?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Two distinct and non-redundant understandings of volatility, as deviation from consistency, exist for a time-series: (1) exhibiting high standard deviation and, closer to the dictionary definition of the term, (2) appearing highly irregular and unpredictable. We find that Bitcoin is a prime example of an asset for which the two concepts of volatility diverge. We show that, historically, Bitcoin combines high Standard Deviation and low Approximate Entropy, relative to Gold and S&P 500. Moreover, subsample analysis for different time-scales (daily, weekly, monthly) shows that lower sampling frequencies drastically reduce the Kurtosis of the distribution of log-returns of Bitcoin. The opposite effect is observed for Gold and S&P 500. These properties suggest that, contrary to the volatility of the two traditional assets, Bitcoin’s high volatility is essentially an intra-day phenomenon that is strongly attenuated for a weekly or monthly time-preference.

PUBLIC INTEREST STATEMENT

This paper nuances the reputation of high volatility of Bitcoin relative to traditional financial assets (Gold and the S&P 500). We show that, although the variations in the price and returns of the cryptocurrency are wider, they are more regular and predictable. Moreover, the volatility of Bitcoin decreases at lower time-frequencies (monthly vs weekly vs daily), whereas it increases in the case of Gold and the S&P 500.

1. Introduction and related work

Owing to its ability to act as an inflation-resistant store of value and a decentralized medium of exchange, Bitcoin has recently reached a market capitalization of $1 trillionFootnote1 and cemented its emergence as a distinct financial asset (Kruckeberg & Scholz, Citation2019). This exponential increase in value has, however, come with a reputation of persistent volatility reflected in indicators based on the standard deviation of Bitcoin’s daily price compared to traditional financial assets (e.g., Gold, S&P 500). This paper challenges and nuances this reputation through the prism of Approximate Entropy.

For both Finance academics (Glantz & Kissell, Citation2014) and practitioners,Footnote2 common measures of price volatility are based on the standard deviation (e.g., in GARCH models dyhrberg) of the price or returns of an asset relative to its simple moving average.

Due to the extreme volatility of their price, Bitcoin and other cryptocurrencies are, heterologically, used as a digital asset rather than currencies. Using a GARCH model, (Dyhrberg, Citation2016) found Bitcoin to possess hedging capabilities that sets the cryptocurrency in between Gold and the US dollar. Katsiampa (Katsiampa, Citation2017) compared different GARCH models for the estimation of the volatility of Bitcoin’s daily price. (Bariviera et al., Citation2017) studied the intra-day (sampling frequency: 5 hours) volatility of Bitcoin, relative to Gold and the Euro and the volatility of Bitcoin was found to be decreasing over time, and its long range memory is not related to market liquidity. Moreover, this behavior across different time-scales of 5 to 12 hours was found to be essentially similar, but no longer time-scales were considered.

These properties limit its use as currency and Bitcoin is typically regarded as a (digital) commodity. It is classified as such by the Commodity Futures Trading Commission (CFTC)Footnote3 and (Shahzad et al., Citation2019) find that it shares “safe-haven” properties with gold, and other commodities against fluctuations in global stock market indices. The fact that the extreme movement upward in the price of the cryptocurrency (e.g., its closing price has increased by 14,414% between 15–09-2014 and 20/05/2021) exclude its use as such, a currency. Our intent is to distinguish these variations from the common parlance and finance notions of volatility.

In this paper, we argue that Bitcoin’s price volatility measured with standard deviation-based indicators has received disproportionate attention when it is only a partial reflection of volatility. Indeed, the standard deviation measures a time series’ dispersion from its average, regardless of the predictability of its deviations. Moreover, the variations in Bitcoin’s price are typically studied intra-day and intra-week (Cf. the “Price Volatility” category of literature in the exhaustive review of Bitcoin research of (Corbet et al., Citation2018)) and its properties for these sampling frequencies are assumed to be inherited by weekly and monthly price variations. Using Approximate Entropy (ApEn) (Pincus, Citation1991) we propose a complementary, non-redundant perspective on Bitcoin’s volatility, relative to two other financial assets, Gold and the S&P 500 Index. Moreover, we study both closing prices and returns for different sampling frequencies (daily, weekly, and monthly) and find drastic changes in the statistical properties and reduction in the volatility of Bitcoin for weekly data, when more traditional assets show the opposite dynamic for longer time-preferences.

