?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The Bank of Japan (BoJ) conducts an unconventional monetary policy that includes exchange-traded fund (ETF) purchases, which can be expected to affect aggregate equity indices. As equity ETF purchases represent a unique and exceptional monetary policy framework, there are few studies on how such purchases have affected the stock markets or the real economy. The motivation of this paper is therefore to reveal the effectiveness of the BoJ’s equity ETF purchases and contribute to the broad literature on unconventional monetary policy by providing new insights. Ordinary least squares regression analysis is conducted to examine the effects of the BoJ’s ETF purchases and determine whether they are predictable, the effect of expected versus unexpected purchases on aggregate equity indexes differs, and price effects are long lasting. Since the October 2014 increase in the annual volume of ETF purchases by the BoJ, such purchases have become less predictable. Expected purchases do not affect prices, whereas unexpected purchases have a significant, positive price impact. However, this impact is found to be temporary in nature.

1. Introduction

After the global financial crisis (GFC) in 2007–2008, major central banks rapidly lowered their policy rates and hit the zero lower bound (ZLB). Consequently, they introduced so-called unconventional monetary policy (Fischer, Citation2016). According to Borio and Zabai (Citation2018), two types of unconventional monetary policies exist: interest rate policy and balance sheet policy. Interest rate policy includes forward guidance on interest rates and a negative interest rate policy. Balance sheet policy includes exchange rate policy, quasi-debt management policy, credit policy, bank reserve policy, and forward guidance on the balance sheet. Each major central bank deploys a mix of unconventional monetary policy measures suitable for each country and region.

The most popular policy tool within unconventional monetary policy is quantitative easing (QE) policy, which is equivalent to domestic balance sheet policy. For example, the US Federal Reserve (Fed) aggressively reduced rates following the GFC, lowering its policy rate target to 0%–0.25% in December 2008.Footnote1 This reduction brought the rate to the brink of the ZLB. Still, the poor domestic inflation and employment outlook spurred the Fed to launch a large-scale asset-purchasing scheme the same month and begin purchasing US Treasuries (USTs) and mortgage-backed securities (MBS). In Europe, the European Central Bank (ECB) gradually lowered its policy rates following the GFC and the 2010 European debt crisis, ultimately dropping its deposit facility rate to 0% in July 2012.Footnote2 The ECB then shifted to an unconventional monetary policy, introducing forward guidance on policy rates in July 2013Footnote3 and a negative interest rate policy in June 2014.Footnote4 The subsequent slowdown in consumer price index inflation raised the specter of deflation, causing the bank to announce a public sector purchase program in March 2015Footnote5 and a corporate sector purchase program in June 2016.Footnote6

Among the major central banks, the Bank of Japan (BoJ) has been a front-runner in unconventional monetary policy. In 2001, the BoJ introduced a QE policy targeting the current account balances at the BoJ (bank reserves) held by financial institutions.Footnote7 After the GFC, the BoJ adopted comprehensive monetary easing at its monetary policy meeting (MPM) in October 2010 by establishing a temporary asset-purchasing program to buy Japanese government bonds (JGBs), commercial paper, corporate bonds, equity ETFs, and Japanese Real Estate Investment Trusts (J-REIT).Footnote8 After the inauguration of Governor Haruhiko Kuroda in April 2013, the BoJ started a quantitative and qualitative easing (QQE) policy to pave the way for more aggressive asset purchases.Footnote9

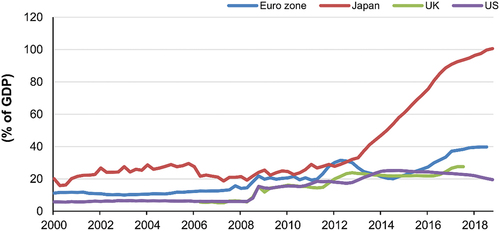

The BoJ’s QE policy was strikingly greater in scale than that of either the Fed or the ECB. As of December 2018, the BoJ’s balance sheet stood at 100.6% of nominal gross domestic product (GDP; see, ). Its QE policy was also distinguished in terms of the breadth of the assets purchased. Its purchase of equity ETFs, which may be considered a type of credit policy as defined by Borio and Zabai (Citation2018), was particularly unusual. However, the policy differs markedly from the credit policy practiced by the Fed and the ECB. While those policies involved corporate bonds and MBS, the assets acquired were fixed-income products. The BoJ is the only major central bank to acquire stocks with no maturity dates.

Figure 1. Central bank assets as a percentage of nominal gross domestic product.

The purchase of stocks is a risk for the BoJ. Share prices are naturally more volatile than bond prices are, and the BoJ faces the potential for substantial losses. In addition, because stocks do not expire, the bank will be forced to sell them at some point to reduce its balance sheet. It cannot passively shrink its balance sheet, as the Fed did, simply by halting reinvestments.

