three different types of regimes such as the pre-economic recessionary period, posteconomic recessionary period, and over the entire sample duration. BDS test also helps to ascertain that whether time series data is identically distributed or not and in case of rejection of the null hypothesis, it is inferred that the nonlinear ARDL model is more appropriate than the standard Linear ARDL model.

4.1. BDS test of nonlinearity

BDS test can formulated as

=

is well-defined as standard deviation of

.

4.2. ADF, PP, Zivot Andrew unit root testing

After estimation of linearity in time series data, or if results from BDS test cannot be able to reject the null hypothesis, particularly in that case most appropriate model for estimating long run and short run cointegrating association is linear ARDL model. However, estimation of linear ARDL model is still dependent upon integration of variables either at different levels, e.g., I (0) and I (1) or at same level such as there is seasonality effect at level and no seasonality effect after differencing the variables first time I (1) but none of variables should become stationary at second differencing or differencing two times I (2). We have incorporated four different type of unit root test like augmented dickey fuller (ADF), Philips-Peron (PP) unit root, Kwiatkowski Philips Schmidt shin KPSS unit root and Zivot Andrew (ZA) unit root for identification of seasonality along with structural breaks in the data.

4.3. Error correction term ECT (−1) and ARDL model

Mathematical form of error correction model (ECM) and ARDL is given below,

In Equationequation 1(1)

(1) ,

is denoted as dependent variable and is represented by KSE-100 indexes of Karachi stock exchange in Pakistan. Independent variables inserted in Equationequation 1

(1)

(1) with their difference operators

are used to find out the short run effect and independent variables without difference operators are employed to estimate long run effect on stock indexes. In other words,

and

are short run coefficient,

and

are long run coefficient.

and

are represented as intercept and error term respectively in model. ARDL model is used to find out the symmetrical effect of macroeconomic variability on stock indexes in presence of certain terroristic disruptions. Long run cointegrating relationship is established if value of F statistic is greater than upper and lower bound critical values. ARDL model can only be applied in case of mixed integration of variables or integration at same order. If value of F statistics falls in between lower and upper bound critical values, then error correction term is alternative procedure to find out that whether model is getting back toward long run equilibrium at particular speed of adjustment (Abdul, Citation2019; Shakil et al., Citation2018). If value of F statistics is lower than upper bound or lower bound critical values, then there exit no cointegration (

=

= 0). ARDL model is shown below,

is log of stock indexes with its difference operator and is included as dependent variable. All independent variables with difference operators are included in equation in order to estimate short effect on stock indexes and independent variables without difference operators e.g.,

+

+

are included to estimate long run effect on dependent variable. In concise words,

and

are short run coefficient, whereas

and

are long run coefficient. Wald test statistics is also utilized in order to formulate joint significant effect in short run e.g., c (1) + c(2) + c(3) + c(4) + c(5) + c(6) ≠0 and in long run (

) on stock indexes.

5. Results

We have divided the results section into four subsections. First section is about the descriptive statistics and data normality. In second portion, it is concluded that the symmetrical ARDL model is more appropriate as compared to the nonlinear ARDL model because the null hypothesis of BDS test statistics cannot be rejected and the time series is linear in nature as is shown in figure no 1. Third portion is about the estimation of seasonality effect and results confirmed that none of the variables is I (2). ARDL model is estimated in the fourth portion .

Tables , , and 4 explains the descriptive statistics of macroeconomic fluctuations and stock indexes in three different regimes such as postcrisis regime, precrisis regime, and over the entire sample. While comparing descriptive statistics of the precrisis period with postcrisis, it can be seen that the maximum values of both inflation and MS are greater as compared to the precrisis crisis period. This means that MS and inflation increases after the global financial crisis however, maximum values of interest rate remain the same. Table explains that the volatility of MS and CPI is greater as compared to the volatility of interest rates in the precrisis regime. However, the standard deviation of both variables, e.g., inflation and money supply is comparatively lower during the pre-economic recession period than the standard deviation in the posteconomic recession period. Another interesting aspect is that the maximum values of the Karachi stock index appreciated in the postcrisis period as compared to the precrisis period. Volatility in KSE-100 indexes is also greater in the posteconomic recession period as compared to the pre-economic recession of 2008 and over the entire sample duration. This means that the maximum, minimum, and standard deviation of the KSE-100 indexes didn’t display a uniform trend of appreciation or depreciation and these values continue to fluctuate under distinct regimes.

Table 1. Variables of interest

Table 2. Descriptive statistics of whole sample period

Table 3. Descriptive statistics of postcrisis period

Table 4. Descriptive statistics of precrisis period

We have also incorporated multiple terroristic attacks such as the number of bomb blasts, army person fatalities, and terroristic killed as control variables and descriptive statistics of terroristic disruptions under three different regimes exhibit that intensity of terroristic disruption is greater during post economic recession period as compared to before recessionary period. The maximum number of the bomb blast, terroristic killed, and army person fatalities in the postcrisis period were 6,157 and 1590 respectively in contrast with 3 bomb blast, 143 army person killed and 341 terrorists killed in the precrisis period. However, the Karachi stock exchange has reached its maximum value of 29984 indexes as compared to 14,321 in the precrisis period. This means that KSE-100 indexes have been continuously increasing under the number of terroristic disruptions in the postcrisis period. This furthermore motivates the researchers to explore the symmetrical effect of macroeconomic fluctuation on stock indexes in presence of terroristic disruptions for shorter and longer horizons and under three different types of regimes. BDS test statistics in table .4 explains that the ARDL model is more appropriate as compared to NARDL because of linearity in data and time series is identically distributed.

