?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Since 2011, the Vietnamese banking system has performed many M&A deals. Some small banks which had weak competitiveness and experienced operating activities risk were on the verge of bankruptcy, and had been acquired by potential financial institutions. Although M&A transactions are known for numerous advantages which are brought back for banking industry, most banks still have not actively participated. Therefore, gaining more information about how M&A activities changed our banking system is essential for providing suitable implications and developments for the future. This report first aims to investigate the efficiency level of 30 Vietnamese commercial banks during 2011–2019 period under intermediation and operating approach using Bootstrap Data Envelopment Analysis. Next, applying Robust Truncated Regression, this paper shows that M&As negatively affect banking efficiency. Meanwhile, a set of explanatory variables following CAMELS standards can contribute to increase the efficiency level.

Public Interest Statement

This paper is a part of the research project investigating the efficiency of the Vietnamese banking system during the restructuring period. By investigating the bootstrap efficiency scores of Vietnamese banksand the effect of M&A on efficiency scores, this paper will help the State Bank of Vietnam guide the banking system to operate more efficiently during the restructuring period.

1. Introduction

In the trend of economic globalization, mergers and acquisitions (M&A) has been put under consideration as one way that can boost Vietnamese companies increase their capacity and expand the range of operations. The financial and banking systems of many countries are influencing each other, participating in the process of development and international economic integration. M&A is becoming more and more popular in Vietnam banking system.

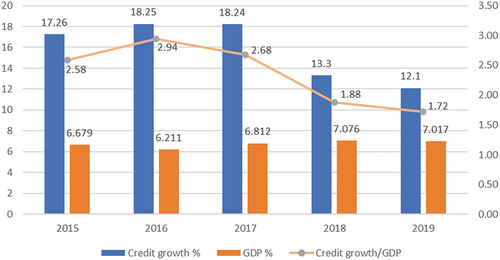

According to the statistics retrieved from General Statistics Office of Vietnam (see ), the credit growth in 2019 is lower than 2018 by 1.2%, which is the lowest rate in the past 4 years while the target set is 14%. Due to the COVID-19 epidemic, Vietnam has suffered a decrease in credit growth at 2.13% for the first 6-month period in 2020, which is lower than the average growth rate of 5.7% for the same period in 2019. According to the State Bank of Vietnam (SBV), although the capital and liquidity of the credit system are abundant, the demand is still weak, making credit growth go down.

Figure 1. Vietnam Credit Growth, GDP rate and Credit growth/GDP ratio, 2015–2019.

The banking system has an undeniable position and is important in both the microeconomic and macroeconomic features. Vietnam commercial banking framework has encountered a huge improvement in the restructuring period by decreasing the number of feeble banks and wrinkling capacity through M&A transactions which expect to build a safe financial framework to increase the competitive ability (Hang et al., Citation2016). M&A in the banking sector in 2020 is expected to be more active than last year. This is the way to expand scale and presence in the financial market of Vietnam. In fact, besides the M&A deals that have to “embrace” a pile of bad debts, many banks have succeeded with the strategy of expanding the scale of growth with the shortcut through M&A.

Therefore, it is necessary to investigate and evaluate how M&A activities affect the efficiency of Vietnam banking system during the restructuring period from 2011 to 2019. This study’s findings are expected to have useful contributions to investors as well as institutions in Vietnam. We aim to review the results of the previous period and contribute to the M&A decision-making in perspective of our banking system for the upcoming years. More specifically, this paper is conducted to narrow down the problems of M&A activities from 2011 to 2019 in the Vietnam banking system. It helps understand the situation that our banking sector is facing now and then evaluate the relationship between M&A activities and the efficiency of commercial banks during the considered period.

Moreover, this research provides the impact of M&A which is beneficial to both state authority and the management to consider the decisions of M&A activities. M&A process is one of the main components in the governmental plan to revive the healthy banking system. Therefore, a review of its impacts will be attributable to evaluate the efficiency of the restructuring plan. For the economy, mergers and acquisitions of commercial banks contribute to the sustainable development of the financial market, making the most of economic potentials. For the banking system, M&A is possibly considered one of the important measures to restructure the banking system. If banks can involve in M&A properly towards the right audience, this will help them take advantage of the parties involved, create the synergistic values of management, human resources, market share, etc. As a result, this action may ensure the sustainable development of each bank and an improvement of the competitiveness and banks operational capacity.

At the same time, from this study, essential implications will be developed, helping to improve the Vietnamese banking system effectiveness. Consistent with the aforementioned objectives, the raised research questions of the study are as follows: (1) What are the efficiency levels of Vietnamese commercial banks during 2011–2019 period? (2) How M&As take an impact on Vietnamese banking efficiency?

The paper is organized as follows. Section 2 provides a brief literature review that includes theoretical background and information obtained from previous studies. Section 3 describes the methodology which will be used in this study and provides a description of the data collection as well as the models and implications. Section 4 presents the results from the efficiency scores and regression models, then determines the relationship between dependent and independent variables. The conclusions and some recommendations will be drawn in Section 5.

2. Literature review

Mergers and acquisitions (M&A) is a common business concept that refers to the combination of two business entities into a single independent entity. The objective of this collaboration is to advance the strengths of both sides. With the form of “mergers”, this is the merger association between two businesses, thereby giving birth to a new business with legal status. Rentsch and Schneider (Citation1991) declared that the definition of true “mergers” is hard to define because there are various acquisitions disguised as mergers to avoid single-company dominance. As for the form of “acquisitions”, in which a large enterprise will acquire a smaller, weaker enterprise, but unlike a merger, the “acquired” enterprise’s legal status remains the same. The acquiring businesses will have full legitimate ownership of the targeted business (Fasua and Osagie, Citation2016).

