?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper examines the role of national culture in the transmission process through which the growth in credit to the private sector can lead to bank stability in 107 countries over 2005 and 2017. We performed the examination using the quantile regression and the dynamic generalised method of moment to explore asymmetry properties in the panel dataset and address endogeneity challenges that can affect the efficiency of the results. We found that national culture dimensions influence the impact of financial innovation on bank stability. On the specific effect of national culture, we found that higher levels of indulgence and long-term orientation serve as a substitute for financial innovation in promoting bank stability. Higher levels of individuality and masculinity have no effects on the impact of financial innovation on bank stability. Higher power distance and uncertainty avoidance complement the relationship between financial innovation and bank stability. Finally, countries with lower levels of indulgence and long-term orientation can increase access to bank credit to boost banking system stability. The implication is that regulators should consider the cultural orientation of their communities in promoting sound financial intermediation.

1. Introduction

The banking system’s stability is critical for economic development. Banking institutions develop screening technologies to identify innovative businesses that can help boost economic activity (Laeven et al., Citation2015). Additionally, financial systems facilitate the importation of technologies to stimulate the development of advanced innovations and accelerate the convergence of per capita income between developing and developed economies (Aghion & Howitt, Citation1992; King & Levine, Citation1993; Aghion et al., Citation2005; Laeven et al., Citation2015; Idun, Citation2021). Stability in the banking system has a more significant impact on economic stability because it enables banks to invest effectively in productivity growth. On the other hand, the real sector’s performance can also influence the banking sector’s resilience. Banks can recoup all loan advances during expansionary periods because firms can sell their products and earn sufficient operating profits to repay their loans. The banking system can contribute to real sector instability.

Financial system integration is accelerating as the World of finance becomes more globalised. Advanced countries’ financial technologies quickly spread to emerging economies. Technological advancements in some economies are also facilitating financial inclusion. However, culture can accelerate or retard the spread of financial and technological innovation among technological imitators, thereby impacting global efforts to accelerate financial globalisation. Thus, the level of national culture can affect the interaction between the banking sector development and the stability of the real sector.

Culture shapes people’s aspirations, ethical values, norms, and general life in a particular society. The people’s culture can affect their decision-making. Nations are convergent in some ways, but certain cultural tenants reflect a community’s peculiarities, alienating them from the rest of the World. The cultural dimension that embodies openness, liberty, confidence, and risk tolerance can accelerate innovations and influence the banking sector’s credit allocation to productive sectors. Similarly, in predominantly collective, authoritative, and masculine societies, the acceptance of technological innovation that increases productivity can be determined by the society’s most powerful and opinionated members.

This article aims to examine the role of national cultural dimensions in determining the effect of financial innovation on bank stability. The article augments recent research that examines culture as a factor in the development of the banking sector (Ashraf et al., Citation2016; Boubakri et al., Citation2017; Cao et al., Citation2019; Mourouzidou-Damtsa et al., Citation2017) and those that suggest that national culture induces innovation by firms (Boubakri et al., Citation2021). While the impact of national culture has been studied in leadership, management, and international trade, recent research has focused on how national culture influences banks’ risk-taking orientation, performance, and choice of exchange rate regimes. This article examines how national culture can contribute to Schumpeterian creative destruction by emphasising how it can boost or dampen financial systems’ credit growth, posing liquidity challenges for banks in their credit distribution, thereby influencing the stability of banking systems. This paper is the first examination of all six of Hofstede’s national culture dimensions in the relationship between credit growth to support innovation and bank stability. Given the countries with usable data on national cultural dimensions, we conducted investigations from 2005 to 2017 using 107 countries. Due to the dataset’s non-parametric nature, we also used quantile regression analyses to examine the effect of national culture dimensions on banking systems’ stability.

Additionally, our analyses are unique. We decomposed national culture dimensions into higher and lower levels, allowing us to examine the national culture continuums that have the most significant impact on the relationship between financial innovation and bank stability. Finally, we addressed the issue of reverse causality by utilising a dynamic instrumental variable estimation procedure that eliminates endogeneity and ensures that panel data estimates are persistent.

We discovered that countries with above-average indulgence and uncertainty avoidance attenuate the impact of financial innovation on bank stability. Conversely, countries with a higher power distance and long-term orientation stimulate financial innovation into bank stability. In addition, we report that the six dimensions of national culture each have a non-linear but insightful impact on the various levels of bank stability.

The article makes several contributions to the empirical literature. First, the paper asserts that the contribution of financial intermediaries to high-quality innovations and financial stability cannot be assessed in isolation from a society’s cultural orientation. The paper contributes to Schumpeterian perspectives by emphasising the critical role of cultural institutions in materialising “creative destruction” to stimulate sound financial intermediation. The argument is that developing or adopting new financial processes to induce sound credit creation depends on the cultural orientation of societies. Because we used quantile regression, we were able to determine the effect of each cultural dimension on various levels of bank stability. The study’s sample size (107 countries) is more significant than comparable studies. Finally, we addressed endogeneity by employing an instrumental variable dynamic GMM with a time-fixed effect.

The next discusses the relevant literature on the issues. Section III presents the methods. Section IV contains the results and their discussions. Section V concludes the paper and offers recommendations.

2. Literature review

The debate over the impact of financial innovation on systemic risk appears unabated. Financial innovation, asset prices, collateralisation, bank diversification, information asymmetry, and profitability, among other factors, contribute to banks’ systemic risks (H. Kim et al., Citation2020; Arif, Citation2020; Islam et al., Citation2020). However, numerous channels exist to demonstrate the beneficial effect of financial innovation on sound financial intermediation to avert financial system instability. First, financial intermediaries employ stringent screening processes to weed out unscrupulous borrowers, ensuring that credit is directed toward productive sectors and thus toward productivity growth (Aghion et al., Citation2005; Laeven et al., Citation2015; Levine, Citation1997). The Schumpeterian perspectives hold financial institutions can identify technological innovators with viable innovations and provide additional funding sources for entrepreneurs to actualise their innovations when financiers employ rigorous screening processes. Because technological innovators receive rents from their innovations because of intellectual property protection (Acemoglu et al., Citation2012), innovators would be able to meet their loan obligations timeously to avoid loan impairment and ensure sound banking systems. By enabling the advancement of credit to innovators and risk spreading, financial innovation can increase liquidity and stimulate economic activity (King & Levine, Citation1993). Additionally, financiers can promote technological advancement by developing new financial products that facilitate exchange and ensure an efficient payment system.

