?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This article analyses the impact of public debt on sustainability as measured by the genuine savings indicator covering the period from 2004 to 2018. The methodology adopted is based on dynamic panel generalized methods of moments (GMM). The results after estimation show a negative and significant contribution of public debt to the WAEMU countries’ development sustainability. However, we note that an improvement in institutional governance, an increase in health expenditures and climate change expenditures contribute significantly to putting these countries on a sustainable development trajectory.

PUBLIC INTEREST STATEMENT

The issue of the development sustainability of developing countries, in particular that of WAEMU countries, has come back to the forefront of debates with the resurgence of public debt in the context of the global pandemic at Covid 19. The article analyzes the impact of public debt on development sustainability covering the period from 2004 to 2018. Thus, to ensure the development sustainability in WAEMU countries, it will be necessary to control the public debt of countries: unsustainable debt has a negative impact on the development sustainability in WAEMU countries. In addition, improved institutional governance, an increase in health expenditures and climate change expenditures contribute significantly to putting these countries on a sustainable development trajectory. Also, to ensure the development sustainability in the countries of the zone, the rents from the exploitation of natural resources must be reinvested in productive capital.

1. Introduction

Achieving the Sustainable Development Goals requires significant investments in infrastructure, human capital, and climate change resilience, among other things. Yet developing countries have limited means to mobilize public revenues or private investments. Thus, for these countries, debt is one of the levers to cover development financing needs, but at unsustainable levels that undermine economic growth. The issue of development sustainability is at the heart of international concerns, especially for developing countries whose economies are dependent on natural resources and the environment (Anani, Citation2020; Sikod et al., Citation2013). Indeed, in a context of restructuring and reduction of the debt burden to a sustainable level following the HIPC (Heavily Indebted Poor Countries) initiative launched in 1996 by the donor community, African economies have now regained substantial fiscal room for manoeuvre, which has enabled them to withstand the deterioration of the global economy since 2009 (AFD, Citation2013). The reserves accumulated over the decade have even made it possible in some cases to carry out economic recovery policies, previously unheard of.

Most African countries are now using their budgetary margins to re-debt and finance considerable needs, particularly in terms of infrastructure, the deficiencies of which are now an obvious brake on the development and competitiveness of their economies. The resumption of growth in these countries can be explained in particular by the availability of investment capital in search of new opportunities in Africa (Mckinsey and Company, Citation2010) and the recovery of commodity prices (Anani, Citation2019; Couharde, Géronimi et al., Citation2012). In addition to these two elements, there are also some remarkable elements, such as the improvement in the macroeconomic situation (exports, national investments), political and economic governance, the adoption of new regulatory mechanisms in the field of governance and the environment (transparency in revenue management, the rights of indigenous populations, environmental management, the Extractive Industries Transparency Initiative promoted by the British government in 2003, the ECOWASFootnote1 Mining Directive in 2009, etc.). For Devarajan and Fengler (Citation2013), it is also worth noting the reduction of conflicts, which can be assumed to have positive and lasting effects in some countries of the union (IMF, Citation2012; Hugon, Citation2013; OECD, Citation2013). These efforts suggest that the countries of the region are on a sustainable development path.

However, the reduction or cancellation of a country’s debt is not without risk as it can lock the country into a vicious circle of indebtedness. Ferry and Raffinot (Citation2016) in their analysis, therefore, consider that any debt reduction implies a risk of moral hazard, i.e. states that have benefited from these reductions probably see their incentive to repay future loans decrease, to the extent that they can anticipate further debt reductions. This vicious circle of indebtedness could therefore slow down the sustainable development trajectory recorded in the WAEMU in the early 2000s, especially since the situation is not very bright. The outstanding public debtFootnote2 represented 56.7% of nominal GDP in 2018, compared with 54.4% in 2017, with a sharp increase in debt service in connection with the increase in domestic debt. Total public debt serviceFootnote3 increased compared to 2017, and represented 56.6% of total revenue in 2018 compared to 34.4% in 2017. The outbreak of the Covid 19 has aggravated the situation with the slowdown in economic activity in all sectors and an increase in the need for financial resources for various expenses, including health investment expenses. This raises the issue of debt through increased public expenditure, and given that debt service is a key variable in a country’s development process, its increase could compromise its sustainability in the sense that higher debt ratios have a negative effect on the growth rate (Ferreira, Citation2009). In addition to these difficulties, the financing needs of African countries, both for their development and for their adaptation to climate change, were raised at the African Union conference in Addis Ababa in 2015 as a reason for the re-indebtedness of these poor countries.

In these conditions of worsening debt of the countries of the Union coupled with the effects of the global health crisis (Covid 19) with its adverse impacts on all economic sectors, the question of the sustainability development trajectory of the Union countries will again become acute (Aragie et al., Citation2021; Gani, Citation2021; Njatang, Citation2021). Thus, the objective of this paper is to determine the impact of the debt evolution in the WAEMU zone on development sustainability in the WAEMU covering the period from 2004 to 2018.