In the perspective of macroeconomics, “efficiency” occurs when society cannot increase the output of one good without cutting back another. An efficient economy lies in the limitation of production capabilities. In terms of corporate perspective, “efficiency” is determined by the ratio of the outcome to the cost to achieve it. This ratio reflects the level of using inputs in the operation process to gain a maximum profit at the smallest cost (McKinley and Banaian, Citation2005).

According to Pasiouras and Kosmidou (Citation2007), Sturm and Williams (Citation2008), the efficiency in the banking system is influenced by both internal and external factors. In particular, internal factors mainly focus on capital adequacy, the ratio between expenses and income, liquidity, size, and return on average total assets. External factors (macroeconomics and financial structure) include inflation rate, real gross domestic product, etc.

To improve the banking system’s supervisory capacity, the State Bank Inspector of Vietnam is implementing an important project to rate credit institutions according to CAMELS standards. This is considered a breakthrough to realize the goal of enhancing the efficiency and effectiveness of the banking inspection system. CAMELS stand for Capital (C), Assets (A), Management (M), Earnings (E), Liquidity (L), and Sensitivity (S). The CAMELS rating system is used as an international measuring tool to rank financial institutions based on six factors represented by its acronyms. The supervisory agencies compute points for each bank according to their scores. Rank 1 is the best and rank 5 is the worst for each factor.

To our knowledge, there have not been many quantitative studies comparing the CAMELS rating financial ratios and bank efficiency. Some mixed results were obtained regarding bank performance and profitability. Fiordelisi et al. (Citation2011) showed the positive relation between capital ratio and bank’s efficiency. Rostami (Citation2015) found the positive relation between Total Equity to Total Asset and bank performance. They also found the negative relation between Cost to Income, Provision of loan to Loans, and bank performance.

In terms of M&A activities, Viet (Citation2015) identified the outstanding features of M&A transactions in Vietnam. Based on the traditional approach analysis, this paper described the fundamental weakness of the M&A in Vietnam, which includes law enforcement and transparent information publicity. Additionally, the study suggested some implications to develop M&A activities, including the improvement of the law, brand name of the corporation, and post-M&A corporate governance. Besides, Hosseini et al. (Citation2017) focused on evaluating a bunch of inbound M&A transactions with foreign parties as buyers between 2008 and 2015. The findings showed the investment trend of international investors in Vietnamese enterprises, emphasizing the real estate and banking areas as attractive occupations in the context of the economy recover after the crisis in 2008. While the postponement of the process of changing from state-owned enterprises into joint stock companies inhibits the growth of M&A capital inflows into Vietnam, the improvement of open policy makes the market more attractive to foreign investors.

Previous studies worldwide showed mixed results about the relation between M&A activities and banks’ performance and efficiency. Altunbaş and Marqués (Citation2008) found out that M&A brings improvements in performance for the European banking system. Beccalli and Frantz (Citation2009) indicated that merger increases cost efficiency and slightly deteriorates profit efficiency. These studies mainly used pre-post analysis, to our knowledge there is lack of empirical research investigating the impact of M&A transactions on banks’ efficiency worldwide and in Vietnam, taking into account the potential control variables.

For these reasons this paper will fill the gap by taking CAMEL system as control variables in investigating the effect of M&A on the efficiency of Vietnamese commercial banks.

3. Methodology

3.1. Sample

In the paper, the examined data set from 30 Vietnamese commercial banks between 2011 and 2019 is collected from annual audited consolidated financial statements. The list of banks is given in Appendix A.

According to the list of investigated banks, there are eight banks involved in M&A during this period, which are Saigon - Hanoi Commercial Joint Stock Bank (SHB), Saigon Commercial Bank (SCB), Vietnam Commercial Bank for Investment and Development (BID), Lien Viet Post Joint Stock Commercial Bank (Lien Viet), Vietnam Maritime Commercial Joint Stock Bank (MSB), HCM City Development Joint Stock Commercial Bank (HDBank), Vietnam Public Joint Stock Commercial Bank (PVcombank) and Saigon Thuong Tin Commercial Joint Stock Bank (STB).

3.2. Variables

3.2.1. Dependent variables

According to Sealey and Lindley (Citation1977), there is an imperfect approach in determining bank inputs and outputs because no approach can reflect all activities. Under intermediation approach, banks play the role of the entity providing financial intermediary services to connect the savings and investment sectors of the economy. Their study found out that intermediation approach is the most suitable one to view banks as financial intermediaries, to analyze and evaluate the operational efficiency of the bank. The intermediation approach specifies the input set as services provided to depositors, non-financial resources, and physical assets, as found by Olson and Zoubi (Citation2011). Meanwhile, the output set is to concentrate on services provided to debtors and income from the cost incurred.

Besides, under operating approach, banks are seen as organizations with the priority of creating profit from the expenses incurred in order to maintain the business (Das & Ghosh, Citation2006). Following Jemric and Vujcic (Citation2002), the set of inputs is determined as the interest and non-interest expenses, while the output set is defined as the interest and non-interest income.

From these choices of inputs and outputs under intermediation approach and operating approach in , the banks’ efficiency scores are calculated using bootstrap DEA method and used as dependent variables. The bootstrap DEA method is explained in Section 3.3.1.

Table 1. Inputs and Outputs for DEA model

Since this study aims to evaluate whether M&A activities contribute to the movement of banking efficiency, the related regression model is considered as follows:

In which:

: Efficiency calculated from the intermediation approach for bank i in year t, 1 ≤ i ≤ 30, 1 ≤ t ≤ 9.

: Efficiency calculated from the operating approach for bank i in year t, 1 ≤ i ≤ 30, 1 ≤ t ≤ 9.

