?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study aimed to examine the effect of financial Literacy and social Media on micro capital through financial technology. This type of research is explanatory/associative, accompanied by hypothesis testing. The unit of analysis of this research is the Creative Industry Sector in East Java, with a population of 376 creative industries. The number of samples is 65 SMEs using the stratified random sampling method. The results of this study prove that financial literacy has a positive and significant effect on financial technology, social media has a significant effect on financial technology, financial literacy has a positive and significant effect on micro capital, social media has a significant effect on micro capital, and financial technology has a significant effect on micro capital.

1. Introduction

The creative industry sector is part of small and medium-sized industries that are quite large in number. Their presence is spread evenly throughout Indonesia and even has a large enough share in the formation of gross domestic product. Many creative industry sectors are included in the SMEs cluster with conventional business governance. Inadequate managerial capabilities, access to capital, information technology, and business uncertainty during the COVID-19 pandemic have made the existence of the SMEs sector even more challenging (Kuchciak & Wiktorowicz, Citation2021)

Access to capital is still an obstacle to the growth of the SMEs sector because banking and non-banking financial institutions still demand formal requirements that are difficult to meet (Taghizadeh-Hesary & Yoshino, Citation2020). The development of information technology makes financial services easy, fast, and accurate so that the dimensions of space and time become flexible. This phenomenon shows that the development of FinTech can provide adequate access to capital for SMEs, but its utilization is not optimal. Therefore, it is necessary to carry out structured and massive financial literacy socialization by optimizing social media’s role in strengthening access to micro capital in the SMEs sector (Kuchciak & Wiktorowicz, Citation2021).

Financial literacy is being widely used to deliver information related to financial services marketing strategies (Lusardi, Citation2019). The success of the financial education process for the public is determined by the quality of the literacy programs owned by financial service providers (Kou et al., Citation2021) because each has priorities and targets as planned (Taghizadeh-Hesary & Yoshino, Citation2020).

The financial services marketing strategy has begun to shift its target by utilizing financial literacy as a FinTech service product (Gal et al., Citation2019), where all financial service information is packaged into one package using an information technology platform (Lupikawaty & Andriyani, Citation2021), making financial services easier. Fast and accurate (Viceisza & Nakasone, Citation2020). Therefore, the quality of financial literacy programs triggers the use of FinTech platforms to become more intensive and the intelligence of the financial community to obtain information and decision-making processes to be effective so that access to micro-capitalization becomes stronger (Kou et al., Citation2021).

Social media in the community also contributes to disseminating information flows, both business information and non-business information (Lagna & Ravishankar, Citation2022). The role of social media that is flexible and has an extensive reach has been utilized as a media for marketing financial services products through the massive use of FinTech platforms (Al Syahrani et al., Citation2021), where the widespread use of FinTech platforms also provides support in socializing financial literacy for users. Financial services have become flexible, easy, and fast (Kuchciak & Wiktorowicz, Citation2021). The growing community of social media users can inspire financial institutions to be more creative and innovative in developing FinTech platforms (Tun-Pin et al., Citation2019). Therefore, in the unfavorable situation of the COVID-19 pandemic, social media has become a widely used platform for business management processes and management development processes (Azman et al., Citation2021). Strengthening the management aspect will certainly encourage the development of a more massive FinTech platform as an effort to provide more adequate financial services for users (Dang & Vu, Citation2020)

Various cases involving communities and institutions managing FinTech platforms show that public understanding is still inadequate regarding rights and obligations (Banding et al., Citation2020). moreover, many illegal FinTech platform managers still operate without following the regulations set by Financial Services Authority, Indonesia (Lestari et al., Citation2020). FinTech platforms aim to facilitate financial services for access to micro-capital (Goldstein et al., Citation2019), but people instead use them for consumptive needs. This often leads to payment failures that ultimately lead to legal disputes (Lestari et al., Citation2020), so FinTech is considered still not optimal in providing access to micro-capitalization for the SMEs sector (Dang & Vu, Citation2020). The empirical description shows that financial literacy and social media are very relevant phenomena to explain how to optimally manage FinTech platforms to improve financial services to the public and high-speed and easy access to micro-capital in the SMEs sector (Mention, Citation2021). Therefore, the FinTech platform must become an instrument for leveraging the SMEs sector’s revival in the ongoing COVID-19 pandemic (Azman et al., Citation2021).

