?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study investigated temporal changes in factor adjustment of the Japanese manufacturing industry by applying a dynamic factor model, in which labor and capital were quasi-fixed to a panel of industries from 1972 to 2012. Estimations show that the adjustment speeds, with which factors approach their optimum levels, have increased over the period. Particularly, factor adjustment rates have significantly increased since 2000. The estimations suggest that Japanese manufacturers have become more flexible in hiring workers and faster in making investments, which reduces adjustment cost significantly. This dynamic gain is ignored from static analysis, underestimating the benefit of labor market reform. The study suggests that policymakers should consider dynamic factor adjustment in assessing policy impacts accurately when implementing an industrial policy.

1. Introduction

Until 1990, Japanese manufacturers hired workers mostly based on lifetime employment systems, in which the manufacturers could enhance productivity by accumulating quality human capital. When economic recession began in the early 1990s, the Japanese manufacturers started utilizing fixed-term and temporary labor contracts to reduce labor costs. Currently, the Japanese government attempts to boost the flexibility of the labor market, by promoting participation of female and elderly workers in the labor market, and thus tackle problems emanating from the aging population and shrinking labor force problem (Jones & Seitani, Citation2019; Kondo & Shigeoka, Citation2017; Oshio et al., Citation2018; Shambaugh et al., Citation2017).

Meanwhile, Japanese manufacturers exercise caution while making investment decisions, which require a long and diligent consensus building process among stakeholders. Japanese manufacturers with risk-averse behavior are stable, despite severe business cycles; however, they are slow in adapting to changing business environments that require speedy investments to maintain a competitiveness edge. Currently, Japanese manufacturers attempt to accelerate their decision-making process while making investments. Further, the Japanese government has implemented industrial policies to boost capital investments, especially by lowering corporate tax rates (Hasumi, Citation2014; Kim & Park, Citation2021; Mooij & Saito, Citation2014).

Against this background, this study empirically investigated temporal changes in the factor adjustment of the Japanese manufacturing industry and sheds some light on this industry’s changing business decision-making process.

This study adopted the adjustment cost approach, in which labor and capital are regarded as quasi-fixed inputs, to examine the resource adjustment problem of the manufacturing industry. Specifically, the study utilized an intertemporal value function, as represented by the Hamilton–Jacobi equation, which denotes the present value of the stream of future profits. Following Epstein (Citation1981), the study obtained a system of dynamic factor demand and output supply equations by applying a dual approach to the intertemporal value function while assuming labor and capital as quasi-fixed inputs.Footnote1 The study then estimated the system by utilizing industrial panel data for the period 1972–2012 to investigate dynamic factor adjustment for the Japanese manufacturing industry.

Researchers have applied a factor adjustment model to investigate the dynamic factor demand for labor and capital (for example, Contreras, Citation2006; Hall, Citation2004; Hamermesh & Pfann, Citation1996; Howard & Shumway, Citation1988), simulate the effects of changing factor prices on factor demands (Pindyck & Rotemberg, Citation1983), and estimate dynamic productivity growth (for example, Luh & Stefanou, Citation1993; Nadiri & Prucha, Citation2001; Rungsuriyawiboon & Stefanou, Citation2008).

Recently, Kim (Citation2020, Citation2021) and Kim and Park (Citation2021) used a factor adjustment model to investigate the Japanese manufacturing industry. These studies provided some perspectives for the dynamic production structure of the Japanese manufacturing industry.

Building on previous studies, our study applied the factor adjustment model to investigate temporal changes in the Japanese manufacturing industry’s resource adjustment problem. For this, we divided our industrial panel into three periods: 1972–1989, 1990–2000, and 2001–2012. Furthermore, while our estimation model is nonlinear per se, we adopted the linear estimation method. We estimated a reduced form of the estimation model, as it was not necessary to identify all the coefficients in the model for the purpose of this study. This enabled us to avoid estimating nonlinear estimations that are sensitive to model specification.