: Logarithm of total assets

: Equity-to-total assets

: Loan-loss-reserve-to total loan

: Cost-to-income ratio

: Return-on-average-assets

: Gross-loan-to deposits

: Merger variable

: error term

3.2.2. Independent variables

3.2.2.1. Variable of interest

In this paper the main independent variable of interest is Merger, which is defined to describe the M&A event. is equal to 1 from the year when the M&A deal occurs, equal to 0 before M&A deal.

3.2.2.2. Control variables

CAMELS system was developed by the US Credit Union Administration (NCUA) in 1987, and widely used not only in the United States but also in many countries around the world. After the Asian economic crisis in 1997, the CAMELS system was recommended by the International Monetary Fund to be applied in crisis countries as one of the measures to rebuild the financial sector. CAMELS model is mainly based on financial factors, through a scale to assess the health of financial institutions. This paper applied CAMELS systems to define the control variables, which are explained as below.

First, Capital Adequacy represents the amount of equity to support a bank’s business. The more risks a bank accepts (e.g., within a loan portfolio), the more equity capital is required to support the bank’s operations and cover potential losses associated with the higher risk. The Equity to Total assets ratio (ETA) is applied under Capital Adequacy segment for this research. This ratio has positive connection with the monetary adequacy of the bank, it is adversely identified with a potential flaw (Dincer et al., Citation2011).

Second, Assets Quality is a general indicator that shows the quality of management, solvency, profitability, and sustainable prospects of a bank. Moreover, it is also the primary cause of bank failures. Usually, this stems from inadequate management in lending policy. If the market knows that the quality of assets is poor, it puts pressure on the short-term funding of the banks, and this could lead to liquidity crises. Hence, the Loan loss reserves to Total loans (LLR_TL) is used to measure the assets quality of the banks by determining the loan quality (Jyothi Venkatesh, Citation2014).

Third, Management Quality is considered as the most difficult indicator to evaluate compared to others, because the management cannot be measured based on recent financial performance (Dincer et al., Citation2011). Numerous expertsconsider Management Quality as the main component in the CAMELS examination framework, because management plays a decisive role in the success of a bank’s operation. The Cost to Income ratio (CIR) is used to measure the efficiency of operational activity. This ratio shows the correlation between the bank’s cost and income. This ratio gives investors a clearer view of the organization’s performance. The smaller the percentage, the more efficient the bank will operate (Roman & Şargu, Citation2013).

Fourth, Earning Ability is an important element of revenue and cost analysis, including the effectiveness of interest policy and action as well as the overall results of operations measured by statistics. The earning ability will lead to the creation of more capital, which is essential to supporting future development from investors. It is also required to cover damaged loans and make full provisioning. According to Rozzani and Rahman (Citation2013), Return on Average Assets (ROAA) is used to evaluate how well banks operate their assets to earn profits. The bank is generally considered having a good earning when the ratio is equal or higher than 5%.

Fifth, Liquidity is a basic criterion for evaluating the quality and safety of a bank’s operations. Liquidity is needed to address new credit prerequisites without the issue to recuperate extraordinary advances or sell term speculations. According to Rostami (Citation2015), the Loans to Deposit ratio (LTD) is implemented to measure the safety of banks. If this ratio is high, the bank will be highly profitable as well as higher liquidity risk. On the other hand, if the rate of LTD is too low, banks do not make full use of the capital, and the efficiency is not high.

Finally, Sensitivity includes the specific level of risk that can affect a financial institution. The assets held by banks are mainly financial assets, which are often sensitive to market fluctuations and certain risks. Most banks’ assets are associated with various degrees of market risk, primarily to the assets that are sensitive to interest rate fluctuations, exchange rates or changes in prices on financial markets. If there is a large proportion of assets sensitive to these factors, it may give a signal that banks are vulnerable.

In terms of logarithmic transformation, it is convenient to use this method in order to convert a high deviation into more normalized variables in a data set. The desired linearity can be created by logarithmic transformation. Using this way to transform one or more variables can reduce the error in the regression model. Therefore, logarithm of total assets (LogTA) is applied in this paper, to show how 1% change in total assets can affect the banks’ efficiency.

Furthermore, these control variables were also used in the literature as summarized in .

Table 2. Variables for regression model

3.3. Method

3.3.1. Bootstrap DEA

This paper applies the bootstrap Data Envelopment Analysis method (DEA) to calculate banks’ efficiency score. DEA is a non-parametric method, used to evaluate efficiencies of a homogenous set of decision-making units (DMUs) in the presence of multiple inputs and outputs. Efficiency is defined as the ratio of the weighted sum of outputs to the weighted sum of inputs.

The original DEA model proposed by Charnes et al. (Citation1978) (CCR) is a model which assumes that any change in the inputs will give equally proportional multiple outputs, also known as Constant Returns to Scale (CRS). Assume that there are n DMUs, with m inputs and s outputs. Let and

be input weights and output weights respectively. Then the efficiency for each DMU j is measured as:

Such that

And

By calculating the efficiency of each DMU, the DMU j is efficient when the efficiency score is equal to 1 and the efficient DMUs will form the efficient frontier; the remaining DMUs are inefficient (when the efficiency score is lower than 1).

In general, the efficient frontier can be generated by an input-oriented approach or an output-oriented approach. The input-oriented approach is an attempt to minimize the quantity of inputs with a given level of outputs, while the output-oriented approach implies maximizing the quantity of outputs with a given level of inputs. In general, there are no restrictions on the chosen approach. However, in the context of measuring banking efficiency, the output-oriented approach is considered more appropriate since the output-oriented DEA can provide insights on how banks can act to produce more outputs through better and more focused commercial strategies and marketing activities (Ouenniche & Carrales, Citation2018).

