?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Microfinance institutions (MFIs) are a prominent financial inclusion initiative in many developing countries. In Zimbabwe, however, less is known about microfinance borrowers, determinants of loan utilisation and borrowers’ repayment behaviour. Demonstrating that MFIs serve those who are economically marginalised and traditionally excluded from the formal financial system is useful in a country where most of the economic activities are in the informal sector. This study investigated the factors associated with the utilisation of microfinance loans and delinquency among microfinance borrowers using the Poisson, logit and the zero-truncated Poisson regression models on 6165 unique borrowers in Zimbabwe. The study findings revealed that microfinance loans were significantly more likely to be accessed by low-income individuals, who took small loans with relatively high instalments. Women were less likely to access microfinance loans, and reliable borrowers were more likely to access repeat loans. The level of income, number of previous loans and loan terms explained the delinquency among borrowers. Largely, the findings suggest that microfinance in Zimbabwe serves the needs of the low-income group. However, policies that seek to improve access to credit for women and youth remain a priority.

1. Introduction

Access to formal credit remains low in developing countries and more so in Sub-Saharan Africa (SSA) where only 7% of adults have borrowed from a formal financial institution (Demirguc-Kunt et al., Citation2018). Low-income earners and micro, small and medium enterprises (MSMEs) in need of finance to start or expand their businesses largely remain credit constrained (IFC, Citation2020). To alleviate such access to finance challenges, many financial inclusion initiatives were proffered across the world (Girón et al., Citation2021). Many governments, donors and development agencies adopted financial inclusion as a development policy tool (Akeju, Citation2022; Chamboko & Guvuriro, Citation2021; Emara & El Said, Citation2021; Kim, Citation2022; Msulwa et al., Citation2021; Ozili, Citation2020). Through various policy agents, many governments promoted the establishment of microfinance institutions (MFIs) to afford financial access to those who are economically marginalised and excluded from the formal financial system (Abrar et al., Citation2021; Hermes & Lensink, Citation2011; Sane & Thomas, Citation2013). These MFIs are often exempted from regulatory requirements or are subject to relaxed regulatory regimes (Sane & Thomas, Citation2013). By expanding access to finance, policy makers hypothesise that the financial tools (including credit) are poverty escape routes (Abrar et al., Citation2021; Ahmed & Hasan, Citation2009; Dunford, Citation2006; Littlefield et al., Citation2003; Msulwa et al., Citation2021).

Women and youth are informally employed, and those residing in remote and rural areas are mostly economically marginalised and excluded from the formal financial system (Chamboko et al., Citation2018). Commercial banks find it costly to do business with these economic agents given their remoteness, fragmentation and the tininess of loans they typically need. Moreover, commercial banks consider extending credit to these economic agents as too risky due to lack of collateral, proof of residence and identity documents; proof of income and transaction history, as well as other information required to generate credit scores (IFC, Citation2020). It is in this context that MFIs are mostly established and promoted to reach out to these last mile clients with microfinance services.

Notwithstanding the positive view about microfinance (provisioning of microcredit, microsavings, microinsurance and micropayments) and the social objectives that microfinance programmes seek to achieve, there has been longstanding doubts on the beneficiaries of these services and programmes (Hermes & Lensink, Citation2007; Quayes, Citation2021). Hulme and Mosley (Citation1996), Scully (Citation2004), and Simanowitz and Walter (Citation2002) argued that microfinance services hardly reach the poor (or the poor are deliberately excluded) as they are deemed too risky. Exclusion criteria include the requirement to save with an MFI or having an already registered business before borrowing (Kirkpatrick & Maimbo, Citation2002; Mosley, Citation2001). Other critics also argued that the poor lack confidence and consider microfinance loans as too risky and hard to borrow from MFIs (Ciravegna, Citation2005). More recently, Churchill (Citation2018), Churchill (Citation2020) and Quayes (Citation2021) questioned how MFIs balance between outreach depth (reaching to the poor) and sustainability.

In Zimbabwe, MFIs have shown healthy growth in terms of number of institutions, their branches and assets (see, section 2). The Reserve Bank of Zimbabwe (RBZ) revealed that MFIs in the country had access to cheaper loans from the bank’s Microfinance Revolving Loan Facility for onward lending to advance the financial inclusion objectives (Reserve Bank of Zimbabwe, Citation2015–2020). However, there is no research evidence on the functioning of these MFIs, particularly looking at the determinants of loan utilization and repayment behaviour among the microfinance borrowers in this Southern African country. The absence of such studies extends beyond Zimbabwe into other Sub-Saharan African countries. Banna et al. (Citation2022) suggests that the lack of studies on issues relating to microfinance borrowers and delinquency in developing countries is probably due to the lack of reliable data. It is important to ascertain whether the clients that the MFIs are serving are indeed the intended ones and to assess the factors that drive loan delinquency. Understanding these issues illuminates the success of MFIs as agents for financial inclusion in developing countries. Such a success can translate to the previously marginalised segment of society engaging in sustainable economic activities that may engender better welfare outcomes (Achugamonu et al., Citation2020).

