?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study used monthly panel data for the period March 2020-April 2021 in analyzing the differences in the impact of the COVID-19 pandemic on price stability in the East Africa Community (EAC) region. We also sought to establish the effectiveness of the governments’ policy response measures in maintaining price stability. Estimates from the Pooled Mean Group (PMG) model revealed evidence of a long-run relationship between COVID-19 and the Consumer Price Index (CPI) in the EAC region. Secondly, COVID-19 significantly increased the CPI across the panel in the long run. In the short run, the impact was significant and positive for Kenya but negative for Rwanda and South Sudan. The question of whether government policy response measures were indeed effective in maintaining price stability posits a dilemma that is rather reminiscent of a paradoxical policy solution. On one hand, governments are concerned with the welfare of their citizens which was worsened by the inception of the pandemic, and thus roll out relief measures to help inject liquidity into businesses and households. Conversely, governments are also wary that their actions might actually increase the money supply and thus trigger inflation. Governments, therefore, need to step up their vaccination drive as this is critical in spearheading the economies’ re-opening and, thus, recovery in the long run. This is contrary to the long-term application of the relief measures. Further, governments within the region need to develop well-managed food reserves that can provide a cushion in the event of price fluctuations emanating from the effects of such economic shocks.

1. Introduction

The Coronavirus (COVID-19) disease is currently one of the most earnest challenges facing humanity in recent times. It has led to a global disruption in agricultural production and food supply chains with severe societal welfare implications (World Food Programme, Citation2020). Besides causing appalling crises in the health sector, there is evidence of the pandemic aggravating the plights of the vulnerable and the poor (Buheji et al., Citation2020; Dzigbede & Pathak, Citation2020; McKibbin & Fernando, Citation2021). This raises concerns about the policies and interventions required to sustain these economies in the short term as well as revamp them in the long run.

The pandemic has yielded an unprecedented shock on the demand and supply chains of commodities which have severely mired both domestic and global trade flows. In a move to contain the spread of the virus, lockdown measures were instituted by governments globally which restricted the mobility of people and commodities; further impeding trade flows and, thus, creating a negative supply shock through supply chain disruptions (Baldwin & Tomiura, Citation2020). On the demand side, the inception of the pandemic saw a substantial stockpiling of essential commodities i.e. food products and medical items which triggered a surge in demand for these valuable items (Kassa, Citation2020; Mold & Mveyange, Citation2020).

In times like this when aggregate supply and aggregate demand are restricted, price hikes are inevitable. This further reduces the value of money & purchasing power hence increasing the cost of production. Besides, inflationary tendencies are unavoidable and given that the duration of the pandemic is unknown, the inflation relationship may not fizzle out rapidly (Jelilov et al., Citation2020). Evidence from theory suggests that the injection of liquidity into the affected economies as policy response measures by governments to support the constrained firms and households may trigger an increase in the flow of money in the economy, thus, stimulating inflation (Fisher, Citation1911; Friedman, Citation1956; Keynes, Citation1936). This is further supported in empirical work (Banerjee et al., Citation2020; Blanchard, Citation2020) in response to the COVID-19 pandemic.

However, the impact of the pandemic on general commodity prices in the East African Community (EAC) region remains relatively unknown. This drives us to investigate the impact of the pandemic on price stability across selected countries within the EAC region. Our study will focus on 4 countries: Kenya, Uganda, Rwanda, and South Sudan.

According to Statista (Citation2022), the inflation rate in East Africa was estimated at 36.5% in 2021; a rise from the 26.8% recorded in 2020. It is important to note that inflationary pressures; if not taken care of, would further exacerbate the plights of the poor through an increase in the price of food and non-food items. It, thus, makes it expedient to implement policy interventions that help keep prices or inflation at sustainable levels. However, this may raise ambiguity due to the potential counteractive effects of the policy response measures on price stability; a dilemma that further motivates this study.

This study, therefore, sets out to test three key hypotheses by providing answers to the following research questions: First, did the COVID-19 pandemic trigger an increase in commodity prices in the selected East African Community (EAC) economies? Secondly, what is the degree of differences in the pandemic’s impact on price stability across the selected countries? And thirdly, how effective were the governments’ policy response measures towards enhancing price stability in the region?

Moreover, following the emergence of the pandemic, many works have been published mostly in descriptive form with much focus shifted on the socio-economic cost of the pandemic, its impact on poverty, and the health system (Ataguba, Citation2020; Buheji et al., Citation2020; Hurnik et al., Citation2020; Ozili, Citation2020). Though these focus areas are relevant in winning the war against the pandemic in the short run and ensuring quick recovery in the post-Covid period, sight cannot be taken off its impact on price levels. One notable study by Coulibaly (Citation2021) provides a concrete analysis of the impact of COVID-19 policy response measures on inflation and the associated spillover effects. This study, however, draws evidence on selected countries in the West African Economic and Monetary Union (WAEMU) and pays more attention to the governments’ policy response measures (fiscal) as opposed to the monetary policy measures. Further, the panel analysis is generalized and does not distinguish the country-specific effects of the pandemic on commodity prices.

We contribute to the literature in three ways: First, to the best of our knowledge, this is the first study to evaluate the impact of COVID-19 on price stability across a panel of countries in the EAC region; Secondly, we analyze the efficiency of the measures instituted by various governments toward ensuring price stability; Thirdly and more importantly, unlike in previous generalized panel studies, we employ the Pooled Mean Group (PMG)-Autoregressive Distributed Lag Model (ARDL) approach to assess the differences in the degree of impact of the pandemic on price stability and the efficiency of policy response measures towards ensuring price stability across the selected countries.

