Abstract

While informal debt is often used as a funding source for retail investors, very little is known about the characteristics of its sources and use. This is particularly true in emerging markets where the use of informal debt is widespread. We examine the determinants of the use of informal debt of individual investors in the Vietnam stock market and find that perceived risk has a positive impact on informal debt decisions, that borrowing sources are primarily from parents and friends and that experience, wealth and borrowing sources have a positive impact. We also find that women perceive higher risks in stock investments than men do.The policy implication is that informal debt sources play a significant part in stock market development, and therefore, a greater level of attention needs to be paid to them. Policies need to be developed that increase and manage informal sources of investment finance.

1. Introduction

Literature finds the importance of informal debt to both entrepreneurs and individuals (Mohieldin & Wright, Citation2000; Turvey & Kong, Citation2010), particularly when firms or individuals have constrained access to formal borrowing sources (Wu et al., Citation2016). Informal debt is widely used in production and consumption across developing countries, for example, in Egypt (Mohieldin & Wright, Citation2000), Vietnam (Barslund & Tarp, Citation2008), Peru (Guirkinger, Citation2008), China (Turvey & Kong, Citation2010), India (Guérin et al., Citation2013), and Thailand (Kislat, Citation2015). However, little is done regarding the use of debt in investments. This paper therefore aims to fill that gap by examining the use of informal debt in stock investment in one of the fast-developing market, Vietnam.

We are motivated by some special characteristics of the Vietnam stock market. First, according to Giang (Citation2021), Vietnam stock market continues to hold the top stock market spot in terms of performance in Asia, as it has rebounded sharply over the past decade from the global financial crisis. Second, differing from the developed markets where institutional investors are the primary players, individual investors dominate the Vietnam stock market, making up 99% of participants. Third, most investors are young (approximately 50% age 26–35) and do not have much experience in stock investment (around 50% have less than 3 years of experience; Phung & Mai, Citation2017). The research on the behaviour of Vietnamese individual investors applied in this study is of significant interest as they are generally new to the market and are still learning. Finally, investors typically use high levels of debt, including formal and informal sources. While Vietnamese law imposes a maximum lending ratio of 1:1, in some instances individual investors use higher levels of debt even up to 1:4 ratio.Footnote1 As the use of leverage clearly increases the risk of investment, this phenomenon motivates us to examine how the perceived risk of individual investors in Vietnam play the role in decision of this risky behaviour, that is, using informal debt in stock investment.

We focus on the use of informal debt because, based on Vietnamese culture and anecdotes as well as our preliminary interviews, investors prefer borrowing from their parents and friends to the banks. One reason is that investors believe they offer an opportunity for their parents or friends to earn extra income should their stock investments succeed. Another reason is that informal borrowing is an alternative source of funds for investors when the access to formal lenders is limited (Guirkinger, Citation2008; Mohieldin & Wright, Citation2000; Nguyen & Berg, Citation2014). Finally, investors may feel less pressured, and even less legally responsible, if they cannot repay the lenders of informal debt.

Traditional finance theories assume that investors are risk averse, so pursuing higher returns is one of the reasons to explain why investors use debts for their stock investment. Formal debt has received research attention by practitioners and researchers (Aydemir et al., Citation2006; Fang et al., Citation2018; Guo et al., Citation2011; Hens & Steude, Citation2009; Karki & Kafle, Citation2020) as it is seen as a possible source of financial market problems, for example, the 2007–2009 global financial crisis and the 2014 Russia financial crisis. However, little is known about the use of informal debt despite his being a possible source of problems. In particular, there is no published article on the use of informal debt in the stock market. Our objectives, therefore, are to examine (i) the extent to which investors use informal debt for stock investments; (ii) the main predictors of the use of informal debt; and (iii) whether, in addition to financial risk, nonfinancial risks such as safety risk, time risk, social risk and opportunity risk can explain the use of informal debt.

This study makes three contributions to the existing literatures. First, it is the first to address the use of informal debt by individual investors for stock investment in Vietnam. Prior research on informal borrowing has tended to focus on rural households, which are often less educated and poorer than urban households (Guérin et al., Citation2013; Kislat, Citation2015). In contrast, most stock investing is by urban investors who are more highly educated and comparatively wealthier. Therefore, prior research on the characteristics of informal debt borrowers may not apply to these stock investor borrowers. Second, because we postulate that informal borrowers are concerned about a wider range of risks than just financial risk, we examine whether risks such as safety risk, time risk, social risk, or opportunity risk impact debt decisions in relation to stock investment. This is a unique approach, as most similar research ignores nonfinancial risks (Kahneman & Tversky, Citation1979; Shefrin, Citation2005). We find that these risks do have an impact on informal debt decisions, which is consistent with the perspectives of consumer behaviour theory, providing a useful integration of consumer theory with finance theory. Finally, consistent with borrowing behaviour of rural households (Barslund & Tarp, Citation2008; Nguyen & Berg, Citation2014), we find that it is also a standard practice for educated and wealthier Vietnamese to borrow from parents and friends for stock investment. This confirms that country-specific borrowing culture has an influence on investor-borrowing decisions.

The remaining sections are presented as follows. Section 2 presents background of the study. Section 3 displays theoretical literature review. Section 4 exhibits empirical literature review. Section 5 describes research design. Section 6 shows empirical results and discussion. Section 7 ends with summary and conclusion.

2. Background of the study

This section introduces the cultural and social background in Vietnam to explain the convention of borrowing cash from informal lenders.

2.1. Vietnam family culture

Vietnam is an emerging economy, being the world’s most 15th populous country in the world. Vietnam has strong economic growth due to the expansion of networks and reform policies. GDP per capita has sharply increased by 123% within 10 years (2008–2018), USD 1149 (2008) compared to USD 2566 (2018), according to the data of the world bankFootnote2 . The culture of Vietnam is one of the oldest in Southeast Asian, approximately 4000 years ago, and strongly influenced by Chinese culture (Confucian social).

