?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study aims to explore the asymmetric relationships between global oil prices and the selected Vietnam macroeconomic indicators using both quantile-on-quantile regression and Granger causality in quantile frameworks. The macroeconomic factors under study, as expected, have a strong relationship with oil price changes. The results suggest that oil prices have a positive impact on the exchange rate, inflation, GDP, and stock market prices across major quantiles, while there is a significantly negative relationship between the unemployment rate and oil prices in the middle-upper quantile. The results of this article offer considerable policy implications for governments, investors, and policymakers.

PUBLIC INTEREST STATEMENT

The purpose of this article is to investigate the impact of oil price shocks on macroeconomic indicators in Vietnam. This study aims to highlight the importance of global oil prices in creating conditions for economic development. This article has significant implications for the government, investors, and policymakers.

1. Introduction

Since the 1990s, economists have been interested in empirical works that suggests a relationship between a country’s macroeconomic performance and oil price shocks (Omolade et al., Citation2019). This was prompted by a growing reliance on oil imports, unprecedented disruptions in the international oil market, and a lack of macroeconomic stability in many countries. Oil price shocks were thus clear to economic agents as a driver of variations in macroeconomic aggregates. Therefore, a massive amount of empirical research with theoretical underpinnings has been conducted to investigate the impact of oil price shocks on macroeconomic fundamentals (Choi et al., Citation2018). These studies show that, even though the effects of oil price shocks on macroeconomic aggregates are the same across countries, the transmission routes are very different because of their different economic structures, energy intensity, and whether they are importing or exporting countries. As a result, the causal associations between macroeconomic factors and oil prices need to be examined in the context of developing countries (Tiwari et al., Citation2022).

The impact of oil and energy prices on macroeconomic variables has received much attention in academic and policy circles. According to Hamilton (Citation1983) and Hamilton (Citation2003), the transmission mechanisms of oil price shocks reveal that an oil-importing country’s macroeconomic performance will deteriorate during periods of high oil prices. An increase in the price of oil leads to higher inflation expectations and unemployment in developing and advanced economies, regardless of the type of shock (Geiger & Scharler, Citation2019; Baek, Citation2021; Tiwari et al., Citation2022; Dramani & Frimpong, Citation2020; Agu & Nyatanga, Citation2020; Choi et al., Citation2018; Ordóez et al. Citation2019; Tien & Hung, Citation2022). High oil prices may also erode the country’s competitiveness in the export of raw materials and intermediate goods (Nonejad, Citation2020; Sharma & Shrivastava, Citation2021; Sheng et al., Citation2020), as well as depreciate the local currency against the US dollar (Känzig, Citation2021; Yildirim & Arifli, Citation2021; Zulfigarov & Neuenkirch, Citation2020). Against this background, the current study contributes to the research on the relationship between oil prices and macroeconomic determinants in Vietnam.

Given the negative influence of increasing oil prices on the economy, policymakers have been working hard to strengthen energy security in order to provide a lower cost and more reliable energy supply. Policymakers have been concentrating their efforts on diversifying the supply of oil and energy for economies that rely on imported energy. As a result, policy proposals emphasize the need to increase renewable energy supply, as nonrenewable energy use causes major business cycle variations and downturns. Not only can energy price shocks have a negative impact on economic growth, but many nations with a strong reliance on imports are particularly vulnerable to energy price volatility (Ordóñez, Monfort, Cuestas et al., Citation2019). Oil prices can change quickly, which makes it hard to predict how much oil prices will be in the future. This uncertainty affects economic activity and how people respond to uncertainty (Punzi, Citation2019).

A lot of recent studies are directly related to our research (Baek, Citation2021; Dramani & Frimpong, Citation2020; Khalfaoui et al., Citation2020; Khraief et al., Citation2021; Sharma & Shrivastava, Citation2021; Yildirim & Arifli, Citation2021; Yıldız et al., Citation2021). Nevertheless, we address two flaws in this research in this paper. Firstly, they merely take into account the correlation between oil prices and single macroeconomic variables (Agu & Nyatanga, Citation2020; Choi et al., Citation2018; Zakaria, Khiam, Mahmood et al., Citation2021). On the other hand, we depart from this approach and investigate the correlation between oil prices and a number of macroeconomic variables, as detailed in the present study, which assists us in providing a broader perspective on those issues. While prior studies, such as Bjørnland et al. (Citation2018) and Sheng et al. (Citation2020), have primarily concentrated on developed countries, we analyze the case of a developing country, Vietnam, which is extremely important when it comes to oil demand growth. As far as we know, this is the first study to look at causal associations between these series for emerging markets over different quantiles of the distributions. This study also makes a new methodological contribution in the form of quantile-on-quantile regression (QQR) and Granger causality in different quantiles, which can be used to look at how oil prices and certain macroeconomic variables move together.

Oil demand has risen in Vietnam over time, highlighting the necessity to look into the impact of oil prices on the country’s macroeconomics. For various reasons, the effect of oil prices on the Vietnamese macroeconomy is crucial. To begin with, Vietnam has witnessed rapid economic expansion in recent decades, which has resulted in increased oil consumption (Suu et al., Citation2021; T. T. Ho & Ho, Citation2018). Second, because Vietnam is a net oil importer, its economy is susceptible to fluctuations in oil prices. Third, because the Vietnamese monetary authorities want low inflation and stable growth, it is critical to analyze the impact of oil prices on the macroeconomy (T. L. Ho & Ho, Citation2021). Finally, because Vietnam has not saved oil and has no oil replacements, the country’s economy has been severely impacted by the rise in oil prices. Examining the oil price-macroeconomy nexus is thus crucial from various policy viewpoints. It will aid in the adoption of an appropriate monetary policy to keep inflation under control in the face of high oil prices.

It should also be noted that some scholars argue that in order to understand the impacts of crude oil price shocks in other markets, it is necessary to understand the source of such shocks (Umar et al., Citation2022, Citation2021b, Citation2021a). Umar et al. (Citation2021c) contend that changes in crude oil prices would have a different impact on the financial markets studied depending on the source of the structural break. As a result, we represent oil price conditions by various quantile levels by selecting quantiles in terms of the low, middle, and high quantiles, which represent bearish, normal, and bullish market conditions, respectively. In other words, the quantile regression analysis enables us to investigate the impact of economic indicator fluctuations under different oil price conditions.

The study adds to the existing literature in the following ways: By evaluating the causation and dependence between these variables across quantiles for Vietnam, we re-evaluate the link between crude oil prices and macroeconomic indicators. We choose the QQR and nonparametric causality-in-quantile approaches for this purpose because they are resistant to misspecification errors, structural breaks, and frequent outliers, all of which are typical in economic time series (Shahzad et al., Citation2019). Put it in other way, we employ the most recent and novel QQR methodology developed by Sim and Zhou (Citation2015) to investigate the interplay between oil prices and key macroeconomic indicators in Vietnam. The main reason for using this innovative approach is its advanced ability to combine both quantile regression and nonparametric approaches (S. H. Hashmi et al., Citation2021). Therefore, it enables us to capture the asymmetric impact of oil price quantiles on macroeconomic quantiles, which is not possible with traditional time series econometric methods (Hung, Citation2021a). The QQR approach demonstrates the asymmetric influence of the independent variable on the dependent variable across various quantiles. Such in-depth estimates give a comprehensive analysis to assess the cross-dependence between macroeconomic indicator quantiles and those of oil prices. The fact that these two variables behave differently across places and time has policy consequences. More specifically, we used Granger causality in different quantiles developed by Troster et al. (Citation2018) to capture causal associations between the two variables. This method synchronizes with the QQR methodology and determines the causality linkage between oil prices and the selected macroeconomic factors at the median, lower, and upper tails of the distribution. The empirical findings derived from this asymmetric causality in the quantile test support and validate the QQR results.