The remainder of this paper is organized as follows. Section 2 discusses some common limitations of standard deviation as a measure of volatility, Section 3 describes the data and methods used in this study, and Section 4 presents descriptive statistics for the closing price and returns of the three considered assets. The main contributions of this paper are presented in Section 5 and consist in an analysis of the tail properties and Approximate Entropy of the aforementioned random variables. Finally, Section 6 concludes this paper with a discussion of the implications and limitations of these findings and their potential value to speculators and traders considering Bitcoin as an investment.

2. Standard deviation as a measure of volatility

The Cambridge definition of the word volatile is “likely to change suddenly and unexpectedly, especially by getting worse”. According to (Pincus & Kalman, Citation2004), two distinct and non-redundant forms of deviation from consistency exist for a time-series: (1) exhibiting high standard deviation, and (2) appearing highly irregular or unpredictable, which corresponds to the common understanding of the term. This distinction has important consequences. Standard deviation only measures an extent of deviation from the mean. It does not reflect the suddenness and unexpectedness of these deviations.

Moreover, standard deviation amalgamates positive and negative deviations when, in common parlance, volatility is understood as deviations for the worst. Information theoretic measures, such as Approximate Entropy (ApEn) (Pincus, Citation1991) offer a way to complement these standard deviations by quantifying regularity in a time-series. Additionally, significant increases in the Approximate Entropy of a time-series have been found by (Pincus & Kalman, Citation2004) to foretell major variations in a time-series.

Let us consider the following toy example of two time-series, of mean , consisting of two different permutations of the same set of values in

:

is a perfectly predictable time-series regularly alternating from

to

to

.

is a random permutation of

and is, by all means, more volatile. However, the two time series series show the same standard deviation of

. The regularity of

is, on the other hand, captured by its lower ApEn of

, when

presents an ApEn of

. Despite its perfect regularity, the standard deviation of

could be made arbitrarily larger than that of

by replacing

in the time-series with any large number. One can also very easily generate completely random

time-series of an arbitrarily lower standard deviation than

.

Moreover, for many assets, the distribution of prices and returns is known to exhibit heavy-tailed behavior (Malevergne et al., Citation2005) that is best modeled by a generalized Pareto distribution (Coles, Citation2001), in which empirical moments are dominated by extreme values. This has been shown to be the case for the log-returns of the S&P 500 index (Hajizadeh et al., Citation2012), Gold (Aggarwal & Soenen, Citation1988), and Bitcoin (Lahmiri & Bekiros, Citation2018). Consequently, the second moments of the corresponding random variable may converge slowly (if at all) and the Law of Large Number would require an impractically large number of observations to apply. Thus, measures of volatility based on sample standard deviation may be uninformative. Because it only quantifies the total “amount” of variation from the average, sample standard deviation is also highly sensitive to extreme variations. The very use of the term “standard” deviation assumes that there is such a thing as a representative deviation, which requires these deviations to be somehow regular. A time-series such as would exhibit an empirical standard deviation of

, but this number can decently not be considered a good estimator of the second moment of the underlying random variable.

3. Data and methods

3.1. Data

We use weekly and monthly Bitcoin and gold price data from 17 September 2014 (the earliest listing of Bitcoin on Yahoo Finance) to 16 January 2021 from Yahoo Finance,Footnote4 which represents a total of 6942 daily, 984 weekly, and 231 monthly observations. Log-returns are calculated by taking the natural logarithm of the ratio of two consecutive prices.

Concerning daily price and returns variations, it should be noted that Bitcoin trades 7 days per week, as opposed to Gold and S&P 500 only trading on weekdays. We consider that there is no price movement during the weekend for the two latter assets, thus somehow artificially reducing their volatility/irregularity relative to Bitcoin, which further reinforces our conclusions.

3.2. Methods

3.2.1. Mean excess functions

For a non-negative random variable , with support in

, the excess distribution over a threshold

is defined (Queensley et al., Citation2019; Ghosh & Resnick, Citation2010, 2011) as follows:

Intuitively, its complement measures the likelihood of

exceeding

, given that

has exceeded

. For instance, if

measures a closing price,

is the likelihood of the price gaining

more units, given that it has reached

monetary units so far. The Mean Excess (

) function, also known as the Mean Residual Life function, is the expectation of this distribution for random variables of finite expectations and is defined,

as follows:

Thus, the empirical ME function of a sample of

observations

can be computed by dividing the total amount of excess over a threshold

by the number of observations realizing such excesses, as follows:

The excess distribution and mean are the foundations for peaks over threshold (POT) modeling (Ghosh & Resnick, Citation2010), which fits distributions to data on excesses and has wide applications notably in risk management, actuarial science, and project management. Moreover, they define three classes of random variables whose mean excess functions exhibits crucially different statistical behaviors:

• A decreasing mean excess function is characteristic of thin-tailed random variables with memory. Gaussian or Poisson random variables possess this property.

