?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

In prior literature it was conjectured that the Indian stock market responses on domestic macroeconomic surprises are expected to be significantly influenced by global surprises. In this paper we empirically established that hypothesis. We used both the Event Analysis and VAR model. We found that global surprises consistently dominate Indian stock market and the influence of domestic macroeconomic surprises on it is relatively less. The understanding of stock market dynamics against domestic macroeconomic surprises and global factors can provide assistance to the policy makers for augmenting policy effectiveness and the corporate finance professionals for enhancing decision making.

PUBLIC INTEREST STATEMENT

The study examines the sensitivities of stock returns under the simultaneous influence of three different surprises, which are global surprise, surprise caused by domestic monetary policy, and surprise by macroeconomic policy. By taking into consideration the different measures of monetary policy, multiple domestic macroeconomic surprises and global factors, the unanticipated elements are segregated. To assess the sensitivities of stock returns to multiple surprises, we considered representative indices. In the VAR analysis, all the surprises are considered as exogenous variable. The result conclusively shows that the Indian stock market responses on macroeconomic surprises are more influenced by global surprise variables than the domestic factors.

1. Introduction

Researches related to the effect of macroeconomic uncertainties on stock market are limited, and many studies focus on domestic factors to explain the shock. The simultaneous impact of global factors on macroeconomy has never been explored. The understanding of such impact is important owing to the integration of the Indian stock market that involves FIIs/FPIs (Foreign Institutional/Portfolio Investors), which are invested in multiple ways through debt instruments, equity instruments, and derivative instruments such as Futures, Options, etc.

India liberalized its economy in 1991 and this liberalization allowed foreign investors to invest in India. Globally, the liberalization of emerging market started in late 1980s (Buckberg, Citation1995). After the stabilization of socio, political, and economic environment, the data of India from 2003 to 2016 () clearly shows fluctuating trend of foreign capital. Net FPI inflows have been in the range of USD 15 billion on an average since 2003, but the absolute quantum shows fluctuations each year. Prima facie, few of such fluctuations can be explained as major events, for example, the reason for net negative inflow of FPI/FII in 2009 can be attributed to the financial crisis and very high net positive

Chart-1. FPI/FII- Net investment in India

inflow of FPI/FII in 2015 can possibly be attributed to change in political regime, as many of the fluctuations probably have limited explanatory power.

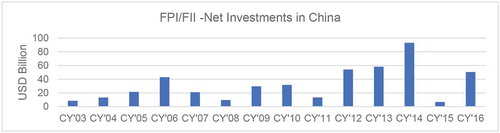

Considering the FPI/FII movement in China (), we observed the fluctuation of net FII/FPI flow, but the average investment per year since 2003 is very similar to India, around 14 Billion USD, though there is difference in absolute quantum in each year.

Chart-2. FPI/FII- Net investment in China

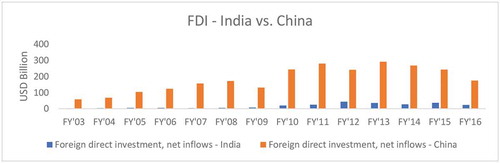

Comparing the FDI in India and China in the similar period (), we observed that the investment quantum is very different. Since 2003, the cumulative net FDI in India is 245 Billion USD, whereas the net investment in China during the same period is almost 10 times.

Chart-3. FDI—India vs. China

Since FDI is long term in nature, the investment of FDI in a particular sector is more strategic and its performance is integrated with domestic economy relevant to that particular sector. Though FPI and FII investments are motivated by different philosophies, but these investments may not completely rely on domestic economic factors. So, the relevant question is regarding the dominance of the shock, i.e., whether the shock created by domestic macroeconomic factors in the Indian economy or the shock created by global factors dominates.

Several researches have been conducted on the impact of monetary policy and macroeconomic factors in a single economy. For example, (B. Bernanke & Blinder, Citation1992; B. S. Bernanke & Kuttner, Citation2005; Kashyap et al., Citation1993; Dedola & Lippi, Citation2005; Kashyap et al., Citation1994; Ehrmann & Fratzscher, Citation2004; Benanke & Gertler, Citation1989; Kiyotaki & Moore, Citation1997; Thorbecke, Citation1997; Ganley & Salmon, Citation1997; Hayo & Uhlenbrock, Citation2000; Angeloni & Ehrmann, Citation2003, etc.) conducted different studies on monetary policy, and (Maysami et al. (Citation2005), Ewing (Citation2002), Gupta and Reid (Citation2013), Coleman and Tettey (Citation2008), and Pal and Garg (Citation2019), etc.) conducted different studies for macroeconomic variables. All these previous studies specifically focused on single market analysis and not analyzed with global linkage.

The role of global investments, particularly in an emerging economy, has emerged as the area of interest in the late 1980s. The studies conducted by Bekaert et al. (Citation2002), Bohn and Tesar (Citation1996), Aitken (Citation1998), Warther (Citation1995), Clark and Berko (Citation1997), etc., have focused on multiple dimensions. The first area of interest is motivation behind global investments and highlights quite a few factors such as considering motivation as portfolio rebalancing, return chasing, feedback-trading, price-pressure, information effect, broadening base, etc. Studies have highlighted many compelling reasons for such global investments in the emerging economies. Some studies such as Henry (Citation2000), Bekaert and Harvey (Citation2000), Stulz (Citation1999), and Choe et al. (Citation1999) have further focused on the impacts of such global investments in the emerging economies and presented evidence for quite a few possibile impacts such as cost of capital, stock market volatility, herding effect, permanent price shift, capital flight, etc. Furthermore, another set of studies such as Dornbusch et al. (Citation2000), Radelet and Sachs (Citation2000), Soydemir (Citation2000), Froot et al. (Citation2001), Pagan and Soydemir (Citation2001), Ferson and Harvey (Citation1998), Giovannini and Jorion (Citation1989), Harvey (Citation1991), etc., has focused on reasons for differential outcome such as institutional framework, dominant interconnection, regional features, etc. Few studies such as Bilson et al. (Citation2001), Abugri (Citation2008), etc. demonstrate the influence of domestic macroeconomic factors along with global factors on the emerging market.

From the varying results of the existing literature, it becomes evident that the motive and impact of foreign portfolio inflow on an emerging economy is country specific and depends on economic fundamentals and institutional framework of the country. The generalized conclusion for India cannot be drawn from the global study or studies on other emerging economies in case the foreign shock dominates over domestic shocks.

In the paper, “Macroeconomic surprises and Stock Market responses—a study on Indian Stock Market”, by Pal and Garg (Citation2019), conjectured that Indian stock market responses on macroeconomic surprises probably have been affected by global factors. Taking clue from that conjecture, this paper investigates an important question regarding the significant transmission of shocks to market returns generated by the domestic macroeconomic shocks and global shocks. The shocks are considered in the form of surprise and the results obtained from the empirical analysis demonstrate that the global surprises substantially and consistently dominate Indian market, whereas the influence of the local macroeconomic surprises is relatively less but varies in magnitude and significance.

Pal and Garg (Citation2019) dealt with sensitivities of stock returns under simultaneous influence of two surprises: surprise caused by domestic monetary policy, and surprise caused by macroeconomic policy. Therefore, it was completely focused on domestic economy. This paper brought the perspective of global linkage. With additional data set of global factors, this paper further examines the sensitivities of stock returns under the simultaneous influence of three different surprises: global surprise, surprise caused by domestic monetary policy, and surprise caused by domestic macroeconomic policy. The effect of domestic macroeconomic policies is captured through multiple indicators, and for this study, we considered GDP growth rates, Consumer Price indices (CPI), Wholesale Price indices (WPI), Index of industrial production (IIP), and current account deficit (CAD) as representative macroeconomic parameters. The surprise of MSCI is used as proxy for the global factors to understand the relative role of global influence. The sensitivities of different Indian stock indices are evaluated against the surprises of domestic macroeconomic factors, surprises of domestic monetary policy and global surprise. The basic hypothesis that we wanted to establish in this paper is that the market responses on macroeconomic surprises are more affected by the global factors. To establish this causality, the data sets used for the domestic monetary and macroeconomic factors are kept similar to those used by Pal and Garg (Citation2019), and thus any improvement in result is likely to be contributed by the surprises caused from the global factors. To do the study more conclusively, we also followed the similar methodology used by Pal and Garg (Citation2019) but augmented their methodology with global surprise factors. Therefore, the efficiency gain in the result is purely attributed to the new explanatory variable. Overall by following closely Pal and Garg (Citation2019), this paper is complementary to Pal and Garg (Citation2019) with new insight.

