Abstract

This study aimed to prove that social goal in improving social living standards is implanted on banking’s objective in Indonesia. This research also tried to prove that there were differences between conventional and Islamic banks in defining the company goals, whether the goals are profit-oriented or socially oriented. This social goal is also aligned with sustainable development goals (SDGs) as international agendas in the world. The banks’ contribution will be measured its impact on sustainable development goals. The developed hypotheses are equipped with good financing quality control. Furthermore, this research will compare the social goals of conventional banks and Islamic banks (sharia banks). This research used 801 data from the annual reports of conventional and Islamic banks in Indonesia from 2011 to 2018. Meanwhile, the reflection of sustainable development goals used several indicators, so that the statistical analysis used is WarpPLS. This research proved that there were differences between Islamic and conventional banks in promoting sustainable development. Generally, high financing or credit will increase sustainable development, while the sufficient/low bank profit demanded from the bank financing/credit also will increase sustainable development achievement. In conclusion, the financing quality is able to differentiate whether the low profits earned by banks are due to social orientation for sustainable development or because of poor market conditions (bad credit/financing).

PUBLIC INTEREST STATEMENT

Sustainable Development Goals are international goals adopted by more than 190 countries, including Indonesia. All parties need to participate to achieve the goals; both individually and involving institutions, including banking institutions. Indonesia is a country with the majority of the population is Muslim. Thus, the right banking system is an Islamic bank. This study has proven that banking with an Islamic system has better implications for the SDGs than conventional banks. Because Islamic principles do not only regulate business systems and ethics but also determine the entities’ goals, that is the goals oriented to the welfare of all society. However, the market capitalization of Islamic banks in Indonesia is still low so that the impact cannot be felt much. Thus, Islamic banking must be supported by extending its market power in the country. The bank with the Islamic principle is also suitable for other countries due to the good system.

1. Introduction

Indonesia becomes one of the countries that supports the achievement of the Sustainable Development Goals program (SDGs) (Central Bureau of Statistics, Citation2016). The program is an international agenda of the United Nations (UN) which is adopted by 194 countries in the world (Financial Ferivices Authority, Citation2017). To achieve the goals, it needs to involve various stakeholders, such as the bank institution.

Banking is an institution that has a clear impact on the real sector (Adekola, Citation2016; Robinson, Citation2001). Banks become capital suppliers to encourage business growth in the real sector, it has been stated in the theory of supply leading policy or supply leading finance (Abusharbeh, Citation2017; Zamzami, Citation2011). In Indonesia, the bank has a responsibility to improve the life quality of people. The social purpose of the bank has been stated in law since 19th century (Law No.10 of Citation1998—Amendment to Law No. 7 Yr 1992 concerning Banking, Pub. L. No. 10, The Unitary State of the Republic of Indonesia (Negara Kesatuan Republik Indonesia), 1998). Therefore, it can be concluded that sustainable development goals are in line with the basic objectives of banking in Indonesia.

In order to achieve the social goals, empirical studies of banks have been conducted. Banks will tend to demand not too high profit from the financing given to the customer. As the result, the customer’s burden will be lighter, and more assets can be used to be empowered in the real sector. In addition, it also increases their purchasing power (Adekola, Citation2016; Ghoniyah & Hartono, Citation2019a; Murerwa, Citation2015). This happens in developing countries like in Nigeria where banks demand low profits and are able to provide stimulants for the country’s economic growth (Adekola, Citation2016), as well as by Islamic banks (or sharia banks) for economic growth in Indonesia (Ghoniyah & Hartono, Citation2019a).

Nevertheless, profit-oriented banking is crucial in order to give feedback to customers/investors, and it can increase a customer’s tendency to save their funds in banks (Klein & Weill, Citation2018). Thus, banks can still contribute to the country’s economic growth by creating good corporate performance, and further, it can be signalled by the high profits achievement (Alkhazaleh, Citation2017; Klein & Weill, Citation2018).

Different perspectives on the ways to improve sustainable development goals also arise from the existence of two different banking systems. Since 1997, Indonesia has implemented two banking systems, they are conventional banking and Islamic banking. Islamic business orientation is not only concerned with company profits, it is an absolute principle that must be applied by Islamic banks. In other words, the company ought to be oriented towards achieving the benefit or well-being of all creatures including the environment (Muhamad, Citation2016). Therefore, the Islamic banks demand low company profits so that it does not burden the community, as an effort to stimulate economic growth (Ghoniyah & Hartono, Citation2019a). Moreover, Islamic banks are focused on channelling the funds in the real sector, not in the financial sector like conventional banks.

The different perspectives on contribution methods towards sustainable development goals by bank institutions raise new questions; whether there is a significant difference between the orientation of Islamic banks and the orientation of conventional banks on SDGs. This research is a continuity of previous research which has proven that Islamic banks in Indonesia demand low profits as a stimulant for increasing the country’s economic growth. This is strengthened by the low nonperforming financing as a control variable. When the financing quality is poor (high nonperforming financing ratio), the low profit of Islamic banks is indicated because of poor banking performance. While when the financing quality is good, the low profit of Islamic banks is to stimulate the Indonesian economy (Ghoniyah & Hartono, Citation2019a).

This study wants to explain how the differences in the contribution between Islamic banks and conventional banks in Indonesia in achieving sustainable development goals. Also, how the tendency of Islamic banks compared to conventional banks, as banks that use Islamic principles as the basis of their business.

2. Literature review

2.1. Sustainable Development Goals (SDGs) in Indonesia

Indonesia is one of the countries that has agreed to implement sustainable development goals (SDGs). The government is committed to success SDGs. The strategic steps taken by Indonesia are: (i) synchronize between objectives of SDGs with national development priorities, (ii) mapping the availability of data and indicators of SDGs, (iii) preparing operational definitions for each indicator of SDGs, (iv) preparing presidential regulations related to the implementation of sustainable development goals, and (v) preparing national action plans also regional action plans related to the implementation of SDGs in Indonesia (Central Bureau of Statistics, Citation2018).

In order to ensure the implementation of SDGs in Indonesia, the government has established a National Secretariat for Sustainable Development Goals (SDGs). This secretariat has to coordinate various activities related to the implementation of SDGs in Indonesia. A number of stakeholders including ministries, statistics Indonesia (BPS), academics, experts, civil society organizations, philanthropic institution, and firms has also been involved in various preparations for implementing SDGs (Central Bureau of Statistics, Citation2016, p. 3).

2.1.1. Indicators of sustainable development goals

Monitoring the achievement of SDGs can be seen by measuring the indicators. The indicators of SDGs are very complex because they have to cover three pillars at once. The pillars are economic, environment, and social (Central Bureau of Statistics, Citation2016; Financial Ferivices Authority, Citation2017; Janusz, Citation2016; Mohammadi et al., Citation2012; Stanny & Czarnecki, Citation2010). United Nations sets several standards for succeeding the SDGs, including unemployment rate, average wages, employment proportion, Gini coefficient, infrastructure development, and Gross Domestic Program (GDP) (Central Bureau of Statistics, Citation2016, p. 122; Clayton et al., Citation2014, pp. 191–192; Nugroho, Citation2017; Paul & Uhomoibhi, Citation2012, p. 215; Raimi & Ogunjirin, Citation2012; Wang et al., Citation2019, p. 29).