In the current study, we therefore seek to empirically determine the factors that predict the utilisation of microfinance loans and delinquency among microfinance borrowers in Zimbabwe. To achieve this, we use reliable data from a private credit bureau in Zimbabwe for loans extended by MFIs between 2013 and 2017. Insights from the study may be particularly unique given that the investigation is carried out in a country that has an ailing economy for a protracted period (Mazhazhate et al., Citation2020) and a large and growing informal sector (Dube & Casale, Citation2019). Lenders in developing countries’ environments may find the investigation of this nature useful from a targeting perspective to ensure that they reach out to the right clients with suitable loan products. In addition, the findings may shed light into the factors that need attention to mitigate credit losses. This paper may also provide useful insights on the role of MFIs on achieving governments’ financial inclusion objectives.

The rest of the paper is structured as follows: Section 2 explores the trends on MFIs in Zimbabwe whilst section 3 provides literature review and hypotheses development. Section 4 describes the data and methods used in the study. Section 5 presents and discusses the results, and Section 6 concludes the paper.

2. MFIs trends in Zimbabwe

During the past decade, Zimbabwe has seen a consistent growth on the number of MFIs operating in the country. , extracted from the Reserve Bank of Zimbabwe (RBZ) Microfinance Industry Reports (2015–2020), shows that since 2009, there has been a steady increase in the number of MFIs. The figure grew from 95 MFIs in 2009 to 229 MFIs in December 2019. A decline in this number is seen in 2020 presumably due to the Corona Virus (Covid-19) pandemic. Similarly, branches of these MFIs grew significantly from only 106 in 2009 to 1,017 in 2019, before declining to 697 in 2020. Also, the client base grew from 58,325 in 2011 to 454,428 in 2019 before sliding down to 303,323 in 2020. Growth in branches and client base could also have been impacted by the Covid-19 pandemic.

Figure 1. MFIs, branch penetration and outreach.

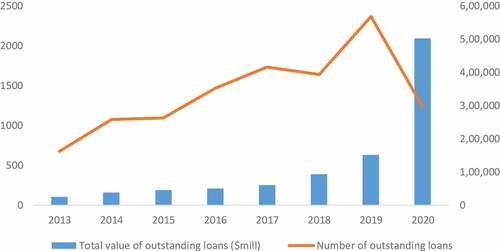

Most of the MFIs in Zimbabwe do not take deposits but provide credit only to their clients. Providing small loans to individuals and microentrepreneurs, usually excluded from commercial banks is the noticeable contribution offered by the MFIs in the country. By December 2020, there were only eight deposit-taking MFIs in the country, while the rest was credit-only MFIs. MFIs’ number and value of outstanding loans are shown in . The number of outstanding loans steadily grew from 2013 to 2019 before substantially declining in 2020. Similarly, the value of outstanding loans steadily grew between 2013 and 2019 and substantially rose in 2020, a situation which could possibly be explained by an increase in the ticket sizes on the advances.

Figure 2. Growth in outstanding loans.

Statistics on the number of MFIs, their branches, clientele size, number and value of outstanding loans suggest that the Zimbabwean microfinance industry is growing. However, the Zimbabwe Association of Microfinance Institutions lamented high default rates and how that threatened the sustainability of the MFIs (The Sunday News, Citation2018). Identifying the predictors of microfinance loan utilization and loan delinquency is thus vital to support the growth of the microfinance industry.

3. Literature review and hypotheses development

Access to credit as a conduit to facilitate upward social mobility is one of the pillars of financial inclusion as a developmental tool. With increased financial inclusion, the economically marginalised can accumulate human or physical capital and/or engage in entrepreneurial activities (Kling et al., Citation2022; Mehrotra & Yetman, Citation2015; Nimbrayan et al., Citation2018; Otioma et al., Citation2019; Van Hove & Dubus, Citation2019). However, financial market imperfections such as transaction costs and information asymmetries hinder commercial banks from serving this stratum of the population. In addition, MFIs whose primordial design was to afford financial access to this stratum of the population (Abdullah & Quayes, Citation2016; Abrar et al., Citation2021; Hermes & Lensink, Citation2011; Sane & Thomas, Citation2013), are drifting to profit-making and commercialisation for sustainability reasons (Chikalipah, Citation2018a). In this section, we review the literature on the factors that influence access to and use of credit from MFIs as well as the repayment behaviour to explore the extent to which the marginalised benefit from financial inclusion initiatives.

The first important factor that explains MFIs clients’ access and use of credit is gender. Aggarwal et al. (Citation2015) reported that while the gender dimension to access and use of credit from MFIs varies internationally, MFIs generally have more women borrowers than men. Reed et al. (Citation2015) reported in the 2015 Microcredit Report that 82% of the poorest clients served by the MFIs were women. Using the MIX database over the period 2001 to 2014, Hessou et al. (Citation2021) showed that more than 60% of active MFI borrowers were women irrespective of whether the MFI has a deposit-taking status or not and whether it is profit oriented or not. Hemtanon and Gan (Citation2020) reported that the Village Funds category of MFIs in Thailand targets low-income rural households mostly with female heads. Abdullah and Quayes (Citation2016), however, showed that although most microcredit borrowers were female, recent trends show an increase in male representation, using a panel of 891 MFIs over a period of 10 years. There are two arguments why MFIs have more women borrowers than men. The first argument is that women are a component of the poorest strata of the population and thus fit in the MFIs’ initial goal (Aggarwal et al., Citation2015). The second argument is that women have greater social impact, are more trustworthy and lead to better loan portfolio quality and financial performance (Aggarwal et al., Citation2015).

