Abstract

This paper expands on financial literacy, access to digital finance, and SME performance in the Central Region of Ghana. First, the study analysed SMEs’ digital platform knowledge and utilisation. It examined the relationship between financial literacy, access to digital finance, and SME performance. The paper discussed the mediating influence of access to digital finance on SMEs’ financial literacy and performance. The study employed the quantitative research approach. Using the purposive sampling technique, a total of 400 responses were gathered from SMEs in Cape Coast, Mankessim, Assin Fosu, Agona Swedru, and Kasoa. The study used self-administered questionnaires to collect data. SPSS was employed to evaluate descriptive statistics. Results show that SMEs in the study areas use Mobile Money more than any other digital platform. PLS-SEM was used to investigate the relationship between financial literacy, digital finance, and SME performance. It was found that financial literacy positively affects access to digital finance. Also, access to digital finance improved performance. Access to digital finance mediates the relationship between financial literacy and SME performance. Access to digital finance is as crucial as financial literacy for increasing performance. Therefore, using digital platforms to trade would boost business performance. Digital trading platform providers should improve advertising and make their systems user-friendly.

PUBLIC INTEREST STATEMENT

Previous research has demonstrated how access to funding and financial knowledge affect business performance. The ability to obtain financing by all ethical and practical ways is explained by having access to finances. Based on this, this study investigated if a manager of a SME’s financial literacy would affect their access to digital finance, which would ultimately affect business performance. The study concluded that Mobile Money was the most well-known and often used digital platform by managers of SMEs in these locations using data from SMEs in certain commercial districts in Ghana’s Central Region. Additionally, obtaining digital skills as a component of financial skills in order to access digital money improves performance in the same way as financial literacy improves the performance of SMEs. As a result, the research advised that programmes for SME managers and owners that teach financial literacy take into account digitalization.

1. Introduction

Approximately 70% of Ghana’s labour force is employed in the informal sector, which is dominated by small companies (Rural Enterprise Program, Citation2017). Small and medium-sized enterprises (SMEs) contribute significantly to the growth of Ghana’s rural economy by providing funds for family assistance and education for children and students across the country. According to a study undertaken by the International Trade Centre (ITC) (2019), fostering SME growth may contribute to achieving the Sustainable Development Goals (SDGs) by affecting individuals, business practices, sectors, and the national economy. SMEs in Ghana contribute significantly to the economy and society, yet they face a number of obstacles (ITC, 2019). According to the ITC, some of these obstacles include access to funding; lack of technology; high transaction costs; a high default risk relative to bigger rivals; interest rate limitations; low-quality credit; bureau information; an absence of acceptable collateral; and bad management. In addition, according to the Rural Enterprise Programme (Citation2017), bad management, lack of cash, a smaller volume per client, and lack of proper SME insurance restrict SMEs from developing and operating effectively. Enterprises fail when company performance is significantly impaired, unemployment rises, and children whose parents work in such businesses suffer considerably.

Numerous studies have been undertaken to identify characteristics that might favourably impact the performance of these firms in an effort to address these performance issues. These aspects include financial literacy; training and seminars; access to finances; sound company governance; venture capital; among others (Citation2022; Agyapong & Attram, Citation2019; Salia & Karim, Citation2019; Gathungu & Sabana, Citation2018; Hussain, Salia & Karim, Citation2018). Even though some of the aforementioned studies focused on financial literacy, which could lead to possible access to funds, they overlooked the significance of digitization, which could potentially lead to an increase in the businesses’ acquisition of funds through online savings, online trading, and internet banking, where loans could be easily acquired using the internet. Given the current situation of the financial world, financial literacy increasingly extends beyond the preparation and presentation of financial statements and business appraisals for fund-raising (Gomber, Koch, & Siering, 2017). In research on financial literacy, access to finance, and corporate success, the capacity of managers to expand access to finance through digitalization has received less attention. Access to digital finance is used as a mediator in this study because digitization is a current trend in both finance and the economy.

There are several studies on the importance of digitalization to economies and how it improves the financial performance of businesses (Agyapong, Citation2021; Ozili, Citation2018; Gomber, Koch, & Siering, 2017). Myovella, Karacuka, and Haucap (Citation2020) presented an innovation-based theory of economic development to explain the influence of technology, namely the digital economy, on economic growth and development. Firms must recognise that by granting access to all permissible digital systems, they may be able to attract more customers, resulting in an increase in revenue. Utilizing the resource-based theory, the impact of financial literacy and access to money on the performance of SMEs has been the subject of substantial research (Tuffour, Amoako, & Amartey, 2020; Agyapong & Attram, Citation2019; Salia & Karim, Citation2019; Gathungu & Sabana, Citation2018; Hussain, Mabula, & Ping, 2018). The Resource-Based Theory provides a framework for identifying which strategic resources a firm may employ to obtain a sustainable competitive advantage leading to performance. Some of these resources accessible are financial, legal, human, organizational, informational and relational. According to the resource-based approach, improving capabilities and resources results in a long-term competitive advantage and performance. Also, in the theory, a firm cannot function effectively if it has limited access to necessary resources. The bulk of these resources, such as human, legal and other resources, can only be obtained with adequate funding (Eniola et al., Citation2016). As a result, one of the most pressing challenges facing small businesses is financial resources, which if not available, can stifle their growth and performance.

Financial literacy has become more important in both emerging and developed economies because it has a substantial impact on financial decisions (Hussain et al., Citation2019). The way a company distributes, spends and manages its cash, according to Agyapong and Attram (Citation2019), is crucial to its performance. This means that a firm’s financial resources must be allocated, utilized and managed properly and efficiently by its management. A manager’s knowledge acquisition has been a matter of debate all over the world. Although other empirical evidence showed the reverse, many scholars think that business owners and managers must have some level of financial expertise or a good educational background to enable managers to make more efficient and effective use of limited resources by establishing efficient and effective financial management systems (Agyapong & Attram, Citation2019; Hussain et al., Citation2019; Amerteifio & Agbeblewu, ; Citation2015;).

According to the aforementioned research, the influence of financial literacy on the performance of SME management is both favourable and considerable. These studies also indicated that access to capital has a significant impact on a company’s success and that financial literacy is required to get capital. Regarding the performance of SMEs, less emphasis has been paid to the relevance of digitization, which might lead to a rise in the acquisition of money by businesses through online savings, online trade, and internet banking. It is necessary to understand how a manager’s financial literacy affects his capacity to access digital funds for commercial purposes. This study, therefore, sought to provide empirical evidence on the level of knowledge and usage of digital platforms by managers of SMEs. It also examined the relationship between financial literacy and access to digital finance, as well as access to digital finance and the performance of SMEs. Finally, the study sought to mediate the relationship between financial literacy and SME performance via access to digital finance.