Table , 8 to reports the results of different types of unit root tests such as augmented dickey fuller, Philips Peron unit root, Zivot Andrew (ZA) unit root, and KPSS. The null hypothesis in the case of ADF and PP states that data is having a unit root or nonstationary. However null hypothesis in the case of the KPSS test is rejected if KPSS test statistics are greater than critical values and rejection of the null hypothesis indicates that time series data is not free from nonstationarity or seasonality effect. We have also undertaken the Zivot Andrew unit root test to find out the seasonality effect in time-series data along with structural breaks. Because of the presence of a structural break in time series, we included a dummy variable to deal with a structural break in time-series data following the methodology of (Tehreem, Citation2018).

Table 5. BDS test of nonlinearity

Table 6. Augmented Dickey fuller test

Unit root tests represented by table 6-9 indicates that none of variables is integrated at second differencing I (2). PP, KPSS, Zivot Andrew, and ADF unit root test indicates that all variables are integrated at same order. They are seasonality effects in time series data of certain variables including stock indexes, interest rates and terroristic disruption at level but after first differencing, these variables become stationary and free from seasonality effect. However, none of variable remain nonstationary after differencing 1 time. Unit root tests along with BDS test of nonlinearity confirm the suitability of linear autoregressive distributive lag model (LARDL) for estimation of short run and long run cointegration between macroeconomic fluctuation and stock indexes in presence of terroristic disruptions and during global financial crisis. Tables –12 present the results of ARDL model during pre-recessionary period, post-recessionary period, and over the entire sample duration.

Table 7. PP unit root test

Table 8. KPSS unit root test

Table 9. Zivot Andrew unit root test

Table 10. ARDL model before crisis

In the long run and before the international recessionary regime, there is a direct and significant association between CPI, and stock indexes but IR and MS formulated an inverse association with stock indexes (see Table ). Findings indicated that in the long run, investors reacted positively to a positive increase in CPI but reacted negatively to an increase in MS and IR. However, in the short run, IR and MS formulate a negative relationship with the increase in stock indexes. This means that in the long run and before the 2008 recessionary period, investors reacted positively to an increase in CPI but for the shorter-horizons, investors reacted negatively to an increase in interest rates. The negative influence of money supply on stock indexes is inconsistent with findings of (Chiang Leong & Hui, Citation2014; Shrestha & Liu, Citation2008), and the positive influence of CPI on KSE-100 indexes in both the shorter and long horizons is inconsistent with the finding of (Adjasi, Citation2009; Adjasi et al., Citation2011). Residual diagnostic tests such as Ramsey reset test for model miss-specification, Breusch pagan test for heteroskedasticity and the LM test for autocorrelation elucidates that model is free from these problems. ECM value of −0.87 means that model is getting back toward long-run equilibrium at a speed of 87% and there exist long-run symmetrical relationships between macroeconomic volatility, terroristic disruptions, and KSE-100 indexes.

Table is divided into two portions such as the long-term and short-term results of the linear impact of macroeconomic fluctuation on KSE-100 indexes in presence of terroristic disruptions. According to the results of the ARDL model estimated for the postcrisis regime, the MS has a direct effect on stock indexes and IR has an inverse significant effect. However, in the short-run and after the international economic crunch, shareholders reacted positively to the money supply only and didn’t react to fluctuations in IR and CPI. This means that the international economic crunch has affected the symmetrical cointegrating association between macroeconomic fluctuation and KSE-100 indexes.

Table 11. ARDL after crisis

Table furthermore reports that the number of bomb blast are having a positive and significant association with KSE-100 indexes only in the long run and shareholders didn’t react to terroristic disruptions such as bomb blasts, security persons killed, and terroristic killed in the short run. One justification for the positive effect of a bomb blast on stock indexes is that investors mainly consider microfirm level financial variables as important determinants of stock indexes (Sheikh et al., Citation2018) and didn’t react negatively to exogenous shocks such as terroristic disruptions. Moreover, such terroristic disruption may not have a negative influence on the profitability of firms (Laborda & Olmo, Citation2019; Liu & Pratt, Citation2017), therefore shareholders recognize this fact and react rationally to exogenous negative environmental turbulence. This makes Pakistan stock exchange resilience against several negative disruptions.

The difference in results regarding the impact of macroeconomic fluctuation on KSE-100 indexes before a crisis and macroeconomic effect on stock indexes after crisis edifies that investors, governmental agencies and regulators, academicians, researchers, policymakers should always consider regime before investing in the stock exchange and making an investment without consideration of regime will lead towards spurious results. Our research article substantially adds to the literature by finding out the macroeconomic effect on stock indexes in presence of terroristic disruption and the role of the international financial crunch in effecting the symmetrical association between macroeconomic volatility and KSE-100 indexes. In existing literature authors have not taken into account multiple terroristic disruptions as a control measure and the role of the international economic recession in changing the stock-macroeconomic relation (Chandra, Citation2012; Joëts et al., Citation2017; Kan, Citation2017; Singhania & Prakash, Citation2014; Spilioti, Citation2016; Umar & Sun, Citation2015).