From 241 SDGs global indicators, only around one-third of the indicators can be used in Indonesia (Central Bureau of Statistics, Citation2016). There are 85 national indicators in accordance with global indicators. Meanwhile, 71 global indicators will be measured by proxied indicators, and the remaining 85 global indicators are not yet available and must be developed in the future.

Some of the social pillar indicators by Statistics Indonesia are: population growth rates, birth rates, infant death rates, life expectancy, literacy rates at the age above 15 years old, workforce participation rates, unemployment rates, poor population levels, human development index, and Gini ratio. The indicators for economic pillar include gross domestic product, inflation rate, total exports, total imports, the number of foreign tourists, the broad money supply, foreign exchange reserves, local investment level, foreign investment, currency exchange rates, and Indonesia composite index (IHSG). Whereas the indicators of environment pillar are still very few, they are the area of reforested activities, the production of crude oil, condensate, and natural gas (Central Bureau of Statistics, Citation2018).

In this study, the indicators used are indicators related to banking business processes, such as unemployment rates, poverty, human development index for a social pillar, gross domestic product, foreign tourists, inflation, and local investment for economic pillar.

2.1.2. Factors affecting sustainable development goals

Developing countries generally have economic problems such as unemployment, poverty, low living standards, and inflation. Thus, developing countries always try to increase national income and create more jobs, in order to improve people’s living standards (Abusharbeh, Citation2017). It can be achieved by welfare equity and sustainable state development.

Banking system becomes essential to increase productivity, and as main internal financial resources through the raising funds ability, credit/financing to encourage investment and production, and creating economic expansion into sectors such as agriculture, industry, and trade (Abusharbeh, Citation2017; Robinson, Citation2001). Some researchers also have proven that banking industry is able to affect the country’s growth (Abusharbeh, Citation2017; Adekola, Citation2016; Al-abedallat, Citation2017; Alkhazaleh, Citation2017; Josephine et al., Citation2016; Klein & Weill, Citation2018; Tabash & Anagreh, Citation2017).

2.2. Banking in Indonesia

Society can use bank services to save funds and payment traffic (Kasmir, Citation2003). Society can also add their capital business or funding sources from banks, it is in the form of credit in conventional banks or financing in Islamic banks. The function of the bank makes the bank known as an intermediary or financial intermediary (PSAK 31, 2000). As an intermediary connected with various parties, it is very possible for banks to give the direct movement of the business, which will have a direct implication on the economic growth of the country (Nugroho, Citation2017).

Banking in Indonesia aims to support the implementation of national development programs in order to improve equity, national stability, and economic growth. As the result, it can improve the social welfare (Law No.10 of Citation1998—Amendment to Law No. 7 Yr 1992 concerning Banking, Pub. L. No. 10, The Unitary State of the Republic of Indonesia (Negara Kesatuan Republik Indonesia), 1998). In other words, the Government recognizes the purpose of banking is not only to make bank profits as a business entity but also as an institution that bridges financial inequality in order to improve people’s life quality.

2.2.1. Islamic perspective

Spiritual teachings do not expect excessive exploitation to gain a return, but it encourages people to be able to achieve the welfare in the world and hereafter. This should be the basis of Muslims to do works and find the blessings of Allah SWT, as stated in surah Al Baqarah verse 198, Al Jumuah verse 10, and al Muzzammil verse 20. The explanation shows that in order to set return targets (profit), it must be proportional and not over-exploit the resources (Muhamad, Citation2016, p. 71). This is also in line with Indonesia law which emphasizes that companies, especially banks, have social obligations to improve the living standard of people. This statement is in line with stakeholder theory as the result of new corporate relation approach. In stakeholder theory, companies no longer exclusive their self and prioritize the company interests, especially shareholders’, instead of changing the company’s goals to achieve sustainable development.

2.2.2. Islamic bank and conventional bank

There are two banking systems in Indonesia, namely banks that apply interest system (conventional banks), and banks that apply buying and selling system (murabahah, isthisna, salam agreement) also cooperation system that will share the profits to the investors ((Islamic bank) (mudharabah and musyarakah agreement); Belkhaoui et al., Citation2020; Law No.10 of Citation1998—Amendment to Law No. 7 Yr 1992 concerning Banking, Pub. L. No. 10, The Unitary State of the Republic of Indonesia (Negara Kesatuan Republik Indonesia), 1998). Another characteristic of Islamic banks is that they consider the ethical and moral values of a business (Al-Homaidi et al., Citation2020, p. 2). For example, although business in the field of alcohol and tobacco for cigarettes are very profitable and have a low risk of failure, they have long-term effects that are harmful to the society. So that Islamic banks cannot invest their fund on it (Goaied & Sassi, Citation2011).

Islamic banks set Islamic principles as a basic foundation. They also make goals in accordance with Islamic principles as the main vision. It is called falah or victory of the world and hereafter (Biyantoro & Ghoniyah, Citation2019; Ghoniyah & Hartono, Citation2019b; Indonesian Bankers Association, Citation2014, p. 5). This emphasizes the bank’s task which must not only seek personal gain but also for the welfare of all creatures including the environment (maqashid syariah). Implicitly, Sustainable Development Goals (SDGs) become one of the objectives that are in line with Islamic banking objectives. Moreover, the allocation of fund distribution which is dominated for real sector makes Islamic banks have great potential to make a positive contribution on national development (Goaied & Sassi, Citation2011; Tabash & Anagreh, Citation2017).

The literature study that strengthens the difference in business orientation between Islamic banks and conventional banks brings up a hypothesis that must be examined. Therefore, this research involves Islamic bank data (dummy 1), and conventional bank data (dummy 0) as the research data. Based on these explanations, the hypothesis is set as follows:

H1: There are differences in the contribution of Islamic banks and conventional banks on the SDGs

2.3. Banking profit

Profitability reflecting the company’s capability to earn profits through various business policies and capital management (Harahap & Yusuf, Citation2005). Profitability is considered to be able to show management performance effectiveness (Kasmir, Citation2003). The bank’s profitability ratio uses the value of net income before taxes compared to the average of total assets (Ferdyant et al., Citation2014). The choice of average total assets as an evaluation on profits earned by banks is due to the possibility of fluctuations in third party funds (public funds in form of savings, current accounts, and deposits).

ROA=Profit before income tax x 100%

Average of total assets

Source: (Ferdyant et al., Citation2014)

2.3.1. Relationship between profit and SDGs

The existence of banks can encourage business growth in the real sector and ultimately improves society’s economy. It also gives other impacts such as increased employment, increased purchasing power, and other forms of welfare (Abusharbeh, Citation2017; Adekola, Citation2016; Robinson, Citation2001; Zamzami, Citation2011). This is in line with the objectives of banking in Indonesia (Law No.10 of Citation1998—Amendment to Law No. 7 Yr 1992 concerning Banking, Pub. L. No. 10, The Unitary State of the Republic of Indonesia (Negara Kesatuan Republik Indonesia), 1998). The existing industrial revolution reinforces that companies cannot just pay attention to themselves and ignore the surrounding environment. Corporate obligations to carry out a form of social responsibility is emerging. To achieve the goal of public welfare, many efforts can be done by banks including demanding a lower company profit (Adekola, Citation2016; Ghoniyah & Hartono, Citation2019a; Murerwa, Citation2015).

