?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This article assesses the opinions of youth tomato growers on the accessibility of agricultural credit and factors that influence the accessibility in the Democratic Republic of the Congo (DRC). Data originated from a household survey for the 2019/2020 farming season. We interviewed 218 youth tomato growers from 6 horticulture production zones in the South-Kivu, eastern DRC. The result reveals a low rate of 20.6% on accessing agricultural credit among tomato growers. The topmost nature of agricultural credit received was cash-based, mostly from informal sources of finance (92.7%). The findings reveal that the lack of information on agricultural credit, the fear of credit default, and the absence of Microfinance Institutions in the study areas were the highest-ranking factors hindering tomato growers from accessing agricultural credit services. Our probit model shows that total household income, gender, and tomato growers’ membership in a cooperative were essential factors that explain the probability of accessing agricultural credit. We recommend formalising the agricultural credit system by improving agri-finance extension service delivery to associations of tomato growers among the young to access and use agricultural microcredit services effectively to enhance agricultural production, which is a proxy for rural employment creation and poverty reduction.

PUBLIC OF INTEREST STATEMENT

The vegetable business size towards tomato production chain for the last two decades have increased in the Eastern DR. Congo, despite its exogenous dependence on importations from neighbouring countries. Perceived as an opportunity for youth job creation along the tomato production chain, the country’s agriculture policy and the private organization’s partners in promoting youth farmers towards horticulture production chain to enable both rural and urban youths to get well employed along with various niches of the production chain. This is through access to agricultural modern inputs and financial transactions. Despite such initiatives, agricultural credit accessibility is still yet low. We debate in the current paper that socioeconomic and institutional factors were relevant in explaining the level of credit accessibility among youth tomato farmers, which before have not been studied. The realistic findings emphasize the importance of considering such factors when designing a sustainable agricultural financial credit delivery model.

1. Introduction

Many factors inhibit small-scale farmers’ potential to be efficient in their farming activities in developing countries. Among others, market failure of agricultural finance has been identified among the key factors (Weber & Musshoff, Citation2012). Besides, rudimentary agricultural techniques and inadequate agricultural production chains are also factors that alleviate productivity in the sector (Weber & Musshoff, Citation2012; M. Tadesse, Citation2014). In Africa, most impoverished people still live in rural areas and primarily work on smallholder subsistence farms for their livelihoods (McArthur & Sachs, Citation2018). Therefore, increased agricultural productivity should increase the income of the rural population, which will boost the demand for non-agricultural products, including industrial goods and services (Badibanga & Ulimwengu, Citation2019). According to the World Bank (Citation2011), the Democratic Republic of the Congo (DRC), is endowed with substantial agricultural potential with 80 million ha of arable land, of which 4 million are irritable, climatic diversity and abundant water. These characteristics enable two annual harvests of various crops and pasture resources to support an estimated 40 million cattle or equivalent. Despite the great potential of being a food basket in Africa (Tollens, Citation2015), DRC has failed to make substantial investments and policy changes to achieve this potential.

Previous research supports the idea that credit access is an essential catalyst in determining the productivity and growth of many businesses, including horticulture farming (Kuwornu et al., Citation2012; Nouman et al., Citation2013). Also, Chandio et al.’s (Citation2021)’ study confirm that formal agricultural credit has a positive and significant impact on sugarcane yield in Pakistan. According to M. Tadesse (Citation2014), credit service is considered more than just another source of inputs because it determines the access to the vital resources for farmers such as land, labour and farming implements. Therefore, agricultural credit and financial education are the first steps in revamping agricultural development and production efficiency (Sileshi et al., Citation2012).

In the Democratic Republic of the Congo, the horticulture sector has always been dominated by small-scale farmers producing for subsistence and commercial purposes (FA0, Citation2011). The agricultural industry is a critical component in supporting more than 75% of its population (IITA, Citation2019). It accounted for about 53% of the GDP (Gross Domestic Production) and represented 66% of employment in 2003 (IITA, Citation2019). The sector has the potential of reducing rural poverty if it receives the needed financial resources. Access to agricultural financial credit in the DRC has many challenges. They include the lack of financial education among smallholder farmers, weakness and lack of appropriate financial products from financial service Providers and the lack of collateral schemes from the government.

According to Meyer (Citation2011), poor access to agricultural financial credit might be attributed to the risks associated with the agricultural sector, particularly among smallholder farmers. These farmers lack collateral to secure credit facilities, coupled with farmers’ misuse of the agricultural credit. Consequently, it fails to achieve its full impact on productivity and ultimately impede their livelihood (Nouman et al., Citation2013). Nonetheless, tomato growers in many parts of the country, including the Ruzizi plain of DRC, are mainly constrained by inadequate access to credit to carry on with their activities. Moreover, the importance of credit in improving farm productivity depends on availability and accessibility and how the credit is allocated. In the same spirit, Saqib et al. (Citation2018) confirm that agricultural credit is an essential input with modern technologies for increased farm productivity.

Therefore, the current study seeks to analyse factors affecting access to agricultural financial credit of youth tomato growers and their perception towards credit uses in the horticulture subsector. Although many existing scientific pieces of research have closely studied the related matters of agricultural finance and explored the related risk that creates difficulties for farmers to access credit (Langat, Citation2013; Olusanya, Citation2012; Sebatta et al., Citation2014), banks compliances and bureaucracy towards agriculture credit access (Kiplimo et al., Citation2015), the importance of various socioeconomics (Kiros et al., Citation2022) and institutional (Chandio, Jiang, Rehman, Twumasi et al., Citation2021) factors whichfactors that explain access to finance for smallholder farmers has not been investigated intensively in sub-Saharan African countries.

The current study sheds light on the status in credit participation of tomato youth growers and helps microfinance institutions to understand farmers’ credit utilisation. Our findings would inform policymakers on the challenges faced by youth tomato growers to access financial credit. Therefore, enabling a driver of farm-level financial policies implementation that improves the capital utilisation of credit in the agricultural sector. The major purpose of this paper is to empirically investigate the factors influencing smallholder farmers’ credit access in the Democratic Republic of Congo (DRC) by using econometric analysis

1.1. Relevant literature review

There is a considerable number of research related to access to financial credit for small-scale farmers. They mostly link socio-economic and institutional factors that determine smallholder farmers’ credit access from one region to another (Chandio, Jiang, Rehman, Twumasi et al., Citation2021; Dube et al., Citation2015; Kiplimo et al., Citation2015; Muayila & Tollens, Citation2012). Other scholars focused on agriculture credit access analysis and agriculture productivity (Ahmad, Citation2011; Chandio, Jiang, Rehman, Akram et al., Citation2021; Chandio et al., Citation2018), or the adoption of improved agriculture (Anang et al., Citation2015). Finally, we identified another set of research that focuses on the relationship between farmers’ access to credit and climate change impacts on agriculture (Chandio et al., Citation2020; Gul et al., Citation2021, Citation2022; Rehman et al., Citation2021, Citation2019)

According to Liu et al. (Citation2019), the currently observed mutations in rural-urbanization and changes in agricultural demand for financial resources have created many unexpected problems in the agriculture ecosystem and, in its various mechanical engineering activities. However, in the financial globalization stages, access to credit, commodities, resources, and intelligence have quickly improved from one nation in the world to another (Dong et al. Citation2019; Lee and Min Citation2014). The climate-smart agronomy techniques, together with the soil characteristics and environmental factors, both of which lead to mitigating greenhouse gases, include adequate irrigation, cultivation, drainage, and fertilizer application. Considering the observed extent in the adoption of improved agriculture technologies, varieties of crops and the enhanced modern cropping systems has led to an increase in demand for agricultural inputs a proxy for the rising of credit demand among smallholder farmers. While to date, in DRCongo the limit towards accessing financial credit by small scalesmall-scale farmers continues to be the topmost binding problem that effectively hinders agriculture productivity. Using the non-parametric method known as the Propensity Score Matching in assessing the effects of credit restrictions on farm household welfare, Muayila and Tollens (Citation2012) in their study conducted in the Democratic Republic of Congo (DRC) reported that 71% of the farm households experienced credit constraints, and hence lower their welfare outcomes than unconstrained households. However, the Socioeconomics factors towards accessing credit among small scalesmall-scale farmers in Bangladesh have been studied by Hossain and Bayes (Citation2009) and reported the selected credit collateral based on land size was significant to access the needed credit, and that only 1.5% of the farmers who own less than 0.20 ha land had access to bank credit, while for those owning more than 2.0 ha land the proportion is 20%.