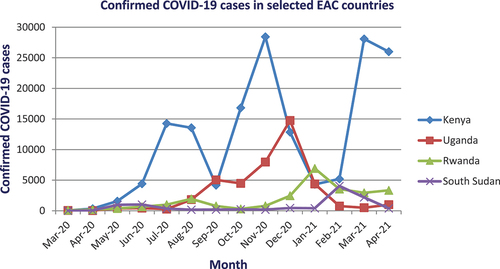

The pandemic has spread rapidly around the world since December 2019 when it was first reported in Wuhan, China. Disrupted global food chains (stemming from both domestic and international trade restrictions) coupled with massive job layoffs attempted at addressing many firms’ revenue losses implies that the effects of the pandemic would eventually squarely fall on prices. The International Food Policy Research Institute (IFPRI, Citation2020) noted that the pandemic has directly affected food prices as well as disrupted the normal flow of household incomes, thus, leading to increased food and nutritional insecurity around the world. shows the trend in the number of confirmed cases of the virus across the selected EAC countries for the period under study.

Figure 1. Number of confirmed COVID-19 cases (March 2020—April 2021).

reveals that among the selected economies in the East Africa Community (EAC) region, Kenya recorded the highest number of confirmed COVID-19 cases while South Sudan recorded the least over the same period. Governments globally instituted and implemented various tax, fiscal and monetary measures to help mitigate the effects brought about by the pandemic. Within the Eastern Africa region, the countries adopted several measures as highlighted in .

Table 1. Major country-specific fiscal/monetary government intervention measures

Understanding the impact of COVID-19 on commodity prices is critical in designing monetary/fiscal measures that are welfare-oriented and can cushion households from the devastating effects of the pandemic.

Further, to the above policy measures, the aforementioned countries rolled out COVID-19 re-financing mechanisms through financial assistance from either the World Bank or the IMF and the vaccination drive initiatives to help combat the disease. The Government of Kenya launched the National COVID-19 vaccination program in March 2021 initially targeting the frontline workers and the highly vulnerable groups. The vaccination commenced on 5th March with an initial 1.02 million doses of AstraZeneca’s vaccine provided through the COVAX pillar (Ministry of Health, Citation2021). A total of 4,482,179 total doses had been administered as of 15 October 2021 (Statista, Citation2021).

In South Sudan, the Vaccination drive commenced on 6 April 2021, with an initial 132,000 doses of AstraZeneca‘s vaccine provided through COVAX. However, a slow roll-out led to South Sudan returning 72,000 doses to COVAX and aimed at administering the remaining 60,000 doses before their expiry date. According to the statistics compiled by Statista (Citation2021), 115, 650; 4, 646, 977; and 2, 793, 657 vaccine doses had been administered in South Sudan, Rwanda, and Uganda respectively by 15 October 2021.

The vaccination drive is a continuous one and aims at targeting the entire population across all the EAC countries. The continuously mutating nature of the disease, however, implies that the road to recovery from the economic disruption caused by the pandemic might be a long and arduous one. The pandemic could yield long-term implications; something that calls for shock mitigation strategies in the event of a pandemic outbreak of this nature. Governments may, thus, need to rethink and re-orient their policy responses in the long-run direction.

Following the introduction, chapter two presents a review of the literature. Chapter three discusses the methodology and highlights the potential econometric issues that are likely to be encountered in this study. Chapter four presents the empirical findings while Chapter five provides conclusions and policy implications.

2. Literature review

Theories explaining the inflation phenomenon have evolved over the years beginning with the Classical school of thought proponents, followed by the Keynesians, and finally the Monetarists. The well-known classical macroeconomic theory that guides the classical theory of inflation was propounded by Fisher (Citation1911). According to this theory, the general price level of goods and services is directly proportional to the quantity of money stock circulating in the economy. The Keynesian theory formulated by Keynes (Citation1936), however, argues that inflation is not directly proportional to the money supply. Instead, inflation is driven largely by an increase in aggregate demand. According to the theory, it is an aggregate demand level above the full employment level of production that will stimulate inflation. The Monetary economists spearheaded by Friedman (Citation1956) support the old quantity theory of money pioneered by classical economists. Monetarism reiterates that an increase in the quantity of money circulating in the economy beyond the output growth rate yields inflation. In this regard, controlling inflation requires judicial application of monetary policies.

As observed by the IMF (Citation2021) and Deloitte (Citation2020), various governments in the EAC region undertook various policy measures ranging from fiscal to monetary in response to the COVID-19 pandemic to contain its spread as well as cushion its population from the dire effects. It, however, remains unknown as to whether the application of these policy instruments in the wake of economic shocks such as the COVID-19 pandemic will help in stabilizing prices in the economy.

Several empirical studies have been undertaken in an attempt to unlock this puzzle. In a systematic literature review, Ataguba (Citation2020) argues that containing the outbreak and its impact on the economy requires an increase in investment in the health system and the adoption of precautionary and traveling-restriction measures. It is, however, important to note that traveling-restriction measures generate an adverse impact on commodity prices through supply and demand chain disruptions. Further, as observed by Jelilov et al. (Citation2020), in crisis or pandemic times like this, where aggregate supply and aggregate demand are restricted, inflationary tendencies are unavoidable and given that the duration of the pandemic is unknown, the inflation relationship may not fizzle out rapidly.

To cushion households and businesses from the effects of the pandemic, governments within the EAC region instituted various tax relief measures that aimed at providing liquidity to the households and businesses to ensure that they survive and stay afloat. Nonetheless, Blanchard (Citation2020) notes that the injection of liquidity into the affected economies as policy response measures by governments to support the constrained firms and households may trigger an increase in the flow of money in the economy, thus, stimulating inflation. According to Hausmann (Citation2020), there are risks that in an effort to contain the spread of the COVID-19 disease, developing countries are more likely to experience inflationary pressures. As supported by IMF (Citation2020), the tendencies are very high of these countries to resort to monetary stimulus or seigniorage measures to finance their anti-COVID-19 measures.