2.4. Sharia bank financing and conventional bank credit

The main function of a bank is to provide credit or financing. This activity is also one of the main bank’s activities. However, credit philosophy of conventional bank is different from the financing of the Islamic bank. Credit is only for making a profit for the bank. Meanwhile, financing is part of the function of the agent because it holds a mandate from the capital owner (bank’s customer) to manage the funds. It is a trust that must be carried out properly (Ghoniyah & Setyowati, Citation2019; Indonesian Bankers Association, Citation2015, p. 26).

The return of financing is the bank’s main income source. The amount of credit given by banks will greatly affect the amount of income that will be earned (Agza & Darwanto, Citation2017; Almanaseer & AlSlehat, Citation2016; Al Karim & Alam, Citation2013). Although financing is the main income source for Islamic banks and credit as the main income source for conventional banks (Belkhaoui et al., Citation2020), they should keep paying attention to the goals of financing activities, that is to improve the quality of living standard of the community, as stated in Indonesia law Number 21 year 2008 about Islamic banking (Indonesian Bankers Association, Citation2015, p. 25). This research used total credit or total financing by banks in analyzing the correlation (Ghoniyah & Setyowati, Citation2019; Riyadi & Yulianto, Citation2014).

2.4.1. Relationship between financing/credit with SDGs

The bank is the only institution that is allowed to collect public funds and has a central role in economic growth through its intermedial function. Banking position is crucial and strategic because bank failures can affect the macroeconomy (Indonesian Bankers Association, Citation2015, p. 25; Robinson, Citation2001; Zamzami, Citation2011). Banking also has a social purpose which is to improve the society’s living standard, because of their business patterns which are collecting and distributing money to the community (Law No.10 of Citation1998—Amendment to Law No. 7 Yr 1992 concerning Banking, Pub. L. No. 10, The Unitary State of the Republic of Indonesia (Negara Kesatuan Republik Indonesia), 1998).

Causality studies in 13 developing countries in Asia show that bank credit can increase economic growth (Habibullah & Eng, Citation2006). Especially if the funding is for production or manufacturing business, then it will have an impact on economic development (Goaied & Sassi, Citation2011). This is in line with previous research which proves that increasing the distribution of funds by banks both in the form of credit and financing can increase the national development (Abusharbeh, Citation2017; Al-abedallat, Citation2017; Alkhazaleh, Citation2017; Ghoniyah & Hartono, Citation2019a; Josephine et al., Citation2016). Thus, the hypothesis is formulated as follows:

H2: The role of banks on SDGs through optimization of credit or financing distribution

Based on the first and second hypotheses, it can be created the third hypothesis as follows.

H3: Credit or financing can support SDGs through banking profits

2.5. Financing quality or credit quality

People gets financing or credit facilities as additional capital for their business. When their business is running well, they will be able to carry out obligations to the bank. However, when the customer’s business faces obstacle and the poor financial condition, they will be unable to repay the loans. This condition is called as nonperforming credit or nonperforming financing. This phenomenon can describe the financing quality of the banks (Indriana & Zuhroh, Citation2012).

The quality of this credit or financing can be reflected in the ratio of nonperforming financing or nonperforming loan. The higher ratio means the worse the credit quality of the bank. In other words, the ratio of nonperforming loan or financing is bigger (Pratiwi, Citation2012). NPF or NPL can be formulated as follows:

NPL/NPF=Non performing financing or credit x 100%

Total Financing or Total Credit

Source: Bank Indonesia Regulation No. 9/24/DPbS year 2007 (Ferdyant et al., Citation2014; Purboastuti et al., Citation2015)

2.5.1. Relationship between financing quality and profitability on SDGs

High nonperforming financing/loan ratio means bad financing or credit. And the bad credit threatens to reduce bank revenues. On the other hand, banks have the obligation to provide sustained good performance so that they can maintain the company’s existence, it is by generating profits (Belkhaoui et al., Citation2020; Ghoniyah & Aryani, Citation2018; Indonesian Bankers Association, Citation2015, p. 2). In other words, the quality of bad credits does not only indicate a bad condition of the debtor’s business, it also can threaten the sustainability of the banks as the investors.

Banking contribution to accelerating economic growth can be shown by the low profits the bank demanded from the financing or credit distributed towards society. This conclusion will be more reliable when financing or credit quality is good. Meanwhile, if the bank’s profit is low and NPF is high, it can be concluded that the company’s performance is not good enough. Thus, they cannot make a major contribution to sustainable development goals, and the low profit achieved is because of the bad condition of business in society (Ghoniyah & Hartono, Citation2019a; Ghoniyah et al., Citation2020).

Therefore, a hypothesis that low banking profits while financing quality is good, it means the banks really have a good contribution to the sustainable development goals. Based on the explanation above, the hypothesis is set as follows:

H4: Controllable profit of banks can increase SDGs by good financing quality as moderating variable

2.6. Research roadmap

Based on the literature review dominated by the basic theories, the research roadmap is described in .

Figure 1. Research roadmap

3. Methodology

The data in this study were all banks in Indonesia, with the research period from 2011 to 2018. Other data used are various indicators of sustainable development goals published by Statistics Indonesia (Central Bureau of Statistics, Citation2018).

The data analysis used is a Structural Equation Model (SEM) approach with an alternative method of Partial Least Square (PLS). PLS approach is distribution-free (does not assume data with a specific distribution, it can be in form of nominal, category, ordinal, interval, and ratio). Therefore, PLS is appropriate for this research because the variable indicators are ratio or per cent, as well as nominal, and ordinal. PLS can also analyse constructs formed with reflective and formative indicators (Ghozali, Citation2014). PLS uses a 3-stage iteration process. Each iteration stage produces an estimation. The first stage produces the weight estimation, the second stage produces an inner model and outer model estimation, and the third stage produces means and location estimation (Ghozali, Citation2014).

4. Results and discussion

4.1. The overview of company

This research used data of banks in Indonesia during the period 2011 to 2018. The banks should publish the annual financial statements during the research period. The annual financial statements can be obtained through each banks’ official website. From 107 conventional banks and 13 Islamic banks in Indonesia, there are only 88 conventional banks and 13 Islamic banks that have an accessible annual report (Financial Ferivices Authority, Citation2018). The data is unbalanced panel because several banks in 2011 and 2012 did not yet exist or in 2018 merged with other banks. So that the total research data were 801 that consists of 98 annual reports of Islamic banks and 703 annual reports of conventional banks

Market capitalization that is dominated by conventional banks can not only be seen from the number of banks. It can also be seen from the maximum value of credits which is much higher than the maximum value of financing by Islamic banks (presented in ). The average credit by conventional banks is still higher than the average of total credit and financing. This indicates that market capitalization and contribution of fresh funds by Islamic banks to the community is still very low. It is possible if the influence Islamic banking has not been able to determine the overall banking performance. Because the huge market power could affect economic growth easier (Idun et al., Citation2020).

Table 1. The overview of banking in Indonesia

The same thing happens to the financing quality of banking. The average credit quality of the conventional bank is better than the average of total financing/credit quality. In other words, the NPL ratio of the conventional bank is lower than Islamic banks’.

4.2. The overview of sustainable development goals in Indonesia

This study used the company’s external factors as the final variable, namely sustainable development goals. In this research, indicators of sustainable development goals used are the ones who have a direct relationship with economic policy (especially banking). The following is an overview of SDGs indicators that is presented in the form of descriptive statistics ().

