?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The agency problem strikes as an ethical, practical, and economic issue in equal measures. The principal objective of the current research is to trace the nature of the agency conflicts in the family-owned pyramidal business groups of corporate Malaysia and how they affect the firm value. It is argued that the principal͐–principal (PP) conflict is more severe in family-owned business firms. To achieve the objectives of the current study, the GMM and the fixed effect estimates are used. In addition, to find the difference between family-owned firms and family-owned firms in the pyramidal business, we have employed the Mann–Whitney test. The null hypothesis is accepted which indicates that the impact of the PP conflict among family firms is different from those in pyramidal business groups. The final sample of 420 firms listed on the Bursa Malaysia is chosen for the analysis. The results of the current study provide support to the hypothesized results that the PP conflict is severe in family-owned groups and has a significant effect on firm value. The findings of the current study also provide support that the PP conflict is prevalent in Malaysia, supporting the earlier evidence regarding the expropriation of minority shareholders rights reported in the studies carried out on samples of Malaysian non-financial firms. This is also in line with our measure of PP conflict severity, which is high in pyramidal family firms. Overall, the results provided support to the expropriation hypothesis. Thus, the findings of this study also confirm the view that in family-owned Malaysian firms, the ethical dilemmas of wealth expropriations do exist and are more intense in the pyramidal family-owned business structures. Instead of relying on traditional methods, the current study employed a synthetic measure to gauge the PP conflict. The study which is among the pioneer on the expropriation of minority shareholders will be helpful for policymakers, researchers and finance professionals in understanding the issues related to principal-principal conflict, and firm value in family-owned pyramidal business groups of Malaysia.

GEL classfication:

PUBLIC INTEREST STATEMENT

The prime objective of the current research is to trace the nature of agency conflicts in family-owned pyramidal business groups in corporate Malaysia and how they affect firm value. It is argued that the PP conflict is more severe in firms operating under family-owned businesses. The final sample of 420 firms listed on the Bursa Malaysia was chosen for the analysis. The results of the current study provide support to the hypothesized results that the PP conflict is severe in family-owned groups and has a significant effect on firm value. The findings of the current study also confirm that PP conflict is prevalent in Malaysia and support earlier evidence regarding the expropriation of minority SH rights as reported in studies carried out on samples of non-financial Malaysian firms. Instead of relying on traditional methods for measuring PP conflict, the current study employed a synthetic measure to gauge this conflict.

1. Background

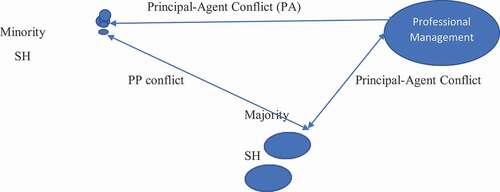

Modern time corporations are characterized by unprecedented wealth, ever-changing global business landscapes and dynamic business potential (Omoush et al., Citation2018). The core structural characteristics of any business corporation are as follows: a) being a separate legal entity with shared ownership, b) have limited liability, c) centralized management under the control of a governing board elected by shareholders (SH), d) transferable ownership (shareholdings), and e) perpetual lifetime. According to Kuan et al. (Citation2017), the key elements that form a firm ownership are the controlling part and the beneficiary part: the former entails the immediate control of organization, whereas the latter claims the earnings. The prime objective of any corporate law is to guide the investors, managers and controllers on how the principle of wealth maximization can be followed in its entirety. One of the core issues linked with wealth maximization is the interest alignment between the owners and managers. According to the agency theory of corporate finance, which is also considered an underpinning theory behind the formulation of the code of corporate governance (CG), there exists a conflict of interest between owners and managers. The agency theory conceptualizes this conflict as principal-agent conflict ().

This principal-agent conflict has been the subject of debate for many decades. However, CG researchers have recently shifted their focus away from the traditional conceptualization of the agency principal-agent conflict to a relatively new conceptualization of agency conflict termed as the PP conflict. The PP conceptualization of the agency theory views ownership concentration (OC) as a reason for another agency conflict between the controlling SH and the minority SH (see ).

The OC in the presence of controllers was considered as a solution to this conflict. Many prior researchers have argued that OC is a proxy of the internal CG mechanism which helps in aligning the interests of ownership and management. However, in the past two decades, many corporate finance researchers (Lozano et al., Citation2016) have shed light on the emerging paradigm of agency conflict namely the PP conflict. In the effort to explain this emerging paradigm, they argued that the traditional conceptualization of conflict between the owners and management which is termed as the principal-agent conflict is only helpful in understanding the conflict of interest between the SH and firm ownership. Whereas in emerging economies, where the corporate legal system is characterized by poor enforcement of laws and ownership is concentrated at multiple levels, this conceptualization is unable to provide a solution for many issues such as the conflict of interest between the majority and minority SH. Thus, we can argue that the total agency cost in any firm could be seen as the sum of agency cost arising from the PA conflict and PP conflict. Agency cost can arise from principal-agent conflict (Grosman et al., Citation2019).

The corporate governance literature in emerging economies is fairly well developed now. After 1997–98 financial crisis and subsequent events of Enron and world .com, ASEAN economies conjectured the necessity of legal reform to govern corporate sector and in doing so they adopted corporate governance based on the Anglo-American capital market form of governance (Hassan et al., Citation2017). But later because of the idiosyncratic institutional environment, researchers emphasized that convergence of emerging economies corporate governance system with those of Anglo-Americans is not necessary (Rodriguez et al., Citation2016). Ownership concentration in emerging economies like developed one plays a significant role in mitigating traditional principal-agent conflict, but it asks researcher to reshape agency theory for emerging issue of Principal–Principal conflict.

