?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Central Bank Digital Currencies (CBDCs) enable negative interest rates. A game is analyzed between a central bank (accounting for the government’s interest) and a representative household choosing to consume, hold CBDC, or hold non-CBDC. The central bank chooses negative interest rate when it realizes that the household is willing to pay the central bank for holding CBDC. The household pays the negative interest rate because of its Cobb Douglas preferences whereby it values holding CBDC while simultaneously holding the competitive non-CBDC with a given interest rate, consuming with various output elasticities, and accounting for transaction efficiencies and costs. More explicitly, intuition and how the players benefit are provided for the following results: The central bank chooses more negative interest rate when the household’s output elasticity for consumption increases, the household’s output elasticity for holding CBDC decreases, the CBDC and non-CBDC transaction efficiencies increase, the household’s transaction efficiency for consumption decreases, the household’s scaling of the transaction cost increases, the scaling parameter for the central bank’s profit per household decreases, the household’s monetary energy decreases, and the non-CBDC interest rate decreases. The results are determined analytically and illustrated numerically where each of nine parameter values is varied relative to a benchmark.

1. Introduction

1.1. Background

The digitization of currency revolutionizes mankind’s use of currencies. Increasingly many central banks research Central Bank Digital Currencies (CBDCs), or have progressed to proof of concept or pilots, or have launched CBDCs (https://cbdctracker.org/). Commonly stated reasons are to promote financial inclusion and simplify the implementation of monetary and fiscal policy. CBDC developments are enabled and incentivized by new technological opportunities, potentially or partly as a countermovement, competitor or alternative to cryptocurrencies controlled by algorithms or actors (https://coinmarketcap.com). One early and essential cryptocurrency is Nakamoto’s (Citation2008) “proof of work” blockchain based electronic cash system labeled Bitcoin.Footnote1 Whereas CBDCs are digital currencies developed by central banks (which are centralized authorities), cryptocurrencies are digital currencies where transactions are recorded and verified through cryptography by a decentralized system. Less common cash usage incentivizes central banks to popularize more acceptable and easily applicable electronic currencies. Some central banks and their associated governments may prefer CBDCs designed to record and possibly control households’ transactions. In recent years credit and debit cards, wire transfers and various other forms of payments have gradually replaced cash. CBDCs may continue such replacements of cash. A survey by the Bank for International Settlements shows that currently, central banks representing a fifth of the world’s population are likely to issue a general purpose CBDC in the next three years (Boar & Wehrli, Citation2021). Households in countries adopting CBDCs as legal tender, and prohibiting all alternatives as legal tender, are forced to adopt their country’s CBDC (unless they can function through commodity exchange). Countries can more commonly be expected to accept alternatives to CBDCs so that households can choose among alternatives. 10 July 2022, 20,172 cryptocurrencies contribute to a market cap of $931 billion.Footnote2 The crypto fields of decentralized finance (DeFi) and non-fungible Tokens (NFT) develop rapidly.

Digital currencies give rise to new possibilities, including differences across currencies regarding transaction efficiencies, convenience, universal accessibility, confidentiality, financial stability, monetary policy, security, privacy, etc. Meanwhile, it also brings various challenges such as new infrastructures, new household behaviors, potentially more efficient and flexible monetary policies, and new functions or disintermediation for banks. Specifically, CBDCs enable central banks to implement negative interests.

Traditionally, the zero-lower bound on interest rate has been a challenge for central banks with paper money. The reasons are multifarious, i.e. the store of value of money requires a non-negative return, potentially adverse implications for bank profitability, and a potentially weak monetary transmission mechanism as the interest rate decreases towards zero.Footnote3 Under various accommodative policy regimes, various regions and countries such as the Euro area, Denmark, Sweden, Japan, and Switzerland have implemented negative interest rates.

1.2. Contribution

This article develops a game model between a representative household and a central bank which includes the government’s interest. This approach grounded in game theory, which has earned 18 Nobel prizes from 1970 to 2017, constitutes the theoretical underpinning of the study. The household converts its resources or monetary energy strategically into consumption, holding of CBDC issued by the central bank with a given interest rate, and holding of non-CBDC which earns an interest rate and can be any asset not issued by and not controlled by a central bank. Each household’s allocation highlights the potential relation between CBDC and non-CBDC, and furthermore the relation to consumption. Each household’s allocation impacts the central bank’s monetary policy, which in turn may impact how non-CBDCs evolve. The central bank chooses the CBDC interest rate, which can be negative or positive. The household has a Cobb Douglas utility with three elasticities, accounting for its strategic choices. The central bank identifies partly with each household, but additionally pays interest to each household when it is positive.

The emergence of digital currencies (CBDCs or non-CBDC) makes it easier to implement negative interest rates, which incentivize consumption rather than saving. CBDC holders subject to negative interest rates are easily subtracted what they owe on the ledger, whereas holders of physical cash not recorded on a ledger must actively provide through some channel cash they possess as interest payment. When a household experiences a negative interest rate, it pays a storage charge instead of earning positive interest. A central bank may have multiple reasons for choosing negative interest rates, e.g., to avoid recession, stimulate economic activity, and avoid deflation. An actor controlling a non-CBDC may choose negative interest rates for similar reasons, and to compete with CBDCs.

This article’s research question and objective are to determine how a household earns utility and allocates monetary energy between consumption, holding CBDC and holding non-CBDC depending on the interest rate of CBDC chosen by the central bank and the non-CBDC interest rate (both of which may be positive or negative), and depending on various preferences, transaction efficiencies and other factors.

The household’s utility accounts for consumption, CBDC and non-CBDC having different transaction efficiencies. A transaction efficiency function is presented which increases with holding CBDC and non-CBDC, and decreases with consumption. The model illustrates how different transaction efficiencies and interest rates of CBDC and non-CBDC impact the players’ strategic choices.

The impact of nine parameters is analyzed analytically and numerically. These are the household’s monetary energy; output elasticities for consumption and CBDC (which implicitly determines the elasticity for non-CBDC); and transaction efficiencies for CBDC, non-CBDC and consumption; the scaling of the household’s transaction cost; the scaling of the central bank’s profit, and the non-CBDC interest rate. These parameters are interesting to study since they impact the players’ strategies, utility and profit. Each parameter has an independent impact on the model, which is essential since it enables identifying which specific ingredients of the model has which specific impact. Numerical analysis illustrates variation of each parameter value relative to a benchmark. The article contributes to all the four areas of the literature reviewed in the next section.