The environmental pillar is represented by the number of unemployment (s_unemployment), the number of poor people (s_poverty), and the human development index (s_IPM). Whereas the economic pillar is represented by the gdp growth rate (e_gdp growth), the number of foreign tourists (e_tourist), the inflation rate (e_inflation), and the level of local investment or domestic investment (e_local investment). These seven indicators refer to Statistics Indonesia data which are related to indicators of sustainable development goals in Indonesia (Central Bureau of Statistics, Citation2018).

4.3. Data analysis

4.3.1. Testing of fit model

To test the fit model, this study used WrapPLS 5.0 by looking at the output of model fit and quality as shown in . Based on , it can be concluded that the research model has fulfilled all the criteria of the fit model. Hence, the results of this research model analysis are fit to predict the phenomenon.

Table 2. The overview of sustainable development goals indicator

Table 3. General output, model fit indices, and P values

The supported data of fit model can be seen at APC, ARS, and AFIV outputs. The p-value for APC and ARS must be smaller than 0.05 (significance). In addition, AVIF as a multicollinearity indicator must be less than 5. The output indicates that the criteria are fulfilled for the goodness of fit models; APC p-value is 0.001, ARS is 0.007 and significant, also AVIF value is 1,719.

4.3.2. Measurement model testing (Outer Model)

The indicators used to measure the variables in this research are formative. In order to test the feasibility of the measurement model, it must meet two conditions. The first condition is the indicator weight must be statistically significant (p < 0.05). The second condition is regarding to multicollinearity, the value of the variance inflation factor (VIF) is smaller than 3.3 (Kock, Citation2011).

The significance value (p-value) of all indicators in this research is shown in . While the full collinearity VIF value of each variable in this research model is presented in .

Table 4. Indicator weights

Table 5. Full collinearity VIFs

Measurement model or outer model describes the relationship between indicators and latent variables. Based on the Indicator Weight output presented in ., it is known that the p-value is less than 0.05. The full collinearity of VIFs output presented in indicates the value of VIFs that do not exceed 3.3. Thus, the measurement model can be accepted.

4.3.3. Structural model testing (Inner Model)

Inner models (inner relations, structural model, and substantive theory) describe the causality relationship between latent variables that are built based on the theory. Structural models were evaluated using R-square for independent constructs, and t-test is to evaluate the structural path. The R-Square values of each endogenous variable in this research model are presented in .

Table 6. Latent variable coefficient

4.3.4. Determination coefficient

The small R-Square value indicates the ability of the independent variables to explain the dependent variable is limited. presents the total contribution of financing or credit to bank profits is 6.8%, while the other 93.2% is influenced by other factors. Meanwhile, total financing and profits of the banks are able to increase sustainable development goals by 8.7%, and the other 92.3% is influenced by other factors besides banking.

Sustainable development goals variable uses national indicators (Central Bureau of Statistics, Citation2016, Citation2018). It is a national and comprehensive assessment in reflecting the condition of Indonesia. Meanwhile, banking is the exogenous variables from one of the institutions in Indonesia. Thus, banks can not be able to give a high determination coefficient on sustainable development goals. The achievement of good state conditions can not only be caused by the role of the banking sector but also the role of various elements and policies across sectors. National assessments are indeed influenced by many factors. Nevertheless, the significance of the banking relationship to sustainable development goals further strengthens the role of banking for the country.

4.3.4.1. Hypothesis testing

Hypothesis testing in this research used t-test to determine the ability of independent variables on the dependent variable partially. While F-test is conducted to determine the effect of the independent variables in influencing the dependent variable simultaneously. As for hypothesis testing, it can be conducted by looking at the p-value path coefficients. The regression coefficients are presented in ., whereas the significance of the effect can be seen in the p-value presented in .

Table 7. Path coefficients

Table 8. P values

Based on the table of path coefficient and p-value, it can be concluded that Islamic banks as dummy variable have an insignificant relationship toward SDGs. However, it is significantly being good moderation between bank profits on SDGs. In other words, there are differences in defining profits between an Islamic bank and conventional bank, in order to achieve SDGs. Comprehensively, the results also can be found in the image below.

Figure 2. Research result model

4.3.4.2. Intervening testing

In this research model, there is a path analysis model between financing/credit, profitability, and SDGs. Therefore, it is necessary to test the indirect effect of bank profitability as an intervening variable. The test of an indirect relationship is presented in .

Table 9. Standard error

Table 10. Indirect Effect

Table 11. Defining the difference in the contribution of the Islamic banks and conventional banks on SDGs

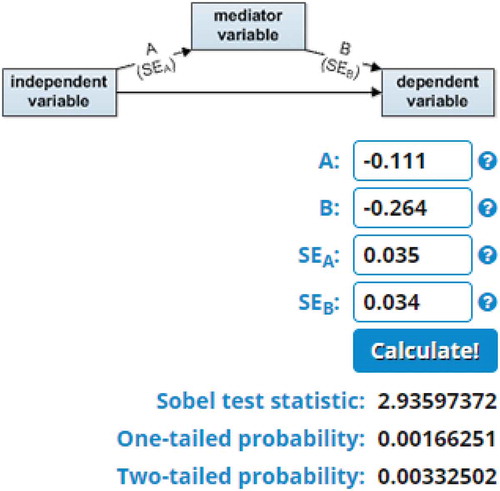

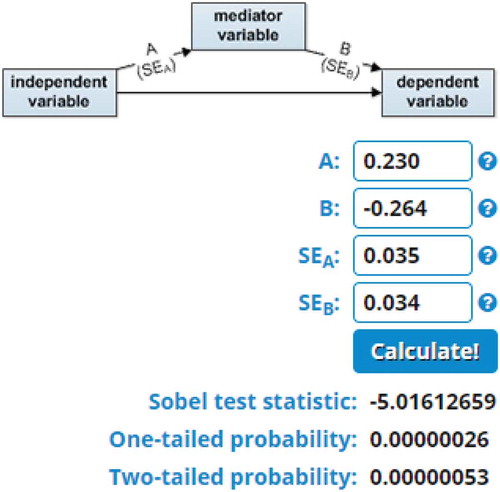

Indirect relationship testing can also be conducted by Sobel test, the results are presented in .

Figure 3. Sobel test result d_sharia → Profits → SDGs

Figure 4. Sobel test credits Result → Profits → SDGs

Based on the results, it can be known that the t statistic is more than +1.69, and the probability value is lower than 1% (p < 0.01). Thus, it is proven that financing or credit has an indirect effect on SDGs through bank profits.

Islamic dummy (d_sharia) can also influence SDGs through banking profits. This indicates that the difference contribution between Islamic banks and conventional banks in increasing SDGs, it is through bank profits.

4.4. Results and discussion

4.4.1. The Differences in the Contribution of Islamic Banks and Conventional Banks on SDGs

Hypothesis 1 explains there are differences in ways between Islamic Banks and Conventional Banks in contributing to sustainable development goals. This can be proven by the results of dummy variables that affect sustainable development goals variable. The dummy is coded 1 for Islamic banks, and 0 for conventional banks. The name of the dummy is d_sharia.

The hypothesis 1 testing can be seen by three relationships. They are the relationship between d_sharia and SDGs directly, the relationship between d_sharia and SDGs through bank profits (intervening), and the role of d_sharia in moderating the bank profits and SDGs. In the first relationship, it cannot be proven that there are significant differences in the contribution of Islamic banks and conventional banks on SDGs (). However, the different contribution on SDGs is proved through profits (intervening). Indeed, d_sharia is able to moderate earnings on SDGs with a significance level of 0.001. Thus, it can be concluded hypothesis 1 which assumes that there are differences in the contribution of Islamic banks and conventional banks, is accepted.

