?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Considered among of the main causes of the 2007 financial crisis, the credit risk transfer activities deserve nowadays particular attention. This study discusses the continuous effectiveness of the credit risk transfer activities by investigating their effects on the bank risk, liquidity and profitability before the crisis event and contributes to the recent scarce literature identifying this effect in the post-crisis period. Using models treating this impact on two samples of US commercial banks over the period from 2001 to 2017, the obtained results suggest an overall amplification of the risk incurred by banks notably before the crisis, a decrease of liquid assets hold on balance sheet and, generally an increase of the profitability. The employment of credit derivatives does not exhibit a conclusive result of its impact on the banking stability and performance. Nevertheless, the effect of residential mortgage loans securitization on bank risk appeared to be negative after the crisis, indicating that the securitization of this type of credit can reduce the bank risk in the detriment of a lower profit, in the new regulatory context required by Basel III.

1. Introduction

The great development of credit risk transfer market was remarkable during the decade preceding the 2007 financial crisis and was the novel key element characterizing this international turmoil. The credit derivatives and the securitization constitute two credit risk transfer means used by banks to appropriate the management of credit risk and enhance the bank performance. Through the use of credit risk transfer, banks are not constrained to conserve the credit in their balance sheet until maturity. They transfer pools of loans from their balance sheet via securitization and/or sell credit risk across credit derivatives to other banks or financial actors, converting hence illiquid loans to liquid securities. This can, ordinarily, contribute to enhance liquidity, reduce the risk of bankruptcy, and create a new technique for optimizing the regulatory capital, promoting thus the profitability (Agostino & Mazzuca, Citation2011; Cardone-Riportella et al., Citation2010; Duffie, Citation2008).

Banks exploit the securitization as a source of funding new assets and granting more loans that can be riskier. They have, excessively, used this opportunity to change their traditional feature as lenders, to “originators and distributors” of loans. In this context, the strategy of banks to use securitization has been diverted from discarding the credit risk to rising profitability; which further accentuated the utilization of the credit risk transfer instruments until the crisis event. The use of these instruments has affected considerably the risk-taking behavior of banks, leading them to admit higher level of risk and hold fewer liquid assets in their balance sheet (Brunnermeier, Citation2009; Le et al., Citation2016; Loutskina, Citation2011). Furthermore, the credit risk transfer activities have introduced an increasingly broad range of underlying assets with non-performing characteristics, more heterogeneous, less liquid and higher level of risk and involved several unregulated and non-monitored structures. Within this framework, the risk cannot be clearly identified and assessed by banks (Pinto, Citation2014).

The excessive development of credit risk transfer activities, the abusive use of the structured and complex financial instruments, the less transparency of credit risk transfer market have exposed the banks and the system to a problem of assessing and identifying the real risk. While, the appropriate credit risk evaluation is a crucial step of an effective bank risk management as analyzed recently by Caruso et al. (Citation2021). The lack of risk assessment may cause dysfunctions leading to a serious disruption of banking and financial system as a whole. The occurrence of the 2007 financial crisis constitutes the most serious dysfunction caused mainly by the credit risk transfer mechanisms and raises several questions related to the effectiveness of these mechanisms. The banking and financial soundness and stability targeted by the use of credit risk transfer technique is then doubted, particularly with the seriousness nature of the 2007 financial crisis. The relationship between the banking performance and stability and the credit risk transfer has been the subject of several studies and reports (Basel Committee on Banking Supervision (BCBS), Citation2004; Bedendo & Bruno, Citation2012; Chiesa, Citation2008; European Central Bank, Citation2014; Gao & Mcconnell, Citation2018; International Association of Insurance Supervisors (IAIS), Citation2003; Wagner & Marsh, Citation2006). Nevertheless, most of these studies miss the effective impact of this mechanism. Some of them, consider that the credit risk transfer promotes banking stability and performance, others assume the opposite. The outbreak of the last financial crisis of 2007–2008 paved the way for more debate on this topic and indicates that credit risk transfer practices have raised the risk at least in this period and could deteriorate the bank performance. Identifying the faithful impact of credit risk transfer technique on banking stability and performance and learning about the effectiveness continuation of its usage requires, therefore, a deep and accurate study. In this research work, we intend to highlight the effect of securitization and credit derivative on banking risk, liquidity and profitability. The current analysis is conducted on a large sample of commercial US banks that have been divided into two categories large and medium-size banks. Furthermore, a range of 17 years is considered in this study, spread out in two periods: 7 years before the crisis and 10 years after the outbreak of this event. This is to better capture the effect of credit risk transfer for different financial circumstances, to enrich the limited recent studies after the crisis and to identify the evolution of using this mechanism after this event in the framework of new regulatory measures of Basel III. Moreover, three indicators assessing the banking risk have been employed in this study for better accuracy. Instead of the classic proxy banks’ capital ratio, three indicators have been considered in this work: (NPLa) which represents the share of non-performing loans in total assets, the z-score which measures the distance-to-default banks and finally ГROA (the standard deviation of asset returns) which measures the volatility of assets returns. Then, the study will focus on the effect of credit risk transfer activities on liquidity, evaluated by the liquid assets hold on the balance sheet, and finally on trofitability measured by the ROE.

The remainder of the article is organized as follow: the section 2 presents a contextual of the related studies. The section 3 explains the data set of the selected samples and the section 4 performs a descriptive analysis. Section 5 reports the empirical analysis and discusses the obtained results. A general conclusion will be presented in the end of the manuscript.

2. Related literature review

The credit risk transfer has introduced considerable changes to the traditional credit market functioning. Both theoretical and empirical analyses conducted on the effectiveness of this mechanism on bank stability and performance have not converged towards a firm conclusion.

The effect of credit risk transfer is still ambiguous. Normally, the expected role of credit risk transfer is to contribute to banking stability and performance. The notable evolution of this mechanism over the decade preceding the 2007–2008 crisis event are signs of benefits generated by the usage of this process. Cebenoyan and Strahan (Citation2004) showed that credit risk transfer promotes better managing the bank risk and rises profit. Securitization have, precisely, served to transfer the risk of banks to the financial market by transforming pools of illiquid loans into negotiable financial securities. This provides further sources of funding and allows the dissemination of these loans and, consequently, of the risk they present across a large number of investors (Hansel & Bannier, Citation2008; Wagner & Marsh, Citation2006). Allen and Gale (Citation2005) stated that the transfer of credit risk leads to a better distribution and diversification of risk. In the same context, Duffie (Citation2008) assumed that this mechanism allows the optimization of banks’ asset portfolio. Jiangli et al. (Citation2007) proposed that banks which use securitization have lower insolvency risk, higher profitability, and countless on traditional sources of liquidity. Using a sample of US bank holding companies from 2001 to 2007, Jiangli and Pritsker (Citation2008) have analyzed the impact of different forms of asset securitizations on banking stability and performance. They found a positive effect of mortgage loan securitizations, which reduces the insolvency risk and increases the bank profitability. In the same outline, Venkatachalam (Citation1996) supported that banks, which use derivatives for hedging purposes could reduce their risk exposure. Minton et al. (Citation2004) and Karaoglu (Citation2005) argued that securitization allows banks to influence their profitability via their decision on the selection of assets to be securitized. Conducting studies on Spanish financial market, Solano et al. (Citation2009) have confirmed that securitization affects positively the bank performance. Ambrose et al. (Citation2005) sustained this positive effect and confirmed that securitization can enhance profitability, improve liquidity, and reduce or redistribute the credit risk. Altunbas et al. (Citation2009), have performed an empirical analyses on European securitization market and have deduced that securitization promotes the bank liquidity and affects the banks’ ability of loan supply.

