?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Drivers of environmental quality have recently been identified in a large body of literature. However, the ecological effects of both regimes of monetary policy remain under-explored so far. Moreover, previous studies use limited samples and econometric approaches. Climate change from the empirical perspective of the country’s monetary policy has recently become a promising avenue to investigate. Motivated by the aforementioned research gaps and increasing attention from energy researchers and policy-makers, this research aims to test the monetary restrictions and expansion on climate change represented by CO2 emissions, after controlling other significant drivers. We use a dataset from 1998 to 2018 for a sample of 14 selected emerging economies and quantitatively advanced techniques for panel data analysis, such as Ordinary Least Squares (OLS), Dynamic OLS, Fully-Modified OLS, and Panel Quantile Regression. We also use a two-step system generalized method of moments to avoid concerns about endogeneity and heteroskedasticity issues. We find strong evidence that contractionary and expansionary monetary policy both eliminate and escalate the environmental degradation through an increase in CO2 emissions, respectively. Moreover, these ecological effects of monetary policy interestingly appear in the middle and large quantiles of CO2 levels. Based on these findings, the research offers some key implications for policymakers looking to initiate green monetary policy for carbon abatement.

PUBLIC INTEREST STATEMENT

This research contributes to the very limited empirical studies on the ecological impacts of monetary policy with an extensive sample of 14 emerging economies. In addition, none of the prior research looks at how both regimes of monetary policy and other climate change predictors could differ across the quantile levels of CO2 emissions.

Policy practitioners should be aware that loosening monetary policy, considered as a new and significant driver of the environmental degradation caused by an increase in CO2 emissions, could hinder the sound transition of policy towards a sustainable low-carbon economy. This gives rise to the establishment of a “green lending program” shaped by commercial banks, which is identified as a critical conduit of monetary policy transmission via the policy interest rate of central banks.

2. Introduction

Most climate change-related debates among world leaders have focused on environmental damage (Yuping et al., Citation2021). The worsening impact of global warming is largely attributed to the rising levels of carbon dioxide (CO2)Footnote1 in the atmosphere, which threatens major agricultural crop production and land use (Rehman, Ma, Ozturk et al., Citation2022), rice crop production (Gul et al., Citation2022), and environmental quality (Grimm et al., Citation2008; Qingquan et al., Citation2020). The rise in greenhouse gas emissions, which is presently at an all-time high, is frequently viewed as the primary cause of climate change or global warming (Rogelj & Schleussner, Citation2019). A great amount of scientific evidence suggests that human-caused consumption of fossil fuels, which is frequently connected to economic expansion in urban areas, is the primary source of global CO2 emissions (Rehman, Ma et al., Citation2021). The possible reason is that it increases energy demand and has an impact on resource structure, resulting in environmental degradation. There is currently an academic consensus supported by empirical evidence that the rising ratio of carbon emissions, among other factors, poses a significant threat to the environment (Adedoyin et al., Citation2020).

It does not come as a surprise that, in recent decades, there has been considerable empirical research on the predictors of climate change represented by CO2 emissions. Some of the key macroeconomic factors of environmental pollution reported in previous studies include, but are not limited to, remittance inflows (Ahmad et al., Citation2021), consumption of aggregate demand (Ahmad & Khattak, Citation2020), international trade (Lv & Xu, Citation2019), renewable energy consumption (Dong et al., Citation2020), globalization (Murshed, Rashid et al., Citation2022; Shahbaz, Solarin et al., Citation2016; Yuping et al., Citation2021), investments in information and communication technology (Wang et al., Citation2021), fertilizer consumption (Rehman, Ma, Ozturk et al., Citation2022), innovation (Khattak et al., Citation2020; Murshed, Mahmood et al., Citation2022), negative and positive shocks to green technologies (Khattak & Ahmad, Citation2021) among others. Given a thorough review of this empirical research, we observe the lack of studies on the ecological impact of monetary policy. Although central banks and policy regulators could not replace appropriate climate policies (Weidmann, Citation2020), it is now commonly agreed that they must intervene to scale up green finance and implement policies to address climate-related financial risks. The justification is that climate change has an impact on monetary policy (Chenet et al., Citation2021) and financial regulation and financial actors play an important role in the global economy (Mazzucato & Semieniuk, Citation2018).

According to Georgantopoulos (Citation2012), given the fact that energy consumption occupies a pivotal role in boosting socio-economic growth and quality of life, governments, through economic policies, frequently attempt to effectively regulate the fundamental causes of climate change, such as energy-led emissions. It is widely acknowledged that central banks could utilize monetary policy to control and manage a country’s money supply, as well as to stabilize inflation and maintain long-term interest rates. Monetary policy is considered a significant predictor of economic growth and, as such, it is viewed as a helpful tool for lowering CO2 emissions. In this regard, Qingquan et al. (Citation2020) argue that changes in policy interest rates have an impact on the patterns of industrial energy consumption, innovative activities, aggregate domestic consumption spending demand, financial development, and per capita income, resulting in a polluted environment. The decreased and increased policy interest rates could turn monetary policy into an expansionary or contractionary monetary policy stance, respectively. Specific regimes of monetary policy could have a differential effect on environmental degradation. It is worth noting that monetary policy is a significantly novel and under-researched determinant of environmental pollution.

The implications of a specific regime of monetary policy on climate change could be justified by the following two mechanisms. First, policymakers could stimulate the green environment by enacting a contractionary monetary policy. Following Chishti et al. (Citation2021), monetary restrictions could disrupt the economic progress through a decrease in industrial production and trigger a lower level of employment, thereby decreasing the use of fossil fuel energy. This leads to ameliorating the environmental quality. However, Qingquan et al. (Citation2020) show that entrepreneurs are more likely to adopt traditional technologies for manufacturing if loans for new innovative activities are available at a higher interest rate. The increased use of less environmentally friendly technologies could result in high levels of CO2 emissions. Second, monetary expansion could lead to an increase in money supply, aggregate domestic consumption spending, and GDP per capita by curtaining interest rates, which makes industrial sectors more motivated to manufacture goods. Producers are able to do more borrowing and purchase/use more capital goods to enhance their production capacity and keep up with rising customer demand, leading to environmental issues caused by an increased level of CO2 emissions. To sum up, a decreased (or increased) pattern of consumption and a low (high) level of energy demand could eliminate (spur) atmospheric degradation. Consequently, the tightening (loosening) monetary policy potentially enhances (deteriorates) the green environment, respectively.

The present paper aims to test the plausible influence of monetary expansions and restrictions on CO2 emissions while controlling other potential drivers of environmental quality for a sample of 14 emerging countries from 1998 to 2018. Based on the long-run outcomes of OLS, DOLS, FMOLS, and two-step system GMM estimation, we observe that loosening monetary policy by cutting interest rates degrades the atmospheric quality. Meanwhile, tightening monetary policy through an increase in interest rates has a favorable impact on environmental quality. Noticeably, these impacts appear from the middle to large quantile of CO2 levels while employing panel quantile regression. In addition, trade openness, financial development via banks’ credit to the private sector, and aggregate domestic consumption spending per capita could deteriorate the atmospheric quality. We could not find the conclusive impact of GDP per capita on environmental degradation based on DOLS and FMOLS approach; however, the results by using quantile regression show both positive and negative impact of economic growth on environmental quality for lower- and upper-middle quantile values of CO2 emissions, respectively.

The current research differs from the existing empirical studies in the following ways. First, this research is among the first to investigate the influence of both regimes of monetary policy on environmental degradation while controlling other significant explanatory variables, such as financial development, aggregate consumption spending, trade openness, and economic growth. For example, Shobande (Citation2021) also tested the impact of monetary policy and environmental quality. However, this research could not divide monetary policy into both regimes, such as monetary restrictions and expansions. Second, we employ an extensive sample of 14 emerging countries with various levels of development to investigate the ecological effects of monetary policy tightening and loosening. To the best of our knowledge, this sample of current research is more relatively extensive than that of previous studies. For example, similar to the research framework, Chishti et al. (Citation2021) tested the impact of both regimes of monetary policy on CO2 emissions for the case of BRICs countries. Third, we apply various econometric regressions such as OLS, DOLS, FMOLS, and two-step system GMM to address the long run association between monetary expansion and restrictions and environmental quality. In addition, one of our innovations is that quantile panel regressions are employed to provide more insights from the main findings based on OLS, DOLS and FMOLS in which different quantiles of CO2 level are taken into account. This approach offers a deep understanding of CO2 determinants while considering the distribution value of carbon emission levels. To the best of our understanding, no previous research on monetary policy-CO2 emission nexus employs this quantile approach. Given these findings, we propose some suggestions for the implementation of appropriate monetary policy in a world with carbon-constrained and climatically disrupted features.