The major contributions made through this research are essentially based on two elements. The first is the use of the genuine savings indicator instead of the commonly used GDP. This genuine savings indicator is more comprehensive than GDP and takes into account the three dimensions of sustainable development (economic, social and environmental). The second element is the introduction of the variable “environmental expenditure” to capture expenditures devoted to combating climate change and/or adapting to climate change. As this expenditures does not appear in any of the national or international databases consulted to date, it has been compiled through the budgets allocated to the ministries of the union countries responsible for the environment and sustainable development. In order to provide some answers, we organise the rest of the paper as follows: Section 1 presents the literature review. In section 2, we present the econometric approach and the estimation method. In section 3, we present and discuss the results of our estimations. Finally, in section 4 we conclude and highlight the policy implications in section 5.

2. Literature review

Two schools of thought clash on the economic theory of external debt and growth, namely the Keynesians and the neoclassicists (Diallo, Citation2007). For the Keynesians, debt does not impose a burden on either future or current generations because of the investments it generates. In this approach, since debt stimulates demand, it has an accelerating effect on a more proportional increase in investment, which in turn stimulates an increase in production. On the other hand, the classics consider debt to be a future tax and attribute it to the state. This is a negative connotation, because according to them, public debt hinders the accumulation of capital and the consumption of present and future generations.

The analysis of the existing empirical literature has mostly resulted in a negative effect of debt on economic growth in developing countries (Ahmed & Maarouf, Citation2021; Ferry & Raffinot, Citation2016; Popescu & Villieu, Citation2014). Thus, Elbadawi et al. (Citation1997) confirmed the effect of debt overhang on economic growth at the level of 99 developing countries and tried to identify the channel through which debt acts negatively on growth. To do so, they identified three transmission channels of the impact of debt on growth. These are the effect of debt on growth, the effect of debt on liquidity due to the drain on debt service and, finally, the effect of debt (indirectly) on public sector spending and deficits. The study concluded that it is the accumulation of debt that has a negative impact on growth. In a companion study in 2002, Patillo et al. (Citation2004) applied a growth accounting model to a group of 61 developing countries and found that doubling the average level of their external debt reduces the growth of both physical capital per capita and total factor productivity by almost one percentage point. However, the focus of these studies has been on growth, not development.

The issue of development sustainability is all the more topical in the current context characterised by the covid 19 pandemic, where most countries have seen their budget deficits worsen. Far from going back over the different facets of sustainable development that can be analysed in terms of weak or strong sustainability, this review will dwell on the one hand on the measures of this notion and on the other hand on the notion of debt seen according to three dimensions of sustainable development.

3. Measuring the sustainability of development

Whether it is isolated academic work, more structured proposals by non-governmental organisations, or work carried out under the aegis of bodies responsible for coordinating public statistical production, it can be said that all this production has had two major founding elements, the work of Nordhaus and Tobin (Citation1973), who were the first to propose an index of sustainable economic well-being (SMEW, for Sustainable Measure of Economic Welfare). However, it was the Brundtland report of the late 1980s, followed shortly afterwards by the implementation of Agenda 21 at the Rio summit, which stimulated the production of sets of sustainable development indicators.

The Brundtland (Citation1987) Report popularised the notion of sustainable development as a form of development that ensures the well-being of present generations without compromising that of future generations. The Brundtland definition has been used extensively to emphasise the need to consider both development and its sustainability. This need is indisputable, but it has sometimes been interpreted to mean that both things can and should be measured together. Many proposals for alternative indicators to GDP have followed this path and attempt to provide a comprehensive view of sustainable development, as Nordhaus and Tobin (Citation1973) had sought to do in their time. For example, the idea that a “green GDP” could constitute an acceptable standard of sustainable development is in line with this logic. There are several types of indicators for measuring sustainability, among which we can mention genuine savings, the index of economic well-being (IEW), and green GDP, which are considered as alternative indicators to GDP.

Problems arise at the level of implementation, and in particular in the way information on these different sustainability factors is accounted for and aggregated to a greater or lesser extent (Blanchet, Citation2012). In this review, we will focus on the genuine savings (adjusted net savings) developed by a team of researchers at the World Bank.

Guenine savings combine data on the evolution of productive capital (savings in the classical sense), its depreciation, the accumulation of human capital, the consumption of exhaustible and renewable natural resources. In order to build a synthetic sustainability index, we need to define the way in which we will weight the evolutions of these different sustainability factors.

According to Clerc and al. (Citation2010), the genuine savings indicator is an aggregate sustainability indicator, very explicitly based on the stock approach. The idea is to quantify globally, for each country, the direction of the evolution of its “enlarged” capital, including both its capital in the usual economic sense of the term, i.e. its global savings rate net of the depreciation of fixed capital, its human capital, the variation of which is estimated in a very imperfect way by education expenditures, and its various natural resources, whether non-renewable (mineral resources) or renewable (forests, etc.). This indicator is supplemented by a count of emissions into the atmosphere of CO2 and other polluting particles, considered to be factors in the degradation of the “capital” that is climate quality and air quality. Such an approach, in principle, is well in line with the idea of quantifying the net “overconsumption” of resources. It does so with an analytical framework that is linked to the concepts of national accounting, and it has the advantage of reminding us that sustainability is not only an environmental issue: a country that preserves its natural resources but totally neglects material investment or the education of the young generations would not be in a more sustainable situation than a country that makes exactly the opposite choices.

