?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Savings remain a critical mechanism for capital accumulation for the purpose of investment in developing countries like Ghana. Using data from the Next Generation Cocoa Youth Programme (MASO) implemented by Solidaridad and partners, a bias correcting count data model was applied to determine the drivers of savings, and the impact of savings on youth economic diversification. The results showed that youth trust on financial institutions as well as usage of mobile phones for digital marketing have a positive and significant effect on their decision to save at 1% significance level. The parametric results revealed a significant positive impact of savings on youth economic diversification at 1% significance level. There is thus the need for the promotion of savings among the youth as a tool by national youth policy to reduce youth unemployment in Ghana.

1. Introduction

1.1. Background to the study

Savings is the process of setting aside a fraction of one’s income for future consumption or the purpose of investment. It could also be defined as a fraction of income kept aside against unforeseen future contingencies (Lidi et al., Citation2017). For most developing countries like Ghana, savings is seen as an essential means of capital formation at both individual and household levels which has the ability to improve economic growth through sustained increase in future national income. Of course, this increase is expected to emanate from future consumption and investment which are both injections to the economy (Donkor & Duah, Citation2013). Though, savings from the simple macroeconomic model is seen as a leakage to the system, it has the potential to engineer investment, ensure growth and boost businesses in the long term (Dagar et al., Citation2021).

Todaro and Smith (Citation2012) from their neoclassical growth model explains that, savings in the form of capital formation at the macro level is strongly correlated to economic growth where countries with high level of savings experienced higher investment and economic growth. In most developing countries like Ghana, internally financing programmes and projects have often been problematic, hence they most often have to resort to external finance through borrowing. An empirical analysis of the savings between the periods of 1980 to 2006 showed that, the region performed poorly in terms of domestic savings rate such that, West Africa consistently recorded the least as compared to North Africa and Middle Africa (Kudaisi, Citation2013). For example, between the periods of 2000 to 2006, West Africa savings rate stood at 9.7% as compared to 19.2% and 28.3% for Middle and North Africa respectively (Kudaisi, Citation2013).

In Ghana, for example, the vision 2020 that sought to push Ghana into a middle-income country by 2020 sought to achieve an annual growth rate of 8% which would require an investment/GDP ratio of 25%, ceteris paribus. This was intended to push the required domestic savings/GDP ratio to 20%, assuming foreign savings remained at 5 percent (World Bank 1993; Kudaisi, Citation2013). The average gross domestic savings as a percentage of GDP (Gross Domestic Product) in Ghana between 1990 to 2001 was found to be as low as 6.4% but rose to about 22.09% in 2019 according to recent world bank indicators (Quartey & Blankson, Citation2008; Trading Economics, Citation2019). These proportions of domestic savings are not enough to internally finance programmes and projects. This, coupled with the fact that the credit and insurance sector are poorly developed, makes savings at the micro level the prime way through which households can mobilize funds and invest (Lidi et al., Citation2017; Mariam & Maiwand, Citation2014).

Conversely, Flynn and Sumberg (Citation2018) indicated that, savings among the youth is one sure way of reducing unemployment in Africa which empowers them to under multiple livelihood activity. Also, Marsden et al. (Citation2020) studies micro level savings in Bangladesh and concluded that savings at the micro level has the potential to transform the economic future of families, villages, and larger community groups, while being sustainable at the same time.

Also, youth unemployment in Ghana has been a major issue for policy makers which is always at the fore front of national discussions. The Ghana national youth policy defines youth as a person between the ages of 15–35 years (Ministry of Youth and Sports, Citation2010). Various public policy initiatives have attempted to curb the situation through programmes aimed at absorbing the idle youth in certain areas of the economy in order for them to have a means of livelihood. Among them incudes; the Youth Employment Agency (YEA) which seeks to employ the youth in areas of teaching, nursing, agriculture and security. Another is the Youth Enterprise Support (YES) programme initiated in 2016 to support the teaming youth with a startup capital to engage in businesses as a means of livelihood. But such programme as expected could not provide support to every youth in the country making it necessary to ask questions as to whether such support alone is sufficient in ending the youth unemployment in the country.