In our knowledge, this was the first time that linear estimation method was utilized to estimate the system of nonlinear equations derived from the generalized Leontief production function. Furthermore, we could find few studies that adopt the factor adjustment approach in investigating dynamic factor adjustment in the Japanese manufacturing industry. Thus, this study can fill the research gap in this significant topic.

Meanwhile, many studies investigated the relationship between labor market reform and recent increase in labor market participation by elderly, female, and part-time workers in Japan. For example, Jones and Seitani (Citation2019) summarized government policies to tackle declining population and aging labor force and resulting changes in the labor market. Kondo and Shigeoka (Citation2017) and Oshio et al. (Citation2018) found a positive association between the government policy of increasing pension eligible age along with mandatory retirement age and the employment of elderly workers. Shambaugh et al. (Citation2017) reported that the expansion of child-care benefits and the liberalization of the worker dispatch law have increased opportunities for women to remain and join in the workforce.

These previous studies investigated the impact of labor market reform on changes in the labor market participation of population and the employment composition of labor force. However, few studies examined the impact of the reform on factor adjustment process with which firms move from one equilibrium to another as market environment changes. In this respect, this study can provide empirical evidence that firms are benefitted from increased labor market flexibility with reduced adjustment costs. This occurs because the more flexible labor market becomes, the shorter firms operate in disequilibrium in their factor input mix.

The previous studies underscore an increased stability in the labor market provided by the reform through expanded employment in woman and part-time workers. However, our study shows that the reform shortens adjustment process with which firms adapt to changing market environment. This benefits the economy by cutting disequilibrium cost occurring during the transition period between steady states. This dynamic gain was ignored in a previous static analysis in which factors are assumed to adjust toward the new equilibrium instantaneously.

Regarding corporate tax reduction, several studies investigated its impact on investment and economy. For example, Hasumi (Citation2014) showed that one percent reduction in capital income tax rate would boost economic growth by about 1.1% annually. Kim and Park (Citation2021) suggested that providing a tax reduction as incentive to firms for raising wage boosted not only capital investment but also employment. Mooij and Saito (Citation2014) estimated that investment was expanded by about 0.4% for each point of the tax rate reduction, promoting economic growth.

These studies examined the impact of industrial policy on investment and economic growth for the Japanese economy. However, our study focuses on the impact of government policy on the speed of investment with which firms adjust to a new equilibrium when relative input prices change. Change in managerial decision-making process over investment can affect the long-run trajectory of an economy, which lasts much longer than the direct impact of industrial policy itself. Our study can shed some light on changing corporate culture resulting from a set of structural reform that the Japanese government implemented to boost the competitiveness of manufacturing firms.

The estimations suggest that both labor and capital gradually move toward their long-run optimum levels. The adjustment speed, with which factors approach their optimum levels, increased throughout the sampling period. Particularly, factor adjustment rates have significantly increased since 2000; the industry eliminates any disequilibrium caused by market fluctuations much faster than before.

Our estimations suggest that Japanese manufacturers have become more flexible in hiring workers and faster in making investments. This change reflects a firm’s response to new business environments, including shrinking labor force and development of information technology (IT). Further, this change is facilitated by the Japanese government, which has pursued industrial policies to enhance labor market flexibility and boost investments in its manufacturing industry.

This study is organized as follows. Section 2 provides a theoretical background for the dynamic dual model and provides the functional form of the estimation model. Section 3 discusses the data and estimation results. Section 4 presents the conclusions.

2. Theoretical framework

In a factor adjustment model, a firm suffers a short-run output loss when it changes a stock of quasi-fixed input. Thus, a typical production function includes investment as an argument, along with the usual factor inputs. Drawing on Kim (Citation2020, Citation2021), we assume production factors consist of both variable and quasi-fixed inputs.

where y is the output produced by variable intermediate input M, a vector of a quasi-fixed factor K, allowing for a portion of output appropriated for net investment. Adjustment costs imply sluggish input adjustments because it is costly to change stocks quickly rather than slowly, and such sluggishness could be construed as a form of asset fixity. In the production function (1), labor and capital are considered quasi-fixed because adjusting the stock of these factors involves some adjustment cost. From this, we can analyze the speed of adjustment if the factor inputs reveal quasi-fixity.