Vietnamese culture places a great emphasise on family value due to unique family structure. In a Vietnamese family, multiple generations live together, including grandparents, parents, children, and unmarried members. Young adults remain in the original family until they get married, regardless of their ages. However, married males, especially the oldest or youngest sons (including his wife and children) stay in the family-of-origin to take care of the parents.

In a Vietnamese family, gender inequality is common regarding authority of decision making. Men, particularly the older one (as the household head), overall have more influence on family decision making, financial and non-financial, than women.

2.2. Cash holding preference

Eighty per cent (80%) of Vietnamese prefer using cash for daily buying and selling transactions, and that cash is the main means of payment in Vietnam.Footnote3 Three reasons account for this. Firstly, there is not any Vietnamese law on the use of non-cash payment. For payees, payment by cash is faster and safer, preventing their personal information being hacked by hackers or virus attacks online. For sellers, cash receipt may avoid the burden of taxes obligations. In practice, Vietnamese laws on bankruptcy or enterprise protection in terms of bankruptcy remain unclear and require a time-consuming process, even though they have fulfilled their tax obligations, causing a consequence that every business itself protects and survives according to their own ways. Next, there are no official community education programs on the use of e-banking for payment, resulting in most people being uncomfortable and unfamiliar with this instrument. Currently, several workshops or seminars on the use of e-banking have been taking place. However, the focus of participants is on undergraduates or higher, meaning that students in high schools (age of 15–18) or secondary schools (age of 12–14) have no ideas about e-banking payment. Finally, frauds in the finance-banking system and cheating payments online are common in Vietnam, becoming a serve problem without appropriate solutions because the origin of these problems emanates from false understandings of information. These causes people to lose trust in the banking system in Vietnam, and as a consequence, households are more likely to keep cash at home than in a bank. Hence in Vietnam individuals are more willing to lend the excess cash to other family members or friends to conduct investments on their behalf, as an alternative of earning interests from deposits.

3. Theoretical framework of the study

This paper focuses on the concept of perceived risk, particularly the different framework between traditional finance and consumer behaviour. In traditional finance theory, risks are usually measured objectively, such as standard deviation or beta, whereas the subjective risk measured through investors’ perspectives is the core value of behavioural finance and consumer behaviour frameworks.

Within the finance framework, investors are seen as being concerned only about financial risk (gain or loss) when investing in stocks. This may lead to an incomplete assessment of the perceived risk of an investment because some critical facets of the risk may be missed. Given that both investors and consumers make decisions under uncertainty, we argue that investors may, in addition to financial risk, be concerned about the other facets of risk that originate from consumer theory (Peter & Tarpey, Citation1975). Within a consumer behaviour framework, consumers are concerned with a wide variety of risks, including financial risk (potential to suffer financial harm); performance risk (perform more poorly than expected); safety risk (create harm to their safety); psychological risk (harm their sense of self and, thus, create negative emotions); social risk (do harm to their social standing); and time risk (lead to loss of time).

3.1. Perceived risk and its facets in the stock investment

“Perceived risk” plays a vital role in decision-making (Bélanger & Carter, Citation2008; Cunningham, Citation1967; Weber et al., Citation2002). Bauer (Citation1960, p. 24) defines perceived risk as “the sense that any action of a consumer will produce consequences which he cannot anticipate with anything approximating certainty, and some of which at least are likely to be unpleasant”. Perceived risk is also characterised as a person’s subjective feelings of certainty to act in an uncertain environment (Cunningham, Citation1967) or a subjective expectation of suffering a loss in pursuit of the desired outcome (Bélanger & Carter, Citation2008). Perceived risk differs from actual risk. The way that risk is perceived can be more or less severe than actual risk. Established research shows that people do not always have a realistic or accurate view of actual risk (Gilbert, Citation2009; Schneier, Citation2006).

Our exploratory investor interviews found that the perceived risk of stock investment consisted of seven facets. These facets are summarised below. Among them, four types of risk (financial risk, safety risk, social risk, time risk) are consistent with the consumer behavioural framework (Peter & Tarpey, Citation1975). Three aspects of risk, opportunity risk, choice risk, and leverage risk, were discovered through our interviews.

4. Empirical literature review and hypotheses development

Because perceived risks can differ from individual to individual, equal outcomes, may not be perceived as equally likely (Levy & Benita, Citation2009). When inadequate or complex information exists., investors tend to perceive risks of an investment as high (Wang et al., Citation2011). Conversely, investors who are overly optimistic or excessively confident about the potential for good performance often earn suboptimal returns (Barber & Odean, Citation2001; Kim & Nofsinger, Citation2003). Shefrin (Citation2001) also documents that, investors expect to earn higher returns from lower-risk stocks, because they regard stocks of financially well run companies as representative of good stocks and therefore, they choose these stocks with expectation of high returns.

Phung and Nguyen (Citation2017) confirm a positive association between perceived risk and perceived returns. Namely, when investors perceive a stock investment as risky, they prudently consider many aspects of risk before buying, which help them be more satisfied with their decisions and returns. Ganzach (Citation2000) also assert that, for the familiar financial assets, the risk-return association is positive because the actual values of risk and expected returns determine this trade-off. But, for unfamiliar financial assets, the risk-return relationship is inverse because the judgments pertain to the global preference.

