?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Financial development impacts a country’s economic growth and development. Due to this, many nations have sought new ways to bring about financial sector development. For developing economies, innovations in the financial sector are a sure bet for the development of financial inclusion. Mobile money is one of them. However, as the financial sector innovate, the Central Bank may lose control, rendering monetary policy ineffective. Therefore, this study examines one such innovation’s effect on monetary policy effectiveness. Using SVAR and monthly data spanning from January 2012 to December 2018, the study found that monetary policy becomes less effective under mobile money growth. The study further revealed that policy rates respond to mobile money growth in Ghana. In conducting monetary policy in Ghana, the study recommends that the monetary policy authority includes mobile money activity.

PUBLIC INTEREST STATEMENT

Over the past decades, mobile money usage and other technologies that facilitate financial transactions have flooded developing economies, of which Ghana is not an exception. These fintechs have led to the provision of financial services like savings, insurance, access to credit among others, especially for the poor and financially excluded from the formal banking system. These developments will have implications for the monetary policy of the central bank. To this end, the study focused on the effect of mobile money on the effectiveness of monetary policy. The results from the study suggest that, mobile money activities in Ghana affect the conduct of monetary policy in Ghana. Thus, monetary policy becomes less effective when money experiences growth in the value of transactions. Therefore, the monetary authority must take a closer look at the mobile money activities and accommodate them in the framing of monetary policy for Ghana.

1. Introduction

The surge in financial innovations is expected to impact developing economies. These innovations are touted to improve financial inclusion and ensure the allocative efficiency of resources (Bernier & Plouffe, Citation2019; Frame & White, Citation2014; Lumsden, Citation2018). Thus, a large percentage of the unbanked (Demirgüç-Kunt & Klapper., Citation2013) would have financial services access. The expanded access through financial innovations would have implications for the conduct of monetary policy by the central banks. Theories on financial innovation and development suggest contrasting positions of which one stand supports the argument that financial innovation strengthens the interest rate channel of monetary policy transmission (Noyer, Citation2007). On the other hand, it could pose a challenge to the conduct of monetary policy.

Financial innovations are well advanced in Africa, leading to mobile money services development in the fintech landscape. Across the region, mobile transfer, mobile payments, and mobile financial transactions have gain dominance (Orekoya, Citation2017). Mobile money services have received a boost due to the development of mobile telecommunication services (Nyamongo & n.d.irangu, Citation2013). Financial services have reached millions due to mobile money services and are used widely for financial transactions in Ghana. Available data reveals that at the end of 2017, mobile money subscribers in Ghana were 23,947,437 out of 37,445,048 mobile phone subscribers. The figures indicated a whopping 83.1% of the total population owns mobile money accounts (Boateng, Citation2018). As of June 2021, the value of transactions done through mobile money was GHS 89.1 billion, a 96.6% increase over the same period in 2020 (BoG, 2021).

The increasing use of mobile money as a means of payment services reduce poverty, boost economic activity, provide savings opportunities and the ability to participate in the financial sector of an economy (Adaba et al., Citation2019; Asamoah et al., Citation2020; Boateng, Citation2018). These benefits notwithstanding, there are unanswered questions about the impact of mobile money on the effectiveness and conduct of monetary policy in Ghana. Mawejje and Lakuma (Citation2019), citing Tumusiime-Mutebile (Citation2015), asserted that mobile money might negatively affect the effectiveness of monetary policy through the interest rate channels. Simpasa et al. (Citation2011) raised concerns about the potential inflationary effect of mobile money in developing countries. They argued that an increase in the velocity of money due to mobile money could undermine monetary policy effectiveness and lead to price instability. The evidence is that mobile money has a moderate effect on monetary aggregates (Mawejje & Lakuma, Citation2019), indicating the possibility of its impact on monetary policy. Aron et al. (Citation2015) and Adam and Walker (Citation2015) found no concrete evidence supporting the inflationary effect of mobile money. The argument for and against the impact of mobile money activity on monetary policy is inconclusive. To the best of our knowledge, there is no research conducted on the impact of mobile money on the effectiveness of monetary policy in Ghana. Therefore, this study seeks to answer the question; what is the influence of mobile money on monetary policy effectiveness in Ghana?

Except for Orekoya (Citation2017), who focused solely on Nigeria, studies on the influence of mobile money on macroeconomic variables have primarily concentrated on Eastern African economies. Studies like Aron et al. (Citation2015) and Mawejje and Lakuma (Citation2019) could not apply to the Ghanaian economy because they were conducted in monetary targeting economies. Given the mobile money growth in Ghana under the inflation targeting regime, an examination of its role in the efficacy of monetary policy cannot be downplayed. To the best of our knowledge, Ghana has not seen any study that has attempted to examine the impact of monetary policy conduct with the hindsight of considering mobile money. Studies on mobile money in Ghana have centred on financial inclusion, poverty reduction and employment. We examine the relationship between mobile money and monetary policy effectiveness in an inflation-targeting framework.

