?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper investigates the notion of the financial Kuznets curve in an emerging country—Jordan. Both variants of the financial Kuznets curve (growth financial Kuznets curve and inequality financial Kuznets curve) have been examined using different time series methodologies applying to a sample period from 1993 to 2017. The unobserved components model results provide evidence for both variants of the financial Kuznets curve when using private credit to GDP as a proxy for financial-sector development. Moreover, non-nested model tests suggest that financial intermediaries are relatively more important than stock markets for income inequality. Overall, this paper provides evidence for the financial Kuznets curve in emerging countries. Moreover, it provides new insights for policymakers in Jordan in their challenge to boost economic growth and decelerate income inequality, by reversing the trend towards the concentration of power in the financial sector and creating public-financial institutions that provide affordable credit to small businesses and households.

PUBLIC INTEREST STATEMENT

Financial development’s positive contributions to economic growth and income inequality are well established in the literature. However, recent evidence finds that the relationship may reverse following a turning point, producing a U-shaped curve or Inverted U-shaped curve, which is a depiction of ‘the financial Kuznets curve’. In this sense, most literature investigates the financial Kuznets curve in developed countries, where the financial sector grew excessively to extract rents from the real economy. Therefore, this study investigates the existence of the financial Kuznets curve in Jordan as a case of an emerging country and confirms the existence of the financial Kuznets curve, which suggest that policymakers in Jordan should carefully address the issue of excessive finance and encourage a balanced growth between financial and real sectors to preserve the favourable contribution of the financial sector.

1. Introduction

The Financial Kuznets curve is a variant of the well-known Kuznets curve, and it is represented by an inverted U-shaped curve (U-shaped curve) for the finance-growth (finance-inequality) relationship. This relationship predicts an adverse impact of finance on economic growth and income inequality following a turning point, whereby excessive finance exerts negative consequences for economies hosting oversized financial sectors and shares many similarities with the “resource curse” that affects mineral-rich countries (Baiardi & Morana, Citation2018, Citation2016; Christensen et al., Citation2016; Moosa, Citation2018).

Table 1. Descriptive Statistics

Table 2. Correlations

The concept of the Financial Kuznets curve is relatively new, and it is derived upon the original Kuznets curve, put forward by Simon Kuznets (Citation1955), which depicts an inverted-U shaped relationship between economic growth and income inequality. Kuznets argues that at the early stages of economic development, income inequality initially rises and only start to decline after a certain level of economic development is reached. Gallup (Citation2012) and Jovanovic (Citation2018) argue that the Kuznets curve works for income inequality progression within the country rather than across countries. Moreover, the financial Kuznets curve is considered as a counterpart of the well-known environmental Kuznets curve, which depicts an inverted U-shaped relationship between measures of environmental degradation and income per capita (Dinda, Citation2004; Moosa, Citation2017; Wang et al., Citation2022).

The financial Kuznets curve symbolizes the excessive finance hypothesis or “the finance curse”, whereby an excessive growth of the financial sector adversely affects the hosting economy. Particularly, an excessively large financial sector competes with real economy sectors for scarce resources and absorb the brightest brains to work in finance, which resembles a brain drain effect. Economists identify two forms of the financial Kuznets curve which are the growth-financial Kuznets curve and the inequality-financial Kuznets curve. The former is graphically represented by an inverted U-shaped curve (similar to the original Kuznets curve) when the economic growth rate is represented as a function of financial development proxy.Footnote1 It follows that the relationship between economic growth and financial development becomes negative (downward sloping) after a threshold, which resembles the case for financialisation.Footnote2 Whereas the latter is represented by a U-shaped curve when income inequality (Gini Index) is represented as a function of financial development proxy.

Greenwood and Jovanovic (Citation1990) were the first to derive on the Kuznets curve and hypothesize the existence of an inverted U-shaped curve between financial development and income inequality. The work on the nonlinearity hypothesis between finance-growth and finance-inequality relationships remains peripheral prior to the global financial crisis (Carré and L’œillet 2018). The pre-crisis literature mainly reports a positive, linear relationship for finance-growth and finance-inequality nexus, with a limited number of studies investigating the nonlinearity hypothesis (Deidda & Fattouh, Citation2002; Rioja & Valev, Citation2004). The new literature, which only comes in the aftermath of the global financial crisis, provides an increasing number of studies that find evidence for nonlinearity between finance-growth and finance inequality relationships, and stress that finance could be “too much” of a good thing (Arcand et al., Citation2015; Beck, Citation2014; Cecchetti & Kharroubi, Citation2012; Denk & Boris, Citation2015).Footnote3

Overall, the interactions between finance, growth, and income inequality are considerably complex and not straightforward. Demirgüç-Kunt and Levine (Citation2009) state that “Yet, we do not have a framework for assessing the dynamic, endogenous relationships among finance, growth, and inequality”. Carré and Guillaume (Citation2018) refers to the finance-growth nexus as a “Gordian Knot”—that is, the relationship is often variable, nonlinear, or insignificant—which also can be drawn to finance-inequality literature. Therefore, it is important to understand nonlinearities in finance-growth and finance-inequality relationships (Beck, Citation2014; Panizza, Citation2018). The literature provides some empirical evidence on nonlinearities between finance, economic growth and income inequality, and the concept of financial Kuznets curve, in the context of developed countries. However, the evidence for emerging (developing) countries remains scarce with a limited number of studies examining this issue (e.g., Kotarski, Citation2015; Nikoloski, Citation2012; Shahbaz et al., Citation2015).

Notwithstanding the vast literature investigating the nexus between financial development, economic growth, and income inequality; only a handful of research publications are investigating this nexus in the Jordanian context, specifically. What’s more, none of these researches has examined the financial Kuznets curve in Jordan. Therefore, we extend the existing literature by providing a robust investigation of the financial Kuznets curve in an emerging country-Jordan.

The contribution of this study is threefold. First, this study provides rigorous empirical evidence on nonlinearity between finance, growth, and income inequality. Hence, this paper provides evidence on whether the financial Kuznets curve exists in Jordan, which, to our knowledge, is not available to date. Second, we examine the relative contribution of financial intermediaries and stock markets to economic growth and income inequality. Third, the application of the unobserved components model is of utmost importance as it accounts for the effect of unspecified variables (missing variables) without the need to identify them explicitly in the model.

2. Literature Review

2.1. Economic growth, income inequality and financial development

There is a long-standing view of the positive contribution of financial development on economic development since the early studies of Bagehot (Citation1873), Schumpeter (Citation1934), and Goldsmith (Citation1969) who stressed the essential role of finance in the real economy. Schumpeter (Citation1934) argued that finance fosters growth by extending “entrepreneurial finance” opportunities. Nevertheless, there remains a contradiction in the views of finance over the past decades. For instance, Nobel laureates Robert Miller and Robert Lucas represents the two extreme views of finance contribution to the real economy. Miller (Citation1998) describes the contribution of finance to growth as “too obvious for a serious discussion”, whereas Lucas (Citation1988) refers to the importance of finance in economic development as “very badly over-stressed”.