1.3. Literature

The literature is divided into four groups, i.e., CBDC design and economy; game theoretic analyses; negative interest rates; and CBDC, monetary policy and policy implications. These four groups are interconnected and relevant as follows. Since the central bank is one of the two players in the article, the first group is about CBDC design and the economy, which provides a foundation for the central bank as a player and crucially impacts how the central bank operates. The second group, naturally, is game theoretic analysis, to illustrate the linkage to the current article which applies game theory as a tool. The third group is about negative interest rates, which some central banks have already started to explore. CBDCs contain the unique feature of being technologically able to implement negative interest rates, which may potentially become important in the future. The fourth group is CBDC, monetary policy and policy implications, which extends from the other three groups into the real economy through policy implications.

1.3.1. CBDC design and economy

Kiff et al. (Citation2020) explore the issuance considerations of retail CBDC which the general public has access to it. They review CBDC research, and summarize the operating models, design considerations and risk management of issuing CBDC. Similarly, Allen et al. (Citation2020) show that CBDC brings a range of new possibilities, but also causes many challenges. They investigate the technical challenges facing CBDC designers, focusing on performance, privacy, and security. They summarize the main potential benefits of CBDC, i.e. efficiency, a broader tax base, flexible monetary policy, payment backstop, and financial inclusion. Ozili (Citation2022) reviews the literature, points out that the motivation of a CBDC is to improve the monetary policy, enhance digital payment efficiency, and increase financial inclusion. He points out limitations of CBDC design, and challenges in meeting multiple competing goals. He finds that a CBDC has cash-like attributes and is a liability of the issuing central bank. Carapella and Flemming (Citation2020) also review the literature, and assess how CBDCs impact commercial banks, monetary policy and financial stability. Oh and Zhang (Citation2020) analyze a CBDC in a two-sector monetary model with a formal and an informal economy. They show that tax reduction and a positive CBDC interest rate are useful to enhance CBDC adoption and improve its effectiveness. This article contributes to this literature by considering how a representative household chooses strategies impacted by the CBDC interest rate, impacted by the non-CBDC interest rate, consumption and various transaction efficiencies.

1.3.2. Game theoretic analyses

This article contributes to this literature by considering a game between the central bank choosing the CBDC interest rate and a representative household choosing consumption, holding CBDC and holding non-CBDC. Wijsman (Citation2021) analyzes households which can earn positive or negative interest rate at one bank, can switch to another bank subject to switching costs, or can invest alternatively. His approach relates to the current article where households also have two possibilities for saving (CBDC and non-CBDC), and have an alternative which is consumption instead of investment. His switching costs have some linkage to transaction costs in the current article. Wijsman (Citation2021) finds that banks may decrease their interest rates if switching costs are higher and alternative household investments are less attractive. He also finds that high switching costs prevent banks from attracting savers from competitors, and less attractive alternatives for households may cause expensive wars of attrition between banks.

Wang and Hausken (Citation2021) consider a game between a representative household choosing to hold a national currency and a global currency, and a government choosing how to tax the two currencies, and how to detect, prosecute and impose penalties for tax evasion. Jia (Citation2020) develops an overlapping generations model to explore the macroeconomic impact of negative interest rates on CBDC. He finds that a negative CBDC interest rate induces agents to save less and consume more, which in turn leads to a decrease in capital investment and output. This article presents related results for how a household saves CBDC or non-CBDC with negative CBDC interest rates. George et al. (Citation2020) evaluate the macroeconomic implications of a CBDC with an adjustable interest rate. They extend the analysis to an open-economy context with foreign capital flows. The study shows that a CBDC with an adjustable interest rate is welfare-improving, and that a quantity rule delivers the best welfare outcome for society.

Welburn and Hausken (Citation2015, Citation2017) adopt game theory to explore economic crises. They analyze six kinds of players, i.e., countries, central banks, banks, firms, households, and financial inter-governmental organizations. Players have various strategies such as setting interest rates, lending, borrowing, producing, consuming, investing, defaulting, etc. This article considers only two players, i.e. a representative household and the central bank, with specific strategies and utilities for each.

1.3.3. Negative interest rates

This article contributes to this literature by considering how a central bank may choose a negative interest rate impacting, and being impacted by a representative household’s consumption, holding of CBDC and non-CBDC, and transaction efficiencies. Davoodalhosseini et al. (Citation2020) argue that an interest-bearing CBDC could be a versatile instrument, which may enhance monetary policy theatrically, i.e., break below the effective lower bound of interest rates, enable non-linear transfer, reduce incentives to adopt alternative means of payments, etc. But in practice the expected benefits might be small. Partly related, the current article shows how an interest-bearing CBDC can operate in conjunction with an interest-bearing non-CBDC for a household which also consumes.

Rognlie (Citation2016) explores monetary policy with negative interest rates. He finds that gains from negative interest rates depend inversely on the level and elasticity of currency demand, that negative interest rates stabilize aggregate demand, but inefficiently subsidize the paper currency.

Altavilla et al. (Citation2019) apply confidential data from the euro area to show that well-performed banks can pass negative rates on to their corporate depositors without experiencing decreased funding. Additionally, a negative interest rate policy can provide further stimulus to the economy via firms’ asset rebalancing. The findings challenge the view that conventional monetary policy becomes ineffective when policy rates reach the zero-lower bound.

Assenmacher and Krogstrup (Citation2018) think that cash prevents central banks from cutting interest rates much below zero. They analyze the practical feasibility of adopting electronic money, which could remove the lower bound constraint on monetary policy. The result is feasible electronic money fully restoring the monetary policy space with negative interest rates.

Grasselli and Lipton (Citation2019) point out that CBDC can overcome the lower bound for interest rates imposed by physical cash. They construct a stock-flow macroeconomic model to investigate the theoretical effectiveness of negative interest rates. They find that negative interest rates can be an effective tool for macroeconomic stabilization.

David-Pur et al. (Citation2020) provide experimental evidence on how zero and negative interest rates impact investments. They show that a zero-interest rate is more efficient than a negative interest rate in terms of the impact on people’s willingness to borrow money and take risks. But there is no impact of the difference between a positive and a negative interest rate on the change in the allocation of risky assets in investment portfolios.

1.3.4. CBDC, monetary policy and policy implications

This article contributes to this literature by allowing positive and negative CBDC interest rates. Bordo and Levin (Citation2017) analyze how digital cash enhances the effectiveness of monetary policy. They argue that a CBDC may potentially facilitate many aspects of monetary policy, thus potentially improving the stability of the financial system. Asimakopoulos et al. (Citation2019) set up a dynamic stochastic general equilibrium model to evaluate the economic consequences of cryptocurrencies. Using US and crypto markets monthly data for the period 2013:M6-2019:M3, a substitution effect is found between the real balances of government currency and cryptocurrency.