The age of the client is the second loan utilisation factor identified in empirical studies. Hemtanon and Gan (Citation2020) reported that the Village Funds category of MFIs mostly serve the old household heads, while the “Savings Group Production” category of MFIs serves the young household heads. Sangwan and Nayak (Citation2020) found that MFIs in India experience a higher loan demand from younger people compared to older people. Kodongo and Kendi (Citation2013) shows that MFIs tend to avoid younger clients (below 30 years) arguing that most MFI loans are targeted for business purposes, yet youthful applicants are unlikely to have adequate business experience.

The third factor relates to the clients’ level of income. As MFIs shift from operating as “not-for-profit” to profit-oriented organisations, the target is shifting from the poorest of the poor to salaried workers and micro-businesses in need of relatively large loan amounts (Chikalipah, Citation2018b). This is in harmony with commercialisation move reported earlier. The data we have for our study enable us to assess the influence of gender, age and income levels on MFIs loan utilisation in Zimbabwe. We also explore the significance of loan variables (loan amount, instalment size, loan term) as the data permit.

Turning to loan repayment, Fadikpe et al.’s (Citation2022) study in the Sub-Saharan Africa (SSA) shows that having more female borrowers is associated with better repayment rates. Similarly, Chikalipah (Citation2018a) shows that women borrowers in the Microfinance industry in SSA are less risky. Earlier studies (e.g., Agier & Szafarz, Citation2013; Baklouti, Citation2013; D’espallier et al., Citation2013, Citation2011; Hulme et al., Citation1996; Schicks, Citation2014; Strøm et al., Citation2014; Todd, Citation1996) suggested that women in particular, and low-income earners in general, default less after borrowing from the MFIs, compared to men and high-income earners, respectively. These studies pointed out that better repayment behaviour by women could be due to them investing in types of business that allow easier repayment (D’espallier et al., Citation2011) or just being conservative (Todd, Citation1996). The conservative explanation links to Croson and Gneezy’s (Citation2009) finding of women being risk averse. Earlier, Sharma and Zeller (Citation1997) reported women’s risk averseness reflected by the less risky business activities they embark on. Another explanation that is suggested in the literature is that women have fewer credit opportunities than men and must therefore religiously repay their loans to ensure continued access to credit (Armendariz & Morduch, Citation2010). Contrary to the above, Sangwan et al. (Citation2020) in agreement with Dorfleitner et al. (Citation2017) show that higher-income households are less likely to be delinquent. The authors attributed this to the idea that higher-income individuals or households are likely to start and operate high return entrepreneurial activities with better cash flow and hence increase their chances to repay.

With respect to the client’s age, earlier studies (e.g., Bhatt & Tang, Citation2002; Dunn & Kim, Citation1999; Kodongo & Kendi, Citation2013; Mokhtar et al., Citation2012) reported that age correlates negatively with the probability of loan default, suggesting that older borrowers are more responsible and disciplined compared to younger borrowers. However, Baklouti (Citation2013) found a nonmonotone relationship and argued that younger borrowers default less as they have more independence compared to the middle-aged borrowers, while the older borrowers default less as they have, and over time become more risk averse, more knowledgeable and more responsible.

Related to other variables in our data, empirical research has also reported on the relationship between credit risk and loan variables such as loan amount and duration as well as number of previous loans. Some studies show that the loan amount associates positively with repayment (e.g., Baklouti, Citation2013; Kodongo & Kendi, Citation2013; Mokhtar et al., Citation2012). However, other studies report the contrary (e.g., Baesens et al., Citation2011; Chikalipah, Citation2018a; Van Gool et al., Citation2012). Dinh and Kleimeier (Citation2007) and Kočenda and Vojtek (Citation2011) reported on the number of previous accorded loans associating with lower default probability, a result that could be due to lender–borrower relationship. However, Baklouti (Citation2013) found that repeat borrowers default more than those who infrequently borrow. Kodongo and Kendi (Citation2013) reported that repayment period or loan duration does significantly influence delinquency regardless of lending methodology (group or individual) or loan size.

Given the growing number of MFIs in Zimbabwe, a country with an ailing economy and expanding informal sector, two hypotheses are proffered for this study:

Hypothesis 1: MFI loan utilisation is concentrated among those who are in the poorest strata of the population (women, youth, and low-income earners)

Hypothesis 2: Those in the poorest strata of the population (women, youth, and low-income earners) have a high propensity to repay their loans compared to other groups.

4. Methodology

4.1. Data

The study uses data from a private credit bureau in Zimbabwe. The focus is on personal loans extended by MFIs between 2013 and 2017. The sample consists of 6,165 microfinance borrowers for the selected period. The variables of interest include the borrowers’ demographics (age, gender and income); loan variables (loan term, loan amount and instalments size); a behavioural variable (number of missed payments), and number of previous loan contracts. The outcome variable for the component that predicts the factors explaining loan utilization is the number of MFI loans an individual has accessed from different MFIs over a five-year period. It is, however, important to note that having taken many loans does not equate to better financial outcomes compared to taking fewer loans. Thus, the scope of the study ends on predicting those who are likely to have repeat loans and profile their characteristics and does not delve into the welfare outcomes of those individuals. On the drivers of loan delinquency, the outcome of interest is the number of missed payments.