If there are adjustment costs associated with quasi-fixed inputs, a firm’s problem can be represented by a value function (Epstein, Citation1981; McLaren & Cooper, Citation1980). A perfectly competitive firm maximizes the current stream of future profits over the infinite time horizon at a base period t, the intertemporal value function can be written as follows:

In the value function, P is the price of output ·), V is the price of variable input M,

is the rental price vector of the quasi-fixed input K, r is the real discount rate, and

is the gross investment in

.

is the constant depreciation rate, k is the initial endowment of

,

is the net change in

, and t is the time trend denoting technical progress. Time subscript t is dropped for brevity, even though all variables are implicit functions of time.

The value function represents the optimal value of problem (2) when an interior solution exists. The value function is the long-run profit function for the competitive firm, denoting the maximized sum of discounted profit flow over the entire planning horizon. To ensure the solution, we needed the regularity assumption that the production function

is twice continuously differentiable and concave. We further assumed that

,

, and that

is twice continuously differentiable, convex in prices and concave in quasi-fixed inputs.

The dynamic optimization problem (2) can be replaced with a sequence of static optimization problems linked over time, assuming the firm expects prices denoting the actual market at time t to persist indefinitely. Therefore, decisions made in period t are based on information available in that period, which contains all relevant information about future prices. Thus, the static optimization problem can be defined by the Hamilton–Jacobi equation:

With the Hamilton–Jacobi equation, the dynamic problem in (2) is converted into a more manageable form. Particularly, the value function is identified as the discounted present value of the current profit plus the marginal value of the optimal change in net investment. According to Epstein (Citation1981), the properties of are fully expressed in the value function

if the regularity conditions on

are satisfied, establishing a dynamic duality between

,

, and

. The dynamic factor demand and supply functions can be derived by applying the envelope theorem to the Hamilton–Jacobi Equationequation (3)

(3)

(3) as follows:

In addition to its regularity properties, the value function is assumed as affine in capital for consistent aggregation across firms, satisfying (Blackorby & Schworn, Citation1982). Furthermore, the value function must have a form such that

is not a function of prices, which allowed us to express the net demand for quasi-fixed inputs in the flexible accelerator form. The restriction on

also facilitates the determination of the curvature properties of the production technology. However, the convexity of

in prices is sufficient for the existence of the curvature properties if

is linear in price (Epstein, Citation1981).

In the estimation, we employed a modified general Leontief function to specify the value function, because the Leontief function satisfies the above requirements and maintains linear homogeneity in prices and concavity in quasi-fixed inputs. We defined the modified generalized Leontief function as follows:

In the function, P is the output price; V is the material price; K is a (2x1) vector of quasi-fixed factors, where is the number of employees and

is fixed capital asset; C is a (2x1) vector of corresponding rental prices, including wage rate and capital rental rate; and t represents the year. Parameters A, B−1, E, G, and F are each (2x2) matrix, and H is a (1x4) vector denoting disembodied technical change.

The optimal net investment demand vector (6) is consistent with the multivariate flexible accelerator model with a constant adjustment coefficient.

3. Data and empirical results

3.1. Data and variables

We used data from the Japan Industrial Productivity (JIP) Database 2015 that represents a balanced panel of Japanese manufacturing industries and compiled a panel of 52 manufacturing industries for the period 1972–2012, from which we constructed all the variables required for the estimation. We started the sample period from the early 1970s, when Japanese manufacturing emerged and started dominating the world with successful structural reforms after the oil shocks in the 1970s. Thus, the sample encompassed the dynamic adjustment of the Japanese economy’s manufacturing sector through the booms in the 1980s, structural transformation after the economic bubble burst in the early 1990s, IT innovation in the 2000s, and two quantitative easing monetary policies before and after the global economic crisis in 2007.