Beniak (Citation2019) explores hypothetical challenges of CBDC implementation for monetary policy, and the impact on the broader economy. Based on an overview of the literature, he concludes that CBDC impacts central bank interest rates, monetary policy implementation and the transmission mechanism. The scale of these effects depends on the design and demand for this new form of money.

Kim and Kwon (Citation2019) apply a monetary general equilibrium model to explore the implications of CBDC on financial stability. The study shows that deposits in CBDC accounts decrease the supply of private credit by commercial banks, which has a negative effect on financial stability via increasing the likelihood of a bank panic. However, once the central bank can lend all the deposits in CBDC account to commercial banks, an increase in the quantity of CBDC can enhance financial stability.

Bindseil (Citation2020) reviews the CBDC advantages, i.e. efficient payments, anti-illegal activities, strengthened monetary policy (negative interest rates are possible), higher seigniories income, etc. Possible risks are structural disintermediation of banks, systemic runs on banks, centralization of the credit allocation process within the central bank, etc. They propose a two-tier remuneration of CBDC as a solution.

Bindseil and Fabio (Citation2020) point out that a two-tier remuneration system for the CBDC would be an efficient solution to issues like bank disintermediation, negative interest rate policy, financial stability, etc. A tiered remuneration of CBDC would achieve four key objectives, namely, offering attractive CBDC as a means of payment to households, offering CBDC in a quantitatively unconstrained manner to any holder (not just citizens), controlling the risks of structural or cyclical bank disintermediation, and enabling negative interest rates.

2. The model

A non-cooperative static simultaneous-move one-period game is played between a representative household and a unitary player comprising the interests and capabilities of a central bank and a government, referred to as the central bank, for simplicity. The household and central bank choose their strategies simultaneously and independently. The static analysis is assumed to represent a stationary situation through time where the players adapt optimally to each other in a manner that can be expressed at one point in time. The stationary situation implicitly accounts for the nature of interest rates where resources usually have to be held for a certain amount of time in order for interest to be earned. Mathematically this amount of time can be made arbitrarily small. Hence, in a stationary situation, interest can be assumed earned at the same point in time in which the players choose their strategies and earn their utilities. Appendix A shows the nomenclature.

2.1. The household’s strategic choices and utility

The representative household has available monetary energy , which also can be interpreted as resources, converted at unit cost 1 into consumption

, CBDC (Central Bank Digital Currency)

, and some non-CBDC

, i.e.

where are scaled equivalently on some appropriate scale, which may be any scale, e.g., of monetary nature. Hence, since

are scaled equivalently in (1), we assume no coefficients before

, which means that the coefficients equal 1. EquationEquation (1)

(1)

(1) means that the household accepts and adopts both CBDC

and non-CBDC

. The household demands optimal amounts of CBDC

and non-CBDC

, and weighs these demands against its consumption

to maximize its utility

developed below.

A CBDC is in this model interpreted as any currency issued by the central bank with an interest rate

,

, where

is the set of all real numbers, which includes e.g., the Chinese e-CNY. A non-CBDC

is interpreted as any asset earning an interest rate

,

, and which is not issued by and not controlled by a central bank. We may think of the non-CBDC

as a cryptocurrency such as Bitcoin. Both interest rates

and

can be positive or negative. That means that the non-CBDC

can earn a higher or lower interest rate than the CBDC

, as illustrated e.g., in Figure panel i. The broad definitions of CBDC

and non-CBDC

in (Equation1

(1)

(1) ) work fine for the purpose of this article, where the household allocates its monetary energy

into the three destinations consumption

, CBDC

with interest rate

, and some non-CBDC

with interest rate

.

Figure 1. The household’s consumption , holding of CBDC

, holding of non-CBDC

, and utility

, and the central bank’s interest rate

and profit

, as functions of the nine parameter values

relative to the benchmark parameter values

. Division of

with 5 and

with 3 is for scaling purposes.

We develop the household’s Cobb Douglas utility in four steps. First, the household has a Cobb Douglas utility with three output elasticities ,

,

,

, for consumption

, CBDC

, and some non-CBDC

, i.e.

which expresses constant returns to scale, since the three exponents sum to 1. Second, the household earns interest ,

, on CBDC

, and earns interest

,

, on the non-CBDC

. Interest rates are usually positive, but can for digital currencies, and especially for CBDC

, be negative. Earning interest rates

and

on CBDC

and non-CBDC

means multiplying

and

with

and

, respectively. Incorporating these multiplications into (Equation2

(2)

(2) ) gives

Third, a simultaneous-move game is analyzed which can be interpreted as a stationary situation where time plays no role. EquationEquation (1)(1)

(1) is interpreted so that the household converts its resources r into consumption

, CBDC

, and non-CBDC

. This conversion involves transaction costs which impacts the household’s utility. In order to transact between consumption

, CBDC

, and non-CBDC

, the household seeks to obtain high transaction efficiency, which means that it has to pay transaction costs. Transactions are never free. Costs are always involved when transacting. With other conditions unchanged, a high transaction efficiency means a lower transaction cost. We define the household’s transaction efficiency

to increase with holding CBDC

and holding non-CBDC

, and decrease with consumption

, i.e.

where ,

, is the household’s transaction efficiency for CBDC

;

,

, is the household’s transaction efficiency for non-CBDC

. The parameter

is the household’s transaction efficiency for consumption

, and

, scales the degree or level of the household’s transaction efficiency. We require

so that the household benefits positively from consumption, expressed as

in (Equation3

(3)

(3) ), despite the transaction cost

in (Equation4

(4)

(4) ). We also assume

, so that the household’s transaction efficiency

for non-CBDC

is higher than or equal to the household’s transaction efficiency

for consumption

.

The transaction efficiency E in (4) satisfies

, see Appendix B. Thus

decreases convexly in consumption

, and increases in the CBDC

and the non-CBDC

. For related accounts of the transaction efficiency

, usually conceptualized as the transaction cost

, see, Feenstra (Citation1986), Bougheas (Citation1994), and Saygılı (Citation2012).

The literature usually considers the inverse of (Equation4

(4)

(4) ) interpreted as the transaction cost, where

scales the transaction cost. Higher transaction efficiency for CBDC

than for non-CBDC

, to sustain negative interest rates

on CBDC

, requires

, which we generally do not require since we in principle can envision even more negative interest rates

for non-CBDC

. Multiplying (Equation4

(4)

(4) ) with (Equation3

(3)

(3) ) gives the household’s utility

Fourth, the household’s resource constraint in (Equation1(1)

(1) ) expresses that the household has two free choice variables, i.e. consumption

and CBDC

, where non-CBDC

follows from solving (Equation1

(1)

(1) ) with respect to

. Inserting

into (Equation5

(5)

(5) ) gives

which has two strategic choice variables and

, and which is the household’s utility

which we analyze in the remainder of the article.