As previously discussed, the BoJ’s equity ETF purchases represent a unique and exceptional monetary policy framework among central banks in developed nations even from a historical perspective. Therefore, there are few studies on how the BoJ’s equity ETF purchases have affected stock markets or the real economy. Ueda (Citation2013) did not explicitly measure the impact of the BoJ’s equity purchases but reported that the comprehensive monetary easing that occurred in 2010 (including the ETF purchasing scheme) and the enhancement of this policy in 2011 had no statistically significant effect on the Topix. Barbon and Gianinazzi (Citation2019) observed the impact of the BoJ’s purchasing operations on stock price returns starting the day policy changes were implemented (31 October 2014 and 29 July 2016). They concluded that every ¥1 trillion in purchasing generated an increase of approximately 20 basis points. However, this increase may also include the effects of changes in the BoJ’s commitment to a more accommodative policy and may not be purely the result of ETF purchases. Harada and Okimoto (Citation2019) examined the impacts of the BoJ’s ETF purchasing program on the Nikkei 225 and found that Nikkei 225 component stocks returns are significantly greater than those of non-Nikkei 225 stocks are when the BoJ purchases ETFs. However, they did not investigate the impact on the Topix, which has been purchased by BoJ mainly since September 2016.

Apart from the BoJ’s equity ETF purchases, Shogbuyi and Steeley (Citation2017) observed how QE policy affected the covariance structure of the equity markets. They concluded that although QE policy reduced the overall volatility of the equity markets, daily operations increased volatility.

Regarding the BoJ’s monetary policy, most existing studies examine the BoJ’s JGB purchasing program after its first QE policy was implemented in 2001. Oda and Ueda (Citation2007) analyzed the yield curve impact of the BoJ’s first QE using a macro-finance model. Kimura and Small (Citation2006) estimated the effect of the BoJ’s initial QE on risky assets, such as corporate bonds. Nakano et al. (Citation2017) investigated how announcements by the BoJ since QQE2 of 2014 and actual supply and demand (i.e., the existing amount of JGB less BoJ holdings) affected JGB yields. Fukunaga et al. (Citation2015) examined the effect of increases in the BoJ’s JGB holdings and the lengthening of its purchasing maturity from the start of the QQE policy in April 2013 through September 2014. Bowman et al. (Citation2015) investigated the impact of the BoJ’s QE on bank lending.

The BoJ has not investigated the effect of its equity ETF purchases. The BoJ conducted a broad analysis of the impact of its JGB purchases in its comprehensive policy assessment of September 2016 but did not extend this analysis to equity ETFs. Therefore, several questions remain open regarding the effectiveness of the BoJ’s equity ETF purchases, such as that of whether these purchases have a meaningful impact on equity prices, and if so, what underlying mechanism influences them. The existing literature does not answer this relatively primitive question. Therefore, the motivation of this research study is to reveal the effectiveness of the BoJ’s unique unconventional monetary policy and contribute to the existing broad literature on QE by providing new insights.

The main contributions of this research study are as follows. First, providing new insight is a reactionary function of central banks. This paper finds that the BoJ determines whether to purchase ETFs on the basis of the equity price returns in the morning session and makes the purchase during the afternoon session, suggesting that equity prices affect the BoJ’s timing of purchases. This paper applies this finding to estimate the reaction function of the BoJ’s equity ETF purchases. Eser and Schwaab (Citation2016) reported that the ECB often decides to buy government bonds given changes in yields that day (i.e., the ECB buys bonds because yields are rising), demonstrating the importance of endogeneity and impact identification. However, they did not estimate the reaction function of the ECB.

This study also divides purchases into anticipated and unanticipated purchases on the basis of the reaction function and determines that only unanticipated purchases have a significant impact on the stock price index. This finding is consistent with those of existing studies on conventional monetary policy. Kuttner (Citation2001) observed, “Interest rates’ response to anticipated target rate changes is small, while their response to unanticipated changes is large and highly significant” (p. 523), This statement is consistent with the financial and economics literature that has determined that unexpected fund flows have a significant impact on equity index returns (Edelen & Warner, Citation2001; Warther, Citation1995). These arguments indicate that anticipated and unanticipated sovereign bond purchasing operations may have dissimilar effects, but existing studiesFootnote10 have not investigated this possibility.

Furthermore, the BoJ’s equity ETF purchasing operations have larger return reversals than the sovereign bond purchasing operations reported in existing studies. In the words of D’Amico and King (Citation2013), this finding indicates that stock effects are minimal relative to flow effects and that the impact of the BoJ’s equity ETF purchasing on equity prices is short-lived. This short horizon could stem from the difference in the BoJ’s market dominance. The BoJ owned 43.2% of all outstanding JGBs as of March 2018, and its equity ETF holdings represented only 2.6% of the First Section of the Tokyo Stock Exchange’s (TSE’s) market value. This percentage also suggests that the signaling effects (or information revelation effects) of equity ETF purchases are weak. These effects are reportedly persistent in sovereign bond purchasing operations (Bauer & Rudebusch, Citation2014; Christensen & Rudebusch, Citation2012; Krishnamurthy & Vissing-Jorgensen, Citation2011). In contrast, because the volume of the BoJ’s ETF purchasing operations is decided in advance annually, daily operations are not indicative of future policy. The signaling effect could also be poor, given the lower correlation between equity ETF purchases and future policy rates than that between sovereign bond purchases and future policy rates.