For the estimation, labor inputs () were proxied by the number of employees, capital stock (

) was given by the real amount of tangible fixed assets, intermediate goods (M) were measured by the total value of intermediate input, and the total value of output (Y) was used for output. Both labor and capital were augmented by the respective quality indices in the database to account for embodied technical change.Footnote2 The quality of employment was estimated as the weighted average composition of employees based on gender, education, age, and employment status (full-time vs. part-time) with weights derived from the ratio of compensation paid to each category of employees. Similarly, the quality of capital stock was estimated by the value-augmented capital stock with values defined by the average shares of compensation paid for specified capital stock components.

Wage rate () was constructed to denote labor price by dividing the total labor cost by the number of employees.Footnote3 The rental price of capital (

) was used for capital price, and material costs (v) and output price (p) were represented by the intermediate input deflator and output deflator, respectively. All prices were changed into price indices with their 2000 prices equaling to ones. All nominal variables were converted into 2000 constant prices using deflators obtained from the JIP database.

3.2. Parameter estimation and hypothesis test

Table presents the coefficient estimates obtained by applying the three-stage least square estimation method to the system of Equationequations (4)(4)

(4) , (Equation5

(5)

(5) ), and (Equation6

(6)

(6) ). While our estimation model was nonlinear per se, we adopted the linear estimation method as identifying all the coefficients in the model was not necessary for our purpose, and nonlinear estimations are sensitive to model specification. Following previous studies, we assumed a constant real discount rate of 4%. We divided the full sample into three sub-samples: 1972–1989, 1990–2000, and 2001–2012, allowing for severe dynamic changes that occurred during the sampling period, which can be best captured by using separate estimations.Footnote4 The sample periods were chosen while considering the burst of the Japanese economy bubble in the early 1990s, which ensued an economic stagnation called The Lost Decade and the subsequent road to economic recovery. An empirical estimation also confirmed the change in regime in those periods.

Table 1. Coefficient estimates of dynamic factor demand for Japanese manufacturing industry

In estimation, various panel data models were used to find the model that best fits the dataset. We used both the Akaike information criterion (AIC) and the Bayesian information criterion (BIC) to compare the performance of various models and choose a model with an industry dummy. Also, we included lagged exogenous variables as instruments to improve efficiency.

For all the estimations, approximately two-thirds of the coefficient estimates were statistically significant at the 5% level, and all the significant estimates were mostly significant at the 1% level. Further, more than half of those insignificant estimates became significant at the 10% level. The estimation model accounts for almost all the total variation in the two equations, with the R2 for the output supply and intermediate input demand for every period. The model accounts for about 35–72% and 48–73% of labor demand and capital demand variations, respectively.

Table presents hypothesis tests for the Japanese manufacturing industry’s dynamic nature of factor demand along with tests for its technological progress. All the tests are nested on the full model, and symmetricity of the value function is assumed by utilizing the likelihood-ratio test.

Table 2. Hypothesis tests of production structure for Japanese manufacturing industry

Instantaneous adjustment of labor and capital was tested to determine whether quasi-fixed factors move to their desirable levels instantaneously; instantaneous adjustment of labor (capital) arises not only when (

) but also when

. The null hypothesis of instantaneous adjustment was rejected for both factors for every period, suggesting a dynamic adjustment of the factors throughout the sampling period. Therefore, the tests confirmed that the factors are not variable inputs for the Japanese manufacturing industry.

Meanwhile, independent adjustment occurred when each quasi-fixed input adjusted to its optimum level independently. For every period, the null hypothesis of independent adjustment of labor with was rejected at the 5% significance level; however, the null hypothesis of independent adjustment of capital with

could not be rejected at the 5% significance level.

The null hypothesis of no technical change, for i = 1, 2, 3, and 4, was rejected for every period; that of no disembodied technical change in labor,

, was rejected only for the first period; and that of no disembodied technical change in capital,

, was rejected significantly only for the second period. Test results suggest that the Japanese manufacturing industry has had a disembodied technical change in capital since 2000.