• A constant mean excess function is characteristic of memorylessness (Feller, Citation1971). Exponential random variables and their discrete analogues, Geometric random variables, notoriously exhibit this property.

• An increasing mean excess function is characteristic of scalable heavy-tailed random variables, among which linear ME functions characterize the Generalized Pareto Distribution class (Embrechts et al., Citation1997), whereas convex ME functions are indicative of log-normality (Cirillo & Taleb, Citation2020). Both classes of random variables can exhibit infinite or slowly converging moments.

Chaotic perturbations are commonly observed at the extremity of plots of empirical ME functions, as a result of finite sample bias, i.e. the fact that points for very high-order statistics in the plot are the result of very few observations. This bias is commonly addressed by discarding points in the plot for very high-order statistics (Ghosh & Resnick, Citation2010).

3.2.2. Maximum to sum ratios

For an order , the convergence of the ratio of the maximum to the sum of exponent

is indicative of the existence of the moment of order

, and if so of the speed of convergence of the empirical moments of order

to its true value, per the Law of Large numbers. Formally, given a sample of

observations

of a positive random variable

, let

be the maximum of order

and

, the sum of order

. We have the following result, following (Bonetti et al., Citation2016; Cirillo & Taleb, Citation2020; Embrechts et al., Citation1997):

Based on the previous equivalence, plots of the Maximum to Sum ratios represent the ratio of the maximum to sum of order as a function of the number of data points for different values of

and indicate a convergence of the moments of order

to a finite value if and only if the ratio converges to zero. The non-convergence of moments, or their very slow convergence (which requires extremely large sample sizes), renders the estimation of statistics such as the Mean, variance/standard deviation, or Kurtosis (respectively, the first, second, and fourth moment) from empirical observations uninformative.

3.2.3. Approximate entropy

Approximate Entropy (ApEn), introduced by (Pincus, Citation1991, 1992; Pincus & Kalman, Citation2004), is a family of information-theoretic statistics quantifying the “extent of randomness” in a continuous-state processes, given a time-series of equally spaced in time observations

, and two parameters

, a positive integer representing the length of successive observations to be compared, and

, a positive real representing a tolerance level. Widely validated and commonly used parameter values for the computation of

are

and

of the Standard Deviation of the considered time-series (Pincus & Kalman, Citation2004). Approximate Entropy assigns a non-negative number

to the time-series, with larger values corresponding to greater randomness or irregularity and smaller values corresponding to more instances of repetitive patterns of variation.

Formally, is computed using the following algorithm:

(1) Compute a sequence of real -dimensional vectors

such that

.

(2) For each , compute

number of

such that

, where

is a distance metric between vectors

and

given by:

.

(3) Compute .

(4) Compute

Thus, measures the logarithmic empirical likelihood that observations that are close (within

) for

successive observations remain close (within the same tolerance

) on the next incremental comparison (Delgado-Bonal & Marshak, Citation2019; Pincus & Huang, Citation1992).

The presence of repetitive patterns of fluctuation in a time-series makes it more predictable than a time series in which such patterns are absent. ApEn reflects the likelihood that similar patterns of observations (within an average distance of ) will not be followed by additional similar observations. Moreover, ApEn has been found to be a useful marker of system stability, with rapid increases foreshadowing significant changes in a time-series (Pincus & Kalman, Citation2004).

An important property of ApEn is that its calculation is model-independent (Pincus & Kalman, Citation2004). It is able to quantify the regularity/predictability of time-series data without making any assumptions concerning the distribution of values and the existence of moments. This property is particularly useful in Finance where for many assets and market indices, the development of models that are able to produce accurate forecasts of future returns or price movements, especially sudden considerable variations, is typically very difficult.

Thus, a lower ApEn reflects a higher likelihood of observing previously observed repetitive patterns and thus a more predictable underlying process. Moreover, following (Lewis & Shedler, Citation1976), we use the coefficients of variation as a normalized measure of dispersion for non-stationary random variables.

4. Descriptive statistics

(), respectively, present descriptive statistics For the distribution of closing prices and log-returns. Though the closing price of Bitcoin presents orders of magnitude higher standard deviation and coefficient of variation than that of Gold and the S&P 500, it is significantly more predictable and presents a lower approximate entropy. Concerning log-returns, the three assets present a roughly similar approximate entropy.

