?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The political climate of any country has become one of the pillars of decision-making for investment and any other financial business. Zimbabwe is one of the countries that have experienced political instability for the longest time. Many studies have looked at the impact of political risk on the stock market and other macroeconomics variables without considering the impact of political risk on the demand for foreign exchange in a country. Using secondary data from the World Bank - World Development Indicator (WDI), International Country Risk Guide (ICRG), and Reserve Bank of Zimbabwe (RBZ), this study examined the effects of political risk on the foreign currency demand in Zimbabwe. The regression results showed a negative and significant association between political risk and foreign exchange reserve both in the short run and long-run period, implying an increase in foreign currency demand as political risk increases. The study also applied an alternate indicator for foreign exchange demand to test whether the main findings are robust to different dependent variable measures. The results from the robustness test are consistent with the main findings of the study. The study makes recommendations for policymaking by the Zimbabwean government and other regulators.

1. Introduction

The political climate of any country has become one of the sources of attraction for investment and any other financial business, which in any case may be through financial markets and institutions. With the world moving towards the fourth industrial revolution an increasing trend of globalization for financial markets, the concept of “political risk” continues to achieve an augmented prominence. Both the management of different firms and various kinds of investors have acknowledged the significance of comprehending political risk (Mawanza, Citation2015), while others remained threatened by its nature as it impends investment terms and conditions.

However, political risk integrated with international business has been loosely defined more so that it is relatively new in the research field. Nonetheless, different authors have taken up the challenge to investigate this area, subsequently coming up with different concepts to explain, analyze, and evaluate the relationship between political risk and finance. Some authors imply political risk as government interference, while others depict political risk in terms of events (Kobrin, Citation1979). The narrative of government interference infers government decisions in regard to the business/private sector, confiscations, expropriation, trade restrictions, or taxations, etc. (Geert Bekaert, 2015).

Zimbabwe is one of the countries that has experienced political instability for the longest time. The regime of the late Robert Mugabe has, in countless instances, interfered with the financial business of the country. The frequent interference of the government in the business and financial affairs of the country affects many macroeconomic variables of the country.

For the past decade, Zimbabwe has faced extreme political and foreign exchange dynamics leading to bruising and significantly affecting its economy. A wobbly economic and political environment has led to wobbly investment prospects. Nonetheless, while the performance of different business financial markets, inclusive of the stock and foreign exchange market, has been deteriorated by an environment posing political hazards, various firms and business companies motionlessly endeavor, on the other hand, to preserve companies in Zimbabwe (Mawanza, Citation2015).

In February 2009, a multicurrency system was established by the Zimbabwean authorities, and the Zimbabwe dollar was recognized as nonexistent. The regulations under the multicurrency system were that authorization of hard foreign currencies was mandatory, and there was the imposition of mandatory taxes on foreign currency exchange. These regulations on the foreign exchange (forex) market became largely liberalized. The “all surrender” requirement on forex earnings as well as proceeds was abolished in March 2009, and the Zimbabwe dollars were demonetized in 2015 since there was no functioning forex market. Zimbabwe dollar-denominated bank accounts (equivalent to about $US6 million at the exchange rate of $Z35 quadrillion per $US1) therefore became dormant. The multicurrency system was extended beyond 2012 till an infinite period, although the Zimbabwe dollar was scheduled to be used after that period. There are five foreign currencies that have been granted official status in Zimbabwe since 2009; however, the US dollar became the principal currency.

Since 2009, fiscal revenue estimates and fiscal expenditure allocations have been denominated in US dollars. The multicurrency era provided substantial benefits, including fiscal discipline by restraining government inflationary funding of the fiscus, financial reintermediation, and the re-monetization of the Zimbabwean economy, higher transparency in the accounting, and pricing of goods and services after the period of hyperinflation. Accordingly, the price levels in US dollars started falling during 2009, while the economy started to recover and rebound (IMF-Zimbabwe Citation2009). The hyperinflation of 2008 saw the abandonment of the Zimbabwe dollar in transactions and de facto widespread dollarization or multicurrency regime adoption. This increased the activities on the black market, which amplified the woes of the economy. These occurrences suggest an increase in demand for foreign currency as political risk intensifies. However, from the above narrative, whether political risk impacts foreign currency demand positively or negatively remains an empirical question. In that regard, this research aims to empirically examine the effects of political risk on foreign currency demand in the case of the Zimbabwean economy.

This study makes a significant contribution to the literature on political risk and foreign currency demand. Specifically, many studies have looked at the impact of political risk on macroeconomic factors, such as GDP, FDI, and others, which other authors have also considered a political risk and the volatility on the stock market. However, this is the first study, to the best of my knowledge, to examine the influence of political risk on foreign currency demand in a country, where in this case, Zimbabwe’s economy. Thus, the study uncovers the extent to which political risk affects foreign currency reserves in the economy using a multidimensional political risk index. Also, the study analyzed both the short-run and long-run impact of political risk on forex demand using a new estimation methodology since the mainstream of empirical studies, particularly on political risk, merely followed a direct linear framework without considering the endogenous nature of this type of model. Thus, the study provides us with a detailed analysis as to the extent to which political risk impacts the foreign currency demand in a country. Furthermore, the study makes recommendations for policymaking by the Zimbabwe government and regulators of the financial market. The implication here is that this study does not make a contribution to academic research only but also aims to help the government, regulatory bodies, and other stakeholders to ensure a stable political economy for development.

The rest of the paper is structured as follows: Section two offers a stylized fact on the background of Zimbabwe. Section three gives the literature review and hypothesis development, and section four discusses the data and the research design. Section five states and discusses the empirical results. Section six draws a conclusion from the findings.

2. Background literature on Zimbabwe’s economy

Zimbabwe is a landlocked Southern African country with a fascinating currency market holding a thought-provoking background, fluctuations, and many more, which shall be explored. Initially, there used to be a currency union between Zimbabwe, Malawi, and Zambia (then Southern Rhodesia, Nyasaland, and Northern Rhodesia, respectively) during the colonial rule. This union came to an end after the Federation of Rhodesia broke away from Nyasaland due to the growth in African nationalism and dissent. Furthermore, in November 1964, the Rhodesian Pound replaced the Central African Pound following the bill that was passed by the Parliament of Southern Rhodesia on the “Reserve Bank of Rhodesia Act” (Noko, Citation2011). It did not take years for Zimbabwe’s currency to transition to yet another currency. This occurred in 1965, when the Rhodesian Dollar replaced the Rhodesian Pound through a unilateral declaration of the Prime Minister, who then was Ian Smith. However, in 1980, Zimbabwe magnified its national pride by implementing the Zimbabwe Dollar as its official currency emerging from the British colonial rule as per the de jure independence (Sikwila, Citation2013).

Post-independence, tied to a flexible basket of currencies, the Zimbabwe Dollar had a crawling band of ±2 percent of the dollar. Its value against the USD dollar at that time was US$1.47 (Noko, Citation2011). Nevertheless, in comparison to the United States, the rate of inflation in Zimbabwe was high, consequently depreciating its dollar (Bryan, Citation2015). Later on, in 1994, the flexible basket was replaced with an independent float while its value was fixed to the US dollar until 2009, when it was removed from the market despite how it was heavily dominating transactions post de jure independence (Noko, Citation2011).