The remainder of this paper is organized as follows: In Section 2, we review the related literature. Section 3 summarizes the related literature. Section 4 reports the empirical results. Section 5 provides the conclusion and implications.

2. Literature review

Several past studies have explored the linkages between oil prices and significant economic activities, namely inflation (Choi et al., Citation2018; Hung, Citation2020; Tiwari et al., Citation2021; Wu & Ni, Citation2011; Zakaria, Khiam, Mahmood et al., Citation2021), unemployment rate (Doğrul & Soytas, Citation2010; Ewing & Thompson, Citation2007; Kocaarslan et al., Citation2020; Ordóñez, Monfort, Cuestas et al., Citation2019), exchange rate (Khraief et al., Citation2021), stock market prices (Alamgir & Amin, Citation2021; S. H. Hashmi et al., Citation2021; Jiang & Liu, Citation2021; N.T. Hung, Citation2022; Nguyen, Citation2021; Umar et al., Citation2022, Citation2021b, Citation2021c, Citation2021a) and economic growth (Sheng et al., Citation2020; Ahmed et al., Citation2019; Zulfigarov & Neuenkirch, Citation2020; Khan et al. Citation2021Alvarado et al., Citation2018; Teng et al., Citation2021, Citation2021; Islam et al., Citation2021; Zakari et al., Citation2021; Godil et al., Citation2022; Cao et al., Citation2021; Khan et al. Citation2021; Muhammad & Khan, Citation2021; Dagar et al., Citation2021; Zhang et al., Citation2021; Khan et al., Citation2019; Muhammad & Khan, Citation2021; Zia et al., Citation2021).

Bjørnland et al. (Citation2018) look into the relationships between macroeconomic variables and oil price volatility in the US. They find that oil price shocks are recurrent sources of economic fluctuations. Omolade et al. (Citation2019) examine the impact of crude oil price shocks on the macroeconomic performance of Africa’s oil-producing countries. The findings unveil that the reaction of output to sharp increases and decreases in oil prices differs. Sheng et al. (Citation2020) reveal that both oil supply and demand shocks are crucial drivers of uncertainty. Their findings also provide evidence that the influence of oil price shocks on macroeconomic uncertainty is regime-dependent and contingent on the state of investor sentiments and perceived volatility in financial markets.

Gupta and Krishnamurti (Citation2018) shed light on how oil prices influence corporate risk-taking and report that with rising oil prices, firms increase risk-taking if the macroeconomic outlook is favorable. Ahmed et al. (Citation2019) look into the influence of oil price volatility on macroeconomic indicators for SAARC countries. Using the same SVAR, the authors confirm the long-run equilibrium association between the two variables. The macroeconomy is sensitive to oil price shocks and possesses different socio-economic implications in the region. Nonejad (Citation2020) documents that economic uncertainty and variables in connection with crude oil production provide information about the future state of the economy and forecast crude oil price fluctuations.

In a recent study, Yildirim and Arifli (Citation2021) focus on the Azerbaijani economy and suggest that a negative oil price shock deteriorates the trade balance, causes currency depreciation, increases inflation, and lowers economic activity. Similarly, Zulfigarov and Neuenkirch (Citation2020) employ VAR models to investigate the nexus between oil prices and economic activity in Azerbaijan. Their outcomes indicate that GDP effects are mainly seen after oil price rises, while the interest rate and the exchange rate mainly react to decreases. Känzig (Citation2021) explores how variations in oil supply expectations impact the oil price and the macroeconomy. He confirms that negative news results in an immediate increase in oil prices, a gradual fall in oil production, and an increase in inventories. Yıldız et al. (Citation2021) reveal no significant impact from supply and demand shocks to the oil prices in the short run. In addition, monetary policy shocks have no immediate effect on output, and demand shocks have no persistent influence on GDP in South Africa. Baek (Citation2021) examines the impact of oil price fluctuations on inflation, exchange rates, and GDP in Indonesia using the SVAR model. He says that a rise in oil prices boosts GDP and makes the Indonesian currency more valuable, but it has a negative effect on inflation. In a similar fashion, Tiwari et al. (Citation2022) employ wavelet analysis to examine the time-frequency relationship between oil prices and macroeconomic factors of emerging market economies. They report a strong relationship between oil prices and individual elements of macroeconomic factors at higher frequencies in these countries. In Ghana, Dramani and Frimpong (Citation2020) use the SVAR model to investigate the effects of specified shocks on macroeconomic aggregates and three bilateral exchange rates. The findings show that shocks to oil supply and demand considerably impact real GDP. Furthermore, the detected shocks significantly impact the bilateral exchange rate between Ghana and the Euro.

In India, Sharma and Shrivastava (Citation2021) study the interaction between oil prices and economic activity using the VECM model and Granger causality test. They show that oil prices have a short-term causal relationship with the unemployment rate, industrial output, GDP, the exchange rate, and stock market prices, but a long-term relationship with inflation. Authors also indicate a negative nexus between oil prices and industrial output, inflation, unemployment, and exchange rates, and a positive nexus with GDP and stock prices. In the same vein, Khalfaoui et al. (Citation2020) use the wavelet framework and suggest the presence of either a unidirectional or a bidirectional causal relationship between money demand and the underlining oil and macroeconomic variables in this nation. Only long-run asymmetric impacts of oil prices on exchange rates are suggested by Khraief et al. (Citation2021) for China and India. Nevertheless, after time-series noise is removed, the asymmetric long-run effect for India becomes symmetric.

According to Amiri et al. (Citation2021), oil price shocks combined with increased oil revenues result in a broadening of the monetary base, which leads to more liquidity and higher inflation rates. Oil prices are also rising, making Iran less competitive in the global market. Pham and Sala (Citation2020) use the SVAR model to investigate the macroeconomic implications of an oil price shock in Vietnam. According to the authors, when real exchange rates and the pace of exports are modeled, the impact of these shocks is greater than when real effective exchange rates and the trade balance are modeled. Through macroeconomic channels, Wei et al. (Citation2019) show that the oil futures market has considerable direct and indirect effects on the Chinese stock market. According to Geiger and Scharler (Citation2019), in response to shocks that result in higher oil prices, survey-based measures of inflation and unemployment expectations rise, while revisions in unemployment expectations are less pronounced in response to oil-specific demand shocks and global business cycle shocks, according to Geiger and Scharler (Citation2019).