The remainder of this study is organized as follows. Section 2 explains the details of the BoJ’s equity ETF purchasing operations. Section 3 provides an empirical analysis of the effectiveness of the BoJ’s ETF purchases, including conducting estimations of the reaction function for the BoJ’s operation and identification strategy. Section 4 proposes a theoretical explanation of the empirical results. Section 5 concludes.

2. Details of the BoJ’s ETF purchasing operation

2.1. Scale and timing

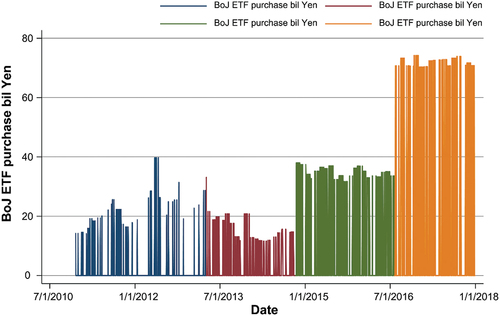

On its website, the BoJ provides daily updates of the results of its ETF purchases. The trend and statistics are depicted in and listed in . The frequency of the BoJ’s purchases increased after the introduction of the QQE in April 2013, and the purchasing volume per offering increased with the launch of the QQE2 in October 2014 and supplementary easing measures implemented in July 2016. The average purchasing volume per offer from the start of their equity 2010 until the ETF purchases at the start of QQE was ¥22.87 billion, and the frequency of their offers was 0.6 times per week. Following the launch of QQE in April 2013, average purchases per offer declined to ¥15.74 billion, but offer frequency increased to 1.4 times per week. After the QQE2 in October 2014, when ETF purchases were raised to an annual level of ¥3 trillion, the volume per offer jumped to ¥34.85 billion, whereas the frequency changed little, at 1.7 times per week. After annual ETF purchases were further increased to ¥6 trillion in July 2016, the volume per offer reached ¥71.43 billion, which reveals that the BoJ responded to the increased annual ETF purchasing volume under QQE2 mainly by increasing its purchasing volume per offer.

Table 1. Summary statistics for the BoJ’s ETF purchases

Figure 2. The BoJ’s exchange-traded fund (ETF) purchasing volume over time, 2010–2018.

2.2. Types of ETFs

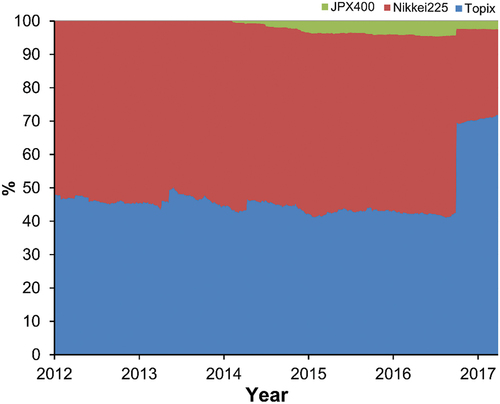

The BoJ’s ETF purchases were initially linked to both the Nikkei225 and the Topix. Subsequent links were established on 31 October 2014, to the JPX400 ETF, and on 18 December 2015, to support firms proactively investing in physical and human capital expenditure (capex)-related ETFs (¥0.3 trillion in purchases per year). The amount of each ETF purchase, other than the capex ETFs, was proportional to the total market capitalization of each ETF. The BoJ altered this amount on 21 September 2016, such that ¥3 trillion of its annual ¥5.7 trillion (¥6.0−¥0.3 trillion) in purchases was used for tracking the three indices in proportion to the ETFs’ market capitalization, whereas the remaining ¥2.7 trillion was reserved for Topix-linked ETFs. shows my estimation of the composition of the BoJ’s ETF purchases based on their market capitalization data. Before September 2016, approximately half of the BoJ’s ETF purchases were linked to the Topix; however, after October 2016, the weight of the ETFs linked to the Topix was approximately 70%.

Figure 3. Composition of the BoJ’s ETF purchases, 2012–2017.