The previous studies in India dealing with macroeconomic and monetary policy surprises have focused only on single economy. This paper brought the perspective of global linkage. To the best of our understanding, no study on Indian economy deals with the impact on stock returns under simultaneous influences of three different surprises: global surprise, surprise caused by domestic monetary policy, and surprise caused by domestic macroeconomic policy. The study makes significant contribution to the information available about the dynamic relationship of stock returns with the local and global variables within a multivariate framework. The empirical relationships found show several vital impacts for investors as well as policymakers. First, the differing magnitudes and duration of shocks caused by the variables add to the volatility in returns; thereby optimizing the portfolio performance of different investors. Second, the institutional investors consider the emerging market stocks as a separate asset class without considering the fundamentals of emerging countries, thus creating a situation of price bubble overshooting asset price and its subsequent busting. The overarching implications extend beyond stock prices, thus impacting the steps taken by policy makers to deal with economic issues like short-term capital inflows, hot money, contagion effects, and exchange rate fluctuations (Aitken, Citation1998). Considering the standpoint regarding a policy while taking into account the global variables, the empirical relationship proposed in this study can provide different insights about the conceptualization and implementation of proper monetary and fiscal policies that play a crucial role in stabilizing the financial markets.

2. Literature review

The extensive research has been conducted with respect to the role of monetary policy on stock market (Angeloni & Ehrmann, Citation2003; Benanke & Gertler, Citation1989; B. Bernanke & Blinder, Citation1992; Dedola & Lippi, Citation2005; Ehrmann & Fratzscher, Citation2004; Ganley & Salmon, Citation1997; Hayo & Uhlenbrock, Citation2000; Kashyap et al., Citation1994, Citation1993; Kiyotaki & Moore, Citation1997; B. S. Bernanke & Kuttner, Citation2005; Thorbecke, Citation1997). The relation of stock market returns with other macroeconomic variables has been verified in different studies, viz, Maysami et al. (Citation2005), Ewing (Citation2002), Gupta and Reid (Citation2013), and Coleman and Tettey (Citation2008).Footnote1 These studies have specifically focused on single market analysis. However, the role of both the macroeconomic surprises and monetary policy surprises on Indian stock market has been extensively examined by Pal and Garg (Citation2019). They conjectured that Indian stock market responses on macroeconomic surprises probably have been notably affected by global variables.

Considering the financial crisis of the developing markets, the act of foreign capital in the economy has been extensively examined. The financial crisis in the emerging economy has raised the inquisitiveness of researchers about the role of foreign capital in the crisis of emerging economy. Different countries have recognized the role of foreign capital and have taken different steps related to policy development and implementation. For example, Malaysia imposed capital control in 1981 to bring stability in the financial market. But the real global integration of emerging market started from the late 1980s, when huge capital started flowing from the developed economy (Buckberg, Citation1995).

Studies have been conducted on the motivation and outcome of foreign investment in the emerging economy. From the findings of these studies, it is clear that motivations and outcomes vary. For example, after liberalization of the emerging market, the cost of capital decreases with foreign investor participation as per the theoretical expectation of IAPM (International Asset Pricing Model) because of risk sharing between the domestic and foreign investors, (Henry, Citation2000). However, Bekaert and Harvey (Citation2000) focused on foreign speculators and argued that many speculators are attracted to the emerging market for diversification benefit, but the reduction of cost of capital is not to the extent as expected by the IAPM model. Bekaert et al. (Citation2002) studied the association in 20 developing markets and estimated the dynamic relationship between shocks in flows and the cost of capital using a vector autoregression model (VAR) with capital flows, returns, dividend yields and world interest rates. They found that during the period of liberalization of a country, portfolio managers rebalance investment toward emerging economy. However, capital leaves from the emerging economy much faster than the rate at which capital flows inside the economy. This type of capital flight explains the financial crisis in Latin America and Asia. Based on US equity investment in the foreign market, Bohn and Tesar (Citation1996) tested both the hypothesis, i.e., portfolio rebalancing and return chasing; however, they rejected portfolio rebalancing hypothesis and favored return chasing hypothesis. They also observed one interesting fact based on US investors’ foreign portfolio from 1980 to 1994, i.e., though investors’ motive is overall return chasing, the returns achieved by investors are actually less than the alternative strategy of following market-weighted portfolio. Further, the loss of return does not translate into lowering of risk, the fact actually points to the conclusion that the investors failed to be at the right market at the right time. Aitken (Citation1998) extensively studied the position of institutional investor in the emerging economies, and the implicit hypothesis is that the foreign investors are return chasers. In this study, he concluded that the emerging market stocks are regarded as a separate asset class by institutional investors without going deeper into the emerging country’s fundamentals, which in turn creates a situation of price bubble overshooting asset price and its subsequent busting. The implications are beyond mere stock prices, as the tasks of policy makers become difficult when they try to frame the right policy related to macroeconomic problems like the appropriate response to stabilize short-term capital inflows, restrict hot money flow, reduce exchange rate fluctuation, and minimize contagion effects. Warther (Citation1995) based on the data of US-based mutual fund argued that the stock returns are highly correlated with unexpected capital flow but not so much with the expected capital flow. He found no evidence that capital flow lags return and therefore rejected the feedback-trading hypothesis, which predicts the lag effect of capital flow. However, he tended to believe that the causality is in support either because of the price-pressure hypothesis or information effect hypothesis. Clark and Berko (Citation1997) worked on foreign investment in the emerging market and used Mexico as a case-in-point. They found evidence in support of broadening base hypothesis, which suggests that the exogenous increase of capital inflow from the foreign investors is to diversify, share risk and lower perceived liquidity risk, and that the inflow causes permanent price rise. Upon segregating the inflow into two components, i.e., forecastable and surprise, they found forecastable inflow does not cause price rise, whereas surprise inflow does. However, they neither found support for price pressure hypothesis, as there is no evidence of lagged surprise inflows to be linked with negative return, nor feedback trading hypothesis, and thus they intended to believe that investors are not return chaser. Nevertheless, they strongly recommended the analysts to focus on emerging market stock performance and consider an integrated market for global equity return. Stulz (Citation1999) found that the portfolio capital inflow has permanent pricing effect but there is no evidence to claim that foreign portfolio flow causes volatility in pricing; rather it has been observed that economic liberalization does not necessarily mean that the movement of world market causes the movement of stock market. However, investors generally take overall view of the emerging market based on one or two emerging markets, but it does not mean that the type of view taken by investors causes irrational contagion across emerging market. Choe et al. (Citation1999) also argued that there is no evidence that foreign investors have destabilized the financial market at the time of Korean crisis during 1996–1997. They found that foreign investor actually follows “herding” before crisis but not at the time of crisis. They defined “herding” as the stock trading done by the group of foreign investors in a short period of time, typically in a day, and found no such capital flight evidence. They further added that equity market has a built-in mechanism, which prevents heavy selling by foreign investors when asset price falls even without trading, as all the transactions have to be carried out at fair market value. Focusing on 2008 financial crisis, Rose and Spiegel (Citation2010) and Rose and Spiegel (Citation2011) also did not find strong evidence on international linkage with global crisis, and the exposure to the United States, either through real channel, such as trade, or financial channel, such as portfolio investment, has little impact on global contagion. Therefore, they concluded “early warning system” for future crisis is difficult.