Under output-oriented Constant Returns to Scale (CRS), the linear programming problem’s dual formulation can be derived as follows: (Huguenin, Citation2012)

In which, represents the efficiency of firm k and

addresses the associated weighting of outputs and inputs of firm j. Besides the CRS model of DEA, there is also a scale assumption, namely Variable Returns to Scale (VRS), which is developed by Banker et al. (Citation1984). This model implies that at different scales, DMUs can still be considered effective as having diverse changes in inputs and outputs (increasing or decreasing), see . Under output-oriented Variable Returns to Scale (VRS), the linear programming problem’s dual formulation can be derived, following Huguenin (Citation2012):

Figure 2. CSR versus VRS efficient frontier (Source: Huguenin, Citation2012).

Bootstrap DEA method is a collection of analytical techniques based on the sample with replacement principle, first developed by Simar and Wilson (Citation2000). Although the traditional DEA application provides some advantages, this method still contains some weaknesses. The scores resulting from traditional DEA method only provides the estimates rather than the confidence intervals. There are also some studies using bootstrap method to evaluate errors estimation (Hung et al., Citation2010; Wanke et al., Citation2011). The bootstrap DEA method can provide more information and improve the properties of conventional DEA scores about the mean distribution, the confidence interval as well as the probability of the mean based on a single sample.

3.3.2. Truncated regression

In order to generate the efficiency level, different approaches can be applied in specific aspects of the research. Since the purpose of the paper is to investigate how strong relationship of variables can influence the efficiency scores, there are two approaches called one-step and two-step approach. Under one-step approach, the measurement of the efficiency level includes the environmental variables; meanwhile, the two-step approach provides the efficiency measurement in separated results then regressed by a set of explanatory variables (Sufian et al., Citation2016). The robust truncated regression model under one-step approach can be estimated using fixed, random or pooled effects, taking into account the study of (Wu et al., Citation2016). In addition, two-step approach is also a proper method when the efficiency scores are measured by DEA model (Badunenko & Tauchmann, Citation2019). Wilson and Simar (Citation2007) found out that several studies widely used two-stage measurement where the banks ‘efficiency scores are treated as dependent variables. Therefore, they developed a procedure of applying truncated regression model. Since the range of DEA scores is from 0 to 1, truncated regression is more appropriate compared to traditional regression model.

4. Data analysis and discussion

4.1. Descriptive statistics

Bootstrap Data Envelopment Analysis is applied in this paper in connection with intermediation and operating approaches. The inputs and outputs set of DEA model under both approaches are collected during 2011–2019 period, from the banks’ financial statements. and will describe the general information of the data set, including mean, standard deviation, maximum and minimum value.

Table 3. Descriptive Statistics of Operating Approach data (Unit: Billion VND)

Table 4. Descriptive Statistics of Intermediation Approach data (Unit: Billion VND)

As can be seen from , the Interest Income accounts for a high proportion compared to other variables, with the maximum value of 106,468 billion VND. This means that during the examined period, commercial banks have done quite well in earning from lending their money to customers or to other financial institutions. On the contrary, the non-interest income remains at a small proportion of income structure. According to Minh Sang and Thi Thanh Tam (Citation2018), even though non-interest income only accounts for a small part, it still brings a positive influence on bank’s profitability.

According to , we can observe that within 270 observations during the examined period, the deposits from customers and lending to customers have a huge proportion in banks’ operating activity. This result provides that banks have an abundant capital source as well as appropriately deal with their assets. In general, this information declares that the sample investigated in this paper includes different operating scales of banks.

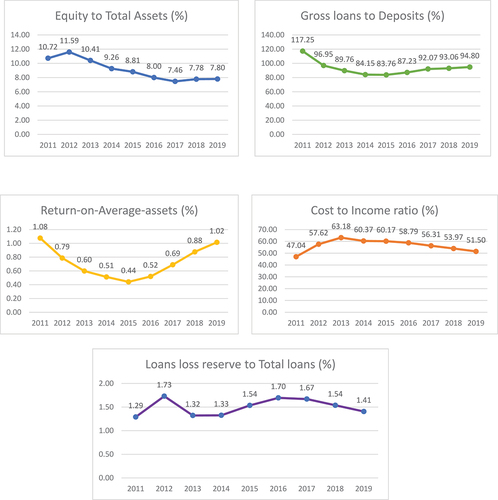

From , there exists a decreasing trend in ETA. However, during the restructuring period, the ratio peaked at 11.59% in 2012 since most small-sized banks were trying to deal with bankruptcy or liquidity problems. In the following years, the ratio had a declining trend until 2018, afterwards there was a slight increase from 7.78% to 7.80% in 2019. In terms of loans, which is the main source for banks’ income due to the high interest rate charged on loans. The loan to deposit ratio decreased between 2011 and 2015; however, this ratio began to increase in the next four years from 83.76% in 2015 to 94.80% in 2019. According to Circular 13 issued by the State Bank of Vietnam, the maximum loan to deposit ratio for banks is 80% and for non-bank credit institutions is 85%. The higher the ratio, the more liquidity risk banks suffer. Under the restructuring plan in 2011–2015 period, the ratio reduced to protect banks from liquidity risk. On the other hand, this rate rose in the next period after the restructuring period, which means that banks nowadays are experiencing higher liquidity risk. This is risky for our banking system due to the unstable recent economy situation.

