Abstract

The real challenge to many practitioners in the financial and investment sector is to accurately profile risk-averse investors to still be inclusive of these investors in the wealth creation process. This study aims to profile risk-averse investors through a structural equation model based on endogenous and exogenous factors. The final sample size consisted of 463 individual investors in the economic hub of South Africa, Gauteng province. These endogenous and exogenous factors may bring about increases or decreases in the risk tolerance levels of investors and accordingly, influence their decisions to initiate, amend or terminate financial behaviours. These factors significantly contributed towards explaining low-risk tolerance behaviour, which assisted with the successful development of a model to profile the risk tolerance behaviour of risk-averse investors. This risk profiling model makes a remarkable and unique contribution to the field of study and the financial industry, since it will assist financial practitioners to profile the risk tolerance behaviour of risk-averse investors more accurately, which will lead to the successful implementation of investment strategies.

1. Introduction

Warren Buffet asserted that “investing is simple, but not easy”. The difficulties that investors and financial practitioners are confronted with in the identification and implementation of suitable investment strategies are represented by this eloquent phrase (Jacobsen et al., Citation2014). These difficulties frequently take on preferences that relate to how risk is perceived by investors and accordingly, how they behave towards risk. The issue with not considering risk tolerance is that perceptions lead to actions. In traditional finance theory, it is stipulated that investors make rational investment decisions to maximise their return on investment (Baghani & Sedaghat, Citation2014; Chaudhary, Citation2013). Nonetheless, in the real world, decisions made by investors deviate from theory and are primarily driven by their attitudes and perceptions towards risk (Jacobsen et al., Citation2014; Van den Bergh, Citation2018). Mutswenje (Citation2014) affirmed that investors have a tendency to behave irrationally with uncertainty and fear of loss for the future, irrespective of how well-educated they are and their considerable level of financial and investment knowledge. Due to the effect of financial choices and every day changes on investment activities, the willingness and abilities to take risks differ among investors (Gilliam et al., Citation2010). Investment decisions are often driven by the investors’ risk perception rather than the actual risk involved in investing (Davey, Citation2012). Therefore, it is important to understand the behaviours associated with risks.

Risk tolerance is a prominent concept applied in the financial industry and it is considered when planning and selecting the investment strategies of investors (Rutgers, Citation2014). Risk tolerance is referred to as the willingness to partake in risky behaviour where there is a possibility that the expected outcome may be unfavourable (Davey & Resnik, Citation2008; Grable, Citation2017; Irwin, Citation1993). Measuring risk tolerance can be difficult as subjectivity plays a part when taking risks. When assessing risk, two major elements need to be considered. These elements are risk attitude, which is the amount of risk a given investor is willing to take, and risk capacity, which refers to the amount of risk a given investor can take. Risk attitude covers psychological and personality aspects, while risk capacity covers financial aspects (Boone & Lubitz, Citation2003). Additionally, to the financial and psychological aspects of risk tolerance, the latter can either be objective or subjective. The subjective aspect of risk tolerance is generally grounded in the economic theory of risk aversion. The objective aspect is grounded on Malkiel’s notion of household financial situation, which affirms that investors’ abilities to take risks depend on their financial conditions (Malkiel, Citation1996).

Accordingly, the willingness of investors to tolerate risks can be measured through risk assessment forms. Risk assessment forms are utilised by financial practitioners to measure the risk tolerance of investors with the intention of matching the investor’s risk profile with a selection of suitable investments (Coronation Fund Managers, Citation2013). However, these forms are not comprehensive enough to consider all the factors that could influence the willingness of investors to tolerate risks. The measurement of risk tolerance is multifaceted and surpasses the completion of a simple risk assessment form. Investors and financial practitioners need to apply four factors when constructing investment strategies, namely financial circumstances, financial needs, risk capacity and risk appetite. The relations between these four frequently contradictory factors are astonishingly multifaceted (Coronation Fund Managers, Citation2018).

Hence, the main problem statement of this study is formulated against the fact that existing and conventional risk assessment forms used by practitioners in the financial industry have shortcomings as it is not comprehensive enough to consider all the factors that may affect the risk tolerance behaviour of investors when making investment decisions. Although several studies have been conducted by researchers, such as Grable et al. (Citation2009), Larkin et al. (Citation2013), Baghani and Sedaghat (Citation2014), Mutswenje (Citation2014), Kuzniak and Grable (Citation2017), Hemrajani and Sharma (Citation2018), and Dickason and Ferreira (Citation2019), as well as Lawrenson (Citation2020), to investigate the factors that influence the risk tolerance of investors when making investment decisions, there is no evident studies that examined the influence of a multitude of both endogenous and exogenous factors on investor risk tolerance behaviour. Previous research studies have also not focused on and addressed the deficiencies of existing and conventional risk assessment forms used by practitioners in the financial industry. Furthermore, South Africa can be a high-risk investment for those investors who usually are less inclined to take on risks. Such risk-averse investors tend to take fewer risks or are not able to take any risks, and consequently, tend to accept lower returns to preserve the real value of their investment portfolios (Goodall, Citation2005). The real challenge to many practitioners in the financial industry is to accurately profile the risk tolerance behaviour of risk-averse investors to still be inclusive of these investors in the wealth creation process. Therefore, the primary objective of this study is to construct a model that will assist to profile the risk tolerance behaviour of risk-averse investors based on endogenous and exogenous factors.

2. Literature review

This section of the paper contextualises the risk profile process and the endogenous and exogenous factors influencing investor risk tolerance behaviour.

Nobre and Grable (Citation2015) asserted that investors expect investment companies to construct, measure and evaluate strategies that will assist them to make successful investment decisions. Financial planners are operating in an environment where it is prudent and legally required to be acquainted with investors’ financial, attitudinal and emotional circumstances before making recommendations with regard to investment decisions (Brayman et al., Citation2017). Risk assessment forms, which are constructed on the basis of institutional intellect with reference to rational investor behaviour, are employed by financial practitioners to measure the risk tolerance behaviour of investors (Coronation Fund Managers, Citation2016; Di Dottorato, Citation2013). Nevertheless, as emphasised by Brayman et al. (Citation2017) a lack of regulatory guidance on risk profiling in the financial industry led to a varied approach to risk profiling assessments.

There have been many deliberations regarding risk profiling and its significance, or deficiency thereof, to establish suitable investment strategies for investors. The main problem is formulated against the fact that existing and traditional risk assessment forms used by practitioners in the financial industry have shortcomings. It is not comprehensive enough to consider all the factors that may affect the risk tolerance behaviour of investors when making investment decisions. The current risk profiling approach in the financial industry involves a standardised and one-size-fits-all approach (Masthead, Citation2019). Dickason (Citation2017) also indicated that risk assessment forms used by financial planners do not make provision to examine and measure irrational behaviour of investors.

Moreover, the gathering of information is a key step in the investment planning process. It is vital that the correct questions are asked to obtain a comprehensive understanding of the investor (Masthead, Citation2019). Investors will provide financial planners with valuable information that should be employed to determine their risk tolerance behaviour. Financial planners need to be discerning given that the information will come from effective communication with the investors and not from standardised risk assessment forms as it consists of too few questions and the incorrect types of questions (Jacobsen et al., Citation2014; Kitches, Citation2018). Brayman et al. (Citation2017) stated that it is argued that only asking a few questions cannot adequately measure the elements associated with an investor’s risk profile. A wider range of possible outcomes should be included to improve risk assessment forms. Therefore, existing risk assessment forms should be improved by recommending a framework that makes provision for client-specific questions by taking into account the factors that influence risk tolerance behaviour. It is fundamental for investors and financial practitioners to comprehend the factors related to risk tolerance behaviour as it has a momentous influence on the investment decisions of investors. Risk tolerance behaviour is influenced by multiple factors that can be summarised into two categories, namely endogenous and exogenous factors (Grable, Citation2016; Guillemette & Nanigian, Citation2014; Van de Venter et al., Citation2012).

provides an illustration of the endogenous and exogenous factors that influence investor risk tolerance behaviour.

Figure 1. Endogenous and exogenous factors influencing investor risk tolerance behaviour.

The endogenous and exogenous factors that influence the risk tolerance behaviour of investors are reviewed in the following subsections.