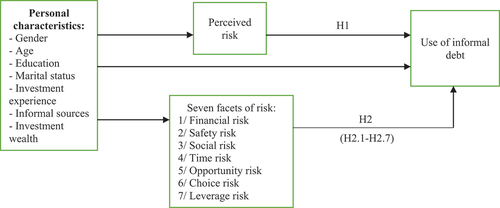

Literature on the risk-debt association is limited. This study argues that, when investors perceive stock investment as risky, they tend to use more informal debt (e.g., from parents or friends) than formal debt (e.g., from bankers or brokerage firms). The main reason is that they may avoid problems of repayment to the informal lenders, i.e., parents or friends, if their stock investment fails. The hypothesis, therefore, proposes a positive relationship between risk perception and informal debt use. The conceptual framework of this study is presented in .

H1: Perceived risk is positively associated with use of informal debt.

H2 (2.1—H2.7): Financial risk, safety risk, social risk, time risk, opportunity risk, choice risk and leverage risk are positively associated with use of informal debt, respectively.

Figure 1. Conceptual framework of the study.

5. Research design

5.1. Data preparation

The data collection process comprised five stages lasting 2 years (2017–2019): (i) preliminary interviews to understand the country-specific borrowing culture; (ii) the questionnaire design; (iii) a pilot test of 50 investors to test the reliability of the questionnaire; (iv) ethics approval for using the questionnaire to conduct the investigation; and (v) a final survey of individual investors in the Vietnam stock market via online and hand delivery. Data collection was primarily supported by brokerage firms in Vietnam. We first contacted directors or managers of brokerage firms and requested lists of emails of anonymous investors, to whom the questionnaires were sent. In addition, we had also met investors through seminars and workshops hosted by the securities companies. To reduce sampling bias, respondents were sourced across four main areas in Vietnam from the south to the north, namely, Ho Chi Minh City (HCM City) in the south, Ha Noi Capital in the north, Da Nang City in the middle of the country, and Mekong Delta in the western region. We received 420 valid responses, representing a response rate of approximately 65%. This final survey spanned 6 months in 2019. Among the respondents, 60% lived in HCM City, the largest city in Vietnam, and 20% of respondents came from each of the other three areas. Two respondents in HCM City did not disclose their gender, so they were removed from the sample, giving a total of 418 responses.

5.2. Method and measures

The study first examines the hypotheses using ordinal regression and multiple linear regression across a number of models. Perceived risk and the facets of risks are the main independent variables to examine hypotheses 1 and 2. Perceived risk is measured based on the suggestion of Peter and Tarpey (Citation1975), computed through the average of seven facets of risk, including financial risk, safety risk, time risk, social risk, opportunity risk, choice risk and leverage risk. Each facet of risk is computed by multiplying the probability of loss (PL) and the importance of loss (IL). The sum of these seven facets together forms the overall perceived risk of stock investment. This measure of perceived risk is assessed as one of the best models of those found in the literature (Dowling & Staelin, Citation1994; Mitchell, Citation1999).

Informal debt is the dependent variable relating to hypotheses 1 and 2. Informal debt is defined as the amount of money investors borrow from informal sources and measured through the question “How would you divide the amount between borrowing and your own money?”. Informal debt is divided into three levels: 1: no borrowing, 2: less than 50% and 3: 50% and above.

Seven demographic variables as control variables include gender, age, education levels, marital status, investment experience, investment wealth and informal sources. The informal borrowing source is classified into two sources: family (parents, brother/sisters, husband/wife, other relatives), and nonfamily (friends, colleagues, boss/manager, neighbours, others). briefly describes the variables in the models. Questions related to the perceived risk, informal borrowing sources and the use of informal debt are attached in the Appendix.

Table 1. A summary of the variables

5.3. Data description

The data description is shown in with three panels: Panels A, B, and C. Panel A shows that male investors dominate the sample, making up approximately 62 per cent, while female investors constitute 38 percent of the sample. Most investors (80%) are young, between the ages of 18 and 35. Only 20% of investors are above the age of 35. Sixty-two per cent (62%) of investors are single, compared with 38% being married. Most investors have a university degree (86%), are single (62%), have investment experience of less than five years (77%) and investment wealth equal to $25,000 per year or less (83%). Overall perceived risk is divided into two groups: low if perceived risk is lower than the average (mean = 88.82) and high if perceived risk equals or is greater than the average. Most investors (78%) borrow money from informal sources (parents, brothers/sisters, friends, colleagues), but only 55% of investors used informal debt for stock investments at the time of the survey. A reason accounts for this is that investors did borrow from informal lenders but have not yet used them for stock investment at the time of the survey.

Table 2. Data statistics of the study

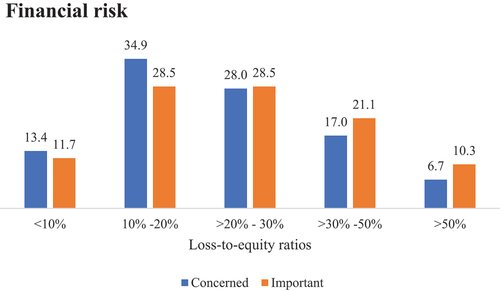

—Panel B indicates mean, median, standard deviation, min, and max. Our data show that, in general, investors perceived risks regarding stock investment as high. Use of informal debt has the minimum of 1, meaning no informal debt used for stock investment and the maximum of 3 showing 50% of informal debt or more used for stock investment. In seven facets of risk, investors perceived leverage risk as the highest, followed by choice risk, safety risk, time risk, opportunity risk, and social risk. In terms of perceived losses (financial risk), as shown in , most investors (over 70%) become concerned at a loss of 10% to 30% of equity. This also means that the majority of investors have paid little attention to the loss on equity of less than 10%. Surprisingly, a small number of investors (7%) are only concerned about the loss when it is greater than 50% of equity.

Figure 2. Financial risk among investors.

—Panel C shows the data statistics of informal borrowing sources. Investors use debt from a number of informal sources that are divided into family and nonfamily. Over 50% of investors borrow money for stock investment from family and nonfamily individuals. Family borrowing sources make up 69%, while nonfamily sources constitute 56%. Parents (36%) and friends (35%) are the main borrowing sources of investors.