2.1. The crisis

Foreign exchange crises are not rare anymore in the global economy. What differs is the nature, extent, and coverage of the currency turmoil. Currency crises have influenced world economic developments since the 1920s. The Zimbabwean currency crisis is only but one of the many crises in the 19th and 20th centuries. The crisis has caused untold suffering amongst the generality of the populace. The Zimbabwean economy faced serious foreign currency shortages in 1999 when the Reserve Bank of Zimbabwe (RBZ) pulled out of the managed float exchange rate management system, causing the Zimbabwean dollar to crash significantly. In subsequent years, the crisis changed from a currency instability problem to serious foreign exchange shortages in 2000.

However, looking at it from a different perspective, the crisis may have been related to President Mugabe’s regime. Desiring to be an autonomous state, the reign of the late Robert Mugabe played a significant role in providing Zimbabweans with as much independence as possible, ranging from political, social to economic within the 1st decade of post-independence. The economic growth was exciting and unequivocally stirred up admiration from the neighboring African states. However, Besada and Moyo (Citation2008) highlight that Mugabe’s regime began to turn sour in 1999, collapsing Zimbabwe’s economy with his ill-starred policies. On the other hand, some authors argue that the red flags surfaced as early as 1997. Nevertheless, the motive to buy the citizens’ loyalty, specifically the Liberation War Veterans, drove the government to make large payments as a way of campaigning for the upcoming elections; a recipe for disaster (Hany Besada, Citation2008, October). These veterans were all given an amount of ZW$50 000 each as a “token of appreciation” (Lionel Nkomazana, Citation2014). The government was then obligated to print more money, consequently depreciating the Zimbabwean dollar in comparison to the major currencies. Nkomazana and Tambudzai further add that the government’s decision through the Reserve Bank of Zimbabwe as it pulled out of the managed float exchange rate management system caused the Zimbabwean Dollar to crash, thus adding more salt to the wound.

Causing more harm than good, in 1998, the government of Zimbabwe, with no justifiable and enough valid reason, intervened in the war in the Democratic Republic of Congo (Lionel Nkomazana, Citation2014). 19 October 1998, the Zimbabwe Human Rights NGO forum released a press release disapproving the aforementioned matter. Quoting the constitution, the press release was against this intervention for the fact that it was not at par with the constitution as per the then Section 96 of the Zimbabwe Constitution.

In 2003, questionable land redistribution occurred as thousands of farms owned by white farmers were seized and allocated to citizens who were somewhere misinformed about this particular business sector (Lionel Nkomazana, Citation2014). When the forex reserves were at a critically low level, considerable sums of foreign exchange were used in financing wars. There is an assertion that about two-fifths of the government budget was allotted and used in financing the war year after year. According to the International Institute for Strategic Studies (IISS) (), the war in DRC cost the Zimbabwean economy not less than US$25 million a month from January to June 2000. The DRC war, however, was not exclusively supported by domestic sources. There were also other private illegal deals and joint business ventures between the two countries that financed the war. But these resulted in diminishing the image of Zimbabwe as a hub for investment. Foreign military interferences have shattered foreign exchange earnings and deteriorated the economic crisis (Tambudzai, Citation2007).

The economic effects of the crisis were the country’s inability to meet its import obligations and other international bills, among them the servicing of international debts. The chronic shortage of foreign currency caused a severe shortage of imported raw materials; more remarkable was the shortage of fuel and electricity, which nearly brought the country to a standstill in 2007 and 2008. The government, together with the private sector, suspended repayment of their international financial obligations after 2004.

2.2. The Zimbabwe’s black market for foreign exchange

Though foreign currency scarcities have been a persistent economic problem for Zimbabwe since independence, the sternness of the problem was first brought to light in 1987, before sinking and reappearing again since 1993. Nonetheless, the black-market premium was very trivial for the larger part of the 1990s, only to start growing towards the end of 1999. By 2002, the country’s black-market activities had grown in-depth and breadth to such an extent that the black-market premium reached its highest percentage figure of 2898 in December 2002 and January 2003. Although the parallel market premium considerably deteriorated in 2004 (when it reached a monthly average premium of 100% and above), it has, however, been on an increasing trend again since 2005 to date (Makochekanwa, Citation2007).

The literature on the parallel market for foreign currency in Zimbabwe is scant, so it is difficult to know exactly how this market started and evolved over time. It seems clear, however, that the dynamics in Zimbabwe’s black market for foreign exchange have followed a number of factors, including political events, movements in international markets, government policy, and other institutional factors. There are indications that the parallel market can be traced back to 1965, if not earlier than that. During the Unilateral Declaration of Independence (UDI) (1965 through to 1980), the country was placed under United Nations sanctions, which meant limited foreign currency inflow into the country, resulting in foreign currency shortages then. Nevertheless, available data on exchange rates shows that, although the parallel market was present as far as January 1975, the divergence between the official and black-market rates only became important in the first ten months of 1987, before the two rates became more or less the same till the end of 1992.

The premium, however, picked again at the start of 1993 until today. Although the premium was averaging less than 1 percent between January 1993 and December 1999, the divergence between the official and parallel rates has since widened beginning 2000. In January 2000, the black-market premium was 11.39 percent, reaching its highest percentage figure of 2898.05 in the two months of December 2002 and January 2003. Tracing the history of the black market for foreign currency in Zimbabwe, at independence in 1980, the word ‘black market for foreign exchange was a vocabulary to the majority and a term whose meaning was the prerogative of the few enlightened economists. However, by 2000, the word became the talk of the urbanites, and as of March 2007, the term “black/parallel market” has become a ubiquitous word that even the grade one pupil and the very uneducated rural grand-grand parent can easily define and interpret it in terms of its effects on their day to day living.

Peeping through the curtains of history, black markets in foreign exchange in many countries have arisen in response to government controls on access to foreign exchange. In most cases, controls are imposed to try to protect the government’s limited stock of foreign exchange reserves. The need for this protection, in turn, is caused by trade deficits and capital flight that result in net demand for foreign exchange at the central bank. Once the government imposes the limitation on holding forex or on transferring it abroad, the demand for another source of that currency emerges (Grosse, Citation1991).

Although literature sites innumerable dimensions through which one can analyze the causes and determinants of parallel markets, Degefe and Moges (Citation1994) grouped these factors into three broad categories. He pointed out that the current account transactions, currency substitution, and capital flight motives of the demand for foreign exchange by the private sector are the three broad causes of the black market for foreign exchange. On the other hand, Grosse (Citation2005) classified his determinants into two broad categories: monetary and the existence of an underground economy. According to the latter author, the vicious monetary circle is initiated by an ‘excessive rate of monetary growth, which leads to higher inflation in the domestic economy relative to trading partners. This will result in increased demand for foreign currencies by citizens to buy relatively cheaper foreign goods and to hold wealth in more stable currencies.