Several previous studies showed the following results, Hamidah et al. (Citation2020); the results of this study are that financial literacy, financial technology, and intellectual capital have a positive and significant effect on the performance of MSMEs in Depok City. Nathan et al. (Citation2022) Perceived ease of use, usefulness, trust, brand image, government support, user innovativeness, and attitude are significantly correlated with FinTech adoption in Vietnam, while financial literacy was not significantly correlated with FinTech adoption. Indrawati (Citation2021) The finding that digital financial literacy significantly affects buying interest in financial technology products and financial behavior has no significant effect on buying interest. In financial technology products. Widyaningsih et al. (Citation2021) The research findings show the high level of financial literacy of the community and MSME actors and digital and financial technology literacy behaviors and attitudes, making it easier to promote the use of digital financial innovation products so that they can expand financial inclusion. It is proven that previous studies found research gaps; that is what makes this research conducted

2. Literature review

2.1. Financial literacy

Financial literacy is an educational program from financial service managers to provide a set of knowledge that can improve the skills of service users in making effective financial decisions through the use of available information sources (Kuchciak & Wiktorowicz, Citation2021). Financial literacy has become part of financial institutions’ marketing strategy by providing information and technology-based financial knowledge to the public. Burchi et al. (Citation2021) The finding show a positive and statistically significant relationship between financial literacy and sustainable entrepreneurial activity. Financial literacy aims to convey messages while at the same time influencing changes in the community using banking services which include: financial knowledge, financial skills, financial behavior, financial attitude, and financial performance (Purwanto & Anwar, Citation2022). Through financial literacy, the public has knowledge of banking service products and plans for funding needs according to their priority scale. Thus, the literacy program carried out by financial institutions will encourage the use of information technology platforms to become more massive so that financial services become more flexible, effective, and efficient through the FinTech platform. Furthermore, the speed and ease of accessing financial services have become part of the lifestyle and needs of the community in the industrial era 4.0. Therefore, financial service managers must be creative and innovative in developing FinTech platforms to encourage financial literacy programs and access to financial services.

Business actors in the Small and Medium Industry sector still do not have access to financial services with an adequate portion. A structured financial literacy program will certainly be able to increase financial knowledge for Small and Medium Industry sector players. The role of social media in people’s lives that continues to develop also encourages financial institutions to take advantage of this open space as a medium of communication and interaction with the community (Yoshino et al., Citation2020). Financial literacy programs educate the public about financial knowledge and are also used by managers of financial institutions to offer financial service products so that Small and Medium Industry sector players can access information directly. According to their needs. Therefore, the literacy program carried out on a massive scale can increase the ability of the Small and Medium Industry sector to recognize financial service products quickly, easily, and flexibly. This condition makes micro capital in this sector stronger (Kuchciak & Wiktorowicz, Citation2021).

Hamidah et al. (Citation2020) partially examined the influence of financial literacy, financial technology, and intellectual capital on MSME performance. In this study, it appears that both financial literacy and financial technology are independent variables. Likewise, research conducted by (Irman et al., Citation2021). Irman et al. (Citation2021) examined the variables of financial literacy and financial technology as for independent variables.

Meanwhile, Tun-Pin et al. (Citation2019) proved that financial literacy affects financial technology in their research. This research is supported by research conducted by Foster and Johansyah (Citation2021) examined the financial literacy variable as the independent variable and financial technology as the dependent variable. In other words, financial literacy is an independent variable, while financial technology is a dependent variable.

So, in the research conducted by Hamidah et al. (Citation2020) with the research conducted by Tun-Pin et al. (Citation2019) and by Foster and Johansyah (Citation2021), there was a research gap. The research gap makes this research more interesting. Namely, digging deeper into the influence of financial literacy on financial technology.