From this introduction, the rest of the current paper is structured as follows. Section 2 draws on the current literature, whereas Section 3 provides data and research methodology. Section 4 shows the empirical results and its implications, followed by the conclusion and policy recommendations of this paper in Section 5.

3. Literature review

3.1. Monetary policy implications for CO2 emissions

It has been discovered that the worsening of greenhouse gas emissions-induced climate change difficulties has evolved into a serious environmental concern on a global scale (Rehman, Ulucak et al., Citation2021). One should note that environmental challenges, such as climate change and its long-term consequences, are common, particularly in developed and growing countries. These environmental difficulties were generated by both human (anthropogenic) and natural economic growth methods (Adebayo et al., Citation2021). In other words, climate events may endanger human survival and future economic output (Ortiz‐Bobea, Citation2020). There is a general consensus that the rising ratio of CO2 emissions leads to a clear threat to environmental quality and hence climate change. Among the newly discovered factors employed to combat these environmental issues, monetary policy could be a plausible instrument to postpone the impact of climate change, based on the notion that financial policies could facilitate the implementation of low-carbon emission transitions. For more details, financial policy tools and regulatory prudential institutions could allow addressing potential underpricing and a lack of transparency in climate risk pricing in financial markets (Serdeczny et al., Citation2017). Moreover, through the credit channel of monetary transmission, financial resources are shifted from a surplus unit to a deficit unit (Burke & Emerick, Citation2016). In addition, policy rates can be used to influence investment in a manner that is beneficial to the environment and saves lives (Shobande, Citation2021).

Monetary policy is considered a new and significant predictor of economic growth, and as such, it is identified as a helpful tool for mitigating CO2 emissions. The monetary authorities of any country could implement a successful monetary policy by managing the money supply and interest rates in response to macroeconomic issues. Monetary policy in an economy is determined by the relationship between the total supply of money and interest rates. The change in monetary policy could affect economic outcomes, such as innovation, aggregate domestic consumption spending, economic growth, energy consumption, the development of the financial market, and openness in international trade (Twinoburyo & Odhiambo, Citation2018), thereby driving environmental quality.

There is increasing empirical research on the relevance of monetary policy for carbon abatement towards the sustainable development of the environment. Dafermos et al. (Citation2018) suggest that the impact of monetary policy on climate change could lead to financial stability via the credit mechanism. Shobande and Shodipe (Citation2019) examine the effect of energy-related policies in reducing the impact of carbon emissions disclosure for the cases of the United States, China, and Nigeria, and show the favorable influence of monetary policy on promoting measures to control climate change via the interest rate mechanism of the monetary pass-through. However, several papers argue that the use of monetary policy to mitigate climate change could lead to carbon bubbles (Assenza et al., Citation2015). McKibbin et al. (Citation2020) indicate the joint effect of monetary policy and climate change on macroeconomic outcomes such as inflation and output.

More recently, Shobande (Citation2021), using a panel VAR and VEC granger causality method, shows the influence of monetary policy in tackling climate change for the case of six countries in the East African Community. The empirical evidence suggests that monetary policy through the credit and interest rate channels could assist the easy transition to low-carbon economies, albeit at the expense of financial instability. Qingquan et al. (Citation2020) use panel fully-modified and panel dynamic least squares estimation for a case of several selected Asian economies. Authors show the long run relationship between CO2 emissions and monetary policy in which ecological improvement as a result of tightening monetary policy is confirmed. For a sample of BRICs economies, Chishti et al. (Citation2021) employing a series of time series method such as OLS, DOLS, FMOLS and PMG-ARDL show the implications of monetary policy and fiscal policy on CO2 emissions, especially for both cases of expansions and restrictions of each macroeconomic policy.

Monetary policy in an economy is determined by the relationship between the total quantity of money supply and policy interest rates. Policy-makers and financial regulators could use numerous tools to navigate outcomes associated with these two variables, including but not limited to innovation, aggregate domestic consumption spending, growth of an economy, energy consumption, financial development, and trade openness (Twinoburyo & Odhiambo, Citation2018). The central bank could implement the monetary expansions (EMP) through cutting interest rate and monetary restrictions (CMP) through increasing interest rate. The mechanisms through which the ecological effect of monetary policy could show its effect are as follows. Monetary expansion, for example, exerts an increase in the money supply, aggregate domestic consumption spending, and per capita income by decreasing policy interest rates, which has a direct impact on economic agents such as consumers and producers. Customers could benefit from this loosening policy through higher lending and consumption power. Aggregate domestic consumption spending would rise in response to an increase in income, inducing the industrial sectors to produce more goods. In this regard, serious price-based competition would drive production companies to adopt low-cost emission physical capital, which would raise CO2 emissions. Furthermore, producers are more likely to begin borrowing and purchasing/using more capital goods in order to strengthen their production capacity and fulfill rising demand from their clients. Furthermore, gross capital formation has been recognized by Ahmad et al. (Citation2021) as one of the primary sources of CO2 emissions. Therefore, a decrease in policy rates caused by the expansionary monetary policy could raise the aggregate domestic consumption spending and boost industrial consumption of fossil fuels. There is sufficient past evidence to assume that an increase in consumption spending and the use of fossil-fuels could stimulate CO2 emissions (Ahmad & Khattak, Citation2020).

In contrast to the monetary expansions, CMP through an increase in policy interest rate could decrease the money supply, aggregate domestic consumption spending, and income per capita. Lending and the purchasing power of customers would be decreased as a result of this tightening regime of monetary policy, and a reduced income would lead to a decrease in aggregate domestic consumption spending. Due to a fall in aggregate domestic consumption spending, industrial sectors would have less incentive to manufacture goods, utilize fossil fuels, borrow from banks, and purchase capital goods. This adaptive production behavior from producers, combined with reduced energy demand from individual customers, would help to minimize CO2 emissions. Z. U. Z. U. Rahman et al. (Citation2019) agreed that a decrease in gross capital formation disturbs CO2 emissions. Therefore, an increase in interest rates reduces aggregate domestic consumption spending and the use of fossil fuels. Again, previous research has shown that lowering aggregate domestic consumption spending and using non-renewable energy reduces CO2 emissions (Ahmad & Khattak, Citation2020). The mechanisms through which loosening and tightening monetary policy affect climate change are displayed in .

Figure 1. Mechanism through which monetary policy could affect climate change (CO2 emissions).

Given the growing literature on the ecological impact of the country’s macroeconomic policy and the implications of monetary policy on environmental quality, it is worth examining the practical impacts of monetary expansions and restrictions on CO2 emissions in the case of emerging economies. reports the related empirical research on the monetary policy—climate change nexus.

Table 1. Summary of related empirical evidence on the ecological effect of monetary policy

3.2. Aggregate domestic consumption spending per capita and CO2 emissions

One should note that aggregate domestic consumption spending per capita is relatively new compared to other CO2 emission drivers. In the example of South Africa, Ahmad and Khattak (Citation2020) identified this new predictor of pollution as a component of per capita income. According to the study, aggregate domestic consumption spending per capita plays a critical function in determining pollution. Additionally, high demand puts pressure on business owners to make items quickly, which requires a large amount of fossil fuel; this process results in an increase in carbon emissions. To support this perspective, Chishti et al. (Citation2021) show that increased domestic consumer expenditure creates a demand-supply imbalance, which stimulates businesses to increase production. Subsequently, low-cost, unsustainable manufacturing techniques are employed, and fossil fuels are utilized to maximize profit. This mechanism eventually leads to an increase in CO2. Although this variable is not directly used in the research model of Qingquan et al. (Citation2020), the author still supports the important role of aggregate domestic consumption spending on carbon emissions. As a less-known and important source of CO2, it’s worth looking into the effects of this factor in this study.