In the opposite side, Krahnen and Wilde (Citation2006) and Trapp and Weib (Citation2016) suggested that the process of securitization rises the systematic risk of the issuing bank. Similarly, Iglesias-Casal et al. (Citation2016) concluded that securitization leads to an increase of Italian and Spanish systematic banks risk. Franke and Krahnen (Citation2006), Instefjord (Citation2005), and Hansel and Krahnen (Citation2007) have also found a positive effect of credit risk securitization on systematic bank risk. Wagner (Citation2007) considered that credit risk transfer tool facilitates the liquidation of bank assets but encourages banks to take on more risk. Similarly, specific studies on European banks that issued cash and synthetic securitizations showed a positive effect of securitization on the increase of systematic risk, particularly, of large banks that are more engaged in the securitization activities (Farruggio & Uhde, Citation2015; Uhde and Michalak, Citation2010). Casu et al. (Citation2013) and Uzun and Webb (Citation2007) indicated that the size of the bank is a determinant factor of securitization activities and confirmed that large banks are more active in securitization transactions. Examining the effect of these transactions on US banks’ performance, these authors have established an increase of profitability at the expense of higher risk, which requires advanced risk evaluation methods as developed recently by Caruso G. et al. 2021 via mixed data clustering techniques.

The credit risk transfer reduces the monitoring and supervising efforts of banks, directing them to accept more risk (Deku et al., Citation2019; Kara et al., Citation2019; Morrison, Citation2005; Wang & Xia, Citation2014). In fact, expecting that they can rapidly liquefy portion of their assets and obtain greater liquidity, banks are encouraged to admit further risk (Cardone-Riportella et al., Citation2010; Kamstra et al., Citation2014; Wagner, Citation2007). In the same Keys et al. (Citation2012), (Citation2010)) have assumed that the securitized assets could be riskier than the similar non-securitized assets, due to a reduction of screening banks efforts. Moreover, Brunnermeier (Citation2009) confirmed that credit risk transfer activities encourage banks to grant more riskier loans. Similarly, Kara et al. (Citation2011) showed that the issuing of asset-backed securities directs the originator bank to laxer credit standards. Nijskens and Wagner (Citation2011) have performed a study on two samples of banks issuing, respectively, Credit Default Swaps (CDS) and Collateralized Loan Obligations (CLOs) before the crisis. They concluded that while the banks may decrease their individual credit risk, they revealed more systemic risk. Hirtle (Citation2009) indicated that banks, which use credit derivatives, increase their ability to grant loans that can be riskier. Bedendo and Bruno (Citation2012) have found an increasing overall risk of banks, which use intensively credit risk tools leading to higher default rate of institutions during the financial crisis. Moreover, the technique of securitization allows, generally, the selling of better assets quality and the retaining of poorer assets quality. Thus, the main portion of default risks remains within the balance-sheet of banks (Greenbaum & Thakor, Citation1987). Dionne and Harchaoui (Citation2003) have conducted an empirical study on Canadian commercial banks and indicated that the securitization has a positive effect on banks’ risk. Accordingly, Mayordomo et al. (Citation2014) suggested that the use of credit derivatives leads to the concentration of risks, mainly if the market participant is significantly large. Depending on the credit derivatives usage purposes, Trapp and Weib (Citation2016) have recently found that banks which use these financial products for non-hedging aims have a higher bank equity tail risk than others. Dewally and Shao (Citation2013) have also found similar results of derivatives usage on the financial stability of US large bank holding companies. Michalak and Uhde (Citation2012) used data on European bank holdings and argued that credit risk securitization increases the bank risk and has a negative impact on bank profitability. Furthermore, according to the analysis of Froot and Stein (Citation1998) and Froot et al. (Citation1993), active risk management influences risk-taking behavior of banks, leading them to retain less capital and grant risky and illiquid loans. This could have positive repercussions on the banks profitability since it reduces the capital cost used and negative impact on liquid assets in balance sheets.

3. Sample selection and data sources

The descriptive and empirical studies have been performed on samples of US commercial banks over the period extended from the second quarter of 2001 to the fourth quarter of 2017. Two sub-periods are considered, separated by the crisis date. The first one is from 2001: quarter 2 to 2007: quarter 2. The second begins from 2007: quarter 3 to 2017: quarter 4. We treat these two periods separately in order to filter the time duration of the bursting of the “subprime” systemic crisis event, and particularly, to distinguish the effects of credit risk transfer practices and their evolution before and after the crisis.

The data of thousands of US commercial banks have been extracted for each quarter of the considered period. Then, samples data were collected by following the quarterly evolution of each bank over the covered period, particularly, in terms of their status. Data of banks that have undergone a merger or acquisition have been removed in order to avoid any discrepancy in our estimations.

Small banks that have total assets lower than 1 billion USD in 2017-quarter 4 have been omitted as these banks didn’t significantly involve in credit risk transfer market. We consider two sub-set of banks based on their total assets amount: large and medium banks, to distinctly identify the effect of credit risk transfer tools.

Collected data are obtained mostly from the Consolidate Report of Condition and Income “call report” which provides quarterly detailed data on US commercial banks. These reports offer regular publications of the financial statements of the studied banks (balance sheets and income statements). Moreover, the “call report” contains key data on credit derivatives and securitization practices. Since the second quarter of 2001, data on securitization have been detailed according to the type of credit securitized, which justify the beginning of the considered studied period. Data on macroeconomic variables are retrieved from the World Development Indicator (WDI) granted by the World Bank.

4. Descriptive analyses

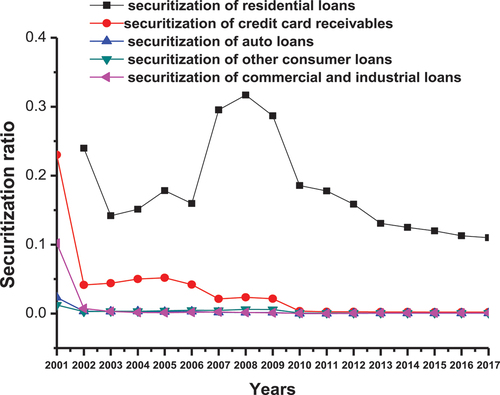

Figure illustrates the evolution of securitization share of each type of credit by total credit. It shows the intensity of securitization practices and the preponderance of mortgage loans securitization all over the investigated period. A peak was reached at the end of 2006 followed by a remarkable fall from 2008 and remains decreasing until the end of the considered period. illustrates clearly the effect of the crisis on the securitization practices of different types of credit, in particular, mortgages.

Figure 1. Securitization of different types of credits relative to the total credit.