The rest of the paper is organised as follows: The next section discusses the theoretical and empirical review of the study; section 3 covers the methods used for the study; and the discussion of results and conclusion are contained in sections 4 and 5 respectively.

2. Theory and hypotheses development

2.1. Resource-based theory

The resource-based theory was first propounded by Wernerfelt (Citation1984). The theory argues that resources are the most important factor for improving firm performance and staying highly competitive (Wernerfelt, Citation1984; Prahaland and Hamel, Citation1990b; J. Barney, Citation1991). These resources include financial (liquid and illiquid), human (competency), technology, marketing, and physical resources. Combining these resources with organisational processes and characteristics, the firm achieves corporate strategy (Andrews et al., Citation1965; J. Barney, Citation1991; Daft, Citation1983; Mata et al., Citation1995). These resources, according to the Resource-Based Theory, are the aspects of a firm that influence its profitability, progress, and performance. Such resources, according to this theory, should be in high demand, scarce and easily reproducible (Barney, Citation2001; Dierickx & Cool, Citation1989). Digital finance in this modern world has become a new development. There have been constant reforms in the use of these digital platforms, where usage has become very simple and fast to use. This has caused digitization to be in high demand among households and firms. Adding digital finance to trading will bring in more users (customers), which will lead to a lot of product sales for the business.

The scarcity of a resource in this context may mean that operating with digital platforms to source funds should be dynamic (Barney, Citation2001; Dierickx & Cool, Citation1989). It should be used in a way that the business will solely benefit from and also suit its operations. For example, SMEs could have a digital platform where getting access to their products and prices would be very accessible to more customers. These platforms could also facilitate payments and delivery of their products. Lastly, digital platforms are easily reproducible. Where one access exhausts its life span, new forms could be developed with a better upgrade. Resource-Based Theory explains that resources have a great impact on performance. Given that the human resources of the firm are financially literate, choosing, utilizing, managing, and disposing of financial assets would be done strategically (Agyapong & Attram, Citation2019). This will improve the performance of the business. Financial choice is one of the most significant decisions made by managers in the management of their firm. These decisions have a substantial impact on the profitability, growth, and long-term survival of a firm. The resource-based theory states that the possession, use, and commitment of resources are strategically important for value creation. That is, internal resources (human resources), when fully used, could help attract additional opportunities to create more value for the business (Minola & Cassia, Citation2012). So, management training to improve their financial skills will be able to get access to digital money and learn about its uses, how to get it, and the risks that come with it.

The Resource-Based theory also states that a firm will perform well when all the required resources are available to such a firm. Financial resources enable organisations to get other forms of resources that are useful in their operations (Stacey, Citation2011). To clarify, obtaining skills in terms of technological upgrades and in all areas of the business would be straightforward if the management of SMEs had sufficient financial resources. Accommodating low-cost digital platforms such as Mobile Money will increase sales. An increase in profit due to high sales would help in acquiring other resources that the business needs. The firm’s performance would also improve if all of these resources were obtained (Agyapong & Attram, Citation2019). The Resource-Based theory literature has largely believed that a firm’s performance is influenced by the proper combination of its resources and abilities. The resource-based theory is a strategy for improving corporate performance by using available resources to gain or retain a competitive advantage over time. Businesses produce value through managing resources for customers to enjoy their offerings, according to the idea (Henard & McFadyen, Citation2012; Wernerfelt, Citation1984). According to this study, organisations with access to digital finance may be able to match current economic trends. This will improve their efficiency, and creditors who supply cash via digital ways, as well as consumers who do business via digitised methods, will benefit. Adoption of digital systems by small SMEs will enhance their cash in hand if adequate measures are taken to account for all hazards (Stacy, Citation2011). There haven’t been many comprehensive studies of how specific knowledge resources, like financial literacy, affect the ability of SMEs to adopt digitised financial systems and get digital funds. This study adds to the literature by focusing on access to digital finance and how it affects the relationship between financial literacy and the performance of SMEs.

There is no literature on the relationship between financial literacy, access to digital finance, and the performance of small and medium-sized enterprises (SMEs) in Ghana. In Ghana’s Central Region, Agona Swedru, Kasoa, Assin Fosu, Mankessim, Cape Coast, Dunkwa, On-Offin, Twiffo Praso, and Jukwa are all highly commercialised cities (Boadi-Kusi, Kyei, Asare, Owusu-Ansah, Awuah, & Darko-Takyi,). The contributions of these localities to regional economic statistics are well-known. Based on this backdrop, this article investigated the level of knowledge and usage of digital platforms by small and medium-sized enterprises (SMEs), the relationship between financial literacy and access to digital financing, and access to digital financing and the performance of SMEs. The last part of the paper looked at how access to digital finance affects the relationship between financial literacy and the performance of small and medium-sized businesses (SMEs) in Agona Swedru, Kasoa, Mankessim, Cape Coast, and Assin Fosu, which are all commercial towns in Ghana’s Central Region.

Hypothesis development

3. Financial literacy and access to digital finance

Buchdadi (2020) concluded that financial literacy improved access to finance. However, digital financing was not considered in the measurement of access to finance. In his paper, financial literacy was restricted to the preparation and presentation of financial statements, with no mention of digitization. Konigsheim, Lukas, and Noth (2017) also showed that being financially literate is linked to being able to use digital financial services in a way that is helpful and useful.

In their study, Kulathunga et al. (Citation2020) identified technical literacy as a body of knowledge distinct from financial literacy. Access to digital finance was viewed as knowledge acquisition in the study, which was done in Kenya and was explained as something management must possess. For the purpose of this research, access to digital finance is perceived as a service that managers in Ghana would have to introduce to their businesses. Studies on the relationship between financial literacy and access to digital finance have received less attention in Ghana. This is why the purpose of this research is to see how financial literacy affects access to digital funding in the selected commercial areas, namely; Agona Swedru, Kasoa, Mankessim, Cape Coast, and Assin Fosu.

Hypothesis 1 There is a positive relationship between financial literacy and access to digital finance.

4. Access to digital finance and performance of SMEs

Kulathunga et al. (Citation2020) discovered that technology literacy boosts SMEs’ performance, with technology knowledge referring to a manager’s capacity to profit from financial growth revolutions by introducing digital financial services. In the study, access to digital finance was regarded as knowledge acquisition and it was presented as something a manager needs to boost the firm’s performance. It was observed that researcher data relating to the digital channels utilised as access to digital finance is either very limited or not empirical. Furthermore, Agyapong (Citation2021)Citation2021 discovered mobile money platforms are widely accepted for payment. It was revealed that organisations are incorporating digitization into their service delivery. However, the study did not analyse the relationship between the usage of digital platforms and an SME’s performance and it was just exploratory research.