Based on this description, the following hypothesis is proposed:

H1: Financial Literacy affects financial technology in the Creative Industry Sector in East Java

H2: Financial Literacy affects micro-capital in the Creative Industry Sector in East Java

2.2. Social media

Social media is online media used by users to communicate, interact, participate, and share information easily by creating social network content and cyberspace without being limited by space and time. Social media has become part of people’s lifestyles in meeting the information needed to support their activities regarding self-actualization and making business decisions. Social Media that is used wisely can provide various financial literacy according to their needs, thus guiding MSME actors to make quick and appropriate decisions in fulfilling their business capital (Purwanto & Anwar, Citation2022). Thanks to social media, complex activities can be carried out easily, quickly, and effectively. Human dependence on social media encourages various parties to use it as a business medium (Abu Daqar et al., Citation2021) because it can become a network to communicate, interact, and participate effectively. FinTech is a social media platform developed by financial institutions to communicate with customers regarding product introduction services and sharing other important information. Therefore, the stronger role of social media in people’s lives will certainly strengthen the development of FinTech platforms by financial institutions. Kuchciak and Wiktorowicz (Citation2021) The empirical analysis was conducted using several data sources, including non-financial statements and a unique self-collected dataset that describes the specifics of the most popular social media platforms (like Facebook, Twitter, YouTube, Instagram, GoldenLine, and LinkedIn) in the activities of commercial and cooperative banks in Poland between 2010 and 2019. Abu Daqar et al. (Citation2021) Finding The smartphone penetration rate is 100% among both generations, while the financial inclusion ratio in Palestine is around 36.4%; these clear indicators are the main FinTech drivers to promote FinTech services in Palestine, and these are global indicators for FinTech adoption intention. Both generations (84%) intend to use e-wallet services; Millennials (87%) and Gen Z is (70%) prefer using real-time services.

In addition, the digitalization era has also accelerated the use of social media to become more intense. Thus, people have more and more options to seek new information and knowledge according to their needs. In business uncertainty during the COVID-19 pandemic, financial institutions have not yet opened access to micro-capital correctly. This situation then affects the behavior of the Small and Medium Industry sector to utilize social media massively to gain access to micro-capitalization. Thus, the development of social media in the digitalization era also affects creative and innovative behavior in gathering information wisely to support strengthening micro-capital for the Small and Medium Industry sector. Based on this description, the following hypotheses can be proposed:

H3: Social Media affects financial technology in the Creative Industry Sector in East Java

H4: Social media affects micro-capitalization in the Creative Industry Sector in East Java

2.3. Financial technology (FinTech)

FinTech is an innovation using an information-based technology platform developed by financial service institutions to create easy and fast financial services. FinTech that is developed in an integrated manner with marketing aspects can provide easy access to financial services for the public. The disseminating of information related to financial services can reach a wider space, and time is more flexible and faster. The massive growth of FinTech in the digitalization era has increased the demand for financial services with wider and more comprehensive coverage of service aspects (Lupikawaty & Andriyani, Citation2021) so that access to capital in the Small and Medium Industry sector becomes easier and faster. Al Syahrani et al. (Citation2021) The findings financial technology plays a crucial role in affecting transaction efficiency, financial achievement, and financial satisfaction. Financial Technology provides opportunities for MSME actors to access various information related to banking service products so that in the future, they can drive the growth of digital entrepreneurship in a structured and massive manner (Mardiana et al., Citation2020). Dang and Vu (Citation2020) In recent years, the application of FinTech in the microfinance sector has brought many good results, such as improving the quality of products and services, easy access to many customer groups, and scaling up the operating model. Abu Daqar et al. (Citation2021) The findings show that reliability/trust and ease of use are the main issues in using a financial service. Millennials are more aware (48%) of FinTech services than Gen Z (38%), which is different from the global view where Gen Z is the highest.

Therefore, FinTech, which was developed as a service medium by financial institutions, has now provided adequate access to select and meet micro-capitalization needs for the Small and Medium Industry sector. Tun-Pin et al. (Citation2019) There are six FinTech business models implemented by startup growth: payments, wealth management, crowdfunding, lending, capital markets, and insurance services (Lee & Shin, Citation2018). Lagna and Ravishankar (Citation2022) Financial technology (FinTech) is seen as possessing the significant potential to provide the poor access to financial services and help them escape the clutches of poverty