Conventional researchers carry out their studies on corporate governance based on the assumption that ownership is dispersed. In contrast, contemporary literatures on corporate governance (Dhar et al., Citation2018; Meyer & Peng, Citation2016) indicated that ownership concentration and poor legal protection in developing countries are the key drivers of the principal-principal conflict. Suggestions for resolving the issue of minority shareholder expropriation are different from those recommended for the principal-agent model (Hamid et al., Citation2016). The principal-principal conflict entails the majority shareholder’s misuse of power and control at the expense of the minority shareholders. This is called expropriation as suggested by Dinh and Calabrò (Citation2019) whereby the minority shareholders have to bear the brunt of poor investments, low firm valuations, assets channeling to subsidiaries as well as low or high dividend payments. Thus, the present study has tried to

2. Literature review

2.1. PP conflict

PP conflicts are described as the collision between two segments of SH known as the controlling SH and the minority SH (Grosman et al., Citation2019). PP conflict is linked with weak governance (Lozano et al., Citation2016) and poor protection of the minority SH (Dinh & Calabrò, Citation2019). Many recent researchers (Ducassy & Guyot, Citation2017; Lozano et al., Citation2016; Zaini et al., Citation2017) have realized that PA conflict is only helpful in mitigating the conflict between owner and manager in economies with diffused ownership structure and active legal institutions. However, in developing and emerging economies, due to weak legal institutions and poor enforcement of property rights, the major conflict is between the majority shareholder and minority shareholder. According to Kuan et al. (Citation2017), PP conflict is common in firms of which ownership and control are in the hands of powerful controllers. They further argued that in such firms, the controller’s excessive powers act as a solution to PA conflicts. However, the low incentive associated with the monitoring of managers leads to another conflict between the majority and minority SH (Basheer, Khan et al., Citation2018).

OC compounded with weak investor protection is the principal cause of PP conflict. OC, because of its existence in almost all parts of the world, has been an interesting phenomenon (Zaini et al., Citation2017). Emerging and transaction economies are countries of which corporate sectors are characterized by high OC and weak institutional support. In the absence of effective CG and strong institutions, OC is seemingly a proxy of internal control. However, this highly concentrated ownership coupled with cross holding leads to the other issue of expropriation of minority SH by controllers. According to Dinh and Calabrò (Citation2019), in contrast to developed economies where ownership is dispersed and legal institutions are strong, emerging economies offer no incentives to controllers to monitor the firms. They further argued that weak external governance mechanism coupled with an ineffective internal control mechanism are supporting the conviction of high private benefits control and exacerbation of minority wealth (Basheer, Waemustafa et al., Citation2018). This indicates that OC fueled by a pyramidical structure lessens the benefit of control over the benefits of expropriation.

Weak external and internal governance leads to severe PP conflict which has a significant impact on economic development (country level) and firm performance (firm level). According to Dinh and Calabrò (Citation2019), there are incentives to expropriation which are high during the crisis. Despite the mass recognition of researchers and the realization of policymakers about the importance of an effective governance mechanism in emerging and developing economies, no significant improvement has been seen. According to Minhas (Citation2019), the very little interest of powerful and politically connected controllers in the improvement of external governance is the main reason for this loss of focus. Minhas (Citation2019) termed it as economic entrenchment. The emerging and developing economies’ political system provided these powerful controllers with enough power to influence public policy.

OC is the sine qua non of PP conflict (Sauerwald & Peng, Citation2013). The agency cost associated with PP conflict arises from the expropriation of minority SH by the controllers or insiders. According to Sauerwald and Peng (Citation2013), there are two reasons why OC is central to PP conflict. Firstly, OC accompanied by weak external institution is a direct cause of PP conflict. Secondly, in emerging economies where the corporate legal system is characterized by weak enforcement, OC is seen as a filler of vacuum left by weak CG. Dinh and Calabrò (Citation2019) argued that the OC of emerging economies is a means of expropriation as no incentives have been given to controllers to control and monitor the firm. Whereas developed countries, that is, the US and the UK give the controlling party enough incentive to monitor firm performance (Basheer, Citation2014). In Hongkong where there is strong investor protection, OC appears to be beneficial to firm performance; on the other hand, OC appears to be detrimental to firm performance in the context of Indonesia where there is weak investor protection.

Levine et al. (Citation2016) claimed that OC is the main reason for the expropriation of minority SH, although in countries where ownership is dispersed, it acts as a proxy of internal governance and helps in the mitigation of traditional principal-agent agency problem. However, in countries with concentrated ownership and powerful controllers, it enables controllers to expropriate minority SH.

2.2. Pyramidal family ownership, PP conflict, and firm value

Family ownership (FO) like OC acts as a proxy of internal governance and helps in aligning the interests of ownership and control. Lee and Barnes (Citation2017) show that family controller in the presence of an independent board has a positive and significant impact on firm performance. However, in family-controlled firms, family control can increase the chances of the expropriation of minority SH and can affect firm value. According to Bloomberg: EXAME magazines (2013), about 80% of Southeast Asian companies with a revenue of 1 USD billion or more are owned by controlling families (Bjornberg et al., Citation2014). Levine et al. (Citation2016) in their vintage paper showed that except for Japan, all east Asian companies have powerful controllers with significant shareholdings.

According to Hrnjic et al. (Citation2019), many companies in numerous countries are under the control of a sole individual or family business. The pyramid structure which organizes firm ownership is typically employed in East Asia, Western Europe, and Latin America. According to researcher, companies in East Asia including Malaysia enhance their control via the pyramidal structure and cross-holdings. The pyramidal structure aims to separate cash flows from voting rights.