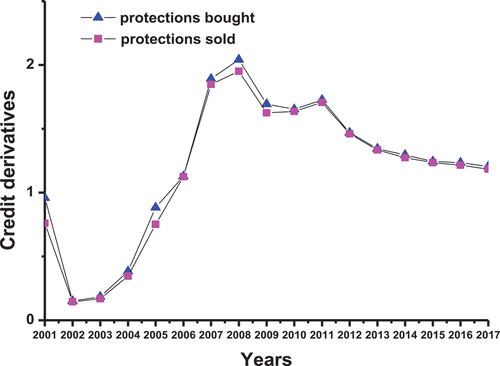

Regarding the credit derivatives, describes the progress of credit derivatives utilization over the time from 2001 to 2017 by US commercial banks. The illustration provides two curves characterizing, distinctly, the share of notional amount of these derivatives contracts purchased and sold in total credit, presented on balance-sheet. It reveals, between 2001 and 2007, an uptrend for both credit protection contracts purchased and sold. shows a drop in 2008 followed by a continuous decreasing until the end of the studied period, which may explain the impact of “subprime crisis” on credit derivatives use.

Figure 2. Evolution of credit derivatives bought and sold relative to the total credit.

5. Effect of credit risk transfer on bank risk, liquidity and profitability: empirical analysis

In this section, we intend to conduct an empirical analysis treating the impact of the credit risk transfer use on the bank stability through its impacts on bank risk, on bank liquidity and profitability. We highlight three accounting-based proxies of bank risk; the first is the share of non-performing loan in total assets (NPLa), the second indicator is the z-score which reflect the probability of insolvency bank and the third is the volatility of return on assets ГROA. The bank liquidity is evaluated by the ratio of liquid assets on balance sheet, and the profitability is assessed by the return on equity ROE.

To properly conduct this study, we first proceeded by a series of descriptive statistics (mean, median, standard deviation, etc.) for each model. Before achieving the estimation, the correlation and multi-collinearity (appendix A) tests have been carried out in order to avoid the collinearity problem.

5.1. Model specification and variables

5.1.1. Model specification

For estimations, we proceed by a panel regression having a general form of model described by the following equation:

Where yit represents the endogenous variable that depends on the proxy of bank risk, liquidity and profitability. α and β are parameters to be estimated. To alleviate a potential endogeneity problem that may arise, we used one period-lagged values of explanatory variables. ∑zit-1,n presents the lagged values of variables measuring the credit risk transfer activity, ∑xit-1,k includes lagged values of control variables which have been introduced into the model in order to highlight the individual characteristics of each bank. ∑cit-1,m is a set of lagged variables describing the macroeconomic situation. εit is an error term.

5.1.2. Credit risk transfer measures

To evaluate the credit risk transfer activity, two measurements have been used: the first concerns the securitization. The data have been extracted from the call report, corresponding to the outstanding principal balance of assets sold and securitized by the reporting bank with servicing retained or with recourse or other seller-provided credit enhancements (according to Jiangli & Pritsker, Citation2008). The call report provides the securitization of different types of loans including 1–4 family residential loans, home equity lines, credit card receivables, auto loans, other consumer loans, commercial and industrial loans, all other loans and all leases.

Second measurement is related to the credit derivatives. It is calculated in the same way as Hirtle (Citation2009) via the difference between the credit protection bought and the credit protection sold. The data are obtained as well from the call report.

5.1.3. Control variables

To investigate the impact of credit risk transfer on bank risk, liquidity and profitability, and in order to avoid omitted variable biases, a set of bank-specific and macroeconomic variables that can affect the explanatory variables have been introduced. We note that the choose of these variables will be specified subsequently according to the explained variable of the estimated model.

The selection of control variables is based on previous works (mainly Baselga-Pascual et al. (Citation2015), Michalak and Uhde (Citation2012), and Trapp and Weib (Citation2016)). We consider, firstly, the log of total assets measuring the size of banks (ass) which is a determinant factor of taking risk by banks and their involvement in credit risk transfer activities (Anginer et al., Citation2014; Farruggio & Uhde, Citation2015). Secondly, the capital ratio is introduced, which is the ratio of banks’ equity to total assets (equi). This factor can influence the decision makers’ behavior of risk (Kim & Santomero, Citation1988; Koehn & Santomero, Citation1980). Then, the loan ratio is calculated through the ratio of loans to total assets (loan). Given the specificity of the regression in Equationequation 5(5)

(5) , the mortgage loan ratio have been introduced independently of the rest of the loans ratio, noted (mortg) and (other loans), respectively. Furthermore, the business model of the bank (bus), which is the ratio of non-interest income to total interest income, is introduced. This variable can inform about the nature of the banks’ activities and their degree of involvement in risky activities. Similarly, the ratio of bank deposits to total assets (dep) is employed to capture the composition of liabilities in bank balance sheets. Indeed, more deposit financing indicates a better performance (Aebi et al., Citation2012). Then, the ratio of liquid assets to total assets (liq) is included. Finally, we involve the return on equity ratio (roe), which is the ratio of the net income to total equity of the bank, and the income growth rate (rev).

In addition to bank-specific variables, the examination of the relationship between credit risk transfer and banking risk, liquidity and profitability requires the introduction of macroeconomic variables that may affect these indicators or the credit risk transfer measures or both. Among of these variables, the growth rate (GDP) has been used. An admissible rate growth is generally associated to a stable macroeconomic condition, to a low banking risk and to a better performance (Borio & Lowe, Citation2002; Festic et al., Citation2011). Then, the inflation rate (inf) has been included. The impact of this variable is ambiguous; it depends on whether the inflation is anticipated by banks or not (Perry, Citation1992; Revell, Citation1979; Uhde & Heimeshoff, Citation2009). Baselga-Pascual et al. (Citation2015) and Baboucek and Jancar (Citation2005) suppose that inflation increases the banking risk. Finally, the interest rate (inte) has been added. Literatures review assume that this factor affects considerably the banking stability and performance, particularly those of Agur and Demertzis (Citation2012), Baselga-Pascual et al. (Citation2015), and Delis and Kouretas (Citation2011) who suggested that a decrease of interest rate increases the bank risk and deteriorates the bank performance, which is the case of the last financial crisis.

5.2. Descriptive statistics

reports main descriptive statistics of the credit risk transfer measures and the endogenous variables of the models. It shows that the proxy of bank risk NPLa displays an increase during the second period for both large and medium banks (respectively, from an average of 0.0060 to 0.0158 and from 0.0043 to 0.0152). At this time, several borrowers are insolvent and, therefore, the share of non-performing loan grows.

Table 1. Basic descriptive statistics of credit risk transfer measures and dependent variables of regressions

This table summarizes the descriptive statistics of credit risk transfer proxies and the dependent variables used in the regressions. The dependent variables are the determinants of banking risk (npla, Z-score and ГROA), of the liquid assets ratio and the ROE. The credit risk transfer measures are the securitization ratio and the ratio of net credit derivatives. Large banks have total asset superior than 20 billion USD and the total asset of medium banks is between 1 and 20 billion USD. Statistics are arranged for two periods: 2001–2007 includes the period 2001:q2 to 2007:q2 and 2007–2017 incorporates 2007: q3 until 2017:q4.