The rest of the paper is organised as follows: the next section presents the pattern and trends of the mobile money landscape in Ghana, linkages between monetary policy and mobile money, including the empirical literature. The third section deliberates on the methodology employed. We then discuss the results of the study in section four. The last section presents the conclusion and policy recommendations/implications of the study.

2. Literature

2.1. Mobile money in Ghana

Mobile money activities started in 2009 in Ghana with just one mobile operator. However, the acceptance of mobile money was slow compared with Eastern African countries like Malawi and Kenya (Mattern, Citation2018). This situation was due to regulation bottlenecks but was later addressed. According to IMARC Group (2019), mobile money services have witnessed growth due to the advantage of their convenience, the availability of agents and the interoperability introduced in the early part of 2019. Aside from this, the Bank of Ghana’s action to ease the operating environment has fostered growth in this sector’s activities (Boateng, Citation2018; Mattern, Citation2018).

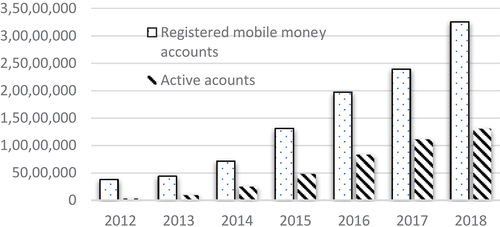

Data available suggests a growth in the number of subscribers to mobile money with/and a corresponding increase in the volume of transactions conducted using mobile money platforms. Cumulatively, the total number of registered mobile money accounts went from 3,778,374 to 32,554,346 accounts (Bank of Ghana, 2019). This number represents a growth of over 300% in mobile money accounts. According to the Bank of Ghana as cited in Boateng (Citation2018), 83.1% of Ghanaians had a mobile money account in 2017.

From , observation reveals that the number of active accounts has also increased over the years. This increase corresponds to the rising values and the number of transactions recorded over the years. Trends suggest the value of transactions has seen an upward trend from 594.12 million Ghana Cedis in 2012 to about 66 billion in the first quarter of 2019. Expectations are that this figure will grow by 26.75% of the 2018 value of transactions over mobile money. These figures and the volume of business transacted over mobile money keeps growing and will present a growing concern for the Bank of Ghana and other regulators of cyberspace.

Figure 1. Registered (cumulative) and active mobile accounts.Source: Bank of Ghana

2.2. Monetary policy and mobile money

From the trends and growth of the monetary values of the volumes of transactions done through mobile money, it is fundamentally significant to assess its possible effect on the conduct of monetary policy in Ghana. The monetary policy goals for the Bank of Ghana include price stability and stable economic growth. Generally, the quantity of money theorists frames the likelihood for mobile money to lead to inflationary pressures (Adam & Walker, Citation2015; Aron et al., Citation2015). According to Simpasa et al. (Citation2011), there is the possibility of mobile money being a driver of high inflation levels. The import of such an argument rested on the likelihood of mobile money leading to monetary expansion. Again, the inflationary pressure from such innovations may result from consumers’ ability to transact business easily, increasing the velocity of money. Still, mobile money could propel productivity and investment by firms (Islam et al., Citation2018). This condition happens through a reduction in the cost of the transaction. Such ease of money transfer does provide liquidity to the firms leading to improved cash flow and investment. By this, firms will seek to advance and pursue growth yielding opportunities by investing their funds. If firms follow such a course, it leads to allocative efficiency and reduction in the general price levels. The argument for mobile money affecting the money demand has two arms. The first strand argues that mobile money may accumulate e-money which hitherto was not so. These holdings by households would tend to affect the demand for money. This state implies mobile money will correlation positively with monetary aggregates (Mehrotra & Yetman, Citation2015; Yetman, Citation2017). The second stance posits an increase in transactional efficiency that emanates from innovations in the financial sector of which mobile money is part. Thus, mobile money tends to reduce the risk of losses due to handling cash. Similarly, mobile money reduces the cost of transacting business and removes business bottlenecks, dealing with a financial institution such as waiting time and locational disadvantages of banks. In such scenarios, the demand for money may reduce (Mawejje & Lakuma, Citation2019; Nyamongo & n.d.irangu, Citation2013).

Demand for money and supply of private sector credits are argued to be channelled through which mobile money could affect monetary policy effectiveness in an economy. On one breath, if mobile money results in inflationary pressures, then monetary authorities might respond by pursuing tight monetary policies leading to high interest rates. Besides, mobile money can affect the private sector credit. Essentially, mobile money deposits held in financial institutions’ escrow accounts can be turned into loanable funds by financial institutions, thereby increasing funds available for credit creation. Nampewo et al. (Citation2016) found that mobile money had emerged as a significant determinant of private sector credit growth in Uganda through its crucial role in savings and deposit mobilization. Finally, mobile money leads to economic efficiency through reduced transaction costs, better resource allocation and credit, supporting aggregate economic activity. In this regard, there is emerging evidence linking mobile money use to increased firm-level investments (Islam et al., Citation2018), agricultural (Aker & Mbiti, Citation2010; Sekabira & Qaim, Citation2017), risk-sharing (Mawejje & Lakuma, Citation2019; Riley, Citation2018), and financial-sector development (Munyegera & Matsumoto, Citation2018). These effects will likely have positive implications for economic growth).

