?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper applied the panel VAR approach and the Impulse Response Functions to investigate the differences in the monetary transmission processes of Islamic and conventional banks using disaggregated bank-level data for Saudi Arabia over the period 2008Q1–2020Q4. Our findings show that: i) Islamic banks play a significant role in transmitting monetary policy decisions to the real economy through the balance sheet channel; ii) Islamic banks’ deposits are more responsive to oil price shocks than Islamic financing; iii) the reaction of Islamic banks to monetary policy and price shocks is relatively weaker than that of conventional banks, suggesting the existence of rigidities, such as excess liquidity, inertia in changing return rates, and the lack of funding and investment sources, and iv) the relatively significant responses of Islamic banks to various shocks make it easier for the Saudi central bank to achieve macroeconomic goals through monetary policy actions in a dual-banking system.

PUBLIC INTEREST STATEMENT

This paper investigates the differences in the monetary transmission processes of Islamic and conventional banks using disaggregated bank-level data for Saudi Arabia. The main findings show that Islamic banks play a significant role in transmitting monetary policy decisions to the real economy through the balance sheet channel, and that their reaction to monetary policy and price shocks is relatively weaker than that of conventional banks, suggesting the existence of rigidities, and the lack of funding and investment sources.

1. Introduction

There is a broad consensus that at least in the short term, monetary policy influences economic activity (Bernanke & Gertler, Citation1995), but which channel transmits this effect? How does monetary policy achieve its goals? These questions have long intrigued economists, such that it is one of the most-recurring research themes in economics.

Understanding the mechanism through which monetary policy propagates is essential to achieving the key objectives of a central bank and enhancing macroeconomic stability, yet there is no consensus on how monetary policy affects economic activity. Studies have identified different channels for monetary policy transmission, and these can be classified into two categories: the price channel (e.g., interest rates, exchange rates, asset prices) and the credit channel (Bernanke & Gertler, Citation1995; Cecchetti, Citation1995). Instead of the first channel, which we consider traditional, we focus in this study on the credit or loan channel. We illustrate how the main theories on which it is based have been formed in reference to the economic and institutional frameworks for the monetary policies of developed and emerging countries. This is particularly needed for Saudi Arabia, where a lack of well-functioning financial markets and a rigid exchange rate regime leaves little room for the interest rate to play a role in the monetary transmission mechanism (Cottalerri and Kourelis, Citation1994). The degree of pass-through from domestic interbank rates to domestic deposit and lending rates is thought to be low, because nominal short-term interest rates in Saudi Arabia generally move in tandem with the U.S. Federal Reserve’s fund target rate (Espinoza & Prasad, Citation2012). According to Prasad and Khamis (Citation2011), under the pegged exchange rate regime, the GCC central banks closely follow the interest rate cycle of the United States, albeit with a degree of divergence, and rely on liquidity and reserve requirements when formulating monetary policy.

In Saudi Arabia, the financial system is dominated by banking institutions (i.e., a bank-based or bank-oriented financial system), and the financial market is relatively small and has limited impact on the economy. Banks are therefore considered the main sources of funding for small and medium-sized firms, with bank loans existing alongside other forms of financing. The supply of loans by banks acts as a basic channel for monetary policy decisions to influence economic activity.

The effects of monetary policy through the lending channel are more pronounced in a bank-oriented financial system than a market-oriented one. Bernanke and Gertler (Citation1995) demonstrate two possible mechanisms in the credit channel, namely the balance sheet channel (BSC) and the bank-lending channel (BLC). The BSC emphasizes the impact of adjustments in monetary policy on the borrower’s balance sheet, while the BLC focuses on the possible effect of monetary policy on the supply of loans from the banking system.

The BLC highlights the important role that banks play in the economy by facilitating the savings–investment process. Bernanke and Gertler (Citation1995) argue that monetary policy can affect bank portfolio behavior through the bank’s assets in terms of loans, securities, and bank reserves. The BLC therefore plays an important role in influencing economic activity, because any changes in monetary policy affect bank behavior in terms of both assets and liabilities. For example, a flexible monetary policy injects reserves into the banking system, which in turn triggers banks into raising the supply of loans, which in turn leads to an increase in investment spending and economic growth.

The primary objective of monetary policy in Saudi Arabia is to support the pegged exchange rate regime. With exchange rates pegged to the US dollar, the Saudi central bank (SAMA: Saudi Arabian Monetary Agency) has limited scope for discretionary monetary policy, so the primary responsibility for macroeconomic stability and demand management falls on fiscal policy. As a result of the pegged exchange rate regime, nominal short-term interest rates throughout Saudi Arabia generally shadow the US Federal Reserve’s fund target rate. Nevertheless, even within the limits of a fixed exchange rate regime, the channels of monetary transmission can play an important role. Identifying and assessing the significance of different transmission mechanisms is therefore necessary to successfully design and conduct monetary policy. Furthermore, Saudi Arabia’s monetary policy framework aims to stimulate bank lending to the private sector, and SAMA has undertaken policy measures to manage liquidity and ensure the availability of credit to support economic growth. This objective alone requires a better understanding of the transmission process and the development of instruments to reinforce the efficiency of monetary policy transmission.

The purpose of this study is therefore to assess the extent to which the bank-lending channel (BLC) of monetary policy transmission applies in Saudi Arabia. This is largely motivated by changes in Saudi Arabia’s monetary policy framework that are aimed at supporting fiscal policy, which aims to mitigate the negative effects of volatile oil prices by stimulating bank lending to the private sector. For some time now, SAMA has undertaken policy measures to manage liquidity and ensure the availability of credit to support economic growth. Bank loans to the private sector grew at an annual average rate of 16% for the year 2020, and this, alongside oil revenues, has greatly contributed to increasing financing capital. If oil prices were to fall, leading to less excess liquidity, the effects may be mitigated through the transmission of monetary policy, so SAMA would be more able to influence economic outcomes through its management of liquidity.

This study contributes to the existing research by utilizing disaggregated bank-level data and exploiting the heterogeneity of the Saudi banking system to reveal how its banks’ lending is influenced by monetary policy decisions. The use of disaggregated data provides evidence to support that banking characteristics are most influential in monetary transmission. To the best of our knowledge, this is the first attempt at quantifying the monetary transmission mechanism in Saudi Arabia using micro-level data that includes Islamic banks. It therefore represents a significant improvement over previous analysis.

From the authors’ point of view, there are at least three reasons for analyzing the importance of the bank-lending channel in the monetary policy transmission mechanism of Saudi Arabia. First, Saudi Arabia’s economic structure is exposed to two main external shocks: changes in US monetary policy and volatile oil prices. Falling oil prices influence other economic factors, such as investment, GDP growth, and employment. Monetary policy decisions can mitigate the negative effects of oil price fluctuations, at least in the short term, by influencing economic activity. This influence is transmitted through many channels, and understanding the mechanisms through which monetary policy is propagated is important for policymakers. Second, Saudi Arabia’s banking system plays a crucial role in financing non-oil operations in the private sector. The central bank (SAMA) aims to influence the supply of credit and financing to this sector due to the correlation between financing availability and the growth of non-oil, GDP-generating activity. Economic theory and the experiences of many emerging economies have shown that the relationship between monetary policy decisions and credit supply is not linear, and it can be influenced by bank characteristics such as size, liquidity, capitalization, ownership, and so on. To improve the effectiveness of monetary policy transmission, SAMA must understand how bank characteristics interplay with monetary policy decisions for credit supply. Finally, the third reason relates to investigating the relative importance of conventional and Islamic financing, as well as how the interaction between them affects financing supply, because this has not been analyzed in the Saudi Arabian context.

