Abstract

Environmental management issues have become a global concern and many governments have developed policies that include environmental regulations. Under this framework, companies have become responding to the demands of all different parties to legitimize their actions. Studies have increased in the field of environmental reporting, but unfortunately, this does not indicate an increase in companies’ awareness of the factors that determine the preparation of sustainability reports and the disclosure of environmental information. This paper uses the qualitative research technique to study the factors influencing environmental information disclosure. A structural analysis approach is applied to establish the interrelationship between the various factors. From our analysis, it has been found that profitability, gender diversity and board independence are the important and critical factors that influence environmental information disclosure. At the end of the research, technical use restrictions of interpretive structural modeling were discussed, and then proposals for developing the research were discussed.

PUBLIC INTEREST STATEMENT

Our research is part of the debate on corporate social responsability. The objective of our research was to use the qualitative research technique to study the factors influencing environmental information disclosure. A structural analysis approach is applied to establish the interrelationship between the various factors. From our analysis, it has been found that profitability, gender diversity and board independence are the important and critical factors that influence environmental information disclosure. Under this framework, companies have become responding to the demands of all different parties to legitimize their actions.

1. Introduction

Many researchers have studied the factors and motives behind the disclosure and disclosure of non-financial information in different contexts, but what has been reached is partial and inconclusive, especially regarding the factors that affect the disclosure of environmental information, which leads to the need for different research methods. (Spence & Gray, Citation2007).

Corporate social responsibility and ethical principles are among the appropriate marketing tools for communication, as social responsibility includes the concept of economic, legal and ethical expansions associated with business (Garoui, Citation2016). The company considers a set of social practices to achieve its goals as a human society by creating trustworthy and honest relationships with clients (Brammer & Pavelin, Citation2008). Perhaps the most important ethical principles are to enhance client confidence and independence, dignity, honesty, and the representation of customer weakness Perhaps the banking sector is also considered one of the companies that has tended towards the principles of social responsibility for banks through concern for stakeholders and cooperation with social institutions.

Although previous studies on corporate social responsibility are few and far between, the banking sector is almost one of the first sectors to participate in corporate social responsibility (Wu & Shen, Citation2013). Numerous studies have proven the social impact hypothesis and the role of social responsibility in achieving a good financial position for companies, and under this framework the continuation of the company becomes linked to the continuity of the company, which is necessary for all stakeholders. (Shen et al., Citation2016). Numerous studies (Nassreddine & Anis, Citation2015) have proven the correlation of the success of the business with the company’s environment and thus the necessity of community participation for the company and the promotion of the interests of all parties as part of the company’s social responsibility, and thus the importance of sustainable participation and disclosure and information that reflects the company’s social practices and falls under this framework (McWilliams & Siegel, Citation2001).Awareness programs in emergency situations such as risks Corona In view of the emerging Corona crisis, the level of participation of institutions varies, so that institutions assume social responsibility according to their capabilities. In this case, the role of banks is not limited to making profits, obtaining returns and financial benefits, but should also focus on environmental, economic and social levels and pay attention to social development. Saudi banks play an important role in the community. The Saudi Bank now has a stronger and more influential social responsibility in the Kingdom of Saudi Arabia, especially after 11 banks announced their support for healthcare and confirmed its important role in reducing the burden of the coronavirus pandemic. The global crisis has provided new positives for Saudi banks. The Saudi Bank announced a donation of around 158.7 million Saudi Riyals to improve public health in Saudi Arabia and respond to COVID-19. The bank’s contribution to supporting the health sector demonstrates its initiative and sense of responsibility. This article studies the concept of corporate social responsibility and identifies and models the key factors for the implementation of the concept of corporate social responsibility. Therefore, we define the problem as follows: “Corporate social responsibility: modeling key factors. These key factors are also categorized based on their motivation and addiction. After reviewing the literature and expert opinion on corporate social responsibility, including bank officials and universities, eight key factors important for the implementation of corporate social responsibility have been identified.

This paper identifies and models factors influencing environmental information disclosure. Therefore, the paper defines the problem as follows: “Corporate social responsibility: modeling key factors. These key factors are also categorized based on their motivation and addiction. After reviewing the literature and expert opinion on corporate social responsibility, including bank officials and universities, six important key factors for the implementation of corporate social responsibility have been identified. The simulation and classification of main factors continues to be done using interpretive structural modeling (ISM) and fuzzy MICMAC. The ISM model is stabilized using the fuzzy MICMAC process, and the main factors are rated according to their power and energy dependency. The Data of factors influencing environmental information disclosure for this study were collected through a questionnaire survey. It turns out that profitability, gender diversity and board independence are the important and critical factors that influence environmental information disclosure.