4.2. Descriptive analysis

provides a summary of the descriptive statistics for the sample. Fifty-nine (59) percent of the borrowers were males. While one in 10 borrowers is of age above 55 years, about a quarter of the sample are below 35 years of age. Slightly above a third (35%) and slightly below a third (30%) are within the age ranges of 35 to 44 and 45 to 54 years, respectively. For the four income categories presented, each claims a reasonable share, ranging from 20% (for < US$250) to 28% (US$350-US$500). On average, borrowers took four loans with a minimum of one and a maximum of nine. The average loan term is 10 months and average instalment size of US$115. Loan delinquency ranges from 0 to 9, however, with a low average of 0.28 missed payments.

Table 1. Descriptive statistics

4.3. Empirical strategy

On determining the factors associated with microfinance loan utilisation, the outcome of interest is the number of loans accessed by individual borrowers over a 5 year-study period. Thus, the dependent variable (number of loans), is discrete and non-negative and can be regarded as count data and assumed to follow a Poisson distribution such that the expectation of

is assumed to be

. The count data model formulation is as follows:

where is the vector of explanatory variables, β is a vector of coefficients associated with

and

is the error term. Given that

is count data, the probability of

conditional to

is expressed as follows:

To ascertain the drivers of loan delinquency and the depth therefore, the analysis was implemented in two steps. The first step treated the outcome as binary, where borrowers were categorised into zero (no missed payments), and 1 for those who missed one or more payments during the five-year period. To model this outcome, the logit model was implemented, and this is mathematically expressed as:

Where is a set of covariates and

represents the vector of regression coefficients.

For the second step which models the depth of delinquency among those who missed payments, the outcome of interest was the number of missed payments during the five-year period. In this case, the outcome was also counted (excluding zero); hence, a zero-truncated Poisson regression model was implemented (an extension of the Poisson regression model).

5. Results and discussion

The results presented in show that women were significantly less likely to take microfinance loans when compared to males [marginal effects (ME) = −0.2; p < 0.10]. The age of the borrower was not an important factor with regard to loan utilisation. Compared to those whose incomes were above US$500, borrowers with lower incomes were significantly more likely to take repeat loans [with ME for those whose incomes were below US$250 as 1.01 (p < 0.01), incomes between US$250 and US$349 as 0.90 (p < 0.01), and those with incomes between US$350 to US$499 as 0.83 (p < 0.01)].

Table 2. Factors associated with microfinance loans utilisation

The results also show that those who took smaller loans were significantly more likely to take repeat loans compared to those who took loans of higher values. Compared to those who took a loan amount of more than US$1500, the ME of repeat borrowing for a loan amount of less than US$500 was 0.75 (p < 0.01), a loan amount between US$500 and US$749 has a ME of 0.49 (p < 0.01), and a loan amount between US$1000 and US$1499 has a ME of 0.46 (p < 0.01). Borrowers who had loans on longer terms were more likely to repeat borrowing [ME = 0.04; p < 0.05] and so were those with higher instalment sizes [ME = 0.0009; p < 0.01]. Those borrowers with higher incidence of missing payment were significantly less likely to have repeat loans [ME = −0.23; p < 0.01].

The results reported on gender and age of the borrower are in line with studies in other countries. A study by Chamboko et al. (Citation2021) in Democratic Republic of Congo and by Milana and Ashta (Citation2020) that compares some developing and developed countries, reported that women and youth continue to have limited access to credit. The results do not support the development thesis postured in support of microfinance programmes. Thus, the hypothesis that MFIs target women and youth as segments that are excluded from traditional financial systems dominated by commercial banks does not hold for the Zimbabwean data.

The fact that the income level correlates negatively with the number of accessed loans suggest that the MFIs in Zimbabwe serve the lower-income groups. This finding supports the original idea of microfinance of reaching out to the poor who hardly access credit from commercial banks. This result on low-income individuals more likely to borrow from MFIs refutes some critics of microfinance who argued that microfinance does not reach the poor (Scully, Citation2004; Simanowitz & Walter, Citation2002). The result on the size of loans negatively correlating with the frequency of borrowing could mean that those who take smaller loans can repay them quickly and be able to take other loans. It is logical that lenders approve larger loans with longer terms and possibly higher instalments to good borrowers and as such they have good chances of getting repeat loans. Of course, missing payments may lead to blacklisting and hence fewer repeat loans.

shows results from a logit model and a zero-truncated Poisson regression model. The results from the logit model show that gender was not a significant predictor of loan delinquency among microfinance borrowers. This result contradicts Chamboko and Bravo (Citation2019) who found women to be less likely to default on their loans in the same market. Besides, there is growing evidence suggesting that women MFI borrowers are less risky (see, Chikalipah, Citation2018a; Fadikpe et al., Citation2022). The results showing that women are less likely to access MFI loans, yet they are not different from men on repayment, demonstrate that reaching out to more women borrowers is not just a social good but makes business sense for MFIs.