The most recent intervention by government is the Nation’s Builders Corpse (NABCO) which seeks to employ young unemployed graduates in areas of agriculture, teaching, research, revenue mobilization and digitization. The NABCO which was established in 2017 budgeted of a total amount of 300 million Ghana cedi with the aim to create over 100, 000 jobs for unemployed graduates (Social Partners Summit (SP) in Africa, 2018). Unlike the YEA, NABCO targeted only graduates that have completed tertiary institutions in Ghana (Atiemo et al., Citation2020). Apart from government, several Non-Governmental Organizations (NGOs) have initiated interventions aimed at curbing the menace of youth unemployment. A typical example is the case of Solidaridad Network and the Mastercard foundation, that have collaborated to empower the youth of Ghana to engage in cocoa production as well as other businesses. So, with all these government and NGOs initiatives, one is right to ask; how has the situation changed? Between 2015 and 2017 for instance, the rate of unemployment reduced from 14.17% to 8.84% which slightly increased to 9.16% in 2019 (STATISTA, Citation2019).

It is indisputable that government cannot employ every youth in the public sector as most of the initiatives seeks to achieve, while the formal private sector has also not been able to provide employment to teeming youth that join the workforce annually. One major way that can boost economic performance and aid in reducing unemployment is economic diversification by the youth where the youth engage in multiple business enterprises mostly in the informal sector to improve their standards of living. At the macro level, economic diversification is defined as a strategy aimed at transforming an economy from single source to multiple sources of income spread over primary, secondary and tertiary sectors, involving majority of the population (United Nations Conference on Climate Change [UNFCC], Citation2016).

Economic diversification is defined in this study as the process by which the youth engage in multiple streams of income generating activities in order to improve their living standards (Dagunga et al., Citation2020; Freire, Citation2019). In this study, we operationalize youth economic diversification as a way by which the youth engage in multiple streams of income generating businesses to improved incomes and welfare. The enterprises could be interrelated or not. Given the potential of economic diversification in reducing youth unemployment in developing countries as spelt out in the literature above, one would expect that savings among the youth should translate into investment into multiple economic activities which will stimulate economic growth (Murshed et al., Citation2021). For example, youth that save are able to accumulate capital which could be invested in the future as compared to those that do not. While this claim is reasonable, there is no country empirical evidence to show its validity. Hence this study seeks to close the gap by examining the effect of savings on economic diversification among the youth in Ghana using data from the Next Generation Cocoa Youth Programme (MASO), a programme which created employment opportunities for some 12,000-youth aged 18–25 in Ghana’s cocoa growing communities. MASO was implemented by a consortium which consisted of Solidaridad, Aflatoun, Ashesi University, Fidelity Bank, Opportunity International and the Ghana Cocoa Board (COCOBOD). The programme was part of the Youth Forward Initiative, which was a partnership led by Mastercard Foundation, Overseas Development Institute, Global Communities, Solidaridad, National Cooperative Business Association-CLUSA (NCBA-CLUSA) and GOAL. The focus of MASO was to link young people to quality employment by helping them to start their own businesses in Ghana and Uganda.

1.2. Literature review

Economic diversification through small and medium agro-enterprises and employment in the rural non-farm economies is helping to build resilient livelihoods for poor people. Many youth earn their incomes in both rural and urban areas and from multiple locations and countries, by engaging in temporary forms of economic activities or migration in search of better jobs (FAO, Citation2012a).

According to Beverly et al. (Citation2008), savings among the youth and asset accumulation often focus on individual constructs such as knowledge, availability of economic resources, and family support. However, an institutional conceptual framework acknowledges the additional role that good policies and programmes as well as and the products and services provided by financial institutions play.

A rapidly growing body of evidence demonstrates that financial inclusion for youth, particularly involvement in savings programmes is associated with a wide range of positive outcomes in areas such as expansion in economic activities, attainment of higher education, enhanced socio-emotional development, and financial well-being (Chowa et al., Citation2013; Huang et al., Citation2014). In fact, available data indicate that the majority of youth in Sub-Saharan Africa and Ghana for that matter, are not saving or using banking services due to unemployment and inadequate economic opportunities. The World Bank estimates that only 9.32 % of young adults (aged 15–24 years) in Sub-Saharan Africa (SSA) saved in a formal financial institution in the past year (Demirguc-Kunt & Klapper, Citation2012), an indication of the negative implications that savings will have on economic diversification by the youth in SSA.