Table 5. Descriptive statistics of Average CAMELS variables during 2011–2019

, also indicate the decreasing trend in ROAA which reached the minimum value at 0.44% in 2015, which is the lowest rate during the examined period. However, banking system experiences a positive sign in increasing this rate between 2016 and 2019, from 0.44% in 2015 to 1.02% in 2019. This claims that banks have been dealing with utilizing their assets quite well, and efficiently generate the profitability relative to average of total assets. Regarding to the ratio expense to income (CIR), the highest rate is 63.18% in 2013, then experiences the declining trend to 51.50% in 2019. This ratio shows the correlation between the bank’s cost and income. This ratio gives investors a clearer view of the organization’s performance. The smaller the ratio, the more efficiently the banks will operate. Therefore, it can be said that in 2011, banking system operated better compared to the following years. With regard to the Loan loss reserve to total loan, this ratio is used to measure the assets quality of the banks by determining the loan quality. From , it can be seen that this ratio suffers similar trend as CIR, reaching the peak in 2012 with 1.73% and declines until 2015. After that, the ratio goes up to 1.70% in 2016 then continuously drops to 1.41% in 2019.

Figure 3. Trend of CAMELS variables during examined period.

4.2. Efficiency scores

Using R software, the tables in Appendix B and Appendix C provide the bootstrap efficiency scores of the sample of 30 commercial banks during 2011–2019 period. Applying operating and intermediation approach, the average range of efficiency scores shows that a group of “Big4” banks, including Vietinbank, BIDV, Agribank and Vietcombank gain the higher efficiency level compared to others, which fluctuates between 0.8 and 0.95, closely to 1. However, due to the unstable economy, few banks have efficiency equal to 1. It can be seen that some banks reach the lower efficiency level under one approach, and a higher level under the other (e.g KienLong bank in 2019). This can be understandable because of different data sets of inputs and outputs, resulting in different efficiency scores which lead to contrasting range.

In the first period during 2011–2015, the world and domestic monetary circumstances were confounded, uncovering numerous insecurities, high inflation, slow economic growth. The stock market plummeted, the real estate market froze, the overall balance of payments was in deficit and the lending interest rate level was high. Many credit institutions have liquidity problems, poor governance, rising bad debts at alarming levels.

Especially in the context of 2011, before the restructuring of the banking system, inflation was at a high level, about 20%; interest rate was up to 26%; and interbank interest rate sometimes reached 35%. The commercial banking system falls into the danger of losing liquidity, not only for small banks. In the years 2011–2012, commercial banks raised interest rate, customers tried to withdraw their deposits from one bank to another. Short-term interest rates are higher than long-term rates, causing the standard curve of interest rates of the commercial banking system to collapse. Most commercial banks fell into an undisciplined situation when they rushed into the race of interest rates. In order to guarantee the safety and stability of the system and prevent breakdowns and unsafety beyond the control of the State, the State Bank of Vietnam established the Vietnam Asset Management Company to deal with high levels of bad debts at many commercial banks, including bad debt for credit extension, for buying corporate bonds and for entrusting credit.

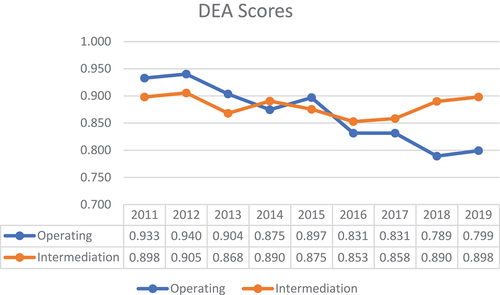

Regarding Variable Returns to Scale model for both approaches (see, ), the average level of efficiency reached its peak at 0.940 and 0.905 in 2012 for operating approach and intermediation approach respectively. The figure also provides that efficiency level in both approaches suffers a decreasing trend between 2013 and 2016, then slightly increase in 2017. However, the increase did not last long, until 2019 the level continued to decline under operating approach.

Figure 4. Bootstrap DEA scores of operating approach and intermediation approach.

The efficiency of banks in the period before restructuring was high, then declined due to the drawbacks from the economic crisis in 2007–2008 and the global economic recession in 2009. When commercial banks were restructured, the financial efficiency of commercial banks has not been improved immediately. In the first restructuring period from 2011 to 2015, financial efficiency experienced at higher level than in the second restructuring period from 2016 to 2020, the financial efficiency has been restored but not at the level before the restructuring.

4.3. Correlation analysis and multicollinearity test

First, we apply Pearson’s Correlation to test whether there exists a significant relation between variables. From and , the significant values are well presented at 10% (*) level. If the Pearson correlation coefficients are higher than 0.85, there might be the multicollinearity. The second step is to implement VIF to ensure that our regression model does not have multicollinearity problem.

Table 6. Pearson’s Correlation of Intermediation Approach

Table 7. Pearson’s Correlation of Operating Approach

From , it can be observed that all the variables have VIF value smaller than 5, which means that multicollinearity problem does not exist.

Table 8. Variance-inflation-factor (VIF)

4.4. Regression results

4.4.1. Intermediation approach results

As can be seen from , the results from Robust truncated regression using STATA software show that within a set of explanatory variables, LogTA, C.I, and Merger have significant relationship with efficiency score at 1% significance level. Moreover, ROAA is also significant at 5% significance level. Merger has the negative impact on the efficiency level of the bank. If banks participate in M&A transactions (when merger equals 1), there is a decrease of nearly 6% in efficiency level. This result is consistent with the negative M&A effect on profit efficiency by Beccalli and Frantz (Citation2009).

Table 9. Truncated regression results from Intermediation approach

Meanwhile, if total assets increase by 1%, efficiency is expected to increase by 0.055/100 ceteris paribus. We also found the positive relation between Cost to Income and bank efficiency, which is not in line with Rostami (Citation2015). In our paper, the loans ratio has no significant relation with banks’ efficiency. Therefore, if banks are viewed as intermediaries between savers and borrowers, they should not worry about potential liquidity problems. We also found that ROAA can help boost the banks’ efficiency.