According to studies such as Siddik, Kabiraj, Shanmugan, Yanjuan, Citation2016; ; Hernando, & Nieto, Citation2007), technological investments take longer than two years to pay off. This raises an essential question that has been ignored in the literature: how much should be digitised and what should the ideal digitization look like in terms of return on investment (both monetary and nonmonetary)? What other factors influence this ideal digitization? It may be fascinating to see if, for example, technological innovation and client awareness are progressing at the same rate. Although the majority of research shows that digital financial services improve a company’s performance and profitability (Abbasi & Weigand, Citation2017; Ozili, Citation2018), the paucity of studies in this area indicates that no studies have been able to refute this conclusion.

Hypothesis 2 There is a positive relationship between access to digital finance and the performance of SMEs

5. Financial literacy, access to digital finance and performance of SMEs

In their study, Eniola and Entebang (2018) stated that an owner-manager who is financially educated and understands the influence of financial decisions on business performance at all stages of growth knows where to acquire the finest goods and services and communicates with suppliers with confidence. Marriott et al. (Citation1996) defined financial literacy as a manager’s ability to behave ethically while also comprehending and evaluating financial facts. Lusardi and Tufano (Citation2008) emphasised the impact of financial literacy on managers’ competency and decision-making. There was also a focus on one type of financial literacy in particular (debt literacy).

Also, the practical experience offers a foundation for knowledge and other components of financial literacy, according to Lusardi and Tufano. According to Atakora (Citation2013), traders with a high degree of education have a greater level of financial literacy than those who are uneducated. The Kumasi Central Market was used as a focus group, and the results showed that market women with more job experience knew more about money.

A few studies (Tuffour, Amoako, & Amartey, 2020; Agyapong & Attram, Citation2019; Salia & Karim, Citation2019; Gathungu & Sabana, Citation2018; Hussain, Mabula, & Ping, 2018) focused on financial literacy and business performance as well as the relationship between financial literacy and access to funds. Although the research above focused on financial knowledge and money availability, it overlooked the impact of digital finance, particularly access to digital finance. SMEs used access to finance to mediate financial literacy and their performance, while digital access was mostly ignored. (Gomber, Koch, and Siering, 2017) say that financial literacy goes beyond making and presenting financial statements because of the way the financial world is right now.

In research on financial literacy, access to finance, and firm performance, the issue of digitization as a feature of management to improve access to money has received less attention. There is a lot of information about how vital a digitalized system is for economies and how it aids corporations in their financial performance (Agyapong, 2020; Ozili, Citation2018; Gomber, Koch, & Siering, 2017). Myovella, Karacuka and Haucap (Citation2020) proposed an innovation-based theory of economic development to explain the influence of technology, particularly the digital economy, on economic growth and development. In their study, digitization promotes economic growth.

According to Kulathunga et al. (Citation2020), techno-finance literacy has a substantial impact on the performance of SMEs, drawing on the assessments based on knowledge base theory and evolutionary theory of economic transformation. According to Kulathunga, Ye, Sharma, and Weerathunga, SMEs must investigate feasible technological changes in the environment to improve their performance. Firms must recognise that by granting access to all sorts of allowed digital systems, they may be able to attract more clients, which will result in greater cash flow.

The relevance of financial literacy and access to funds on the performance of SMEs has been extensively studied by (Tuffour, Amoako, & Amartey, 2020; Agyapong & Attram, Citation2019; Salia & Karim, Citation2019; Gathungu & Sabana, Citation2018; Hussain, Mabula, & Ping, 2018). The above studies found the impact of financial literacy on the performance of SMEs to be positive and significant. These studies also found that access to funds greatly affects the performance of a business and that to be able to acquire funds requires some level of financial literacy. With regard to SME performance, the importance of digitization, which could lead to an increase in the acquisition of funds by the business through online savings, online trading, and internet banking, has received less attention. There is a need to know how a manager’s financial literacy level could influence his ability to access funds digitally for a business. This is why the study looks at how access to digital finance affects the relationship between financial literacy and SME performance.

Hypothesis 3 There is a mediating effect of access to digital finance on the relationship between financial literacy and the performance of SMEs

6. Methodology

Sample

Agona Swedru, Kasoa, Cape Coast, Mankessim, and Assin Fosu were chosen as the research locations. Because of the business activities that take place in these towns, these locations were chosen. According to the Directorate of Chamber of Commerce in Ghana’s Central Region, these towns are part of an eight-town cluster that is highly commercial and contributes significantly to the region’s small company performance (Boadi-Kusi, Kyei, Asare, Owusu-Ansah, Awuah, & Darko-Takyi,). It is home to a large number of enterprises and firms, as well as a sizable population. These towns are usually bustling and well-known for their business activity, which draws visitors from all over the world. These locations were chosen for this study because they are the busiest in the region. They have retail stores and business warehouses. This made gathering the information needed to meet the study’s objectives much easier. The SMEs in the commercial areas of the Central Region were the study’s target population. Based on the Regional Project on Enterprise Development Ghana, the Teal (2002) classification of SMEs was used, where microenterprises have fewer than 5 employees, small enterprises have 5–29 employees, and medium enterprises have 30–99 employees. Therefore, owner-managers in charge of businesses with an employee size of between 0 and 99 were the target population.

Managers of SMEs were selected using the purposive sampling approach in the five selected commercial districts of Ghana’s Central Region. This technique was used because there was no data on the total number of SMEs operating in these areas. The study used an estimated minimum sample size of 384, proposed by Krejcie and Morgan (Citation1970) as the minimum sample. The data was collected between the periods of April 2021 and July 2021. To curb biased responses, every firm that exhibits the characteristics of an SME qualified for the study. Owner-managers of small and medium-sized companies in these locations responded to the survey. A total of 400 responses were received from the 400 questionnaires shared. Only those who consented to take part in the study were involved. Self-administered questionnaires were utilised to collect information for this study. The questionnaire, which was the main data collection strategy, consisted of both closed and open-ended items and was delivered to the targeted group. Questions were asked in the English language. Some business owners were unable to read or write. There was a need for questionnaires to be interpreted and translated for them. This was done by research assistants who were employed specifically for this study.

To avoid common methods of bias or variance, questions were interspersed with unrelated items to determine how thoroughly respondents answered the questions. There were two parts to the questionnaires. The first portion of the survey was used to collect demographic data, which was categorically measured. The questionnaire’s second part was divided into three sections. The purpose of the first portion, Section A, was to assess financial literacy. All of the questions in this section were rated on a ten-point scale, with one being the lowest and ten being the highest. Section B was used to assess digital financial access, which was similarly graded on the same scale. The final component, Section C, consisted of performance-related questions. Respondents were asked to rate their performance on a ten-point scale, exactly as they had in the previous sections.