Youth are a rapidly growing percentage of the Ghanaian population, and many are economically vulnerable. Financial inclusion for youth, particularly the promotion of savings culture, is associated with a number of positive socio-economic outcomes attracting global attention (Zou et al., Citation2015). However, the majority of youth in Ghana are not saving, and limited qualitative research exists to aid understanding of the possible explanations.

A study conducted by (Zou et al., Citation2015) on the “Youth Save” project implemented in Ghana and Kenya indicates that, support from parents, school staff, and financial institutions are precursors for youth participation in saving, even though youth participants in the Youth Save Project struggled with limited financial resources and conflicting demands for money. Zou et al. (Citation2015) further opined that the lack of financial resources due to low economic opportunities has been one of the leading obstacles to youth savings in Ghana. However, most of the youth are currently in school and not working, so their source of income is not diversified and unstable since they still rely on others for survival.

Anyaehie and Areji (Citation2015) have also established that economic diversification has the ability to ensure sustainable development by meeting the poor’s basic needs such as provision of job, food, health, clothing as well as opening diverse opportunities to reduce unemployment. Loison (Citation2015) and Dagar et al. (Citation2021) further stressed that economic diversification in Sub-Saharan Africa (SSA) is necessary as it helps to reduce household poverty, contribute to economic growth as well as reducing unemployment. Asfaw et al. (Citation2019) also evaluated the relationship between economic diversification and household welfare using panel data from three West African countries and found diversification to significantly contribute to household welfare through increase in incomes.

2. Materials and methods

2.1. Study area and sampling procedure

The study was carried out in Ghana among cocoa growing regions and eleven administrative districts where MASO is being implemented. The selected regions were the Volta, Ashanti, Western North, Central, Oti and Ahafo regions of Ghana. Since its inception, MASO enrolled over 12,000 youth in 4 cohorts, and trained close to 70% of youth that had been enrolled. Initial data processing was conducted to remove observations with significant outliers. Hence the total sample size used for this study was 10,656 youth.

2.2. Theoretical framework and estimation technique

The theoretical framework for the study is grounded on the utility maximization theory which states that, a youth will save his/her income if the expected utility for saving is higher than the utility for not saving.

Following Terza (Citation1998) and Miranda (Citation2004), the study employed count data modelling (endogenous-switching Poisson regression model) as an econometric tool for the data analysis. This is because the explained variable in the study (i.e., economic diversification) was count in nature comprising the total number of economic activities the youth engaged in. These activities ranged from agriculture (cultivation of cash crops like cocoa, other food crops, animal rearing), business (Agro-processing, petty trading, apprenticeship, mobile money vendor), Industry (transport work, construction work, artisanship) and formal salaried work.

For an ith youth from a random sample , the economic diversification followed the standard Poisson distribution expressed in equation 1 as follows:

Where represents economic diversification,

is savings,

is a vector of explanatory variables,

represents the coefficients of explanatory variables, and

is the error term which accounted for unmeasured variables. Given a vector of explanatory variables

(which encompassed some or all elements of

were considered by a directory process as in equation 2:

was a vector of coefficients of variables estimated. We further assume

to embody all endogenous variables and

and

jointly and normally distributed with a mean zero and covariance matrix

where

are independent.

The joint restrictive probability density expression of , given

can be illustrated as in Equationequation 3

(3)

(3) :

where represents the probability density function for the stochastic error term

.

The endogenous-switching Poisson regression model is a two-stage estimation method with the ability to account for problems of endogeneity that may arise. The first stage assumed a Poisson distribution which examined the factors influencing youth economic diversification. The second stage assumed probit distribution which estimated the drivers of savings by the youth in Ghana (Miranda, Citation2004). The empirical model for savings and economic diversification are expressed by equation 4 and 5 respectively:

Where Z is the vector of explanatory variables as defined in Table . Equation (4) and (5) were estimated using the STATA 15 software.

Table 1. Definition of variables, measurement and summary statistics

3. Results and discussions

3.1. Summary statistics of youth-specific, socioeconomic and institutional factors

The study followed recent empirical studies on household savings and economic diversification such as Asfaw et al. (Citation2019), Freire (Citation2019) and Dagunga et al. (2020a, b) to postulate a number of youth-specific, socioeconomic and institutional variables expected to have influence on savings or economic diversification. Results of the summary statistics are presented by Table . The results showed that, the average age of a youth that participated in the MASO training programme was about 21 years old.