Table 1. Descriptive statistics for closing prices

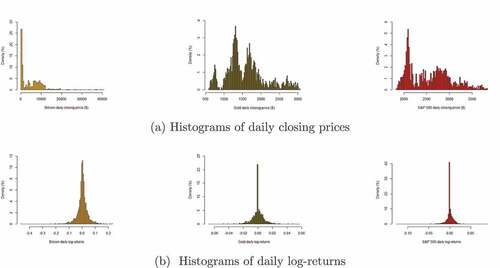

In , we observe that Bitcoin’s closing price presents a long right-tail, when the closing prices of Gold and S&P 500 are thin-tailed. However, for the three assets, the distributions of log-returns present both left and right long tails. Bitcoin standing out with a multi-modal distribution, when Gold and S&P 500 are both strongly unimodal with mode at zero.

Figure 1. Histograms for daily data

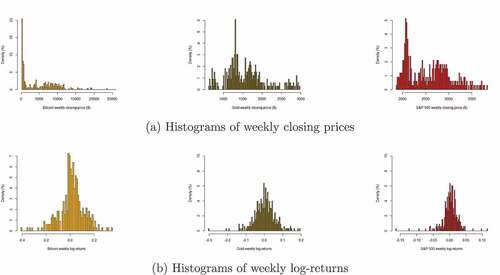

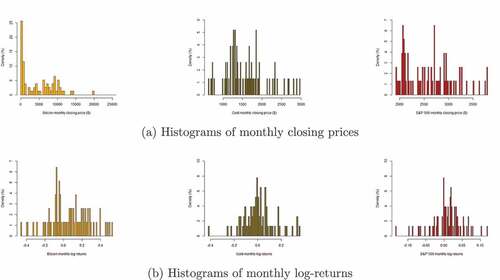

Moreover, Histograms for daily log-returns in , weekly log-returns in , and monthly log-returns in show an important dynamic, for different sampling frequencies. Bitcoin’s log-returns get progressively more thin-tailed, the longer the time-preference.

Figure 2. Histograms for weekly data

Figure 3. Histograms for monthly data

This graphical observation is confirmed by the statistics in . There is a drastic decrease in the kurtosis of both Bitcoin’s closing price and returns, between daily and weekly observations. For monthly returns, this kurtosis is even negative, indicating a platykurtic random variable. In other words, the monthly log-returns of Bitcoin are flatter and show thinner tails than a Gaussian distribution of similar mean and standard deviation (DeCarlo, Citation1997).

Table 2. Descriptive statistics for log-returns

Thus, the distributions of weekly and monthly log-returns of Bitcoin remarkably presents a significantly lower Kurtosis than Gold and S&P 500, in addition to a lower ApEn and coefficient of variation. Thus, over the complete time-horizon of this study, Bitcoin is less volatile than Gold and S&P 500 for a weekly time-preference. We will confirm these results using moving coefficients of variation and ApEn in Section 5.3, and further study the tail properties and convergence of moments of the three assets in Section 5.1 and Section 5.2.

5. Results and discussion

For different sampling frequencies (daily, weekly, and monthly), corresponding to a progressively longer time-preference, we have studied the tail properties of the closing prices and log-returns of Bitcoin, Gold, and the S&P 500 index, using two widely used graphical tools from the extreme value analysis; Mean Excess Function plots, to classify the tail behavior of distributions, and Maximum-to-Sum Ratio plots to study the existence of moments. Moreover, we use the coefficient of variation (standard deviation-to-mean ratio) and approximate entropy to study the volatility and predictability of closing prices and log-returns.

5.1. Tail distributions of closing prices and log-returns

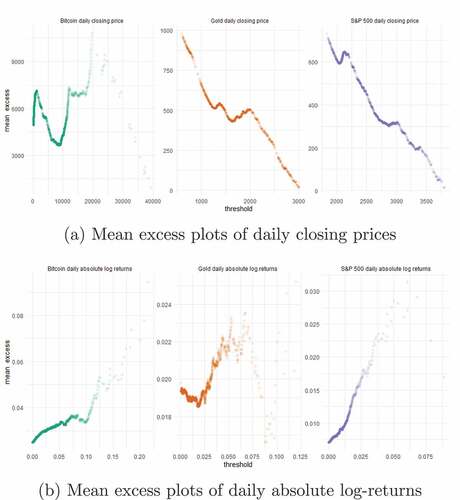

Consistently with the histograms in , for daily data, the closing price of Bitcoin presents an increasing empirical ME function represented in , past the threshold. This indicates that, conditional of having passed that value, the price of Bitcoin is likely to further increase. The daily closing price of Gold and S&P 500 both exhibit decreasing ME functions consistent with thin-tailed distributions. However, the latter figure shows that the absolute log-returns of all three assets have increasing ME functions consistent with heavy-tailed distributions. Interestingly, the absolute log-returns of S&P 500 show an ME function that is even more linear than that of Bitcoin, which is consistent with generalized Pareto behavior.