Also, a number of studies have been carried out regarding agricultural credit, particularly in developing countries like India, Bangladesh, Pakistan, Nigeria, Congo, Ghana, etc. Most of these non-experimental and observational studies regarding agricultural credit found that the availability of informal and formal credit by the farmers has a significant effect on agriculture ventures. Considering the example of India, (Kumar et al., (Citation2010) found that agricultural credit has a positive treatment effect on an indicator of farmers’ wealth. While Shah and Khan (Citation2008) reported a positive relationship between farm productivity and agricultural credit in the context of a backward district in Northern Pakistan. Also, Saqib et al. (Citation2018) studied the variances in access to and utilization of agricultural credit among smallholder farmers in the Mardan district in Pakistan while considering data extracted from 87 farmers’ household surveys. They reported a positive and significant relationship between the large land farm size and access and utilization of agriculture credit, and the years of schooling, years of farming experience and landholding size were significant factors that explained accessibility on credit.

Wakilur et al. (Citation2011) also came up with evidence of a strong positive correlation between agricultural credit at reasonable cost and agricultural production. There are quite a lot of scientific papers and reports suggesting that the lack of access to credits by farmers has unfavourable effects on the agriculture subsector. As argued by Carter (Citation2008), credit affects agricultural performance by relaxing the working capital constraints, inducing farmers to adopt the new modern technologies and the intensive use of fixed resources.

The recent literature related to the study of Chandio et al. (Citation2021) revealed that formal education, the experience of farming, landholding size, road access and extension contacts positively and significantly influenced the demand for formal credit in Sindh, Pakistan. In addition, in the same study area, the conclusions of Chandio, Jiang, Rehman, Akram et al. (Citation2021)’ study confirmed a positive impact of formal credit on sugarcane productivity, i.e credit access and use in the production process can enhance the crop production and overall income of the farmers. Kiros et al. (Citation2022), while studying the factors affecting farmers’ access to formal financial credit in Basona Worana District, found that some variables such as education status, experience on credit use, livestock ownership, distance from lending institutions were not significant contrary to other previous studies (Hossain & Bayes, Citation2009; Saqib et al., Citation2018).

A closer look at the above findings attests that agriculture credit failure mechanism for rationing farmers, limited their access to and participation in credit services are common challenges across the different regions, despite its significant role to revamp the agriculture subsector’s productivity. However, very little work has been done on the factors and constraints that influence the access and uses of agriculture credit among youth farmers in the context of the DRC. Therefore, our study aims at filling this research gap.

The remainder of this research is organised as follows: Section 2 presents the methodology, Section 3 presents the results, and Section 4 discusses the findings.

2. Methodology

2.1. Description of the study area

Study area

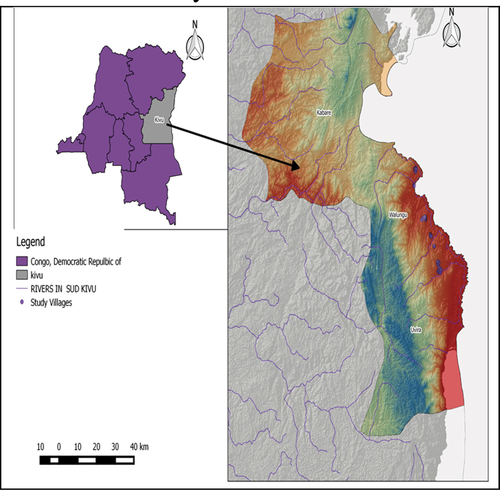

The current study is carried out in Ruzizi Plain County, DRCongo. Ruzizi Plain County is a share of agricultural land of175000Hectares between DRCongo, Burundi, and Rwanda, where the share of the DRCongo is estimated at 45.7% of the land, which represents the study area of the current research. The county has been selected due to its attractiveness in tomato production in the region and, most of the youth farmer population relying on this crop, as a crucial source of their income. Based on the 2009 censuscensus, the total population was estimated at245000habitantsat 245,000 habitants.

Sampling procedure and Sample Size

This study employs a cross-sectional research design, according to Bryman and Cramer (Citation2011), as the research design used to obtain an overall picture of what is happening in a group at a particular point in time. Furthermore, the study used the Multistage sampling procedure to select the youth tomato farmers in the study area, and this is based on the four Multistage samplings. The first stage is purposively selecting the Ruzizi Plain county of South-Kivu, DRCongo, because of the predominance of tomato cultivation in the region. The second stage is randomly selecting the six villages out of the number of tomato cultivation villages in Ruzizi Plain, DRCongo. In the third stage, tomato production zones are randomly selected in the villages. In the fourth stage, thirty-nine (39) youth tomato growers are randomly selected from six villages, and a total of 234 youth tomato farmers are sampled. ButHowever, due to incomplete and missing data, 16 items were dropped: 218 youth tomato farmers were considered for the present study.

Slovin’s sampling formula resolved the sample size determination with a 95% confidence level (A. Tadesse, Citation2011).

where n: is the sample size; N: is the population size; E:Ee is the level of precision assumed to be 5%.

2.2. Data analysis

2.2.1. The variable definition and their respective prior hypothesis

The study employed both descriptive and other quantitative methods to analyse the data set. Firstly the current, descriptive statistics were used to describe the socioeconomics and-demographic characteristics of youth tomato growers in the sampled households and, their perception scores towards credit access in tomato farming. Secondly, the Likert scale ranks validated by Kendalls’ coefficient test of agreement and concordance were used for checking the plausibility of the respective perceptions and responses towards agricultural credit accessibility among youth tomato growers.

Kendall’s concordance (W) coefficient was used to determine the extent of disagreement or agreement among respondents related to the ranked list of response items, the potential opportunities and constraints in accessing agricultural credit. The value of (W), ranges from 0 to 1. A coefficient of 0 implies perfect disagreement, and 1 signifies perfect agreement. Kendall’s coefficient (W) was given as:

where N =is the number of items being ranked; T =is the sum of ranks for each item being ranked; M =is the number of rankings.

The hypotheses are:

H0: There is no agreement among respondents on the presented list of constraints and opportunities on agricultural credit accessibility in the study areas.

H1: There is agreement among respondents on the presented list of constraints and opportunities on agricultural credit accessibility in the study areas.