At the same time, investors’ confidence in the economic prospects of the country becomes weaker, prompting them to consider and transfer their investments to other countries (and therefore other currencies), creating excess demand for foreign currency and contributing to the capital flight. Grosse (Citation2005) further argued that even in the absence of monetary factors explained above, a country may still find that goods produced locally are perceived as inferior in quality to similar goods produced abroad; and thus, demand arises for foreign exchange to buy those high-quality foreign products. The second variety of reasons for the development of black markets, according to Grosse (Citation2005), is the existence of an underground economy in the country. That is, when some participants engage in illegal business activities—such as the sale of gold, sale of contraband products, and drug trafficking—then a need arises for financial services that circumvent the legal, financial system. Nkurunziza (Citation2020) delineated the analysis of the black-market premium into three categories. Firstly, the “real trade” approach, which emphasizes the fact that a parallel market serves mainly commercial purposes. Secondly, the monetary approach puts emphasis on monetary factors in elucidating the parallel market. Lastly, the portfolio balance method, also known as the currency substitution approach, is based on the assumption that agents use the parallel market to change the structure of their assets between foreign and domestic currencies.

Although Zimbabwe’s parallel market for foreign currency fit into the three authors’ respective broad determinants (N.B. these authors’ broad category determinants overlap), Zimbabwe’s parallel market dealings became hectic, as the intensifying political instability and macroeconomic instability pushed money out of the country following the controversial land reform since 1999; and most importantly the fact that the country been increasingly isolated from the international community. For instance, Zimbabwe withdrew from the British Commonwealth in 2003, and this has resulted in both the World Bank and IMF suspending all programs of assistance. Hence, the prevalence of the black market as a result of the above-mentioned factors affects the demand for foreign exchange through the formal market.

2.3. Zimbabwe’s multi currency system

According to the Zimbabwe National Statistic Agency (ZIMSTAT, Citation2016), the Zimbabwean economy started experiencing a severe liquidity crisis towards the last quarter of 2015 because of a declining money supply. When the country implemented the multicurrency regime in 2009, the Reserve Bank of Zimbabwe (RBZ), which is the monetary authority, surrendered its monetary policy power. Principally, the RBZ lost the capacity to engage in seigniorage, which comprises the printing of banknotes to either replenish worn-out notes or to satisfy money supply needs in response to the demand for products in the economy.

The shortfall of the money supply affects not only the money in circulation but also the supply of credit by financial institutions and the propensity of spending by consumers. The literature on deflation postulate that the resultant effect should be that bank deposits should account for the majority of the money supply in the country (Anderloni and Carluccio 2006; Braga, 2006; Corr, Citation2006; Memdani & Rajyalakshmi, Citation2013; Zikhali, Citation2020).

The ZIMSTAT (Citation2016) on money supply indicates that money supply had risen to $US4,75 billion by the end of 2015, ascribing to enhance confidence in the banking sector from the all-time low-slung confidence experienced throughout the hyperinflation in 2008. It is worth mentioning that the lending portfolio of banks is currently tilted towards lending for consumptive purposes, and bank deposits are greatly geared towards demand deposits. This phenomenon does not urger well for liquidity enhancement and money creation.

Regardless of the increasing domestic confidence after the hyperinflation period, a substantial proportion of Zimbabweans is still financially excluded. Many studies show that the proportion of the Zimbabwean populace that is financially included is basically for transaction motive including receiving wages and salaries as well as other employment money deposits and money from other sources (Anderloni & Carluccio, Citation2007; BMRB, Citation2006; Corr, Citation2006; Kempson, Citation2006; Makone, Citation2020; Noko, Citation2011). The tendency to save is mostly low because of average low disposable incomes. Most grownups in Zimbabwe do not save due to a lack of residual income after paying for living expenses, school fees, and other emergencies. Usually, the percentage of income apportioned for emergencies is reserved as savings at home. On the other hand, the bank deposit and savings interest rates that banks offer are significantly low and unattractive (Makone, Citation2020).

According to ZIMSTAT (Citation2016), about $US7,4 billion is being speculated in the informal sector of Zimbabwe’s economy. This has impelled the Zimbabwean government to formalize the activities of the informal sector in the country in fulfillment of the “Agenda for Sustainable Socioeconomic Transformation (ZIMASSET)” in Zimbabwe. The government recognizes that the fiscus is trailing significant amounts of money from this untouched sector and formalizing such activities would highly help to a larger extent in realizing the objectives of financial inclusion. Nevertheless, the challenge of both domestic and external confidence still persists. The investor confidence in Zimbabwe averaged −37.2 as of the last quarter of 2016 (ZIMSTAT, Citation2016). This has impelled diverse studies to examine the financial inclusion confidence challenges of informal traders, after the multicurrency system was implemented in Zimbabwe.

3. Literature and hypothesis development

In analyzing the impact of political risk in Zimbabwe, Mawanza (Citation2015) surveyed 25 MNC’s through distributing questionnaires amongst different managers for the 25 multinational firms with an intent to derive their perceptions of decision-making and the nature of political risk. Aiming to provide risk management strategies, the research proves the existence of a relationship between political risk and foreign direct investment through multinational firms. Similarly, Rafat and Farahani (Citation2019) applied an instrumental variable regression that strongly proved a statistically significant correlation between FDI and political risk. Proving their significance at the 5 percent level, the six indicators of political risk in their study (socioeconomic condition, external conflicts, law and order, religious and ethnic tensions, investment profile, and military) implied a negative impact on the flows of FDI. The idea here is that there is a strong relationship between FDI and Political risk, which implies that unsolved conflicts that would result in political stability will reduce the flow of FDI. Iuliana (Citation2010) affirms the above conclusions regarding political risk and FDI

Research based on comparative qualitative analysis of five developed and five developing economies proved through a created average value of different political risk components that, whether it could be micro, macro governance, or instability, both economies are vulnerable to political risk (Makone, Citation2020; Waszkiewicz, Citation2017). The distinguishable aspect between the two (developed and developing countries) is access to international capital and the huge gap of political risk impact on their financial markets. Furthermore, from capital flow and foreign investment, the influence extends to impact volatility of financial markets. The overall research finding presents that threats associated with political instability do influence the volatility of financial markets.

In a paper to explore the reaction of financial markets to the rising terrorist attacks, Johnston and Nedelescu (Citation2005) concluded that financial markets absorb the shocks of terrorism attacks. Research with more of a theoretical view engrossed much on the September 11 attacks, notes gigantic disfigurement to infrastructure and communication systems that were brought about by the attack on the World Trade Centre in New York. Furthermore, they state the closure of some financial markets in New York with the financial industry consequently suffering an enormous and disastrous cost.

Chesney et al. (Citation2011) further authenticate the significant effect of terrorist attacks on financial markets in their empirical study. Through the event study and GARCH-EVT approach, their research obtained a significant negative impact based on the behavior of their selected markets. Even though these markets (European, American, and Swiss stock markets) recorded different levels of being impacted, with the Swiss being the most affected, the study revealed that 55 out of 77 events of terrorism had a negative impact on these markets. According to this study, the impact of political risk may be felt immediately as far as terrorist attacks are concerned and reduced post attacks. The impact of terrorism may be felt by financial markets, stock markets, in this case, this is likely to interpret that duration at which the strength lasts post the attacks is likely to be determined by the magnitude of the strength.