The event of the global financial crisis has brought the contribution of finance into question. In his presidential address to the American association of finance, Zingales (Citation2015) argues that ample empirical evidence indicates that some financial-sector components can degenerate to rent-seeking activity. Moreover, thriving literature finds evidence for the negative effects of excessive finance on growth and income equality (Allen et al., Citation2014; Cecchetti & Kharroubi, Citation2012; Panizza, Citation2012).

The current literature on the relationship between financial development and economic development can be divided into three main strands, the first strand posits a favourable effect of financial development on economic growth and income inequality. The second strand shows that finance could have an adverse effect on the real economy in terms of economic growth and income inequality, which is mostly found in the financialisation literature. According to the financialisation literature, the financial sector is harming the real economy by competing for scarce resources, the brain drain from real to financial sectors and accumulation of debt (Hein, Citation2012; Kneer, Citation2013; Sinapi, Citation2013). Finally, the nonlinearity hypothesis literature or what is called “the new literature” refers to the new line of finance-growth research triggered by the global financial crisis to investigate the excessive finance hypothesis (e.g., Arcand et al., Citation2015; Beck, Citation2014; Cournède & Denk, Citation2015; Denk & Boris, Citation2015; Panizza, Citation2018). Different explanations have been provided for the nonlinearity between finance-growth and finance-inequality relationships, pertaining either to the aspects of the financial sector and/or the characteristics of the hosting economy (Khatatbeh, Citation2019; Panizza, Citation2018).

Cecchetti and Kharroubi (Citation2012) reassess finance-growth nexus and find that excessive growth of the financial sector becomes a drag on economic growth, as the financial sector competes with real sectors for resources, which they refer to as the “crowding out” effect. Particularly, they show that the relationship between financial-sector growth and economic growth takes the form of an inverted U-shaped curve. In the same vein, Arcand et al. (Citation2015) find that the financial development effect on economic growth is subject to diminishing marginal returns as the financial system grows beyond a certain threshold. They find this threshold occurs when private credit reaches a level of 100% to GDP. Many successive studies confirmed these results (Beck, Citation2014; Law & Singh, Citation2014; Moosa, Citation2018).Footnote4

Cournède and Denk (Citation2015) contend that an increase in financial activity is associated with an increase in GDP growth, below some threshold; however, the relationship reverses after the threshold. In this sense, the threshold represents a turning point—in terms of financial-sector size (activity) relative to GDP—after which the relationship between finance and growth reverse. The same authors find that the same conclusion could be drawn to the finance–inequality relationship and the threshold estimated about 100% of GDP for intermediated credit and stock market capitalisation (Cournède & Denk, Citation2015; Denk & Boris, Citation2015).

2.2. The Financial Kuznets Curve

The origins of the financial Kuznets curve are ascribed to Greenwood and Jovanovic (Citation1990) who derive on the well-known Kuznets curve and hypothesise the existence of an inverted U-shaped curve between financial development and income inequality. They argue that income inequality tends to increase at the early stages of financial development, where the initial level of income restricts financial structure development needed to enhance growth. From this perspective, only wealthy and politically connected people have access to finance at the early stages of financial development (Rajan & Zingales, Citation2003; Stiglitz, Citation2016). Thus, the low-income class is barred from benefitting from a fully developed financial system, until an adequate level of financial-sector development relaxes credit restraints.

The seminal work of Greenwood and Jovanovic (Citation1990) on nonlinearity between financial development and income inequality has paved the way for successive works on the nonlinearity hypothesis and financial Kuznets curve. Cecchetti and Kharroubi (Citation2012) find evidence for an inverted U-shaped curve between financial development and growth rate. They suggest that the financial sector contributes to economic growth up to a certain threshold, after which further growth of the financial sector hinders economic growth. Cournède and Denk (Citation2015) report similar results for the OECD countries. They find that a disproportionate growth of household credit relative to business credit is harmful to economic growth. Ductor and Grechyna (Citation2015) argue that the nonlinear relationship between financial development and economic growth varies according to the relative growth between financial and real sectors. Law and Singh (Citation2014) examine the nonlinearity between financial development and economic growth in panel data of 87 developed and developed countries. They apply a dynamic panel threshold methodology and find that a further extension of the financial sector beyond the optimal size—as determined by some threshold—as “not necessarily good” for economic growth.

Kim and Lin (Citation2011) apply a threshold regression methodology to a panel data of 65 countries. They suggest that the favourable effect of financial development on income inequality would reverse when the financial development level grows beyond a certain threshold. Law et al. (Citation2014) show that the inequality narrowing effects of financial development are contingent on the level of the country’s institutional quality (measured as an aggregate index of six indicators of the worldwide governance indicators). Therefore, favourable effects of financial development on income inequality are only achieved after a certain level (threshold) of institutional quality is reached.

Economists examine two forms of financial Kuznets curve, which represents the relationship between either economic growth or income inequality on the Y-axis and financial development on the X-axis. Nikoloski (Citation2012) was the first to go by the name of the “financial Kuznets curve” for the Inverted-U shaped curve between financial development and income inequality. He examines Greenwood and Jovanovic’s (Citation1990) hypothesis, using panel data for 76 countries over the period 1962–2006. He finds evidence for an inverted U-shaped relationship between financial development and income inequality and reports a threshold when the ratio of credit to the private sector to GDP rise to around 114%. Brei et al. (Citation2018) and Tan and Law (Citation2012) show that nonlinearity between finance and inequality follows a U-shaped curve. Their results are consistent with the financialization hypothesis, which posits that the relationship between finance and the real economy follows a beneficial to a detrimental path. Moreover, Khatatbeh (Citation2019) shows that there is no universal form of financial Kuznets curve, and some countries’ curves may have more than a turning point (higher-order curve). Many studies report similar evidence for a U-shaped/inverted U-shaped curve of the relationship between financial development and income inequality in different contexts. For example, Kotarski (Citation2015) provide evidence for China, Shahbaz et al. (Citation2015) for Iran, Pata (Citation2020) for Turkey, Jauch and Watzka (Citation2016) and Kavya and Shijin (Citation2020) for a sample of advanced and emerging countries, and Baiardi and Morana (Citation2018) and Akan et al. (Citation2017) for a sample of European countries.