Figure 4. Mean excess plots for daily data

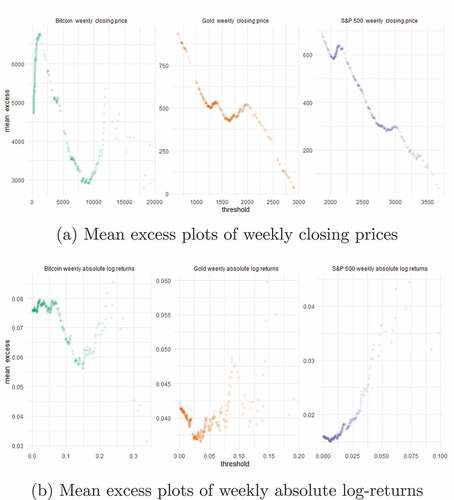

The ME functions for weekly distributions presented in generally present the same behavior as daily, with a notable exception; the ME function of Bitcoin’s weekly absolute return becomes mainly decreasing for this sampling frequency, when that of S&P becomes sharply convex, indicating even more severely heavy-tailed behavior and more disproportionate influence of extrema on moments.

Figure 5. Mean excess plots for weekly data

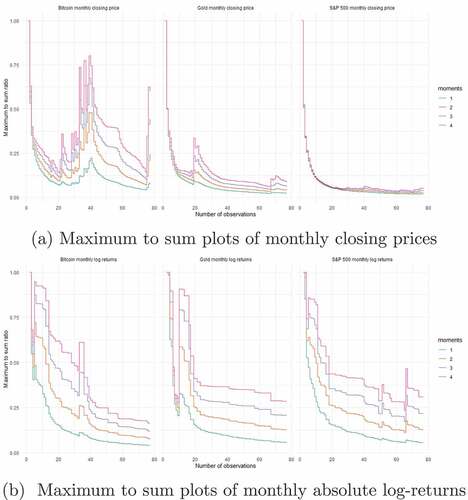

Although there only exist 76 observations of monthly closing prices and returns since September 2014, the ME functions of monthly data represented in see an accentuation of the previous observations. The distribution of Bitcoin’s monthly absolute log-return shows thin-tailed behavior, Gold an ME function that is consistent with an Exponential distribution and S&P 500, an increasing ME function.

Figure 6. Mean excess plots for monthly data

Thus, for the three sampling frequencies, Bitcoin is the only asset that shows heavy-tailed closing prices. However, the log-returns of Bitcoin get progressively more “well-behaved” and thin-tailed for a longer time-preference, when the opposite effect is observed for S&P 500’s, with returns becoming more extremely heavy-tailed. These findings raise the question of the finiteness of moments, particularly of second moments that are commonly used as indicators of volatility, and of the convergence of their empirical estimators. We address this question in the next section.

5.2. The convergence of empirical moments

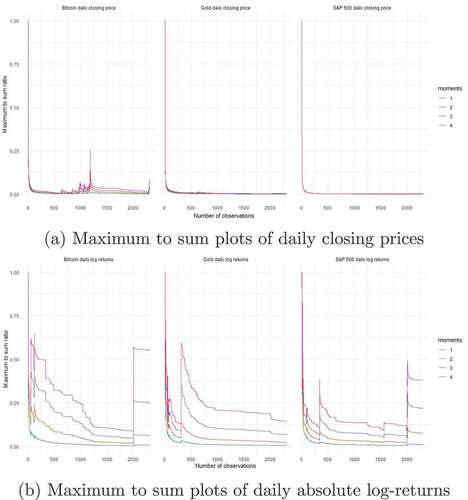

presents the maximum-to-sum ratios of daily closing prices and absolute log-returns. As noted in the previous section, the price of Bitcoin shows heavy-tailed behavior and thus slower convergence of moments compared to the other two assets. Moreover, the absolute log-returns of both Bitcoin and S&P 500 are consistent with generalized Pareto behavior and except for the mean, their higher moments are dominated by extrema and do not converge. Notably, the standard deviations of the log-returns of both assets cannot be reliably estimated from samples.