Interestingly, not only does the strength of terrorist activity decline post the incident making it dependent on the time period, it also deteriorates or upsurges depending on the type of financial market. Tayyeba et al. (Citation2010) studied Karachi Stock Exchange, Forex, and Interbank markets using the OLS model, investigating the correlation of terrorist activities and financial markets of Pakistan within a period of two years. Also, Suleman (Citation2012) also examines the Karachi Stock Exchange using a rather different method by employing the EGARCH model, investigating how volatility and returns relate to terrorist attack news. The model results show a negative impact on the financial sector compared to other sectors that were used, such as oil and gas. These results are marked by the returns on the Karachi Stock Exchange 100 index depicting a significantly negative effect.

Remarkably, Park and Newaz (Citation2018) stand on a different side of the argument with the concept that stock markets are not vulnerable to terrorist attacks as compared to foreign exchange markets, basing their argument on the magnitude of the attack and the performance of the financial market. Their paper studies the stock and foreign exchange markets of 36 countries within a time frame of 15 years, covering a total of 15 2241 attacks, including days of attacks and nonattack days. The meta-analysis event study approach in their paper concludes that contrasting other researchers, the impact of terrorism attacks on financial markets do not twitch a nerve. Even though the pinch may be felt by foreign exchange markets, only a few markets depict the significant adverse impact.

As noted, political risk is a challenge to many economies, and some researchers have gone into the depth of sourcing indicators of early warning signs. Although terrorist attacks may occur in a politically stable economy, their occurrence is more prevalent in politically unstable economies. It can be argued that factors that open up for political disturbances in a nation may give room or trigger terrorist attacks, particularly when the security system of the nation is not strong. This stands to explain why previous authors factor terrorist attacks in measuring the political stability of an economy (Bratton & Gyimah-Boadi, Citation2015, May).

From this literature review, it is quite evident that the approach to measuring the impact of political risk differs from researcher to researcher. Furthermore, different academia uses different proxies for political risk as per the index. Moreover, even though studies are more biased towards the type of risks that affect financial markets in a nutshell, this literature review proves that indeed political risk affects financial markets. Therefore, given the elucidation in this section concerning the concept of political risk, the foreign currency market, empirical evidence, and stylized facts that characterize the Zimbabwe economy, we hypothesize that:

H1a: Political risk has a positive causal impact on foreign currency demand in Zimbabwe in the short run.

H1b: Political risk has a positive causal impact on foreign currency demand in Zimbabwe in the long run

4. Research methodology

In this section, we offer the main methodological strategy implemented in this study. This comprises the variables employed in the study, how the variables were calculated, the data utilized, and sources of the data.

4.1. Data sources and measurement of study variables

The study entirely utilizes secondary data. The data was extracted from the database of the World Bank - World Development Indicator (WDI), International Country Risk Guide (ICRG), and Reserve Bank of Zimbabwe (RBZ). Time series yearly data on Total foreign reserves, Interest rate, Public debt, inflation rate, Political risks rating, and Trade openness in Zimbabwe covering the period 1980 to 2019 were exploited in the study. Summary of all the variables utilized in the study is presented in below.

Table 1. Measurement, notation, and sources of Variables

Forex demand for this study was proxy by total foreign reserves held by the reserve bank of Zimbabwe over the period under review. Total foreign reserves comprise holdings of monetary gold, special drawing rights, reserves of IMF members held by the IMF, and holdings of foreign exchange under the control of monetary authorities. This is because it is economically assumed that changes or variations in the total foreign reserves of a country reflect the demand or supply of a country’s forex. As such, total foreign reserves are projected to relate negatively with the demand for forex. Accordingly, other conditions held constant; an increase in demand for forex is mirrored by the decline in the total reserves of the country. The natural log of the foreign reserve variable, unlike the covariates, was utilized in the estimation. This was done purposely first to produce a more “normal” or symmetric residual data identical to that of the other variables, which were symmetrical in their original form. Secondly, the log form of the foreign reserve was taken to reduce its large values to a similar scale of the other variables originally calculated in ratio. Political risk is measured as quantified by International Country Risk Guide (ICRG). The political risk component entails a total of 100 points which is simply a tallying of all the 12 constituents, namely government stability, socioeconomic conditions, investment profile, internal conflict, external conflict, corruption, military in politics, religious tension, law and order, ethnic tension, democratic accountability, and bureaucracy quality. The maximum rating of 100 reflects the lowest risk, and a score of zero is the highest risk. However, for the purpose of this study, the researcher subtracted the actual index from 100 so that the higher values correspond to the higher political risk and vice versa. The inflation rate is proxied by the consumer price index over the period under review. Public debt in this study is measured by the total debt of the central government expressed as a percentage of gross domestic product. Interest rate is the cost of borrowing, and this is measured by the short-term lending rate in the study. Trade openness, is the totality of imports and exports normalized by GDP.

4.2. The empirical approach and model

Following the empirical modeling of Arthur et al. (Citation2021) and Asiedu et al. (Citation2021), the study adopted the bound cointegration autoregressive distributed lag ARDL model to investigate the short-run and long-term effects of multidimensional political risk index on Zimbabwe forex demand. The empirical model comprehensively tackles the primary objective of the study. Pesaran et al. (Citation2001) expound that there are three salient merits of the ARDL method compared to other individual methods. First, a pretest for unit roots is not required if the variables captured are essentially I (0), purely I (1), or slightly integrated. Second, endogenous complications and the incapability to test hypotheses in long-term estimated coefficients identified by the Engle Granger method (1987) are resolved. Third, the short-term and long-term coefficients of the cited model are calculated at the same time. Finally, the efficient approach to testing the features of small samples, which is limited by fit, is favored over other multivariate cointegrations. The empirical estimation of the bounds ARDL test method between the primary variables is stated as follows:

Where p and q are the orders of lag for the dependent variables and the independent variables, respectively. is the random error.

and b are the coefficients to be calculated and Δ signifies the first difference operator. Equation one purely portrays the variables of interest, which are illustrated with their past values. Optimal lag lengths are detected using the AIC.

4.3. Estimation procedure

First, Augmented Dickey Fuller (ADF) and Phillips Perron (PP) are used to determine the order of integration of the variables in the model. The ADF and PP tests are performed using this equation below to establish the parameters.

Where Δ indicates the difference operator; signifies variable Y at time t;

and

are parameters to be calculated, k represents the augmented number of lags and εt the white noise term. Given equation two above, the consequent hypothesis is then tested for: H0: P1 (

is non-stationary) H1: P<1 (

is stationary). After the stationary variable tests, the bound test is performed on the ARDL model to start the long-term relationship between the lagged variables for cutoff significance applying the F-test in the first stage. This is followed by an assessment of the short- and long-term associations of the variables utilizing the direct ARDL model as stated in Equation 1. Then, the presence of cointegration is validated by measuring the F-statistic value for the combined lagged levels of the variables and compared with the critical bound’s values. This is accomplished by analyzing the subsequent-bound test hypothesis:

(No co-integration)

(co-integrated). The F statistical value calculated is compared with the critical values of Pesaran et al. (Citation2001). If the number of the estimated F statistic is less than the number of the lower critical limit, we accept the null hypothesis and affirm that there is no cointegration between the variables. On the contrary, if the calculated F statistic exceeds the value of the upper critical limit, we reject the null hypothesis and declare that there is a long-term equilibrium connection between the variables under study. However, if the value of the calculated F statistic is between the lower and upper critical limit values, the result of the cointegration test is not decisive. The presence of cointegration implies that there is a long-term relationship in the series. Now, if cointegration is found between the variables, then the long-run series relationship and the short-run or the error correction model (ECM) individually can be estimated as follows:

4.4. Long-run relationship estimate

4.5. Error correction model estimate

Finally, the short-run dynamic coefficients are obtained by estimating an error correction model associated with the long-run estimates. This is specified as follows:

where is the speed of adjustment coefficient with a negative sign,

is the one lag period error correction term.