5.4. Correlation tests

This study undertook the correlation test of the variables, as shown in . The results indicate that informal debt use is correlated with leverage risk at 0.12 (p < 0.05), financial risk at 0.11 (p < 0.05), and perceived risk at 0.16 (p < 0.01). This suggests that, for example, 16% of the variation in the use of informal debt is explained by the variation in perceived risk. Gender (1 for men and 0 for women) has a negative correlation with the perceived risk at −0.15 (p < 0.05), meaning that female investors are more likely than male investors to account for the variation in perceived risk. The correlation between marital status (1 for married investors and 0 for single investors) and informal debt at −0.13 (p < 0.01) reveals that single investors are more likely than married investors to explain the variation in the use of informal debt. Investment experience has a correlation with informal debt at −0.20 (p < 0.01), meaning that 20% of the variation in the use of informal debt is explained by the variation in investment experience.

Table 3. Results of correlation test

5.5. Reliability tests

We examine the reliability coefficients (Cronbach’s alpha) of the seven facets of risk, as shown in . All Cronbach’s alphas of each risk type are more than a threshold of 0.7Footnote4; for example, 0.705 (choice risk) and 0.861 (leverage risk). However, safety risk and perceived risk, both have a Cronbach’s alpha less than 0.7 (0.684 for safety risk and 0.629 for perceived risk). According to Hair et al. (Citation2014, p. 619), reliability between 0.6 and 0.7 may be acceptable. In addition, safety risk was formed with the combination of the two items, and perceived risk developed from the sum of seven facets of risk that mostly have the reliability greater than 0.7. In general, each facet of risk and overall perceived risk fulfils acceptable or high internal consistency, enabling them to be variants in a model. The overall perceived risk is correlated with its seven facets at significant levels, which, ranked in descending order, are time risk, leverage risk, choice risk, opportunity risk, social risk, safety risk, and financial risk.

Table 4. Results of the reliability of perceived risk and its facets

6. Empirical findings

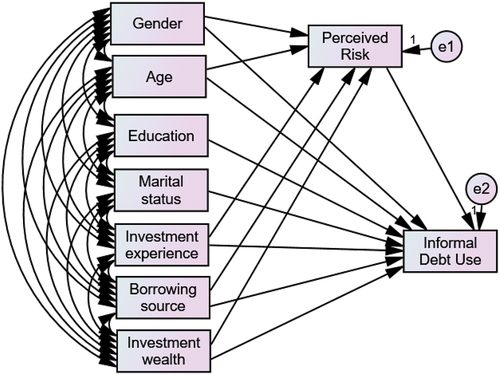

We developed four models to examine hypotheses 1 and 2 regarding the linkage between perceived risk of stock investment (and seven facets of risk) and informal debt use, using multiple linear regression (MLR), ordinal logit regression (OLR) and structural equation modelling approach (SEM), as shown in , and . The structural equation modelling model (SEM) is employed in this study, as it can examine “a series of dependence relationships simultaneously”, and particularly, it is useful in testing theories with multiple dependence relationships (Hair et al., Citation2014, p. 542).

Figure 3. Borrowing sources, perceived risk and informal debt using the SEM approach.

Table 5. Perceived risk and informal debt use

Table 6. Facets of risk and informal debt use

Regarding hypothesis 1, the results indicate a significantly strong association between perceived risk and informal debt use after controlling for demographics, as shown in . Namely, Model 1 using MLR show positive coefficients of 0.02 (p < 0.01) between perceived risk, and informal debt use, meaning that a higher risk perception leads to a higher use of informal debt for stock investments. Model 2 using OLR reports the coefficient of −0.32 (p < 0.1) between perceived risk and informal debt use, suggesting that low perceived-risk investors are less likely to use informal debt than investors with a higher risk perception. Model 3, using SEM approach, also shows a significant relationship between perceived risk and informal debt use. Taken together, our results support hypothesis 1, showing that investors with a higher risk perception tend to use more informal debt, and it is robust using three methods.

There are two possible reasons for this finding. First, investors have limited access to formal lenders. According to our data, 62% of investors have less than USD 10,000 for stock investment per year. Based on securities law, investors may borrow a maximum of 50% of this amount from formal lenders (e.g., brokerage firms), meaning that these investors may borrow more USD 5000 or less. The constrained access to the formal lenders is also confirmed by previous studies (Barslund & Tarp, Citation2008; Guirkinger, Citation2008; Mohieldin & Wright, Citation2000; Nguyen & Berg, Citation2014). Second, it may relate to the borrowing culture and the relationship between informal lenders and borrowers. We found that the main informal lenders to investors are parents and friends. Investors borrow money from these lenders, particularly parents, to avoid the pressure of the commitment to repay the money. Aforementioned, in Vietnamese culture parents are often aware that helping family members is important, and as a result, they are willing to lend to children when asked. That is, parents have a low level of concern as to the reasons why their children need their money and focus on being of value by helping their children.

We also develop models using the MLR, OLR and SEM approaches to investigate hypotheses H2.1-H2.7 regarding the relationship between seven facets of risk and informal debt use. The results, as shown in , indicate that financial risk, social risk, and choice risk are significantly associated with informal debt use.

Social risk is significantly associated with informal debt use, and this result is robust using three approaches: MLR, OLR and SEM. Namely, the coefficient between social risk and informal debt use was 0.09 (p < 0.05) in Model 1 and 0.003 (p < 0.05) in Model 3, showing that a higher level of social risk leads to a higher informal debt used for stock investment. Model 2 shows the coefficient of −0.52 (p < 0.05) between social risk and informal debt use, meaning that investors with a lower social l risk are less likely to use informal debt than investors with a higher social risk

Financial risk is positively related to the informal debt use, and this consequence is robust using two approaches: MLR and OLR. In model 1, the coefficient of 0.09 (p < 0.05) between financial risk and informal debt use means that financial risk is more perceived, informal debt is more used for stock investment. Model 2 displays the coefficient of −0.62 (p < 0.01), proposing that investors with a lower financial risk tend to use less informal debt than investors with a higher financial risk.