Concerning the potential relationship between mobile money and inflation, there are two alternative views. Mobile money could prove to be inflationary if it affects the velocity of money in circulation without necessarily improving the levels of aggregate output. Simpasa et al., Citation2011), for example, espouse this viewpoint. However, there could be countervailing effects where mobile money improves productivity and economic efficiency, lower transaction costs and higher output, resulting in a lesser or non-existent inflationary effect (Aron et al., Citation2015).

3. Methodology

3.1. Econometric strategy

The study adopted the New Keynesian model used by Ahiakpor et al. (Citation2019) and Aron et al. (Citation2015) to assess the effect of mobile money on monetary policy effectiveness. The output model in the study is based on the Keynesian IS model and is given as:

It must be noted that, output gap is measures as potential output () less actual output (

). The

s are coefficients that capture the impact of the respective variables on the output gap. The output gap, short term interest rate, inflation rate, nominal exchange rate, foreign and domestic price levels are represented by

,

,

,

,

, and

respectively.

is a random walk error term that is assumed to be white noise. Equation one (1) is re-specified as:

Equation two (2) presents the output gap as a function of short-term interest rate, inflation rate and real exchange rate (Where the real exchange rate is the nominal exchange rate adjusted for inflation).

The study adopts Calvo’s (Citation1983) nominal price adjusting models as cited in Ahiakpor et al. (Citation2019) to model the monetary policy impact on inflation in the following manner:

By implication, the output cap, real interest rate and past inflation outcomes influence inflation. Thus, equation three (3) can be written as:

For this study’s objective and following the empirical works of Aron et al. (Citation2015), Mawejje and Lakuma (Citation2019) Mehrotra and Yetman (Citation2015), the above models 2 and 4 are augmented to include mobile money (MOMO), short term interest rate (SR) and interaction between the short-term interest rate and mobile money (MSR), financial inclusion (FI) and the interaction of mobile money,), the exchange rate (ER) and claims on private sector (PSC).

3.2. Data, variables, and measurement

The data used for the study were monthly data from the year 2012 January to December 2018. This data gives about 84 observations, enough to estimate a Vector Autoregressive model. Data availability influenced the choice for this period. Also, the start date coincides with the period where mobile money experienced rapid penetration and caught attention due to the Bank of Ghana policy reforms. The output is proxied in this study by the Bank of Ghana’s Composite Index of Economic Activity (CIEA; see: Ahiakpor et al., Citation2019), providing monthly information on the country’s economic productivity. The Bank of Ghana provided the value of mobile money transactions. This data was later converted into monthly data series using EVIEWS. The cubic spline method was used to interpolate the annual data to monthly data base on the structure of CIEA. The quadratic sum approach to interpolate the data from yearly to monthly data series since it provides an efficient and simple approach to data transformation from low frequency to high frequency data. Though there may be a problem of non-negativity in the data, this was solved by taking the natural log of the data used for the study. For mobile money, we used the values rather than the volume of transactions made since the value of the transactions made will have much more effect on the total money supply. We obtained the monthly series of inflation rates from the Bank of Ghana. The IMF’s Global Economic Monitor dataset website provided the monthly bilateral exchange rate. The study used the Ghana Cedi to Dollar bilateral exchange rate. We obtained the monetary policy rate from the Bank of Ghana. Ghana uses policy rate as the key monetary policy instrument to signal the Bank’s monetary policy stance. Financial inclusion was measured using the number of bank branches available per 1000 people. We believe that the innovation in the provision of financial services like mobile money results in financial inclusion. Hence mobile money could affect monetary policy through its effect on financial inclusion. We estimated the output gap (yt) using the Hodrick-Prescott (HP) filter (λ = 1400 as recommended for monthly series) to obtain a time-varying trend. Monthly series is preferred because it is easier to identify trends changes and better for long-term strategic forecasting.

3.3. Structural VAR model

This study employs the structural vector autoregressive (SVAR) model of 9 variables to measure how inflation and output gaps respond to mobile money, monetary policy and its interaction with monetary policy. There are two reasons for adopting SVAR for this study instead of other time-series modelling approaches. Given the objectives of the study, shock to the structural innovation to study policy response is important. In this case, SVAR offers the more appropriate approach for the study. Secondly, SVAR offer rooms to examine the contemporaneous effect of variables on the dependent variable which Vector-Autoregressive Regression are less effective in doing so except explaining endogenous relationships from past values (See: Pfaff, Citation2008). It is worth noting that the VAR’s residuals do not lend themselves to any economic interpretation. However, the SVAR models typically result from macroeconomic models, and hence restrictions are broadly consistent with economic theory and outcomes that make economic sense (Brischetto & Voss, Citation1999). Due to this, SVAR shocks resulting from unobserved structural forms are meaningful economically. The identification restriction of a structural VAR is needed from the variance-covariance matrix of the reduced from residual. In this manner, the study imposes short-run restriction following an SVAR of the form:

From equation seven (7), is an

parameters matrix for

while

is

vector of explained or endogenous variables at time period t,

is a vector of

constant variables and

is a vector of

structural shocks that are white noise. Solving Equationequation 7

(7)

(7) gives an equivalent approximation as

EquationEquation 8(8)

(8) is such that

and

For the structural identification among the parameter to be estimated, the short-run restriction imposed for

In formulating the identification restrictions for the SVAR, we follow theoretical and empirical studies to arrange the variable in order of influence. Theoretically, the output gap may cause a change in price levels. For example, low productivity leads to inflation if demand exceeds the economy’s output levels. Similarly, the inflationary gap put upward pressure on prices since the monetary value of output produced exceeds the potential output, creating demand pressures leading to a price increase in practice, the resultant inflation in the economy will lead to a response in policy rate rise. In cases where the recessionary gap persists, monetary policy may be reviewed downward to foster investment and boost aggregate demand. Again, the amount of mobile money holdings will influence the money supply, especially in cases where mobile money is bank-backed (escrow account holdings). This situation will lead to a monetary policy response because of mobile money transactions and holdings in the economy. Such policies affect the money supply through credit channels through their impact on price variations in the loanable fund. It also follows that mobile money activities result in financial inclusion. Thus, a shock in mobile money is expected to have a positive impact on financial inclusion and private sector credit. This event will impact the interest rate and monetary conduct in the economy. There may be a contemporaneous response of the exchange rate to the policy rate. However, in some cases, the behaviour of the exchange rate may lead to changes in the policy rate to avert inflationary pressure on the economy.

Impulse response function (IRFs) was generated to examine the response of the variable of interest to the structural shocks. This was done for the key variables of interest to the study. Thus, the IRFs of used for this study focused the response of output gap, inflation and monetary policy to shocks in mobile money, monetary policy and interaction of monetary policy and mobile money.

4. Results and discussions

4.1. Preliminary test and summary statistics

Since we are using time-series data, we first examined the time-series properties of the variables. The study used the Augmented Dickey-Fuller unit root test to scrutinise the stationarity of the variables. After the variables stationarity property confirmation, we estimated the Structural VAR (SVAR) model to analyse the effectiveness of monetary policy in Ghana.

presents the ADF test results. The results indicate that the log of mobile money and the interaction between mobile money and short-term interest rate are stationary at levels. However, all the other variables were non-stationary at levels but became stationary after first differencing. The Philip-Perron (test) was used to confirm the stationarity of the variables. In cases where the ADF and PP are stationary at levels, the level variables were used for the VAR estimation. However, when there were conflicting results, the PP results are used since it is generally considered to be more robust than the ADF test. The results suggest that all the variables were stationary at first difference except the log of mobile money for the ADF test. The PP test showed that Output gap, log of private sector credit, and the interaction of mobile money with short term rate (log of MSR) were stationary at levels whereas the remaining variables were stationary at first difference.

Table 1. Unit root test using ADF

4.2. Summary statistics

presents the summary statistics of the variables used for the study. The mean of inflation was 13.3, indicating that over the estimation period, Ghana’s monthly inflation levels averaged 13.3 with a standard deviation of 3.2895. The highest level of monthly inflation recorded was 19.2%, and the lowest was 8.64%.

Table 2. Summary statistics

The policy rate for the study period was 19.67 on average, with a 4.089 standard deviation. During the study period, the lowest monthly rate was 12.5, and the highest monetary policy rate was 26%. The log of the value of mobile money transactions ranged from 3.539 to 9.888, with a mean of 7.42. The exchange rate had its highest to be 4.917 and the lowest of 1.6886. However, the average exchange rate was GHS 3.40 to a dollar. The output gap ranged between −0.17916 and 0.12713.

4.3. Pre-estimation test

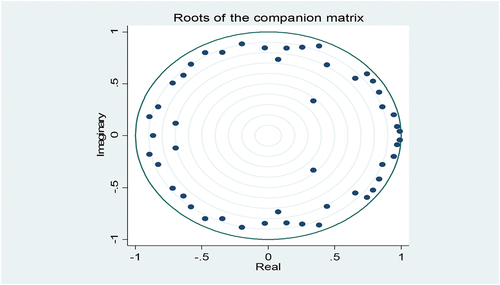

Having an appropriate lag length for VAR and SVAR models is imperative. As a result, the appropriate lag was determined using the lag length criterion for VAR models. Based on the results, the number of lags selected by the Schwarz Bayesian Information Criterion (SBIC) suggested a lag length of 1. The remaining criteria, like the Hannan-Quinn (HQC), indicated two lags, the Final Prediction Error (FPE) and the Akaike Information Criterion (AIC), all suggested a lag length of 4 (See: ). Based on these results, the study used a lag length of 4. The Lagrange-Multiplier test for Serial Correlation reveals that we failed to reject the null hypothesis of no autocorrelation for the lag length used (), indicating no higher-order serial correlation of the residuals. This result indicates no higher-order serial correlation of the residuals. The check for stability of the VAR and SVAR models showed that the SVAR satisfies the stability conditions since the eigenvalues of the characteristic components lie within the unit circles (See: ). The log-likelihood test for identifying restrict was found to be statistically significant at 5%.