2. Literature review

2.1. Factors important for the implementation of corporate social responsibility

Issues related to corporate social responsibility have become one of the issues that have increased attention over the past years (Nassreddine etal., Citation2017). The sustainability report is one of the reports that reveal the economic, social and environmental policies of companies and a reference to the company’s performance in the context of sustainable development. Therefore, companies are not only concerned with economic benefits, but also interest Sustainability and social issues (Arnold & Valentin, Citation2013; Suyono & Farooque, Citation2018).

Under this framework, CSR is considered as an effort made by companies to try to reduce negative impacts and thus maximize the economic, social and environmental impact on all stakeholders in order to achieve development and sustainability (Block & Wagner, Citation2014; Liu et al., Citation2017).

Under this framework, there are many factors that affect the disclosure of environmental information for companies(see ).

2.1.1. Sustainability committee

Companies are working to develop sustainability committees because they play a fundamental role in achieving sustainability opportunities and as they are also one of the most important components of corporate governance (Rossi & Tarquinio, Citation2017). The primary role of the sustainability committees is to focus on issues related to corporate social responsibility. Perhaps the company’s commitment to stakeholders makes the creation of a sustainability committee necessary in line with the theory of stakeholders (Ashfaq & Rui, Citation2018; Baraibar-Diez & Odriozola, Citation2019; Salvioni, D. M., & Gennari, F., Citation2019; Tingbani et al., Citation2020)

2.1.2. Industry

Manufacturers share more knowledge about corporate social responsibility than non-manufacturers, according to several reports (Cowen et al. (Citation1987). As a result, if an organization is in an environmentally sensitive sector, it will receive higher CSR scores. Companies in high-risk industries are more likely to issue sustainability reports.

2.1.3. Firm size

The relevance of this variable and its relationship to the disclosure of information relevant to corporate social responsibility has been highlighted in recent literature (“Ezeddine etal., Citation2020). Larger organizations are releasing more sustainability reports using GRI Legendre and Coderre (Citation2013) guidelines, according to several surveys. Jain and Winner (Citation2016) also confirm that larger companies more readily comply with GRI reporting standards.

2.1.4. Profitability

Several studies have shown that businesses with high profits are more likely to reveal details about social responsibilities (Martínez-Ferrero et al., Citation2013). Profitability has a strong and positive impact on corporate decisions to invest in corporate social success, according to Artiash et al. (Citation2010). Furthermore, Branco et al. (Citation2014) found that winning companies are more likely to be entrepreneurial.

Companies that disclose environmental information in the form of symbols usually pay attention to their environmental strategies, environmental goals and environmental protection measures in narrative form, but do not have the corresponding quantitative information in the information reports. Previous studies have pointed out that companies with poor performance tend to disclose environmental information through long reports of complex words and sentences. Legality theory can be used to analyze the contribution of such disclosures to profitability. Legitimacy refers to “within established social norms, values and beliefs, actions taken by a company are considered normal, compliant and commendable”. These are the views or opinions of stakeholders based on the behavior of the company.

Legitimacy refers to “within the framework of established social norms, values and beliefs, actions taken by a company are considered normal, compliant and commendable”, which corresponds to the views or opinions of the parties stakeholders based on company behavior. Legitimacy is very important to build the competitiveness of a business. From a social legitimacy perspective, the company’s external environmental advertising can create a social image that pays attention to the environment and assumes social responsibility. Symbolic disclosure can also mask the laxity of the company’s environmental initiatives, shape a charming social image, then bring resources to the company, solidify relationships with stakeholders and recruit competitive employees. All these elements can ultimately be reflected in the profitability of the company. Therefore, companies can also seek good profitability in the market through the promotion and beautification of the environment.

2.1.5. Gender diversity

Gender diversity is one aspect of board diversity. Recently, gender diversity on the board has become Issues worthy of attention in the company. Some people think that the values of men and women are different in the Responsibility society. Many researchers conducted a meta-analysis study using 160 independent samples of gender differences. They discovered that women are more Men maintain their relationships and are responsible for the needs of others. Several studies report that women are more likely than men to act ethically and avoid organizational policy violation. In addition, it is recommended that women pay more attention to Perceived risks to health and the environment compared to men.

