?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Using the Stochastic Frontier Analysis on data for 33 sub-Saharan African countries over the period 2007 to 2018, we determine the drivers of the inefficiencies in financial stability and also estimate the existing financial stability gaps. The results confirm that credit to the private sector and the level of unemployment are significant drivers of financial stability in SSA, while employment, domestic savings, and regulatory quality significantly decrease the inefficiencies in financial stability. Further, it is revealed that government domestic debt arrears promote financial stability inefficiencies in SSA. Countries within the East Africa Community Countries (EAC) have the highest mean efficiency and the least financial stability gap for the period studied. It is therefore recommended that government borrowing from the domestic economy should be towards projects that have undergone proper appraisal as a means to reduce arrears accumulation. Employment is recommended to improve income while encouraging domestic savings as a conscious effort to enable the financial sector to perform its intended essential role in the economy

1. Introduction

The finance literature identifies several possible causes of vulnerability in the financial sector; Inflation, unemployment, nonperforming loans, and worsened terms of trade (Beck et al., Citation2015; Klein, Citation2013). One other important cause of financial-sector vulnerability is government domestic arrears. The International Monetary Fund (IMF; Citation2019) report explains that when governments, private companies, and SOEs are unable to service their bank loans, the banking sector tends to experience a deterioration in the quality of their assets and an increase in their nonperforming loans (NPLs), which is a threat to financial stability. Given the critical role of the financial sector in channeling financial resources into the economy, studies relating to its stability is of much importance. This research, therefore, seeks to provide answers to the following research questions: what are the levels of potential financial stability among SSA countries? What are the gaps in financial stability among the SSA countries and what factors drive the inefficiencies in financial stability among the SSA countries?

It is important to note that the overall growth of an economy among other factors, depends on the performance of the financial sector (Kulu & Appiah-Kubi, Citation2021; Saravani et al., Citation2015). The private sector, which is known to be the engine of economic growth in most sub-Sahara African (SSA) countries competes with the government for credits for investment activities. Credit is seen as the fuel that powers the private sector, hence the more credit available to the private sector, the better its role in achieving growth and development. A common form of crowding out occurs when government finances most of its activities through domestically generated funds such as issuing of debt, etc. Anyanwu et al. (Citation2018) also explains that government can generate large amounts of money domestically hence potentially impacting the real interest rate by suffocating the lending capacity of the private sector and deterring other businesses from engaging in capital investments. Financial institutions facilitating these activities have their share of the impact when there are significant delays in servicing government debt. International Monetary Fund (IMF; Citation2019) indicates that out of 30 countries in SSA, 24 of them had government domestic arrears by the close of the year 2018, with an average stock of 3.3 percent of GDP and a maximum of 18 percent of GDP.

Though not as huge as the foreign indebtedness, the stock of domestic debt has grown in recent years and is also smaller in HIPC countries than in non-HIPC countries (Christensen, Citation2005). An increase in the domestic debt and consequently arrears increases the instability in the financial system (Cantah et al., Citation2022). Indeed, these vulnerabilities within the private sector can be minimized when activities and interactions, especially between the lender and the borrower, are well regulated. Also, activities such as the effectiveness of government policies increased employment and domestic savings that improve the liquidity positions of financial institutions and go a long way to reduce inefficiencies.

With the significant role of the financial sector in intermediating and acting as a lubricant in the economy coupled with the rising government domestic debt arrears in SSA, the research questions stated are well directed and worthy of answering. Estimates in this study are also made for sub-regional communities in SSA namely the Economic Community of West Africa States (ECOWAS), East Africa Community Countries (EAC), and the Economic Community of Central Africa countries (ECCAS). This is geared towards the proposal of policy recommendations to be implemented at the sub-regional community level. Thus, community-level decisions complementing the country levels’ have the possibility of impacting more. This study, therefore, advances the frontier of knowledge by unearthing the efficiency level, potential, and gaps in financial stability among some SSA countries and sub-regional communities, as well as revealing the drivers of the inefficiencies for the appropriate address. Lists of countries in SSA and the sub-regional groups considered for the study are provided in Appendix Table and Table . Countries with an asterisk are found to be members of their respective sub-regional communities as well as the Southern Africa Development Community (SADC). Due to this overlapping, the SADC was not considered for this study. The rest of the paper is arranged as follows: the next section looks at the empirical literature; the methodology for the study is discussed in section three; in section four, we discuss the findings from the study and section five concludes with policy recommendations.