3.3. Temporal changes in factor adjustment

Table presents the adjustment rates for labor () and capital (

) across the sample periods. The adjustment rates for labor and capital are estimated as negatively significant for all periods, ensuring the dynamic stability of the estimation model. The rates are also significantly different from −1, indicating that both labor and capital were slow in moving toward their steady-state levels. The estimates suggest that the number of employees and capital stock approached 12.4–35.7% and 7.7–17.3% annually to their long-run optimal levels, respectively.Footnote5 This implies that both factors are not only quasi-fixed in nature but are also under constant disequilibrium.

Table 3. Coefficient estimates of adjustment matrix and its eigenvalues for Japanese manufacturing industry for selected periods

Estimations show that adjustment rates changed significantly across the sampling periods. The adjustment rate for labor changed from approximately −0.124 in 1973–1989 to −0.169 in 1990–2000 and then to −0.357 in 2001–2012. Thus, labor approached its long-run equilibrium level annually by 12.4%, 16.9%, and 35.7% in 1973–1989, 1990–2000, and 2001–2012, respectively. This shows that the speed of labor adjusting to its optimal level steadily increased throughout the sampling periods. Particularly, the speed of adjustment drastically increased from 2000 and more than doubled from 1990–2000 to 2001–2012.

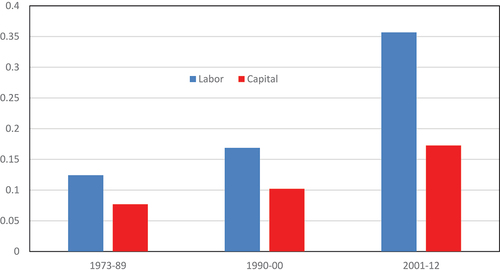

To illustrate temporal changes in factor adjustments, Figure depicts the adjustment speed of labor (green) and capital (red) across the periods. Noticeably, the adjustment rates increase for both labor and capital throughout the sample period. The adjustment rates change more significantly in labor compared with capital, and both rates have increased greatly since 2000.

Figure 1. Temporal changes in factor adjustment in the Japanese manufacturing industry.

Our estimations suggest that, over the years, Japanese manufacturing firms have been adjusting their employment to changing market environments much faster than before and are currently adopting a relatively more flexible employment system to reduce labor costs under severe international competition. Over the years, firms have utilized more fixed-term labor contracts instead of life-time contracts. Further, they hire temporary workers extensively to satisfy the labor demand. Until 1990, long-term employment had been the norm; however, over the years, it has been replaced by flexible employment systems, which has become significant and prevalent since 2000.

The Japanese government has pursued various industrial policies to enhance the flexibility of the labor market, such as the labor market reform to increase the participation of female and elderly workers in the labor market and thus offset the shrinking labor force. Our study shows positive government policy impacts on enhancing labor market flexibility. However, an increased use of information communication technology (ICT) has helped improve the efficiency of the labor market since 2000. The technology enhances matching between firms and workers, reducing the frictional time of jobseekers (Raja et al., Citation2013; Valberg, Citation2020).

The Japanese government has raised the eligibility age for public pension benefit and required firms to employ workers until they become eligible for the benefits. The government also expanded child-care benefits and liberalized the worker dispatch law to enhance labor market participation of women and part-time workers. In this regard, recent studies suggested that the government policy has been a main driver of increased labor market participation of elderly, female, and part-time workers (Jones & Seitani, Citation2019; Kondo & Shigeoka, Citation2017; Oshio et al., Citation2018; Shambaugh et al., Citation2017). Our estimations are consistent with these studies.

However, our study focuses on changing trend of dynamic adjustment process that is supported by changing government incentives and labor market environments. In this sense, our study is fundamentally dynamic compared with previous studies that focused on employment composition at any given time.