3.3. Financial development and CO2 emissions

Although the financial industry is vital to a country’s economic success, its negative environmental impacts could not be ignored, as they affects energy consumption, gross domestic product, and environmental quality (Charfeddine & Khediri, Citation2016). Energy demand and consumption are increasing due to the development of the financial industry. The availability of financing sources, for example, raises residents’ living conditions and stimulates human activities that use more energy. According to Shahbaz, Van Hoang et al. (Citation2017), financial development increases foreign direct investment (FDI), economic growth, and energy consumption. However, modern technology and financial growth may minimize energy usage and pollution. Some claim that financial development is good for the environment since it may reduce CO2 emissions. Using BRICS panel data from 1992 to 2004, Malla (Citation2009) revealed a negative correlation between CO2 emissions and financial development. Jalil and Feridun (Citation2011) utilized the Autoregressive Distributed Lag (ARDL) approach to study China, covering the period of 1953–2006 and found that increases in financial development led to an improvement of environmental quality, possibly due to lower CO2 emissions. Saidi and Mbarek (Citation2017) used the generalized method of moments (GMM) for emerging economies and found that financial development helps improve environmental quality. Shahbaz et al. (Citation2018) studied the impact of financial development, energy innovation, and FDI on environmental quality in France from 1955 to 2015. Salahuddin et al. (Citation2018) found a negative relationship between financial development and environmental quality in Kuwait.

The second group of academicians believes financial growth harms the environment. For example, Boutabba (Citation2014) found a link between financial development and environmental deterioration in India, while Al-Mulali et al. (Citation2015) found the same evidence for a group of 23 European nations for the period of 1990–2013. Charfeddine and Khediri (Citation2016) confirmed the findings of Al-Mulali et al. (Citation2015) by investigating the UAE from 1975 to 2011. Shahbaz, Mallick et al. (Citation2016) explored a similar connection with GDP and energy use in Pakistan. They created a stock market and a banking index. The growth in the banking development index enhanced Pakistan’s CO2 emissions. Using the ARDL approach, Bekhet and Othman (Citation2017) found that financial development increases CO2 emissions in Malaysia. Given the premise of the Environmental Kuznets Curve (EKC) hypothesis, Pata (Citation2018) found that financial development increased carbon emissions. Zakaria and Bibi (Citation2019) used panel data and found that financial development reduces environmental quality, whereas institutional quality boosts it. Charfeddine and Kahia (Citation2019) used Panel Vector Autoregressive (PVAR) to illustrate how financial development accelerates carbon emissions in 24 MENA nations.

3.4. Gross domestic per capita and CO2 emissions

The effects of economic growth on environmental contamination have been tested by validating the EKC hypothesis. Over the last five decades, academicians have examined the EKC hypothesis’s validity and reached inconclusive results. Among the country-specific investigations, Koc and Bulus (Citation2020) used an ARDL model and discovered that the EKC hypothesis does not exist. The authors stated that, while economic expansion first increases CO2 emissions and then decreases them, continued growth of the South Korean economy stimulates CO2 emissions once more, following an N-shaped linkage. Similarly, Pata and Caglar (Citation2021) recently used the augmented ARDL technique to determine that the EKC hypothesis for CO2 emissions is not valid in Turkey. In contrast, Ali et al. (Citation2021) argued in another study on Pakistan that the economic growth-CO2 emission nexus exhibits an inverted U-shape, hence validating the EKC theory. Similarly, Rana and Sharma (Citation2019) quantitatively established the EKC hypothesis’s existence in the context of India. In cross-country research on the EKC hypothesis for CO2 emissions, Dong et al. (Citation2018) examined a sample of 14 Asia-Pacific countries and verified the EKC hypothesis. Additionally, the authors determined that these countries’ usage of comparatively cleaner energy resources contributes significantly to confirming the EKC theory. In contrast, M. M. M. M. Rahman et al. (Citation2021) recently established that the EKC hypothesis does not hold true for selected newly industrialized economies. Bibi and Jamil (Citation2021) validated the EKC hypothesis using CO2 emissions as an index of environmental quality in other research, including 21 Latin American and Caribbean economies.

3.5. Trade openness and CO2 emissions

In general, free trading activities increase global trade volume and wealth, benefiting both developed and developing countries. But this growing tendency has environmental effects (Shahbaz, Nasreen et al., Citation2017). The environmental impact of trade openness may be separated into two hypotheses. The first theory divides the influence of trade openness on pollution into scale, technology, and composition effects (Farhani, Chaibi et al., Citation2014). The Pollution Haven Hypothesis (Copeland & Taylor, Citation2004) is the second one, implying that trade liberalization attracts foreign direct investment. Polluting companies will prefer to produce in nations with lower environmental requirements, thereby creating a “pollution haven”. Given these theories, four hypotheses are developed as follows: (1) Trade openness boosts CO2 emissions, (2) CO2 emissions enhance trade openness, (3) Feedback hypothesis: trade openness and CO2 emissions interaction, and (4) Neutral hypothesis: trade openness is independent of carbon emissions.

For more details, using the Vector Error Correction Model (VECM), M. Nasir and Ur Rehman (Citation2011) support hypothesis (1) by showing that trade openness positively influences CO2 emissions in Pakistan; that is, increasing trade openness has been shown to increase pollution. In the work of Farhani, Shahbaz et al. (Citation2014), an application of VECM, FMOLS, and DOLS has confirmed this. For hypothesis (2), the ARDL bounds test and VECM causality were used (Shahbaz, Khan et al., Citation2017). The Granger causality test linked carbon emissions to trade liberalization. Hypothesis (3) states that trade openness and carbon emissions are causally linked. Using a panel regression model for 105 countries, Shahbaz, Nasreen et al. (Citation2017) found bidirectional causation between the global groups and middle-income groups; that is, trade openness influences CO2 emissions. Hypothesis (4) rejects the relationship between trade openness and CO2 emissions, although there is little evidence to support it. Using a linear econometric model, it is difficult to find a causal link between trade and the environment at the national level (Frankel & Romer, Citation1999). When exploring the impact of trade on the EKC, Kearsley and Riddel (Citation2010) employed the panel regression model and indicated that trade openness was not typically connected with an increase in CO2 emissions. Due to inconclusive evidence to support the aforementioned hypotheses, the link between trade openness and carbon emissions has to be explored further.

4. Data and methodology

4.1. Data

The data for all selected proxies of current research is retrieved from the World Development Indicators covering the period of 1998–2018. From the original list of emerging countries based on market classifications of MSCIFootnote2, we collect the countries without missing data for all variables, which finally obtains 14 countries. These emerging economies consist of Brazil, Chile, Colombia, Mexico, Peru, the Czech Republic, Egypt, Hungary, South Africa, Indonesia, Korea, Malaysia, the Philippines, and Thailand. The primary aim of gathering data from these emerging countries is to create a well-balanced panel dataset, which will allow us to produce more robust results.

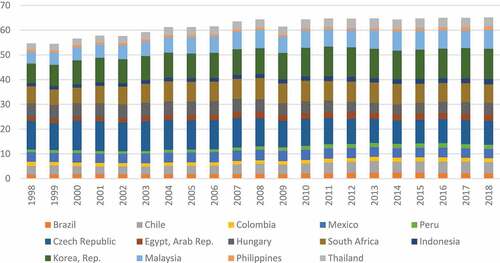

As of 2019, the GDP growth rate of the 14 selected emerging countries in this sample is 2.922% higher than the average world GDP growth rate of 2.687%.Footnote3 To continue their rapid economic growth, these economies become dependent substantially on energy consumption, which generates a massive quantity of CO2 emissions, as illustrated in , which depicts the overall picture of per-capita carbon emissions in these economies. It is observed that there is a gradually increasing CO2 emissions with the growth rate of per capita CO2 metric tons of 19.14% covering the period 1998–2018, suggesting the significant implications of energy consumption for economic growth of these economies. As a result, the Climate and Clean Air Coalition predicts that 92% of the world’s population would be subjected to severe pollution by 2030 if substantial actions and policies are not implemented urgently (NOAA, Citation2020). As a result, it gives rise to conducting research in order to examine the endogenous as well as exogenous variables that could shape environmental quality and hence climate change.

Figure 2. The overall picture of per capita CO2 emissions for 14 selected emerging countries covering the period of 1998–2018.