The second indicator of bank risk (z-score) denotes an increase from 30.5828 to 50.4259 for large banks and from 33.0363 to 45.8515 for medium banks as shown in 1. Measuring the distance to insolvency, the evolution of the z-score value appears obvious. This value is higher during the second period indicating the restoration of a relative stability of the two bank categories during the second period. The third measure of risk (ГROA) marks the value of 0.0037 as mean of large banks during the first period and 0.003 for the second, recording a slight decrease and indicating that bank profitability is, relatively, less volatile through the second period. The mean of this variable is almost constant for medium-size banks for the two periods, at around 0.003.

The ratio of liquid assets shows, for large banks, a mean growing from 0.1675 during the first period to 0.2085 in the second and passing from 0.232 to 0.202 for medium-sized banks, respectively, during the first and the second period. We note that the liquid assets ratio is lower for large banks, particularly, in the pre-crisis period. These banks hold, generally, fewer liquid assets than smaller banks.

The mean of ROE records a decrease both for large banks, declining from 0.1002 during the pre-crisis period to 0.0515 in the post-crisis period, and for medium-sized banks diminishing from 0.0853 throughout the first period to 0.0481 during the second one. The decrease in this ratio, in mean, to the half value reflects the difficulties incurred by the US banking sector, caused by the crisis.

Concerning the proxies of credit risk transfer, the securitization ratio displays a mean of 0.1095 in the first period and of 0.104 in the second period for large banks as indicated in . For medium banks, the same variable shows a mean of 0.0034 in first period and of 0.0012 in the second. According to these statistics, it can be denoted that large banks use risk transfer tools more than their smaller counterparts and the two categories of banks employ moderately less intensively these tools during the second period. Regarding the second proxy of credit risk transfer activity (the net credit derivatives ratio), shows that the mean is positive for large banks both in the first (0.0045) and second period (0.0047). However, the average of this proxy has a negative sign for medium banks over the two sample-periods, −6 x 10,−5 and −3.13 x 10−6, respectively, revealing that large banks purchase more protections against credit risk whereas those of smaller size sell more. This behavior can be explained by the fact that the loan portfolio of large banks had relatively high level of risk and they intend to protect themselves against this risk. Whereas, medium banks opt for the sale of protections in order to enhance their profits.

5.3. Impact of credit risk transfer on bank risk

5.3.1. Model 1: the non-performing loans (NPLa) model

The ratio of non-performing loan has been used as a measure of banking risk. A high value of this ratio can lead to the bankruptcy (Mayordomo et al., Citation2014; Poghosyan & Cihak, Citation2011). In order to identify the effect of credit risk transfer on the bank risk, NPLa is regressed on a set of variables. The regression is described in the following equation:

Where NPLait exhibits the dependent variable. zit-1,n denotes lagged values of explanatory variables measuring the credit risk transfer activity; credit securitization ratio (sec) and net credit derivatives ratio (derv). The vector xit-1,k includes lagged values of bank characteristic variables which are: the log of total assets (ass), the capital ratio (equi), the loan ratio (loan), the business model of the bank (bus), the ratio of bank deposits (dep), the ratio of liquid assets (liq), the return on equity ratio (roe) and the income growth rate (rev). cit-1,m indicates the set of lagged macroeconomic variables, which are the GDP growth rate (gdp), the inflation rate (inf) and the interest rate (inte). α and β are parameters to be estimated and εit is an error term.

5.3.2. Model 2: the z-score model

The second model has z-score as a dependent variable. This indicator is widely used in several empirical researches examining banking stability (Köhler, Citation2015; Laeven & Levine, Citation2009; Michalak & Uhde, Citation2012; Uhde & Heimeshoff, Citation2009). The z-score, defined as the ROA plus capital ratio divided by the standard deviation of ROA, describes the distance to institution default. A higher value of this metric indicates a more stable bank. Following (Bedendo & Bruno, Citation2012), the z-score have been calculated across four quarter. Thus, this model will be estimated on annual data to avoid biased estimations. The model is presented as follows:

Where z-score designates the dependent variable assessing the banking risk. Zit-1,n regroups lagged values of variables measuring the credit risk transfer. To improve the precision on the effect of this mechanism, we have introduced in addition to the net credit derivative ratio (derv), the securitization of residential mortgage loan ratio (secmo), separately of other credit securitization ratio (sect). This parameter is included since the securitization of this credit type is considered as one of the major causes of Subprime crisis. The vector xit-1,k includes lagged values of bank-specific control variables: log of total assets (ass), the loan ratio (loan), the business model of the bank (bus), the ratio of bank deposits (dep), the ratio of liquid assets (liq) and the income growth rate (rev). cit-1,m is a vector of lagged macroeconomic variables including the GDP growth rate (gdp), the inflation rate (inf) and the interest rate (inte). αi, βn, βk and βm are parameters to be estimated and εit is an error term.

5.3.3. Model 3: the model of ГROA

To highlight our previous studies treating the effect of credit risk transfer on banking stability, a third modelling approach, using the ГROA as banks’ risk measure, is proposed. Defined as the volatility of the return on assets (the pre-tax revenue divided by total assets), this variable is considered as an appropriate indicator informing about the bank’s loan portfolio and hence about the banks risk exposures (Michalak & Uhde, Citation2012). As in the previous model, ГROA is calculated during four quarters of data and the estimation will be realized on annual data. The following equation describes the third model:

The first term of EquationEq. (4)(4)

(4) is the standard deviation of ROA ratio. Zit-1,n is a set of lagged values of credit risk transfer proxies, including the securitization of residential mortgage loan ratio (secmo) introduced separately of the securitization of other loan (sect) and the net credit derivative ratio (derv). The vector xit-1,k incorporates lagged values of variables related to banks characteristics which are mainly the log of total assets (ass), the equity ratio (equi), the loan ratio (loan), the business model of the bank (bus), the ratio of bank deposits (dep) and the ratio of liquid assets (liq). Cit-1,m contains lagged rates of macroeconomic variables including the GDP growth rate (gdp), the inflation rate (inf) and the interest rate (inte). αi, βn, βk and βm are parameters to be estimated and εit is an error term. Table reports the results of empirical estimations of the three models presented in EquationEq. (2

(2)

(2) ), EquationEq. (3)

(3)

(3) and EquationEq. (4)

(4)

(4) for both large and medium banks. Results concern the pre-crisis period as well as the period succeeding the triggering of the financial turmoil.

Table 2. Effect of credit risk transfer activities on banking risk

The table reports the estimation results of the credit risk transfer effect on banking stability assessed by the npla, z-score and ГROA. The credit risk transfer is measured by Sec: securitization ratio and derv: ratio of net credit derivatives. The secmo: securitization of residential mortgage ratio (1–4 mortgages) is introduced to the second and third model as an additional proxy of credit risk transfer activity and sect: securitization of other loans ratio. Ass: log of total assets, equi: capital ratio, loan: loan ratio, bus: the business model of the bank, dep: the ratio of bank deposits, liq: the ratio of liquid assets, roe: the return on equity ratio, rev: the income growth rate, gdp: the growth rate, inte: the interest rate, inf: the inflation rate.