Table reports that only consumer price index has a long run symmetrical relationship with stock indexes for entire sample period, but in the short-run, a decrease in the interest rate causes appreciation in stock indexes. Findings also suggested that terroristic disruptions such as bomb blast and security persons killed impact positively on KSE-100 indexes in the short run and bomb blast are having a positive effect on stock indexes in the long run. In the existing literature, some researchers have found a positive impact of terroristic activities on stock market integration (R. Kumar & Dhankar, Citation2017) because these terroristic attacks can’t be able to adversely influence the investor’s sentiments. Another possibility of this positive reaction of terroristic disruptions on stock indexes is that terroristic disruption in form of environmental turbulence can’t be able to negatively impact a firm’s profitability and microlevel firm variables, therefore investors react rationally and didn’t react negatively. However, the magnitude of the impact of multiple environmental turbulences such as terroristic disruptions on stock indexes is very lower and is significant at 10% level only.

Table 12. ARDL model when whole sample is selected

5.1. Role of global financial crisis in effecting symmetrical relationship between money supply (M2), interest rates (IR), and consumer price index (CPI)

5.1.1. Money supply (MS)

In the long run and before global economic recession period, CPI is having a significant direct relationship with stock indexes but a negative relationship is formulated between MS, IR and stock indexes. This means that investors reacted positively to CPI fluctuation and reacted negatively to fluctuations in IR and MS. In the short run and before the recessionary period, the relationship between MS and stock indexes remains negative and significant. In the short run and long run, investors reacted negatively to positive fluctuations in MS during the precrisis regime. However, after the recessionary period, investors reacted positively to positive fluctuations in the money supply. This means that during the post-recessionary period, 1% increase in money supply causes 0.398% and 0.52% appreciative impact on stock indexes for shorter and longer horizons respectively. In contrast with the results of the postcrisis regime, e.g., 1% appreciation in MS causes 0.54% and 0.12% depreciation in stock indexes respectively during pre-economic recessionary regime for longer and shorter period. In the case of a developing country’s context, the international economic crisis of 2008 has effected nature of the relationship between MS and stock indexes, as association between MS and stock indexes is directly proportional during the postcrisis regime, but money supply has formulated an inverse relationship with stock indexes during pre-economic crunch regime.

These results are inconsistent with (Camilleri et al., Citation2019; Ho, Citation2018; Joëts et al., Citation2017; Kocaarslan & Soytas, Citation2019; Narayan et al., Citation2018; Rexford, Citation2019; Simbolon & Purwanto, Citation2018) because these studies have not considered the role of global financial crisis in effecting the symmetrical nature of relationship between money supply and stock indexes.

5.1.2. Consumer price index (CPI) and interest rate (IR)

Before international economic recession, investors reacted positively to positive fluctuations in CPI in long run but reacted negatively to positive fluctuations in MS and interest rate in short run. However, after economic recessionary period, relationship between MS and KSE-100 indexes is directly proportion and relationship between interest rate and stock indexes is inversely proportional in long run. This means that global financial crisis has effected nature of relationship between money supply, interest rate, CPI and stock index. In long run and before crisis, consumer price index is directly proportional to stock index but after crisis investors didn’t react to fluctuations in inflation. Investors should consider the regime before investing in stock indexes and academicians should consider precrisis and postcrisis regime before establishing relationship between fluctuations in macro economy and KSE-100 indexes. Our findings are inconsistent with (Camilleri et al., Citation2019; Jehan & Rashid, Citation2014; Mazuruse, Citation2014; Rexford, Citation2019) because these studies have not deliberately studied the role of global financial crisis in effecting symmetrical association between variations in macro economy and stock indexes. Interestingly, money supply remain statistically insignificant over the entire sample duration, and value of F statistics of ARDL model estimated for whole sample period is also lower as compared to pre-economic crisis and postcrisis regime’s ARDL model.

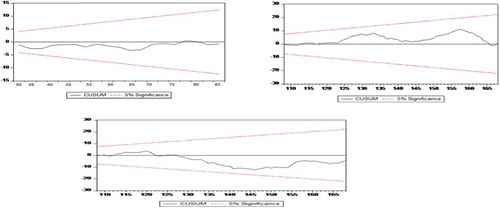

Figure 2. ARDL models estimated for three different type of regimes are stable

Table presents the summarized form of results after estimating ARDL model for precrisis and postcrisis regimes. (a–c) indicates that ARDL models estimated for three different type of regimes are stable.

Table 13. Effect of regimes on macroeconomic-stock price nexus

6. Conclusions and practical implications

In this research article, we have incorporated certain macroeconomic factors such as MS, CPI, and IR to establish a long-run cointegration between macroeconomic variations and KSE-100 indexes utilizing time-series data from 2002 to 2015. Monthly level data regarding particular macroeconomic factors have been collected from the Pakistan Bureau of statistics and monthly data on stock indexes has been collected from the Pakistan stock exchange web portal. The period is divided into three portions to get the representation of three regimes. The first portion is represented as a precrisis period comprising of 84 months from January 2002 to December 2008. The postcrisis period is comprised of 84 months from January 2009 to December 2015 and the third period is represented as a whole sample period in which we have included the whole sample without dividing the time series. Data on multiple categories of terroristic attacks are collected from daily timelines from the South Asian terrorism portal representing terroristic attacks in South Asian regions. Each daily timeline representing multiple categories of terroristic attacks such as Bomb blasts, Army person killed, civilians killed and terrorists killed has been scanned and transformed into monthly data from January 2002 to December 2015. To the best of our knowledge, this is the first research article that examined the role of the 2008 international economic depression in effecting the symmetrical associationship between macroeconomic variability and KSE-100 indexes in presence of terroristic disruptions.