The adjustment rate for capital changed from approximately −0.077 in 1973–1989 to −0.102 in 1990–2000 and then to −0.173 in 2001–2012. Thus, capital approaches its long-run equilibrium level annually by approximately 7.7%, 10.2%, and 17.3% in 1973–1989, 1990–2000, and 2001–2012, respectively. The speed with which capital fills its disequilibrium gap has increased steadily and greatly. Noticeably, the adjustment speed has drastically increased since 2000.

Estimations show that Japanese manufacturing firms have fastened their investments’ decision-making processes throughout the years. We noticed that, compared with the adjustment speeds of labor, adjustment of capital is much slower due to capital lumpiness. This is because capital is much more expensive than labor, and investment decisions require a time-consuming, long-term plan.

Our estimations suggest that, since 2000, Japanese manufacturing firms have accelerated their investment speed to meet rapidly changing business environments. The emergence of the ICT (information and communication technology) industry accelerated the investment decision-making process because of the fast-moving industry, which requires speedy investments to sustain competitiveness. Increased use of ICT enables firms to make speedy adjustment in physical capital by facilitating the decision-making process that requires collecting information and coordinating between stakeholders. Also, to leverage ICT investment successfully, firms must make large complementary investments and innovate in areas such as business organization, workplace practices, human capital, and intangible capital (Spiezia, Citation2012: 202).

Additionally, the Japanese government has pursued various industrial policies to enhance the investment of its manufacturing firms. Particularly, the government reduced the capital tax rate greatly to boost firms’ investments. Our estimations confirmed the positive impacts of government policy in boosting investments.

4. Conclusions

This study applied a factor adjustment model to investigate temporal changes in the Japanese manufacturing industry’s resource adjustment problem. Estimations show that the speed of labor adjusting to its optimal level steadily increased throughout the sampling periods. Particularly, the speed of adjustment increased drastically from 2000.

Our estimations suggest that, over the years, Japanese manufacturing firms have moved from long-term employment systems to flexible employment systems, under which they hire fixed-term and temporary workers more extensively than before. This change is supported by the Japanese government’s policy, which has enhanced the labor market participation of female and elderly workers to tackle the shrinking labor force problem. Regarding capital adjustment, the speed of adjustment has also increased steadily throughout the years, with a drastic increase after 2000.

Estimations show that Japanese manufacturing firms have increased their investment speed to match rapidly changing business environments. ICT has helped accelerate the decision-making process since 2000, and within the emerging ICT industry, speedy investment is also necessary to sustain competitiveness. This change is also supported by the Japanese government, which has reduced corporate tax rates greatly to boost capital investments.

The Japanese government has implemented various policies to reform its labor market to tackle aging population and shrinking labor force. Recent studies suggested that the government policy has increased labor market participation of elderly, female, and part-time workers. Compared with these studies, however, our study focuses on changing trend of dynamic adjustment process that is supported by changing government incentives and labor market environments.

In this respect, our study suggests that firms can reduce adjustment costs when labor market flexibility is enhanced. This is because the more flexible labor market becomes, the shorter firms operate in disequilibrium in their factor input mix. This benefit is fundamentally dynamic, lasting over a period until a new equilibrium reaches when market environment changes. This dynamic gain is ignored from previous static analysis as firms are always assumed to be in equilibrium. Thus, our study suggests that the benefit of labor market reform is underestimated if this dynamic gain is not considered.

The study suggests that policymakers should consider dynamic factor adjustment in assessing policy impacts accurately when implementing industrial policies that affect output supply and factor demand. Furthermore, the government should apply policy measures to facilitate a change in corporate behavior to be favorable for labor market flexibility and speedy investment. This helps to make firms remain competitive under the market environment characterized by globalization and ICT revolution.

Further study is required to confirm increased factor adjustment for the Japanese manufacturing industry. One future pursuit is using firm-level data to analyze the dynamic adjustment of individual firms, instead of the aggregate industry, represented more by the behavior of large firms that are more likely to maintain overemployment of quasi-factors than small and medium enterprises.