In this study, we focus on changes in depositing and lending behavior of conventional and Islamic banks in response to monetary shocks. The originality of this study lies in seeking to understand the importance of Islamic banks in the loan-supply mechanism and the effectiveness of SAMA’s monetary policy in the dual-banking system. Monetary policy is more effective when transmitted through the overall banking system, through both conventional and Islamic banks. If Islamic banks do not respond to monetary policy decisions, the overall impact of monetary policy on economic activity will be lower. In fact, monetary policy mainly affects real economy via prices (interest rates) or quantities (credits). The effectiveness of central banks’ actions necessitates the responsiveness of all banking components in transmitting the effects of monetary policy to economic activity. This becomes even more imminent in economies where the share of Islamic segment is as developed as the conventionnel one. In Saudi Arabia, the share of Islamic banking system visibly raises with 28.5% share in total assets, 31.1% in total loans, and 30.9% in total deposits in 2020.Footnote1 If conventional banks’ actions cannot affect the cost of financing or supply of Islamic credits, this can weaken monetary policy transmission through the interest rate or credit channel. Thus, analyzing how monetary policy actions influence Islamic banking in Saudi Arabia with dual banking system is of great salience for the success of monetary policy.

Besides, a key innovation in our analysis concerns how the transmission of shocks from the monetary base to economic activity via the credit channel is examined. This paper makes several important contributions to the literature on monetary policy transmission. First, to the best of our knowledge, no study has explicitly looked the bank-lending channel in oil-exporting countries. Second, by including monetary policy, oil prices, non-oil GDP, and consumer price shocks as the main variables in this framework, we are taking a novel approach by considering different types of shock, thus ensuring the robustness of the results. Third, we explore the impact of a bank’s business model on the bank-lending channel. The business models of conventional and Islamic banks are likely to show differences, so it is important to control for bank specialization. Finally, most of the literature applies a linear panel framework or dynamic panel methods (e.g., a GMM system), but we adopt the panel VAR approach proposed by Holtz-Eakin et al. (Citation1988), which builds upon the traditional VAR framework introduced by Sims (1980) with a panel data setup.

This paper is organized as follows: Section 2 provides a review of the literature. Section 3 describes the data and discusses the econometric methodology. Section 4 examines the results. Finally, section 5 concludes the paper and offers policy implications.

2. Literature review

This literature review summarizes the traditional channels for monetary transmission with a focus on the credit channel. Bernanke and Blinder (Citation1988), Christiano and Eichenbaum (Citation1992), and Mishkin (Citation1995), among others, have identified four main channels through which monetary policy actions are transmitted to the economy—namely interest rates, exchange rates, asset prices, and credit—through the bank-lending channel and balance sheet channel.

While the influence of monetary policy on conventional banks is frequently discussed, research investigating the role of Islamic banks in monetary policy transmission is still very scarce.

Without claiming to be exhaustive, this literature review will be composed of two parts. The first one deals with the theoretical effect of monetary policy in the presence of Islamic banking while the second one will be dedicated to empirical literature review on the bank-lending channel of monetary policy transmission.

2.1. Theoretical literature on the effect of monetary policy in the presence of Islamic banking

The monetary policy transmission mechanism in a dual-banking system (DBS), where Islamic and conventional banking coexist, is interesting because Islamic banking plays a special role in the financial system by offering interest-free financial products to markets. The different relationship between Islamic banks and interest rates may therefore lead to asymmetries in the effect of monetary policy actions by the central bank. In theory, the products offered by Islamic banks are free from interest and instead based on the profit/loss-sharing (PLS) principle. When central banks change the base interest rate, Islamic banks have no reason to raise the cost of financing for its borrowers. The stable prices of Islamic products, due to the sharia-compliant behavior of Islamic banking, means that monetary policy decisions do not produce any real effect, at least in theory, so monetary policy decisions are neutral. For example, some investors, such as individuals and small businesses, want to avoid riba (usury), so they cannot meet their financial needs from conventional banks. These clients may be indifferent to any differences in the returns of profit-sharing investment accounts or the cost of Islamic credit mainly due to their deeply held religious beliefs. As long as there is no perfect substitutability between Islamic banking products and other sources of funding, the monetary policy transmission mechanism will not operate perfectly. For example, in the interest rate channel, an expansionary monetary policy causes bank interest rates to lower, leading to greater demand for credit and more investment spending. At the same time, the financing costs and returns of Islamic banking instruments are unaffected because they are fixed in accordance with the PLS principle.

An important implication of Islamic banking’s presence for monetary policy transmission is that the effects on investment will be greater for firms that depend on conventional bank loans than for firms that finance their activities through Islamic banking. The stagnant costs of Islamic financing mean that the effects of monetary policy on this segment of financial system are neutral, while the same does not hold for conventional banks.

In reality, Islamic banks operate alongside conventional banks in a competitive market for credits and deposits. According to Khatat (Citation2016), in an environment dominated by interest rates, and in the presence of competition between conventional and Islamic banks, the Islamic banks are forced to align their pricing of financial products in line with those of conventional banks. There is therefore a spillover effect of interest rate changes on funding costs and returns from profit-sharing investment accounts (PSIAs) for Islamic banks.

For the interest channel, and in the case of an expansionary monetary policy, there is no reason for Islamic banks to respond to the impact of a political decision by reducing financing costs for firms. Furthermore, in the bank-lending channel, an expansionary monetary policy increases Islamic banks’ reserves and deposits, thus increasing the funds available for lending and investment spending.

This interaction between Islamic and conventional banks in the competitive market enhances the responsiveness of Islamic banking to monetary policy, reducing thereby the asymmetries in monetary policy transmission. Monetary policy then has a greater effect on investment by all firms in the economy, regardless of the banking style they use.

2.2. Empirical literature on the bank-lending channel

No study has looked at the bank-lending channel of monetary policy transmission in Saudi Arabia using bank- or micro-level data. Most studies in this area have evaluated various channels of the monetary policy transmission in Saudi Arabia using macro-level data.

Ziaei (Citation2012) used an SVAR model to evaluate different channels of monetary policy transmission in Saudi Arabia over the 1999–2007 period. He found that an increase in the base interest rate leads to a fall in output but no impact on prices, so there clearly is an active interest rate channel in Saudi Arabia. Credit was also found to have a positive and statistically significant impact on domestic demand, and bank credit largely explained fluctuations in output in the long term, with the effect being more pronounced than with the exchange rate channel, which played a very limited role in transmitting monetary shocks to the real economy. A shock on the nominal effective exchange rate led to a decrease in prices but had no effect on output.

Westelius (Citation2013) used a VAR model on annual data (1980–2010) to investigate the relationship between bank credit and non-oil output in Saudi Arabia. He estimated the model three times—namely over the entire 1980–2010 period, over the 1980–1995 period, and over the 1996–2010 period—to examine whether the influence of bank credit on the non-oil economy had evolved over time. He found that i) when the full sample was considered, the response of the non-oil GDP to a positive standard-deviation shock to bank credit was positive but statistically insignificant; ii) there was a statistically insignificant effect for the earlier 1980–1995 period but a significant one for the later 1996–2010 period; and iii) credit explained most of the forecast error variance decomposition of the non-real GDP over the 1996–2010 period, compared with a weaker explanatory power over the 1980–1995 period.

As in Saudi Arabia, empirical evidence for the monetary transmission mechanism (MTM) in other GCC countries is limited and restricted to macro-level analyses. Cevik and Teksöz (Citation2012) used an SVAR model on quarterly data for the 1990–2010 period to estimate the importance of the various monetary policy transmission channels in GCC countries. They found that the interest rate channel and the bank-lending channel were relatively potent for influencing non-hydrocarbon output and consumer prices. They also found that the exchange rate channel did not play an important role in the transmission process because of pegged exchange rate regimes.