Imad Moosa (Citation2016) examines the growth variant of the financial Kuznets curve using a sample of 95 countries. He finds evidence for the financial Kuznets curve as a form of an inverted U-shaped curve between the real growth rate and the ratio of the market value of publicly traded shares to GDP. He reports different turning points of the curve for High-, Middle- and low-income countries, which occurs at 46%, 30%, 27%, respectively. Baiardi and Morana (Citation2016) examine the effect of financial development on the original Kuznets curve. They suggest that the value of the turning point on the original Kuznets curve is conditioned upon the level of financial development.

2.3. The effect of financial structure on finance-growth and finance–inequality relationships

The literature provides mixed empirical evidence concerning the effect of financial structure (financial intermediaries versus financial markets) on economic growth and income inequality. Nevertheless, financial structure is believed to be a major determinant of the contribution of financial development to economic growth and income inequality, and economists constantly debate in favour of one structure over the other (Levine, Citation2005; Lin et al., Citation2009). On one hand, proponents of the bank-based financial structure suggest that functions performed by banks allow for better risk management and better allocation of resources, which are considered as conducive to economic growth (Levine, Citation2005; Lin et al., Citation2009; Rioja & Valev, Citation2012). Rioja and Valev (Citation2014) examine the impact of financial structure on capital investment in panel data of 62 high- and low-income countries. They conclude that banks foster higher capital growth. Similarly, Zhang and Naceur (Citation2019) suggest that banks rather than financial markets are the main channel through which finance affects income inequality. Brei et al. (Citation2018) find evidence for nonlinearity between finance and inequality, they conclude that market-oriented expansion of the financial sector is associated with rising income inequality, while expansion through traditional banks’ lending is not.

On the other hand, proponents of financial markets suggest that markets provide better informational efficiency and transparency (Brei et al., Citation2018). Many studies find a positive impact of stock market development on economic growth, particularly in developed countries (Beck, Citation2012; Cournède & Denk, Citation2015; Levine & Zervos, Citation1999). Hsieh et al. (Citation2019) find that higher financial development, through the expansion of financial markets, decreases income inequality, whereas it increases income inequality if it happens through the growth of traditional financial intermediaries. Allen et al. (Citation2018) and Levine (Citation2021) provide a comprehensive review of relevant financial structure literature.

2.4. The empirical literature in the context of Jordan

Despite the extant literature on finance-growth and finance-inequality relationships, only a few studies have examined the nexus between finance and economic growth in the Jordanian context. Moreover, we find no research paper that investigates the nexus between financial development and income inequality despite the importance of this subject. Furthermore, none of the reviewed papers investigates the nonlinearity hypothesis (financial Kuznets curve hypothesis) between finance, growth, and inequality in the Jordanian context, specifically.

Only a handful of researches examine the finance-growth nexus in Jordan. For instance, Al-Zubi et al. (Citation2006) examine the link between financial development and economic growth using panel data of eleven Arab countries for the period 1980–2001, including Jordan. They find that all indicators of financial development are insignificant except for the ratio of public credit to domestic credit, which has a positive effect on economic growth. Al-Jarrah et al. (Citation2012) investigate the finance-growth relationship in Jordan during the period 1992 to 2011. They find no evidence for causality between credit to the private sector to GDP ratio and economic growth, although they report a high correlation between financial development indicators and economic growth rate.

Al-naif (Citation2012) investigates whether the relationship between financial development and economic growth in Jordan is supply-leading or demand-pulling to economic growth. He reports a one-directional causality relationship from financial development to economic growth in both the long- and short-run, which suggests that financial development causes economic growth—following the supply leading hypothesis. Batayneh et al. (Citation2021) find that economic growth has a positive short- and long-run effect on financial development. A study by Alrabadi et al. (Citation2016), shows that the relationship between financial development and economic growth is bi-directional when measuring financial development as the ratio of credit to private sector to GDP. Zanella et al. (Citation2021) conduct a broad study to examine finance-growth link in a large sample comprising 108 countries for the period 1980–2017. They find that Jordan as an emerging country corroborates with the “supply-leading hypothesis”, whereby financial development causes economic growth through allowing better access to credit markets for entrepreneurs.

The above-cited studies in the Jordanian context rely mainly on financial intermediation indicators of financial development (banking-sector development indicators). Nevertheless, recent studies have more focus on stock market development variables. A recent study by Jarrar (2021) finds a negative effect of stock market development (measured by stock market total value traded to GDP) on economic growth. Several studies suggest that the Amman stock market needs more development to enhance its contribution to economic growth (Al-Zubi et al., Citation2006; Mugableh, Citation2021).

3. Data and Methodology

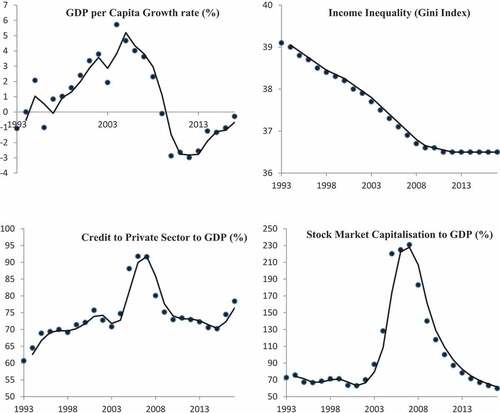

The financial sector in Jordan is considered as the main engine to the Jordanian economy, especially with the lack of natural resources. The current governor central bank of Jordan (CBJ), Dr Ziad Fariz says that “our view is that the growth and success of the Jordanian banking sector is a key driver for the economic development of the country as a whole”.Footnote5 Figure shows time series plots of the main study variables. The main indicators of financial-sector development show a slump after its peak in 2007. The total credit to private sector (CREDIT) has reached about 78% of the GDP in 2017 (the end of the sample period), about 13% less from its peak in 2007. Similarly, the stock market capitalization (SMCAP) is around 60% of GDP in 2017, down from around 230% in 2007.Footnote6 The real GDP growth rate is about 2.1%, compared to the world GDP growth rate of 3.8% in 2017, and the Gini index was hovering moderately around 37 for the past two decades. Descriptive statistics and correlations are exhibited in Tables , respectively.

Figure 1. Time-Series plots of the study variables (1993–2017).

The objective of this study is to investigate the financial Kuznets curve hypothesis in Jordan. For this purpose, we examine the effect of finance on economic growth and income inequality, separately, using time series data from 1993 to 2017.Footnote7 Data series were obtained from the World Bank Development Indicators database (WDI). The proxy for economic growth is real GDP per capita growth rate (Growth), which is the classical choice of finance-growth literature for time-series studies (for example, Cecchetti & Kharroubi, Citation2012; Demetriades & Hussein, Citation1996; Demetriades & Rousseau, Citation2016; King & Levine, Citation1993). The proxy for income inequality is the Gini index (Gini). In addition, the literature reveals a differential impact of financial-sector structure on economic growth and income inequality; therefore, credit to private sector is used as a proxy for bank-sector development and stock market capitalisation is used as a proxy for stock market development. The aforementioned proxies of financial development are measures of the sizes of different components of the financial sector. Levine (Citation2021) argue that these proxies “ do not accurately measure” the concepts that emerge from theories of financial development. Nevertheless, he does not undermine the importance of inferences provided by the existing body of literature using these measures.