Large banks have total asset superior than 20 billion USD and the total asset of medium bank is between 1 and 20 billion USD. Statistics are arranged for two subperiods: period 1 includes the period 2001:q2 to 2007:q2 and period 2 incorporates 2007: q3 until 2017:q4.

* Statistical significance at the 10% level.

** Statistical significance at the 5% level.

*** Statistical significance at the 1% level.

As shown in Table , the global effect of credit risk transfer on banking stability is negative especially in the pre-crisis period. Our finding completes previous recent research studies supporting the positive relationship between the bank risk and the credit risk transfer (Trapp & Weib, Citation2016; Iglesias-Casal et al., Citation2016; Uhde and Michalak, Citation2010 and Hänsel and Krahnen, Citation2007).

Addressing to the first model with npla as dependent variable, we notice (in Table ) that securitization is positive and significant at 1% for large banks and at 5% for medium banks, reflecting the impact of using the credit risk transfer mechanism on the deterioration of the loan portfolio, especially, before the financial crisis event. This indicates that banks, which employ securitization, grant poor quality loans. The credit risk transfer reduces monitoring incentives of banks leading to the deterioration of loan portfolio quality (Cardone-Riportella et al., Citation2010; Keys et al., Citation2010; Morrison, Citation2005). The measurement of credit derivatives use did not show a significant effect. Table reports also estimation results of model 2 having z-score as dependent variable. As shown in this table, the securitization of residential mortgage ratio has been introduced in order to improve the results since this type of loan is among the main causes of the financial crisis. We notice that this variable enters the regression significantly negative in the first period for both large and medium banks. This result is expected and is observed also for the securitization of other loans ratio for large banks, indicating that banks that are more engaged on credit risk transfer activities are closer to the default. Thus, the credit risk transfer has a negative effect on banking stability measured by the z-score technique. Our finding agrees with previous studies using this technique and support the negative relationship between this mechanism use and banking stability (Bedendo & Bruno, Citation2012; Michalak & Uhde, Citation2012). The net credit derivative ratio reveals a significant and negative impact on medium-banks stability. In fact, these banks generally use credit derivatives as protection sellers which tend to increase their risk level, affecting negatively their stability. This negative impact of the net credit derivative ratio disappears after the crisis. However, we state that the securitization ratio of residential mortgages loans (1–4 mortgages) is significantly positive during the second period, indicating a positive effect on banking stability, especially for large banks. Our finding match with the results obtained recently by Le et al. (Citation2016) where they did not underline an increases of banking risk after the crisis due to securitization. This could be explained by the fact that, in the post-crisis period, the securitization, particularly, of mortgages is a subject of supervision by the competent authorities within a relatively stricter regulatory framework (Basel III). This period has been characterized by an establishment of several reforms aiming the consolidation of the financial system. Moreover, the securitization was recommended during this period for reasons of liquidity production within the context of liquidity scarcity. Providing liquidity contributes, in fact, to the banking soundness as indicated by Jiangli and Pritsker (Citation2008). Further investigation of Table dealing with the model 3, reveals that the securitization does not show a significant effect during the first period for large banks. This result of the non-significant impact on ΓROA could be due to the relative stability of other assets return, especially the non-interest banks income. During the second period, the effect of the mortgage securitization ratio becomes significant and negative suggesting a stable effect. This positive effect on bank stability during the second period indicates that the securitization of this type of credit can attenuate the assets return volatility within the context of the liquidity scarcity and a contraction of non-interest banks income. This effect can be attributed to the appropriate management that has been recommended by international authorities and new regulations.

The effect of the securitization of other credit on the ΓROA of medium banks is significant and positive prior to the crisis in accordance with the results provided by Bedendo and Bruno (Citation2012), indicating that this category of bank is more sensitive to the securitization activity in the first period. The non-significant effect after the crisis can be explained by a reluctance of these banks to use this tool through this period compared to larger homologous. The mortgage securitization ratio (1–4 mortgages), being the most important type of loan securitization, displays a negative significance at 10% level during the second period, asserting a stable effect of the securitization of this loan type on banking stability that has been concluded for large banks.

The net credit derivatives reveal a significant and negative effect on the ΓROA of medium banks during the first period. This result is expected since these banks are generally protection sellers. The sale of protection can contribute to enhance their profitability and stability in short term. However, the crisis event has limited this impact during the second period as concluded by the results exposed in .

5.4. Impact of credit risk transfer on bank liquidity and profitability

In the previous section, the credit risk transfer mechanism is found to affect considerably the banking risk, which can determine the continuity of this mechanism use. The following section illustrates how this mechanism could affect banking liquidity and performance.

5.4.1. Impact of credit risk transfer on bank liquidity

The model treating the impact of credit risk transfer on bank liquidity is presented as follow:

Where liq presents the dependent variable measuring the bank liquidity. It is defined by the liquid assets’ ratio.Footnote1 Zit-1,n involves lagged values of the credit risk transfer proxies; the credit securitization ratio and the net credit derivatives ratio. The vector xit-1,k includes lagged values of bank-specific control variables; log of total assets (ass), the equity ratio (equi), the loan ratio (loan), the business model of the bank (bus), the ratio of bank deposits (dep), the non-performing loan ratio (npla) and the income growth rate (rev). cit,m is a vector of lagged rates of macroeconomic variables including the GDP growth rate (gdp), the inflation rate (inf) and the interest rate (inte). αi, βn, βk and βm are parameters to be estimated and εit is an error term.

The estimation results are reported in . The first column of the table shows a significant and negative effect at 1% and 5% of the securitization ratio, respectively, on large and medium banks liquidity. In accordance with Loutskina (Citation2011), this result suggests that the increasing access of banks to securitization could decrease their liquid assets on balance sheets. Securitization can play a substitute role for liquid funds. It allows banks to easily convert loans on liquid financial instruments when it is necessary, disheartening them to hold enough liquid assets in their balance-sheets. However, the negative effect of securitization on liquidity is alleviated for medium banks after the crisis. This can be explained by the reluctance of these banks to the securitization use due to the uncertainty inherent to the securitization market in this period. In addition, the access to securitization market is costly and could take much more time comparatively to large banks. Thus, the difficult access to the securitization market might restrain medium banks to raise the liquid securities on their balance sheets, especially in frail economic conditions.

Table 3. Effect of credit risk transfer activities on bank liquidity and profitability

Regarding the net credit derivative ratio, the impact on liquidity is weakened compared to the securitization. The results suggest a negative impact on the liquid assets of medium-size banks before the crisis and of large banks after the crisis event. In fact, large banks still active in credit risk transfer market even in recession when liquidity is scarce.

Liquidity is among of the important determinants of credit risk transfer mechanism use (Bedendo & Bruno, Citation2012). After the crisis event, the credit risk transfer practices are recommended in some segment of derivatives and securitization market to satisfy the liquidity needs of banks. This may increase their credit supply ability, aiming the revival of the economy (Bedendo & Bruno, Citation2012; Brunnermeier, Citation2009).