On estimating a panel VAR model for the GCC countries over the 1978–2009 period, Espinoza and Prasad (Citation2012) found that the United States’ monetary policy had a strong and statistically significant impact on money supply, non-oil activity, and inflation in the GCC countries. They found that an increase of 150 basis points in the federal funds rate slowed the growth of the money supply by more than 1 percentage point and reduced non-oil activity by 1.5% 10 quarters after the shock.

Empirical literature about the influence of an MTM on economic activities in the presence of Islamic banks has emerged more recently. Al-Darwish et al. (Citation2015) examined the interest rate and credit channels of monetary policy transmission in Saudi Arabia using a time series econometric analysis with aggregate data. They discovered that a rise in the US fed funds rate significantly and negatively affected prices, but it did not affect non-oil output. Credit, meanwhile, was found to have a statistically significant positive effect on non-oil output, implying that Saudi Arabia’s credit channel is active. The authors suggest that it may be helpful to investigate monetary transmission through the bank-lending channel with micro-level data.

Many scholars have addressed the DBS—such as Kasri and Kassim (Citation2009), Chong and Liu (Citation2009), and Rama and Kassim (Citation2013)—to analyze the interactions between Islamic and conventional banks. They have explored what determines the liabilities of Islamic banks and the impact of conventional banks’ interest rates on depositors’ behavior. They revealed a strong correlation between the returns on Islamic banks’ PSIAs and the interest rates for conventional banks’ deposit accounts. For the impact of interest rate changes on the demand for Islamic financing in a DBS, Kader and Leong (Citation2009), Kassim et al. (Citation2009), and Rama and Kassim (Citation2013) found that any increase in the lending rate encourages customers to seek financing from Islamic banks and vice versa. The authors attributed this result to direct competition between Islamic and conventional banks and the profit-motivated behavior of their customers. Islamic banks in a DBS are therefore exposed to interest rate risks despite operating on interest-free principles.

Aysan et al. (Citation2018) used a panel VAR model with quarterly data from Turkey. They found that the responses of Islamic banks to policy rate changes, in terms of deposits and credit, are more pronounced. They attributed the difference in responses to the inertia of Islamic banks in reacting, whereas conventional banks can more readily accommodate policy rate changes. During a period of adjustment, Islamic banks’ depositors may withdraw their deposits if the returns offered by alternative investments become more profitable. For the loan responses, the authors attribute the difference to the lending behavior of small and medium-sized enterprises (SMEs). They posit that Islamic banks are significantly more willing to finance SMEs than conventional banks. However, Islamic banks may be unable to continue financing SMEs after policy rate changes, because they may not be able to compensate for depositors’ withdrawals, while conventional banks can secure funding through alternative borrowing instruments. Islamic banks’ lending to SMEs is therefore more sensitive to monetary shocks. The authors concluded that central banks should be aware that monetary expansion or contraction may have more favorable or unfavorable effects on unemployment and growth because Islamic banks are more responsive to monetary shocks.

The study of Rafay and Farid (Citation2019) revealed the significant role that the major balance sheet items (i.e., deposits and financing) of Islamic banks plays in the monetary transmission process in Pakistan. They argued that Islamic deposits begin to decline in response to an increase in the discount rate. The authors attributed this result to the fact that bank depositors in Islamic banks may withdraw their deposits if the new policy conditions mean that the returns offered by alternative investments are greater. In addition, the variance decomposition of Islamic financing showed the significant role of Islamic deposits in explaining the forecast error variance in Islamic finance. The authors concluded that Islamic deposits are a factor in shaping monetary policy.

Caporale et al. (Citation2020) contributed to the existing literature on Islamic finance by adopting a more suitable and sophisticated econometric framework to analyze monetary transmission in a country with a DBS, all under different macroeconomic conditions. More specifically, they estimated a threshold VAR (TVAR) model to investigate whether the reactions of Islamic and conventional banks differed during the different phases of the business cycle. Their results show Islamic credit to be less responsive than conventional credit to interest rate shocks in both high- and low-growth periods for Malaysia. The sub-sample estimation, however, suggested that this gap had narrowed in recent years. Moreover, the relative importance of Islamic credit in driving output growth was notable in the low-growth period.

Finally, Rashid et al. (Citation2020) examined the impact of monetary policy on credit supply decisions for Islamic and conventional banks operating in Malaysia. They found that the credit supply of Islamic banks was less responsive to tight monetary policy when compared to their conventional counterparts. Moreover, smaller, less-liquid Islamic and conventional banks were more responsive to increased interest rates in the economy. The authors concluded that the central bank needs to take into account the nature of Islamic banking and the size of a bank and its liquidity position when formulating monetary policy.

At the end of this literature review, we conclude that no studies have scrutinized the determinants of the assets and liabilities of Islamic banks in Saudi Arabia. Our study therefore aims to fill this gap by assessing the interactions between Islamic and conventional banks. Furthermore, to the best of our knowledge, the monetary policy transmission in the presence of Islamic banks remains to be examined with micro-level data. The only available study is that of Ben Amar et al. (Citation2015), who used quarterly aggregate data for bank lending and balance sheets for the period 1990–2013, to investigate the effectiveness of monetary policy transmission in Saudi Arabia’s Islamic banks. The results indicated that the bank-lending channel is relatively effective at influencing non-oil private output but less effective at influencing consumer prices. In addition, a positive shock on the financing offered by Islamic banks or the loans granted by conventional banks results in improved economic activity. Finally, the authors concluded that the DBS likely improves the responsiveness of Islamic banks to monetary policy, as they align their pricing of financial assets with those of conventional banks, thus making them more sensitive to monetary policy decisions.

3. Data and empirical methodology

3.1. Definition of variables and summary statistics

The econometric analysis was based on a panel dataset for eight conventional banks and four Islamic banks for the period 2008–2020, at quarterly frequency.Footnote2 The banks’ financial data were obtained from the banks’ balance sheets and income statements, while the macroeconomic data were gathered from SAMA’s economic reports and statistics database. presents the definitions of the variables used in our analysis and their summary statistics.

Table 1. Descriptive statistics

This paper includes four objective variables, namely the monetary policy indicator (MPI), credits (financing in the case of Islamic banks), deposits, and oil prices. A further two objective variables are the aggregate price level (CPI) and the non-oil GDP. The money reserve (monetary base) is considered to be the monetary policy indicator,Footnote3 which SAMA controls through its liquidity-management operations (Alghaith et al., Citation2015). The bank credit variables include aggregate bank credits, conventional bank credits, and Islamic financing.Footnote4 We followed the same method for the deposits.Footnote5 Finally, the oil price was included to capture international shocks and wealth effects. This was considered to be an exogenous variable because it is unlikely to be influenced by economic factors in Saudi Arabia. The other variables were considered to be endogenous and relevant for modeling monetary policy transmission in the dual-banking system.

Nevertheless, it is worth making two points at this stage. First, while it is common practice in many previous studies to use the overnight interbank rate as a monetary policy variable, we believe that the movements of reserve money will better capture liquidity shocks in the Saudi context for the following reasons: First, under the pegged exchange rate regime, SAMA has limited flexibility when setting interest rate policy, as short-term interest rates closely follow the US Federal Reserve’s interest rates.Footnote6 SAMA therefore relies on reserve requirements and other market-based instruments such as repo operations and the issuance of bills to implement monetary policy (Alghaith et al., Citation2015). In view of this, growth in money reserves or other monetary aggregates may be a better indicator of the monetary policy position. Second, we acknowledge that other variables, such as exchange rate, can be potentially more relevant for capturing international shocks than oil prices. However, we chose the oil price for the following reasons. 1) Saudi Arabia is among the world’s largest oil exporters and highly dependent on oil exports. In this context, it would be negligent to ignore the significance of oil price movements for GDP growth, public spending, and consumer prices in Saudi Arabia (Algahtani, Citation2016). 2) We believe the exchange rate channel is inactive in Saudi Arabia due to the pegged exchange rate regime, but oil prices are set by the market, so their movements better capture international shocks.