The average age of youth with savings was significantly different from those who do not save, with those who saved having an average of 22 years while non-saving youth had an average age of 21 years. This may imply that as a youth increases in years, they become more likely to save. There was no significant difference between the gender of participants for savers and non-savers. The average for both savers and non-savers were not different from the average for the pool sample. This average implies that, the proportion of males in the study was about 58% while that of females being about 42% though there was no statistically difference between the savers and non-savers as shown by a p-value of 0.576 under the chi-square test.

About 33.7% of the sampled youth were married. Majority of the youth that save were married of about 34.8% while the proportion of married youth that do not save was as low as 4.5%. This suggest that younger married youth are more likely to save than unmarried youth. This was expected because, the married ones will need to plan their family through savings which they can later invest it other business enterprises to improve their standard of living. The proportion of married youth who save were statistically different from those that do not save at 1% significance level. Also, the study included the number of employee’s youth have employed in their business enterprises and the results showed that, on the average youth with businesses employ about 2 other members in addition to themselves. Those who save was found to significantly employ one more person than those who do not save.

With socioeconomic factors considered in this study, the average farm size of a youth in the study area was found to be about 5 acres. Meanwhile, the disaggregated analysis between youth that save and those that do not show that, a significant difference exists between the farm size of those who save and those that do not such that those who save have an average farm size of about 13 acres as against 0.89 acres for those that do not save. The study also included youth perception of the MASO programme on entrepreneurial skill development and the results showed that, majority of the youth (41%) that saved perceived that MASO programme helped to equip them with entrepreneurial skill as compared to those that do not (29.5%).

Migration of the youth to other areas is another socioeconomic factor considered in this study. The results showed that, an average of about 14.3% of the youth have migrated to other areas. There was also statistical difference between youth that migrates and those that did not with those that migrated being about 32.4% while those that do not was about 3.7%. The higher proportion of migrant youth saving suggest that, they might probably earn more on travelling as compared to those that do not.

Finally, the study included four structural/institutional factors considered in this study. The results reveal that, youth that belonged to community development groups were about 6.1 % on the average. The proportion of youth that belonged to community development group and saves was statistically different from zero and higher than the pool sample at about 14.4% as compared to their counterparts that do not save at about 1.3%. The higher proportion of these group of people engaging in savings could imply that, participation in community groups offers some education on the need to invest through savings as a means of capital formation. Majority of the youth was found to play some leadership roles in their communities. About 95.6% of the pooled sample have some leadership functions to undertake.

There was statistically significant difference among youth with leadership functions for savers and non-savings. Interestingly a higher proportion (99%) of the youth with leadership functions are not able to save as compared to those that do (89.6%). Even though the proportion of youth with leadership functions is also high, the pressure on leaders to spend and ensure that their given assignment keeps running might be the reason for the slight difference in savings between savers and non-savers.

About 2.6% of the youth perceive financial institutions were unavailable in their localities. And as expected, about 3.9% of the youth with this perception do not save while 1.1% of their counterparts with same perception make efforts to save with other saving groups or move to other areas with financial institutions to save. Also, about 21% of the youth trusted the available financial institutions while 67% of the youth do not trust or have confidence on the financial institutions in their localities.

Also, we looked at how digitization through online business transactions are practiced by the youth of Ghana. The descriptive statistics indicated that, about 23.2 % of the youth uses their mobile phones for online businesses. There was statistical difference between youth that save and those that do not under this variable. The results showed that, majority of the youth (22.1%) that uses their mobile phones for online businesses saves as compared to those that do not (12.1%).

3.2. Distribution of youth savings across regions in Ghana

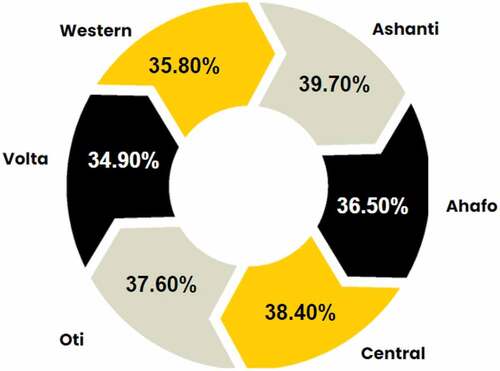

The study examined the dynamics of youth savings across various regions in Ghana. Results on the proportion of savings among the youth is presented in Figure . The results revealed that, most of the youth that saves are from the Ashanti region at about 39.7%. General the proportion of youth savings across the selected districts were above 30 %. There was only slight variation between the rates among the selected regions.