Decision rule: If F calculated is greater than the F critical, we reject the null hypothesis. The F calculated is used to test the significance of the coefficient and is given as:

The F critical has two degrees of freedom, that is, for the numerator and the denominator. The degrees of freedom for the numerator is given as:

The degrees of freedom for the denominator is calculated as:

Thirdly, the current study further employs a probit regression model to analyse the differences in the probability extent among youth tomato farmers’ access to agricultural credit. Qualitative dependence response model such as Probit has been applied in many studies (Dainelli et al., Citation2013; Danso-Abbeam et al., Citation2014; Ghimire & Abo, Citation2013) in the field of credit access and technology decision because of their advantage in involving a limited dependent variable.

According to Gujarati (Citation2004), binary choice models are analysed in the general framework of probability models. The choice of the probit model is based on the assumption of its realistic standard normal distribution. The dependent variable is coded “0” or “1” corresponding to the response given by a youth farmer on whether or not they have access to credit. Nagler (Citation2002) has shown that the probit model constraint estimate probabilities of the dependent variable to lie between 0 and 1 and relaxes the independent variables as a constant across probability values of the dependent variable. Moreover, our research adopts tothe use of the probit model as it provides the advantage of generating a satisfactory error distribution as well as reasonable extents of probabilities in interpreting the marginal effects of explanatory variables in the model.

The Probit model assumes that apart from the observed values of 0 and 1 for the dependent variable Ω, a latent unobserved continued variable Ω* determines the value of the dependent variable Ω. The dependent variable Ω* is dichotomous, representing the youth tomato farmers’ credit access condition and taking the value “1” for those who access credit and “0” otherwise. We assume that Ω* can be specified as follows:

where X1, X2, … … … … … … . , Xj represents a vector of random variables, βj represents a vector of unknown parameters, and εi defines a random disturbance term (Nagler, Citation2002). The measurements and the prior expectations hypothesis of the empirical probit model variables are presented in Table .

Table 1. Socio-demographic characteristics and variables’ definition

3. Dependent and independent variables

Based on the scholarly claims of Sebatta et al. (Citation2014), the agricultural credit accessibility is mainly explained by farmers’ socio-demographic and economic characteristics in agricultural business. In the current study, youth tomato growers’ households were the potential users of agricultural credit related to their farming purposes, and it was assumed that household characteristics could influence the extent of agricultural credit accessibility. The variability in age, land size, education, and income are more likely to affect access to agricultural credit services and hence affect the tomato farmers’ income.

Consider the dependent variable Ω* is dichotomous with exclusive possibilities of either “0” or “1”, explaining the status of the youth tomato farmers’ credit access condition.

where

If, Ω* is taking the value “1” account for those youth tomato farmers who access credit,

and when,

Ω* is taking the value “0” account for those youth tomato farmers who have no access to credit

Age: access to credit is expected to increase with an increase ofincrease in tomato growers’ age since agricultural economic activities increase with age until it reaches a certain stage in life where it begins to decrease. The supply of credit will improve with age level if the lenders consider age as an indicator of experience that will be taken for paying back the credit. Gilligan et al. (Citation2005) found a positive relationship between access to agricultural credit and the age of farmers. Therefore, we hypothesize that:

H1: The age of the farmer has a positive influence on credit access.

The educational level of the household: The household head’s educational level could have a positive or negative effect on access to agricultural credit. On the one hand, education may positively impact managerial skills, which means more economic activities would increase credit demand. On the other hand, education will negatively affect if the household head is employed off-farm and earns more income from other sources or if the household head is more likely to save. Gilligan et al. (Citation2005); Simtowe et al. (Citation2008) have shown a positive relationship between education level and credit access. Also Nasarawa State, Nigeria, Etonihu et al. (Citation2013) revealed that education level had a significant positive relationship with farmers’ accessibility to agricultural credit in Nasarawa State, Nigeria. Consequently, we hypothesize that..

H2.: Formal education can have positive and negative influences on credit access.

Family size: this variable was captured as the number of people in tomato farming households at the survey time during the farming season 2019/2020. The family size is expected to affect accessibility to agricultural credit. Sebatta et al. (Citation2014) studied farmers’ access to agricultural finance in Zambia, Kiros et al. (Citation2022) in Ethiopia and revealed that household size positively correlated with accessibility to agricultural credit. Therefore, we hypothesize that:

H3.: Household size has a positive influence on credit access.

Farm Size: The total farm size is expected to increase the demand for the credit arising from the demand of needed production factors, such as labour, fertilisers, and other variable inputs. Hence, farm size should have a more significant effect on credit demand and positively influence the probability of being credit rationed (Gilligan et al., Citation2005; Simtowe et al., Citation2008). We further hypothesize that..

H4.: Farm size has also a positive and significant influence on credit access.

Distance: Long distance to the nearest microfinance institution is expected to negatively affect the probability of access to credit because the distance travelled will increase the transaction costs of access to agricultural credit. Gilligan et al. (Citation2005) claimed that the far the farmer is located from the bank institutions, the higher the likelihood of missing the needed credit. Hence, we can hypothesize as..

H5: Distancing between the lender and bank institution has also a negative and significant influence on credit access.

Income level of the household: This indicator has been perceived as an indicator of wealth. Wealthier households are expected to have a higher demand for credit. Besides, lenders might supply most credits to more prosperous households because their risk of default is lower since their assets can more easily be liquidated to offset debts (Ololade & Olagunju, Citation2013). Thus, there is a positive relationship between household income and accessibility to agricultural credit. We further hypothesize that:

H6: Household-level of income has a positive influence on credit access.

Gender: The gender of the household head is expected to have a positive influence on the access to agricultural credit because male household heads in the DRC generally have more access to productive resources proxy to credit collateral, which increases their demand for credit. On the other hand, a female-headed household is expected to have more access to credit because most microfinance institutions focus on women’s economic empowerment (Simtowe et al., Citation2008). We then hypothesize that:

H7: Gender of the Household head can either have a positive or a negative influence on credit access

Membership in cooperative: Membership of household head in an association is expected to increase the demand for credit. Lenders can also take membership as a proxy for social capital (Muayila & Tollens, Citation2012). Membership is expected to increase access to credit of members, especially when lenders view membership in an association as a decreasing factor of default probability. Thus, the net effect on the likelihood of being credit rationed cannot be predetermined. Hence, we hypothesize as followas follows:

H8: Having a Membership status in a farmer group/cooperative can either have a positive or a negative influence on credit access.

Extension service: this is a significant factor in agriculture innovation as it involves farmers’ exposure to modern technologies for enhancing the agriculture sector. Hence, the Extension service has been hypothesised to affect access to credit among youth tomato farmers. Akpan et al. (Citation2013) examined the determinants of access and demand for credit among poultry farmers in the Ikot Ekpene area of Akwa Ibom State, Nigeria. The findings revealed that the visit of extension agents was an important determinant in influencing access to credit. Therefore, we hypothesize that:

H9.: Contact with extension agents has a positive and significant influence on credit access.

Farming Experience: estimatedThe estimated number of years in tomato farming activities was hypothesiszed to impact credit accessibility. In their research on the determinants of loan acquisition from financial institutions by small-scale farmers in the Ohafia agricultural zone of Abia State of Nigeria, (Henri-Ukoha et al. (Citation2011) revealed that farming experience enhances significantly the chance of accessing agricultural credit. Hence we do hypothesize as follows:

H10.: Farming experience has a positive and significant effect on credit access.