7. Measures

Independent variable

The concept of financial literacy was measured using previously validated instruments to include; financial skills, financial behaviour, and financial knowledge (Houst, 2012). The questionnaires consisted of 15 items which respondents were asked to rate the number of times they perform such activities.

Dependent Variable and Mediating Variable

This section consists of performance-related questions. Performance was measured using validated instruments; Capital expenditure, revenue growth and cost of production (Cicea, Popa, Marinescu, & Catalina, 2019). Respondents were asked to rate their performance on a ten-point scale, exactly as they had in the previous sections. To ensure that construct measures are truly distinct from those of other constructs, Discriminant Validity was used. This indicates that the constructs used are unique and capture phenomena that the model’s other constructs do not (MacKinnon, 2008). To measure access to digital finance, Alliance for financial inclusion (Citation2016) measurement for access to finance was adopted and modified. The items were; extent of access to digital finance, proximity to digital finance and tightness of digital platform conditions. Items were put on a rating scale to rate their access to digital finance. Lastly, the performance of SMEs was measured using a ten-point rating scale. The questionnaire was divided into four sections. Section A asked questions on the demographics of the respondents, section B was to assess financial literacy. All of the questions in this section were rated on a ten-point scale, with one being the lowest and ten being the highest. Section C measured access to digital finance, which was similarly graded on the same scale.

7.1. Mediation procedure

Hair, Hult, Ringle and Sarstedt (2017), defined mediating as the effect that occurs when a third constructor variable is introduced between two other related constructs or variables. The third variable, also known as the mediating variable, absorbs a portion of the relationship between the dependent and independent variables in the partial least square route model. In this method, the mediator reveals a true link between the dependent and independent variables. In this study, the relationship between financial literacy (independent variable) and the performance of SMEs in Central Region commercial areas (dependent variable), is mediated by access to digital finance. Hair et al established a systematic mediator analysis process in partial least square structural equation modelling. The present mediation literature, according to Hair et al (2017), discusses two forms of mediation: complete and partial mediation. Complementary and competitive partial mediation are two types of partial mediation. depicts the mediation procedure used in this investigation.

Figure 1. Mediator analysis procedure in PLS-SEM.

8. Empirical method

8.1. Knowledge and frequency of use of digital platforms

showed the results of descriptive statistics on the knowledge of digital platforms of respondents (managers and or owners of SMEs)

Table 1. Knowledge of digital platforms by managers of SMEs

Respondents were given five sets of digital platforms to rank their level of expertise on each platform, with 1 being the least and 10 being the most. There was also the option to incorporate and rate any additional digital platform they wanted; in addition to the one, they were given. The mean (M) and standard deviations (SD) for each of the items indicated as digital platforms, with the possibility to add any other, are calculated in . We may deduce from that SMEs’ managers and/or owners have a higher level of expertise in mobile money than any other digital platform (M = 8.16, SD = 1.952).

Table 2. Frequency of use of digital platforms by managers of SMEs

Furthermore, respondents evaluated mobile banking much higher than the other options, with (M = 4.20, SD = 3.481) being the second highest. Payment (card acquiring and other services) was the following item after mobile banking and it received the same rating approach (M = 3.46, SD = 2.841). Cryptocurrency (M = 1.77, SD = 1.823) and Paypal (M = 1.74, SD = 1.840) came in fourth and fifth respectively. The option to select any other digital platform except the ones specified above had the lowest average (M = 1.03, SD = .461).

showed the results of descriptive statistics on the frequency of use of digital platforms by respondents (managers and or owners of SMEs)

, showed the result of descriptive statistics on the use of digital platforms by respondents. Respondents were given five sets of digital platforms and asked to rate their frequency of usage of each digital platform on a scale of one to ten, with one being the least used and ten being the most used. The mean (M) and standard deviations (SD) for each of the items mentioned as digital platforms are determined in shows that SMEs’ managers and/or owners utilize mobile money more frequently than any other digital platform (M = 8.15, SD = 2.052).

Table 3. Validity and reliability

In addition, respondents gave mobile banking a better rating than the rest, with (M = 3.81, SD = 3.435) to the statement. Payment (card acquiring and other services) was the next item after mobile banking and it was rated similarly to mobile banking. (M = 2.98, SD = 2.672) followed by Cryptocurrency with (M = 1.42, SD = 1.382) and lastly Paypal with (M = 1.39, SD = 1.209). The option to select any other digital platform except the ones specified above had the lowest average (M = 1.26, SD = 1.402). From the analysis, the study found that, among the digital platforms in this study, Mobile Money was the most used.

9. Assessment of the PLS-SEM

The measuring models used in this study were explained in this section. Model measurement evaluation was done by using indicator loadings, internal consistency reliability (Composite reliability, construct reliability, Cronbach’s Alpha,), discriminant validity (Fornell-Lacker) Collinearity (VIF) and convergent validity (AVE-Average variance extracted). To give indications for the measurement model’s evaluation, a consistent PLS approach was used. The following tables describe the findings.

9.1. Assessment of measurement models for the study

To assess the measurement models of the study, internal consistent reliability (Cronbach’s Alpha, Composite reliability), Convergent Validity (AVE), discriminant validity (Fornell Lacker criterion) and cross-loadings of variables were examined.

9.2. Assessing internal consistency reliability

The composite reliability was used to assess the constructs’ internal consistency dependability in this study. Cronbach’s alpha is a less adequate metric of internal consistency than composite reliability (Rossiter, 2002). shows that all latent variables in this investigation are dependable since they all loaded around the .70 threshold by the end of the trial (Bagozzi, and Yi, 1988). Financial literacy had the highest composite dependability score (.939), followed by SMEs’ performance (.929) and last, access to digital finance (.894).

According to Cronbach (1951), a data collection instrument must have a Cronbach alpha value of 70% or higher to be considered reliable. As shown in the table above, reliability was above acceptable levels (Cronbach’s alphas >.70, Average Variance Extracted >.50, composite reliability >.70), according to scholars (Fornell and Larcker, 1981). Convergent validity was also evident in the factor loadings (which ranged from .585 to .631). This model’s constructs can account for more than half of the variation in their indicators, with Financial Literacy being the most important and Access to Digital Finance being the least important. As part of the measurement model evaluation, discriminant validity was also assessed.