2. Literature review

The current empirical literature on financial stability has focused mostly on its drivers. Indeed, several variables are the predominant factors affecting the stability of financial institutions across the globe. It is important to note that the choice of these variables and their possibility of statistical significance is dependent on the economy under study. Notable in the existing literature is the Ozili (Citation2018) and the International Monetary Fund (IMF; Citation2019) for African countries. Ozili (Citation2018) studied the main determinants in 48 African countries for the period 1996 to 2015. Banking instability was measured using four varied indicators, namely: loan loss coverage ratio, insolvency risk (using the Z-score), non-performing loans to gross loans ratio (for asset quality ratio) as well as the standard deviation of financial development. The study found that the main drivers of financial stability include banking efficiency, banking concentration, government effectiveness, presence of foreign banks, political stability, investor protection, regulatory quality, control of corruption, and the levels of unemployment. More importantly, the study highlights the relevance of the quality of institutions in determining the stability in the African financial system.

Another study by Vo et al. (Citation2019), examined the variables that influence instability in the financial system in the case of developing countries. Using the period 2000 to 2017, panel data for 17 developing countries was created. In ensuring robustness, estimation techniques, such as the fixed and random effect as well as the pooled OLS, were employed. Using the growth in credit as a proxy for financial instability, the empirical findings indicated that inflation rate, growth in GDP, changes in foreign exchange reserves, growth in the rate of the monetary base, the ratio of return on equity of the banking sector, returns in the stock market, as well as the lending rate are the main drivers of financial instability. Particularly for developing markets, the results of the study appear to be in line with the post-Keynesians relating to the mechanisms that lead to instability of the financial system. Again, Jokipii and Monnin (Citation2013), examine the effects of economic factors, such as inflation and growth in real output on stability in the banking sector. They employed a quarterly for 18 OECD countries for the period 1980 to 2008. Estimations from the VAR model show that growth in real output directly affects stability in the banking sector. The study, however, found no relationship between the rate of inflation and stability in the banking sector. Also focusing on economic factors, Segoviano and Goodhart (Citation2009) confirm that unexpected fluctuations in the cycles of the economy, as well as the effect of the booms and recessions, can lead to instability in the banking system. The study, however, concludes that the identified relationship is different from country to country. Bank performance and unemployment level have been argued to have a relationship. While controlling for unemployment, Heffernan and Fu (Citation2008) analyzed the drivers of bank determinants using 96 banks in China for the period 1999 to 2006. They made a prediction that increasing unemployment can decrease aggregate demand and cause a rise in the default rate on loans, therefore, introducing an inverse relationship between the unemployment level and the performance of banks. Performance of banks being a key driver of bank stability, unemployment is then predicted to directly influence stability in the banking sector. The analysis of the study, therefore, showed that there is a negative relationship between the level of unemployment and bank performance and therefore the stability of the banking system.

Das et al. (Citation2010) examined the association between public debt management and stability in the financial system as well as the medium through which the two variables are interrelated. The paper concludes that improper management of debt and debt structures can highly prevent the ability of a ruler in ensuring financial stability. This is because the risk perception of investors in the country is affected, intensifying pressures, at the initial stages on the financial institution’s capital reserves, incomes, balance sheet, and eventually on the balance sheet of the sovereign, therefore increasing sovereign risk. The relationship between sovereign risk and financial stability can work through a feedback circle, thus, inappropriate management of debt has the possibility of worsening the stability of the financial system, which in turn intensifies sovereign risk (Das et al., Citation2010). It is further concluded that appropriate debt management can help guarantee financial stability through the creation of a liability structure for public debt that ensures the sustenance of low levels of refinancing risk.

In a recent study, Van Duuren et al. (Citation2020) studied whether the association between financial stability and financial stability transparency index is dependent on the quality of institutions. Using annual data for the period 2000 to 2011, the study used the fixed effect estimation technique. The non-performing loans ratio is also used as a proxy for financial stability. The findings confirm previous findings that transparency in financial stability enhances the degree of stability in a country’s financial system. The findings, however, suggest that transparency in financial stability is statistically significant and negatively associated with non-performing loans of banks that have minimal institutional quality. Thus, controlling for other macroeconomic variables, the annual data spanning the period 2004 to 2012, used the z-score of banks as a proxy for financial stability and commercial banks’ outstanding loans as a proxy for financial inclusion. The analysis showed that financial stability is inversely affected by the outstanding deposits with commercial banks. This indicates that in SSA, there are less diversified deposit accounts held with the commercial banks. Outstanding loans from the studied commercial banks do have a direct role in financial stability. On the control variables, the study further showed that financial crisis, credit to the private sector, and inflation negatively affect financial stability while per capita GDP affects financial stability positively. With the discussion on the financial stability gap, Fahr and Fell (Citation2017) argued that macroprudential policies are needed for closing the gap in financial stability while monetary policies are needed for the stabilization of prices.

