?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper aims to examine the role of corporate governance (CG) on earnings management (EM) in Indian commercial banks. In addition, the study examines the role of board gender diversity within the CG framework using data from 22 publicly traded commercial banks in India from 2010 to 2019. The study uses Principal Component Analysis (PCA) to develop a comprehensive CG measure. Using a Panel Corrected Standard Error (PCSE) approach, the study finds that CG has a significant negative impact on EM in Indian commercial banks. The findings further revealed a positive association between gender diversity of boards and EM, indicating that the lack of gender diversity on a bank’s board outweighs the benefits of gender-diverse boards. Our study shows that CG mechanisms are more effective when combined together than individual governance mechanisms. The study also provides new insight into the role of board gender diversity as a CG mechanism on EM in banks in the context of a developing country. The study provides practical implications for investors, managers, regulators and policymakers.

PUBLIC INTEREST STATEMENT

Earnings management involves managing reported earnings to achieve some private gain. Decision-makers rely on reported earnings to make crucial decisions, and when these reported numbers are manipulated, the financial reporting purpose is distorted. Banks are usually seen as trustworthy institutions where the public saves their money, and literature says these financial institutions are more vulnerable to such earnings manipulation. The presence of strong corporate governance can mitigate managers’ discretionary behaviour. Corporate governance is concerned with balancing the interests of owners and other stakeholders in all organisations through rules, procedures, accountability, and transparency in decision-making and disclosure. To investigate the relationship between corporate governance and earnings management, we looked at the Indian banking sector. According to the empirical evidence, improved corporate governance reduces earnings management in Indian banks. The policymakers can strengthen the governance mechanism in banks to reduce excessive managerial discretion.

1. Introduction

Earnings management (EM) was defined by Schipper (Citation1989) as “disclosure management in the sense of a purposeful intervention in the external financial reporting process with the intent of obtaining some private gain.” EM is frequently a consequence of loopholes in the corporate governance system in an organisation. Corporate Governance (CG) is concerned with rules, procedures, legislation, accountability, and transparency in decision-making and disclosure to balance the interests of owners and other stakeholders in all organisations. Some stakeholders (e.g., managers and controlling shareholders) can take advantage of the ambiguity in the corporate governance system for personal gain. EM and accounting fraud are the most common outcomes of a weak corporate governance structure (Arora & Sharma, Citation2016; Bai & Chu, Citation2018; El-Kassar et al., Citation2015). Any firm’s low quality of governance offers the manager more flexibility to manipulate earnings. Such practices need to be restricted because these frequently result in scams that severely affect society (Perols & Lougee, Citation2011). These opportunistic EM practices can be curbed by strong and vigilant corporate governance mechanisms (Abdou et al., Citation2021; Xie et al., Citation2003).

In this paper, we examine the role of CG in influencing EM in the Indian banking system by including gender diversity on the board as an additional governance mechanism. Since the global financial crisis of 2008, the composition of bank boards has received considerable attention. Because banks were the epicentre of the 2008 financial crisis, it was argued that a more gender-diverse board could have alleviated the worst effect of the crisis (Ghosh, Citation2017). Lagarde (Citation2010) said, “If Lehman Brothers had been ‘Lehman Sister’, today’s economic crisis clearly would look quite different” (p. 1). Women directors are generally less tolerant of opportunistic behaviour and they actively participate in the monitoring process (Gul et al., Citation2011; Levi et al., Citation2014; Liu et al., Citation2014). As opposed to the active monitoring behaviour, sometimes female directors in the top leadership position acclimate to male-dominated culture. Therefore, it has been documented that female director may not put extra effort to improve the monitoring (Adams & Funk, Citation2012; Sheedy & Lubojanski, Citation2018). The Indian banking boards are dominated mainly by men. In India, women make up nearly 10% of the top executive cadre in government-run banks (Bandyopadhyay, Citation2020). Similar to other countries, from 2015 onwards, India has also enforced a woman quota on the corporate board of listed companies (The Economic Times, Citation2015). Therefore, it is imperative to look into the board gender diversity in the Indian banking sector.

Earlier studies examining the impact of CG on EM mainly concentrated on non-financial firms (Bouvatier et al., Citation2014; Lassoued et al., Citation2017). Only a handful of studies, particularly in developed nations, have taken place in the banking sector (e.g., Cornett et al., Citation2009; Leventis et al., Citation2012; Vasilakopoulos et al., Citation2018). In recent years, some studies have examined the role of CG on EM in the banking industry in developing countries (e.g., Ahmed et al., Citation2021; Doan et al., Citation2020; Pinto et al., Citation2019; Tran et al., Citation2020; Zainuldin & Lui, Citation2020). It is argued that, unlike in developed countries, CG in developing countries is comparatively weak and complex due to political interference, lack of shareholders’ involvement, lack of sound institutional setting and corruption (Bae et al., Citation2018; Mahmood et al., Citation2018). It is easier for bank managers to indulge in EM for private gain in a weak governance structure. Therefore, examining such a relationship in this context can help us understand whether CG mechanisms effectively mitigate EM. In the Indian context, Kumari and Pattanayak (Citation2017) studied the connection between CG, EM, and bank performance. However, there has been little focus on the issue of gender diversity of the board which is a prominent and emerging CG issue in developing countries. The role of women directors in EM in the banking sector has rarely been studied (Fan et al., Citation2019). In addition, there is a paucity of research evaluating the relationship between CG and EM in the Indian banking sector.

We focused on India because we have seen recent rising frauds, governance issues, and mismanagement in the financial service sector, especially banks like ICICI, PMC, YES, and Punjab National Bank.Footnote1 YES bank and PMC bank underreported non-performing loans to meet financial statements goals. A sizeable portion of past cases of corporate financial fraud resulted from “intentional representation of amounts or disclosures in the financial statements” (Apostolou et al., Citation2000). The primary motivation for this study comes from observing these recent incidences, as Perols and Lougee (Citation2011) suggested a positive association between EM and financial frauds. Companies that use income-increasing accruals for EM must comply with accrual reversal penalties or commit fraud to obtain the intended result (Dechow et al., Citation1996; Lee et al., Citation1999; Perols & Lougee, Citation2011). In addition, unlike developed countries, the Indian banking sector is primarily dominated by public sector banks. Given that the government is both the controlling shareholder and the regulator of public sector banks, it provides a unique research setting (Pandey et al., Citation2022). The Indian banking regulator, Reserve Bank of India (RBI), has also recently proposed changing banks’ corporate governance structure in its discussion paper in June 2020. This comes after the rising bank frauds and poor governance issues in banks. Therefore, the current study is relevant in the Indian context when there is so much concern and debate about CG in banks.

We focused on the banking industry because EM practices and governance structures in financial institutions like banks need greater attention than non-financial organisations because of the ambiguity in the nature of the banking business. Banks are highly leveraged organisations that are in the business of facilitating leverage for others. The high leverage and financial structure of assets make banks more ambiguous, increasing information asymmetry and giving managers more discretionary power (Bouvatier et al., Citation2014; Morgan, Citation2002). There is also a divergence between the interest of depositors and shareholders (Crespí et al., Citation2004). Shareholders are interested in undertaking high-risk projects to maximise their wealth at the cost of attenuating the value of deposits.