Our study suggests that business decision-making regarding employment and investment has changed to become more flexible and faster throughout the years. This results from both government industrial policy and changing economic environment like increased use of ICT and deepening globalization. To investigate actual changes occurred in corporate firms would make an interesting topic for future study. This might require close observation of business practices and field survey of managers who are engaged in firm’s decision-making process.

Finally, the Pandemic (COVID-19) creates various consequences and effects on corporate behaviors. In this regard, it would be interesting to see how corporate behaviors in the pre- and post-COVID affect dynamic factor adjustment.

Acknowledgements

The author wishes to thank anonymous referees for their valuable comments and suggestions. Financial support from the Japan Society for the Promotion of Science of Research (JSPS KAKENHI Grant Number 17K03745) is gratefully acknowledged.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Sangho Kim

Sangho Kim is a full professor at College of International Management in Ritsumeikan Asia Pacific University. He received his Ph.D. degree in economics at Michigan State University in 1990. His main research interests are economic development, international trade, and productivity. His recent publications include Journal of the Asia Pacific Economy (2021), Sustainable Production and Consumption (2021), Global Economic Review (2020), Applied Economics (2018), Contemporary Economic Policy (2016, 2014). Some of his research projects were conducted with international organizations including ADB (2009, 2008), APEC (2014, 2008), and MPC (2014, 2007). Prior to his appointment at APU in 2012, He worked at Honam University in Korea. He is currently on editorial board for several academic journals including Journal of Asian Business and Economic Studies and Journal of Market Economy.

Notes

1. Behavioral equations can be obtained either primarily from the first-order optimization conditions of the Hamilton-Jacobi equation (Berndt et al., Citation1981; Treadway, Citation1970) or dually by applying the envelope theorem to the equation (Epstein, Citation1981; Epstein & Denny, Citation1983; McLaren & Cooper, Citation1980)

2. Disembodied technical change is captured by vector in the value function (6).

3. In the JIP database, there are two variables representing the total labor costs: compensation to employees and total labor cost. Of the two, the total labor cost is used here to calculate wage rate because this paper is interested in the dynamic adjustment of labor demand. However, the two variables are highly correlated, with a correlation coefficient of 0.972. The two variables do not make any difference to the estimation.

4. Estimations based on the whole sample can be obtained from the author upon request.

5. To check the robustness of estimates, future discount rates that are lower by 1% and reflect low Japanese interest rate were used in the estimation without any discernable change in adjustment rates.

References

- Berndt, E. R., Fuss, M., & Waverman, L. (1981). The substitution possibilities for energy: Evidence from U.S. and Canadian manufacturing industries. In E.R. Berndt & B. C. Field (Eds.), Model and measuring natural resource substitution (pp. 230–13). MIT Press.

- Blackorby, C., & Schworn, W. (1982). Aggregate investment and consistent intertemporal technologies. Review of Economic Studies, 49(4), 595–614. https://doi.org/10.2307/2297289

- Contreras, J. (2006). An empirical model of factor adjustment dynamics. MPRA Paper, (9797). https://mpra.ub.uni-muenchen.de/9797/1/ContrerasCBOWP2006-13.pdf

- Epstein, L. G. (1981). Duality theory and functional forms for dynamic factor demands. Review of Economic Studies, XLVIII(1), 81–95. https://doi.org/10.2307/2297122

- Epstein, L. G., & Denny, M. S. (1983). The multivariate flexible accelerator model: Its empirical restriction and an application to U.S. Manufacturing. Econometrica, 51(3), 647–674. https://doi.org/10.2307/1912152

- Hall, R. E. (2004). Measuring factor adjustment costs. ” Quarterly Journal of Economics, 119(3), 899–927. https://doi.org/10.1162/0033553041502135

- Hamermesh, D. S., & Pfann, G. A. (1996). Adjustment costs in factor demand. Journal of Economic Literature, XXXIV, 1264–1292. https://www.jstor.org/stable/2729502

- Hasumi, R. (2014). The effect of corporate tax rate reduction: A simulation analysis with a small open economy DSGE model for Japan. RIETI Discussion Paper Series 14-J–040.