,

,

are the short-run dynamic coefficient of the model’s adjustment long-run equilibrium. The presence of a significant association in the first differences of the variables provides evidence of the direction of causality in the short term, while long-term causality is revealed by a significant t-statistic on the error correction term (Ecm—1). Furthermore, to investigate the directional causality between forex demand and political risk, the conventional Granger causality was employed.

Finally, the validity and reliability of the parameters or results are validated using several diagnostic tests that include Ramsey RESET, Hetreoscedacity, serial correlation, CUSUM and CUSUMSQ statistics.

5. Results and discussion

5.1. Unit root test

To certify that the precondition for estimating an ARDL model is observed, the stationary properties of the variables were verified with the Augmented Dickey Fuller (ADF) test and verified with the Phillips Perron (PP) test. The results are shown in .

Table 2. Stationary test

These tests were run simultaneously to ensure that the variables did not enter their respective frameworks in an explosive but in a robust manner. The result of the unit root test indicates the presence of non-stationarity in the variables in their level form, except for INT and INF. However, with the first difference, the remaining variables (lnFR, PR, TO, PD) became stationary according to their probability values less than 5%. Therefore, the variables are established to be integrated of order one and zero at a significance level of 1% or 5%, which meets the precondition to estimate the ARDL model.

5.2. Tests for Cointegration

Once the precondition for estimating an ARDL model was met, the ARDL-bound test or the cointegration test was calculated. This was completed to determine whether there exist long-term associations between the core variables when GDP is considered as the explained variable, in line with the study objective and hypothesis. The results of the ARDL bound test or cointegration are available in .

Table 3. Cointegration test results

The results of the cointegration test reveal that the estimated F-statistical values (5.991215) of 1%, 5%, and 10% are greater than the upper limits. Thus, the null hypothesis that there is no cointegration is declined. This implies that these variables are cointegrated and have a long-term association. Given the existence of cointegration or a long-term relationship between the variables, the study advances with the estimation of both the long-term and short-term relationship (error correction model). The long-term relationship between the variables indicates that there is at least one unidirectional granger causality, which is verified by the F-statistical and lagged error-correcting term. The short-term causal impact is represented by the F statistic for the independent variables, while the t statistic for the coefficient of the lagged error correction term denotes the long-term causal relationship (Narayan & Smyth, Citation2006; Odhiambo, Citation2009).

5.3. Regression Results

shows the results of the error correction model, which covers both the short-term and long-term relationships between the variables. The upper section of the results in represents the short-term measurement, while the lower portion contains the long-term measurements.

Table 4. Short and long-run regression results

5.3.1. Short run analysis

From the results in the upper segment of , there is a negative significant short-run association between political risk and foreign exchange reserve at a one percent level of significance. This outcome suggests that a unit increase in the political risk of the Zimbabwe economy is associated with a 2.79 percent decrease in foreign reserves of the country in the short run, all things being equal. In other words, an upsurge in political instability or risk of the Zimbabwe economy results in a 2.79 increase in demand for forex. By implication, as the political risk in the country increases, the risk on investment returns increases accordingly, and as a result, citizens or investors opt for foreign currencies which are more stable to secure or insure their wealth against observable shocks. Hence, the increase in demand for forex. This outcome of the results clearly mirrors the findings of the World Bank (2015) on Zimbabwe’s economy, which indicated a fall in the economic growth of the country partly due to shortages of foreign currency. Also, the results are inconsonant with the 2018 report of Price Water House Coopers, which indicated that the increased economic crisis or political risk in Zimbabwe’s economy has led to an increase in the demand and use of foreign currency in the country. Moreover, the findings are consistent with the classical assertion of Aliber (Citation1975), that investors seek external currencies purposely to change the risk features of their assets in which their assets are denominated.

Table 5. Post diagnostic test results

Table 6. Robustness test results-dependent variable: Total reserves minus gold holdings scaled by gross domestic product

Table 7. Robustness test results-dependent variable: Foreign exchange rate

Table 8. Granger causality test

The interest rate was found to positively impact foreign reserves of the Zimbabwean economy but statistically insignificant in the short run. By implication, ceteris paribus, a unit increase in the interest rate of the country will result in a possible 0.04 percent increase in foreign reserves on the grounds that capital chases interest. That is, conferring to the capital mobility principle, capital in the form of foreign currencies will move from the regions of low-interest rate to regions of high-interest rate area like Zimbabwe in the short run, ceteris paribus. Hence, an increase in the supply of forex. However, this result was found to be insignificant, probably due to the dollarization, which limited the Reserve Bank of Zimbabwe in using its instruments of either money supply or interest rates to influence economic activities (Hanke & Kwok, Citation2009). Better still, this could also be because of the rampant corruption and financial mismanagement (political risks), which have so eroded the credibility of the country’s banking system that Zimbabweans abroad are sending home less money.

The inflation rate coefficient was also found to be negative and statistically significant, implying that the inflation rate in the Zimbabwe economy increased the intensity of demand for forex during the period under study. Accordingly, an increase in the inflation rate leads to a decrease in the foreign reserve of the country as the citizenry or economic stakeholders start to substitute local currency with foreign currency in their transactions purposely to hedge themselves against hyperinflation. This finding is in line with the claims of Pasara and Garidzirai (Citation2020), who postulated in their study that the rate of growth of inflation in the Zimbabwe economy suppressed the exchange rate that led to the increase in demand for foreign currencies and the subsequent emergence of the black market to meet this growing demand.

Trade openness was found to be negatively related to foreign reserve because its coefficient is negative and statistically significant at a 5 percent level. Thus, a unit increase in trade openness leads to a proportionate decrease of 1.94 percent in foreign reserves of the Zimbabwe economy, ceteris paribus. This outcome was expected since Zimbabwe’s economy is an import-dependent economy (Bonga et al., Citation2015) and as such, will demand more foreign currencies to facilitate its external transaction or purchases. The increasing demand for foreign currency, in turn, results in a decrease in the foreign reserves of the country. Public debt was also found to be positively related to foreign reserves because its coefficient is positive and statistically significant at a 5 percent level. Thus, a unit upsurge in central government debt is associated with a 200.85 percent increase in the foreign reserves of the Zimbabwe economy. Government secures or borrows external funds to supplement internally generated funds to finance the state budget. By so doing, the foreign reserve of the country increases in the short run. This result is consistent with the findings of Azar and Aboukhodor (Citation2017) who established in their study that high debt-to-GDP significantly affects the demand for foreign exchange positively. However, the lag of public debt or the previous year’s public debt was found to be negative as against the current public debt positive coefficient. This means the previous or lagged public debt would reduce the foreign reserves of Zimbabwe by less than the proportionate USD in the next economic year. This could be because outstanding debts may be due payment and thus will be settled with foreign currencies which were used to hedge them. Hence, a fall in foreign reserve or withdrawal of foreign reserve. Nevertheless, this variable was found statistically insignificant.