Few studies have actually highlighted that the impact is dependent on economic fundamentals and institutional framework. Dornbusch et al. (Citation2000) argued that minimizing the risk of contagion is one of the major objectives for policy makers of international finance. The transmission of the shocks in an economy is country specific and related to various other international linkages such as trade link, investor behavior, country’s liquidity position, information asymmetries, coordination, etc. Therefore, the macroeconomic factors and institutional resilience are important, particularly for the emerging markets, as the emerging markets are susceptible to high degree of volatility of capital flow, as these markets are not generally prepared to deal with unstable capital flow and prone to contagion. The extensive literature survey by Singh (Citation2010) supported the gains from trade and role of WTO in the development of free trade but highlighted the institutional role in the emerging economy. The gain from trade is realized only comprehensive economic reforms are undertaken by the emerging economies, and trade is only one of such reforms. Radelet and Sachs (Citation2000) also supported the institutional angle of emerging economy based on the East Asian financial crisis. They found few commonalities among all the affected countries, which are fragile financial institutions, macroeconomic shortcomings, poor legal framework, and deep corruptions. These poor institutional frameworks lead to financial panic, and at the time of panic, small event can even lead to larger financial crisis by triggering capital flight. Soydemir (Citation2000) using a VAR model investigated the transmission pattern between stock markets of the developed and emerging economies, and attributed the economic fundamental and trade linkage as the two probable causes for variations in the transmission pattern. By focusing in 415 country-industry equity portfolio during 2007 to 2009 financial crisis, Bekaert et al. (Citation2014), found support on “wake-up call” hypothesis, which talks about crisis in one region gives a wake-up call to the investors in other region to reassess the fundamentals in that region. They did not find any contagion from US market to global market, even though crisis originated from the United States, rather they found influences of local economic fundamentals were more in the respective equity markets. The exposure to external factors, such as trade, banking, and other financial linkages played major role on transmission and as a result, countries with weak economic fundamentals, low sovereign rating, high fiscal deficit, high current account deficit, etc. were affected more by the financial crisis. Fratzscher (Citation2012) found evidence on “flight-to-safety” hypothesis at the time of 2008 financial crisis. At the time of crisis significant capital reallocation happened from emerging economy to advance economy, while the capital movement was just opposite before and after the crisis. The drivers of capital flow are both push factors, i.e. factors in advance economies that affected all economies, and pull factors, i.e. country specific factors. At the time of crisis and during subsequent recovery, push factors such as macroeconomic factors, policies in advance economy, etc. particularly in the United States, influenced capital flow to emerging economy, Whereas, during post crisis recovery, pull factors, such as country specific macroeconomic conditions, policies, institutional setup, etc. also played critical role. However, the real and financial linkage of countries played little role on capital flow. Therefore, they concluded that not the capital control measures but the improved macroeconomic conditions and institutional set up can reduce countries’ vulnerability to external shocks.

Dominant interconnection and regional features also play crucial role in relation to the outcome. Froot et al. (Citation2001) found that the inflows associated with international portfolios are correlated within region, and the co-movement of inflows and return has positive relation in the emerging economies. Further, this co-movement has some predictive power, as the current inflow predicts future inflow and the expected future inflow drives price. Therefore, with reduction in the inflow, the market experiences price pressure and this price pressure can be substantial for emerging economies. Pagan and Soydemir (Citation2001) studied the extent of linkage in Latin American economy with other parts of the world and observed that the Latin American market is significantly connected with the Mexican stock market. They further found that investors of the Latin American market react more heavily during the downturn than during upturn, which becomes evident in the Mexican stock market. Moreover, the response is not same across all Latin American countries. Such strong external linkage of the Latin American countries with the Mexican market makes several monetary policy actions less effective. By assuming an integrated global market, Ferson and Harvey (Citation1997) provided an empirical framework related to the global asset pricing by linking macroeconomic parameters with global economic risk. The study comprised of many preordained global conditioning variables, and MSCI world market return was one of the key variables. Giovannini and Jorion (Citation1989) focused on the return of global financial assets and recognized the global linkage; they also included in their asset pricing model the returns on a portfolio comprising of US stock, dollar, Deutsche mark, sterling, and Swiss franc assets. They found that the expected return and volatility of return varies over time and their results are generally consistent with other studies on time variant analysis of the global financial assets, for instance, Cumby and Obstfeld (Citation1981), Cumby and Obstfeld (Citation1984), etc. Harvey (Citation1991) argued that in an economically unified global market, the predictable return on the collection of securities in a specific country is dependent on country’s world risk exposure and used the MSCI world equity indices as a measure of the linkages. By focusing on 2008 financial crisis after Lehman collapse, Boubaker et al. (Citation2016) found evidence about the linkage between US stock markets and other developed and emerging markets. The countries focused were Canada, France, Germany, Japan, the United Kingdom, Brazil, China, Malaysia, Russia, and Singapore. Focusing on USA and EU-27 countries before and after the global financial crisis, Turk et al. (Citation2017) found that the economies of few countries, such as Germany, France, Italy, and the United Kingdom showed strong linkage with the US economy before and after crisis, whereas Portugal and Romania did not show similar trend. Maghyereh et al. (Citation2015) investigated the association between the United States and Middle East and North African (MENA) stock market during the pre-crisis as well as post-crisis period in the year 2008. While they found low linkage between MENA markets and US market in the pre-crisis period, the linkage became very strong at the time of crisis. However, after the crisis, the linkage again started weakening to the pre-crisis low level. Zhang and Li (Citation2014) analyzed the data of Chinese and US stock market from January 2000 to January 2012 and found no long-term linkage between the two markets. However, they found that the correlation between the two markets increased significantly at the time of financial crisis in 2008. Moreover, the Chinese investors trading decision was greatly influence by the overnight information of the US stock market, and this influence was particularly high when the Chinese stocks experienced extreme movements. Tong and Wei (Citation2011) concluded composition of foreign capital flow in emerging economies is important determinant for the outcome of emerging economies at the time of crisis. They disaggregated overall capital flow into foreign direct investment, foreign portfolio flows and foreign loans, and found that emerging economies with higher exposure in foreign portfolio investments and foreign loan were affected more during 2008–2009 financial crisis, whereas emerging economies with more exposure in foreign direct investment were relatively insulated at that period.

Few studies have tried to focus on the influence of macroeconomic factors related to the emerging market return with the influence of global factors. Bilson et al. (Citation2001) examined the influence of domestic macroeconomic factors with data from 20 emerging markets and found that the explanatory power of domestic macroeconomic variables for equity return is more than that of the global factors; and hence, the local factors are more relevant. They also found that the commonality of equity market return exists within regions and not across regions. Abugri (Citation2008) conducted the study on the shocks created in the stock market return by taking into consideration the macroeconomic factors of the Latin American countries and also evaluated the role of global linkage, which was measured by the MSCI world index and the US 3-month T-bill yield. With the help of VAR model, it has been observed that the global factors show constant importance in elucidating the stock market returns of all the markets. Wongbangpo and Sharma (Citation2002) studied ASEAN-5 (Indonesia, Malaysia, Philippines, Singapore, and Thailand) and found that stock markets dynamically interact with each other during both the long term and the short term, and was fundamentally driven by the macroeconomic variables, primarily by GNP (Gross National Product), Money Supply and Nominal Interest Rate, but not so much by the Exchange Rate. Wang and Guo (Citation2020) studied stock markets in China and G20 stock markets from January 2005 to March 2018. They found that at the time of market instability, the influence of the US and European markets is more on the Chinese market than that when the market is stable. Moreover, in general, the influence of US and European markets is lower than the influence of Asian countries, viz, South Korea, and India. The underlaying influencing factors at the time of crisis are not emanating from the economic fundamentals. However, in the post crisis period, the industrial similarities between China and other nations generally explain the influence; and hence, those influencing factors are mostly based on the economic fundamentals.

From the varying results of the multiple literature, the motive and impact of the inflow of foreign portfolio to an emerging economy seems to be country specific and is largely dependent on the social, economic, and political set up. The linkage characteristic is also time varying. Though there might be some commonality in the emerging markets of a region, the commonality does not exist across regions. Hence, the general conclusion related to the emerging market behavior cannot be drawn. Therefore, in the India context, a specific study is needed to understand whether foreign surprises dominate over domestic surprises.

3. Methodology and data

We primarily followed the detailed approach presented in the paper by Pal and Garg (Citation2019), where they found that the surprises of domestic monetary policy and domestic macroeconomic policy influence stock market return. The stock market response is heterogeneous and it varies with the type of industries and size of the firms. The dynamics and magnitude of responses are different for different surprises. The responses are consistently prominent for monetary policy surprises, whereas, the responses related to other macroeconomic surprises are rather low. They conjectured that the stock market response on domestic macroeconomic response is low because the market is possibly dependent on the global factors.

In the empirical literature, the stock market reaction with respect to macroeconomic or monetary policy surprises can be understood in the following three broad ways. First, the reaction is examined through a vector autoregression (VAR) framework covering few macroeconomic or monetary policy factors, stock prices and related predictive variables. Second, the event-based studies observe the stock price movements in relation to the macroeconomic or monetary policy surprises resulting from the announcements. Third, the reaction of stock prices after the policy announcements is explained depending on the heteroscedasticity of policy shocks (Rigobon, Citation2003; Rigobon & Sack, Citation2004).