According to Agu and Nyatanga (Citation2020), oil price volatility has a positive and statistically significant effect on poverty rates both in the short and long run. The results of the estimation also demonstrate that interest rates and GDP growth have a statistically significant and favorable impact on Nigeria’s poverty rate. Choi et al. (Citation2018) use an unbalanced panel of 72 advanced and developing economies to investigate the influence of global oil price changes on domestic inflation. They find that the effect is asymmetric, with positive oil price shocks having a higher impact than negative ones. Zakaria, Khiam, Mahmood et al. (Citation2021) examine the impact of global oil prices on inflation rates in South Asian countries, concluding that oil prices and inflation in the region are cointegrated. Ahmed et al. (Citation2019) investigate the impact of oil price shocks on unemployment in an oil-importing country like Spain to see if they affect unemployment differently in times of financial distress, and they find that unemployment’s response to oil shocks is clearly different in the pre-crisis period compared to the crisis period.

Even though there are several research studies on the oil-macroeconomic variables nexus in the literature, most of them are limited to studying the link for developed nations only (Pham & Sala, Citation2020). To our knowledge, the QQR technique has been completely overlooked in analyzing the macroeconomy and oil prices in Vietnam. As a result, we want to fill in this gap in the literature by looking at oil price shocks and macroeconomic indicators in Vietnam on our own.

3. Methodology

We use the following techniques in our research: To evaluate if the quantiles of the distribution follow a unit root process, Koenker and Xiao (Citation2004) devised the quantile autoregression unit root test. We employ the cointegration test introduced by Xiao (Citation2009) to test the null hypothesis of constant cointegrating coefficients after the null hypothesis of a unit root is not rejected. After that, QQR was employed to investigate the relationship between the variables under consideration. Finally, we utilize Granger-causality in quantiles proposed by Troster et al.’s (Citation2018).

The quantile-on-quantile regression is a more advanced version of traditional quantile regression. This method is robust and is best suited for investigating non-linear distributions of asymmetrical variables that produce robust estimates while assuming the prime distribution of data (Akadiri et al., Citation2022; S. H. Hashmi et al., Citation2021). Sim and Zhou (Citation2015) stated that this approach produces more inclusive results than traditional quantile regression. Put differently, this model is in contrast to the quantile regression approach introduced by Koenker and Bassett (Citation1978), and can be viewed as an addition to the basic simple linear regression model, providing a more comprehensive description of the relationships between variables (Akadiri et al., Citation2022; Hung et al., Citation2022).

4. The quantile-on-quantile approach (QQR)

Because quantiles can depict asymmetry between high and low distributions, the QQR approach appears appropriate to bearish relationship between oil prices (OIL) and other selected macroeconomic variables (X). Look at this link below:

where and

denote the oil prices and other selected indicators at period

,

is the

quantile of the conditional distribution of

and

is the error quantile whose

conditional quantile is made-up to be zero, and

illustrates slope of this nexus.

We can extend Equationequation (1)(1)

(1) by a first order Taylor expansion of a quantile of

as follows:

where presents the partial derivative of

, indicative of a marginal impact as the slope. It is obvious that

is the functional form of

and

while

is the functional form of X and

, hence

and

are functional form of

and

. If we present

and

by

and

, respectively, then we have

If we replace (2) into fundamental QQR Equationequation (1)(1)

(1) , we have

where (*) provides the conditional quantile of of macroeconomic factors. A similar minimization is used to arrive at equation as in ordinary least squares (OLS).

where is the quantile loss function demonstrating as

and

is the kernel density function and h represents kernel density function bandwidth parameter. As per Sim and Zhou (Citation2015), we chose

bandwidth of density function for optimal parameters of QQR framework.

5. Granger-causality in quantiles

A series Zt does not Granger-cause another series Yt, according to Granger, if past Zt does not help forecast future Yt given past Yt. Assume that It ≡ (,

)′

, d = s + q is an explanatory vector, and

is the historical information set of

. From Zt to Yt, the null hypothesis of Granger non-causality is:

where is the

given

conditional distribution function.

In this case, does not Granger cause

in mean if

The means of and

are

and

, respectively. If

is the τ -quantile of

, then (7) can be rewritten as follows:

where Ʈ is a compact set such that Ʈ ⊂ [0,1] is satisfied, and ‘s conditional τ -quantiles satisfy the following constraints:

Pr a.s. for all

6. Data

We use time series values spanning 20 years, from 1999 to 2020, to investigate the effects of oil prices on the Vietnamese economy. The period chosen is solely determined by data availability. The domestic indicators are unemployment, economic growth (GDP per capita), exchange rate, CPI inflation, and VNI stock exchange, which are collected from different sources (The World Bank, Datastream). The macroeconomic variables used in our empirical analysis are inspired by previous research, such as Sharma and Shrivastava (Citation2021). The data on crude oil prices have been obtained from Datastream. We code the indicators as follows: crude oil prices in US dollars (OIL), economic growth (GDP), unemployment rate (UR), exchange rate (EX), inflation (CPI), and stock market prices (VNI). To increase the number of observations, the annual series is then converted into monthly frequency using a widely used interpolation technique, the quadratic match-sum method, following Shahbaz et al. (Citation2018), Hung (Citation2021a). Every single variable that is being looked at in this study is changed to a logarithmic form to get rid of heteroscedasticity issues.

reports the descriptive statistics for the examined variables in Vietnam over the sample period. The mean values for OIL, EX, VNI, and GDP are positive, while this figure is negative for the cases of CPI and UR in this country. The exchange rate has the highest mean value (7.326929), which ranges from 7.056498 to 7.567891. The standard deviation coefficients indicate that the CPI fluctuated considerately (0.965100), followed by the VNI (0.670498) and OIL (0.490173). This suggests that CPI, VNI, and OIL are the most volatile among all variables. With respect to skewness, all variables have negative skewness values while GDP has positive skewness, which indicates the mean is less than the median and the series are negatively skewed. More so, CPI and VNI are leptokurtic, while others have kurtosis less than 3, suggesting platykurtic distributions. In addition, the results of the Jarque-Bera test are statistically significant, which means that all of the variables that were looked at are not normally distributed.

Table 1. Descriptive statistics

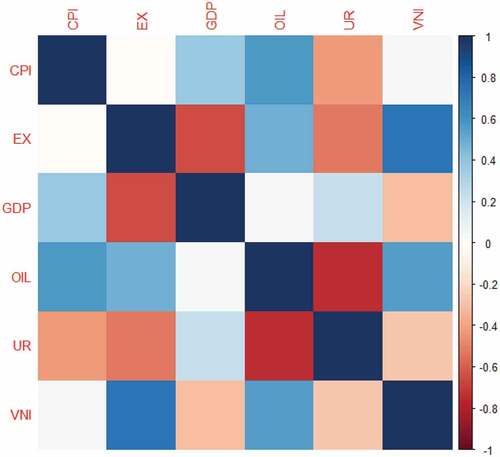

shows a first look at the standard relationship between oil prices, exchange rate, inflation, unemployment rate, GDP, and stock market prices in Vietnam. There is evidence of a strong connection between the examined indicators. Precisely, the heatmap plot demonstrates the direction among CPI, EX with OIL showing a positive trend, the UR, and VNI with OIL showing a negative trend.

Figure 1. Pearson correlation matrix for OIL, EX, CPI, UR, GDP and VNI in Vietnam.