The table reports the estimation results of the credit risk transfer effect on bank liquidity and profitability. The credit risk transfer is measured by Sec: securitization ratio and derv: ratio of net credit derivatives. The secmo: securitization of residential mortgage ratio (1–4 mortgages) is introduced to the second model as an additional proxy of credit risk transfer activity and sect: securitization of other loans ratio. Ass: log of total assets, equi: capital ratio, loan: loan ratio, mortg: mortgage loan ratio, other loans: other loans ratio, bus: the business model of the bank, dep: the ratio of bank deposits, liq: the ratio of liquid assets, roe: the return on equity ratio, rev: the income growth rate, gdp: the growth rate, inte: the interest rate, inf: the inflation rate.

Large banks have total asset superior than 20 billion USD and the total asset of medium bank is between 1 and 20 billion USD. Statistics are arranged for two subperiods: period 1 includes 2001:q2 to 2007:q2 and period 2 incorporates 2007: q3 until 2017:q4.

* Statistical significance at the 10% level.

** Statistical significance at the 5% level.

*** Statistical significance at the 1% level.

5.4.2. Impact of credit risk transfer on bank profitability

The following estimating model has been proposed to evaluate the bank profitability via the return on equity (ROE):

ROE is the banks’ return on equity. zit-1,n is the set of the lagged values of credit risk transfer measures which are for this regression; the residential mortgage securitization ratio (1–4 mortgages), the other credit securitization ratio and the net credit derivatives ratio. Bank characteristics xit-1 regroups the lagged values of banks control variables that the literatures have found determinant to affect the bank profitability such as log of total assets (ass), mortgage loan ratio (mortg), other loan ratio (other loans), deposit ratio (dep), the non-performing loan ratio (npla), and the liquid asset ratio (liq). cit-1 represents lagged rates of the macroeconomic variables; the GDP growth rate, the inflation rate (inf) and the interest rate (inte). εit is an error term.

The results of investigation of the credit risk transfer impact on bank profitability are resumed in the last column of Table . They suggest that the securitization affects positively and significantly the ROE of medium and large banks before the crisis event. In harmony with results showed by Jiangli et al. (Citation2007) and Cebenoyan and Strahan (Citation2004), we deduce that securitization allows banks to increase their profit. After the crisis, the other credit securitization ratio has not shown a significative impact that could due to the contraction of their use in this period. However, it is remarkable that the securitization of residential mortgage loan ratio affects negatively the ROE of medium and large banks in the post-crisis period, indicating that the securitization of this credit type can deteriorate the bank profit. Before the crisis, the securitization products, particularly of mortgage loans, are complex and credit risk transfer market was opaque and unregulated. In this period, banks use intensively the securitization to promote liquidity, loans supply and consequently their profitability. After the crisis event, the regulatory authorities have established a new regulatory framework (Bale 3) aiming to preserve further capital to recover the liquidity and insolvency risk. This increase the capital cost of banks activity and decrease their profitability (Structured Finance Association (SFA), Citation2020). In addition, the effects of the credit derivatives are found to be non-conclusive. The net credit derivative ratio does not show a significant effect on the profit of the two categories of banks.

While the effect of credit risk transfer on bank risk and performance has been analyzed through several models and the robustness of the results was checked through various indicators, the present work merits to be extended to other multivariate models such as explored by Ahelegbey et al. (Citation2017) and Avdijev et al. (Citation2020). Furthermore, the robustness of the obtained results could be examined using methods that take into consideration the dependence of variables, such as the copula distributions investigated by Fantazzini et al. (Citation2008) to measure the operational risk.

6. Conclusion

Being at the heart of the recent financial crisis, the credit risk transfer tools attract particular attention. The occurrence of this international turmoil has exposed many menaces and failures related to the employment of these instruments. The astonishing growth of the credit risk transfer market has changed the main aim of using this mechanism from the alleviation of the credit risk, to a purely commercial purpose targeting the increase of the bank return at the expense of higher level of risk. These changes have contributed to the fragility of the financial system.

In this research work, the effectiveness of the continuity of the credit risk transfer instruments has been investigated by carrying out the impact of these instruments use on the bank risk, liquidity and profitability in pre- and post-crisis period. Using three models (NPLa, z-score and ГROA model) handling this impact on bank risk, our results suggested, generally, an amplification of the risk incurred by banks. Assuming to easily discard these loans through securitization and credit derivatives, banks have attenuated the lending requirements. Although, the study of the residential mortgage loan securitization effect, introduced independently to the other securitization loans, shows that it can promotes banking stability in the post-crisis period.

The results on liquidity and profitability suggest that the securitization reduces the banks’ holding of liquid assets on balance sheet since it can be considered as a substitute of liquid funds and rises, generally, the profitability. The securitization of the mortgage loans could limit the profitability after the crisis event in the context of new regulatory restrictions recommended in the Basel III framework.

The investigations on the credit derivatives show that their effects are, globally, non-conclusive. A limited impact has been raised on the risk, liquidity and profitability of the bank.

The empirical finding has revealed that regulatory measures taken on the eve of the crisis by international financial authorities, especially the Basel Committee, concerning the credit risk transfer activities can be considered as a right orientation to the stability and the welfare perspectives of the bank. The application of Basel III guidelines, particularly recommended by Pillar 1, may reduce the risk exposures of banks and enhance their capacity to manage the credit risk of securitization exposures. These recommendations and those planned in Basel IV aim to help banks to overcome the difficulties caused by the crisis, allowing the bank to benefit from the advantages of these practices and avoid the misuse of these instruments.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Acknowledgement

The author is grateful to Professor Khalil Hajlaoui for his technical assistance and scientific guidance that significantly improved the paper quality

Additional information

Funding

Notes

1. Following Kashyap and Stein (Citation2000), the liquidity ratio is calculated as follow: (securities available for sale + fed funds sold and securities purchased under agreement to resell+ securities held to maturity)/ total assets. We have not considered the cash in treasury (because the majority of this component is retained as reserve requirements).

References

- Aebi, V., Sabato, G., & Schmid, M. (2012). Risk management, corporate governance, and bank performance in the financial crisis. Journal of Banking & Finance, 36(12), 3213–21. https://doi.org/10.1016/j.jbankfin.2011.10.020

- Agostino, M., & Mazzuca, M. (2011). Empirical investigation of securitization drivers: The case of Italian banks. The European Journal of Finance, 17(8), 623–648. https://doi.org/10.1080/1351847X.2010.505727

- Agur, I., & Demertzis, M., (2012). Excessive bank risk taking and monetary policy. ECB Working Paper No. 1457. https://ssrn.com/abstract=2128478.

- Ahelegbey, D. F., Billio, M., & Casarin, R. (2017). Bayesian graphical models for structural vector autoregressive processes. Journal of Applied Econometrics, 31(2), 357–386. https://doi.org/10.1002/jae.2443

- Allen, F., & Gale, D. M. (2005). Systemic risk and regulation. In M. Carey & R. M. Stulz (Eds.), The risks of financial institutions (pp. 341–368). University of Chicago Press.