2.1. Endogenous factors

Endogenous factors are referred to as inherent characteristics or personality elements unique to individuals (Grable, Citation2016). Endogenous factors comprise demographical factors (age, gender, ethnicity, marital status, employment status, education, income and wealth, homeownership, household size and financial dependants), socio-cultural factors (religion, financial and investment knowledge and health status), the investor lifecycle (growth investor phase and defensive (cautious) investor phase) and behavioural finance biases (representativeness, overconfidence, anchoring, gambler’s fallacy, availability bias, loss aversion, regret aversion, mental accounting, self-control; Grable, Citation2016; Grable & Joo, Citation2004; Irwin, Citation1993; Van den Bergh−lindeque, Citation2020). These endogenous factors are discussed below.

Demographical factors: refers to statistical data of the socio-economic characteristics of a population (Merriam-Webster Dictionary, Citation2022).Numerous demographical factors, namely age, gender, ethnicity, marital status, employment status, education,, income and wealth, homeownership, as well as household size and number of financial dependants are to be taken into consideration when examining its relation to risk tolerance behaviour (Sung & Hanna, Citation1996; Van den Bergh−lindeque, Citation2020).

Socio-cultural factors: refers to the differences between groups of individuals in relation to the social class and society in which they live (Cambridge Dictionary, Citation2022). Socio-cultural factors comprises religion, financial and investment knowledge and health status (Van den Bergh−lindeque, Citation2020).

Investor lifecycle: signifies the investment behaviour of investors over the different phases of their lives given their age and time horizon (Cocco et al., Citation2005; Shaikat, Citation2020). According to the life cycle theory, the risk tolerance behaviour of investors declines with age given that they have less time to recuperate probable losses (Marx et al., Citation2010). The investor lifecycle can be categorised into two categories, namely the growth investor phase and defensive (cautious) investor phase (Van den Bergh−lindeque, Citation2020).

Behavioural finance biases: Investigates how the unpredictable nature of human psychology influences investment decision-making (Rossini & Maree, Citation2015). The behavioural finance biases encompasses representativeness, overconfidence, anchoring, gambler’s fallacy, availability bias, loss aversion, regret aversion, mental accounting and self-control. These behavioural finance biases are described in .

Table 1. Behavioural finance biases

2.2. Exogenous factors

Exogenous factors are referred to as factors or events that are related to the external environment which may bring about changes and fluctuations in financial markets (Van den Bergh−lindeque, Citation2020). Exogenous factors include political-legal factors, technological factors, tax implications, macroeconomic factors (interest rates, exchange rates, inflation, gross domestic product (GDP)), market fluctuations and volatility and the international stock market and economic events (Kuzniak & Grable, Citation2017; Rossini & Maree, Citation2015; Van den Bergh−lindeque, Citation2020). As financial markets are characterised by fluctuations and changes, investors and financial practitioners should be considerate to changes in the external environment and the effect these changes may have on investment decision-making. Having knowledge of the external environment will assist investors and financial practitioners to draw on opportunities and to prepare for future challenges or risks (Rossini & Maree, Citation2015). These exogenous factors are discussed below.

Political-legal factors: It is vital for investors and financial practitioners to consider political-legal factors as it should not be ignored or underestimated given that political-legal risks are taking on new and different shapes (Rossini & Maree, Citation2015). Governments are confronted with income inequalities and high levels of sovereign debt in advanced economies. The effective management of political-legal events and risks will enable investors and financial practitioners to enter and navigate new markets. While political-legal events cannot be shunned away from, it can be managed (Culp, Citation2012).

Technological factors: The financial industry has changed since 2010 as technological advances have been at the heart of the financial industry and imperative for financial companies to enhance client services. The rise and the increasing importance of technology will be the most competitive trend in the financial industry (Rossini & Maree, Citation2015). Technological advances will allow financial advice to be presented more strategically and in a professional and compliant manner. Technology offers new enhanced communication and distribution channels between investors and financial practitioners and enables financial practitioners to obtain more insight into investors’ needs and preferences. Technology also provides investors with access to investment information through a number of channels, for example, mobile devices, computers and televisions, whereby they remain informed with the most recent news in the financial markets (Rossini & Maree, Citation2015).

Tax implications: During the construction of an investment plan, investors should consider the effect of taxation on the investment and what the most tax-efficient choice is for the investment (Discovery, Citation2018; Marx et al., Citation2010). This would assist in deterring the type of investment to practice. Tax implications on investments differ for each type of investment. Consequently, an investment with a high return might not be the best investment if it is associated with an exorbitant capital gains tax (Mayo, Citation2000; Old Mutual, Citation2014). To minimise the effect of taxation on investment returns, investors with high tax brackets prefer to invest in tax-deferred investments (Fischer & Gallmeyer, Citation2016). Based on the effect of taxation on investment returns, an investor should have enough knowledge about the implications of taxes on investments or the investor should acquire the assistance of a financial practitioner to minimise the effect of taxation and maximise the total return on the investment (Witz & Zemon, Citation2017).

Macroeconomic factors: As stated by Kuzniak and Grable (Citation2017), macroeconomic factors may influence the risk tolerance behaviour of investors in two manners. Firstly, negative events may lessen investors’ financial capabilities resulting in a negative shift in financial risk tolerance and causing investors to be less risk tolerant. Secondly, investors’ perceptions, instead of the actual impact of macroeconomic factors and events, can influence investors’ willingness to take financial risks. The macroeconomic factors, namely interest rates, exchange rates, inflation and GDP are described in .

Market fluctuations and volatility: According to Haugen (Citation1987) financial markets are not strictly efficient or strictly inefficient. Lintner (Citation1988) stated that investors base their investment decisions on prediction, market timing and financial performance. Hence, when investors make irrational investment decisions it can bring about inefficiencies in the financial markets. In a study conducted by Guillemette and Finke (Citation2014) it was found that the risk tolerance behaviour of investors tends to be affected by recent stock market movements and fluctuations over the short term. However, the risk tolerance behaviour of investors was found to be relatively stable over the long term. Furthermore, investors’ risk tolerance levels increased as stock market valuations increased and decreased throughout market downturns. Malmendier and Nagel (Citation2011) established that the risk tolerance behaviour of investors is affected by macroeconomic shocks experienced throughout their lifetime. Investors who experienced a stock market boom throughout their life cycle were regarded as more risk-tolerant than those who did not encounter a boom in the stock market. Furthermore, investors who encountered a constant bull market had a greater propensity to hold shares and a larger portion of wealth in the form of shares.

International stock market and economic events: Investors’ risk tolerance behaviour are likely to be strongly affected by recent news about major stock market and economic events (Hanna & Lindamood, Citation2007; Yao et al., Citation2004). Miller and Campbell (Citation1959) affirmed that when investors are provided with two opposing sets of information, they are more influenced by the information most recently received, either positive or negative, if time has passed between the first and second set of information and the decision is made right away after the second set of information is presented. Yip (Citation2000) found that financial risk tolerance remains steady over time and is not influenced by major crashes in the stock market. On the other hand, Shefrin (Citation2002) found that investors are not consistent in their risk tolerance, as it is reliant on numerous factors of which one is recent experiences, when confronted with risks. Schooley and Worden (Citation2016) stated that investors’ reactions to negative events in the financial markets tend to be much more emotional.

Table 2. Macroeconomic factors

As South African markets change and experience volatility, this article places more emphasis on risk averse investors that might be less inclined to take on risks. Investors are classified into different risk profiling categories based on their risk-taking propensities. The following section focuses on the risk profiling of risk averse investors.

2.3. Risk profiling of risk averse investors

Investors have different attitudes towards risk and as a result are classified into different risk profiling categories based on their willingness to take risks (Goodall, Citation2005). The willingness of investors to tolerate risks should be determined and carefully considered when constructing investment plans as it will assist investors and financial practitioners with the selection of the most appropriate asset allocation for the investors’ investment portfolios (Klement, Citation2015). Risk averse investors can be categorised as moderately conservative (cautious) and conservative as discussed below (Coronation Fund Managers, Citation2018; Goodall, Citation2005).