7. Results and discussions

7.1. Quantile unit root and quantile cointegration results

Before carrying out the QQR and Granger Causality approaches, analysis begins with the quantile unit root test to remove possible biased outcomes and have a more robust inference to scrutinize the stationarity characteristics of the examined variables (Çıtak et al., Citation2021; Koenker and Xiao, Citation2004). The quantile unit root test model is preferred over the traditional ADF and PP tests as the data does not have a normal distribution (Shahbaz et al., Citation2018).

The outcomes of quantile unit root test are documented in . In this article we utilize 19 sub-quantiles spanning from . The estimated t-statistics value is compared to the critical values (CV) to identify the existence of the quantile unit root. The null hypothesis of H0 =

cannot be rejected at the 5% level of significance for each quantile if the estimated t-statistics value is smaller than CV. If the estimated t-statistics value is bigger than CV, however,

in various quantiles is assumed. The findings of the quantile unit root test indicate that OIL, VNI, EX, UR and CPI are nonstationary at a 5% level of significance for all quantiles of the conditional distribution. On the other hand, we observe that GDP is level stationary at quantiles from 0.2th to 0.65th. Overall, the remaining values of this indicator and other series show non-stationary behavior at high levels. The quantile cointegration analysis proposed by Xiao (Citation2009) was used to correct the fact that the cointegration linkage between oil prices and macroeconomic factors is over the quantile distribution. In other words, we implement it to evaluate the long-term relationship properties between the indicators.

Table 2. Quantile autoregression unit root analysis

reports the findings of the quantile cointegration for each pair of oil and macroeconomic variables in Vietnam. It represents the supremum norm value of the coefficients of β and γ and CV1, CV5, and CV10 are the critical values of statistical significance at 1%, 5%, and 10%, respectively. The given supremum norm value and coefficients are likewise bigger than all critical values at 1%, 5%, and 10% levels of significance, implying a significant non-linear long-run association between oil prices and macroeconomic factors in this country. As a result, this study moves to estimate the quantile on the quantile regression trend with coefficients.

Table 3. Quantile cointegration test

7.2. Findings of quantile-on-quantile regression

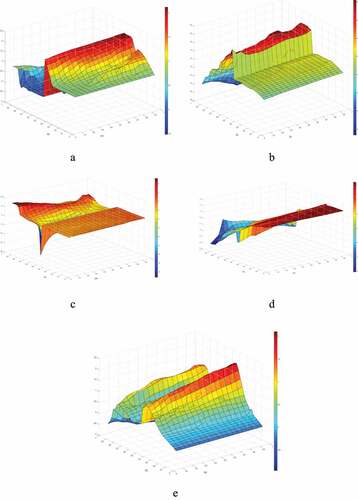

Following the illustration of a long-run cointegrating association between oil prices and macroeconomic determinants, this study used the quantile-on-quantile regression (QQR) approach developed by Sim and Zhou (Citation2015) to explore the impact of oil prices on the exchange rate, inflation, GDP, unemployment rate, and stock market prices in Vietnam from 1999 to 2020. Three-dimensional graphs depict the slope coefficients of the QQR. The findings of the QQR are reported in . These plots uncover the coefficient of slope estimates,, which determines the impact of the

quantile of oil prices on the

quantile of macroeconomic factors, at dissimilar values of

and

for Vietnam.

Figure 2. (a) The impact of oil prices on inflation. (b) The impact of oil prices on exchange rate. (c) The impact of oil prices on economic growth. (d) The impact of oil prices on unemployment rate. (e) The impact of oil prices on stock market prices.

The oil impact on CPI in Vietnam is described in ). The coefficient of the slope ranges from −0.5 to 2. In the lower (0.1–0.4) and middle tail (0.5–0.7) of OIL and all quantiles of CPI, the effect of OIL is strong and positive. Nevertheless, in the higher tail (0.75–0.95) of OIL and lower quantiles of CPI, the impact of OIL is weak and negative. Overall, in all quantiles, the impact of oil prices on inflation in Vietnam is significantly positive, which suggests that in all quantiles, an upsurge in inflation is caused by an upsurge in oil prices, which is consistent with Zakaria, Khiam, Mahmood et al. (Citation2021). These findings support the notion that Vietnam’s reliance on imported oil has increased in recent decades, causing inflation to be linked to global oil prices. By raising interest rates and reducing investment, a contractionary monetary policy can harm long-term output. This is because rising oil prices make it more expensive for people to buy things like food and clothes.

Similarly, ) discloses the influence of oil prices on the exchange rate in Vietnam. The coefficient of slope ranges between −4 and 8. In the lower and middle quantiles of OIL (0.1–0.7) and all different quantiles of EX, the influence of OIL on EX is strong and positive. However, at the higher quantiles of OIL (0.7–0.9) and lower quantiles of CPI (0.1–0.4), the value of the slope coefficient is weak and negative. In general, the findings show that strong and positive effects exist between oil prices and the exchange rate in Vietnam. Therefore, oil prices are a dramatic driver of the Vietnamese exchange rate. This outcome contradicts existing studies such as Pham and Sala (Citation2020), Wei et al. (Citation2019), and Geiger and Scharler (Citation2019), which indicate that oil prices are a significant factor in the exchange rate. The positive nexus between oil prices and the exchange rate indicates that when real oil prices rise in different market conditions, the real exchange rate tends to depreciate. This result is in line with Zulfigarov and Neuenkirch (Citation2020) and Känzig (Citation2021), reflecting that an increase in oil prices results in a depreciation in the exchange rate.

For the pair of OIL-GDP, as shown in ), the overall influence of oil prices on economic growth is both positive and negative. Oil prices have a strong positive impact on GDP at the higher quantiles (0.8–0.95), while this effect is less strong at the lower and initial quantiles of oil prices. On another surface of the plot, it is evident that oil prices negatively influence GDP at middle quantiles (0.5–0.65). Nevertheless, this negative influence gets weaker at the higher quantiles for both variables. These results demonstrate that both negative and positive impacts exist between oil and GDP in Vietnam. As a result, OIL contributes to an increase in economic growth in the low and higher tails, which indicates that a surge in OIL increases economic development in the lower and higher tails. On the other hand, in the middle quantiles, an increase in GDP is caused by a decrease in oil prices. The dispersion hypothesis, which states that frictions in reallocating factors of production across sectors exacerbate the negative effect of price fluctuations, is the leading explanation for this situation. One of the immediate consequences of an increase in oil prices is a decrease in demand for fuel-inefficient vehicles. Because labor and capital are immobile in the short run, factors of production cannot freely move from the fuel-inefficient automobile industry to other sectors (Hamilton, Citation2005). Following a sudden drop in demand, workers and capital in this sector of the economy may be idle for an extended period of time. This could result in a significant decrease in output.