Financial innovation has some negative aspects that necessitate scrutiny of its interventions, particularly in the competitive banking sector, where it is inextricably linked to banks’ risk-taking behaviour and performance (Ashraf & Arshad, Citation2017; Ashraf et al., Citation2016; Boubakri et al., Citation2017; Gaganis et al., Citation2020; El Ghoul & Zheng, Citation2016). Tufano (Citation2003) asserts that financial innovation can be used to skirt regulations (thereby exposing banks to systemic shocks) and minimise tax payments (thereby putting a strain on sovereign revenue mobilisation). Additionally, financial innovations can result in excessive liquidity, resulting in the development of high-risk financial products that disrupt economic activity (Merton, Citation1995; Pagano & Volpin, Citation2010; Kero, Citation2013). However, the impact of financial innovation on economic outcomes can be seen through the lens of the cultural institutions that define social norms, values, aspirations, what is desirable, and, more broadly, the behaviour and attitudes of society members. Thus, the influence of financial innovation on bank stability can be seen through the cultural lenses of society.

The influence of national culture on banking sector outcomes can be deduced from the suggestion that inclusive institutions promote financial development more than exclusive institutions. According to Acemoglu and Johnson (Citation2012), inclusive institutions promote the rule of law, effective governance, and property rights protection. Additionally, inclusive institutions encourage innovation and product variety by ensuring incumbents’ intellectual property rights (Romer, Citation1990; Acemoglu et al., Citation2012; Aghion & Howitt, Citation1992; Rousseau, Citation1998). The societal, cultural orientation is one aspect of institutional quality that can pervade economic activities. Hofstede’s Cultural Dimension provides a comprehensive framework for explaining nations’ cultural orientation and how culture can influence economic and social outcomes. National culture dimensions such as Individualism empowers political institutions to drive banks’ risk-taking behaviour. In regimes characterised by inclusive institutions, we expect the banks to leverage the political environment to achieve intermediation goals. National culture can influence the channel through which banks induce systemic liquidity because culture guides the behaviour of financial market participants.

According to Hofstede, organisations or nations have six dimensions of culture. These cultural dimensions include power distance, individualism/collectivism, aversion to uncertainty, masculinity/femininity, long-term versus short-term orientation, and indulgence/restraint (Minkov & Hofstede, Citation2014, Citation2011). The term “power distance” refers to how less powerful people accept and expect an unequal distribution of power among society’s members. A higher power distance score indicates that power is concentrated. In comparison, a lower score indicates that power is evenly distributed such that any member of society can challenge authority without fear or favour. This cultural dimension is relevant to this study as it influences decisions on adopting banking system innovations. For example, suppose a subordinate expects a superior to determine which new banking products or services to patronise. This relationship between the superior and the follower will affect how the innovations are adopted instead of the subordinate exercising free will and adopting the innovations without the superior’s consent. Financial innovation can have a more beneficial impact in a society where adoption decisions are evenly distributed among members than if the same is centralised. A community with a shorter distance between its centres of power can also import technological innovation for development. Bank and technological innovations that appeal to authoritative members of society may have a greater degree of acceptability in promoting bank stability, all other factors being equal.

Individualism/collectivism is the second dimension of national culture. Individualism refers to the degree to which members of society work for their own or the group’s/interests. Individuals in a highly individualistic society are more concerned with themselves or their immediate families than society. The lower the index, the higher the collective community level, with high commitment to the group, loyalty to societal culture, and adherence to societal cohesion. Individualism countries are typically developed countries. Incorporating national culture into the nexus between financial innovation and bank stability will aid in elucidating the critical role of developmental level and institutional quality in enhancing the soundness of financial systems. Bank managers operating in societies with a higher degree of Individualism will increase the risk even if they are foreign nationals, meaning they do not have to share the same national culture (Cao et al., Citation2019). Individualistic societies are more likely to accommodate banks’ risk-taking behaviour (Mourouzidou-Damtsa et al., Citation2017) to ensure effective and sound financial intermediation.

On the other hand, the cushion hypothesis suggests that high collective societies encourage individual risk-taking. The suggestion is that cooperative society have systems to support members who fail in competitive engagements. The implication is that risk-taking and competitive behaviour in collective communities are likely to be high because of collective supports channels.

The third dimension of national culture is the avoidance of uncertainty. This is a measure of a society’s ambiguity tolerance. On the continuum, a community with a higher tolerance for ambiguity is more likely to accept new developments and alter the status quo. In contrast, a society with a lower tolerance for ambiguity (a greater degree of uncertainty avoidance) is more likely to avoid innovations. Uncertainty avoidance is critical to this study because, in societies that avoid innovation, bank innovations may harm financial intermediation, jeopardising the banks’ stability.

Masculinity/femininity is the fourth dimension of national culture. According to Hofstede, masculinity is defined as “a social preference for achievement, heroism, assertiveness, and material rewards for success,” whereas femininity is defined as “a social preference for cooperation, modesty, caring for the weak, and a high quality of life.” Masculinity/femininity connote the roles of males/females in society. Whereas masculinity prioritises male values in the community, femininity prioritises female values. A low score on Hofstede’s index indicates feminism, which suggests that a more significant segment of society is concerned with the welfare of others and the quality of life. A more masculine culture scores higher, indicating a willingness to compete and a desire to be the best.

The fifth dimension of national culture is Long-term/short-term orientation which indicates the degree to which traditions are upheld and protected instead of future challenges. A society that records low values of this index maintains rules and conventions and are less likely to prioritise present and future challenges. Such communities are less likely to accept changes. On the other hand, societies that are long-term oriented embrace changes to improve and prepare for the future. Short-term oriented communities are considered normative, whereas long-term oriented communities are considered pragmatic. A low score on long-term orientation depicts that the countries show adherence to traditions, less propensity to save for the future and prefer quick results. This can affect their receptibility of innovations towards the stability of the banking systems.