- Howard, W. H., & Shumway, C. R. (1988). Dynamic adjustment in the U.S. dairy industry. American Journal of Agricultural Economics, 70(4), 837–847. https://doi.org/10.2307/1241925

- Jones, R. S., & Seitani, H. (2019). Labor market reform in japan to cope with a shrinking and ageing population. OECD Economic Department Working Paper No. 1568.

- Kim, S. (2020). Productivity growth in dynamic factor adjustment for the Japanese manufacturing industry. Global Economic Review, 49(2), 171–185. https://doi.org/10.1080/1226508X.2020.1744466

- Kim, S. (2021). Dynamic factor demand in the Japanese manufacturing industry. Journal of Asian Business and Economic Studies, 28(1), 20–30. https://doi.org/10.1108/JABES-12-2019-0123

- Kim, S., & Park, J.-H. (2021). Dynamic factor adjustment and corporate tax reduction in the Japanese manufacturing industry. Journal of the Asia Pacific Economy, 26(4), 653–667. https://doi.org/10.1080/13547860.2020.1811190

- Kondo, A., & Shigeoka, H. (2017). The effectiveness of demand-side government intervention to promote elderly employment: Evidence from Japan. Industrial & Labor Relations Review, 70(4), 1008–1036. https://doi.org/10.1177/0019793916676490

- Luh, Y.-H., & Stefanou, S. E. (1993). Learning-by-doing and the sources of productivity growth: A dynamic model with application to U.S. agriculture. Journal of Productivity Analysis, 4(4), 353–370. https://doi.org/10.1007/BF01073544

- McLaren, K. R., & Cooper, R. J. (1980). Intertemporal duality: Application to the theory of the firm. Econometrica, 48(7), 1755–1762. https://doi.org/10.2307/1911933

- Mooij, R. D., & Saito, I. (2014). Japan’s corporate income tax: Facts, issues and reform options. IMF Working Paper WP/14/138. International Monetary Fund (IMF).

- Nadiri, M. I., & Prucha, I. R. (2001). Dynamic factor demand models and productivity analysis. In C. R. Hulten, E. R. Dean, & M. J. Harper (Eds.), New development in productivity analysis (pp. 103–171). University Chicago Press.

- Oshio, T., Usui, E., and S. (2018). Labor force participation of the elderly in Japan. NBER Working Paper, (24614). https://doi.org/10.3386/W24614

- Pindyck, R. C., & Rotemberg, J. J. (1983). Dynamic factor demands and the effects of energy price shocks. American Economic Review, 73(5), 1066–1079. http://links.jstor.org/sici?sici=0002-8282%2819831.O%3B2-J&origin=repec

- Raja, S., Imaizumi, S., Kelly, T., & Narimatsu, J. (2013). Connecting to work: How information and communication technologies could help expand employment opportunities. World Bank Working Paper, 80977. http://hdl.handle.net/10986/16243

- Rungsuriyawiboon, S., & Stefanou, S. E. (2008). The dynamics of efficiency and productivity growth in U.S. electric utilities. Journal of Productivity Analysis, 30(3), 177–190. https://doi.org/10.1007/s11123-008-0107-5

- Shambaugh, J., Nunn, R., & Portman, B. (2017). Lessons from the rise of women’s labor force participation in Japan. Brookings Institution. Hamilton Project

- Spiezia, V. (2012). ICT investments and productivity: Measuring the contribution of ICTS to growth. OECD Journal: Economic Studies (pp. 199-211). https://doi.org/10.1787/eco_studies-2012-5k8xdhj4tv0t

- Treadway, L. G. (1970). Adjustment costs and variable inputs in the theory of the competitive firm. Journal of Economic Theory, 2(4), 329–347. https://doi.org/10.1016/0022-0531(70)90017-7

- Valberg, S. (2020). ICT, gender, and the labor market: A cross-Country analysis. In D. Maiti, F. Castellacci, & A. Melchior (Eds.), Digitalisation and development (pp. 375–405). Springer.