The results of this study also prove that generally conventional and Islamic bank concern about the goals of improving people’s welfare. Therefore, the profit demanded is not too high (the low profits increase the country’s sustainable development goals). The difference in the contribution of Islamic banks and conventional banks is on how big the impact of their profits. Too high bank profit demanded to tend to reduce the country’s level of sustainable development (coefficient −0.26). However, in Islamic banks, an increase in profit will only reduce 0.16 point of the country’s sustainable development level (coefficient of bank profit −0.026 plus 0.08 coefficient of sharia dummy, it becomes −0.16).

The high interest of credit will burden the community. The expensive cost of capital makes the community has problems with their finances of the business, especially if the market condition also in a bad situation (systematic risk). Thus, the high profits demanded by the banks will destruct the business of the community.

This research also proves that excessively high profit demand of bank can slowdown the economic growth. It works for all types of banking in Indonesia. However, banks that use sharia principles have a smaller destructive impact than conventional banks. Besides that, the market capitalization of an Islamic bank is much smaller than a conventional bank. The market share of Islamic banks in Indonesia is still below 10%. Islamic banking first emerges in Indonesia in 1992, now the number of Islamic banks is only 13 banks. While the number of conventional banks are more than 120 banks, most of them have been established for a long time.

From a business perspective of banking, the negative relationship of Islamic bank profit on SDGs shows that Islamic banks have the orientation to achieve social goals. However, Islamic bank still has a higher need of high profit than the conventional banks. It happens because Islamic banks in Indonesia are still in the developing stage so they need more funds to be superior and more stable (Gupta & Mahakud, Citation2020). While large banks that dominate the market like conventional banks have been easier to generate profits, and have been reached the business stability (Gupta & Mahakud, Citation2020; Idun et al., Citation2020).

The explanation is strengthened by the strong relationship between Islamic dummy and bank profits. Islamic banks are able to produce lower profits than conventional banks (the relation of d_sharia on profits, ). It means an Islamic bank is still in a stage to stabilize the business condition of the company, in order to achieve business sustainability.

4.4.2. The Effect of Financing or Credit on SDGs

Financing or credit can affect the banking profit (at the significance level of p 0.001). The positive relationship between credit or financing on profit is natural. It is because the bank’s main source of income comes from the return of the financing/credit (Firdaus & Ariyanti, Citation2009). This finding is in line with empirical evidence from previous researchers where an increase in credit distribution can increase the level of banking profitability (Agza & Darwanto, Citation2017; Almanaseer & AlSlehat, Citation2016; Cahyani, Citation2016; Haq, Citation2015; Jaurino & Wulandari, Citation2017).

Hypothesis 2 explains that credit or financing can achieve sustainable development goals in Indonesia. This can be known by the impact of Credits on SDGs directly. Based on , it is known that the impact of financing/credit distribution is significant at alpha 1% (p < 0.01). Thus, hypothesis 2 is accepted. Scientifically, this finding also supports the research of (Abusharbeh, Citation2017; Al-abedallat, Citation2017; Alkhazaleh, Citation2017; Josephine et al., Citation2016). All researchers agreed that the distribution of financing/credit to society or the business sector would be able to increase the country’s economic growth.

Hypothesis 3 explains that financing or credit affect sustainable development through banking profit, it can be called an indirect effect. The relationship is negative significant at alpha 1% (p < 0.01), hence hypothesis 3 is accepted. This result strengthens banking position as a company that gives stimulant for society in order to increase people’s living standard, through the economic sector.

Supply-Leading Finance Theory is a classical theory which was originally intended to stimulate the growth of the agricultural sector. In the past, the sector suffered a setback due to the lack of ability to fulfil production capital (Robinson, Citation2001, p. 138). A cheap cost of capital for farmers is expected to increase production and ultimately improve the economic conditions of the community. This concept is then implemented for other sectors (Robinson, Citation2001, p. 141), which in this study the financing of Islamic banking gives contribution comprehensively for sustainable development of the country. This pattern is in line with the condition of Indonesia as a developing country which generally requires more capital or fund.

The impact of financing or credit on sustainable development is very significant. It has a positive effect. This is consistent with Islamic benefit principle. According to existing theories, the existence of stimulants from financial assistance (funding facilities) to the community can improve people living standard or in this case is the country’s sustainable development. The results show that increasing the amount of credit/financing given by banks will increase the country’s sustainable development value.

The contribution of credit on SDGs through negative profits emphasizes that banks ought to demand sufficient or not too high company profits. Credit directly has a positive effect on SDGs, but through profits the effect is negative. It is because the small amount of profits demanded for banks on credit, in order to stimulate the people’s economy. It can be conducted easily by the banks with the large of market power (Idun et al., Citation2020).

The increased credit makes profits increase, but the increased in credit distribution was bigger than the profit enhancement, so the impact of bank profits on SDGs is negative. This negative effect is also because the bank has a charge to increase SDGs or the welfare of the community. In this case, the community is customers who receive financing. This is because the smaller the profit demanded by a bank (company), the smaller the burden (cheap capital cost for the customer), and more funds can be used for the real sector (maintain the disposable income and consumer spending growth).

4.4.3. The effect of financing quality on banking profits and SDGs

Hypothesis 4 assumes that limiting the profit of the banks can increase SDGs if it is moderated by good financing quality. There is a nonlinear relationship between the increase in profit and its impact on SDGs. As a stimulant, banks can increase the country’s economy through cheap and affordable financing/credit. That is how the low or sufficient profit gained from the bank financing/credit will raise the people’s purchasing power (consumer spending).

Through a certain level of profit, the bank is considered as a company that does not demand too high profit. This controllable profit must be balanced by good financing quality or credit quality. Thus, it can avoid misinterpretation that the nonmaximum profit is indeed not caused by bad credit quality.

Based on , it is known that profit actively affects the value of sustainable development goals, with a significance level of 1% (p < 0.01). As the moderation variable, financing quality/credit quality is able to control high profits, in order to improve SDGs. This is proven by the significant negative effect on financing quality in moderating the bank’s earnings on SDGs. Thus, hypothesis 4 is accepted.

This study proves that profit controlling is a manifestation in achieving sustainable development goals. In Indonesia, the bank’s quality credit/financing tends to strengthen the fact that low bank profits are due to social orientation to achieve sustainable development.

Credit quality can differentiate whether the low profits earned by banks are as the efforts to stimulate the economy of the community or it is because of poor credit/financing quality of the bank. Low earnings with poor credit quality (high NPF) will make the rate of sustainable development worse. It is because the market condition is in bad condition, businesses are running slowly, and the community could not pay the bank loan. Thus, the low profit achieved is because of a lot of bad credit/financing.

The low profit is accompanied by good credit quality, it shows the smallest destructive impact on SDGs (small NPF), and reinforces the fact that low profit demanded by the bank is indeed oriented towards the country’s sustainable development enhancement. Moreover, Islamic dummy that positively moderating the earnings control (low earnings) on SDGs, it emphasizes the difference in the contribution of Islamic banks and conventional banks. Islamic banks have a less destructive impact than conventional banks.