According to Hurnik et al. (Citation2020), the COVID-19 global pandemic will continue to yield nontrivial consequences for the majority of the developing economies. Measuring its impacts on food security and prices, in general, could be quite challenging since its full effects are still yet to be fully visualized. However, as pointed out by Rahman et al. (Citation2020), the pandemic is already affecting food systems directly by impacting food supply and demand and indirectly by decreasing the purchasing power as well as the capacity to produce and distribute food. This could ultimately have far-reaching consequences on food prices and by extension on food security and nutrition, especially for the already vulnerable segment of the African population (World Bank, Citation2020).

Coulibaly (Citation2021) found the number of COVID-19 cases to significantly increase the Consumer Price Index (CPI) among West African Economic and Monetary Union (WAEMU) countries. The government policy response measures were, however, found to negatively influence CPI. Buheji et al. (Citation2020) revealed that it is hard for the poor to cope with strict Covid protocols of lockdown and social distancing as most are casual and informal sector workers depending on daily and hourly remunerations. The study calls for more specialized programs during future lockdowns for the poor.

Similarly, in a simulation study in Ghana, Dzigbede and Pathak (Citation2020) identified a significant direct association between the coronavirus pandemic and poverty measures over time using daily and monthly economic indicators and the latest Ghana Living Standards Survey (GLSS) data. The study, thus, suggested that an extension in government expenditure under a prevailing cash transfer program would help to reduce the economic shocks associated with the pandemic and subsequently, improve the livelihood of the poor and the vulnerable. However, Ozili (Citation2020) sounded some caution on how the government spends in an attempt to help the vulnerable and businesses during this period. The study showed that in Nigeria, the government’s recovery response by giving monetary assistance to businesses and some small households could not help significantly due to the extreme fear of contracting the disease.

In containing the COVID-19 outbreak and its impact on the economy, some studies have suggested an increase in investment in the health system and precautionary and traveling-restriction measures. For instance, using the OLS technique to estimate the effect of traveling records and contacts on the rate of coronavirus infections, Ogundokun et al. (Citation2020) postulated that governments should ensure that agencies invest in proper precautionary and Covid-safety measures. However, precautionary measures are also found to aggravate the devastating impact of the pandemic on livelihood and prices.

In assessing the impact of the pandemic on food trade among some selected commonwealth countries, Vickers et al. (Citation2020) revealed that lockdown measures culminated with temporary trade restrictions were found to have impacted food demand and pricing by causing an acute disruption in the global food supply chains. In their survey, the authors posit that a protracted pandemic could pose both short-run and medium-term impacts on food availability and eventually undermine the long-term food security of many countries. The distribution of the economic cost of COVID-19 has also been varied concerning income status, with higher income countries bearing more. Using the ARDL model, Erokhin and Gao (Citation2020) discovered that the pandemic’s impact on food insecurity was more noticeable in high-income economies than in low-income economies.

Ebrahimy et al. (Citation2020) globally analyzed the drivers and dynamics of inflation during the coronavirus pandemic by differentiating between the lockdown period which was noted for mobility restrictions, and the reopening phase period when mobility restrictions were lifted. The immediate proof from emerging markets and developed economies pointed to the increased price of food. However, no proof of inflation could be visualized when broader indexes were factored into their analysis. Albeit the time is short to assess the inflation trends following the economy reopening, inflation expectation measures do not reveal a palpable trend of upward inflationary moves. In the fresh phase of the outbreak of the coronavirus pandemic, the demand for pandemic-related goods such as preventive medications & household cleaning was observed to surge across all the surveyed regions namely South Africa, Brazil, Chile, China, Colombia, Mexico, and Russia. What is commonly noticeable across various countries, nevertheless, is a rise in the variance of expectations, probably suggesting a rise in uncertainty. These trends insinuate that those inflationary expectations have not demonstrated a clear-cut rise or fall trend since the beginning of the coronavirus pandemic.

From the reviewed literature, it is clear that the impact of COVID-19 on price stability in the Eastern Africa region has not been investigated. Most of the studies tend to focus more on the pandemic’s effect on health systems, food security, and nutrition. Besides, most of these studies are descriptive with no implicit model estimated. This study, thus, contributes to the literature by investigating the impact of the pandemic on price stability across four selected economies in the Eastern Africa region using a PMG-ARDL model. The study also explores the effects of the governments’ policy response measures towards enhancing price stability. Furthermore, we assess the differences in the degree of impact of COVID-19 on price stability across the selected countries; a feat that remains relatively unexplored.

3. Methodology

3.1. Theoretical model

This paper adopts the quantity theory of money in modeling CPI determinants with some modifications to control for market factors such as the exchange rate and interest rate. Following Fisher (Citation1911), a change in the price level can be expressed in a growth model. Fisher’s equation can be expressed as follows:

Given that V is assumed to be constant, change in the price level ( can be expressed in functional form as follows:

Where is the money supply,

is the velocity of money,

is the inflation rate, and

is the output. However, in open economies such as Eastern Africa where the trade balance is negative, the exchange rate plays a big role in determining the inflation rates. This study, therefore, controls for exchange rate fluctuation. COVID-19 pandemic acts as a shock to inflation and is our main variable in this study. In this regard, Equationequation (2)

(2)

(2) is rewritten as follows:

Where π is the inflation rate that will be proxied by CPI in our empirical model. M is the money supply, Y is the output, and COV represents the number of confirmed COVID-19 cases. is the nominal exchange rate. We use broad money supply (M2) in our empirical model to measure money supply.