On the other hand, FinTech will grow well in the digitalization era because social media can provide adequate space to create creative and innovative behavior for financial institutions to develop financial services through information technology. Financial literacy programs designed according to digital marketing needs must contribute positively to the development of FinTech. Thus, strengthening literacy socialization can provide adequate educational value by disseminating fast and up-to-date information regarding services from financial institutions. Therefore, as a conceptual resource, FinTech must be able to become a medium that is easily accessible and utilized quickly and flexibly for the community to meet the needs of financial services, especially access to micro capital for the Small and Medium Industry sector (Banding et al., Citation2020) Based on this description, the following hypotheses can be proposed:

H5: Financial technology affects micro-capital in the Creative Industry Sector in East Java

2.4. Micro capital

Micro capital is business capital that does not exceed one billion rupiahs. The Small and Medium Industries Sector generally still has business capital that is far from ideal for supporting normal business activities, thus requiring access to capital support from financial institutions or other similar institutions (Al Syahrani et al., Citation2021). Access to capital in the Small and Medium Industry sector often faces difficulties meeting formal requirements when dealing with financial institutions. As a result, financial institutions also have difficulty meeting financing targets. On the other hand, social media has a strategic role in people’s lives, demanding easy, fast, and flexible services without being limited by space, place, and time. Financial institutions have used Social Media as a very effective marketing medium to support the needs and fulfill people’s lifestyles.

The literacy program is an integral part of the FinTech platform developed by financial institutions to improve financial services. FinTech allows the Small and Medium Industry sector to have many choices in making smart and fast decisions. Access to capital can be chosen according to the knowledge possessed through FinTech, which is increasingly complete and easily accessible. Therefore, the many FinTech platforms offered and social media also accelerate the spread of financial literacy to be more intensive and effective, thus taking advantage of the growth in access to micro capital to become stronger for the Small and Medium industries sector.

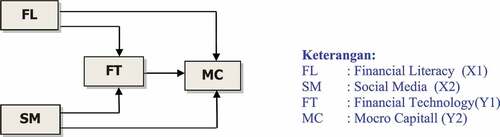

3. Research model

3.1. Analysis model

shows that the model can be expressed in the form of an equation as follows:

Figure 1. Model path analysis.

4. Research methodology

The population in this study was 376 SMEs in the industrial centers of East Java (Sidoarjo, Mojokerto, Surabaya, Pasuruan, and Gresik). The creative industry sector studied includes handicrafts, shoes, bags, wallets, suitcases, accessories, headscarves, Muslim clothing, delivery, and similar businesses.

The sample size is 65 respondents taken by stratified random sampling method. The sample criteria are SMEs actors and owners, active in business for at least ten years and still actively operating until the end of March 2021.

4.1. Variable operational definition

4.1.1. Research instruments

The data in this study were collected through a questionnaire instrument containing a list of questions that must be answered by creative industry business actors who meet the criteria as members of the population. As a research instrument, the questionnaire must meet the requirements of validity and reliability. This study uses the validity test of the Pearson product-moment correlation coefficient formula, and the reliability test uses Cronbach’s alpha. An instrument is declared valid if the correlation coefficient is positive and significant with the item-total correlation value greater than 0.30. The instrument is declared reliable if the value of Cronbach’s alpha is more significant than 0.6. lists the variable operational definition used in this study.

Table 1. Variable operational definition

5. Results

5.1. Validity and reliability

shows that the correlation coefficient of the four variables has an r-count value between 0.3436–0.8316, with a positive value greater than 0.30. Likewise, the Cronbach Alpha of the four variables has a value between 0.7324–0.8043, which is greater than 0.60. The correlation coefficient and Cronbach Alpha value indicate that the research instrument used to collect data from respondents is valid and reliable.

Table 2. Validity and reliability test results

5.2. Path analysis

The linearity test must refer to the parsimony concept, i.e., if all the models used as the basis for testing are significant, it means that the model is said to be linear or the linear function is substantial. The results of testing the linearity assumption for each influence between variables are presented in .

Table 3. Linearity assumption test results

shows that all forms of influence between variables in the structural model are linear. Thus, the assumption of linearity in the path analysis has been met.

5.3. Structural model

Path analysis uses standard regression values whose data is processed through Statistical Product and Service Solutions (SPSS) Version 22 software. The direct influence path coefficient test results are presented in .