3.2. The panel VAR approach

The empirical assessment of the bank-lending channel in Saudi Arabia follows the methodological approaches of prior studies in other countries, such as the work of Kashyap and Stein (Citation2000), Kassim et al. (Citation2009), and Juurikkala et al. (Citation2011), Zaheer et al. (Citation2013). This work, however, was adapted to an emerging economy with underdeveloped financial markets and heterogeneous players in the banking sector (i.e., the dual-banking system). We investigated the cross-sectional differences in the way that conventional and Islamic banks responded to monetary policy shocks in Saudi Arabia over the period from Q1-2008 to Q4-2020. The country and sample period provide a unique setting for analyzing this differential response. Indeed, Saudi Arabia is one of the few countries in the world where well-developed conventional and Islamic banking sectors have co-existed for a considerable period, specifically from 1990 when Islamic banking was introduced in Saudi Arabia. Out of the twelve banks that grant loans, four are exclusively Islamic.

In particular, the framework recognizes that:

Firms depend on bank loans (i.e., a bank-based system) in the absence of active and well-developed capital markets. We posit that changes in monetary policy that affect banks’ reserves are reflected in adjustments in the supply of loans.

Saudi Arabia’s financial system characterized by the coexistence of Islamic and conventional banks. We expect that the presence of Islamic banks could cause differential effects in terms of how banks’ lending responds to monetary policy.

Due to the pegged exchange rate regime, SAMA closely follows interest rate movements in the United States. The monetary policy rate is therefore not independent, so SAMA relies on the monetary base to implement monetary policy.

In Saudi Arabia, an important implication of the bank-lending channel is that monetary policy will have a greater effect on investment by private firms in non-oil sectors, which are more dependent on bank loans, than it will on investment by oil and stated-owned businesses, which receive funding directly from the government rather than through banks.

An assessment of the bank-lending channel using disaggregated data can be achieved by testing a hypothesis that asserts that the transmission of monetary policy is asymmetric depending on the size, liquidity, and capitalization of Islamic or conventional banks. The bank-specific data was gathered from the balance sheets of the 12 Saudi banks, and this represented about 64% of GDP and 98% of the total assets in the banking system.

The empirical analysis involved studying the monetary transmission mechanism for Islamic and conventional banks, because these may respond differently in terms of bank lending. It was especially important to identify how effectively central banks can influence the level of reserves (deposits) and consequently bank lending (credits). To this end, we assume there is a dynamic relationship among deposits (or credits) and the monetary policy indicator as a reduced form panel VAR (PVAR).

The choice of a PVAR approach was based on three reasons. First, the PVAR approach allows the endogenous interactions between monetary shocks and credit to be determined. This allows the lagged effects of monetary shocks on deposits and consequently credits to be understood as a determination of whether credit feeds back into monetary shock. Second, a panel Granger causality analysis allows the direction of the complicated link between monetary shocks and credit to be determined, thus allowing a discussion about possible bidirectional relationships. Third, impulse-response functions (IRFs) help to evaluate the dynamic links between monetary shocks and credits.

The main purpose of the IRF analysis consists at allowing the dynamic impacts of changes in each of the endogenous variables over time. IRFs envisage the impact of an isolated shock in one variable to the other variables, showing how these innovations are propagated through the system. They only take into account the time-lagged relationships between the endogenous variables. Orthogonalized IRFs are variants of IRFs taking into account the contemporaneous correlations between the variables as well (Brandt & Williams, Citation2007). They used Cholesky decomposition assuming that, for the direction of the contemporaneous relationships, a specific ordering is chosen. However, the results of alternative orderings can be presented in the case where no theory is available guiding this choice (Norman et al., Citation1997).

The PVAR model extends the traditional VAR framework that was introduced by Sims (1980) by using a panel data setup.Footnote7 This flexible method was proposed by Holtz-Eakin et al. (Citation1988). The PVAR model is structured as a system of endogenous and independent variables, with all variables being treated in an unrestricted manner. This is useful when there is a strong correlation between the outlined variables. The PVAR model also accommodates for cross-sectional dynamic heterogeneity, thus providing further information about the sources of heterogeneity in the system. This technique therefore helps to identify the dynamic heterogeneity among the considered groups of banks. In addition, the PVAR approach makes it easier to capture all time variations for the coefficients as well as the shock variance.

Moreover, the length of the series is not sufficient to provide a robust estimation of separate VAR models for each bank, so when setting up the model, we focused on a small number of variables that possibly convey the dynamics of key monetary shocks. For all these reasons, the PVAR modelling is more suitable for our study. According to Love and Zicchino (Citation2006), the key assumption in the PVAR methodology is that the variables entering the system earlier contemporaneously affect the following variables with a lag, while those coming later affect the previous variables only with a lag. It is therefore a system of equations rather than a one-equation model.

According to Abrigo and Love (Citation2016), for the model selection, estimation, and inference of homogeneous PVAR using the GMM estimation approach,Footnote8 one can define a homogenous PVAR of order p with panel-specific effects as follows:

where is the vector of endogenous stationary variables, containing

and

in the VAR system for bank

and time

.

where is the vector of country-specific effects, as proposed by Holtz-Eakin et al. (Citation1988). In all estimations, we control for bank-level heterogeneity by incorporating

. Finally,

represents the vector of idiosyncratic errors, with

,

and

for all

.

In dynamic panel specifications, the pooled estimation with fixed effects might be biased when the time dimension is fixed and reduced firm shocks correlate across the banks. A standard fixed-effect estimator is biased due to the existence of correlation between the regressors and the fixed effects. To handle this issue, the model is estimated via the GMM with the Helmert forward mean-differencing transformation following the work of Love and Zicchino (Citation2006). The Helmert transformation controls for fixed country effects while preserving the orthogonality between the endogenous variables and their lags, thus allowing the latter to be used as instruments in GMM estimations.

The PVAR model is considered stable when the eigenvalues of the estimated model are all inside the unit circle. Once the coefficients have been estimated, we analyze the potential effects of monetary shocks (MPI) on deposits (Islamic deposits) and credit (Islamic financing) by generating IRFs.

4. Empirical results

4.1. Panel unit root tests

To address concerns about the presence of unit roots in the considered variables, we conducted a unit root test using Fisher’s test statistics for panel unit root (Maddala and Wu, Citation1999). The choice of this type of test was based on the fact that it does not require a balanced panel, unlike, for example, the LLC test (Levin, Lin and Chu, Citation2002) or the IPS test (Im, Pesaran, and Shin, 2003).

presents the results of the Fisher test with the augmented Dickey–Fuller (ADF) and the Phillips–Perron (PP) unit root tests. The null hypothesis was that all series are non-stationary, while the alternative hypothesis stated that at least one of the series in the panel is stationary. Since PVAR models employ Helmert-transformed variables, presents the results for the original variables and their Helmert transformations. The results showed that both Fisher-ADF and Fisher-PP rejected the presence of unit roots at conventional significance levels. Therefore, all the variables were considered as stationary, indicating the appropriateness of using them in PVAR analysis.

Table 2. Results from the unit root tests

4.2. Lag order selection

To proceed with the PVAR model, we needed to select the lag order using the benchmark model, which includes the logarithms of MPI and credit. We could then estimate additional specifications using the same optimal lag order.

provides the overall coefficient determination (CD) that captures the proportion of variation that is explained by the PVAR model, with higher values being preferable to lower ones, in conjunction with Hansen’s J-test for over-identification,Footnote9 as well as the three information criteria suggested by Andrews and Lu (2001) for GMM estimation and modifications of the well-known Akaike, Bayesian, and Hannan-Quinn information criteria. The modified information criteria are called MAIC, MBIC, and MQIC, respectively.