In the long run and before the international economic recession, there is a direct significant association between CPI and stock indexes but money supply and IR formulated an inverse relationship with stock indexes. Findings suggested that in the long run, investors reacted positively to a positive increase in CPI but reacted negatively to an increase in the MS and IR. However, in the short run, IR and MS are inversely proportionate to increase in KSE-100 indexes. This means that in the long run and before the economic depression of 2008, investors reacted positively to an increase in CPI, but investors reacted negatively to an increase in interest rates for shorter horizons. According to the results of the ARDL model estimated for the postcrisis regime, the money supply has a positive effect on stock indexes and IR has a negative significant effect. However, in the short run and after the international economic recession, investors reacted positively to the money supply only and didn’t react to fluctuations in IR and CPI. This means that the global economic depression of 2008 has affected the symmetrical cointegration between fluctuations in macroeconomy and KSE-100 indexes.

6.1. Practical implications

This research article purposes interesting practical implications for short-term and long-term investors. Investors should always consider tail events like global financial crisis before investing in Pakistan stock exchange because taking financial decision without considering regime may lead toward disastrous results. Investors reacted differently to macroeconomic fluctuations before crisis and after crisis, this means that global economic recession of 2008 has changed the nature of symmetrical association between macroeconomic volatility and KSE-100 indexes. This article also poses practical implications for academicians and researcher to consider the regime before establishing relationship between macroeconomic volatility and stock prices. International economic recession has not only distressed stock exchange of Pakistan in 2008 but world’s most premier institutions have also been effected by crisis. Therefore, establishing relationship between CPI-MS-IR variability and stock indexes without considering pre-economic recessionary period and post economic recession regime may lead toward spurious results. Conclusion from this research article also poses important question for future research that whether the association between variations in macro economy and stock indexes remain same before COVID-19 and after COVID-19.

6.1.1. Practical implication for policy makers and Central Bank of Pakistan

This research article also poses important practical relevance for policymakers and the central bank of Pakistan. The State Bank of Pakistan should also consider the regime before changing policy rates, as an increase in interest rate and flow of capital before crisis adversely impacted KSE-100 indexes because of the increase in the cost of borrowing and possibility that flow of capital may increase the inflation. An increase in the cost of borrowing not only makes it difficult to initiate new businesses for small local investors but also limits business diversification opportunities for larger organizations. It is proved that such practices before economic crisis regime have negatively affected stock indexes. However, before the crisis regime, an increase in the cost of borrowing and capital flow not only depreciates the stock indexes for shorter horizons, but also the long-run impact of an increase in both the fundamental variables has an adverse influence on stock indexes. This may be because of increase in the cost of borrowing not only adversely impact the short-run investors, so they keep on selling their shares on reduced prices because of increasing interest rates on their borrowings but also an increase in the cost of borrowing impact long-term investors. However, after the crisis regime, appreciation in flow of capital positively affected the increase in overall values of stock indexes. This shows that consideration of regime is very important for making policy rate adjustments rather than considering the whole period.

Interestingly, before the global financial crisis and for both shorter and longer horizons, the MS has formulated a negative association with stock indexes. However, for shorter and longer horizons and during the postcrisis regime, MS has a direct impact on stock indexes. This research article also poses important practical relevance for the Central Bank of Pakistan to consider the regime before making adjustments toward increasing or decreasing the flow of capital and policy rates within the economy. An increase in money supply is more favorable after the crisis rather than before the crisis regime for short-term and long-term investors of KSE-100 indexes.

Additional information

Funding

Notes on contributors

Umaid A. Sheikh

Umaid A Sheikh has completed several academic degrees including BBA-Hons and Master of Business Administration from Comsats University, Islamabad. He has also completed his M.Phil. in Accounting and Finance with A grade in thesis and 87% overall aggregate average. His research works appear in other scientific journals indexed by Scopus, WOS, and ABDC.

Dr. Muzaffar Asad is working as an Assistant Professor at the University of Bahrain, College of Business Administration. He completes his Ph.D. in Entrepreneurial Finance and has supervised several research projects in the field of entrepreneurship, finance, and business management

Dr. Aqeel serves as an Assistant Professor at NUST business school in Islamabad

Dr. Zahid Ahmed is serving as an Associate professor at the University of Central Punjab. He is having a Ph.D. degree in statistics

Dr. Mosab is acting as Director of the MBA program at AL-Ain University of Science and Technology

Notes

1. “Money supply = MS”

2. “Consumer price index = CPI”

3. “Interest rate = IR”

References

- Abbas, G., McMillan, D. G., & Wang, S. (2017). Conditional volatility nexus between stock markets and macroeconomic variables: Empirical evidence of G-7 countries. Journal of Economic Studies, 45(1), 77–24. https://doi.org/10.1108/JES-03-2017-0062

- Abdul, R. (2019). The nexus of electricity access, population growth, economic growth in Pakistan and projection through 2040: An ARDL to co-integration approach. International Journal of Energy Sector Management, 13(3), 747–763. https://doi.org/10.1108/IJESM-04-2018-0009