4. Debt as seen through the three dimensions of sustainable development

Rising debt ratios and government payment difficulties are fundamentally rooted in two types of vulnerabilities: the exposure of economies to shocks and certain institutional and political fragilities (Brooks and al., Citation1998). Indeed, for Bua et al. (Citation2014), during the economic crisis, the implementation of fiscal stimulus packages and the decline in development aid contributed to the increase in domestic public debt in sub-Saharan African countries. This debt is mainly held by the banking system, which is hampered by a weak judicial system (Andrianaivo & Yartey, Citation2009). Institutional weaknesses have limited the role of African banks in financing the private sector. They are becoming reluctant to channel resources to the private sector, preferring to hold safer and more profitable government securities (Abuka & Egesa, Citation2007). These developments have increased the risks of a return to public over-indebtedness and it is possible that the recent progress made in debt control may be reversed (Chauvin & Golitin, Citation2010; Presbitero, Citation2009; Quattri & Fosu, Citation2012). In addition, Emran and Farazi (Citation2009) manage to confirm the crowding-out hypothesis that increased government borrowing from banks reduces the availability of credit to the private sector in 60 developing countries over the period 1975–2006. This result was also found by (Bonis & Stacchini, Citation2013) who report that, during the period 1970–2010, increased government debt led to a decline in credit to the private sector in 43 countries (including 23 OECD countries).

At the social level, debt, whether public or private, makes it possible to characterise all social relations. The question that arises is how to qualify these different social relations that develop under the influence of debt. To do this, it is important to start from the definition of sustainable development set out in the Brundtland report (Brundtland, Citation1987) as being “development that strives to meet the needs of the present without compromising the ability to meet the needs of future generations”. On the one hand, in its definition, sustainable development requires “the satisfaction of needs”, which implies, in addition to the satisfaction of basic needs, the set of goods and rights to which people aspire (Jacob, Citation1988). This will enable a high level of well-being to be achieved. However, with a high level of indebtedness, it would be impossible to satisfy one’s various needs because current income will be used to repay debts. On the other hand, this definition is about giving future generations the capacity to satisfy their own needs. This raises the problem of the transmission of available resources from one generation to the next. However, it is likely that it will be difficult to meet future needs in the same way as today. The debts incurred by a country today are a burden for future generations and therefore a very large debt may compromise the ability of future generations to take care of themselves and thus the sustainability of the economy. A problem of equity between generations therefore arises. Indeed, the attitude of current generations in terms of debt management conditions the well-being of future generations and in particular the sustainability of the development trajectory.

In another significant development, the re-indebtedness of Heavily Indebted Poor Countries (HIPCs) was justified at the Addis Ababa Conference in July 2015 by the financing needs of these countries, both for their development and for their adaptation to climate change. Poor countries, including those in West Africa, are the most affected by the negative effects of climate change (prolonged droughts, rising sea levels and rainfall, rampant desertification, etc.). These negative effects could reduce Africa’s GDP by 2 to 4% by 2040 and by 10 to 25% by 2100.Footnote4 This will inevitably have consequences for the productive apparatus of African countries. Poor countries, particularly in Africa, have few resources to cope with the effects of climate change. For an effective response to the major challenges in the fight against the effects of climate change, African countries, particularly West African countries, certainly benefit from public development aid, but in most cases they contract debts or go back into debt.

In conclusion, with reference to the existing literature, we assume that the current debt velocity is a function of moral hazard factors, institutional factors (low institutional quality), factors related to climate change and climate adaptation, domestic indebtedness, the domestic savings deficit, tax revenue and external resource deficit arising from low exports of goods and services, the preference for the present, the significant decline in the fiscal effort of HIPC recipient governments.

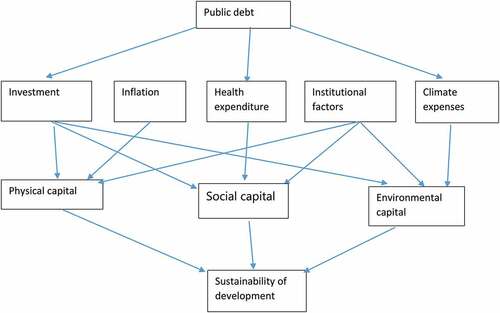

5. Conceptual framework

The conceptual framework of this study is based on the concept of sustainable development, which implies taking into account the economic, social and environmental dimensions in economic analysis. It is a matter of rethinking the relationship between human beings and nature. It is a question of taking a critical look at a mode of development that too often damages the environment and relegates the majority of humanity to poverty. It is therefore necessary to remedy the shortcomings of a development model based on economic growth alone by reconsidering our ways of doing things in order to maintain the integrity of the environment, ensure social equity and aim for economic efficiency in order to create an innovative and prosperous economy that is environmentally and socially responsible (Ahmed & Maarouf, Citation2021; Diallo, Citation2007). To achieve this ideal of harmonious development in the context of WAEMU countries, the important role that debt can play cannot be overlooked. It is in this context that this paper measures the impact of public debt on the sustainability of WAEMU economies.