The last dimension of culture is indulgence/restraint, which indicates how members of societies are controlled. Lower scores imply people have discretion concerning their desires and impulses, whilst higher scores suggest a greater degree of indulgence or freedom to pursue one’s course. In restrained communities, cynicism and pessimism are high, indicating very close socialisation where people’s actions and desires are controlled. A society with a higher degree of indulgence can assimilate new ideas and innovations than societies with a higher degree of restraint.

In general, culture is the overall character—“the collective mental programming of people in an environment” (Attah-Boakye et al., Citation2020). National culture influences the degree to which firms can adopt innovative practices (Van Everdingen & Waarts, Citation2003), firm’s entrepreneurial activities (Turro et al., Citation2014), firm’s financial performance and management outcomes (Hooghiemstra et al., Citation2015). National culture also induces a firm’s risk-taking behaviour (Li, Griffin, Yue, & Zhao, Citation2013), dividend policy (Shao, Kwok, Guedhami, Citation2010) and earnings quality (Kanagaretnam, Lim, & Lobo, Citation2011). National culture dimensions also influence a firm’s innovation orientation (Boubakri et al., Citation2021; Chen et al., Citation2017). The authors found that firms in higher individualistic (uncertainty-avoidance) countries induce (reduce) higher patent impact and convert research and development expenditure into product innovations. On the effect of national culture on the performance of banks during the global financial crisis, Boubakri et al. (Citation2017) establish that uncertainty avoidance, collectivism, and power distance have a first-order impact on bank performance during the crisis. Culture as an informal institutional framework can determine the action of both financiers and their clients to influence information flow to induce bank stability.

Despite the emerging discourse on the role of national culture in financial intermediation and financial stability, the extant literature has not evaluated the role of culture in the Schumpeterian perspective where financiers are facilitators of technological innovation and stability of the financial systems. This paper addresses the role of the six national culture dimensions in the transmission of financial innovation into bank stability.

3. Methods

We collected secondary data on the variables from the Global Financial Development Database (2020), World Development Indicator (WDI) (2020) and Hofstede’s Insight Online Edition. The GFDD provided data on bank concentration (BC) and the Z-score (BS). The WDI provide data on control variables, namely GDP per capita (GD), inflation (INF), trade openness (TRADE) and cellular mobile coverage (MOB). We obtained data on the national culture dimensions from Hofstede’s National Culture database. The period for the study is 2005–2017. The number of countries included is 107 making the expected number of observations for the panel data structure 1391. However, there are unavailable observations in the dataset, so we worked with unbalanced data. There is a reason to believe that the unbalanced nature of our dataset would not affect the efficiency of our estimates because the generalised methods of moment (GMM) technique take care of such irregularities by using the first differences of the variables in its estimation. Notwithstanding, the first differencing associated with the GMM technique led to the loss of a degree of freedom. The empirical section shows that the degree of freedom becomes less than 1000 for all our GMM estimations due to the use of first differencing in the estimations.

Model Specification

The paper used the dynamic generalised method of moments (GMM) estimation techniques to meet the objectives of the role of the national culture dimensions in the effect of financial innovation on bank stability. The GMM procedure has advantages of reducing endogeneity, heteroskedasticity and serial correlation. The GMM model requires the use of instruments that are correlated with the explanatory variables but at the same time uncorrelated with the error term. We used the first lags of the explanatory variables as transformed instruments. For the untransformed instruments, we used the six national culture dimensions. To address the issue of endogeneity, we carried out the Sargan test of overriding identity. The null hypothesis of the Sargan test states that the instrument used is endogenous, meaning they corrected with the explanatory variables and uncorrected with the error term.

Similarly, to address the issue of serial correction, we used the Arellano-Bond AR(2) test to investigate the presence or absence of serial correlation. For this test, a higher p-value (P-value greater than 0.05) indicates the absence of serial correlation. The GMM method treated the lags of the dependent variable (bank stability) as endogenous, and the model is stated as follows:

where,

BS is bank stability measured by the z-score;

Control var is the set of control variables, namely, GDP per capita (GDP), inflation(INF), technological infrastructure coverage (MOB), Trade openness (TRADE) and bank concentration (BC).

FIN is financial innovation

NCD is the national culture dimensions

are the period effects; and

is the error term.

We included GDP per capita because a nation’s income determines economic activity and can influence firms’ decisions to innovate, sell their products, and use a portion of the proceeds to repay loan obligations. Inflation can affect the cost of borrowing, reducing firms’ willingness to seek additional funding from banks. Cellular penetration measures the technological infrastructure and spread of internet banking, SMS banking, mobile money banking, and bank transfers, among other services. Trade openness is a proxy for the degree to which globalisation has resulted in the spillover effect of shocks from interdependent economies, resulting in financial instability. Finally, the level of bank concentration influences the banks’ competitive behaviour, which affects their risk-taking behaviour.

The GMM procedure is suitable for the study because our dataset contains smaller time-series dimensions than cross-sections. The study also used quantile regression to analyse the effect of each of the national culture dimensions of bank stability. Introduced by Koenker and Bassett (Citation1978), quantile regression estimates the linear relationship between the regressors and a specified quantile of the dependent variable. One significant application of quantile regression is the least absolute deviations (LAD) estimator, which fits the response variable’s conditional median.

Quantile regression enables a more comprehensive description of the conditional distribution than conditional mean analysis alone, allowing us to describe how regressor variables affect the median or perhaps the 10th or 95th percentile of the response variable. Additionally, because quantile regression requires no strong distributional assumptions, it is a robust method for modelling these relationships.

3.1. Measurement of financial innovation

The Bank for International Settlement classifies financial innovation into price-risk-transferring innovations, credit-risk-transferring instruments, liquidity generating innovations, credit-generating instruments and equity-generating instruments. Price-risk-transfer innovations alleviate investors or consumers of volatility in exchange rates and inflation rates. Credit-risk-transferring instruments are those that banks and other financial institutions use to transfer their default risks. Also, liquidity-generating innovations include those that increase the liquidity of the financial market, allow surplus units to draw on new sources of funds and permit stakeholders to circumvent capital constraints imposed by regulations. Similarly, credit-generating innovations are meant to increase borrowings by offering borrowers a greater depth of credit allocation. Finally, equity-generating instruments are introduced to boost the capital base of financial institutions (Abor, Citation2018).