Pal and Garg (Citation2019) adopted both the event study and VAR approach. We followed the same methodology and same data sets of domestic monetary and macroeconomic factors, but augmented the methodology using a new explanatory variable, the surprises caused by global factors. Thus we introduced a new data sets of global factors. By keeping the data sets used for domestic monetary and macroeconomic factors same as those used by Pal and Garg (Citation2019) but introducing new data sets of global factors and augmenting their fundamental methodology with these new data sets of global factors, we wanted to establish clearly the dominance of global factors while explaining market response in relation to macroeconomic surprises. Thus, we could conclude any improvement in result from the study of Pal and Garg (Citation2019) is only because of the new explanatory variable introduced in this study, i.e., the surprises caused by global factors, and not because of any new methodology or any new data sets of domestic monetary and macroeconomic factors. Moreover, the original data sets for domestic monetary and macroeconomic factors from 2004 to 2016 is large enough to get adequate insights. Therefore, we felt there is no compelling reasons to change the data sets of domestic monetary and macroeconomic factors, rather augmenting the fundamental methodology with the new explanatory variable, the surprises caused by global factors, is an efficient approach for our stated objective.

Briefly the followed methodology is that the surprise is defined as the difference between the actual data and the forecast data. The surprises are categorized as surprise caused by the domestic macroeconomic factors, surprise by the domestic monetary policy, and surprise by the global factors. In case of the domestic macroeconomic parameters, the data is not in continuous time series, the forecast data is the median forecast from the survey of a panel of professional forecasters captured in Bloomberg prior to the release of actual data. The domestic macroeconomic indicators considered for our study are Gross Domestic Product (GDP), Wholesale Price Index (WPI), Consumer Price Index (CPI), Index of Industrial Production (IIP), and Current Account Deficit (CAD). The surprises associated with these indicators are measured by the difference between the forecast data obtained through the Bloomberg professional survey and the actual data at the date of data release. The variation between the forecast and actual data is the measure of surprise; hence, the surprises are represented in percentage, excluding the CAD surprise that is presented in USD billion.

In case the continuous time series data is available for the domestic monetary policy and global parameters, the surprise is estimated with the help of the market data. For those surprises where the continuous time series data is available, the surprise is estimated by the market data. The domestic monetary policy surprise is measured by the 91 days T Bill yield in the secondary market and the data is available in continuous time series. Any action related to the monetary policy—such as decisions on Bank rate, Repo/Reverse Repo, CRR, SLR, etc., are considered as the Monetary Policy announcement event. The monetary policy surprise is the disparity between the 91 days T bill yield both after and before the announcement.

Several measurements have been employed in literature to measure global linkages. Bilson et al. (Citation2001), Ferson and Harvey (Citation1998), Harvey (Citation1991), Harvey (Citation1995), Buckberg (Citation1995), and Abugri (Citation2008), etc., used MSCI World Index. We followed this approach and adopted the MSCI world index as a proxy to measure Global linkage. The MSCI World Index captures the representation of 23 developed countries but does not constitute of any emerging market data including India. Therefore, it is expected to be free from the representative bias considering the data set of India. The MSCI world index is tracked every day, and the data is captured in continuous time series. Any of the announcement date of the monetary or macroeconomic policy is the “event date.” Our objective is to understand the role of sudden change of global factors on the Indian stock market for every event date causing the monetary and macroeconomic surprises. We interpreted that any change in the MSCI world index on the “event date” is the measure of global surprise on that particular even date. The difference of MSCI world index before and after any of the event date is the MSCI surprise, which is the proxy for global surprise.

Along with the general objective to understand the linkage of various surprises with stock market return, we expected similar industry effect and size affect, as it was observed in the paper by Pal and Garg (Citation2019). In that study, they analyzed 20 indices, which we replicated in this study also. But for the purpose of this paper, we presented few representative stock market indices in alignment with our study objective. These indices can be considered as the representative of large-sized firms; hence, the indices considered in this study are (a) benchmark indices—SENSEX (comprises 30 large well-established companies in BSE that are representative of different segments of the Indian economy with high stock-trade volume) and NIFTY 50 (comprise NSE 50 well established Indian companies stocks representing 13 sectors); (b) sectoral indices, i.e., indices pertinent for understanding responses that are particularly associated with an industry—BSE Health (represents Health sector), BSE IT (represents Information Technology sector), BSE Metal (represents Metal sector), and BSE BankEx (represenrs Banking sector); (c) size-specific indices for comprehending the impact of size—NIFTY 100 Midcap and NIFTY 50 Midcap (represent medium-sized firms), NIFTY 100 Smallcap (represents small-sized firms), and BSE Sensex and NIFTY 50 (represent large-sized firms).

In this study, we used the same data sets used by Pal and Garg (Citation2019) in their previous study and the data is available from 1 April 2004 to 31 July 2016.

4. Event study and findings

We updated the regression equation presented by Pal and Garg (Citation2019) with global variables, and the regression equation takes the following form:

The stock return is measured by the first differences of the logarithm of the stock indices and represented in percentage. The macroeconomic surprise variables have been normalized for better interpretation by dividing its standard error. The surprises of MSCI are also measured by the first differences of the logarithm of the MSCI indices. We carried out nine regressions with one stock index at a time; and for each stock index, we considered the stock return as the dependent variable.

Table demonstrates the results of the event study. Furthermore, we observed the impact of domestic monetary policy surprises and the surprises of MSCI world index control shocks created in the stock indices. We also observed that the coefficients of other domestic macroeconomic surprises are strongly insignificant; hence, those surprises are aligned with the low effect size of each surprise variable, and the result is coherent with the result obtained from other study by Pal and Garg (Citation2019).

Table 1. Event study: results

The R2 value without and with global variables are tabulated in Column 11 and Column 12 of Table . Though R2 value is low, the value improves with the introduction of global variables, except NIFTY 100 Smallcaps, which means that Smallcaps are less integrated with global surprises, which is not the case for other indices. The movement of stock price relies on different factors in addition to those mentioned in the model; hence, the overall R2 value is expected to be low and the result obtained is found to be coherent with other studies (B. S. Bernanke & Kuttner, Citation2005).

The industry effect and size effect is similar to the previous study by Pal and Garg (Citation2019). Some sectors such as metal shows more sensitivity toward monetary policy and MSCI. The metal sector acts as a representative of those sectors that are susceptible to economic cycle and open for international trade. As anticipated, such sectors are highly impacted by monetary policy and global factors, which is represented by the higher coefficient of monetary policy and MSCI surprises. On the contrary, the sectors such as Healthcare are more resilient at the time of economic downturn; hence, these sectors are less influenced by the monetary policy and global surprises and demonstrate relatively lower value of the respective coefficients.

The responses related to returns of the large-sized firms are evident from BSE Sensex and NIFTY 50. For the medium-sized firms the outcomes associated with stock returns are represented by NIFTY 50 Midcap and NIFTY 100 Midcap and for the small-sized firms, it is by NIFTY 100 Smallcap. Therefore, the differences in the outcomes of return to monetary policy and global factors for the large-, medium-, and small-sized firms are evident through the coefficients of monetary policy and MSCI surprises, respectively. It has been observed that the directional response of large-, medium-, and small-sized firms are consistent with the surprises of both the monetary policy and MSCI, and this implies that the global surprises are significantly important in elucidating the returns in Indian stock market.

Overall, the first level robustness of this result can be demonstrated from the fact that the outcome is consistent with different stock indices. For example, the large firms response is captured by two different data sets BSE Sensex and NIFTY 50, and the medium-sized firms are represented by NIFTY 50 Midcap and NIFTY 100 Midcap. The results are consistent for both the data sets.