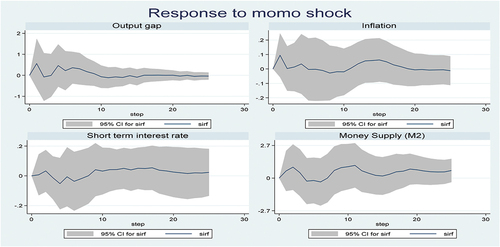

4.4. Responses to mobile money shocks

shows the impulse responses of the output gap, inflation, monetary policy, and money supply to shocks in mobile money. Observation shows that a shock in mobile money widens the output gap at the initial stages up to the 5th period. The gap, however, begins to close from the 10th period, restoring equilibrium after the 15th period. The shocks in mobile money turn to spark off a cyclical behaviour in the first five periods. It reached a peak after five periods and since then witnessed a steady decline, approaching equilibrium. This finding indicates that shocks in mobile money may take a very long time to affect productive activity in the desired way. According to Mawejje and Lakuma (Citation2019), even if mobile money facilitates easy transactions, it may not result in greater productivity. As a result, the output gap is likely to widen. Thus, in the initial stages of adoption, mobile money transaction in Ghana is mainly for payment and consumption. This situation may result in economic activity expanding beyond its potential level, as seen in the initial periods of the shocks.

Figure 2. IRFs of the macroeconomic variables to mobile money shocks.

However, the credit facilities offered by mobile money operators can increase investment and credit access, which enhance productivity and output growth resulting in the output gap reduction. The results as presented depict these two phases of a shock to the innovation by one standard deviation. On the other hand, the long-term impact of mobile money resulting in economic efficiency cannot be over-emphasised. The mobile money landscape has provided businesses in Ghana with reduced transaction cost. Expectations are that improved resource allocation and credit activities will allow investment that supports total economic activity. The inference is that the output gap will narrow in the long term, as seen after the 17th period and beyond. This finding might be due to firm-level investment reaction to increased mobile money transactions, or it could be due to direct investment by enterprises made possible by mobile money (Islam et al., Citation2018). Also, such response could be attributed in part to developments in the productive sectors like agriculture, enhanced risk-sharing, greater financial inclusion, which engenders economic growth and development in any economy (Aker & Mbiti, Citation2010; Mawejje & Lakuma, Citation2019; Munyegera & Matsumoto, Citation2018; Riley, Citation2018; Sekabira & Qaim, Citation2017).

A positive shock in mobile money leads to a sharp increase in the inflation rate for the first months. It immediately follows a downwards trend up to the 9th month. However, from the 10th to about the 15th month, inflation rises and peaked and begins to fall. This result confirms the earlier findings of Aron et al. (Citation2015), Adam and Walker (Citation2015) and GSMA (Citation2019), suggesting that the spread in mobile money may not cause inflationary pressure. Nevertheless, this is true for only the first few months with it is met with an appropriate shock or response in the monetary policy rate. This reaction of inflation may be due to the response of short-term interest rates to shocks in monetary policy. As indicated by , monetary policy responds to the shocks in mobile money with an increase in short-term interest rate in the first month, as mobile money shock affects the conduct of monetary policy. Thus, monetary policy responds to the initial shocks in mobile money to improve the effect of mobile money shocks on inflation and output gaps.

Aside from the response of inflation and short-term interest rates, innovations in MOMO induces an increase in money supply consistent with earlier arguments by Simpasa et al. (Citation2011), Simpasa et al., Citation2011), GSMA (s), among others. In this case, the Bank of Ghana may respond to the MM shock by adjusting the policy rate upwards. Thus, the conduct of monetary policy is influenced by the activities of mobiles money in the Ghanaian economy.

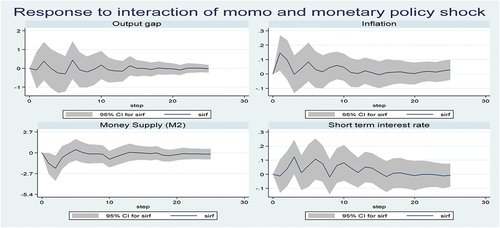

4.5. Responses to the interaction of MOMO and monetary policy shocks

indicates that a shock to the interaction term of mobile money and monetary policy set the output gap unto a cyclical path of ups and downs but became stable after 18 months. The upturns are somewhat short-lived. On average, there seems to be downward pressure on the output gap, which may be due to the combined effect of monetary policy tightening and positive shock to mobile money. In other words, the monetary policy tightening moderates the impact of mobile money on the extent of its influence on the output gap.