Moreover, the study found that the long-run component of the model given by the lagged error correction term, ECM (−1) is correctly signed and significant. It means that the regressors, to a large extent, are indeed causally related to the dependent variable through this error-correction term. A significant ECM (−1) coefficient means that, all things being equal, whenever the actual value of the dependent variable (foreign reserve) falls below the value consistent with its long-term equilibrium relationship, changes in the independent variables help bring it up to the long-term equilibrium value. Thus, the value of the ECM (−1) coefficient indicates that the speed of adjustment of foreign reserves to the long-term equilibrium, whenever there is an imbalance, is 0.69 percent.

5.3.2. Long run analysis

All explanatory variables or regressors exerted a significant long-run impact on the dependent variable as depicted by the estimation in the lower segment of Table . Parallel to the short-run coefficient estimates, political risk was found to exert a statistically significant negative effect on foreign reserves in the long run. The results of the long-run coefficient show that the coefficient of political risk (0.056) is bigger than it was in short run. By implication, as the political risk of Zimbabwe persists over time, it heightens the risk on investment returns. As such, economic stakeholders or citizens accordingly intensify their demand for foreign currencies, such as the dollar, which is more stable and safer against most shocks, to secure their wealth against observed risks in country. The results are still consistent with the assertion of Aliber (Citation1975). It also clearly reflects the 2015 economic report of the World Bank on the Zimbabwe economy. The report indicated that many companies had been shut down mainly due to the crippling shortage of foreign currency with which to buy raw material.

In the long run, contrary to the short-run coefficient, the interest rate was found to be positive and statistically significant. This suggests that the persistence of high-interest rates led to an increase in the foreign reserves in the Zimbabwe economy under the period in review. It can be deduced that capital in the form of foreign currencies moved from the regions of low-interest rates to Zimbabwe’s economy, which in this case happens to be a region of a high-interest rate area. Hence, the supply of foreign currencies increases as the host country’s interest rate increases on the ticket of capital mobility phenomenon. This result is contrary to the study of Azar and Aboukhodor (Citation2017), who found that an increase in the domestic call money rate will lower forex reserves by 0.165 percent. The long-run estimated coefficient of the inflation rate was also found to be negative and statistically significant at 1 percent. Thus, these results suggest that as inflation in the country increases, the value of domestic currency also decreases, which then compels citizens to go in for more foreign currency to safeguard their value for money in the long run. The outcome of this result is consistent with the results of Pasara and Garidzirai (Citation2020) who reported that inflation has a negative impact on the exchange rate.

Based on the estimation results, trade openness has a statistically negative long-run impact on foreign reserve. Therefore, a unit increase in trade openness of the Zimbabwe economy is associated with 4.41 percent decrease in their foreign reserves in the long run. In other words, there is an increase in the demand of foreign currency by 4.41 percent as the trade openness of the country increase by a unit. It is not astonishing that trade openness has a significant negative effect on the foreign reserves of Zimbabwe, even though it could exert a positive effect in other economies. Most countries that import substantially more than they export occasionally face foreign exchange shortages. Most Sub-Saharan African countries like the Zimbabwe economy is an import-dependent economy according to the report of De Vylder et al. (Citation2007), and thus have a great demand for foreign currency to meet their import needs. Hence, heighten the reduction in foreign reserves in the country.

Considering the long-run impact of public debt, an appreciation in the public debt of Zimbabwe leads to a decrease in the country’s foreign reserves. Thus, in the long run, a unit increase in the public debt of the country results in a 89.93 percent decrease in the foreign reserves of the country. Hence, the decrease in foreign reserves reflects an increase in the demand for forex. This outcome is conceivable since in the long run most debts are due for payment, and thus, foreign currencies most often than not are demanded to settle these external debts. This outcome is in line with the annual economic review report of the ”Reserve Bank of Zimbabwe” (Citation2016), which indicated that government institutions and other huge private firms have been able to pay some of their due external debts. However, most of the firms are still struggling to repay all foreign suppliers because they cannot access foreign exchange.

5.4 Post Estimation Diagnostic results

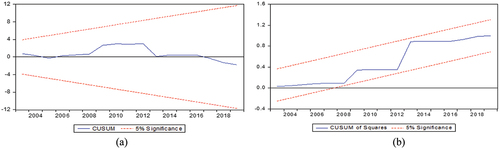

To endorse the validity of the estimated ARDL model, the study subjected the model results to all the obligatory diagnostic tests, ranging from the autoregressive test, white heteroscedasticity test, the Jarque-Bera normality test, the serial LM correlation test to CUSUM Square stability test. The outcomes are shown in .

The Diagnostic tests for the ARDL model display that the errors are normally distributed and not correlated serially. The test results also establish the absence of heteroscedasticity problems and incorrect model specification problems. The high R squared and low standard errors of the model imply that the model is robust, and the results can be trusted. Finally, the graphs of CUSUM and square of CUSUM approve the stability and precision of the estimated parameters in the long and short term, since the blue lines fall within the critical limits of 5 percent significance level for both CUSUM and CUSUM squared in , respectively.

Figure 1. Module Stability Graph

5.5. Robustness and further test

Two sets of robustness tests were performed to verify the robustness of the results obtained for the effect of political risk on forex demand. Firstly, the study applied an alternate measure of forex demand to test whether the main findings are robust to different dependent variable measure or indicators. Total reserve minus gold holdings scaled by gross domestic product, in this case, was deployed. Also, the interest rate was replaced with money supply (broad money) to test whether the results of the study will remain robust to different specifications of control. The results from this robustness test are also consistent with the main findings of the study and not considerably dissimilar to the main findings. The results of the robustness test indicate that there is a negative relationship between political risk and the ratio of foreign reserves to gross domestic product. Thus, a unit increase in political risk leads to a 0.186 and 0.352 unit decrease in the foreign reserve of Zimbabwe in the short run and long run, respectively. The main independent variable of interest, political risk, remains statistically significant once again in both the long run and the short run even upon estimation with a different measure for total reserves and a different control measure. Hence, the conclusions from the study’s main findings are robust even to the estimation of different dependent indicators and control specifications. The result of the robustness test is reported in below.