The below shows the mechanisms by which the independent variables chosen in this study influence development sustainability.

Figure 1. Conceptual framework of the relationship between public debt and development sustainability.Source: Authors (2021)

6. Econometric approach and estimation methodology

6.1. Estimation techniques

This paper seeks to capture the impact of public debt on the genuine savings indicator in WAEMU countries, and the econometric estimation method adopted is based on the dynamic panel techniques developed in the work of Arellano and Bond (Citation1991), the generalized methods of moments (GMM) in dynamic panels. The choice of this technique is justified by the fact that it provides solutions to the problems of simultaneity bias, endogeneity, reverse causality, over-instrumentation bias and omitted variables. For our model, we have therefore chosen a GMM estimation on a dynamic panel, i.e. a model in which at least one lag of the dependent variable appears as an explanatory variable. It also consists of lagging the variables by one or two periods to correct for endogeneity (Arellano & Bond, Citation1991). And these lagged variables serve at the same time as instruments. Thus, the interest of using such an estimator is multiple. On the one hand, it allows the dependent variable to be lagged by two periods as instruments of the explained variable and also allows the variable to be lagged by more than two periods, thus avoiding correlation with the error term. Finally, the Arellano Bond estimator solves the stationarity problem on the one hand (first difference of the variables) and on the other hand avoids the autocorrelation problem. The use of a dynamic panel can be justified in this context by the fact that the effect of the variables selected on true savings can only be better appreciated in year n + 1.

7. Empirical specification

A number of variables enter into the explanation of the sustainability of development represented here by genuine savings, which takes into account the dimensions of sustainable development. However, in this research, we only take into account the variables indicated by the literature and which are crucial for the WAEMU zone by highlighting the effect of public debt on the guenine savings indicator. In order to achieve the objectives set, we retain the following empirical specification:

Where IEV is the sustainability indicator developed by the World Bank in 2006. This indicator is calculated as the sum of net savings (EPN) and current expenditure on education (DED) minus depreciation of natural resources in energy, mining and forestry (ΣDRN) and damages related to pollution by CO2 (DL):

The depreciation of natural resources is calculated as the sum of the mining rent (Rm) which is the income from fossil fuels and minerals, the energy rent (Re) and the forest rent (Rf):

Net saving takes into account the economic dimension, current expenditure on education takes into account the social dimension and is considered as an asset improving the productivity and wealth production of a country. On the other hand, natural resource depreciation and pollution damage are considered as a process of liquidation of natural assets contributing negatively to income and genuine savings. Both variables take into account the environmental dimension.

Despite the fact that genuine savings have a number of limitations, we use them for two main reasons as outlined by (Anani, Citation2020). The first reason is that it allows us to gauge the real level of a country’s total wealth in the broad sense (produced, human and natural capital), and thus to assess the potential sustainability or otherwise of the country’s various capitals (physical, natural and human capital) management, as well as of their interactions. The second reason is that it makes it possible to assess a country’s vulnerability, understood at the macroeconomic level as the risk for countries of seeing the sustainability of their trajectory hampered by hazards (Guillaumont, Citation2006). DETOT The debt ratio: represents the weight of the total debt, the dependent variable. The debts contracted today by a country constitute a burden for future generations and thus, a very large debt may compromise the sustainability of the economy. The physical capital stock (K) at time t is measured by the following formula:

I is the amount of additional investment. δ is the rate of depreciation, which is assumed to be 0.03. The initial capital stock of the country K0 is given by the following formula: where (I/Y) is the average share of physical investment in output over the period, γ is the average growth rate of output per capita over the period, n is the average growth rate of population.

DEPSANT, represents a large share of GDP and employment according to (Cornilleau, Citation2012). Therefore, their increase may impact the level of debt and thus the sustainability of the country. DEPCLIM, expenditures on climate change and/or adaptation to climate change. For reasons of non-exhaustive availability of information and data, we consider in our estimates the budgets allocated to the ministries in charge of the environment in each WAEMU country, which gives us a representative idea of the expenditures related to the fight against climate change and adaptation to climate change. Although limiting because this measure does not include money injected by other entities (national and international), further work can re-use the same broader indicator if the data is available; FACTINST, institutional factors, measured in our estimation along the lines of Kaufmann et al. (Citation1999). It is calculated as the average of six measures of institutions: (i) citizen participation and accountability, (ii) political stability and absence of violence, (iii) government effectiveness, (iv) regulatory burden, (v) rule of law, and (vi) absence of corruption. Many recent studies have shown that the quality of a country’s institutions is an important explanatory factor of its economic development (Belaïd et al., Citation2009); INFLAT, is a phenomenon about which there is much controversy among economists: the debate is about the consequences, which are sometimes considered positive, as well as about the causes. It is a central element that can affect the depreciation of capital. the constant term;

the error term.