- Altunbas, Y., Gambacorta, L., & Marques-Ibanez, D. (2009). Securitization and the bank lending channel. European Economic Review, 53(8), 996–1009. https://doi.org/10.1016/j.euroecorev.2009.03.004

- Ambrose, B. W., Lacour-Little, M., & Sanders, A. B. (2005). Does regulatory capital arbitrage, reputation, or asymmetric information drive securitization? Journal of Financial Services Research, 28(1–3), 113–133. https://doi.org/10.1007/s10693-005-4358-2

- Anginer, D., Demirguc-Kunt, A., & Zhu, M. (2014). How does bank competition affect systemic stability? Journal of Financial Intermediation, 23(1), 1–26. https://doi.org/10.1016/j.jfi.2013.11.001

- Avdijev, S., Giudici, P., & Spelta, A. (2020). Measuring contagion risk in international banking. Journal of Financial Stability, 42(C), 36–51. https://doi.org/10.1016/j.jfs.2019.05.014

- Baboucek, I., & Jancar, M., (2005). A VAR analysis of the effects to macroeconomic shocks to the quality of the aggregate loan portfolio of the Czech-banking sector. Working Paper 1, Czech National Bank.

- Basel Committee on Banking Supervision (BCBS). (2004, October). Credit risk transfer.

- Baselga-Pascual, L., Trujillo-Ponce, A., & Cardone-Riportella, C. (2015). Factors influencing bank risk in Europe: Evidence from the financial crisis. North American Journal of Economics and Finance, 34 c , 138–166. https://doi.org/10.1016/j.najef.2015.08.004

- Bedendo, M., & Bruno, B. (2012). Credit risk transfer in U.S. commercial banks: What changed during the 2007–2009 crisis? Journal of Banking and Finance, 36(12), 3260–3273. https://doi.org/10.1016/j.jbankfin.2012.07.011

- Borio, C., & Lowe, P., (2002). Asset prices, financial and monetary stability: Exploring the nexus. Working Paper 114, Bank for International Settlements.

- Brunnermeier, M. K. (2009). Deciphering the liquidity and credit crunch 2007–2008. Journal of Economic Perspective, 23(1), 77–100. https://doi.org/10.1257/jep.23.1.77

- Cardone-Riportella, C., Samaniego-Medina, R., & Trujillo-Ponce, A. (2010). What drives bank securitization? The Spanish experience. Journal of Banking and Finance, 34(11), 2639–2651. https://doi.org/10.1016/j.jbankfin.2010.05.003

- Caruso, G., Gattone, S. A., Fortuna, F., & Di Battista, T. (2021). Cluster analysis for mixed data: An application to credit risk evaluation. Socio-Economic Planning Sciences. Elsevier, 73(C 100850). https://doi.org/10.1016/j.seps.2020.100850

- Casu, B., Clare, A., Sarkisyan, A., & Thomas, S. (2013). Securitization and bank performance. Journal of Money, Credit, and Banking, 45(8), 1617–1658. https://doi.org/10.1111/jmcb.12064

- Cebenoyan, S., & Strahan, P. E. (2004). Risk management, capital structure and lending at banks. Journal of Banking and Finance, 28(1), 19–43. https://doi.org/10.1016/S0378-42660200391-6

- Chiesa, G. (2008). Optimal credit risk transfer, monitored finance, and banks. Journal of Financial Intermediation, 17(4), 464–477. https://doi.org/10.1016/j.jfi.2008.07.003

- Deku, Y. S., Kara, A., & Zhou, Y. (2019). Securitization, bank behavior and financial stability: A systematic review of the recent empirical literature. International Review of Financial Analysis 61 (c) , 245–254 doi:10.1016/j.irfa.2018.11.013.

- Delis, M. D., & Kouretas, G. P. (2011). Interest rates and bank risk-taking. Journal of Banking and Finance, 35(4), 840–855. https://doi.org/10.1016/j.jbankfin.2010.09.032

- Dewally, M., & Shao, Y. (2013). Financial derivatives, opacity, and crash risk: Evidence from large US banks. Journal of Financial Stability, 9(4), 565–577. https://doi.org/10.1016/j.jfs.2012.11.001

- Dionne, G., & Harchaoui, T. M., (2003). Banks capital, securitization and credit risk: An empirical evidence for Canada. Working Paper No. 03-01.HEC, Montreal.

- Duffie, D., (2008). Innovations in credit risk transfer: Implications for financial stability. Working Papers No. 255. Bank for International Settlements, Basel.

- European Central Bank.,(2014). The case for a better functioning securitization market in the European Union. A discussion paper. Frankfurt am Main: ECB.

- Fantazzini, D., Dalla Valle, L., & Giudici, P. (2008). Copulae and operational risks. International Journal of Risk Assessment and Management, 9(3), 238–250. https://doi.org/10.1504/IJRAM.2008.019743

- Farruggio, C., & Uhde, A. (2015). Determinants of loan securitization in European banking. Journal of Banking & Finance, 56 (c) , 12–27. https://doi.org/10.1016/j.jbankfin.2015.01.015

- Festic, M., Kavkler, A., & Repina, S. (2011). The macroeconomic sources of systemic risk in the banking sectors of five new EUmember states. Journal of Banking and Finance, 35(2), 310–322. https://doi.org/10.1016/j.jbankfin.2010.08.007

- Franke, G., & Krahnen, J. P. (2006). Default risk sharing between banks and markets: The contribution of collateralized debt obligations. In M. Carey & R. M. Stulz (Eds.), The risks of financial institutions (pp. 603–634). University of Chicago Press.

- Froot, K. A., Scharfstein, D. S., & Stein, J. C. (1993). Risk management: Coordinating corporate investment and financing policies. The Journal of Finance, 48(5), 1629–1658. https://doi.org/10.1111/j.1540-6261.1993.tb05123.x

- Froot, K., & Stein, J. (1998). Risk management, capital budgeting, and capital structure policy for financial institutions: An integrated approach. Journal of Financial Economics, 47(1), 55–82. https://doi.org/10.1016/S0304-405X9700037-8

- Gao, C., & Mcconnell, J. J. (2018). Investment performance of credit risk transfer securities (CRTs): The early evidence. The Journal of Fixed Income, 28(2), 6–15 https://doi.org/10.3905/jfi.2018.28.2.006.

- Greenbaum, S. I., & Thakor, A. V. (1987). Bank funding modes: Securitization versus deposits. Journal of Banking and Finance, 11(3), 379–401. https://doi.org/10.1016/0378-42668790040-9

- Hansel, D. N., & Krahnen, J. P., (2007). Does credit securitization reduce bank risk? Evidence from the European CDO market. Mimeo (Working Paper), Goethe-University Frankfurt.

- Hansel, D. N., & Bannier, C. E., (2008) Determinants of European banks’ engagement in loan securitization. Series 2, discussion paper no. 2008.

- Hirtle, B. (2009). Credit derivatives and bank credit supply. Journal of Financial Intermediation, 18(2), 125–150. https://doi.org/10.1016/j.jfi.2008.08.001

- Iglesias-Casal, A., Lopez-Penabad, M. C., Lopez-Andion, C., & Maside-Sanfiz, J. M. (2016). Market perception of bank risk and securitization in Spain. Journal of Business Economics and Management, 17(1), 92–108. https://doi.org/10.3846/16111699.2013.807867

- Instefjord, N. (2005). Risk and hedging: Do credit derivatives increase bank risk? Journal of Banking & Finance, 29(2), 333–345. https://doi.org/10.1016/j.jbankfin.2004.05.008

- International Association of Insurance Supervisors (IAIS). (2003). Credit risk transfer between insurance, banking and other financial sectors.