Secondly, the foreign exchange rate, which captures the relative price of forex, was also deployed, unlike the main analysis where total reserves, which capture the quantity of forex were used. An exchange rate between two currencies is the rate at which one currency will be exchanged for another. It is also regarded as the value of one country’s currency in terms of another currency (O’Sullivan & Sheffrin, Citation2003). Accordingly, the foreign exchange rate was used as one of the proxies for forex demand to examine further the outcome of the main results even to the estimation of an alternate measure of forex demand. The results from the robustness check are exactly in conformity with the core findings of the study and not significantly divergent to the baseline findings. The main variable of interest, political risk, stayed statistically significant in both the long run and the short-run relationship. The results of the robustness test indicate that there is a negative relationship between political risk and exchange rate. Thus, a unit increase in political risk leads to a 0.077 and 0.2968 unit decrease in foreign exchange of Zimbabwe in the short run and long run, respectively. By implication, the upsurges in political risk led to a depreciation of the Zimbabwe currency and thus, under a freely floating exchange rate regime, the citizenry or market players react to the political risk by selling the Zimbabwe currency to buy the currency of more stable economies, such as the US dollars. Hence, the upsurge of political risk destabilizes the economy and weakens the domestic currency, which in turn leads to an increase in demand for forex or foreign currency. This outcome is in line with the study of Bahmani-Oskooee et al. (Citation2019), who established that nations experiencing a high grade of corruption, a great risk to investment, or a high notch of political instability tend to experience a real exchange rate depreciation. The results are reported in below.

5.5.1 Further test

A further analysis was undertaken solely between the dependent variable (forex demand) and the main independent variable (political risk) to establish the direction of causality between them. Accordingly, the conventional granger causality test was deployed as a double check on the causal relationship established from political risk to forex demand in both the short- and long-run relationship. From the granger causality test results, it is evident under the political risk equation that the null hypothesis, which posits that the coefficients of the first lag and the second lag are jointly not different from zero, was rejected at 5% level of significance. This means that there is a causal link flowing from political risk to foreign reserve or forex demand. However, the null hypothesis that the coefficients of the first lag and the second lag in the foreign reserve equation are jointly zero was not rejected at 5% level of significance. This means that there is no causality flowing from forex demand or foreign reserves to political risk. Hence, the study concludes further that there is a unidirectional causality running from political risks to forex demand in the Zimbabwe economy. The results are offered in below.

6. Conclusion and recommendations

The main objective of this study was to examine the effect of political risk on foreign currency demand using the case of the Zimbabwe economy while controlling for interest rate, trade openness, public debt, and inflation. To realize this objective, the study merged annual data from varied sources covering the period of 1980 to 2019. The regression results from the study showed a negative significant short run and long-run association between political risk and foreign exchange reserve. As such, an upsurge in the political risks of the Zimbabwe economy results in a corresponding increase in demand for forex. By implication, as the political risk in the country increases, the risk on investment returns increases accordingly, and as a result, citizens or investors opt for foreign currencies which are more stable to secure or insure their wealth against observable shocks.

The study also applied an alternate indicator for forex demand to test whether the main findings is robust to different dependent variable measure or indicators. The results from the robustness test are consistent with the main findings of the study and not considerably dissimilar to the main findings. As such, the main independent variable of interest that is political risk, remains statistically significant in both the long run and the short run even upon estimation with a different measure for forex demand and a different control measure. Moreover, a unidirectional causality from political risk to forex demand was found by the study. Lastly, the results found that interest rate, trade openness, public debt, and inflation are very critical factors to be considered in the nexus between political risks and forex demand.

Given the outcome of the current study’s findings, it is recommended that the Zimbabwe government should endeavor to accelerate and maintain a stable political climate that has a gross impact on the overall performance of the Zimbabwe economy. This can be achieved by, firstly, political leaders or government putting aside personal interest for the benefit of the country by putting in place pragmatic measures to increase the anti-corruption effort towards the reduction of corruption. Also, the government should ensure peaceful coexistence of ethnic groups and strengthen government stability to improve political risk ratings and thus boost the reputation of the economy as a safe haven for both local citizens and foreign investors. In order to improve the currency exchange position of the Zimbabwean economy, the government must put in measures that will boost the nation’s production to enhance its exports while minimizing its imports. Hence, our paper reveals the relevance of ensuring political stability in Zimbabwe for a conducive environment to boost the nation’s export for an appreciation in its exchange rate. Lastly, for the Zimbabwe government to swiftly grasp its self-satisfying economic growth vision, it is advisable that she pays much attention to maintaining a stable interest rate, fortifying trade openness, improving its public debt level by widening its tax net to the informal sectors to boost internally generated funds, and ensuring a healthy exchange rate since these variables exert both short- and long-run influence on the stability of forex demand in the country.

Future studies may consider the impact of political risk on black market activities and its subsequent effect on the Zimbabwean foreign currency reserves. We agree with prior theories that once the government imposes a limitation on holding foreign currency or on its transfer abroad, the demand for another source of that currency emerges (Grosse, Citation1991). Since we are unable to capture the percentage of currency exchange activities through the black market in our model due to the unavailability of data for the Zimbabwe black market, future studies on this will be insightful.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Aliber, R. Z. (1975). Exchange risk, political risk, and investor demand for external currency deposits. Journal of Money, Credit and Banking, Blackwell Publishing, 7(2), 161–21. https://doi.org/10.2307/1991347

- Anderloni, L., & Carluccio, E. (2007). Access to bank accounts and payment services. In L. Anderloni, M. D. Braga, & E. M. Carluccio (Eds.), New frontiers in banking services: Emerging needs and tailored products for untapped markets (pp. 5–105). Springer Science & Business Media.

- Arthur, B., Kyei Tutu, B., & Afenya Salase, M. (2021). Does foreign direct investment generate long-term growth in Ghana? Asian Journal of Economic Modelling, 9(3), 214–229. https://doi.org/10.18488/journal.8.2021.93.214.229

- Asiedu, M., Bimpong, P., Hezkeal Nan Khela, T., & Arthur, B. (2021). Long-run money demand function: Search for stability in twenty (20) non-EMU member countries. Asian Journal Of Economic Modelling, 9(1), 58–87. https://doi.org/10.18488/journal.8.2021.91.58.87

- Azar, S. A., & Aboukhodor, W. (2017). Foreign exchange reserves and the macro-economy in the GCC countries. Accounting and Finance Research, 6(3), 72–87. https://doi.org/10.5430/afr.v6n3p72

- Bahmani-Oskooee, M., Amor, T. H., Nouira, R., & Rault, C. (2019). Political risk and real exchange rate: What can we learn from recent developments in panel data econometrics for emerging and developing countries? Journal of Quantitative Economics, 17(4), 741–762. https://doi.org/10.1007/s40953-018-0145-4

- Besada, H., & Moyo, N. (2008). Zimbabwe in crisis: Mugabe’s policies and failures. The Centre for International Governance Innovation Technical Paper, (38), 1–40. http://dx.doi.org/10.2139/ssrn.1286683

- BMRB (2006). Access to financial services by those on the margins of banking: Final report for the financial inclusion taskforce.

- Bonga, W. G., Sithole, R., & Shenje, T. (2015). Export sector contribution to economic growth in Zimbabwe: A causality analysis. The International Journal of Business & Management, 3(10), 1–13. https://www.researchgate.net/publication/283537589_Export_Sector_Contribution_to_Economic_Growth_in_Zimbabwe_A_Causality_Analysis

- Bratton, M., & Gyimah-boadi, E. (2015, May). Political risks facing African democracies: Evidence from afrobarometer. Africaportal, 1–32. https://www.africaportal.org/publications/political-risks-facing-african-democracies-evidence-from-afrobarometer/

- Bryan, T. (2015, July 1). The death of the Zimbabwe dollar. Global Financial Data.