Overall, financial innovations can be grouped into the product, process and financial system/institutional innovations (Tufano, Citation2003). Product innovations are the new financial products such as cashless accounts, home-savers accounts, off-shore banking, premier banking, mobile money and special deposits. Process innovations are meant to facilitate financial services delivery. They include automated teller machines, electronic cards, telephone banking, SMS banking, internet banking, etc. these days, the proliferation of ICT infrastructure fuels process innovations and these have influenced the choice of cellular/mobile telecommunication infrastructure as proxies for technological or process innovations (Idun, Citation2021). Laeven et al. (Citation2015), as well as Idun and Aboagye (Citation2014) and Idun (Citation2021), used the speed with which a country adopts credit information sharing systems as a measure for financial innovation. Finally, institutional innovations are the changes in the financial system or the emergence of a new financial institution because of regulation. Laeven et al. (Citation2015), Idun and Aboagye (Citation2014), and Idun (Citation2021) used the growth in the financial system’s credit disbursement as a measure of financial system innovation.

Following Laeven et al. (Citation2015), Idun and Aboagye (Citation2014), and Idun (Citation2021), the researcher employed the growth in bank credit to the private sector (to capture innovations in banking systems intermediation that enhance credit generation and boost liquidity). Other studies have used patents’ impact and research and development expenditure. These measures relate to attempts by firms to innovate and development of new products, respectively. However, expenditure on R&D and processes leading to the acquisition of patent rights can be financed with the growth in credit to the private sector. This assertion is in line with the Schumpeterian growth theory, which suggests that new sources of finance are used to finance innovations by firms (Aghion & Howitt, Citation1992; Aghion et al., Citation2005; Laeven et al., Citation2015). Our measurement of financial innovation assumes that firms will use bank loans to finance their innovations, even though other studies suggest that innovative firms prefer to use equity to finance corporate innovations (Boubakri et al., Citation2021).

There are compelling reasons firms would want to use additional credit facilities to finance their innovation activities instead of equity. To begin with, not all firms have the capacity to raise additional funds through initial public offerings (IPOs), barring the excessive costs associated with IPOs. Bank credits can enhance financial leverage, increasing their performance because managers would have to cover at least the finance cost within the an accounting period. Bank credit leads to an interest tax shield because of the interest payment, which can increase return on equity and enhance shareholders’ value (owners). Firms with an optimal debts in their financing structure can increase tax benefits to the tune of 5.2% of firm value (Graham, Citation2002; Ko & Yoon Citation2011). Martin (Citation2003) also showed with Canadian data that more debt financing could decrease the commitment level of firm-specific capital and make entry into an industry profitable. The implication is that more debt financing can help managers increase shareholders’ wealthven though more debt financing can also increase the incentive for shareholders to assume more risk (Green & Talmor, Citation1986). Finally, the acquisition of bank loans can send signals to the financial market that the firm is well-managed, and therefore, financiers are willing to extend more credits to the firm’s manager.

3.2. Measurement of bank stability

Bank stability is seen as the ability of a bank to withstand shocks because of its strong liquidity or capitalisation position. Bank stability in gauging a bank’s risk of insolvency is measured by value-at-risk and expected shortfalls. The capital assets pricing model (CAPM) can also be used to determine the chances of individual banks by regressing the bank’s expected return by the market return of an index. Basel II and Basel III recommend these measures, but they are applicable for only listed banks since they are market-based measures and therefore unsuitable for unlisted banks. For unlisted banks, accounting-based risk measures can be used. Some studies have used the ratio of non-performing loans to total assets and the variations in the z-score to proxy bank stability or the bank’s probability of failure. Haldane (Citation2009), however argues that these traditional accounting measures fail to capture the downside risks of banks in periods of financial crises—to capture the interdependence of banks in a banking system and the contagion effect of systemic risks. Therefore, in the post-2007/2008-crisis period, attention of researchers has been drawn to the use of measures that capture the rippling effect of a bank’s failure on systemic risk. The study used the parsimonious z-score, which rely on regulated accounting data in its estimation as a proxy for bank stability to maintain uniformity in measurement. The standard z-score is estimated as

where,

ROA is a bank’s return on assets; and

SD(ROA) is the standard deviation of ROA

The numerator shows the bank’s buffer to withstand unfavourable conditions such as a bank run or inadequate deposits and the denominator reflects the variability of the bank’s earnings. The higher the numerator, the better positioned a bank is to continue operating in the wake of crises. Therefore, a larger equity-capital-based bank is considered more stable given the variability in its earnings. A higher z-score indicates a lower risk of a bank and vice-versa.

Various variations of the z-score have been used in the other empirical studies. Some studies used the overall sample standard deviation as the denominator and the ROA and equity-assets ratio as the numerator (Laeven & Levine, Citation2009; Cihak, Citation2007; Beck & Laeven, Citation2006). Other writers also used mean figures of ROA, equity-to-total assets, and the standard deviation of ROA to estimate the z-score (Bertay, Demirguc-Kunt & Huizinga, Citation2013). However, the denominator in the equation of their measure of the z-score is time-invariant, which may not capture the risk profile of banks across time. This problem can be minimised by using higher frequencies of the variables in equation (1) to estimate the z-score.

4. Findings and discussions

4.1. Descriptive statistics

We transformed the six national culture dimensions into 12 dummy variables, each for higher and lower dimensions (see ). For example, the dummy for above-average power distance (PD) takes 1 if a country has a power index average above our sample mean of power distance (66.93) and 0 if a country’s score is below this average. We repeated the dummy creation procedure for all the other 11 categorisations. We, therefore, had 12 above—and below averages for the six dimensions.

Table 1. Definition and roles of the variables

Table shows the distribution from the categorisation of the cultural dimensions. We see that 59% of our sample countries have above-average power distance whilst 41% have a below-average level of power distance. The distribution on power distance indicates that the nations are mostly authoritarian communities where members look up to people of authority when making decisions. Also, the mean score for Individualism is 37.54. 38% of the countries have their level of Individualism above the average score, and 62% have scores below the mean average which shows that majority of the countries are collective communities that strive for the betterment of society more than individual goals. The average score for masculinity is 46.95, which indicates the communities are tilting towards feminists’ societies which emphasises the embracement of the minority views. 48% of the nations have above average level of masculinity whilst 52% have an above level of masculinity.