4.2. Empirical model

According to Qingquan et al. (Citation2020) and Chishti et al. (Citation2021), monetary policy (MP) is integrated into the baseline model of aggregate Cobb-Douglas production function:

In general, environmental quality represented as carbon emissions is directly correlated with economic activities, we could obtain:

Replacing EquationEquation (1)(1)

(1) into EquationEquation (2)

(2)

(2) , the determinants of CO2 emissions can be written as:

Given previous literature on the other significant factors driving climate change such as financial development (Le & Ozturk, Citation2020; Zafar et al., Citation2019), trade openness (T. T. T. T. Nguyen et al., Citation2020), gross domestic product per capita (Bengochea-Morancho et al., Citation2001), and aggregate domestic consumption spending per capita (Ahmad & Khattak, Citation2020), we propose the baseline model as follows:

where and

index country and year, respectively. The dependent variable

is measured by carbon emissions per capita, which reflect climate change (Shobande & Enemona, Citation2021; Shobande & Ogbeifun, Citation2021). Real interest rate (

) is widely employed to capture the monetary policy indicator (Asongu et al., Citation2019; Cloyne et al., Citation2020; Gertler & Karadi, Citation2015), which stimulates environmentally friendly investments (Shobande, Citation2021).

As a proxy for financial development, domestic credit to the private sector by banks () is employed. It is anticipated that climate finance will be helped by a healthy financial industry (Shobande, Citation2021). Openness in international trade (

) is captured given the hypothesis of pollution haven (Sigman, Citation2002). Real gross domestic product per capita (

) is a measure of economic growth. The economic expansion is predicted to result in a rise in carbon dioxide, which may have implications for climate change (Shobande, Citation2021). Aggregate domestic consumption spending per capita (

) is a proxy for an economy’s aggregate demand, which is calculated by GDP plus exports, minus imports as a share of the total population. This proxy is correlated with atmospheric pollution (Ahmad & Khattak, Citation2020).

To ensure consistency, absolute variables are converted into logarithmic form (i.e, CO2, GDPPCC and ADCSP) while leaving the percentage of variables unchanged (T. T. T. T. Nguyen et al., Citation2020). As a result, a final model is displayed as:

To separate aggregate monetary policy () into a specific regime of restrictions and expansions, we integrate the identity function viz.

and

for each corresponding regime such as loosening policy—CMP and tightening policy—EMP, which is identified as:

in which,

The description and sources of data are reported in below.

Table 2. Data description

4.3. Stationary test

We test stationary properties of all series on the basis of Levin et al. (Citation2002) and Im et al. (Citation2003). The general specification from the approach of Levin et al. (Citation2002) test could be elaborated as follows:

where ~

. Specification (9) reflects the unit root test in case of H0:

≠ 0 and the series show stationary property in case of H0:

< 0. Levin et al. (Citation2002) test is employed to process the regression of Augmented Dicker-Fuller on the Ordinary Least Squares (OLS) for pooled panel dataset. However, Im et al. (Citation2003) build the assumption to make correction of OLS drawbacks by utilizing the varying autoregressive process for estimated individuals. Therefore, group-mean of individual t-statistic with the following specification in which

= 1, 2, …, N and

= 1, 2, …, T is developed based on Specification (6).

The terms of are extracted to stand for the t-statistics to test the unit root of ith individual process (where

—lagged order, widely employed to choose optimal lag order). As a result,

on a basis of Im et al. (Citation2003) is possible to examine the null hypothesis H0:

against HA:

.

4.4. Co-integration tests

The test for panel co-integration is largely reliant on the following equation:

The test is dependent on the covariates of are not co-integrated themselves.

stand for the vector capturing the co-integrating feature, which could be varied across panels. A vector

includes coefficients on

which is considered as deterministic terms to address panel-specific impacts and homogenous time trends.

is error term, which is correlated to white noise

~

. Kao (Citation1999) suggests the co-integrated assumptions with

; hence, the panels show common slope parameters. Five categories of test are proposed such as Modified DF-t, DF-t, Augmented-DF-t, Unadjusted modified DF-t, Unadjusted DF-t from the regression of Dickey Fuller as:

where is the parameter of estimated residuals from Auto Regression, while Augmented Dicker-Fuller regression is specified as:

in which illustrates the number of lagged difference terms. Importantly, the asymptotic distribution for all tests are turned into N(0,1). On the contrary, Pedroni (Citation1999) assesses that each panel-specific co-integrating vector from EquationEquation (11)

(11)

(11) has different slope parameters. Then, Pedroni (Citation1999) use the estimated residuals to examine the unit root test based on Augmented Dickey-Fuller regression but this approach allow each

rather than the same

similar to Kao (Citation1999) and follows the convergence properties after applying standardization procedure.

4.5. OLS, dynamic OLS (DOLS), and fully-modified OLS (FMOLS)

We perform panel OLS and DOLS techniques to obtain the long-run association between monetary policy regimes on climate change. The panel OLS and DOLS could generally specified as follows:

To calculate the coefficients, OLS estimator could formed as:

To build the panel estimator of DOLS, Pedroni (Citation2001b) uses the following specification by integrating lead and lag dynamic:

and to calculate coefficients:

in which = 2(k +1)x1, and

denotes

.

For the choice of DOLS, we determine lagged and lead variables to address the errors of autocorrelation on error term .

FMOLS is characterized by using Newey West for coefficient’s correction. Pedroni (Citation2001a) suggested using this technique to estimate coefficients, which captures long-run impacts. According to M. A. Nasir et al. (Citation2019), we outlined how the formula works to obtain the regression coefficients where i and t represent individual effect and time period, respectively.

where,

and is:

As a result, for long-run variance, we designate as the asymptotic covariance matrix. Dynamic covariance is abbreviated as

. Furthermore,

is a lower triangular matrix with partition computation, and

and

stand for independent and dependent variables, respectively.

4.6. Quantile panel regression

The justification of the use of quantile panel regression is that this estimation allows to investigate the influence of explanatory variables on dependent variables (i.e, CO2 emissions) while considering the conditional distribution. Originally, Koenker and Bassett (Citation1978) used quantile regression to generate findings by a generalization of median regression analysis with respect to specific quantile values. The model is specified as:

where is the dependent indicator and

is a vector of explanatory indicators together with

as its coefficients.

is quantile level, which penalized the impacts of dependent variables. Therefore, quantile regression will address the extreme values as well as heavy distribution, which is possibly present in the studied sample. From the literature of Koenker (Citation2004), we clearly demonstrate the way estimated coefficients are solved:

where and

index the individual-level (max:

) and time period (max:

), k denotes the index of quantiles (max:

),

is a vector of independent indicators,

denotes relative weight given to

th quantile, and

is quantile loss function.

is the term towards zero, or penalty term, which is generally employed for fixed-effect estimators.

There are various advantages of using quantile panel data regression. First, this approach could correct the sample size bias caused by endogenous regressors (Canay, Citation2011). Second, the use of this method eliminates bias caused by the distributional heterogeneity (Zhu et al., Citation2016). Third, this method is used in several existing papers in the field of environmental economics, such as Allard et al. (Citation2018). As a result, we employ this method to make results more robust when taking into account outlying data of the explained variable, whereas standard OLS regression does not manage outliers well, especially when the error-term is non-normally distributed (Flores et al., Citation2014).

4.7. Descriptive statistics

To provide an understanding of the preliminary features of the dataset, the analysis of descriptive statistics is reported in . For all variables, the skewness value is positive and greater than zero. As a result, all variables have shown indications of skewness to the right. Furthermore, the excess kurtosis is greater than zero, indicating that all variable distributions exhibit the fat-tailed characteristic. Based on the skewness and kurtosis results, all variables are ruled out as being normally distributed. The results are also confirmed by the Jarque-Bera test at 1% level of significance for all studied variables. These findings support the idea of employing the set of quantitative techniques outlined in the following section.

Table 3. Descriptive statistics

5. Empirical findings

To begin with, we confirm the stationary property of time series by the Levin-Lin-Chu (LLC) and Im-Pearsan-Shin (IPS) tests before testing the presence of cointegration tests based on the Pedroni and Kao’s approach. One should note that Pearsan’s test for the existence of cross-sectional reliance is performed in residuals after OLS-based regression for all variables, showing a t-statistics value of −1.143 and a p-value of 0.253 > 0.1. This implies no serious concern regarding dependent property among studied variables. Moreover, the validity of the first dependence test also allows us to employ panel quantile regression (T. T. T. T. Nguyen et al., Citation2020) and use first-generation unit root tests depending on LLC and IPS (M. A. Nasir et al., Citation2019). After that, given the existence of long run associations among modeled variables, we use OLS, DOLS, FMOLS, two-step system GMM to show the empirical evidence on the ecological effect of monetary policy while controlling other explanatory variables, followed by Quantile Panel Regression to provide more insights.