3. Research methods and empirical analysis

3.1. Simple OLS regression analysis

First, this paper uses OLS regressions to analyze whether the BoJ’s ETF purchases had any impact on equity price indices. This setting is similar to those in Krishnamurthy and Vissing-Jorgensen (Citation2012) and D’Amico and King (Citation2013), who analyzed the impact of government bond purchases on bond prices as follows:

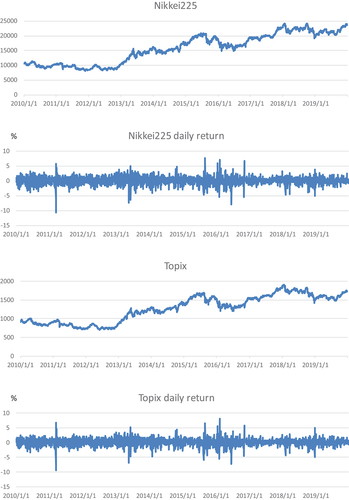

where ∆s represents the daily return on the Nikkei225 or the Topix, and ∆sp represents the daily return on the S&P500. S&P500 returns are necessary to control the linkage between Japan and US stock markets. ∆fx represents the return on the exchange rate of US dollar (USD)/Japanese yen (JPY) from 3:00 p.m. the previous day to 3:00 p.m. the current day. The foreign exchange (FX) rate is important information, particularly for determining stock prices for exporters, typically large manufacturing companies, and 3:00 p.m. is the time that trading on the TSE ends. In addition, the USD/JPY captures the degree of uncertainty of the financial markets. Fatum and Yamamoto (Citation2016) found that the JPY is the safest among the safe-haven currencies and that the JPY appreciates as market uncertainty increases because of higher geopolitical risk and economic policy uncertainty. Therefore, the USD/JPY is an important determinant for the Japanese equity markets. boj represents the BoJ’s ETF purchasing volume (in billions of yen). Descriptive statistics on asset price returns are available in . shows the historical charts for the USD/JPY, the Nikkei225, the Topix, and the S&P500 and their daily returns. The hypothesis here is that BoJ’s equity ETF purchasing has a positive impact on equity prices.

Table 2. Descriptive statistics based on the BoJ’s ETF purchases

Figure 4. Historical charts for the Nikkei225, Topix, S&P500, and USD/JPY, 2010–2019.

Figure 4. Continued.

provides the estimation results. An unexpected finding is that the BoJ’s ETF purchases have a statistically significant negative effect on equity returns. However, such an effect is natural, given the timing of the bank’s ETF purchases. Financial market participants broadly understand that the BoJ checks the movement of equity prices during the morning session and conducts ETF purchases in the afternoon session when equity indices fall to a certain extent (Lewis, Citation2017). Therefore, the BoJ’s ETF purchasing activity is a signal that equity prices declined that day. Consequently, the results in are consistent with the view of market participants, which is also consistent with Eser and Schwaab’s (Citation2016) findings that the ECB’s bond purchases sometimes corresponded to a rise in bond yields (i.e., a decline in prices). They attributed this relationship to the impact identification problem, wherein the ECB tends to purchase bonds when yields rise. Therefore, to estimate the impact of asset purchases by central banks, we must identify the causality between asset prices and asset purchases. The daily frequency is too low; at least a twice per day frequency is necessary to identify the impact of the BoJ’s ETF purchases.

Table 3. Estimation results of simple OLS regression EquationEquation (1)(1)

(1)

3.2. Reaction function for the BoJ’s ETF purchases

The literature on estimating the reaction function for a central bank’s market operations is rather abundant in foreign exchange interventions. This study follows Dominguez (Citation1998) and Kim and Sheen (Citation2002) and constructs a probit model that explains a binary variable for the BoJ’s purchases (i.e., a variable that takes the value of 1 for a day with purchases and the value of 0 for a day without purchases) in terms of equity price index returns during the morning session.

where ∆sam represents the returns in the morning session for the Nikkei225 or the Topix, and Ф represents a cumulative standard normal distribution. The parameter is expected to be negative.

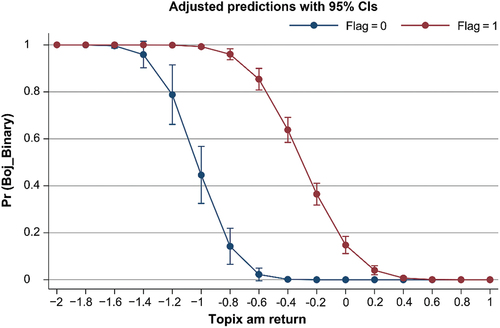

reveals that the parameters for Topix and Nikkei225 morning returns are statistically significant and negative, indicating that the greater the drop in the indices during the morning session the greater the likelihood of an ETF purchasing operation being conducted by the BoJ. Interestingly, the R2 value for the Topix is higher, suggesting that the BoJ gives greater weight to the Topix in deciding whether to proceed with ETF purchases. The R2 value for the subsample from 15 December 2010 to 3 April 2013, is also higher, suggesting that the rule for ETF purchasing became complicated after the launch of the QQE in April 2013. Additionally, the QQE period from 4 April 2013 to 29 December 2017, had smaller coefficients for the Topix and the Nikkei225. This finding suggests that the bank carried out ETF purchases under the QQE even after less significant market drops, which is consistent with the rise in their actual purchasing frequency. The required decline in the equity indices for a 50% probability for the BoJ making a purchase is—1.0% for the Topix during the December 2010 to April 2013 sample period (before the QQE) and—0.3% during the April 2013 to December 2017 sample period (after the QQE; see, ).