Table 2. Facts on the Hofstede’s national culture dimensions

Similarly, the average level of uncertainty avoidance is 66.49, which is high. Of this, 52% of the sample have above-average uncertainty avoidance scores, leaving only 48% with below-average uncertainty avoidance scores. This means that the communities are receptive to new ideas and ways of doing things. Such communities are inclined to accept financial innovation, and we must determine how uncertainty avoidance influence the relationship between financial innovation and bank stability.

In addition, the average level of long-term orientation is 43.35 in a continuum of 0 to 100. This means the societies are essentially short-term oriented. The implication is that our sample countries mostly prefer innovations that can solve their immediate financial problems. Among the countries, 46% scored above average long-term orientation, and 54% achieved a below-average level of long-term orientation. Finally, the level of indulgence for the observation is 46.46. 45% of the communities had an above-average index of indulgence, whilst 55% had below-average scores of indulgences. This shows that our sample countries are less receptive to openness. We expect low indulgence countries to have other means of ensuring that bank stability is maintained other than relying on financial innovation to promote bank stability.

Table also shows that national culture dimensions differ across per capita income clubs. Power distance is highest in lower-middle-income countries and lowest in high-income countries (53.33). Conversely, Individualism, long-term orientations and indulgence are highest in high-income countries than the other income groups. Similarly, uncertainty avoidance is higher in upper-middle-income countries (71.50) and high-income countries (66.79) than lower-middle-income countries (63.50) and low-income countries (52.33). Masculinity tends to be higher in upper-middle-income countries. Lower-middle income countries recorded the lowest level of masculinity.

The distribution of cultural dimensions across the countries in our sample is shown in Table . Malaysia (100) and Slovakia have the greatest power distance, while Guatemala, Panama, and Saudi Arabia have 95. Austria had the smallest power distance (11). Surprisingly, countries with solid religious inclinations, such as Israel, also had low levels of power distance, in contrast to Malaysia and Saudi Arabia. Australia ranked highest in terms of Individualism (90), while Guatemala ranked lowest in terms of Individualism (70). Generally, countries with a high degree of power distance also demonstrated a low degree of Individualism and vice versa. On the other hand, Japan, Argentina, and the Czech Republic have a moderate power distance and individualism.

Table 3. Distribution of national culture dimensions for the sampled countries

Similarly, Slovakia has a certainty level of masculinity (100), which creates a community for the strong when combined with a certainty level of power distance. Scandinavian countries such as Norway, Latvia, and Denmark have low masculinity rates, indicating that their communities support the weak. Greece has the highest uncertainty avoidance index at 100, while Singapore has the lowest index at 8. Ghana’s long-term orientation is the lowest among the 107 nations, even though the country has a solid index for power distance and indulgence. Conversely, Taiwan has the most potent form of long-term orientation. Venezuela, Mexico, Puerto Rico, El Salvador and Columbia have high indulgence. It shows that the South American countries inculcate a risk-loving attitude among their societal members, which indicates that they tend to be receptive to innovations. In the same token, Egypt, Latvia, Albania, and Belarus are among the countries with the weakest level of indulgence. The divergence among cultural dimensions among the countries indicates the different levels of financial innovation and bank stability.

Table illustrates the average values of financial innovation and bank stability. Bank stability for the whole sample averages 14.40. Countries such as Jordan, Panama, Libya, Morocco, Luxembourg and Tunisia have very high above-average levels of bank stability. However, these countries have below-average level of financial innovation (0.024), signifying that financial innovation may not directly impact bank stability. In the same token, countries with below-average levels of bank stability mostly have above-level growth in credits.

Table 4. Averages of Z-scores and financial innovation (growth in credit) for the sampled countries 2005–2017

4.2. Empirical results

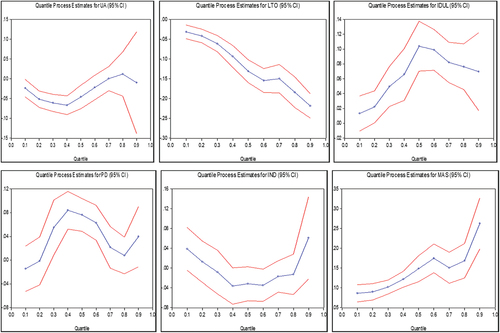

Figure depicts the graphical results from the quantile regression for the relationship between the national culture dimensions and bank stability. It shows that uncertainty avoidance generally positively influences bank stability even though getting to the 90th quantiles. The relationship appears to dip downward, indicating that at the highest level of bank stability, as did in indulgence, can be detrimental to global banking stability. This relationship between uncertainty avoidance and bank stability is also reflected at the lower level of bank stability. From the 10th to 40th quantiles (lower level of bank stability), we see that an increase in uncertainty avoidance leads to a drop in bank stability. The relationship between uncertainty avoidance and bank stability implies cultures with high risk-loving propensities are more likely to ensure their banking system stability.

Figure 1. Quantile regression estimates of the relationship between national culture dimensions and bank stability source: authors.

The second quadrant at the top panel of Figure represents the quantile relationship between long-term orientation and bank stability. In general, there is a significantly strong negative relationship between long-term orientation and bank stability at the various levels. This implies that in regimes with a long-term planning focus, bank stability is likely stifled. In the subsequent analyses in this paper, we will see whether financial innovation can reduce the indirect implication of long-term orientation on bank stability.

In the third quadrant of the top panel, indications are that the level of indulgence has an inverted u-shaped relationship with the level of bank stability. At the median level of bank stability, the relationship between indulgence and bank stability is at a peak. Below the median level of bank stability, rising levels of indulgence have a positive impact on bank stability which indicates that high risk-taking propensity among the community can harm reduce stability. Conversely, above the median level of bank stability, an increase in indulgence attenuates banking system stability. Therefore, the level of bank stability optimises the influence of bank stability and indulgence. Some indulgence levels are good for bank stability, but higher levels of indulgence can be detrimental to global bank stability.