The pyramid structure as a tool for maintaining company control devoid of any majority stock ownership. The controlling shareholder is the one who controls the management. The authors’ view of the minority shareholder is different from that who indicated that the minority shareholders, that is, the company’s “working control” play a crucial role of mending any significant mistakes made by the majority shareholders. Nevertheless, it is difficult to sustain minority control particularly in small companies with very few stockholders. Larger companies have wider stock distributions which make it harder to remove a controlling minority.

Family control coupled with a pyramid structure appears as the most prevalent form of organizational structure in East Asian economies Dinh and Calabrò (Citation2019). According to Dinh and Calabrò (Citation2019), the identity of the controllers has a significant relationship with PP conflict. Therefore, we are analyzing whether the family-controlled firms have any relations with the PP conflicts. Levine et al. (Citation2016) indicate that family as a controlling shareholder would set their priority on top of the other shareholder’s priority. Furthermore, the family may implement strategies that would give them benefit as they have large voting power and frequent involvement in management which can sometimes negatively affect the firm’s performance. According to Dinh and Calabrò (Citation2019), the identity of the controllers has a significant relationship with PP conflict. Therefore, we are analyzing whether the family-controlled firms have any relations with the PP conflict.

In most parts of the worlds and especially in emerging and developing economies such as south-east Asian countries, the OC coupled with FO has both formal and informal control over the CG mechanisms. According to Miller (Citation2018), OC in the form of FO reduces the agency cost by aligning the interest of the owners and the managers. The findings are consistent with the proposition of Miller (Citation2018) which found that FO among Fortune 500 firms is a key determinant of performance. However, the expropriation hypothesis views FO as a source of the expropriation of minority SH. Many prior studies (Kuan et al., Citation2017; Sauerwald & Peng, Citation2013) have argued that the expropriation of minority SH is higher than non-family firms.

Family-owned companies are common in Asia particularly in China, Singapore, Hong Kong, Taiwan and Australia. Studies have proven that these family-owned companies demonstrate commendable performance. A review of empirical studies carried out on Malaysian firms between 1999 and 2005 by Sukmadilaga and Ghani (Citation2019) to conclude that family-owned firms have higher equity returns than their non-family-owned counterparts. Hence, family-owned firms positively affect the firms’ performance. Family-owned firms contribute more than half of the country’s GDP.

The affiliation of family firms in a family group makes the expropriation of the minority SH easier and less expensive (Kuan et al., Citation2017). Rahman and Mansor (Citation2018) claimed group affiliation as one of the reasons for expropriation. Copious prior researchers (Kuan et al., Citation2017; Lozano et al., Citation2016) considered expropriation of minority SH as an antecedent of PP conflict. According to Rahman and Mansor (Citation2018), expropriation is a process of gaining self-interest or maximizing self-welfare via the abuse of power or control that one has in the company. Authors concluded expropriation as a value destruction activity; they further argued that it leads the companies to poor financial management. Rahman and Mansor (Citation2018) studied the expropriation of minority SH by the majority SH in East Asian listed firms and argued that expropriation happens in many forms but two of the most prevalent are tunneling and propping in the earlier transfer of resources which occur from a smaller firm to a larger firm while in the later stage it happens from a larger firm to a smaller firm in a pyramidical ownership structure (Hamid et al., Citation2016). Related party transaction (RPT) is another mechanism in which insiders try to expropriate the interests of outside SH via self-dealings (Hamid et al., Citation2016). Ariff and Hashim (Citation2013) argued that RPT, which is a business deal of agreement between two sister concerns or related firms, is common in Malaysia. However, the Asian financial crisis in 1997 revealed that these related party transactions in Malaysia are value destructive (Ariff & Hashim, Citation2013).

2.3. Ownership concentration in Malaysia

One of the main features of the corporate sector in Malaysia is the high level of OC and involvement in managerial decisions (Zaini et al., Citation2017). An earlier study by Janang et al. (Citation2018) indicated that the Malaysian ownership structure is highly concentrated. Manurung and Kusumah (Citation2017) stated that the average shareholding of the 10 largest firms out of the 150 Malaysian Bursa listed firms was 63.52 with a lower range of 20.04. Meanwhile, managerial ownership was at 9.95% which showed a decreasing trend from the prior findings (24%). This indicates that ownership in the Malaysian corporate sector is highly concentrated, and that companies are under the control of powerful controllers which can direct managers to peruse his/her self-interest at the cost of minority SH.

In the context of East Asian countries, Malaysia is among those with the highest ownership concentration in which the top five shareholders owned 58.8% of outstanding shares in 1998 alone and 62% between 1996 and 2000. Author reported that 96.76% of companies in Malaysia possess high ownership concentrations. In such environment, most of the public-listed firms are under the control of major shareholders or primary owners. The majority of the Malaysian owners control their companies via indirect shareholdings of a chain of private companies. This means that direct shareholdings access alone is not a good indicator of the owners’ actual shareholdings because the impact of indirect shareholdings greatly surpasses that of direct shareholdings given the preference of the owners to conceal their true ownership via indirect shareholdings. As such, this present study ascertains the actual owners of companies manually, that is, by considering the accumulation of the company owner’s direct and indirect shareholdings.

Furthermore, in Malaysia, this concentrated ownership is also compounded by cross holdings (Zaini et al., Citation2017). According to Rahman and Mansor (Citation2018), about one-fourth of the Malaysian corporate sector is being controlled by 10 families and recently, Al-Jaifi (Citation2017) argued that around 55% of the corporations are in control of the controllers and among them in the majority the families are controllers. Thus, it is interesting to revisit the agency conflict in the non-financial sector of Malaysia.