Moderately conservative (cautious) investors: These investors have an investment horizon of three or more years and tend to tolerate slightly more risk than conservative investors, but are still resistant to significant downside risks (Bridges, Citation2020). Investors in this category are close to retirement and require liquidity, steady growth and a reasonable income level. The core objective of moderately conservative (cautious) investors is capital preservation as they seek to preserve the real value of their investment portfolios. Consequently, they require a minimum level of risk and are willing to accept lower returns on their investments (Hallman & Rosenbloom, Citation2009). Their investment portfolios are diversified and comprise a greater portion of defensive, low risk assets, such as cash and bonds, and a smaller portion of growth, high risk assets, such as property and equities, to provide partial protection against tax and inflation. These investors prefer little exposure to equities in preference for higher returns to be generated over the long term (Goodall, Citation2005; Tools for Money, Citation2018).

Conservative investors: These investors have an investment horizon of three years or less and tend to tolerate less risk or are not able to tolerate any risk, and consequently, tend to accept lower returns. Their core objective is also to preserve the real value of their investment portfolios (Discovery, Citation2019a). Most investors in this category are retired with short life expectancies and require high liquidity with access to their investments in less than three years, steady growth and a high level of income (Australian Investors Association, Citation2022). Given the investors’ short time horizon, they do not have sufficient time to recover from any losses. Their investment portfolios mainly comprise defensive, low risk assets, such as cash, bonds and unlisted property. These investors seek their investment portfolios to produce inflation-adjusted income streams to cover their living expenses (Coronation Fund Managers, Citation2017; Goodall, Citation2005; Tools for Money, Citation2018).

3. Methodology

Given the establishment of the significant influence of endogenous and exogenous factors on investor risk tolerance behaviour, it is of considerable importance for financial practitioners to take endogenous and exogenous factors and accordingly, the risk profiling model into consideration when assessing investors’ risk tolerance behaviour. The research question for this paper stemmed from the factors explained in the literature review: How does endogenous factors, namely demographical factors, socio-cultural factors, the investor life cycle and behavioural finance biases, and exogenous factors (political-legal factors, technological factors, tax implications, macroeconomic factors, market fluctuations and volatility and the international stock market and economic events) influence the behaviour of risk averse investors? Therefore, the primary objective of this paper was to construct a model that will assist to profile the risk tolerance behaviour of risk-averse investors based on endogenous and exogenous factors.

3.1. Research paradigm and approach

A quantitative research approach was employed for this study by means of a self-structured questionnaire using validated scales. This research approach allowed for a systematic and objective manner to gather information from the selected sample. Williams and Noyes (Citation2007), Creswell and Plano Clark (Citation2011), and Plano Clark and Ivankova (Citation2016) emphasised the reliance of the quantitative research approach in terms of collecting and analysing data for the purpose of illustration, describing, predicting or controlling variables of interest. The traditional notion of “the absolute truth of knowledge” was challenged by this study and hence a positivistic research paradigm was followed. Dudovskiy (Citation2016) stated that positivism holds that only reliable knowledge, based on experience and attained through scientific methods, is considered to be truthful knowledge. Creswell (Citation2003) asserted that the positivist research paradigm commences with the process of theory, the collection of data that supports or rejects the theory and accordingly, the implementation of the necessary amendments before additional tests are performed.

3.2. Research population and sampling technique

The research population for this paper entailed individual investors from a specific investment company in South Africa. This study made use of purposeful sampling, a non-probability sampling method, which incorporates the majority of characteristic and representative elements of the population (Babbie, Citation2010; Grinnell & Unrau, Citation2008). The inclusion criteria to participate in this study is to be 18 years or older; a current investor with some form of investment product at the investment company; and should live in the Gauteng province in South Africa. The Gauteng province was chosen for this study as it comprises the largest portion of the South African population (Stats, Citation2022). Investors were included in this study if they met the inclusion criteria to make a valuable contribution to the findings of this study (Quinlan, Citation2011). As a result, every individual chosen to participate in this study was done so with a purpose (Babbie, Citation2010).

Since the sample was selected using purposive sampling, a sample size of 463 individual investors (n = 463) was selected, whereby all the inclusion criteria were met to obtain the representative sample. This sample size is deemed acceptable as other studies in the same research field used similar sample sizes, namely Eckel and Grossman (Citation2002), Grable and Joo (Citation2004), Strydom et al. (Citation2009), Sages and Grable (Citation2010), Olweny et al. (Citation2013), Shusha (Citation2017), Dickason and Ferreira (Citation2018b), and Abdillah et al. (Citation2019), as well as Shah et al. (Citation2020). The selected sample size was appropriate for the analysis of the study, as it sufficiently met all the requirements for the statistical analysis used that facilitated the investigation of the underlying phenomena and achievement of the empirical objective.

3.3. Research instrument and reliability

An electronic questionnaire was utilised where the responses were collected from the clientele of a private investment firm in South Africa. For the dependent variable, the risk tolerance scale was constructed based on previously validated scales used by researchers and independent risk tolerance scales used by investment companies around South Africa. The study aimed to construct a new consolidated risk tolerance scale by combining the components of the theoretical and industry scales by Grable and Lytton (Citation2001), Yao et al. (Citation2004), Blais and Weber (Citation2009), Gilliam et al. (Citation2010), Discovery (Citation2019b), Liberty (Citation2019), AMP (Citation2020), and Sanlam (Citation2020). The construction of the amended risk tolerance scale was one of the major contributions of this study to measure and report on the risk tolerance behaviour of risk-averse investors and how they will behave towards risk in different financial risk events. Factor analysis, namely exploratory factor analysis (EFA), was used to identify the financial risk events that influence the risk tolerance behaviour of investors. The KMO and Bartlett’s test of sphericity generated satisfactory results for factor analysis. The KMO index attained a value of 0.851, which is greater than the minimum value of 0.5 and indicates great sampling adequacy (Malhotra et al., Citation2017). Bartlett’s test of sphericity had an approximate chi-square statistic of 2757.082 with 136 degrees of freedom and was statistically significant (p = 0.000 < 0.05). This denoted that the variables are related and that the data are suitable for factor analysis. The low-risk tolerance (risk averse) scale had a Cronbach’s alpha value of 0.679, which denotes fair reliability.

Since the study aimed at creating a profile for risk-averse investors in South Africa based on endogenous and exogenous factors, various demographical information (age, gender, education, income, net worth, household size and number of dependents) and socio-cultural information (financial and investment knowledge) were collected. The demographical questions were constructed based on previous evidence by Wallach and Kogan (Citation1961), McInish (Citation1982), Morin and Suarez (Citation1983), Hawley and Fujii (Citation1993), Roszkwoski et al. (Citation1993), Sung and Hanna (Citation1996), Grable and Joo (Citation2004), Grable et al. (Citation2009), Yao et al. (Citation2011), Dickason (Citation2017), Van den Bergh (Citation2018), and Shah et al. (Citation2020). Most research studies primarily focused on the influence of demographical factors on investor risk tolerance behaviour and the influence of socio-cultural factors on investor risk tolerance behaviour is less studied. However, the socio-cultural questions were constructed based on previous evidence by Irwin (Citation1993), Hammitt et al. (Citation2009), and Yao et al. (Citation2011).

The self-report on investor life cycle was also tested using a self-constructed scale based on the life cycle theory reported in Marx et al. (Citation2010), Reilly and Brown (Citation2012), and Harty (Citation2014). Factor analysis, namely EFA, was used to identify the most significant statements that investors consider when establishing where they would describe themselves to be in the investor life cycle. The KMO and Bartlett’s test of sphericity generated appropriate results for factor analysis. The KMO index attained a value of 0.717, which is greater than the minimum value of 0.5 and can be regarded as good sampling adequacy (Malhotra et al., Citation2017). Bartlett’s test of sphericity had an approximate chi-square statistic of 1004.109 with 28 degrees of freedom and was statistically significant (p = 0.000 < 0.05). This signified that the variables are related and that the data are suitable for factor analysis. Based on the scale, investors were divided into two categories, namely the growth investor phase and the defensive (cautious) investor phase. The growth investor category had a Cronbach’s alpha value of 0.781, indicating good reliability, while the defensive (cautious) investor phase had a Cronbach’s alpha value of 0.663, indicating fair reliability (Pallant, Citation2020). This self-report scale is inherent to the subjective investment pattern of South African investors residing in Gauteng.