Based on the experience, the United States conducted extensive research to test this association The relationship between gender diversity on the board of directors and company performance. In 2009, the US Securities Regulatory Commission (SEC) issued new disclosure rules requiring listed companies to disclose Do Diversity Consideration when hiring new directors. Despite this trend, previous research results reported in the United States were mixed. Female directors were found to be Neutral or Negative Company Performance.

According to (Garcı´a-meca & Sa´nchez-ballesta, Citation2010), the strength of the board of directors is closely linked to the degree of independence and diversity of its members, and it should be noted that women’s representation on corporate boards of directors is one of the most significant dimensions of corporate governance in many publications and studies of members of the board of directors. Some have argued that women may be more aware of environmental issues and more concerned with reducing perceived risks (Post et al., Citation2011). literature anticipates that female board members will augment the financial performance of organizations by bringing their unique abilities, skills, experiences with them to boards (Kılıç and Kuzey (Citation2016), Boulouta (Citation2013).

2.1.6. Board independence

The independence of managers is closely linked to their expertise and interactions with stakeholders in ensuring the company’s survival and satisfaction of all stakeholders. According to Garoui (Citation2016), getting independent directors helps businesses achieve strategic goals and offers insights that can impact companies’ environmental reports.

3. Methodology

Interpretive structural modeling (ISM) is an immersive computer-assisted learning method that organizes a set of directly related heterogeneous elements into a systematic model. A collection of associations can be displayed in the form of a map using interpretive modeling to highlight the most relevant ideas that define the relationship between groups of elements. Interpretive modeling (ISM) is a method of assembling a multi-level structural form that highlights the most relevant ideas that characterize the relationship between groups of elements. It is focused on the use of experts’ practical experience. Raj et al. (Citation2008) used the ISM approach to figure out how the manufacturing competitive enablers communicate with one another. Raj et al. (Citation2008), to present the most important characteristics related to explanatory modeling: (1) “This method is explanatory, whereby a group judgment decides whether and how the different elements are related. (2) It is also structural, on the basis of the relationship; the general structure is extracted from the complex of complex variables. 3) It’s a modeling technique in which a digraph model is used to represent individual relationships and the overall structure. (4) It aids in imposing order and direction on the system’s dynamic relationships between the various elements. (5) It’s designed to be a community learning process, but it can also be used by individuals. The following steps are significant in the methodology of interpretive modeling, according to (Kannan et al., Citation2009):1. The variables (criteria) that have been considered for the system in question are mentioned. 2. A contextual relationship is formed among the variables listed in step 1 in order to determine which pairs of variables should be examined.3. For variables, a structural self-interaction matrix (SSIM) is formed, which shows pairwise relationships between the variables in the system under consideration. 4. The SSIM is used to build a reachability matrix, which is then tested for transitivity. Contextual relationship slavery is a simple assumption in the ISM. If variable A is related to B and B is related to C, then A must also be related to C. 5. The step 4 usability matrix has been divided into phases. 6. Based on the accessibility matrix’s above relationships, a directed graph is drawn, with transitive connections omitted. Step 7ʹs ISM model, number eight, was updated to look for conceptual discrepancies and make any required changes. ISM strategies rely on expert opinions and are very useful for forming contextual relationships between various types of variables. They are focused on different management techniques, brainstorming, nominal techniques, and so on. The aim of this study is to determine the contextual relationships between enablers and experts from the banking sector in Saudi Arabia and academic experts, they were consulted. Structural self-interaction matrix (SSIM) is an ISM approach that uses expert opinion to determine the contextual relationship between particular enablers. Each variable’s contextual relationship, the presence of a relationship between any two cofactors I and j), and the trend in the relationship in question. Four symbols are used in this paper to show the orientation of the enabler-enabler relationship (i and j): V: i enablers would aid in the attainment of enablers j; A: The j enablers will assist in the achievement of the i enablers; X: The two enabling factors i and j will assist in each other’s fulfillment; and O: the enabling factors i and j are irrelevant.