Using a Panel Corrected Standard Error (PCSE) technique and Two-stage Least Square (2SLS), we provide evidence that CG helps in discouraging EM in Indian commercial banks. However, the gender diversity of the board does not necessarily constrain the manager’s opportunistic behaviour. This is because the Indian banking sector falls far short of the international standards regarding gender diversity and inclusion. According to a report by a research organisation, the composition of women employees in the banking sector is around 50% for many countries (e.g., US, Brazil, Japan and others) but only 24% for India (Bhaskaran, Citation2021). Therefore, it is possible that the female directors in high leadership positions have become accustomed to a culture where they monitor the same way as their male counterparts (Fan et al., Citation2019). Our research contributes to the existing literature in banking, CG and EM in the setting of a developing country. Our study shows that the CG attributes independently may not be efficient to reduce the EM behaviour, but working on all of these attributes collectively can enhance reporting transparency and reduce EM. In addition, we provide evidence of a lack of diversity on bank boards in India, limiting the role of gender diversified boards in discouraging EM. As far as our best knowledge is concerned, the study has made an early attempt to inspect the role of CG on EM in Indian commercial banks by incorporating the board gender diversity as a CG mechanism within the CG framework.

Following is how the rest of the article is organised: section 2 deals with the background and extant literature and section 3 captures the methodology. The results and analysis are discussed in section 4 and, finally, section 5 deals with the conclusion.

2. Background and literature review

CG can be measured through multiple attributes, and these attributes are more or less the same regardless of the nature of the organisation. A thorough analysis of the current literature reveals that the board structure, composition, audit committee, compensation etc., are the key characteristics used as proxies for CG. These governance attributes greatly influence the overall performance of any firm. Some stakeholders (e.g., managers) may exploit lacunae in the corporate governance structure because of their position for private gain (Kumari & Pattanayak, Citation2017; Vasilakopoulos et al., Citation2018).

There is a greater significance of board of directors in the CG structure of a bank (Andres & Vallelado, Citation2008; Vasilakopoulos et al., Citation2018). In the layout and composition of the board, the board size is the most commonly used attribute in the literature on CG. The number of directors on the board is usually taken as a proxy for board size (Andres & Vallelado, Citation2008; Xie et al., Citation2003). There is a difference of opinion about the outcome of board size on EM. Earlier studies have argued that smaller boards are relatively better than bigger ones in monitoring (R. Adams & Mehran, Citation2003; Mersni & Ben Othman, Citation2016; Rahman et al., Citation2006; Vasilakopoulos et al., Citation2018). This improved monitoring may reduce the tendency of the EM. Therefore, EM and board size have a direct association (Kao & Chen, Citation2004).

On the other hand, some authors argued and identified an inverse connection between board size and EM (Abdou et al., Citation2021; Alam et al., Citation2020). Firms with a larger board can employ more people to oversee and advise on management decisions. This increased supervision and monitoring reduces the discretion of managers. Cornett et al. (Citation2009) argued that commercial banks generally have larger board sizes than other forms. More independent directors may also have corporate and financial experience in a larger board, which ultimately helps prevent EM practices.

The board’s independence is another vital component of the board’s composition. The proportion of non-executive or independent directors is usually used as a proxy for board independence measurement (Andres & Vallelado, Citation2008; Klein, Citation2002). Outside or independent directors may alleviate the agency issue between managers and shareholders as they have the least conflict of interest while monitoring managers. Management oversight and control are enhanced when boards are controlled by independent directors (Alves, Citation2014). Cornett et al. (Citation2009) observed that the board’s independence had a significant negative impact on EM on a sample of US bank holding companies. They concluded that the higher autonomy of the board constrains EM behaviour. Similar findings have been drawn by Lin and Hwang (Citation2010), Bajra and Cadez (Citation2018), and Rajeevan and Ajward (Citation2020). In India, Kumari and Pattanayak (Citation2017) found an indirect connection between independent boards and EM on a sample of private sector banks.

Many researchers assume that the behaviours of EM can be mitigated by diligent boards (Abbadi et al., Citation2016; Xie et al., Citation2003). When the duration of the board meeting is high, the discretionary accrual decreases, and the board can better track the managers. Similar to the board meetings frequency, the high occurrence of the Audit Committee (AC) meetings provides greater scrutiny and vigilance on managers, financial reporting, and internal control. This eliminates the distortion of income (Xie et al., Citation2003). The manager’s discretion to exploit earnings can be curbed by active supervision of a substantial shareholder community, board and AC (Davidson et al., Citation2005). An independent AC is another essential aspect of the corporate governance process. An independent AC will better track financial statements, external audits, and the internal control framework and limit managers’ opportunistic actions (Patrick et al., Citation2015). This could raise the standard of reporting. Similar to the board’s independence, the number of independent members in the AC measures its independence (Ghosh et al., Citation2010; Lin et al., Citation2013; Xie et al., Citation2003). Lin et al. (Citation2013) observed an inverse correlation between EM and AC independence on a survey of 408 Chinese firms. Similar findings are found by Abbott et al. (Citation2000). However, some studies found either positive or insignificant associations between AC independence and EM (Choi et al., Citation2004; Ghosh et al., Citation2010).

In addition to board and AC independence, gender diverse boards can improve the board quality by bringing creativity, critical thinking, reducing bias and better problem-solving (Abdou et al., Citation2021). The presence of women directors on board is usually taken as board gender diversity. It is believed that women directors are more likely to think independently because they do not belong to the “old boys’ network” (Fan et al., Citation2019). Thus, having women directors can intensify the monitoring process and reduce managers’ opportunistic behaviour. On the contrary, some authors pointed out the opposite role of women directors (Adams & Funk, Citation2012; Sheedy & Lubojanski, Citation2018; Sila et al., Citation2016). The presence of gender diversity on the board may not necessarily curtail the discretionary behaviour of managers because female directors in the senior brass have acclimatised to a dominating male culture, making them reluctant to act differently. Fan et al. (Citation2019) found an inverted U-shaped relationship between EM and women on board in the context of US banks. Their study concluded that banks are more prone to mislead earnings when only a few female directors are on the board. However, the magnitude of EM decreases when at least three female directors are present.

2.1. Theoretical framework and hypothesis development

The agency theory highlights the separation between management and ownership, which results in agency relationship. An agency relationship is defined as “a contract under which one or more persons (the principal(s)) engage another person (the agent) to perform some service on their behalf which involves delegating some decision-making authority to the agent” (Jensen & Meckling, Citation1976, p. 308). This principal-agent relationship opens up the possibility of information asymmetry and conflict of interest. When the agents utilise this information asymmetry by virtue of their position in the organisation, which fulfils their personal interest at the cost of the principal’s welfare, it gives rise to a conflict of interest. In publicly traded companies, the managers (agents) are involved in the day-to-day operations, whereas the shareholders (principals) rely on the reports presented to them by the managers (e.g., annual reports). Companies’ financial reports are prone to distortion because managers are motivated to provide discretionary disclosure (Donnelly & Mulcahy, Citation2008). EM decreases earnings quality, and prior literature suggests that it is opportunistic rather than efficient (Healy & Wahlen, Citation1999; Siregar & Utama, Citation2008; Yu, Citation2008). “Earnings management is related to agency theory since it can create or exacerbate agency costs” (Davidson et al., Citation2004, p. 6). This agency cost can be reduced with a sound corporate governance mechanism (Baek et al., Citation2009). The role of board of directors is crucial in overseeing the managers and ensuring that their interests are aligned with those of the shareholders (Fama & Jensen, Citation1983). Although agency theory suggests that CG can mitigate EM, the empirical literature is inconclusive about the role of CG in EM. Therefore, we framed the following hypothesis:

H1: There is an impact of CG on the EM in commercial banks.