4. Results and discussions

4.1. Descriptive statistics and association analysis

Descriptive analysis in Table showedshows that most youth tomato growers in Ruzizi plain were in the active young age range, from 15–35from 15 to 35 years, with an age of 34-years. Most of the respondents attended secondary school, and all have completed the secondary education level, considering the national equivalence of 6 years post-primary school being significant at 5% level showing that all the respondents were able to read and write as of the national schooling curricula. Also, the households of youth tomato farmers had an average mean size of 8 people at the survey time. The results also revealed that the distance between farmers’ home-based, the Banks, and Microfinance institutions were taken as a proxy of simplifying access to various financial services. Our results in Table revealed an average mean distance of 3 kilometres3 km, indicating a positive association between distance and credit access.

The average season income was found to be 990 634.53 Congolese Francs (FCs), as converted to USD 235.8. The survey results in Table showsshow that the majority (71.6%) of household heads were males, while a few (28, .4%) were females headed. These findings highlight the significant role of male-headed in tomato farming households towards accessibility to agricultural financial credit. Moreover, our survey results in Table revealed a low (12.4%) access to extension services among youth tomato farmers, thus lowering their probability of accessing agricultural credit in the study areas. Membership to farmers’ cooperatives increases the potential of enhancing members’ capacity for dealing with relevant agricultural credit information. Our results in Table indicate also,also indicate that 46.8% of tomato farmers were cooperative members, which increased their chance of accessing agricultural credit.

4.2. Agricultural credit accessibility by production zones

The actual changes in farming systems, from the traditional to the adoption of modern varieties of crops and increased cropping patterns among farmers, is an observed fact in the DRCongo. Consequently, hasit has led to a rise in demand for agricultural modern inputs. The DRCongo agriculture subsector is dominated by more than 85% of small scalesmall-scale farmers that are unable to afford high expenses related to the adopted modern farming patterns, this has currently led to increased demand for agricultural credit, as part of agriculture inputs for enhancing farm productivity and efficiency. However, the lack of agriculture credit continues to be a severe problem in rural DRCongo. Based on the current evidence in the study of Muayila and Tollens (Citation2012) in their financial analysis in DRCDRC, it was reported that 71% of the farm households experienced various credit constraints. Those constraints areThese constraints include: the high applied interest rate, the level of collateral compliances, the bank bureaucracy and the credit transaction costs, combined with information asymmetry towards credit accessibility in remote areas, and these have directly impacted on their household welfare.

To tackle these listed constraints, the fifth government of DRC havehas made some efforts for correcting the finance market failure in promoting agriculture credit to farmers, but those efforts have not yielded significant results. Furthermore, the government, IMFs and NGOs partners have recently adopted a memorandum of understanding (MoU) related to financial inclusion approaches towards youth farmers’ groups, this for supporting their agribusiness startups after their structuralization and Lélegalisation status. ThoughAlthough barriers to credit access are still significant, we are expecting inexpect in the near future the plausible results of the described approach.

The survey results in Table revealed the extent of agricultural credit accessibility by production zones in the tomato production areas of South-Kivu. The results indicate a low (20, 6%) rate of accessibility to agricultural credit among youth tomato growers. This situation was significantly affected by the location of tomato farmers. This low rate of accessibility to agricultural credit may be attributed to high credit market failure and transaction costs. This situation has led to a low flow of improved inputs among farmers leading to low productivity. Nouman et al. (Citation2013) reported that adequate access to agricultural credit among farmers is a good catalyst for increasing farming production efficiency. They also argued that agricultural credit accessibility would provide farmers with the funds to purchase the needed and improved technologies in their farming ventures as a proxy for enhancing their productivity.

Table 2. Agricultural credit access by territory

4.3. Types of agricultural credit provided

The results in Table showsshow the descriptive towards the types of provided agricultural credit by micro-finance agencies to farmers in the region. The results revealed that almost 66.6% of the provided agricultural credit was cash-based, while only 24.4% of credit was provided in kind-based, and 8.8% of the agricultural credit provided credit was combined, both in kind-based and cash-based from cooperatives and, other agricultural programmes from NGOs. This trend may be explained due to the lack of financial behaviour among farmers in the region. In other words, the majority of agricultural credits flow in cash rather than in kind. Also, the country’s lack of a convenient seeds system could be orienting the agricultural credit policy. Such a system would be based on the supply of agriculture improved technology as credit vouchers, which is totally in kind while allowing access to all needed agriculture improved inputs and promoting farming contracts.

Table 3. Types of agricultural credit provided by financial institutions

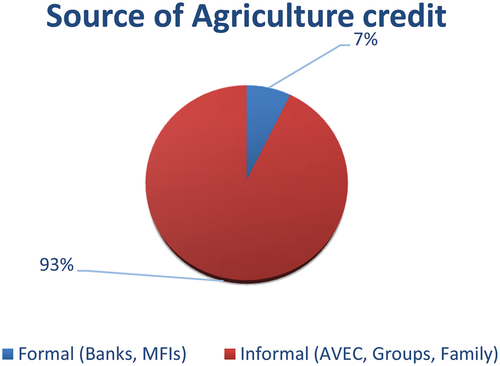

4.4. Source of agricultural credit

Results in Figure reveal a meagre proportion (7.3%) of the formal microfinance system providing agricultural credit to youth tomato growers in the study area compared to the informal sources (92.7%). The results imply that informal agricultural credit sources are most predominant in the region. They include Village Savings-Loans Associations (VSLA), groups of money lenders and relatives. On the other hand, the formal agricultural credit sources included commercial banks, government, and credit cooperatives. The possible reasons behind this predominance of the informal sources of agricultural finance in the region can be the lack of agricultural finance policies in the country and the wrong perception of microfinance institutions towards the agricultural sector’s risk, coupled with lack of the associated collateral. Dittoh (Citation2006) shows that farmers’ smallholder has marginal participation in the formal credit market in developing countries. ThusThus, it could be taken as an advantage for revamping the subsector’s growth.

Figure 1. Source of agricultural credit in the study area.

4.5. Purposes and uses of agricultural credit

The results in Table focused on the agreement and concordance among tomato growers’ responses on the ranked list of different uses of the received agricultural credit in the farming season 2019/2020. The results reveal a positive and moderate agreement among youth tomato farmers in their alternatives using of the received agricultural credit, which is significant at 1% level. Hence, most (55.5%) of tomato growers used the received agricultural credit to pay for the previously contracted debts ranked as the first alternative. And, 24.4% of youth tomato growers used the obtained credit for other household expenses. The results are congruent with Nimoh et al. (Citation2011), who observed a significant diversion of credit to non-farming ventures. Similarly, Anyiro and Oriaku (Citation2011) indicated that about 83% of smallholder farmers in Abia State, NigeriaNigeria, diverted their borrowed agricultural funds to other activities rather than for the purpose for which the credit was applied. And, 8% of tomato growers affected the credit on the expansion of their tomato farming ventures, and 6.6% only ranked the use of credit for purchasing the needed inputs for their tomato activities as the fourth alternative. The associated significance of Kendalls’ performance test gives information on farmers’ attitude towards using the received Agriculture credit. Better use of financial resources in the agriculture sector requires appropriate orientation to witness enhancement and growth in the tomato subsector.