Figure 1. Regional distribution of savings among the youth of Ghana.

3.3. Economic diversification amongst youth in Ghana

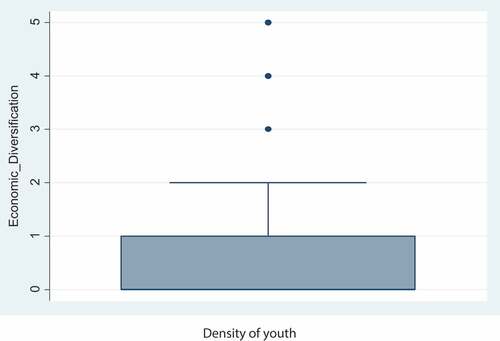

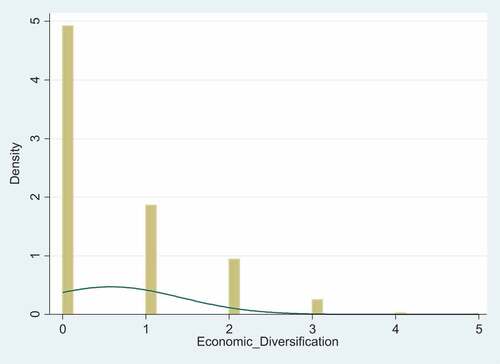

Economic diversification in this study was a count variable comprising the number of business enterprises the youth undertakes.

Figure is a box and whisker plot showing the distribution of youth economic diversification in the country. The box plot show that, there were some youth with no business enterprise since the minimum is zero. Those people constituted about 25% of the distribution also known as the first quartile or the 25th percentile. The third quartile or the 75th percentile was found to be 1. This implies that, about 75% of the youth engages in at least one form of business activity (0 to 1). The maximum value of the distribution that is not an outlier as indicated by the upper whisker is 2. That implies that, a significant number of the youth had up to two different business enterprises. Meanwhile, there were some outliers such that some youth engaged in three, four and five different business enterprises. Hence, youth economic diversification was not normally distributed as could be seen in the above box plot and the density plot in Figure . It was skewed to the right such that, majority of the youth engaged in one or more business enterprises. This suggest that, one cannot model economic diversification based on the ordinary least squares estimator which assumes a normally distributed dependent variable. Other models such as the poison distribution could be used which does not assume the normality assumption of the ordinary least square’s estimator. As such the endogenous switching poison estimator is used in this study to estimate the impact of savings on youth economic diversification in Ghana.

Figure 2. Distribution of economic diversification among the youth in Ghana.

Figure 3. Density plot of Economic Diversification.

3.4. Reasons for non-savings by the youth

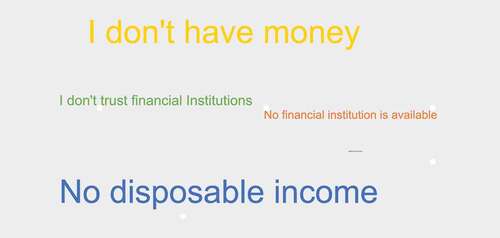

The study further examined the reasons for non-savings among the youth in Ghana and the word cloud below in Figure shows the reasons for non-savings among the youth.

Figure 4. Reason why the youth do not save regularly in Ghana.

The results revealed that, youth perceived to have no disposable income or without money was found to be the main reasons for non-savings by the youth. This is indicated by the font size of the word as displayed in the word cloud. Words with larger font represents reasons with higher frequencies and vice versa. Unavailability of financial institutions and lack of trust on financial institutions were also some of the reasons for non-savings by the youth. Distance to financial institutions was included in the word cloud was found to be an insignificant reason to appear and so it is not visible in the word cloud diagram. The reasons suggest that, apart from lack of disposable income or unavailability of income as some stated, lack of trust in financial institutions and unavailability of financial institutions were the main reasons given by the youth for not saving.