5. VAR analysis and the result

We extended the six factor VAR model outlined in Pal and Garg (Citation2019) by introducing the global variables. The VAR model adopted by Pal and Garg (Citation2019) is quite efficient because of three main reasons. First, the structural VAR model, which was adopted by Pal and Garg (Citation2019), was developed by Campbell and Ammer (Citation1993) and subsequently augmented by B. S. Bernanke and Kuttner (Citation2005) to predict stock market return, is based on the economic fundamentals, and the solutions of the VAR model is derived mathematically depending on the economic theory. Second, a parsimonious VAR model that incorporates shocks in the predictor variables consisting of dividend yield, term spread, and Treasury-bill yield is capable of explaining the average return better, (Petkova, Citation2006) and Campbell (Citation1996). The VAR model of Campbell and Ammer (Citation1993) and B. S. Bernanke and Kuttner (Citation2005) uses all these predictive variables. The efficiency of predicting stock return by this VAR model structure was also highlighted by Pal and Garg (Citation2019). Third, the surprises vectors in their models are treated as pure exogenous variable, unlike many other models, where the surprises are treated as endogenous within the VAR system, which is not the case in reality. So, treatment of surprise variable as pure exogenous makes this VAR model more realistic. Though the statistical significance of impulse response will not be relevant for such exogenous variables because the interval bounds statistical significance of impulse response is more relevant for variables that are within the VAR system, the impulse response for such purely exogenous variables can be obtained through multiplier approach as proposed by B. S. Bernanke and Kuttner (Citation2005). Therefore, this VAR model is efficient without any analytical limitations. Moreover, by adopting the same methodology and augmenting it with global factors, the efficiency gain in the result, ceteris paribus, can be attributed to the global factor only. Therefore, we updated the VAR model given by introducing the domestic monetary policy surprises, five domestic macroeconomic surprises, and one global surprises. With all these surprises, the Global Macroeconomic Surprise Vector has been constructed. The state vector takes the following forms after modifying the VAR equation proposed by Campbell and Ammer (Citation1993) and B. S. Bernanke and Kuttner (Citation2005), which was subsequently updated in the study of Pal and Garg (Citation2019), to accommodate all the surprises that occur due to domestic monetary policy, domestic macroeconomic factors, and global factors.

where, is the state vector and takes

matrix form.

is the

coefficient matrix.

is

matrix that encapsulates the exogenous response of

to the Global Macroeconomic Surprises.

is the Global Macroeconomic Surprise Vector that encapsulates all the surprises. The domestic monetary policy and macroeconomic surprises are contemporaneous exogenous varaibles, which is evident in the previous study by Pal and Garg (Citation2019). By the same logic, the global surprises are also exogenous. Therefore, all these surprises represented by

are contemporaneous exogenous variables.

is the orthogonal component and is represented by

matrix.

As per Campbell and Ammer (Citation1993), the state vector is represented as

where,

= log of excess return on a stock from the beginning of period

to period

, and it is measured relative to risk free rate, which is 91 days T bill rate

= the real interest rate, which is the difference between monthly average of 91 days T bill yield and inflation, where the inflation is measured by the log difference of the nonseasonally adjusted CPI

= the change in the nominal interest rate in one successive period

= the yield spread between

period nominal interest rate and the one period nominal interest rate, i.e.,

—

. The inclusion of

in VAR equation is to eliminate the unit root problem associated with nominal interest rate (Campbell, Citation1991).

= the dividend yield measured by the log dividend-price ratio.

= the relative bill rate, which is the differential between T-bill rate at any point of time and one-year backward moving average, i.e.,

According to the suggestion of B. S. Bernanke and Kuttner (Citation2005) and subsequent deployment by Pal and Garg (Citation2019), without any exogenous surprise component supplied in the VAR equation, the forecast error of that VAR equation can be effectively broken down into two parts; one is related to the exogenous surprise component ( and the other is the component other than the exogenous surprise component (

, which is essectially orthogonal to exogenous surprise component (

. Since

is the general forecasting error related to the Global Macroeconomic Surprise Vector at time

, it is orthogonal to

Therefore, both A and

in EquationEquation (2)

(2)

(2) can be calculated using the VAR estimators primarily proposed by Campbell and Ammer (Citation1993) and B. S. Bernanke and Kuttner (Citation2005), and subsequently deployed by Pal and Garg (Citation2019) in their VAR model. The unexpected excess return,

, can be estimated from the VAR model as,

where, is appropriate

selection matrix.

Using the multiplier analysis, it is possible to calculate the impulse response. For a specific exogenous variable, if the unit shock takes place during period and no additional shocks occur in the successive period, the increment of the k-month response for the increment of 1-percentage-point surprise can be presented as

for that specific variable. This method of orthogonalization does not consider any simultaneous reaction from the macroeconomic response (B. S. Bernanke & Kuttner, Citation2005).

Similar to the previous study of Pal and Garg (Citation2019), in this study, the VAR models are also run separately with each indices. The return of indices goes as in the VAR equation. The other predictive variables are also same as those in Pal and Garg (Citation2019). These variables are Real Interest rate

, which has been calculated as the difference in 91 days T bill rate and nonseasonally adjusted CPI;

i.e., the change in the nominal interest rate measured with the change in the T-bill rate ; Spread between 10 years bond and 91 days T Bill rate (

; Dividend Price ratio (

; and Relative Bill rate (

, which is the difference in the 91 days T bill rate and 12 months lagged moving average. The Global Macroeconomic Surprise Vector constitutes of domestic exogenous monetary policy surprise variable, five exogenous domestic macroeconomic surprise variables, and one exogenous global surprise variables. Those variables refer to surprises caused by domestic monetary policy, surprises caused by domestic macroeconomic factors, i.e., GDP, WPI, CPI, IIP, CAD, and surprise caused by global factors represented as MSCI.

The data points are also same as provided in Pal and Garg (Citation2019). The monthly estimates of all the variables together with their surprises have been taken into account. In case the event-based data points are multiple in any month for a particular macroeconomic parameter, we took the average of the data points for each such event-based surprises against that macroeconomic parameter for that month. If in any month, there is no policy announcement, the monthly surprise value of that month is considered null. The data for all variables are available from 1 April of 2004 except the data of dividend price ratio, which is available only from September 2005. The cutoff date of our analysis is considered till 31 July 2016. The dividend price ratio being one of the most critical variables in the VAR equation, we constructed the VAR equation with the data from October 2005 to July 2016 for all the indices except NIFTY 100 Small Cap index. For NIFTY 100 Small Cap index, the data of price to dividend ratio is available from 17 November 2011, thus, the VAR analysis could be conducted using comparatively smaller data set.

The dynamic responses of stock return for change in 1 (one) percentage point in case of seven global macroeconomic surprises were evaluated for a span of 10 months using this VAR(1) model, and the incremental response in the k-month related to the 1 percentage point change in respective surprise is estimated as φ.