3. Empirical approach

3.1. Data and sample

All the necessary data has been collected from the RBI website and CMIE Prowess. The CG data has been hand collected from the annual reports of respective banks. GDP data has been gathered from the World bank database. Our final sample consists of 22 commercial banks listed in India, including ten private sector banks and twelve nationalised banks. The time frame of the study covers ten years, from 2010 to 2019. We have chosen a 10-year time frame to ensure adequate and persistent observations, strengthening our findings. The foreign banks operate in India as their parent companies’ branches and are not listed on the Indian stock exchanges. Foreign banks are kept out of this study due to the unavailability of CG data.

3.2. Methodology

3.2.1. Earnings management estimation

There are several established models for detecting EM in non-financial firms (e.g., Healy Model, Jones Model, DeAngelo model and Modified Jones Model). The modified Jones model developed by Dechow et al. (Citation1995) is considered one of the most acceptable methods for detecting EM in non-financial firms (Abdou et al., Citation2021; Kalantonis et al., Citation2021). However, this model cannot be applied directly to the banking business because of its unique nature of business (Chaity & Islam, Citation2021; Kumari & Pattanayak, Citation2017). Therefore, we used two commonly used variables in the banking literature-Loan loss provision (LLP) and realised securities gains and losses (RSGL) to estimate EM in banks. We initially segregated both LLP and RSGL into discretionary and non-discretionary parts. In order to capture the Discretionary Loan Loss Provision (DLLP) in banks, we employed the model introduced by Kumari and Pattanayak (Citation2017). This model is the modified version of the Beatty et al. (Citation2002) model. It was modified because of the differences in the reporting practices of Indian banks relative to banks in other parts of the world (Kumari & Pattanayak, Citation2017).

Where, DLLP = Discretionary Loan Loss Provision;

LOSS = Loan Loss Provisions;

LASSET = Natural Log of Total Assets;

NPL = Non-Performing Loans;

BDW = Bad Debt Written Off;

LLR = Loan Loss Allowance;

TLOAN = Term Loan;

LNSTLOAN = Log of Short-Term Loan;

SLOAN = Secured Loan;

LNUNSLOAN = Log of Unsecured Loan;

LOANPS = Loan to Priority Sector;

ADVPS = Advance to Public Sector;

LOANF = Loan to Foreign Country;

= Error Term.

Except LASSET, all other above variables in EquationEq. (1)(1)

(1) are expressed as a percent of Total Loans. I = Firm identifier. T = Time period. We have taken log transformation of STLOAN and UNLOAN to avoid collinearity problem.

Prior literature suggests that Realized Security Gains and Losses are also subject to manipulations (Beatty & Harris, Citation1999; Beatty et al., Citation2002). To calculate the Discretionary Realized Security Gains and Losses (DRSGL), we followed the Beatty et al. (Citation2002) model. This model was used in other previous studies of EM in banks (e.g., Cornett et al., Citation2009; Kumari & Pattanayak, Citation2017).

Where, LASSET = Natural log of total assets;

URSGL = Unrealized security gains and losses;

RSGL = Realized security gains and losses; and

= error term

Both RSGL and URSGL in EquationEq. (2)(2)

(2) are expressed as a percentage of Total Assets. The error term in EquationEq. (2)

(2)

(2) is the DRSGL, and the estimates are reported in Appendix A.

Finally, to capture the net effect of EM, we have taken the difference between DRSGL and DLLP. Our estimation of EM differs from Kumari and Pattanayak (Citation2017) where they took the addition of both the discretionary variables to capture EM. However, similar to Cornett et al. (Citation2009), we also believe that a high level of LLP reduces earnings while a higher level of RSGL increases earnings. Therefore, the net effect of EM is captured by EquationEq. (3)(3)

(3) .

3.2.2. Principal component analysis

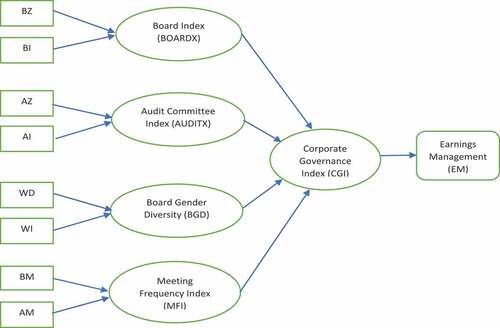

Since the primary purpose of the paper is to investigate the impact of CG on the EM, we focused on developing a CG index using Principal Component Analysis (PCA). When many corporate governance variables are introduced separately in the regression model, there is a chance of multicollinearity and PCA controls the same (Tarchouna et al., Citation2017). In addition, it is also possible that different CG machineries may act as substitutes to tackle the same agency problem (Florackis, Citation2005; Weir et al., Citation2002). It is argued that comprehensive measurement can have a more significant impact than individual measurement (AlQadasi & Abidin, Citation2018; Tarchouna et al., Citation2017). Prior research suggests that EM can be reduced using comprehensive CG mechanism (Orazalin, Citation2020; Tang et al., Citation2013). Further, the measurement error carried in the individual structural variables is reduced when the aggregate measure is used (Srinidhi et al., Citation2014; Tarchouna et al., Citation2017). We introduced eight CG variables to run PCA (Table ). The summary statistics of the CG variables are presented in Table . Based on the loadings of the variables, we found four principal components. Therefore, using the component coefficient matrix, we constructed those four principal components as sub-indexes for further analysis (Figure ). Finally, we averaged those four sub-indexes to arrive at a single CG index. The sub-indexes approach has also previously been used in corporate governance literature (Javaid, Citation2015; Sarkar et al., Citation2012).

Figure 1. Conceptual model.

Table 1. Corporate governance variables

Table 2. Descriptive statistics

Before conducting PCA, we checked for Kaiser-Meyer-Olkin (KMO) and Bartlett’s sphericity test. Bartlett’s test has the null hypothesis that the variables are not correlated enough to be factorable. Based on the p-value of Bartlett’s test (0.000), we reject the null hypothesis and ensure that variables are factorable. The KMO also shows a value of more than 0.50, indicating the sufficiency of our data to run PCA. The four principal components capture 81.67% of the variation, which is quite good.