The low profit earned by bank sector does not merely indicate the existence of a company’s goal which aims to stimulate the country’s development. In contrast, there are other indications such as the failure of banks to maintain the credit quality. Therefore, the low profit could be due to bad credit. This research is able to differentiate whether the low bank profit is because of the social orientation of the bank or because of the poor financing/credit conditions.

Good credit quality is determined by good understanding and management by employees who handle the financing division of the banks. It includes the objectives and procedures for financing process, planning, and financing strategies, managing and monitoring financing, also bank financing/credit supervision. Therefore, the banking financing/credit business must be organized in such a way, based on prudence principles and best practices that have been applied internationally and are proven to be reliable (Indonesian Bankers Association, Citation2015, p. 3).

This result is reforming with previous research. The previous research showed financing quality weakens the interpretation that the low Islamic banking profits were because the bank tended to encourage sustainable development. The positive coefficient of moderation made the financing quality could not differentiate whether the low profit of Islamic banks was caused by social orientation or caused by poor market conditions (Ghoniyah & Hartono, Citation2019a).

The in-depth analysis showed that Islamic bank financing is more oriented towards the distribution of the real sector, with a cooperation agreement as their financing system (financing based on loss and profit-sharing principle). Meanwhile, conventional banks implement an interest system in their credit business. The conventional bank also invests in the financial sector, money market, and foreign exchange. In other words, there is a tendency for Islamic banks to play with a higher level of risk. Therefore, Islamic banks still have to improve their risk management (Belkhaoui et al., Citation2020; Ghoniyah & Hartono, Citation2019a, p. 105).

5. Conclusion

The four hypotheses proposed in this research are accepted. The first hypothesis about the difference in the contribution of Islamic banks and conventional banks on SDGs is proven by moderating the role of earnings. Both types of banks have earnings control (sufficient earnings) to stimulate the country’s development, and Islamic banks have smaller destructive effects than conventional banks. In the second hypothesis, credit or bank financing can directly enhance the country’s sustainable development. In the third hypothesis, the impact of credit/financing is reflected through the low profit (controllable profit/sufficient profits), in order to stimulate community economic growth. Meanwhile, the fourth hypothesis, it proves that the financing quality is able to differentiate whether the low profits earned by banks are due to social orientation for sustainable development or because of poor market conditions (bad credit/financing).

In conclusion, the bank could contribute to SDGs through their credit or financing, as long as the financing has good quality and the aims of the bank itself. Whether the aim of the bank is capitalism or falah oriented, it can be reflected by the profits demanded for themself.

Islamic banking gives financing through trading principle and profit lost sharing principle, and the fund is distributed to the real sector. While conventional banks implement interest system in their credit business, and also invest their fund in the financial sector, money market, and foreign exchange. Thus, Islamic banking has a better contribution than conventional banking and Islamic banking has smaller destructive impact than conventional banking.

5.1. Theoretical implication

The result of this research is expected to provide a renewal theory, and broadening the point of view in assessing the profits of a company, especially banking companies. At a certain profit target, the company not only strives to business sustainability but also having high concern for social interests. While a high-profit level indicates the company selfishness to earn profits for themselves, so it has a destructive impact on the social. This research also supports the law that banks must have social goals above personal goal which is materialistic.

This research is also expected to be able to change the entity’s paradigm. An entity should not only make material interests such as profit as the main focus but also focus on humanitarian goals such as social and environmental points. An entity should consider these goals as important as economic goals.

Previous research with the same topic proves the compatibility of Islamic bank goals with sustainable development, and this study proves it by involving conventional banks as a comparison (Islamic dummy as moderating variable). In principle, there is a difference between Islamic banks and conventional banks in interpreting the corporate goals and in affecting sustainable development goals. However, it has not been able to prove the differences absolutely. This is because of the fact that market capitalization of Islamic bank is still very low, which a bank that has large market power can have more impact on sustainable economic growth (Idun et al., Citation2020). Moreover, the Islamic bank policies must be standardized with the format of Central Bank of Indonesia which is still oriented at the interest rate (convert profits or profit-sharing rates of Islamic banks in the form of interest rates). Thus, it is necessary to develop deeper scientific matters related to sharia banking policy independently. Furthermore, it can be a proper policy that accordance with Islamic principles.

5.2. Managerial implication

The managerial benefit of this research is that stakeholders recognize economic, social, and environmental pillars as three pillars that must be attained and considered comprehensively. It also reminds stakeholders including practitioners about the noble purpose of an entity (in this case is banking). In the end, the sustainable goals of a company can be achieved because of business patterns and business objective that has paid attention to the environmental and social elements.

Previous research related to the same topic proves the suitability of Islamic banks objectives with sustainable development goals. Conventional bank as a financial institution that dominates the market, has a lower orientation of credit distribution in the real sector. This becomes the duty for the government in formulating and realigning the orientation of banking company to match the reason the banking company founded.

Islamic banks which have more friendly implications than conventional banks can be a reference in setting and applying business objectives (social objectives). However, the lack of risk management by Islamic banks must become the attention of the Financial Services Authority, the Government, and the institution itself, to improve the company’s internal quality. Thus, Islamic banking can become a sustainable company.

5.3. Future research agenda

Business Sustainability is still becoming a problem for Islamic banking in Indonesia. It is because the age of Islamic banks in Indonesia is still young compared to conventional banks. Islamic banks still need to improve their business management to achieve business sustainability, so that it can give a more optimal impact on the country’s sustainable development. Furthermore, it needs a deeper study related to business sustainability.

Additional information

Funding

Notes on contributors

Nunung Ghoniyah

Nunung Ghoniyah is an associate professor and a senior lecturer in Faculty of Economics, Universitas Islam Sultan Agung (UNISSULA). Her research interests are in business management for SMEs, finance, economic, Islamic banking, and Islamic Business Ethics. Sustainable Development Goals (SDGs) is the current issue which must be encouraged by every entity including the Banking Sector. This study tried to accommodate it and found that the effort of Corporate sector (Banking sector) in achieving the Global Sustainable Goals must be seen by the proper ethic of the corporate to achieve it. Thus, the future research is combining her research in Islamic banking, economic, SDGs, and Islamic Business Ethics.

Sri Hartono is an associate professor at the Economics Faculty, UNISSULA. Interest in financial management, business feasibility studies, business budgeting, and management accounting. His current research is the effectiveness of corporate governance in increasing the Maqasid Shariah index of Islamic Banking.