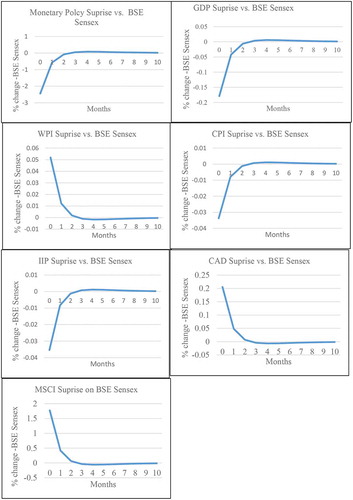

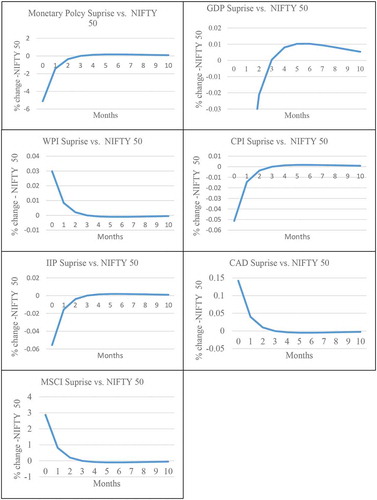

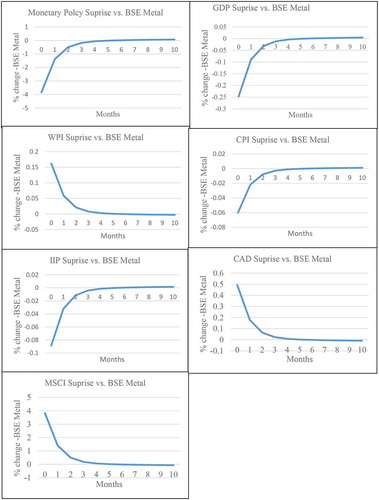

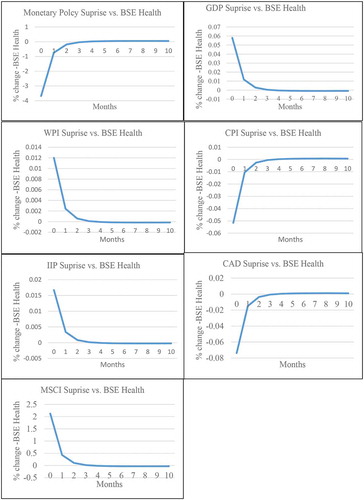

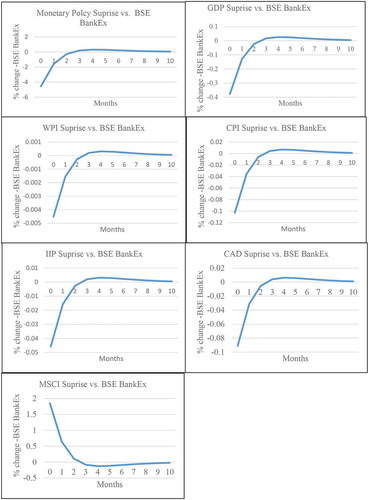

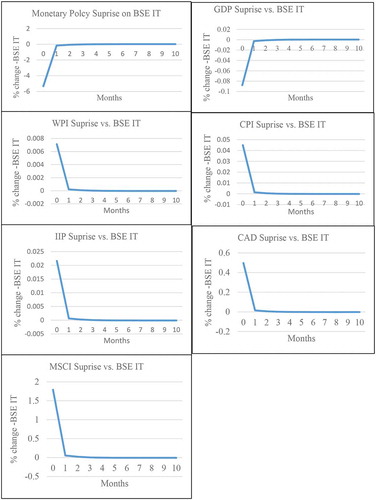

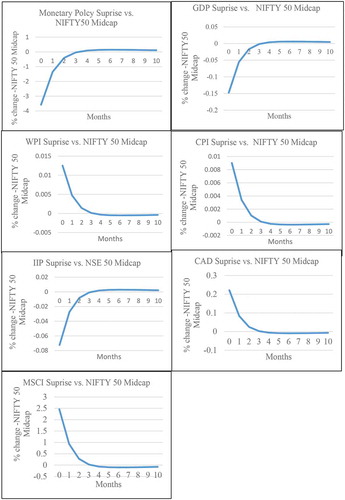

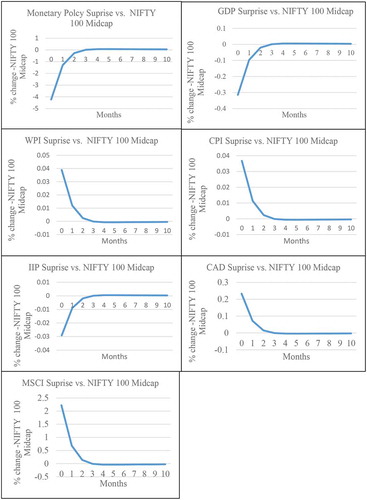

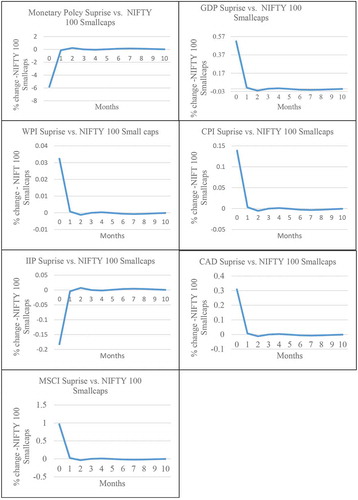

Using this model, the impulse response with regard to all the indices return in association with 1 percentage point change in the surprises is caused by domestic monetary policy, domestic macroeconomic factors represented by five macroeconomic parameters, and global factors represented by MSCI over 10 months horizon, which is shown in Figure to Figure .

In general, as per our expectation, the global surprises dominate the stock return. The results demonstrate the unfailing importance of the MSCI world index for all the indices. Through the integration of the stock markets, it has been observed that the world market surprise acts as a vital pricing factor. Therefore, the positive sign of MSCI world index surprise on stock return means that the Indian stock market has been notably unified with the world market at least in the short term.

In the event study, we found that the industry effect on stock market return is caused by the domestic monetary policy surprise and global surprises, but we found no differential industry effect on the stock market return caused by the domestic macroeconomic surprises. Nevertheless, in VAR, we noticed the differential industry effect caused by all the surprises, i.e., domestic monetary policy, domestic macroeconomic factors, and global factors. For the domestic macroeconomic policy surprises, the effect of initial surprise is less and minuscule over the 10 months period, but the period for recovery differs with respect to category of the industry. This result of domestic monetary and macroeconomic surprises is essentially same with respect to the previous study by Pal and Garg (Citation2019), where they observed the industry effect through differential impulse response across various industrial categories. However, in this study, our specific interest was to understand if the industry effect exists for global surprises also, and as per our expectation, we found the differential effect of global surprises across industry. For conducting the VAR analysis, our expectation was to choose a cyclical sector and recession proof sector for differential outcome; hence, we selected the BSE Metal as a typical index for capturing the characteristics of a cyclical sector and BSE Healthcare for capturing the nature of a recession proof sector. Figures and respectively demonstrate the dynamic response of BSE Metal and BSE Healthcare. We found that the initial response of BSE Metal is higher than BSE Healthcare as per our expectation for all the surprises, including the global surprise. We further observed the difference in response with respect to BSE Sensex. Moreover, we also expected the dominance of global surprise on the response of stock return, and in general, the global surprise dominates all other forms of surprises that influence the stock price, which is in line with our expectation. We further tested the differential impact of global surprises on other industry categories as represented by the respective stock indices. In the Banking sector represented by BSE BankEx (Banking Index), we expected that the reaction of stock on global surprises will be relatively less because there is restriction of FII and FPI investment in the Indian Public Sector Banks. Further, the Reserve Bank of India (RBI) monitors compliance with these limits on daily basis by setting a cut-off below the permissible limit. According to our expectation, it is observed that the impulse response derived from our VAR model is similar to our prediction (Figure ). In the impulse response of BSE IT Index (Figure ), we found that the recovery path of the impulse caused by the global shocks almost mimic the impact caused by domestic surprises, though the impact caused by global shocks are much more. This is also the theoretical expectation, as the Indian IT service companies follow generic business model and critically relies on the export services to offshore clients.

In the event study, we found that the size effect on stock market return is caused by the domestic monetary policy surprise and global surprises. We also specifically observed the differential impact of global surprises on the small-, medium-, and large-sized firms. According to our anticipation, we found the differential dynamic response of small-, medium-, and large-sized firms on the global surprises in the VAR analysis. We selected BSE Sensex (Figure ) and NIFTY 50 (Figure ) as the proxy of large-sized firms, NIFTY 50 Midcap (Figure ) and NIFTY 100 Midcap (Figure ), as the proxy of medium-sized firms, and NIFTY 100 Small Cap (Figure ) as the proxy of small-sized firms. We observed that the small-sized firms show less integration with global surprises. If the global surprises increase, the portfolio manager probably prefers safer stocks in India and bets on the large- and medium-sized firms, rather than the smaller-sized stocks. This result is consistent with the event study result, where the NIFTY 100 Small Cap has shown lower R2 value. However, this differential effect in relation to the size effect is also partially imminent from the industry effect because while the different indices can be used as the proxy for the firm size, however, the composition of firms in the indices brings the industry effect, (Pal & Garg, Citation2019).

Similar to event study result, the first level robustness of this result can be demonstrated from the consistency of the outcome for different stock indices. For example, consistency of the large-sized firms is represented by the two different indices BSE Sensex (Figure ) and NIFTY 50 (Figure ), and of medium-sized firms is represented by NIFTY 50 Midcap (Figure ) and NIFTY 100 Midcap (Figure ).

Figure 1. Impulse Response—1 percentage point change of Global Macroeconomic Surprise vector vs. BSE Sensex

Figure 2. Impulse Response—1 percentage point change of Global Macroeconomic Surprise vector vs. NIFTY 50

Figure 3. Impulse Response—1 percentage point change of Global Macroeconomic Surprise vector vs. BSE Metal

Figure 4. Impulse Response—1 percentage point change of Global Macroeconomic Surprise vector vs. BSE Health to

Figure 5. Impulse Response—1 percentage point change of Global Macroeconomic Surprise vector vs. BSE BankEx

Figure 6. Impulse Response—1 percentage point change of Global Macroeconomic Surprise vector vs. BSE IT Index

Figure 7. Impulse Response—1 percentage point change of Global Macroeconomic Surprise vector vs. NIFTY 50 MidCap

Figure 8. Impulse Response—1 percentage point change of Global Macroeconomic Surprise vector vs. NIFTY 100 MidCap

Figure 9. Impulse Response- 1 percentage point change of Global Macroeconomic Surprise vector vs. NIFTY 100 Small Caps

6. Conclusion

The integration of the Indian stock market with the effective involvement of FPIs and FIIs investment is evident, and many stock market reactions are nongoverned by domestic macroeconomic surprises; rather, these surprises rely on global developments. In this study, we aimed to comprehend the stock market reaction caused by surprises of domestic monetary policy and domestic macroeconomic factors together with the surprises of global factors to understand the level of global linkages with the Indian stock market. Therefore, this study deals with sensitivities of stock returns under the simultaneous influence of the three different surprises: global surprise, surprise caused by domestic monetary policy, and surprise by macroeconomic policy. Pal and Garg (Citation2019) dealt with simultaneous influence of two surprises: surprise caused by domestic monetary policy, and surprise by macroeconomic policy. In this paper, to understand simultaneous influence of the three different surprises, we extended the study done by Pal and Garg (Citation2019) and followed the same methodology and data sets of domestic monetary and macroeconomic factors but introduced new data sets of global factor and augmented the methodology with the global factor. Overall by following closely Pal and Garg (Citation2019), this study is complementary to Pal and Garg (Citation2019) with new insight.