8. Data presentation

The data used for the estimates come mainly from the database of the Central Bank of West African States (BCEAO, Citation2020), the World Bank (World Development Indicators, Citation2019) and the ministries of finance and economy of the various WAEMU countries (country budget document). The data for the six measures used in the institutional quality measurement are taken from the World Governance Indicators (Citation2019). The study covers the eight (08) WAEMU countries, namely: Benin, Burkina Faso, Côte d’Ivoire, Guinea Bissau, Mali, Niger, Senegal and Togo. Also, the period covered by this study goes from 2004 to 2018 due to the low availability of data. In order to be used, the data were leveled and some of the data log-linearized to reduce the size effect.

9. Descriptive analysis of variables

Table (Means and standard deviation) below presents the statistics on the different variables for all countries (2004–2018). On average, the genuine savings indicator (Iev) is 5.4 over the period for all countries with a variation from one country to another of 1.2. For our variable of interest, the stock of debt to GDP, the average is 3.005 with a variation from one country to another of 0.37. For the capital stock, the share of climate expenditure in GDP, their averages are respectively 9.14; 11.93. The institutional factor variable, which is an average of six governance indicators expressed on a scale of [−2.5 + 2.5] where −2.5 means very poor governance and +2.5 very good governance, is positive with an average of 0.63, which is almost in the middle of the range. This suggests that significant efforts in governance in the WAEMU zone are still possible. The average inflation level in the zone is 2.59 with a standard deviation of 0.57, which seems low for developing countries and indicates an active inflation control policy on the part of monetary authorities. The average health expenditures of the countries in the region was 9,796 over the study period.

Table 1. Means and standard deviation

Table 2. Estimation results

10. Empirical results

First, the Wald test associated with the coefficients of the variables is Wald chi2 (7) = 201.07 with Prob > chi2 = 0.0000. We therefore reject the null hypothesis of joint nullity of the coefficients associated with the variables. As for the validity and reliability of the instruments, they are indicated by the Sargan/Hansen overidentification test. The result of this test does not reject the hypothesis of validity of the lagged variables in level and difference as instruments (p = 0.971). As for the Arellano and Bond test on first and second order autocorrelation, it does not allow to reject the presence of first order autocorrelation (p = 0.007) and absence of second order autocorrelation (p = 0.253).

As we have pointed out above, the genuine savings indicator gives an idea of the level of sustainability of a country’s development. Thus, improving the level of sustainability implies that the development path is in a growth dynamic. Note that its previous level is a determinant of its current level. In our estimations, the sustainability of development is negatively and significantly explained by the guenine savings of year (t-1) at the 1% threshold (P>|z| = 0.000) with a coefficient of (−1.280). This can be explained by the fact that rents linked to the exploitation of natural resources are not reinvested in productive capital in the sense of the weak sustainability principle to keep the total capital stock (natural and manufacturing) intact. As it stands, our results show that intergenerational equity is not guaranteed.

Our results also show that the variable of climate change expenditures and environmental protection has a positive impact on the development sustainability of WAEMU countries. It is significant at the 1% level (P>|z| = 0.000). For each 1% increase in the level of public expenditures on climate change and environmental protection, the level of adjusted net savings increases by 0.05687. This result should lead WAEMU countries to invest more optimally in climate change policies, both in terms of mitigation and adaptation measures. These countries must also strengthen their investments in environmental protection. These different measures should contribute to strengthening the sustainability of development in these countries.

As regards inflation and debt/GDP ratio, they negatively impact the level of development sustainability with a coefficient (−3.411) and (−1.367) respectively, all significant at the 1% threshold (P>|z| = 0.000). Thus, any one point increase in the level of inflation leads to a decrease in adjusted net savings of 3.411. This suggests that genuine savings wear out with an increase in the level of inflation. Indeed, the appearance of inflation in a modern economy does not necessarily relieve debt repayment (Bouzou, Citation2010). An increase in inflation would almost immediately translate into an increase in the cost of variable-rate loans and new loans, loans that will be paid for by both present and future generations and which therefore suffer a depreciation of their adjusted net savings. The pursuit of the inflation control policy instigated by the Central Bank of West African States (BCEAO) must be encouraged in order to put these states on the path of sustainable development initiated in 2006.

Regarding to the debt/GDP ratio, a 1% increase in the debt/GDP ratio leads to a decrease in adjusted net savings of 1.367. In a more conventional logic, the sustainability of a country’s external debt, i.e. its international debt capacity, is defined by the stability of the debt/GDP ratio (d). Δd represents the variation of the debt/GDP ratio and the external debt becomes unsustainable when Δd > 0. Thus, in this case, we can say that debt unsustainability has a negative impact on development sustainability. This calls for a control of the level of indebtedness which, according to Reinhart and Rogoff (Citation2009), is the fragility of the institutional structures and the political system that explain the recurrence of sovereign defaults. Moreover, an alternative approach argues that the causes of debt intolerance are to be found in the economic structure of countries and in particular in their intrinsic vulnerability to macroeconomic shocks (Catão & Kapur, Citation2006). Generally, the threshold for making debt sustainable is 70% according to the WAEMU convergence criteria.