9.3. Assessing discriminant validity

The capacity of a construct to capture phenomena that aren’t represented by other constructs in the model is referred to as discriminant validity (MacKinnon, 2008). The Fornell-Lacker criteria were employed to evaluate discriminant validity in this study. To compare the square root of the AVE values to the latent variable correlations, the Fornell-Larcker criterion was employed (Fornell & Larcker, 1981). The square root of each construct’s AVE should, in particular, be higher than the greatest correlation with any other construct (Hair et al. 2013). As demonstrated in , the square root of each variable is significantly greater than its correlations with other study components. This means that each construct is distinct from the others and no two can accurately represent the same occurrence.

Table 4. Fornell-lacker criterion

From , it could be deduced that all the factorial loadings in their respective latent variables (constructs) are larger than all the other correlation values among the latent variables. This implies that each construct was truly distinct from the other thus ensuring uniqueness in measurement.

Assessing Indicator Loadings

represents the cross loading structure for access to digital finance indicates that 6 out of the 14 items range from (.740-.800). Financial literacy had 9 out of the 15 items ranging from (.720–857) and performance had 8 out of the 14 items ranging from (.715-.851). This indicates that the factor extracts sufficient variance

Table 5. Cross loading of variables

9.4. Assessing the structural model

shows the findings of assessing multicollinearity among the variables for this study. In the context of PLS-SEM, a tolerance value of .20 or lower and a VIF value of 5 or higher indicate a potential collinearity problem, respectively (Hair et al., 2011). A VIF rating of 5 indicates that the other formative indicators associated with the same concept account for 80% of the variance in the indicator. In terms of access to digital financing and financial expertise, shows a minimum VIF of 1.593 and a maximum VIF of 1.893. According to the findings of this investigation, there was no multicollinearity between the indices.

Table 6. Collinearity amongst constructs

The absence of common method bias is further supported by the VIF results in . The existence of a VIF value of more than 3.3, according to Kock and Lynn’s (2012) criterion, is a symptom of pathological collinearity, as well as an indicator that a model may be contaminated by common method bias. As a consequence, if all VIFs generated from a comprehensive collinearity test are equal to or less than 3.3, the model is free of vertical and lateral collinearity, as well as common method bias (Kock, 2013).

10. Results

10.1. SEM For dependent and independent variables

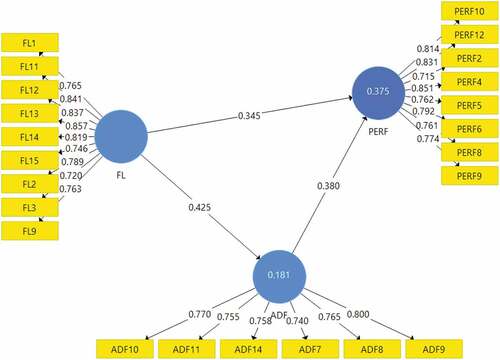

To increase the overall model’s reliability, any indicator that loaded below the threshold of .7 was removed, as advised by Hair et al (2016). Financial literacy (FL4, FL5, FL6, FL7, FL8 and FL10) were removed, as well as access to digital finance (ADF1, ADF2, ADF3, ADF4, ADF5, ADF6, ADF12 and ADF13) and performance (PERF 1, PERF3, PERF 7 and PERF11, PERF 13 PERF 14) depict the structural equation model based on the study’s objective three.

Figure 2. Structural equation modelling.

10.2. Assessing coefficient of determination and predictive relevance

According to Hair et al. (2014), structural models with coefficients of determination (R2) of .025, .500 and .750 are weak, moderate and significant, respectively. Whiles predictive relevance Q2 of “.002, .150 and .350” are deemed “small, medium and large,” respectively, for structural models, according to the author. Financial literacy and access to digital finance have a modest (.181) coefficient of determination, accounting for 18.1 % of the variation in SMEs’ performance, according to . The findings show that the model has a moderate predictive significance on the endogenous variable in terms of predictive relevance (0.1007). This indicates that the independent variables can predict the dependent variable with accuracy.

Table 7. Path estimation results for financial literacy and access to digital finance

Based on route estimation in , the PLS-SEM results indicated that financial literacy had a significant and a positive influence on access to digital finance (β = .425, p-value = .000). From the analysis in , it was found that where a manager is financially literate, there is a 42.5% chance of trading with digital platforms. That is once a manager has a high level of financial knowledge, he or she may access digital finance.

The PLS-SEM results showed that Access to Digital Finance had a substantial positive effect on the performance of SMEs (β = .380, p-value = .000) based on path estimate. This is illustrated in .

Table 8. Path estimation result of access to digital finance and performance of SMEs

Based on the results from , access to digital finance improved performance by 38%. As a result, the study supports the assertion that access to digital finance can enhance SMEs’ performance.

11. Post hoc analysis

The particular indirect effect was analysed to establish the type of mediating effect proposed based on the positive significant effect of the mediating variable (access to digital finance) on financial literacy and SMEs performance (Niltz et al., 2016; Hair et al., 2017). The relationship between financial literacy, access to digital finance and SMEs’ performance was assessed using mediation analysis. As a result, the hypothesis was put to test in terms of the indirect and direct effects. display the results of the specific direct and indirect effects.

Table 9. Total mediating effect

Table 10. Indirect Relationship

indicates the significance of each of the model’s recommended paths. It shows that access to digital finance, has a positive impact on SMEs’ performance, with a significant p-value of .000 and a coefficient of .380. There was a positive significant association between financial literacy and access to digital finance, with a p-value of .000 and a coefficient of .425. Also, financial literacy has a positive relationship with SMEs’ performance and the relationship is significant, with a p-value of .000 and a coefficient of .345. The coefficient of determination and predictive significance of the model on the dependent variable are shown in .

According to the findings, access to digital finance accounts for 18.1% of the total variation in the dependent variable. The complete model explains 37.2% of the variance in SMEs’ performance. According to Chin (1998), an R2 value of 48 % indicates moderate variance, which is sufficient (Hair et al, 2017). Furthermore, the findings show that the mediating variable is responsible for 17.9% of the variance in access to digital finance and 37.2% of the variation in performance throughout the whole model. Stone-Q2 Geisser’s statistic was used to determine the model’s predictive relevance (Stone, 1974). The model has a predictive relevance of 10.07 % for access digital to finance and 16.40 % for performance, according to Hair et al indicating lower predictive significance (2016).

shows that the relationship between financial literacy and SMEs’ performance is mediated by access to digital finance. Based on Carrión et al. (2017) criteria, it can be determined that partial mediation exists. This is because financial literacy has a substantial direct influence on SMEs’ performance (p-value = .000, ). Findings from these results show that having access to digital finance can improve the relationship between financial literacy and performance by 16.2% when adopted.

Based on these findings, the path between financial literacy and performance is reduced to 16.2%. This means performance can be achieved quicker with access to digital finance. To explain the effects of technology, particularly the digital economy, on economic growth and development, Myovella et al. (Citation2020) offered the innovation-based theory of economic development. Thus, techno-finance literacy has a significant influence on SMEs’ performance. Kulathunga et al. (Citation2020) supported these findings drawing on an evaluation base perspective and evolutionary theory of economic change.