- Jiangli, W., Pritsker, M., & Raupach, P., (2007). Banking and securitization. Working Paper. FDIC, Federal Reserve Board and Deutsche Bundesbank.

- Jiangli, W., & Pritsker, M., (2008). The impacts of securitization on U.S. bank holding companies. Working Paper, Federal Reserve Bank of Chicago Proceedings; 377–393.

- Kamstra, M. J., Roberts, G. S., & Shao, P. (2014). Does the secondary loan market reduce borrowing costs? Review of Finance, 18(3), 1139–1181. https://doi.org/10.1093/rof/rft011

- Kara, A., Marques-Ibanez, D., & Ongena, S., (2011). Securitization and lending standards: Evidence from the wholesale loan market. Working Paper, Tilburg University. series no 1362.

- Kara, A., Marques-Ibanez, D., & Ongena, S. (2019). Securitization and credit quality in the European Market. European Financial Management, 25(2), 407–434. https://doi.org/10.1111/eufm

- Karaoglu, E., (2005). Regulatory capital and earnings management in banks: The case of loan sales and securitizations. FDIC Center for Financial Research Working Paper No. 2005-05.

- Kashyap, A. K., & Stein, J. C. (2000). What do a million observations on banks say about the transmission of monetary policy? American Economic Review, 90(3), 407–428. doi:10.1257/aer.90.3.407.

- Keys, B. J., Mukherjee, T., Seru, A., & Vig, V. (2010). Did securitization lead to lax screening? Evidence from subprime loans. Quarterly Journal of Economics, 125(1), 307–362. https://doi.org/10.1162/qjec.2010.125.1.307

- Keys, B. J., Seru, A., & Vig, V. (2012). Lender screening and the role of securitization: Evidence from prime and subprime mortgage markets. Review of Financial Studies, 25(7), 2071–2108. https://doi.org/10.1093/rfs/hhs059

- Kim, D., & Santomero, A. M. (1988). Risk in banking and capital regulation”. Journal of Finance, 43(5), 1219–1233. https://doi.org/10.1111/j.1540-6261.1988.tb03966.x

- Koehn, M., & Santomero, A. M. (1980). Regulation of bank capital and portfolio risk. Journal of Finance, 35(5), 1235–1244. https://doi.org/10.1111/j.1540-6261.1980.tb02206.x

- Köhler, M. (2015). Which banks are more risky? The impact of business model on bank stability. Journal of Financial Stability, 16 (c) , 195–212 https://doi.org/10.1016/j.jfs.2014.02.005.

- Krahnen, J. P., & Wilde, C.,(2006). Risk transfer with CDOs and systemic risk in banking. CFS Working Paper No. 2006/04. http://dx.doi.org/10.2139/ssrn.889541.

- Laeven, L., & Levine, R. (2009). Bank governance, regulation and risk taking. Journal of Financial Economics, 93(2), 259–275. https://doi.org/10.1016/j.jfineco.2008.09.003

- Le, T. H. T., Narayanan, R. P., & Vo, L. V. (2016). Has the effect of asset securitization on bank risk taking behavior changed? Journal of Financial Services Research, 49(1), 39–64. https://doi.org/10.1007/s10693-015-0214-1

- Loutskina, E. (2011). The role of securitization in bank liquidity and funding management. Journal of Financial Economics, 100(3), 663–684. https://doi.org/10.1016/j.jfineco.2011.02.005

- Mayordomo, S., Rodriguez-Moreno, M., & Peña, J. I. (2014). Derivatives holdings and systemic risk in the U.S. banking sector. Journal of Banking and Finance, 45, 84–104 https://doi.org/10.1016/j.jbankfin.2014.03.037.

- Michalak, T. C., & Uhde, A. (2012). Credit risk securitization and bank soundness in Europe. The Quarterly Review of Economics and Finance, 52(3), 272–285. https://doi.org/10.1016/j.qref.2012.04.008

- Minton, B. A., Sanders, A., & Strahan, P., (2004). Securitization by banks and finance companies: Efficient financial contracting or regulatory arbitrage? Working Paper, Ohio State University.

- Morrison, A. D. (2005). Credit derivatives, disintermediation and investment decisions. Journal of Business, 78(2), 621–647. https://doi.org/10.1086/427641

- Nijskens, R., & Wagner, W. (2011). Credit risk transfer activities and systemic risk: How banks became less risky individually but posed greater risks to the financial system at the same time. Journal of Banking and Finance, 35(6), 1391–1398. https://doi.org/10.1016/j.jbankfin.2010.10.001

- Perry, P. (1992). Do banks gain or lose from inflation? Journal of Retail Banking, 14 (2) , 25–30.

- Pinto, J. M., (2014) The economics of securitization: Evidence from the European markets. Working Papers: Economics. N. 2, p 30.

- Poghosyan, T., & Cihak, M. (2011). Determinants of bank distress in Europe: Evidence from a new data set. Journal of Financial Services Research, 40(3), 163–184. https://doi.org/10.1007/s10693-011-0103-1

- Revell, J. (1979). Inflation and financial institutions. Financial Times.

- Solano, P. M., Yagüe-Guirao, J., & López-Martínez, F. (2009). Asset securitization: Effects on value of banking institutions. The European Journal of Finance, 15(2), 119–136. https://doi.org/10.1080/13518470802466188

- Structured Finance Association (SFA)., (2020). Credit risk transfers (CRT) transactions white paper. Overview of Current Structures and Regulatory Issues in CRT.

- Trapp, R., & Weib, G. N. F. (2016). Derivatives usage, securitization, and the crash sensitivity of bank stocks. Journal of Banking and Finance, 71 (c) , 183–205. https://doi.org/10.1016/j.jbankfin.2016.07.001

- Uhde, A., & Heimeshoff, U. (2009). Consolidation in banking and financial stability in Europe: Empirical evidence. Journal of Banking and Finance, 33(7), 1299–1311. https://doi.org/10.1016/j.jbankfin.2009.01.006

- Uhde, A., & Michalak, T. C. (2010). Securitization and systematic risk in European banking: Empirical evidence. Journal of Banking and Finance, 34, 3061–3077. https://doi.org/10.1016/j.jbankfin.2010.07.012

- Uzun, H., & Webb, E. (2007). Securitization and risk: Empirical evidence on US banks. The Journal of Risk Finance, 8(1), 11–23. https://doi.org/10.1108/15265940710721046

- Venkatachalam, M. (1996). Value-relevance of banks’ derivatives disclosures. Journal of Accounting and Economics, 22(1–3), 327–355. https://doi.org/10.1016/S0165-41019600433-8

- Wagner, W., & Marsh, I. (2006). Credit risk transfer and financial sector stability. Journal of Financial Stability, 2(2), 173–193. https://doi.org/10.1016/j.jfs.2005.11.001

- Wagner, W. (2007). The liquidity of bank assets and banking stability. Journal of Banking and Finance, 31(1), 121–139. https://doi.org/10.1016/j.jbankfin.2005.07.019

- Wang, Y., & Xia, H. (2014). Do lenders still monitor when they can securitize loans? Review of Financial Studies, 28 (8) , 2354–2391 https://doi.org/10.1093/rfs/hhu006.