The capital stock has a positive effect on the development sustainability in WAEMU countries with a coefficient of 1.934574 significant at the 1% level (P>|z| = 0.000). A 1% increase in the capital stock leads to an increase in genuine savings of 1.935 points. The countries of the zone must therefore increase their physical investment either through policies of large-scale construction of sustainable infrastructures that can generate capital accumulation.

As far as institutional factors are concerned, they contribute positively and significantly to the sustainability of the countries development in the zone. An increase of one point in the improvement of governance leads to an increase of 2.037 points in genuine savings. This result corroborates the one found by (Belaïd et al., Citation2009) who showed that the quality of a country’s institutions is an important explanatory factor of its economic development. Institutional factors referring to institutional quality and political instability impact development sustainability through the quality of governance and the way regulations are implemented and enforced. As Edison (Citation2003) points out, countries with good institutional quality are on a sustainable development trajectory. The institutional variable also tells us about the direction of the relationship between political stability and development sustainability. The more political stability there is in developing countries (the WAEMU zone), the more appropriate the conditions are for the promotion of sustained and equitable economic growth (Feng, Citation1997, Citation2003; Sirowy & Inkeles, Citation1990)

11. Conclusion

The general objective of this research is to determine the impact of public debt on the sustainability of development, as captured here by the genuine savings indicator in the WAEMU zone over the period 2004 to 2018. After estimations, the results show a negative and significant contribution of the guenine savings indicator of the year (t-1), public debt, as well as inflation. As for the variables capital stock, health expenditures, institutional factors, climate change expenditures and environmental protection, they influence positively and significantly the genuine savings variable. Thus, we can note that the previous level of the genuine savings indicator (ievt-1) is a determinant of its current level and our results show that it is imperative that rents from the exploitation of natural resources be reinvested in productive capital to maintain the sustainability of the development of the countries of the zone (Ogwumike & Ogunleye, Citation2008).

12. Economic policy implications

Following the results, economic policy implications emerge. Also, to ensure the sustainability of the WAEMU countries development, it will be necessary to control the public debt of member countries. This should be a challenge to public authorities at a time of the Covid 19 pandemic when most countries have seen their budget deficits widen further and one of the ways to cope with the crisis and continue to provide public services is to resort to debt. A good policy of monitoring the optimal level of debt is therefore necessary to ensure intergenerational equity because, as our results show so well, unsustainable debt has a negative impact on the sustainability of the union countries development. Also, the continuation of the anti-inflationary policy of the BCEAO must be encouraged. However, the countries of the zone must invest more in health and in programmes and policies to combat climate change and protect the environment. It is also noted that the capital stock has a positive effect on the genuine savings indicator and therefore leads to a holistic reflection on public investment, which must be sustainable.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Komlan Ametowoyo Adeve

Komlan Ametowoyo Adeve, is a Lecturer at University of Kara (Department of Economics). Author of several scientific publications, experienced researcher, he is a specialist in environmental economics, natural resources economics, public economics, public finance, macroeconomics, development economics and applied economics.

Essosinam Franck Karabou

Essosinam Franck Karabou, is a Lecturer at the University of Kara (Department of Economics). Author of several scientific publications, experienced researcher, he is a specialist in public economics, public finance, macroeconomics, development economics and applied economics.

Notes

1. ECOWAS: Economic Community of West African States.

2. WAEMU Multilateral Surveillance Report, (2018).

3. BCEAO data, 2018

4. Agence Ecofin n° 130 “Climate change: Africa will pay a high price for the debt of industrialised countries”.

References

- Abuka, C. A., & Egesa, K. A. (2007). An assessment of private sector credit evolution in the East African Community: The candidates for a region wide reform strategy for the financial sector 1 | semantic scholar. The Bank ofUganda Staff Papers Journal, 1(2), 107–13. https://www.semanticscholar.org/paper/An-assessment-of-private-sector-credit-evolution-in-Abuka-Egesa/dc45eeb40216b755ae63e46c79fb3dbaabc18574

- AFD. (2013). Endettement soutenable et développement durable: Extraits de Au Sud du Sahara, La lettre du Département Afrique subsaharienne de l’agence Française de Développement, n°2, janvier 2013. Techniques Financières Et Développement, 110, 37–44. https://doi.org/10.3917/tfd.110.0037

- Ahmed, O., & Maarouf, A. (2021). La dette publique extérieure de Djibouti: Soutenabilité et impact sur la croissance économique. https://halshs.archives-ouvertes.fr/halshs-03280083/document

- Anani, E. T. G. (2019). Le boum du secteur minier des années 2000 : Enjeux de développement et de soutenabilité dans la zone UEMOA, dans Enjeux et perspectives économiques en Afrique francophone (Dakar, 4 – 6 février 2019). Montréal: Observatoire de la Francophonie économique de l’Université de Montréal, 528–543 p. 17. https://ofe.umontreal.ca/fileadmin/ofe/documents/Actes/Conf_OFE_UCAD_2019/64-_E-T-G-ANANI.pdf