Table 4. Purpose and use of agricultural credit

4.6. Test of agreement between tomato farmers towards related constraints on accessing agricultural credit

Table shows the list of constraints in accessing agricultural credit among tomato growers in the region. The test’s purpose was to determine whether youth tomato growers were facing the same constraints on accessing credit in their farming ventures in the area. The result of the empirical test with the value of F-Khi2 = 43,69 as necessary at a 1% level of significance confirmed that the ranked list of constraints does affect the tomato growers. And hence, The lack of agricultural credit information had a high mean score of 3.44 and was the first, topmost constraint on accessing agricultural credit. The Fear of credit default with a score of 3.04 was ranked as the second. Our findings are supported by M. Tadesse (Citation2014) and Weber and Musshoff (Citation2012) in Ethiopia and Tanzania, respectively. They found that the attitude of fear due to the wrong perception towards the uncertainty of the agricultural subsector among small scalesmall-scale farmers has led to low participation in market finance. This can partly be attributed to the assumption that small-scale agriculture is risky. The non-existence of financial institutions in the rural areas scored 3.01 and has been ranked as the third most challenging constraint hindering accessibility to agricultural credit. They also reported that the long administration process on credit access, coupled with the lack of credit collateral, was ranked as fourth and fifth respectively as the most challenging problems constraining them from getting access to agricultural credit.

Table 5. Constraints of accessing agricultural credit

4.7. Probit estimation of the tomato households on agricultural credit accessibility

The results in the analysis of factors affecting accessibility to agricultural credit among youth tomato growers are presented in Table . The likelihood ratio chi-square (χ2) of 27.42 indicates that the estimated model, taken jointly, is statistically significant at a 1% level. This test testifies a robust explanatory power of the model in the studied reality towards youth farmers’ accessing agricultural credit. The results also showed that the selected explanatory variables correctly predict about 18% of the model. To avoid a multicollinearity problem, we ensure that the variable age and experience were not highly correlated. The results in Table reveal that gender of the tomato growers in the study areas has a significant and negative influence on the marginal probability of accessing agricultural credit. This implies that being a female youth tomato producer increases the likelihood of accessing agricultural financial credit. Similarly, there was a significant negative link between household income and access to agricultural credit. This indicates that youth tomato growers with lower incomes are less likely to access agricultural credit than those with high incomes. Besides, membership in youth farmers’ groups/cooperatives had a significant and positive influence on the probability of accessing agricultural credit, confirming our prior hypothesised signs. This is supported by the new financial, and scientific claim that lenders can also take farmers’ membership as a proxy to social capital.

Table 6. Probit estimation of factors explaining the accessibility of tomato farmers on agricultural credit accessibility

4.8. Discussion

The results reveal that the probability of youth tomato farmers accessing agricultural finance depends on gender status. Keeping all other factors constant, being a male tomato grower reduces by 16.8% the chance of accessing agricultural credit instead of being a female tomato grower. This could be explained by the boom of programmes focusing on rural women’s financial empowerment in eastern DRC. The trend has been promoted the participation of more female-headed households in credit programmes than has been the case with male-headed households. Our results align with the results of other studies that have confirmed more involvement of women in the rural economy, which has led to the fact that women receive more attention from MFIs that provide them more credit than men. Results that are incongruent with the findings of Akudugu (Citation2012), in his research conducted in the Ghana context, reported that male-headed farmers were having less likelihood of accessing agriculture credit, in Uganda (Mpuga, Citation2010), in Nigeria, Ajagbe (Citation2012), and Ololade and Olagunju (Citation2013) in their respective studies found that female tomato growers were more likely to get access to credit as opposed to male tomato growers. Lenders reported that women were more credit-worthy and had higher loan repayment rates than men. These results contrast with Awotide et al. (Citation2016), who found also that male-headed households tend to have a larger output than their female counterparts due to their better access to productive inputs such as financial credit. While another study by Girma and Abebaw (Citation2015) conducted in Ethiopia did not find a significant relationship between gender and credit access.

Also, the results show a significant relationship between the household’s income and the likelihood of accessing financial, agricultural credit. This could be explained by the fact that income level in this study was perceived as household wealth and endowment that could be evaluated as collateral for the demand of formal credit. All things remaining constant, most of our surveyed youth tomato growers were producing at a small-scale basis and hence were considered poor-resourced and had a tiny capital endowment. Thus, the income level of youth tomato growers decreased the likelihood of accessing agricultural credit by 1.3%. The findings are supported by some lenders’ financial claims that small farmers are poor farmers and are very risky borrowers. The results contradict the conclusion of Duy et al. (Citation2012). They established a positive and significant association between household income and agricultural credit access, claiming that a household’s capital endowments are vital in the demand for formal credit and the loan amount.

The results in Table show that being a member of a farmers’ cooperative increases the probability among youth tomato growing’ households of accessing agricultural credit by 13.7%. This may be explained by the perception of MFIs’ belief that membership in farmers’ associations decreases credit default risk. Thus, the net effect on the probability of being credit rationed cannot be predetermined. Holding all other factors constant, membership in farmers’ groups/cooperatives can be used to proxy social capital Omonona, and Ajani (Citation2009). These findings corroborate the results of Brata (Citation2005), Nugroho and O’hara (Citation2008). They report a significant and positive relationship between borrowing from the banks and membership to business associations in Nigeria and Ethiopia. Also, it could be argued that financial credit through groups initiates peer selection effect among farmers who know each other, decreasing individual credit default and increasing farm income. Since, many microfinance institutions provide group lending credit, belonging to a farmers’ cooperative would ultimately increase the probability of accessing agricultural credit. We thereafter notice the contextual inconsistencies in the findings, that makes interesting the analysis of our research, the above results diverge and contradict the findings of Admasu and Paul (Citation2010) and Chanyalew (Citation2015), in their study conducted in Ethiopia and revealed that access to institutional loans is very limited when it comes to farmer cooperatives and especially to those engaged in production niches activities in general.

Despite the expected prior hypothesized magnitude and, the evidence theory that supports each adopted explanatory variable in our research, we discover some regional disparities in the findings from different regions and countries that were not consistent. And that varies from different context-specific investigations across various group ages and communities, and hence led all the variables to be likely context-specific. With attention to the age of the youth tomato farmer, we hypothesized a positive influence on the likelihood of accessing credit, but surprisingly from the DRC context, it did show any statistical significance. This may be explained by the financial market failure in the rural areas of DRC, and especially towards farm groups on accessing formal credit. Our findings align with the results of Girma and Abebaw (Citation2015) in their studies conducted in Ethiopia, they also did not find a statistically significant association between the two variables, while opposing the results of various studies piloted in Nigeria (Akpan et al., Citation2013) testified that age of the household is positively related to their loan demand. They claimed that older farmers were more likely to access credit. Because in the African context, old farmers have accumulated resources endowment and assets such as land and livestock capital that are solvable as credit collateral compared to young farmers. Nevertheless, Bing et al. (Citation2008) in their study conducted in China found a negatively significant relationship between age and credit access. The same statement has been done by Chandio et al. (Citation2021) in the context of Pakistan who showed that aged farmers are risk-averse and reluctant to access credit.

In regards to the influence of education level of the farmer, in coping with credit access strategies, we have hypothesised the existing positive association between educational level and access to credit, though it showed any significance in our study context and being incongruent with the findings of Wiboonpongse et al. (Citation2006). In his study conducted in Thailand, he reported an absence of a significant relationship between the two variables. We also noticed there are discrepancies in the findings of various studies conducted in different countries: for example, in Nigeria(Akpan et al., Citation2013), Kenya (Messah & Wanjai, Citation2011), Pakistan (Khan & Hussain, Citation2011), Ethiopia(Ethiopia (Girma & Abebaw, Citation2015), and Ghana (Akudugu, Citation2012). The education level of farmers was found to have a positive influence on credit access. while surprisingly contrast, another study from China (Bing et al., Citation2008) reported a negative influence on credit demand. In EthiopiaEthiopia, Kiros et al. (Citation2022) found that educational status is not linked to access to finance. Overall, the findings show that education level is one of the key variables that provide exposure to farmers and hence play a key role in influencing the decision to apply for financial credit.