The lower panel of Figure shows the results of the relationship between power distance (PD), individuality (IND) and masculinity (MAS). The quantile relationship between PD and bank stability is rising at the lower levels of bank stability. As the level of stability falls, power distance positively affects bank stability. The result shows an indirect relationship between bank stability and power distance. Conversely, at the higher levels of bank stability, below the 80th percentiles, higher power distance leads to lower bank stability. Beyond the 80th percentile, rising power distance induces bank stability. The relationships between power distance and bank stability optimise at the 40th quantile.

The second quadrant of the lower panel of Figure shows that the relationship between Individualism and bank stability is U-shaped. At the lower level of bank stability, higher Individualism leads to a decline in bank stability. Between the 40th and 80th deciles, the relationship flattened and, after that, rose. The minimum threshold (60th decile of bank stability) optimises the relationship between Individualism and bank stability. Tajaddini and Gholipour (Citation2017) found that mortgage borrowers from regimes with above-average Individualism are more likely to default on their mortgage agreement in both regular and crisis periods.

Finally, the last quadrant of the lower panel shows that at the 95% confidence level that there is a strong positive relationship between masculinity and bank stability. This translates to mean that male-dominated roles improve bank stability.

4.3. The role of national culture in the relationship between financial innovation and bank stability

Table depicts the GMM estimates on the role of the national culture in the effect of financial innovation on bank stability. The first column of the table has the acronyms of the variables. The above subjects are estimated from the second through to the six column of the table. As stated earlier, the six national culture dimensions were decomposed into above-average and below-average dummies. The resulting dummies were interacted with the proxy for financial innovation to determine the collective impact on bank stability. The second to the seventh columns of Table contains the above-average national culture dimensions and financial innovation levels. Similarly, the eighth to thirteenth columns include the interactions between the below-average culture dimensions and financial innovation on bank stability. We interpreted the role of national culture by adding the coefficients of the interaction terms to the coefficients of financial innovation for all estimations.

From the upper panel of Table , the lag of bank stability (BS(−1)) strongly impacts the current level of bank stability, confirming endogeneity. This shows that the previous year’s bank stability has a rippling effect on the current situation of bank stability. Inflation has a positive impact on bank stability for all estimations. The implication is that the banks factor in the expected level of inflation in their liquidity and credit management to assuage the negative impact of rising prices on their intermediation operations. Similarly, trade openness (TRADE) has a strong positive effect on bank stability. Trade can provide the banks with diversified clientele, reducing their sovereign risk and inducing more excellent stability. However, the level of bank concentration has an indirect impact on bank stability which implies that the drive for market share encourages the banks to engage in risky activities that have detrimental effects on bank stability. Large banks can increase the loan rates, which stifles liquidity and makes it harder for firms to honour their loan obligations (Pagano, Citation1993).

Table 5. The role of national culture dimensions in the relationship between financial innovation and bank stability

From column 2, high levels of indulgence (INDULH) have a strong negative moderation effect in the relationship between financial innovation and bank stability. Communities with a high level of indulgence are those with high risk-taking propensity. This means that risk-taking, an inherent quality in financial innovation, can injure bank stability. Conversely, low indulgence plays a positive role in the relationship between financial innovation and bank stability. The result is in line with the established relationship between indulgence and bank stability in Figure that indulgence positively impacts stability at the lower level of bank stability. The implication is that only low to moderate indulgence can promote financial innovation, leading to bank stability. The result is in line with Tajaddini and Gholipour (Citation2017), who reported that borrowers from regions of high level of indulgence (low level of pragmatism) are more (less) prone to mortgage loan default.

Column EQ03 contains significant results for the interaction between financial innovation and long-term orientation. The joint effect shows that long-term exposure can dampen the effect of financial innovation on bank stability. The moderating effect of long-term orientation is negative which means it serves as a substitute to financial innovation in inducing bank stability. When financial innovation fails to achieve the desired results in financial intermediation, the society’s long-term focus can enhance bank stability. This assertion can be true because long-term planning can lessen the effect of liquidity or systemic shock emanating from the wrong sides of financial innovation.

Column EQ05 depicts the interaction’s strong significant negative effect of financial innovations on bank stability for countries with above-average power distance. Members of such communities depend on top hierarchy people to inspire their decisions to embrace the diffusion of financial innovations. When such inspirations are not forthcoming, members of society may be reluctant to adapt changes in the financial environment which can circumvent the focus of financial innovation towards bank stability. Similarly, financial innovation is detrimental to bank stability for countries with a below-average levels of power distance which confirms the assertion that power distance communities may not induce financial innovation to promote bank stability. Boubakri et al. (Citation2017) also found that banks operating in higher power-distance regimes would increase their performance during crises.

The last significant moderation effect examined is the role of uncertainty avoidance in the relationship between financial innovation and bank stability. Column EQ06 shows that financial innovation has a strong positive impact on bank stability for countries with an above-average levels of uncertainty avoidance. Conversely, financial innovation has a strong negative impact on bank stability for countries with a below-average levels of uncertainty avoidance. The results imply that communities with low to moderate risk tolerance can channel financial innovation into bank stability. High risk-tolerance cultures can cause financial instability with increased liquidity in the real sectors. The implication is that low to moderate risk-tolerance societies positively impact bank stability when more credits are channelled into innovations. The results are consistent with Chen et al. (Citation2017), which found that firms with higher levels of uncertainty avoidance correlate with fewer and fewer patents and efficient research and development expenditure. The findings contrast with that of Ashraf et al. (Citation2016) that risk-taking is high in countries with below-average uncertainty avoidance. In the same token, Boubakri et al. (Citation2017) reported that banks operating in environments with higher uncertainty avoidance are more likely to increase their performance during crisis periods.

The last but one panel of Table shows the effects of the time-dummies on bank stability. Essentially, we find that the period of the global financial crises (2007–2008) had strong negative effects on bank stability. The 2009 experienced an appreciable level of bank stability. However, structural shocks in liquidity also occurred in 2011 and 2014 after the recovery in 2012.