5.1. Panel unit root test

In , it is worth noticing that the stationary property of all variables is confirmed at the 1% significance level, indicating the I(1) property of study proxies. Therefore, we could proceed with all variables without any deletion and allow determining the long-run relation among variables.

Table 4. LLC-based and IPS-based unit root test of stationary

5.2. Co-integration analysis

Pedroni (Citation1999) co-integration test suggests seven statistics with the null hypothesis of no presence of cointegration for all panel units. Four of these statistics are panel statistics, while the remaining three are group test statistics. In , the null hypothesis of no co-integration among variables is rejected based on the results of four of seven statistics. This implies the existence of co-integration among variables in the panel. To confirm this finding, we utilize the approach of Kao (Citation1999) as illustrated in . It holds true that the majority of tests reject the null hypothesis of no co-integration among a group of modeled variables. Therefore, we demonstrate the existence of co-integration in our research variables. This finding statistically gives strong evidence that the variables have a long run relationship.

Table 5. Panel co-integration tests by Pedroni (Citation1999)

Table 6. Panel co-integration tests by Kao (Citation1999)

5.3. Estimation results using OLS, DOLS, and FMOLS

As displayed in , the findings from OLS, DOLS, and FMOLS estimations provide several remarks. First, it is observed that there is a positive long-run link between monetary policy loosening (EMP) and CO2. With respect to the magnitude of coefficients on EMP and CO2, 1% decrease in real interest rates leads to approximately 2.18%, 3.48%, and 3.91% increases in CO2 emissions, respectively. It is plausible to note that monetary expansion through a decrease in policy interest rates could boost economic demand and development by increasing industrial production and employment. This expands the use of fossil fuels, resulting in an increase in the seriously detrimental consequences of CO2 emissions.

Table 7. Long-run coefficient by OLS, DOLS, and FMOLS (Y = CO2)

As regards CMP, the coefficients of OLS, DOLS, and FMOLS reveal 1.05%, 2.57% and 2.83% decreases in environmental degradation, respectively, as a result of the conduct of monetary restrictions at 1%. The potential justification is that, in response to the negative effects of inflation, the central banks frequently raise interest rates, making banks’ loans more expensive and affecting firms’ profitability. As a result, this implementation impedes manufacturing goods, the level of employment, GDP, and thus CO2 emissions. These findings are in line with the work of Chishti et al. (Citation2021) and provide evidence on the significant impact of both monetary regimes on carbon emissions and hence climate change. Possibly, central banks employ the CMP in response to an intolerably high inflation ratio caused by excessive demand. To mitigate the negative effects of inflation, the central banks raise interest rates, making bank lending more expensive and less profitable. As a result, this implementation has a detrimental effect on the production of goods, employment, GDP, and CO2 emissions. One should note that for both monetary regimes (contractionary and loosening monetary), the magnitude of OLS coefficients on EMP-CO2 and CMP-CO2 emissions is relatively less than that of DOLS and FMOLS, suggesting appropriate regression estimation relying on the DOLS and FMOLS approaches.

Second, based on the OLS, DOLS, and FMOLS estimation of a bank’s credit to the private sector as a share of GDP (CREDIT), it shows that a 1% increase in bank credit could contribute to a 0.49%, 0.76% and 0.77% increase in CO2 emissions, respectively. This is consistent with the work of M. A. Nasir et al. (Citation2019), who show the unfavorable influence of financial development through an increase in the bank’s credit on CO2 emissions. It could be implied that the natural development of financial markets could lead to an increase in the degree of carbon released, possibly due to the credit supply of banks to firms or corporations with energy-intensive production. According to Raghutla and Chittedi (Citation2020), development of financial services may increase demand for economic output, which could persuade consumers to use more energy, resulting in increased carbon emissions. One should note that the growth of the financial industry has boosted energy demand and consumption. For example, the availability of financial sources improves citizens’ living standards and stimulates human activities that consume more energy. Financial development, according to Shahbaz, Van Hoang et al. (Citation2017), boosts foreign direct investment (FDI), economic growth, and energy consumption, which have an adverse impact on environmental quality.

Third, in the case of income per capita (GDPPCC), we observe the positive impact of income per capita on CO2 emissions using OLS, suggesting the ecological implications of economic growth. However, these coefficients are statistically insignificant in DOLS and FMOLS regression estimation. This might be inconclusive because of the offsetting effect between the stimulating and deteriorating influence of economic growth on carbon emissions, which gives us rise to further investigation into panel quantile regression.

Fourth, with respect to significant coefficients on ADCSP based on DOLS and FMOLS regression, we find the positive impact of aggregate domestic consumption spending on CO2, indicating environmental quality deteriorates when people expand ADCSP (Ahmad & Khattak, Citation2020; Chishti et al., Citation2021). Accordingly, 4.27% and 3.66% of the increase in carbon are statistically attributed to an increase in per-capita domestic consumption spending, respectively. It is possible that increased domestic consumer spending produces a demand-supply mismatch, which encourages enterprises to expand output. As a result, low-cost, unsustainable production processes are used, and fossil fuels are also employed to maximize profit. This process finally results in a CO2 emission rise. One should mention that this finding is not significant for OLS-based estimation, similar to the work of Chishti et al. (Citation2021).

Finally, trade openness could be a pivotal determinant of CO2 when we observe the statistically positive influence of openness in international trade on environmental pollution at a 1% significance level, which is in line with T. T. T. T. Nguyen et al. (Citation2020). It means that a 1% increase in trade openness will trigger a 0.32%, 0.34% and 0.42% increase in CO2 for both cases of OLS, DOLS, and FMOLS techniques, respectively. This could be implied from the scale effect (Antweiler et al., Citation2001) in which trade openness expands, boosting economic development and hence indirectly increasing emissions. In addition, this could be supported by the Pollution Haven Hypothesis (Copeland & Taylor, Citation2004), suggesting that foreign direct investment is attracted by trade liberalization. Polluting corporations will prefer to manufacture in countries with less stringent environmental regulations, resulting in the creation of a “pollution haven”.

5.4. Panel quantile regression estimation

In , we show how our independent variables affect different quantiles of dependent variables (i.e, CO2 emission). Our quantile empirical findings present several confirming conclusions. First, the quantile effect could be observed in both regimes of monetary policy (i.e, CMP and EMP). For more details, it shows that the middle and large quantiles of CO2 emissions are affected by monetary expansions and restrictions. In other words, the larger amount of environmental pollution driven by an expansionary and tightening monetary policy could not be seen at low quantile of CO2 level. These findings suggest the effectiveness of monetary policy in leading to significant changes in carbon emissions for the most polluting countries. This monetary tool should be given much attention by policymakers to address climate change. Second, financial development represented by banks’ credit to the private sector has the same and significant impact on every quantile, lending support to the triggering effect of financial market development on environmental degradation as aforementioned above.

Table 8. Quantile panel regression (Y = CO2)

Third, gross domestic product per capita (GDPPCC) shows an inconsistent correlation with CO2 emissions, offering an interesting story. Specifically, when economic development causes CO2 emissions to decrease at lower quantiles (below Q50), the negative effects of economic development are witnessed at higher distribution values of CO2 emissions. This could be a reason for the insignificant growth implications of carbon emissions, reported previously in FMOLS and DOLS estimations, in which the positive impact of economic growth could offset the negative side. Fourth, aggregate domestic consumption spending per capita (ADCSP) has a deteriorating influence on environmental quality by increasing carbon emissions, which is valid across all distribution values of CO2 emissions. This confirms that ADCSP could be one of critically emerging factors driving carbon emission as explored in recent studies (Ahmad & Khattak, Citation2020). Finally, trade openness (TRADE) has a positive effect on CO2 distribution values close to the middle quantiles (Q25-Q75). Summing-up, research variables such as monetary policy, financial development, economic growth, aggregate consumption spending, and trade openness are among significant predictors of CO2 emissions; interestingly, these have different quantile effects on carbon emissions.