With the use of both the Event analysis and VAR analysis, it was conclusively established that the stock indices are notably affected by the global surprises, and compared to the domestic macroeconomic surprises, the global surprise shows more importance while elucidating the returns of Indian markets. It means that the Indian stock market is notably unified with the world market at least in the short-term; and thus, the role played by global surprises are unfailingly much more crucial than the domestic macroeconomic surprises.

Most of the previous studies dealing with macroeconomic and monetary policy surprises have focused only on single economy. To the best of our knowledge, there is no study in the Indian context that links domestic monetary policy and domestic macroeconomic policy surprise with global surprises. Pal and Garg (Citation2019) conjectured that the Indian stock market responses on macroeconomic surprises probably have been notably affected by the global variables. Our results are different from study of Bilson et al. (Citation2001), wherein they found that in 20 emerging market, the impact of domestic macroeconomic variables for equity return is more than that of the global factors; and hence, the local factors are more relevant in explaining the stock market return. But our study result supports the findings of Abugri (Citation2008), which highlighted the shocks created in the stock market return by the macroeconomic factors in Latin American countries and by the global factors, the global factors dominate to explain the market return.

As the global surprise has notable and constant impact on market returns in India, the fact further emphasizes on the significance of external shocks to the Indian markets. For understanding the full risks exposures, investors in the Indian markets need to consider the external shocks to Indian markets along with the domestic economic environment. Further, it is important to analyze the focus on Indian stock market performance and consider Indian stock market as an integrated market for global equity return, otherwise the disproportionate dynamics in Indian market may not be fully understood.

Further, the findings from this study also indicate that the higher integration of the Indian market with the global economy will probably result into higher exposure to external shocks such as fluctuation of capital flow in either direction, sentiments of international capital market, and motivation of global market participants. Our findings act as the basic building block for understanding the deeper implications. Fundamentally, the overall impact of global linkage in Indian economy is dependent on real motivations of investors, Indian economic fundamentals and institutional framework. Therefore, the insights of the real motivations, such as portfolio rebalancing, return chasing, feedback-trading, broadening base, etc., along with the understanding of institutional resilience and dynamics of monetary and macroeconomic policy factors are important to assess whether India is generally prepared to deal with high degree of volatility of capital flow and not prone to contagion. In addition to the stock market volatility, the impacts of such global linkage in India can be in terms of cost of capital, permamnet price shift, capital flight, etc. With regard to these exogenous global surprises, the adoption of sensible policy preparation, categorization, and efficient implementation of such policies by domestic policymakers can assist in sterilizing their unfavorable impacts.

To understand fully the level of integration, it is important to analyze the regional integration along with country’s integration with world financial markets. The dominant interconnection and regional features play an important role in the outcome. This could be another area for future exploration.

Additional information

Funding

Notes on contributors

Santanu Pal

Santanu Pal obtained his PhD in Finance from Indian Institute of Management Lucknow. Currently he is associated with one of the leading Indian Corporates. His research interests are Macroeconomic policy, Macroeconomic uncertainty, Interaction of Macroeconomy with Market and Firms. He is reachable at [email protected]

Ajay K. Garg

Ajay K Garg is a Professor in Indian Institute of Management Lucknow. His research interest lies in Earnings Management, Public Issues and Value Creating Restructuring Strategies. He can be reached at [email protected]

Notes

1. The detailed literature review on Monetary policy and Macroeconomic factors is provided by Pal and Garg (Citation2019) in Macroeconomic surprises and stock market responses—A study on Indian stock market. Cogent Economics & Finance, 7, 1, 598, 248.

References

- Abugri, B. A. (2008). Empirical relationship between macroeconomic volatility and stock returns: Evidence from Latin American markets. International Review of Financial Analysis, 17(2), 396–28. https://doi.org/10.1016/j.irfa.2006.09.002

- Aitken, B. (1998). Have institutional investors destabilized emerging markets? Contemporary Economic Policy, 16(2), 173–184. https://doi.org/10.1111/j.1465-7287.1998.tb00510.x

- Angeloni, I., & Ehrmann, M. (2003). Monetary policy transmission in the euro area: Any changes after EMU? European Central Bank Working Paper, No. 240.

- Bekaert, G., Ehrmann, M., Fratzscher, M., & Mehl, A. (2014). The global crisis and equity market contagion. The Journal of Finance, 69(6), 2597–2649. https://doi.org/10.1111/jofi.12203

- Bekaert, G., & Harvey, C. R. (2000). Foreign speculators and emerging equity markets. The Journal of Finance, 55(2), 565–613. https://doi.org/10.1111/0022-1082.00220

- Bekaert, G., Harvey, C. R., & Lumsdaine, R. L. (2002). The dynamics of emerging market equity flows. Journal of International Money and Finance, 21(3), 295–350. https://doi.org/10.1016/S0261-5606(02)00001-3

- Benanke, B., & Gertler, M. (1989). Agency costs, net worth, and business fluctuation. American Economic Review, 79(1), 14–31. https://www.jstor.org/stable/1804770

- Bernanke, B., & Blinder, A. (1992). The federal funds rate and the channels of monetary transmission. American Economic Review, 82(4), 901–921. https://www.jstor.org/stable/2117350.

- Bernanke, B. S., & Kuttner, K. N. (2005). What explains the stock market’s reaction to federal reserve policy? Journal of Finance, 60(3), 1221–1257. https://doi.org/10.1111/j.1540-6261.2005.00760.x.

- Bilson, C. M., Brailsford, T. J., & Hooper, V. J. (2001). Selecting macroeconomic variables as explanatory factors of emerging stock market returns. Pacific-Basin Finance Journal, 9(4), 401–426. https://doi.org/10.1016/S0927-538X(01)00020-8

- Bohn, H., & Tesar, L. L. (1996). U.S. equity investment in foreign markets: Portfolio rebalancing or return chasing? The American Economic Review, 86(2), 77–81. https://www.jstor.org/stable/2118100.

- Boubaker, S., Jouini, J., & Lahiani, A. (2016). Financial contagion between the US and selected developed and emerging countries: The case of the subprime crisis. The Quarterly Review of Economics and Finance, 61, 14–28. https://doi.org/10.1016/j.qref.2015.11.001

- Buckberg, E. (1995). Emerging stock markets and international asset pricing. The World Bank Economic Review, 9(1), 51–74. https://doi.org/10.1093/wber/9.1.51

- Campbell, J. Y. (1991). A variance decomposition for stock returns. The Economic Journal, 101(2), 157–179. https://doi.org/10.2307/2233809

- Campbell, J. Y. (1996). Understanding risk and return. The Journal of Political Economy, 104(405), 298–345. https://doi.org/10.1086/262026

- Campbell, J. Y., & Ammer, J. (1993). What moves the stock and bond markets? A variance decomposition for long‐term asset returns. Journal of Finance, 48(1), 3–37. https://doi.org/10.1111/j.1540-6261.1993.tb04700.x

- Choe, H., Kho, B. C., & Stulz, R. M. (1999). Do foreign investors destabilize stock markets? The Korean experience in 1997. Journal of Financial Economics, 54(2), 227–264. https://doi.org/10.1016/S0304-405X(99)00037-9

- Clark, J., & Berko, E. (1997). Foreign investment fluctuations and emerging market stock returns: The case of Mexico. Staff report 24, Federal Reserve Bank of New York, New York. https://www.newyorkfed.org/medialibrary/media/research/staff_reports/sr24.pdf.

- Coleman, K. A., & Tettey, K. F. A. (2008). Impact of macroeconomic indicators on stock market performance: The case of the Ghana Stock Exchange. Journal of Risk Finance, 9(4), 365–378. https://doi.org/10.1108/15265940810895025

- Cumby, R. E., & Obstfeld, M. (1981). A note on exchange-rate expectations and nominal interest differentials: A test of the fisher hypothesis. The Journal of Finance, 36(3), 697–703. https://doi.org/10.1111/j.1540-6261.1981.tb00654.x

- Cumby, R. E., & Obstfeld, M. (1984). International interest rate and price level linkages under flexible exchange rates: A review of recent evidence. National Bureau of Economic Research.