The final panel of Table contains the results of the Sargan Overriding Identity Tests, the Arellano and Bond Serial Correlation Tests, and the observations following the first differencing. The Sargan test determines whether the instruments included correlating with the term “innovation.” The Sargan test’s higher p-values demonstrate no conflicting identity and that the instruments are efficient because they do not correlate with the errors. Similarly, the high p-values of the AR(2) tests demonstrate that the estimations are free of serial correlations. The diagnostic tests indicate that the results and persistent endogeneity issues do not impair the results’ efficacy.

5. Conclusion

We examined how national culture can help managers of financial institutions effectively channel new credits into a a productive sectors that can induce the soundness of the banking sector. We expect countries with a high levels of indulgence, Individualism, and masculinity to cause more remarkable risk-taking behaviour among bank managers which can be detrimental to banking systems stability. Similarly, we expect countries with high levels of long-term orientation, power distance and uncertainty avoidance to make managers be risk-averse and hence take decisions that can induce banking system stability barring other external shocks. This study contributes to the literature by emphasising that national culture is critical in advancing and imitating the use of innovations in sound financial intermediation. The study reports that high levels of indulgence and uncertainty avoidance can induce a a positive relationship between financial innovation and bank stability.

Conversely, high levels of long-term orientation and power distance dampen the impact of financial innovation on bank stability. We did not find any evidence that individuality and masculinity influence the effects of financial innovation on bank stability. The management of financial institutions should consider the cultural orientations of the societies within which they operate when advancing credit that would ensure sound financial systems. Central Banks should incorporate national culture dimensions into macro-prudential regulations to promote good banking systems. Further studies can investigate whether the insignificant role of Individualism and masculinity in the relationship between financial innovations and bank stability is due to the confounding effect of financial transparency in the credit market. We also recommend that the researchers’ community conduct further investigation into using the equity market since this study concentrated on the credit market.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Abor, J. Y., Amidu, M., & Issahaku, H. (2018). Mobile telephony, financial inclusion and inclusive growth. Journal of African Business, 19(3), 430–27. https://doi.org/10.1080/15228916.2017.1419332

- Acemoglu, D., Gancia, G., & Zilibotti, F. (2012). Competing engines of growth: Innovation and standardisation. Journal of Economic Theory, 147(2), 570–601. https://doi.org/10.1016/j.jet.2010.09.001

- Acemoglu, D., Johnson, S., & Robinson, J. A. (2012). The colonial origins of comparative development: An empirical investigation: Reply. The American Economic Review, 102(6), 3077–3110. https://doi.org/10.1257/aer.102.6.3077

- Aghion, P., & Howitt, P. (1992). A model of growth through creative destruction. Econometrica, 60(2), 323–351. https://doi.org/10.2307/2951599

- Aghion, P., Howitt, P., & Mayer-Foulkes, D. (2005). The effect of financial development on convergence: Theory and evidence. Quarterly Journal of Economics, 120(1), 173–222.

- Allen, F., & Gale, D. (2004a). Financial intermediaries and markets. Econometrica, 72(4), 1023–1061. https://doi.org/10.1111/j.1468-0262.2004.00525.x

- Arif, A. (2020). Effects of securitisation and covered bonds on bank stability. Research in International Business and Finance, 53, 101196. https://doi.org/10.1016/j.ribaf.2020.101196

- Ashraf, B. N., & Arshad, S. (2017). Foreign bank subsidiaries’ risk-taking behavior: Impact of home and host country national culture. Research in International Business and Finance, 41, 318–335. https://doi.org/10.1016/j.ribaf.2017.04.039

- Ashraf, B. N., Zheng, C., & Arshad, S. (2016). Effects of national culture on bank risk-taking behaviour. Research in International Business and Finance, 37, 309–326. https://doi.org/10.1016/j.ribaf.2016.01.015

- Attah-Boakye, R., Adams, K., Kimani, D., & Ullah, S. (2020). The impact of board gender diversity and national culture on corporate innovation: A multi-country analysis of multinational corporations operating in emerging economies. Technological Forecasting and Social. Change, 161, 120247. https://doi.org/10.1016/j.techfore.2020.120247

- Beck, T., & Laeven, L. (2006). Resolution of Failed Banks by Deposit Insurers. Cross-Country Evidence, World Bank Policy Research Working Paper, 3920.

- Bertay, A. C., Demirgüç-Kunt, A., & Huizinga, H. (2013). Do we need big banks? Evidence on performance, strategy and market discipline. Journal of Financial Intermediation, 22(4), 532–558. https://doi.org/10.1016/j.jfi.2013.02.002

- Boubakri, N., Chkir, I. E., Saadi, S., & Zhu, H. (2021). Does national culture affect corporate innovation? International evidence. Journal of Corporate Finance, 66, 101847. https://doi.org/10.1016/j.jcorpfin.2020.101847

- Boubakri, N., Mirzaei, A., & Samet, A. (2017). National culture and bank performance: Evidence from the recent financial crisis. Journal of Financial Stability, 29, 36–56. https://doi.org/10.1016/j.jfs.2017.02.003

- Cao, Z., El Ghoul, S., Guedhami, O., & Kwok, C. (2019). National culture and the choice of exchange rate regime. Journal of International Money and Finance, 102091. https://doi.org/10.1016/j.jimonfin.2019.10209

- Chen, Y., Podolski, E. J., & Veeraraghavan, M. (2017). National culture and corporate innovation. Pacific-Basin Finance Journal, 43, 173–187. https://doi.org/10.1016/j.pacfin.2017.04.006

- Čihák, M. (2007). Systemic loss: A measure of financial stability. Czech Journal of Economics and Finance, 57(1–2), 5–26.

- El Ghoul, S., & Zheng, X. (2016). Trade credit provision and national culture. Journal of Corporate Finance, 41, 475–501. https://doi.org/10.1016/j.jcorpfin.2016.07.00

- Gaganis, C., Hasan, I., & Pasiouras, F. (2020). National culture and housing credit. Journal of Empirical Finance, 56, 19–41. https://doi.org/10.1016/j.jempfin.2019.12.003

- Graham, J., & Harvey, C. (2002). How do CFOs make capital budgeting and capital structure decisions? Journal of Applied Corporate Finance, 15(1), 8–23. https://doi.org/10.1111/j.1745-6622.2002.tb00337.x

- Green, R. C., & Talmor, E. (1986). Asset substitution and the agencycosts of debt financing. Journal of Banking & Finance, 10(3), 391–399. https://doi.org/10.1016/S0378-4266(86)80028-0

- Haldane, A. (2009). Why banks failed the stress test. BIS Review, 18.