Indeed, SSA countries and sub-regions operate with different monetary policies and exchange rate regimes which may affect their status of stability in the financial system. Frameworks of monetary policy in SSA have two main types (Kasekende & Brownbridge, Citation2011). Thus, the monetary targeting frameworks and the fixed exchange rate regimes (including the CFA monetary unions). Most SSA economies such the those in the ECOWAS and EAC have the intention of introducing a monetary union and having a common currency. For this transition, there will be the requirement for a period of management in the exchange rate to align the bilateral exchange rates of all the potential members of the union.

For the system of the exchange rate, SSA operates three main categories: pegged, intermediate, and floating, where the majority of the countries in SSA operate the pegged system. For countries operating the pegged, the most popular anchor currency used is the euro and the US dollar is the next. Countries like Botswana, Mauritius, Tanzania, Ghana, and Nigeria, operate the intermediate and floating regimes. It is therefore expected that the differences in the monetary and exchange rate systems will have consequences on the ability to ensure stability in the financial system.

A critical look at the reviewed literature indicates that no attention has been given to the factors affecting the inefficiency in financial stability as well as the estimates of the gaps in financial stability, especially in SSA. The critical role financial institutions play in the effective performance of the overall economy cannot be overemphasized. It is therefore essential to make known the extent of the gaps, the potential as well as the efficiency levels of financial stability especially for the respective countries so that the impact that the differences (among countries) in the monetary policy and exchange rate system may pose can be curtailed. This is aimed at alerting policymakers, and other stakeholders about the appropriate policies directions.

3. Data and methods

3.1. Data

The study employed secondary data covering the period 2007 to 2018 for 33 SSA countries. The period and countries considered for the study were selected based on data availability especially data for financial stability. The variables employed include financial stability, credit to the private sector, unemployment, employment, institutional quality, inflation, domestic debt, savings, government domestic arrears, government effectiveness, and regulatory quality. The variables were sourced from the world bank’s World Development Indicators (WDI), Worldwide Governance Indicators (WGI), Global Financial Development (GFD), the IMF database, and the Heritage Foundation. Description of the variables used and their respective sources are presented in Table (Appendix C).

3.2. Model specification and estimation technique

3.2.1. The stochastic frontier model

A working horse in the literature on productivity and efficiency is the Stochastic Frontier Production Function (SFPF), independently created by Aigner et al. (Citation1977) and Meeusen and van Den Broeck (Citation1977). The SFPF refers to the peak output from the given point of input and technology to a structural part of the production function and a decomposed disturbance term. In recent literature, this technique has been employed in determining the efficiency and potential values of significant variables. Following other studies such as Osiewalski et al. (Citation1997) and Mamo et al. (Citation2018), who respectively used the Stochastic Frontier Analysis (SFA) to measure the productivity gap and yield gap of smallholder wheat producers in Ethiopia, the SFA model is employed in determining the financial stability gap in this study. The model is specified as follows

where is financial stability,

represents predictors of financial stability such as institutional quality, unemployment, and credit to the private sector.

is a single-sided error, specific to each country, and creates the difference between actual and potential financial stability. It is the log difference between the highest and the actual observation (Thus, in this study,

According to Ahmadzai (Citation2017),

is the percentage loss due to inefficiency. The SFA model is used because it is argued that it has the possibility of offering richer specifications, mostly in panel data cases (Hjalmarsson et al., Citation1996). The empirical Stochastic Frontier model is specified as

where, is the log of financial stability of the SSA countries at time

,

is credit to the private sector,

is unemployment,

represents institutional quality,

is inflation and

represent government domestic debt.

is a single-sided error for the combined effects while

is the conventional error term that controls, statistical errors and omitted variables. The SFA will provide estimates of the efficiency values

which will subsequently be used in determining the potential financial stability

This will be calculated using the formula

Again, we specify the inefficiency effect model, in Equationequation (4)(4)