Table 4. Estimation probit model results EquationEquation (2)(2)

(2)

Figure 5. Estimated probability of the BoJ’s ETF purchases using the probit model.

indicates the predictive power of my probit model with the Topix during the estimation period from December 2010 to April 2013 and from April 2013 to December 2017, respectively. The model’s predictive power is significantly higher before the QQE; its percentage of correct classifications (i.e., the model predicts a purchase and the BoJ subsequently makes one, as well as the reverse) is 99.65%. This percentage was lower after the QQE, at 90.89%.

Table 5. Predictive power of the probit model

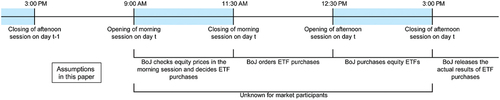

Based on this finding, the anticipated timeframe for the BoJ’s ETF purchases can be observed in .

Figure 6. Assumed timeframe for the BoJ’s ETF purchasing operation.

3.3. OLS regression with half-day data

For an accurate estimation of the effects of the BoJ’s ETF purchases, the stock returns in the afternoon session (12:30 p.m.–3:00 p.m.) must be regressed by the BoJ’s ETF purchasing volume. This identification strategy follows Edelen and Warner (Citation2001). The explanatory variables include the morning returns for equity price indices and afternoon returns for the USD/JPY.

where ∆spm and ∆sam represent returns in the afternoon and morning sessions for the Nikkei225 and the Topix, respectively, ∆fxpm represents the returns on the USD/JPY from 11:30 a.m. to 3:00 p.m., and boj represents the BoJ’s ETF purchasing volume (in billions of yen). The duration of the USD/JPY is from 11:30 a.m. and not 12:30 p.m. because stock prices in the afternoon session should reflect the information available after the morning session, which ends at 11:30 a.m. S&P500 returns are excluded because the information is already discounted in the morning session. The parameter is expected to be positive (i.e., the BoJ’s equity ETF purchasing is expected to increase equity prices).

Given these adjustments, the BoJ’s ETF purchasing coefficient is a statistically significant positive figure (). In addition, parameters on the BoJ’s ETF purchases are greater before the QQE, indicating the diminishing marginal impact of the BoJ’s ETF purchases. Before the QQE, ¥70 billion in purchases led to a 0.81% rise in the Nikkei225 in the afternoon session and a 0.22% increase after the QQE.

Table 6. OLS regression results for afternoon returns Equation (3)

3.4. Expected and unexpected purchases

Using the results of the probit model in Section 3.2, this study now explores how the BoJ’s expected and unexpected JGB purchasing operations influence equity prices. Before the QQE, the timing of the BoJ’s ETF purchases was almost predictable. However, because the rule for ETF purchases became complicated after the QQE, the timing of the BoJ’s ETF purchases should feature some surprises.

This study defines purchasing operations in the probit model with a probability higher than 95% as expected and those with a probability lower than 95% as unexpected.Footnote11 Therefore, Equation (3) is modified as follows:

where ∆spm and ∆sam represent returns in the afternoon and morning sessions for the Nikkei225 and Topix, respectively; ∆fxpm represents the returns on the USD/JPY from 11:30 a.m. to 3:00 p.m.; and bojexp and bojunexp denote expected and unexpected purchases, respectively, in billions of yen. The estimation results in indicate that the coefficient for unexpected purchases is statistically significant for either the Topix or the Nikkei225, whereas the coefficient for expected purchases is not significant for the Nikkei 225. In addition, the coefficient for expected purchases is less than that for unexpected purchases. These findings are consistent with those of Warther (Citation1995), who examined the effect of aggregate-level fund flows on equity indices and found that unexpected fund flows have a significant impact on equity index returns.

Table 7. Impact of expected and unexpected ETF purchases by the BoJ EquationEquation (4)(4)

(4)

For expected purchases, the BoJ’s acquisition of ETFs is discounted in advance by the markets (perhaps during the morning session), limiting the impact on returns in the afternoon session. However, in the case of unexpected purchases, limited prior discounting occurs, which leads to a statistically significant impact on equity prices in the afternoon session. Another possible explanation for the results in is that expected purchases by the BoJ are absorbed by arbitrageurs in the afternoon session, but unexpected purchases are not. This explanation is discussed in detail in Section 4.

These findings are consistent with existing monetary policy studies that indicate that policy changes require the element of surprise to have a significant influence on asset prices (Kuttner, Citation2001).