To test the behavioural finance biases that risk averse investors are subject towards, validated scales constructed by Dickason (Citation2017) and Ferreira (Citation2018), which comprises statements derived from theory, was used to identify and analyse the effect of the behavioural finance biases, as endogenous factors, on investor risk tolerance behaviour.

To identify and analyse the effect of exogenous factors on investor risk tolerance behaviour, several variables, namely political-legal, technological, tax implications, macroeconomic factors (interest rates, exchange rates, inflation, GDP), international events and market fluctuations were constructed. These constructs comprises self-structured questions that were derived from theory and findings identified by previous researchers (Antelme, Citation2018; Chester, Citation2016; Guillemette & Finke, Citation2014; Grable, Citation2000; Hanna & Lindamood, Citation2007; Kuzniak & Grable, Citation2017; Mavee & Schimmel-pfenning, Citation2017; Money Matters, Citation2022; Newcomb, Citation2012; Patel, Citation2019; Pettinger, Citation2021; Schooley & Worden, Citation2016; Woodyard & Grable, Citation2018; Yao et al., Citation2004). Factor analysis, namely EFA, was conducted to identify the most significant financial risk events pertaining to the external environment that are likely to influence investor risk tolerance behaviour. All of the constructs generated appropriate results for factor analysis with KMO indexes attaining the minimum value of 0.5 and the Bartlett’s test of sphericity was statistically significant (p = 0.000 < 0.05; Malhotra et al., Citation2017; Sarstedt & Mooi, Citation2019). Also, all of the constructs had Cronbach’s alpha values above 0.65 making them reliable (Pallant, Citation2020).

3.4. Model specification and justification

As a result of the large categorical dataset and number of scaled variables, a structural equation model (SEM) was deemed the best model to represent the data. In this case, the SEM provided multivariate statistical analysis to demonstrate the complex relationship between the dependent variable (risk tolerance behaviour) and independent variables (endogenous and exogenous factors) to facilitate the achievement of the primary objective of this paper as discussed in the methodology section. For this study, the implementation of a structural model provided the combination of multiple statistical techniques such as factor analysis and regression analysis. This allowed the researchers to observe and measure the structural relationships between the complex categorical dependent and independent variables. Additionally, the structural model facilitated the analysis of a series of dependent and independent relationships simultaneously. Based on the significant contribution of this model benefits as mentioned above, a structural model provided the researchers with the most advantageous statistical approach for the dataset and research objectives. The Statistical Packages of Social Sciences (IBM SPSS) version 26 and Amos were employed for the preliminary data analysis and the SEM.

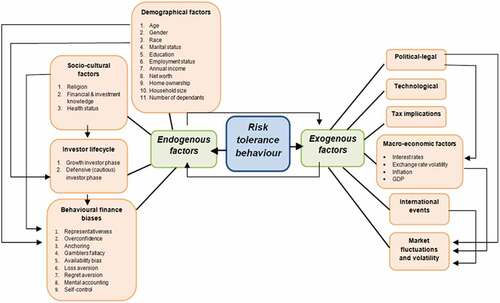

Considering the sample size, Hox and Bechger (Citation1998) and Weston and Gore (Citation2006) asserted that a sample size of 200 is adequate for multivariate normal data, whereas a sample size of 400 is adequate for non-normal data. Given that maximum likelihood estimation, which assumes multivariate normal data, was used to estimate the model, the sample size of 463 investors was considered adequate for conducting SEM with IBM SPSS Amos™, Version 26 (IBM SPSS Amos, Citation2020). illustrates the conceptual model for the SEM, which indicates the relationship between the dependent variable (risk tolerance behaviour) and independent variables (endogenous and exogenous factors) to establish the influence of the pre-identified endogenous factors and exogenous factors on the risk tolerance behaviour of risk averse investors.

Figure 2. Conceptual model of investor risk tolerance behaviour, endogenous factors and exogenous factors.

4. Results

demonstrates the standardised regression weight results for the specified structural model.

Table 3. Standardised regression weight results for the specified structural model

demonstrates that demographic factors, namely age (standardised regression coefficient = 0.110) and net worth (standardised regression coefficient = −0.134) contributed significantly towards explaining low-risk tolerance behaviour at the p < 0.05 level. However, the remaining demographic factors, namely gender, education, annual income, household size and the number of financial dependents, did not significantly contribute towards explaining low-risk tolerance behaviour. Furthermore, the socio-cultural factor, namely financial and investment knowledge (standardised regression coefficient = −0.165) contributed significantly towards explaining low-risk tolerance behaviour at the p < 0.001 level. Regarding the investor life cycle, the growth investor phase (standardised regression coefficient = 0.138) contributed significantly towards explaining low-risk tolerance behaviour at the p < 0.05 level. On the contrary, the defensive (cautious) investor phase did not significantly contribute towards explaining low-risk tolerance behaviour (p > 0.10).

Relating to the behavioural finance biases, it can be seen from that the representativeness bias (standardised regression coefficient = 0.185), the anchoring bias (standardised regression coefficient = 0.304) and the loss aversion bias (standardised regression coefficient = −0.243) contributed significantly towards explaining low-risk tolerance behaviour at the p < 0.001 level. The overconfidence bias (standardised regression coefficient = 0.117), the availability bias (standardised regression coefficient = 0.127) and the mental accounting bias (standardised regression coefficient = 0.146) contributed significantly towards explaining low-risk tolerance behaviour at the p < 0.05 level. However, the gambler’s fallacy bias, the regret aversion bias and the self-control bias did not significantly contribute towards explaining low-risk tolerance behaviour (p > 0.10).

Concerning the factors of the external environment, illustrates that international events (standardised regression coefficient = −0.468), as well as market fluctuations and volatility (standardised regression coefficient = 0.470), contributed significantly towards explaining low-risk tolerance behaviour at the p < 0.001 level. Also, inflation (standardised regression coefficient = −0.206) and GDP (standardised regression coefficient = 0.309) contributed significantly towards explaining low-risk tolerance behaviour at the p < 0.05 level. On the other hand, political-legal factors, technological factors, tax implications, interest rates and exchange rate volatility did not significantly contribute towards explaining low-risk tolerance behaviour (p > 0.10).

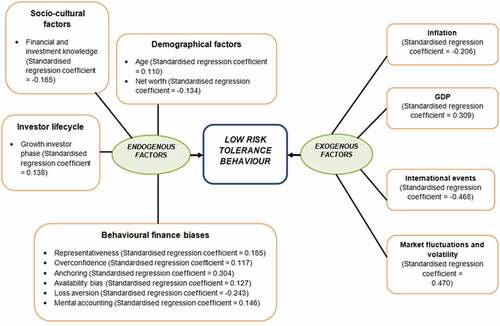

These results led to the following proposed model to profile the risk tolerance behaviour of risk-averse investors based on the endogenous and exogenous factors that contributed significantly towards explaining low-risk tolerance behaviour, which is depicted in . Concerning the endogenous factors, it can be inferred from that the demographic factor, namely net worth (standardised regression coefficient = −0.134) contributed the greatest degree towards explaining low-risk tolerance behaviour, while age (standardised regression coefficient = 0.110) contributed to a lesser degree towards explaining low-risk tolerance behaviour. The socio-cultural factor, namely financial and investment knowledge (standardised regression coefficient = −0.165) contributed significantly towards explaining low-risk tolerance behaviour to a rather small degree.

Figure 3. Proposed model to profile the risk tolerance behaviour of risk averse investors based on endogenous and exogenous factors.

Furthermore, considering the investor life cycle as an endogenous factor, only the growth investor phase (standardised regression coefficient = 0.138) contributed significantly towards explaining low-risk tolerance behaviour and explained low-risk tolerance behaviour to a rather small degree. Regarding the behavioural finance biases as endogenous factors, the anchoring bias (standardised regression coefficient = 0.304) contributed the greatest degree towards explaining low-risk tolerance behaviour, followed by the loss aversion bias (standardised regression coefficient = −0.243), the representativeness bias (standardised regression coefficient = 0.185), the mental accounting bias (standardised regression coefficient = 0.146), the availability bias (standardised regression coefficient = 0.127) and the overconfidence bias (standardised regression coefficient = 0.117), respectively.