2.2. The central bank’s strategic choice and profit

We consider the central bank and the government as one unitary player, referred to as the central bank for simplicity, with the ability to choose the CBDC interest rate ,

. Common objectives for central banks usually include financial stability including price stability, and controlling inflation, unemployment, interest rates, or exchange rates. To obtain these objectives central banks are often assumed to choose discretionary policies. Some literature, e.g., Taylor (Citation1993), assumes that central banks follow certain rules, without evidence of specific rules actually being applied. One may hypothesize that central banks follow certain norms, e.g., as philosophically expounded by Kant (Citation1785) for which evidence is also not apparent. Given the common presence of maximizing behavior for players tasked with reaching objectives, this article assumes that also the central bank maximizes to reach its stated objectives. Although the literature agrees that central banks have objectives, the literature does not agree on what central banks actually maximize to reach these objectives. One might assume that central banks minimize deviations from specified targets related to financial stability including price stability, inflation, unemployment, interest rates, or exchange rates. One problem with that approach is that it is not directly linked to what each household may perceive as its objectives. Each household may not agree with the specified targets, may not agree with which of the many objectives the central bank seeks to reach, or may consider the central bank’s objectives as too abstract. As outlined in the previous section 2.1, each household may find it easier to focus more concretely on its resource allocation into consumption, holding CBDC and holding non-CBDC, instead of somehow conceptualizing the general price level or some of the other central bank’s objectives. To formalize how the central bank maximizes to reach objectives, this article assumes that the central bank identifies partly with each household, with the utility in (Equation6

(6)

(6) ). That assumption is made by reasoning that the central bank’s wide-ranging objectives listed above are compatible with creating an environment within which each household can flourish in the sense of maximizing its utility. That the central bank’s profit per household function is linear in the household’s utility is assumed to be a suitable first approximation. Future research may explore whether various kinds of nonlinear relationships may be appropriate. Additionally, the central bank pays interest

to each household, which is subtracted from (Equation6

(6)

(6) ) to yield the central bank’s profit per household

where the parameter ,

, is multiplied with the first term for scaling purposes. That is, the subtracted term

is measured along some monetary scale, and

enables the first term to be measured along the same monetary scale, and hence we refer to

as profit. EquationEquation (7)

(7)

(7) expresses that the central bank identifies partly with each household, weighted with the parameter

, and subtracting the interest

paid to each household.

2.3. Methodology

The article applies non-cooperative game theory (Fujiwara-Greve, Citation2015; Von Neumann & Morgenstern, Citation1944) assuming two players, i.e. a representative household and a central bank. Each player is fully rational and has complete information about the game and all parameter values. The players choose their strategies simultaneously and independently to maximize their utilities. For the household the utility is a Cobb Douglas utility multiplied with a transaction efficiency . For the central bank the utility is a profit function defined as a benefit minus a cost

. Both players’ utilities depend on the two players’ three strategic choice variables

,

and

. The game is a so-called variable sum game which means that the sum of the players’ utilities depend on their strategies. The game’s solution amounts to determining a Nash equilibrium Nash (Citation1951) from which no player prefers to deviate unilaterally when choosing its strategy.

3. Analyzing the model

3.1. Analyzing the household

Lemma 1. The household’s consumption , holding of CBDC

, and holding of non-CBDC

are

with characteristics shown in and discussed after the Proposition.

Proof. Appendix C.

3.2. Analyzing the central bank

Lemma 2. The central bank’s CBDC interest rate for the household’s holding of CBDC

is

with characteristics shown in and discussed after the Proposition.

Proof. Appendix D.

3.3. Analyzing the household and the central bank

Lemma 3. The household’s utility and the central bank’s profit per household

are

with characteristics shown in and discussed after the Proposition.

Proof. Follows from inserting (Equation8(8)

(8) ) and (Equation9

(9)

(9) ) into (Equation6

(6)

(6) ) and (Equation7

(7)

(7) ).

Proposition

Proof. Follows from (Equation22(23)

(23) ), (Equation23

(24)

(24) ), (Equation24

(25)

(25) ), (25) in Appendix E, where

implies

since

.

The Proposition states, first, that the household’s consumption , holding of CBDC

, and holding of non-CBDC

, increases, is independent, and decreases in its output elasticity

for consumption

. That is, as consumption becomes more important, the household consumes more and holds less non-CBDC

. When

, which is satisfied when

is not too high, increasing

causes the central bank to decrease its interest rate

, which is consistent with higher consumption

, and causes lower household’s utility

, consistently with the lower interest rate

.

Second, the household’s consumption , holding of CBDC

, and holding of non-CBDC

, is independent, increases, and decreases in its output elasticity

for holding CBDC

. That is, as holding CBDC

becomes more important, the household holds more CBDC

, and holds less non-CBDC

.

Third, the household’s consumption , holding of CBDC

, and holding of non-CBDC

, decreases convexly, increases concavely, and decreases convexly, in its transaction efficiency

for CBDC

. That is, as CBDC

transactions become more efficient, the household holds more CBDC

, consumes less, and holds less non-CBDC

.

Fourth, the household’s consumption , holding of CBDC

, and holding of non-CBDC

, decreases convexly, decreases convexly, and increases concavely, in its transaction efficiency

for non-CBDC

. That is, as non-CBDC transactions become more efficient, the household holds more non-CBDC

, consumes less, and holds less CBDC

.

Fifth, the household’s consumption , holding of CBDC

, and holding of non-CBDC

, decreases concavely, increases convexly, and increases convexly, in its transaction efficiency

for consumption

. That is, as consumption

transactions become more efficient, which in (Equation6

(6)

(6) ) implies less weight to consumption

due to the term

, the household consumes less, and holds more CBDC

and more non-CBDC

.

Sixth, the household’s consumption , holding of CBDC

, and holding of non-CBDC

, are independent of the household’s scaling

of the transaction cost. The central bank’s interest rate

and the household’s utility

decrease convexly in

. That is, higher transaction cost

is costly for the household. That cost is to some extent experienced by the central bank in (Equation7

(7)

(7) ) which compensates by choosing lower interest rate

which makes the second cost term

lower in absolute value, and positive if the interest rate

is negative.

Seventh, the household’s consumption , holding of CBDC

, and holding of non-CBDC

, are independent of the scaling parameter

for the central bank’s profit. The central bank’s interest rate

increases convexly in

, which according to (Equation7

(7)

(7) ) enables the central bank to profit substantially. The household’s utility

increases concavely in

when

, and otherwise increases convexly, as the household benefits from the higher interest rate

.