3. Methodology

This study used both static and dynamic panel data analysis. The study basically employs panel data analytical tools to achieve the set goals of the research. The choice of panel data approach is informed by a number of methodological advantages it offers. For example, Etebu (Citation2016) postulated that panel data allow for the exploration of many effects that are otherwise unidentifiable using cross-section and time series data. However, it is important to note that panel longitudinal data give room for the examination of crucial researchable questions that cannot be covered or catered using time series or cross-section data (Brooks, Citation2019). The panel data analysis is the most suitable for capturing the variations of the performance indicators over time. Similarly, it controls the individual country-specific heterogeneity as well as the changes in the countries’ operating environment as applicable in this study.

Another concern regarding our panel model is the issue of endogeneity. This two-way directional relationship is not accounted for in the FE models. Endogeneity could also arise from the deleted variables detected by the error term. The FE method employed in this study can address the unobservable variables as long as they remain time-invariant (Imai & Kim, Citation2019). Conversely, time-variant factors would require an estimation methodology that would be able to control the simultaneity drivers. This study also employed the Generalized Method of Moments (GMM) which, firstly, allowed us to approximate a dynamic model in which the lagged dependent variable is located on the right because the off-balance sheet activities tend to be impacted—other than the other variables—by activities in the period prior. Secondly, the method used lagged values of explanatory variables in both level and differences, to implement the prospective endogenous variables.

The panel data method promotes the observation polling into minor cross-sectional units across several time or period intervals. This method allows for more meticulous, wide-ranging, and genuine results which are unattainable using other basic analysis like the time series or cross-section analysis (Basheer et al., Citation2019). Below is the general form of the panel model:

in our case, as our sample is spread over 5 years from 2013 to 2017 and the total number of family firms is 420, therefore

i = 1, … … … … … … … … .420=1, … … … … … … …, 5

and the total number of family firms in the pyramidal structures are identified as 218; therefore, in the second case

i = 1, … … … … … … … … .218=1, … … … … … … …, 5

The error vector is given by

wherethe individual is each industrial companies’ effect and

is the normal distribution error.

Having a dynamic specification of our model besides the conventional static FE models is useful to account for the autocorrelation that arose from using the lagged dependent variable at the right-hand side. The dynamic model is specified as follows:

whereas is one period lagged FV,

includes strictly exogenous regressors,

includes endogenous regressors, all of which may be correlated with

, the unobserved individual effect. First-differencing the equation removes the

and the associated omitted-variable bias.Footnote1

For certain models, the AR (2) in GMM difference captures the occurrence of second-order serial correlation. In such cases, the models are re-estimated by means of the system GMM, which employs the lagged values of the explanatory variables in both levels and differences, to implement the possible endogenous variables. The system GMM estimator has been proven to have a better performance than the initial differenced GMM estimator in the Monte Carlo simulations where there was a high persistence among the variables (Bjorvatn & Farzanegan, Citation2013).

3.1. Measuring the severity of the PP conflict

In Malaysia (Downs et al., Citation2016) and other East Asian countries (Habib et al., Citation2017), individual-related party transactions or those in combination of loan guarantee and labor redundancy (as a unique measure of the costs of political control) have been studied as a measure of expropriation of minority SH. However, Ducassy and Guyot (Citation2017) in their study on a sample of European firms have constructed a synthetic measure of the severity of the PP conflict. In doing so, they included a set of variables which are shown to be linked to the severity of agency problems. Using the factor loading of these variables, they measured the severity of PP conflict in Malaysia and subsequently multiplied the dummy variable of OC that they construed as a variable of PP conflict. Following the study of Ducassy and Guyot (Citation2017), we used the principal factor analysis to construct the PP conflict and to gauge its severity; the score is multiplied by the mean of the OC. The means of the variables used in the construction of the severity of the conflict are shown in .

Table 1. Means of the variables used in the principal factor analysis

The values in the table indicate that 67% of Malaysian family firms are being controlled by the controllers and almost 52% are being controlled by the controlling owing 10% or more shares. The correlation of these tables is shown in . All the variables except for dividend are significantly and positively correlated whereas the dividend is significantly and negatively correlated with each variable.

Table 2. Correlation between the variables used in the principal factor analysis

In , the results of the factor analysis obtained through the tetrachoric correlation are reported. We find the eigenvalue of one factor of both the family-owned firms and family-owned business structures to be more than one. According to Ducassy and Guyot (Citation2017), the threshold value is set as 1. As the factor loadings of all the factors were above the threshold value and based on the recommendation, all the factors were hence included in the final analysis.

Table 3. Factor scores of the variables used in the principal factor analysis

The final analysis in measuring the PP conflict entails measuring its severity. Based on the recommendations of Ducassy and Guyot (Citation2017), we constructed a dummy which gives equally to zero if the OC of a firm in the sample is less than or equal to 20%. For the computation of the severity of the PP conflict, we multiplied the value of the OC of the firms by more than 20% with the factor scores shown in . The results in confirm the severity of the PP conflict as the mean values of each year is higher than the highest mean values reported by Ducassy and Guyot (Citation2017). The results also provided support to our proposition that the PP conflict is more severe in family-owned pyramidal structures.

Table 4. The annual value of the severity of PP Conflict

4. Data analysis and research findings

4.1. Descriptive analysis

The descriptive statistics of the study variables are provided in . The sample’s general characteristics are revealed by presenting the minimum, maximum, mean and standard deviations derived from the 2013 to 2017 unbalanced panel data.

Table 5. Descriptive statistics

4.2. Correlation analysis

An examination is carried out on the bivariate correlations between the explanatory variables to determine the highly correlated independent variables that lead to the emergence of multicollinearity. The Pearson correlation matrix which measures the study variables’ degree of relationship is shown in . The relationship between ROA and Tobin’s Q showed the highest correlation coefficient with a value of 0.830.