Concerning the exogenous factors, which comprise factors of the external environment, it can be inferred from that market fluctuations and volatility (standardised regression coefficient = 0.470) contributed the greatest degree towards explaining low-risk tolerance behaviour, followed by international events (standardised regression coefficient = −0.468), GDP (standardised regression coefficient = 0.309) and inflation (standardised regression coefficient = −0.206), respectively.

5. Summary of results to profile risk-averse investors based on endogenous and exogenous factors

provides a summary of the endogenous and exogenous factors that uniquely contributed towards explaining the risk tolerance behaviour of risk-averse investors and the degree to which each of these factors explains the low-risk tolerance behaviour of these investors.

Table 4. Proposed weights to profile the risk tolerance behaviour of risk-averse investors

It can be summarised from that by considering the endogenous factors that the demographical factor, namely net worth contributed the greatest degree towards explaining low-risk tolerance behaviour. Researchers, namely Hawley and Fujii (Citation1993) and Hallahan et al. (Citation2003)also found net worth to significantly contribute towards explaining low risk tolerance behaviour. The demographical factor, namely age contributed a slightly lesser degree towards explaining low-risk tolerance behaviour. Research studies conducted within South Africa by Metherell (Citation2011), Van Schalkwyk (Citation2012), Mabalane (Citation2015), Van den Bergh (Citation2018), and Ferreira and Dickason-Koekemoer (Citation2019) also found age to significantly contribute towards explaining low risk tolerance behaviour. However, these demographic factors explain low-risk tolerance behaviour to a rather small degree.

The socio-cultural factor, namely financial and investment knowledge contributed significantly towards explaining low-risk tolerance behaviour to a rather small degree. Several international research studies (Grable, Citation2000; Grable & Joo, Citation2004; Griesdorn et al., Citation2014; Haliassos & Bertaut, Citation1995; Irwin, Citation1993; Jacobs-Lawson & Hershey, Citation2005; Marinelli et al., Citation2017; Sages & Grable, Citation2010) and South African research studies (Antonites & Wordsworth, Citation2009; Van Schalkwyk, Citation2012) found significant relationships between financial and investment knowledge and risk tolerance behaviour. Haliassos and Bertaut (Citation1995) affirmed that risk-averse investors are likely to take less risks as a result of a lack of financial and investment knowledge.

Considering the investor life cycle as an endogenous factor, only the growth investor phase of the life cycle contributed significantly towards explaining low-risk tolerance behaviour and explains low-risk tolerance behaviour to a rather small degree. This finding is in contrast to theory as risk-averse investors with low-risk tolerance behaviour should be in the defensive (cautious) investor phase of the life cycle (Cocco et al., Citation2005; Discovery, Citation2019a; Shaikat, Citation2020). However, it can be derived from this finding based on theory that the investors in the growth phase of the investor life cycle may be younger individuals with long investment horizons who are risk-averse as they are willing to take less risks (Marx et al., Citation2010). Relating to the behavioural finance biases, the anchoring bias contributed the greatest degree towards explaining low-risk tolerance behaviour, followed by the loss aversion bias, the representativeness bias, the mental accounting bias, the availability bias and the overconfidence bias, respectively. The anchoring bias explains low-risk tolerance behaviour to a moderate degree, the loss aversion bias explains low-risk tolerance behaviour to a relatively moderate degree and the remaining behavioural finance biases explain low-risk tolerance behaviour to a rather small degree. Similar to these findings, Pompian (Citation2016) found that risk averse investors with low-risk tolerance behaviour are subject to biases such as anchoring, loss aversion and mental accounting. Dickason and Ferreira (Citation2018a) found that risk-averse investors with low-risk tolerance behaviour are subject to the loss aversion bias and mental accounting bias.

Concerning the exogenous factors, which comprise factors about the external environment, it can be inferred from that market fluctuations and volatility, international events and GDP explain low-risk tolerance behaviour to a moderate degree, while inflation explains low-risk tolerance behaviour to a rather moderate degree. Accordingly, market fluctuations and volatility contributed the greatest degree towards explaining low-risk tolerance behaviour, followed by international events, GDP and inflation, respectively. Very little attention has been given in research to identify and analyse the influence of exogenous factors on the risk tolerance behaviour of risk-averse investors in practice. However, Kuzniak and Grable (Citation2017) examined the relationship between investor risk tolerance behaviour and the GDP of a country and established that investors who live in countries with a high GDP are more likely to tolerate higher levels of risk, than investors living in countries with a lower GDP. Brandt and Wang (Citation2003) found that investors are more risk-averse during periods of economic recessions and are more risk-tolerant during periods of economic growth. Looking from a South African perspective, although South Africa holds promise for growth, its GDP has been staggering combined with rising unemployment, low saving rates and high consumer indebtedness (World Bank, Citation2021). This may cause investors in South Africa to be less willing to tolerate risk when considering factors about the external environment.

To conclude, the endogenous and exogenous factors that contributed the greatest degree towards explaining the low-risk tolerance behaviour of risk-averse investors should mainly be considered. However, the endogenous and exogenous factors that explain low-risk tolerance behaviour to a relatively small degree, given the complexity of the SEM, should not be disregarded as they also uniquely contributed towards explaining the low-risk tolerance behaviour of risk-averse investors.

The following section presents the conclusion of this study with an overview of the contribution of this study to the field of research and the limitations of the study to make recommendations and contribute towards possibilities for future research endeavours.

6. Conclusion and practical implications

Risk-averse investors tend to take fewer risks or are not able to take any risks and subsequently, tend to accept lower returns. These investors seek to preserve the real value of their capital, rather than to increase the real value of their capital. Their willingness to take risks and decisions to initiate, amend or terminate risky behaviours are influenced by endogenous and exogenous factors. Although numerous studies have been conducted to investigate the factors that influence investor risk tolerance behaviour when making investment decisions, there is no evident studies that examined the influence of a multitude of both endogenous and exogenous factors on the risk tolerance behaviour of risk-averse investors. Furthermore, previous research studies have not focused on and addressed the deficiencies of existing and conventional risk assessment forms used by practitioners in the financial industry.

The main aim of this study to profile the risk tolerance behaviour of risk-averse investors based on endogenous and exogenous factors was achieved through the development of a risk profiling model utilising SEM. Several pre-identified endogenous and exogenous factors significantly and uniquely contributed towards explaining the low-risk tolerance behaviour of risk-averse investors. This led to the successful development of the model to profile the low-risk tolerance behaviour of risk-averse investors based on the endogenous and exogenous factors. The degree to which each of these endogenous and exogenous factors explains the low-risk tolerance behaviour of risk-averse investors should also be considered.

This risk profiling model makes a remarkable and unique contribution to the field of study and the financial industry. It should be considered by investors, financial practitioners and researchers not only in South Africa, but also internationally, to be acquainted with and to comprehend the endogenous and exogenous factors that influence the low-risk tolerance behaviour of risk-averse investors. This risk profiling model will assist with the identification of the endogenous factors unique to risk-averse investors that influence their risk tolerance behaviour. It will also assist with the identification of the exogenous factors relating to the external environment that may hamper the abilities of risk-averse investors to take more risks given the South African and world-wide economic climate and financial market conditions. Furthermore, the risk profiling model should be considered to facilitate the more practical, executable and accurate profiling of the low-risk tolerance behaviour of risk-averse investors and accordingly, to ensure the successful implementation of investment strategies in practice. This study also contributes significantly towards academia and the financial industry by addressing worldwide deliberations regarding the deficiencies of existing and conventional risk assessment forms. In particular, investment companies should give careful consideration to these endogenous and exogenous factors to guide them and assist with the improvement of existing and conventional risk assessment forms.

This study acknowledges certain limitations within the research, which provides future researchers with new opportunities. A non-probability purposive sampling method was used to obtain the representative sample from a specific investment company in Gauteng, South Africa. It can be recommended to use an alternative sampling method and accordingly, adjust or extend the inclusion criteria of the research study as preferred by the researcher to draw a representative sample from the population. Given the complexity of the risk profiling model, the review and further investigation of the pre-identified endogenous and exogenous factors incorporated into the model to profile risk-averse investors’ low-risk tolerance behaviour will assist in further refining and simplifying the model. Specifically, the endogenous and exogenous factors that explain low-risk tolerance behaviour to a rather small degree should be reviewed and further investigated.