Eighth, the household’s consumption , holding of CBDC

, and holding of non-CBDC

, increase linearly in the household’s monetary energy, or resources,

. When

, the central bank’s interest rate

increases in

, as the central bank identifies partly with the household’s utility in (Equation6

(6)

(6) ), and pays higher interest rate

on the household’s increased holding of CBDC

. When

, the household’s utility

increases in

, as the household benefits from the higher interest rate

on its increased holding of CBDC

.

Ninth, the household’s consumption , holding of CBDC

, and holding of non-CBDC

, are independent of the non-CBDC’s interest rate

. The central bank’s interest rate

and the household’s utility

increase concavely in

. That is, the household benefits from the higher interest rate

on its holding of non-CBDC

, which induces the central bank competitively to increase its interest rate

to prevent the household from changing its holding from CBDC

to non-CBDC

.

summarizes the main results in the Proposition with an upward arrow , sideways arrow

, or downward arrow

, respectively, depending on whether the first order derivative (listed first) and second order derivative (listed second) are positive, zero or negative. The derivatives are for the variable in the row with respect to the parameter in the column. Empty cells means that the signs of the derivatives contain if-conditions as expressed in the Proposition and Appendix E. Only one sideways arrow

is listed if the first order derivative and all higher order derivatives equal zero. Only the upward arrow

is listed for

since

.

Table 1. Upward arrow , sideways arrow

, or downward arrow

, respectively, depending on whether the first order derivative (listed first) and second order derivative (listed second) in the proposition are positive, zero or negative. The derivatives are for the variable in the row with respect to the parameter in the column.

4. Illustrating the solution

To illustrate the solution in section 3, this section alters the nine parameter values relative to the benchmark parameter values

. First,

expresses relatively low weight or elasticity for consumption

. Second,

reflects equal and higher weight or elasticity for CBDC

and non-CBDC

. Third,

reflects intermediate transaction efficiency for non-CBDC

. Fourth,

reflects twice as high transaction efficiency for CBDC

. Fifth,

reflects low transaction efficiency for consumption

. Sixth,

expresses zero interest rate for non-CBDC

, as a plausible benchmark relative to which the CBDC interest rate

may be higher or lower. Seventh,

is chosen so that the CBDC interest rate

at the benchmark. Eighth,

are chosen due to simplicity and since the value 1 seems plausible when no other value may appear more plausible. With these benchmark parameter values the benchmark solution is

. In Figure each of the nine parameter values is altered from its benchmark, while the other eight parameter values are kept at their benchmarks. Division of

with 5 and

with 3 is for scaling purposes.

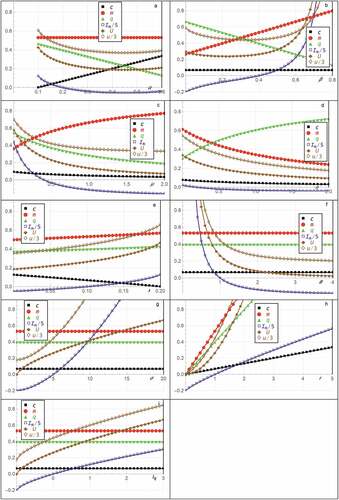

In Figure , as the household’s output elasticity for consumption

increases, its consumption

, holding of CBDC

, and holding of non-CBDC

, increases, is independent, and decreases. When

is high, the household values consumption

more and non-CBDC

less. Except when

is very high, as

increases, the central bank’s interest rate

decreases and becomes negative when

. Furthermore, the household’s utility

decreases since it earns less interest on its holding of CBDC

, and the central bank’s profit per household

decreases since it identifies partly with the household as expressed in (Equation7

(7)

(7) ) compared with (Equation6

(6)

(6) ).

In Figure , as the household’s output elasticity for CBDC

increases, its consumption

, holding of CBDC

, and holding of non-CBDC

, is independent, increases, and decreases. When

is high, the household values CBDC

more and non-CBDC

less. Valuing CBDC

more is consistent with higher CBDC interest rate

, which eventually causes higher household’s utility

and higher central bank’s profit per household

.

In Figure as the household’s output transaction efficiency for CBDC

increases, its consumption

, holding of CBDC

, and holding of non-CBDC

, decreases convexly, increases concavely, and decreases convexly. More efficient CBDC

transactions cause the household to hold more CBDC

, consume less, and hold less non-CBDC

. That the household holds more CBDC

is costly for the central bank, as expressed with

in (Equation7

(7)

(7) ), which is negative when

. Hence, as

increases, the central bank decreases its interest rate

which eventually becomes negative. That’s costly for the household which receives decreasing utility

, and costly for the central bank which identifies partly with the household and receives decreasing profit

.

In Figure , as the household’s transaction efficiency for non-CBDC

increases, its consumption

, holding of CBDC

, and holding of non-CBDC

, decreases convexly, decreases convexly, and increases concavely. More efficient non-CBDC

transactions cause the household to hold less CBDC

, consume less, and hold more non-CBDC

. With the specified parameter values, that causes the central bank to decrease its interest rate

marginally, causing the household’s utility

and the central bank’s profit per household

to decrease.

In Figure , as the household’s transaction efficiency for consumption

increases, its consumption

, holding of CBDC

, and holding of non-CBDC

, decreases concavely, increases convexly, and increases convexly. More efficient consumption

transactions enable the household to hold more CBDC

and more non-CBDC

, and consume less. The central bank responds by increasing its CBDC interest rate

, which causes higher household’s utility

and higher central bank’s profit per household

.

In Figure , as the household’s scaling of the transaction cost increases, its consumption

, holding of CBDC

, and holding of non-CBDC

, do not change. The higher cost

has to be born by someone, so the central bank decreases its interest rate

which becomes negative, and the household’s utility

and the central bank’s profit per household

decrease.

In Figure , as the scaling parameter for the central bank’s profit per household increases, the household’s consumption

, holding of CBDC

, and holding of non-CBDC

, do not change. In contrast to higher

which is a cost, higher

is a benefit, and thus the central bank increases its interest rate

, and the household’s utility

and the central bank’s profit per household

increase.

In Figure , as the household’s monetary energy, or resources, , increases, its consumption

, holding of CBDC

, and holding of non-CBDC

, increase. That’s beneficial for both players causing the central bank’s interest rate

and profit

, and the household’s utility

, to increase.

In Figure , as the non-CBDC interest rate increases, the household’s consumption

, holding of CBDC

, and holding of non-CBDC

, do not change. Higher

causes the central bank to increase its CBDC interest rate

, which causes the central bank’s interest rate

and profit

, and the household’s utility

, to increase.