Table 3. Drivers of loan delinquency and depth among microfinance borrowers

Similarly, the age of the borrower was not a significant predictor of loan delinquency. Given that young people are less likely to access MFI loans, and yet they are not riskier borrowers compared to the other age groups suggest that there is an opportunity for MFIs to increase their outreach to young people as this does not negatively affect their business. Instead, such outreach promotes their social good. The results also show that the size of the instalment was not a significant predictor of loan delinquency.

However, loan delinquency significantly varied with income size such that compared to those borrowers who reported to have an income of more than US$500, those whose income was below US$250 [OR = 0.43; p < 0.01]; income between US$250 and US$349 [OR = 0.59; p < 0.01] and income between US$350 and US$500 [OR = 0.14; p < 0.01], were less likely to be delinquent. This result of higher-income individuals (and therefore less poor) being more delinquent is contradictory to expectations but supported by numerous studies (D’espallier et al., Citation2011, Citation2013; Schicks, Citation2014; Strøm et al., Citation2014). In a recent study, Chamboko and Bravo (Citation2019) made the same observation of low-income individuals more likely to repay their loans (less default) compared to those with relatively higher incomes. The study attributed the finding to payslip-based lending where lenders rely on how much a borrower earns without a complete assessment of one’s debt load. In the absence of good credit history information and sharing systems (a common situation in developing countries), higher-income borrowers can easily get multiple and relatively larger loans thereby risking their ability to repay. Another possible explanation is that poor individuals consider MFIs as their main formal financial services provider and thus seek to maintain good relations by repaying their loans.

The logit model results also show that higher number of previous loans was significantly associated with less chances of having fallen into delinquency (OR = 0.72; P < 0.01). This could be attributed to relationship lending whereby some MFIs may emphasize on granting repeat loans to regular clients even when they face temporary repayment problems. That way, these borrowers can recover and improve their repayment. Inherent in the loan approval process, the results reveal that longer loan terms were significantly associated with not missing payments (OR = 0.89; p = 0.01), a finding suggesting that lenders were incentivised to grant longer terms to reliable borrowers with a good repayment behaviour.

As a robustness check, we now turn to results from the zero-truncated Poisson regression model. Compared to the borrowers earning above US$500, those earning below US$250 were associated with fewer counts of missed payments. The marginal effects estimate shows that those earning less than US$250 missed three payments less compared to those earning above US$500 (p < 0.01). Also, borrowers earning between US$350 and US$500 missed 2 payments less than those earning above US$500 (p = 0.016). The results also show that a higher number of previous loans was significantly associated with less chances of having fallen deep into delinquency (ME = −0.25; p < 0.01). These zero-truncated Poisson regression model results confirm the income and number of previous payment loans results reported in the logit model.

6. Conclusion

MFIs are mostly established and promoted to serve those economically marginalised and excluded from the formal financial system and are now an important part of the financial system in many developing countries. However, there has been limited attention on the functioning of MFIs, particularly looking at the determinants of loan utilization among microfinance borrowers and their repayment behaviour. Understanding whether the clients that MFIs serve are indeed the intended ones and assessing the factors that drive loan delinquency illuminate the success of these MFIs as agents for financial inclusion in developing countries. In this paper, we investigate the factors associated with the utilisation of microfinance loans and delinquency among MFI borrowers in Zimbabwe using data from 6165 unique obligors. The study revealed that microfinance loans were more likely to be accessed by low-income individuals, those who took small loans, on longer terms and relatively higher instalments. However, women were less likely to access microfinance loans, and no evidence was found on youth accessing microfinance loans than other age groups. Reliable borrowers were more likely to access repeat loans. On repayment, the level of income, number of previous loans and loan terms explained the delinquency among borrowers. The findings suggest that microfinance in Zimbabwe to a large extent serves the needs of those in the low-income group. However, policy initiatives or product innovation that increase women’s and youth’s access to credit remain a priority.

To expand on these findings, further research may consider using tailor-made surveys to collect primary data with an expansive set of variables that may affect the utilisation of microfinance loans and repayment behaviour. These may include locality (rural/urban), marital status, employment status and sources of income among others.

Disclaimer

The paper carries the details of the authors. Thus, the findings of the study and the conclusions thereof are entirely those of the authors. As such, they do not represent the views of the affiliated organizations.