Acknowledgements

Special thanks to Prof PMS Van Heerden for assisting in the co-supervision of this study, Programme Leader for Risk Management, North-West University, South Africa.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Abdillah, W., Sari, R. P., & Hendrawaty, E. (2019). Understanding determinants of individual intention to invest in digital risky investment. Jurnal Dinamika Manajemen, 10(1), 124–20. https://doi.org/10.15294/jdm.v10i1.18243

- AMP. (2020, February 5). What style of investor are you? Retrieved March 27, 2022, from https://www.amp.com.au/insights/grow-my-wealth/investor-style

- Antelme, M. (2018). Matters of land. In Corospondent: Land Matters, Autumn 2018. Retrieved March 27, 2022, from https://www.coronation.com/globalassets/sa-personal/publications/corospondent/corospondent-april-2018/2018-april-sa-retail-corospondent.pdf

- Antonites, A. J., & Wordsworth, R. (2009). Risk tolerance: A perspective on entrepreneurship education. Southern African Review, 13(3), 69–85.

- Australian Investors Association. (2022). Risks. Retrieved March 25, 2022, from https://www.investors.asn.au/education/investment-basics/risks/

- Babbie, E. (2010). The practice of social research (12th ed.). Cengage Learning.

- Baghani, M., & Sedaghat, P. (2014). Effect of risk perception and risk tolerance on investors’ decision making in Tehran stock exchange. International Academic Journal of Accounting and Financial Management, 1(1), 79–87.

- Blais, A. R., & Weber, E. U. (2009). The domain-specific risk taking scale for adult populations: Item selection and preliminary psychometric properties. Judgement and Decision Making, 1(1), 33–47.

- Boone, N. M., & Lubitz, L. S. (2003). A review of difficult investment policy issues. Journal of Financial Planning, 16(5), 56–63.

- Brandt, M. W., & Wang, K. Q. (2003). Time-varying risk aversion and unexpected inflation. Journal of Monetary Economics, 50(7), 1457–1498. https://doi.org/10.1016/j.jmoneco.2003.08.001

- Brayman, S., Grable, J. E., Griffin, P., & Finke, M. (2017). Assessing a client’s risk profile: A review of solution providers. Journal of Financial Service Professionals, 71(1), 71–81.

- Bridges. (2020). Investment risk profiles. Retrieved March 25, 2022, from https://www.bridges.com.au/pdf_flyers/ed_flyers/investing/investment_risk_profiles

- Byrne, A., & Brooks, M. (2008). Behavioral finance: Theories and evidence. Research Foundation Literature Reviews, 3(1), 1–26.

- Cambridge Dictionary. (2022). Sociocultural. Retrieved March 23, 2022, from https://dictionary.cambridge.org/dictionary/english/sociocultural

- Chaudhary, A. K. (2013). Impact of behavioural finance in investment decisions and strategies - a fresh approach. International Journal of Management Research and Business Strategy, 2(2), 85–92.

- Chester, N. (2016). Brexit: The investment implications. In Corospondent, Winter 2016. Retrieved March 27, 2022, from https://www.coronation.com/globalassets/sa-personal/publications/corospondent/correspondent-july-2016/2016-july-corospondent-retail.pdf

- Cocco, J. F., Gomes, F. J., & Maenhout, P. J. (2005). Consumption and portfolio choice over the life cycle. The Review of Financial Studies, 18(2), 491–533. https://doi.org/10.1093/rfs/hhi017

- Coronation Fund Managers. (2013). Profile’s unit trusts & collective investments. Profile Media.

- Coronation Fund Managers. (2016). Profile’s unit trusts & collective investments. Profile Media.

- Coronation Fund Managers. (2017). Profile’s unit trusts & collective investments. Profile Media.

- Coronation Fund Managers. (2018). Profile’s unit trusts & collective investments. Profile Media.

- Coronation Fund Managers. (2019). The numbers that drive retirement. In Corospondent: Skittish times, Summer 2019. Retrieved March 24, 2022, from https://www.coronation.com/globalassets/sa-personal/publications/corospondent/corospondent-january-2019/2019-january-corospondent-retail.pdf

- Creswell, J. W. (2003). Research design: Qualitative, quantitative and mixed methods approaches (2nd ed.). SAGE.

- Creswell, J. W., & Plano Clark, V. L. (2011). Designing and conducting mixed methods research (2nd ed.). SAGE.

- Culp, S. (2012, August 27). Political risk can’t be avoided, but it can be managed. Retrieved March 24, 2022, from https://www.forbes.com/sites/steveculp/2012/08/27/political-risk-cant-be-avoided-but-it-can-be-managed/?sh=55f649d43acb

- Davey, G. (2012). Risk profiling: Art and science. Retrieved March 27, 2022, from http://enhanceifa.com/Risk%20Profiling%20Art%20&%20Science.pdf

- Davey, G., & Resnik, P. (2008). Risk tolerance, risk profiling and the financial planning process. Retrieved March 27, 2022, from http://www.riskprofiling.com/WWW_RISKP/media/RiskProfiling/Downloads/PR_RT.pdf

- Di Dottorato, T. (2013). Behavioral finance and financial markets: Micro, macro and corporate [Thesis – PhD]. Università Politecnica Delle Marche.

- Dickason, Z. (2017). Modelling investor behaviour in the South African context [Thesis – PhD]. North-West University.

- Dickason, Z., & Ferreira, S. J. (2018a). Establishing a link between risk tolerance, investor personality and behavioural finance in South Africa. Cogent Economics & Finance, 6(1), 1–13. https://doi.org/10.1080/23322039.2018.1519898

- Dickason, Z., & Ferreira, S. J. (2018b). The effect of age and gender on financial risk tolerance of South African investors. Investment Management and Financial Innovations, 15(2), 96–103. https://doi.org/10.21511/imfi.15(2).2018.09

- Dickason, Z., & Ferreira, S. J. (2019). Risk tolerance of South African investors: Marital status and gender. Gender & Behaviour, 17(2), 12999–13006.

- Discovery. (2018). The tax implications of 3 popular investment vehicles. Retrieved March 24, 2022, from https://www.discovery.co.za/corporate/smart-money-tax-implications-of-investment-vehicle

- Discovery. (2019a). Understanding the impact of a risk profile. Retrieved March 25, 2022, from https://www.discovery.co.za/investments/discovery-investigator-impact-risk-profile

- Discovery. (2019b). Your risk profile assessment. Retrieved March 27, 2022, from https://www.discovery.co.za/discovery_coza/web/linked_content/pdfs/invest/your_risk_portrait.pdf

- Dudovskiy, J. (2016). Positivism research philosophy. Retrieved March 25, 2022, from https://research-methodology.net/research-philosophy/positivism/

- Eckel, C. C., & Grossman, P. J. (2002). Sex differences and statistical stereotyping in attitudes towards financial risk. Evolution and Human Behaviour, 23(4), 281–295. https://doi.org/10.1016/S1090-5138(02)00097-1

- Ferreira, S. J. (2018). Reputational risk: depositor behaviour in South Africa [Thesis – PhD]. North-West University.

- Ferreira, S. J., & Dickason-Koekemoer, Z. (2019). The relationship between depositor behaviour and risk tolerance in a South African context. Advances in Decision Sciences, 23(3), 1–19.

- Fischer, M., & Gallmeyer, M. (2016). Taxable and tax-deferred investing with the limited use of losses. Review of Finance, 21(5), 1847–1873.

- Fourie, F. C. V. N., & Burger, P. (2009). How to think and reason in macroeconomics (3rd ed.). Juta.

- Gilliam, J., Chatterjee, S., & Grable, J. (2010). Measuring the perception of risk tolerance: A tale of two measures. Journal of Financial Counseling and Planning, 21(2), 40–53.

- Goodall, B. (2005). Investment planning. LexisNexis Butterworths.

- Grable, J. E. (2000). Financial risk tolerance and additional factors that affect risk taking in everyday money matters. Journal of Business and Psychology, 14(4), 625–630. https://doi.org/10.1023/A:1022994314982

- Grable, J. E. (2016). Financial risk tolerance. In J. J. Xiao (Ed.), Handbook of consumer finance research (pp. 19–31). Springer International Publishing.