4.4.2. Operating approach results

Under operating efficiency, most independent variables have significant relation with the efficiency level, except the LLR.TL (see ). Compared to intermediation approach, the operating aspect has more control variables affecting the banks’ efficiency. More specifically, LogTA and E.TA are significant at 1% significance level, while others are significant at 5% significance level. In this case, LogTA, E.TA, CI, GL.D and ROAA have positive influence on efficiency level. Only merger has negative impact on the efficiency level, which is similar to the result under intermediation approach. If the banks join in M&A activities, the decrease in operating efficiency level accounts approximately for 4%.

Table 10. Truncated regression results from Operating approach

Meanwhile, if total assets increase by 1%, efficiency is expected to increase by 0.138/100 ceteris paribus. Compared to the results above, operating aspect shows similar relation between earning ability and management quality with the efficiency level. However, under operating approach, the capital adequacy can be taken into account to improve banking efficiency. The finding is consistent with Fiordelisi et al. (Citation2011), which showed that the capital ratio can help increase banks’ efficiency. In addition, banks having better capital level tend to gain higher efficiency scores. We also found the positive relation between Cost to Income and bank efficiency, which is not in line with Rostami (Citation2015). We also found that ROAA and loan ratio can help boost the banks’ efficiency.

4.4.3. Discussion

Overall, the results in both cases indicate that even if the banks participate in M&A transactions, they might suffer a slight decline in the efficiency level. This result can be explained due to the efficiency score trend during the examined period (see Appendix B and Appendix C). The scores do not always go up or go down, they fluctuate year-by-year. Although there are several banks experiencing the increase in efficiency score during the first phase of restructuring period (2011–2015), they still suffer the decreasing trend in the following years. This might be resulting from the instabilities of the banking system: our country’s economic structure and growth model also revealed many weaknesses. However, the period when economic growth was unsustainable and tended to decrease along with high inflation rate, M&A transactions would become a better solution for saving banks from going bankrupt. After M&A, banks will have an increase in their assets and during the following years after the first phase of restructuring period, banks have been utilizing their assets quite well, which gives the increase in ROAA up to 1.02% in 2019. However, this ratio should be improved to 5% or higher in order to reach the sufficient rate of generating profits relative to total assets.

Moreover, under intermediation approach, banks are considered as intermediaries, whose efficiency is affected by the ratios expense to income CI and ROAA. They help improve the efficiency during the second restructuring phase at a higher level than operating approach, which viewed banks with a business perspective. This means that banks playing the role as intermediaries give good management quality. Meanwhile, most CAMELS variables significantly positively affect the efficiency thorough business perspective, which implies that banks should consider the CAMELS procedure to improve their efficiency level, especially to concentrate on earning from loans and capital funding without using debt.

5. Conclusions and recommendations

In summary, this paper aims to investigate the level of efficiency within 30 Vietnamese commercial banks during 2011–2019 period using bootstrap DEA model to measure the efficiency score under intermediation approach and operating approach. Then truncated regression is implemented to figure out how M&A affects the level of banking efficiency.

First, the results from DEA scores point out that in general, banks have higher efficiency level under intermediation approach than operating approach. The level of efficiency for the second phase of restructuring is lower than the first phase. M&A activities in the 2005–2010 period were promoted in order to change the model of joint stock commercial banks to comply with the provisions of the law on Credit Institutions, creating chances for banks to operate equally and avoiding market fragmentation by administrative regulations. During this period, M&A took place under the main forms: foreign banks acquired domestic banks, or domestic commercial banks buy and sell shares from each other. The reality of the global banking industry shows that M&A is not only for restructuring when the system is weak, but also an effective tool for each economy to have strong financial institutions. In the project of Restructuring the banking system phase 2 (2016–2020), the government clearly stated the purpose of this policy is to handle and restructure credit institutions by encouraging M&A of small banks and small credit institutions to merge into other big banks. However, due to the barrier of ownership ratio, most banks still consider whether to join in M&A activities.

Second, in terms of truncated regression, the results show that M&A does not improve banks’ efficiency in a positive way under both approaches. However, there is only a slight decrease in the efficiency level. This might be resulting from the tendency of commercial banks joining in M&A activities in recent years, which is still quite modest compared to the potential market. M&A has just stopped at a solution that plays a role to save banks that are on the verge of bankruptcy, avoid the breakdown of the banking system. Our banking system also needs to face with the challenges such as the conflict of interest between shareholder groups of the acquirer and the merged banks; or the encountered problems of selling capital to foreign partners without losing state capital. In addition, the set of explanatory variables following CAMELS standards has more significant relations with efficiency under operating than intermediation aspect. As a result, in both cases, the earning ability (return-on-average-asset) and the management quality (cost-to-income ratio) have positive impact on the efficiency of the banking system.

Therefore, it is essential to determine in which situations banks should consider undertaking M&A transactions. The efficiency level over the whole period is improved in one aspect (intermediation) but limited in the other one (operating). With different data sets of inputs and outputs, the scores turn out to be at diverse range, they do not follow a specific trend. However, this results also indicate that the restructuring plan for the second phase should be examined carefully so that it can boost the competitiveness in banking industry for the following years. Business administration and management consider the limitation of the majority of Vietnamese commercial banks in the context of international integration, especially small-sized banks. Commercial banks are often confused in planning M&A strategies, in orientating and defining goals, leading to the confusion in choosing the right partner. Another recommendation is that the government should develop detailed guidelines as a framework for linking legal documents to regulate all aspects of the M&A implementation process. For the sake of their own bank shareholders, banks sometimes provide inaccurate financial information (actual bad debts) to partners. This sometimes prevents the merger process and causes distrust among banks which are planning to participate in M&A. In addition, it is necessary to build disciplines forcing parties participating in M&A to disclose transparent and accurate information sources. Hence, this can support the parties to accurately assess and analyze their financial capacity and opportunities for cooperation in M&A decision making.