Figure 7. Maximum to sum plots for daily data

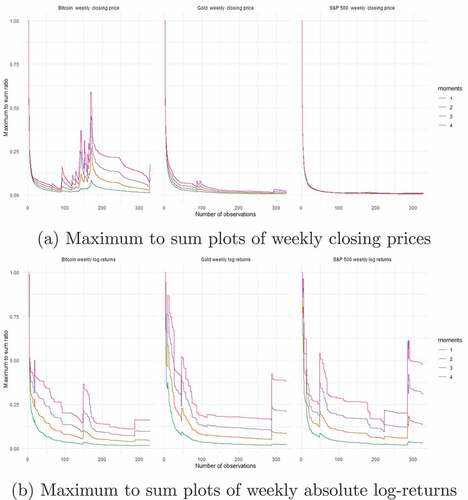

Maximum-to-sum ratios for weekly data in and monthly data in also confirm and precise our observations based on ME functions. A lower sampling frequency makes the log-returns of Bitcoin more thin-tailed and empirical moments convergent to their theoretical value. The variance of absolute log-returns of Bitcoin converges even faster than Gold’s, for weekly and monthly data, and exhibits a behavior consistent with a log-normal random variable with finite variance for these two sampling frequencies. However, the absolute log-returns of Gold and S&P 500 adopt a progressively more Paretian behavior for longer time-preferences, and empirical second moments are non-convergent for weekly and monthly data. These results inform our analysis of volatility, in the next section. Non-convergent second moments for the returns of Gold and S&P 500 mean that the any empirical computation of standard deviation from samples would be dominated by maxima and should be taken as an underestimate of the real standard deviation of the underlying random variable.

Figure 8. Maximum to sum plots for weekly data

Figure 9. Maximum to sum plots for monthly data

5.3. Volatility

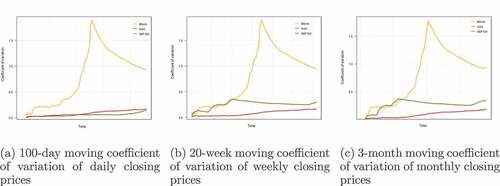

We have computed 100-day, 20-week, and 3-month rolling standard deviations of the closing prices and log-returns for the three assets. Results are, respectively, presented in and . Unsurprisingly, the closing price of Bitcoin shows the highest moving standard deviation among the three assets in . However, we observe a significant increase in the moving standard deviation of Gold for lower sampling frequencies when Bitcoin’s and S&P 500’s remain relatively stable.

Figure 10. Moving coefficients of variation of closing prices. For lower sampling frequencies, sample standard deviation gets progressively higher for Gold, when it remains relatively stable for Bitcoin and S&P 500

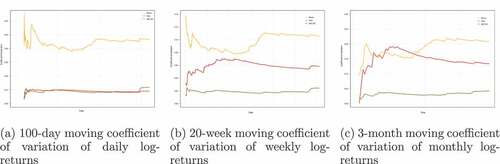

Figure 11. Moving coefficient of variation of log-returns. For lower sampling frequencies, sample standard deviation gets progressively higher for S&P 500, even exceeding Bitcoin’s for monthly log-returns, when it remains stable for Bitcoin and Gold

The same increase is observed concerning the standard deviations of log-returns, with S&P 500 taking the stead of Gold, while Bitcoin and Gold maintain stable standard deviation for lower sampling frequencies. Remarkably, the monthly log-returns of S&P 500 show an even higher rolling standard deviation than Bitcoin’s, for several months. Furthermore, this high volatility of monthly S&P 500 log-returns is likely underestimate, due to the slower convergence of this random variables empirical second moments (relative to Bitcoin’s and Gold), discussed in Section 5.2 and summarized in .

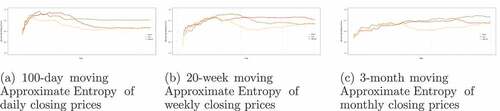

Given the non-convergence of empirical second moments, as well as the inherent limitations of standard deviation, discussed in Section 2, we have complemented our analysis of the three assets’ volatility by computing 100-day, 20-week, and 3-month rolling Approximate Entropy of their closing prices and log-returns. Results are, respectively, presented in and . Our main finding is that Bitcoin’s closing price shows a significantly lower moving ApEn than Gold and S&P 500 for all sampling frequencies. Moreover, Bitcoin’s moving ApEn is stable for different time-preferences, when the moving ApEn of the two other assets is, once again, sensitive to the change in the time-scale. This predictability explains the remarkable success and accuracy of Bitcoin price prediction models based on the Stock-to-Flow ratio (Ammous, Citation2018).