Table 4. The summary of regression

Based on the results of testing the coefficients in and , the model in the form of path analysis can be expressed in the form of the following equation:

Table 5. Indirect effect path coefficient

6. Discussion

6.1. Financial literacy affects financial technology in the creative industry sector

Financial literacy has a weak effect on financial technology but is significant (coefficient 0.292, sig. 0.028). Although the influence is weak, financial technology will increase significantly if financial literacy increases. Therefore, efforts to educate the public on financial services and financial intelligence, as the main content in financial literacy, can be directed into menus available on the FinTech platform so that people can access them in an easy and fast way. Financial institutions focus on optimizing financial literacy programs to support the strengthening of financial services for the community in a very flexible, easy, and fast way. Therefore, the FinTech platform as a communication medium that is quite effective in the digitalization era can optimize its literacy program as a whole, complete and cannot be separated from the content of the developed FinTech platform. Literacy programs designed in a structured manner will certainly strengthen the content of the FinTech platform to be more adequate so that financial services for the community become easier, faster, and more accurate.

The existence of FinTech goes hand in hand with changes in people’s lifestyles, dominated by technology users information you want fast and practical. Problems in economic activities such as buying and selling, making payments, not having much time to look for ATM machines, or being reluctant to visit shopping centers can be overcome more effectively and efficiently. Increasing financial literacy in the community will lead to the emergence of Financial Technology that can provide breakthroughs for MSME actors. With FinTech, MSME players can find it easier to get information or use of various existing financial products.

The findings of this study: 1) there is a positive and significant direct effect of financial literacy on FinTech; 2) there is an indirect effect of financial literacy on micro-capital through FinTech, which is positive and significant.

6.2. Financial literacy affects micro-capital in the creative industry sector

Financial literacy has a weak direct effect on the role of micro capital but is significant, with a coefficient of 0.314 and a significant level of 0.041. This shows that microfinance literacy can still not educate the public about finance optimally. In the era of digitalization, microfinance literacy should play an important and strategic role in transforming financial knowledge in society because various media are available that can be used optimally. The community as actors in the creative industry sector has been established with their social media life, so it is appropriate that microfinance literacy is also integrated with the life of their social media existence. Community users of financial services will gain financial intelligence when financial institutions can provide services easily, completely, and accurately according to their needs. Ease of accessing the information on financial services will certainly strengthen the creative industry sector in meeting its capital requirements. Therefore, literacy as an introduction and education program for knowledge about financial intelligence for the community also accelerates the dissemination of financial service information. It provides many choices for the public to make smart, effective, and accurate financial decisions. Literacy programs with adequate financial content will certainly strengthen good knowledge in the learning process for the creative industry sector so that access to capital fulfillment will be better.

The findings in this study: 1) there is a positive and significant direct effect of financial literacy on micro capital; 2) there is an indirect effect of financial literacy on micro-capital through FinTech, which is positive and significant.

6.3. Social media has an effect on financial technology in the creative industry sector

Social media has a weak direct effect on financial technology but is significant (coefficient 0.326, sig. 0.043). This shows that the higher the social media presence, the higher the FinTech significantly. This social media can be used to develop FinTech platforms to be friendlier in providing better financial services. Small and Medium Enterprises (SMEs) who are in a new civilization and are accustomed to socializing on social media use this media as a place to find and get information as needed. Social Media makes financial services easily accessible without being hindered by space, time, and place. Therefore, as a very effective medium in the digitalization era, social media is optimized for developing an adequate FinTech platform so that FinTech as a financial service platform can provide optimal benefits for the community. Social media can build a better FinTech platform so that the offered FinTech can be a good friend and partner for the SMI sector.

The findings of this study: 1) there is a positive and significant direct influence of social media on FinTech; 2) there is an indirect effect of social media on micro capital through FinTech, which is positive and significant.

6.4. Social media has an effect on micro-capitalization in the creative industry sector

Social media has a weak effect on micro-capitalization but is significant (coefficient 0.323, sig. 0.037). This shows that the higher the social media, the higher the micro-capitalization. In the era of digitalization, financial institutions can optimally utilize social media to introduce financial services in a structured and massive manner so that the public can obtain an adequate supply of information to support smart decisions regarding the fulfillment of financial services. The creative industry sector actors who are already established with their social media lives are appropriate if social media is made part of the digital marketing aspect that is more friendly to the lives of the creative industry sector actors in the current digital era. Ease of accessing information on financial services will certainly strengthen the creative industry sector to meet capital needs.