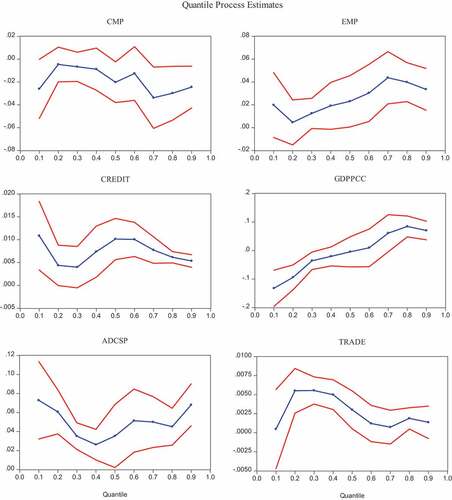

For illustration of the aforementioned findings, we use charts based on the quantile regression results. As represented in , the blue line captures the marginal impact of factors driving CO2 emissions while the red lines show these confidence intervals to imply the significant effects of these determinants on carbon emission and hence climate change. If this confidence interval bands include zero value, the link among variables of interest is insignificant. The findings are consistent with those reported previously. For more details, both regimes of monetary policy, such as loosening and tightening, lead to increases in and reductions in CO2 emissions, respectively, at middle quantile values and greater. In addition, financial development and ADCSP have a consistently detrimental effect on environmental quality across the majority of quantile values, while at the middle quantiles (Q25-Q75), trade openness has a positive impact on CO2 emissions. Except for the growth of economic activities, we observe both stimulating and deteriorating impact of economic growth on carbon emissions. This might be justification for the inconclusive impact of economic growth on CO2 emissions as noted in the OLS, DOLS, and FMOLS regressions of .

Figure 3. Quantile regression estimates with 90% confidence intervals for the impacts of climate change determinants.

5.5. Two-step system GMM estimation

According to Bashir et al. (Citation2020), Nguyen, Dinh, Seetharam et al. (Citation2022) and T. P. Nguyen, Dinh, Tran Ngoc et al. (Citation2022), GMM is used for panel datasets with large-N and small-T (in our study, using 14 countries and 20 years may not satisfy this condition). Based on this view, we do not use the GMM estimation regression. However, we strongly believe that it is still necessary to include the GMM-typed estimation in the manuscript to reinforce the findings and avoid econometric concerns such as endogeneity and heteroskedasticity.Footnote4 Therefore, we proceed to process the data based on the two-step system GMM which was widely used in previous studies (Bakhsh et al., Citation2021; Berk et al., Citation2020). We employed this approach originally suggested by (Arellano & Bover, Citation1995) and Blundell and Bond (Citation1998) due to its benefits. For more details, the main reason for using system GMM instead of OLS is that the latter models do not adjust for bias and inconsistency, which leads to the occurrence of unobserved time-invariant country effect omission (Blundell et al., Citation2001; Hoeffler, Citation2002). Second, two-step system GMM models in regression are more consistent and efficient estimate strategies that also assess the robustness and realization of issues that are associated between the past and the present. To summarize, Arellano and Blundell’s GMM estimation is far more methodical and competent than previous GMM estimate procedures.

One should note that, to control for the influence of the model variable selection on the main regression results (EMP and CMP), we use the nested stepwise regression (Zhan et al., Citation2021) approach by gradually removing one-by-one control variable out of the research model to consider the sign change of the main research variable.

It is observed at the bottom of the table that AR(1) and AR(2) values are statistically significant and insignificant in all models and tables, respectively. This suggests that there is no first-order serial correlation with the residuals and just second-order serial correlation with the error term. Furthermore, insignificant p-values of the Sargan/Hansen test demonstrate that there is no endogenous issue or over-identification, implying that the legitimate instruments may be employed. As a result, the estimated accuracy of all models adopting the two-step approach GMM is qualified by these post-estimation tests.

As reported in the , regression coefficients on CMP and EMP are significantly negative and positive, suggesting that monetary restrictions and expansion could enhance and deteriorate environmental quality, respectively. This confirms the aforementioned findings. In addition, the findings for other control variables such as financial development, economic growth, aggregate domestic consumption spending, and trade openness are qualitatively similar to those reported previously.

Table 9. Two-step system GMM estimation (Y =CO2)

5.6. Implications of the research findings

The following implications are proposed as follows. First, we are among the first to consider the ecological effects of both regimes of monetary policy (i.e., loosening and tightening monetary implementation). Specifically, contractionary monetary policy is significantly workable as it reduces CO2 emissions and hence improves the atmospheric quality. Meanwhile, the deteriorating impact of monetary expansions on the environment is evident, implying the absence of eco-friendly loosening monetary policy towards a sustainable environment. In the policy context, and notably in relation to the Sustainable Development Goals, it is critical to consider the significant impact of monetary policy on environmental quality by navigating monetary-based policies towards flexible regimes between tightening and loosening implementation in an attempt to combat environmental issues in particular and climate change in general.

Second, banks’ credit to the private sector as a proxy for financial development has a stimulating impact on economic growth, which could lead to an increase in energy consumption and simultaneously have unexpected ecological consequences. The expansion of financial systems might stimulate economic growth, which necessitates increased energy consumption. Moreover, more efficient financial intermediation can supply more credit to firms, lowering the cost of their high energy-intensive goods and services. In addition, financial development stimulates greater international and domestic investment, which in turn degrades the environment by consuming more energy resources (Zhang, Citation2011).

Third, trade openness has a deteriorating impact on environmental quality as it increases the scale of production and the level of economic growth, leading to an increase in CO2 emissions from the perspective of the scale effect. The degree to which an economy is open to trade with other economies across the world is referred to as “trade openness”. It assists these countries in raising exports in order to enhance domestic output by increasing the scale of industries, potentially resulting in greater pollution (Jun et al., Citation2020).

Fourth, the impact of economic growth shows an interesting case in which economic growth could both increase and decrease environmental pollution below and above the middle quantile values of CO2 emissions, respectively. Fourth, the influence of ADCSP on environmental degradation is evidently found, highlighting the relevance and importance of using this indicator as a determinant of carbon emissions. To sum up, we provide . in order to illustrate the results at a glance.

Figure 4. Estimation outcomes of OLS, DOLS, FMOLS, GMM and panel quantile regression.

6. Conclusion and policy implications

Global warming and climate change, considered the most pressing environmental challenges in recent decades, are largely attributed to greenhouse gas emissions, particularly CO2 emissions (Esso & Keho, Citation2016). To date, it is worth discovering the empirical impact of newly emerging factors, possibly addressing CO2 emissions and hence climate change. This article seeks to shed light on the driving role of monetary policy in CO2 emissions in the selected emerging economies that have experienced rapid economic and financial growth relative to the rest of the world. In the background of an increasing body of research devoted to identifying determinants of climate change, the ecological role of monetary policy has been ignored in previous studies, especially for both regimes of monetary policy on environmental degradation (i.e., monetary expansions and restrictions). This gives rise to concerns about the extent to which monetary policy could be utilized to combat climate change. In an attempt to fill this void, we elaborate the econometric framework in which OLS, DOLS, and FMOLS are employed to address the ecological implications of determinants of CO2 emissions for a case of 14 selected emerging countries. To avoid concern of endogeneity and heteroskedasticity issues, two-step system GMM is also employed.

We find a long-run association of monetary policy with environmental pollution in which monetary restrictions via an increase in interest rates could have a favorable effect on reducing CO2 pollution while monetary expansions through a decrease in interest rates could have the opposite influence. More interestingly, these effects could be observed in a middle and higher quantiles of CO2 levels. We also control a set of other explanatory variables and find the ecologically deteriorating effects of trade openness, aggregate domestic consumption spending per capita, and financial development through banks’ credit to the private sector. These determinants of climate change show different impacts on the distribution quantile values of CO2 emissions. More interestingly, we find the positive and negative impact of GDP per capita on atmospheric improvement for upper- and lower-middle quantile values of carbon emissions.

Climate change is non-negotiable and immediate actions by policy-makers are essential to avoid negative climatic consequences, mitigate its economic impact, and avert atmospheric disaster. Findings of current paper could make policy practitioners aware of the ecological benefits of contractionary monetary policy on the improved environmental quality, and hence climate change. One should note that considering loosening monetary policy as a new and critical determinant of the environmental degradation caused by an increase in CO2 emissions could hinder the sound transition policy towards a sustainable low-carbon economy. For example, with monetary restrictions through an increase in policy interest rates, central banks could play a significant role in establishing a “green lending program” among commercial banks. As a critical conduit of monetary policy transmission, banks affected by the monetary restrictions could raise their lending rate. This possibly decreases the financing demand of manufacturing firms from the banking system, resulting in less investment in costly traditional technologies. As a result, if this policy is implemented properly, restrictions on monetary policy are expected to reduce CO2 emissions levels by encouraging the use of green technologies and reducing its reliance on detrimental technologies.