3.5. Savings and economic diversification among the youth of Ghana

Table presents results on the effect of savings on economic diversification of the youth in Ghana. The first two columns present results of an endogenous-switch Poisson model while the last two columns represent results on an exogenous-switch Poisson model. This two were estimated to determine whether savings which is the variable of interest is exogenous or endogenous. Also, the switched variable shows the determinants of savings among the youth of Ghana. The results as could be seen by the significance of rho in the first part indicates that, savings was endogenous. This means that, savings influences and could be influenced by youth economic diversification. The significance of the rho justifies the use of the endogenous switching Poisson model and the model could be said to be best fits and the results for the model reliable for policy and development planning for the youth in the country. We first discuss the drivers of savings from the empirical estimates in section 3.3.1 while the impact of savings on economic diversification of the youth is discussed in section 3.3.2.

Table 2. Effect of savings on economic diversification of the youth in Ghana

3.5.1. Drivers of savings among the youth of Ghana

Guided by the economic theory and lessons from the training programme, we postulated five explanatory variables to have had an influence on youth decision to save. The results reveal that, three out of the five variables have a significant influence on youth decision to save. Youth who perceive financial institutions were unavailable at their locality had lessor probability of saving as compared to those with financial institutions. This is rational because, youth living at areas with financial institutions available are motivated to save with them. Also, these institutions may offer financial education to the youth of these areas and so they are more likely to save as compared to those without the opportunity.

Availability of financial institutions is one thing but equally important is the trust of customers or youth on these institutions. The recent financial clean-up exercise in Ghana which started from August, 2017 resulted in the collapse of about 9 universal banks, 347 microfinance companies, 155 microcredit companies and 15 savings and loans companies (Affum, Citation2020). Undoubtedly no individual wish to be a victim where his/her funds will be locked up in these institutions due to the hurdles faced by government in refunding affected depositors funds which can be very frustrating. Trust is therefore important to consider in a study such as this. The results from Table reaffirms the fact that, youth in Ghana only saved at sources they have trust or confidence in.

There was a positive influence of youth trust on financial institutions on their decision to save which was significant at 1%. Boosting trust on financial institutions is therefore a required if savings by the youth is to be encouraged.

Youth engagement in digital marketing measured by their usage of mobile phones for online business was also found to have a positive influence on savings. Zhang et al. (Citation2022) reveal that digital infrastructure helps to empower youth and the results is intuitive because such youth will be more familiar with cashless transactions and the need to save. Also, with the mobile phone for these businesses, youth can easily save with their desired financial institutions through their mobile banking and will not necessarily have to walk to these banks or institutions to save their money. They can even save with their telecommunication networks among others and hence the result.

3.5.2. Impact of savings on youth economic diversification in Ghana

Table shows the drivers of economic diversification by the youth which shows the impact of savings, the main focus of this study. The results revealed that, savings had a positive and significant effect on youth economic diversification in Ghana. This implies that, youth that saves are more able to invest in many economic activities that improves their well-being as compared to those that do not save.

With the other determinants of economic diversification, the age of the youth was found to have a positive effect on economic diversification. That means that, the older youth are more likely to engage in multiple economic activities as compared to the younger. This could be associated to the fact that most of the growing youth assume responsibility as they grow up. Male youth was also found to diversify more than the female youth. Dagunga et al. (Citation2020) in their recent study using the seventh round of the Ghana living standards survey (GLSS7) found seemingly contrary results where they found that female headed households to have higher probability for income diversification in Ghana as compared to male headed households. The results in this study however differs from this because the focus is on the youth. Also, most of the male youth at certain age will have to engage in more economic activities in order to increase their income to settle down by marrying and building the family. This postulation is confirmed by the results for the married as compared to the unmarried.

The married youth had higher probability of engaging in many economic activities as compared to the unmarried. Youth who have employed a higher number of employees was found to diversify more than those that do not. This implies that, such youth are able to expand from one business to another thereby employing more. It would not be an overstatement for one to state that, empowering the youth to engage in business could be a sustained way of reducing the youth employment in the country since they will further create employment for others thereby creating a workable multiplier effect.

Also, youth who perceive that the MASO training programme helped to equip their entrepreneurial skills were found to diversify more than their counterparts who perceived otherwise. This imply that, the MASO programme could be a suitable tool for youth empowerment towards economic diversification.

Finally, youth that belonged to community development groups as well as those with leadership functions were found to engage in multiple economic activities. Youth participation in community development groups as well as youth in leadership could therefore be seen key measures of empowering the youth of Ghana.