Table 3. PVAR lag order selection criteria

We showed that the null hypothesis that over-identified restrictions are valid could not be rejected at the 5% significance level for all lag order levels (1, 2, 3 or 4). In addition, the MBIC, MAIC and MQIC criteria have the smallest value for the first lag order, so for the rest of the analysis, we fit a one-lag PVAR model using GMM estimations to investigate depositors’ and creditors’ responses to changes in the monetary policy indicator.

4.3. Panel VAR results

Given the small number of endogenous variables included in the baseline model and the lag order of 1, GMM estimations should yield robust results without imposing additional restrictions. The baseline model and other PVAR specifications employed in this study were found to be stationary and satisfied the eigenvalue stability conditions.

Following the estimation of the PVAR models,Footnote10 we computed the orthogonalized IRFs to track the reaction of one variable in the system to changes in another variable in the same system over time. The IRFs provided a time profile impact of the shock at a given period, and this allowed us to evaluate the magnitude of each shock’s effect upon the relevant variable. The Orthogonal IRFs were obtained via Cholesky’s factorization scheme.

In the presentation, we focused on the behavior of Islamic financing and deposits in response to monetary policy shocks. We then investigated how it differs from that of conventional credits and deposits. We therefore reported how Islamic financing (credits) and deposits respond to shocks in the monetary base, inflation, and oil prices. The following figures show the IRF plots with 95% confidence bands, having been estimated using Monte Carlo simulations with 1,000 repetitions and Gaussian approximation.

4.3.1. Responses to monetary shocks

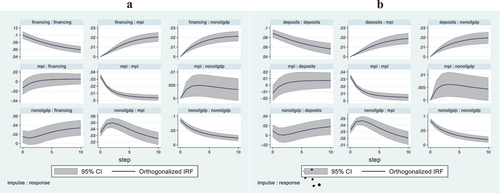

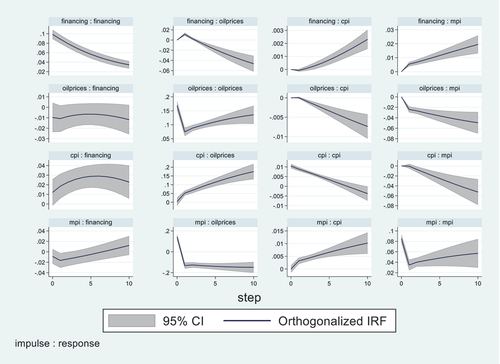

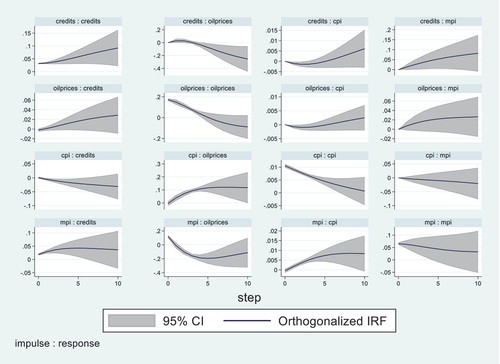

illustrates the responses of Islamic financing and conventional banks’ credits. The results show that the MPI (monetary reserves) has particularly strong implications for financing by Islamic banks, suggesting its importance as a transmission channel of monetary policy, which supports our original conjecture. As can be seen from the (orthogonal) IRFs profiles in , a positive shock in the MPI leads to a statistically significant positive response in both Islamic financing and conventional credit (and the opposite for negative shocks). However, the amplitude of the response differs according to the types of banks. In fact, a one standard deviation in MPI shocks is associated with almost 2% increase after ten quarters for Islamic banks (), whereas for conventional banks, the increase reached 3% after ten quarter with a peak level equal to 5% at the fifth period ().

Figure 1. Impulse responses of financing and deposits to MPI shocks: Islamic banks.

Figure 2. Impulse responses of credits and deposits to MPI shocks: conventional banks.

These findings suggest that the existence of an active bank-lending channel is particularly relevant for conventional banks when there are shocks in bank reserves. There are various explanations for this result. First, Saudi Arabia has a less-developed Islamic money market, so Islamic banks accumulate more liquid assets than their conventional counterparts, as argued by Boukhatem and Djelassi (Citation2020a).Footnote11 Islamic banks therefore use their excess liquidity to protect their financing in the face of tighter monetary policy. Second, Saudi Islamic banks are heavily reliant on quasi-debt instruments in the form of markups and rents (Murabaha, Ijaraa) as modes of financing, so the effects of an expansionary monetary policy (i.e., the injection of liquidity) do not extend to their financing activities, such as Mudharaba and Musharaka, due to the high level of risk associated with such financial products and legal and institutional obstacles.Footnote12 On the other hand, conventional banks in the same situation may be able to increase their financing through interest-based lending instruments like bonds and commercial papers.

In addition, unlike the positive responses for financing, Islamic banks’ responses to monetary shocks are negative for deposits. The initial level is viewed at quarter 10. The conventional bank deposits, on the other hand, give a negative response to bank reserve shocks at the beginning, and gradually turn into positive after 4 quarters. The behavior of conventional banks may be due to them being able to change interest rates to accommodate the reduced funds they have available to lend. Conventional banks also have fewer reserves, so they increase the deposit interest rate to raise more funds for their financing activities. Moreover, an increase in the issuing of bills by the central bank encourages conventional banks to increase their demand for deposits. Therefore, conventional banks can quickly accommodate changes in the monetary base, whereas monetary shocks trigger a period of adjustment in Islamic banks rates, because they distribute ex-post returns. Our results suggest that during the adjustment period, the depositors of Islamic banks may withdraw their funds once conventional deposits offer higher returns.

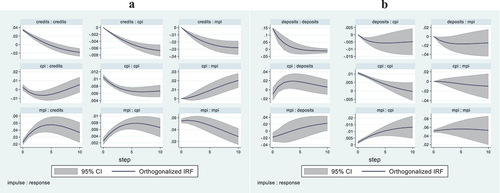

4.3.2. Responses to output shocks

show the simulated response of financing (credits) and deposits to output shocks in Islamic and conventional banks respectively. Two observations can be made. First, both Islamic financing and conventional credits seem to be affected by output shocks, with relative persistence over time. However, the amplitude of the response differs from Islamic banks to conventional ones, and seems to be greater for conventional banks. In fact, one standard deviation in non-oil GDP is associated with about 4% increase in financing volume after ten quarters for Islamic banks (); whereas, for conventional banks, the increase is 6% for the same time horizon (). These results may reflect the absence of differences between the lending behaviors of the two types of banks when facing risks caused by changes in real variables. Theoretically, the risks faced by Islamic banks to the assets side are shared with depositors, which is not the case with their conventional counterparts.Footnote13 The practice of Islamic financial intermediation differs from its conceptual foundations, however, as outlined in Boukhatem and Djelassi (Citation2020b). Islamic bankers try to secure their financing through collateral and the assignment of ownership rights in cases of default. In addition, Islamic bankers try to protect depositors against profit shocks by holding large reserves and appropriate capital. This is not intrinsically different from the behavior of conventional banks.

Figure 3. Impulse responses of financing and deposits to non-oil GDP shocks: Islamic banks.

Figure 4. Impulse responses of credits and deposits to non-oil GDP shocks: conventional banks.