The current work could not avoid some limitations, which could leave potential spaces for further research on monetary policy—climate change nexus. First, there are some other determinants of CO2 emissions, which are not included in the present study such as renewable energy, globalization, innovation, and among others. Recently, digital industry (Wang et al., Citation2022), industrial structure (Zhao et al., Citation2022), and financial inclusion (Shahbaz et al., Citation2022), for example, is considered as an effective way to combat CO2 emission. By integrating these potentially relevant factors, further research could enrich the model employed in this paper. Second, current research mainly focuses on the ecological effect of monetary policy, which implies the deployment of similar research on the impact of other macroeconomic policies such as fiscal policy.

Our research highlights

Conventional Panel Ordinary Least Squares (OLS), Dynamic OLS, Fully-Modified OLS, Panel Quantile Regression, and two-step system GMM are applied to a sample of 14 selected emerging countries covering the period of 1998-2018.

Both regimes of monetary policy are captured in the identity function.

Contractionary and expansionary monetary policy both eliminate and escalate the environmental degradation through the increase in CO2 emissions, respectively.

The ecological effects of monetary policy are most visible in the middle-large quantile levels of CO2.

Correction

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

Acknowledgements

This research is funded by University of Economics Ho Chi Minh City (UEH). The first author is also greatful to the financial support from Van Lang University (VLU). This paper captures a part of the thesis conducted by Thanh Phuc Nguyen, Ph.D. Candidate of UEH, under the supervision of Tho Ngoc Tran. We also appreciate the valuable comments and suggestions from Le Van, Ho Hoang Gia Bao, Ha Van Dinh, Tri Minh Nguyen, Bao Cong Nguyen To and Luu Van Anh Dung that greatly improved the quality of this research. We are also very grateful to four anonymous referees for their constructive comments and suggestions. We are responsible for any remaining errors.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Thanh Phuc Nguyen

His research interests revolve around banking & finance, risk management, and financial management. He has currently served as an anonymous reviewer for Journal of Asian Business and Economic Studies (UEH).

His current research interests include banking & finance, risk management, and financial markets. Currently, he serves as a member of the National Financial and Monetary Policy Advisory Council.

She is currently a senior lecturer and the Dean of the School of Finance (University of Economics Ho Chi Minh City). Her current research interests include banking & finance, risk management, and financial markets.

He is a Ph.D. student at the University of Economics Ho Chi Minh City (UEH). He is also a lecturer at Vietnam’s Ho Chi Minh City University of Technology (HUTECH). His research interests include behavioural finance and markets, as well as empirical asset pricing.

She is a Ph.D. Candidate in the School of International Business Marketing from University of Economics Ho Chi Minh City, Vietnam (UEH). Her current research interests include sustainable marketing management and strategy, public relations, and minimalism.

Notes

1. To be readable, we display the word abbreviations and its interpretation in Table of the Appendix. We thank one anonymous reviewer for this suggestion.

3. Author’s calculation is based on the World Bank database in 2019.

4. We truly appreciate this suggestion from one anonymous reviewer.

References

- Adebayo, T. S., Akinsola, G. D., Bekun, F. V., Osemeahon, O. S., & Sarkodie, S. A. (2021). Mitigating human-induced emissions in Argentina: Role of renewables, income, globalization, and financial development. Environmental Science and Pollution Research, 28(47), 67764–29. https://doi.org/10.1007/s11356-021-14830-5

- Adedoyin, F. F., Alola, A. A., & Bekun, F. V. (2020). An assessment of environmental sustainability corridor: The role of economic expansion and research and development in EU countries. Science of the Total Environment, 713, 136726. https://doi.org/10.1016/j.scitotenv.2020.136726

- Ahmad, M., Khan, Z., Rahman, Z. U., Khattak, S. I., & Khan, Z. U. (2021). Can innovation shocks determine CO2 emissions (CO2e) in the OECD economies? A new perspective. Economics of Innovation and New Technology, 30(1), 89–109. https://doi.org/10.1080/10438599.2019.1684643

- Ahmad, M., & Khattak, S. I. (2020). Is aggregate domestic consumption spending (ADCS) per capita determining CO2 emissions in South Africa? A new perspective. Environmental and Resource Economics, 75(3), 529–552. https://doi.org/10.1007/s10640-019-00398-9

- Al-Mulali, U., Ozturk, I., & Lean, H. H. (2015). The influence of economic growth, urbanization, trade openness, financial development, and renewable energy on pollution in Europe. Natural Hazards, 79(1), 621–644. https://doi.org/10.1007/s11069-015-1865-9

- Ali, M. U., Gong, Z., Ali, M. U., Wu, X., & Yao, C. (2021). Fossil energy consumption, economic development, inward FDI impact on CO2 emissions in Pakistan: Testing EKC hypothesis through ARDL model. International Journal of Finance & Economics, 26(3), 3210–3221. https://doi.org/10.1002/ijfe.1958

- Allard, A., Takman, J., Uddin, G. S., & Ahmed, A. (2018). The N-shaped environmental Kuznets curve: An empirical evaluation using a panel quantile regression approach. Environmental Science and Pollution Research, 25(6), 5848–5861. https://doi.org/10.1007/s11356-017-0907-0

- Antweiler, W., Copeland, B. R., & Taylor, M. S. (2001). Is free trade good for the environment? American Economic Review, 91(4), 877–908. https://doi.org/10.1257/aer.91.4.877

- Arellano, M., & Bover, O. (1995). Another look at the instrumental variable estimation of error-components models. Journal of Econometrics, 68(1), 29–51. https://doi.org/10.1016/0304-4076(94)01642-D

- Asongu, S. A., Le Roux, S., & Tchamyou, V. S. (2019). Essential information sharing thresholds for reducing market power in financial access: A study of the African banking industry. Journal of Banking Regulation, 20(1), 34–50. https://doi.org/10.1057/s41261-018-0065-4

- Assenza, T., Gatti, D. D., & Grazzini, J. (2015). Emergent dynamics of a macroeconomic agent based model with capital and credit. Journal of Economic Dynamics and Control, 50, 5–28. https://doi.org/10.1016/j.jedc.2014.07.001

- Bakhsh, S., Yin, H., & Shabir, M. (2021). Foreign investment and CO2 emissions: Do technological innovation and institutional quality matter? Evidence from system GMM approach. Environmental Science and Pollution Research, 28(15), 19424–19438. https://doi.org/10.1007/s11356-020-12237-2

- Bashir, U., Yugang, Y., & Hussain, M. (2020). Role of bank heterogeneity and market structure in transmitting monetary policy via bank lending channel: Empirical evidence from Chinese banking sector. Post-Communist Economies, 32(8), 1038–1061. https://doi.org/10.1080/14631377.2019.1705082

- Bekhet, H. A., & Othman, N. S. (2017). Impact of urbanization growth on Malaysia CO2 emissions: Evidence from the dynamic relationship. Journal of Cleaner Production, 154, 374–388. https://doi.org/10.1016/j.jclepro.2017.03.174

- Bengochea-Morancho, A., Higón-Tamarit, F., & Martínez-Zarzoso, I. (2001). Economic growth and CO2 emissions in the European Union. Environmental and Resource Economics, 19(2), 165–172. https://doi.org/10.1023/A:1011188401445

- Berk, I., Kasman, A., & Kılınç, D. (2020). Towards a common renewable future: The system-GMM approach to assess the convergence in renewable energy consumption of EU countries. Energy Economics, 87, 103922. https://doi.org/10.1016/j.eneco.2018.02.013

- Bibi, F., & Jamil, M. (2021). Testing environment Kuznets curve (EKC) hypothesis in different regions. Environmental Science and Pollution Research, 28(11), 13581–13594. https://doi.org/10.1007/s11356-020-11516-2

- Blundell, R., & Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87(1), 115–143. https://doi.org/10.1016/S0304-4076(98)00009-8

- Blundell, R., Bond, S., & Windmeijer, F. (2001). Estimation in dynamic panel data models: Improving on the performance of the standard GMM estimator. Emerald Group Publishing Limited.