6. Limitations

The paper contributes to the effect of M&A on banking efficiency. However, it still includes some flawed assessments. Since the M&A activities took place in the past mainly according to the orientation and arrangement of the State Bank of Vietnam, the success of such activity requires commercial banks to voluntarily participate in M&A. The research only focused on commercial banks; hence the results do not perfectly describe the overall of the banking system. In addition, due to the lack of available data, there also exists a limitation in sample size. For further investigation, more banks (e.g., foreign banks) should be included in testing the efficiency level.

In terms of scores measuring, the data set of inputs and outputs depends on the approaches of the research. During the data collecting process, it may appear some negative values. Therefore, in order to apply DEA model properly, a constant value should be added to create positive inputs and outputs without changing the results. Moreover, measuring scores is one of the important steps to indicate the impact of explanatory variables on the level of efficiency, and how strongly the relation match under regression. Following CAMELS standards, further research should include the “sensitivity” factor as well as apply different approaches such as production and value-added in order to evaluate banks’ performance in various aspects. Additionally, this paper only applies output-oriented to measure the efficiency, future studies can take input-oriented approach under consideration, which may find the consistent motives of M&A in our banking system.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Phuong Anh Nguyen

Phuong Anh Nguyen is a researcher and lecturer in the Department of Finance and Banking at the International University, Vietnam National University of Ho Chi Minh City. Her research interests include bank efficiency, bank risk management, control and optimization. Her research works have been published in international journals such as Applied Economics, Journal of Optimization Theory and Application, SIAM Journal of Control and Optimization.

Thi Thanh Thuy Nguyen was a research assistant at the International University, Vietnam National University of Ho Chi Minh City, Vietnam. Her research interests include bank efficiency and bank risk management.

Thi Thanh Thuy Nguyen

Phuong Anh Nguyen is a researcher and lecturer in the Department of Finance and Banking at the International University, Vietnam National University of Ho Chi Minh City. Her research interests include bank efficiency, bank risk management, control and optimization. Her research works have been published in international journals such as Applied Economics, Journal of Optimization Theory and Application, SIAM Journal of Control and Optimization.

Thi Thanh Thuy Nguyen was a research assistant at the International University, Vietnam National University of Ho Chi Minh City, Vietnam. Her research interests include bank efficiency and bank risk management.

References

- Altunbaş, Y., & Marqués, D. (2008). Mergers and acquisitions and bank performance in Europe: The role of strategic similarities. Journal of Economics and Business, 60(3), 204–25. https://doi.org/10.1016/j.jeconbus.2007.02.003

- Badunenko, O., & Tauchmann, H. (2019). Simar and Wilson two-stage efficiency analysis for Stata The Stata Journal, 19(4), 950–988. ISBN: https://doi.org/10.1177/1536867X19893640.

- Banker, R. D., Charnes, A., & Cooper, W. W. (1984). Some models for estimating technical and scale inefficiencies in data envelopment analysis. Management Science, 30(9), 1078–1092. https://doi.org/10.1287/mnsc.30.9.1078

- Beccalli, E., & Frantz, P. (2009). M&A operations and performance in banking. Journal of Financial Services Research, 36(2), 203–226. https://doi.org/10.1007/s10693-008-0051-6

- Charnes, A., Cooper, W. W., & Rhodes, E. (1978). Measuring the efficiency of decision making units. European Journal of Operational Research, 2(6), 429–444. https://doi.org/10.1016/0377-2217(78)90138-8

- Das, A., & Ghosh, S. (2006). Financial deregulation and efficiency: An empirical analysis of Indian banks during the post reform period. Review of Financial Economics, 15(3), 193–221. https://doi.org/10.1016/j.rfe.2005.06.002

- Dincer, H., Gencer, G., Orhan, N., & Sahinbas, K. (2011). A performance evaluation of the Turkish banking sector after the global crisis via CAMELS ratios. Procedia - Social and Behavioral Sciences, 24, 1530–1545. https://doi.org/10.1016/j.sbspro.2011.09.051

- Fasua, H. K., Osagie, O. (2016). Proactive Merger and Acquisition and Firm Performance Research Journal of Finance and Accounting . 7(14), 15–19 https://www.iiste.org/Journals/index.php/RJFA/article/view/32101 .

- Fiordelisi, F., Marques-Ibanez, D., & Molyneux, P. (2011). Efficiency and risk in European banking. Journal of Banking and Finance, 35(5), 1315–1326. https://doi.org/10.1016/j.jbankfin.2010.10.005

- Gupta, N., Mahakud, J., & McMillan, D. (2020). Ownership, bank size, capitalization and bank performance: Evidence from India. Cogent Economics & Finance, 8(1), 1808282. https://doi.org/10.1080/23322039.2020.1808282

- Hang, Vy, P. D., Bandaralage, J., & Hang, H. T. T. (2016). Mergers, acquisitions and market concentration in the banking sector: The case of Vietnam. Asian Journal of Economics and Empirical Research, 3(1), 49–58. https://doi.org/10.20448/journal.501/2016.3.1/501.1.49.58

- Hosseini, J. C., Thu, N. K., & Trang, N. T. T. (2017). Vietnam Inbound M&A Activity: The Role of Government Policy and Regulatory Environment. The South East Asian Journal of Management, 11(1), 58–69 https://www.semanticscholar.org/paper/Vietnam-Inbound-M%26A-Activity%3A-The-Role-of-Policy-Hosseini-Thu/1291105c1ca01e3501f4ee9991453efd87c4c1ec.