- Grable, J. E. (2017). Financial risk tolerance: A psychometric review. Research Foundation Briefs, 4(1), 1–27.

- Grable, J. E., & Joo, S. H. (2004). Environmental and biopsychosocial factors associated with financial risk tolerance. Journal of Financial Counseling and Planning Education, 15(1), 73–82.

- Grable, J. E., & Lytton, R. H. (2001). Assessing the concurrent validity of the SCF risk tolerance question. Association for Financial Counseling and Planning Education, 12(2), 43–53.

- Grable, J. E., McGill, S., & Britt, S. (2009). Risk tolerance estimation bias: The age effect. Journal of Business & Economic Research, 7(7), 1–12.

- Griesdorn, T., Lown, J., DeVaney, S., Cho, S., & Evans, D. (2014). Association between behavioural life-cycle constructs and financial risk tolerance of low-to-moderate-income households. Journal of Financial Counseling and Planning, 25(1), 27–40.

- Grinnell, R. M., & Unrau, Y. A. (2008). Social work research and evaluation: Foundations of evidence-based practice. Oxford University Press.

- Guillemette, M. A., & Finke, M. (2014). Do large swings in equity values change risk tolerance? Journal of Financial Planning, 27(6), 44–50.

- Guillemette, M. A., & Nanigian, D. (2014). What determines risk tolerance? Financial Services Review, 23(1), 207–218.

- Haliassos, M., & Bertaut, C. C. (1995). Why do so few hold stocks? The Economic Journal, 105(432), 1110–1129. https://doi.org/10.2307/2235407

- Hallahan, T. A., Faff, R. W., & McKenzie, M. (2003). An exploratory investigation of the relation between risk tolerance scores and demographic characteristics. Journal of Multinational Financial Management, 13(4–5), 483–502. https://doi.org/10.1016/S1042-444X(03)00022-7

- Hallman, V. G., & Rosenbloom, J. (2009). Private wealth management: The complete reference for the personal financial planner (8th ed.). McGraw-Hill.

- Hammitt, J. K., Haninger, K., & Treich, N. (2009). Effects of health and longevity on financial risk tolerance. The Geneva Risk and Insurance Review, 34(2), 117–139. https://doi.org/10.1057/grir.2009.6

- Hanna, S. D., & Lindamood, S. 2007. Risk tolerance: Cause or effect. In Academy of Financial Services Proceedings (pp. 1–9).

- Harty, N. (2014, January 22). Financial planning and the investor life cycle. Retrieved March 27, 2022, from https://www.jamaicaobserver.com/business/Financial-planning-and-the-investor-life-cycle-_15839917

- Haugen, R. A. (1987). Introductory investments theory. Prentice-Hall.

- Hawley, C. B., & Fujii, E. T. (1993). An empirical analysis of preferences for financial risk: Further evidence on the Friedman-Savage model. Journal of Post Keynesian Economics, 16(2), 197–204. https://doi.org/10.1080/01603477.1993.11489978

- Hemrajani, P., & Sharma, S. K. (2018). Influence of urgency on financial risk-taking behaviour of individual investors: The role of financial risk tolerance as a mediating factor. The IUP Journal of Applied Finance, 24(1), 30–43.

- Hox, J. J., & Bechger, T. M. (1998). An introduction to structural equation modelling. Family Science Review, 11(1), 354–373.

- IBM SPSS Amos. (2020). IBM SPSS Amos structural equation modeling. Retrieved March 27, 2022, from https://www.ibm.com/products/structural-equation-modeling-sem

- Irwin, C. E. (1993). Adolescence and risk taking: How are they related? In N. J. Bell & R. W. Bell (Eds.), Adolescent risk taking (pp. 7–28). SAGE.

- Jacobs-Lawson, J. M., & Hershey, D. A. (2005). Influence of future time perspective, financial knowledge, and financial risk tolerance on retirement saving behaviors. Financial Services Review, 14(1), 331–344.

- Jacobsen, B. J., Speidel, P., Keshemberg, T. L., & Hodapp, R. (2014). Measure and manage risk tolerance more effectively. Journal of Financial Planning, 27(5), 20–25.

- Kannadhasan, M. (2006). Role of behavioural finance in investment decisions. Retrieved March 24, 2022, from https://www.researchgate.net/profile/Manoharan-Kannadhasan/publication/265230942_ROLE_OF_BEHAVIOURAL_FINANCE_IN_INVESTMENT_DECISIONS/links/55ac75b608ae481aa7ff5a80/ROLE-OF-BEHAVIOURAL-FINANCE-IN-INVESTMENT-DECISIONS.pdf

- Kitches, M. (2018, February 2). When clients misperceive risk. Financial Planning, 49–52.

- Klement, J. (2015). Investor risk profiling: An overview. Research Foundation Briefs, 1(1), 1–19.

- Kuzniak, S., & Grable, J. E. (2017). Does financial risk tolerance change over time? A test of the role macroeconomic, biopsychosocial and environmental, and social support factors plays in shaping changes in risk attitudes. Financial Services Review, 26(4), 315–338.

- Larkin, C., Lucey, B. M., & Mulholland, M. (2013). Risk tolerance and demographic characteristics: Preliminary Irish evidence. Financial Services Review, 22(1), 1–26.

- Lawrenson, J. (2020). Modelling financial risk tolerance of female South African investors [Thesis – PhD]. North-West University.

- Liberty. (2019). Risk analyser. Retrieved March 27, 2022, from https://www.blueprintonline.co.za/blueprintportal/Calculators/main.htm

- Lintner, G. (1988). Behavioural finance: Why investors make bad decisions. The Planner, 13(1), 7–8.

- Mabalane, M. D. (2015). Cultural and demographic differences in financial risk tolerance [Dissertation – Masters]. University of Pretoria.

- Malhotra, N. K., Nunan, D., & Birks, D. F. (2017). Marketing research: An applied approach (5th ed.). Pearson.

- Malkiel, B. G. (1996). A random walk down Wall Street. W.W. Norton & Co.

- Malmendier, U., & Nagel, S. (2011). Depression babies: Do macroeconomic experiences affect risk-taking? Quarterly Journal of Economics, 126(1), 373–416. https://doi.org/10.1093/qje/qjq004

- Marinelli, N., Mazzoli, C., & Palmucci, F. (2017). Mind the gap: Inconsistencies between subjective and objective financial risk tolerance. Journal of Behavioral Finance, 18(2), 219–230. https://doi.org/10.1080/15427560.2017.1308944

- Marx, J., de Swardt, C., Beaumont-Smith, M., & Erasmus, P. (2009). Financial management in Southern Africa (3rd ed.). Pearson.

- Marx, J., Mpofu, R. T., De Beer, J. S., Nortjé, A., & Van de Venter, T. W. G. (2010). Investment management (3rd ed.). Van Schaik.

- Masthead. (2019, May 14). There’s more to risk than risk profiling. Retrieved March 24, 2022, from https://www.masthead.co.za/newsletter/theres-more-to-risk-than-risk-profiling/

- Mavee, N., & Schimmel-pfenning, A. (2017, March 30). What makes the rand so volatile: global or home-made factors? Econ 3x3. Retrieved March 24, 2022, Retrieved http://www.econ3x3.org/article/what-makes-rand-so-volatile-global-or-home-made-factors

- Mayo, H. B. (2000). Investments: An introduction (6th ed.). Harcourt.

- Mazzoli, C., & Marinelli, N. (2011). The role of risk in the investment decision process: Traditional vs behavioural finance. In C. Lucarelli & G. Brighetti (Eds.), Risk tolerance in financial decision making (pp. 8–66). Palgrave Macmillan.

- McInish, T. H. (1982). Individual investors and risk-taking. Journal of Economic Psychology, 2(2), 125–136. https://doi.org/10.1016/0167-4870(82)90030-7

- Merriam-Webster Dictionary. (2022). Demographic. Retrieved March 23, 2022, from https://www.merriam-webster.com/dictionary/demographic

- Metherell, C. (2011). The impact of demographic factors on subjective financial risk tolerance: A South African study [Thesis – Masters]. UKZN.