Considering the farmer household size, we hypothesized a positive influence on credit access, since the large the family size, constitute in the African context labour that can easily work and generates resources, that are needed to pay back the obtained credit. However, in our research, we did not find a significant association between household size and access to financial credit. Hence, based on the existing literature, it has shown up wide inconsistencies across countries to explain the two related variables. Considering the Asian context, the family size was reported to have a positive effect on credit access in India and China (Tang et al., Citation2010), while showed up a negative effect in the African context, taking the case of Kenya (Messah & Wanjai, Citation2011), and Nigeria (Akpan et al., Citation2013). The reason behind the positive effect in the Asian context and its negative influence in the African countries could be related to variations in socio-cultural aspects and the disparities in labour economic valuations in Asia as compared to Africa.

Despite that the distance between the rural lenders and the financials and IMFs institutions haves not shown a significant relationship in this study, it supported our prior expectation, that claimed the negative relationship. And hence, corroborate with the findings of several studies to have a negative influence on loan access. For instance, studies conducted in Nigeria (Akpan et al., Citation2013), Pakistan(Pakistan (Khan & Hussain, Citation2011), and Ghana (Akudugu, Citation2012) showed a negative and significant relationship between distance to financial institutions and IMFs agencies and loan access. This is not astonishing as the distance is positively correlated to the transaction cost of borrowing and related information.

With regards to farm size, it showed a positive association with credit access as hypothesized in our research. Our results are consistent with many other studies except Kiros et al. (Citation2022) in the Ethiopian context because the land is a suitable asset that lender institutions in the African context do prefers as collateral for credit access. Studies from various countries such as: Pakistan (Khan & Hussain, Citation2011), China (Tang et al., Citation2010) and Ghana (Akudugu, Citation2012) show that farm size was positively influencing access to formal agriculture credit. This could suggest the fact that farmers with larger farm sizes are mostly engaged in expanding and modernising their farming activities, which led to higher exploitation costs as a proxy for credit demand while using their farm size as collateral.

To the best of our knowledge, our research is the first to demonstrate the influence of numerous socioeconomic and institutional characteristics of smallholder youth farmers on accessing financial agricultural credit in South-Kivu, DRC. It also illustrates the relevant contribution to the existing literature regarding credit access among youth farmers to improve agricultural productivity.

5. Conclusion and policy implications

This research examines the determinants of accessing agricultural credit among youth tomato farmers in Ruzizi Plain, of the DRC, using the surveys data from 218 smallholder farmers. The study has been conducted in the South-Kivu province of DRC and is mostly based on the field survey. A multistage sampling technique has been used to collect the data from smallholder farmers. We applied the probit estimation binary model to analyzse the data. The evidence from this study reveals that tomato growers’ membership in a cooperative has a positive and significant influence on the access to formal agricultural credit by smallholder youth tomato farmers, while the total household income level, gender of the household head have a negative effect on credit access. In the consequences of agricultural credit from financial institutions in South-Kivu/DRC, still, small-scale farmers have low access to agriculture credit due to the lack of agricultural credit information, fear of credit default, and absence of microfinance institutions coupled to the financial market imperfections. The current research noticed significant discrepancies in various findings from different countries and regions’ contexts compared to the DRC context in accessing determinants of agriculture credit accessibility among farmers. However, the selected explanatory variables were relevant theoretically to validate the related hypothesis. Based on the study findings, our research recommends that there is a high need to improve access to extension services for youth tomato growers’ groups and, also to sensitize youth farmers’ to adhere to tomato cooperatives groups as this increases the probability of access to agricultural credit from financial institutions. Provision of agricultural credit-related information through farmers’ groups is also important and likely to change the risk attitude toward credit for youth farmers who are not currently accessing agricultural credit from financial institutions. In addition, financial institutions should supply agricultural credit to small-scale farmers at a low-interest rate and the terms and conditions should be made easy and flexible. Also, the government should invest in correcting the financial market imperfections for enabling youth farmers’ access to credit.

All in all, this work presents fresh avenues to explore relevant socioeconomics and institutional factors that condition agricultural credit accessibility among youth tomato farmers in DRC’s financial market. However, our study did not analyse the effects of credit access on tomato yield and the associated risks of credit default among youth farmers. Future research should investigate the impact of agricultural credit on tomato productivity among youth farmers while testing their efficiencies in using financial resources, as we anticipate.

Acknowledgements

This paper is part of the author’ research followership grants 2000001374 “Enhancing Capacity to Apply Research Evidence (CARE) in Policy for Youth Engagement in Agribusiness and Rural Economic Activities in Africa” Project in the International Fund for Agricultural Development (IFAD), trough IITA [2000001374]. We also wish to thank Dr Paul Dontsop, Dr Victor Manyong, Dr Zoumana Bamba, and the Kivu Agribusiness Group research team for their help during fieldwork and data collection.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Alexis Nyamugira Biringanine

Safari Mulume Bonnke is a fellow researcher at the International Institute of Tropical Agriculture/ DRAgriculture/DR Congo in the socioeconomist team, South-Kivu and Tanganyika. He is also an Agripreneurs, Co-founderagripreneur, co-founder of the Kivu Agribusiness Group (KAG), which is an agribusiness platform and a consultation program that empowers groups of farmers with agribusiness skills. He is a PhD candidate in Agriculture Economics and agribusiness, Sokoine University of Agriculture, Tanzania. His research interest includesinterests include agricultural value chain analysis, agribusiness development and marketing, finance and food production, consumer behaviour.

References

- Admasu, A., & Paul, I. (2010). Assessment on the mechanisms and challenges of small scale agricultural credit from commercial banks in Ethiopia: The case of Ada‟aLibenworeda of Ethiopia. Journal of Sustainable Development in Africa, 12(3), 323–302.

- Ahmad, N. (2011). Impact of institutional credit on agricultural output: A case study of Pakistan. Theoretical and Applied Economics, XVIII(10), 99–22.

- Ajagbe, F. A. (2012). Analysis of access to and demand for credit by small scale entrepreneurs: evidence from Oyo State, Nigeria. Journal of Emerging Trends in Economics and Management Sciences, 3(3), 180–183.

- Akpan, S. B., Patrick, I. V., & Udoka, S. J. (2013). Determinants of credit access and demand among poultry farmers in Akwa Ibom state, Nigeria. Journal of Experimental Agriculture International, 3(2), 293–307. https://doi.org/10.9734/AJEA/2013/2810

- Akudugu, M. (2012). “Estimation of the determinants of credit demand by farmers and supply by Rural Banks in Ghana‟s. Asian Journal of Agriculture and Rural Development, 2(2), 189–200.