(4) capturing the significant drivers of inefficiencies in financial stability in SSA

where represents employment,

is domestic savings,

represents governments’ domestic debt arrears,

is government effective,

represents regulatory quality.

measures the degree to which actual financial stability falls short of potential financial stability given by the stochastic frontier equation. The variable of interest in Equationequation (4)

(4)

(4) is the government domestic debt arrears. The theoretical basis is that according to the postulates of the Post-Keynesians Hypothesis, including Minsky (Citation1977), “uncontrolled expansion of credit” contributes to the instability and inefficiencies in financial institutions. Given this argument, we hold the view that uncontrolled lending to the government, especially when the repayment (by the government) is not made on time, will possibly cause instability or inefficiencies in the financial system. Further, the gap in financial stability will be derived as the difference between the actual and potential financial stability. Thus, using the Equationequation (5)

(5)

(5) below.

4. Results and discussion

presents the descriptive statistics of the variables used for the study. The differences in the number of observations indicate that there are missing observations for some variables in certain years for some countries. For the variables employed, domestic debt recorded the highest standard deviation. This indicates the wide disparity among the countries under consideration in terms of government domestic borrowing. The mean values −0.865 and −0.714 suggest that government effectiveness and regulatory quality, respectively, are low among SSA countries. The mean value for change in the stock of government arrears measured as a percentage of GDP for the period is about 3 percent, which is in line with International Monetary Fund (IMF; Citation2019) reports.

Table 1. Descriptive statistics of variables (2007 to 2018)

The Variance Inflation Factor (VIF) test presented (see ) shows that all the variables used have VIF score of less than 10. This indicates a minimal level of correlation among the variables hence the estimated model does not suffer multicollinearity.

4.1. Results of the stochastic frontier model

The stochastic frontier model in Equationequation (2)(2)

(2) and the inefficiency model in Equationequation (3)

(3)

(3) are estimated simultaneously based on the usual stochastic frontier production function using maximum likelihood estimation (MLE). The model parameter estimates of frontier and inefficiency are presented in respectively. As expected, credit provided to the private sector is found to be positive and statistically significant at 1 percent. This implies that as more credits are provided to the private sector for their activities, financial stability is boosted. It is argued that this act increases investment made by the private sector, hence improvements in savings with the financial institutions. A higher interest rate on loans reduces private sector investment therefore credit to the private sector can improve financial stability through private investment when the cost of interest for firms is lower than the return on private investment. Moreover, the low cost of credit reduces banks’ agency cost and non-performing loans, which in turn strengthens banks’ balance sheet and reduce their liquidity risk thereby improving their efficiency without forgetting that the strength of the bank’s balance sheet contributed to the global financial crisis in 2008. Van Duuren et al. (Citation2020) however, found credit to the private sector to be a significant variable in determining financial stability but negative. A negative and statistically significant relationship was found between unemployment and financial stability. This confirms the findings by Heffernan and Fu (Citation2008), Ozili (Citation2018), and Segoviano and Goodhart (Citation2009). A rise in unemployment can reduce aggregate demand, hence causing an increase in loan default rates. This, therefore, introduces a negative relationship between the unemployment level and the performance of banks (Heffernan & Fu, Citation2008). Again, in line with Segoviano and Goodhart (Citation2009), no statistically significant relationship was found between inflation and financial stability. Institutional quality and debt had their respective expected signs but were found to be statistically insignificant.