Table 6. Correlation analysis

Generally, the panel data models can be categorized into two types, that is, static and dynamic. The major difference between these two models is that the static model does not contain any lagged dependent variable and that they are more advanced and robust than a static model. In the following section, we discuss these two models in further detail. The fixed effect model is a model that shows the difference in intercepts for different entities with constant slope across entities and time. It can be a one-way entity fixed effect, a one-way time fixed effect, or a two-way fixed effect (entity and time) (Minviel & Latruffe, Citation2017). The most often used methods are the Least Square Dummy Variable Estimator (LSDV) for a small amount of entities and the Fixed Effect Estimators (FEE) for large amount of entities (Minviel & Latruffe, Citation2017).

For the selection of the most appropriate estimates, we used several diagnostic tests (see ). Firstly, the White Heteroscedasticity test was used to capture the heteroscedasticity issues in our aggregate model.

Table 7. Various tests to determine the most appropriate panel data estimates for the aggregate model

The Bresuch Pagan LM test was used to decide between the pooled OLS and Random effects estimations. The test examines whether the pooled OLS method yields a BLUE estimator that is free from autocorrelation, meaning that the cross-sections’ specific term is equal to zero. The LM test results presented in postulate that the random effects model is preferred over the pooled OLS. The next step is to choose between the fixed and random effects model. In this regard, the Hausman specification test is used to compare the fixed effect estimator µ1 with the random effect estimator µ2 (Smith, Citation2019). The null hypothesis is that estimator µ2 is an efficient and unbiased estimator of the true parameters. If this is the case, there should be no systematic difference between the two estimators. The results in imply the rejection of the null hypothesis and that the fixed effects model is favored. The Arellano–Bond test for zero autocorrelation is estimated in the GMM analysis of the work and the results are reflected in the following table. We tested the cross-sectional dependence for each model using the Pearson test. The test results show that cross-sectional dependence exists between the cross-sections. With balanced panel data sets, we can use the Feasible Generalised Least Squares (FGLS) and the Panel Corrected Standard Error (PCSE). But since our panel data sets are unbalanced, we used the robust and clustering option for every model. We clustered the data across banks (Kouassi & Setlhare, Citation2016).

4.3. Analysis

The econometric analysis began with the panel dataset pooling and estimation using the OLS regression. However, OLS disregards the data’s panel structure and the countries’ heterogeneities, whereby all the observations are treated as a single sample hence yielding an estimator that is biased and unreliable. The pooled OLS was found to be an unsuitable estimation method by the Breusch–Pagan Lagrange multiplier test. The panel fixed effect (FE) was used to fix the biasness produced in the pooled OLS estimator by taking into account each country’s distinct nature and the control for the unobserved heterogeneity which is persistent over time and linked to the dependent variable (Brooks, Citation2019). When used on a model with a lagged dependent variable, the pooled OLS begins to develop correlations with certain individual effects which are potentially residual-prone.

Consequently, it produces inconsonance and biased results because of the correlation and individual specific effects. Therefore, the individual specific effects and their correlation with the lagged variable set a limitation for the pooled OLS. The fixed effect method offers a solution for the individual effect problem. However, the correlation with the lagged-dependent variable with residuals remains an issue. Erban and Chapman (Citation2019) argued that while fixed effect provides a solution for the individual effect problem, for idiosyncratic errors it is highly sensitive to serial correlation, normality, and heteroscedasticity. Erban and Chapman (Citation2019) further argued that random effects also suffer from correlation issue which leads to inconstancy and biases. Thus, we can argue that in order to solve the endogeneity issue, more advanced panel data techniques such as GMM can be used.

Issues like the correlation between the lagged-dependent variable and residual, endogeneity and unobserved heterogeneity raise doubts about the robustness of the fixed and random effect models. The GMM estimation, derived by Peters and Taylor (Citation2017), offers a solution to the issues of fixed and random effect models. It is a dynamic and single left-hand side variable which depends on its past realizations. The estimation developed by Peters and Taylor (Citation2017) is termed as difference GMM estimator as it uses all the accessible lagged values of the dependent variable and exogenous regressors. It uses the lagged values of the exogenous regressor as instruments.

Meanwhile, Peters and Taylor (Citation2017) criticized the GMM difference estimator and claimed it to be an inefficient and weak instrument. To support their criticism on the difference GMM estimator, they developed a system GMM estimator which along with the lagged difference includes the lagged levels. Abrigo and Love (Citation2016) argued that both the GMM difference and the GMM system offer solutions to problems with the fixed and random effect models. However, Abrigo and Love (Citation2016) had earlier argued that compared to the difference GMM estimator, the system GMM estimator yields more reliable and accurate solutions. The advantage of panel data analysis over other techniques include the reduction of collinearity among the independent variables and the increased number of observations and degree of freedom; improved efficiency for the econometrics estimation while taking into account the heterogeneity of the variables as well as their suitability for studying dynamics changes in a firm or industry (Brooks, Citation2019).

The results of the GMM and the fixed effect of EquationEquation 3(3)

(3) are given in Table 87. For firm value, we used the two measures, namely, Tobin’s Q and return on asset (ROA). The results of the study as reported in reveal the fact that PP conflict has a negative relationship with firm value in both measures. The results provide support to the expropriation hypothesis, which argues that family firms owned by controllers owing more than 20% stakes are more vulnerable to the expropriation of minority SH wealth (Liew et al., Citation2015).

Table 8. The regression results of Equationequation 3(3)

(3) (Family-owned Firms)

FO also has a negative relationship with firm value, and the findings are consistent with the prior findings of Yoong et al. (Citation2015). The negative relationship between FO and firm value rejects the traditional conceptualization of the agency theory and confirms the presence of PP conflict. The control variables of the current study also have a significant relationship with firm value.