5. Discussion, economic intuition and policy implications

Nine results in the previous section are noteworthy. First, as the household’s output elasticity for consumption increases, it consumes more, holds the same amount of CBDC

, and holds less non-CBDC

. Except when

is high, the central bank’s interest rate

and the players’ utility

and profit

decrease. The intuition is that higher household consumption causes the household to decrease holding something. It chooses to hold less non-CBDC

. The central bank’s decreased benefit from the positive term in (Equation7

(7)

(7) ) induces it to strike a different tradeoff or balance between benefit and cost expressed with the negative term in (Equation7

(7)

(7) ), causing decreased and negative CBDC interest rate

. As

increases from the low value

, we get the conventional relationship where the household responds to decreasing CBDC interest rate

by consuming more. Interestingly, as

increases above

and the central bank’s interest rate

becomes negative, the household pays the central bank for holding its CBDC

. That is possible according to the Cobb Douglas logic in (Equation6

(6)

(6) ) since the household values holding CBDC

, despite having to pay for it, in combination with the other ingredients of (Equation6

(6)

(6) ). Naturally, a limit exists for how much the household is willing to pay the central bank. Hence the central bank’s negative interest rate

levels out and starts increasing from a minimum

when

. The increasing

in principle curtails the household’s consumption

, which nevertheless continues to increase since

as the household’s output elasticity

for consumption

constitutes a stronger force and has higher impact. The policy implication is that the household and central bank should be conscious about how they impact each other. Negative CBDC interest rate

can indeed be associated with increased consumption

. The central bank needs to assess the household’s Cobb Douglas preferences broadly within the economy, to determine how negative the CBDC interest rate

can be allowed to be.

Second, and as a contrast, as the household’s output elasticity for holding CBDC

increases, it holds more CBDC

and less non-CBDC

, the CBDC interest rate

increases, and the players’ utility

and profit

eventually increase. The intuition is that the household chooses to hold CBDC

or non-CBDC

depending on what it considers most valuable. Furthermore, if holding CBDC

is sufficiently valuable for the household, the central bank increases its interest rate

from negative to positive. The household benefits in terms of the interest payment. The central bank benefits due to identifying partly with the household, which offsets its cost of the interest payment to the household. The policy implication is to be conscious of how a household assesses the value of holding CBDC

relative to holding non-CBDC

, which impacts the household’s strategies choices and the CBDC interest rate

.

Third, the household’s consumption , holding of CBDC

, and holding of non-CBDC

, decreases, increases, and decreases, in its transaction efficiency

for CBDC

. The CBDC interest rate

decreases and becomes negative, and the players’ utility

and profit

decrease. The intuition is that more efficient CBDC

transactions encourage the household to consume less, hold more CBDC

, and hold less non-CBDC

. That the household holds more CBDC

is costly for the central bank unless it decreases its interest rate

to become negative so that it receives interest payment from the household for holding CBDC

. The household receives decreasing utility

due to paying increased interest rate to the central bank. The central bank receives decreased profit

due to identifying partly with the household. The policy implication is to realize the implications of increased CBDC transaction efficiency

, eventually causing negative CBDC interest rate

because of the household’s increased holding of CBDC

.

Fourth, the household’s consumption , holding of CBDC

, and holding of non-CBDC

, decreases, decreases, and increases, in its transaction efficiency

for non-CBDC

. The CBDC interest rate

decreases and becomes negative, and the players’ utility

and profit

decrease. The intuition is that more efficient non-CBDC

transactions encourage the household to consume less, hold less CBDC

, and hold more non-CBDC

. That’s costly for the central bank which has to pay more in interest to the household. These results are qualitatively in the same direction as for the third result when the transaction efficiency

for CBDC

increases, except that the household’s holding of CBDC

and holding of non-CBDC

, intuitively, move in the opposite direction. The explanation is that both the transaction efficiencies

and

appear in the numerator in (Equation4

(4)

(4) ), which both have the opposite impact compared with the impact of the household’s transaction efficiency

for consumption

, which appears in the denominator in (Equation4

(4)

(4) ). The policy implication is to realize the implications of increased non-CBDC transaction efficiency

, eventually causing negative CBDC interest rate

because of the household’s increased holding of non-CBDC

.

Fifth, as the household’s transaction efficiency for consumption

increases, its consumption

, holding of CBDC

, and holding of non-CBDC

, decreases, increases, and increases. The central bank increases its interest rate

, and the players’ utility

and profit

increase. The intuition is that more efficient consumption

transactions enable the household to consume less, and hold more CBDC

and more non-CBDC

. The central bank appreciates this decreased consumption and responds by increasing its CBDC interest rate

, which is the opposite of results 3 and 4 where the CBDC interest rate

decreases. The policy implication is to realize that increasing the household’s transaction efficiency

for consumption

eventually causes positive CBDC interest rate

, contrary to results 3 and 4 where increasing transaction efficiencies

and

for CBDC

and non-CBDC

eventually cause negative CBDC interest rate

.

Sixth, the CBDC interest rate and the players’ utility

and profit

decrease in the household’s scaling

of the transaction cost. The intuition is that a higher transaction cost

is expensive for the household, which is partly experienced by the central bank, and compensated by choosing lower and negative CBDC interest rate

. The policy implication is to be conscious about the scaling

of the household’s transaction cost, which dysfunctionally can cause negative CBDC interest rate

and low players’ utility

and profit

.

Seventh, and in contrast to the sixth result, the CBDC interest rate and the players’ utility

and profit

increase in the scaling parameter

for the central bank’s profit per household

. The intuition is that higher

benefits the central bank, enabling it to pay higher and eventually positive CBDC interest rate

to the household, incurred as a cost

in (Equation7

(7)

(7) ), which in turn benefits the central bank which identifies partly with the household. The policy implication is to realize which factors constitute a benefit for the central bank, which is weighed against the central bank’s potential cost of paying interest to the household for holding CBDC

.

Eighth, as the household’s monetary energy, or resources, , increases, the players’ three free choice variables

,

, and the three dependent variables

, increase. The intuition is that a more resourceful household can consume more and hold more CBDC

and more non-CBDC

, which benefits the household and the central bank which identifies partly with the household. This in turn enables the central bank to pay more interest to the household for holding CBDC

. The policy implication is to assess how each household can be made more resourceful, which causes all the variables to increase.