Table 2. Stochastic frontier estimates

Table 3. Drivers of inefficiencies in financial stability

4.2. Results of the inefficiency model

In this model, employment, domestic savings, government effectiveness, and regulatory quality are found to have an inverse relationship with the inefficiencies in financial stability. Employment is statistically significant at 1 percent, indicating that an increase in the level of employment improves the volumes of income hence a possibility of increased savings. Domestic saving is also found to relate negatively to inefficiencies in financial stability. Thus, improved savings increases the volumes of reserves or funds with financial institutions. This enhances their credit-related activities hence reduction in inefficiencies. Improved saving deposits, on the other hand, enable banks to create more credits which strengthen their balance sheet and thereby improve the assets of banks leading to an increase in efficiencies. The Monetarists are of the view that financial instability is all about financial institutions being illiquid. Thus, regulators could therefore help to minimize the possibility of panic withdrawals or bank runs. For instance, through the imposition of liquidity buffers and also in a general liquidity crisis, the central bank could play its role as the lender of last resort to banks. Vo et al. (Citation2019) and Borio and Drehmann (Citation2011) for instance, explain that a counter-response by the central bank to the outcome of inflation from the policy implementation, in turn, decreases liquidity that exists in the money market as well as within the financial institutions that could lead to panic in banks and bank runs hence worsening the illiquidity in the money market. The negative sign of the regulatory quality indicates the fact that the formulation and implementation of sound policies and regulations that permit and promote the development of the private sector help in reducing the inefficiencies in financial stability. This confirms the argument by Ozili (Citation2018) who finds a direct relationship between the efficiency of financial stability and regulatory quality. Government effectiveness, though, had the expected sign, it was found to have no statistically significant effect on the inefficiencies in the financial stability of SSA countries.

Arrears in government domestic borrowing is found to be positive and statistically significant at 1 percent. The inability of the government to make repayment on domestically generated debt at the required time increases nonperforming loans (NPLs) of domestic financial institutions. This confirms the International Monetary Fund (IMF; Citation2019) staff reports that government domestic arrears make banks suffer deterioration in the quality of their assets and a rise in NPLs. This distorts the activities of financial institutions, hence paving way for inefficiencies. A financial system that functions well is crucial for the promotion and maintenance of economic growth. Therefore, inefficiencies in financial stability potentially undermine the basic functions of the financial system.

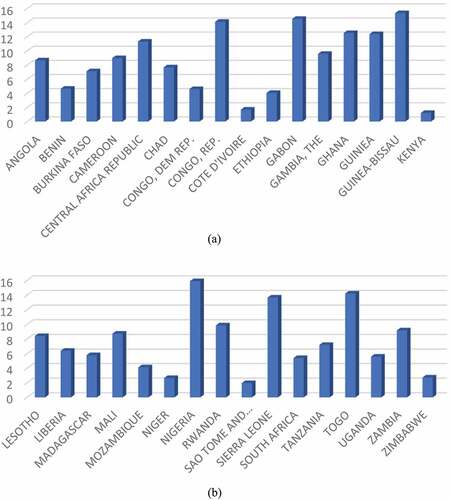

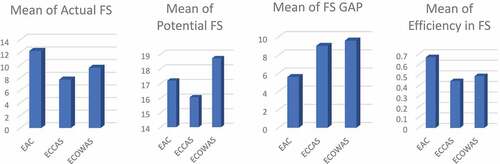

present the mean values of efficiencies, potential, actual, and gaps in financial stability for SSA countries and sub-regional communities in SSA, respectively. There are also presented bar graphs (in ) for visual appreciation. In terms of the mean efficiency for countries, Kenya has the highest ratio followed by Cote d’Ivoire, Niger, Ethiopia, and South Africa. Accordingly, these aforementioned countries recorded the least mean gaps. For the period under consideration, Togo recorded the least ratio in the mean efficiency of financial stability followed by Sierra Leone, the Republic of Congo, Guinea Bissau, and Guinea. Nigeria records the highest potential financial stability value followed by Gabon and Guinea Bissau. Again, for the sub-regional communities, it is found that Eastern Africa’s EAC recorded the highest mean efficiency and actual financial stability. ECOWAS has the highest mean potential financial stability. This confirms findings by Kulu and Appiah-Kubi (Citation2021) which highlight how the greater market share of some banks in Ghana presents positive signs for potential financial stability. Also, for the period the ECCAS had the least mean efficiency and the least actual financial stability. This is in line with the International Monetary Fund (IMF; Citation2019) that huge fiscal shocks have led to the substantial accumulation of arrears among five oil-exporting countries in Central Africa. Thus, this study shows that accumulation of arrears promotes inefficiencies in financial stability hence not surprising that the Central Africa region has the least mean values for efficiency and actual financial stability. It is important to note that there is the risk of cross-country negative spillover effect, especially within the sub-regional communities and also the fact that member countries facing serious financial risks mislead the sub-regional estimates. The noted issues are, however, some of the reasons behind having the estimates for both countries and sub-regional community level. The identified gaps in financial stability for the various countries and the sub-regional communities provide a bigger picture and discussion on financial stability. Knowing the level of stability (actual financial stability) alone may not be enough for the campaign in ensuring overall growth and development through the enhancement of activities in the financial system. Thus, the potential financial stability gives an indication of the benchmark or how far a country or region can go. This is thus, expected to awaken the units in question to work towards reaching the revealed potential. The ECOWAS sub-region records the highest value for potential and second-highest for actual financial stability yet attains the highest for the gap. This explains that there is a wider difference between the two indicators. Thus, given the actual or current stability status, ECOWAS has more room for improvement.