The matrix of enablers in SSIM (see, ) is translated to the binary digits of the “Primary Accessibility Matrix” (for example, 1 and 0). This conversion is carried out according to the following guidelines:

Table 2. Shows the structural self-interaction matrix (SSIM) for the given problem

If the SSIM entry is V, the reachability matrix entry (i,j) becomes 1 and the reachability matrix entry (j, i) becomes 0.

If the SSIM entry is A, the reachability matrix entry I j) becomes 0 and the reachability matrix entry (j, i) becomes 1.

If the SSIM entry is X, the reachability matrix’s I j) entry becomes 1 and the (j, i) entry becomes 1.

If the entry in the SSIM is O, then (i, j) entry in the reachability matrix becomes 0 and the (j, i) entry becomes 0.

After crossing over is incorporated as mentioned in step 4 in the ISM methodology, a final accessibility matrix for the enablers is obtained as shown in .

The Final Reachability Matrix is created using the Initial Reachability Matrix () once it has been created. The Final Reachability Matrix () is built using basic transitivity logic. If enabler A can be reached from enabler B (B to A) and enabler C can be reached from enabler A (A to C), Then, from enabler B (B to C), enabler C can be reached, and the value from enabler B (B to C), and the values in the Final Reachability Matrix are changed accordingly. The above-mentioned rationale is used to build .

Table 3. Initial reachability matrix

Table 4. Final reachability matrix

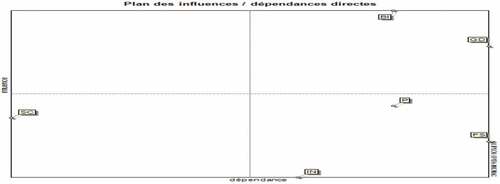

is used to assess each enabler’s driving power and dependability. The row summation of each enabler gives the driving force, which is the number of other enablers it drives, while the column summation gives the dependency, which is the number of other enablers it is reliant on (). Calculating driving power (DP) and determining dependency is illustrated in .

Table 5. Driving power and dependence of enablers

Table 6. Summation of rows and columns

Profitable businesses reveal more social information to the public in order to justify their presence (Haniffa & Cooke, Citation2005). Previous research has assumed a positive relationship between voluntary disclosure and profitability (Kansal et al., Citation2014; Giannarakis, 2014). Gender diversity in boardrooms can affect reporting quality, enforcement, and ethical conduct, according to new research. The presence of women on the board of directors has a positive impact on the standard of sustainability reporting. According to Bear et al. (Citation2010), female board members have a favorable impact on power ratings in corporate social responsibility. Furthermore, having more women on the board improves the board’s effectiveness in managing stakeholders and encourages the implementation of sustainability programs such as climate change reporting.

Only the binary number, 0 or 1, is considered when constructing an ISM model. The relationship is denoted by the symbol 1 if there is correlation, and the relationship is denoted by the number 0 if there is no correlation. However, there is no space for debate about the relationship’s potency. Any relationship between the two elements may be strong, very strong, weak, very weak, or non-existent (Garoui, Citation2016). The indirect and secret relationships between the elements of the structure obtained with the ISM technique are analyzed with MICMAC (which only tracks the direct relationships between these elements).

We asked industry experts and academics to assess the relationship between two critical factors in corporate social responsibility. The relationship between any of the two elements can be very strong, strong, weak, very weak, or no relationship. The Direct Influences Matrix (MID) describes the direct influence relationships between the variables defining the system (Nassreddine & Anis, Citation2015).

Table

Influences are rated from 0 to 3, with the possibility of signaling potential influences

0: No influence

1: low

2: Medium

3: Strong

P: Potential

The MIDP Potential Direct Influences Matrix represents current and potential influences and dependencies between variables. It completes the MID matrix, also taking into account possible relationships in the future(Garoui and Jarboui, Citation2014).

Table

The influences are rated from 0 to 3:

0: No influence

1: low

2: Medium

3: Strong

4. Result and discussion

This table shows the number of elements in the matrix (0,1,2,3,4) as well as the filling rate, which is determined by dividing the number of MID values other than 0 by the total number of elements in the matrix.

If it can be seen that every matrix would converge to a stable state after a certain number of iterations (generally 4 or 5 for a matrix of size 30), it seems fascinating to be able to track the evolution of this stability over time. In the absence of mathematically defined parameters, the number of permutations (bubble sort) needed for each iteration to classify all the variables of the MID matrix in influence and dependence was chosen.