Figure 3. Response of key variables to shocks in the interaction of MOMO and monetary policy.

Money supply fell in several short periods before rising after the first two periods preceding the innovation shocks. The climb of the money supply from its descending point after the shock seems gradual and consistent over the period. The money supply approaches equilibrium in the longer term. This rise in the money supply may result from the volume and the value of mobile money transactions conducted outside the banking system through mobile money vendors. There is an immediate rise in inflation aftershocks to the innovations followed by a drop in inflation. This behaviour of monthly inflation could be attributed to central bank actions about short term interest rates. Careful observation of the inflation after the shock of the interaction of mobile money and policy rate shows a rather oscillating behaviour before the inflation variable reaches equilibrium.

This result is expected given that the policy rate set by Ghana’s central bank influences price behaviour in the country. The response of the short-term interest rate seems to mimic the inflation pattern in . This finding implies that a rise in inflation may follow a hike in the monetary policy rate.

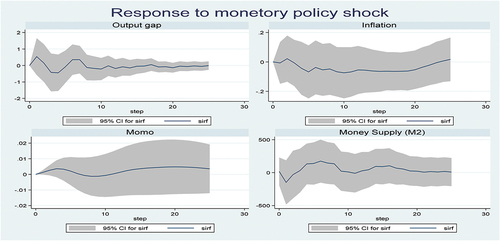

4.6. The response of key variables to monetary policy shocks

According to , a positive shock to monetary policy does not produce a contemporaneous effect on output. The output gap widens in the beginning but gradually contract after the sixth month. We discovered that the output gap oscillates around the equilibrium at a reduced wave in the estimation horizon. The widening of the output gap is due to an increase in the prices of loanable funds, leading to a reduction in the amount borrowed for investment purposes. Thus, the investment rate decreases, leading to a decline in output, causing a rise in the output gap for successive periods due to monetary policy tightening before reverting to the equilibrium level.

Figure 4. Response of key variables to monetary policy.

The effect of a contractionary monetary policy also leads to an initial rise in inflation up to the second month under the estimation horizon. Afterwards, inflation begins to slide down and somewhat become stable below one standard deviation for ten periods. However, inflation gathers moment after the 20th period and begins to explode. For periods where mobile money is decreasing, inflation shocks seem to respond appropriately. When mobile money became popular in the 10th period of the estimating horizon, inflation began to rise. When mobile money operations are present, this finding suggests a lag effect in the response of inflation to monetary policy action. Thus, mobile money may delay the impact of monetary policy on monetary aggregates and the output gap. In this sense, monetary policy in the light of mobile money operation is weak but not outrightly ineffective.

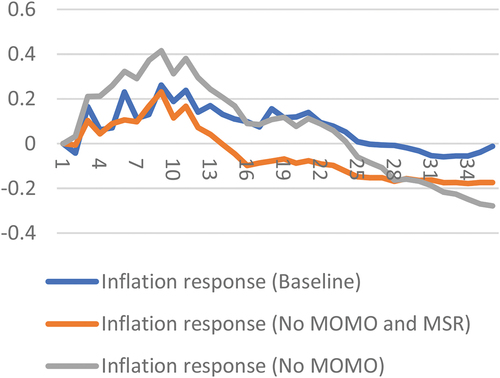

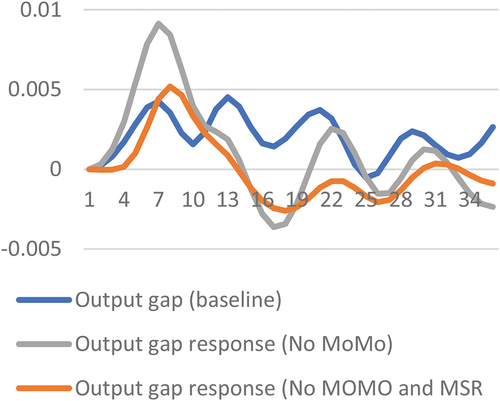

4.7. Counterfactual analysis of the effect of mobile money on monetary policy effectiveness

To perform the counterfactual analysis of the effect of Mobile Money (MOMO) on the effectiveness of the monetary policy, we shut out the mobile money channel as the first step, leaving the interaction of mobile money and monetary policy. Afterwards, both mobile money and its interaction term were removed, and the responses of inflation and output gap to monetary policy shocks were examined. present these results. The results indicate that a positive shock in monetary policy rates leads to an initial rise in inflation for all three scenarios. In a situation where there is no mobile money influence and the interaction term, inflation starts to decline after the 9th period and decline sharply to the 15th period. Compared with the baseline, the decline in inflation where mobile money effects are absent (mobile money and its interaction with policy rate), monetary policy seems to be more effective in reducing inflation levels. This finding may be due to mobile money activities, which increases money in circulation and the transaction rate leading to demand pressures that cause prices to rise.

Figure 5. Response of inflation to monetary.

Figure 6. Response of output gap to policy monetary policy.