3.2. Empirical model

The theoretical model derived above has been extended and modified empirically to assess the role of monetary policy in determining inflation. For instance, Adjei (Citation2018) employs an ARDL framework in modeling the determinants of inflation in Ghana while Diouf (Citation2007) uses general-to-specific modeling and cointegration techniques to analyze how consumer price inflation is determined in Mali along the monetarist, structural, and external theoretical specifications. Similarly, Ayubu (Citation2013) modeled the inflationary reaction to monetary policy in Tanzania using the Structural Vector Autoregressive (SVAR) model and the Vector Error Correction Model (VECM). On the contrary, the studies by Diop et al. (Citation2008) and Coulibaly (Citation2021) lend credence to the fiscal policy as opposed to the monetary policy actions as most important in explaining inflation in the WAEMU countries. Whereas the study by Diop et al. (Citation2008) uses the panel ARDL approach, that by Coulibaly (Citation2021) employs the panel fixed effects estimator.

Our study adopts the panel ARDL model developed by Pesaran et al. (Citation1999). We prefer this method over other panel estimation techniques and more particularly, the Generalized Method of Moments (GMM) approach due to three key reasons. First, panel ARDL is more suitable given our larger time dimension (T = 14) compared to the country-case dimension (N = 4). Conversely, the GMM approach is more applicable for short panels i.e. in panel cross-sectional data where T < N. In this case, one can simply estimate the levels equation directly (without first-differencing). Secondly, panel ARDL is more suitable in the case where our variables are integrated of order I (0) or I (1) or a combination of both. Further, it is preferred when the dependent variable is not stationary at levels. Third and more importantly, it is within the panel ARDL framework that we can visualize the differences in the degree of impact of the COVID-19 pandemic across the selected EAC countries. The approach entails including the lagged value of the regressand as a regressor to capture the inertia of inflation. To establish the technique to be used, whether the Mean Group (MG), Dynamic Fixed Estimator (DFE), or the Pooled Mean Group (PMG), we employ the Hausman (Citation1978) model specification test.

Following the above theoretical modeling, we specify the following model:

Where are the coefficients of lagged dependent variables,

are the

coefficients’ vector,

is inflation rate proxied by CPI &

is a

vector of regressors indicated in Equationequation (3)

(3)

(3) . The subscript

refers to the cross-sectional unit, i.e. country

refers to the time or study period. The term

allows for cross-sectional fixed effects &

is the error term. The terms

and

are the optimal lag orders. The re-parameterized ARDL model (p, q) -Error Correction Model (ECM) can be shown in Equationequation (5)

(5)

(5) as follows:

Where denotes the group-specific speed of adjustment coefficient (with the expectation that

and

is a vector of the long-run relationships. The Error Correction Term (ECT) is given by;

. Finally, the short-run dynamic coefficients are represented by

and

.

EquationEquation (5)(5)

(5) shows both the short-run coefficients (with difference operators) and the long-run coefficients (without difference operators). More precisely, the following model will be estimated:

Where CPI denotes the Consumer Price Index (proxy to the prices of commodities in the economy). M2 refers to the broad money supply, CBR denotes the Central Bank Rate, R denotes the average commercial banks’ lending rate, and TB represents trade balance (the difference between a country’s monthly exports and imports).

Just like in Equationequation (5)(5)

(5) , we can also re-parametrize Equationequation (6)

(6)

(6) in the spirit of an ARDL-ECM framework as follows:

Where Equationequation (7)(7)

(7) presents a summarized and simplified ARDL-ECM framework that captures the speed of adjustment term, the ECT component, the lag length, and both the short-run and long-run coefficients.

3.3. Descriptive statistics

3.3.1. Consumer price index ( )

)

An index that measures the changes in the price level of a weighted average market bundle of consumer commodities purchased by households. It’s expressed in a natural log. It’s our dependent variable and is used as a proxy for commodity prices in the economy.

3.3.2. COVID-19 confirmed cases (COV)

The number of confirmed cases in a country since the first case was reported (March 2020-April 2021). It’s expressed in a natural logarithm and is expected to influence CPI positively (Coulibaly, Citation2021).

3.3.3. Broad money supply (M2)

Includes all cash and coins in circulation, short-term bank deposits & money market short-term securities. M2 is expressed in the natural logarithm. M2 Money is expected to influence CPI positively. A higher quantity of money in circulation above the growth rate of real output increases the inflation rate since more money chases the same quantity of goods (Adjei, Citation2018; Fisher, Citation1911; Friedman, Citation1956).

3.3.4. Exchange rate (E)

The rate at which one country’s currency exchanges for another. This is recorded monthly and will be expressed in terms of the US dollar. The exchange rate variable is expressed in a natural log. A decline in the exchange rate (domestic currency appreciation) induces a fall in the domestic prices of commodities in an economy. Currency appreciation is, therefore, expected to be inversely related to CPI (Asekunowo, Citation2016; Diouf, Citation2007; Lim & Sek, Citation2015).

3.3.5. Central bank rate (CBR)

The rate at which commercial banks borrow from the Central bank. A higher CBR implies constrained credit to commercial banks and subsequently to its creditworthy clients. This reduces the money supply in the economy and consequently CPI.

3.3.6. Banks’ lending rate (R)

The rate at which the majority of the deposit money banks lend to their credit-worthy customers. It is measured in percentage form and recorded monthly. It’s expected to be negatively related to CPI since the higher cost of borrowing dampens the demand for commodities in the economy. This consequently lowers the prices of commodities hence lowering the inflation rate (Adjei, Citation2018; Mordi et al., Citation2007).

3.3.7. Trade balance (TB)

Measured as the difference between the total value of exports and imports of commodities in USD million and is recorded monthly. The trade balance is expressed in a natural logarithm. A positive trade balance (exports>imports) is expected to negatively impact inflation while a negative trade balance (exports<imports) is expected to positively impact inflation. Considering that imports are made in foreign currencies, the demand for foreign currencies generally rises and this yields a depreciation impact on the domestic currency. Therefore, the price of goods in relation to the domestic currency becomes expensive, thus, triggering inflation (Lim & Sek, Citation2015).