- Chesney, M., Reshetar, G., & Karaman, M. (2011). The impact of terrorism on financial markets: An empirical study. Journal of Banking and Finance, 35(2), 253–267. https://doi.org/10.1016/j.jbankfin.2010.07.026

- Corr, C. (2006). Financial exclusion in Ireland: An exploratory study and policy review. Combat Poverty Agency.

- De Vylder, S., Nycander, G. A., Laanatza, M., & Froude, A. (2007). The least developed countries and world trade. Sida.

- Degefe, B., & Moges, K. (1994). Post devaluation: From stagflation to stagflation. In M. Taddesse & A. B. Kello (Eds.), The Ethiopian economy: Problems of adjustment,proceedings of the second annual conference on the Ethiopian economy.

- Grosse, R. (1991). Peru’s black market in foreign exchange. Journal of International Studies and World Affairs, 33(3), 153–167. https://www.jstor.org/stable/165936

- Grosse, R. (Ed.). (2005). International business and government relations in the 21st century. Cambridge University Press.

- Hanke, S. H., & Kwok, A. K. (2009). On the measurement of Zimbabwe’s hyperinflation. The Cato Journal, 29(2), 353. https://ssrn.com/abstract=2264895

- Hany Besada, N. M. (2008, October). Zimbabwe in crisis; Mugabe’s policies and failures. The Centre for International Governance Innovation.

- IMF.(2009). Zimbabwe: Staff Report for the 2009 Article IV Consultation. 09/139. https://www.imf.org/external/pubs/ft/scr/2009/cr09139.pdf

- Iuliana, M. (2010). Business climate, political risk and FDI in developing countries: Evidence from panel data. International Journal of Economics and Finance, (5), 54–65. https://www.academia.edu/34032733/Business_Climate_Political_Risk_and_FDI_in_Developing_Countries_Evidence_from_Panel_Data

- Johnston, R. B., & Nedelescu, O. M. (2005). IMF Working paper: The Impact of Terrorism on Financial Markets (pp. 3–4). IMF WP/05/60.

- Kempson, E. (2006). Policy level response to financial exclusion in developing economies: Lessons for developing countries. In Paper for access to finance: Building inclusive financial systems. May 30-31 2006. World Bank .

- Kobrin, S. J. (1979). Political risk: A review and reconsideration. Journal of International Business Studies, 10(3), 67–80. https://doi.org/10.1057/palgrave.jibs.8490631

- Lionel Nkomazana, F. N. (2014). Overview of the economic causes and effects of dollarisation; Case of Zimbabwe. Mediterranean Journal of Sciences, 5(7), 69–73. https://doi.org/10.5901/mjss.2014.v5n7p69

- Makochekanwa, A. (2007). Zimbabwe’s black market for foreign exchange. Journal of Economics, 98(1), 25–40. https://ideas.repec.org/p/pre/wpaper/200713.html

- Makone, I. (2020). A critical assessment of the conceptualisation of political risk analysis for hybrid regimes: the case of Zimbabwe (Doctoral dissertation Stellenbosch University).

- Mawanza, W. (2015). An assessment of the political risk management strategies by multinational. International Journal of Business and Social Science, 6(3), 117–127. https://ijbssnet.com/journals/Vol_6_No_3_March_2015/13.pdf

- Memdani, L., & Rajyalakshmi, K. (2013). Financial inclusion in India. International Journal of Applied Research and Studies, 2(8), 1–10. https://www.researchgate.net/publication/324248472_Financial_Inclusion_in_India

- Narayan, P. K., & Smyth, R. (2006). What determines migration flows from low‐income to high‐income countries? An empirical investigation of Fiji–Us migration 1972–2001. Contemporary Economic Policy, 24(2), 332–342. https://doi.org/10.1093/cep/byj019

- Nkurunziza, J. D. (2020). Exchange rate policy and the parallel market for foreign currency in Burundi [ Thesis, St. Antony’s College, CSAE and Department of Economics University of Oxford]. http://publication.aercafricalibrary.org/handle/123456789/512

- Noko, J. (2011). Dollarization: The case of Zimbabwe. Carto Journal, 31(2), 339–365. https://ssrn.com/abstract=2253506

- O’Sullivan, A., & Sheffrin, S. M. (2003). Economics: Models in action. Prentice Hall: Addison Wesley Longman.

- Odhiambo, N. M. (2009). Electricity consumption and economic growth in South Africa: A trivariate causality test. Energy Economics, 31(5), 635–640. https://doi.org/10.1016/j.eneco.2009.01.005

- Park, J. S., & Newaz, M. K. (2018). Do terrorist attacks harm financial markets; A meta-analysis of event studies and determinants of adverse impact. Global Finance Journal, 37 (C) , 227–247. https://doi.org/10.1016/j.gfj.2018.06.003

- Pasara, M. T., & Garidzirai, R. (2020). Causality effects among gross capital formation, unemployment and economic growth in South Africa. Economies, 8(2), 26. https://doi.org/10.3390/economies8020026

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289–326. https://doi.org/10.1002/jae.616

- Rafat, M., & Farahani, M. (2019). The country risks and foreign direct investment (FDI)1. Iran Economic Review, 23(1), 235–260. https://ier.ut.ac.ir/article_69107.html

- THE RESERVE BANK of Zimbabwe - annual report (2016). https://www.rbz.co.zw/documents/ar/2016AnnualReport.pdf

- Sikwila, M. N. (2013). Dollarization and the Zimbabwe’s economy. Journal of Economics and Behavioural Studies, 5(6), 398–405. https://doi.org/10.22610/jebs.v5i6.414

- Suleman, M. T. (2012). The stock market reaction to terrorist attacks: Empirical evidence from a frontline state. Australasian Accounting, Business and Finance Journal, 6(1), 97–110. https://ro.uow.edu.au/cgi/viewcontent.cgi?article=1281&context=aabfj

- Tambudzai, Z. (2007). Military burden determinants in Southern Africa, 1996-2005: A cross-section and panel data analysis. Economic development in Africa conference, St Catherineís College.

- Tayyeba, G., Anwar, H., Shafiqullah, B., & Sanam, W. K. (2010). The impact of terrorism on the financial markets of Parkistan. European Journal of Social Sciences, 18(1), 98–108. https://mpra.ub.uni-muenchen.de/41990/1/Impact_of_Terrorism_on_the_Financial_Markets_of_Pakistan.pdf

- Waszkiewicz, G. (2017). Political risk on financial markets in developed and developing economies. Journal of Economics and Management, 14(39), 113–132. https://doi.org/10.22367/jem.2017.28.07

- Zikhali, W. (2020). Changing money, changing fortunes: Experiences of money changers in Nkayi, Zimbabwe. Canadian Journal of African Studies/Revue Canadienne Des Études Africaines, 6(6), 1–18. https://doi.org/10.1080/00083968.2020.1802610

- ZIMSTAT, I. (2016). Zimbabwe demographic and health survey 2015: Final report.