12. Discussion

From the analysis, the study found that, among the digital platforms in this study, Mobile Money was the most popular. It could be observed that when it comes to knowledge of digital financial services, say MoMo, management of SMEs has that to some extent. This makes Momo easy to use as compared to the others. Knowledge of other digital products was lower because respondents explained that there was little or no training from the providers on their usage as compared to MoMo. Nonetheless, the inclusion of MoMo into their businesses has expanded their client base. This has improved the finances of the business through digital trading, savings, etc., leading to an increase in financial performance as explained by the Resource-Based Theory. Also, these findings were consistent with the findings of a report published by the GSMA in 2015 that found knowledge of digital platforms, such as Mobile Money, has not been a hurdle for its users as compared to other digital platforms (GSMA, Citation2015).

Business owners registered as Mobile Money agents deal directly with banks to ease payment and receipt of cash transactions on a regular basis, and this increases their level of knowledge (Atakora, Citation2013). In his study, Atakora (Citation2013) stated that understanding of Mobile Money as compared to other kinds of digital platforms is influenced by the experience with digital platforms among traders. Thus, utilising Mobile Money regularly may provide you with sufficient understanding of how to transmit and record received funds. This helps to explain why SME managers ranked their knowledge of mobile money higher than the rest of the digital platforms.

Also, the study found that, among the digital platforms in this study, Mobile Money was the most used. These findings resonate with a report by the Ministry of Finance (2018), which states that the most popular digital platform in Ghana was Mobile Money. According to Manjang and Naghavi (2021), mobile money was very popular in households owing to its flexibility in usage. This could be explained by the fact that mobile money is easy and simple to use. It may require little effort as compared to the others to complete a transaction. GSMA (Citation2015) reported that, when utilising Mobile Money, for example, one may transact business without being conversant with the system because an agent is ready to help. Other digital platforms do not have such a system. Due to little or no training for products like mobile banking, cards, and QR-codes and insecurities such as fraud with the use of mobile banking, their level of confidence to use these products, especially mobile banking, is very low. Mobile money, on the other hand, has agents that transact businesses on behalf of businesses and individuals whenever the need arises. This contributes to the frequency of use of Mobile Money as compared to the others. It was also found that products like Paypal and cryptocurrency were not legally regulated in Ghana, which is not well known to lead to less usage.

The study examined the relationship between financial literacy and access to digital finance. It was revealed that once a manager has a high level of financial knowledge, he or she may access digital finance. This result confirms the assumptions of the resource-based theory, which suggests that the acquisition of higher knowledge in operations builds the capabilities and competencies of the human resources of a firm to yield competitive advantage and higher firm performance. This means that broader knowledge of finance will influence management’s ability to seek funds from all legal sources, including digital means. In support of these results, Königsheim, Lukas, and Nöth (2017) found that financial competence is strongly associated with the likelihood of utilising digital financial services.

The study also examined the relationship between access to digital finance and the performance of SMEs. Based on the results, access to digital finance improved performance. As a result, the study supports the assertion that access to digital finance can enhance SMEs’ performance. This is backed by Ozili (Citation2018) and Abbasi and Weigand (Citation2017), who found that having access to digital financing has a beneficial impact on business performance. Also, (Agyapong & Attram, Citation2019; Hussain et al., Citation2019; Okello et al., Citation2017), they found usage of digital currencies for digital channels, firms’ access to funds has an impact on performance and growth. This is further supported by the Resource-Based Theory, which states that businesses or corporations will function successfully if all the necessary resources, including digital ones, are available. Therefore, firms would perform much better if a resource (a digital way of getting cash) was made accessible and available. Financial resources enable organisations to get other forms of resources that are useful in their operations (Stacey, Citation2011). Even though the study confirms that access to digital finance enhances performance, other authors posit that such an effect might be in the long run (Siddik, Kabiraj, Shanmugan, & Yanjuan, 2016; Van Uyen, & Phuong, 2015; Ceylan, Emre, & Asl, 2008; Hernando, & Nieto, 2007).

The study examined the mediating role of access to digital finance between financial literacy and the performance of SMEs. Access to digital finance partially mediates the relationship between financial literacy and the performance of SMEs. This means that managers of SMEs can equally achieve improved performance when there is an existence of financial literacy in the acquisition of digital finance. A study by (Tuffour, Amoako, & Amartey, 2020; Agyapong & Attram, Citation2019; Salia & Karim, Citation2019) showed that financial literacy has a significant impact on a firm’s performance because it leads to higher financial decisions, which improve the performance of a business. The studies recommended the need for SMEs to explore more options to raise funds for their businesses. With regards to these recommendations, access to digital finance was adopted in this study to test how a manager’s financial literacy could lead to his or her quest to include digitization in their operation using the resource-based theory and the evolutionary theory of change. With the results above, it is observed that the assumptions made by the theories mentioned above hold. The resource-based theory posits that a firm would perform well when all the resources needed for business operations are made available. The above results show that, where a manager of an SME is financially literate and uses all his or her knowledge to operate digitally to acquire digital funds, it is statistically proven that the performance of the firm will increase by 16.2%.

The findings are also in line with the assumptions made by the resource-based theory, which states that competitive advantage can be achieved by a firm when they can use their internal capabilities to influence the external environment to their advantage. This emphasised the need to seek out innovative ways to improve company performance (Nelson, Citation2009). Early developers of the theory explained technologies with regard to plants and machinery. Adoption of digitised systems for trade indicates that you are innovative as a business. From this perspective, some internal characteristics, such as access to digital finance practices, may be dependent on the evolution of technology by firms. As the economy is always in the process of change, there is a need for businesses to also evolve. This means performance can be achieved quicker with access to digital finance.

Managers should consider expanding their payment models to embrace digital payments to grow their client base and sales. Specifically, they should grow and broaden their mode of transactions to include the digitization of trade receipts and payments. This is because most customers today prefer the cashless manner of commerce for security reasons like robbery. This will in turn result in more sales, which will lead to increased revenue and improved financial performance for the SME. Managers of SMEs should also get training and workshops on how to use technology.

Also, as a policy, the government and relevant stakeholders should make laws to regulate online trading. This will increase the confidence of managers of these SMEs to adopt digitization in trading. The Ghana Chamber of Commerce and other stakeholders must encourage managers of SMEs and citizens to use the digital platforms available in Ghana using the media and any other rightful channel. The government and other stakeholders should make efforts to pass a law that will regulate the operations of these digital service providers. This is because most businesses depend on them to trade and that any negative action by them would impede the performance of SMEs and, consequently, their survival.