3.2.3. Empirical model

In order to test the relationship between CG and EM, we have used the Panel Corrected Standard Errors (PCSE) approach to estimate our model. We have used the PCSE method because our model has heteroskedasticity and cross-sectional dependency (Table ). The PCSE approach simultaneously corrects the problem of autocorrelation, heteroskedasticity and cross-sectional dependence (Doku et al., Citation2019; Sandow et al., Citation2021). In the presence of autocorrelation, heteroskedasticity and cross-sectional dependency, OLS provides biased estimates. Beck and Katz (Citation1995) developed the PCSE technique, which is viewed as a viable alternative because it addresses the issues raised by OLS. Beck and Katz (Citation1995) proposed replacing OLS standard errors with panel corrected standard errors in PCSE and suggested that the PCSE estimator is particularly robust regarding the efficiency achieved from standard errors, based on Monte Carlo simulation.

Table 3. Cross-Section dependency test

In the PCSE approach, the data is initially modified to remove serial correlation. Next, the transformed data is subjected to OLS, with standard errors corrected for cross-section dependency, heteroskedasticity and autocorrelation, ultimately improving estimation efficiency. The Feasible Generalised Least Squares (FGLS) also serves a similar purpose served by PCSE. However, FGLS requires time (T) to be greater than cross-section (N). Since, in our panel dataset, N is greater than T (N >T), PCSE is more appropriate. Our baseline model takes the following form:

The description of the regression variables is given in Table . We further tested the model with each sub-indexes using EquationEq. (5)(5)

(5) to identify the impact of each of these indexes.

Table 4. Regression variables

3.2.4. Description of control variables

We have used some control variables for our study based on previous literature. We have captured bank size as the natural log of total assets. In general, large corporations are subject to greater scrutiny by the regulators, investors and analysts, avoiding the opportunistic actions of those companies’ managers. In contrast to large corporations, small firms are usually not subject to much scrutiny by the public compared to large firms and can conceal information from the public. Thus, managers of small firms appear to be more interested in income smoothing relative to large firms. Similar views are expressed by Albrecth and Richardson (Citation1990) and Lee and Choi (Citation2002). Similar results are found in the case of Vietnamese banks (Thinh & Thu, Citation2020), and banks in MENA (emerging) countries (Lassoued et al., Citation2018). The capital adequacy ratio is taken as the proxy for bank capitalisation. The well-capitalised banks are subject to less scrutiny by the regulators and therefore have the propensity to manipulate earnings (Cornett et al., Citation2009; Leventis et al., Citation2012). The less capitalised banks are subject to strict oversight by the regulators, limiting the EM actions of managers in these banks. Following previous research (Fonseca & González, Citation2008; Vishnani et al., Citation2019), we have used the GDP growth rate to control macroeconomic factors.

4. Results and analysis

4.1. Descriptive and correlation analysis

The summary statistics are presented in Table . The mean value of EM is 0.3896, which indicates the absolute value of discretion exercised by bank managers. Followed by previous research (e.g., Jin et al., Citation2019; Zainuldin & Lui, Citation2020), we have taken the absolute value of EM to capture the total magnitude of discretion. The size of the board (BZ) varies from 6–17, with a mean of 10.75 and a median of 11. This means that most banks in India have an average of 11 directors on the board over the ten years. As per Section 149(1) of the Companies Act, 2013, every listed company must have a minimum of 3 directors. Board Independence (BI) has a mean value of 6.4, with the lowest and highest independent directors of 2 and 13, respectively. This means most Indian banks have, on average, six independent directors on their board during the study period. The Companies Act, 2013 requires one-third (1/3) of the directors on the board to necessarily be independent. The board meeting frequency (BM) has a mean value of 12.44, indicating that most banks in India hold 12 board meetings on average during a year. The most diligent boards hold 28 meetings, while the least engaged boards hold four meetings during a year. It is to be noted that the minimum value of 4 board meetings is due to the private banks since nationalised banks must hold a minimum of 6 board meetings as per clause 12 of the Nationalised Bank scheme, 1970. As per the Companies Act, 2013, two-thirds of the audit members must be independent.

The sample banks in our study have a mean (median) value of 5.43 (5) with a least of 3 members and an extreme of 10 in the audit committee (AC). The mean value (3.422) of AC independence (AI) indicates that the majority of the banks have fulfilled the Companies Act, 2013 guidelines about AC independence. The frequency of AC meetings (AM) is also high, with mean, median, the maximum value of 10.05, 10 and 18, respectively. The bank size (SIZE) has a mean value of 12.15 with minimal variations across all banks in terms of total assets. The bank with the largest and the smallest total assets have a value of 15.11 and 8.72, respectively. The capital adequacy ratio (CAR) has a mean value of 13.23%. It clearly shows that banks in India are maintaining high CAR above the Basel norms. Finally, the GDP growth rate shows a mean value of 0.06 and fluctuations can be observed from the maximum and minimum values in Table .

The correlation coefficient among the explanatory variables is presented in Table . The correlation coefficient among all the variables is less than 0.80 (except for one correlation between MFI and CGI), suggesting that multicollinearity is not severe in our data (Gujarati, Citation1995). The high correlation between MFI and CGI is not a problem since we have not included MFI and CGI together in the regression model. We have also checked the variance inflation factor (VIF) which is less than 5 for all explanatory variables.

Table 5. Correlation matrix

4.2. Discussion

Table displays the PCSE regression result related to CG and control variables. The coefficient of CG index (CGI) is negative at the 10% level of significance. The negative coefficient of CGI indicates that the overall corporate governance practices help to reduce the EM practices in the Indian commercial banks. However, the gender diversity of the board seems to behave in the opposite direction of the CGI, as evident from the significant (at 10% level) and positive coefficient of BGD. This means that board gender diversity does not necessarily constrain managers’ opportunistic behaviour in Indian commercial banks. Women in top positions in banks are reluctant to exercise their diligence, and as a result of being attuned to an environment in which their participation is limited, they behave similarly to their male peers. Some studies (Adams & Ragunathan, Citation2017; Sheedy & Lubojanski, Citation2018) report similar results for financial firms. This is also because the number of women directors or women independent directors is deficient (mostly one) in the Indian commercial banks. As per the critical mass theory, a certain threshold (minimum three) must be met to normalise the presence of minority gender on the board (Kanter, Citation1977a, Citation1977b). The two major studies by Kanter (Citation1977a, Citation1977b) sparked the discussion on “critical mass” in women and politics. When the board has a marginal number of women directors, it is treated as representatives or symbols of women. Therefore, they are less likely to perform their active monitoring role. The Indian banking sector falls far short of the international standards in terms of gender diversity.