Sum of rows and columns of MID

This table provides information on the row and column sums of the MID matrix

This plan is determined from the MID direct influence matrix.

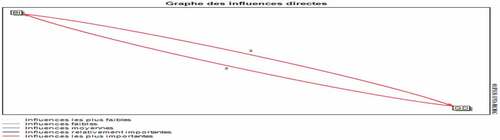

This graph is determined from the MID direct influence matrix.

The primary goal of this research was to identify the critical factors that influence environmental information. It was then followed by the establishment of a formal relationship between them in order to represent the factors’ driving and dependent natures. Interaction with experts in the related field yielded the necessary knowledge. Extra care was taken to ensure that the findings were correct and reliable. The ISM technique has been found to be effective in modeling these variables.

On similar problems, researchers such as Mannan et al. (Citation2016) have used this technique to turn an unstructured system model into a structured one. As shown in Figure 1, the selected critical factors were categorized as drivers or dependents based on their driving abilities or other factors.

The model’s results assist us in concluding that all of the selected variables have an impact on environmental data. This demonstrates that the variables were selected with care and diligence. The study’s findings indicate that among the critical factors, “Profitability” has been described as a bottom-level independent critical factor driving environmental information disclosure. The factor “gender diversity” still has a lot of clout. Among the critical factors, “board independence” has been listed as the top dependency variable in the ISM model. Profitable businesses reveal more social information to the public in order to justify their presence (Haniffa & Cooke, Citation2005). Previous research has assumed a positive relationship between voluntary disclosure and profitability (Kansal et al., Citation2014; Giannarakis, 2014). Token disclosure companies strive to portray the behavior and vision of the business in their reporting. Although this method of disclosure lacks solid environmental achievements as a backing, it can help companies establish an image of environmental responsibility in the market, seek social legitimacy, and put pressure on stakeholders in the capital market, market products and other areas to obtain scarce resources.

According to (Garcı´a-meca & Sa´nchez-ballesta, Citation2010), the strength of the board of directors is closely linked to the degree of independence and diversity of its members, and it should be noted that women’s representation on corporate boards of directors is one of the most significant dimensions of corporate governance in many publications and studies of members of the board of directors. Some have argued that women may be more aware of environmental issues and more concerned with reducing perceived risks (Post et al., Citation2011). literature anticipates that female board members will augment the financial performance of organizations by bringing their unique abilities, skills, experiences with them to boards (Kılıç and Kuzey (Citation2016), Boulouta (Citation2013).

Gender diversity in boardrooms can affect reporting quality, enforcement, and ethical conduct, according to new research. The presence of women on the board of directors has a positive impact on the standard of sustainability reporting. According to Bear et al. (Citation2010), female board members have a favorable impact on power ratings in corporate social responsibility. Furthermore, having more women on the board improves the board’s effectiveness in managing stakeholders and encourages the implementation of sustainability programs such as climate change reporting.

The Saudi Bank now has a stronger and more influential social responsibility in the Kingdom of Saudi Arabia, especially after 11 banks announced their support for healthcare and confirmed its important role in reducing the burden of the coronavirus pandemic.

This paper examines voluntary environmental disclosure practices and specifically addresses the factors affecting the disclosure of environmental information. We note that the awareness of companies in preparing environmental reports is linked to profitability, gender diversity and board independence.

5. Limitations and future scope

Reliance on structural equation modeling showed a high ability to verify and highlight the factors that affect environmental information disclosure, and therefore it can be used in further research and develop a linear structural relationship for many other factors that affect the disclosure of environmental information.

6. Conclusion and implications

Our study showed that profitability, gender diversity and board independence are the main factors and the main motive for the disclosure of environmental information. Based on the findings it is recommended that that women’s representation on corporate boards of directors is one of the most significant dimensions of corporate governance that may be more aware of environmental issues and more concerned with reducing perceived risks.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Garoui Nassreddine

Garoui Nassreddine is an Assisstant Professor of Finance. He is also an Associate editor of the Journal of Behavioral Economics, Finance, Entreprneurship, Accounting and transport. He is also a reviewer in many international journals such as: Contomporary Economics, Business and Economic Horizons and Africain Journal of Business and Management. His papers have been published by international journals: Contomporary Economics, Environmental Economics, Cogent Economic and Finance, Applied Mathematics, The Romanian Economic Journal, International Review of Business and Management Research, International Journal of Economic Finance and Administrative Science …. His domain of research is oriented mainly to Corporate Governance, Corporate Social Responsibility, Accounting Disclosure, Cognitive Maps and Managerial Decision Making.