Choice risk also has a significant association with informal debt, using the SEM approach. Specifically, Model 4 shows a linkage between choice risk and informal debt use at 0.003 (p < 0.1), suggesting that more concerns about risks of choosing stocks lead to more use of informal debt for stock investment.

In general, the hypotheses of H2.1, H2.3 and H2.6 were supported, showing that investors with higher social risk, financial risk and choice risk tend to use more informal debt. Among these three facets of risk, social risk strongly accounts for use of informal debt. The higher use of informal debt from investors, who are more concerned about losing social standing or feel lower esteem from investment failures, indicates that this type of investors prefers keeping the borrowing behaviour within a more closed-loop, confidential connection, to minimise the possibility of bearing the image of a “loser” to the general society.

7. Further analyses of demographics

We further develop three with a number of models using four MLR, OLR, binary logit regression (BLR) and SEM approaches to investigate demographic predictors of perceived risk and facets of risk, and informal debt use between male and female investors. reports demographic predictors of perceived risk. shows demographic determinants of facets of risk. displays the linkage between informal borrowing sources and informal debt among all investors, male investors and female investors.

Table 7. Demographic predictors of perceived risk

Table 8. Determinants of facets of risk

Table 9. Borrowing sources and informal debt use

7.1. Gender gap and borrowing sources

We found gender gaps and borrowing sources are significant to explain perceived risk, facets of risk and informal debt use. Namely, female investors tend to use more informal debt and be more concerned about risks of stock investment than male investors. For example, the coefficient of −0.69 (p < 0.05; see, ) between gender (Male = 1) and perceived risk, and between gender (Female = 0) and perceived risk at 0.55 (p < 0.01). In addition, gender (male = 1) has an association with safety risk at −0.14 (p < 0.05), opportunity risk at −0.37 (p < 0.1), and choice risk at −0.12 (p < 0.05; see, ). These results suggest that male investors are less concerned with risks of stock investment than the female counterparts. In other words, male investors are more likely to take on risk than female investors, which is consistent with prior studies showing that men are more risk tolerant than women (Frijns et al., Citation2008; Grable & Roszkowski, Citation2008; Lawrenson et al., Citation2020) and that, men are more overconfident than women (Barber & Odean, Citation2001).

also indicates differences in use of borrowing sources leading to heterogeneity in use of informal debt among male and female investors. The result indicates that male investors are more interested in nonfamily borrowing sources, whereas female investors focus on family borrowing sources. Namely, for male investors, the friends and colleague lender groups are significant in explaining male investors’ informal debt behaviour. Compared with other nonfamily sources, male investors’ use of informal debt is affected by borrowing from friends at 1.24 (p < 0.05) and colleagues at 1.14 (p < 0.05). Moreover, nonborrowing from family sources is negatively associated with the use of informal debt at −1.18 (p < 0.05), indicating that male investors who do not use family borrowing sources are less likely to use informal debt for stock investment.

For female investors, the parent and husband lender groups are significant in forming female investors’ informal debt behaviour. Namely, female investors’ use of informal debt is influenced by borrowing from parents at 2.68 (p < 0.05) and partners at 2.35 (p < 0.1). Additionally, nonborrowing from nonfamily sources is associated with the use of informal debt at −1.3 (p < 0.1), suggesting that female investors who do not borrow money from nonfamily sources tend to use lower levels of informal debt. In general, this gender difference gap in borrowing behaviour is consistent with Vietnamese culture, where women are more interested in internal relationships, while men are more interested in external relationships.

Regarding the informal borrowing source, it is significant in explaining use of informal debt, perceived risk and some facets of risk. These results are robust to these three methods of MLR, OLR and SEM. For example, —Model 1 reports the coefficient of 0.56 (p < 0.01) between informal borrowing sources (borrowing = 1) and use of informal debt, showing that investors who borrow funds from informal lenders tend to use more debts for stock investment than investors who do not.

shows the coefficient of 0.81 (p < 0.05) between the informal borrowing source and the perceived risk in Model 1, suggesting that, borrowers who ever borrow informally such as from parents, relatives or friends perceive higher risks on stock investment than those who never use informal debt to invest stocks. with 12 models using MLR and binary logit regression (BLR) shows a positive association between the informal borrowing source and opportunity risk at 0.17 (p < 0.05) (in Model 5) and leverage risk at 0.38 and 0.45 (p < 0.01) (in Model 9 and 10), respectively. This suggests that borrowers of informal sources are more concerned about opportunity risk and leverage risk.

Two reasons account for this. First, past informal borrowing sources may make investor more conservative, or more concern about the risk of stock investment at present, which is consistent with previous studies (Nofsinger, Citation2008; Thaler & Johnson, Citation1990) that losses make investors to be more careful about their current decisions. Stress and fear also affect investors’ decision-making (Moueed et al., Citation2020). Second, it pertains to social responsibility. Borrowers (i.e., investors) perceive higher risk about their investments because the outcomes and welfares of others rest on their shoulders (Bolton et al., Citation2015; Charness & Jackson, Citation2009; Fornasari et al., Citation2020; Füllbrunn & Luhan, Citation2015; Phung et al., Citation2021). The fact that primary informal lenders are investors’ parents and friends make them more prudent to their investment decisions.

7.2. Analysis of other demographics

Ages have a negative association with leverage risk and time risk at −0.15 (p < 0.05) and −0.59 (p < 0.01), respectively (see, ), suggesting that an increase in age is related to the decrease in leverage risk (and time risk). That is, older investors are less concerned with leverage and time risks, which is consistent with previous studies (Frijns et al., Citation2008; Grable, Citation2000) that risk-taking levels increase with an increase in age.