References

- Abusharbeh, M. T. (2017). The impact of banking sector development on economic growth: Empirical analysis from Palestinian economy. Journal of Emerging Issues in Economics, Finance, and Banking, 6(2), 978–23. www.globalbizresearch.org

- Adekola, O. A. (2016). The Effect of Banks Profitability on Economic Growth in Nigeria. IOSR Journal of Business and Management (IOSR-JBM), 18(3), 1–09. https://doi.org/10.9790/487X-18320109

- Agza, Y., & Darwanto. (2017). Pengaruh Pembiayaan Murabahah, Musyarakah, dan Biaya Transaksi terhadap Profitabilitas Pembiayaan Rakyat Syaria. IQTISHADIA, 10(1), 228–248. https://doi.org/http://dx.doi.org/10.21043/iqtishadia.v10i1.2550

- Al Karim, R., & Alam, T. (2013). An evaluation of financial performance of private commercial banks in Bangladesh: Ratio analysis. Journal of Business Studies Quarterly, 5(2), 65–77. http://jbsq.org/wp-content/uploads/2013/12/December_2013_5.pdf

- Al-abedallat, A. Z. (2017). The role of the Jordanian banking sector in economic development. International Business Research, 10(4), 139. https://doi.org/10.5539/ibr.v10n4p139

- Al-Homaidi, E. A., Tabash, M. I., & Ahmad, A. (2020). The profitability of islamic banks and voluntary disclosure: Empirical insights from Yemen. Cogent Economics & Finance, 8, 1778406. https://doi.org/10.1080/23322039.2020.1778406

- Alkhazaleh, A. M. K. (2017). Problems and perspectives in management. Problems and Perspectives in Management, 15(2), 55–64. https://doi.org/10.21511/ppm.15(2).2017.05

- Almanaseer, D. S. R., & AlSlehat, D. Z. A. (2016). The impact of financing revenues of the banks on their profitability: An empirical study on local Jordanian Islami Banks. European Journal of Business and Management, 8(12), 195–202. https://www.iiste.org/Journals/index.php/EJBM/article/view/29810

- Belkhaoui, S., Alsagr, N., & van Hemmen, S. F. (2020). Financing modes, risk, efficiency and profitability in Islamic banks: Modeling for the GCC countries. Cogent Economics & Finance, 8, 1750258. https://doi.org/10.1080/23322039.2020.1750258

- Biyantoro, A., & Ghoniyah, N. (2019). Sharia compliance and Islamic corporate governance | Trikonomika. TRIKONOMIKA, 18(2), 69-73. https://doi.org/http://dx.doi.org/10.23969/trikonomika.v18i2.1465

- Cahyani, S. M. (2016). Pengaruh Pembiayaan Jual-Beli, Pembiayaan Bagi Hasil, CAR, NPF, dan Sensitivitas Inflasi terhadap ROA BUS. STIE Pebarnas: Surabaya. http://eprints.perbanas.ac.id/1561/1/ARTIKELILMIAH.pdf

- Central Bureau of Statistics. (2016). Potret Awal Tujuan Pembangunan Berkelanjutan (Sustainable Development Goals) di Indonesia. Kajian Indikator Lintas Sektor. Badan Pusat Statistik: Jakarta. https://www.bps.go.id/publication/download.html?nrbvfeve=OWEwMDJmMDA2N2M4OWU1MTFmMDQyYzEz&xzmn=aHR0cHM6Ly93d3cuYnBzLmdvLmlkL3B1YmxpY2F0aW9uLzIwMTcvMDIvMDEvOWEwMDJmMDA2N2M4OWU1MTFmMDQyYzEzL2thamlhbi1pbmRpa2F0b3ItbGludGFzLXNla3Rvci0tcG90cmV0LWF3YWwtdHVqdWFu

- Central Bureau of Statistics. (2018). Statistical Yearbook of Indonesia 2018. https://doi.org/0126-2912

- Clayton, A. H., Pinnock, F. H., & Ajagunna, I. (2014). Tourism in a transforming world economy – The impacts of the brave new world. Worldwide Hospitality and Tourism Themes, 6(2), 191–196. https://doi.org/10.1108/WHATT-01-2014-0007

- Ferdyant, F., ZR, R. A., & Takidah, E. (2014). Pengaruh Kualitas penerapan good corporate governance dan risiko Pembiayaan terhadap profitabilitas Perbankan Syariah. Jurnal Dinamika Akuntansi Dan Bisnis, 1(2), 134–149. https://doi.org/10.24815/jdab.v1i2.3584

- Financial Ferivices Authority. (2017). Tujuan Pembangunan Berkelanjutan. Badan Pusat Statistik: Jakarta. Retrieved 1 June, 2018, from https://www.ojk.go.id/sustainable-finance/id/publikasi/prinsip-dan-kesepakatan-internasional/Pages/Tujuan-Pembangunan-Berkelanjutan.aspx

- Financial Ferivices Authority. (2018). Statistik Perbankan Indonesia per 31 Desember 2017. Jakarta: Otoritas Jasa Keuangan. https://www.ojk.go.id/id/kanal/perbankan/data-dan-statistik/statistik-perbankan-indonesia/default.aspx

- Firdaus, H. R., & Ariyanti, M. (2009). Manajemen Perkreditan Bank Umum. Alfabetta.

- Ghoniyah, N., & Aryani, D. (2018). ANALISIS BUSINESS SUSTAINABILITY PADA PERBANKAN SYARIAH DI INDONESIA. In Forum Manajemen Indonesia (FMI) ke-10. Forum Manajemen Indonesia. http://fmi.or.id/downloads/https://www.researchgate.net/publication/341232364_ANALISIS_BUSINESS_SUSTAINABILITY_PADA_PERBANKAN_SYARIAH_DI_INDONESIA

- Ghoniyah, N., & Hartono, S. (2019a). The contribution of Islamic banks towards the achievement of sustainable development goals: The case of Indonesia. Economics and Finance in Indonesia, 65(2), 93–110. https://doi.org/10.47291/efi.v65i2.620

- Ghoniyah, N., & Hartono, S. (2019b). THE ROLE OF ISLAMIC CORPORATE GOVERNANCE IN PREVENTING FRAUD. In AICIF 7th (ASEAN Universities International Conference on Islamic Finance). Gontor: UNIDA Gontor Press. https://drive.google.com/file/d/1ZOHlUfMV7je8qyFlfyoQw0Hlr2EqM9Jn/view ATAU https://www.researchgate.net/publication/341232113_THE_ROLE_OF_ISLAMIC_CORPORATE_GOVERNANCE_IN_PREVENTING_FRAUD#fullTextFileContent

- Ghoniyah, N., Mutamimah, & Amilahaq, F. (2020). Minimizing frauds on the Indonesian Islamic banks (pp. 221–225). Atlantis Press. https://doi.org/10.2991/aebmr.k.200410.034

- Ghoniyah, N., & Setyowati, A. R. (2019). Faktor Penentu Penyaluran Kredit Perbankan pada Bank Umum di Indonesia. In Irsan, T., Musdalifah, A., Dio, C. D., Dian, I. A., Ahmad, R., & S. Kom (Eds.), Forum Manajemen Indonesia (FMI) ke-11. Badan Penerbit Fakultas Ekonomi dan Bisnis, Universitas Mulawarman. http://fmi.or.id/downloads/https://www.researchgate.net/publication/341232254_FAKTOR_PENENTU_PENYALURAN_KREDIT_PERBANKAN_PADA_BANK_UMUM_DI_INDONESIA

- Ghozali, I. (2014). Ekonometrika Teori, Konsep, dan Aplikasi dengan IBM SPSS 22. Badan Penerbit Universitas Diponegoro. https://scholar.google.co.id/citations?user=kbmkIQQAAAAJ&hl=en#d=gs_md_cita-d&u=%2Fcitations%3Fview_op%3Dview_citation%26hl%3Den%26user%3DkbmkIQQAAAAJ%26citation_for_view%3DkbmkIQQAAAAJ%3ASIv7DqKytYAC%26tzom%3D-420

- Goaied, M., & Sassi, S. (2011). Financial development, Islamic banking and economic growth: Evidence from MENA region. International Journal of Business and Management Science, 4(2), 105–128. https://papers.ssrn.com/sol3/papers.cfm?Abstract_id=2890991

- Gupta, N., & Mahakud, J. (2020). Ownership, bank size, capitalization and bank performance: Evidence from India. Cogent Economics & Finance, 8, 1808282. https://doi.org/10.1080/23322039.2020.1808282

- Habibullah, M. S., & Eng, Y.-K. (2006). Does financial development cause economic growth? A panel data dynamic analysis for the Asian developing countries. Journal of the Asia Pacific Economy, 11(4), 377–393. https://doi.org/10.1080/13547860600923585

- Haq, R. N. A. (2015). Pengaruh Pembiayaan dan Efisiesi terhadap Profitabilitas Bank Umum Syariah. Pebarnas Review, 1(1), 107-12. http://jurnal.perbanas.id/index.php/JPR/article/download/12/11

- Harahap, S. S. W., & Yusuf, M. (2005). Akuntansi Perbankan Syariah. LPFE-Usakti.