References

- Arnold, D. G., & Valentin, A. (2013). Corporate social responsibility at the base of the pyramid. Journal of Business Research, 66(10), 1904–13. https://doi.org/10.1016/j.jbusres.2013.02.012

- Artiach, T., Lee, D., Nelson, D., & Walker, J. (2010). The determinants of corporate sustainability performance. Accounting & Finance, 50(1), 31–51. https://doi.org/10.1111/j.1467-629x.2009.00315.x

- Ashfaq, K., & Rui, Z. (2018). Revisiting the relationship between corporate governance and corporate social and environmental disclosure practices in Pakistan. Social Responsibility Journal, 15(1), 90–119. https://doi.org/10.1108/SRJ-01-2017-0001

- Baraibar-Diez, E., & Odriozola, M. D. (2019). CSR committees and their effect on ESG performance in UK, France, Germany and Spain. Sustainability, 11(18), 5077. https://doi.org/10.3390/su11185077

- Bear, S., Rahman, N., & Post, C. (2010). The impact of board diversity and gender composition on corporate social responsibility and firm reputation. Journal of Business Ethics, 97(2), 207–221. https://doi.org/10.1007/s10551-010-0505-2

- Block, J. H., & Wagner, M. (2014). The effect of family ownership on different dimensions of corporate social responsibility: Evidence from large US firms. Business Strategy and the Environment, 23(7), 475–492. https://doi.org/10.1002/bse.1798

- Boulouta, I. (2013). Hidden connections: The link between board gender diversity and corporate social performance. Journal of Business Ethics, 113(2), 185–197. https://doi.org/10.1007/s10551-012-1293-7

- Brammer, S., & Pavelin, S. (2008). Factors influencing the quality of corporate environmental disclosure. Business Strategy and the Environment, 17(2), 120–136. https://doi.org/10.1002/bse.506

- Branco, M. C., Delgado, C., Gomes, S. F., & Eugénio, T. C. P. (2014). Factors influencing the assurance of sustainability reports in the context of the economic crisis in Portugal. Managerial Auditing Journal, 29(3), 237–252. https://doi.org/10.1108/MAJ-07-2013-0905

- Cowen, S. S., Ferreri, L. B., & Parker, L. D. (1987). The impact of corporate characteristics on corporate social responsibility disclosure: A typology and frequency based analysis. Accounting Organizations and Society, 12(2), 111–112. https://doi.org/10.1016/0361-3682(87)90001-8

- Ezeddine, B. M., Nassreddine, G., & Kamel, N. (2020). Do optimistic managers destroy firm value? Journal of Behavioral and Experimental Finance, 26 c , 100292. https://doi.org/10.1016/j.jbef.2020.100292

- Garcı´a-meca, E., & Sa´nchez-ballesta, J. P. (2010). The association of board independence and ownership concentration with voluntary disclosure: A meta-analysis. European Accounting Review, 3(3), 603–627. https://doi.org/10.1080/09638180.2010.496979

- Garoui, N., & Jarboui, A. (2014). Corporate governance: Behavioral approach and cognitive mapping technique. Contemporary Economics, 8(2), 229–242 doi: 10.5709/ce.1897-9254.143.

- Garoui, N. (2016). Determinants of financial information disclosure: A visualization test by cognitive mapping technique. Journal of Economics, Finance and Administrative Science, 21(40), 8–13. https://doi.org/10.1016/j.jefas.2016.03.002

- Haniffa, R. M., & Cooke, T. E. (2005). The impacts of culture and governance on corporate social reporting. Journal of Accounting and Public Policy, 24(5), 391–430. https://doi.org/10.1016/j.jaccpubpol.2005.06.001

- Jain, R., & Winner, L. H. (2016). CSR and sustainability reporting practices of top companies in India. Corporate Communications: An International Journal, 21(1), 36–55. https://doi.org/10.1108/ccij-09-2014-0061

- Kannan, G., Pokharel, S., & Sasi Kumar, P. (2009). A hybrid approach using ISM and fuzzy TOPSIS for the selection of reverse logistics provider. Resources, Conservation and Recycling, 54(1), 28–36. https://doi.org/10.1016/j.resconrec.2009.06.004

- Kansal, M., Joshi, M., & Batra, G. S. (2014). Determinants of corporate social responsibility disclosures: Evidence from India. Advances in Accounting, 30(1), 217–229. https://doi.org/10.1016/j.adiac.2014.03.009

- Kılıç, M., & Kuzey, C. (2016). The effect of board gender diversity on firm performance. Gend. Manag, 31(7) , 431–455 https://doi.org/10.1108/GM-10-2015-0088.