- Anani, E. T. G. (2020). Le boom du secteur minier des années 2000: Enjeux de soutenabilité dans la zone UEMOA. Mondes en développement, n° 189(189), 99–124. https://doi.org/10.3917/med.189.0099

- Andrianaivo, M., & Yartey, C. A. (2009). Understanding the growth of African financial markets. In SSRN scholarly paper ID 1474590. Social Science Research Network. https://ssrn.com/abstract=1474590

- Aragie, E., Taffesse, A. S., & Thurlow, J. (2021). The short-term economywide impacts of COVID-19 in Africa: Insights from Ethiopia. African Development Review, 33, S152–S164. https://doi.org/10.1111/1467-8268.12519

- Arellano, M., & Bond, S. (1991). Some tests of specification for panel data: Monte carlo evidence and an application to employment equations. The Review of Economic Studies, 58(2), 277. https://doi.org/10.2307/2297968

- BCEAO. (2020). Données statistiques économiques et financières. Banque Centrale des Etats de l'Afrique de l'Ouest.

- Belaïd, R., Gasmi, F., & Recuero Virto, L. (2009). La qualité des institutions influence-t-elle la performance économique ? Le cas des télécommunications dans les pays en voie de développement [*] | Cairn.info, Revue d’économie du développement, 17(3), 51–81.

- Blanchet, D. (2012). La mesure de la soutenabilité: Les antécédents, les propositions et les principales suites du rapport Stiglitz-Sen-Fitoussi. Revue de l’OFCE, 120(1), 287. https://doi.org/10.3917/reof.120.0287

- Bonis, R. D., & Stacchini, M. (2013). Does government debt affect bank credit? International Finance, 16(3), 289–310. https://doi.org/10.1111/j.1468-2362.2013.12037.x.

- Bouzou, N. (2010). Nicolas Bouzou - Stratégie pour une réduction de la dette publique française, Fondapol.

- Brooks, R., Cortes, M., Fornasari, F., Ketchekmen, B., Metzgen, Y., Powell, R., . & Ross, K. (1998). External debt histories of ten low-income developing countries : Lessons from their experience. IMF Working Paper, 1998(072), WP/98/72. International Monetary Fund. https://doi.org/10.5089/9781451849318.001 https://www.elibrary.imf.org/view/journals/001/1998/072/article-A001-en.xml

- Brundtland (1987). Le rapport Brundtland pour le développement durable - Geo.fr.

- Bua, G., Pradelli, J., & Presbitero, A. F. (2014). Domestic public debt in low-income countries: Trends and structure, policy research. Working Paper Series. 6777, The World Bank.

- Catão, L., & Kapur, S. (2006). Volatility and the debt-intolerance paradox by Luis Catão and Sandeep Kapur. IMF Staff Papers, 53(2), 195–218. https://doi.org/10.2307/30036011

- Chauvin, S., & Golitin, V. (2010). Besoins de financement et viabilité de la dette extérieure dans les pays d’Afrique subsaharienne. Bulletin de la Banque de France, 179, 31–51. https://core.ac.uk/download/pdf/6389553.pdf

- Clerc, M., Gaini, M., & Blanchet, D. (2010). Recommendations of the Stiglitz-Sen-Fitoussi Report: A few illustrations. L’economie francaise–2010 edition, Insee. http://www.insee.fr/en/publications-et-services/default.asp

- Cornilleau, G. (2012). Croissance et dépenses de santé. Les Tribunes de la Sante, 36(3), 29–40. https://doi.org/10.3917/seve.036.0029

- Couharde, C., Géronimi, V., & Taranco, A. (2012). Les hausses récentes des cours des matières premières traduisent-elles l’entrée dans un régime de prix plus élevés ? Revue Tiers Monde, 211(3), 13–34. https://doi.org/10.3917/rtm.211.0013

- Devarajan, S., & Fengler, W. (2013). L’essor économique de l’Afrique. Motifs d’optimisme et de pessimisme [1] | Cairn.info, Revue d’économie du développement, 21(4), 97–113. https://www.cairn.info/revue-d-economie-du-developpement-2013-4-page-97.htm

- Diallo, B., (2007). Dette extérieure et financement du développement économique en guinée. Actes de Conférence 2007, 231–261. https://www.afdb.org/fileadmin/uploads/afdb/Documents/Knowledge/Conference_2007_09-part-II-2.pdf

- Edison, H. (2003). Qualité des institutions et résultats économiques : Un lien vraiment étroit? Finances et Développement, p. 3 35–37. https://www.imf.org/external/pubs/ft/fandd/fre/2003/06/pdf/edison.pdf

- Elbadawi, I., Ndulu, B., & Ndung’u, N. (1997). Debt overhang and economic growth in sub-saharan Africa, external finance for low-income countries. FMI, Zubair Iqbal and Ravi Kanbur.