The output gap seems unresponsive in all three scenarios. The cycle in output gap widens in cases where mobile money activity exists. A careful observation of reveals that over time, the output gap begins to close. However, given the estimation time horizon, monetary policy is less likely to influence output levels. As previously stated, the output gap will widen due to the impact of monetary policy on the price of loanable funds. However, mobile money could make such gaps explosive in the economy, making the output gap persistent due to a surge in aggregate demand for the economy. Another explanation is that mobile money provides a means of saving and investment activity for users, making money available for business transactions. This explanation would suffice given that Ghana’s economy is mainly informal.

5. Conclusion and policy implication

The study examines the effect of mobile money on monetary policy effectiveness for Ghana. The core outcomes of monetary policy conduct in this study were output and price stability. The presence of mobile money activities in the country has implications for the conduct of monetary policy even under the inflation targeting regime. The result revealed that mobile money shocks affect the short-term interest rate. Thus, increases in mobile money transactions have a consequential effect on the monetary policy stance in the economy, which is crucial to price stability and output in the economy. The results indicate that monetary policy has a slight effect on inflation and the output of the Ghanaian economy.

It was observed that shocks in mobile money have a slight ability to lead to inflation but remains stable for a very long time before a decline. And monetary policy may respond to shocks in the innovations of the money supply. The study discovered that the interaction between mobile money and monetary policy rate cause a decline in inflation but not immediately. Similarly, the study found the monetary policy to be effective in reducing inflation in the long run. However, the counterfactual analysis revealed that in the face of mobile money activity, monetary policy becomes less effective in achieving its goal of stabilising prices and closing the output gap. The implications are clear for policymakers. It is worth noting that in economies where financial innovations such as mobile money are fast gaining attention, it weakens the interest rate effect on the money supply in the economy. This outcome explains that financial innovations provide alternative modes of savings and investments, making money market transactions less attractive.

More so, in an economy like Ghana where informal sector activities dominate, financial innovation that leads to financial inclusion when not regulated and supervised by the Bank of Ghana could impact monetary policy effectiveness negatively. The reason is that mobile money can make finance more accessible to both consumers and investors. This situation could cause pricing pressures, resulting in higher prices and a wider production gap in the economy. Therefore, we strongly advise the Central Bank of Ghana to carefully assess monetary policy behaviour considering the Ghanaian economy’s rapid use of mobile money.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Emmanuel Agyapong Wiafe

Emmanuel Agyapong Wiafe a Lecturer at the Department of Economics, School of Liberal Arts and Social Sciences, Ghana Institute of Management and Public Administration (GIMPA), Achimota, Ghana. His main areas of expertise are development economics, applied econometrics and macroeconomic issues for developing countries. The current research on mobile money aligns with the researcher’s works on impact of interoperability payment, mobile payment systems macroeconomic developments.

Christopher Quaidoo

Christopher Quaidoo, is a Lecturer at the Department of Banking and Finance, University of Professional Studies, Accra, Ghana. His main research interests are in the fields of corporate finance, monetary economics and development economics.

Samuel Sekyi

Samuel Sekyi is a Senior Lecturer of Economics at SD Dombo University of Business and Integrated Development Studies, Ghana. His main areas of expertise and interest are in the fields of Microeconometrics, health economics, development economics, agricultural economics and finance.

References

- Adaba, G. B., Ayoung, D. A., & Abbott, P. (2019). Exploring the contribution of mobile money to well-being from a capability perspective. The Electronic Journal of Information Systems in Developing Countries, 85(4), e12079. https://doi.org/10.1002/isd2.12079

- Adam, C., & Walker, S. E. (2015). Mobile money and monetary policy in East African countries. Said Business School Discussion Paper. https://www.sbs.ox.ac.uk/sites/default/files/research-projects/mobile-money/Monetary-policypaper.pdf Oxford University

- Ahiakpor, F., Cantah, W., Brafu-Insaidoo, W., & Bondzie, E. (2019). Trade openness and monetary policy in Ghana. International Economic Journal, 33(2), 332–15. https://doi.org/10.1080/10168737.2019.1610027

- Aker, J. C., & Mbiti, I. M. (2010). Mobile phones and economic development in Africa. Journal of Economic Perspectives, 24(3), 207–232. https://doi.org/10.1257/jep.24.3.207

- Aron, J., Muellbauer, J., & Sebudde, R. (2015). Inflation forecasting models for Uganda: Is mobile money relevant? CEPR Discussion Papers 10739, Centre for Economic Policy Research Discussion Papers.