- Legendre, S., & Coderre, F. (2013). Determinants of GRI G3 application levels: The case of the fortune global 500. Corporate Social Responsibility and Environmental Management, 20(3), 182–192. https://doi.org/10.1002/csr.1285

- Liu, M., Shi, Y., Wilson, C., & Wu, Z. (2017). Does family involvement explain why corporate social responsibility affects earnings management? Journal of Business Research, 75(c), 8–16. https://doi.org/10.1016/j.jbusres.2017.02.001

- Mannan, B., Khurana, S., Haleem, A., & Nisar, T. (2016). Modeling of critical factors for integrating sustainability with innovation for Indian small- and medium-scale manufacturing enterprises: An ISM and MICMAC approach. Cogent Business & Management, 2331–1975, Taylor & Francis, Abingdon, 3(1), 2–15 . https://doi.org/10.1080/23311975.2016.1140318

- Martínez-Ferrero, J., Garcia-Sanchez, I. M., & Cuadrado-Ballesteros, B. (2013). Effect of financial reporting quality on sustainability information disclosure. Corporate Social Responsibility and Environmental Management, 22(1), 45–64. https://doi.org/10.1002/csr.1330

- McWilliams, A., & Siegel, D. (2001). Corporate social responsibility: A theory of the firm perspective. The Academy of Management Review, 26(1), 117–127. https://doi.org/10.5465/amr.2001.4011987

- Nassreddine, G., & Anis, J. (2015). Mental models of governance actors with respect to the environmental information. Environmental Economics 6(4) , 38–47.

- Nassreddine, G., Raida, C., & Ezzeddine, B. M. (2017). Mapping environmental pollution disclosures in Tunisia. Environmental Economics 8 (2), 67–75 http://doi.org/10.21511/ee.08(2).2017.07.

- Post, C., Rahman, N., & Rubow, E. (2011). Green governance: ‘boards of directors’ composition and environmental corporate social responsibility. Business and Society, 50(1), 189–223. https://doi.org/10.1177/0007650310394642

- Raj, T., Shankar, R., & Suhaib, M. (2008). An ISM approach for modelling the enablers of flexible manufacturing system: The case for India. International Journal of Production Research, 46(24), 6883–6912. https://doi.org/10.1080/00207540701429926

- Rossi, A., & Tarquinio, L. (2017). An analysis of sustainability report assurance statements: Evidence from Italian listed companies. Managerial Auditing Journal, 32(6), 578–602. https://doi.org/10.1108/MAJ-07-2016-1408

- Salvioni, D. M., & Gennari, F. (2019). Stakeholder perspective of corporate governance and CSR committees. Symph. Emerg. Issues Manag, 1, 28–39 doi: http://doi.org/10.4468/2019.

- Shen, C. H., Wu, M. W., Chen, T. H., & Fang, H. (2016). To engage or not to engage in corporate social responsibility: Empirical evidence from global banking sector. Economic Modelling, 55(c) , 207–225. https://doi.org/10.1016/j.econmod.2016.02.007

- Spence, C., & Gray, R. H. 2007. Social and environmental reporting and the business case, ACCA Research Report 98. ACCA:.

- Suyono, E., & Farooque, O. (2018). Do governance mechanisms deter earnings management and promote corporate social responsibility? Accounting Research Journal, 31(3), 479–495. https://doi.org/10.1108/ARJ-09-2015-0117

- Tingbani, I., Chithambo, L., Tauringana, V., & Papanikolaou, N. (2020). Board gender diversity, environmental committee and greenhouse gas voluntary disclosures. Bus. Strategy Environ 29 (6) , 1–17 https://doi.org/10.1002/bse.2495.

- Wu, M. W., & Shen, C. H. (2013). Corporate social responsibility in the banking industry: Motives and financial performance. Journal of Banking & Finance, 37(9), 3529–3547. https://doi.org/10.1016/j.jbankfin.2013.04.023