Figure 12. Moving Approximate Entropy of closing prices

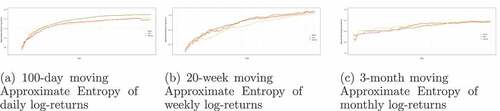

Figure 13. Moving Approximate Entropy of log-returns

Albeit in a less marked way, the log-returns of Bitcoin also exhibit lower moving ApEn than those of the two other assets. The highest discrepancy in moving ApEn is observed for weekly log-returns. These findings, along with our study of Bitcoin tail behavior and standard deviation, indicate that Bitcoin generally offers a high level of predictability, along with high yield, which make it attractive to investors and speculators, but its high standard deviation excludes its use as a currency.

6. Conclusion

The tail behavior and unpredictability of both the closing price and log-returns of the two traditional assets have been shown to be sensitive to the time-scale. As a result of the disproportionate influence of extrema in these heavy-tailed distributions, standard deviations do not converge for the returns of all three variables and can therefore not be accurately estimated from samples. Sample standard deviations should be taken with caution as the Law of Large Number would require an impractically large number of observations to apply. If the daily price volatility of Bitcoin excludes its use as a currency, we have shown that the volatility of both its closing price and log-returns significantly decrease for a weekly and monthly sampling frequencies, the log-returns of Bitcoin presenting even thinner tails and comparable coefficient of deviation to S&P 500 for weekly data.

Moreover, it is commonly accepted that the bull-bear conversion cycles of Bitcoin typically last 4 years and are not particularly influenced by macroeconomics, monetary policy and exchange rate changes, but rather by so-called halving events, i.e. when the reward for mining bitcoin transactions is cut in half. Consequently, indices based on the cost of electricity required for Bitcoin mining have been shown to be robust indicators for bubble-like behavior (Xiong et al., Citation2020). As a reflection of this cyclicity, and using approximate entropy, we have shown that, though the variations in the variation in the price and returns of Bitcoin are wide, they exhibit a higher amount of regularity than those of Gold and the S&P 500.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Nassim Dehouche

Nassim Dehouche holds a Ph.D. and M.Sc. in Operations Research from Paris-Dauphine University, and a State Engineer degree from Houari Boumedienne University of Science and Technology. His research interests revolve around Operations Research, Combinatorial Optimization, and Data Analysis. In a career spanning three continents, he has had the opportunity to undertake or participate in different projects in the fields of Energy, Non-Profit Project Management, Healthcare Management and Transportation.

Notes

1. Pound, J. (2021, February) Bitcoin hits $1 trillion in market value as cryptocurrency surge continues, CNBC. Retrieved on 20/05/2021 from https://www.cnbc.com/2021/02/19/bitcoin-hits-1-trillion-in-market-value-as-cryptocurrency-surge-continues.html

2. Fidelity Learning Center (2020) Standard Deviation, Technical Indicator Guide. https://www.fidelity.com/learning-center/trading-investing/technical-analysis/technical-indicator-guide/standard-deviation on 25/05/2021

3. Commodity Futures Trading Commission (2021) Bitcoin. Retrieved on 20/05/2021 from https://www.cftc.gov/Bitcoin/index.htm

4. Yahoo Finance, Bitcoin-US Dollar quotes. Retrieved on 20/01/2021 from https://finance.yahoo.com/quote/BTC-USD/history?p=BTC-USD

Yahoo Finance, COMEX—COMEX Delayed Price. Retrieved on 20/01/2021 from https://finance.yahoo.com/quote/GC%3DF/history?p=GC%3DF

Yahoo Finance, SNP—SNP Real Time Price. Retrieved on 20/01/2021 from https://finance.yahoo.com/quote/%5EGSPC/history?p=%5EGSPC

References

- Aggarwal, R., & Soenen, L. (1988). The nature and efficiency of the gold market. Journal of Portfolio Management, 14(3), 18–18. https://doi.org/10.3905/jpm.1988.409152

- Ammous, S. (2018). The Bitcoin Standard: The Decentralized Alternative to Central Banking. Wiley.

- Bariviera, A. F., Basgall, M. J., Hasperué, W., & Naiouf, M., et al. (2017). Some stylized facts on the bitcoin market. Physica A, 484, 82–90. https://doi.org/10.1016/j.physa.2017.04.159

- Bonetti, M., Cirillo, P., Musile Tanzi, P., & Trinchero, E., et al. (2016). An analysis of the number of medical malpractice claims and their amounts. PLoS ONE, 11(4), e0153362. https://doi.org/10.1371/journal.pone.0153362

- Cirillo, P., & Taleb, N. N. (2020). Tail risk of contagious diseases. Nature Physics, 16(6), 606–613. https://doi.org/10.1038/s41567-020-0921-x

- Coles, S. (2001). An Introduction to Statistical Modeling of Extreme Values. Springer.