We begin by examining the nonlinearity hypothesis between finance-growth and finance-inequality using the variable addition tests to check the linear specification versus the quadratic specification. This is done by testing the significance of adding the quadratic term of financial development proxy to the regression equation. The linear and non-linear functional forms are specified as follows:

where is the dependent variable,

is the financialisation variable, and

is the error term. If the introduction of the quadratic term turns out to be significant, this provides support for the financial Kuznets curve hypothesis (or nonlinearity in general). The Lagrange-Multiplier test (LM), likelihood ratio test (LR), and F-test statistics will be used to judge the significance of adding the quadratic term

.

Following, we estimate the financial Kuznets curve using the unobserved components model (UCM), introduced by Andrew Harvey (Citation1989), which is a form of structural time series model estimated in a time-varying parametric framework (TVP). UCM is used to decompose an observable time series into trend, cyclical and seasonal components, which accounts for any missing variables without the need to express them explicitly, thereby avoiding omitted variables bias, which is bound to be evident in two variables regressions (Moosa, Citation2018). Moreover, it overcomes many traditional obstacles in time series and econometrics analysis as it can be used to represent a time series with any order of integration. In this study, the UCM is specified as follows,

where, is the dependent variable. The terms

represent the trend component.

is the financial development variable, and

is the irregular component. In addition, the trend, which represents the long-run tendency of the time series, is specified as follows,

where and

represent the stochastic level and slope of the trend, respectively. It is assumed that

and

are independent of each other. The empirical analysis is carried out using the STAMP software.Footnote8

Then, this paper investigates the relative importance of banks sector development and stock market development concerning their influence on economic growth and income inequality. For this purpose, we use non-nested model selection tests following Choe and Moosa (Citation1999). Non-nested model selection tests are used to compare rival models with respect to their theoretical underpinnings or auxiliary assumptions (Pesaran, Citation1990). The tests are run both ways (M1 vs M2 and M2 vs M1), where

where is the dependent variable and

and

are proxies of bank-sector development and stock market development, respectively.Footnote9 Six tests are used. (i) the Cox N-test as derived in Pesaran (Citation1974); (ii) the adjusted Cox (NT) test as derived by Godfrey and Pesaran (Citation1983); (iii) the Wald-type (W) test proposed by Godfrey and Pesaran (Citation1983); (iv) the J-test, proposed by Davidson and MacKinnon (Citation1981); (v) the JA-test is due to Fisher and McAleer (Citation1981); and (vi) the encompassing (EN) test proposed, inter alia, by Mizon and Richard (Citation1996). The first five test statistics follow a t-distribution while the encompassing test statistic follows an F-distribution.

Finally, the validity of the financial Kuznets curve hypothesis implies an optimal size of the financial sector, which can be determined as the turning point after which the growth of the financial sector exerts adverse effects on the real economy. Khatatbeh (Citation2019) provides a mathematical exposition of the financial Kuznets curve, which is represented by a quadratic function that takes the following form

Where is a proxy of financialisation (financial development).Footnote10

is the dependent variable, which can be either a proxy of income inequality; when applying the income inequality variant of financial Kuznets curve (e.g., Baiardi & Morana, Citation2018; Nikoloski, Citation2012; Shahbaz et al., Citation2015), or a proxy of economic growth; when applying the economic growth variant of financial Kuznets curve (e.g., Imad Moosa, Citation2016; Moosa, Citation2018). Consequently, Imad Moosa (Citation2016) and Khatatbeh (Citation2019) show that the optimal size of the financial sector, which is implied by the turning point of the curve can be determined by differentiating Equationequation (1)

(1)

(1) above with respect to

and rearranging, which gives

4. Results and Discussion

The first step in our empirical strategy is to examine the nonlinearity hypothesis using variable addition tests. Table displays the results of the variable addition tests that comprises three statistics used to judge the significance of the linear specification versus the quadratic specification, using two proxies of financial development. If these statistics turn out to be significant, this implies that the quadratic specification provides a better model fit for the relationship under examination. Hence, it is an evidence for the nonlinearity of finance-growth and/or finance-inequality relationships, and in turn the financial Kuznets curve hypothesis.

Table 3. Results of the Variable Addition Test (Quadratic versus Linear)

The results displayed in Table lend support to the quadratic specification only in one case, which is the private credit to GDP and Gini index. Therefore, the result provides evidence for non-linearity between finance and income inequality, when using private credit to GDP as a proxy for financial development.

Having found an evidence for potential nonlinearity between finance and income inequality, we continue to estimate the financial Kuznets curve (Equationequation 3(3)

(3) ) using the unobserved components model. The results of UCM are displayed in Table , which shows the estimations result for the two variants of the financial Kuznets curve using two proxies of financial development. Unsurprisingly, there is no evidence for the financial Kuznets curve when using stock market capitalisation to GDP as a proxy of financial development. However, evidence for nonlinearity hypotheses is found for both finance-growth and finance-inequality relationships, when using private credit to GDP as a proxy for financial development. First, evidence for growth financial Kuznets curve, which is represented by an inverted U-shaped curve is revealed by the significant negative quadratic term

, which implies that the expansion of the financial sector following a certain point exerts adverse effects on economic growth. These results lend support to the recent findings of Moosa (Citation2018), Khatatbeh (Citation2019), and Moosa (Citation2018) argues that financial development, as measured by private credit to GDP, exerts a negative effect on the economic growth beyond a certain threshold which gives evidence to the notion of the financial Kuznets curve. He emphasises that in low-income countries, which do not have many resources, a small transfer of resources from the real economic activity to financial activity exerts significant adverse effects on economic growth.

Table 4. Estimation Results of the Unobserved Components Model

Second, evidence for the income inequality variant of the financial Kuznets curve is revealed by the positive significant quadratic term , which implies a U-shaped curve relationship between financial development and income inequality, using private credit to GDP as a proxy for financial development. A U-shaped curve suggests a negative relationship between financial development and income inequality at low levels of financial development, whereas it becomes positive after passing a certain point (turning point), which implies that finance aggravates income inequality at higher levels of financial development. This result is consistent with the recent findings in the literature (Baiardi & Morana, Citation2018, Citation2016; Brei et al., Citation2018; Nikoloski, Citation2012; Shahbaz et al., Citation2015; Tan & Law, Citation2012).