- Abdullah, O. A. H. (2018). Identification of macroeconomic determinants for diversification and investment strategy for Islamic unit trust funds in Malaysia. International Journal of Emerging Markets, 13(4), 653–675. https://doi.org/10.1108/IJoEM-03-2017-0074

- Adjasi, C. K. D. (2009). Macroeconomic uncertainty and conditional stock‐price volatility in frontier African markets: Evidence from Ghana. The Journal of Risk Finance, 10(4), 333–349. https://doi.org/10.1108/15265940910980641

- Adjasi, C. K. D., Biekpe, N. B., & Osei, K. A. (2011). Stock prices and exchange rate dynamics in selected African countries: A bivariate analysis. African Journal of Economic and Management Studies, 2(2), 143–164. https://doi.org/10.1108/20400701111165623

- Agyire‐Tettey, K. F., & Kyereboah‐Coleman, A. (2008). Impact of macroeconomic indicators on stock market performance: The case of the Ghana Stock Exchange. The Journal of Risk Finance, 9(4), 365–378. https://doi.org/10.1108/15265940810895025

- Ajaz, T., Nain, M. Z., Kamaiah, B., & Sharma, N. K. (2017). Stock prices, exchange rate and interest rate: Evidence beyond symmetry. Journal of Financial Economic Policy, 9(1), 2–19. https://doi.org/10.1108/JFEP-01-2016-0007

- Aksoy, M., & Demiralay, S. (2019). The effects of terrorism on Turkish financial markets. Defence and Peace Economics, 30(6), 733–755. https://doi.org/10.1080/10242694.2017.1408737

- Ali, C. A. (2019). Energy consumption and agricultural economic growth in Pakistan: Is there a nexus? International Journal of Energy Sector Management, 13(3), 597–609. https://doi.org/10.1108/IJESM-08-2018-0009

- Alkhuzaie, A. S., & Asad, M. (2018). Operating cashflow, corporate governance, and sustainable dividend payout. International Journal of Entrepreneurship, 22(4), 1–9.

- Almansour, A. Z., Asad, M., & Shahzad, I. (2016). Analysis of corporate governance compliance and its impact over return on assets of listed companies in Malaysia. Science International, 28(3), 2935–2938.

- Al‐Najjar, B., & Taylor, P. (2008). The relationship between capital structure and ownership structure: New evidence from Jordanian panel data. Managerial Finance, 34(12), 919–933. https://doi.org/10.1108/03074350810915851

- Andriansyah, A., & Messinis, G. (2019). Stock prices, exchange rates and portfolio equity flows: A Toda-Yamamoto panel causality test. Journal of Economic Studies, 46(2), 399–421. https://doi.org/10.1108/JES-12-2017-0361

- Anisak, N., & Mohamad, A. (2019). Foreign Exchange Exposure of Indonesian Listed Firms. Global Business Review, 0972150919843371. https://doi.org/10.1177/0972150919843371

- Asad, M., & Farooq, A. (2009). Factors influencing KSE 100 index/share prices. Pardigms A Journal of Commerce, Economics, and Social Sciences, 3(1), 34–51. https://doi.org/10.24312/paradigms030102

- Asad, M., & Qadeer, H. (2014). Components of working capital and profitability: A case of fuel and energy sector of Pakistan. Pardigms A Journal of Commerce, Economics, and Social Sciences, 8(1), 50–64. https://doi.org/10.24312/paradigms08010

- Aslam, F., & Kang, H.-G. (2015). How different terrorist attacks affect stock markets. Defence and Peace Economics, 26(6), 634–648. https://doi.org/10.1080/10242694.2013.832555

- Bano, S., Zhao, Y., Ahmad, A., Wang, S., & Liu, Y. (2019). Why did FDI inflows of pakistan decline? From the perspective of terrorism, energy shortage, financial instability, and political instability. Emerging Markets Finance and Trade, 55(1), 90–104. https://doi.org/10.1080/1540496X.2018.1504207

- Barberis, N., Shleifer, A., Vishny, R. (1998). A model of investor sentiment, Journal of Financial Economics. Journal of Financial Economics, 9, 307–343. doi:10.1016/S0304-405X(98)00027-0

- Barros, C. P., Caporale, G. M., & Gil‐Alana, L. A. (2009). Basque terrorism: Police action, political measures and the influence of violence on the stock market in the basque country. Defence and Peace Economics, 20(4), 287–301. https://doi.org/10.1080/10242690701750676

- Barros, C. P., & Gil-Alana, L. A. (2009). Stock market returns and terrorist violence: Evidence from the Basque Country. Applied Economics Letters, 16(15), 1575–1579. https://doi.org/10.1080/13504850701578918

- Camilleri, S. J., Scicluna, N., & Bai, Y. (2019). Do stock markets lead or lag macroeconomic variables? Evidence from select European countries. The North American Journal of Economics and Finance, 48(1), 170–186. https://doi.org/org/10.1016/j.najef.2019.01.019

- Chandra, A. (2012). Cause and effect between FII trading behaviour and stock market returns: The Indian experience. Journal of Indian Business Research, 4(4), 286–300. https://doi.org/10.1108/17554191211274794

- Charfeddine, L., & Barkat, K. (2020). Short- and long-run asymmetric effect of oil prices and oil and gas revenues on the real GDP and economic diversification in oil-dependent economy. Energy Economics, 86(1), 104680. https://doi.org/org/10.1016/j.eneco.2020.104680

- Chiang Leong, C., & Hui, T.-K. (2014). Macroeconomic and non-macroeconomic variables linking to Singapore hotel stock returns. In Advances in hospitality and leisure (Vol. 10, pp. 2–21). Emerald Group Publishing Limited. https://doi.org/org/doi:10.1108/S1745-354220140000010000

- Christofi, A. C., Christofi, P. C., & Philippatos, G. C.. (1993). An application of the arbitrage pricing theory using canonical correlation analysis. Managerial Finance, 19(3/4), 68–85.