3.5. Return reversal

If unexpected purchases affect equity prices through the price pressure hypothesis (Warther, Citation1995), that is, if the BoJ’s ETF purchases affect equity prices through changes in supply and demand conditions in the market, they lead to a temporary divergence in equity prices from their fundamental values, subsequently prompting reversal of returns to their fundamental values. To examine this effect, this study estimates a regression model using the OLS method that explains stock returns in the morning session in terms of the previous day’s unexpected purchases.

where ∆sam and ∆spm represent returns in the morning and afternoon sessions for the Nikkei225 and the Topix, respectively; ∆fxam represents returns on the USD/JPY from 3:00 p.m. the previous day to 11:30 a.m. the current day; ∆sp represents daily returns on the S&P500; and bojunexp represents the BoJ’s unexpected ETF purchasing volume (in billions of yen). The duration of the USD/JPY is from 3:00 p.m. the previous day because stock prices in the morning session should reflect the information available after the previous day’s afternoon session, which ends at 3:00 p.m.

The estimation results are shown in . The coefficients for the previous day’s unexpected purchases for both the Nikkei225 and the Topix are significantly negative, which confirms that a return reversal indeed occurred, supporting the notion that the price pressure hypothesis took effect. This finding is consistent with that of Edelen and Warner (Citation2001), who investigated large institutional fund flows and determined that such flows led to significant return reversals.

Table 8. OLS regression results for returns reversals EquationEquation (5)(5)

(5)

Thus, the BoJ’s ETF purchases have a significant effect on daily equity prices; however, given the return reversal the following day, a long-term persistent impact on equity prices is unlikely. These results challenge the objective of the BoJ’s ETF purchases—to influence the equity risk premium.Footnote12

4. Theoretical and practical underpinnings of the estimated outputs

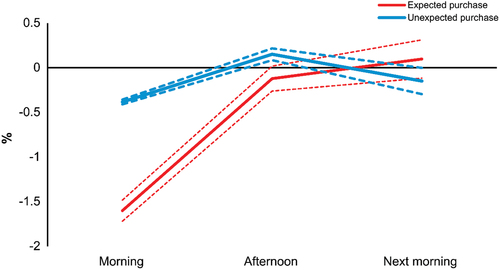

The results in and can be summarized in . When the BoJ conducts expected ETF purchases, the morning session’s Topix return is deeply negative, which is why market participants can expect afternoon purchases by the BoJ. The expected purchases lead to negative Topix returns in the afternoon session and approximately zero returns in the next day’s morning session. In contrast, when the BoJ engages in unexpected purchases, the morning session’s Topix returns are higher than that of unexpected returns, which makes it difficult to correctly forecast the BoJ’s future purchases. The Topix return is positive in the afternoon session and negative in the morning session the next day. What are the possible theoretical and practical underpinnings of this phenomenon?

Figure 7. Topix returns when the BoJ purchases ETFs.

Warther (Citation1995) suggested that fund flows affect asset prices via two channels—information revelation and price pressure. Applying this hypothesis to a central bank’s asset-purchasing program enables information revelation to be regarded as the signaling effect (Oda & Ueda, Citation2007). Through its bond purchases, a central bank signals the market that it will continue to guide yields in the future to low levels, thus affecting long-term interest rates (Bernanke et al., Citation2004). The same thing could happen with equity ETF purchases. For example, when equity prices declined significantly in the morning session and the BoJ subsequently skipped making equity ETF purchases, some market participants began expecting a scaling back of the policy (Lewis, Citation2020). That said, the BoJ announces its annual equity purchases in advance, making its daily buying activity unlikely to include information on future policies. Therefore, asset prices are affected through the price pressure channel. In fact, the occurrence of return reversals the day after an unexpected ETF purchase helps support the price pressure hypothesis. Because the BoJ announces only its annual equity purchasing volume, the pace of purchases during the year is uncertain. Therefore, the BoJ’s purchases could change the expectation of market participants regarding the pace of near-future purchases. For example, market participants might expect a slower pace of purchasing going forward if the BoJ made significant purchases in the past.

Furthermore, the finding that unexpected ETF purchases have a significant impact on equity prices should be consistent with the “Limits of Arbitrage” in Gromb and Vayanos (Citation2010) and “Slow-Moving Capital” in Duffie (Citation2010). The BoJ’s unexpected purchases can be regarded as a demand shock accompanying the uncertainty arising from the lack of prior BoJ announcements regarding the timing of its ETF purchases. If arbitrageurs (i.e., frequent investors) are unable to supply liquidity immediately in the case of a demand shock, given constraints, such as leverage regulation or capital shortages, the positive demand shock cannot be quickly absorbed, causing stock prices to increase. Meanwhile, for expected purchases, price concessions are sought in advance, causing prices to change prior to the actual purchase. Still, the argument holds that price pressures last one-half of a day at most and that price changes are not as sustainable as indicated by Duffie (Citation2010). However, the duration is much shorter than the duration found in existing studies because equity-index-linked ETFs have high liquidity and are only one of several derivative products available on the market.