- Anang, B. T., Sipilainen, T., Backman, S., & Kola, J. (2015). Factors influencing smallholder farmers access to agricultural microcredit in Northern Ghana. African Journal of Agricultural Research, 10(24), 2460–2469. https://doi.org/10.5897/AJAR2015.9536

- Anyiro, C. O., & Oriaku, B. N. (2011). Access to and investment of formal micro credit by small holder farmers in Abia state, Nigeria. A case study of Absu Micro Finance Bank, Uturu. The Journal of Agricultural Sciences, 6(2), 69–76. https://doi.org/10.4038/jas.v6i2.3861

- Awotide, B. A., Karimov, A. A., & Diagne, A. (2016). Agricultural technology adoption, commercialization and smallholder rice farmers’ welfare in rural Nigeria. Agricultural and Food Economics, 4(1), 1–24. https://doi.org/10.1186/s40100-016-0047-8

- Badibanga, T., & Ulimwengu, J. (2019). Optimal investment for agricultural growth and poverty reduction in the democratic Republic of Congo a two-sector economic growth model. Applied Economics, 52(2), 135–155. https://doi.org/10.1080/00036846.2019.1630709

- Bing, Z., Guo-yu, Ping-gui, Z., Yang, C., & Shuai, Y. (2008). Empirical study on the financial repression of rural households‟ debit and credit and the effects on their welfare in less developed regions – Take Suqian city of Jiangsu province as an example. Journal of Modern Accounting & Auditing, 4(12), 27–34.

- Boucher, S. R., Carter, M. R., & Guirkinger, C. (2008). Risk rationing and wealth effects in credit markets: Theory and implications for agricultural development. American Journal of Agricultural Economics, 90(2), 409–423.

- Brata, A. G. (2005). Accessing formal credit: Social capital versus ‘social position’(Lesson from a Javanese Village). 7th IRSA International Conference, Jakarta, 3–4.

- Bryman, A., & Cramer, D. (2011). Quantitative data analysis with IBM SPSS 17, 18 & 19. Ro. https://doi.org/10.4324/9780203180990

- Chandio, A. A., Jiang, Y., Rehman, A., & Akram, W. (2021). Does formal credit enhance sugarcane productivity? A farm-level Study of Sindh, Pakistan. SAGE Open, 11(1), 215824402098853. https://doi.org/10.1177/2158244020988533

- Chandio, A. A., Jiang, Y., Rehman, A., & Rauf, A. (2020). Short and long-run impacts of climate change on agriculture: An empirical evidence from China. International Journal of Climate Change Strategies and Management, 12(2), 201–221. https://doi.org/10.1108/IJCCSM-05-2019-0026

- Chandio, A. A., Jiang, Y., Rehman, A., Twumasi, M. A., Pathan, A. G., & Mohsin, M. (2021). Determinants of demand for credit by smallholder farmers’: A farm level analysis based on survey in Sindh, Pakistan. Journal of Asian Business and Economic Studies, 28(3), 225–240. https://doi.org/10.1177/2158244020988533

- Chandio, A. A., Jiang, Y., Wei, F., & Guangshun, X. (2018). Effects of agricultural credit on wheat productivity of small farms in Sindh, Pakistan: Are short-term loans better? Agricultural Finance Review, 78(5), 592–610. https://doi.org/10.1108/AFR-02-2017-0010

- Chanyalew, D. (2015). Ethiopia’s indigenous policy and growth: Agriculture, pastoral and rural development. Addis Abab.

- Dainelli, F., Giunta, F., & Cipollini, F. (2013). Determinants of SME credit worthiness under Basel rules: The value of credit history information. PSL Quarterly Review, 66(264), 21–47.

- Danso-Abbeam, G., Ansah, I. G. K., & Ehiakpor, D. S. (2014). Microfinance and micro-small-medium scale enterprises (MSME’s) in Kasoa Municipality, Ghana. Journal of Economics, Management and Trade, 88, 1939–1956.

- Dittoh, S. (2006). Effective aid for small farmers in Sub-Saharan Africa: southern civil society perspective. Ghana Case Study.

- Dong, K., Dong, X., & Dong, C. (2019). Determinants of the global and regional CO2 emissions: What causes what and where? Applied Economics, 51(46), 5031–5044.

- Dube, L., Mariga, T., & Mrema, M. (2015). Determinants of access to formal credit by smallholder tobacco farmers in Makoni District, Zimbabwe. Greener Journal of Agricultural Sciences, 5(1), 034–042. https://doi.org/10.15580/GJAS.2015.1.011515003

- Duy, V. Q., D’haese, M., Lemba, J., Hau, L. L., & D’Haese, L. (2012). Determinants of household access to formal credit in the rural areas of the Mekong Delta, Vietnam. African and Asian Studies, 11(2), 261–287. https://doi.org/10.1163/15692108-12341234

- Effective aid for small farmers in Sub-Saharan Africa: Southern civil society perspective. Ghana Case Study, (2006).

- Etonihu, K. I., Rahman, S. A., & Usman, S. (2013). Determinants of access to agricultural credit among crop farmers in a farming community of Nasarawa state, Nigeria. Journal of Development and Agricultural Economics, 5(5), 192–196. https://doi.org/10.5897/JDAE12.062

- FA0. (2011). Annual report on FAO activities in support of producers‘ organizations and agricultural cooperatives.

- Ghimire, B., & Abo, R. (2013). An empirical investigation of Ivorian SMEs access to bank finance: Constraining factors at demand-level. Journal of Finance and Investment Analysis, 2(4), 29–55.

- Gilligan, D., Harrower, S., & Quisumbing, A. (2005). How accurate are reports of credit constraints? Reconciling theory with respondents’ claims in Bukidnon, Philippines.

- Girma, M., & Abebaw, D. (2015). Determinants of formal credit market participation by rural farm households: Micro-level evidence from Ethiopia. Paper for presentation at the 13th International Conference on the Ethiopian Economy, Addis Ababa, Ethiopia.

- Gujarati, D. N. (2004). Basic Econometrics. McGraw-Hill Companies.

- Gul, A., Chandio, A. A., Siyal, S. A., Rehman, A., & Xiumin, W. (2021). How climate change is impacting the major yield crops of Pakistan? an exploration from long- and short-run estimation. Environmental Science and Pollution Research, 18, 26660–26674. https://doi.org/10.1007/s11356-021-17579-z

- Gul, A., Xiumin, W., Chandio, A. A., Rehman, A., Siyal, S. A., & Asare, I. (2022). Tracking the effect of climatic and non-climatic elements on rice production in Pakistan using the ARDL approach. Environmental Science and Pollution Research, 29, 31886–31900. https://doi.org/10.1007/s11356-022-18541-3

- Henri-Ukoha, A., Orebiyi, J. S., Obasi, P. C., Oguoma, N. N., Ohajianya, D. O., & Ibekwe, U. C. (2011). Determinants of loan acquisition from the financial institutions by small-scale farmers in Ohafia Agricultural zone of Abia State, South East Nigeria. Journal of Development and Agricultural Economics, 3(2), 67–74.

- Hossain, M., & Bayes, A. (2009). Rural economy & livelihoods: Insights from Bangladesh. A H Development Publishing House. https://www.amazon.com/Rural-Economy-Livelihoods-Insights-Bangladesh/dp/9848810064

- IITA. (2019). innovations Scaling up. https://doi.org/0331.4340

- Khan, R., & Hussain, T. (2011). Demand for formal and informal credit in agriculture: A case study of cotton growers in Bahawalpur. Interdisciplinary Journal of Contemporary Research in Business, 2(10).

- Kiplimo, J. C., Ngenoh, E., Koech, W., & Bett, J. K. (2015). Determinants of access to credit financial services by smallholder farmers in Kenya. Journal of Development and Agricultural Economics, 7(9), 303–313. https://doi.org/10.5897/JDAE2014.0591

- Kiros, S., Meshesha, G. B., Zone, S., State, A. R., & Chen, M. (2022). Factors affecting farmers ’ access to formal financial credit in Basona Worana district, North Showa Zone, Amhara regional state, Ethiopia factors affecting farmers ’ access to formal financial credit in Basona Worana district, North. Cogent Economics & Finance, 10(1), 0–22. https://doi.org/10.1080/23322039.2022.2035043

- Kumar, A., Singh, K. M., & Sinha, S. (2010). Institutional credit to agriculture sector in India : Status, performance and determinants. Agricultural Economics Research Review, 23(December), 253–264.