If our GMM model is an identified model, meaning that there is only one instrument per each endogenous variable. In this case, we cannot test for the over identification restrictions and we do not need to report the Sargan test (Sargan, Citation1958). Since we are estimating a dynamic model that incorporates endogenous variables; thus, this model is strongly believed to contain autoregressive errors’ structure. Having signs of autocorrelations means that the used instruments are not valid and the GMM estimator is no longer consistent. We report GMM test of autocorrelation that examines whether the used instruments in the differenced equation are correlated with the error term or not. The test has a null hypothesis of no autocorrelation. Two statistics are reported under this test, the test for AR (1) process in first differences that is expected to reject the null hypothesis since. The second result, which is more important, examines AR (2) in first difference and detects the second-order serial correlation. In general, the rule of thumb in the lag length selection is to keep the number of instruments less than the number of groups and to accept the null hypotheses of the two previously explained post-estimation tests that ensure that the used instruments are valid and exogenous.

The results of the family-owned pyramidal business structures are shown in . The P-P conflict and family ownership both are in negative and significant relationship with the value of the Malaysian family-owned pyramidal business structures. In addition, the significant value of lagged coefficient is providing support to the notion that the GMM is a robust measure as it basically indicates that the loss of observation during GMM estimation had no effect on the findings. From the significant coefficient one should take into account the persistency of firm value while explaining the impact of the PP conflict and family ownership.

Table 9. The regression results of Equationequation 3(3)

(3) (Family-Owned Pyramidal Business Structures)

The Mann–Whitney test is used to compare the results of family firms and family firms in pyramidal business groups. The results simply accept the null hypothesis that there exists a significant difference between family firms and family-owned firms in pyramidal structures hence confirming the null hypothesis.

5. Conclusion

The CG literature in emerging economies is fairly well developed now. After the 1997–98 financial crisis and subsequent events of Enron and world.com, ASEAN economies conjectured the necessity of legal reforms to govern the corporate sector. In doing so, they adopted the Anglo-American capital market form of CG. However, due to the idiosyncratic institutional environment, researchers later emphasized that the convergence of the emerging economies’ CG system with those of the Anglo-American is not necessary. OC in emerging economies, like in the developed ones, plays a significant role in mitigating traditional principal-agent conflict, but it demands the researcher to reshape the agency theory for emerging PP conflict issues (Lozano et al., Citation2016). In fact, for the past three decades, CG practices have been deemed as a solution for traditional PA conflict, and OC as an internal mechanism in assuaging owner-manager conflict (Lozano et al., Citation2016). Hence, the new stream of research is a prerequisite in exploring the ambiguous roles of OC in mitigating and exacerbating agency problems (Sheikh & Qureshi, Citation2017).

Due to the traditional conceptualization of the agency theory, the principal-agent conflict has been the subject of debate for many decades. However, many recent researchers (Kuan et al., Citation2017; Lozano et al., Citation2016; Renders & Gaeremynck, Citation2012) on CG have shifted their focus away from the traditional conceptualization of the agency principal-agent conflict to a relatively new conceptualization of agency conflict which is termed as PP (PP) conflict. The PP conceptualization of the agency theory views OC as a reason for another agency conflict between the controlling SH and minority SH.

The prime objective of the current research is to trace the nature of agency conflicts in family-owned pyramidal business groups in corporate Malaysia and how they affect firm value. It is argued that the PP conflict is more severe in firms operating under family-owned businesses. The final sample of 420 firms listed on the Bursa Malaysia was chosen for the analysis. The results of the current study provide support to the hypothesized results that the PP conflict is severe in family-owned groups and has a significant effect on firm value. The findings of the current study also confirm that PP conflict is prevalent in Malaysia and support earlier evidence regarding the expropriation of minority SH rights as reported in studies carried out on samples of non-financial Malaysian firms. Instead of relying on traditional methods for measuring PP conflict, the current study employed a synthetic measure to gauge this conflict.

The GMM and fixed effect estimates are used to achieve the research objectives. The results of the current study show agreement with the expropriation hypothesis. The two-sample Wilcoxon rank-sum (Mann–Whitney) test was used to determine the difference between family-owned firms and family-owned firms in pyramidal business. The null hypothesis is accepted which indicates that the impact of PP conflict on family firms is different from that of the pyramidal business groups. This is also in line with our measure of PP conflict severity, which is high in pyramidal family firms. Overall, the results provided support to the expropriation hypothesis. Thus, the findings of this study also confirm the view that in family-owned Malaysian firms, the ethical dilemmas of wealth expropriations do exist and are more intense in the pyramidal family-owned business structures. Having controlling shareholders in a firm could lead to the expropriation of the minority shareholders. Greater controlling power means that the minority shareholders are less protected (Levine et al., Citation2016). In Malaysia, minority shareholder protection is very weak. A controlling shareholder also weakens the board’s ability to make decisions. With concentrated shareholdings, there is a lower possibility of aggressive coups and pressures for the board and management to achieve a better performance. Concentrated ownership has been proven to devaluate a company. The controlling shareholder is predisposed to making self-serving decisions such as making irrational dividend payments and investing in risky projects detrimental for the firm. The study has examined the non-financial family-controlled firms. However, another study with different controlling shareholders such as government is recommended. Similarly, it is recommended to examine the direct and indirect impact of financial decision on the PP conflict and firm value relationship.

Additional information

Funding

Notes on contributors

Muhammad Farhan Basheer

Muhammad Farhan Basheer (PhD) currently affiliated with the Lahore Business School, university of Lahore, Pakistan. Muhammad Farhan does research in Financial Economics. His current projects are ‘Pyramidal ownership and firm performance, Agency Theory, and Entrepreneurial Finance

Shuchi Gupta

Shuchi Gupta (PhD) currently affiliated with the College of Business Administration(Accounting Deptt), University of Hail, KSA. Dr.Shuchi Gupta does research in Accounting & Finance, International Trade, Accounting Information System, Economics, Management.