Acknowledgements

The authors would like to thank the anonymous reviewers for the valuable comments which greatly improved this paper.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Abdullah, S., & Quayes, S. (2016). Do women borrowers augment financial performance of MFIs? Applied Economics, 48(57), 5593–13. https://doi.org/10.1080/00036846.2016.1181831

- Abrar, A., Hasan, I., & Kabir, R. (2021). Finance-growth nexus and banking efficiency: The impact of microfinance institutions. Journal of Economics and Business, 114(March–April), 105975. https://doi.org/10.1016/j.jeconbus.2020.105975

- Achugamonu, B. U., Adegbite, E. O., Omankhanlen, A. E., Okoye, L. U., & Isibor, J. A. (2020). Dynamics of digital finance and financial inclusion nexus in Sub-Saharan Africa. Proceedings of the 33rd International Business Information Management Association Conference (IBIMA) 10-11 April 2019 Granada, Spain. Retrieved April 5, 2022, from http://eprints.covenantuniversity.edu.ng/13791/1/Dynamics%20of%20Digital.pdf

- Aggarwal, R., Goodell, J. W., & Selleck, L. J. (2015). Lending to women in microfinance: Role of social trust. International Business Review, 24(1), 55–65. https://doi.org/10.1016/j.ibusrev.2014.05.008

- Agier, I., & Szafarz, A. (2013). Microfinance and gender: Is there a glass ceiling on loan size? World Development, 42(February), 165–181. https://doi.org/10.1016/j.worlddev.2012.06.016

- Ahmed, S., & Hasan, T. (2009). Microfinance institutions in Bangladesh: Achievements and challenges. Managerial Finance, 35(12), 999–1010. https://doi.org/10.1108/03074350911000052

- Akeju, K. F. (2022). Household financial behaviour: The role of financial inclusion instruments in Nigeria. Journal of Sustainable Finance & Investment, 1–13. https://doi.org/10.1080/20430795.2022.2034595

- Armendariz, B., & Morduch, J. (2010). The economics of microfinance (2nd ed.). MIT Press.

- Baesens, B., Verbeke, W., Sercu, P., & Gool, J. V. (2011). Credit scoring for microfinance: Is it worth it? International Journal of Finance and Economics, 17(2), 103–123. https://doi.org/10.1002/ijfe.444

- Baklouti, I. (2013). Determinants of microcredit repayment: The case of tunisian microfinance bank. African Development Review, 25(3), 370–382. https://doi.org/10.1111/j.1467-8268.2013.12035.x

- Banna, H., Mia, M. A., Nourani, M., & Yarovaya, L. (2022). Fintech-based financial inclusion and risk-taking of microfinance institutions (MFIs): Evidence from Sub-Saharan Africa. Finance Research Letters, 45(March), 102149. https://doi.org/10.1016/j.frl.2021.102149

- Bhatt, N., & Tang, S. Y. (2002). Determinants of repayment in microcredit: Evidence from programs in the United States. International Journal of Urban and Regional Research, 26(2), 360–376. https://doi.org/10.1111/1468-2427.00384

- Chamboko, R., & Bravo, J. M. (2019). Frailty correlated default on retail consumer loans in Zimbabwe. International Journal of Applied Decision Sciences, 12(3), 257–270. https://doi.org/10.1504/IJADS.2019.100436

- Chamboko, R., Cull, R., Giné, X., Heitmann, S., Reitzug, F., & Van der Westhuizen, M. (2021). The role of gender in agent banking: Evidence from the Democratic Republic of Congo. World Development, 146(October), 105551. https://doi.org/10.1016/j.worlddev.2021.105551

- Chamboko, R., & Guvuriro, S. (2021). The role of betting on digital credit repayment, coping mechanisms and welfare outcomes: Evidence from Kenya. International Journal of Financial Studies, 9(1), 1–12. https://doi.org/10.3390/ijfs9010010

- Chamboko, R., Heitmann, S., & Morne Van der Westhuizen, R. (2018). Women and digital financial services in Sub-Saharan Africa: Understanding the challenges and harnessing the opportunities. World Bank.

- Chikalipah, S. (2018a). Credit risk in microfinance industry: Evidence from sub-Saharan Africa. Review of Development Finance, 8(1), 38–48. https://doi.org/10.1016/j.rdf.2018.05.004

- Chikalipah, S. (2018b). Do microsavings stimulate financial performance of microfinance institutions in Sub-Saharan Africa? Journal of Economic Studies, 45(5), 1072–1087. https://doi.org/10.1108/JES-05-2017-0131

- Churchill, S. A. (2018). Sustainability and depth of outreach: Evidence from microfinance institutions in sub-Saharan Africa. Development Policy Review, 36(S2), 676–695. https://doi.org/10.1111/dpr.12362

- Churchill, S. A. (2020). Microfinance financial sustainability and outreach: Is there a trade-off? Empirical Economics Volume, 59(3), 1329–1350. https://doi.org/10.1007/s00181-019-01709-1

- Ciravegna, D. (2005). The role of microcredit in modern economy: The case of Italy. Flacso Working Paper, Costa Rica. www.flacso.or.cr/fileadmin/documentos/FLACSO/auCiravegna2.DOC

- Croson, R., & Gneezy, U. (2009). Gender differences in preferences. Journal of Economic Literature, 47(2), 448–474. https://doi.org/10.1257/jel.47.2.448

- D’espallier, B., Guerin, I., & Mersland, R. (2013). Focus on women in microfinance institutions. The Journal of Development Studies, 49(5), 589–608. https://doi.org/10.1080/00220388.2012.720364

- D’espallier, B., Guérin, I., & Mersland, R. (2011). Women and repayment in microfinance: A global analysis. World Development, 39(5), 758–772. https://doi.org/10.1016/j.worlddev.2010.10.008

- Demirguc-Kunt, A., Klapper, L., Singer, D., Ansar, S., & Hess, J. (Eds.). (2018). The global findex database 2017: Measuring financial inclusion and the Fintech revolution. World Bank.