3.4. Summary statistics

This study presents summary statistics for the whole panel (group) as well as different statistics per panel. Country-specific statistics are fundamental in visualizing the limits and spread of variables for each country employed in this study.

3.4.1. General panel statistics

This is presented in .

Table 2. General panel statistics

The Consumer Price Index (CPI) across the four countries averaged 4134.55 points. The variable had a high standard deviation of 7078.39 around the mean value and varied in the intervals of between 107 and 18,863.10. On average, the number of confirmed COVID-19 cases across the four countries was 4022 monthly over the study period. Covid cases exhibited a dispersion of 6758.11 with a minimum of 0 and a maximum of 28,426 confirmed cases in a given month over the study period. Trade deficit across the panel exhibited a standard deviation of 266.28 and varied within the intervals of between 128.60 million USD and 1083.11 million USD. The average trade balance (trade deficit) across the countries in a given month in the COVID-19 period was about 419.16 million USD. This is worrying and signifies the growing trend in trade deficit across the EAC countries; a situation that might have escalated in the wake of the pandemic. A trade deficit implies overreliance on imports which in turn weakens a domestic country’s currency. Currency depreciation is in turn associated with increased CPI or inflation. The mean exchange rate over the period under study was 1236.33 and varied in the intervals of 103.74 and 3791.46 against the USD. The variable had a standard deviation of 1474.29 around the mean value. The broad money supply (M2) averaged about 9640.91 million USD monthly across the panel and exhibited a dispersion of 11,805.39. The lowest monthly recorded M2 money across the panel was 591.14 million USD with the highest value recorded at 30,663.40 million USD. The commercial banks’ lending rate averaged 15.63% with the lowest spread of 2.68. The lowest rate charged was 11.75% with the highest rate being 20.93%. The higher the lending rate, the more constrained access to credit is which in turn reduces the amount of money in circulation in an economy and subsequently the inflation rate. On the other hand, CBR averaged 7.96 across the panel with a spread of 3.31 around the mean value. The lowest CBR charged by Central banks to the money borrowed from them by the commercial banks was 4.5% with the highest being 15% over the period under study.

3.4.2. Country-specific panel statistics

To visualize the different statistics per panel, a comprehensive summary of statistics was also conducted for the four countries (see ).

3.5. Data sources

This study utilized monthly panel data for the period March 2020-April 2021 which covered four countries: Kenya, Rwanda, South Sudan, and Uganda. The first case of COVID-19 in East African Community (EAC) countries was reported in March 2020 hence the choice for this study period. The data on CPI, exchange rate, CBR, trade balance, M2 money, and Commercial Bank’s lending rate was obtained from country-specific Central Banks and the National Bureau of Statistics databases. The data on COVID-19 confirmed cases were sourced from WHO reports and country-specific ministries of health databases.

4. Empirical findings

4.1. Pre-Estimation tests

To obtain efficient and unbiased estimates, several pre-estimation tests were carried out.

4.1.1. Correlation analysis

Correlation analysis was conducted to ensure the absence of multicollinearity. The pairwise correlation matrix revealed a weak degree of correlation among the independent variables (see )

4.1.2. Panel unit root test

The panel unit root test was conducted to check for the order of integration of the variables. The panel ARDL model requires that the variables be integrated of order 0 or 1 or a combination of both. This study will adopt the IPS unit root test which assumes heterogeneous slopes across the panels (Im et al., Citation1997). The null hypothesis postulates that all panels contain unit roots while the alternative hypothesis states that some panels are stationary. If the probability value is less than the 0.05 level of significance, we reject the null hypothesis of non-stationarity. The unit root test results are presented in .

Table 3. Stationarity test results

From the stationarity test results (see, ), it was apparent that we estimate a panel ARDL model. The model requires that the variables should be integrated of order 0 or 1 or a combination of both. The optimal Lag length for each variable was determined using Schwarz’s Bayesian Information Criterion (SBIC). We adopted a lag selection of (1 0 0 0 0 0 0) which was common for each variable across the countries forming the panel.

4.1.3. Hausman model specification test

Hausman’s (Citation1978) test was carried out to determine the most suitable model to be estimated among the MG, DFE, and the PMG estimators. In choosing between the MG and PMG, the null hypothesis states that MG and PMG estimates are not significantly different; hence, PMG is more efficient. Similarly, in choosing between the DFE and PMG, the null hypothesis postulates that DFE and PMG estimates are not significantly different; hence, PMG is more efficient. Failing to reject the null hypothesis implies that we employ the PMG model. A chi2 (6) probability value of 0.241 was obtained in the MG vs PMG case while a chi2 (6) probability value of 0.427 was obtained in the DFE vs PMG case. In both model selection cases, the probability value of Chi2 was found to be higher than the 0.05 level of significance. We, thus, failed to reject the null hypothesis and concluded that the PMG was the most suitable estimator to be used in this study.

The PMG estimator proposed by Pesaran et al. (Citation1999) assumes the homogeneity of long-run coefficients and allows the intercepts, short-run coefficients, and error variances to differ freely across groups. It is, therefore, consistent and efficient under the assumption of long-run slope homogeneity. Besides, PMG is an intermediate estimator between the MG and DFE estimators. On the other hand, the MG estimator earlier proposed by Pesaran and Smith (Citation1995) provides consistent estimates of the mean of the long-run coefficients but these will be inefficient if the slope homogeneity holds. In other words, MG fails to recognize the fact that certain parameters may be the same across groups hence less informative compared to the PMG.

4.2. Estimation results

To analyze the impact of COVID-19 on price stability (proxied by CPI) among selected EAC countries, we estimated the full PMG model. The model also enabled us to analyze the degree of impact of COVID-19 on commodity prices across the EAC countries (see, for results).