Rabeeya Raoof

Rabeeya Raoof (PhD) has completed her PhD in Management Sciences from Lahore Business School, University of Lahore (UoL) in 2019. At present, she works as professor in the Lahore Business School, UoL. Her research interest areas are based on economics, entrepreneurship, finance and human resource management. Her current research projects are Social capital, business coping strategies, Pyramidal ownership and entrepreneurial performance.”

Waeibrorheem Waemustafa

Waeibrorheem Waemustafa (PhD), currently affiliated with the College of Business, university of Utara Malaysia. Dr. Waeibrorheem Waemustafa does research in Accounting & Finance, Credit risk in Islamic banking, Theory of gharar, Liquidity risk, Unsystematic risk.

Notes

1. We had tested the deeper lags of FV, but the only significant coefficient was found for the one-period lagged measure. The results are not reported but are available upon request.

References

- Abrigo, M. R., & Love, I. (2016). Estimation of panel vector autoregression in Stata. The Stata Journal, 16(3), 778–18. https://doi.org/10.1177/1536867X1601600314

- Al-Jaifi, H. A. (2017). Ownership concentration, earnings management and stock market liquidity: Evidence from Malaysia. Corporate Governance: The International Journal of Business in Society, 17(3), 490–510. https://doi.org/10.1108/CG-06-2016-0139

- Ariff, A. M., & Hashim, H. (2013). The breadth and depth of related party transactions disclosures. International Journal of Trade, Economics and Finance, 4(6), 388–392. https://doi.org/10.7763/IJTEF.2013.V4.323

- Basheer, M. F. (2014). Impact of corporate governance on corporate cash holdings: An empirical study of firms in manufacturing industry of Pakistan. International Journal of Innovation and Applied Studies, 7(4), 1371.

- Basheer, M. F., Hidthiir, M. H., & Waemustafa, W. (2019). Impact of bank regulatory change and bank specific factors upon off-balance-sheet activities across commercial banks in south Asia. Asian Economic and Financial Review, 9(4), 419

- Basheer, M. F., Khan, S., Hassan, S. G., & Shah, M. H. (2018). The Corporate Governance and Interdependence of Investment and Financing Decisions of Non-Financial Firms in Pakistan. The Journal of Social Sciences Research, 5, 316–323.

- Basheer, M. F., Waemustafa, W., & Ahmad, A. A. (2018). The paradox of managerial ownership and financial decisions of the textile sector: An Asian market perspective. The Journal of Social Sciences Research, 5, 184–190.

- Bjornberg, A., Elstrodt, H.-P., & Pandit, V. (2014). The family business factor in emerging markets. McKinsey Q, 80(90), 70–80.

- Bjorvatn, K., & Farzanegan, M. R. (2013). Demographic transition in resource rich countries: A blessing or a curse? World Development, 45, 337–351. https://doi.org/10.1016/j.worlddev.2013.01.026

- Brooks, C. (2019). Introductory econometrics for finance. Cambridge university press.

- Dhar, S., Kovid, R. K., & Dharwal, M. (2018). Corporate governance, related party transactions and firm performance: A panel data analysis. MUDRA: Journal of Finance and Accounting, 5(2), 1–13.

- Dinh, T. Q., & Calabrò, A. (2019). Asian family firms through corporate governance and institutions: A systematic review of the literature and agenda for future research. International Journal of Management Reviews, 21(1), 50–75. https://doi.org/10.1111/ijmr.12176

- Downs, D. H., Wong, W.-C., & Ong, S. E. (2016). Related party transactions and firm value: Evidence from property markets in Hong Kong, Malaysia and Singapore. The Journal of Real Estate Finance and Economics, 52(4), 408–427. https://doi.org/10.1007/s11146-015-9509-0

- Ducassy, I., & Guyot, A. (2017). Complex ownership structures, corporate governance and firm performance: The French context. Research in International Business and Finance, 39, 291–306. https://doi.org/10.1016/j.ribaf.2016.07.019

- Erban, R., & Chapman, S. J. (2019). Stochastic modelling of reaction–diffusion processes. (Vol. 60). Cambridge University Press.

- Etebu, C. (2016). Impact of stress on employee’s productivity in financial institutions in Nigeria. European Journal of Business and Management, 8(1). 138–142.

- Grosman, A., Aguilera, R. V., & Wright, M. (2019). Lost in translation? Corporate governance, independent boards and blockholder appropriation. Journal of World Business, 54(4), 258–272. https://doi.org/10.1016/j.jwb.2018.09.001

- Habib, A., Muhammadi, A. H., & Jiang, H. (2017). Political connections, related party transactions, and auditor choice: Evidence from Indonesia. Journal of Contemporary Accounting & Economics, 13(1), 1–19. https://doi.org/10.1016/j.jcae.2017.01.004

- Hamid, M. A., Ting, I. W. K., & Kweh, Q. L. (2016). The relationship between corporate governance and expropriation of minority shareholders’ interests. Procedia Economics and Finance, 35, 99–106. https://doi.org/10.1016/S2212-5671(16)00014-9

- Hassan, Y., Hijazi, R., & Naser, K. (2017). Does audit committee substitute or complement other corporate governance mechanisms. Managerial Auditing Journal, 32(7), 658–681. https://doi.org/10.1108/MAJ-08-2016-1423

- Hrnjic, E., Reeb, D. M., & Yeung, B. (2019). Financial Decisions, Behavioral Biases, and Governance in Emerging Markets. In The Oxford Handbook of Management in Emerging Markets (pp. 161). Oxford University Press.