- Kuwornu, J. K., Ohene-Ntow, I. D., & Asuming-Brempong, S. (2012). Agricultural credit allocation and constraint analyses of selected maize farmers in Ghana. Journal of Economics, Management and Trade, 2, 353–374.

- Langat, R. (2013). Determinants of lending to farmers by commercial banks in Kenya (Issue November) [University of Nairobi]. http://erepository.uonbi.ac.ke/bitstream/handle/11295/58537/Langat_Determinants-of-lending-to-farmers-by-commercial-banks-in-Kenya.pdf?isAllowed=y&sequence=3

- Lawal, J. O., Omonona, B. T., & Ajani, O. I. Y. (2009). Effects of social capital on credit access among cocoa farming households in Osun State.

- Lee, K. H., & Min, B. (2014). Globalization and carbon constrained global economy: a fad or a trend? Journal of Asia-Pacific Business, 15(2), 105–121.

- Liu, Z., Yang, J., Zhang, J., Xiang, H., & Wei, H. (2019). A bibliometric analysis of research on acid rain. Sustainability, 11(11), 3077.

- McArthur, J. W., & Sachs, J. D. (2018). Agriculture, aid, and economic growth in Africa. The World Bank, 33(1), 1–20. https://doi.org/10.1093/wber/lhx029

- Messah, O., & Wanjai, P. (2011). Factors that influence the demand for credit among small-scale investors: A case study of Meru Central District, Kenya. Research Journal of Finance and Accounting, 2(2). www.iiste.org

- Meyer, R. L. (2011). Subsidies as an instrument in agriculture finance: A review. https://openknowledge.worldbank.org/handle/10986/12696

- Mpuga, P. (2010). Constraints in access to and demand for rural credit: Evidence from Uganda. African Development Review, 22(1), 115–148. https://doi.org/10.1111/j.1467-8268.2009.00230.x

- Muayila, K., & Tollens, E. (2012). Assessing the impact of credit constraints on farm household economic welfare in the hinterland of Kinshasa, Democratic Republic of Congo. African Journal of Food Agriculture, Nutrition and Development, 12(3), 6095–6109. https://doi.org/10.18697/ajfand.51.10705

- Nagler, J. (2002). Interpreting probit analysis. http://www.nyu.edu/classes/nagler/quantz/notes/probitI.pdf

- Nimoh, F., Kwasi, A., Tham-Agyekum, & Kwame, E. (2011). Effect of formal credit on the performance of the poultry industry: The case of urban and peri-urban Kumasi in the Ashanti Region. Journal of Development and Agricultural Economics.

- Nouman, M., Siddiqi, M., & Asim, S. (2013). Impact of socio-economic characteristics of farmers on access to agricultural credit. Sarhad Journal of Agriculture, 29(3), 469–476. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2336223

- Nugroho, A. E., & O’hara, P. A. (2008). Microfinance sustainability and poverty outreach: A case study of microfinance and social capital in rural Java.

- Ololade, R. A., & Olagunju, F. I. (2013). Determinants of access to credit among rural farmers in Oyo State, Nigeria. Global Journal of Science Frontier Research Agriculture and Veterinary Sciences, 13(2), 16–22.

- Olusanya, S. (2012). Determinants of lending behaviour of commercial banks: Evidence from Nigeria, A co-integration analysis (1975-2010). Journal of Humanities and Social Science, 5(5), 71–80. https://doi.org/10.9790/0837-0557180

- Rehman, A., Ma, H., Ahmad, M., Irfan, M., Traore, O., & Chandio, A. A. (2021). Towards environmental sustainability: Devolving the influence of carbon dioxide emission to population growth, climate change, Forestry, livestock and crops production in Pakistan. Ecological Indicators, 125, 107460. https://doi.org/10.1016/j.ecolind.2021.107460

- Rehman, A., Ozturk, I., & Zhang, D. (2019). The causal connection between CO2 emissions and agricultural productivity in Pakistan: Empirical evidence from an autoregressive distributed lag bounds testing approach. Applied Sciences (Switzerland), 9(8), 1692. https://doi.org/10.3390/app9081692

- Saqib, S. E., Kuwornu, J. K., Panezia, S., & Ali, U. (2018). Factors determining subsistence farmers’ access to agricultural credit in flood-prone areas of Pakistan. Kasetsart Journal of Social Sciences, 39(2), 262–268. https://doi.org/10.1016/j.kjss.2017.06.001

- Sebatta, C., Wamulume, M., & Mwansakilwa, C. (2014). Determinants of smallholder farmers’ access to agricultural finance in Zambia. Journal of Agricultural Science, 6(11), 63. https://doi.org/10.5539/jas.v6n11p63

- Shah, M., & Khan, H. J. (2008). Impact of agricultural credit on farm productivity and income of farmers in mountainous agriculture in northern Pakistan: A case study of selected villages in district Chitral. Sarhad Journal of Agriculture, 24(4), 713–718. https://agris.fao.org/agris-search/search.do?recordID=PK2010000209

- Sileshi, M., Nyikal, R., & Wangia, S. (2012). Factors affecting loan repayment performance of smallholder farmers in East Hararghe, Ethiopia.

- Simtowe, F., Zeller, M., & Diagne, A. (2008). Who is credit constrained? Evidence from Rural Malawi. Agricultural Finance Review, 68(2), 255–27. https://doi.org/10.1108/00214660880001229

- Tadesse, A. (2011). Market chain analysis of fruits for Gomma Woreda. Jimma Zone, Oromia National Regional State.

- Tadesse, M. (2014). Fertilizer adoption, credit access, and safety nets in rural Ethiopia. Agricultural Finance Review, 74(3), 290–310. https://doi.org/10.1108/AFR-09-2012-0049

- Tang, S., Guan, Z., & Jin, S. (2010). Formal and informal credit markets and rural credit demand in China. Selected paper prepared for presentation at the Agricultural and Applied Economics Association. Association. AAEA, CAES and WAEA Joint Annual Meeting,Kyoto,Japan.

- Tollens, E. (2015). Les parcs agro-industriels et l’agriculture familiale. Les défis du secteur agricole en RDC. Conjonctures Congolaises, 148–158. https://www.eca-creac.eu/sites/default/files/pdf/2015_conjonctures_congolaises.pdf#page=147

- Wakilur, R., Jianchao, L., & Cheng, E. (2011). Policies and performances of agricultural/rural credit in Bangladesh: What is the influence on agricultural production ? African Journal of Agricultural Research, 6(31), 6440–6452. https://doi.org/10.5897/AJAR11.1575

- Weber, R., & Musshoff, O. (2012). Is agricultural microcredit really more risky? Evidence from Tanzania. Agricultural Finance Review, 72(3), 416–435. https://doi.org/10.1108/00021461211277268

- Wiboonpongse, A., Sriboonchitta, S., & Chaovanapoonphol, Y. (2006). The demand for loans for major rice in the Upper North of Thailand. Contributed Paper for Presentation at International Association of Agricultural Economics Conference, Gold Coast, Australia.

- World Bank. (2011). République Démocratique du Congo: Accélérer la croissance et l’emploi. Rapport de synthèse. World Bank.