The effect of oil prices on the unemployment rate in Vietnam is documented in ). The scale of the coefficient of slope ranges from −4 to 2. The influence of OIL on UR is negative at the middle and higher quantiles of OIL and most quantiles of UR. However, the impact of OIL on UR is positive and strong in the initial quantiles (0.1–0.3) of OIL and all quantiles of UR as indicated by the slope coefficient. Obviously, oil prices do not impact unemployment directly, but it depends on how that influence translates into other macroeconomic factors. The rise in oil prices will alert the economy to potential increases in production costs, and businesses will have to operate against shrinking profits and extremes in expectations. We discover that an increase in oil prices leads to an increase in unemployment. This reflects the deterioration of economic conditions in the manufacturing sector and, possibly, its economic ramifications. Moreover, crude oil prices are negatively correlated with unemployment cycles. The positive association between rising oil prices and employment could be attributed to complementarities and substitutability among various labor market sectors. This outcome is noteworthy considering the research on oil price shocks and the labor market.

In ), the nexus between oil prices and stock market prices is dominantly positive, as shown by an overwhelming yellow color throughout the graph, with only a few exceptions where the blue and light blue colors are present. The relationship between the initial lower quantiles (0.1–0.2) of OIL and the lowermost to uppermost quantiles (0.1–0.95) of VNI is presented in light blue, suggesting a weak negative correlation. Similarly, this is true for the uppermost quantiles (0.8–0.95) of OIL. However, the rest of the quantiles of both the indicators are linked positively, as indicated by the yellow and red colors. To sum it up, oil prices affected stock market prices positively and this association is asymmetric during different market states, which implies that higher oil prices promote stock market prices in Vietnam. These results are consistent with the findings of multiple studies which have uncovered the asymmetric hedging characteristics of oil prices (Khalfaoui et al., Citation2020; Khraief et al., Citation2021; Sharma & Shrivastava, Citation2021).

This tendency for stocks to move in lockstep with global oil prices is completely unexpected, especially in oil-importing countries like Vietnam. One possible reason for this tendency in the same direction, according to Alamgir and Amin (Citation2021), is that both oil and stock prices react to variations in global aggregate demand, a collection of common underlying causes. On the one hand, lowering aggregate demand would reduce oil demand, putting downward pressure on the price of oil. A softening in aggregate demand, on the other hand, will affect corporate profit, causing the stock price to fall.

7.3. Findings of Granger causality in quantiles

The Granger causality in quantiles developed by Troster et al. (Citation2018) is also utilized in this article. shows the Granger causality results and contains the p-values of the test for the examined variables. The test is administered over equivalent grids of 19 quantiles (0.05, 0.10, and 0.95). The findings disclose that oil prices, exchange rates, unemployment rates, economic growth, and stock market prices have bidirectional causal relationships at a 10% significance level in most quantiles. Nevertheless, in the pair of OIL-CPI, there is unidirectional causality from oil prices to inflation in the quantile (0.75), except for the rest of the quantiles of both OIL and CPI. Therefore, oil prices affected the macroeconomic factors in Vietnam during the period shown. Overall, the findings show that oil prices react to macroeconomic factors statistically at all the different levels of the time series.

Table 4. Granger causality in quantile test results

Depending on the stage of economic activity, economic operators and market participants react differently to oil price dynamics and macroeconomic trends. In this regard, compared to linear analysis, which considers asymmetric interactions between variables, it may provide a better understanding of the relationship between oil prices and macroeconomic indices. As a result, in this work, we employed the QQR model to look into the asymmetric effect of oil prices on macroeconomic parameters in Vietnam. Our key findings indicate that the variables of interest have a nonlinear connection.

Consistent with Bjørnland et al. (Citation2018) and Sheng et al. (Citation2020), our results document that crude oil has a significant impact on macroeconomic determinants. Our findings support Gupta and Krishnamurti (Citation2018) and Nonejad (Citation2020) results that oil price volatility strongly impacts the main macroeconomic factors. Similar, results have been documented for Azerbaijan (Zulfigarov & Neuenkirch, Citation2020), for South Africa (Yıldız et al., Citation2021). Finally, some of these results are in line with Sharma and Shrivastava (Citation2021), Khalfaoui et al. (Citation2020), Khraief et al. (Citation2021), Amiri et al. (Citation2021), and Geiger and Scharler (Citation2019) because oil price shocks would mainly impact economic activity.

7.4. Robustness check

The current study employs the QQR model to scrutinize the quantile of oil prices on macroeconomic factors at discrete values of corresponding quantiles. The traditional quantile regression is used to validate the research results of the QQR model. shows the quantile regression and OLS estimates of the slope coefficient that measure the effect of oil prices on macroeconomic fundamentals in Vietnam.

Table 5. QRA estimates of oil prices and other indicators

It is clear from the table that all pairs are statistically significant except for the pairs of OIL-VNI and OIL-GDP, which show some quantile levels. Specifically, the influence of all pairs is positive at all quantiles except for significant negative coefficients for the OIL-UR pair. The quantile regression coefficients of the middle quantiles are greater than those of the lower and upper quantiles, indicating a strong relationship between macroeconomic indicators. These findings back up the OLS estimate. As a general rule, results from traditional regression and causality Granger are usually close to each other in different distribution parts.

8. Conclusions and implications

The present article employs a newly developed econometrics approach to look into the causal associations between oil prices and macroeconomic determinants in Vietnam using data from 1999 to 2020. Using quantile on quantile regression and causality Granger in quantile tests, this study makes several contributions to the existing literature and policy implications on the nexus between oil prices, inflation, exchange rate, unemployment rate, economic growth, and stock market prices. Unlike traditional techniques, quantile-on-quantile regression and Granger causality in quantile tests assist us in approximating how the quantiles of independent indicators affect the quantiles of the dependent indicators, therefore providing a more detailed explanation of the overall dependency structure between the examined variables. To the best of the author’s knowledge, no prior study has explored these relationships using the novel QQR and Granger causality in different quantiles methods. The results suggest that oil prices have a positive impact on the exchange rate, inflation, GDP, and stock market prices across major quantiles, while there is a significantly negative relationship between the unemployment rate and oil prices in the middle-upper quantile. Moreover, the quantile regression is used as a robustness test, and the results comply with the QQR findings.

Overall, oil price fluctuation deteriorates macroeconomic activity in Vietnam. This sensitivity stems from the Vietnamese economy’s weak fundamentals, such as its significant reliance on oil and lack of diversification. Our findings, combined with different quantile properties, explore the significance of policy formulation to enhance the country’s resilience to negative oil price innovations. Within this work, Vietnamese governments should prioritize export diversification by developing policies that encourage investment in non-oil sectors such as manufacturing, tourism, agriculture, and mining and entice foreign direct investment (FDI) into these industries. Monetary policy framework modernization may also improve the economy’s resilience. Adopting a modern framework for monetary policy, such as inflation targeting with floating exchange rates, can improve the country’s external competitiveness, make it easier to diversify, and make it more resilient by giving the exchange rate more flexibility.

An asymmetric influence of oil price innovations on the exchange rate has been established from a policy standpoint, reflecting the influence of both negative and positive real oil price shocks on the exchange rate. This means that the long-run depreciation of the Vietnamese VND against the USD occurs predominantly due to the asymmetric effects of oil price volatility. We propose that the central bank be given more veto power in order to intervene effectively in the foreign exchange rate market while dealing with domestic currency fluctuations. In addition, our findings also uncover a remarkable relationship between oil prices and the stock market, which has significant contributions to financial economics, as policymakers should take note.