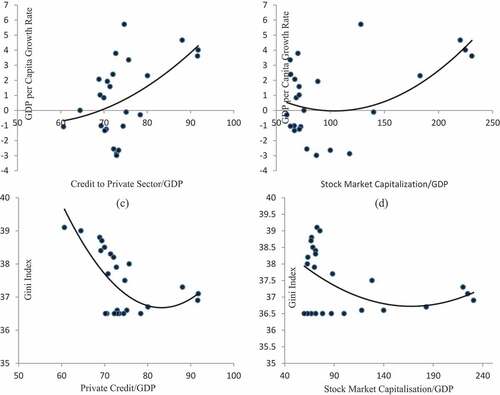

After estimating both variants of the financial Kuznets curve, the turning points can be determined based on equation (9). The turning point for growth financial Kuznets curve is reached when the ratio of private credit to GDP is around 86%. Similarly, the turning point for the inequality financial Kuznets curve is reached when the ratio of private credit to GDP is around 82%.Footnote11 This leaves ample space for “good” growth (development) of the financial sector in Jordan. Remarkably, the estimated values of these turning points are quite close to the average turning point of the ratio of private credit to GDP of 100%, as reported by Arcand et al. (Citation2015) and Cecchetti and Kharroubi (Citation2012). Figure shows a graphical representation of the relationships between financial development indicators on the X-axis and Real GDP growth rate/Gini index on the Y-axis, which is also a representation of the growth financial Kuznets curve (private credit to GDP and real GDP growth rate) and income inequality-financial Kuznets curve (private credit to GDP and Gini index) in panels (a) and (c).

Figure 2. Scatter Plots of the Relationship Between Financial Development Indicators, Real GDP per Capita, and Gini Index (1993–2017).

The second issue under investigation is whether intermediation activities (private credit to GDP) or non-intermediation activities (stock market capitalisation to GDP) of the financial sector are more important to growth and inequality. Non-nested models test can be used to obtain rigorous empirical evidence on this issue by choosing between a model relating economic growth (income inequality) to private credit-to-GDP ratio (Banks Model), and another model relating economic growth (income inequality) to stock market capitalisation-to-GDP ratio (Stocks Model), such in Equationequations (6)(6)

(6) and (Equation7

(7)

(7) ) above. The banks model (M1) is tested against the stocks model (M2), and vice versa. When testing M1 against M2, a significant test statistic implies that M2 is preferred to M1 if the test statistics of M2 against M1 are insignificant, and vice versa.

The results are displayed in Table . Columns group (a) shows that neither model is preferred when relating banks and stocks to economic growth as shown by the insignificant test statistics. This suggests that both models (M1 and M2) are misspecified, and the preferred model should include both variables. Similarly, columns group (b) shows the results of models relating banks and stocks to the Gini index. These results show that when testing M1 against M2, all test statistics are insignificant, however, when testing M2 against M1 are significant. Following the premises mentioned in the methodology section, the results overwhelmingly reject M1 against M2 but do not reject M2 against M1, which suggests that M1 is a preferred to M2 model when relating to the Gini index. This can be taken as evidence that banks (intermediation activities) play a more important role in income inequality than the stock market does. This is not a surprising result as the stock market capitalisation of the Amman stock exchange was descending following its peak in 2007, reaching unprecedented new lows.Footnote12 Gimet and Lagoarde-Segot (Citation2011) and Zhang and Naceur (Citation2019) argue that banks have a stronger effect on income inequality. Beck et al. (Citation2007) find that financial development (credit to private sector to GDP) reduces income inequality and boost the share of the poorest quintile of the population. These results may be seen in line with the evidence put forward by Choe and Moosa (Citation1999), Beck (Citation2014), and Sturn and Zwickl (Citation2016).

Table 5. Results of Non-Nested Model Selection Tests

The evidence for the financial Kuznets curve in Jordan has far-reaching policy implications. The excessive growth of the financial sector beyond a certain point creates systemic risk and generates economic rents through the transfer of income from the productive economy. Hence, the concentration of power in the hands of the financial sector must be reversed to prevent the crowding-out effect (Cecchetti & Kharroubi, Citation2015) and brain drain effect (Kneer, Citation2013) caused by the “too much” finance. To achieve this objective, Khatatbeh and Moosa (Citation2021) suggest that giant financial institutions should be reduced in size by break-up or deleveraging. Moreover, increasing credit access for small businesses and low-income households by creating public financial institutions, which also will increase the competitiveness and efficiency of the private financial institution as they lose market power.

5. Conclusions

The significant contributions of financial development to economic growth and income inequality are well established in the literature. However, recent findings suggest that excessive finance can be “too much of a good thing”, and adversely affects the hosted economy. In this paper, we investigate the notion of the financial Kuznets curve in the Jordanian context using different time-series methodologies. The empirical results presented above suggests four main conclusions: (i) the variable addition tests suggest evidence for nonlinearity between finance and inequality, when using private credit to GDP as a proxy for financial development, (ii) empirical evidence is found for both variants of financial Kuznets curve when using private credit to GDP as a proxy for financial development, (iii) the existence of financial Kuznets curve suggest a turning point after which an expansion of the financial sector will adversely affect economic growth and income inequality, which are estimated to be reached when the private credit to GDP ratio exceeds 86% for growth financial Kuznets curve, and 82% for inequality financial Kuznets curve, and (iv) financial intermediaries (banks and other financial institutions) are relatively more important than stock markets for income inequality.

The current level of financial development in Jordan remains below the reported threshold, therefore, Jordan has ample space for further financial development to boost economic growth and reduce income inequality. Moreover, policymakers in Jordan should call into question the performance and contribution of the Amman stock exchange to enhancing economic growth and income equality. We believe that the development of Jordanian financial markets is the way forward to reap the benefits of growth and enhance income distribution. Furthermore, policymakers should also consider encouraging a balanced growth between financial and real sectors as a remedy to avoid the “too much” finance problem, particularly, they must aim to reduce the concentration of power in the financial sector to reduce income inequality and economic vulnerability and creating public-financial institutions that provides affordable credit to small businesses and households. Finally, the findings of this paper also suggest that the financial Kuznets curve may also exist in developing (emerging) countries. Future research may focus on other aspects of nonlinearity between finance, economic growth and income inequality as identified in Panizza (Citation2018). For example, the nonlinearity may arise from the type of finance, as household’s and firms’ debts grow disproportionately.

Correction

This article has been republished with minor changes. These changes do not impact the academic content of the article.