- Corredor, P., Ferrer, E., & Santamaria, R. (2015). The impact of investor sentiment on stock returns in emerging markets: The case of central european markets. Eastern European Economics, 53(4), 328–355. https://doi.org/10.1080/00128775.2015.1079139

- Fatima, A., Rashid, A., & Khan, A.-Z. (2018). Asymmetric impact of shocks on Islamic stock indices: A cross country analysis. Journal of Islamic Marketing, 10(1), 2–86. https://doi.org/10.1108/JIMA-04-2017-0043

- Floros, C., & Vougas, D. V. (2008). The efficiency of Greek stock index futures market. Managerial Finance, 34(7), 498–519. https://doi.org/10.1108/03074350810874451

- Ghulam, A. (2018). Conditional volatility nexus between stock markets and macroeconomic variables. Journal of Economic Studies, 45(1), 77–99. https://doi.org/10.1108/JES-03-2017-0062

- Gregoriou, A., Healy, J., & Gupta, J. (2015). Determinants of telecommunication stock prices. Journal of Economic Studies, 42(4), 534–548. https://doi.org/10.1108/JES-06-2013-0080

- Günsel, N., Türsoy, T., & Rjoub, H. (2009). The effects of macroeconomic factors on stock returns: Istanbul Stock Market. Studies in Economics and Finance, 26(1), 36–45. https://doi.org/10.1108/10867370910946315

- Ho, S.-Y. (2018). Macroeconomic determinants of stock market development in South Africa. International Journal of Emerging Markets, 14(2), 322–342. https://doi.org/10.1108/IJoEM-09-2017-0341

- Hussain, S. S. J., Josef, S. P., Ravinesh, K. R., & Tanveer, A. (2017). The impact of terrorism on industry returns and systematic risk in Pakistan: A wavelet approach. Accounting Research Journal, 30(4), 413–429. https://doi.org/10.1108/ARJ-09-2015-0114

- Jehan, Z., & Rashid, A. (2014). The response of macroeconomic aggregates to monetary policy shocks in Pakistan. Journal of Financial Economic Policy, 6(4), 314–330. https://doi.org/10.1108/JFEP-04-2013-0016

- Joëts, M., Mignon, V., & Razafindrabe, T. (2017). Does the volatility of commodity prices reflect macroeconomic uncertainty? Energy Economics, 68, 313–326. https://doi.org/org/10.1016/j.eneco.2017.09.017

- Jung, Y. C., Das, A., & McFarlane, A. (2020). The asymmetric relationship between the oil price and the US-Canada exchange rate. The Quarterly Review of Economics and Finance, 76(1), 198–206. https://doi.org/org/10.1016/j.qref.2019.06.003

- Kan, Y. Y. (2017). Macroeconomic environment of bull markets in Malaysia. Qualitative Research in Financial Markets, 9(1), 72–96. https://doi.org/10.1108/QRFM-05-2016-0015

- Kocaarslan, B., & Soytas, U. (2019). Asymmetric pass-through between oil prices and the stock prices of clean energy firms: New evidence from a nonlinear analysis. Energy Reports, 5(1), 117–125. https://doi.org/10.1016/j.egyr.2019.01.002

- Kumar, R., & Dhankar, R. S. (2017). Financial instability, integration and volatility of emerging South Asian stock markets. South Asian Journal of Business Studies, 6(2), 177–190. https://doi.org/10.1108/SAJBS-07-2016-0059

- Kumar, S. (2019). Asymmetric impact of oil prices on exchange rate and stock prices. The Quarterly Review of Economics and Finance, 72(1), 41–51. https://doi.org/org/10.1016/j.qref.2018.12.009

- Laborda, R., & Olmo, J. (2019). An empirical analysis of terrorism and stock market spillovers: The case of Spain. Defence and Peace Economics, 1–19. https://doi.org/10.1080/10242694.2019.1617601

- Laila, M., & Guruprasad, S. (2019). Impact of terrorism on stock markets across the world and stock returns: An event study of Taj attack in India. Journal of Financial Crime, 26(3), 793–807. https://doi.org/10.1108/JFC-09-2018-0093

- Laopodis, N. T. (2008). Real investment and stock prices in the USA. Managerial Finance, 35(1), 78–100. https://doi.org/10.1108/03074350910922609

- Liang, C. C., Troy, C., & Rouyer, E. (2020). U.S. uncertainty and Asian stock prices: Evidence from the asymmetric NARDL model. The North American Journal of Economics and Finance, 51(1), 101046. https://doi.org/org/10.1016/j.najef.2019.101046

- Liu, A., & Pratt, S. (2017). Tourism’s vulnerability and resilience to terrorism. Tourism Management, 60(1), 404–417. https://doi.org/org/10.1016/j.tourman.2017.01.001