The second observation bears on the responses of deposits to output shocks. Non-oil GDP shocks are found to be significantly affecting conventional and Islamic deposits, yet with different magnitude and time profile. The effects of Islamic deposits are essentially null during the first two quarters after the non-oil GDP shocks; but at about the fourth quarter, Islamic deposits begin to rise gradually until quarter 10 (). On the other hand, non-oil GDP shocks drive up the conventional deposits, with a peak effect after three quarters and then decaying very slowly (). The amplitude of the response seems to be largely greater for conventional banks. The fact that both Islamic and conventional deposits respond following a change in the non-oil GDP is consistent with the view that income is an important determinant of deposits’ decisions, even though Islamic deposits respond with lags to output shocks.Footnote14

4.3.3. Responses to price shocks

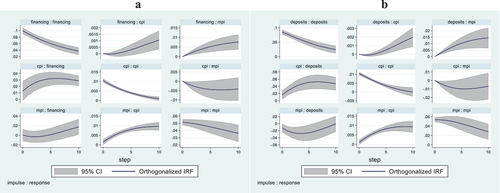

The response patterns of conventional credits, Islamic financing, and deposits to price shocks (CPI) tend to differ ( to A4 of the appendix). While Islamic deposits and financing respond positively to prices shocks, conventional ones respond negatively, suggesting that in conventional banks, depositors demand higher interest due to higher inflation shrinking the net return. Once their demand for higher returns is not met by banks, the depositors consider switching to other banks or withdrawing their deposits to invest in other investments or simply keep in cash. However, the results for Islamic banks reflect the growth targets for real deposits. Since Islamic banks can sell their products on a markup basis (murabaha) and obtain income from leased assets (ijaraa), this gives banks and depositors a good bulwark against inflation. It is likely that the depositors of an Islamic bank that focuses on asset-backed investments might suffer less than conventional banks’ depositors, where banks rely mainly on a nominal interest rate, especially when real returns are diminished by adverse price shocks.

The conventional banks’ credits response to inflation can be explained by shifting supply and demand conditions for lending in different inflation conditions. Due to the uncertainty created by positive inflation shocks, credit supply and demand is significantly deteriorated (Brooks, Citation2007). Banks’ preferences for making loans are reduced in favor of other investments that offer greater returns, such as government bonds. Moreover, firms’ demand for conventional credits shrinks due to greater capital expenditure and increased production costs for goods. Islamic products are therefore generally better positioned to bear the brunt of inflation, as the burden can be integrated into the markup, so the supply of financing is unaffected by price shocks. The demand for Islamic financing, however, often has a direct hit on margins due to inflation shocks, but this is presumably not strong enough to trigger a reduction in financing. Islamic banks try to be competitive and apply low but attractive profit rates, resulting in greater stability for Islamic banks in real terms.

4.3.4. Responses to oil price shocks

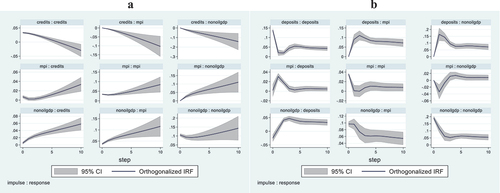

Few empirical studies in the literature have examined the differences in the relationships that conventional and Islamic banks have with oil in oil-exporting countries. Conceptually, since Islamic banks are often funded by sharia-compliant deposits, higher oil prices tend to be associated with greater liquidity, so deposit inflows can be used for lending. A positive relationship between the oil price and Islamic financing is therefore likely. Conventional banks have greater access to wholesale funding than Islamic banks, so oil prices may have a different impact on conventional credit. It is therefore likely that Islamic banks, which focus on a stable deposit base, will suffer less than conventional banks—which rely more on wholesale funding, especially with lower liquidity—in the wake of adverse oil price shocks. To test this hypothesis and check the robustness of our results, we introduced a new variable to represent the oil price, because this is an important indicator for measuring macroeconomic stability in Saudi Arabia, which is the largest oil-exporter in the world.

The figures from A1 to A4 in the appendix depict the Islamic and conventional banks’ responses to oil price shocks in terms of credits and deposits. The IRFs show a positive response for conventional credits to positive oil prices shocks and a negative response for Islamic financing with stable and persistent amplitude over time (). Conventional banks may have been pro-cyclicity with respect to oil price changes. When oil prices are high, they may be providing loans more than Islamic banks do. Wang and Luo (Citation2020) find the same results using a sample of 279 banks in the MENA region. Their analysis indicate that the credit risk of bank loan portfolios is negatively associated with increased oil prices and this effect is more salient in conventional and low liquidity banks. If oil prices rise, the income and government spending in oil exporting countries will also increase, thus affecting bank lending favorably through the government spending channel. According to Miyajima (Citation2017), there exist a relation between the lending behavior of Saudi conventional banks and state ownership. The lending by Saudi banks with greater state ownership appears pro-cyclical with respect to oil price performance. As oil prices increase, lending by banks with high state ownerships tend to rise more than lending by other banks. IMF (2017) consider that, when oil prices decline and the fiscal balance becomes strained, banks with high state ownership tend to purchase government bonds and reduce lending more than other banks do. In our study, we have four state ownership banks (National Commercial Bank, Samba, Ryad Bank and Saudi Investment Bank). All these banks are conventional, and their share in total conventional credits are about 58% between Q1-2008 and Q4-2020. So, the trend of conventional credit responses to oil price shocks are more driven by the lending behavior of state ownership banks. On the other hand, the 4 Islamic banks in our sample are private ownership and the negative response of their financing to oil price shocks can be explained by the existence of rigidities, such as excess liquidity and the limited investment opportunities.

Concerning the response of deposits to oil price shocks, the IRFs show a negative response for conventional banks and a shifting pattern for Islamic banks, with the response being negative in the initial quarters but becoming positive later (). During an oil price boom, the excess liquidity held by Islamic banks is bolstered by more oil-related liquidity entering the financial system. This new liquidity leads to excess bank resources, meaning Islamic banks have less need for deposits during an oil price boom, thus explaining the initial negative response to oil price shocks.

Finally, in a typical oil-dependent economy like Saudi Arabia, where oil revenues drive the economy, we see that the response of monetary reserves (MPI) to oil price shocks is positive (). In Saudi Arabia, oil revenues are a major source for the foreign exchange reserves, which in turn affect the monetary base. Holding foreign exchange reserves is necessary for a central bank to offset any variations in the domestic currency, especially for an export-oriented country like Saudi Arabia. Moreover, oil revenues affect the monetary base through changes in the government’s spending, which is financed by oil revenues that are converted to the local currency. If the government spends money to pay its suppliers, the central bank draws it from the fiscal account and credits it to the reserves account of the relevant commercial bank. The positive response of conventional credits to positive oil prices shocks prove that conventional banks are the most benefiting from the government spending channel.

5. Conclusion

In this paper, we provide new insights for why the bank-lending channel works differently for Islamic banks when compared to their conventional counterparts. We did this by examining the sensitivity of Saudi banking activities to monetary shocks. More precisely, we examined the responses of conventional and Islamic financing and conventional and Islamic deposits to monetary shocks, as represented by the monetary base. In addition, we evaluated whether their responses differed when faced with shocks in the goods market (i.e., non-oil GDP, consumer prices) and the oil market (oil price). To carry out our empirical analysis, we used a panel dataset of commercial banks in Saudi Arabia for a period from Q1-2008 to Q4-2020. We applied the panel VAR framework, which is structured as a system of endogenous and independent variables, where all variables are treated in an unrestricted manner. In addition, the PVAR approach made it easier to capture all time variations for the coefficients, as well as the variance in shocks. We summarize the results below.

First, a positive shock in the MPI triggers statistically significant positive responses in financing from Islamic and conventional banks. However, the amplitude of the shock is greater for conventional banks, suggesting the presence of excess liquidity in Islamic banks. Second, we found that the deposits of Islamic banks respond negatively to tight monetary policy, while their conventional counterparts respond positively. The inertia of Islamic banks in repricing their products and their dependency on the behavior of Islamic depositors are likely behind this phenomenon. Third, we noted that output shocks affected both types of financing, and the impact of such shocks appears to be persistent for both types of lending. Fourth, Islamic deposits respond positively to output shocks after some lags, while the response of conventional deposits is negative during the initial quarter but then shifts to a positive and persistent one. Fifth, we found that Islamic financing and deposits responded positively to price shocks, while their conventional counterparts responded negatively. Finally, unlike conventional credits, Islamic financing responds negatively to oil price shocks. However, concerning the responses of deposits to oil price shocks, the responses of Islamic banks are positive, while those of conventional banks are negative.