Acknowledgement

We are grateful to the editor and two anonymous referees for useful comments.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Ibrahim N. Khatatbeh

Ibrahim N. Khatatbeh is an assistant professor of finance at the Hashemite University, Jordan. He obtained a PhD in finance from RMIT University, Australia. His main research interests are in multidisciplinary research and His work has been published in several fields including finance, insurance, and public policy.

Wasfi Al Salamat

Wasfi Al Salamat is an associate professor of finance at the Hashemite University, Jordan. He received a PhD in Finance from the University of Wales at Bangor, UK. His research interests are Corporate Finance; Financial Economics; Dividend Policy; Capital Structure; and Financial Analysis.

Mohammed N. Abu-Alfoul

Mohammed N. Abu-Alfoul has a PhD in Economics from Swinburne University of Technology, Australia. His research interests are economic growth, informal economy, and econometrics.

Jamil J. Jaber

Jamil J. Jaber is an academic staff at the University of Jordan-Aqaba branch, Jordan. He has a PhD in actuarial statistics and financial risk management from the National University of Malaysia, Malaysia. His research interests are actuarial statistics, financial risk management, and risk modelling.

Notes

1. Mostly, economists use the ratio of credit to private sector to GDP or the ratio of stock market capitalisation to GDP as proxies for financial development or financialisation. Imad Moosa (Citation2016) used the ratio of publicly traded shares to GDP as a proxy for financialisation.

2. Moosa (Citation2018) contends that financialisation is the later stage of financial development, when the financial sector becomes excessively large and starts to exert negative consequences of the real economy. See, for Imad Moosa (Citation2016), Moosa (Citation2018).

3. The “new literature” refers to the new line of finance-growth research triggered by the global financial crisis to investigate the excessive finance hypothesis (Panizza, Citation2014).

4. Arcand et al. (Citation2015) were first published in 2012 as a working paper.

5. https://leadingedgeguides.com/guide-Jordan-2018-shock-proof-financial-sector/, Accessed September1st, 2021

6. Central Bank of Jordan (CBJ), Financial Stability Report (2018). https://www.cbj.gov.jo/EchoBusv3.0/SystemAssets/PDFs/EN/JFSR2018E%20-20-10-2019.pdf. Accessed September 1st, 2021

7. The data series ends in 2017 because of data availability issues related to Gini coefficient.

8. Mendelssohn (Citation2011) provide a review of the STAMP software.

9. Banks is a shortened name for “banks and other financial institutions”

10. Financialisation is an alternative term of financial development that is generally used when referring to the negative effect of the financial sector. However, in some strands of finance literature, financialisation and financial development are used interchangeably.

11. It is worth mentioning that the above estimated turning points have never been crossed-over in Jordan during the sample period except for years 2005 to 2007.

12. When measured relative to GDP, for example, the stock market capitalisation to GDP were hovering just over 60% in 1990s, whereas it plummeted to below 60% by the end of the sample period in 2017. Also, it is worth noting the stock market capitalisation to GDP had reached 230% in 2007.

References

- Akan, Y., Köksel, B., & Destek, M. A. (2017). The financial kuznets curve in European Union. EconWorld2017 at rome proceedings, Rome, Italy, (pp. 25–17).

- Al-Jarrah, I., Al-Zu’bi, M. F., Jaara, O., & Alshurideh, M. (2012). Evaluating the impact of financial development on economic growth in Jordan. International Research Journal of Finance and Economics, 94(2012), 123–139.

- Al-naif, K. L. (2012). Causality relationship between financial development and economic growth in Jordan: Supply-leading and demand-pulling hypotheses test. Middle Eastern Finance and Economics, 16(16), 1000–1009.

- Al-Zubi, K. M., AM Al-Rjoub, S., & Abu-Mhareb, E. (2006). Financial development and economic growth: A new empirical evidence from the MENA countries, 1989-2001. Applied Econometrics and International Development, 6(3), 139–150.

- Allen, F., Carletti, E., Qian, J., & Valenzuela, P. (2014). Does finance accelerate or retard growth? theory and evidence.

- Allen, F., Xian, G., & Kowalewski, O. (2018). Financial structure, economic growth and development. In Thorsten Beck and Ross Levine (Ed.), Handbook of finance and development (pp. 31–62). Edward Elgar Publishing, Inc Cheltenham.

- Alrabadi, D., Hanna, W., & Kharabsheh, B. A. (2016). Financial deepening and economic growth: The case of Jordan. Journal of Accounting and Finance, 16(6), 158. https://articlegateway.com/index.php/JAF/article/view/1067

- Arcand, J. L., Berkes, E., & Panizza, U. (2015). Too much finance? Journal of Economic Growth, 20(2), 105–148. https://doi.org/10.1007/s10887-015-9115-2

- Bagehot, W. (1873). Lombard Street: A description of the money market. HS King.

- Baiardi, D., & Morana, C. (2016). The financial kuznets curve: Evidence for the euro area. Journal of Empirical Finance, 39(December), 265–269. https://doi.org/10.1016/j.jempfin.2016.08.003

- Baiardi, D., & Morana, C. (2018). Financial development and income distribution inequality in the euro area. Economic Modelling, 70(April), 40–55. https://doi.org/10.1016/j.econmod.2017.10.008

- Batayneh, K., Salamat, W. A., Momani, M. Q. M., & McMillan, D. (2021). The impact of inflation on the financial sector development: Empirical evidence from Jordan. Cogent Economics & Finance, 9(1), 1970869. https://doi.org/10.1080/23322039.2021.1970869

- Beck, T. (2012). The role of finance in economic development–benefits, risks, and politics. In Dennis C. Mueller (Ed.), Oxford handbook of capitalism (pp. 161–203). Oxford’s University Press.

- Beck, T. (2014). Finance and growth: Too much of a good thing. Revue d’économie du développement, 22(HS02), 67–72. https://www.cairn.info/revue-d-economie-du-developpement-2014-HS02-page-67.html

- Beck, T., Demirgüç-Kunt, A., & Levine, R. (2007). Finance, inequality and the poor. Journal of Economic Growth, 12(1), 27–49. Bank for International Settlements. https://doi.org/10.1007/s10887-007-9010-6

- Brei, M., Ferri, G., & Gambacorta, L. 2018. Financial structure and income inequality. In BIS working papers No 756.

- Carré, E., & Guillaume, L. (2018). The literature on the finance–growth nexus in the aftermath of the financial crisis: A review. Comparative Economic Studies, 60(1), 161–180. https://link.springer.com/article/10.1057/s41294-018-0056-6

- Cecchetti, S. G., & Kharroubi, E. (2012). Reassessing the impact of finance on growth. In BIS WP 381. Bank for International Settlements.