- Mathur, S. K., & Shekhawat, A.. (2018). Exchange rate nonlinearities in India’s exports to the USA. In S. Abhishek Ed., Studies in economics and finance: Vol. ahead-of-print. (Issue ahead-of-print). https://doi.org/10.1108/SEF-07-2015-0179

- Mazuruse, P. (2014). Canonical correlation analysis: Macroeconomic variables versus stock returns. Journal of Financial Economic Policy, 6(2), 179–196. https://doi.org/10.1108/JFEP-09-2013-0047

- MengYun, W., Imran, M., Zakaria, M., Linrong, Z., Farooq, M. U., & Muhammad, S. K. (2018). Impact of terrorism and political instability on equity premium: Evidence from Pakistan. Physica A: Statistical Mechanics and Its Applications, 492(2), 1753–1762. https://doi.org/org/10.1016/j.physa.2017.11.095

- Mollick, A., & Nguyen, K. H. (2015). U.S. oil company stock returns and currency fluctuations. Managerial Finance, 41(9), 974–994. https://doi.org/10.1108/MF-02-2014-0029

- Mouna, A. (2019). Transmission of shocks between Chinese financial market and oil market. In B.-A. Mouna Ed., International journal of emerging markets: Vol. ahead-of-p. (Issue ahead-of-print). https://doi.org/10.1108/IJOEM-07-2017-0244

- Narayan, S., Le, T.-H., & Sriananthakumar, S. (2018). The influence of terrorism risk on stock market integration: Evidence from eight OECD countries. International Review of Financial Analysis, 58(2), 247–259. https://doi.org/org/10.1016/j.irfa.2018.03.011

- Nguyen, T., & Ngo, C. (2014). Impacts of the US macroeconomic news on Asian stock markets. The Journal of Risk Finance, 15(2), 149–179. https://doi.org/10.1108/JRF-09-2013-0064

- Othman, A. H. A., Alhabshi, S. M., & Haron, R. (2019). The effect of symmetric and asymmetric information on volatility structure of crypto-currency markets: A case study of bitcoin currency. Journal of Financial Economic Policy, 11(3), 432–450. https://doi.org/10.1108/JFEP-10-2018-0147

- Pandey, V., & Vipul. (2018). Volatility spillover from crude oil and gold to BRICS equity markets. Journal of Economic Studies, 45(2), 426–440. https://doi.org/10.1108/JES-01-2017-0025

- Peiró, A. (2016). Stock prices and macroeconomic factors: Some European evidence. International Review of Economics & Finance, 41(Suppl.C), 287–294. https://doi.org/org/10.1016/j.iref.2015.08.004

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289–326. https://doi.org/10.1002/jae.616 3 doi:10.1002/(ISSN)1099-1255

- Rajesh, S. (2019). Dynamism between selected macroeconomic determinants and electricity consumption in India. International Journal of Social Economics, 46(6), 805–821. https://doi.org/10.1108/IJSE-11-2018-0586

- Reid, M., & Gupta, R. (2013). Macroeconomic surprises and stock returns in South Africa. Studies in Economics and Finance, 30(3), 266–282. https://doi.org/10.1108/SEF-Apr-2012-0049

- Rexford, A. (2019). Corporate performance volatility and adverse macroeconomic conditions. Journal of Financial Economic Policy: Vol. Ahead-of-p. (Issue ahead-of-print). https://doi.org/10.1108/JFEP-11-2018-0158

- Salvatore, C. (2019). The long-run interrelationship between exchange rate and interest rate: The case of Mexico. Journal of Economic Studies, 46(7), 1380–1397. https://doi.org/10.1108/JES-04-2019-0176

- Saumya, R. D. (2012). Investor sentiment, risk factors and stock return: Evidence from Indian non‐financial companies. Journal of Indian Business Research, 4(3), 194–218. https://doi.org/10.1108/17554191211252699

- Shahbaz, M. (2013). Linkages between inflation, economic growth and terrorism in Pakistan. Economic Modelling, 32(1), 496–506. https://doi.org/org/10.1016/j.econmod.2013.02.014

- Shaikh, I. (2019). The impact of terrorism on Indian securities market. Economic Research-Ekonomska Istraživanja, 32(1), 1744–1764. https://doi.org/10.1080/1331677X.2019.1638284

- Shaker, R. Z., Asad, M., & Zulfiqar, N. (2018). Do predictive power of fibonacci retracements help the investor to predict future? A study of Pakistan Stock Exchange. International Journal of Economics and Financial Research, 4(6), 159–164.