Concerning the resource-based theory used in this study, it is recommended that further developments in the theory should stress the importance of intangible resources and digitization in yielding performance. The current state of this theory focuses more on tangible resources with less attention on intangible resources and other technological changes such as knowledge and digitization. This is because digitization is a form of technological change (resources) in the business world.

13. Contribution to theory and literature

The research added to the body of knowledge by highlighting the significance of digitized finance in the relationship between financial literacy and SMEs’ performance in Ghana. First of all, the main contribution to this increases the understanding of financial literacy and access to digital finance. Previous studies have explained the important role financial literacy play in fund acquisition of which access to digital finance was less talked about particularly in the Ghanaian small business environment. However, this study finds that access to digital finance is mostly influenced by management’s literacy in finance.

Second, with respect to access to digital finance mediating the relationship between financial literacy and performance, little or no attention has been given to it. Most studies in this area focused on digitization and its implications for economies, financial literacy and its implication on business. Studies on digital platforms accessible to developing countries like Ghana have been extensively studied. These studies were all exploratory research and failed to talk about how the adoption of these digital services has an impact on these businesses. This mediating effect is explained using the Resource-Based Theory. The theory explains that a business’s performance will improve where the business in question has the required resources that are tangible and intangible (knowledge-financial literacy).

In solving the problem of performance among SMEs, Gathungu and Sabana (Citation2018) mediated access to finance on entrepreneur financial literacy and performance and had a significant relationship. Adomako, Danso and Ofori (2016) in their studies moderated financial literacy on access to finance and performance and also had a positive and significant relationship. These studies emphasised the fact that funds were the pressing needs of businesses and recommended that businesses include innovative ways to seek funds. For the purpose of this study, the inclusion of access to digital finance as a mediating variable is motivated by the current financial and economic development which focuses on digitisation.

14. Implications for practitioners

The study is useful to SMEs in the commercial areas in the Central Region of Ghana. The outcome of the study is expected to inform managers of SMEs about the need to enhance their financial literacy to fulfil current financial demands and make more informed financial decisions to help their business performance. It gives insight into the benefit of trading with various digital platforms accessible in the country to enhance the performance of their businesses. Policymakers such as the government, regulators of digital financial services, the Ministry of Trade and Industries and other lawful policymakers should establish legislation to accommodate different legal forms of digital financial services to boost the performance of SME.

15. Limitations and further research

A cross-sectional survey was used to gather data for the study. However, the longitudinal study methodology could have revealed a more accurate measurement of these organizations’ performance. It is suggested that more research be done on how financial technology literacy affects the use of digital financial platforms. Also, studies on how age influences the usage of financial technology and the frequency with which it is used should be conducted. A longitudinal replication of this study will also aid in exposing how access to digital finance will affect corporate performance in the long run.

16. Conclusions and implications

The findings revealed that financial literacy had a significant relationship with access to digital finance. This showed that if management is financially knowledgeable, they can easily access cash via digital means. Also, access to digital finance was found to have a significant and positive relationship with performance. This means that having access to digital financing has a significant effect on SMEs’ performance. It was discovered that access to digital finance partially mediates the relationship between financial literacy and SME performance. This indicates that management can achieve quicker performance if they can introduce digital platforms in their business.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Stephanie Efua Frimpong

Stephanie Efua Frimpong is a Graduate Assistant at the University of Cape Coast’s Department of Finance. The University of Cape Coast Business School awarded her a Master of Commerce (Finance) degree. Her current research interests include digitalization, development economics, and small and medium-sized enterprises. This report is part of a larger study on the influence of digitalization and financial literacy on the performance of small and medium-sized enterprises (SMEs) in Ghana.

Gloria Kakrabah-Quarshie Agyapong is a Senior Lecturer in the Department of Marketing and Supply Chain Management, University of Cape Coast, Ghana. She holds a PhD on Business Administration (Marketing) and is Associate Member of the Chartered Institute of Marketing (UK). Her research interests include service quality management, public sector marketing communications, small business digitization and marketing and social media advertising.

Daniel Agyapong is a Professor Finance and Entrepreneurship at the Department of Finance, University of Cape Coast. Daniel has books in manuscript on entrepreneurship and small business management, sales management-qualitative and quantitative techniques in 2019. His research interests include financial literacy, high start-up firms, digitization, and SME performance.

References

- Abbasi, T., & Weigand, H. (2017). (IDEAS). The impact of digital financial services on firm’s performance: a literature review. http://arxiv.org/pdf/1705.10294

- Ackah, J., & Vuvor, S. (2011). Master’s Thesis in Business Administration, MBA programme (Blekinge Tekniska). https://www.diva-portal.org/smash/get/diva2:829684/FULLTEXT01.pdf;The. The challenges faced by small, & medium enterprises (SMEs) in obtaining Credit.

- Agbenyo, Daniel. (2015). Challenges facing small and medium scale enterprises (smes)sin accessing credit (a case study of kumasi metropolis). A Thesis submitted to the department of accounting and finance, kwame nkrumah university of science and technology, kumasi.

- Agyapong, D. (2021). Implications of digital economy for financial institutions in Ghana: an exploratory inquiry. Transnational Corporations Review, 13(1), 51–21. https://doi.org/10.1080/19186444.2020.1787304

- Agyapong D. (2021). Implications of digital economy for financial institutions in Ghana: an exploratory inquiry. Transnational Corporations Review, 13(1), 51–61. 10.1080/19186444.2020.1787304

- Agyapong, D., & Attram, A. B. (2019). Effect of owner-manager’s financial literacy on the performance of SME’s in the Cape Coast Metropolis in Ghana. Journal of Global Entrepreneurship Research, 9(1). https://doi.org/10.1186/s40497-019-0191-1

- Alliance for Financial Inclusion. (2016, Sep). Alliance for Financial Inclusion. www.afi-global-org:https://www.afi-global.org/sites/default/files/publications/afi_smefwg_wg_guideline_note_stg2.pdf

- Andrews, K. R., Christensen, C. R., Guth, C. R., & Learned, E. P. 1965. Strategic choice in knowledge-based organizations: The case of the electronic industries in Algeria 1969. Irwin.

- Anggadwita, G., & Mustafid, Q. Y. (2014). Identification of factors influencing the performance of small medium enterprises (SMEs). Procedia-Social and Behavioral Sciences, 115, 415–423. https://doi.org/10.1016/j.sbspro.2014.02.448

- Atakora, A. (2013). Managing the effectiveness of financial literacy programs in Ghana. International Journal of Management and Business Research, 135–148.