- Dinh, T. H. T., & Kleimeier, S. (2007). A credit scoring model for Vietnam’s retail banking market. International Review of Financial Analysis, 16(5), 471–495. https://doi.org/10.1016/j.irfa.2007.06.001

- Dorfleitner, G., Just-Marx, S., & Priberny, C. (2017). What drives the repayment of agricultural microloans? Evidence from Nicaragua. The Quarterly Review of Economics and Finance, 63(February), 89–100. https://doi.org/10.1016/j.qref.2016.02.009

- Dube, G., & Casale, D. (2019). Informal sector taxes and equity: Evidence from presumptive taxation in Zimbabwe. Development Policy Review, 37(1), 47–66. https://doi.org/10.1111/dpr.12316

- Dunford, C. (2006). Evidence of microfinance’s contribution to achieving the Millennium Development Goals (MDG). Paper presented in Global Microcredit Summit Halifax, Nova Scotia, Canada, 12–15 November 2006. Retrived on 6 April 2022 from https://community-wealth.org/sites/clone.community-wealth.org/files/downloads/paper-dumford.pdf

- Dunn, L. F., & Kim, T. (1999). An empirical investigation of credit card default. Ohio State University, Department of Economics Working Papers, (13–99).

- Emara, N., & El Said, A. (2021). Financial inclusion and economic growth: The role of governance in selected MENA countries. International Review of Economics & Finance, 75(September), 34–54. https://doi.org/10.1016/j.iref.2021.03.014

- Fadikpe, A. A. A., Danquah, R., Aidoo, M., Chomen, D. A., Yankey, R., Dongmei, X., & Trinidad Segovia, J. E. (2022). Linkages between social and financial performance: Evidence from Sub-Saharan Africa microfinance institutions. PLoS one, 17(3), 0261326. https://doi.org/10.1371/journal.pone.0261326

- Girón, A., Kazemikhasragh, A., Cicchiello, A. F., & Panetti, E. (2021). Financial inclusion measurement in the least developed countries in Asia and Africa. Journal of the Knowledge Economy, 13(2), 1198–1211. https://doi.org/10.1007/s13132-021-00773-2

- Hemtanon, W., & Gan, C. (2020). Microfinance participation in Thailand. Journal of Risk and Financial Management, 13(6), 122. https://doi.org/10.3390/jrfm13060122

- Hermes, N., & Lensink, R. (2007). Impact of microfinance: A critical survey. Economic and Political Weekly, 42(6), 462–465. https://www.jstor.org/stable/4419226

- Hermes, N., & Lensink, R. (2011). Microfinance: Its impact, outreach, and sustainability. World Development, 39(6), 875–881. https://doi.org/10.1016/j.worlddev.2009.10.021

- Hessou, H. T. S., Lensink, R., Soumaré, I., & Tchakoute Tchuigoua, H. (2021). Provisioning over the business cycle: Some insights from the microfinance industry. International Review of Financial Analysis, 77, [101825]. https://doi.org/10.1016/j.irfa.2021.101825

- Hulme, D., & Mosley, P. (1996). Finance against poverty (Vol. 2). Psychology Press.

- IFC. (2020). Banking on SMEs: Trends and challenges. perspectives from SME banking leaders. World Bank Group.

- Kim, K. (2022). Assessing the impact of mobile money on improving the financial inclusion of Nairobi women. Journal of Gender Studies, 31(3), 306–322. https://doi.org/10.1080/09589236.2021.1884536

- Kirkpatrick, C., & Maimbo, S. (2002). The Implications of the evolving microfinance agenda for regulatory and supervisory policy. Development Policy Review, 20(3), 293–304. https://doi.org/10.1111/1467-7679.00172

- Kling, G., Pesqué-Cela, V., Tian, L., & Luo, D. (2022). A theory of financial inclusion and income inequality. The European Journal of Finance, 28(1), 137–157. https://doi.org/10.1080/1351847X.2020.1792960

- Kočenda, E., & Vojtek, M. (2011). Default predictors in retail credit scoring: Evidence from Czech banking data. Emerging Markets Finance and Trade, 47(6), 80–98. https://doi.org/10.2753/REE1540-496X470605

- Kodongo, O., & Kendi, L. G. (2013). Individual lending versus group lending: An evaluation with Kenya’s microfinance data. Review of Development Finance, 3(2), 99–108. https://doi.org/10.1016/j.rdf.2013.05.001

- Littlefield, E., Morduch, J., & Hashemi, S. (2003). CGAP focus note 24: Is microfinance an effective strategy to reach the millennium development goals? Consultative Group to Assist the Poor.