- Shakil, M. H., Mustapha, I. M., Tasnia, M., & Saiti, B. (2018). Is gold a hedge or a safe haven? An application of ARDL approach. Journal of Economics, Finance and Administrative Science, 23(44), 60–76. https://doi.org/10.1108/JEFAS-03-2017-0052

- Sheikh, U. A., Asad, M., Ahmed, Z., & Mukhtar, U. (2020). Asymmetrical relationship between oil prices, gold prices, exchange rate, and stock prices during global financial crisis 2008: Evidence from Pakistan. Cogent Economics and Finance, 8(1), 1. https://doi.org/10.1080/23322039.2020.1757802

- Sheikh, U. A., Asad, M., & Mukhtar, U. (2020). Modelling Asymmetric effect of Foreign direct investment inflows (FDI), Carbon emission (CC2) and Economic growth(EG) on energy consumption(CE) of South Asian region: A symmetrical and asymmetrical panel autoregressive distributive lag model approach. Accountancy Business and the Public Interest, 193–221. http://visar.csustan.edu/aaba/SheikhAsadMukhtar2020.pdf

- Sheikh, U. A., Chaudhry, H., & Mukhtar, U. (2018). Financial and non-financial determinants of Asian automobile stock prices. Accountancy Business and the Public Interest, 17, 142–162. http://visar.csustan.edu/aaba/SheikhChaudhryMukhtar2018.pdf

- Shin, Y., Yu, B., & Greenwood-Nimmo, M. (2013). Modelling asymmetric cointegration and dynamic multipliers in a nonlinear ARDL framework. In R. C. Sickles & W. C. Horrace (Eds.), BT - Festschrift in Honor of Peter Schmidt: Econometric Methods and Applications (pp. 281–314). Springer New York. https://doi.org/10.2139/ssrn.1807745

- Shin, Y., Yu, B., & Greenwood-Nimmo, M. (2014). Modelling Asymmetric Cointegration and Dynamic Multipliers in a Nonlinear ARDL Framework BT - Festschrift in Honor of Peter Schmidt. In R. C. Sickles & W. C. Horrace, (Eds.), Econometric Methods and Applications (pp. 281–314). New York: Springer. https://doi.org/10.1007/978-1-4899-8008-3_9

- Shrestha, K. M., & Liu, M. (2008). Analysis of the long‐term relationship between macro‐economic variables and the Chinese stock market using heteroscedastic cointegration. Managerial Finance, 34(11), 744–755. https://doi.org/10.1108/03074350810900479

- Sikhosana, A., & Aye, G. C. (2018). Asymmetric volatility transmission between the real exchange rate and stock returns in South Africa. Economic Analysis and Policy, 60, 1–8. https://doi.org/org/10.1016/j.eap.2018.08.002

- Simbolon, L., & Purwanto. (2018). The influence of macroeconomic factors on stock price: The case of real estate and property companies. In Global tensions in financial markets (Vol. 34, pp. 2–19). Emerald Publishing Limited. https://doi.org/org/doi:10.1108/S0196-382120170000034010

- Singhania, M., & Prakash, S. (2014). Volatility and cross correlations of stock markets in SAARC nations. South Asian Journal of Global Business Research, 3(2), 154–169. https://doi.org/10.1108/SAJGBR-04-2012-0056

- Spilioti, S. N. (2016). Does the sentiment of investors explain differences between predicted and realized stock prices? Studies in Economics and Finance, 33(3), 403–416. https://doi.org/10.1108/SEF-11-2014-0218

- Tabash, M. I., Sheikh, U. A., & Asad, M. (2020). Market miracles: Resilience of Karachi stock exchange index against terrorism in Pakistan. Cogent Economics & Finance, 8(1), 1821998. https://doi.org/10.1080/23322039.2020

- Tehreem, F. (2018). An aggregate and disaggregate energy consumption, industrial growth and CO2 emission: Fresh evidence from structural breaks and combined cointegration for China. International Journal of Energy Sector Management, 12(1), 130–150. https://doi.org/10.1108/IJESM-08-2017-0007

- Tiwari, A. K., Dar, A. B., Bhanja, N., Arouri, M., & Teulon, F. (2015). Stock returns and inflation in Pakistan. Economic Modelling, 47, 23–31. https://doi.org/org/10.1016/j.econmod.2014.12.043

- Tuna, G. (2018). Interaction between precious metals price and Islamic stock markets. International Journal of Islamic and Middle Eastern Finance and Management, 12(1), 96–114. https://doi.org/10.1108/IMEFM-06-2017-0143

- Ulusoy, V., & Demiralay, S. (2017). Energy demand and stock market development in OECD countries: A panel data analysis. Renewable and Sustainable Energy Reviews, 71, 141–149. https://doi.org/org/10.1016/j.rser.2016.11.121

- Umar, M., & Sun, G. (2015). Country risk, stock prices, and the exchange rate of the renminbi. Journal of Financial Economic Policy, 7(4), 366–376. https://doi.org/10.1108/JFEP-11-2014-0073

- Wickremasinghe, G. (2011). The Sri Lankan stock market and the macroeconomy: An empirical investigation. Studies in Economics and Finance, 28(3), 179–195. https://doi.org/10.1108/10867371111141954

- Yan, H., Yang, S., & Zhao, S. (2016). Research on convertible bond pricing efficiency based on nonparametric fixed effect panel data model. China Finance Review International, 6(1), 32–55. https://doi.org/10.1108/CFRI-04-2015-0030

- You, W., Guo, Y., Zhu, H., & Tang, Y. (2017). Oil price shocks, economic policy uncertainty and industry stock returns in China: Asymmetric effects with quantile regression. Energy Economics, 68, 1–18. https://doi.org/org/10.1016/j.eneco.2017.09.007

- Zafar, M. W., Zaidi, S. A. H., Sinha, A., Gedikli, A., & Hou, F. (2019). The role of stock market and banking sector development, and renewable energy consumption in carbon emissions: Insights from G-7 and N-11 countries. Resources Policy, 62, 427–436. https://doi.org/org/10.1016/j.resourpol.2019.05.003