It is natural that business actors currently take advantage of Social media and are very good at promoting their products or services. Media social media is a means of promotion. From promotions that have been done on social media, other social media users will begin to recognize or at least see and know what is on offer. Usually, the promotions carried out are packaged as attractively as possible to lure potential consumers into stopping at the sales booth, for example, using one of the social media, namely Instagram, which is very popular. The purpose of the promotion is to increase sales. The increase in sales will certainly affect the sustainability of a business.

Therefore, as part of fulfilling lifestyles in society, social media has transformed knowledge and financial intelligence for social media users through disseminating content and various financial service information. Social media also offers an alternative for the public to make creative and innovative financial decisions so that access to fulfillment and strengthening capital for the creative industry sector is getting better.

The findings of this study: 1) there is a positive and significant direct influence of social media on micro capital; 2) there is an indirect influence of the role of social media on micro capital through FinTech, which is positive and significant.

6.5. Financial technology affects micro-capitalization in the creative industry sector

Financial technology has a strong enough influence on micro capital and is significant (coefficient 0.418; sig. 0.039). This shows that the higher the financial technology, the higher the micro capitalization. The public’s response to FinTech as a financial service medium is quite good; this aligns with understanding financial service instruments obtained through literacy and information dissemination from various social media.

FinTech regulation today is a global demand for the financial industry. Currently, the problem faced by developed and developing countries like Indonesia is the same, namely how to develop FinTech. This means that the level-playing-field similarities between developed and developing countries should be an opportunity for developing countries to catch up with regulations. It is hoped that the growth of FinTech in Indonesia can develop well and safely in the future. In Indonesia, regulations regarding FinTech have been accommodated by the Financial Services Authority Regulation Number 77/POJK.01/2016 concerning Information Technology-Based Lending and Borrowing Services and Regulation Number 31/POJK.05/2016 concerning Pawnshops. This proves that the Government of Indonesia has taken the development of FinTech in Indonesia seriously. Regulations that accommodate, of course, will create legal certainty and a sense of security for investors and fund seekers. The rules issued by Bank Indonesia through Bank Indonesia Regulation Number 18/40/PBI/2016 concerning the Implementation of Payment Transaction Processing are made to support the implementation of FinTech and E-Commerce in Indonesia.

The SME sector in the digitalization era must be able to optimize the existence of FinTech to support its business activities through these various financial services. Therefore, the financial services available through the FinTech platform also offer a large selection of services that the public can access. However, this is still not running optimally, so a more patient maturation process is needed so that the strengthening of capital for the creative industry sector can grow and develop better.

The findings of this study: 1) there is a direct influence of FinTech on micro capital; 2) the existence of FinTech can become a significant mediation between financial literacy and social media on micro capital; in other words, FinTech has a positive and significant influence on financial literacy and social media on micro capital for the better

7. Conclusion

The first hypothesis, which states that financial literacy significantly affects financial technology, is accepted. Therefore, a well-run literacy program will certainly provide a strong impetus for the development of FinTech as a fast, easy, and accurate financial service medium.

The second hypothesis, which states that financial literacy significantly affects micro capitalization, is accepted. Therefore, the level of regularity in delivering financial literacy according to user needs also accelerates financial intelligence for the creative industry sector, so that the strengthening of micro capital is getting better.

The third hypothesis, which states that social media significantly affects financial technology, is accepted. Therefore, social media developed through active participation can open up flexible space and time, making financial technology provide better benefits.

The fourth hypothesis, which states that social media significantly affects micro-capitalization, is accepted. Therefore, social media that provides an open space to play an active role in disseminating information about the community’s needs will provide access to knowledge and more adequate financial services, thereby strengthening capital for the creative industry sector.

The fifth hypothesis, which states that financial technology has a significant effect on micro capital, is accepted. Therefore, financial technology, which is designed to provide easy access to the services offered, will certainly strengthen the creative industry sector’s capital.