Initiatives to improve the efficiency of the stock market will boost the Vietnamese economy’s economic activity. For instance, they can remove legal and regulatory barriers to stock market development, develop the country’s infrastructure, strengthen the stock market’s capacity, and restore market participants’ trust in this country. Finally, increased oil prices lead to increased unemployment, which has vital implications for policymakers. Policymakers can reduce oil price uncertainty to lessen the negative impact of rising oil prices, which will help to reduce unemployment. In the long run, more energy security and diversification away from oil may make the labor market less sensitive to changes in oil prices.

The current study offers new avenues for future research. For example, the data could be divided into different time periods to determine whether the oil price pass-through effect varies over time. Additional research could be done to see how changes in oil prices affect macroeconomic factors in developed and developing economies. The supply and demand effects of the pass-through could also be investigated further. To put it another way, we believe it will be a worthwhile topic for future research to see if the empirical results will be similar after considering robustness concerns in relevant empirical studies for other countries.

Acknowledgements

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply. This research is funded by University of Finance-Marketing, Ho Chi Minh City, Vietnam.

Ethics approval and consent to participate: Not applicable.Consent for publication: Not applicable

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

Please contact author for data and program codes requests. R and Matlab are used to organize data.

Additional information

Funding

References

- Agu, O. C., & Nyatanga, P. (2020). Oil price fluctuation, macroeconomic indicators and poverty in Nigeria. African Journal of Development Studies, 10(1), 49.

- Ahmed, K., Bhutto, N. A., & Kalhoro, M. R. (2019). Decomposing the links between oil price shocks and macroeconomic indicators: Evidence from SAARC region. Resources Policy, 61, 423–19. https://doi.org/10.1016/j.resourpol.2018.03.001

- Akadiri, S. S., Adebayo, T. S., Nakorji, M., Mwakapwa, W., Inusa, E. M., Izuchukwu, O. O., Grünberger, O., Lissalde, S., Mazella, N., Samouëlian, A., & Simon, S. (2022). Impacts of globalization and energy consumption on environmental degradation: What is the way forward to achieving environmental sustainability targets in Nigeria? Environmental Science and Pollution Research, 1–14. https://doi.org/10.1007/s11356-021-17416-3

- Alamgir, F., & Amin, S. B. (2021). The nexus between oil price and stock market: Evidence from South Asia. Energy Reports, 7, 693–703. https://doi.org/10.1016/j.egyr.2021.01.027

- Alvarado, R., Ponce, P., Criollo, A., Córdova, K., & Khan, M. K. (2018). Environmental degradation and real per capita output: New evidence at the global level grouping countries by income levels. Journal of Cleaner Production, 189, 13–20. https://doi.org/10.1016/j.jclepro.2018.04.064

- Amiri, H., Sayadi, M., & Mamipour, S. (2021). Oil price shocks and macroeconomic outcomes; Fresh evidences from a scenario-based NK-DSGE analysis for oil-exporting countries. Resources Policy, 74, 102262. https://doi.org/10.1016/j.resourpol.2021.102262

- Baek, J. (2021). Crude oil prices and macroeconomic activities: A structural VAR approach to Indonesia. Applied Economics, 53(22), 2527–2538. https://doi.org/10.1080/00036846.2020.1862750

- Bjørnland, H. C., Larsen, V. H., & Maih, J. (2018). Oil and macroeconomic (in) stability. American Economic Journal: Macroeconomics, 10(4), 128–151. https://doi.org/10.1257/mac.20150171

- Cao, H., Khan, M. K., Rehman, A., Dagar, V., Oryani, B., & Tanveer, A. (2021). Impact of globalization, institutional quality, economic growth, electricity and renewable energy consumption on Carbon Dioxide Emission in OECD countries. Environmental Science and Pollution Research, 28(1), 1–12. https://doi.org/10.1007/s11356-020-11060-z

- Chishti, M. Z., Iqbal, J., Mahmood, F., & Azeem, H. S. M. (2020). The implication of the oscillations in exchange rate for the commodity-wise trade flows between Pakistan and China: An evidence from ARDL approach. Review of Pacific Basin Financial Markets and Policies, 23(4), 2050030. https://doi.org/10.1142/S0219091520500307

- Choi, S., Furceri, D., Loungani, P., Mishra, S., & Poplawski-Ribeiro, M. (2018). Oil prices and inflation dynamics: Evidence from advanced and developing economies. Journal of International Money and Finance, 82, 71–96. https://doi.org/10.1016/j.jimonfin.2017.12.004

- Çıtak, F., Şişman, M. Y., & Bağcı, B. (2021). Nexus between disaggregated electricity consumption and CO2 emissions in Turkey: New evidence from quantile-on-quantile approach. Environmental and Ecological Statistics, 28(4), 843–860. https://doi.org/10.1007/s10651-021-00504-5

- Dagar, V., Khan, M. K., Alvarado, R., Usman, M., Zakari, A., Rehman, A., Tillaguango, B., & Tillaguango, B. (2021). Variations in technical efficiency of farmers with distinct land size across agro-climatic zones: Evidence from India. Journal of Cleaner Production, 315, 128109. https://doi.org/10.1016/j.jclepro.2021.128109

- Doğrul, H. G., & Soytas, U. (2010). Relationship between oil prices, interest rate, and unemployment: Evidence from an emerging market. Energy Economics, 32(6), 1523–1528. https://doi.org/10.1016/j.eneco.2010.09.005

- Dramani, J. B., & Frimpong, P. B. (2020). The effect of crude oil price shocks on macroeconomic stability in Ghana. OPEC Energy Review, 44(3), 249–277. https://doi.org/10.1111/opec.12182

- Ewing, B. T., & Thompson, M. A. (2007). Dynamic cyclical comovements of oil prices with industrial production, consumer prices, unemployment, and stock prices. Energy Policy, 35(11), 5535–5540. https://doi.org/10.1016/j.enpol.2007.05.018

- Geiger, M., & Scharler, J. (2019). How do consumers assess the macroeconomic effects of oil price fluctuations? Evidence from US survey data. Journal of Macroeconomics, 62, 103134. https://doi.org/10.1016/j.jmacro.2019.103134

- Godil, D. I., Sarwat, S., Khan, M. K., Ashraf, M. S., Sharif, A., & Ozturk, I. (2022). How the price dynamics of energy resources and precious metals interact with conventional and Islamic stocks: Fresh insight from dynamic ARDL approach. Resources Policy, 75, 102470. https://doi.org/10.1016/j.resourpol.2021.102470

- Gupta, K., & Krishnamurti, C. (2018). Do macroeconomic conditions and oil prices influence corporate risk-taking? Journal of Corporate Finance, 53, 65–86. https://doi.org/10.1016/j.jcorpfin.2018.10.003

- Hamilton, J. D. (1983). Oil and the macroeconomy since World War II. Journal of Political Economy, 91(2), 228–248. https://doi.org/10.1086/261140

- Hamilton, J. D. (2003). What is an oil shock? Journal of Econometrics, 113(2), 363–398. https://doi.org/10.1016/S0304-4076(02)00207-5

- Hamilton, J. D. (2005). Oil and the Macroeconomy. The New Palgrave Dictionary ofEconomics, 91(2), 1–17. https://doi.org/10.1086/261140