Our findings suggest that the financing and deposits of Islamic banks are significantly responsive to changes in the monetary base, indicating the presence of the balance sheet channel in these banks for transmitting monetary policy. Nevertheless, the reaction of Islamic banks to monetary policy and price shocks is relatively weaker than that of conventional banks, suggesting the existence of rigidities, such as excess liquidity, inertia of Islamic banks in changing return rates, and lack of funding and investment sources. Despite these functional rigidities, the existence of a significant response by Saudi Islamic banks to monetary and oil price shocks, as well as the existence of an effective bank-lending channel for influencing economic activity (non-oil GDP) suggest that the dual structure likely enhances the responsiveness of Islamic banks to monetary policy, because they align their financing and depositing practices with those of conventional banks, which are generally sensitive to monetary policy decisions. The relatively significant responses of Islamic banks to various shocks make it easier for the Saudi central bank to achieve the desired macroeconomic objectives through monetary policy actions in a dual-banking system.

Finally, and in order to improve the efficiency of the bank-lending channel in monetary policy transmission, Saudi central bank has to monitor the micro-dynamics of individual banks’ behaviors. Moreover, since Islamic banks take certain advantages in the lending of SMEs which in turn add significantly to labor force participation in domestic economies, the employment and domestic output control from Saudi central bank can be eased through Islamic banking. Nevertheless, Saudi central banks should be conscious that Islamic banks may cause monetary contractions which will probably have repercussions on unemployment and growth.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Notes on contributors

Jamel Boukhatem

Jamel Boukhatem is full professor at the Faculty of Economic Sciences and Management of Tunis. His research focuses on monetary and financial macroeconomics. He has published papers in several indexed and high ranked Journals such as Emerging Markets and the Global Economy, Research in International Business and Finance, Journal of Applied Business Research, Bosra Istanbul Review, Annals of Financial Economics, Finance Research Letters, Quarterly Review of Economics and Finance, Quantitative Finance and Economics, Annals of Operations Research, Renewable and Sustainable Energy Reviews, International Journal of Economics and Financial Issues, Future Business Journal, and Heliyon Journal.

Notes

1. Our calculations from financial statements of Saudi banks.

2. The selected banks are Rajhi, Alinmaa, AlBaled, Aljazeera, NCB-AlAhly, Arab National Bank, Ryad Bank, Alawwal, The Saudi Investment Bank, Saudi Fransi BanK, Samba, and Saab.

3. Reserve money is narrowly defined as the monetary base, and it is the sum of currency outside banks and bank reserves.

4. Such financing is granted to customers without charging interest in order to be sharia-compliant. In Saudi Arabian Islamic banks, these methods fall mainly into four broad categories: Murabaha, Ijaraa, Istisnaa, and Musharakah. Murabaha is a financing agreement where the bank purchases a commodity or asset and sells it to the client at a price based on the purchase price plus a profit that is agreed with the client, meaning that the client is aware of both the cost and the bank’s profit. Ijaraa is an agreement whereby the bank, acting as a lessor, purchases or builds an asset for lease according to the request of the customer (the lessee), who agrees to lease the asset for a specified period for an agreed rent, and at the end of the period, ownership is transferred from the bank to the customer. Istisnaa financing is a financing agreement whereby the bank contracts the manufacture of a commodity with certain known specifications according to the client’s request. The client then becomes a debtor to the bank for the manufacturing price plus a profit. Musharaka is an agreement between the bank and a customer where the bank invests in a certain enterprise or the ownership of a certain property, ending with the customer acquiring the full ownership. Any profits or losses are shared per the terms of the agreement.

5. In Saudi Arabian Islamic banks, deposits comprise demand deposits and customers’ time investments based on the profit-sharing principle.

6. See Espinoza and Prasard (2012) and Alghaith et al. (Citation2015).

7. In general, VAR models have been found to be an especially useful tool for estimating dynamic interactions between endogenous variables of interest. However, in empirical financial applications, sufficiently long data is typically a major constraint, and “the curse of dimensionality” frequently becomes a problem.

8. The GMM estimator was developed by Arellano and Bond (1991), Arellano and Bover (1995), and Blundell and Bond (1998) to tackle the endogeneity issue in the presence of unobserved fixed country effects.

9. This coefficient checks whether the overidentification restriction is rejected at the 5% significance level.

10. The results of estimated PVAR models are presented in the tables to A4 of the appendix.

11. Boukhatem and Djelassi (Citation2020a) argue that the four Saudi Islamic banks have, on average, lower loan-to-deposit ratios, much higher interbank ratios, and more comfortable liquidity ratios than conventional banks.

12. For more details about the weakness of the PLS mode of financing and the evolution of Islamic banking to a non-PLS system, refer to the work of Boukhatem and Djelassi (Citation2020b).

13. A profit shock undergone by entrepreneurs will have a negative effect on the income of Islamic banks and the wealth of investment account holders (local risk). Since the depositors’ claims on banks are not guaranteed in nominal terms, decreases in the bank’s income will have a negative impact on the wealth of any depositors whose portfolio included a significant number of investment accounts. This structure may better resist shocks to the asset side of balance sheet because such shocks can be instantaneously absorbed by the liabilities side. This type of adjustment helps the stability of the banking system. In the case of the conventional banking system, there exists a dichotomy between assets and liabilities, and any shock that hits the assets side can generate instability (Boukhatem & Djelassi, Citation2020b).

14. Non-oil GDP, as a measure of output, can be considered as a proxy for domestic demand.

References

- Abrigo, M. R. M., & Love, I. (2016). Estimation of panel vector autoregression in Stata. The Stata Journal, 16(3), 778–24. https://doi.org/10.1177/1536867X1601600314

- Al-Darwish, A., Alghaith, N., Behar, A., Callen, T., Deb, P., Hegazy, A., Khandelwal, P., Pant, M., & Qu, H. (2015). Monetary and macroprudential policies in Saudi Arabia: tackling emerging economic challenges to sustain strong growth. Washington, DC: International Monetary Fund.

- Algahtani, G. (2016). The effect of oil price shocks on economic activity in Saudi Arabia: econometric approach. International Journal of Business and Management, 11(8), 124–133. https://doi.org/10.5539/ijbm.v11n8p124

- Alghaith, N., Al-Darwish, A., Deb, P., & Khandelwal, P. (2015). Monetary and macroprudential policies in Saudi Arabia, in the Saudi Arabia: tackling emerging economic challenges to sustain growth. In Middle East and Central Asia departmental paper series (pp. 37–59).Washington, DC: International Monetary Fund.

- Aysan, A. F., Disli, M., & Ozturk, H. (2018). Bank lending channel in a dual banking system: why are Islamic banks so responsive? World Economy, 411 , 674–698. https://doi.org/10.1111/twec.12507

- Ben Amar, A., Hachicha, N., & Saadallah, R. (2015). The effectiveness of monetary policy transmission channels in the presence of Islamic banks: the case of Saudi Arabia. International Journal of Business, 20(3), 1083–4346. https://ijb.cyut.edu.tw/var/file/10/1010/img/861/V203-4.pdf

- Bernanke, B. S., & Blinder, A. S. (1988). Credit, money and aggregate demand. American Economic Review, 78(2), 435–439. https://doi.org/10.4236/jmf.2018.82017

- Bernanke, B. S., & Gertler, M. (1995). Inside the black box: the credit channel of monetary policy transmission. Journal of Economic Perspectives, 9(4), 27–48. https://doi.org/10.1257/jep.9.4.27

- Boukhatem, J., & Djelassi, M. (2020a). Liquidity risk in the Saudi banking system: is there any Islamic banking specificity? The Quarterly Review of Economics and Finance, 77(C), 206–219. https://doi.org/10.1016/j.qref.2020.05.002

- Boukhatem, J., & Djelassi, M. (2020b). The risk-sharing paradigm in islamic financial system: myth or reality? In S. Goutte & G. K.Ed. Risk factors and contagion in commodity markets and stocks markets. 161–196. World scientific Publishing. chap. 7.