Ninth, the CBDC interest rate and the players’ utility

and profit

increase in the non-CBDC interest rate

. The intuition is that the central bank faces the competition from the higher non-CBDC interest rate

by increasing its own CBDC interest rate

. The household benefits from holding non-CBDC

due to the higher non-CBDC interest rate

, which causes the central bank to benefit due to identifying partly with the household. This in turn enables the central bank to pay higher CBDC interest rate

to ensure that the household keeps holding CBDC

. Hence a reinforcing virtuous circle (the opposite of a vicious circle) arises which benefits everyone. The policy implication is to realize the positive relationship between the CBDC interest rate

and the non-CBDC interest rate

.

6. Shortcomings and future research

Future research, which implicitly specifies shortcomings of the current research, should consider several CBDCs and non-CBDCs, including other assets such as bonds, stocks, etc. Additional players can be introduced, such as distinguishing between the central banks and governments, modeling commercial banks, firms, financial institutions, accounting for different kinds of households, etc. Alternative functional forms may be explored. Non-functional forms may also be explored, which may enable more generality, but fewer analytical solutions. Empirical evidence should be compiled for how households choose consumption, holding of CBDC and non-CBDC, with positive and negative CBDC interest rates. Households with different characteristics can be incorporated. The players may be assigned different risk attitudes. The players’ Cobb Douglas utilities may account for additional factors beyond transaction efficiency, such as privacy, convenience, security, taxes. The players’ strategy sets may be extended. For example, each potentially different household may be allowed to choose production and leisure in addition to consumption. The analysis may be generalized to account for more than one time period, and allow players to move in various sequences or simultaneously in repeated games. Digital currencies are a relatively new innovation with markets that may be subject to rapid price swings, fluctuations and uncertainty. The sensitivity analysis in the current article accounts for substantial variation in nine parameter values, which may change with arbitrary rapidity in the sense that the time dimension is not present in the current model. A dynamic analysis accounting for the time dimension may capture the implications over time of price swings, fluctuations, uncertainty, etc. from multiple angles.

7. Conclusion

This article presents a game model between a representative household and a central bank assumed to incorporate the interests of a government. The household has resources converted into consumption, holding of CBDC (Central Bank Digital Currency) controlled by a central bank, and holding of non-CBDC which can be any asset not issued by and not controlled by a central bank. The central bank determines its interest rate. The non-CBDC also has an interest rate. Both these two interest rates can be positive or negative. A Cobb Douglas utility with three elasticities for the household is developed, which represents consumption, holding of CBDC, and holding of non-CBDC. This conceptualization is assumed to be realistic for how households operate in the real world, i.e. choosing to consume while also choosing to hold two currencies with different interest rates and transaction efficiencies. The central bank identifies partly with each household, and pays interest to each household, which is subtracted to yield the central bank profit per household.

The article determines the household’s consumption and holding of CBDC and the central bank’s interest rate analytically, from which the dependent variables follow. Various interesting results follow. First, as the household’s output elasticity for consumption increases, it consumes more and holds less non-CBDC, while the CBDC interest rate decreases and becomes negative. The central bank eventually imposes negative CBDC interest rate on the household since it identifies partly with the household which substitutes from holding non-CBDC and into consumption.

Second, as the household’s output elasticity for holding CBDC increases, it holds more CBDC and less non-CBDC. Hence in contrast, the central bank eventually imposes positive CBDC interest rate on the household since it identifies partly with the household which substitutes from holding non-CBDC and into holding CBDC.

Third and fourth, the household’s consumption, holding of CBDC, and holding of non-CBDC, decreases, increases (decreases), and decreases (increases), in its transaction efficiency for CBDC (non-CBDC). Increasing both the CBDC and non-CBDC transaction efficiencies eventually induces the central bank to choose negative interest rate, since it otherwise either must pay the household too much in interest or must identify with the household’s decreased utility from consuming less and holding less CBDC.

Fifth, as the household’s transaction efficiency for consumption increases, it consumes less, and holds more CBDC and more non-CBDC. In contrast to the third and fourth results, that encourages the central bank to increase its interest rate which becomes positive. The central bank pays more interest to the household, but identifies with the household and benefits from the household’s benefit.

Sixth, the CBDC interest rate and the players’ utility and profit decrease in the household’s transaction cost, which is detrimental for both players, causing the central bank to burden the household with negative interest rates.

Seventh, and in contrast to the sixth result, the CBDC interest rate and the players’ utility and profit increase in the scaling parameter for the central bank’s profit, which benefits both players.

Eighth, as the household’s monetary energy, or resources, increases, the household consumes more and holds more CBDC and non-CBDC, and the central bank increases its interest rate.

Ninth, the CBDC interest rate and the players’ utility and profit increase in the non-CBDC interest rate. A higher non-CBDC interest rate induces the central bank competitively to increase the CBDC interest rate, to prevent the household from changing its holding from CBDC to non-CBDC.

The results are illustrated numerically, varying nine parameter values relative to a benchmark.

Authorship

Both authors contributed to all parts of the article.

Data availability

The article contains no associated data. All data generated or analyzed during this study are included in this published article.

Acknowledgements

Two anonymous referees are thanked for useful comments.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

1. The Bitcoin White Paper was published by Satoshi Nakamoto on metzdowd.com's Cryptography Mailing List on October 31, 2008. It was subsequenctly published in Decentralized Business Review; https://www.debr.io/article/21260.

2. https://coinmarketcap.com/, retrieved 10 July 2022.

3. Other drawbacks of paper currencies are that they are less easily tracked, need to be replaced, can be lost and counterfeited, and can be cumbersome to transport.

References

- Allen, S., Čapkun, S., Eyal, I., Fanti, G., Ford, B. A., Grimmelmann, J., Juels A, Kostiainen K, Meiklejohn S, Miller A, Prasad E, & Zhang, F. (2020). Design choices for central bank digital currency: Policy and technical considerations. NBER Working Paper. National Bureau of Economic Research. 27634, Cambridge, Massachusetts.

- Altavilla, C., Burlon, L., Giannetti, M., & Holton, S. (2019). Is there a zero lower bound? The effects of negative policy rates on banks and firms. European Central Bank. Manuscript.

- Asimakopoulos, S., Lorusso, M., & Ravazzolo, F. (2019). A new economic framework: A DSGE model with cryptocurrency. CAMP Working Paper. 07, Free University of Bozen-Bolzano, Bolzano.

- Assenmacher, K., & Krogstrup, S. (2018). Monetary policy with negative interest rates: Decoupling cash from electronic money. International Journal of Central Banking, 17(1), 67–22. https://doi.org/10.5089/9781484370025.001

- Beniak, P. (2019). Central bank digital currency and monetary policy: A literature review. University Library of Munich. Manuscript.

- Bindseil, U. (2020). Tiered CBDC and the financial system. European Central Bank. Manuscript.