- Hooghiemstra, R., Hermes, N., & Emanuels, J. (2015). National culture and internal control disclosures: A cross‐country analysis. Corporate Governance: An International Review, 23(4), 357–377. https://doi.org/10.1111/corg.12099

- Idun, -A.-A.-A. (2021). Does finance lead to economic growth convergence in Africa? The Journal of Developing Areas, 55(3), 23–56. https://doi.org/10.1353/jda.2021.0051

- Idun, -A.-A.-A., & Aboagye, A. Q. Q. (2014). Bank competition, financial innovations and economic growth in Ghana. African Journal of Economics and Management, 5(1), 30–51.

- Islam, M., Olalere, E. O., Sobhani, F. A., & Shahriar, M. S. (2020). The effect of product market competition on stability and capital ratio of banks in Southeast Asian countries. Borsa Istanbul Review, 20(3), 292–300. https://doi.org/10.1016/j.bir.2020.03.001

- Kanagaretnam, K., Lim, C. Y., & Lobo, G. J. (2011). Effects of national culture on earnings quality of banks. Journal of International Business Studies, 42(6), 853–874. https://doi.org/10.1057/jibs.2011.26

- Kero, A. (2013). Banks’ risk taking, financial innovation and macroeconomic risk. The Quarterly Review of Economics and Finance, 53(2), 112–124. https://doi.org/10.1016/j.qref.2013.01.001

- Kim, H., Batten, J. A., & Ryu, D. (2020). Financial crisis, bank diversification, and financial stability: OECD countries. International Review of Economics & Finance, 65, 94–104. https://doi.org/10.1016/j.iref.2019.08.009

- King, R. G., & Levine, R. (1993). Finance, entrepreneurship, and growth: Theory and evidence. Journal of Monetary Economics, 32(3), 513–542. https://doi.org/10.1016/0304-3932(93)90028-E

- Ko, J. K., & Yoon, S. S. (2011). Tax benefits of debt and debt financing in Korea. Asia‐pacific Journal of Financial Studies, 40(6), 824–855. https://doi.org/10.1111/j.2041-6156.2011.01059.x

- Koenker, R., & Bassett, G. (1978). Regression quantiles. Econometrica, 46(1), 33–50. https://doi.org/10.2307/1913643

- Laeven, L., & Levine, R. (2009). Bank governance, regulation and risk taking. Journal of Financial Economics, 93(2), 259–275. https://doi.org/10.1016/j.jfineco.2008.09.003

- Laeven, L., Levine, R., & Michalopoulos, S. (2015). Financial innovation and endogenous growth. Journal of Financial Intermediation, 24(1), 1–24. https://doi.org/10.1016/j.jfi.2014.04.001

- Levine, R. (1997). Financial development and economic growth: Views and agenda. Journal of Economic Literature, 35(2), 688–726.

- Li, K., Griffin, D., Yue, H., & Zhao, L. (2013). How does culture influence corporate risk-taking? Journal of Corporate Finance, 23, 1–22. https://doi.org/10.1016/j.jcorpfin.2013.07.008

- Li, X., Tripe, D., & Malone, C. (2017). Measuring bank risk: An exploration of z-score. SSRN Electronic Journal.

- Martin, R. (2003). Debt financing and entry. International Journal of Industrial Organization, 21(4), 533–549. https://doi.org/10.1016/S0167-7187(02)00088-7

- Merton, R. C. (1995). Financial innovation and the management and regulation of financial institutions. Journal of Banking & Finance, 19(3–4), 461–481. https://doi.org/10.1016/0378-4266(94)00133-N

- Minkov, M., & Hofstede, G. (2011). Is national culture a meaningful concept? Cross-Cultural Research, 46(2), 133–159. https://doi.org/10.1177/1069397111427262

- Minkov, M., & Hofstede, G. (2014). Clustering of 316 European regions on measures of values. Cross-Cultural Research, 48(2), 144–176. https://doi.org/10.1177/1069397113510866

- Mourouzidou-Damtsa, S., Milidonis, A., & Stathopoulos, K. (2017). National culture and bank risk-taking. Journal of Financial Stability, (40), 132–143. https://doi.org/10.1016/j.jfs.2017.08.007

- Pagano, M. (1993). Financial markets and growth: An overview. European Economic Review, 37(2–3), 613–622. https://doi.org/10.1016/0014-2921(93)90051-B

- Pagano, M., & Volpin, P. (2010). Credit ratings failures and policy options. Economic Policy, 25(62), 401–431. https://doi.org/10.1111/j.1468-0327.2010.00245.x

- Romer, P. M. (1990). Endogenous technological change. The Journal of Political Economy, 98(5, Part 2), S71–S102. https://doi.org/10.1086/261725

- Rousseau, P. L. (1998). The permanent effects of innovation on financial depth. Journal of Monetary Economics, 42(2), 387–425.

- Shao, L., Kwok, C. C., & Guedhami, O. (2010). National culture and dividend policy. Journal of International Business Studies, 41(8), 1391–1414. https://doi.org/10.1057/jibs.2009.74

- Tajaddini, R., & Gholipour, H. F. (2017). National culture and default on mortgages. International Review of Finance, 17(1), 107–133. https://doi.org/10.1111/irfi.12113

- Tufano, P. (2003). Financial innovation. In Handbook of the economics of finance (pp. 307–335). Elsevier.

- Turró, A., Urbano, D., & Peris-Ortiz, M. (2014). Culture and innovation: The moderating effect of cultural values on corporate entrepreneurship. Technological Forecasting and Social Change, 88, 360–369. https://doi.org/10.1016/j.techfore.2013.10.004

- Van Everdingen, Y., & Waarts, E. (2003). The effect of national culture on the adoption of innovations. Marketing Letters, 14(3), 217–232. https://doi.org/10.1023/A:1027452919403