- Hashmi, S. H., Fan, H., Fareed, Z., & Shahzad, F. (2021). Asymmetric nexus between urban agglomerations and environmental pollution in top ten urban agglomerated countries using quantile methods. Environmental Science and Pollution Research, 28(11), 13404–13424. https://doi.org/10.1007/s11356-020-10669-4

- Hashmi, S. M., Chang, B. H., & Bhutto, N. A. (2021). Asymmetric effect of oil prices on stock market prices: New evidence from oil-exporting and oil-importing countries. Resources Policy, 70, 101946. https://doi.org/10.1016/j.resourpol.2020.101946

- Ho, T. T., & Ho, T. H. (2018). Operating the impossible trinity before and after the global financial crisis 2007-2008: Evidence in Vietnam. International Journal of Trade and Global Markets, 11(1–2), 40–49. https://doi.org/10.1504/IJTGM.2018.092491

- Ho, T. L., & Ho, T. T. (2021). Economic growth, energy consumption and environmental quality: Evidence from Vietnam. International Energy Journal, 21(2).

- Hung, N. T. (2020). Analysis of the time-frequency connectedness between gold prices, oil prices and Hungarian financial markets. International Journal of Energy Economics and Policy, 10(4), 51. https://doi.org/10.32479/ijeep.9230

- Hung, N. T. (2021a). Quantile dependence between green bonds, stocks, bitcoin, commodities and clean energy. Economic Computation and Economic Cybernetics Studies and Research, 55(3), 71–86. https://doi.org/10.24818/18423264/55.3.21.05

- Hung, N. T. (2021b). Effect of economic indicators, biomass energy on human development in China. Energy & Environment, 0958305X211022040. https://doi.org/10.1177/0958305X211022040

- Hung, N. T. (2022). Asymmetric connectedness among S&P 500, crude oil, gold and Bitcoin. Managerial Finance, 48(4), 587–610. https://doi.org/10.1108/MF-08-2021-0355

- Hung, N. T., Trang, N. T., Thang, N. T., Douzals, J.-P., Guibal, R., Grimbuhler, S., Grünberger, O., Lissalde, S., Mazella, N., Samouëlian, A., & Simon, S. (2022). Quantile relationship between globalization, financial development, economic growth, and carbon emissions: Evidence from Vietnam. Environmental Science and Pollution Research, 1–19. https://doi.org/10.1007/s11356-022-20126-z

- Islam, M., Khan, M. K., Tareque, M., Jehan, N., & Dagar, V. (2021). Impact of globalization, foreign direct investment, and energy consumption on CO2 emissions in Bangladesh: Does institutional quality matter? Environmental Science and Pollution Research, 28(35), 48851–48871. https://doi.org/10.1007/s11356-021-13441-4

- Jiang, W., & Liu, Y. (2021). The asymmetric effect of crude oil prices on stock prices in major international financial markets. The North American Journal of Economics and Finance, 56, 101357. https://doi.org/10.1016/j.najef.2020.101357

- Känzig, D. R. (2021). The macroeconomic effects of oil supply news: Evidence from OPEC announcements. American Economic Review, 111(4), 1092–1125. https://doi.org/10.1257/aer.20190964

- Khalfaoui, R., Padhan, H., Tiwari, A. K., & Hammoudeh, S. (2020). Understanding the time-frequency dynamics of money demand, oil prices and macroeconomic variables: The case of India. Resources Policy, 68, 101743. https://doi.org/10.1016/j.resourpol.2020.101743

- Khan, M. K., Teng, J. Z., & Khan, M. I. (2019). Effect of energy consumption and economic growth on carbon dioxide emissions in Pakistan with dynamic ARDL simulations approach. Environmental Science and Pollution Research, 26(23), 23480–23490. https://doi.org/10.1007/s11356-019-05640-x

- Khan, M. K., Abbas, F., Godil, D. I., Sharif, A., Ahmed, Z., & Anser, M. K. (2021). Moving towards sustainability: How do natural resources, financial development, and economic growth interact with the ecological footprint in Malaysia? A dynamic ARDL approach. Environmental Science and Pollution Research, 28(39), 55579–55591. https://doi.org/10.1007/s11356-021-14686-9

- Khan, M. K., Trinh, H. H., Khan, I. U., & Ullah, S. (2021). Sustainable economic activities, climate change, and carbon risk: An international evidence. Environment, Development and Sustainability, 24, 1–23. https://doi.org/10.1007/s10668-021-01842-x

- Khan, S., Khan, M. K., & Muhammad, B. (2021). Impact of financial development and energy consumption on environmental degradation in 184 countries using a dynamic panel model. Environmental Science and Pollution Research, 28(8), 9542–9557. https://doi.org/10.1007/s11356-020-11239-4

- Khraief, N., Shahbaz, M., Mahalik, M. K., & Bhattacharya, M. (2021). Movements of oil prices and exchange rates in China and India: New evidence from wavelet-based, non-linear, autoregressive distributed lag estimations. Physica A: Statistical Mechanics and Its Applications, 563, 125423. https://doi.org/10.1016/j.physa.2020.125423

- Kocaarslan, B., Soytas, M. A., & Soytas, U. (2020). The asymmetric impact of oil prices, interest rates and oil price uncertainty on unemployment in the US. Energy Economics, 86, 104625. https://doi.org/10.1016/j.eneco.2019.104625

- Koenker, R., & Bassett, G., Jr. (1978). Regression quantiles. Econometrica: Journal of the Econometric Society, 46(1), 33–50. https://doi.org/10.2307/1913643

- Koenker, R., & Xiao, Z. (2004). Unit root quantile autoregression inference. Journal of the American Statistical Association, 99(467), 775–787. https://doi.org/10.1198/016214504000001114

- Muhammad, B., & Khan, M. K. (2021). Foreign direct investment inflow, economic growth, energy consumption, globalization, and carbon dioxide emission around the world. Environmental Science and Pollution Research, 28(39), 55643–55654. https://doi.org/10.1007/s11356-021-14857-8

- Nguyen, V. B. (2021). The difference in the fdi-co₂ emissions relationship between developed and developing countries. Hitotsubashi Journal of Economics, 62(2), 124–140. https://www.jstor.org/stable/27084655

- Nonejad, N. (2020). A detailed look at crude oil price volatility prediction using macroeconomic variables. Journal of Forecasting, 39(7), 1119–1141. https://doi.org/10.1002/for.2679

- Omolade, A., Ngalawa, H., & Kutu, A. (2019). Crude oil price shocks and macroeconomic performance in Africa’s oil-producing countries. Cogent Economics & Finance.