- Brandt, P. T., & Williams, J. T. (2007). Multiple time-series models. Sage Publications.

- Brooks, P. K. 2007. “The bank lending channel of monetary transmission: does it work in Turkey?” Working Paper no. 07/272, International Monetary Fund, Washington, DC.

- Caporale, G. M., Çatık, A. N., Helmi, M. H., Ali, F. M., & Tajik, M. (2020). The bank lending channel in the Malaysian Islamic and conventional banking system. Global Finance Journal, 45(C), 1–26. https://doi.org/10.1016/j.gfj.2019.100478

- Cecchetti, S. (1995). Distinguishing theories of the monetary transmission mechanism. Federal Reserve Bank of St Louis Economic Review, 77(3), 83–97. https://fraser.stlouisfed.org/title/820/item/24578/toc/500922

- Cevik, S., & Teksöz, K., 2012. Lost in transmission? The effectiveness of monetary policy transmission channels in the GCC countries. IMF Working Papers, WP/12/191.

- Chong, B. S., & Liu, M. H. (2009). Islamic banking: Interest-free or interest-based? Pacific-Basin Finance Journal, 17(1), 125–144. https://doi.org/10.1016/j.pacfin.2007.12.003

- Christiano, L. J., & Eichenbaum, M. (1992). Current real-business-cycle: Theories and aggregate labor-market fluctuations. The American Economic Review, 82(3), 430–450.

- Cottarelli, C., & Kourelis, A. (1994). Financial Structure, Bank Lending Rates, and the Transmission Mechanism of Monetary Policy. Staff Papers (International Monetary Fund), 41(4), 587–623. https://doi.org/10.2307/3867521

- Espinoza, R., & Prasad, A., 2012. Monetary policy transmission in the GCC countries. IMF Working Paper. International Monetary Fund, WP/12/132.

- Holtz-Eakin, D., Newey, W., & Rosen, H. S. (1988). Estimating vector autoregressions with panel data. Econometrica, 56(6), 1371–1395. https://doi.org/10.2307/1913103

- Juurikkala, T., Karas, A., & Solanko, L. (2011). The role of banks in monetary policy transmission: empirical evidence from Russia. Review of International Economics, 19(1), 109–121. https://doi.org/10.1111/j.1467-9396.2010.00935.x

- Kader, R. A., & Leong, Y. K. (2009). The impact of interest rate changes on islamic bank financing. International Review of Business Research Papers, 5(3), 189–201. https://mpra.ub.uni-muenchen.de/100644/1/MPRA_paper_100644

- Kashyap, A. K., & Stein, J. C. (2000). What do a million observations on banks say about the transmission of monetary policy? American Economic Review, 90(3), 407–428. https://doi.org/10.1257/aer.90.3.407

- Kasri, R., & Kassim, S. (2009). Empirical determinants of saving in the Islamic banks: evidence from Indonesia. JKAU: Islamic Economics, 22(2), 181–201. https://doi.org/10.4197/islec.22-2.7

- Kassim, S., Majdi, A. S., & Yusof, R. M. (2009). Impact of monetary policy shocks in the conventional and Islamic banks in a dual banking system: evidence from Malaysia. Journal of Economic Cooperation and Development, 30(1) , 41–58. http://irep.iium.edu.my/id/eprint/19850

- Khatat, M. E. H., 2016. Monetary policy in the presence of Islamic banking. IMF Working Paper. International Monetary Fund, WP/16/72.

- Levin, A., Lin, C. F., & Chu, J. (2002). Unit root tests in panel data: Asymptotic and finite-sample properties. Journal of Econometrics, 108(1), 1–24. https://doi.org/10.1016/S0304-4076(01)00098-7

- Love, I., & Zicchino, L. (2006). Financial development and dynamic investment behavior: Evidence from panel VAR. The Quarterly Review of Economics and Finance, 46(2), 190–210. https://doi.org/10.1016/j.qref.2005.11.007

- Maddala, G. S., & Wu, S. (1999). A comparative study of unit root tests with panel data and a new simple test. Oxford Bulletin of Economics and Statistics, 61(S1), 631–652. https://doi.org/10.1111/1468-0084.0610s1631

- Mishkin, F. (1995). Symposium on the monetary transmission mechanism. The Journal of Economic Perspectives, 9(4), 3–10. https://doi.org/10.1257/jep.9.4.3

- Miyajima, K., 2017. What influences bank lending in Saudi Arabia? Working Paper no. 17/31, International Monetary Fund, Washington, DC.

- Norman, R., Swanson, C., & W.j. (1997). Granger impulse response functions based on a causal approach to residual orthogonalization in vector autoregressions. Journal of the American Statistical Association, 92(437), 357–367. https://doi.org/10.1080/01621459.1997.10473634

- Prasad, A., & Khamis, M. (2011). Monetary policy and the transmission mechanism in the GCC countries. In Gulf cooperation council countries: enhancing economic outcomes in an uncertain global economy (pp. 47–63). International Monetary Fund.

- Rafay, A., & Farid, S. (2019). Islamic banking system: A credit channel of monetary policy – evidence from an emerging economy. Economic Research Journal, 32(1), 742–754.

- Rama, A., & Kassim, S. (2013). Analyzing determinants of assets and liabilities in Islamic banks: evidence from Indonesia. Review of Islamic Economics, Finance, and Banking, 1(1), 34–53. https://www.iqtishadconsulting.com/assets/media/file/file-analyzing-determinants-of-assets-and-liabilities-in-islamic-banks-evidence-from-indonesia.pdf

- Rashid, A., Hassan, M. K., & Shah, M. A. R. (2020). On the role of Islamic and conventional banks in the monetary policy transmission in Malaysia: do size and liquidity matter? Research in International Business and Finance, 52(C), 101123. https://doi.org/10.1016/j.ribaf.2019.101123

- Wang, R., & Luo, H. (2020). Oil prices and bank credit in MENA countries after 2008 financial crisis. International Journal of Islamic and Middle Eastern Finance and Management, 13(2), 219–247. https://doi.org/10.1108/IMEFM-03-2019-0103

- Westelius, N. J., 2013. External linkages and policy constraints in Saudi Arabia. IMF Working Paper. International Monetary Fund, WP/13/59.

- Zaheer, S., Ongena, S., & Van Wijnbergen, S. J. G. (2013). The transmission of monetary policy through conventional and Islamic banks. International Journal of Central Banking, 9(4), 175–224. https://www.ijcb.org/journal/ijcb13q4a6.pdf

- Ziaei, S. M. (2012). Transmission mechanisms of monetary policy in Saudi Arabia: evidence from SVAR analysis. Journal of Modern Accounting and Auditing, 7(8), 990–1012. https://doi.org/10.17265/1548-6583/2012.07.007

Appendix

Figure A1. Impulse responses of financing to CPI and oil prices’ shocks: Islamic banks

Figure A2. Impulse responses of credits to CPI and oil prices’ shocks: conventional banks

Figure A3. Impulse responses of deposits to CPI and oil prices’ shocks: Islamic banks

Figure A4. Impulse responses of deposits to CPI and oil prices’ shocks: conventional banks

Table A1. Main results of a 5-variable VAR with financing for Islamic banks

Table A2. Main results of a 5-variable VAR with deposits for Islamic banks

Table A3. Main results of a 5-variable VAR with credits for conventional banks

Table A4. Main results of a 5-variable VAR with deposits for conventional banks