- Emran, M. S., & Farazi, S. (2009). Lazy banks? Government borrowing and private credit in developing countries. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.1418145

- Feng, Y. (1997). Democracy, political stability and economic growth. British Journal of Political Science, 27(3), 391–418. https://doi.org/10.1017/S0007123497000197

- Feng, Y. (2003). Democracy, governance, and economic performance: theory and evidence. MIT press. https://doi.org/10.7551/mitpress/2329.001.0001

- Ferreira, C. (2009). Public debt and economic growth: A granger causality panel data approach, working papers No 24/2009/DE/UECE. ISEG - Departamento de Economia. http://hdl.handle.net/10400.5/1863

- Ferry, M., & Raffinot, M. (2016). Réductions de dette, aléa moral et ré-endettement des pays à faible revenu | Cairn.info. Techniques Financières et Développement, 123(2), 51–66. https://doi.org/10.3917/tfd.123.0051

- Gani, W. (2021). The causal relationship between corruption and irresponsible behavior in the time of COVID-19: Evidence from Tunisia. African Development Review, 33, S165–S176. https://doi.org/10.1111/1467-8268.12518

- Guillaumont, P. (2006). La Vulnérabilité Économique, Défi Persistant à la Croissance Africaine. African Development Review, 19(1), 123–162. https://doi.org/10.1111/j.1467-8268.2007.00157.x.

- Hugon, P. (2013). L’économie de l’Afrique. La Découverte.

- IMF (2012). Une reprise en cours, mais qui reste en danger, Perspectives de l’économie mondiale. Washington, avril.

- Jacob, A. (1988). John Rawls, Catherine Audard (Trad.), Théorie de la justice, Seuil, 1987. Persée, L’Homme et la société, 87(1), 122–123. https://www.persee.fr/doc/homso_0018-4306_1988_num_87_1_3217

- Kaufmann, D., Kraay, A., & Zoido-Lobaton, P. (1999). Governance matters. Policy Research Working Paper Series, 2196. The World Bank. https://deliverypdf.ssrn.com/delivery.php?ID=438094071086117068009000086088109123056020030032038022077093106012094006076103110022025071027022094069001053011029010101107104000122090113099066068078080100004126122069115109022026103091098&EXT=pdf&INDEX=TRUE

- Mckinsey and Company (2010). L’envol des entreprises en Afrique: Réussir sur le marché porteur de demain | Morocco | McKinsey & Company, https://www.mckinsey.com/ma/africas-business-revolution

- Njatang, D. K. (2021). Impact économique de la COVID-19 au Cameroun: Les résultats du modèle SIR-macro. African Development Review, 33, S126–S138. https://doi.org/10.1111/1467-8268.12516

- Nordhaus, W., & Tobin, J. (1973). Is growth obsolete?. NBER Chapters. National Bureau of Economic Research, Inc.

- OCDE. (2013). Perspectives de l’OCDE sur les compétences 2013: Premiers résultats de l’Evaluation des compétences des adultes. https://doi.org/10.1787/9789264204096-fr

- OCDE (2013). Perspectives de l’OCDE sur les compétences 2013: Premiers résultats de l’Evaluation des compétences des adultes. https://doi.org/10.1787/9789264204096-fr

- Ogwumike, F. O., & Ogunleye, E. K. (2008). Resource-led development: An illustrative example from Nigeria. African Development Review, 20(2), 200–220. https://doi.org/10.1111/j.1467-8268.2008.00182.x

- Patillo, C., Ricci, L., & Poirson, H., 2004. Dette Extérieure et Croissance Economique. Imf Working Papers.

- Popescu, A., & Villieu, P. (2014). Déficit budgétaire, dette publique et croissance dans les pays d’Europe centrale et orientale. Mondes En Developpement, 167(3), 53–72. https://doi.org/10.3917/med.167.0053

- Presbitero, A. F. (2009). Debt-relief effectiveness and institution-building. Development Policy Review, 27(5), 529–559. https://doi.org/10.1111/j.1467-7679.2009.00458.x

- Quattri, M. A., & Fosu, A. (2012). On the impact of external debt and aid on public expenditure allocation in sub-saharan Africa after the launch of the hipc initiative. 2012 Conference, August 18-24, 2012, Foz do Iguacu, Brazil 126879. International Association of Agricultural Economists.

- Reinhart, C. M., & Rogoff, K. S. (2009). The aftermath of financial crises | NBER. American Economic Review, American Economic Association, 99(2), 466–472. https://doi.org/10.1257/aer.99.2.466

- Sikod, F., Djal‐Gadom, G., & Totouom, E. A. L. F. (2013). Soutenabilité Economique d’une Ressource Epuisable: Cas du Pétrole Tchadien. African Development Review, 25(3), 344–357. https://doi.org/10.1111/j.1467-8268.2013.12033.x

- Sirowy, L., & Inkeles, A. (1990). The effects of democracy on economic growth and inequality: A review |. SpringerLink, Studies in Comparative International Development, 25, 126–157. https://link.springer.com/article/10.1007/BF02716908

- World Development Indicators (2019). World development indicators | databank.

- World Governance Indicators (2019). WGI 2020 interactive > home.