- Barney, J. (1991). Firm resources and sustained competitive advantage. Journal of Management, 17(1), 99–120. https://doi.org/10.1177/014920639101700108

- Barney, J. B. (2001). Resource-based theories of competitive advantage: A ten-year retrospective on the resource-based view. Journal of Management, 27(6), 643–650. https://doi.org/10.1177/014920630102700602

- Daft, R. L. (1983). Organization Theory and design. the University of Michigan: West Publishing Company.

- De Mel, S., McKenzie, D., & Woodruff, C. (2012). Business training and female enterprise start-up, growth and dynamics: Experimental evidence from Sri Lanka. Journal of Development Economics, No 199–210.

- Dierickx, I., & Cool, K. (1989). Asset stock accumulation and sustainability of competitive advantage. Management Science, 35(12), 1504–1511. https://doi.org/10.1287/mnsc.35.12.1504

- Eniola, A. A., Entebang, H., & Law, K. L. (2016). Financial literacy and SME firm performance. International Journal of Research Studies in Management, 5(1), 31–43. https://doi.org/10.5861/ijrsm.2015.1304

- Gathungu, J. M., & Sabana, B. M. (2018). Entrepreneur financial literacy, financial access, transaction costs and performance of microenterprises in Nairobi City County in Kenya. Global Journal of Management and Business Research. 18(6–A https://journalofbusiness.org/index.php/GJMBR/article/view/2548)

- GSMA. (2015). State of industry report, mobile money.

- Henard, D. H., & McFadyen, M. (2012). Resource dedication and new product performance: A resource-based view. Journal of Product Innovation Management. How Does Technological and Financial Literacy. n.d. 29(2), 193–204. https://doi.org/10.1111/j.1540-5885.2011.00889.x

- Hernando I and Nieto M J. (2007). Is the Internet delivery channel changing banks’ performance? The case of Spanish banks. Journal of Banking & Finance, 31(4), 1083–1099. 10.1016/j.jbankfin.2006.10.011

- Hussain J, Salia S and Karim A. (2018). Is knowledge that powerful? Financial literacy and access to finance. JSBED, 25(6), 985–1003. 10.1108/JSBED-01-2018-0021

- Hussain, J., Salia, S., & Karim, A. (2019). Is knowledge that powerful? Financial literacy and access to finance. Journal of Small Business and Enterprise Development, 25(6), 985–1003. https://doi.org/10.1108/JSBED-01-2018-0021

- Kapurubandara, M., & Lawson, R. (2007). SMEs in developing countries need support to address the challenges of adopting e-commerce technologies. In Proceedings of the Bled eConference, (p. p. 24). 2007 (Merging and Emerging Technologies, Processes, and Institutions: Conference Proceedings.) Slovenia.

- Krejcie, R. V., & Morgan, D. W. (1970). Determining sample size for research activities. Educational and Psychological Measurement, 30(3), 607–610. https://doi.org/10.1177/001316447003000308

- Kulathunga, K., Ye, J., Sharma, S., & Weerathunga, P. (2020). How does technological and financial literacy influence SME performance: Mediating role of ERM practices. Informatiom, 11(6), 296. https://doi.org/10.3390/info11060297

- Lusardi, A., & Tufano, P. (2008). Debt literacy, financial experiences and overindebtedness. National Bureau of Economic Research. 14(4), 332–368. https://doi.org/10.1017/S1474747215000232

- Marriott, N., Mellett, H., Marriott, N., & Mellett, H. (1996). Health care managers’ financial skills: Measurement, analysis and implications. Accounting Education, 5(1), 61–74. https://doi.org/10.1080/09639289600000006

- Mata, J. F., Fuerst, W. L., & Barney, J. B. (1995). Information Technology and sustained competitive advantage: A resource-based (pp. 489–505). Management Information Systems Research Center, University of Minnesota.

- Minola, T., & Cassia, L. (2012). Hyper-growth of SMEs: Toward a reconciliation of entrepreneurial orientation and strategic resources. International Journal of Entrepreneurial Behaviour, & Research, 18(2), 179–197. https://doi.org/10.1108/13552551211204210

- Myovella G, Karacuka M and Haucap J. (2020). Digitalization and economic growth: A comparative analysis of Sub-Saharan Africa and OECD economies. Telecommunications Policy, 44(2), 101856 10.1016/j.telpol.2019.101856

- Nelson, R. R. (2009). An evolutionary theory of economic change. Harvard University Press.

- Okello, G. C., Mpeera, J. N., Munene, J. C., & Malinga, C. A. (2017). The relationship between access to finance and growth of SMEs in developing economies: Financial literacy as a moderator. Review of International Business and Strategy, 27(4), 520–538. https://doi.org/10.1108/RIBS-04-2017-0037

- Ozili, P. K. (2018). Impact of digital finance on financial inclusion and stability. Borsa Istanbul Review, 18(4), 329–340. https://doi.org/10.1016/j.bir.2017.12.003

- Prahaland, C. K., & Hamel, G. (1990b). the core competence of the corporation. University of Illinois at Urbana-Champaign’s Academy for Entrepreneurial Leadership Historical Research Reference in Entrepreneurship.

- Roxas, H., Ashill, N. J., & Chadee, D. (2017). Effects of entrepreneurial and environmental sustainability orientations on firm performance: A study of small businesses in the Philippines. Journal of Small Business Management Forthcoming, 55, 163–178. https://doi.org/10.1111/jsbm.12259

- Rural Enterprises Program. (2017). Standard manual on financial management for micro and small enterprises (The International Fund for Agricultural Development).

- Siddik M Nur, Sun G, Kabira S, Shanmugan J and Yanjuan C. (2016). Impacts of e-banking on performance of banks in a developing economy: empirical evidence from Bangladesh. Journal of Business Economics and Management, 17(6), 1066–1080. 10.3846/16111699.2015.1068219

- Simeyo, O., Lumumba, M., Nyabwanga, R. N., Ojera, P., & Odondo, A. J. (2011). Effect of provision of microfinance on performance of micro enterprises: A study of youth micro-enterprises under Kenya rural enterprises program (K-REP), Kisii County. African Journal of Business Management, 5(20), 8290–8300. https://doi.org/10.5897/AJBM11.1419

- Stacey, R. D. (2011). Strategic management and organisational dynamics: The challenge of complexity to ways of thinking about organisations. Pearson.

- Tuffour J Kwadwo, Amoako A Asantewa and Amartey E Otuko. (2022). Assessing the Effect of Financial Literacy Among Managers on the Performance of Small-Scale Enterprises. Global Business Review, 23(5), 1200–1217. https://doi.org/10.1177/0972150919899753

- Wernerfelt, B. (1984). A resource based view of a firm. Strategic Management Journal, 5(2), 171–180. https://doi.org/10.1002/smj.4250050207