8. Implications

Based on the conclusions of the research results, the implications of the research results can be stated as follows:

Financial literacy is a structured knowledge and information dissemination program to increase public awareness and understanding of various access services. If this can be used to make wise decisions regarding access to financial services, then the community and the creative industry sector can easily, quickly, and accurately gain access to services.

Social media is online media that fellow users use to communicate, interact, participate, and easily share information by creating social network content and cyberspace without being limited by space and time. If this can be managed and utilized wisely, financial Literacy and FinTech can be effective service mediums to improve financial services with easy, fast, and flexible access.

Financial Technology is the implementation of innovative results using information technology platforms developed by financial institutions to create effective and flexible services without being limited by space, time, and place. If this can be adequately developed in an integrated manner with social media, then all forms of financial services can be accessed easily, quickly, and effectively.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Abu Daqar, M. A. M., Arqawi, S., & Abu Karsh, S. (2021). Fintech in the eyes of millennials and generation Z (the financial behavior and Fintech perception) http://dx.doi.org/10.21511/bbs.15(3).2020.03, 15(3), 20–28.

- Al Syahrani, A. L., Sujianto, A. E., Latifah, N. A., & Sulaiman, S. H. (2021). Financial technology, transaction efficiency and financial satisfaction: the mediating role of financial achievement. Indonesian Economic Review, 1(1), 8–15 https://iconev.org/index.php/ier/article/view/2.

- Azman, N. H. N., Masron, T. A., & Ibrahim, H. (2021). The significance of Islamic social finance in stabilising income for Micro-Entrepreneurs during the covid-19 outbreak. Journal of Islamic Monetary Economics and Finance, 7(S1), 115–136 https://doi.org/10.21098/jimf.v7i0.1307.

- Banding, M. P., Ashar, A., Juliana, A., Azis, M. I., & Thresia, Y. (2020). Financial technology for smes capital problems with crowdfunding method. Media Ekonomi Dan Manajemen, 35(2), 150–163. https://doi.org/10.24856/mem.v35i2.1503

- Burchi, A., Włodarczyk, B., Szturo, M., & Martelli, D. (2021). The effects of financial literacy on sustainable entrepreneurship. Sustainability (Switzerland), 13(9), 1–21. https://doi.org/10.3390/su13095070

- Dang, T. T., & Vu, H. Q. (2020). Fintech in microfinance: A new direction for microfinance institutions in Vietnam. The Journal of Business Economics and Environmental Studies, 10(3), 13–22. https://doi.org/10.13106/jbees.2020.vol10.no3.13

- Foster, B., & Johansyah, M. D. (2021). Analysis of the effect of financial literacy, practicality, and consumer lifestyle on the use of chip-based electronic money using SEM. Sustainability, 14(1), 32. https://doi.org/10.3390/su14010032

- Gal, P., Nicoletti, G., von Rüden, C., Oecd, S. S., & Renault, T. (2019). Digitalization and productivity: In search of the holy grail-firm-level empirical evidence from European countries. International Productivity Monitor, 37, 39–71 https://ideas.repec.org/a/sls/ipmsls/v37y20192.html.

- Goldstein, I., Jiang, W., & Karolyi, G. A. (2019). To FinTech and beyond. The Review of Financial Studies, 32(5), 1647–1661. https://doi.org/10.1093/rfs/hhz025

- Hamidah, N., Prihatni, R., & Ulupui, I. G. K. A. (2020). The effect of financial literacy, fintech (financial technology) and intellectual capital on the performance of msmes in depok city, west java. Journal of Social Science, 1(4), 152–158. https://doi.org/10.46799/jsss.v1i4.53

- Indrawati, A. (2021). Digital financial literacy, and financial technology: Case studies of faculty of economics university 17 August 1945 Samarinda. DiE: Jurnal Ilmu Ekonomi Dan Manajemen, 12(1), 1–10. https://doi.org/10.30996/die.v12i1.5102

- Irman, M., Budiyanto, B., & Suwitho, S. (2021). Increasing financial inclusion through financial literacy and financial technology On MSMEs. International Journal of Economics Development Research (IJEDR), 2(2), 356–371. https://doi.org/10.37385/ijedr.v2i2.273