Education levels have an inverse relationship with social risk at −0.22 (p < 0.05; see, ), proposing that more highly educated investors are less concerned about social risk. This is perhaps because educated investors are confident about their ability to invest in stocks and achieve good results, which increases their prestige or self-esteem in a given group. Our results are in line with findings (Grable, Citation2000; Grable & Roszkowski, Citation2008; Hallahan et al., Citation2004) that education levels are positively associated with financial risk tolerance.

Marital status (Married = 1) shows a positive coefficient with safety risk, social risk and opportunity risk (See, ). That is, married investors are more concerned than single investors about social risk, safety risk and opportunity risk, implying that married investors take less risk than single investors. This may be because married investors have greater responsibilities for their families and children (Hallahan et al., Citation2003, Citation2004), and as a result, they are more cautious about assuming a variety of risks before making decisions on stock investments.

Investment experience is negatively associated with perceived risk, safety risk, social risk, opportunity risk and the use of informal debt, suggesting that more experienced investors tend to use less informal debt and are less concerned about the risks of stock investment and social risk. This implies that more experienced investors take greater risks, which is consistent with the finding of Corter and Chen (Citation2005) that respondents with more investment experience have more risk-tolerance responses and higher-risk portfolios.

Investment wealth has a negative relationship with the use of informal debt at −0.09 (p < 0.05; see, ), and −0.35 (p < 0.01) with opportunity risk (see, ). These results mean that investors with greater investment wealth are less concerned about opportunity risk and use less informal debt for stock investment. Our results also imply that more wealthy investors tend to assume more risk, which is consistent with the findings of previous studies (Hallahan et al., Citation2003, Citation2004) that wealthy individuals are more risk tolerant.

8. Conclusions, implications and further research

8.1. Conclusions

We investigated the determinants of informal debt decisions for emerging market investors and found that perceived risk of stock investments is the main predictor of informal debt use. This result is robust using multiple linear regression, ordinal logit regression and structural equation modelling approaches. In addition, we found that social risk, financial risk and choice risk have a positive impact on informal debt use. The hypotheses of H1 and H2.1, H2.3 and H2.6 were supported. This study also explored demographic predictors of informal debt use, perceived risk and the facets of risk.

8.2. Implications

Because individual investors, as the primary participants, contribute to stock market development and economic growth across developing countries, policy-makers and relevant organisations need to have more support for individual investors.

First, informal sectors play a vital role in emerging country stock markets. This implies that severe market crashes could have significant adverse impacts on family networks. Therefore, policy-makers should have appropriate policies to manage leverage in the stock market effectively. We also reiterate that investors are concerned not only about stock investment-related risks but also about nonfinancial risks. Among the nonfinancial risks, social risk has an impact on the use of informal debt, implying that social standing plays a vital role in determining borrowing behaviours.

Second, the positive link of perceived risk to the use of informal debt implies that investors who perceive a higher risk of stock investments tend to use higher levels of informal debt. Importantly, financial risk has a strong impact on the use of informal debt, showing that the greater the loss on equity, the more informal debt is used. In fact, most investors are not concerned about losses on equity of less than 10%, and a small number of investors (7%) are only concerned about losses if they are more than 50% of equity. This may cause problems that affect stock market development, as individual investors prefer informal debt and are not afraid of losses.

Next, parents and friends are the main lenders of investors, and as a result, investors’ borrowing may affect these lenders’ lives if stock investments fail. More seriously, investors’ failure spreads out to the community if parents or friends do not lend investors their own money. In some instances, when asked to lend their children money, if parents do not have money, they themselves will borrow money from third parties rather than refuse the request. Therefore, this borrowing process needs to be transparent so investors know precisely the origin of the money they borrow so they can better control the nature of risk-taking in stock investments and reduce the negative flow-on effects. Additionally, more workshops related to stock investment are needed to provide a better understanding of borrowing and its impact on investment decisions for investors and those related to investors, including parents and friends of investors.

Finally, the use of informal debt is explained by women who borrow money from parents or their partners and by men who borrow money from their friends or colleagues. It is apparent that women rely on internal relationships, while men use external networks for their borrowing. This implies that there are gender gaps in a society where men are more powerful and influential than women in the household. Men are more exposed to social networks, leading them to be more successful in the workplace, while the role of women in society remains blurred. Inequality between men and women is indicated in a very old and famous saying, that “behind every successful man, there stands a woman”.

8.3. Further research

This study suggests further research due to some limitations. This study finds several facets of risk including safety risk, opportunity risk, leverage risk and time risk are not significant to explain informal debt use, and consequently, these factors need to be re-examined in subsequent research. Moreover, this study does not investigate whether loan interest levels affect the use of informal debt. Further research could separate payees and non-payees of loan interest, shedding light on its relationship with borrowing behaviour. In addition, this study focuses on the use of informal debt, while formal debt also plays an important role in the stock market. Further research could examine the extent to which investors divide their debt portfolios between formal debt and informal debt and the factors that explain this borrowing behaviour.

Supplemental Material

Download MS Word (289.4 KB)Disclosure statement

No potential conflict of interest was reported by the author(s).

Supplementary material

Supplemental data for this article can be accessed online at https://doi.org/10.1080/23322039.2022.2111811

Additional information

Funding

Notes

4. According to Hair et al. (Citation2014)’s guidelines, to ensure that a variable has sufficient reliability, Internal consistency (the item-to-total correlations) exceeds 0.5, and the inter-item correlation exceeds 0.3.