- Cecchetti, S. G., & Kharroubi, E. (2015). Why does financial sector growth crowd out real economic growth? In BIS WP 490. Bank for International Settlements.

- Choe, C., & Moosa, I. A. (1999). Financial system and economic growth: The Korean Experience. World Development, 27(6), 1069–1082. https://doi.org/10.1016/S0305-750X(99)00042-X

- Christensen, J., Shaxson, N., & Wigan, D. (2016). The finance curse: Britain and the world economy. The British Journal of Politics and International Relations, 18(1), 255–269. https://doi.org/10.1177/1369148115612793

- Cournède, B., & Denk, O. (2015). Finance and economic growth in OECD and G20 countries. OECD Economics Department Working Papers, No. 1223, OECD Publishing, Paris. https://doi.org/10.1787/5js04v8z0m38-en

- Davidson, R., & MacKinnon, J. G. (1981). Several tests for model specification in the presence of alternative hypotheses. Econometrica: Journal of the Econometric Society, 49(3), 781–793. https://doi.org/10.2307/1911522

- Deidda, L., & Fattouh, B. (2002). Non-linearity between finance and growth. Economics Letters, 74(3), 339–345. https://doi.org/10.1016/S0165-1765(01)00571-7

- Demetriades, P. O., & Hussein, K. A. (1996). Does financial development cause economic growth? Time-series evidence from 16 countries. Journal of Development Economics, 51(2), 387–411. https://doi.org/10.1016/S0304-3878(96)00421-X

- Demetriades, P. O., & Rousseau, P. L. (2016). The changing face of financial development. Economics Letters, 141(April), 87–90. https://doi.org/10.1016/j.econlet.2016.02.009

- Demirgüç-Kunt, A., & Levine, R. (2009). Finance and inequality: Theory and evidence. Annu. Rev. Financ. Econ, 1(1), 287–318. https://doi.org/10.1146/annurev.financial.050808.114334

- Denk, O., & Boris, C. (2015). Finance and income inequality in OECD countries. OECD Economics Department Working Papers, No. 1224, OECD Publishing, Paris. https://doi.org/10.1787/5js04v5jm2hl-en

- Dinda, S. (2004). Environmental kuznets curve hypothesis: A survey. Ecological Economics, 49(4), 431–455. https://doi.org/10.1016/j.ecolecon.2004.02.011

- Ductor, L., & Grechyna, D. (2015). Financial development, real sector, and economic growth. International Review of Economics & Finance, 37(May), 393–405. https://doi.org/10.1016/j.iref.2015.01.001

- Fisher, G. R., & Michael, M. (1981). Alternative procedures and associated tests of significance for non-nested hypotheses. Journal of Econometrics, 16(1), 103–119. https://doi.org/10.1016/0304-4076(81)90078-6

- Gallup, J. L. (2012). Is there a kuznets curve. 575-603. Portland State University.

- Gimet, C., & Lagoarde-Segot, T. (2011). A closer look at financial development and income distribution. Journal of Banking & Finance, 35(7), 1698–1713. https://doi.org/10.1016/j.jbankfin.2010.11.011

- Godfrey, L. G., & Hashem Pesaran, M. (1983). Tests of non-nested regression models: Small sample adjustments and monte carlo evidence. Journal of Econometrics, 21(1), 133–154. https://doi.org/10.1016/0304-4076(83)90123-9

- Goldsmith, R. W. (1969). Financial structure and development. New Haven, Conn: YaleUniversity Press.

- Greenwood, J., & Jovanovic, B. (1990). Financial development, growth, and the distribution of income. Journal of Political Economy, 98(5, Part 1), 1076–1107. https://doi.org/10.1086/261720

- Harvey, A. C. (1989). Forecasting, structural time series models and the kalman filter. Cambridge University Press, Cambridge.

- Hein, E. (2012). The macroeconomics of finance-dominated capitalism and its crisis. Edward Elgar Publishing, Inc Cheltenham, UK and Northampton, MA, USA.

- Hsieh, J., Chen, T.-C., & Lin, S.-C. (2019). Financial structure, bank competition and income inequality. The North American Journal of Economics and Finance, 48(April), 450–466. https://doi.org/10.1016/j.najef.2019.03.006

- Jarrar, F., & Suleiman, A. (2021). The impact of stock market development on economic growth in Jordan. Journal of Applied Economic Sciences (JAES), 16(71), 57–73. A recent study by Jarrar (2021) finds a negative effect of stock market development (measured by stock market total value traded to GDP).

- Jauch, S., & Watzka, S. (2016). Financial development and income inequality: A panel data approach. Empirical Economics, 51(1), 291–314. https://doi.org/10.1007/s00181-015-1008-x

- Jovanovic, B. (2018). When is there a kuznets curve? some evidence from the ex-socialist countries. Economic Systems, 42(2), 248–268. https://doi.org/10.1016/j.ecosys.2017.06.004

- Kavya, T. B., & Shijin, S. (2020). Economic development, financial development, and income inequality nexus. Borsa Istanbul Review, 20(1), 80–93. https://doi.org/10.1016/j.bir.2019.12.002

- Khatatbeh, I. N. (2019). The macroeconomic consequences of financialisation. RMIT University.

- Khatatbeh, I. N., & Moosa, I. A. (2021). Financialization and income inequality: An extreme bounds analysis. The Journal of International Trade & Economic Development, 1–16. https://doi.org/10.1080/09638199.2021.2005668

- Kim, D.-H., & Lin, S.-C. (2011). Nonlinearity in the financial development–income inequality nexus. Journal of Comparative Economics, 39(3), 310–325. https://doi.org/10.1016/j.jce.2011.07.002

- King, R. G., & Levine, R. (1993). Finance and growth: Schumpeter might be right. The Quarterly Journal of Economics, 108(3), 717–737. https://doi.org/10.2307/2118406

- Kneer, C. (2013). Finance as a magnet for the best and brightest: Implications for the Real Economy. De Nederlandsche Bank, Working paper 392.

- Kotarski, K. (2015). Financial deepening and income inequality: Is there any financial kuznets curve in China? The political economy analysis. China Economic Journal, 8(1), 18–39. https://doi.org/10.1080/17538963.2015.1001051

- Kuznets, S. (1955). Economic growth and income inequality. The American Economic Review, 45(1), 1–28.

- Law, S. H., & Singh, N. (2014). Does too much finance harm economic growth? Journal of Banking & Finance, 41(April), 36–44. https://doi.org/10.1016/j.jbankfin.2013.12.020

- Law, S. H., Tan, H. B., & Azman-Saini, W. N. W. (2014). Financial development and income inequality at different levels of institutional quality. Emerging Markets Finance and Trade, 50(sup1), 21–33. https://doi.org/10.2753/REE1540-496X5001S102

- Levine, R. (2005). Chapter 12 finance and growth: Theory and evidence. In Philippe Aghion, Steven N. Durlauf (Ed.), Handbook of Economic Growth, 1(Part A), 865–934. https://doi.org/10.1016/S1574-0684(05)01012-9

- Levine, R. (2021). Finance. Growth, and Inequality.