- Miller, N., & Campbell, D. T. (1959). Recency and primacy in persuasion as a function of the timing of speeches and measurements. Journal of Abnormal and Social Psychology, 59(1), 1–9. https://doi.org/10.1037/h0049330

- Money Matters. (2022). Important economic factors which affect investment. Retrieved March 24, 2022, from https://accountlearning.com/important-economic-factors-affect-investment/

- Morin, R. A., & Suarez, A. F. (1983). Risk aversion revisited. Journal of Finance, 38(4), 1201–1216. https://doi.org/10.1111/j.1540-6261.1983.tb02291.x

- Mutswenje, V. S. (2014). A survey of the factors influencing investment decisions: The case of individual investors at the NSE. International Journal of Humanities and Social Science, 4(4), 92–102.

- Newcomb, W. H. (2012). Risk tolerance questionnaire. Retrieved November 15, 2019, from https://newcombfinancialadvisors.com/uploads/NFA_-_Risk_Tolerance_Questionnaire_-_20121231.pdf

- Nobre, L. H. N., & Grable, J. E. (2015). The role of risk profiles and risk tolerance in shaping client decisions. Journal of Financial Service Professionals, 69(3), 18–21.

- Old Mutual. (2014). Premiums & problems (109th ed.).

- Olweny, T., Namusonge, G. S., & Onyango, S. (2013). Financial attributes and investor risk tolerance at the Nairobi securities exchange - a Kenyan perspective. Asian Social Science, 9(3), 138–147. https://doi.org/10.5539/ass.v9n3p138

- Pallant, J. (2020). SPSS survival manual: A step by step guide to data analysis using SPSS (7th ed.). McGraw Hill.

- Patel, N. (2019). The effect of interest rates on investments. Retrieved March 24, 2022, from https://finance.zacks.com/effect-interest-rates-investments-5809.html

- Pettinger, T. (2021, June 5). Factors affecting investment. Economicshelp. Retrieved March 24, 2022, Retrieved https://www.economicshelp.org/blog/136672/economics/factors-affecting-investment/

- Plano Clark, V. L., & Ivankova, N. V. (2016). Mixed methods research: A guide to the field. SAGE.

- Pompian, M. M. (2016). Risk profiling through a behavioral finance lens. Research Foundation Briefs, 2(1), 1–26.

- Quinlan, C. (2011). Business research methods. Cengage Learning.

- Reilly, F. K., & Brown, K. C. (2012). Analysis of investments & management of portfolios (10th ed.). Cengage Learning.

- Rossini, L., & Maree, J. (2015). The business of financial advice: A guide for financial advisers to building a service-based business. Juta.

- Roszkwoski, M. J., Snelbecker, G. E., & Leimberg, S. R. (1993). Risk tolerance and risk aversion. The Tools and Techniques of Financial Planning, 4(1), 213–225.

- Rutgers. (2014). Investment risk tolerance assessment. Retrieved March 27, 2022, from https://pfp.missouri.edu/research/investment-risk-tolerance-assessment/

- Ryan, C. (1988). McGregor’s dictionary of stock market terms. Juta.

- Sages, R. A., & Grable, J. E. (2010). Financial numeracy, net worth, and financial management skills: Client characteristics that differ based on financial risk tolerance. Journal of Financial Service Professionals, 64(6), 57–65.

- Sanlam. (2020). Financial planning process. Retrieved March 27, 2022, from https://www.sanlam.co.za/personal/financialplanning/Pages/financial-planning-process.aspx

- Sarstedt, M., & Mooi, E. (2019). A concise guide to market research: The process, data, and methods using IBM SPSS statistics (3rd ed.). Springer.

- Schooley, D. K., & Worden, D. D. (2016). Perceived and realized risk tolerance: Changes during the 2008 Financial Crisis. Journal of Financial Counseling and Planning, 27(2), 265–276. https://doi.org/10.1891/1052-3073.27.2.265

- Shah, N. H., Khalid, W., Khan, S., Arif, M., & Khan, M. A. (2020). An empirical analysis of financial risk tolerance and demographic factors of business graduates in Pakistan. International Journal of Economics and Financial Issues, 10(4), 220–234. https://doi.org/10.32479/ijefi.9365

- Shaikat, N. M. (2020). Individual investor life cycle. Retrieved March 23, 2022, from https://ordnur.com/academic-study/finance/individual-investor-life-cycle/

- Shefrin, H. (2002). Beyond greed and fear: Understanding behavioural finance and the psychology of investing. Oxford University Press.

- Shusha, A. A. (2017). Does financial literacy moderate the relationship among demographic characteristics and financial risk tolerance? Evidence from Egypt. Australasian Accounting, Business and Finance Journal, 11(3), 67–86. https://doi.org/10.14453/aabfj.v11i3.6

- Singh, S. (2012). Investor irrationality and self-defeating behaviour: Insights from behavioural finance. The Journal of Global Business Management, 8(1), 116–122.

- Stats, S. A. (2022). Find Statistics. Retrieved March 25, 2022, from http://www.statssa.gov.za/

- Strydom, B., Christison, A., & Gokul, A. (2009). Financial risk tolerance: A South African perspective. Working paper no. 01-2009. Working papers in finance. University of Kwazulu-Natal.

- Sung, J., & Hanna, S. D. (1996). Factors related to risk tolerance. Financial Counseling and Planning, 7(1), 11–19.

- Tools for Money. (2018). The five most commonly used investment risk tolerance categories. Retrieved March 25, 2022, from https://www.toolsformoney.com/investment_risk_tolerance.htm

- Van de Venter, G., Michayluk, D., & Davey, G. (2012). A longitudinal study of financial risk tolerance. Journal of Economic Psychology, 33(4), 794–800. https://doi.org/10.1016/j.joep.2012.03.001

- Van den Bergh, A. (2018). Analysing risk tolerance during the investor lifecycle [Dissertation – Masters]. North-West University.

- Van den Bergh−lindeque, A. (2020). The influence of endogenous and exogenous factors on investor risk-tolerance behaviour [Thesis – PhD]. North-West University.

- Van der Merwe, E., & Mollentze, S. (2010). Monetary economics in South Africa. Oxford University Press.

- Van Schalkwyk, C. H. (2012). Member choice in a defined benefit contribution pension plan: decision-making factors [Thesis – PhD]. University of Johannesburg.

- Wallach, M. A., & Kogan, N. (1961). Aspects of judgement and decision making: Interrelationships and changes with age. Behavioural Science, 6(1), 23–26. https://doi.org/10.1002/bs.3830060104

- Weston, R., & Gore, P. A. (2006). A brief guide to structural equation modeling. The Counseling Psychologist, 34(5), 719–751. https://doi.org/10.1177/0011000006286345

- Williams, D. J., & Noyes, J. M. (2007). How does perception of risk influence decision-making? Implications for the design of risk information. Theoretical Issues in Ergonomics Science, 8(1), 66–85. https://doi.org/10.1080/14639220500484419

- Witz, J., & Zemon, D. (2017). How to choose the right investment strategy: Consider investment goals, risk tolerance, and economic outlook when planning your strategy. Urology Times, 45(6), 27–28.

- Woodyard, A. S., & Grable, J. E. (2018). Insights into the users of robo-advisory firms. Journal of Financial Service Professionals, 72(5), 56–66.

- World Bank. (2021, July 13). Preserving macroeconomic stability, revitalizing jobs and improving investment climate critical for South Africa’s Post-COVID-19 recovery. Press Release. Retrieved March 27, 2022, from https://www.worldbank.org/en/news/press-release/2021/07/13/preserving-macroeconomic-stability-revitalizing-jobs-and-improving-investment-climate-critical-for-south-africa-s-post-c

- Yao, R., Hanna, S. D., & Lindamood, S. (2004). Changes in financial risk tolerance, 1983-2001. Financial Services Review, 13(1), 249–266.

- Yao, R., Sharpe, D. L., & Wang, F. (2011). Decomposing the age effect on risk tolerance. The Journal of Socio-Economics, 40(6), 879–887. https://doi.org/10.1016/j.socec.2011.08.023

- Yip, U. Y. (2000). Financial risk tolerance: a state or a trait [Thesis – PhD]. University of New South Wales.