Table 7. 2SLS regression (dependent variable: EM)

The variables Board Index (BOARDX), Audit Committee Index (AUDITX) and Frequency of board and audit committee meetings (MFI) are, although negative but insignificant. This could be due to a lack of experts on the board and AC, as Ghosh et al. (Citation2010) claimed that the higher presence of experts on the AC improves the supervision rather than the proportion of independent members. The independence of independent directors is also questionable in India (Laskar, Citation2021). The regulator has spoken about who is not allowed to be an independent director, but it is nearly quiet on their expertise or qualifications. Furthermore, according to primeinfobase.com, over the last five years, 4088 independent directors have left the boards making Indian boards devoid of qualified people (Haldea, Citation2020). Further, having more board and audit committee members and more meetings do not necessarily limit EM. It is possible that it will elevate the company’s cost. There may be a coordination issue that causes sluggish decision making, outweighing the benefits of having more board and audit members. Therefore, it can be inferred that the CG attributes are more efficient in discouraging EM when they function collectively. This finding is consistent with previous research (e.g., Aguilera et al., Citation2008; Ward et al., Citation2009), which suggests that while individual CG mechanisms appear ineffective, when combined with other CG mechanisms, they have a significant impact on outcome. The coefficient of GDP growth is significant at a 5% level. The negative coefficient of GDP implies that bank managers in India become more optimistic and charge less LLP discretionarily during economic growth seasons. During a downturn, the business cycle gets affected and it severely affects the repayment capacity of the bank customers. With the anticipation of more defaults, bank managers charge more LLP during downturns and vice-versa. Our finding related to GDP is consistent with Vishnani et al. (Citation2019) in the Indian context. The SIZE variable is insignificant because all the banks are listed and regulated and thus, their size hardly has little bearing on EM. This finding is in line with Kumari and Pattanayak (Citation2017). The significant (at 1% level) and negative coefficient of CAR indicates that banks with a lower level of capital engage more in EM. This is because low capitalised banks have an incentive to postpone the loan write-offs and accelerate the recognition of securities gains (Cornett et al., Citation2009).

4.3. Additional analysis

We have further tested our baseline model with the help of two-stage least square regression to control for the potential endogeneity issue. The 2SLS method resolves any endogeneity issue arising from the omitted variable bias (cross-section and time-invariant) and the simultaneity bias. Table displays the results of 2SLS regression with error-component two-stage least squares (EC2SLS). The EC2SLS method employs Baltagi’s random-effects estimator and offers a broader range of instruments capable of yielding small-sample efficiency gains (Baltagi & Liu, Citation2009). The CGI index is significant (at 5% level) and negatively related to EM. This further validates our findings and our results are robust. Since 2SLS regression uses instrumental variables, we have checked the validity of our instruments. A significant J-statistic may indicate an erroneous instrument or a misspecified structural equation. The p-value for the Hansen J test shows that our instruments are valid and that model is correctly specified.

Table 6. PCSE regression result (dependent variable: EM)

5. Conclusion

This paper attempted to examine the role of CG on the EM of Indian commercial banks. The study uses a Panel Corrected Standard Error (PCSE) approach to account for heteroskedasticity and cross-sectional dependence. The study uses Principal component analysis (PCA) to develop a CG index based on four sub-indexes. The study found that CG helps to mitigate the EM in Indian commercial banks. However, the Board gender diversity of Indian commercial banks fails to discourage the EM, owing to a lack of sufficient female directors on the board. The study also shows that low-capitalised banks are more involved in EM. While increased economic growth pushes managers to engage more in EM, bank size has little bearing on EM.

The study has several ramifications for managers, investors, policymakers and regulators. The managers can focus on improving the disclosure quality and developing a comprehensive CG mechanism. Investors should pay attention not only to corporate governance practices followed by banks but also to the quality of information disclosed in the financial statements. This might help to improve the quality of corporate disclosures made by corporations in order to communicate firm performance and governance to outside investors. The study may aid policymakers and regulators in identifying banking sector specific significant corporate governance parameters that should be prioritised to improve financial reporting in developing countries such as India. Gender diversity is becoming more important to institutional investors in their investment decisions. Some socially responsible indices (e.g., MSCI KLD 400 Social Index) also encourage gender diversified boards. Our study shows that most Indian banks have appointed, on average, one women director, which is below the critical mass of at least three women directors. In order to mitigate EM, the regulators (e.g., SEBI and RBI) and policymakers (e.g., MCA) may further encourage the participation of women directors so that at least three independent women directors are present on the board of Indian commercial banks. In addition, the regulators must recognise that banks engage in earnings management actions, particularly with LLP, notwithstanding India’s rule-based provisioning framework. As a result, the regulator and external auditor must exercise extreme caution and vigilance. The implementation of Ind-AS into Indian banking is expected to alleviate the problem of EM further.

The study contributes to the existing body of knowledge in the field of banking in developing countries. The findings support the agency theory and critical mass theory. For any developing country, such as India, the banking sector is a significant component of the financial system (it accounts for more than 70% of total assets in the Indian financial sector). As a result, this industry requires special attention, care, and vigilance. The scope of our study is limited to India only. Further research can be carried out on this topic by performing a cross-country study having different ownership structures, such as institutional ownership, foreign ownership and government ownership.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Sarit Biswas

Sarit Biswas is a research scholar in the area of Finance & Control at Indian Institute of Management Shillong, India. His research interest includes Corporate Governance, Earnings management and Banking. He has participated at various national and international conferences, seminar and workshops. He has also contributed a few research articles in peer-reviewed international and national journals.

Mousumi Bhattacharya

Prof. Mousumi Bhattacharya is an Associate Professor at Indian Institute of Management Shillong. Prof. Pradip H Sadarangani is a Professor at Indian Institute of Management Shillong and Prof. Justin Yiqiang Jin is an Associate Professor at DeGroote School of Business, McMaster University. The team’s research interest includes earnings management, corporate governance and banking.

Notes

1. The female CEO of ICICI Bank was accused of fraud years before she was forced to resign as CEO in 2018, and a lawsuit was filed against her in 2019. The PNB officials misused the banking system which resulted in a big scam in the year 2018. In 2019, the PMC bank crisis was brought to light for the first time. YES Bank was placed under a 30-day moratorium by the Reserve Bank of India (RBI) on 5 March 2020.

References

- Abbadi, S. S., Hijazi, Q. F., & Al-Rahahleh, A. S. (2016). Corporate governance quality and earnings management: evidence from Jordan. Australasian Accounting, Business and Finance Journal, 10(2), 54–20. https://doi.org/10.14453/aabfj.v10i2.4

- Abbott, L. J., Parker, S., & Peters, G. F., 2000. The effectiveness of blue ribbon committee recommendations in mitigating financial misstatements: An empirical study. Working Paper . http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.515.4227&rep=rep1&type=pdf

- Abdou, H. A., Ellelly, N. N., Elamer, A. A., Hussainey, K., & Yazdifar, H. (2021). Corporate governance and earnings management nexus: Evidence from the UK and Egypt using neural networks. International Journal of Finance & Economics, 26(4), 6281–6311. https://doi.org/10.1002/ijfe.2120

- Adams, R., & Mehran, H. (2003). Is corporate governance different for bank holding companies? FRBNY Economic Policy Review, 9(1), 123–142. https://doi.org/10.2139/ssrn.387561

- Adams, R. B., & Funk, P. (2012). Beyond the glass ceiling: Does gender matter? Management Science, 58(2), 219–235. https://doi.org/10.1287/mnsc.1110.1452

- Adams, R. B., & Ragunathan, V. (2017). Lehman Sisters. SSRN https://doi.org/10.2139/ssrn.3046451

- Aguilera, R. V., Filatotchev, I., Gospel, H., & Jackson, G. (2008). An organisational approach to comparative corporate governance: Costs, contingencies, and complementarities. Organisation Science, 19(3), 475–492 https://doi.org/10.1287/orsc.1070.0322.