- Ordóñez, J., Monfort, M., & Cuestas, J. C. (2019). Oil prices, unemployment and the financial crisis in oil-importing countries: The case of Spain. Energy, 181, 625–634. https://doi.org/10.1016/j.energy.2019.05.209

- Pham, B. T., & Sala, H. (2020). The macroeconomic effects of oil price shocks on Vietnam: Evidence from an over-identifying SVAR analysis. The Journal of International Trade & Economic Development, 29(8), 907–933. https://doi.org/10.1080/09638199.2020.1762710

- Punzi, M. T. (2019). The impact of energy price uncertainty on macroeconomic variables. Energy Policy, 129, 1306–1319. https://doi.org/10.1016/j.enpol.2019.03.015

- Shahbaz, M., Zakaria, M., Shahzad, S. J. H., & Mahalik, M. K. (2018). The energy consumption and economic growth nexus in top ten energy-consuming countries: Fresh evidence from using the quantile-on-quantile approach. Energy Economics, 71, 282–301. https://doi.org/10.1016/j.eneco.2018.02.023

- Shahzad, S. J. H., Mensi, W., Hammoudeh, S., Sohail, A., & Al-Yahyaee, K. H. (2019). Does gold act as a hedge against different nuances of inflation? Evidence from Quantile-on-Quantile and causality-in-quantiles approaches. Resources Policy, 62, 602–615. https://doi.org/10.1016/j.resourpol.2018.11.008

- Sharma, P., & Shrivastava, A. K. (2021). Economic activities and oil price shocks in Indian outlook: Direction of causality and testing cointegration. Global Business Review. 0972150921990491.

- Sheng, X., Gupta, R., & Ji, Q. (2020). The impacts of structural oil shocks on macroeconomic uncertainty: Evidence from a large panel of 45 countries. Energy Economics, 91, 104940. https://doi.org/10.1016/j.eneco.2020.104940

- Sim, N., & Zhou, H. (2015). Oil prices, US stock return, and the dependence between their quantiles. Journal of Banking and Finance, 55, 1–8. https://doi.org/10.1016/j.jbankfin.2015.01.013

- Suu, N. D., Tien, H. T., & Wong, W. K. (2021). The impact of capital structure and ownership on the performance of state enterprises after equitization: Evidence from Vietnam. Annals of Financial Economics, 16(2), 2150007. https://doi.org/10.1142/S201049522150007X

- Teng, J.-Z., Khan, M. K., Khan, M. I., Chishti, M. Z., & Khan, M. O. (2021). Effect of foreign direct investment on CO2 emission with the role of globalization, institutional quality with pooled mean group panel ARDL. Environmental Science and Pollution Research, 28(5), 5271–5282. https://doi.org/10.1007/s11356-020-10823-y

- Tien, H. T., & Hung, N. T. (2022). Volatility spillover effects between oil and GCC stock markets: A wavelet-based asymmetric dynamic conditional correlation approach. International Journal of Islamic and Middle Eastern Finance and Management. ahead-of-print No. ahead-of-print. https://doi.org/10.1108/IMEFM-07-2020-0370

- Tiwari, A. K., Umar, Z., & Alqahtani, F. (2021). Existence of long memory in crude oil and petroleum products: Generalised Hurst exponent approach. Research in International Business and Finance, 57, 101403. https://doi.org/10.1016/j.ribaf.2021.101403

- Tiwari, A. K., Raheem, I. D., Bozoklu, S., & Hammoudeh, S. (2022). The oil price‐macroeconomic fundamentals nexus for emerging market economies: Evidence from a wavelet analysis. International Journal of Finance & Economics, 27(1), 1569–1590. https://doi.org/10.1002/ijfe.2231

- Troster, V., Shahbaz, M., & Uddin, G. S. (2018). Renewable energy, oil prices, and economic activity: A Granger-causality in quantiles analysis. Energy Economics, 70, 440–452. https://doi.org/10.1016/j.eneco.2018.01.029

- Umar, Z., Riaz, Y., & Zaremba, A. (2021a). Patterns of spillover in energy, agricultural, and metal markets: A connectedness analysis for years 1780-2020. Finance Research Letters, 43, 101999. https://doi.org/10.1016/j.frl.2021.101999

- Umar, Z., Jareño, F., & Escribano, A. (2021b). Oil price shocks and the return and volatility spillover between industrial and precious metals. Energy Economics, 99, 105291. https://doi.org/10.1016/j.eneco.2021.105291

- Umar, Z., Jareño, F., & Escribano, A. (2021c). Static and dynamic connectedness between oil price shocks and Spanish equities: A sector analysis. The European Journal of Finance, 27(9), 880–896. https://doi.org/10.1080/1351847X.2020.1854809

- Umar, Z., Aharon, D. Y., Esparcia, C., & AlWahedi, W. (2022). Spillovers between sovereign yield curve components and oil price shocks. Energy Economics, 109, 105963. https://doi.org/10.1016/j.eneco.2022.105963

- Wei, Y., Qin, S., Li, X., Zhu, S., & Wei, G. (2019). Oil price fluctuation, stock market and macroeconomic fundamentals: Evidence from China before and after the financial crisis. Finance Research Letters, 30, 23–29. https://doi.org/10.1016/j.frl.2019.03.028

- Wu, M. H., & Ni, Y. S. (2011). The effects of oil prices on inflation, interest rates and money. Energy, 36(7), 4158–4164. https://doi.org/10.1016/j.energy.2011.04.028

- Xiao, Z. (2009). Quantile cointegrating regression. Journal of Econometrics, 150(2),248–260. Statistical Association, 99(467), 775-787. https://doi.org/10.1016/j.jeconom.2008.12.005

- Yildirim, Z., & Arifli, A. (2021). Oil price shocks, exchange rate and macroeconomic fluctuations in a small oil-exporting economy. Energy, 219, 119527. https://doi.org/10.1016/j.energy.2020.119527

- Yıldız, B. F., Hesami, S., Rjoub, H., & Wong, W. K. (2021). Interpretation of oil price shocks on macroeconomic Aggregates of South Africa: Evidence from SVAR. Journal of Contemporary Issues in Business and Government Vol, 27(1).

- Zakari, A., Toplak, J., Ibtissem, M., Dagar, V., & Khan, M. K. (2021). Impact of Nigeria’s industrial sector on level of inefficiency for energy consumption: Fisher Ideal index decomposition analysis. Heliyon, 7(5), e06952. https://doi.org/10.1016/j.heliyon.2021.e06952

- Zakaria, M., Khiam, S., & Mahmood, H. (2021). Influence of oil prices on inflation in South Asia: Some new evidence. Resources Policy, 71, 102014. https://doi.org/10.1016/j.resourpol.2021.102014

- Zhang, L., Godil, D. I., Bibi, M., Khan, M. K., Sarwat, S., & Anser, M. K. (2021). Caring for the environment: How human capital, natural resources, and economic growth interact with environmental degradation in Pakistan? A dynamic ARDL approach. Science of the Total Environment, 774, 145553. https://doi.org/10.1016/j.scitotenv.2021.145553

- Zia, S., Noor, M. H., Khan, M. K., Godil, D. I., Godil, D. I., Quddoos, M. U., Anser, M. K., & Anser, M. K. (2021). Striving towards environmental sustainability: How natural resources, human capital, financial development, and economic growth interact with ecological footprint in China. Environmental Science and Pollution Research, 28(37), 52499–52513. https://doi.org/10.1007/s11356-021-14342-2

- Zulfigarov, F., & Neuenkirch, M. (2020). The impact of oil price changes on selected macroeconomic indicators in Azerbaijan. Economic Systems, 44(4), 100814. https://doi.org/10.1016/j.ecosys.2020.100814