References

- Aydemir, A. C., Gallmeyer, M. F., & Hollifield, B. (2006). Financial leverage does not cause the leverage effect. Paper presented at the AFA 2007 Chicago Meetings Paper

- Barber, B. M., & Odean, T. (2001). Boys will be boys: Gender, overconfidence, and common stock investment. The Quarterly Journal of Economics, 116(1), 261–29. https://doi.org/10.1162/003355301556400

- Barslund, M., & Tarp, F. (2008). Formal and informal rural credit in four provinces of Vietnam. The Journal of Development Studies, 44(4), 485–503. https://doi.org/10.1080/00220380801980798

- Bauer, R. A. (1960). Consumer behavior as risk taking. In R. Hancock (Ed.), Dynamic marketing for a changing world (pp. 389–398). American Marketing Association.

- Bélanger, F., & Carter, L. (2008). Trust and risk in e-government adoption. The Journal of Strategic Information Systems, 17(2), 165–176. https://doi.org/10.1016/j.jsis.2007.12.002

- Bolton, G. E., Ockenfels, A., & Stauf, J. (2015). Social responsibility promotes conservative risk behavior. European Economic Review, 74, 109–127. https://doi.org/10.1016/j.euroecorev.2014.10.002

- Charness, G., & Jackson, M. O. (2009). The role of responsibility in strategic risk-taking. Journal of Economic Behavior & Organization, 69(3), 241–247. https://doi.org/10.1016/j.jebo.2008.10.006

- Corter, J. E., & Chen, Y.-J. (2005). Do investment risk tolerance attitudes predict portfolio risk? Journal of Business and Psychology, 20(3), 369. https://doi.org/10.1007/s10869-005-9010-5

- Cunningham, M. S. (1967). The major dimensions of perceived risk. In D. F. Cox (Ed.), Risk taking and information handling in consumer behavior (pp. 82–108). Mass: Harvard University Press.

- Dowling, G. R., & Staelin, R. (1994). A model of perceived risk and intended risk-handling activity. Journal of Consumer Research, 21(1), 119–134. https://doi.org/10.1086/209386

- Fang, X., Wang, B., Liu, L., & Song, Y. (2018). Heterogeneous traders, the leverage effect and volatility of the Chinese P2P market. Journal of Management Science and Engineering, 3(1), 39–57. https://doi.org/10.3724/SP.J.1383.301003

- Fornasari, F., Ploner, M., & Soraperra, I. (2020). Interpersonal risk assessment and social preferences: An experimental study. Journal of Economic Psychology, 77, 102183. https://doi.org/10.1016/j.joep.2019.06.006

- Frijns, B., Koellen, E., & Lehnert, T. (2008). On the determinants of portfolio choice. Journal of Economic Behavior & Organization, 66(2), 373–386. https://doi.org/10.1016/j.jebo.2006.04.004

- Füllbrunn, S., & Luhan, W. J. (2015). Am I my peer’s keeper? Social responsibility in financial decision making. Ruhr Economic Paper. (pp. 551)

- Ganzach, Y. (2000). Judging risk and return of financial assets. Organizational Behavior and Human Decision Processes, 83(2), 353–370. https://doi.org/10.1006/obhd.2000.2914

- Giang, N. K. (2021). Asia’s Hottest Stock Market Has Vietnam Primed for Inflows. www.bloomberg.com/news/articles/2021-05-04/frenzied-retail-investors-lead-charge-back-into-vietnam-stocks

- Gilbert, D. (2009). Stumbling on happiness. Vintage Canada.

- Grable, J. E. (2000). Financial risk tolerance and additional factors that affect risk taking in everyday money matters. Journal of Business and Psychology, 14(4), 625–630. https://doi.org/10.1023/A:

- Grable, J. E., & Roszkowski, M. J. (2008). The influence of mood on the willingness to take financial risks. Journal of Risk Research, 11(7), 905–923. https://doi.org/10.1080/13669870802090390

- Guérin, I., d’Espallier, B., & Venkatasubramanian, G. (2013). Debt in rural South India: Fragmentation, social regulation and discrimination. The Journal of Development Studies, 49(9), 1155–1171. https://doi.org/10.1080/00220388.2012.720365

- Guirkinger, C. (2008). Understanding the coexistence of formal and informal credit markets in Piura, Peru. World Development, 36(8), 1436–1452. https://doi.org/10.1016/j.worlddev.2007.07.002

- Guo, W.-C., Wang, F. Y., & Wu, H.-M. (2011). Financial leverage and market volatility with diverse beliefs. Economic Theory, 47(2), 337–364. https://doi.org/10.1007/s00199-010-0548-8

- Hair, J., Black, W., Babin, B. J., & Anderson, R. E. (2014). Multivariate data analysis. 7thed, Pearson.

- Hallahan, T., Faff, R., & McKenzie, M. (2003). An exploratory investigation of the relation between risk tolerance scores and demographic characteristics. Journal of Multinational Financial Management, 13(4), 483–502. https://doi.org/10.1016/S1042-444X(03)

- Hallahan, T., Faff, R., & McKenzie, M. (2004). An empirical investigation of personal financial risk tolerance. Financial Services Review, 13(1), 57–78. https://go.gale.com/ps/i.do?id=GALE%7CA149213490&sid=googleScholar&v=2.1&it=r&linkaccess=abs&issn=10570810&p=AONE&sw=w&userGroupName=tacoma_comm

- Hens, T., & Steude, S. C. (2009). The leverage effect without leverage. Finance Research Letters, 6(2), 83–94. https://doi.org/10.1016/j.frl.2009.01.002

- Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica: Journal of the Econometric Society, 47(2), 263–291. https://doi.org/10.1142/9789814417358_0006

- Karki, D., & Kafle, T. (2020). Investigation of factors influencing risk tolerance among investors using ordinal logistic regression: A case from Nepal. Cogent Economics & Finance, 8(1), 1849970. https://doi.org/10.1080/23322039.2020.1849970