- Ahmed, M. G., Ganesan, Y., Hashim, F., & Sadaa, A. M. (2021). The effect of chairman tenure on governance and earnings management: A case study in Iraq. The Journal of Asian Finance, Economics and Business, 8(3), 1205–1215. https://doi.org/10.13106/jafeb.2021.vol8.no3.1205

- Alam, N., Ramachandran, J., & Nahomy, A. H. (2020). The impact of corporate governance and agency effect on earnings management–A test of the dual banking system. Research in International Business and Finance, 54 (1) , 101242. https://doi.org/10.1016/j.ribaf.2020.101242

- Albrecth, W. D., & Richardson, F. M. (1990). Income smoothing by economy sector. Journal of Business Finance and Accounting, 17(5), 713–730. https://doi.org/10.1111/j.1468-5957.1990.tb00569.x

- AlQadasi, A., & Abidin, S. (2018). The effectiveness of internal corporate governance and audit quality: The role of ownership concentration–Malaysian evidence. Corporate Governance, 18(2), 233–253. https://doi.org/10.1108/CG-02-2017-0043

- Alves, S. (2014). The effect of board Independence on the earnings quality: Evidence from Portuguese listed companies. Australasian Accounting, Business and Finance Journal, 8(3), 23–44. https://doi.org/10.14453/aabfj.v8i3.3

- Andres, P., & Vallelado, E. (2008). Corporate governance in banking: The role of the board of directors. Journal of Banking & Finance, 32(12), 2570–2580. https://doi.org/10.1016/j.jbankfin.2008.05.008

- Apostolou, B., Hassell, J. M., & Webber, S. A. (2000). Forensic expert classification of management fraud risk factors. Journal of Forensic Accounting, 1(2), 181–192.

- Arora, A., & Sharma, C. (2016). Corporate governance and firm performance in developing countries: Evidence from India. Corporate Governance, 16(2), 420–436. https://doi.org/10.1108/CG-01-2016-0018

- Bae, S. M., Masud, M., Kaium, A., & Kim, J. D. (2018). A cross-country investigation of corporate governance and corporate sustainability disclosure: A signaling theory perspective. Sustainability, 10(8), 2611 https://doi.org/10.3390/su10082611.

- Baek, H. Y., Johnson, D. R., & Kim, J. W. (2009). Managerial ownership, corporate governance and voluntary disclosure. Journal of Business & Economic Studies, 15 (2), 44–61. https://www.proquest.com/scholarly-journals/managerial-ownership-corporate-governance/docview/235802972/se-2?accountid=39988

- Bai, X., & Chu, T. 2018 . Corporate governance and earnings management: A banking industry perspective . SSRN. https://dx.doi.org/10.2139/ssrn.3318144.

- Bajra, U., & Cadez, S. (2018). The impact of corporate governance quality on earnings management: Evidence from European companies cross-listed in the US. Australian Accounting Review, 28(2), 152–166. https://doi.org/10.1111/auar.12176

- Baltagi, B. H., & Liu, L. (2009). A note on the application of EC2SLS and EC3SLS estimators in panel data models. Statistics & Probability Letters, 79(20), 2189–2192. https://doi.org/10.1016/j.spl.2009.07.014

- Bandyopadhyay, T. (2020). Where have all the women bankers gone? Retrieved March 29, 2022, from Rediff website: https://www.rediff.com/business/column/where-have-all-the-women-bankers-gone/20200107.htm

- Beatty, A., & Harris, D. G. (1999). The effects of taxes, agency costs and information asymmetry on earnings management: A comparison of public and private firms. Review of Accounting Studies, 4(3), 299–326 https://doi.org/10.1023/A:1009642403312.

- Beatty, A. L., Ke, B., & Petroni, K. R. (2002). Earnings management to avoid earnings declines across publicly and privately held banks. The Accounting Review, 77(3), 547–570. https://doi.org/10.2308/accr.2002.77.3.547

- Beck, N., & Katz, J. (1995). What to do (and not to do) with time-series cross-section data. American Political Science Review, 89(3), 634–647. https://doi.org/10.2307/2082979

- Bhaskaran, R. (2021). Indian banks remain male bastions despite gender inclusion policies by govt, RBI | policy circle. Policy circle. Retrieved March 29, 2022, from Policy Circle website:, https://www.policycircle.org/industry/gender-inclusion-bank jobs/#:~:text=Except%20for%20three%20banks%2C%20the,only%20one%20woman%20board%20member

- Bouvatier, V., Lepetit, L., & Strobel, F. (2014). Bank income smoothing, ownership concentration and the regulatory environment. Journal of Banking & Finance, 41 (1) , 253–270. https://doi.org/10.1016/j.jbankfin.2013.12.001

- Chaity, N. S., & Islam, K. Z. (2021). Bank efficiency and practice of earnings management: A study on listed commercial banks of Bangladesh. Asian Journal of Accounting Research 7 (2) 114–128 . https://doi.org/10.1108/AJAR-09-2020-0080

- Choi, J., Jeon, K., & Park, J. (2004). The role of audit committees in decreasing earnings statement: Korean evidence. International Journal of Accounting, Auditing & Performance Evaluation, 1(1), 37–60. https://doi.org/10.1504/IJAAPE.2004.004142

- Cornett, M. M., McNutt, J. J., & Tehranian, H. (2009). Corporate governance and earnings management at large US bank holding companies. Journal of Corporate Finance, 15(4), 412–430 https://doi.org/10.1016/j.jcorpfin.2009.04.003.

- Crespí, R., García-Cestona, M. A., & Salas, V. (2004). Governance mechanisms in Spanish banks. Does ownership matter? Journal of Banking & Finance, 28(10), 2311–2330. https://doi.org/10.1016/j.jbankfin.2003.09.005

- Davidson, W. N., Jiraporn, P., Kim, Y. S., & Nemec, C. (2004). Earnings management following duality-creating successions: Ethnostatistics, impression management and agency theory. Academy of Management Journal, 47(2), 267–275. https://doi.org/10.5465/20159577

- Davidson, R., Goodwin-Stewart, J., & Kent, P. (2005). Internal governance structures and earnings management. Accounting and Finance, 45(2), 241–267. https://doi.org/10.1111/j.1467-629x.2004.00132.x

- Dechow, P. M., Sloan, R. G., & Sweeney, A. P. (1995). Detecting earnings management. Accounting review 70 (2) , 193–225. http://www.jstor.org/stable/248303

- Dechow, P., Sloan, R., & Sweeney, A. (1996). Causes and consequences of earnings manipulations: An analysis of firms subject to enforcement actions by the SEC. Contemporary Accounting Research, 13(1), 1–36. https://doi.org/10.1111/j.1911-3846.1996.tb00489.x

- Doan, A. T., Lin, K. L., & Doong, S. C. (2020). State-controlled banks and income smoothing. Do politics matter? The North American Journal of Economics and Finance, 51 (1) , 101057. https://doi.org/10.1016/j.najef.2019.101057

- Doku, J. N., Kpekpena, F. A., & Boateng, P. Y. (2019). Capital structure and bank performance: Empirical evidence from Ghana. African Development Review, 31(1), 15–27. https://doi.org/10.1111/1467-8268.12360

- Donnelly, R., & Mulcahy, M. (2008). Board structure, ownership and voluntary disclosure in Ireland. Corporate Governance: The International Review, 16(5), 416–429. https://doi.org/10.1111/j.1467-8683.2008.00692.x

- El-Kassar, A. N., Messarra, L. C., & Elgammal, W. (2015). Effects of ethical practices on corporate governance in developing countries: Evidence from lebanon and Egypt. Corporate Ownership & Control, 12(3), 494–504 https://doi.org/10.22495/cocv12i3c5p1.