- Imai, K., & Kim, I. S. (2019). When should we use unit fixed effects regression models for causal inference with longitudinal data? American Journal of Political Science, 63(2), 467–490. https://doi.org/10.1111/ajps.12417

- Janang, J. T., Tinggi, M., & Kun, A. (2018). Technical inefficiency effects of corporate governance on government linked companies in Malaysia. International Journal of Business and Society, 19(3), 918–936.

- Kouassi, E., & Setlhare, L. L. (2016). Asymptotic properties of Pesaran’s CD test revisited. Economics Bulletin, 36(4), 2569–2578.

- Kuan, J. S. T. S., Goh, C. F., Tan, O. K., & Salleh, N. M. (2017). Principal-principal conflicts and socioemotional wealth in family firms. International Journal of Economics and Finance, 9(10), 128–135. https://doi.org/10.5539/ijef.v9n10p128

- Lee, K., & Barnes, L. (2017). Corporate governance and performance in Hong Kong founded family firms: Evidence from the Hang Seng composite industry index. The Journal of Developing Areas, 51(1), 401–410. https://doi.org/10.1353/jda.2017.0023

- Levine, R., Lin, C., & Xie, W. (2016). Spare tire? Stock markets, banking crises, and economic recoveries. Journal of Financial Economics, 120(1), 81–101. https://doi.org/10.1016/j.jfineco.2015.05.009

- Liew, K., Lei, Z., & Zhang, L. (2015). Mechanical analysis of functionally graded carbon nanotube reinforced composites: A review. Composite Structures, 120, 90–97. https://doi.org/10.1016/j.compstruct.2014.09.041

- Lozano, M. B., Martínez, B., & Pindado, J. (2016). Corporate governance, ownership and firm value: Drivers of ownership as a good corporate governance mechanism. International Business Review, 25(6), 1333–1343. https://doi.org/10.1016/j.ibusrev.2016.04.005

- Manurung, D. T., & Kusumah, R. W. R. (2017). Effect of corporate governance, financial performance and environmental performance on corporate social responsibility disclosure. International Journal of Arts and Commerce, 6(5), 15–28.

- Meyer, K. E., & Peng, M. W. (2016). Theoretical foundations of emerging economy business research. Journal of International Business Studies, 47(1), 3–22. https://doi.org/10.1057/jibs.2015.34

- Miller, D. (2018). Discussion of “Managing reputation: Evidence from biographies of corporate directors”. Journal of Accounting and Economics, 66(2–3), 470–475. https://doi.org/10.1016/j.jacceco.2018.08.006

- Minhas, R. (2019). Corporate, corporate governance and Institutions: A bibliographical review and agenda in context of asian “family” firms. Our Heritage, 67(10), 1541–1549.

- Minviel, J. J., & Latruffe, L. (2017). Effect of public subsidies on farm technical efficiency: A meta-analysis of empirical results. Applied Economics, 49(2), 213–226. https://doi.org/10.1080/00036846.2016.1194963

- Omoush, K. S., Qirem, R. M., & Hawatmah, Z. M. (2018). The degree of e-business entrepreneurship and long-term sustainability: An institutional perspective. Information Systems and E-business Management, 16(1), 29–56. https://doi.org/10.1007/s10257-017-0340-4

- Peters, R. H., & Taylor, L. A. (2017). Intangible capital and the investment-q relation. Journal of Financial Economics, 123(2), 251–272. https://doi.org/10.1016/j.jfineco.2016.03.011

- Rahman, W. N. W. A., & Mansor, N. (2018). Real earnings management in family group affiliation: A research proposal. International Journal of Accounting, 3(11), 82–96.

- Renders, A., & Gaeremynck, A. (2012). Corporate governance, principal‐principal agency conflicts, and firm value in European listed companies. Corporate Governance: An International Review, 20(2), 125–143. https://doi.org/10.1111/j.1467-8683.2011.00900.x

- Rodriguez, G., Villegas, J., & Cabrera, R. (2016). Corporate governance changes, firm strategy and compensation mechanisms in a privatization context. Management, 29(2), 199–221.

- Sargan, J. D. (1958). The estimation of economic relationships using instrumental variables. Econometrica:Journal of the Econometric Society, 393–415.

- Sauerwald, S., & Peng, M. W. (2013). Informal institutions, shareholder coalitions, and principal–principal conflicts. Asia Pacific Journal of Management, 30(3), 853–870. https://doi.org/10.1007/s10490-012-9312-x

- Sheikh, N. A., & Qureshi, M. A. (2017). Determinants of capital structure of Islamic and conventional commercial banks: Evidence from Pakistan. International Journal of Islamic and Middle Eastern Finance and Management, 10(1), 24–41. https://doi.org/10.1108/IMEFM-10-2015-0119

- Smith, M. (2019). Research methods in accounting. SAGE Publications Limited.

- Sukmadilaga, C., & Ghani, E. K. (2019). Analysis of abnormal operating performance between family owned firms and state owned firms in Indonesia and Malaysia. International Journal of Financial Research, 10(3), 107. https://doi.org/10.5430/ijfr.v10n3p107

- Yoong, L. C., Alfan, E., & Devi, S. S. (2015). Family firms, expropriation and firm value: Evidence from related party transactions in Malaysia. The Journal of Developing Areas, 49(5), 139–152. https://doi.org/10.1353/jda.2015.0048

- Young, M. N., Peng, M. W., Ahlstrom, D., Bruton, G. D., & Jiang, Y. (2008). Corporate governance in emerging economies: A review of the principal–principal perspective. Journal of Management Studies, 45(1), 196–220. https://doi.org/10.1111/j.1467-6486.2007.00752.x

- Zaini, S. M., Sharma, U. P., & Samkin, G. (2017). Impact of ownership structure on level of voluntary disclosure in annual reports: comparison between listed family-controlled and nonfamily-controlled companies in Malaysia. Australian Academy of Accounting and Finance Review, 3(3), 140–155.