- Idun, -A.-A.-A., Aboagye, A. Q. Q., & Bokpin, G. A. (2020). The effect of bank market power on economic growth in Africa: The role of institutions. Cogent Economics & Finance, 8, 1799481. https://doi.org/10.1080/23322039.2020.1799481

- Indonesian Bankers Association. (2014). Memahami Bisnis Bank Syariah. PT Gramedia Pustaka Utama.

- Indonesian Bankers Association. (2015). Mengelola Bisnis Pembiayaan Bank Syariah. PT Gramedia Pustaka Utama.

- Indriana, D., & Zuhroh, I. (2012). Analisis Kualitas Pembiayaan Perbankan Syariah tahun 2006-2010. Jurnal Ekonomi Pembangunan, 10(2), 121–136. https://doi.org/10.22219/JEP.V10I2.3723

- Janusz, R. (2016). Determinants of the EU sustainable development policy effectiveness. DEA approach. Economic and Environmental Studies, 16(40), 551–576. http://cejsh.icm.edu.pl/cejsh/element/bwmeta1.element.desklight-db730aba-4ce7-4ceb-b0ac-e5a1deb0cb6b

- Jaurino, J., & Wulandari, R. (2017). The effect of Mudharabah and Musyarakah on the profitability of Islamic banks. In The 3rd PIABC (Parahyangan International Accounting and Business Conference. http://journal.unpar.ac.id/index.php/piabc/article/view/2457/2172

- Josephine, O. N., Oladele Akeeb, O., & Makwe Emmanuel, U. (2016). Bank liquidity and economic growth of Nigeria. Research Journal of Finance and Accounting, 7(14), 20-33. https://iiste.org/Journals/index.php/RJFA/article/view/32102

- Kasmir. (2003). Manajemen Perbankan, Edisi 1. PT Raja Grafindo Persada.

- Klein, P.-O., & Weill, L. (2018). Bank profitability and economic growth. BOFIT Discussion Paper No. 15/2018. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3207171

- Kock, N. (2011). Using WarpPLS in e-collaboration studies: Mediating effects, control and second order variables, and algorithm choices. International Journal of ECollaboration, 7(3), 1–13. https://www.igi-global.com/gateway/article/55424

- Law No.10 of 1998 - Amendment to Law No. 7 Yr 1992 concerning Banking, Pub. L. No. 10, The Unitary State of the Republic of Indonesia (Negara Kesatuan Republik Indonesia) (1998). Indonesia: Undang-Undang. The Unitary State of the Republic of Indonesia (Negara Kesatuan Republik Indonesia). http://hukum.unsrat.ac.id/uu/uu_10_98.htm

- Mohammadi, F., Emadzadeh, M., & Ansari, A. (2012). The major determinants of sustainable development in selected Pacific, East and West Asian Countries. University of Isfahan, 39(2), 55–62. https://doi.org/10.22108/IES.2634.15546

- Muhamad. (2016). Manajemen Keuangan Syariah, Analisis Fiqih & Keuangan. UPP STIM YKPN.

- Murerwa, C. B. (2015). Determinants of Banks’ financial performance in developing economies: Evidence from Kenyan Commercial Banks. United States International University. http://erepo.usiu.ac.ke/bitstream/handle/11732/705/DETERMINANTSOFBANKPERFORMANC20715.pdf?sequence=4&isAllowed=y

- Nugroho, Y. (2017). Tujuan Pembangunan Berkelanjutan/SDGs, Memikirkan Mekanisme Pendanaan. Bidang Kajian dan Pengelolaan Isu-isu Sosial, Budaya, dan Ekologi Strategis: Deputi II Kepala Staff Kepresidenan. https://www.sdg2030indonesia.org/an-component/media/upload-book/Yanuar_Nugroho_-_Kantor_Staff_Presiden.pdf

- Paul, D. I., & Uhomoibhi, J. (2012). Solar power generation for ICT and sustainable development in emerging economies. Campus-Wide Information Systems, 29(4), 213–225. https://doi.org/10.1108/10650741211253813

- Pratiwi, D. D. (2012). Pengaruh CAR, BOPO, NPF Dan FDR Terhadap Return On Asset (ROA) Bank Umum Syariah (Studi Kasus Pada Bank Umum Syariah Di Indonesia Tahun 2005 – 2010). Universitas Diponegoro: Semarang. http://eprints.undip.ac.id/35651/1/Skripsi_PRATIWI.pdf

- Purboastuti, N., Anwar, N., & Suryahani, I. (2015). Pengaruh Indikator Utama Perbankan terhadap Pangsa Pasar Perbankan Syariah. JEJAK Jurnal Ekonomi Dan Kebijakan (Journal of Economics and Policy), 8(1), 13-22. https://doi.org/10.15294/jejak.v8i1.3850

- Raimi, L., & Ogunjirin, O. D. (2012). Fast‐tracking sustainable economic growth and development in Nigeria through international migration and remittances. Humanomics, 28(3), 209–219. https://doi.org/10.1108/08288661211258101

- Riyadi, S., & Yulianto, A. (2014). Pengaruh Pembiayaan Bagi Hasil, Pembiayaan Jual Beli, Financing to Deposit Ratio, dan Non Performi ng Financing terhadap Profitabillitas Bank Umum Syariah di Indonesia. Accounting Analysis Journal, 3(4), 466-474. https://doi.org/10.15294/AAJ.V3I4.4208

- Robinson, M. S. (2001). The microfinance revolution, sustainable finance for the poor. World Bank. https://openknowledge.worldbank.org/handle/10986/28956

- Stanny, M., & Czarnecki, A. (2010). Level and determinants of sustainable rural development in the Region of Green Lungs of Poland. In Andrew, F. (Ed.), Rural Areas and Development (pp. 197–212). Institute of Agricultural and Food Economics - Narional Research Institute. European Rural Development Network. https://ageconsearch.umn.edu/record/139802

- Tabash, M. I., & Anagreh, S. (2017). Do Islamic banks contribute to growth of the economy? Evidence from United Aram Emirates (UAE). Banks and Bank System, 12(1), 113–118. https://doi.org/10.21511/bbs.12(1-1).2017.03

- Wang, C., Han, X., Xin, S., Liu, D., Xu, M., Ma, J., & Yu, Y. (2019). An empirical analysis of Denmark’s energy economy and environment and its sustainable development policy. Journal of Sustainable Development, 12(2), 29. https://doi.org/10.5539/jsd.v12n2p29

- Zamzami, Z. Z. (2011). Model Kemitraan dalam Pola Pembiayaan Perkebunan Sawit. Jurnal Paradigma Ekonomika, 1(3), 88-99. http://garuda.ristekdikti.go.id/journal/article/308060