- Fama, E. F., & Jensen, M. C. (1983). Separation of ownership and control. The Journal of Law and Economics, 26(2), 301–325. https://doi.org/10.1086/467037

- Fan, Y., Jiang, Y., Zhan, X., & Zhu, Y. (2019). Women on boards and bank earnings management: From zero to hero. Journal of Banking and Finance, 107(10), 105607. https://doi.org/10.1016/j.jbankfin.2019.105607

- Florackis, C. (2005). Internal corporate governance mechanisms and corporate performance: Evidence for UK firms. Applied Financial Economics Letters, 1(4), 211–216. https://doi.org/10.1080/17446540500143897

- Fonseca, A. R., & González, F. (2008). Cross-country determinants of bank income smoothing by managing loan-loss provisions. Journal of Banking & Finance, 32(2), 217–228. https://doi.org/10.1016/j.jbankfin.2007.02.012

- Ghosh, A., Marra, A., & Moon, D. (2010). Corporate boards, audit committees, and earnings management: Pre- and post-sox evidence. Journal of Business Finance & Accounting,37, 37(9–10), 1145–1176. https://doi.org/10.1111/j.1468-5957.2010.02218.x

- Ghosh, S. (2017). Why is it a man’s world, after all? Women on bank boards in India. Economic Systems, 41(1), 109–121. https://doi.org/10.1016/j.ecosys.2016.05.007

- Gujarati, D. N. (1995). Basic Econometrics. 3rd ed. McGraw-Hill.

- Gul, F. A., Srinidhi, B., & Ng, A. C. (2011). Does board gender diversity improve the informativeness of stock prices? Journal of Accounting and Economics, 51(3), 314–338. https://doi.org/10.1016/j.jacceco.2011.01.005

- Haldea, P. (2020). Myth of independent directors: They can only be effective if they are independent of promoters. Financial express. Retrieved March 29, 2022, from Financialexpress.com website: https://www.financialexpress.com/opinion/myth-of-independent-directors-they-can-only-be-effective-if-they-are-independent-of-promoters/2104809/

- Healy, P. M., & Wahlen, J. M. (1999). A review of the earnings management literature and its implications for standard setting. Accounting Horizons, 13(4), 365–383. https://doi.org/10.2308/acch.1999.13.4.365

- Javaid, F. (2015). Impact of corporate governance index on firm performance: Evidence from Pakistani manufacturing sector. Journal of Governance and Regulation, 4(3), 163–174. https://doi.org/10.22495/jgr_v4_i3_c1_p6

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behaviour, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)

- Jin, J. Y., Kanagaretnam, K., Liu, Y., & Lobo, G. J. (2019). Economic policy uncertainty and bank earnings opacity. Journal of Accounting and Public Policy, 38(3), 199–218. https://doi.org/10.1016/j.jaccpubpol.2019.05.002

- Kalantonis, P., Schoina, S., & Kallandranis, C. (2021). The impact of corporate governance on earnings management: Evidence from Greek listed firms. Corporate Ownership & Control, 18(2), 140–153. https://doi.org/10.22495/cocv18i2art11

- Kanter, R. M. (1977a). Men and Women of the Corporation. Basic Books.

- Kanter, R. M. (1977b). Some effects of proportions on group life. Am. J. Sociol, 82(5), 965–990 https://www.jstor.org/stable/2777808.

- Kao, L., & Chen, A. (2004). The effects of board characteristics on earnings management. Corporate Ownership & Control, 1(3), 96–107. https://doi.org/10.22495/cocv1i3p9

- Klein, A. (2002). Audit committee, board of director characteristics, and earnings management. Journal of Accounting and Economics, 33(3), 375–400. https://doi.org/10.1016/S0165-4101(02)00059-9

- Kumari, P., & Pattanayak, J. K. (2017). Linking earnings management practices and corporate governance system with the firms’ financial performance: A study of Indian commercial banks. Journal of Financial Crime, 24(2), 223–241. https://doi.org/10.1108/JFC-03-2016-0020

- Lagarde, C. (2010). Women, power and the challenge of the financial crisis. International Herald Tribune: Op-Ed.

- Laskar, A. (2021). Independent directors have failed minority shareholders: Sebi chief. Mint. Retrieved March 29, 2022, from mint website: https://www.livemint.com/news/india/independent-directors-have-failed-minority-shareholders-says-sebi-chief-11617698351094.html

- Lassoued, N., Attia, R., & Sassi, H. (2017). Earnings management and ownership structure in emerging market evidence from banking industry. Managerial Finance, 43(10), 1117–1136 https://doi.org/10.1108/MF-11-2015-0312.

- Lassoued, N., Attia, M. B. R., & Sassi, H. (2018). Earnings management in Islamic and conventional banks: Does ownership structure matter? Evidence from the MENA region. Journal of International Accounting, Auditing and Taxation, 30 (1) , 85–105. https://doi.org/10.1016/j.intaccaudtax.2017.12.003

- Lee, T. A., Ingram, R. W., & Howard, T. P. (1999). The difference between earnings and operating cash flow as an indicator of financial reporting fraud. Contemporary Accounting Research, 16(4), 749–786. https://doi.org/10.1111/j.1911-3846.1999.tb00603.x

- Lee, B. B., & Choi, B. (2002). Company size, auditor type, and earnings management. Journal of Forensic Accounting, 3 (1) , 27–50.

- Leventis, S., Dimitropoulos, P., & Jallow, K. (2012). The role of corporate governance in earnings management: Experience from US banks. Journal of Applied Accounting Research, 13(2), 161–177. https://doi.org/10.1108/09675421211254858

- Levi, M., Li, K., & Zhang, F. (2014). Director gender and mergers and acquisitions. Journal of Corporate Finance, 28 (1) , 185–200. https://doi.org/10.1016/j.jcorpfin.2013.11.005

- Lin, J. W., & Hwang, M. I. (2010). Audit quality, corporate governance, and earnings management: A meta‐analysis. International Journal of Auditing, 14(1), 57–77 https://doi.org/10.1111/j.1099-1123.2009.00403.x.

- Lin, T., Hutchinson, M., & Percy, M. (2013). Earnings management and the role of the audit committee: An investigation of the influence of cross-listing and government official on the audit committee. Journal of Management & Governance, 19(1), 197–227. https://doi.org/10.1007/s10997-013-9284-3

- Liu, Y., Wei, Z., & Xie, F. (2014). Do women directors improve firm performance in China? Journal of Corporate Finance, 28 (1) , 169–184. https://doi.org/10.1016/j.jcorpfin.2013.11.016

- Mahmood, Z., Kouser, R., Ali, W., Ahmad, Z., & Salman, T. (2018). Does corporate governance affect sustainability disclosure? A mixed methods study. Sustainability, 10(1), 207. https://doi.org/10.3390/su10010207

- Mersni, H., & Ben Othman, H. (2016). The impact of corporate governance mechanisms on earnings management in Islamic banks in the Middle East region. Journal of Islamic Accounting and Business Research, 7(4), 318–348. https://doi.org/10.1108/JIABR-11-2014-0039

- Morgan, D. P. (2002). Rating banks: Risk and uncertainty in an opaque industry. American Economic Review, 92(4), 874–888. doi:10.1257/00028280260344506.