- Dedola, L., & Lippi, F. (2005). The monetary transmission mechanism: Evidence from the industries of five OECD countries. European Economic Review, 49(6), 1543–1569. https://doi.org/10.1016/j.euroecorev.2003.11.006

- Dornbusch, R., Park, Y. C., & Claessens, S. (2000). Contagion: Understanding how it spreads. The World Bank Research Observer, 15(2), 177–197. https://doi.org/10.1093/wbro/15.2.177

- Ehrmann, M., & Fratzscher, M. (2004). Taking stock: Monetary policy transmission to equity markets. Journal of Money, Credit, and Banking, 36(4), 719–737. https://doi.org/10.1353/mcb.2004.0063

- Ewing, B. T. (2002). Macroeconomic news and the returns of financial companies. Managerial and Decision Economics, 23(8), 439–446. https://doi.org/10.1002/mde.1093

- Ferson, W. E., & Harvey, C. R. (1997). Fundamental determinants of national equity market returns: A perspective on conditional asset pricing. Journal of Banking & Finance, 21(11–12), 1625–1665. https://doi.org/10.1016/S0378-4266(97)00044-7

- Ferson, W. E., & Harvey, C. R. (1998). Fundamental determinants of national equity market returns: A perspective on conditional asset pricing. Journal of Banking & Finance, 21(11–12), 1625–1665.

- Fratzscher, M. (2012). Capital flows, push versus pull factors and the global financial crisis. Journal of International Economies, 88(2), 341–356. https://doi.org/10.1016/j.jinteco.2012.05.003

- Froot, K. A., O’Connell, P. G. J., & Seasholes, M. S. (2001). The portfolio flows of international investors. Journal of Financial Economics, 59(2), 151–193. https://doi.org/10.1016/S0304-405X(00)00084-2

- Ganley, J., & Salmon, C. (1997). The industrial impact of monetary policy shocks: Some stylised facts. Working Paper No. 68, Bank of England.

- Giovannini, A., & Jorion, P. (1989). Time variation of risk and return in the foreign exchange and stock markets. Journal of Finance, 44(2), 307–325. https://doi.org/10.1111/j.1540-6261.1989.tb05059.x

- Gupta, R., & Reid, M. (2013). Macroeconomic surprises and stock returns in South Africa. Studies in Economics and Finance, 30(3), 266–282. https://doi.org/10.1108/SEF-Apr-2012-0049

- Harvey, C. R. (1991). The world price of covariance risk. The Journal of Finance, 46(1), 111–157. https://doi.org/10.1111/j.1540-6261.1991.tb03747.x

- Harvey, C. R. (1995). The risk exposure of emerging equity markets. The World Bank Economic Review, 9(1), 19–50. https://doi.org/10.1093/wber/9.1.19

- Hayo B., Uhlenbrock B. (2000) Industry Effects of Monetary Policy in Germany. In von Hagen J., Waller C.J. (Eds.) Regional Aspects of Monetary Policy in Europe. ZEI Studies in European Economics and Law, 1. Boston, MA: Springer. https://doi.org/10.1007/978-1-4757-6390-4_5

- Henry, P. B. (2000). Stock market liberalization, economic reform, and emerging market equity price. The Journal of Finance, 55(2), 529–564. https://doi.org/10.1111/0022-1082.00219

- Kashyap, A. K., Lamont, O. A., & Stein, J. C. (1994). Credit conditions and the cyclical behavior of inventories. Quarterly Journal of Economics, 109(3), 565–592. https://doi.org/10.2307/2118414

- Kashyap, A. K., Stein, J. C., & Wilcox, D. W. (1993). Monetary policy and credit conditions: Evidence from the composition of external finance. American Economic Review, 83(1), 78–98. www.jstor.org/stable/2117497.

- Kiyotaki, N., & Moore, J. (1997). Credit cycles. Journal of Political Economy, 105(2), 211–248. https://doi.org/10.1086/262072

- Maghyereh, I. A., Awartani, B., & Hilu, A. K. (2015). Dynamic transmissions between the U.S. and equity markets in the MENA countries: New evidence from pre- and post-global financial crisis. The Quarterly Review of Economics and Finance, 56, 123–138. https://doi.org/10.1016/j.qref.2014.08.005

- Maysami, R. C., Howe, L. C., & Rahmat, M. A. (2005). Relationship between macroeconomic variables and stock market indices: Cointegration evidence from stock exchange of Singapore’s All-S sector indices. Journal Pengurusan (UKM Journal of Management), 24(24), 47–77. https://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.546.4232&rep=rep1&type=pdf.

- Pagan, J. A., & Soydemir, G. A. (2001). Response asymmetries in the Latin American equity market. International Review of Financial Analysis, 10(2), 175–185. https://doi.org/10.1016/S1057-5219(01)00043-6

- Pal, S., & Garg, A. K. (2019). Macroeconomic surprises and stock market responses—A study on Indian stock market. Cogent Economics & Finance, 7(1), 1598248. https://doi.org/10.1080/23322039.2019.1598248

- Petkova, R. (2006). Do the Fama–French factors proxy for innovations in predictive variables? Journal of Finance, 61(2), 581–612. https://doi.org/10.1111/j.1540-6261.2006.00849.x

- Radelet, S., & Sachs, J. (2000). The onset of the East Asian financial crisis. University of Chicago Press.

- Rigobon, R. (2003). Identification through heteroscedasticity. Review of Economics and Statistics, 85(4), 777–792. https://doi.org/10.1162/003465303772815727

- Rigobon, R., & Sack, B. (2004). The impact of monetary policy on asset prices. Journal of Monetary Economics, 51(8), 1553–1575. https://doi.org/10.1016/j.jmoneco.2004.02.004

- Rose, A., & Spiegel, M. (2010). Cross-country causes and consequences of the 2008 crisis: International linkages and American exposure. Pacific Economic Review, 15(3), 340–363. https://doi.org/10.1111/j.1468-0106.2010.00507.x

- Rose, A., & Spiegel, M. (2011). Cross-country causes and consequences of the 2008 crisis: An update. European Economic Review, 55(3), 309–324. https://doi.org/10.1016/j.euroecorev.2010.12.006

- Singh, T. (2010). Does international trade cause economic growth? A survey. The World Economy, 33(11), 176–222. doi: 10.1111/j.1467-9701.2010.01243.x.

- Soydemir, G. (2000). International transmission mechanism of stock market movements: Evidence from emerging equity markets. Journal of Forecasting, 19(3), 149–176. https://doi.org/10.1002/(SICI)1099-131X(200004)19:3<149::AID-FOR735>3.0.CO;2-C

- Stulz, R. M. (1999). International portfolio flows and security market. Working Paper No. 99-3, SSRN.

- Thorbecke, W. (1997). On stock market returns and monetary policy. Journal of Finance, 52(2), 635–654. https://doi.org/10.1111/j.1540-6261.1997.tb04816.x

- Tong, H., & Wei, S. J. (2011). The composition matters: Capital inflows and liquidity crunch during a global economic crisis. The Review of Financial Studies, 24(6), 2023–2052. https://doi.org/10.1093/rfs/hhq078

- Turk, A., Ak, R., & Bingul, B. A. (2017). Decoupling and re-coupling hypothesis during EU financial crises. The Journal of European Theoretical and Applied Studies, 5(1), 11–24. http://thejetas.org/img/71477650.pdf.

- Wang, S., & Guo, Z. (2020). A study on the co‐movement and influencing factors of stock markets between China and the other G20 members. International Journal of Financial Economics, 25(1), 43–62. https://doi.org/10.1002/ijfe.1727

- Warther, V. A. (1995). Aggregate mutual fund flows and security returns. Journal of Financial Economics, 39(2–3), 209–235. https://doi.org/10.1016/0304-405X(95)00827-2

- Wongbangpo, P., & Sharma, S. C. (2002). Stock market and macroeconomic fundamental dynamic interactions: ASEAN‐5 countries. Journal of Asian Economics, 13(1), 27–51. https://doi.org/10.1016/S1049-0078(01)00111-7

- Zhang, B., & Li, X. M. (2014). Has there been any change in the co-movement between the Chinese and US stock markets? International Review of Economics and Finance, 29, 525–536. https://doi.org/10.1016/j.iref.2013.08.001