- Kim, K. A., & Nofsinger, J. R. (2003). The behavior and performance of individual investors in Japan. Pacific Basin Finance Journal, 11(1), 1–22. https://www.researchgate.net/publication/267421484_The_Behavior_and_Performance_of_Individual_Investors_in_Japan

- Kislat, C. (2015). Why are informal loans still a big deal? Evidence from North-east Thailand. The Journal of Development Studies, 51(5), 569–585. https://doi.org/10.1080/00220388.2014.983907

- Lawrenson, J., & Dickason-Koekemoer, Z. (2020). A model for female South African investors’ financial risk tolerance. Cogent Economics & Finance, 8(1), 1794493. https://doi.org/10.1080/23322039.2020.1794493

- Levy, M., & Benita, G. (2009). Are equally likely outcomes perceived as equally likely? Journal of Behavioral Finance, 10(3), 128–137. https://doi.org/10.1080/15427560903146641

- Mitchell, V.-W. (1999). Consumer perceived risk: Conceptualisations and models. European Journal of Marketing, 33(1/2), 163–195. https://doi.org/10.1108/03090569910249229

- Mohieldin, M. S., & Wright, P. W. (2000). Formal and informal credit markets in Egypt. Economic Development and Cultural Change, 48(3), 657–670. https://doi.org/10.1086/452614

- Moueed, A., & Hunjra, A. I. (2020). Use anger to guide your stock market decision-making: Results from Pakistan. Cogent Economics & Finance, 8(1), 1733279. https://doi.org/10.1080/23322039.2020.1733279

- Nguyen, V. C., & Berg, V. D. M. (2014). Informal credit, usury, or support? A case study for Vietnam. The Developing Economies, 52(2), 154–178. https://doi.org/10.1111/deve.12042

- Nofsinger, J. R. (2008). The psychology of investing. 3rded. Pearson Prentice Hall.

- Peter, J. P., & Tarpey, L. XsSr. (1975). A comparative analysis of three consumer decision strategies. Journal of Consumer Research, 2(1), 29–37. https://doi.org/10.1086/208613

- Phung, T. M. T., & Mai, N. K. (2017). Personality traits, perceived risk, uncertainty, and investment performance in Vietnam. Global Business and Finance Review, 22(1), 67–79. http://dx.doi.org/10.17549/gbfr.2017.22.1.67

- Phung, T. M. T., & Nguyen, H. T. (2017). Perceived risk, investment performance and intentions in emerging stock markets. International Journal of Economics and Financial Issues, 7(1), 269–278. http://dergipark.gov.tr/ijefi/issue/32002/353185

- Phung, T. M. T., Tran, Q. N., Nguyen, N. H., & Nguyen, T. H. (2021). Financial decision-making power and risk taking. Economics Letters, 206, 1–5. https://doi.org/10.1016/j.econlet.2021.109999

- Schneier, B. (2006). Beyond fear: Thinking sensibly about security in an uncertain world. Springer Science & Business Media.

- Shefrin, H. (2001). Do investors expect higher returns from safer stocks than from riskier stocks? The Journal of Psychology and Financial Markets, 2(4), 176–181. https://doi.org/10.1207/S15327760JPFM0204_1

- Shefrin, H. (2005). A behavioral approach to asset pricing. Elsevier Academic.

- Thaler, R. H., & Johnson, E. J. (1990). Gambling with the house money and trying to break even: The effects of prior outcomes on risky choice. Management Science, 36(6), 643–660. https://doi.org/10.1287/mnsc.36.6.643

- Turvey, C. G., & Kong, R. (2010). Informal lending amongst friends and relatives: Can microcredit compete in rural China? China Economic Review, 21(4), 544–556. https://doi.org/10.1016/j.chieco.2010.05.001

- Wang, M., Keller, C., & Siegrist, M. (2011). The less you know, the more you are afraid of—A survey on risk perceptions of investment products. Journal of Behavioral Finance, 12(1), 9–19. https://doi.org/10.1080/15427560.2011.548760

- Weber, E. U., Blais, A. R., & Betz, N. E. (2002). A domain‐specific risk‐attitude scale: Measuring risk perceptions and risk behaviors. Journal of Behavioral Decision Making, 15(4), 263–290. https://doi.org/10.1002/bdm.414

- Wu, J., Si, S., & Wu, X. (2016). Entrepreneurial finance and innovation: Informal debt as an empirical case. Strategic Entrepreneurship Journal, 10(3), 257–273. https://doi.org/10.1002/sej.1214

Appendix

I/Informal debt

Thinking about the total money used for stock investment, how would you divide this amount between borrowing and your own money?

II/Perceived risk

(1: not at all concerned/important, 2: slightly concerned/important, 3: somewhat concerned/important, 4: moderately concerned/important, 5: extremely concerned/important).

III/ Informal borrowing sources

Family borrowing sources

Thinking about borrowing from family sources such as parents, a spouse, sisters, brothers, relatives, to invest in shares, which of the following do you borrow from? (You can choose more than one answer):

□ 1. Parents.

□ 2. Grandparents.

□ 3. Brothers/sisters.

□ 4. Parents in law.

□ 5. Brothers/sisters in law.

□ 6. Cousins/nieces/nephews.

□ 7. Husband/wife.

□ 8. Other family sources

□ 9. I do not borrow from any family sources.

Nonfamily borrowing sources

Borrowing from nonfamily sources such as friends, teachers, coworkers, which do you borrow from? (You can choose more than one answer):

□ 1. Friends

□ 2. Girlfriends/boyfriends/partners

□ 3. Teachers/lecturers

□ 4. Colleagues/coworkers

□ 5. Bosses/managers

□ 6. Business partners

□ 7. Neighbours

□ 8. Other nonfamily sources

□ 9. I do not borrow from any nonfamily sources.