4. Conclusions and recommendations

In this study, we estimate the impact of savings on economic diversification by youth in Ghana using secondary data from the Next Generation Cocoa Youth Programme (MASO) being implemented by Solidaridad, and partners in the cocoa regions of Ghana. The study employs count data modelling (i.e. endogenous switching Poisson model) that also corrects unobserved biases to estimate the drivers of savings as well as the impact of savings on youth economic diversification. The regression results show that savings was endogenously determined and significantly influenced by the availability of financial institutions, trust in financial institutions as well as usage of mobile phones for busines transactions. The parametric estimates also revealed that savings, age, gender, marital status, entrepreneurial skills development from MASO, membership in community development groups as well as youth with leadership functions had significant positive impact on youth economic diversification.

The study recommends that, savings among the youth should be encouraged by the government of Ghana and development partners since it helps in reducing youth unemployment through the creation of multiple income generating opportunities. There is the need for continuous clean-up of the financial sector by the Bank of Ghana (BoG) to engender confidence in the youth to save. Meanwhile, government should set up financial institutions including development banks targeting rural dwellers to boost rural youth savings and support economic diversification. The youth should be encouraged to involve themselves in community development initiatives as well as take up leadership roles as these significantly influence economic diversification of the youth in the country. Capacity building programmes like the MASO programme should be encouraged in the country due their lasting impact on youth economic diversification.

Correction

This article has been republished with minor changes. These changes do not impact the academic content of the article.

Acknowledgements

We are grateful to Solidaridad Network, West Africa for making the data available for this study.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Affum, F. (2020). The unintended effects of bank of Ghana’s clean-up exercise on unaffected financial institutions: Evidence from Yilo Krobo Municipality, Ghana. Asian Journal of Economics, Business and Accounting, 17(1), 1–15.

- Anyaehie, M. C., & Areji, A. C. (2015). Economic diversification for sustainable development in Nigeria. Open Journal of Political Science, 5(2), 87–94. https://doi.org/10.4236/ojps.2015.52010

- Asfaw, S., Scognamillo, A., Di Caprera, G., Sitko, N., & Ignaciuk, A. (2019). Heterogeneous impact of livelihood diversification on household welfare: Cross-country evidence from Sub-Saharan Africa. World Development, 117(1), 278–295. https://doi.org/10.1016/j.worlddev.2019.01.017

- Atiemo, P., Quaynor, D., & Asante, P. Y. S. (2020). Employability Status of NABCO Trainees for the Job Market. World Academics Journal of Management, 8(1), 1–8. https://isroset.org/pub_paper/WAJM/1-WAJM-02989.pdf

- Beverly, S., Sherraden, M., Zhan, M., Williams Shanks, T. R., Nam, Y., & Cramer, R. (2008). Determinants of asset building (Urban Institute Poor Finances Series). The Urban Institute.

- Brown, R., & Foster, J. (2019). Remittances and savings in migrant-sending countries. Pacific Economic Bulletin. http://hdl.handle.net/1885/158095

- Chowa, G., Masa, R., Wretman, C., & Ansong, D. (2013). The impact of household possessions on youth’s academic achievement in the Ghana YouthSave experiment: A propensity score analysis. Economics of Education Review, 33(1), 69–81. econedurev.2012.08.005. https://doi.org/10.1016/j.econedurev.2012.08.005

- Dagar, V., Khan, M. K., Alvarado, R., Usman, M., Zakari, A., Rehman, A., Tillaguango, B., & Tillaguango, B. (2021). Variations in technical efficiency of farmers with distinct land size across agro-climatic zones: Evidence from India. Journal of Cleaner Production, 315(1), 128109. https://doi.org/10.1016/j.jclepro.2021.128109

- Dagunga, G., Amoakowaa, A., Mabe, F. N., Ehiakpor, D. S., & Mabe, F. N. (2020). Interceding role of village savings groups on the welfare impact of agricultural technology adoption in the upper east region, Ghana. Scientific African, 8(1), e00433. https://doi.org/10.1016/j.sciaf.2020.e00433

- Demirguc-Kunt, A., & Klapper, L. (2012). Measuring financial inclusion: The Global Findex Database. World Bank eAtlas of Financial Inclusion. http://www.app.collinsindicate.com/worldbankatlas-fi/en-us

- Donkor, J., & Duah, F. A. (2013). Relationship between savings and credit in rural banks with specific reference to Ghana. International Journal of Business and Social Science, 4(8), 210–221. http://ijbssnet.com/journals/Vol_4_No_8_Special_Issue_July_2013/20.pdf

- FAO. (2012a). Decent rural employment for food security. A case for action.