- Huguenin, J.-M. (2012 Data envelopment analysis (DEA). A pedagogical guide for decision makers in the public sector). . (Swiss Graduate School of Public Administration, IDHEAP, Lausanne) 978-2-940390-54-0 https://serval.unil.ch/resource/serval:BIB_0FC432348A97.P001/REF .

- Hung, S. W., Lu, W. M., & Wang, T. P. (2010). Benchmarking the operating efficiency of Asia container ports. European Journal of Operational Research, 203(3), 706–713. https://doi.org/10.1016/j.ejor.2009.09.005

- Jemric, I., & Vujcic, B. (2002). Efficiency of banks in Croatia: A DEA approach. Comparative Economic Studies, 44(2–3), 169–193. https://doi.org/10.1057/ces.2002.13

- Jyothi Venkatesh, C. S. (2014). Comparative performance evaluation of selected commercial banks in kingdom of Bahrain using CAMELS method. Bahrain Institute of Banking and Finance. http://library1.nida.ac.th/termpaper6/sd/2554/19755.pdf

- McKinley, V., Banaian, K. (2005 Central Bank Operational Efficiency: Meaning and Measurement Central Bank Modernisation, 45–81. https://ssrn.com/abstract=2508461.

- Minh Sang, N., & Thi Thanh Tam, T. (2018). Impacts Of Non-Interest Income On Risks And Profitability In Vietnam’s Commercial Banks (in Vietnamese). Dalat University Journal of Science,8(1S) , 118–132. https://tckh.dlu.edu.vn/index.php/tckhdhdl/article/view/460.

- Olson, D., & Zoubi, T. A. (2011). Efficiency and bank profitability in MENA countries. Emerging Markets Review, 12(2), 94–110. https://doi.org/10.1016/j.ememar.2011.02.003

- Ouenniche, J., & Carrales, S. (2018). Assessing efficiency profiles of UK commercial banks: A DEA analysis with regression-based feedback. Annals of Operations Research, 266(1–2), 551–587. https://doi.org/10.1007/s10479-018-2797-z

- Pasiouras, F., & Kosmidou, K. (2007). Factors influencing the profitability of domestic and foreign commercial banks in the European Union. Research in International Business and Finance, 21(2), 222–237. https://doi.org/10.1016/j.ribaf.2006.03.007

- Rentsch, J. R., & Schneider, B. (1991). Expectations for postcombination organizational life: A study of responses to merger and acquisition scenarios. Journal of Applied Social Psychology, 21(3), 233–252. https://doi.org/10.1111/j.1559-1816.1991.tb02725.x

- Roman, A., & Şargu, A. C. (2013). Analysing the financial soundness of the commercial banks in Romania: An Approach based on the camels framework. Procedia Economics and Finance, 6(13), 703–712. https://doi.org/10.1016/s2212-5671(13)00192-5

- Rostami, M. . (2015). Determination of Camels model on bank’s performance. International Journal of Multidisciplinary Research and Development, 2(10), 652–664 http://www.allsubjectjournal.com/archives/2015/vol2/issue10/123.

- Rozzani, N., & Rahman, R. (2013). Camels and performance evaluation of banks in Malaysia: conventional versus Islamic. Journal of Islamic Finance and Business Research, 2(1), 36–45.

- Sealey, C. W., & Lindley, J. T. (1977). Inputs, Outputs, and a Theory of Production and Cost At Depository Financial Institutions. The Journal of Finance, 32(4), 1251–1266. https://doi.org/10.1111/j.1540-6261.1977.tb03324.x

- Simar, L., & Wilson, P. W. (2000). A general methodology for bootstrapping in non-parametric frontier models. Journal of Applied Statistics, 27(6), 779–802. https://doi.org/10.1080/02664760050081951

- Sturm, J. E., & Williams, B. (2008). Characteristics determining the efficiency of foreign banks in Australia. Journal of Banking and Finance, 32(11), 2346–2360 https://www.sciencedirect.com/science/article/abs/pii/S037842660800006X?via/3Dihub.

- Sufian, F., Kamarudin, F., & Nassir, A. M. (2016). Determinants of efficiency in the Malaysian banking sector: Does bank origins matter? Intellectual Economics, 10(1), 38–54. https://doi.org/10.1016/j.intele.2016.04.002

- Viet, P. Q. (2015). Some Recommendations of M&A Activity in Vietnam Today. Issues in Economics and Business, 1(1), 30. https://doi.org/10.5296/ieb.v1i1.7893

- Wanke, P. F., Barbastefano, R. G., & Hijjar, M. F. (2011). Determinants of efficiency at major Brazilian port terminals. Transport Reviews, 31(5), 653–677. https://doi.org/10.1080/01441647.2010.547635

- Wilson, P. W., & Simar, L (2007). Estimation and inference in two-stage, semi-parametric models of production processes. Journal of Econometrics, 136(1) , 31–64. https://doi.org/10.1016/j.jeconom.2005.07.009

- Wu, Y. C., Wei Kiong Ting, I., Lu, W. M., Nourani, M., & Kweh, Q. L. (2016). The impact of earnings management on the performance of ASEAN banks. Economic Modelling, 53(C), 156–165 https://doi.org/10.1016/j.econmod.2015.11.023

Appendix A.

List of Commercial Banks

Appendix B.

Bootstrap DEA scores of 30 commercial banks during 2011–2015

Appendix C.

Bootstrap DEA scores of 30 commercial banks during 2016-2019

Appendix D.

VIF values

Appendix E.

Truncated Regression of Intermediation Approach

Appendix F.

Truncated Regression of Operating Approach

Appendix G.

Bootstrap DEA scores from RStudio