- Boutabba, M. A. (2014). The impact of financial development, income, energy and trade on carbon emissions: Evidence from the Indian economy. Economic Modelling, 40, 33–41. https://doi.org/10.1016/j.econmod.2014.03.005

- Burke, M., & Emerick, K. (2016). Adaptation to climate change: Evidence from US agriculture. American Economic Journal: Economic Policy, 8(3), 106–140. https://doi.org/10.1257/pol.20130025

- Canay, I. A. (2011). A simple approach to quantile regression for panel data. The Econometrics Journal, 14(3), 368–386. https://doi.org/10.1111/j.1368-423X.2011.00349.x

- Charfeddine, L., & Kahia, M. (2019). Impact of renewable energy consumption and financial development on CO2 emissions and economic growth in the MENA region: A panel vector autoregressive (PVAR) analysis. Renewable Energy, 139, 198–213. https://doi.org/10.1016/j.renene.2019.01.010

- Charfeddine, L., & Khediri, K. B. (2016). Financial development and environmental quality in UAE: Cointegration with structural breaks. Renewable and Sustainable Energy Reviews, 55, 1322–1335. https://doi.org/10.1016/j.rser.2015.07.059

- Chenet, H., Ryan-Collins, J., & van Lerven, F. (2021). Finance, climate-change and radical uncertainty: Towards a precautionary approach to financial policy. Ecological Economics, 183, 106957. https://doi.org/10.1016/j.ecolecon.2021.106957

- Chishti, M. Z., Ahmad, M., Rehman, A., & Khan, M. K. (2021). Mitigations pathways towards sustainable development: Assessing the influence of fiscal and monetary policies on carbon emissions in BRICS economies. Journal of Cleaner Production, 292, 126035. https://doi.org/10.1016/j.jclepro.2021.126035

- Cloyne, J., Ferreira, C., & Surico, P. (2020). Monetary policy when households have debt: New evidence on the transmission mechanism. The Review of Economic Studies, 87(1), 102–129. https://doi.org/10.1093/restud/rdy074

- Copeland, B. R., & Taylor, M. S. (2004). Trade, growth, and the environment. Journal of Economic Literature, 42(1), 7–71. https://doi.org/10.1257/.42.1.7

- Dafermos, Y., Nikolaidi, M., & Galanis, G. (2018). Climate change, financial stability and monetary policy. Ecological Economics, 152, 219–234. https://doi.org/10.1016/j.ecolecon.2018.05.011

- Dong, K., Dong, X., & Jiang, Q. (2020). How renewable energy consumption lower global CO2 emissions? Evidence from countries with different income levels. The World Economy, 43(6), 1665–1698. https://doi.org/10.1111/twec.12898

- Dong, K., Sun, R., Li, H., & Liao, H. (2018). Does natural gas consumption mitigate CO2 emissions: Testing the environmental Kuznets curve hypothesis for 14 Asia-Pacific countries. Renewable and Sustainable Energy Reviews, 94, 419–429. https://doi.org/10.1016/j.rser.2018.06.026

- Esso, L. J., & Keho, Y. (2016). Energy consumption, economic growth and carbon emissions: Cointegration and causality evidence from selected African countries. Energy, 114, 492–497. https://doi.org/10.1016/j.energy.2016.08.010

- Farhani, S., Chaibi, A., & Rault, C. (2014). CO2 emissions, output, energy consumption, and trade in Tunisia. Economic Modelling, 38, 426–434. https://doi.org/10.1016/j.econmod.2014.01.025

- Farhani, S., Shahbaz, M., Sbia, R., & Chaibi, A. (2014). What does MENA region initially need: Grow output or mitigate CO2 emissions? Economic Modelling, 38, 270–281. https://doi.org/10.1016/j.econmod.2014.01.001

- Flores, C. A., Flores-Lagunes, A., & Kapetanakis, D. (2014). Lessons from quantile panel estimation of the environmental Kuznets curve. Econometric Reviews, 33(8), 815–853. https://doi.org/10.1080/07474938.2013.806148

- Frankel, J. A., & Romer, D. H. (1999). Does trade cause growth? American Economic Review, 89(3), 379–399.

- Georgantopoulos, A. G. (2012). Electricity consumption and economic growth: Analysis and forecasts using VAR/VEC approach for Greece with capital formation. International Journal of Energy Economics and Policy, 2(4), 263–278. https://dergipark.org.tr/en/pub/ijeeep/issue/31902/350690

- Gertler, M., & Karadi, P. (2015). Monetary policy surprises, credit costs, and economic activity. American Economic Journal: Macroeconomics, 7(1), 44–76. https://doi.org/10.1257/mac.20130329

- Grimm, N. B., Faeth, S. H., Golubiewski, N. E., Redman, C. L., Wu, J., Bai, X., & Briggs, J. M. (2008). Global change and the ecology of cities. science, 319(5864), 756–760. https://doi.org/10.1126/science.1150195

- Gul, A., Xiumin, W., Chandio, A. A., Rehman, A., Siyal, S. A., & Asare, I. (2022). Tracking the effect of climatic and non-climatic elements on rice production in Pakistan using the ARDL approach. Environmental Science and Pollution Research, 1–15. https://doi.org/10.1007/s11356-021-17416-3

- Hoeffler, A. (2002). The augmented Solow model and the African growth debate. Oxford Bulletin of Economics and Statistics, 64(2), 135–158. https://doi.org/10.1111/1468-0084.00016

- Im, K. S., Pesaran, M. H., & Shin, Y. (2003). Testing for unit roots in heterogeneous panels. Journal of Econometrics, 115(1), 53–74. https://doi.org/10.1016/S0304-4076(03)00092-7

- Jalil, A., & Feridun, M. (2011). The impact of growth, energy and financial development on the environment in China: A cointegration analysis. Energy Economics, 33(2), 284–291. https://doi.org/10.1016/j.eneco.2010.10.003

- Jun, W., Mahmood, H., & Zakaria, M. (2020). Impact of trade openness on environment in China. Journal of Business Economics and Management, 21(4), 1185–1202. https://doi.org/10.3846/jbem.2020.12050

- Kao, C. (1999). Spurious regression and residual-based tests for cointegration in panel data. Journal of Econometrics, 90(1), 1–44. https://doi.org/10.1016/S0304-4076(98)00023-2

- Kearsley, A., & Riddel, M. (2010). A further inquiry into the pollution haven hypothesis and the environmental kuznets curve. Ecological Economics, 69(4), 905–919. https://doi.org/10.1016/j.ecolecon.2009.11.014

- Khattak, S. I., & Ahmad, M. (2021). The cyclical impact of green and sustainable technology research on carbon dioxide emissions in BRICS economies. Environmental Science and Pollution Research, 29, 22687–22707. https://doi.org/10.1007/s11356-020-11060-z

- Khattak, S. I., Ahmad, M., Khan, Z. U., & Khan, A. (2020). Exploring the impact of innovation, renewable energy consumption, and income on CO2 emissions: New evidence from the BRICS economies. Environmental Science and Pollution Research, 27(12), 13866–13881. https://doi.org/10.1007/s11356-020-07876-4

- Koc, S., & Bulus, G. C. (2020). Testing validity of the EKC hypothesis in South Korea: Role of renewable energy and trade openness. Environmental Science and Pollution Research, 27(23), 29043–29054. https://doi.org/10.1007/s11356-020-09172-7

- Koenker, R. (2004). Quantile regression for longitudinal data. Journal of Multivariate Analysis, 91(1), 74–89. https://doi.org/10.1016/j.jmva.2004.05.006

- Koenker, R., & Bassett, G.,sJr. (1978). Regression quantiles. Econometrica: Journal of the Econometric Society, 46(1), 33–50. https://doi.org/10.2307/1913643

- Le, H. P., & Ozturk, I. (2020). The impacts of globalization, financial development, government expenditures, and institutional quality on CO2 emissions in the presence of environmental Kuznets curve. Environmental Science and Pollution Research, 27(18), 22680–22697. https://doi.org/10.1007/s11356-020-08812-2

- Levin, A., Lin, C.-F., & James Chu, C.-S. (2002). Unit root tests in panel data: Asymptotic and finite-sample properties. Journal of Econometrics, 108(1), 1–24. https://doi.org/10.1016/S0304-4076(01)00098-7