Figure 1. Financial stability (FS) gap in SSA countries.

Figure 2. Mean potential, actual, efficiency and gap in financial stability for sub-regional communities in SSA.

Table 4. Mean of efficiency, potential, actual, and gap in financial stability (FS) in SSA countries (2007 to 2018)

Table 5. Mean of efficiency, potential, actual, and gap in financial stability (FS) in sub-regional groups in SSA (2007 to 2018)

5. Conclusions and recommendations

The essential role of the financial sector in the various economies necessitates such a study. The stochastic Frontier Analysis is used in estimating the financial stability gap and the significant drivers of the inefficiencies in the financial stability of SSA countries. The study found that credit to the private sector and the level of unemployment are the main drivers of financial stability in SSA. Employment, domestic savings, and regulatory quality significantly decrease the inefficiencies in financial stability while government domestic debt arrears enhance financial stability inefficiencies in SSA. Again, the findings show that the top five countries with the highest mean efficiency in financial stability include Kenya, Cote d’Ivoire, Niger, Ethiopia, and South Africa. The top five countries with the highest mean potential financial stability include Nigeria, Gabon, Guinea Bissau, Ghana, and Angola. The top five countries with the highest mean of actual financial stability include Kenya, Cote d’Ivoire, Nigeria, Niger, and Benin. Again, Kenya, Cote d’Ivoire, Sao Tome Principe, Niger, and Zimbabwe are the top five countries with the least mean values of financial stability gap. At the sub-regional community level, the findings show that East Africa’s EAC has the highest mean efficiency value with ECCAS recording the least. West Africa’s ECOWAS has the highest mean value of potential financial stability with Central Africa’s ECCAS having the least. On the mean of financial stability gap, East Africa’s EAC is found to have the least value, while ECOWAS has the highest for the period under study.

It is therefore recommended that government borrowing from the domestic economy should be limited to projects that have undergone proper and the requisite appraisal. This is to ensure that they have a good corresponding economic rate of return so that repayment can be made on time. Financial institutions should minimize credit to the government in financing their budget deficit (while government finds alternative ways of revenue mobilization), and make more credits available to private investors after the requisite appraisals. SSA countries are recommended to introduce employment-oriented programs that are expected to improve income volume and encourage domestic savings in the region. Decisions on the recommendations made at the sub-regional community levels are also encouraged. This is to help member states of the sub-regional groups to improve their financial stability, as a conscious effort to enable them to perform their intended essential role in the economy

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Ahmadzai, H. (2017). Crop diversification and technical efficiency in Afghanistan: Stochastic frontier analysis (No. 17/04). The University of Nottingham, Centre for Research in Economic Development and International Trade (CREDIT), Nottingham.

- Aigner, D., Lovell, C. K., & Schmidt, P. (1977). Formulation and estimation of stochastic frontier production function models. Journal of Econometrics, 6(1), 21–15. https://doi.org/10.1016/0304-4076(77)90052-5

- Anyanwu, A., Gan, C., & Hu, B. (2018). Government domestic debt, private sector credit, and crowding out effect in oil-dependent countries. Journal of Economic Research, 22(2017), 127–151. https://dx.doi.org/10.2139/ssrn.3214288

- Beck, R., Jakubik, P., & Piloiu, A. (2015). Key determinants of non-performing loans: New evidence from a global sample. Open Economies Review, 26(3), 525–550. https://doi.org/10.1007/s11079-015-9358-8

- Borio, C., & Drehmann, M. (2011). Financial instability and macroeconomics: Bridging the gulf. World Scientific Book Chapters, 237–268. https://doi.org/10.1142/9789814322096_0017

- Cantah, W. G., Brafu-Insaidoo, W. G., & Bondzie, E. A. (2022). Domestic arrears and financial stability: The role of institutional factors. Eastern Economic Journal, 48(1), 45–62. https://doi.org/10.1057/s41302-021-00195-7

- Christensen, J. (2005). Domestic debt markets in sub-Saharan Africa. IMF Staff Papers, 52(3), 518–538. https://doi.org/10.2307/30035974

- Das, M. U. S., Surti, J., Ahmed, M. F., Papaioannou, M. M. G., & Pedras, M. G. (2010). Managing public debt and its financial stability implications. International Monetary Fund, 10, 280.