Table 4. Pooled mean group (PMG) regression results-full model

The results in revealed that the ECT was negative and statistically significant for Kenya and Rwanda but insignificant for Uganda. For the case of Kenya, the model overcorrects itself while for the case of Rwanda, any deviations from the long-run equilibrium are corrected at an adjustment speed of 21.5%. On the other hand, a positive ECT for South Sudan suggests model explosion i.e. no convergence in the long run.

In the long run, we found that Covid cases, trade balance, broad money (M2), and Central Bank Rate (CBR) significantly increased the Consumer Price Index (CPI) at a 1% level of significance. First, we find that a 1% increase in the number of confirmed COVID-19 cases significantly increased the CPI by 0.006% ceteris paribus. The COVID-19 pandemic has led to a global disruption in agricultural production, food supply chains, and domestic & international trade due to mobility restrictions. These effects have affected food prices and disrupted the normal flow of household incomes. Further, due to restricted aggregate supply and demand, price hikes become inevitable, something that further reduces the value of money and purchasing power, thus, ultimately increasing the cost of production (Jelilov et al., Citation2020). The findings are also consistent with that by Coulibaly (Citation2021) who also found a significant and positive impact of COVID-19 on CPI among the WAEMU countries. Also, consistent with our expectations, the short-run estimates revealed that the pandemic significantly increased the CPI for Kenya. Contrary to our expectations, the pandemic led to a decline in commodity prices in the case of Rwanda and South Sudan. These findings are, however, supported by Hurnik et al. (Citation2020) who pointed out that due to the recency of the pandemic, measuring its impacts on food security and prices, in general, could be quite challenging given that its effects are still yet to be fully visualized.

Secondly, in the long run, we find that a 1% increase in trade deficit significantly increased the CPI by 0.17% ceteris paribus. The COVID-19 pandemic resulted in increased importation of commodities across the EAC countries such as Personal Protective Equipment (PPEs), oxygen ventilators, testing reagents, and even foodstuffs. Massive importation negatively impacts the strength of a country’s domestic currency as it leads to currency depreciation. This is eventually reflected through increased commodity prices for domestic food and non-food items. These findings are consistent with the studies by Lim and Sek (Citation2015) and Adjei (Citation2018) which also associate higher importation of commodities with increased inflationary pressures for developing economies. In the short run, however, the impact of the trade deficit on CPI was found to be significant and negative in the case of Kenya and South Sudan; a finding that contradicts the economic theory.

Thirdly, a 1% increase in M2 money significantly increased the CPI in the long run by 0.680% ceteris paribus. An increase in the quantity of money circulating in the economy results in to increase in commodity prices since too much money is chasing the same or even fewer quantity of commodities in an economy. As a result, money loses value. This argument has been widely supported in the theoretical and empirical literature (Adjei, Citation2018; Fisher, Citation1911; Friedman, Citation1956; Keynes, Citation1936). These findings are also corroborated in the short-run in the case of Rwanda and South Sudan but contradictory in the case of Kenya. It could, however, be argued that there was a gap between the time when the Kenyan government rolled out its tax relief measures (which aimed at injecting more liquidity into the economy) and the time when the benefits were realized by the targeted recipients. Considering our study period, this time gap justifies why the impact was negatively felt in the short-run but positively felt in the long run.

Fourth, we surprisingly find a positive and significant link between Central Bank Rate (CBR) and CPI in the long run. It is expected that a higher CBR will limit the amount of credit that commercial banks can obtain from the Central banks. Consequently, commercial banks will also have less credit to extend to their credit-worthy clients hence less money is expected to flow into the economy. In the short-run, however, CBR was found to be significantly and negatively associated with CPI in Kenya and Rwanda. This is consistent with our expectations and also supports the economic theory since a reduced CBR implies an increased amount of money that commercial banks can borrow from the Central Banks. This increases the commercial banks’ liquidity, thus, enabling them to lend out more to their credit-worthy customers hence increasing the money supply in an economy (Mordi et al., Citation2007). In an extended view, we also surprisingly find a positive and significant impact of the lending rate on CPI in South Sudan considering that a higher lending rate lowers the amount of money that can be potentially borrowed from the commercial banks by credit-worthy clients. This has the effect of reducing the quantity of money circulating in the economy hence lowering the inflation rates.

The exchange rate variable was found to be positively and significantly associated with CPI in the short-run in the case of South Sudan. Consistent with our expectations, an increase in the exchange rate (domestic currency depreciation) induces a rise in the domestic prices of commodities in an economy. These findings are also consistent with previous studies by Diouf (Citation2007), Lim and Sek (Citation2015), and Asekunowo (Citation2016). The effect was rather insignificant across the other countries both in the short-run and in the long-run.

Concerning the efficiency of the governments’ policy response measures, this study delved more into the monetary policy indicators (money supply, lending rate, and CBR) with their pass-through effects being witnessed through exchange rate fluctuations and trade balance. We note that most of the response measures, and more so the tax relief measures, were aimed at injecting more liquidity into the businesses/households. This generated a direct impact on the money supply with other effects equally being felt in the economies via the ripple effects on the other variables. Therefore, we conclude that expansionary monetary policy or fiscal policy; if not well controlled, can trigger inflation. This calls for a need for a coordinated and or controlled monetary or fiscal policy response in the wake of any pandemic or epidemic if we are to realize price stability in the long run. This study does acknowledge that the balancing act of cushioning the vulnerable population while at the same time maintaining price stability is indeed a daunting one and demands fiscal/monetary prudence to realize its effectiveness.

5. Conclusions

This study primarily sought to investigate the impact of the COVID-19 pandemic on price stability across some selected EAC countries. Specifically, the study also analyzed the degree of variation of this impact across the selected countries. The findings revealed that COVID-19 significantly increased CPI across the panel in the long run. In the short run, the impact was positive and significant for Kenya but negative and significant for the case of Rwanda and South Sudan. We, thus, concluded that the pandemic indeed increased commodity prices across all the selected countries at least in the long run.