- Asamoah, D., Takieddine, S., & Amedofu, M. (2020). Examining the effect of mobile money transfer (MMT) capabilities on business growth and development impact. Information Technology for Development, 26(1), 146–161. https://doi.org/10.1080/02681102.2019.1599798

- Bernier, M., & Plouffe, M. (2019). Financial innovation, economic growth, and the consequences of macroprudential policies. Research in Economics, 73(2), 162–173. https://doi.org/10.1016/j.rie.2019.04.003

- Boateng, K. (2018). Ghana’s progress on reaching out to the unbanked through financial inclusion. International Journal of Management Studies, 5(2), 1–9. https://doi.org/10.18843/ijms/v5iS2/01

- Brischetto, A., & Voss, G. (1999). A structural vector autoregression model of monetary

- Calvo, G. A. (1983). Staggered prices in a utility maximizing framework. Journal of Monetary Economics, 12(3), 383–398. https://doi.org/10.1016/0304-3932(83)90060-0

- Demirgüç-Kunt, A., and Klapper, L. , & . (2013). Financial inclusion in Africa Triki, T, and Faye, I. In Financial Inclusion in Africa (pp. 74). AFDB.

- Frame, W. S., & White, L. J. (2014). Technological change, financial innovation, and diffusion in banking (pp. 1–5). Leonard N. Stern School of Business, Department of Economics.

- GSMA (2019) ”2018 State of the Industry Report on Mobile Money”. Retrieved June 20th, 2021, from https://www.gsma.com/mobilefordevelopment/resources/2018-state-of-the-industry-report-on-mobilemoney/

- Islam, A., Muzi, S., & Rodriguez Meza, J. L. (2018). Does mobile money use increase firms’ investment? Evidence from enterprise surveys in Kenya, Uganda, and Tanzania. Small Business Economics, 51(3), 687–708. https://doi.org/10.1007/s11187-017-9951-x

- Lumsden, E. (2018). The future is mobile: Financial inclusion and technological innovation in the emerging world. Stanford Journal of Law, Business & Finance, 23(1), 1–44.

- Mattern, M. (2018,). How Ghana became one of Africa’s top mobile money markets (CGAP publication). https://www.cgap.org/blog/how-ghana-became-one-africas-top-mobile-money-markets

- Mawejje, J., & Lakuma, P. (2019). Macroeconomic effects of mobile money: Evidence from Uganda. Financial Innovation, 5(1), 1–20. https://doi.org/10.1186/s40854-019-0141-5

- Mehrotra, A. N., & Yetman, J. (2015). Financial inclusion-issues for central banks. In BIS Quarterly Review. Bank for International Settlements 83–96 . https://www.bis.org/publ/qtrpdf/r_qt1503h.htm

- Munyegera, G. K., & Matsumoto, T. (2018). ICT for financial access: Mobile money and the financial behavior of rural households in Uganda. Review of Development Economics, 22(1), 45–66. https://doi.org/10.1111/rode.12327

- Nampewo, D., Tinyinondi, G. A., Kawooya, D. R., & Ssonko, G. W. (2016). Determinants of private sector credit in Uganda: The role of mobile money. Financial Innovation, 2(1), 1–16. https://doi.org/10.1186/s40854-016-0033-x

- Noyer, C. (2007). Financial innovation, monetary policy and financial stability. Economic and Financial review-European Economic and Financial Centre, 14(4), 187.

- Nyamongo, E., & Ndirangu, L. (2013). Financial innovations and monetary policy in Kenya, MPRA Paper No. 52387. https://mpra.ub.uni-muenchen.de/52387/1/MPRA_paper_52387.pdf

- Orekoya, S. (2017). Mobile money and monetary policy in Nigeria. NIDC Quarterly, 32(34), 20–34. http://demo.ndic.gov.ng/wp-content/uploads/2020/08/NDIC-Quarterly-Vol.-32-Nos-34-2017-Article-Mobile-Money-and-Monetary-Policy-in-Nigeria.pdf

- Pfaff, B. (2008). VAR, SVAR and SVEC models: Implementation within R package vars. Journal of Statistical Software, 27(4), 1–32. https://doi.org/10.18637/jss.v027.i04

- Riley, E. (2018). Essays on mobile money services, microenterprises and role models in developing countries [ Unpublished doctoral dissertation], University of Oxford.

- Sekabira, H., & Qaim, M. (2017). Mobile money, agricultural marketing, and off‐farm income in Uganda. Agricultural Economics, 48(5), 597–611. https://doi.org/10.1111/agec.12360

- Simpasa, A., Gurara, D., Shimeles, A., Vencatachellum, D., & Ncube, M. (2011). Inflation dynamics in selected East African countries: Ethiopia, Kenya, Tanzania and Uganda. AfDB Policy Brief. https://www.afdb.org/fileadmin/uploads/afdb/Documents/Publications/07022012Inflation%20East%20Africa%20-%20ENG%20-%20Internal.pdf

- Tumusiime-Mutebile, E. (2015). Emmanuel Tumusiime-Mutebile: Mobile money and the economy. https://www.bis.org/review/r150304i.htm

- Yetman, J. (2017). Adapting monetary policy to increasing financial inclusion. IFC Bulletins chapters. In The role of data in supporting financial inclusion policy (Vol. 47, Bank for International Settlements (ed.)). Bank for International Settlements 25 https://www.bis.org/ifc/publ/ifcb47m_rh.pdf .

Appendices

Figure A1. Root of the companion matrix mod.

Table A1. Lagrange-multiplier test

Table A2. Selection-order criteria