- Levine, R., & Zervos, S. (1999). Stock markets, banks. and economic growth: The World Bank.

- Lin, J. Y., Sun, X., & Jiang, Y. (2009). Toward a theory of optimal financial structure: The world bank. (pp. 5038).

- Lucas, R. E. (1988). On the mechanics of economic development. Journal of Monetary Economics, 22(1), 3–42. https://doi.org/10.1016/0304-3932(88)90168-7

- Mendelssohn, R. (2011). The STAMP software for state space models. Journal of Statistical Software, 41(2), 1–18. https://doi.org/10.18637/jss.v041.i02

- Miller, M. H. (1998). Financial markets and economic growth. Journal of Applied Corporate Finance, 11(3), 8–15. https://doi.org/10.1111/j.1745-6622.1998.tb00498.x

- Mizon, G. E., & Richard, J.-F. (1996). The encompassing principle and its application to testing non-nested hypotheses. Econometrica: Journal of the Econometric Society, 12(5), 845–858. https://doi.org/10.2307/1911313

- Moosa, I. (2016). International evidence on the financial kuznets curve. Economia Internazionale/International Economics, 69(4), 365–378.

- Moosa, I. A. (2017). The econometrics of the environmental Kuznets curve: An illustration using Australian CO2 emissions. Applied Economics, 49(49), 4927–4945. https://doi.org/10.1080/00036846.2017.1296552

- Moosa, I. A. (2018). Does financialization retard growth? Time series and cross-sectional evidence. Applied Economics, 50(31), 3405–3415. https://doi.org/10.1080/00036846.2017.1420899

- Mugableh, M. I. (2021). Causal links among stock market development determinants: Evidence from Jordan. The Journal of Asian Finance, Economics and Business, 8(5), 543–549. https://doi.org/10.13106/jafeb.2021.vol8.no5.0543

- Nikoloski, Z. (2012). Financial sector development and inequality: Is there a financial kuznets curve? Journal of International Development, 25(7), 897–911. https://doi.org/10.1002/jid.2843

- Panizza, U. (2012). Finance and economic development. In International development policy: Aid, emerging economies and global policies (pp. 141–160). London: Palgrave Macmillan UK.

- Panizza, U. (2014). Financial development and economic growth: Known knowns, known unknowns, and unknown unknowns. Revue d’économie du développement, 22, (HS02):35–65. https://www.cairn.info/revue-d-economie-du-developpement-2014-HS02-page-35.html

- Panizza, U. (2018). Nonlinearities in the relationship between finance and growth. Comparative Economic Studies, 60(1), 44–53. https://doi.org/10.1057/s41294-017-0043-3

- Pata, U. K. (2020). Finansal Gelişmenin Gelir Eşitsizliği Üzerindeki Etkileri: Finansal Kuznets Eğrisi Hipotezi Türkiye İçin Geçerli mi? Atatürk Üniversitesi İktisadi ve İdari Bilimler Dergisi, 34(3), 809–828. https://doi.org/10.16951/atauniiibd.648695

- Pesaran, M. H. (1974). On the general problem of model selection. The Review of Economic Studies, 41(2), 153–171. https://doi.org/10.2307/2296710

- Pesaran, M. H. (1990). Non-nested hypotheses. In J. Eatwell, M. Milgate, & P. Newman (Eds.), Econometrics (pp. 167–173). Palgrave Macmillan UK.

- Rajan, R. G., & Zingales, L. (2003). The great reversals: The politics of financial development in the twentieth century. Journal of Financial Economics, 69(1), 5–50. https://doi.org/10.1016/S0304-405X(03)00125-9

- Rioja, F., & Valev, N. (2004). Does one size fit all?: A reexamination of the finance and growth relationship. Journal of Development Economics, 74(2), 429–447. https://doi.org/10.1016/j.jdeveco.2003.06.006

- Rioja, F., & Valev, N. (2012). Financial structure and capital investment. Applied Economics, 44(14), 1783–1793. https://doi.org/10.1080/00036846.2011.554376

- Rioja, F., & Valev, N. (2014). Stock markets, banks and the sources of economic growth in low and high income countries. Journal of Economics and Finance, 38(2), 302–320. https://doi.org/10.1007/s12197-011-9218-3

- Schumpeter, J. A. (1934). The theory of economic development. Harvard University Press, Cambridge.

- Shahbaz, M., Loganathan, N., Tiwari, A. K., & Sherafatian-Jahromi, R. (2015). Financial development and income inequality: Is there any financial Kuznets curve in Iran? Social Indicators Research, 124(2), 357–382. https://doi.org/10.1007/s11205-014-0801-9

- Sinapi, C. (2013). The role of financialization in financial instability: A post-Keynesian institutionalist perspective. Limes Plus, 9(3), 207–232. https://www.ceeol.com/search/article-detail?id=497434

- Stiglitz, J. E. (2016). New theoretical perspectives on the distribution of income and wealth among individuals. In Kaushik Basu and Joseph E. Stiglitz (Ed.), Inequality and growth: Patterns and policy (pp. 1–71). Springer.

- Sturn, S., & Zwickl, K. (2016). A reassessment of intermediation and size effects of financial systems. Empirical Economics, 50(4), 1467–1480. https://doi.org/10.1007/s00181-015-0979-y

- Tan, H.-B., & Law, S.-H. (2012). Nonlinear dynamics of the finance-inequality nexus in developing countries. The Journal of Economic Inequality, 10(4), 551–563. https://doi.org/10.1007/s10888-011-9174-3

- Wang, Q., Wang, X., & Rongrong, L. (2022). Does urbanization redefine the environmental Kuznets curve? An empirical analysis of 134 Countries. Sustainable Cities and Society, 76(January), 103382. https://doi.org/10.1016/j.scs.2021.103382

- Zanella, F., Oyelere, P., & McMillan, D. (2021). Is financial development crucial for all economies? Cogent Economics & Finance, 9(1), 1923883. https://doi.org/10.1080/23322039.2021.1923883

- Zhang, R., & Naceur, S. B. (2019). Financial development, inequality, and poverty: Some international evidence. International Review of Economics & Finance, 61(May), 1–16. https://doi.org/10.1016/j.iref.2018.12.015

- Zingales, L. (2015). Presidential address: Does finance benefit society? The Journal of Finance, 70(4), 1327–1363. https://doi.org/10.1111/jofi.12295