5. Conclusion

The BoJ introduced comprehensive monetary easing at its MPM on 5 October 2010, which established an asset-purchasing program to buy equity ETFs. The BoJ’s equity ETF purchases are exceptional among central banks in developed nations even from a historical perspective. However, scant research exists on how this policy has affected stock markets or the real economy. This study seeks to answer the following questions: Have the BoJ’s ETF purchases had a meaningful impact on equity price indices? If so, what is the mechanism underlying the impact?

First, by estimating a probit model for BoJ purchasing decisions, this paper determined that the BoJ conducts ETF purchasing operations in the afternoon sessions when equity indices decline to a certain extent during the morning session, making the operations highly predictable. This strategy is consistent with market participants’ sense of practicality.

Second, expected and unexpected operations have entirely different effects on stock prices. This study found a statistically significant impact on stock prices only in the latter case. The existing literature on monetary policy has demonstrated that policy changes need an element of surprise to have a significant influence on asset prices—this study reached the same conclusion regarding the BoJ’s ETF purchasing operations.

Third, this paper confirmed a reversal effect, with stock prices suffering a statistically significant decline on the morning of the day after unexpected purchasing operations occur. In other words, the BoJ’s ETF purchases have only a temporary effect on stock prices. These results challenge the objective of the BoJ’s ETF purchases—to influence the equity risk premium.

This paper highlights possible future research avenues on a central bank’s QE program. First, distinguishing between expected and unexpected purchases is important for both equity ETF purchases as well as sovereign bond purchases. For example, the BoJ started to announce a schedule of JGB purchasing operations in March 2017, which made the timing of the purchases perfectly predictable. This predictability could change the impact of the JGB purchasing operation. Second, this paper investigated the impact of equity ETF purchases on stock prices. However, conducting an analysis of the risk premium might be more plausible as the BoJ’s objective is the equity risk premium and not stock prices. In the future, an analysis of the influence of the BoJ’s equity ETF purchasing operations on the risk premium should be conducted.

Acknowledgements

I would like to thank Sumihiro Takeda, Yoshitaka Fukui, Taiju Kitano, Mikihiro Matsuoka, Mitsuru Morita, Masao Muraki, Masaaki Shirakawa, and Michael Spencer for their helpful comments.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

10. See, for example, Gagnon et al. (Citation2011), Joyce et al. (Citation2011), Hancock and Passmore (Citation2011), Hamilton and Wu (Citation2012), Krishnamurthy and Vissing-Jorgensen (Citation2012), D’Amico and King (Citation2013), and Neely (Citation2015).

11. The standard threshold is 50%; however, given the high predictability of my probit model, 50% tilts the sample size.

References

- Barbon, A., & Gianinazzi, V. (2019). Quantitative easing and equity prices: Evidence from the ETF Program of the Bank of japan. The Review of Asset Pricing Studies, 9(2), 210–20. https://doi.org/10.1093/rapstu/raz008

- Bauer, M. D., & Rudebusch, G. D. (2014). The signaling channel for federal reserve bond purchases. International Journal of Central Banking, (September), 233–289.

- Bernanke, B., Reinhart, V., & Sack, B. (2004). Monetary policy alternatives at the zero bound: An empirical assessment. Brookings Papers on Economic Activity, 2(2), 1–100. https://doi.org/10.1353/eca.2005.0002

- Borio, C., & Zabai, A. (2018). Unconventional monetary policies: A re-appraisal. Research Handbook on Central Banking, 398–444. https://doi.org/10.4337/9781784719227.00026

- Bowman, D., Cai, F., Davies, S., & Kamin, S. (2015). Quantitative easing and bank lending: Evidence from Japan. Journal of International Money and Finance, 571, 15–30. https://doi.org/10.1016/j.jimonfin.2015.05.002

- Christensen, J. H. E., & Rudebusch, G. D. (2012). The response of interest rates to US and UK quantitative easing. The Economic Journal, 122(564), 385–414. https://doi.org/10.1111/j.1468-0297.2012.02554.x

- D’Amico, S., & King, T. B. (2013). Flow and stock effects of large-scale treasury purchases: Evidence on the importance of local supply. Journal of Financial Economics, 108(2), 425–448. https://doi.org/10.1016/j.jfineco.2012.11.007

- Dominguez, K. M. (1998). Central bank intervention and exchange rate volatility. Journal of International Money and Finance, 17(1), 161–190. https://doi.org/10.1016/S0261-5606(97)98055-4

- Duffie, D. (2010). Presidential address: Asset price dynamics with slow-moving capital. The Journal of Finance, 65(4), 1237–1267. https://doi.org/10.1111/j.1540-6261.2010.01569.x

- Edelen, R. M., & Warner, J. B. (2001). Aggregate price effects of institutional trading: A study of mutual fund flow and market returns. Journal of Financial Economics, 59(2), 195–220. https://doi.org/10.1016/S0304-405X(00)00085-4

- Eser, F., & Schwaab, B. (2016). Evaluating the impact of unconventional monetary policy measures: Empirical evidence from the ECB’s Securities Markets Programme. Journal of Financial Economics, 119(1), 147–167. https://doi.org/10.1016/j.jfineco.2015.06.003

- Fatum, R., & Yamamoto, Y. (2016). Intra-safe-haven currency behavior during the global financial crisis. Journal of International Money and Finance, 66(September), 49–64. https://doi.org/10.1016/j.jimonfin.2015.12.007

- Fischer, S. (2016, January 3). Monetary policy, financial stability, and the zero lower bound. A speech at the Annual Meeting of the American Economic Association, San Francisco, California.