The question of whether government policy response measures were indeed effective in maintaining price stability posits a dilemma that is rather reminiscent of a paradoxical policy solution. On one hand, governments are concerned with the welfare of their citizens which was worsened by the inception of the pandemic and thus roll out relief measures to help inject liquidity into businesses and households. On the other hand, governments are also wary that their actions might actually increase the money supply and thus trigger inflation in the economy. This calls for a need for a coordinated and or controlled monetary or fiscal policy response in the wake of any pandemic or epidemic if we are to realize price stability in the long run.

There is also a need for governments to rethink and re-orient their policy responses in the long-run direction. This stems from the fact that most of the governments’ policy response measures, and more particularly, the tax relief measures, increased the stock of money in circulation in the economy which in turn triggered the increase in commodity prices. Therefore, more implicit policies that are geared toward the creation of more job opportunities are indeed critical in spearheading the recovery process in the long run. This is in contrast to the long-term application of the relief measures and takes cognizance of the fact that the disease is continuously mutating which renders the road to recovery from the economic disruption caused by it to be a long and arduous one.

More concretely, governments within the EAC region should develop well-managed food reserves as well as shock management kitties that can cushion their citizens from the price fluctuations that emanate from the effects of economic shocks of this nature. It is also integral that governments step up their vaccination drive initiatives; a feat that will then guarantee safe and gradual economies’ re-opening for the full resumption of economic activities in the region.

Finally, future studies should attempt a differentiated analysis of COVID-19 impact on both food & non-food inflation since this impact may vary substantially across different commodities based on the degree of severity of the lockdown measures. This study is limited by the fact that governments’ across the EAC region adopted a wide range of policy response measures that could not be uniformly integrated into our estimated models for all the selected countries. However, our study indicators captured a majority of the major measurable policy instruments whose effectiveness on commodity prices can be visualized.

Acknowledgements

To the anonymous reviewers for their insightful contributions to this Article.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Adjei, S. K. (2018). Inflation determinants - Milton Friedman’s theory and the evidence from Ghana, 1965-2012 (using ARDL framework). International Journal of Applied Economics, Finance, and Accounting, 3(1), 21–21. https://doi.org/10.33094/8.2017.2018.31.21.36

- Asekunowo, V. O. (2016). The causes of persistent inflation in Nigeria. CBN Journal of Applied Statistics, 7(2), 49–75. http://hdl.handle.net/10419/191688.

- Ataguba, J. E. (2020). COVID 19 pandemic, a war to be won: understanding its economic implications for Africa. Applied Health Economics and Health Policy, 18(3), 325–328. https://doi.org/10.1007/s40258-020-00580-x

- Ayubu, V. S. (2013). Monetary policy and inflation dynamics. An empirical case study of Tanzanian economy. Sweden Press.

- Baldwin, R., & Tomiura, E. (2020). Thinking ahead about the trade impact of COVID-19. In R. Baldwin & B. W. Di Mauro (Eds.), Economics in the Time of COVID-19 (pp. 59–72). Centre for Economic Policy Research (CEPR.

- Banerjee, R., Mehrotra, A., & Zampolli, F. (2020). Inflation at risk from covid‐19. Bank for International Settlements Bulletin, No. 28.

- Blanchard, O. (2020). Is there deflation or inflation in our future? VoxUE. Accessed April 24, 2020. https://voxeu.org/article/there-deflation-or-inflation-our-future

- Buheji, M., Cunha, K. C., Beka, G., Mavric, B., Carmo de Souza, Y. L., Silva, S. S. C., Hanafi, M., & Yein, T. C. (2020). The extent of COVID-19 pandemic socio-economic impact on global poverty. A global integrative multidisciplinary review. American Journal of Economics, 10(4), 213–224. https://doi.org/10.5923/j.economics.20201004.02

- Coulibaly, S. (2021). COVID-19 policy responses, inflation and spillover effects in the West African economic and monetary union. African Development Review, 33(S1), S139–S151. https://doi.org/10.1111/1467-8268.12527

- Deloitte. (2020). Economic impact of the Covid-19 pandemic on East African economies. Accessed May 2020. https://www.google.com/search?client=firefoxd&q=Deloitte+%282020%29.+Economic+impact+of+the+Covid-19+pandemic+on+East+African+economies

- Diop, A., Dufrenot, G., & Sanon, G. (2008). Long‐run determinants of inflation in WAEMU. In A. M. Gulde & C. Tsangarides (Eds.), The CFA franc zone: Common currency, uncommon challenges (pp. 54–76). IMF.

- Diouf, A. M. (2007). Modeling inflation for Mali. IMF Working Paper, WP/07/295. Washington D.C.: IMF.

- Dzigbede, K. D., & Pathak, R. (2020). COVID-19 economic shocks and fiscal policy options for Ghana. Journal of Public Budgeting, Accounting & Financial Management, 32(5), 903–917. https://doi.org/10.1108/JPBAFM-07-2020-0127

- Ebrahimy, E., Igan, D., & Peria, S. M. (2020). The impact of covid-19 on inflation: potential drivers and dynamics. In Research special notes series on covid-19. Washington, D.C.: International Monetary Fund (IMF).

- Erokhin, V., & Gao, T. (2020). Impacts of COVID-19 on trade and economic aspects of food security: Evidence from 45 developing countries. International Journal of Environmental Research and Public Health, 17(16), 5775–5803. http://dx.doi.org/10.3390/ijerph17165775

- Fisher, I. (1911). The purchasing power of money. MacMillan.