- Fahr, S., & Fell, J. (2017). Macroprudential policy – Closing the financial stability gap. Journal of Financial Regulation and Compliance, 25(4), 334–359. https://doi.org/10.1108/JFRC-03-2017-0037

- Heffernan, S., & Fu, M. (2008). The determinants of bank performance in China. SSRN Electronic Journal. Retrieved July 7, 2017, from http://dx.doi.org/10.2139/ssrn.1247713

- Hjalmarsson, L., Kumbhakar, S. C., & Heshmati, A. (1996). DEA, DFA and SFA: A comparison. Journal of Productivity Analysis, 7(2–3), 303–327. https://doi.org/10.1007/BF00157046

- International Monetary Fund (IMF). (2019). Staff report— Press release; Staff report; Debt sustainability analysis, and statement by the executive director for the Republic of Congo. IMF Country Report 19/244.

- Jokipii, T., & Monnin, P. (2013). The impact of banking sector stability on the real economy. Journal of International Money and Finance, 32(2013), 1–16. https://doi.org/10.1016/j.jimonfin.2012.02.008

- Kasekende, L., & Brownbridge, M. (2011). Post-crisis monetary policy frameworks in sub-Saharan Africa. African Development Review, 23(2), 190–201. https://doi.org/10.1111/j.1467-8268.2011.00280.x

- Klein, N. (2013). “Non-performing loans in CESEE: Determinants and macroeconomic performance. International Monetary Fund (IMF) Working paper, WP/13/72

- Kulu, E., & Appiah-Kubi, G. D. (2021). The relationship between market share and profitability of Ghanaian banks. International Journal of Business, 8(4), 257–269. https://doi.org/10.18488/journal.62.2021.84.257.269

- Mamo, T., Getahun, W., Chebil, A., Tesfaye, A., Debele, T., Assefa, S., & Solomon, T. (2018). Technical efficiency and yield gap of smallholder wheat producers in Ethiopia: A stochastic frontier analysis. African Journal of Agricultural Research, 13(28), 1407 1418. https://doi.org/10.5897/AJAR2016.12050

- Meeusen, W., & van Den Broeck, J. (1977). Efficiency estimation from Cobb-Douglas production functions with composed error. International Economic Review, 18(2), 435–444. https://doi.org/10.2307/2525757

- Minsky, H. P. (1977). The financial instability hypothesis: An interpretation of Keynes and an alternative to “standard” theory. Challenge, 20(1), 20–27. https://doi.org/10.1080/05775132.1977.11470296

- Osiewalski, J., Koop, G., & Steel, M. F. (1997). A stochastic frontier analysis of output level and growth in Poland and western economies. Center for Economic Research, Tilburg University

- Ozili, P. K. (2018). Banking Stability Determinants in Africa. International Journal of Managerial Finance, 14(4), 462–483. https://doi.org/10.1108/IJMF-01-2018-0007

- Saravani, Z., Tash, M. N. S., & Mahmodpour, K. (2015). Evaluation of bank market share and its affective determinants: Sepah bank. International Research Journal of Applied and Basic Sciences, 9(7), 1003–1009. https://www.irjabs.com

- Segoviano, M. A., & Goodhart, C. A. E. (2009). Banking stability measures. No. 627, International Monetary Fund Working Paper No. 04, International Monetary Fund, Washington, DC

- van Duuren, T., de Haan, J., & van Kerkhoff, H. (2020). Does institutional quality condition the impact of financial stability transparency on financial stability? Applied Economics Letters, 27(20), 1635–1638. https://doi.org/10.1080/13504851.2019.1707762

- Vo, D. H., Nguyen, V. M., Quang-Ton Le, P. H. A. T., & Pham, T. N. (2019). The determinants of financial instability in emerging countries. Annals of Financial Economics, 14(2), 1950010. https://doi.org/10.1142/S2010495219500106

Appendices

Table A6. List of SSA countries considered for the study

Table B7. List of countries in the sub-regional communities understudy

Table C8. Variable description and sources

Table D9. Variance inflation factor test for multicollinearity