- Kou, G., Xu, Y., Peng, Y., Shen, F., Chen, Y., Chang, K., & Kou, S. (2021). Bankruptcy prediction for SMEs using transactional data and two-stage multiobjective feature selection. Decision Support Systems, 140, 113429. https://doi.org/10.1016/j.dss.2020.113429

- Kuchciak, I., & Wiktorowicz, J. (2021). Empowering financial education by banks—social media as a modern channel. Journal of Risk and Financial Management, 14(3), 118. https://doi.org/10.3390/jrfm14030118

- Lagna, A., & Ravishankar, M. N. (2022). Making the world a better place with fintech research. Information Systems Journal, 32(1), 61–102. https://doi.org/10.1111/isj.12333

- Lee, I., & Shin, Y. J. (2018). Fintech: Ecosystem, business models, investment decisions, and challenges. Business Horizons, 61(1), 35–46. https://doi.org/10.1016/j.bushor.2017.09.003

- Lestari, D., Darma, D. C., & Muliadi, M. (2020). Fintech and micro, small and medium enterprises development: Special reference to Indonesia. Entrepreneurship Review, 1(1), 1–9. https://doi.org/10.38157/entrepreneurship-review.v1i1.76

- Lupikawaty, N. R. E. M., & Andriyani, T. (2021). The effect of financial technology on financial inclusion smes in Palembang City https://doi.org/10.2991/ahsseh.k.210122.015. Proceedings of the 4th Forum in Research, Science, and Technology (FIRST-T3-20), 84-88

- Lusardi, A. (2019). Financial literacy and the need for financial education: Evidence and implications. Swiss Journal of Economics and Statistics, 155(1), 1–8. https://doi.org/10.1186/s41937-019-0027-5

- Mardiana, S. L., Faridatul, T., Herlindawati, D., & Mardiyana, L. O. (2020). The contribution of financial technology in increasing society’s financial inclusions in the industrial era 4.0. IOP Conference Series: Earth and Environmental Science, 485(1), 12136. https://doi.org/10.1088/1755-1315/485/1/012136

- Mention, A.-L. (2021). The age of FinTech: Implications for research, policy and practice. The Journal of FinTech, 1(1), 2050002. https://doi.org/10.1142/S2705109920500029

- Nathan, R. J., Setiawan, B., & Quynh, M. N. (2022). Fintech and financial health in Vietnam during the COVID-19 Pandemic: In-depth descriptive analysis. Journal of Risk and Financial Management, 15(3), 125. https://doi.org/10.3390/jrfm15030125

- Purwanto, E., & Anwar, M. (2022). Application of the edu finance model to improve financial literature in creative industry in Sidoarjo district. Jurnal Siasat Bisnis, 26(1), 57–69. https://doi.org/10.20885/jsb.vol26.iss1.art4

- Taghizadeh-Hesary, F., & Yoshino, N. (2020). Sustainable solutions for green financing and investment in renewable energy projects. Energies, 13(4), 788. https://doi.org/10.3390/en13040788

- Tun-Pin, C., Keng-Soon, W. C., Yen-San, Y., Pui-Yee, C., Hong-Leong, J. T., & Shwu-Shing, N. (2019). An adoption of fintech service in Malaysia. South East Asia Journal of Contemporary Business, 18(5), 134–147 https://seajbel.com/wp-content/uploads/2019/05/seajbel5-VOL18_241.pdf.

- Viceisza, A., & Nakasone, N. E. (2020). Understanding consumer take-up of fintech and its potential value https://fintech.morgan.edu/wp-content/uploads/Understanding-consumer-take-up-of-fintech-and-its-potential-value.pdf. The Fintech Center, November, 2-32

- Widyaningsih, D., Siswanto, E., & Zusrony, E. (2021). the role of financial literature through digital financial innovation on financial inclusion (case study of Msmes in Salatiga City). International Journal of Economics, Business and Accounting Research (IJEBAR), 5(4), 1301–1312 https://jurnal.stie-aas.ac.id/index.php/IJEBAR/article/view/3705.

- Yoshino, N., Morgan, P. J., & Long, T. Q. (2020). Financial literacy and fintech adoption in Japan. ADB Institute, March, 1-35. https://www.adb.org/sites/default/files/publication/574806/adbi-wp1095.pdf