- Bindseil, U., & Fabio, P. (2020). CBDC remuneration in a world with low or negative nominal interest rates. European Central Bank. Manuscript.

- Boar, C., & Wehrli, A. (2021). Ready, steady, go? - Results of the third BIS survey on central bank digital currency. BIS Papers. Bank for International Settlements.

- Bordo, M. D., & Levin, A. T. (2017). Central bank digital currency and the future of monetary policy. In NBER Working Paper. 23711. National Bureau of Economic Research.

- Bougheas, S. (1994). Asset and currency prices in an exchange economy with transactions costs. Journal of Macroeconomics, 16(1), 99–107. https://doi.org/10.1016/0164-0704(94)90046-9

- Carapella, F., & Flemming, J. (2020). Central bank digital currency: A literature review. FEDS Notes. https://www.federalreserve.gov/econres/notes/feds-notes/central-bank-digital-currency-a-literature-review-20201109.htm

- David-Pur, L., Galil, K., & Rosenboim, M. (2020). To decrease or not to decrease: The impact of zero and negative interest rates on investment decisions. Journal of Behavioral and Experimental Economics, 87, 101571. https://doi.org/10.1016/J.SOCEC.2020.101571

- Davoodalhosseini, M., Rivadeneyra, F., & Zhu, Y. (2020). CBDC and monetary policy. Bank of Canada. Manuscript.

- Feenstra, R. C. (1986). Functional equivalence between liquidity costs and the utility of money. Journal of Monetary Economics, 17(2), 271–291. https://doi.org/10.1016/0304-3932(86)90032-2

- Fujiwara-Greve, T. (2015). Non-cooperative game theory. Springer.

- George, A., Xie, T., & Alba, J. D. A. (2020). Central bank digital currency with adjustable interest rate in small open economies. SSRN. 3605918. National University of Singapore.

- Grasselli, M. R., & Lipton, A. (2019). On the normality of negative interest rates. Review of Keynesian Economics, 7(2), 201–219. https://doi.org/10.4337/ROKE.2019.02.06

- Jia, P. (2020). Negative interest rates on central bank digital currency. Nanjing University. Manuscript.

- Kant, I. (1785). Groundwork on the metaphysic of morals. Harper & Row, Publishers, Inc.

- Kiff, J., Alwazir, J., Davidovic, S., Farias, A., Khan, A., Khiaonarong, T., Malaika M, Monroe MH, Sugimoto N, Tourpe H, & Zhou, P. (2020). A survey of research on retail central bank digital currency. IMF Working Paper. 20/104, Washington, DC: International Monetary Fund.

- Kim, Y. S., & Kwon, O. (2019). Central bank digital currency and financial stability. Seoul. Manuscript. Bank of Korea

- Nakamoto, S. (2008). Bitcoin: A peer-to-peer electronic cash system. Decentralized Business Review. https://bitcoin.org/bitcoin.pdf

- Nash, J. F. (1951). Non-cooperative games. Annals of Mathematics, 54(2), 286–295. https://doi.org/10.2307/1969529

- Oh, E. Y., & Zhang, S. (2020). Central Bank digital currency and informal economy. University of Portsmouth. Manuscript.

- Ozili, P. K. (2022). Central bank digital currency research around the world: a review of literature. Journal of Money Laundering Control, Forthcoming. https://doi.org/10.1108/JMLC-11-2021-0126

- Rognlie, M. (2016). What lower bound? Monetary policy with negative interest rates. Northwestern University.

- Saygılı, H. (2012). Consumption (In)efficiency and financial account management. Bulletin of Economic Research, 64(3), 319–333. https://doi.org/10.1111/j.1467-8586.2010.00387.x

- Taylor, J. B. (1993). Discretion versus policy rules in practice. Carnegie-Rochester Conference Series on Public Policy, 39, 195–214. https://doi.org/10.1016/0167-2231(93)90009-L

- Von Neumann, J., & Morgenstern, O. (1944). Theory of games and economic behavior. Princeton University Press.

- Wang, G., & Hausken, K. (2021). Governmental taxation of households choosing between a national currency and a cryptocurrency. Games, 12 (2), 34. Article 34 https://doi.org/10.3390/g12020034

- Welburn, J. W., & Hausken, K. (2015). A game theoretic model of economic crises. Applied Mathematics and Computation, 266, 738–762. https://doi.org/10.1016/j.amc.2015.05.093

- Welburn, J. W., & Hausken, K. (2017). Game theoretic modeling of economic systems and the European debt crisis. Computational Economics, 49(2), 1–50. https://doi.org/10.1007/s10614-015-9542-3

- Wijsman, S. (2021). Will banks introduce negative interest rates to household deposits? A game theoretical model. FEB Research Report MSI_2107, 1–27, KU Leuven.

Appendix A

Nomenclature

Table

Appendix B

The derivatives for the transaction efficiency

Differentiating the transaction efficiency in (Equation4

(4)

(4) ) with respect to

,

and

gives

The second derivatives of the transaction efficiency in (Equation4

(4)

(4) ) with respect to

,

and

gives

Appendix C

Proof of Lemma 1

Differentiating the household’s utility in (Equation6

(6)

(6) ) with respect to its free choice variables

and

gives

which are equated with zero and solved to yield and

in (Equation10

(10)

(10) ). The dependent variable

follows from solving (Equation1

(1)

(1) ) with respect to

and inserting

and

. The second order conditions, inserting (Equation15

(15)

(15) ) and (Equation10

(10)

(10) ), are

The term in (Equation16

(16)

(16) ) equals

when

has its maximum

. Hence

when

. Since the household has two decision variables

and

, we determine the Hessian matrix

To show that in (Equation17

) is negative semi-definite, it is sufficient to show that (Equation1

(1)

(1) )

and (Equation2

(2)

(2) )

hold. Condition 1 obviously holds since

. Condition 2 also holds,

, since

.

Appendix D

Proof of Lemma 2

Differentiating the central bank’s profit per household in (Equation7

(7)

(7) ) with respect to its free choice variable

gives

which is equated with zero and solved to yield

The second order conditions, inserting (Equation15(15)

(15) ), are satisfied as negative, i.e.

Inserting (Equation8(8)

(8) ) into (Equation19

(19)

(19) ) gives (Equation9

(9)

(9) ).

Appendix E

Proof of the Proposition

Differentiating (Equation8(8)

(8) ) for

, differentiating (Equation9

(9)

(9) ) for

, and differentiating (Equation6

(6)

(6) ) (inserting (Equation8

(8)

(8) ) and (Equation9

(9)

(9) )) for

, give

where means proportional to.