- Fukunaga, I., Kato, N., & Koeda, J. (2015). Maturity structure and supply factors in Japanese government bond markets. Monetary and Economic Studies, 33(November), 45–95.

- Gagnon, J., Raskin, M., Remache, J., & Sack, B. (2011). The financial market effects of the Federal Reserve’s large-scale asset purchases. International Journal of Central Banking, 7(March), 3–43.

- Gromb, D., & Vayanos, D. (2010). Limits of arbitrage. Annual Review of Financial Economics, 2(1), 251–275. https://doi.org/10.1146/annurev-financial-073009-104107

- Hamilton, J. D., & Wu, J.C. (2012). The effectiveness of alternative monetary policy tools in a zero lower bound environment. Journal of Money, Credit and Banking, 44(s1), 3–46. https://doi.org/10.1111/j.1538-4616.2011.00477.x

- Hancock, D., & Passmore, W. (2011). Did the federal reserve’s MBS purchase program lower mortgage rates. Journal of Monetary Economics, 58(5), 498–514. https://doi.org/10.1016/j.jmoneco.2011.05.002

- Harada, K., & Okimoto, T. (2019). The BOJ’s ETF purchases and its effects on Nikkei 225 stocks. International Review of Financial Analysis, 77(October), 101826. https://doi.org/10.1016/j.irfa.2021.101826

- Joyce, M., Lasaosa, A., Stevens, I., & Tong, M. (2011). The financial market impact of quantitative easing in the United Kingdom. International Journal of Central Banking, 7(September), 113–161.

- Kim, S.-J., & Sheen, J. (2002). The determinants of foreign exchange intervention by central banks: Evidence from Australia. Journal of International Money and Finance, 21(5), 619–649. https://doi.org/10.1016/S0261-5606(02)00011-6

- Kimura, T., & Small, D. H. (2006). Quantitative monetary easing and risk in financial asset markets. Topics in Macroeconomics, 6(1), 1–54. https://doi.org/10.2202/1534-5998.1274

- Krishnamurthy, A., & Vissing-Jorgensen, A. (2011). The effects of quantitative easing on long-term interest rates. Brookings Papers on Economic Activity, 2(2), 215–265. https://doi.org/10.1353/eca.2011.0019

- Krishnamurthy, A., & Vissing-Jorgensen, A. (2012). The aggregate demand for treasury debt. Journal of Political Economy, 120(2), 233–267. https://doi.org/10.1086/666526

- Kuttner, K. N. (2001). Monetary policy surprises and interest rates: Evidence from the fed funds futures market. Journal of Monetary Economics, 47(3), 523–544. https://doi.org/10.1016/S0304-3932(01)00055-1

- Lewis, L. (2017, November 7). Japan faces ‘Brewster’s millions’ challenge. Financial Times. https://www.ft.com/content/844a6cd4-c2d5-11e7-a1d2-6786f39ef675

- Lewis, L. (2020, January 22). One vital prop could be wobbling for the Japanese stock market. Financial Times. https://www.ft.com/content/164012f0-20c7-11ea-b8a1-584213ee7b2b

- Nakano, M., Takahashi, A., Takahashi, S., & Tokioka, T. (2017). On the effect of Bank of Japan’s outright purchase on the JGB yield curve. Asia-Pacific Financial Markets, 25, 47–70. https://doi.org/10.1007/s10690-018-9238-5

- Neely, C. J. (2015). Unconventional monetary policy had large international effects. Journal of Banking & Finance, 52(March), 101–111. https://doi.org/10.1016/j.jbankfin.2014.11.019

- Oda, N., & Ueda, K. (2007). The effects of the Bank of Japan’s Zero interest rate commitment and quantitative monetary easing on the yield curve: A Macro-Finance Approach. The Japanese Economic Review, 58(3), 303–328. https://doi.org/10.1111/j.1468-5876.2007.00422.x

- Shogbuyi, A., & Steeley, J. M. (2017). The effect of quantitative easing on the variance and covariance of the UK and US equity markets. International Review of Financial Analysis, 52(July), 281–291. https://doi.org/10.1016/j.irfa.2017.07.009

- Ueda, K. (2013). Response of asset prices to monetary policy under abenomics. Asian Economic Policy Review, 8(2), 252–269. https://doi.org/10.1111/aepr.12026

- Warther, V. A. (1995). Aggregate mutual fund flows and security returns. Journal of Financial Economics, 39(2–3), 209–235. https://doi.org/10.1016/0304-405X(95)00827-2