- Corbet, S., Lucey, B., Urquhart, A., & Yarovaya, L., et al. (2018). Cryptocurrencies as a financial asset: A systematic analysis. International Review of Financial Analysis, 62, 182–199. https://doi.org/10.1016/j.irfa.2018.09.003

- DeCarlo, L. T. (1997). On the meaning and use of kurtosis. Psychological Methods, 2(3), 292–307. https://doi.org/10.1037/1082-989X.2.3.292

- Delgado-Bonal, A., & Marshak, A. (2019). Approximate entropy and sample entropy: A comprehensive tutorial. Entropy, 21(6), 541. https://doi.org/10.3390/e21060541

- Dyhrberg, A. H. (2016). Bitcoin, gold and the dollar - A GARCH volatility analysis. Finance Research Letters, 16, 85–92. https://doi.org/10.1016/j.frl.2015.10.008

- Embrechts, P., Mikosch, T., & Kluppelberg, C., et al. (1997). Modelling Extremal Events: For Insurance and Finance. Springer-Verlag.

- Feller, W. (1971). Introduction to Probability Theory and Its Applications (2nd edition, Vol. II). Wiley. Section I.3.

- Ghosh, S., & Resnick, S. (2010). A discussion on mean excess plots. Stochastic Processes and Their Applications, 120(8), 1492–1517. https://doi.org/10.1016/j.spa.2010.04.002

- Ghosh, S., & Resnick, S. (2011). When does the mean excess plot look linear? Stochastic Models, 27(4). https://doi.org/10.1080/15326349.2011.614198

- Glantz, M., & Kissell, R. (2014). Price Volatility in Multi-Asset Risk Modeling(pp. 119–154). Academic Press. https://doi.org/10.1016/B978-0-12-401690-3.00004-4.

- Hajizadeh, E., Seifi, A., Fazel Zarandi, A. H., & Turksen, A. B., et al. (2012). A hybrid modeling approach for forecasting the volatility of S&P 500 index return. Expert Systems with Applications, 39(1), 431–436. https://doi.org/10.1016/j.eswa.2011.07.033

- Katsiampa, P. (2017). Volatility estimation for bitcoin: A comparison of GARCH models. Economics Letters, 158(2017), 3–6. http://dx.doi.org/10.1016/j.econlet.2017.06.023

- Kruckeberg, S., & Scholz, P. (2019). Cryptocurrencies as an Asset Class? In S. Gouette, G. Khaled, and S. Saadi (Eds.), Cryptofinance and Mechanisms of Exchange – The Making of Virtual Currency. (pp.162–179). Springer. 10.1007/9783030307387.030307387

- Lahmiri, S., & Bekiros, S. (2018). Chaos, randomness and multi-fractality in bitcoin market. Chaos, Solitons, and Fractals, 106, 28–34. https://doi.org/10.1016/j.chaos.2017.11.005

- Lewis, P. A. W., & Shedler, G. S. (1976). Statistical analysis of non-stationary series of events in a data base system. IBM Journal of Research and Development, 20(5), 465–482. https://doi.org/10.1147/rd.205.0465

- Malevergne, Y., Pisarenko, V., & Sornette, D., et al. (2005). Empirical distributions of stock returns: Between the stretched exponential and the power law? Quantitative Finance, 5(4), 379–401. https://doi.org/10.1080/14697680500151343

- Pincus, S. M. (1991). Approximate entropy as a measure of system complexity. Proceedings of the national academy of science USA, 188, 2297–2301.

- Pincus, S. M., & Huang, W.-M. (1992). Approximate entropy: statistical properties and applications. Communications in Statistics - Theory and Methods, 21(11), 3061–3077. https://doi.org/10.1080/03610929208830963

- Pincus, S. M., & Kalman, E. (2004). Irregularity, volatility, risk, and financial market time series. Proceedings of the national academy of science USA, 101, 13709–13714. 38.

- Queensley, C., Chukwudum, P. M., & Mung’atu, J. K., et al. (2019). Optimal threshold determination based on the mean excess plot. Communications in Statistics - Theory and Methods. In Press. https://doi.org/10.1080/03610926.2019.1624772

- Shahzad, S., Hussain, S. J., Bouri, E., Roubaud, D., Kristoufek, L., Lucey, B. (2019). Is bitcoin a better safe-haven investment than gold and commodities? International Review of Financial Analysis, 63(C), 322–330. https://doi.org/10.1016/j.irfa.2019.01.002

- Xiong, J., Liu, Q., & Zhao, L. (2020). A new method to verify bitcoin bubbles: based on the production cost. North American Journal of Economics & Finance, 51, 1–17. https://doi.org/10.1016/j.najef.2019.101095