- Flynn, J., & Sumberg, J. (2018). Are savings groups a livelihoods game changer for young people in Africa? Development in Practice, 28(1), 51–64. https://doi.org/10.1080/09614524.2018.1397102

- Freire, C. (2019). Economic diversification: A model of structural economic dynamics and endogenous technological change. Structural Change and Economic Dynamics, 49(1), 13–28. https://doi.org/10.1016/j.strueco.2019.03.005

- Huang, J., Sherraden, M., Kim, Y., & Clancy, M. (2014). Effects ofchild development accounts on early social-emotional development: An experimental test. JAMA Pediatrics, 168(3), 265–271. https://doi.org/10.1001/jamapediatrics.2013.4643

- Kudaisi, B. V. (2013). Savings and its determinants in West Africa countries. Journal of Economics and Sustainable Development, 4(18), 107–119.

- Lidi, B. Y., Bedemo, A., & Belina, M. (2017). Determinants of saving behavior of farm households in rural ethiopia: the double hurdle approach. Developing Country Studies, 7(12), 17–26. https://core.ac.uk/download/pdf/234683271.pdf

- Loison, S. A. (2015). Rural Livelihood Diversification in Sub-Saharan Africa: A Literature Review. Journal of Development Studies, 51(9), 1125–1138. https://doi.org/10.1080/00220388.2015.1046445

- Mariam, A., & Maiwand, A. (2014). Determinants of household savings: a case study of yazman-Pakistan. International Journal of Scientific and Engineering Research, 5(12), 1624–1631.

- Marsden, J., Marsden, K., Rahman, M., Danz, T., Danz, A., & Wilson, P. (2020). Learning and savings groups in Bangladesh: An alternative model for transforming families and communities. Development in Practice, 30(1), 52–67.

- Ministry of Youth and Sports (2010) Definition of youth. Available at https://www.youthpolicy.org/factsheets/country/ghana/

- Miranda, A. (2004). FIML estimation of an endogenous switching model for count data. The Stata Journal, 4(1), 40–49. https://doi.org/10.1177/1536867X0100400103

- Murshed, M., Rahman, M., Alam, M. S., Ahmad, P., & Dagar, V. (2021). The nexus between environmental regulations, economic growth, and environmental sustainability: Linking environmental patents to ecological footprint reduction in South Asia. Environmental Science and Pollution Research, 28(36), 49967–49988. https://doi.org/10.1007/s11356-021-13381-z

- Quartey, P., & Blankson, T. (2008). The Economy of Ghana: Analytical Perspectives on Stability, Growth & Poverty. Boydell and Brewer.

- STATISTA, (2019) Ghana: Youth unemployment rate from 1999 to 2019 https://www.statista.com/statistics/812039/youth-unemployment-rate-in-ghana/ accessed on 18th September, 2020

- Terza, J. (1998). Estimating count data models with endogenous switching: Sample selection and endogenous treatment effects. Journal of Econometrics, 84(1), 129–154. https://doi.org/10.1016/S0304-4076(97)00082-1

- Todaro, M. P., & Smith, S. C. (2012). Economic development (11th ed.). Addison-Wesley.

- Trading Economics (2019). Ghana Gross Domestic Savings (% of GDP). https://tradingeconomics.com/ghana/gross-domestic-savings-percent-of-gdp-wb-data.html. Accessed on 18th September, 2020

- United Nations Conference on Climate Change [UNFCC], (2016). The concept of economic diversification in the context of response measures, https://unfccc.int/sites/default/files/resource/Technical%20paper_Economic%20diversification.pdf. Accessed on 20th September, 2020.

- Zhang, C., Khan, I., Dagar, V., Saeed, A., & Zafar, M. W. (2022). Environmental impact of information and communication technology: Unveiling the role of education in developing countries. Technological Forecasting and Social Change, 178(1), 121570. https://doi.org/10.1016/j.techfore.2022.121570

- Zou, L., Myers, S., Njenga, G., Appiah, E., Opai-Tetteh, D., & Sherraden, M. S. (2015). Facilitators and Obstacles in Youth Saving: Perspectives from Ghana and Kenya. Global Social Welfare, 2(2), 65–74. https://doi.org/10.1007/s40609-015-0028-y