- Mazhazhate, C., Mujakachi, T. C., & Munuhwa, S. (2020). Towards pragmatic economic policies: Economic transformation and industrialization for revival of Zimbabwe in the new dispensation era. International Journal of Engineering and Management Research, 10(5), 75–81. https://doi.org/10.31033/ijemr.10.5.14

- Mehrotra, A. N., & Yetman, J. (2015). Financial inclusion-issues for central banks. BIS Quarterly Review, (March), 83–96. https://www.bis.org/publ/qtrpdf/r_qt1503h.htm

- Milana, C., & Ashta, A. (2020). Microfinance and financial inclusion: Challenges and opportunities. Strategic Change, 29(3), 257–266. https://doi.org/10.1002/jsc.2339

- Mokhtar, S. H., Nartea, G., & Gan, C. (2012). Determinants of microcredit loans repayment problem among microfinance borrowers in Malaysia. International Journal of Business and Social Research, 2(7), 33–45. https://thejournalofbusiness.org/index.php/site/article/view/118

- Mosley, P. (2001). Microfinance & Poverty in Bolivia. The Journal of Development Studies, 37(4), 101–132. https://doi.org/10.1080/00220380412331322061

- Msulwa, B., Chamboko, R., Weideman, J., Lee, C., & Nordin, K. (2021). The impact of formal financial services uptake on asset holdings in Kenya: Causal evidence from a propensity score matching approach. African Review of Economics and Finance, 13(1), 298–320. https://journals.co.za/doi/epdf/10.10520/ejc-aref-v13-n1-a12

- Nimbrayan, P. K., Tanwar, N., & Tripathi, R. K. (2018). Pradhan mantri Jan dhan yojana (PMJDY): The biggest financial inclusion initiative in the world. Economic Affairs, 63(2), 583–590. https://doi.org/10.30954/0424-2513.2.2018.38

- Otioma, C., Madureira, A. M., & Martinez, J. (2019). Spatial analysis of urban digital divide in Kigali, Rwanda. GeoJournal, 84(3), 719–741. https://doi.org/10.1007/s10708-018-9882-3

- Ozili, P. K. (2020). Theories of financial inclusion. In Özen, E. and Grima, S. (Ed.), Uncertainty and challenges in contemporary economic behaviour (Emerald Studies in Finance, Insurance, and Risk Management) (pp. 89–115). Bingley: Emerald Publishing Limited. https://doi.org/10.1108/978-1-80043-095-220201008

- Quayes, S. (2021). An analysis of the mission drift in microfinance. Applied Economics Letters, 28(15), 1310–1316. https://doi.org/10.1080/13504851.2020.1813240

- Reed, L. R., Rao, D. S. K., Rogers, S., Rivera, C., Diaz, F., Gailly, S., Maesden, J., & Sanchez, X. (2015). Mapping pathways out of poverty. The State of the Microcredit Summit Campaign Report, 2015, 1–62. https://www.results.org/wp-content/uploads/SOCR2015_English_Web.pdf

- Reserve Bank of Zimbabwe. (2015-2020). Microfinance industry reports. RBZ.

- Sane, R., & Thomas, S. (2013). Regulating microfinance institutions. Economic and Political Weekly, 48(5), 59–67. https://www.jstor.org/stable/23391209

- Sangwan, S., Chandra, N. D., & Samanta, D. (2020). Loan repayment behavior among the clients of Indian microfinance institutions: A household level investigation. Journal of Human Behavior in the Social Environment, 30(4), 474–497. https://doi.org/10.1080/10911359.2019.1699221

- Sangwan, S., & Nayak, N. C. (2020). Factors influencing the borrower loan size in microfinance group lending: A survey from Indian microfinance institutions. Journal of Financial Economic Policy, 13(2), 223–238. https://doi.org/10.1108/JFEP-01-2020-0002

- Schicks, J. (2014). Over-indebtedness in microfinance–an empirical analysis of related factors on the borrower level. World Development, 54(February), 301–324. https://doi.org/10.1016/j.worlddev.2013.08.009

- Scully, N. (2004). Microcredit: No panacea for poor women. Global Development Research Centre.

- Sharma, M., & Zeller, M. (1997). Repayment performance in group-based credit programs in Bangladesh: An empirical analysis. World Development, 25(10), 1731–1742. https://doi.org/10.1016/S0305-750X(97)00063-6

- Simanowitz, A., & Walter, A. (2002). Ensuring impact: Reaching the poorest while building financially self-sufficient institutions, and showing improvement in the lives of the poorest families: Summary of article appearing in pathways O,” occasional papers 23745. University of Sussex, Imp-Act: Improving the Impact of Microfinance on Poverty: Action Research Program

- Strøm, R. Ø., D’Espallier, B., & Mersland, R. (2014). Female leadership, performance, and governance in microfinance institutions. Journal of Banking & Finance, 42(May), 60–75. https://doi.org/10.1016/j.jbankfin.2014.01.014

- The Sunday News. (2018, September 17). Money lenders hit by defaults. News. Retrieved April 6, 2022, from https://www.sundaynews.co.zw/money-lenders-hit-by-defaults/

- Todd, H. (1996). Women at the center: Grameen bank borrowers after one decade. Dhaka University Press.

- Van Gool, J., Verbeke, W., Sercu, P., & Baesens, B. (2012). Credit scoring for microfinance: Is it worth it? International Journal of Finance & Economics, 17(2), 103–123. https://doi.org/10.1002/ijfe.444

- Van Hove, L., & Dubus, A. (2019). M-PESA and financial inclusion in Kenya: Of paying comes saving? Sustainability, 11(3), 568. https://doi.org/10.3390/su11030568