- Friedman, M. (1956). The quantity theory of money-a restatement. In M. Friedman (Ed.), Studies in the quantity theory of money. Chicago: University of Chicago Press. p. 3-21.

- Hausman, J. A. (1978). Specification tests in econometrics. Econometrica, 46(6), 1251–1271. https://doi.org/10.2307/1913827

- Hausmann, R. (2020). Flattening the COVID‐19 curve in developing countries. Project Syndicate.

- Hurnik, J., Kober, C., Plotikov, S., & Vavra, D. (2020). Socio-economic impact analysis of COVID-19. OG Research. Accessed August 2020. https://www.unicef.org/ethiopia/reports/socio-economic-impactanalysis-covid-19

- IFPRI. (2020). Coronavirus and the implications for food systems and policy. International Food Policy Research Institute. https://www.ifpri.org/news-release/coronavirus-and-implications-food-systems-and-policy-agrilinks

- Im, K. S., Pesaran, M. H., & Shin, Y. (1997). Testing for unit roots in heterogeneous panels. Mimeo, Department of Applied Economics, University of Cambridge.

- IMF. (2020). World economic outlook: The great lockdown. International Monetary Fund.

- IMF. (2021). Policy Responses to COVID-19. International Monetary Fund. Accessed May 6, 2021. https://www.imf.org/en/Topics/imf-and-covid19/Policy-Responses-to-COVID-19

- Jelilov, G., Iorember, P. T., Usman, O., & Yua, P. M. (2020). Testing the nexus between stock market returns and inflation in Nigeria: Does the effect of COVID-19 pandemic matter? Journal of Public Affairs, 20(4), 1–9. https://doi.org/10.1002/pa.2289

- JHU-CSSE. (2021). Coronavirus (COVID-19) statistics data. New cases and deaths. Center for Systems Science and Engineering.

- Kassa, W. (2020). COVID-19 and trade in SSA: impacts and policy response (issue 1, No. 1). World Bank.

- Keynes, J. M. (1936). The general theory of employment, interest, and money. Macmillan.

- Lim, Y. C., & Sek, S. K. (2015). An examination on the determinants of inflation. Journal of Economics, Business and Management, 3(7), 678–682. https://doi.org/10.7763/JOEBM.2015.V3.265

- McKibbin, W., & Fernando, R. (2021). The global macroeconomic impacts of COVID-19: Seven scenarios. Asian Economic Papers. https://doi.org/10.1162/asep_a_00796.

- Ministry of Health (2021). Updates on covid-19 vaccination exercise. https://www.health.go.ke/wp-content/uploads/2021/10/MINISTRY-OF-HEALTH-KENYA-COVID-19-IMMUNIZATION-STATUS-REPORT-30TH-SEPT-2021.pdf

- Mold, A., & Mveyange, A. (2020). The Impact of the COVID-19 crisis on trade: Recent evidence from East Africa. Brookings Institution.

- Mordi, C. N. O., Essien, E. A., Adenuga, A. O., Omanukwue, P. N., Ononugbo, M. C., Oguntade, A. A., Abeng, M. O., & Ajao, O. M. (2007). The dynamics of inflation in Nigeria. Main report: Occasional Paper No. 2. Research and Statistics Department. Central Bank of Nigeria.

- Ogundokun, R. O., Lukman, A. F., Kibria, G. B., Awotunde, J. B., & Aladeitan, B. B. (2020). Predictive modeling of COVID-19 confirmed cases in Nigeria. Infectious Disease Modelling, 5, 543–548. https://doi.org/10.1016/j.idm.2020.08.003

- Ozili, P. K. (2020). COVID-19 pandemic and economic crisis: The Nigerian experience and structural causes. Journal of Economic and Administrative Science, ahead-of-print(ahead-of-print). https://doi.org/10.1108/JEAS-05-2020-0074

- Pesaran, M. H., & Smith, R. P. (1995). Estimating long-run relationships from dynamic heterogeneous panels. Journal of Econometrics, 68(1), 79–113. https://doi.org/10.1016/0304-4076(94)01644-F

- Pesaran, M. H., Shin, Y., & Smith, P. R. (1999). Pooled mean group estimation of dynamic heterogeneous panels. Journal of the American Statistical Association, 94(446), 621–634. https://doi.org/10.2307/2670182

- Rahman, S., Hossain, I., Mullick, A. R., & Khan, M. H. (2020). Food security and the coronavirus disease 2019 (COVID-19): A systemic review. Journal of Medical Science and Clinical Research, 8(5), 180–184. https://dx.doi.org/10.18535/jmscr/v8i5.34

- Statista. (2021). Cumulative number of COVID-19 vaccination doses in East Africa 2021, by country. Accessed October 18, 2021. https://www.statista.com/statistics/1238313/cumulative-number-of-covid-19-vaccination-doses-in-east-africa-by-country/

- Statista. (2022). Inflation rate in East Africa from 2020 to 2023. Accessed May 16, 2022. https://www.statista.com/statistics/1175327/impact-of-covid-19-on-projected-inflation-in-east-africa/#:~:text=The%20inflation%20rate%20in%20East,an%20increase%20in%20energy%20inflation

- Vickers, B., Ali, S., Zhuawu, C., Zimmermann, A., Attaallah, H., & Dervisholli, E. (2020). Impacts of the COVID-19 pandemic on food trade in the commonwealth. International Trade Working Paper 2020/15. London: Commonwealth and FAO.

- World Bank. (2020). Global Economic Prospects, June 2020.: https://openknowledge.worldbank.org/handle/10986/33748

- World Food Programme. (2020). COVID-19 economic and food security implications in East Africa. Accessed March 28, 2020. https://reliefweb.int/report/south-sudan/covid-19-economic-and-food-security-implications-east-africa-release-10-28-march

Appendix

Table A1. Different statistics per panel

Table A2. Pairwise correlation matrix