- Orazalin, N. (2020). Board gender diversity, corporate governance, and earnings management: Evidence from an emerging market. Gender in Management, 35(1), 37–60. https://doi.org/10.1108/GM-03-2018-0027

- Pandey, A., Tripathi, A., & Guhathakurta, K. (2022). The impact of banking regulations and accounting standards on estimating discretionary loan loss provisions. Finance Research Letters, 44 (1) , 102068. https://doi.org/10.1016/j.frl.2021.102068

- Patrick, E. A., Paulinus, E. C., & Nympha, A. N. (2015). The influence of corporate governance on earnings management practices: A study of some selected quoted companies in Nigeria. American Journal of Economics, Finance and Management, 1(5), 482–493.

- Perols, J. L., & Lougee, B. A. (2011). The relation between earnings management and financial statement fraud. Advances in Accounting, 27(1), 39–53. https://doi.org/10.1016/j.adiac.2010.10.004

- Pinto, I., Gaio, C., & Gonçalves, T. (2019). Corporate governance, foreign direct investment, and bank income smoothing in African countries. International Journal of Emerging Markets, 15(4), 670–690 https://doi.org/10.1108/IJOEM-04-2019-0297.

- Rahman, R. A., Ali, F. H., & Haniffa, R. (2006). Board, audit committee, culture and earnings management: Malaysian evidence. Managerial Auditing Journal, 21(7), 783–804. https://doi.org/10.1108/02686900610680549

- Rajeevan, S., & Ajward, R. (2020). Board characteristics and earnings management in Sri Lanka”. Journal of Asian Business and Economic Studies, 27(1), 2–18. https://doi.org/10.1108/JABES-03-2019-0027

- Sandow, J. N., Duodu, E., Oteng-Abayie, E. F., & Seetharam, Y. (2021). Regulatory capital requirements and bank performance in Ghana: Evidence from panel corrected standard error. Cogent Economics & Finance, 9(1), 2003503. https://doi.org/10.1080/23322039.2021.2003503

- Sarkar, J., Sarkar, S., & Sen, K. (2012). A corporate governance index for large listed companies in India. pace university accounting research paper (2012/08). WP-2012-009. IGIDR . http://www.igidr.ac.in/pdf/publication/WP-2012-009.pdf

- Schipper, K. (1989). Earnings management. Accounting Horizons, 3 (4), 91. https://www.proquest.com/scholarly-journals/earnings-management/docview/208918065/se-2?accountid=39988

- Sheedy, E., & Lubojanski, M. (2018). Risk management behaviour in banking. Managerial Finance, 44(7), 902–918. https://doi.org/10.1108/MF-11-2017-0465

- Sila, V., Gonzalez, A., & Hagendorff, J. (2016). Women on board: Does boardroom gender diversity affect firm risk? Journal of Corporate Finance, 36 (1) , 26–53. https://doi.org/10.1016/j.jcorpfin.2015.10.003

- Siregar, S. V., & Utama, S. (2008). Type of earnings management and the effect of ownership structure, firm size and corporate governance practices: Evidence from Indonesia. The International Journal of Accounting, 43(1), 1–27. https://doi.org/10.1016/j.intacc.2008.01.001

- Srinidhi, B. N., He, S., & Firth, M. (2014). The effect of governance on specialist auditor choice and audit fees in US family firms. The Accounting Review, 89(6), 2297–2329 https://doi.org/10.2308/accr-50840.

- Tang,H.W., Chen,A., & Chang,C.C. (2013). Insider trading, accrual abuse, and corporate governance in emerging markets—Evidence from Taiwan. Pacific-Basin Finance Journal, 24 (1) , 132–155. https://doi.org/10.1016/j.pacfin.2013.04.005

- Tarchouna,A., Jarraya,B., & Bouri,A. (2017). How to explain non-performing loans by many corporate governance variables simultaneously? Acorporate governance index is built to US commercial banks. Research in International Business and Finance, 42 (1) , 645–657. https://doi.org/10.1016/j.ribaf.2017.07.008

- Thinh,Q.T., & Thu,T.N.A. (2020). Influence of financial indicators on earnings management behavior: Evidence from Vietnamese commercial banks. Banks and Bank Systems, 15(2), 167 doi:10.21511/bbs.15(2).2020.15.

- Times, T. E. (2015). Sebi asks listed firms to appoint women directors by month-end. Retrieved March 29, 2022, from The Economic Times website: https://economictimes.indiatimes.com/sebi-asks-listed-firms-to-appoint-women-directors-by-month-end/articleshow/46572826.cms?from=mdr

- Tran, Q. T., Lam, T. T., & Luu, C. D. (2020). Effect of corporate governance on corporate social responsibility disclosure: empirical evidence from Vietnamese commercial banks. Journal of Asian Finance, Economics and Business, 7(11), 327–333. https://doi.org/10.13106/jafeb.2020.vol7.no11.327

- Vasilakopoulos, K., Tzovas, C., & Ballas, A. (2018). The impact of corporate governance mechanisms on EU banks’ income smoothing behavior. Corporate Governance: International Journal of Business in Society, 18(5), 931–953. https://doi.org/10.1108/CG-09-2017-0234

- Vishnani, S., Agarwal, S., Agarwalla, R., & Gupta, S. (2019). Earnings management, capital management and signalling behaviour of Indian banks. Asia-Pacific Financial Markets, 26(3), 285–295. https://doi.org/10.1007/s10690-018-09265-x

- Ward, A. J., Brown, J. A., & Rodriguez, D. (2009). Governance bundles, firm performance, and the substitutability and complementarity of governance mechanisms. Corporate Governance: An International Review, 17(5), 646–660. https://doi.org/10.1111/j.1467-8683.2009.00766.x

- Weir, C., Laing, D., & McKnight, P. J. (2002). Internal and external governance mechanisms: Their impact on the performance of large UK public companies. Journal of Business Finance, 29(5), 579–611. https://doi.org/10.1111/1468-5957.00444

- Xie, B., Davidson, W. N., & Dadalt, P. J. (2003). Discretionary accruals and corporate governance: The roles of the board and the audit committee. Journal of Corporate Finance, 9(1), 295–316 https://doi.org/10.1016/S0929-1199(02)00006-8.

- Yu, F. (2008). Analyst coverage and earnings management. Journal of Financial Economics, 88(2), 245–271. https://doi.org/10.1016/j.jfineco.2007.05.008

- Zainuldin, M. H., & Lui, T. K. (2020). Earnings management in financial institutions: A comparative study of Islamic banks and conventional banks in emerging markets. Pacific Basin Finance Journal, 62 (1) , 101044 https://doi.org/10.1016/j.pacfin.2018.07.005.